Kerry Group's Financial and Strategic Management

VerifiedAdded on 2020/10/22

|13

|3411

|375

AI Summary

The assignment provides an analysis of Kerry Group's financial and strategic management in 2016. It discusses the company's focus on unique taste, nutrition, and functional ingredients, as well as its ability to adapt to changing market conditions. The report also explores Kerry Group's performance during the interim period, including revenue growth and strategic acquisitions. Overall, the assignment aims to provide a comprehensive understanding of Kerry Group's financial and strategic management practices.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCE AND STRATEGIC MANAGEMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

KERRY GROUP.............................................................................................................................3

Overall Interim performance.......................................................................................................3

Directors point of view.............................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

KERRY GROUP.............................................................................................................................3

Overall Interim performance.......................................................................................................3

Directors point of view.............................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Finance and strategic management is considered as study of funding with perspective of

long term aspect, which considers various strategic business enterprise. In the present scenario,

financial management is increasing in rapid aspect for the purpose of developing set of decisions.

It refers to particular planning for application of management for organizational financial

resources to accomplish its objectives and goals. Managing control over funds helps the business

in maximising value of shareholders for a long run. The present report has target organization

with financial and strategic management of Kerry Group. It will articulate directors point of view

with context to problems linked with financial and strategic management. In the same series, it

will also present information related to overall interim performance of year 2016. With the

context of interim performance, it had stated consolidated interim financial position of specific

business entity with its debt position.

KERRY GROUP

Kerry Group plc along with its subsidiaries manufacture, delivers and develop technology

which is based on nutrition and taste solution for beverages, pharmaceutical industries and food

in Europe, America, Asia pacific, Middle East and Africa. Generally, it operates in two segments

which are classified as Consumer food and nutrition manufacturers. The segment of consumer

food manufacturers and supply branded chilled food and added value branded food to Irish and

in market of United Kingdom. It also offers dairy products, meat, savoury products and various

meal solutions with retailer’s perspective to e-commerce channels and convenience stores under

different brands such as Dairygold, Fire & smoke, Galtee, Cheestrings and many more. The

products with private label are also produced such as, meals which are chilled and frozen, dairy

and cheese products and cooked meat. The taste and nutrition segment distribute and

manufactures portfolio of functional activities and ingredients as they offer technologies of

nutrition and taste along with system and solutions.

Overall Interim performance

Kerry Group has stated solid financial performance for the interim duration of year 2016.

Its overall performance had been highlighted with improvement in quality and operational

process along with increment in trading profits by 7.4% to 322 m and 70 basis points to 10.6%.

In the same series, there dividend got raised to 16.8% from 12%. In first half of 2016, firm

achieved growth by challenging different market conditions, slow economic growth, instability

3

Finance and strategic management is considered as study of funding with perspective of

long term aspect, which considers various strategic business enterprise. In the present scenario,

financial management is increasing in rapid aspect for the purpose of developing set of decisions.

It refers to particular planning for application of management for organizational financial

resources to accomplish its objectives and goals. Managing control over funds helps the business

in maximising value of shareholders for a long run. The present report has target organization

with financial and strategic management of Kerry Group. It will articulate directors point of view

with context to problems linked with financial and strategic management. In the same series, it

will also present information related to overall interim performance of year 2016. With the

context of interim performance, it had stated consolidated interim financial position of specific

business entity with its debt position.

KERRY GROUP

Kerry Group plc along with its subsidiaries manufacture, delivers and develop technology

which is based on nutrition and taste solution for beverages, pharmaceutical industries and food

in Europe, America, Asia pacific, Middle East and Africa. Generally, it operates in two segments

which are classified as Consumer food and nutrition manufacturers. The segment of consumer

food manufacturers and supply branded chilled food and added value branded food to Irish and

in market of United Kingdom. It also offers dairy products, meat, savoury products and various

meal solutions with retailer’s perspective to e-commerce channels and convenience stores under

different brands such as Dairygold, Fire & smoke, Galtee, Cheestrings and many more. The

products with private label are also produced such as, meals which are chilled and frozen, dairy

and cheese products and cooked meat. The taste and nutrition segment distribute and

manufactures portfolio of functional activities and ingredients as they offer technologies of

nutrition and taste along with system and solutions.

Overall Interim performance

Kerry Group has stated solid financial performance for the interim duration of year 2016.

Its overall performance had been highlighted with improvement in quality and operational

process along with increment in trading profits by 7.4% to 322 m and 70 basis points to 10.6%.

In the same series, there dividend got raised to 16.8% from 12%. In first half of 2016, firm

achieved growth by challenging different market conditions, slow economic growth, instability

3

of geopolitical factors in specific developing market and currency volatility. In the same series,

there is increment in retail fragmentation, penetration of regional brands, online shopping and

ongoing growth with context of snacking had contributed for churning of significant product

along with raise in demand of product differentiation and offering in innovative aspect. The trend

of consumer reflects growth with reference to wealth, natural, health offerings and specific

propositions of clean label which, is highly focused on increasing attention towards development

of both segments and demand for meal solutions.

The combination of nutrition, taste and capabilities of general wellness along with

approach of unique system which had continued for increment in engaging customer and various

innovation. The Asia had attained strong growth in channel of food service in every region. In

the year 2015, internationalisation and integration with reference to business had been acquired

as its outcome was successful progress. The UK and Irish consumer food are very competitive

for alterations in market place and uncertainty of economy in market of UK. The portfolio had

been repositioned for continuing its performance with advantages such as convenience and

snacking trend. The growth rate of market was outperforming with proper maintenance of

momentum of good business. The revenue of group was not changed at €3 billion which

articulate appropriate growth of volume, as it is outset through movements in currency and

pricing had been lowered with context of first half of year 2015. The growth had been observed

in business volume by 3.2% which reflects very good performance of firm in market of America.

However, growth of volume was lower in EMEA region with context of specific regional

developing market. Simultaneously there was strong momentum of business growth in Asia.

Against the background its net pricing decreased by 2.2% and in same series cost of raw material

by approx. 4%.

In the year 2016, 3.5% growth was attained through taste and Nutrition with context of

volume of business and its pricing was lowered by 2.2%. In the same series, volume of Kerry's

food business was increased by2.3% and pricing were decreased by 2.1%. There was continuous

improvement in overall quality of business and efficiency of operations. There was increment in

trading profit by 7.4% with €322 million. It could be interpreted that its trading profit margin

was raised through 70 bps to 10.6%. It reflects that improvement of 70 bps in trading margin

with 12.8% in taste and nutrition and 30 bps with context of consumer food as it is margining to

8.3% and decreases spending on its connect programs with contribution of 10 bps. The earning

4

there is increment in retail fragmentation, penetration of regional brands, online shopping and

ongoing growth with context of snacking had contributed for churning of significant product

along with raise in demand of product differentiation and offering in innovative aspect. The trend

of consumer reflects growth with reference to wealth, natural, health offerings and specific

propositions of clean label which, is highly focused on increasing attention towards development

of both segments and demand for meal solutions.

The combination of nutrition, taste and capabilities of general wellness along with

approach of unique system which had continued for increment in engaging customer and various

innovation. The Asia had attained strong growth in channel of food service in every region. In

the year 2015, internationalisation and integration with reference to business had been acquired

as its outcome was successful progress. The UK and Irish consumer food are very competitive

for alterations in market place and uncertainty of economy in market of UK. The portfolio had

been repositioned for continuing its performance with advantages such as convenience and

snacking trend. The growth rate of market was outperforming with proper maintenance of

momentum of good business. The revenue of group was not changed at €3 billion which

articulate appropriate growth of volume, as it is outset through movements in currency and

pricing had been lowered with context of first half of year 2015. The growth had been observed

in business volume by 3.2% which reflects very good performance of firm in market of America.

However, growth of volume was lower in EMEA region with context of specific regional

developing market. Simultaneously there was strong momentum of business growth in Asia.

Against the background its net pricing decreased by 2.2% and in same series cost of raw material

by approx. 4%.

In the year 2016, 3.5% growth was attained through taste and Nutrition with context of

volume of business and its pricing was lowered by 2.2%. In the same series, volume of Kerry's

food business was increased by2.3% and pricing were decreased by 2.1%. There was continuous

improvement in overall quality of business and efficiency of operations. There was increment in

trading profit by 7.4% with €322 million. It could be interpreted that its trading profit margin

was raised through 70 bps to 10.6%. It reflects that improvement of 70 bps in trading margin

with 12.8% in taste and nutrition and 30 bps with context of consumer food as it is margining to

8.3% and decreases spending on its connect programs with contribution of 10 bps. The earning

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

per share was raised from 7.5% to 133.8 cent. In the same series its basic earnings per share was

reduced through 6.5% as 126.4. The dividend of H1 is of 16.8 cent per share with 12% increment

from year 2015.

Growth volume

1st half of year 2016

Total revenue 2379 million

Trading profit 304 million

Trading margin 12.80%

The innovative and largest portfolio had been provided through Kerry with context to

taste and nutrition solution. Further, various functional ingredients and actives for different

beverage, global food and pharmaceutical industry. Kerry's portfolio of taste and nutrition along

with general wellness had enabled platform of technology which had continued its advantages by

making services easy available for consumer who prefer local food, health and wellness.

Generally, consumers demand clean, simple edibles with clear labelling, functional indulgence,

variety in culinary and enhanced nutritional value. It had indirectly driven requirements of retail

and food services with innovation and market ready solutions. In the same series, Kerry was

capable to maintain a specific and strong innovation and pipeline with context to every region in

particular duration along with acquisition investment in year 2015 which had achieved progress

integration of each acquired business. The acquired technologies are broadening with reference

to every region for developing unique taste and nutrition application. These businesses is

performing well for giving significant scope with context to expanding in international market.

There was increment in revenue by €2,379 million through taste and nutrition which reflects

growth of 3.5% in business volume and states 2.2% lower net pricing.

Growth in volume in each region

5

reduced through 6.5% as 126.4. The dividend of H1 is of 16.8 cent per share with 12% increment

from year 2015.

Growth volume

1st half of year 2016

Total revenue 2379 million

Trading profit 304 million

Trading margin 12.80%

The innovative and largest portfolio had been provided through Kerry with context to

taste and nutrition solution. Further, various functional ingredients and actives for different

beverage, global food and pharmaceutical industry. Kerry's portfolio of taste and nutrition along

with general wellness had enabled platform of technology which had continued its advantages by

making services easy available for consumer who prefer local food, health and wellness.

Generally, consumers demand clean, simple edibles with clear labelling, functional indulgence,

variety in culinary and enhanced nutritional value. It had indirectly driven requirements of retail

and food services with innovation and market ready solutions. In the same series, Kerry was

capable to maintain a specific and strong innovation and pipeline with context to every region in

particular duration along with acquisition investment in year 2015 which had achieved progress

integration of each acquired business. The acquired technologies are broadening with reference

to every region for developing unique taste and nutrition application. These businesses is

performing well for giving significant scope with context to expanding in international market.

There was increment in revenue by €2,379 million through taste and nutrition which reflects

growth of 3.5% in business volume and states 2.2% lower net pricing.

Growth in volume in each region

5

Illustration 1: Volume growth by

Region

(Source: Kerry Interim Management

Report, 2016)

Americas Region

Solid performance had been maintained by Kerry in North America and its performance

was improved in market of Latin American in year 2016. In the same series, its performance was

boosted through technology which was acquired by firm in 2015. This reflected progress for

integration of its acquisitions strategy. The sales revenue was increased by 15.2% to €1244

million which reflects progress of business volume by 3.5% and lower pricing by 2%.

EMEA Region

The market conditions of EMEA was challenging because of continuous price deflation

with reference to regional developed markets and geopolitical instability. There was presence of

significant product churn which is considered as dominant market feature of manufacturers of

food and beverages. and various retailers had responded competitively for raising consumer

demand for purpose of enhancing convenience line and nutritional offerings with context to

deflationary environment. There was appropriate growth in regional food service sector for

giving the best growth opportunity with reference to consumer proposition of Kerry. The sales

revenue of 734 million is representing business volume as it signifies specific growth in volume

of business of 0.3% and lower pricing for 2.7%. The growth of competitive market was

6

Region

(Source: Kerry Interim Management

Report, 2016)

Americas Region

Solid performance had been maintained by Kerry in North America and its performance

was improved in market of Latin American in year 2016. In the same series, its performance was

boosted through technology which was acquired by firm in 2015. This reflected progress for

integration of its acquisitions strategy. The sales revenue was increased by 15.2% to €1244

million which reflects progress of business volume by 3.5% and lower pricing by 2%.

EMEA Region

The market conditions of EMEA was challenging because of continuous price deflation

with reference to regional developed markets and geopolitical instability. There was presence of

significant product churn which is considered as dominant market feature of manufacturers of

food and beverages. and various retailers had responded competitively for raising consumer

demand for purpose of enhancing convenience line and nutritional offerings with context to

deflationary environment. There was appropriate growth in regional food service sector for

giving the best growth opportunity with reference to consumer proposition of Kerry. The sales

revenue of 734 million is representing business volume as it signifies specific growth in volume

of business of 0.3% and lower pricing for 2.7%. The growth of competitive market was

6

developed along with economic and geopolitical issues which directly gives challenging impacts

on market place.

Asia pacific

Kerry attained excellent performance in H1 of Asia pacific region. There was

establishment of technologies for market development across regional markets which is highly

successful. The volume of business had raised by 9.5% and net pricing was lowered by 1.8%.

The total reported revenue was €367 million which represents decrement of 11.4% because of

business disposal which gives adverse impact on net acquisitions and translation of negative

currency provides major impact of 5.8%. The key drivers of firm are its food service, beverage

and food service as it helps enterprise in managing continuous growth via lifestyle nutrition.

As per its financial outcomes it is struggling with its market scope, solid performance had

been delivered by market expansion, appropriate cash generation by 7.5% increment in its

adjusted earnings per share. Kerry Group had kept its performance in very efficient aspect,

especially in North America as it had improved its performance in Latin America Its growth was

lowered in EMEA region which had contrasted with 0.3% and simultaneously excellent

performance in Asia with increased volume of business by 9.5%.

Consumer foods

1st half of year 2016

Total revenue 697 million

Trading profit 58 million

Trading margin 8.30%

There are various conditions of trading in consumer food market of UK and Irish which

are very competitive due to adaption of alteration in market landscape through its retailers,

different consumer trend which consist of e-tail's growth and trends which are deflationary.

Market share was gained by discounters as they had continued for broadening r focus of retailer

on EDLP strategies. Its volume growth was directly led by strong performance with context of

meal solutions. With reference to its trading profit it improved business which is underlying and

offset via currency and disposals. Its margin improved and driven via efficiency program on

ongoing aspect and portfolio had been repositioned.

7

on market place.

Asia pacific

Kerry attained excellent performance in H1 of Asia pacific region. There was

establishment of technologies for market development across regional markets which is highly

successful. The volume of business had raised by 9.5% and net pricing was lowered by 1.8%.

The total reported revenue was €367 million which represents decrement of 11.4% because of

business disposal which gives adverse impact on net acquisitions and translation of negative

currency provides major impact of 5.8%. The key drivers of firm are its food service, beverage

and food service as it helps enterprise in managing continuous growth via lifestyle nutrition.

As per its financial outcomes it is struggling with its market scope, solid performance had

been delivered by market expansion, appropriate cash generation by 7.5% increment in its

adjusted earnings per share. Kerry Group had kept its performance in very efficient aspect,

especially in North America as it had improved its performance in Latin America Its growth was

lowered in EMEA region which had contrasted with 0.3% and simultaneously excellent

performance in Asia with increased volume of business by 9.5%.

Consumer foods

1st half of year 2016

Total revenue 697 million

Trading profit 58 million

Trading margin 8.30%

There are various conditions of trading in consumer food market of UK and Irish which

are very competitive due to adaption of alteration in market landscape through its retailers,

different consumer trend which consist of e-tail's growth and trends which are deflationary.

Market share was gained by discounters as they had continued for broadening r focus of retailer

on EDLP strategies. Its volume growth was directly led by strong performance with context of

meal solutions. With reference to its trading profit it improved business which is underlying and

offset via currency and disposals. Its margin improved and driven via efficiency program on

ongoing aspect and portfolio had been repositioned.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

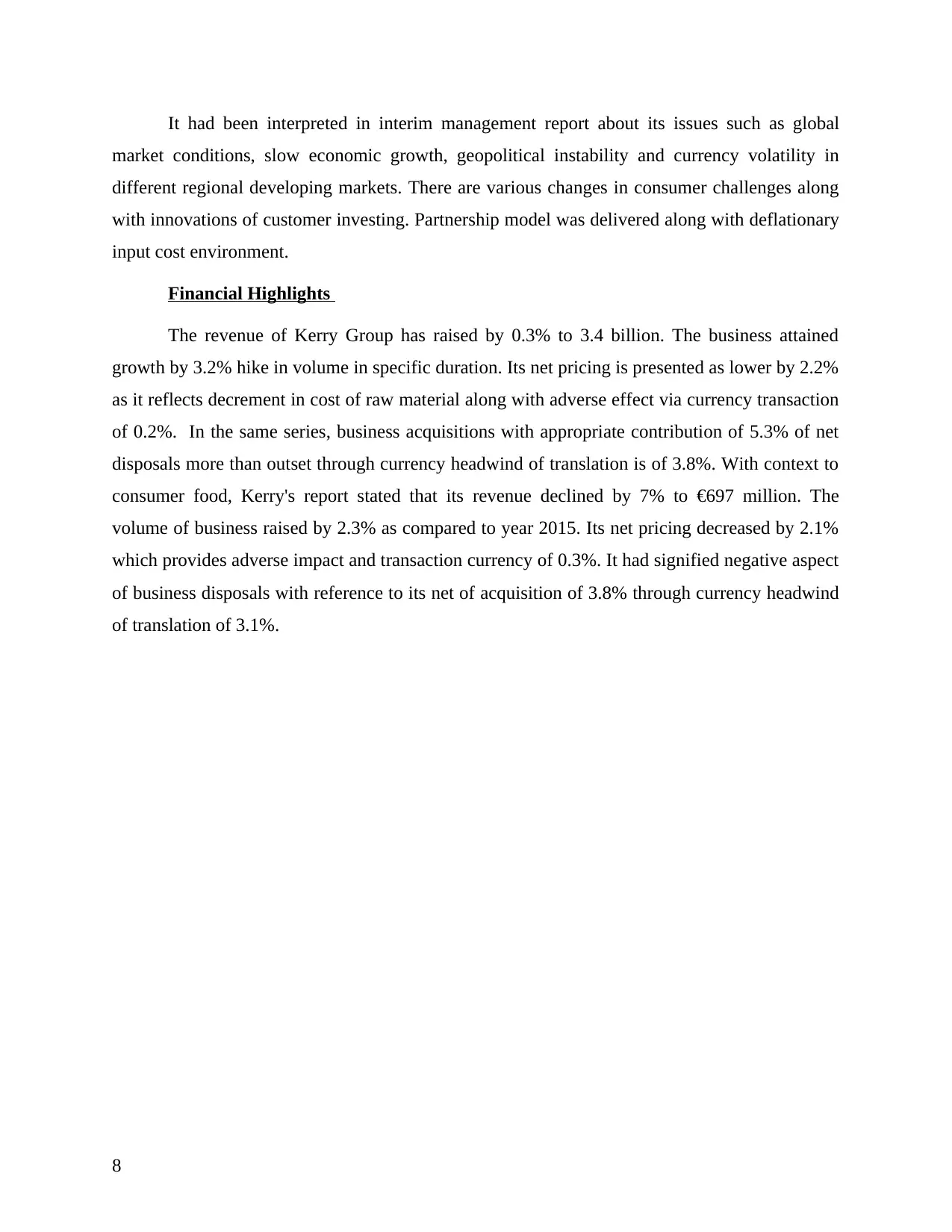

It had been interpreted in interim management report about its issues such as global

market conditions, slow economic growth, geopolitical instability and currency volatility in

different regional developing markets. There are various changes in consumer challenges along

with innovations of customer investing. Partnership model was delivered along with deflationary

input cost environment.

Financial Highlights

The revenue of Kerry Group has raised by 0.3% to 3.4 billion. The business attained

growth by 3.2% hike in volume in specific duration. Its net pricing is presented as lower by 2.2%

as it reflects decrement in cost of raw material along with adverse effect via currency transaction

of 0.2%. In the same series, business acquisitions with appropriate contribution of 5.3% of net

disposals more than outset through currency headwind of translation is of 3.8%. With context to

consumer food, Kerry's report stated that its revenue declined by 7% to €697 million. The

volume of business raised by 2.3% as compared to year 2015. Its net pricing decreased by 2.1%

which provides adverse impact and transaction currency of 0.3%. It had signified negative aspect

of business disposals with reference to its net of acquisition of 3.8% through currency headwind

of translation of 3.1%.

8

market conditions, slow economic growth, geopolitical instability and currency volatility in

different regional developing markets. There are various changes in consumer challenges along

with innovations of customer investing. Partnership model was delivered along with deflationary

input cost environment.

Financial Highlights

The revenue of Kerry Group has raised by 0.3% to 3.4 billion. The business attained

growth by 3.2% hike in volume in specific duration. Its net pricing is presented as lower by 2.2%

as it reflects decrement in cost of raw material along with adverse effect via currency transaction

of 0.2%. In the same series, business acquisitions with appropriate contribution of 5.3% of net

disposals more than outset through currency headwind of translation is of 3.8%. With context to

consumer food, Kerry's report stated that its revenue declined by 7% to €697 million. The

volume of business raised by 2.3% as compared to year 2015. Its net pricing decreased by 2.1%

which provides adverse impact and transaction currency of 0.3%. It had signified negative aspect

of business disposals with reference to its net of acquisition of 3.8% through currency headwind

of translation of 3.1%.

8

Illustration 2: Issues faced by Kerry

(Source: Kerry Interim Management

Report, 2016)

The trading profit of Kerry's group was raised by 7.4% to €322 million. As its trading

margin increased on basis of 70 bps to 10.6%. With reference to improvisation in product mix,

business efficiency programmes and operating leverage, together gives positive effect on

acquisitions as it exits all non-core activities of business. The finance cost in this duration raised

to 39 million because of acquisition which is financing in partly aspect and it offset strong cash

flow. In the same series, Kerry Group had undertaken two bolt-on-acquisition as it helps in

establishing manufacturer based in new geographies. The charges of tax of this specific period

was €36 million which represent effective tax rates due to variations in geographical split of

earned margin, appropriate investment in R&D and alterations in local statutory tax rates. With

9

(Source: Kerry Interim Management

Report, 2016)

The trading profit of Kerry's group was raised by 7.4% to €322 million. As its trading

margin increased on basis of 70 bps to 10.6%. With reference to improvisation in product mix,

business efficiency programmes and operating leverage, together gives positive effect on

acquisitions as it exits all non-core activities of business. The finance cost in this duration raised

to 39 million because of acquisition which is financing in partly aspect and it offset strong cash

flow. In the same series, Kerry Group had undertaken two bolt-on-acquisition as it helps in

establishing manufacturer based in new geographies. The charges of tax of this specific period

was €36 million which represent effective tax rates due to variations in geographical split of

earned margin, appropriate investment in R&D and alterations in local statutory tax rates. With

9

reference to items of non-trading, it gave charge of €3 in its 1st half of year 2016, initially

because of integration cost of acquisition. In its initial period, there was gain of €27 million as

result of profit with context to businesses disposal. Further, with free cash flow Kerry Group had

attained FCF of €379 million in H1. The cash flow improvement was because of low level of

investment in non-current assets and working capital in similar duration.

With context of balance sheet of Kerry Group, it could be stated that there was decrement

in property, equipment and plant by €46 million to €1385 million. All specified additions were

articulated in particular period for out-setting translation movements of foreign exchange and

alteration in depreciation. There was decrement in intangible assets from €35 million to €3414

million, but initially it was because of exchange rate which helps in translating tangible assets

with proper comparison to assets which are not denominated in Euro. In the same series, current

assets of firm increased through €147 million to €1989 as initially it was due to increment in

cash in hand. In this statement, its net deficit with context of benefit schemes was stated as €314

million. There was increase in its net deficit by the end of year because of decline in discount

rate of UK, US and Eurozone's which is partially outset through increase in contribution of cash.

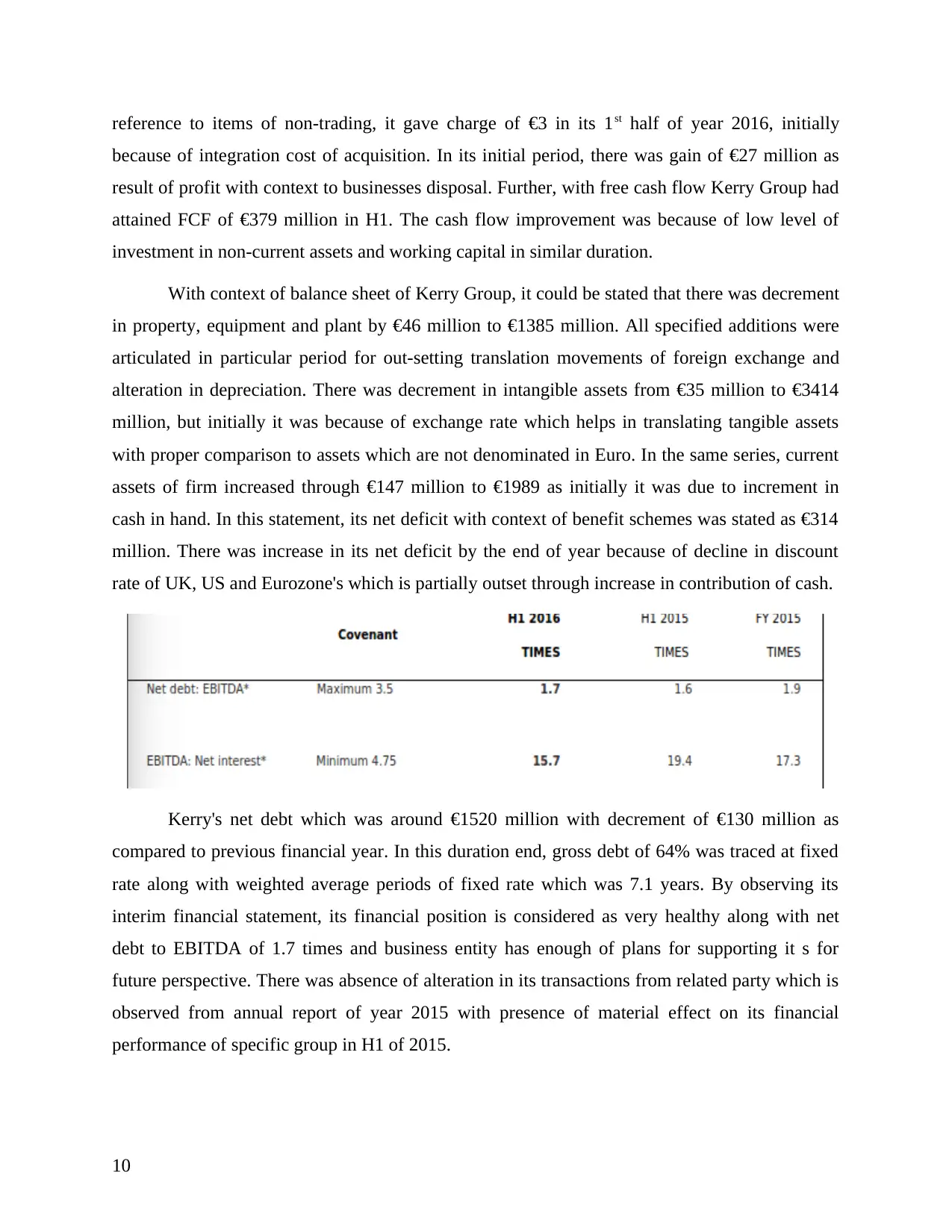

Kerry's net debt which was around €1520 million with decrement of €130 million as

compared to previous financial year. In this duration end, gross debt of 64% was traced at fixed

rate along with weighted average periods of fixed rate which was 7.1 years. By observing its

interim financial statement, its financial position is considered as very healthy along with net

debt to EBITDA of 1.7 times and business entity has enough of plans for supporting it s for

future perspective. There was absence of alteration in its transactions from related party which is

observed from annual report of year 2015 with presence of material effect on its financial

performance of specific group in H1 of 2015.

10

because of integration cost of acquisition. In its initial period, there was gain of €27 million as

result of profit with context to businesses disposal. Further, with free cash flow Kerry Group had

attained FCF of €379 million in H1. The cash flow improvement was because of low level of

investment in non-current assets and working capital in similar duration.

With context of balance sheet of Kerry Group, it could be stated that there was decrement

in property, equipment and plant by €46 million to €1385 million. All specified additions were

articulated in particular period for out-setting translation movements of foreign exchange and

alteration in depreciation. There was decrement in intangible assets from €35 million to €3414

million, but initially it was because of exchange rate which helps in translating tangible assets

with proper comparison to assets which are not denominated in Euro. In the same series, current

assets of firm increased through €147 million to €1989 as initially it was due to increment in

cash in hand. In this statement, its net deficit with context of benefit schemes was stated as €314

million. There was increase in its net deficit by the end of year because of decline in discount

rate of UK, US and Eurozone's which is partially outset through increase in contribution of cash.

Kerry's net debt which was around €1520 million with decrement of €130 million as

compared to previous financial year. In this duration end, gross debt of 64% was traced at fixed

rate along with weighted average periods of fixed rate which was 7.1 years. By observing its

interim financial statement, its financial position is considered as very healthy along with net

debt to EBITDA of 1.7 times and business entity has enough of plans for supporting it s for

future perspective. There was absence of alteration in its transactions from related party which is

observed from annual report of year 2015 with presence of material effect on its financial

performance of specific group in H1 of 2015.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

For quantifying implications of Brexit, in its interim duration it was very difficult to state

it, the Kerry Group had recognized uncertainty in broader aspect of macroeconomic which is

caused through voting of UK electorate for leaving European union. It had weakened consumer

confidence as outcome of this particular uncertainty but Kerry group was confident about its

positioning of business for addressing different opportunities and challenges for presenting this

decision. In the same series, uncertainties and risk was faced by founded group such as

integration and identification of acquisition target for decreasing its innovation rate, risks of

safety of quality and food, fails to retain key talents, systems of implementing risk, growth in

developing market, risk which are ongoing operational and compliance along with application of

unauthorised group Intellectual property. On the contrary, increment of risk along with potential

impact in H2 of 2015 which consist of fluctuations in cost of raw material along with currency

volatility and uncertainty link to macroeconomic from electorate of UK voting for leaving

European Union. This group usually manages specific risk with the help of control and risk

management process (Kerry Toward 2020, 2018).

Directors point of view

The Kerry Group has prepared its interim financial statements by following going

concern concept. There is presence of various resources for managing its operational existence

with reference to predictable future prospective. The directors represented the budget of this

specific group for duration which is not less than 1 year, as it plans for medium term are set on

its five year plan. They have also considered implications of cash flow with its plans as it

consists of proposed capital expenditure and it is compared along with borrowing committed

facilities are forecasted with its gearing ratio (Kerry Group revenues steady despite challenging

market conditions, 2016).

With context of dividend, board had declared 16.8 percent per share as its interim

dividend. Anticipating, the international trading environment would be challenging for second

half of 2016 for unique nutrition and taste, positioning of system model for attaining

requirements of customer and functional ingredients which are altering in marketplace. They

provide surety for delivering underlying performance of trading in full year as it had considered

increased currency headwinds of exchange rate of 5%. Its growth had been adjusted in earning

per share of year 2016 which is expected towards middle till lower end of range of 6% to 10% of

320 to 332 cents per share.

11

it, the Kerry Group had recognized uncertainty in broader aspect of macroeconomic which is

caused through voting of UK electorate for leaving European union. It had weakened consumer

confidence as outcome of this particular uncertainty but Kerry group was confident about its

positioning of business for addressing different opportunities and challenges for presenting this

decision. In the same series, uncertainties and risk was faced by founded group such as

integration and identification of acquisition target for decreasing its innovation rate, risks of

safety of quality and food, fails to retain key talents, systems of implementing risk, growth in

developing market, risk which are ongoing operational and compliance along with application of

unauthorised group Intellectual property. On the contrary, increment of risk along with potential

impact in H2 of 2015 which consist of fluctuations in cost of raw material along with currency

volatility and uncertainty link to macroeconomic from electorate of UK voting for leaving

European Union. This group usually manages specific risk with the help of control and risk

management process (Kerry Toward 2020, 2018).

Directors point of view

The Kerry Group has prepared its interim financial statements by following going

concern concept. There is presence of various resources for managing its operational existence

with reference to predictable future prospective. The directors represented the budget of this

specific group for duration which is not less than 1 year, as it plans for medium term are set on

its five year plan. They have also considered implications of cash flow with its plans as it

consists of proposed capital expenditure and it is compared along with borrowing committed

facilities are forecasted with its gearing ratio (Kerry Group revenues steady despite challenging

market conditions, 2016).

With context of dividend, board had declared 16.8 percent per share as its interim

dividend. Anticipating, the international trading environment would be challenging for second

half of 2016 for unique nutrition and taste, positioning of system model for attaining

requirements of customer and functional ingredients which are altering in marketplace. They

provide surety for delivering underlying performance of trading in full year as it had considered

increased currency headwinds of exchange rate of 5%. Its growth had been adjusted in earning

per share of year 2016 which is expected towards middle till lower end of range of 6% to 10% of

320 to 332 cents per share.

11

The directors had taken responsibility for interim report with context of transparency

regulations 2007 of Ireland. It had gained capability for growth and development in this

changing market place. Its business model would be focussing on customer needs and will work

on taste, nutrition and general wellness of system and technology which supported by group's

industry leading technology. It signifies strategic advantage with context of trend of consumer

along with its requirements (Kerry Group AGM, 2016). This model would be delivering across

broad e-commerce landscape, retail and food service throughout its global market. It would be

sustaining growth, as it developed market with established technology, strong alliances of

customer and leadership via convenience, nutritional beverage and food solution and tasteful. It

would be directly laying emphasis on opportunities of business development in different regional

markets along with prospects for surviving in Asian markets.

CONCLUSION

From the above study it had been concluded that financial and strategic management is

very important for purpose of accomplishing goals and objectives of an organization. It had been

assessed that it directly involves in defining business of organization along with identifying and

quantifying availability of potential resources. Kerry Group had played well by considering

unique taste, nutrition, functional ingredients and capabilities of system along with localised

innovation. Further, it articulated that Kerry's model is resilient and placed in efficient aspect for

responding to volatility and alteration in macroeconomic and consumer landscape. It had shown

that 2015 acquisition of group performed very well in interim duration.

12

regulations 2007 of Ireland. It had gained capability for growth and development in this

changing market place. Its business model would be focussing on customer needs and will work

on taste, nutrition and general wellness of system and technology which supported by group's

industry leading technology. It signifies strategic advantage with context of trend of consumer

along with its requirements (Kerry Group AGM, 2016). This model would be delivering across

broad e-commerce landscape, retail and food service throughout its global market. It would be

sustaining growth, as it developed market with established technology, strong alliances of

customer and leadership via convenience, nutritional beverage and food solution and tasteful. It

would be directly laying emphasis on opportunities of business development in different regional

markets along with prospects for surviving in Asian markets.

CONCLUSION

From the above study it had been concluded that financial and strategic management is

very important for purpose of accomplishing goals and objectives of an organization. It had been

assessed that it directly involves in defining business of organization along with identifying and

quantifying availability of potential resources. Kerry Group had played well by considering

unique taste, nutrition, functional ingredients and capabilities of system along with localised

innovation. Further, it articulated that Kerry's model is resilient and placed in efficient aspect for

responding to volatility and alteration in macroeconomic and consumer landscape. It had shown

that 2015 acquisition of group performed very well in interim duration.

12

REFERENCES

ONLINE

Kerry Group revenues steady despite challenging market conditions. 2016. [Online]. Available

through: <https://www.agriland.ie/farming-news/kerry-group-revenues-steady-despite-

challenging-market-conditions/>.

Kerry Group AGM. 2016. [Online]. Available

through:<https://www.kerrygroup.com/investors/news/Interim-Management-Statement-

Q1-2016.pdf>.

Kerry Interim Management Report. 2016. [Online]. Available

through:<https://www.kerrygroup.com/investors/results-presentations/2016-H1-Results-

Presentation-4-8-16.pdf>.

Kerry Toward 2020. 2018. [Online]. Available

through:<https://www.kerrygroup.com/sustainability/towards-2020-1/>.

13

ONLINE

Kerry Group revenues steady despite challenging market conditions. 2016. [Online]. Available

through: <https://www.agriland.ie/farming-news/kerry-group-revenues-steady-despite-

challenging-market-conditions/>.

Kerry Group AGM. 2016. [Online]. Available

through:<https://www.kerrygroup.com/investors/news/Interim-Management-Statement-

Q1-2016.pdf>.

Kerry Interim Management Report. 2016. [Online]. Available

through:<https://www.kerrygroup.com/investors/results-presentations/2016-H1-Results-

Presentation-4-8-16.pdf>.

Kerry Toward 2020. 2018. [Online]. Available

through:<https://www.kerrygroup.com/sustainability/towards-2020-1/>.

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.