Identify and Interpret Compliance Requirements

38 Pages7454 Words49 Views

Added on 2023-01-05

About This Document

This assessment task focuses on identifying and interpreting compliance requirements in the finance and mortgage broking industry. It covers topics such as responsible lending obligations, client requirements and objectives, code of ethics, credit guide requirements, and sources for staying up to date with compliance requirements.

Identify and Interpret Compliance Requirements

Added on 2023-01-05

ShareRelated Documents

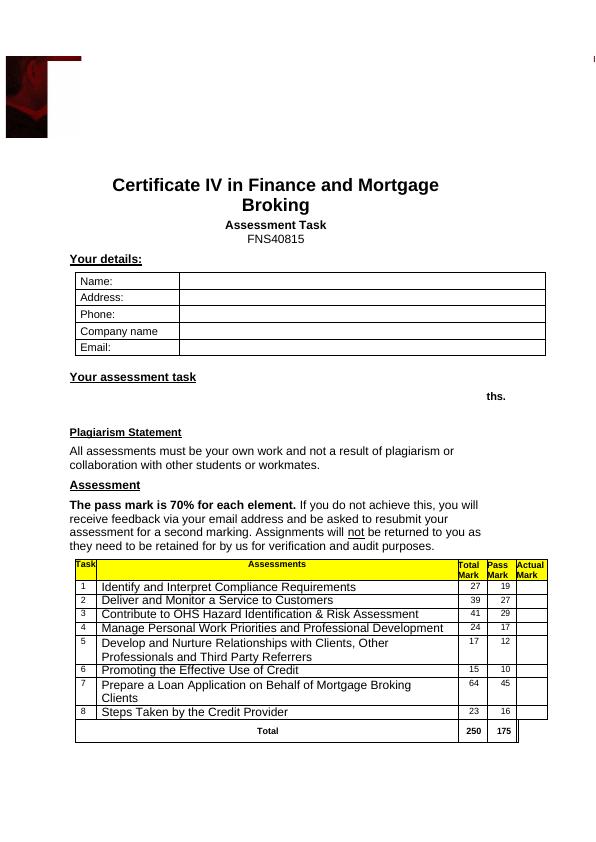

Certificate IV in Finance and Mortgage

Broking

Assessment Task

FNS40815

Your details:

Name:

Address:

Phone:

Company name

Email:

Your assessment task

ths.

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or

collaboration with other students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will

receive feedback via your email address and be asked to resubmit your

assessment for a second marking. Assignments will not be returned to you as

they need to be retained for by us for verification and audit purposes.

Task Assessments Total

Mark

Pass

Mark

Actual

Mark

1 Identify and Interpret Compliance Requirements 27 19

2 Deliver and Monitor a Service to Customers 39 27

3 Contribute to OHS Hazard Identification & Risk Assessment 41 29

4 Manage Personal Work Priorities and Professional Development 24 17

5 Develop and Nurture Relationships with Clients, Other

Professionals and Third Party Referrers

17 12

6 Promoting the Effective Use of Credit 15 10

7 Prepare a Loan Application on Behalf of Mortgage Broking

Clients

64 45

8 Steps Taken by the Credit Provider 23 16

Total 250 175

Broking

Assessment Task

FNS40815

Your details:

Name:

Address:

Phone:

Company name

Email:

Your assessment task

ths.

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or

collaboration with other students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will

receive feedback via your email address and be asked to resubmit your

assessment for a second marking. Assignments will not be returned to you as

they need to be retained for by us for verification and audit purposes.

Task Assessments Total

Mark

Pass

Mark

Actual

Mark

1 Identify and Interpret Compliance Requirements 27 19

2 Deliver and Monitor a Service to Customers 39 27

3 Contribute to OHS Hazard Identification & Risk Assessment 41 29

4 Manage Personal Work Priorities and Professional Development 24 17

5 Develop and Nurture Relationships with Clients, Other

Professionals and Third Party Referrers

17 12

6 Promoting the Effective Use of Credit 15 10

7 Prepare a Loan Application on Behalf of Mortgage Broking

Clients

64 45

8 Steps Taken by the Credit Provider 23 16

Total 250 175

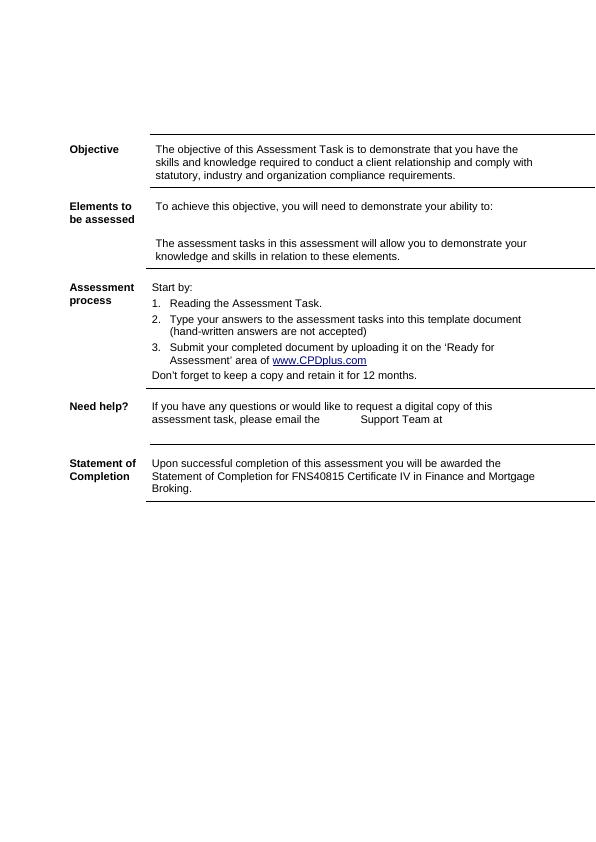

Assessor’s Initials:

Assessment Date:

Assessment Date:

Objective The objective of this Assessment Task is to demonstrate that you have the

skills and knowledge required to conduct a client relationship and comply with

statutory, industry and organization compliance requirements.

Elements to

be assessed

To achieve this objective, you will need to demonstrate your ability to:

The assessment tasks in this assessment will allow you to demonstrate your

knowledge and skills in relation to these elements.

Assessment

process

Start by:

1. Reading the Assessment Task.

2. Type your answers to the assessment tasks into this template document

(hand-written answers are not accepted)

3. Submit your completed document by uploading it on the ‘Ready for

Assessment’ area of www.CPDplus.com

Don’t forget to keep a copy and retain it for 12 months.

Need help? If you have any questions or would like to request a digital copy of this

assessment task, please email the Support Team at

Statement of

Completion

Upon successful completion of this assessment you will be awarded the

Statement of Completion for FNS40815 Certificate IV in Finance and Mortgage

Broking.

skills and knowledge required to conduct a client relationship and comply with

statutory, industry and organization compliance requirements.

Elements to

be assessed

To achieve this objective, you will need to demonstrate your ability to:

The assessment tasks in this assessment will allow you to demonstrate your

knowledge and skills in relation to these elements.

Assessment

process

Start by:

1. Reading the Assessment Task.

2. Type your answers to the assessment tasks into this template document

(hand-written answers are not accepted)

3. Submit your completed document by uploading it on the ‘Ready for

Assessment’ area of www.CPDplus.com

Don’t forget to keep a copy and retain it for 12 months.

Need help? If you have any questions or would like to request a digital copy of this

assessment task, please email the Support Team at

Statement of

Completion

Upon successful completion of this assessment you will be awarded the

Statement of Completion for FNS40815 Certificate IV in Finance and Mortgage

Broking.

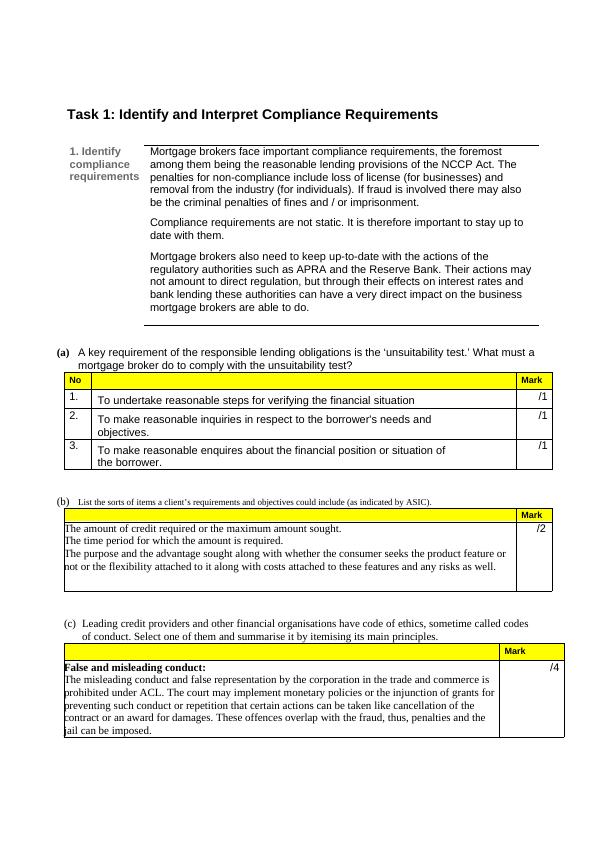

Task 1: Identify and Interpret Compliance Requirements

1. Identify

compliance

requirements

Mortgage brokers face important compliance requirements, the foremost

among them being the reasonable lending provisions of the NCCP Act. The

penalties for non-compliance include loss of license (for businesses) and

removal from the industry (for individuals). If fraud is involved there may also

be the criminal penalties of fines and / or imprisonment.

Compliance requirements are not static. It is therefore important to stay up to

date with them.

Mortgage brokers also need to keep up-to-date with the actions of the

regulatory authorities such as APRA and the Reserve Bank. Their actions may

not amount to direct regulation, but through their effects on interest rates and

bank lending these authorities can have a very direct impact on the business

mortgage brokers are able to do.

(a) A key requirement of the responsible lending obligations is the ‘unsuitability test.’ What must a

mortgage broker do to comply with the unsuitability test?

No Mark

1. To undertake reasonable steps for verifying the financial situation /1

2. To make reasonable inquiries in respect to the borrower's needs and

objectives.

/1

3. To make reasonable enquires about the financial position or situation of

the borrower.

/1

(b) List the sorts of items a client’s requirements and objectives could include (as indicated by ASIC).

Mark

The amount of credit required or the maximum amount sought.

The time period for which the amount is required.

The purpose and the advantage sought along with whether the consumer seeks the product feature or

not or the flexibility attached to it along with costs attached to these features and any risks as well.

/2

(c) Leading credit providers and other financial organisations have code of ethics, sometime called codes

of conduct. Select one of them and summarise it by itemising its main principles.

Mark

False and misleading conduct:

The misleading conduct and false representation by the corporation in the trade and commerce is

prohibited under ACL. The court may implement monetary policies or the injunction of grants for

preventing such conduct or repetition that certain actions can be taken like cancellation of the

contract or an award for damages. These offences overlap with the fraud, thus, penalties and the

jail can be imposed.

/4

1. Identify

compliance

requirements

Mortgage brokers face important compliance requirements, the foremost

among them being the reasonable lending provisions of the NCCP Act. The

penalties for non-compliance include loss of license (for businesses) and

removal from the industry (for individuals). If fraud is involved there may also

be the criminal penalties of fines and / or imprisonment.

Compliance requirements are not static. It is therefore important to stay up to

date with them.

Mortgage brokers also need to keep up-to-date with the actions of the

regulatory authorities such as APRA and the Reserve Bank. Their actions may

not amount to direct regulation, but through their effects on interest rates and

bank lending these authorities can have a very direct impact on the business

mortgage brokers are able to do.

(a) A key requirement of the responsible lending obligations is the ‘unsuitability test.’ What must a

mortgage broker do to comply with the unsuitability test?

No Mark

1. To undertake reasonable steps for verifying the financial situation /1

2. To make reasonable inquiries in respect to the borrower's needs and

objectives.

/1

3. To make reasonable enquires about the financial position or situation of

the borrower.

/1

(b) List the sorts of items a client’s requirements and objectives could include (as indicated by ASIC).

Mark

The amount of credit required or the maximum amount sought.

The time period for which the amount is required.

The purpose and the advantage sought along with whether the consumer seeks the product feature or

not or the flexibility attached to it along with costs attached to these features and any risks as well.

/2

(c) Leading credit providers and other financial organisations have code of ethics, sometime called codes

of conduct. Select one of them and summarise it by itemising its main principles.

Mark

False and misleading conduct:

The misleading conduct and false representation by the corporation in the trade and commerce is

prohibited under ACL. The court may implement monetary policies or the injunction of grants for

preventing such conduct or repetition that certain actions can be taken like cancellation of the

contract or an award for damages. These offences overlap with the fraud, thus, penalties and the

jail can be imposed.

/4

Sub-total /9

Continued

(d) In point form, list the key information that the NCCP Act requires to be contained in a Credit Guide.

Mark

The following points must be contained in the credit guide:

The name, contact details along with the Australian credit license number of the licensee.

Details on account of any charges to be payable by the consumer.

Details of the commission to be received from the lender.

Information about the complaint handling, contact details of the dispute resolution procedures.

Details in respect to the licensee’s obligation for providing the written copy of an unsuitability

assessment on the request.

/3

(e) It is important to keep up to date with compliance requirements so that the required changes can be made to

organization procedures and product offerings. Suggest three sources that you can use.

Mark

1. The professional associations practice can be utilized as the sound system or the guidance in order to

meet with the compliance rules.

2. The professional associations like MFAA and the FBAA can inform its members about the changes

before it takes place.

3. The compliance officers of the mortgage broking companies who can provide assistance to the

practitioners in meeting with the compliance standards.

/3

(f) Explain the requirement for Australian Credit Licensees to keep a training register.

Mark

ASIC requires that the business is required to document as compliance measure which might vary with the level

of documentation in the larger and the smaller organization. As the compliance system is established, it is then

implemented and monitored. Training has a crucial role in this process but it is not sufficient. The Compliance

and the ethical aspect should become the dominant value in the business. It involves the training courses and the

individuals assessment services for the financial advisers.

/2

(g) Explain APRA’s current attitude towards bank lending for investment properties.

Mark

APRA has imposed certain restriction which had an impact over the property investment lending. The banks

have responded to the same by making changes in the serviceability needs and making it difficult for the take

finance by the investors. The borrowing ability has reduced and interest rates have increased and repayment on

the loan is at the huge rate.

/2

Sub-total / 10

Continued

Continued

(d) In point form, list the key information that the NCCP Act requires to be contained in a Credit Guide.

Mark

The following points must be contained in the credit guide:

The name, contact details along with the Australian credit license number of the licensee.

Details on account of any charges to be payable by the consumer.

Details of the commission to be received from the lender.

Information about the complaint handling, contact details of the dispute resolution procedures.

Details in respect to the licensee’s obligation for providing the written copy of an unsuitability

assessment on the request.

/3

(e) It is important to keep up to date with compliance requirements so that the required changes can be made to

organization procedures and product offerings. Suggest three sources that you can use.

Mark

1. The professional associations practice can be utilized as the sound system or the guidance in order to

meet with the compliance rules.

2. The professional associations like MFAA and the FBAA can inform its members about the changes

before it takes place.

3. The compliance officers of the mortgage broking companies who can provide assistance to the

practitioners in meeting with the compliance standards.

/3

(f) Explain the requirement for Australian Credit Licensees to keep a training register.

Mark

ASIC requires that the business is required to document as compliance measure which might vary with the level

of documentation in the larger and the smaller organization. As the compliance system is established, it is then

implemented and monitored. Training has a crucial role in this process but it is not sufficient. The Compliance

and the ethical aspect should become the dominant value in the business. It involves the training courses and the

individuals assessment services for the financial advisers.

/2

(g) Explain APRA’s current attitude towards bank lending for investment properties.

Mark

APRA has imposed certain restriction which had an impact over the property investment lending. The banks

have responded to the same by making changes in the serviceability needs and making it difficult for the take

finance by the investors. The borrowing ability has reduced and interest rates have increased and repayment on

the loan is at the huge rate.

/2

Sub-total / 10

Continued

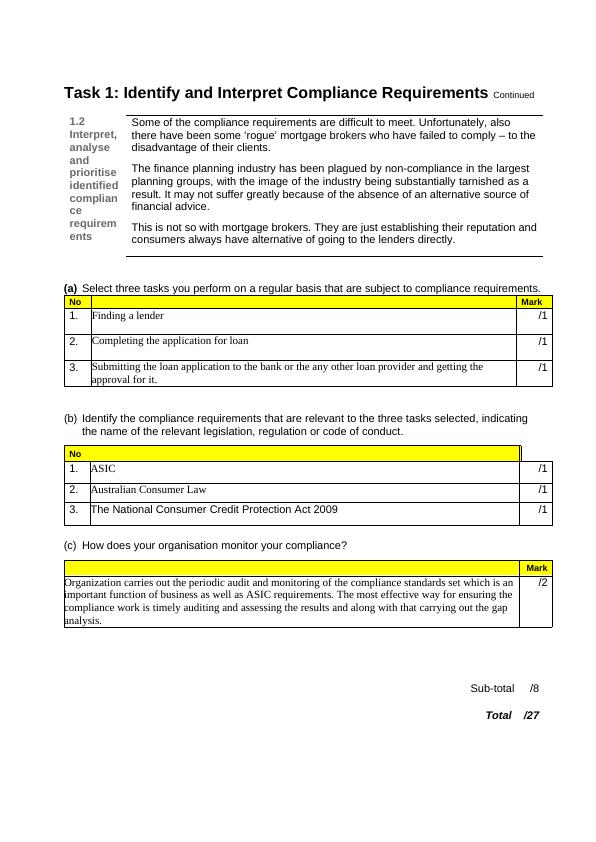

Task 1: Identify and Interpret Compliance Requirements Continued

1.2

Interpret,

analyse

and

prioritise

identified

complian

ce

requirem

ents

Some of the compliance requirements are difficult to meet. Unfortunately, also

there have been some ‘rogue’ mortgage brokers who have failed to comply – to the

disadvantage of their clients.

The finance planning industry has been plagued by non-compliance in the largest

planning groups, with the image of the industry being substantially tarnished as a

result. It may not suffer greatly because of the absence of an alternative source of

financial advice.

This is not so with mortgage brokers. They are just establishing their reputation and

consumers always have alternative of going to the lenders directly.

(a) Select three tasks you perform on a regular basis that are subject to compliance requirements.

No Mark

1. Finding a lender /1

2. Completing the application for loan /1

3. Submitting the loan application to the bank or the any other loan provider and getting the

approval for it.

/1

(b) Identify the compliance requirements that are relevant to the three tasks selected, indicating

the name of the relevant legislation, regulation or code of conduct.

No

1. ASIC /1

2. Australian Consumer Law /1

3. The National Consumer Credit Protection Act 2009 /1

(c) How does your organisation monitor your compliance?

Mark

Organization carries out the periodic audit and monitoring of the compliance standards set which is an

important function of business as well as ASIC requirements. The most effective way for ensuring the

compliance work is timely auditing and assessing the results and along with that carrying out the gap

analysis.

/2

Sub-total /8

Total /27

1.2

Interpret,

analyse

and

prioritise

identified

complian

ce

requirem

ents

Some of the compliance requirements are difficult to meet. Unfortunately, also

there have been some ‘rogue’ mortgage brokers who have failed to comply – to the

disadvantage of their clients.

The finance planning industry has been plagued by non-compliance in the largest

planning groups, with the image of the industry being substantially tarnished as a

result. It may not suffer greatly because of the absence of an alternative source of

financial advice.

This is not so with mortgage brokers. They are just establishing their reputation and

consumers always have alternative of going to the lenders directly.

(a) Select three tasks you perform on a regular basis that are subject to compliance requirements.

No Mark

1. Finding a lender /1

2. Completing the application for loan /1

3. Submitting the loan application to the bank or the any other loan provider and getting the

approval for it.

/1

(b) Identify the compliance requirements that are relevant to the three tasks selected, indicating

the name of the relevant legislation, regulation or code of conduct.

No

1. ASIC /1

2. Australian Consumer Law /1

3. The National Consumer Credit Protection Act 2009 /1

(c) How does your organisation monitor your compliance?

Mark

Organization carries out the periodic audit and monitoring of the compliance standards set which is an

important function of business as well as ASIC requirements. The most effective way for ensuring the

compliance work is timely auditing and assessing the results and along with that carrying out the gap

analysis.

/2

Sub-total /8

Total /27

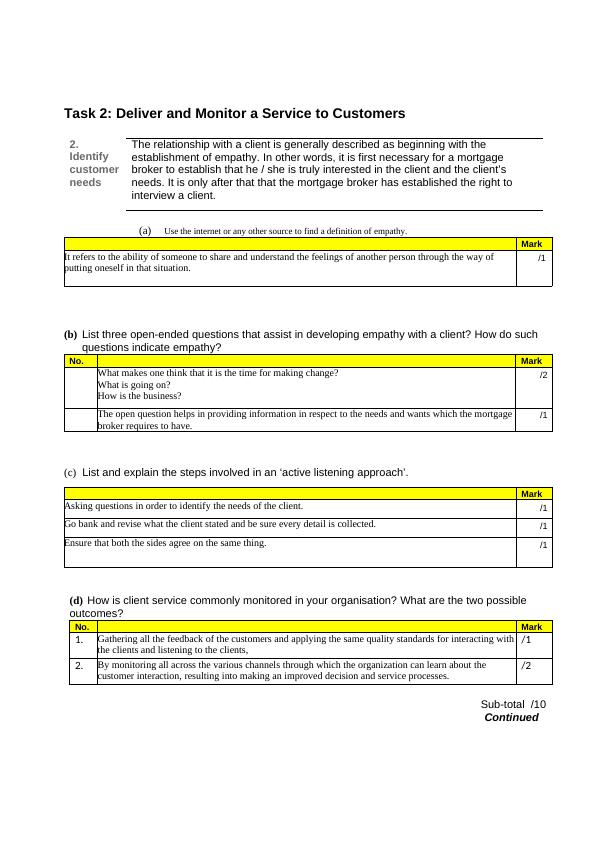

Task 2: Deliver and Monitor a Service to Customers

2.

Identify

customer

needs

The relationship with a client is generally described as beginning with the

establishment of empathy. In other words, it is first necessary for a mortgage

broker to establish that he / she is truly interested in the client and the client’s

needs. It is only after that that the mortgage broker has established the right to

interview a client.

(a) Use the internet or any other source to find a definition of empathy.

Mark

It refers to the ability of someone to share and understand the feelings of another person through the way of

putting oneself in that situation. /1

(b) List three open-ended questions that assist in developing empathy with a client? How do such

questions indicate empathy?

No. Mark

What makes one think that it is the time for making change?

What is going on?

How is the business?

/2

The open question helps in providing information in respect to the needs and wants which the mortgage

broker requires to have.

/1

(c) List and explain the steps involved in an ‘active listening approach’.

Mark

Asking questions in order to identify the needs of the client. /1

Go bank and revise what the client stated and be sure every detail is collected. /1

Ensure that both the sides agree on the same thing. /1

(d) How is client service commonly monitored in your organisation? What are the two possible

outcomes?

No. Mark

1. Gathering all the feedback of the customers and applying the same quality standards for interacting with

the clients and listening to the clients,

/1

2. By monitoring all across the various channels through which the organization can learn about the

customer interaction, resulting into making an improved decision and service processes.

/2

Sub-total /10

Continued

2.

Identify

customer

needs

The relationship with a client is generally described as beginning with the

establishment of empathy. In other words, it is first necessary for a mortgage

broker to establish that he / she is truly interested in the client and the client’s

needs. It is only after that that the mortgage broker has established the right to

interview a client.

(a) Use the internet or any other source to find a definition of empathy.

Mark

It refers to the ability of someone to share and understand the feelings of another person through the way of

putting oneself in that situation. /1

(b) List three open-ended questions that assist in developing empathy with a client? How do such

questions indicate empathy?

No. Mark

What makes one think that it is the time for making change?

What is going on?

How is the business?

/2

The open question helps in providing information in respect to the needs and wants which the mortgage

broker requires to have.

/1

(c) List and explain the steps involved in an ‘active listening approach’.

Mark

Asking questions in order to identify the needs of the client. /1

Go bank and revise what the client stated and be sure every detail is collected. /1

Ensure that both the sides agree on the same thing. /1

(d) How is client service commonly monitored in your organisation? What are the two possible

outcomes?

No. Mark

1. Gathering all the feedback of the customers and applying the same quality standards for interacting with

the clients and listening to the clients,

/1

2. By monitoring all across the various channels through which the organization can learn about the

customer interaction, resulting into making an improved decision and service processes.

/2

Sub-total /10

Continued

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Certificate IV in Finance and Mortgage Broking - Assessmentlg...

|41

|11056

|310

Identify and Interpret Compliance Requirementslg...

|53

|14564

|1

FNS40815 Certificate IV in Finance and Mortgage Brokinglg...

|41

|11459

|2762

Certificate IV in Finance and Mortgage Broking Assessment Tasklg...

|42

|13051

|480

Certificate IV in Finance and Mortgage Broking Assessment Task - Deskliblg...

|15

|5213

|409

FNS40811 Certificate IV in Finance and Mortgage Broking Assignmentlg...

|48

|20179

|30