Detailed Analysis of Metropolitan Inc.'s Cash Flow Statement

VerifiedAdded on 2023/04/21

|8

|1198

|440

Report

AI Summary

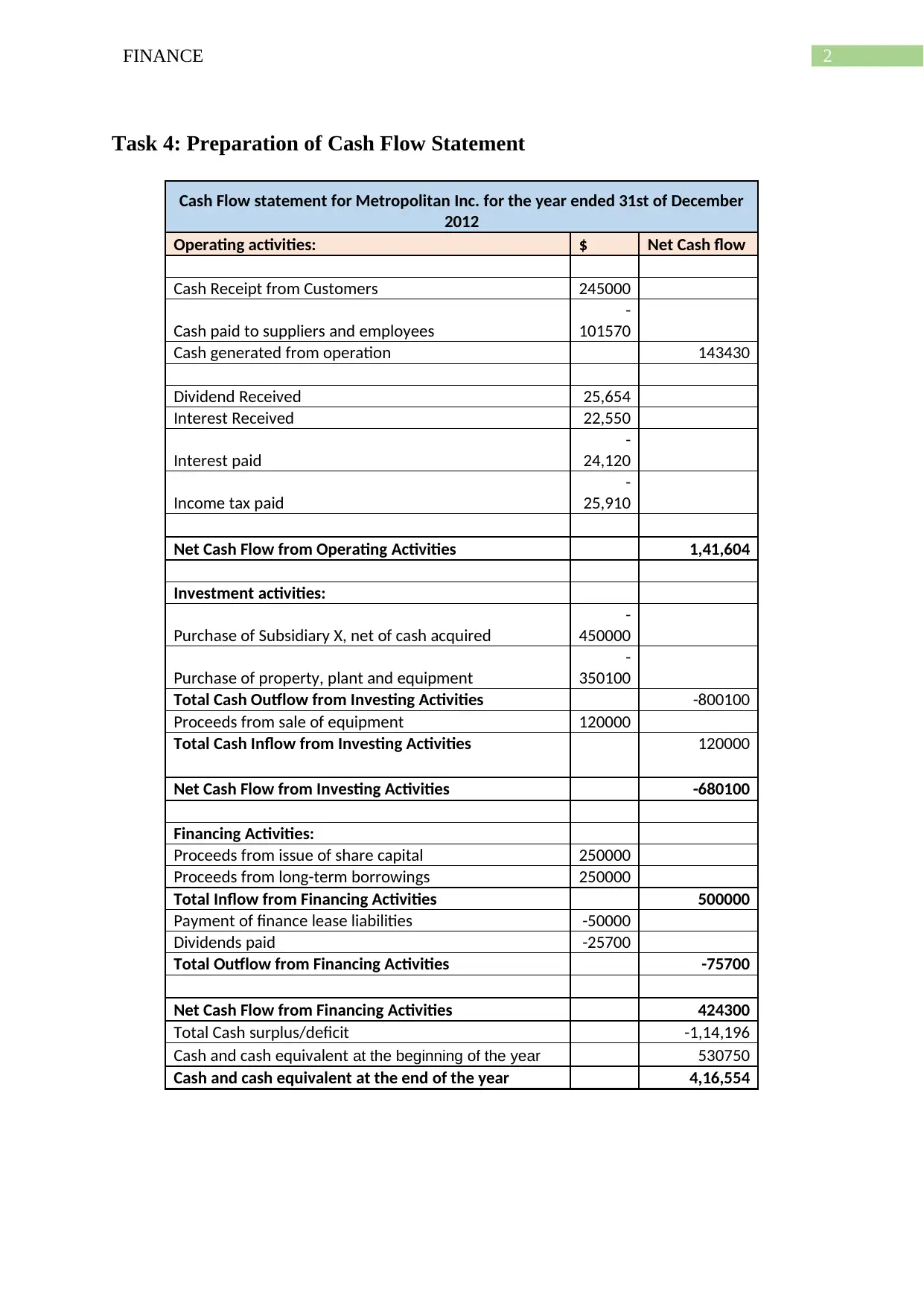

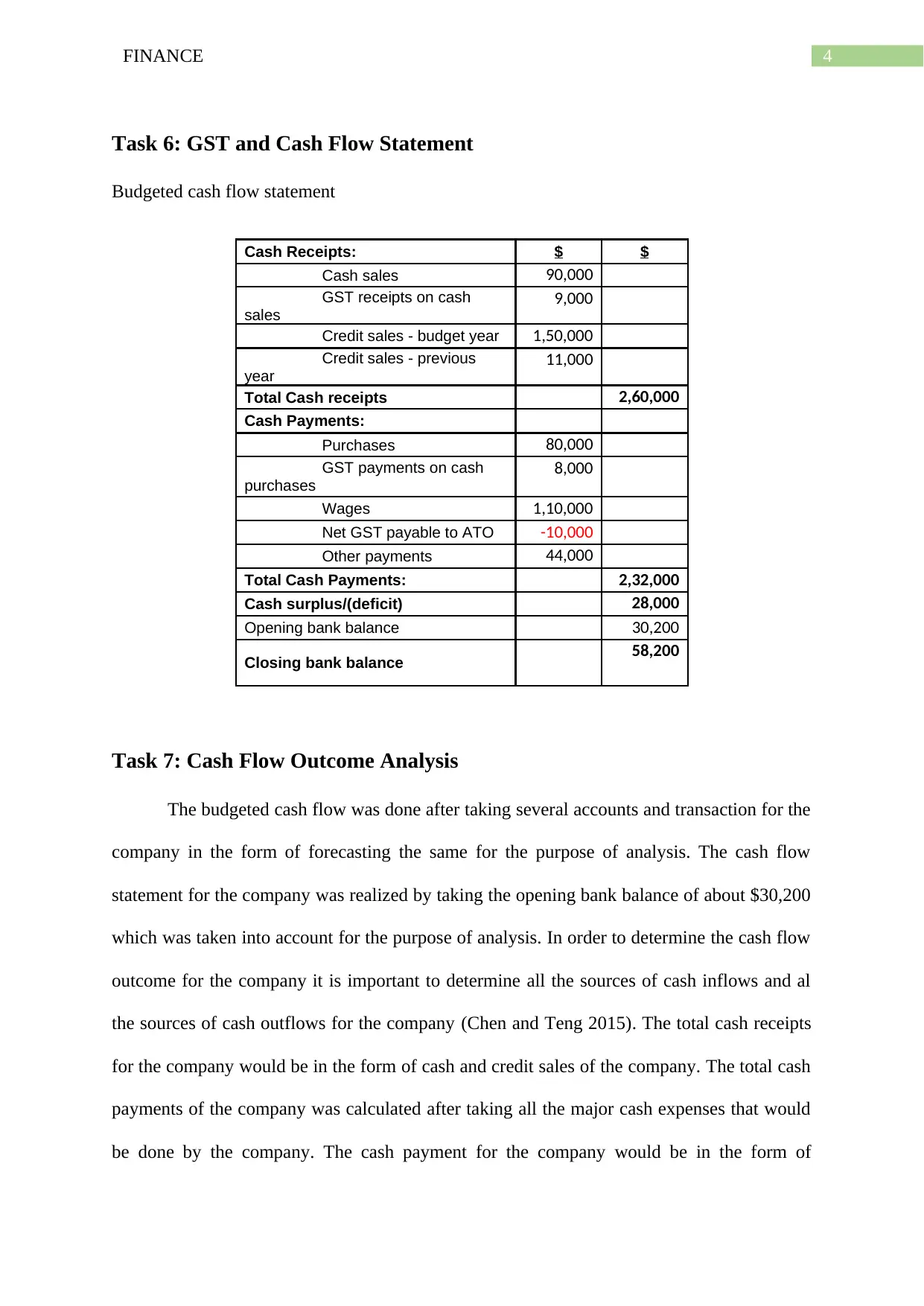

This finance report provides a comprehensive analysis of Metropolitan Inc.'s cash flow statement, covering operating, investing, and financing activities for the year ended December 31, 2012. It includes a detailed breakdown of cash inflows and outflows, highlighting key areas such as cash receipts from customers, payments to suppliers and employees, capital expenditures, and financing activities. The report also examines the impact of GST on the cash flow statement, presents a budgeted cash flow forecast, and analyzes the petty cash book. The analysis further discusses the implications of the cash flow outcomes and provides insights into the company's financial decision-making processes, emphasizing the importance of maintaining an optimal capital structure and carefully reviewing the company's financial performance in changing business conditions. This document is available on Desklib, a platform offering a wide range of study resources, including past papers and solved assignments for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.