Develop a Risk Management Strategy

VerifiedAdded on 2022/12/26

|15

|3546

|54

AI Summary

This document discusses the development of a risk management strategy for finance and mortgage broking. It covers the importance of risk management frameworks, the process of risk assessment, and the management of strategic risks. The document provides insights into the various statutes and regulations governing risk management in the financial services sector.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCE AND MORTGAGE

BROKING

BROKING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Page1

FINANCE AND MORTGAGE BROKING

WRITTEN ACTIVITY – 1

Develop a Risk Management Strategy

Introduction

While doing internship with The Institute of Risk Management (IRM), which is my

dream destination after completing my studies, this task was given to me for

presentation to Martin Financial Services (MFS), an upcoming Financial Services

organisation. It is now imperative that employers have started recognising that relying

on piecemeal approach towards risks related to credit, market, operational and

regulatory events can prove to be costlier than investing in risk education. In this

context, Chief Risk Officer (CRO) at MFS needs to pay attention towards development

of Strategic Thinking, Communication & Leadership Skills, Innovative Decision-

making and Ethical Judgment. Individual skills of the staff members, who lead the risk

aversion activities within MFS, will also help the RM in providing insight into the

competencies required from stakeholders for developing a risk program which proves to

be sustainable, describes Bernstein, (2012).

(A) Risk Management Frameworks

Financial sector is subject to various risks, some of which can be anticipated, but most

others are sometimes unexpected or cannot be managed effectively. Hence, adoption of

risk management frameworks will help the CRO of MFS in effective planning and

understanding of risks, especially those which have are not going according to

management’s plan, asserts Curtin, (2005). The major advantage of having an effective

risk management framework for MFS is to become pro-active instead of becoming

reactive when managing risks. As per ISO 31000, the standards set for Enterprise Risk

Management are based on the following 7Rs and 4Ts for developing a risk framework,

as per Jones & Ashenden, (2005).

FINANCE AND MORTGAGE BROKING

WRITTEN ACTIVITY – 1

Develop a Risk Management Strategy

Introduction

While doing internship with The Institute of Risk Management (IRM), which is my

dream destination after completing my studies, this task was given to me for

presentation to Martin Financial Services (MFS), an upcoming Financial Services

organisation. It is now imperative that employers have started recognising that relying

on piecemeal approach towards risks related to credit, market, operational and

regulatory events can prove to be costlier than investing in risk education. In this

context, Chief Risk Officer (CRO) at MFS needs to pay attention towards development

of Strategic Thinking, Communication & Leadership Skills, Innovative Decision-

making and Ethical Judgment. Individual skills of the staff members, who lead the risk

aversion activities within MFS, will also help the RM in providing insight into the

competencies required from stakeholders for developing a risk program which proves to

be sustainable, describes Bernstein, (2012).

(A) Risk Management Frameworks

Financial sector is subject to various risks, some of which can be anticipated, but most

others are sometimes unexpected or cannot be managed effectively. Hence, adoption of

risk management frameworks will help the CRO of MFS in effective planning and

understanding of risks, especially those which have are not going according to

management’s plan, asserts Curtin, (2005). The major advantage of having an effective

risk management framework for MFS is to become pro-active instead of becoming

reactive when managing risks. As per ISO 31000, the standards set for Enterprise Risk

Management are based on the following 7Rs and 4Ts for developing a risk framework,

as per Jones & Ashenden, (2005).

Page2

01. Recognition (identifying the risks)

CRO at MFS will need to identify financial risks in accordance with various Acts and

Statutes which govern them, say Bohle & Quinlan, (2000). These include –

(a) The Corporations Act, 2001 which controls laws which deal with business

risks in Australia, both at federal level and interstate level.

(b) The Banking Code of Practice maintains risk standards related to practice

and service in financial services sector for small business customers.

02. Ranking (evaluating the risks)

(a) Two acts applicable for evaluating risks in MFS are Insurance Act,

1973 and Insurance Contracts Act, 1984.

03. Resourcing (through controls)

(a) Controls of financial services to be provided by MFS will be enforced

through ASIC which regulates, through administration of relevant laws to

promote investor’s, creditor’s and consumer’s protection, asserts Holmes,

(2004).

(b) Financial Law controls and regulates insurance, commercial banking, capital

markets and financial services management organizations such as MFS.

04. Reaction (to defunct planning)

(a) The Financial Transaction Reports Act, 1988 is used with the Anti-Money

Laundering and Counter-Terrorism Financing Act, 2006. The main use of

the FTR Act is to assist administrations in enforcing taxation laws and avoid

defunct planning by organizations such as MFS, as per Holmes, (2004).

(b) In this respect all businesses which are to comply with the AML/CTF Act,

2006 also need to comply with the Privacy Act, 1988 with regard to

handling of consumer’s personal information by MFS.

05. Responding (to severe risks)

(a) The Credit Act, 1995 & Consumer Credit (Victoria) Act, 1995 have the

purpose of ensuring transparency in the credit agreements conducted by

MFS.

(b) In Australia, cheques are governed both by the Cheques Act, 1986 (Cth) and

the prevailing Common Law, assert Lingard & Rowlinson, (2005).

06. Reporting and Monitoring (the risk performance)

01. Recognition (identifying the risks)

CRO at MFS will need to identify financial risks in accordance with various Acts and

Statutes which govern them, say Bohle & Quinlan, (2000). These include –

(a) The Corporations Act, 2001 which controls laws which deal with business

risks in Australia, both at federal level and interstate level.

(b) The Banking Code of Practice maintains risk standards related to practice

and service in financial services sector for small business customers.

02. Ranking (evaluating the risks)

(a) Two acts applicable for evaluating risks in MFS are Insurance Act,

1973 and Insurance Contracts Act, 1984.

03. Resourcing (through controls)

(a) Controls of financial services to be provided by MFS will be enforced

through ASIC which regulates, through administration of relevant laws to

promote investor’s, creditor’s and consumer’s protection, asserts Holmes,

(2004).

(b) Financial Law controls and regulates insurance, commercial banking, capital

markets and financial services management organizations such as MFS.

04. Reaction (to defunct planning)

(a) The Financial Transaction Reports Act, 1988 is used with the Anti-Money

Laundering and Counter-Terrorism Financing Act, 2006. The main use of

the FTR Act is to assist administrations in enforcing taxation laws and avoid

defunct planning by organizations such as MFS, as per Holmes, (2004).

(b) In this respect all businesses which are to comply with the AML/CTF Act,

2006 also need to comply with the Privacy Act, 1988 with regard to

handling of consumer’s personal information by MFS.

05. Responding (to severe risks)

(a) The Credit Act, 1995 & Consumer Credit (Victoria) Act, 1995 have the

purpose of ensuring transparency in the credit agreements conducted by

MFS.

(b) In Australia, cheques are governed both by the Cheques Act, 1986 (Cth) and

the prevailing Common Law, assert Lingard & Rowlinson, (2005).

06. Reporting and Monitoring (the risk performance)

Page3

(a) The Financial Services Reform Act, 2001 will monitor the financial services

and products offered by MFS, as per Lingard & Rowlinson, (2005).

07. Reviewing (at appropriate intervals risk management framework)

(a) The Australian Prudential Regulation Authority works as a

statutory authority under the Prudential Regulator set up by the

Commonwealth Government for reviewing the organizations such as MFS

working in the financial services sector, assert Edwards & Bowen, (2005).

Managements of organizations such as MFS are require to formulate their Risk

Aversion Policies so as to –

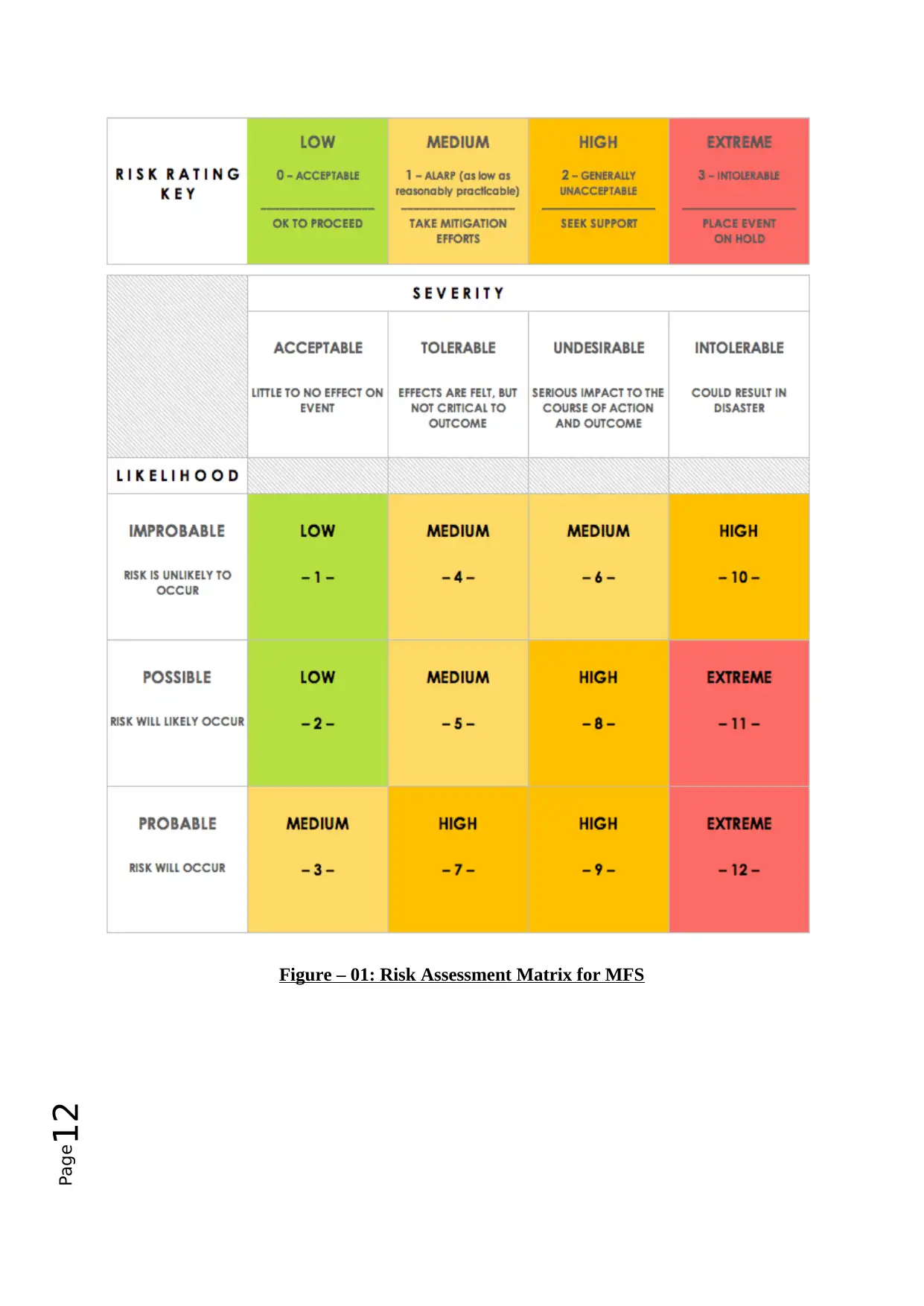

01. Tolerate

Risks having a low probability and potential impact.

02. Treat

Differently risks having moderate probability and potential impact.

03. Transfer

The effect of risks having high probability and potential impact.

04. Terminate

The risks having very high probability and potential impact.

Figure – 01: Risk Assessment Matrix is shown in APPENDIX.

(B) Risk Assessment Process

The process involving development of Risk Management Framework requires risk

assessment of identification, development and evaluation of strategies for risk treatment

of risks associated with MFS. Although the Australian Insurance Law functions on the

line of Commercial Contract Law, it is subjected to regulations which affect the

working of insurance contracts and insurance industry in Australia, as per Mares,

(2008).

This has happened because of the effect created by the Resilience and Collateral

Protection Act, 2016 (Cth), also known as Collateral Protection Act, 2016. This

presents a new security provisions which is applicable to financial property and the

(a) The Financial Services Reform Act, 2001 will monitor the financial services

and products offered by MFS, as per Lingard & Rowlinson, (2005).

07. Reviewing (at appropriate intervals risk management framework)

(a) The Australian Prudential Regulation Authority works as a

statutory authority under the Prudential Regulator set up by the

Commonwealth Government for reviewing the organizations such as MFS

working in the financial services sector, assert Edwards & Bowen, (2005).

Managements of organizations such as MFS are require to formulate their Risk

Aversion Policies so as to –

01. Tolerate

Risks having a low probability and potential impact.

02. Treat

Differently risks having moderate probability and potential impact.

03. Transfer

The effect of risks having high probability and potential impact.

04. Terminate

The risks having very high probability and potential impact.

Figure – 01: Risk Assessment Matrix is shown in APPENDIX.

(B) Risk Assessment Process

The process involving development of Risk Management Framework requires risk

assessment of identification, development and evaluation of strategies for risk treatment

of risks associated with MFS. Although the Australian Insurance Law functions on the

line of Commercial Contract Law, it is subjected to regulations which affect the

working of insurance contracts and insurance industry in Australia, as per Mares,

(2008).

This has happened because of the effect created by the Resilience and Collateral

Protection Act, 2016 (Cth), also known as Collateral Protection Act, 2016. This

presents a new security provisions which is applicable to financial property and the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Page4

Personal Property Securities Act 2009 (Cth), says Mares, (2008). Although this step is

created to compete with international standards which apply to derivative transactions,

its impact does not limit itself only to the risk management markets but also affects

MFS.

Since this Act has a wider effect, it becomes relevant to the organizations, such as MFS

who practice Financial Services under the Finance Law, explains Hiles, (2004). The

following statutes also govern the process of Risk Management –

(a) The Australian Securities and Investments Commission (ASIC), an independent

government body which acts as corporate regulator in Australia.

(b) The Financial Management and Accountability Act, 1997 also regulates proper

management of public property and money.

(c) Financial Sector (Shareholdings) Act, 1998 was enacted for relaxing restrictions

on ownership of banks and insurers.

(d) The National Credit Code (NCC) was inducted for regulating all credit contracts.

NCC is under ASIC and is also included in the National Consumer Credit

Protection Act, 2009.

(e) The Payment Systems and Netting Act, 1998, grants certain legal powers of

protection to banks for approvals under Real-Time Gross Settlement (RTGS).

(f) Enforcement of Corporations Act, 2001 is principally under ASIC which

regulates the disclosure and conduct obligations of financial services providers

such as MFS.

(g) Income Tax Assessment Act, 1997 (ITAA97) is the main statute regulated by the

Australian Taxation Office (ATO) for controlling income tax compliance,

according to Borghesi & Gaudenzi, (2012).

(C) Strategic Risk

Broadly defined as Strategic Risk, this risk basically occurs because CROs of financial

service organizations do not effectively communicate the management’s policies to the

stakeholders connected with Risk Management Procedure, as detailed by Edwards &

Bowen, (2005). Losses resulting because of a badly planned and unsuccessfully

communicated business plan further lead to missed opportunities. Some of the important

factors of such a situation can be creation of ineffective products, ineffective services

due to failure of the staff in responding to changes in MFS’s business environment or

Personal Property Securities Act 2009 (Cth), says Mares, (2008). Although this step is

created to compete with international standards which apply to derivative transactions,

its impact does not limit itself only to the risk management markets but also affects

MFS.

Since this Act has a wider effect, it becomes relevant to the organizations, such as MFS

who practice Financial Services under the Finance Law, explains Hiles, (2004). The

following statutes also govern the process of Risk Management –

(a) The Australian Securities and Investments Commission (ASIC), an independent

government body which acts as corporate regulator in Australia.

(b) The Financial Management and Accountability Act, 1997 also regulates proper

management of public property and money.

(c) Financial Sector (Shareholdings) Act, 1998 was enacted for relaxing restrictions

on ownership of banks and insurers.

(d) The National Credit Code (NCC) was inducted for regulating all credit contracts.

NCC is under ASIC and is also included in the National Consumer Credit

Protection Act, 2009.

(e) The Payment Systems and Netting Act, 1998, grants certain legal powers of

protection to banks for approvals under Real-Time Gross Settlement (RTGS).

(f) Enforcement of Corporations Act, 2001 is principally under ASIC which

regulates the disclosure and conduct obligations of financial services providers

such as MFS.

(g) Income Tax Assessment Act, 1997 (ITAA97) is the main statute regulated by the

Australian Taxation Office (ATO) for controlling income tax compliance,

according to Borghesi & Gaudenzi, (2012).

(C) Strategic Risk

Broadly defined as Strategic Risk, this risk basically occurs because CROs of financial

service organizations do not effectively communicate the management’s policies to the

stakeholders connected with Risk Management Procedure, as detailed by Edwards &

Bowen, (2005). Losses resulting because of a badly planned and unsuccessfully

communicated business plan further lead to missed opportunities. Some of the important

factors of such a situation can be creation of ineffective products, ineffective services

due to failure of the staff in responding to changes in MFS’s business environment or

Page5

because of unplanned resource allocations, assert Bohle & Quinlan, (2000). This is

gathering more importance because organizations, including MFS, are becoming more

dependent on the growing telecommunication technology, as explained by Jones &

Ashenden, (2005). As

a result, many service providers are becoming increasingly exposed to risks which result

because of innovative and disruptive techniques being used by spurious operators,

according to Lingard & Rowlinson, (2005).

For MFS, the Strategic Risks which the CRO has to avert and control include risks

harming MFS brand, its economic policies, MFS’s business models and the overall

competitive position of MFS in the related sector, according to Holmes, (2004). As

explained above, technology is becoming a big threat, hence it needs to be scaled down.

Financial service providers need a secure regulating system to minimize recurring

strategic risks. In order to comprehend all kinds of strategic risks, MFS should focus on

collecting data when focussing on external sources, such as customers, competitors and

the industry analysts. Identification and knowledge about the policies of competitors,

who are offering services and products different from those offered by MFS is essential

for formulating the Strategic Risk Management Policy, explain Edwards & Bowen,

(2005).

because of unplanned resource allocations, assert Bohle & Quinlan, (2000). This is

gathering more importance because organizations, including MFS, are becoming more

dependent on the growing telecommunication technology, as explained by Jones &

Ashenden, (2005). As

a result, many service providers are becoming increasingly exposed to risks which result

because of innovative and disruptive techniques being used by spurious operators,

according to Lingard & Rowlinson, (2005).

For MFS, the Strategic Risks which the CRO has to avert and control include risks

harming MFS brand, its economic policies, MFS’s business models and the overall

competitive position of MFS in the related sector, according to Holmes, (2004). As

explained above, technology is becoming a big threat, hence it needs to be scaled down.

Financial service providers need a secure regulating system to minimize recurring

strategic risks. In order to comprehend all kinds of strategic risks, MFS should focus on

collecting data when focussing on external sources, such as customers, competitors and

the industry analysts. Identification and knowledge about the policies of competitors,

who are offering services and products different from those offered by MFS is essential

for formulating the Strategic Risk Management Policy, explain Edwards & Bowen,

(2005).

Page6

FINANCE AND MORTGAE BROKING

WRITTEN ACTIVITY – 2

Developing an Implementation Plan

Management of Implementation Strategy

Australian regulating agencies expect the financial service providers to implement a

robust policy for managing their strategic risks and this should also include a formalized

process for assessing those risks which emerge in their business model because of ever

changing technology and also because of changes occurring in the external

stakeholder’s positioning, as per Edwards & Bowen, (2005). It is also expected by the

regulating agencies, say Jones & Ashenden, (2005), that all service providers develop

an appropriate structure for systematic assessment of the risks depending on the

strategic choices made by the management.

According to the various statutes and regulations in force, explain Borghesi &

Gaudenzi, (2012), the Chief Risk Officer (CRO) at Martin Financial Services (MFS)

should view Strategic Risks in the context of the below explained three categories. As

per Bernstein, (2012), this will help the CRO in framing those growth and strategy

policies, which are often clouded during discussions, by asking the questions mentioned

hereunder.

1. Strategic Positioning Risks

(a) Is MFS following the right course of action?

(b) Can MFS achieve the strategic objectives set by the management?

FINANCE AND MORTGAE BROKING

WRITTEN ACTIVITY – 2

Developing an Implementation Plan

Management of Implementation Strategy

Australian regulating agencies expect the financial service providers to implement a

robust policy for managing their strategic risks and this should also include a formalized

process for assessing those risks which emerge in their business model because of ever

changing technology and also because of changes occurring in the external

stakeholder’s positioning, as per Edwards & Bowen, (2005). It is also expected by the

regulating agencies, say Jones & Ashenden, (2005), that all service providers develop

an appropriate structure for systematic assessment of the risks depending on the

strategic choices made by the management.

According to the various statutes and regulations in force, explain Borghesi &

Gaudenzi, (2012), the Chief Risk Officer (CRO) at Martin Financial Services (MFS)

should view Strategic Risks in the context of the below explained three categories. As

per Bernstein, (2012), this will help the CRO in framing those growth and strategy

policies, which are often clouded during discussions, by asking the questions mentioned

hereunder.

1. Strategic Positioning Risks

(a) Is MFS following the right course of action?

(b) Can MFS achieve the strategic objectives set by the management?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page7

2. Strategic Execution Risks

(a) Does MFS have the right talent having competent capabilities and the right

infrastructure for executing the chosen strategies?

3. Strategic Consequence Risks

(a) Will the strategic choices of MFS create new risks or unintended

consequences?

Financial service providers, as per Bohle & Quinlan, (2000), require effective

management of their strategic risks for better integration with their stakeholders who are

responsible for managing strategic risks. But recent trends have shown, explain Bohle &

Quinlan, (2000), that emerging organizations such as MFS are taking the management

to new heights. Organizations such as MFS, through their professional managers and

efficient supporting staff, are making these stakeholders to be held responsible by

offering them stock options. This step, according to Winch, (2010); Curtin, (2005), is

allowing the managements to avert risks and also helps them to enforce a strict mandate

of stakeholders holding regular meetings for reviewing the strategic risks through

following steps.

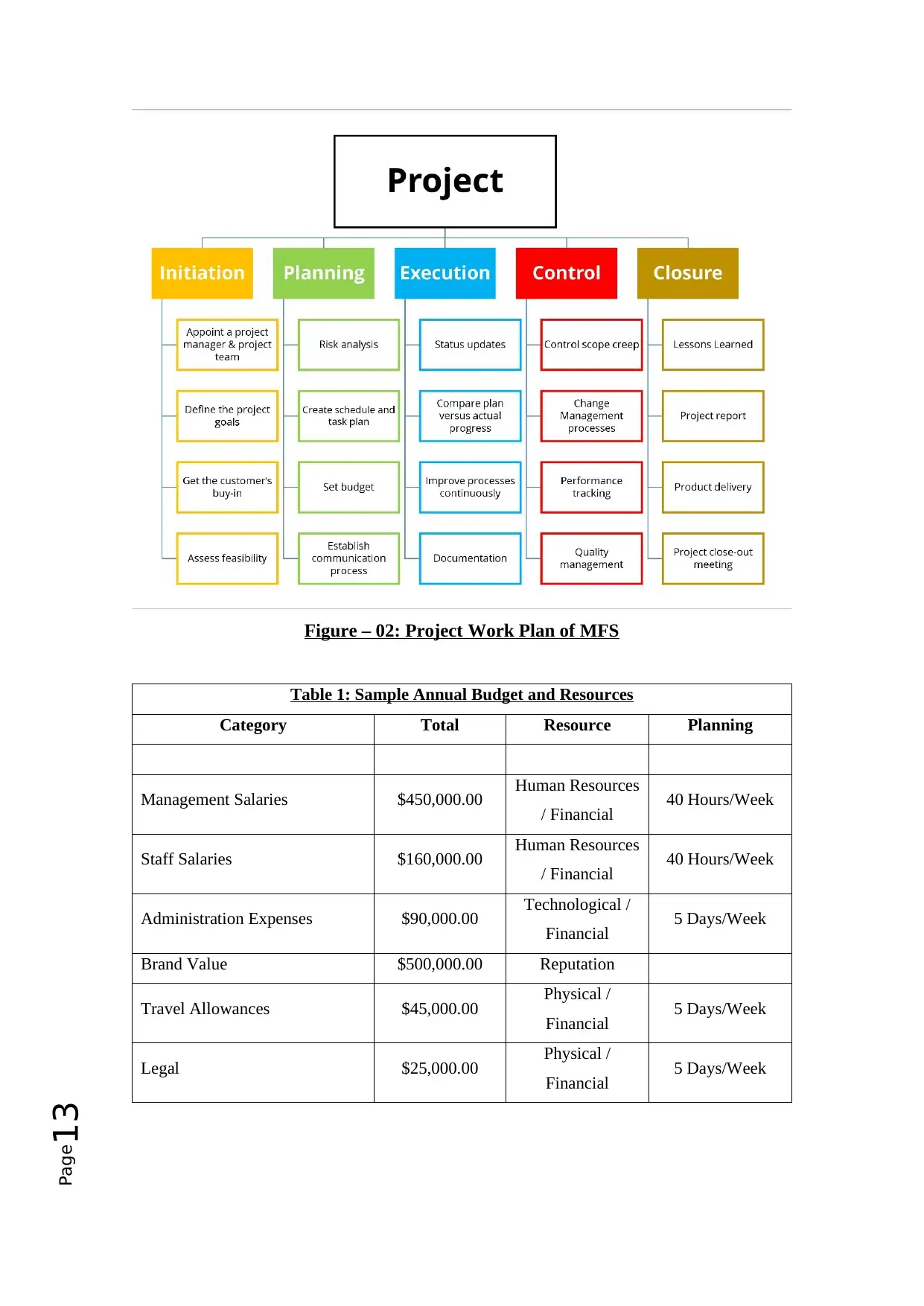

(A) The Work Plan

Basically, the objective of a Project Work Plan (See Figure – 2: Project Work Plan in

Appendix) is to first establish and then communicate with the stakeholders what is

being planned and to ensure that all stakeholders understand that they have a common

goal of implementing the improvements, asserts Bernstein, (2012).

(B) Resources and Budget

Resources for the project and the budget requirements need to be established by the

CRO of MFS in consultation with the management and all the information should be

included within the Implementation Plan being prepared, as per Bernstein, (2012). Care

must be taken to include all the components which are essential for the plan, such as

Salaries, Administrative Costs, Legal Expenses and other Overheads. (See Table 1:

Sample Budget and Resources in Appendix)

(C) Stakeholders

2. Strategic Execution Risks

(a) Does MFS have the right talent having competent capabilities and the right

infrastructure for executing the chosen strategies?

3. Strategic Consequence Risks

(a) Will the strategic choices of MFS create new risks or unintended

consequences?

Financial service providers, as per Bohle & Quinlan, (2000), require effective

management of their strategic risks for better integration with their stakeholders who are

responsible for managing strategic risks. But recent trends have shown, explain Bohle &

Quinlan, (2000), that emerging organizations such as MFS are taking the management

to new heights. Organizations such as MFS, through their professional managers and

efficient supporting staff, are making these stakeholders to be held responsible by

offering them stock options. This step, according to Winch, (2010); Curtin, (2005), is

allowing the managements to avert risks and also helps them to enforce a strict mandate

of stakeholders holding regular meetings for reviewing the strategic risks through

following steps.

(A) The Work Plan

Basically, the objective of a Project Work Plan (See Figure – 2: Project Work Plan in

Appendix) is to first establish and then communicate with the stakeholders what is

being planned and to ensure that all stakeholders understand that they have a common

goal of implementing the improvements, asserts Bernstein, (2012).

(B) Resources and Budget

Resources for the project and the budget requirements need to be established by the

CRO of MFS in consultation with the management and all the information should be

included within the Implementation Plan being prepared, as per Bernstein, (2012). Care

must be taken to include all the components which are essential for the plan, such as

Salaries, Administrative Costs, Legal Expenses and other Overheads. (See Table 1:

Sample Budget and Resources in Appendix)

(C) Stakeholders

Page8

Stakeholders are those persons who can be directly or indirectly affected by the

implementation of the project. These may include project owners, project managers,

staff members responsible for coordinating the project, departments, whether internal or

external, who are supporting the project, suppliers, financial collaborators and the

customers, assert Edwards & Bowen, (2005). To complete this process, it is advisable

that the CRO uses a Stakeholder Analysis Tool (See Figure – 2: Stakeholder Analysis

Tool in Appendix). This facilitates the management in understanding the project

through this visual medium. This also helps all the stakeholders in identifying their

support areas. This will help the CRO in creating an action plan for implementing the

project, according to Winch, (2010); Jones & Ashenden, (2005). Finally, all the

stakeholders make use of

the plan and work as a team for discovering ways to improvise relationships and

strategies for ensuring efficient completion of the project, according to Winch, (2010);

Jones & Ashenden, (2005).

(D) Monitoring Method

The most effective method, according to Hiles, (2004), of monitoring the progress of a

project’s Strategic Risk Management is through the question – Are the goals and

objectives being achieved? In case the answer is YES, the management needs to

acknowledge the fact and communicate the progress to the stakeholders by rewarding

them. In case the answer is NO, then the management must search for answers to the

following questions, as detailed by Lingard & Rowlinson, (2005).

1. Are the goals achievable as per the specified timeline (See Figure – 4: Project

Timeline in Appendix) of the plan? If not, for what reason?

2. Will changing the Timeline help in achieving the set goals?

3. Are adequate resources, such as equipment, money, training and facilities being

provided for achieving the goals?

4. Are the objectives and goals still realistic?

5. Can changing the priorities put more focus on goals being achieved?

6. Will changing the goals help in achieving them?

Monitoring Frequency

Frequency of monitoring and reviewing the progress, assert Mares, (2008); Edwards &

Bowen, (2005), depends largely on the structure and working environment of the

Stakeholders are those persons who can be directly or indirectly affected by the

implementation of the project. These may include project owners, project managers,

staff members responsible for coordinating the project, departments, whether internal or

external, who are supporting the project, suppliers, financial collaborators and the

customers, assert Edwards & Bowen, (2005). To complete this process, it is advisable

that the CRO uses a Stakeholder Analysis Tool (See Figure – 2: Stakeholder Analysis

Tool in Appendix). This facilitates the management in understanding the project

through this visual medium. This also helps all the stakeholders in identifying their

support areas. This will help the CRO in creating an action plan for implementing the

project, according to Winch, (2010); Jones & Ashenden, (2005). Finally, all the

stakeholders make use of

the plan and work as a team for discovering ways to improvise relationships and

strategies for ensuring efficient completion of the project, according to Winch, (2010);

Jones & Ashenden, (2005).

(D) Monitoring Method

The most effective method, according to Hiles, (2004), of monitoring the progress of a

project’s Strategic Risk Management is through the question – Are the goals and

objectives being achieved? In case the answer is YES, the management needs to

acknowledge the fact and communicate the progress to the stakeholders by rewarding

them. In case the answer is NO, then the management must search for answers to the

following questions, as detailed by Lingard & Rowlinson, (2005).

1. Are the goals achievable as per the specified timeline (See Figure – 4: Project

Timeline in Appendix) of the plan? If not, for what reason?

2. Will changing the Timeline help in achieving the set goals?

3. Are adequate resources, such as equipment, money, training and facilities being

provided for achieving the goals?

4. Are the objectives and goals still realistic?

5. Can changing the priorities put more focus on goals being achieved?

6. Will changing the goals help in achieving them?

Monitoring Frequency

Frequency of monitoring and reviewing the progress, assert Mares, (2008); Edwards &

Bowen, (2005), depends largely on the structure and working environment of the

Page9

organization (MFS) under which it is conducting its operations. Organizations, such as

MFS, which are progressive and technology savvy and are experiencing continuous and

rapid changes, both from inside and outside, according to Bernstein, (2012); Holmes,

(2004) will propose to monitor the implementation plan at least once every month. The

CRO should report to the Boards of Directors about the implementation status of the

plan in detail, as per Mares, (2008) Edwards & Bowen, (2005).

Result Reporting

It is essential, as per Bernstein, (2012); Holmes, (2004) for the CRO to submit a written

report and describe the following –

1. Answer the key questions about monitoring the implementation.

2. Accurately report about the trends affecting the progress of the plan in reaching

towards its goals.

3. Recommendations, if any, about the current status of the goals and achievements.

4. Actions, if any, needed to be taken by the management.

(E) Evaluation Methods

Deviating from Plan

The implementation plan serves only as a guideline and should not be followed like a

roadmap, explains Borghesi & Gaudenzi, (2012). The CRO and the management

usually keep changing the direction which the process should take as the plan proceeds

through the period of implementation. Changes made to the plan are done to facilitate

the best possible result outcome and this is technically termed as Evaluation, as per

Curtin, (2005); Borghesi & Gaudenzi, (2012). The plan also reflects changes resulting

because of changes occurring in the external factors which reflect in the organization’s

working environment and its organizational goals. Evaluation also occurs when the

organization faces changes in availability of resources while trying to carry on with the

original plan.

Changing the Plan

The CRO must ensure that a visible mechanism has been identified for making the

changes in the plan, as per Holmes, (2004); Bohle & Quinlan, (2000). In this context,

the CRO must report about the following –

organization (MFS) under which it is conducting its operations. Organizations, such as

MFS, which are progressive and technology savvy and are experiencing continuous and

rapid changes, both from inside and outside, according to Bernstein, (2012); Holmes,

(2004) will propose to monitor the implementation plan at least once every month. The

CRO should report to the Boards of Directors about the implementation status of the

plan in detail, as per Mares, (2008) Edwards & Bowen, (2005).

Result Reporting

It is essential, as per Bernstein, (2012); Holmes, (2004) for the CRO to submit a written

report and describe the following –

1. Answer the key questions about monitoring the implementation.

2. Accurately report about the trends affecting the progress of the plan in reaching

towards its goals.

3. Recommendations, if any, about the current status of the goals and achievements.

4. Actions, if any, needed to be taken by the management.

(E) Evaluation Methods

Deviating from Plan

The implementation plan serves only as a guideline and should not be followed like a

roadmap, explains Borghesi & Gaudenzi, (2012). The CRO and the management

usually keep changing the direction which the process should take as the plan proceeds

through the period of implementation. Changes made to the plan are done to facilitate

the best possible result outcome and this is technically termed as Evaluation, as per

Curtin, (2005); Borghesi & Gaudenzi, (2012). The plan also reflects changes resulting

because of changes occurring in the external factors which reflect in the organization’s

working environment and its organizational goals. Evaluation also occurs when the

organization faces changes in availability of resources while trying to carry on with the

original plan.

Changing the Plan

The CRO must ensure that a visible mechanism has been identified for making the

changes in the plan, as per Holmes, (2004); Bohle & Quinlan, (2000). In this context,

the CRO must report about the following –

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Page10

1. The reasons causing the changes.

2. Is it essential to make the changes?

3. Finally, what changes are required to be made and their effect on the objectives,

goals, management’s responsibilities and Project’s Timeline.

While managing the various versions of the plan due to changes being made to the plan,

the CRO must preserve the old copies of the plan. To facilitate the various stakeholders

in understanding the effects of the changes, the CRO must make written notes about the

planning activities as this will help the management in making their next strategic

planning more accurate and efficient, according to Holmes, (2004); Bohle & Quinlan,

(2000).

REFERENCE LIST

Bernstein, P. L. 2012. Against The Gods. The Remarkable Story of Risk. John Wiley &

Sons, New York.

Bohle, P. and Quinlan, M. 2000. Managing Occupational Health and Safety: A

Multidisciplinary Approach, 2nd ed. Macmillan Education AU, South Yarra.

Borghesi, A. and Gaudenzi, B. 2012. Risk Management: How to Assess, Transfer and

Communicate Critical Risks. Springer, New York.

Curtin, T. 2005. Managing a Crisis. Palgrave Macmillan, New York.

Edwards, P. and Bowen, P. 2005. Risk Management in Project Organisations, 1st ed.

University of New South Wales Press, Sydney.

Hiles, A. 2004. Business Continuity: Best Practices - World-Class Business Continuity

Management, 2nd ed. Rothstein Associates Inc., Brookfield.

Holmes, A. 2004. Smart Risk. Capstone Publishing Limited, West Sussex.

Jones, A and Ashenden, D. 2005. Risk Management for Computer Security. Elsevier

Butterworth – Heinemann, Burlington, MA.

1. The reasons causing the changes.

2. Is it essential to make the changes?

3. Finally, what changes are required to be made and their effect on the objectives,

goals, management’s responsibilities and Project’s Timeline.

While managing the various versions of the plan due to changes being made to the plan,

the CRO must preserve the old copies of the plan. To facilitate the various stakeholders

in understanding the effects of the changes, the CRO must make written notes about the

planning activities as this will help the management in making their next strategic

planning more accurate and efficient, according to Holmes, (2004); Bohle & Quinlan,

(2000).

REFERENCE LIST

Bernstein, P. L. 2012. Against The Gods. The Remarkable Story of Risk. John Wiley &

Sons, New York.

Bohle, P. and Quinlan, M. 2000. Managing Occupational Health and Safety: A

Multidisciplinary Approach, 2nd ed. Macmillan Education AU, South Yarra.

Borghesi, A. and Gaudenzi, B. 2012. Risk Management: How to Assess, Transfer and

Communicate Critical Risks. Springer, New York.

Curtin, T. 2005. Managing a Crisis. Palgrave Macmillan, New York.

Edwards, P. and Bowen, P. 2005. Risk Management in Project Organisations, 1st ed.

University of New South Wales Press, Sydney.

Hiles, A. 2004. Business Continuity: Best Practices - World-Class Business Continuity

Management, 2nd ed. Rothstein Associates Inc., Brookfield.

Holmes, A. 2004. Smart Risk. Capstone Publishing Limited, West Sussex.

Jones, A and Ashenden, D. 2005. Risk Management for Computer Security. Elsevier

Butterworth – Heinemann, Burlington, MA.

Page11

Lingard, H. and Rowlinson, S. 2005. Occupational Health and Safety in Construction

Project Management. Taylor & Francis, Oxon.

Mares, R. 2008. The Dynamics of Corporate Social Responsibilities. Martinus Nijhoff

Publishers, Leiden.

Winch, G. M. 2010. Managing Construction Projects, 2nd ed. John Wiley & Sons, West

Sussex.

APPENDIX

Lingard, H. and Rowlinson, S. 2005. Occupational Health and Safety in Construction

Project Management. Taylor & Francis, Oxon.

Mares, R. 2008. The Dynamics of Corporate Social Responsibilities. Martinus Nijhoff

Publishers, Leiden.

Winch, G. M. 2010. Managing Construction Projects, 2nd ed. John Wiley & Sons, West

Sussex.

APPENDIX

Page12

Figure – 01: Risk Assessment Matrix for MFS

Figure – 01: Risk Assessment Matrix for MFS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page13

Figure – 02: Project Work Plan of MFS

Table 1: Sample Annual Budget and Resources

Category Total Resource Planning

Management Salaries $450,000.00 Human Resources

/ Financial 40 Hours/Week

Staff Salaries $160,000.00 Human Resources

/ Financial 40 Hours/Week

Administration Expenses $90,000.00 Technological /

Financial 5 Days/Week

Brand Value $500,000.00 Reputation

Travel Allowances $45,000.00 Physical /

Financial 5 Days/Week

Legal $25,000.00 Physical /

Financial 5 Days/Week

Figure – 02: Project Work Plan of MFS

Table 1: Sample Annual Budget and Resources

Category Total Resource Planning

Management Salaries $450,000.00 Human Resources

/ Financial 40 Hours/Week

Staff Salaries $160,000.00 Human Resources

/ Financial 40 Hours/Week

Administration Expenses $90,000.00 Technological /

Financial 5 Days/Week

Brand Value $500,000.00 Reputation

Travel Allowances $45,000.00 Physical /

Financial 5 Days/Week

Legal $25,000.00 Physical /

Financial 5 Days/Week

Page14

Figure - 03: Stakeholder Analysis Tool

Figure - 04: Project Timeline

Figure - 03: Stakeholder Analysis Tool

Figure - 04: Project Timeline

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.