Identify and Interpret Compliance Requirements

53 Pages14564 Words1 Views

Added on 2023-01-13

About This Document

This assessment task focuses on identifying and interpreting compliance requirements in mortgage broking. It covers topics such as the unsuitability test, credit guide, code of ethics, and APRA's attitude towards bank lending for investment properties.

Identify and Interpret Compliance Requirements

Added on 2023-01-13

ShareRelated Documents

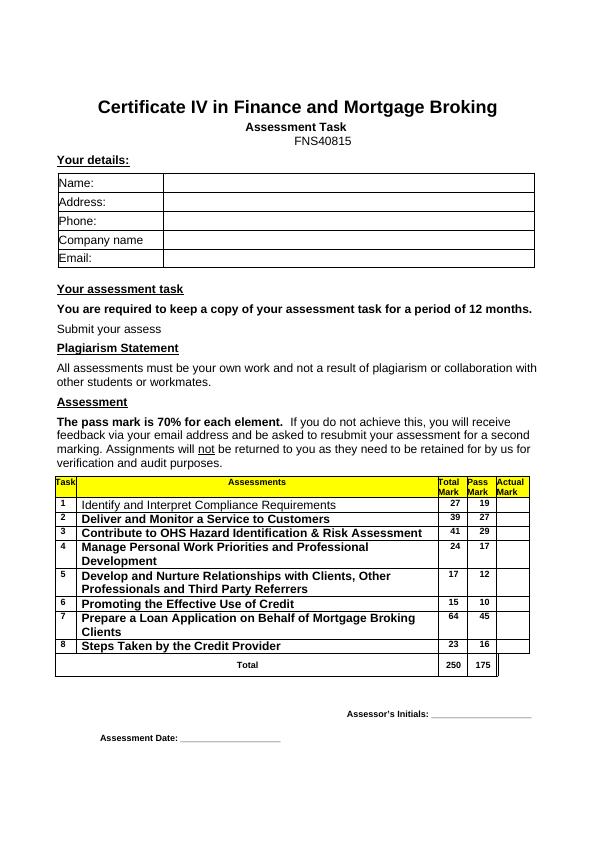

Certificate IV in Finance and Mortgage Broking

Assessment Task

FNS40815

Your details:

Name:

Address:

Phone:

Company name

Email:

Your assessment task

You are required to keep a copy of your assessment task for a period of 12 months.

Submit your assess

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration with

other students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will receive

feedback via your email address and be asked to resubmit your assessment for a second

marking. Assignments will not be returned to you as they need to be retained for by us for

verification and audit purposes.

Task Assessments Total

Mark

Pass

Mark

Actual

Mark

1 Identify and Interpret Compliance Requirements 27 19

2 Deliver and Monitor a Service to Customers 39 27

3 Contribute to OHS Hazard Identification & Risk Assessment 41 29

4 Manage Personal Work Priorities and Professional

Development

24 17

5 Develop and Nurture Relationships with Clients, Other

Professionals and Third Party Referrers

17 12

6 Promoting the Effective Use of Credit 15 10

7 Prepare a Loan Application on Behalf of Mortgage Broking

Clients

64 45

8 Steps Taken by the Credit Provider 23 16

Total 250 175

Assessor’s Initials: ____________________

Assessment Date: ____________________

Assessment Task

FNS40815

Your details:

Name:

Address:

Phone:

Company name

Email:

Your assessment task

You are required to keep a copy of your assessment task for a period of 12 months.

Submit your assess

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration with

other students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will receive

feedback via your email address and be asked to resubmit your assessment for a second

marking. Assignments will not be returned to you as they need to be retained for by us for

verification and audit purposes.

Task Assessments Total

Mark

Pass

Mark

Actual

Mark

1 Identify and Interpret Compliance Requirements 27 19

2 Deliver and Monitor a Service to Customers 39 27

3 Contribute to OHS Hazard Identification & Risk Assessment 41 29

4 Manage Personal Work Priorities and Professional

Development

24 17

5 Develop and Nurture Relationships with Clients, Other

Professionals and Third Party Referrers

17 12

6 Promoting the Effective Use of Credit 15 10

7 Prepare a Loan Application on Behalf of Mortgage Broking

Clients

64 45

8 Steps Taken by the Credit Provider 23 16

Total 250 175

Assessor’s Initials: ____________________

Assessment Date: ____________________

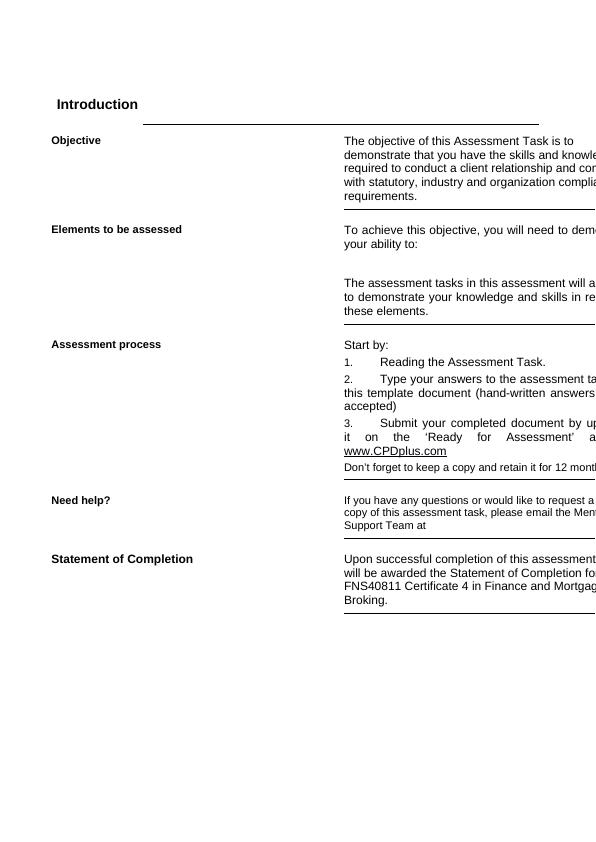

Introduction

Objective The objective of this Assessment Task is to

demonstrate that you have the skills and knowle

required to conduct a client relationship and com

with statutory, industry and organization complia

requirements.

Elements to be assessed To achieve this objective, you will need to demo

your ability to:

The assessment tasks in this assessment will a

to demonstrate your knowledge and skills in re

these elements.

Assessment process Start by:

1. Reading the Assessment Task.

2. Type your answers to the assessment ta

this template document (hand-written answers

accepted)

3. Submit your completed document by up

it on the ‘Ready for Assessment’ a

www.CPDplus.com

Don’t forget to keep a copy and retain it for 12 month

Need help? If you have any questions or would like to request a

copy of this assessment task, please email the Ment

Support Team at

Statement of Completion Upon successful completion of this assessment

will be awarded the Statement of Completion for

FNS40811 Certificate 4 in Finance and Mortgag

Broking.

Objective The objective of this Assessment Task is to

demonstrate that you have the skills and knowle

required to conduct a client relationship and com

with statutory, industry and organization complia

requirements.

Elements to be assessed To achieve this objective, you will need to demo

your ability to:

The assessment tasks in this assessment will a

to demonstrate your knowledge and skills in re

these elements.

Assessment process Start by:

1. Reading the Assessment Task.

2. Type your answers to the assessment ta

this template document (hand-written answers

accepted)

3. Submit your completed document by up

it on the ‘Ready for Assessment’ a

www.CPDplus.com

Don’t forget to keep a copy and retain it for 12 month

Need help? If you have any questions or would like to request a

copy of this assessment task, please email the Ment

Support Team at

Statement of Completion Upon successful completion of this assessment

will be awarded the Statement of Completion for

FNS40811 Certificate 4 in Finance and Mortgag

Broking.

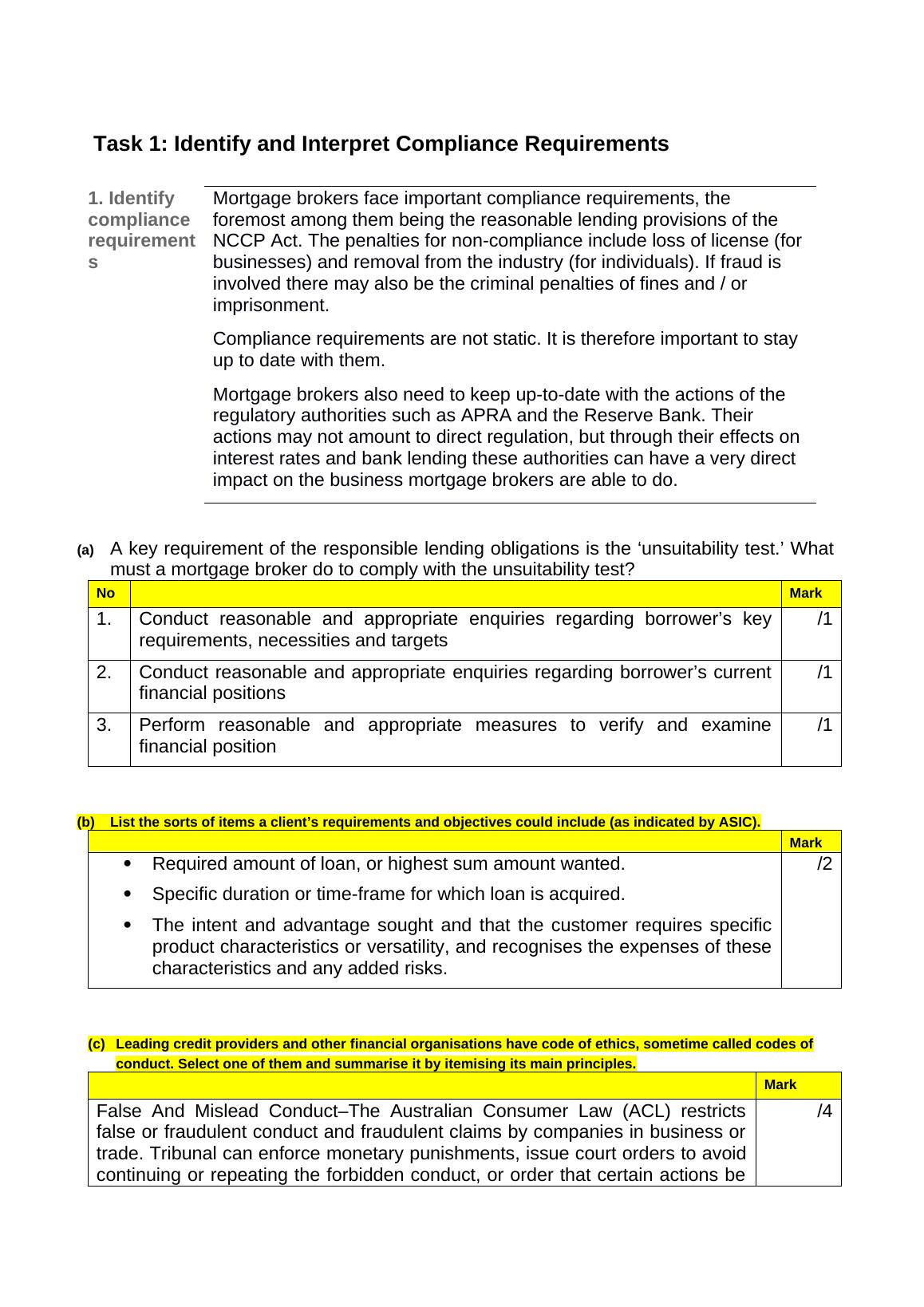

Task 1: Identify and Interpret Compliance Requirements

1. Identify

compliance

requirement

s

Mortgage brokers face important compliance requirements, the

foremost among them being the reasonable lending provisions of the

NCCP Act. The penalties for non-compliance include loss of license (for

businesses) and removal from the industry (for individuals). If fraud is

involved there may also be the criminal penalties of fines and / or

imprisonment.

Compliance requirements are not static. It is therefore important to stay

up to date with them.

Mortgage brokers also need to keep up-to-date with the actions of the

regulatory authorities such as APRA and the Reserve Bank. Their

actions may not amount to direct regulation, but through their effects on

interest rates and bank lending these authorities can have a very direct

impact on the business mortgage brokers are able to do.

(a) A key requirement of the responsible lending obligations is the ‘unsuitability test.’ What

must a mortgage broker do to comply with the unsuitability test?

No Mark

1. Conduct reasonable and appropriate enquiries regarding borrower’s key

requirements, necessities and targets

/1

2. Conduct reasonable and appropriate enquiries regarding borrower’s current

financial positions

/1

3. Perform reasonable and appropriate measures to verify and examine

financial position

/1

(b) List the sorts of items a client’s requirements and objectives could include (as indicated by ASIC).

Mark

Required amount of loan, or highest sum amount wanted.

Specific duration or time-frame for which loan is acquired.

The intent and advantage sought and that the customer requires specific

product characteristics or versatility, and recognises the expenses of these

characteristics and any added risks.

/2

(c) Leading credit providers and other financial organisations have code of ethics, sometime called codes of

conduct. Select one of them and summarise it by itemising its main principles.

Mark

False And Mislead Conduct–The Australian Consumer Law (ACL) restricts

false or fraudulent conduct and fraudulent claims by companies in business or

trade. Tribunal can enforce monetary punishments, issue court orders to avoid

continuing or repeating the forbidden conduct, or order that certain actions be

/4

1. Identify

compliance

requirement

s

Mortgage brokers face important compliance requirements, the

foremost among them being the reasonable lending provisions of the

NCCP Act. The penalties for non-compliance include loss of license (for

businesses) and removal from the industry (for individuals). If fraud is

involved there may also be the criminal penalties of fines and / or

imprisonment.

Compliance requirements are not static. It is therefore important to stay

up to date with them.

Mortgage brokers also need to keep up-to-date with the actions of the

regulatory authorities such as APRA and the Reserve Bank. Their

actions may not amount to direct regulation, but through their effects on

interest rates and bank lending these authorities can have a very direct

impact on the business mortgage brokers are able to do.

(a) A key requirement of the responsible lending obligations is the ‘unsuitability test.’ What

must a mortgage broker do to comply with the unsuitability test?

No Mark

1. Conduct reasonable and appropriate enquiries regarding borrower’s key

requirements, necessities and targets

/1

2. Conduct reasonable and appropriate enquiries regarding borrower’s current

financial positions

/1

3. Perform reasonable and appropriate measures to verify and examine

financial position

/1

(b) List the sorts of items a client’s requirements and objectives could include (as indicated by ASIC).

Mark

Required amount of loan, or highest sum amount wanted.

Specific duration or time-frame for which loan is acquired.

The intent and advantage sought and that the customer requires specific

product characteristics or versatility, and recognises the expenses of these

characteristics and any added risks.

/2

(c) Leading credit providers and other financial organisations have code of ethics, sometime called codes of

conduct. Select one of them and summarise it by itemising its main principles.

Mark

False And Mislead Conduct–The Australian Consumer Law (ACL) restricts

false or fraudulent conduct and fraudulent claims by companies in business or

trade. Tribunal can enforce monetary punishments, issue court orders to avoid

continuing or repeating the forbidden conduct, or order that certain actions be

/4

undertaken such as cancelling agreements and granting damages. Offense

also coincides with criminal code violations and penalties and prison

sentences can be levied as well.

Sub-total /9

Continued

(d) In point form, list the key information that the NCCP Act requires to be contained in a Credit Guide.

Mark

A credit guide required to be in written form and must specify:

Name of the licensee, his contacts information along with Australian-

credit licence no.

Details about fees-payable as well as charges-payable by client.

Details about commissions which is receivable from the moneylender.

Names of 6 prime licensees.

Information regarding the processing of complaints, along with contact

information regarding internally and externally dispute settlement

procedures.

Details regarding the current obligations of the applicant to provide, after

request, written copy of unsuitable evaluation.

Presenting credit guidelines should seem like a formal requirements but

it is a way to introduce business to the consumer and explain what it can

do in a positive way. however it also provides an occasion to explain

certain company characteristics like the variety of services offered and

the processes for addressing grievances that the organisation is

expected to have.

/3

(e) It is important to keep up to date with compliance requirements so that the required changes can be made

to organization procedures and product offerings. Suggest three sources that you can use.

Mark

1) First one is Professional associations bodies like Finance Brokers

Association of Australia (FBAA) and Mortgage and Finance Association

of Australia (MFAA), as well as communicate its members of alteration in

any requirement prior to happen.

/3

also coincides with criminal code violations and penalties and prison

sentences can be levied as well.

Sub-total /9

Continued

(d) In point form, list the key information that the NCCP Act requires to be contained in a Credit Guide.

Mark

A credit guide required to be in written form and must specify:

Name of the licensee, his contacts information along with Australian-

credit licence no.

Details about fees-payable as well as charges-payable by client.

Details about commissions which is receivable from the moneylender.

Names of 6 prime licensees.

Information regarding the processing of complaints, along with contact

information regarding internally and externally dispute settlement

procedures.

Details regarding the current obligations of the applicant to provide, after

request, written copy of unsuitable evaluation.

Presenting credit guidelines should seem like a formal requirements but

it is a way to introduce business to the consumer and explain what it can

do in a positive way. however it also provides an occasion to explain

certain company characteristics like the variety of services offered and

the processes for addressing grievances that the organisation is

expected to have.

/3

(e) It is important to keep up to date with compliance requirements so that the required changes can be made

to organization procedures and product offerings. Suggest three sources that you can use.

Mark

1) First one is Professional associations bodies like Finance Brokers

Association of Australia (FBAA) and Mortgage and Finance Association

of Australia (MFAA), as well as communicate its members of alteration in

any requirement prior to happen.

/3

2) Secondly codes of these professional associations regarding practice

may be utilised as effective guide line for compliance's requirements.

3) Lastly, bigger mortgage-broking entities normally employ compliance

officers as they aid practitioners to comply with relevant standards.

(f) Explain the requirement for Australian Credit Licensees to keep a training register.

Mark

ASIC entails a corporation to document conformance policies, while it

recognizes that verification levels will differ from comprehensive policy and

processes handbooks in bigger organizations to check-lists in smaller entities. It

is enforced and sustained once a conformance structure has been formed.

Throughout this phase, training does have an essential function but it's not

sufficient in its own. Compliance and moral behaviors must become a prevailing

organizational value.

/2

(g) Explain APRA’s current attitude towards bank lending for investment properties.

Mark

The Australian Prudential Regulation Authority (APRA) has instituted restrictions

which have affected investment and borrowing. The banks adapted to

amendments in APRA by adjusting serviceability conditions on investor

mortgages; rendering it harder for the investors to access finance. Lending

ability has also been limited, lending rates have increased and mortgage

payments are levied at an even greater rate on outstanding debt.

/2

Sub-total /

10

Continued

may be utilised as effective guide line for compliance's requirements.

3) Lastly, bigger mortgage-broking entities normally employ compliance

officers as they aid practitioners to comply with relevant standards.

(f) Explain the requirement for Australian Credit Licensees to keep a training register.

Mark

ASIC entails a corporation to document conformance policies, while it

recognizes that verification levels will differ from comprehensive policy and

processes handbooks in bigger organizations to check-lists in smaller entities. It

is enforced and sustained once a conformance structure has been formed.

Throughout this phase, training does have an essential function but it's not

sufficient in its own. Compliance and moral behaviors must become a prevailing

organizational value.

/2

(g) Explain APRA’s current attitude towards bank lending for investment properties.

Mark

The Australian Prudential Regulation Authority (APRA) has instituted restrictions

which have affected investment and borrowing. The banks adapted to

amendments in APRA by adjusting serviceability conditions on investor

mortgages; rendering it harder for the investors to access finance. Lending

ability has also been limited, lending rates have increased and mortgage

payments are levied at an even greater rate on outstanding debt.

/2

Sub-total /

10

Continued

Task 1: Identify and Interpret Compliance Requirements Continued

1.2

Interpret

, analyse

and

prioritis

e

identifie

d

complia

nce

require

ments

Some of the compliance requirements are difficult to meet. Unfortunately,

also there have been some ‘rogue’ mortgage brokers who have failed to

comply – to the disadvantage of their clients.

The finance planning industry has been plagued by non-compliance in the

largest planning groups, with the image of the industry being substantially

tarnished as a result. It may not suffer greatly because of the absence of an

alternative source of financial advice.

This is not so with mortgage brokers. They are just establishing their

reputation and consumers always have alternative of going to the lenders

directly.

(a) Select three tasks you perform on a regular basis that are subject to compliance

requirements.

No Mark

1. Search/Find out lender /1

2. Completion of loan application effectively /1

3. Send the loan request application to banking institution or other lender, and

waiting until it is accepted by them.

/1

(b) Identify the compliance requirements that are relevant to the three tasks selected,

indicating the name of the relevant legislation, regulation or code of conduct.

No

1. The National Consumer Credit Protection Act 2009 /1

2. ASIC /1

3. Australian Consumer Law /1

(c) How does your organisation monitor your compliance?

Mark

Enacting audits and control of enforcement areas and practices is both integral

business feature and requirement of ASIC regulations. Only other way of ensuring

systems work would be to inspect it and evaluate the findings, performing periodic

and ongoing analyzes and assessments of discrepancies.

/2

1.2

Interpret

, analyse

and

prioritis

e

identifie

d

complia

nce

require

ments

Some of the compliance requirements are difficult to meet. Unfortunately,

also there have been some ‘rogue’ mortgage brokers who have failed to

comply – to the disadvantage of their clients.

The finance planning industry has been plagued by non-compliance in the

largest planning groups, with the image of the industry being substantially

tarnished as a result. It may not suffer greatly because of the absence of an

alternative source of financial advice.

This is not so with mortgage brokers. They are just establishing their

reputation and consumers always have alternative of going to the lenders

directly.

(a) Select three tasks you perform on a regular basis that are subject to compliance

requirements.

No Mark

1. Search/Find out lender /1

2. Completion of loan application effectively /1

3. Send the loan request application to banking institution or other lender, and

waiting until it is accepted by them.

/1

(b) Identify the compliance requirements that are relevant to the three tasks selected,

indicating the name of the relevant legislation, regulation or code of conduct.

No

1. The National Consumer Credit Protection Act 2009 /1

2. ASIC /1

3. Australian Consumer Law /1

(c) How does your organisation monitor your compliance?

Mark

Enacting audits and control of enforcement areas and practices is both integral

business feature and requirement of ASIC regulations. Only other way of ensuring

systems work would be to inspect it and evaluate the findings, performing periodic

and ongoing analyzes and assessments of discrepancies.

/2

Sub-total /8

Total /27

Task 2: Deliver and Monitor a Service to Customers

2.

Identify

custome

r needs

The relationship with a client is generally described as beginning with the

establishment of empathy. In other words, it is first necessary for a

mortgage broker to establish that he / she is truly interested in the client and

the client’s needs. It is only after that that the mortgage broker has

established the right to interview a client.

(a) Use the internet or any other source to find a definition of empathy.

Mark

The capacity to communicate the emotions or perceptions of another by thinking

how it would be in the scenario of that individual.

/1

(b) List three open-ended questions that assist in developing empathy with a client? How

do such questions indicate empathy?

No. Mark

What is going on?

How is the business?

What makes you believe it's perhaps time for something new?

/2

The open ended question offers information regards to need, want of an

individual and every mortgage broker should have this information. Herein,

underneath some open ended questions are mentioned which are as

follows:

/1

(c) List and explain the steps involved in an ‘active listening approach’.

Mark

In the aspect of active listening approach, different steps are included and some of

them are mentioned underneath:

Ask questions- In this step, need and want of clients are find out so

/1

Total /27

Task 2: Deliver and Monitor a Service to Customers

2.

Identify

custome

r needs

The relationship with a client is generally described as beginning with the

establishment of empathy. In other words, it is first necessary for a

mortgage broker to establish that he / she is truly interested in the client and

the client’s needs. It is only after that that the mortgage broker has

established the right to interview a client.

(a) Use the internet or any other source to find a definition of empathy.

Mark

The capacity to communicate the emotions or perceptions of another by thinking

how it would be in the scenario of that individual.

/1

(b) List three open-ended questions that assist in developing empathy with a client? How

do such questions indicate empathy?

No. Mark

What is going on?

How is the business?

What makes you believe it's perhaps time for something new?

/2

The open ended question offers information regards to need, want of an

individual and every mortgage broker should have this information. Herein,

underneath some open ended questions are mentioned which are as

follows:

/1

(c) List and explain the steps involved in an ‘active listening approach’.

Mark

In the aspect of active listening approach, different steps are included and some of

them are mentioned underneath:

Ask questions- In this step, need and want of clients are find out so

/1

that accordingly next steps can be taken out.

Go back- Restate what the customer stated about his or her desires

to be sure that the pertinent details were heard and understood, and

allow the presenter to continue. The views and emotions of the

customer could then be used as a reference to further queries.

/1

Summarise- In the end make assure that both parties are agreed on

terms and conditions.

/1

(d) How is client service commonly monitored in your organisation? What are the two

possible outcomes?

No. Mark

1. Institutions will benefit from customer interactions by tracking consistency

through multiple channels, resulting in better decisions, operation, and

procedures. Tracking, assessing and controlling efficiency and level of

service must remain a target, but automation of "client's voice" throughout

multiple channels is just as critical.

/1

2. Through taking the view that value control is a systemic mechanism instead

of a tactical one, companies will begin to see user experience enhanced and

thus consumers are greatest champions.

/2

Sub-total /10

Continued

Task 2: Deliver and Monitor a Service to Customers Continued

2.1 Deliver

a service to

customers

In a survey on the reasons for referrals conducted by David Maister, only

10% were due to the quality of technical work. The remaining 90% of

referrals were due to the quality of service.

This indicates that the key to maintaining client relationships and gaining

referrals is the provision of outstanding service. This has been described by

Maister as ‘over-servicing’.

(a) Describe three ways in which a mortgage broking organisation can attempt to

‘overservice’ clients?

No. Mark

1. Investment in company and automation- The task tracking systems, metrics /1

Go back- Restate what the customer stated about his or her desires

to be sure that the pertinent details were heard and understood, and

allow the presenter to continue. The views and emotions of the

customer could then be used as a reference to further queries.

/1

Summarise- In the end make assure that both parties are agreed on

terms and conditions.

/1

(d) How is client service commonly monitored in your organisation? What are the two

possible outcomes?

No. Mark

1. Institutions will benefit from customer interactions by tracking consistency

through multiple channels, resulting in better decisions, operation, and

procedures. Tracking, assessing and controlling efficiency and level of

service must remain a target, but automation of "client's voice" throughout

multiple channels is just as critical.

/1

2. Through taking the view that value control is a systemic mechanism instead

of a tactical one, companies will begin to see user experience enhanced and

thus consumers are greatest champions.

/2

Sub-total /10

Continued

Task 2: Deliver and Monitor a Service to Customers Continued

2.1 Deliver

a service to

customers

In a survey on the reasons for referrals conducted by David Maister, only

10% were due to the quality of technical work. The remaining 90% of

referrals were due to the quality of service.

This indicates that the key to maintaining client relationships and gaining

referrals is the provision of outstanding service. This has been described by

Maister as ‘over-servicing’.

(a) Describe three ways in which a mortgage broking organisation can attempt to

‘overservice’ clients?

No. Mark

1. Investment in company and automation- The task tracking systems, metrics /1

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Certificate IV in Finance and Mortgage Broking - Assessmentlg...

|41

|11056

|310

Identify and Interpret Compliance Requirementslg...

|38

|7454

|49

FNS40815 Certificate IV in Finance and Mortgage Brokinglg...

|41

|11459

|2762

Certificate IV in Finance and Mortgage Broking Assessment Tasklg...

|42

|13051

|480

Certificate IV in Finance and Mortgage Broking Assessment Task - Deskliblg...

|15

|5213

|409

FNS40811 Certificate IV in Finance and Mortgage Broking Assignmentlg...

|48

|20179

|30