Financial Performance Analysis of BHP Billiton: Finance for Business

VerifiedAdded on 2020/05/28

|13

|2753

|35

Report

AI Summary

This report provides a detailed financial analysis of BHP Billiton's performance from 2015 to 2017. The analysis begins with an overview of the income statement, highlighting revenue and expense trends, including a decrease in revenue in 2016 followed by an increase in 2017. The statement of financial position is then examined, showing changes in current assets and liabilities. The cash flow statement reveals fluctuations in operating and financing activities. The core of the analysis focuses on financial ratios, including profitability ratios (gross margin, net profit margin, return on equity), liquidity ratios (current ratio, quick ratio), capital structure ratios (debt ratio, equity ratio), and efficiency ratios (accounts receivable turnover, asset turnover). The report concludes that BHP Billiton's financial position improved in 2017 after a challenging 2016, demonstrating effective asset utilization and an ability to meet its financial obligations. The report uses data from the company's financial statements to calculate and interpret these key financial metrics, offering insights into the company's performance and financial health.

Running head: FINANCE FOR BUSINESS

Finance for Business

Name of the Student

Name of the University

Authors Note

Course ID

Finance for Business

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR BUSINESS

Table of Contents

Introduction:...............................................................................................................................2

Income statement analysis:........................................................................................................2

Statement of financial position:.................................................................................................3

Cash Flow Statement:................................................................................................................3

Financial Ratio Analysis............................................................................................................4

Profitability Ratios:....................................................................................................................4

Liquidity Ratios:.........................................................................................................................5

Capital structure ratio:................................................................................................................7

Efficiency ratios:........................................................................................................................8

Conclusion:................................................................................................................................9

Reference List:.........................................................................................................................11

Table of Contents

Introduction:...............................................................................................................................2

Income statement analysis:........................................................................................................2

Statement of financial position:.................................................................................................3

Cash Flow Statement:................................................................................................................3

Financial Ratio Analysis............................................................................................................4

Profitability Ratios:....................................................................................................................4

Liquidity Ratios:.........................................................................................................................5

Capital structure ratio:................................................................................................................7

Efficiency ratios:........................................................................................................................8

Conclusion:................................................................................................................................9

Reference List:.........................................................................................................................11

2FINANCE FOR BUSINESS

Introduction:

The current study is based on the determination of the financial position of BHP

Billiton. The study will take into the considerations the financial performance that has been

reported by BHP Billiton by analysing the performance posted for the year 2015-17. To

gauge into the financial position of the firm the study will take account of the income

statement, statement of financial position and cash flow statement with objective of gaining a

detailed understanding of BHP Billiton performance. In addition to this, several ratio analysis

will be conducted to gain an additional understanding of the firm’s liquidity, as these ratios

will be covering the areas of profitability, capital structure ratios, and liquidity and efficiency

ratios.

Income statement analysis:

On analysing the income statement of BHP Billiton it was found that, the revenue

reported by the firm for the year 2016 stood $30.9 billion. The revenue reflects the fall in

revenue of $13.7 billion from the reported figures of $44.6 billion in the year 2015. The

falling revenue was largely responsible for the weaker average price realization across all the

major commodities. The total amount of expenses for the year 2016 reduced by $1.5 billion

as the expense for the firm stood $35.5 billion for the year ended 2016. The expenses reduced

by 4% in comparison to the amount reported in 2015 and a large part of expenses was

reduced in the employee benefit expenses (BHP Billiton 2018). Additionally the expenditure

on depreciation and amortization also reduced by $497 million in the year 2016.

The profit after taxation from the continuing and discontinued operations, which was

attributable to the shareholders of the BHP Billiton, has increased after reporting a loss of

$6.4 billion in the financial year of 2016 to a profit of $5.9 billion in the financial year of

2017 (BHP Billiton 2018). Additionally the revenue for BHP Billiton also increased by $7.4

Introduction:

The current study is based on the determination of the financial position of BHP

Billiton. The study will take into the considerations the financial performance that has been

reported by BHP Billiton by analysing the performance posted for the year 2015-17. To

gauge into the financial position of the firm the study will take account of the income

statement, statement of financial position and cash flow statement with objective of gaining a

detailed understanding of BHP Billiton performance. In addition to this, several ratio analysis

will be conducted to gain an additional understanding of the firm’s liquidity, as these ratios

will be covering the areas of profitability, capital structure ratios, and liquidity and efficiency

ratios.

Income statement analysis:

On analysing the income statement of BHP Billiton it was found that, the revenue

reported by the firm for the year 2016 stood $30.9 billion. The revenue reflects the fall in

revenue of $13.7 billion from the reported figures of $44.6 billion in the year 2015. The

falling revenue was largely responsible for the weaker average price realization across all the

major commodities. The total amount of expenses for the year 2016 reduced by $1.5 billion

as the expense for the firm stood $35.5 billion for the year ended 2016. The expenses reduced

by 4% in comparison to the amount reported in 2015 and a large part of expenses was

reduced in the employee benefit expenses (BHP Billiton 2018). Additionally the expenditure

on depreciation and amortization also reduced by $497 million in the year 2016.

The profit after taxation from the continuing and discontinued operations, which was

attributable to the shareholders of the BHP Billiton, has increased after reporting a loss of

$6.4 billion in the financial year of 2016 to a profit of $5.9 billion in the financial year of

2017 (BHP Billiton 2018). Additionally the revenue for BHP Billiton also increased by $7.4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR BUSINESS

billion or by 24% from the revenue reported in 2016. Thus, the company has significantly

gained strength from the loss reported in 2016 with increase in revenue and reduction in

expenses for the year 2017 (Asquith and Weiss 2016).

Statement of financial position:

On considering the statement of financial position, it can be stated that current assets

of the firm increased by $1,345 billion as the current assets for the year 2015 stood $16,369

billion that subsequently increased to $17,714 billion. The current liabilities of BHP Billiton

has reduced over the year as the current liabilities for the year ended 2016 stood 12340 while

in the year 2017 it subsequently reduced by $974 billion to stand at $11,366 (BHP Billiton

2018). The unit cash costs for BHP Billiton copper assets decreased by 4% to US1.15 percent

following the idle capacity and other forms of strike related costs that is incurred by the firm

(Henderson et al. 2015). Overall BHP Billiton has reported strong assets reflecting the

company has been sufficient in utilizing its assets to meet its debt obligations as and when

they become due.

Cash Flow Statement:

The net operating cash flow following interest and tax has reduced in 2016 by $8.7

billion from the figures reported in 2015. The primary reason for such fall in operating cash is

due to the decrease in the cash generated from operations. Additionally in 2015, the net

financing cash inflows of $248 million represented an increase by $8.6 billion from the

financial year of 2015 and this is largely because of the issue of multicurrency hybrid notes

during the year 2016 (BHP Billiton 2018). However, in 2017, the cash flow from operations

increased by $6.2 billion and the rise is mainly attributable to the higher prices of commodity

with constant focus on the cash cost efficiency. The net cash from financing activities in 2017

has increased by $9.4 billion reflecting that BHP Billiton has immensely focused on

billion or by 24% from the revenue reported in 2016. Thus, the company has significantly

gained strength from the loss reported in 2016 with increase in revenue and reduction in

expenses for the year 2017 (Asquith and Weiss 2016).

Statement of financial position:

On considering the statement of financial position, it can be stated that current assets

of the firm increased by $1,345 billion as the current assets for the year 2015 stood $16,369

billion that subsequently increased to $17,714 billion. The current liabilities of BHP Billiton

has reduced over the year as the current liabilities for the year ended 2016 stood 12340 while

in the year 2017 it subsequently reduced by $974 billion to stand at $11,366 (BHP Billiton

2018). The unit cash costs for BHP Billiton copper assets decreased by 4% to US1.15 percent

following the idle capacity and other forms of strike related costs that is incurred by the firm

(Henderson et al. 2015). Overall BHP Billiton has reported strong assets reflecting the

company has been sufficient in utilizing its assets to meet its debt obligations as and when

they become due.

Cash Flow Statement:

The net operating cash flow following interest and tax has reduced in 2016 by $8.7

billion from the figures reported in 2015. The primary reason for such fall in operating cash is

due to the decrease in the cash generated from operations. Additionally in 2015, the net

financing cash inflows of $248 million represented an increase by $8.6 billion from the

financial year of 2015 and this is largely because of the issue of multicurrency hybrid notes

during the year 2016 (BHP Billiton 2018). However, in 2017, the cash flow from operations

increased by $6.2 billion and the rise is mainly attributable to the higher prices of commodity

with constant focus on the cash cost efficiency. The net cash from financing activities in 2017

has increased by $9.4 billion reflecting that BHP Billiton has immensely focused on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR BUSINESS

reduction of debt with $3.3 billion of debt repayment (Warren and Jones 2018). The overall

cash flow reported by the firm stood strong in the year 2017 with net increase in cash and

cash equivalents of 3,510 billion.

Financial Ratio Analysis

Profitability Ratios:

The profitability ratios can be defined as those ratios, which helps in representing the

financial metrics of an organization (Powers, Crosson and Needles 2014). These ratios are

generally used to ascertain whether the organization has been successfully generating revenue

against the income reported by the firm. The gross for the firm has been on a rising trend as

the company has reported a rising gross profit margin of 66.62% for the year ended 2015. In

the subsequent year of 2016 and 2017, the company reported the gross margin of 72.01 and

85.77% respectively (Beatty and Liao 2014). The increase in gross margin can be attributed

to the rising trend of sales reported by BHP Billiton as the company reported the sales

revenue of $30,912 million for the year 2016 that subsequently increased in the year 2017 to

$38,285 million.

The net profit margin on the other hand for the year 2015 stood 4.28% whereas in the

following year of 2016 BHP Billiton reported a negative net profit margin of -20.66%. This

primarily attributed to the reduction in revenue by US $13 billion or subsequently 31% from

the revenues posted in the financial year of 2015. In the following year of 2017, BHP Billiton

reported an increasing net profit margin of 15.38% and the rise in net profit margin is largely

because of the increase in the revenue of the firm (Board 2015). The operating profit margin

for the year 2015 stood 19.4% whereas in the year 2016 the operating profit margin was

reported to be negative with figures standing -20.2%. However, the operating margin gained

strength as the figures stood positively at 30.7%.

reduction of debt with $3.3 billion of debt repayment (Warren and Jones 2018). The overall

cash flow reported by the firm stood strong in the year 2017 with net increase in cash and

cash equivalents of 3,510 billion.

Financial Ratio Analysis

Profitability Ratios:

The profitability ratios can be defined as those ratios, which helps in representing the

financial metrics of an organization (Powers, Crosson and Needles 2014). These ratios are

generally used to ascertain whether the organization has been successfully generating revenue

against the income reported by the firm. The gross for the firm has been on a rising trend as

the company has reported a rising gross profit margin of 66.62% for the year ended 2015. In

the subsequent year of 2016 and 2017, the company reported the gross margin of 72.01 and

85.77% respectively (Beatty and Liao 2014). The increase in gross margin can be attributed

to the rising trend of sales reported by BHP Billiton as the company reported the sales

revenue of $30,912 million for the year 2016 that subsequently increased in the year 2017 to

$38,285 million.

The net profit margin on the other hand for the year 2015 stood 4.28% whereas in the

following year of 2016 BHP Billiton reported a negative net profit margin of -20.66%. This

primarily attributed to the reduction in revenue by US $13 billion or subsequently 31% from

the revenues posted in the financial year of 2015. In the following year of 2017, BHP Billiton

reported an increasing net profit margin of 15.38% and the rise in net profit margin is largely

because of the increase in the revenue of the firm (Board 2015). The operating profit margin

for the year 2015 stood 19.4% whereas in the year 2016 the operating profit margin was

reported to be negative with figures standing -20.2%. However, the operating margin gained

strength as the figures stood positively at 30.7%.

5FINANCE FOR BUSINESS

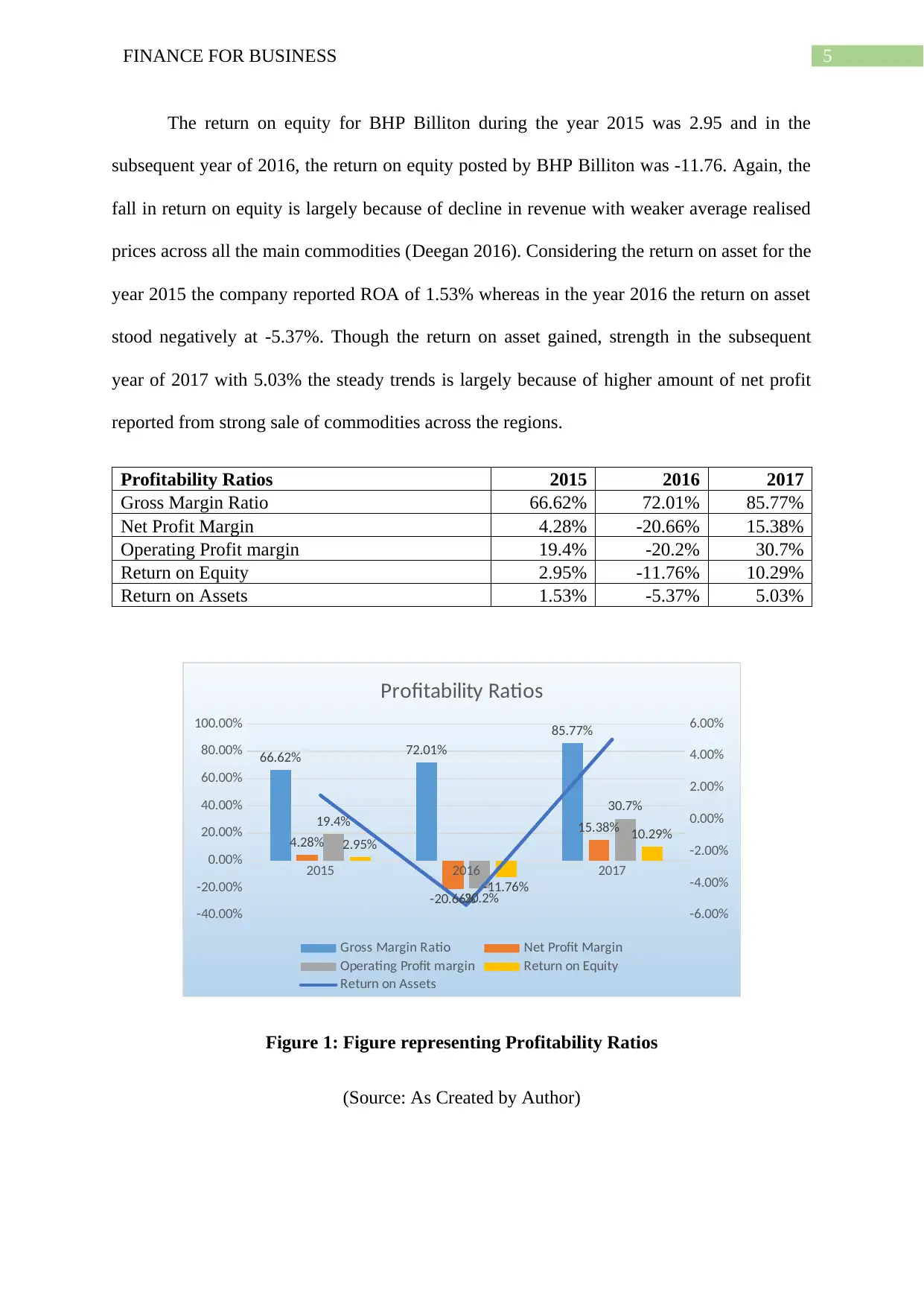

The return on equity for BHP Billiton during the year 2015 was 2.95 and in the

subsequent year of 2016, the return on equity posted by BHP Billiton was -11.76. Again, the

fall in return on equity is largely because of decline in revenue with weaker average realised

prices across all the main commodities (Deegan 2016). Considering the return on asset for the

year 2015 the company reported ROA of 1.53% whereas in the year 2016 the return on asset

stood negatively at -5.37%. Though the return on asset gained, strength in the subsequent

year of 2017 with 5.03% the steady trends is largely because of higher amount of net profit

reported from strong sale of commodities across the regions.

Profitability Ratios 2015 2016 2017

Gross Margin Ratio 66.62% 72.01% 85.77%

Net Profit Margin 4.28% -20.66% 15.38%

Operating Profit margin 19.4% -20.2% 30.7%

Return on Equity 2.95% -11.76% 10.29%

Return on Assets 1.53% -5.37% 5.03%

2015 2016 2017

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

66.62% 72.01%

85.77%

4.28%

-20.66%

15.38%19.4%

-20.2%

30.7%

2.95%

-11.76%

10.29%

Profitability Ratios

Gross Margin Ratio Net Profit Margin

Operating Profit margin Return on Equity

Return on Assets

Figure 1: Figure representing Profitability Ratios

(Source: As Created by Author)

The return on equity for BHP Billiton during the year 2015 was 2.95 and in the

subsequent year of 2016, the return on equity posted by BHP Billiton was -11.76. Again, the

fall in return on equity is largely because of decline in revenue with weaker average realised

prices across all the main commodities (Deegan 2016). Considering the return on asset for the

year 2015 the company reported ROA of 1.53% whereas in the year 2016 the return on asset

stood negatively at -5.37%. Though the return on asset gained, strength in the subsequent

year of 2017 with 5.03% the steady trends is largely because of higher amount of net profit

reported from strong sale of commodities across the regions.

Profitability Ratios 2015 2016 2017

Gross Margin Ratio 66.62% 72.01% 85.77%

Net Profit Margin 4.28% -20.66% 15.38%

Operating Profit margin 19.4% -20.2% 30.7%

Return on Equity 2.95% -11.76% 10.29%

Return on Assets 1.53% -5.37% 5.03%

2015 2016 2017

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

66.62% 72.01%

85.77%

4.28%

-20.66%

15.38%19.4%

-20.2%

30.7%

2.95%

-11.76%

10.29%

Profitability Ratios

Gross Margin Ratio Net Profit Margin

Operating Profit margin Return on Equity

Return on Assets

Figure 1: Figure representing Profitability Ratios

(Source: As Created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR BUSINESS

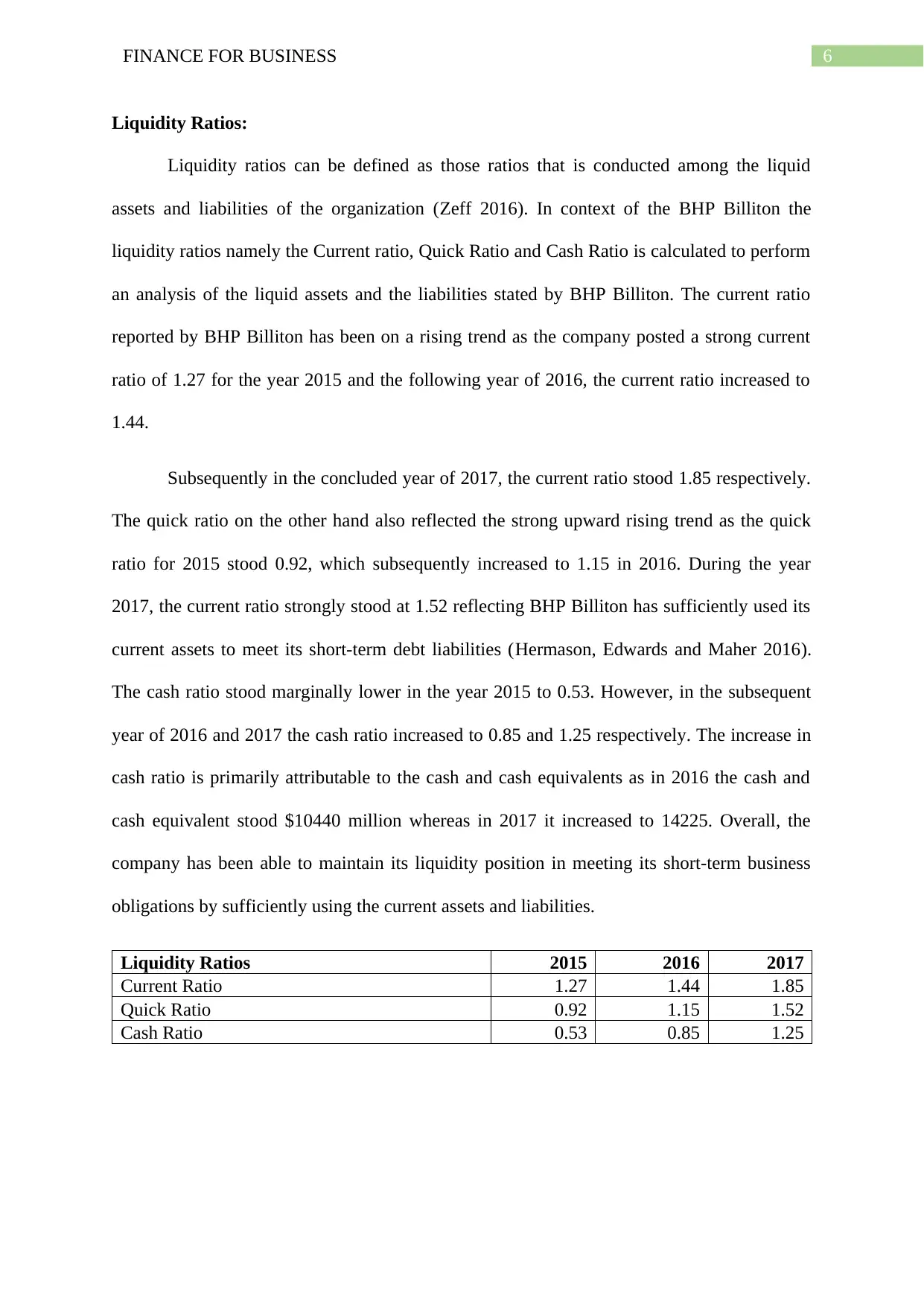

Liquidity Ratios:

Liquidity ratios can be defined as those ratios that is conducted among the liquid

assets and liabilities of the organization (Zeff 2016). In context of the BHP Billiton the

liquidity ratios namely the Current ratio, Quick Ratio and Cash Ratio is calculated to perform

an analysis of the liquid assets and the liabilities stated by BHP Billiton. The current ratio

reported by BHP Billiton has been on a rising trend as the company posted a strong current

ratio of 1.27 for the year 2015 and the following year of 2016, the current ratio increased to

1.44.

Subsequently in the concluded year of 2017, the current ratio stood 1.85 respectively.

The quick ratio on the other hand also reflected the strong upward rising trend as the quick

ratio for 2015 stood 0.92, which subsequently increased to 1.15 in 2016. During the year

2017, the current ratio strongly stood at 1.52 reflecting BHP Billiton has sufficiently used its

current assets to meet its short-term debt liabilities (Hermason, Edwards and Maher 2016).

The cash ratio stood marginally lower in the year 2015 to 0.53. However, in the subsequent

year of 2016 and 2017 the cash ratio increased to 0.85 and 1.25 respectively. The increase in

cash ratio is primarily attributable to the cash and cash equivalents as in 2016 the cash and

cash equivalent stood $10440 million whereas in 2017 it increased to 14225. Overall, the

company has been able to maintain its liquidity position in meeting its short-term business

obligations by sufficiently using the current assets and liabilities.

Liquidity Ratios 2015 2016 2017

Current Ratio 1.27 1.44 1.85

Quick Ratio 0.92 1.15 1.52

Cash Ratio 0.53 0.85 1.25

Liquidity Ratios:

Liquidity ratios can be defined as those ratios that is conducted among the liquid

assets and liabilities of the organization (Zeff 2016). In context of the BHP Billiton the

liquidity ratios namely the Current ratio, Quick Ratio and Cash Ratio is calculated to perform

an analysis of the liquid assets and the liabilities stated by BHP Billiton. The current ratio

reported by BHP Billiton has been on a rising trend as the company posted a strong current

ratio of 1.27 for the year 2015 and the following year of 2016, the current ratio increased to

1.44.

Subsequently in the concluded year of 2017, the current ratio stood 1.85 respectively.

The quick ratio on the other hand also reflected the strong upward rising trend as the quick

ratio for 2015 stood 0.92, which subsequently increased to 1.15 in 2016. During the year

2017, the current ratio strongly stood at 1.52 reflecting BHP Billiton has sufficiently used its

current assets to meet its short-term debt liabilities (Hermason, Edwards and Maher 2016).

The cash ratio stood marginally lower in the year 2015 to 0.53. However, in the subsequent

year of 2016 and 2017 the cash ratio increased to 0.85 and 1.25 respectively. The increase in

cash ratio is primarily attributable to the cash and cash equivalents as in 2016 the cash and

cash equivalent stood $10440 million whereas in 2017 it increased to 14225. Overall, the

company has been able to maintain its liquidity position in meeting its short-term business

obligations by sufficiently using the current assets and liabilities.

Liquidity Ratios 2015 2016 2017

Current Ratio 1.27 1.44 1.85

Quick Ratio 0.92 1.15 1.52

Cash Ratio 0.53 0.85 1.25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR BUSINESS

Current Ratio Quick Ratio Cash Ratio

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

1.27

0.92

0.53

1.44

1.15

0.85

1.85

1.52

1.25

Liquidity Ratios

2015 2016 2017

Figure 2: Figure representing Liquidity Ratios

(Source: As Created by Author)

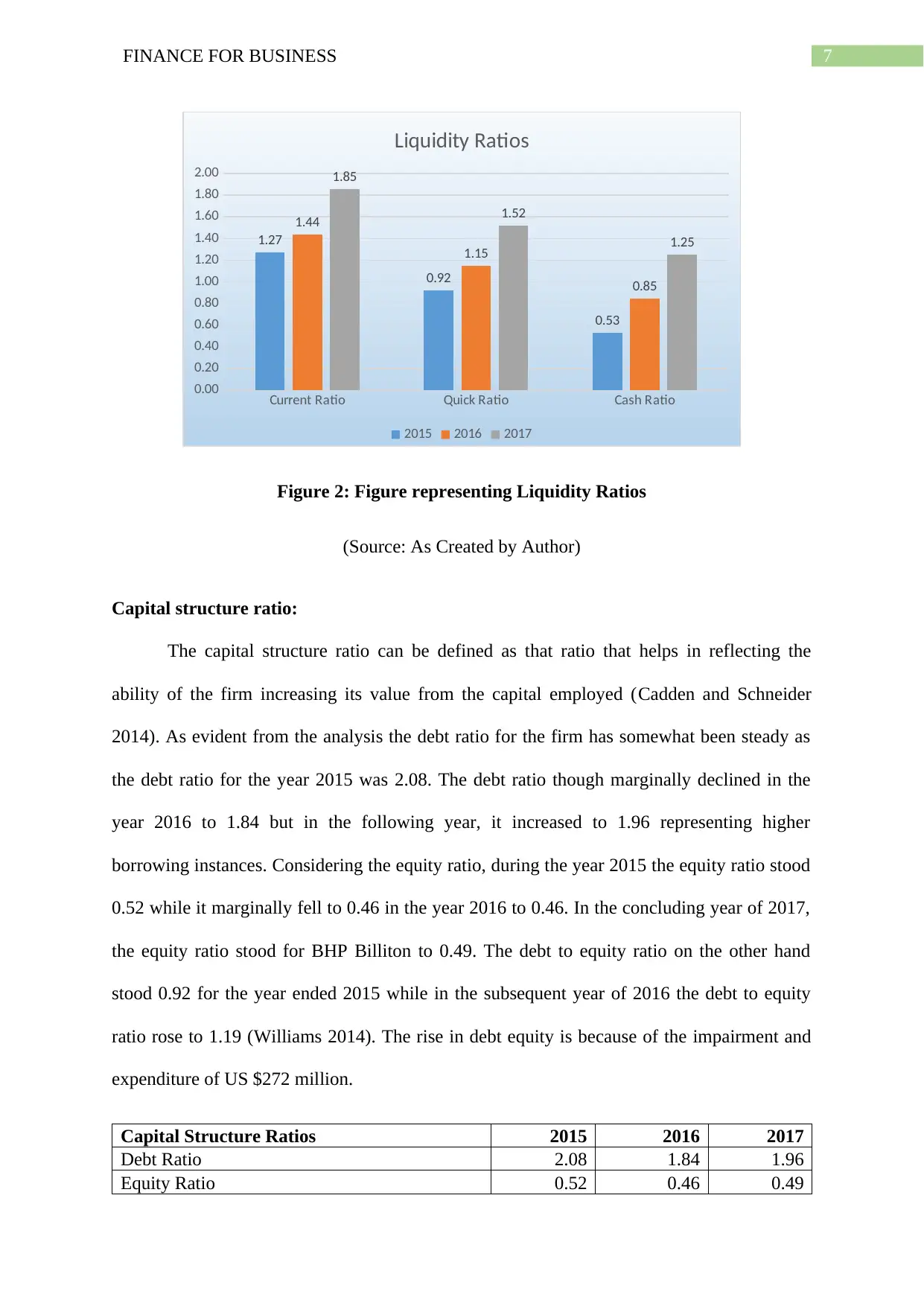

Capital structure ratio:

The capital structure ratio can be defined as that ratio that helps in reflecting the

ability of the firm increasing its value from the capital employed (Cadden and Schneider

2014). As evident from the analysis the debt ratio for the firm has somewhat been steady as

the debt ratio for the year 2015 was 2.08. The debt ratio though marginally declined in the

year 2016 to 1.84 but in the following year, it increased to 1.96 representing higher

borrowing instances. Considering the equity ratio, during the year 2015 the equity ratio stood

0.52 while it marginally fell to 0.46 in the year 2016 to 0.46. In the concluding year of 2017,

the equity ratio stood for BHP Billiton to 0.49. The debt to equity ratio on the other hand

stood 0.92 for the year ended 2015 while in the subsequent year of 2016 the debt to equity

ratio rose to 1.19 (Williams 2014). The rise in debt equity is because of the impairment and

expenditure of US $272 million.

Capital Structure Ratios 2015 2016 2017

Debt Ratio 2.08 1.84 1.96

Equity Ratio 0.52 0.46 0.49

Current Ratio Quick Ratio Cash Ratio

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

1.27

0.92

0.53

1.44

1.15

0.85

1.85

1.52

1.25

Liquidity Ratios

2015 2016 2017

Figure 2: Figure representing Liquidity Ratios

(Source: As Created by Author)

Capital structure ratio:

The capital structure ratio can be defined as that ratio that helps in reflecting the

ability of the firm increasing its value from the capital employed (Cadden and Schneider

2014). As evident from the analysis the debt ratio for the firm has somewhat been steady as

the debt ratio for the year 2015 was 2.08. The debt ratio though marginally declined in the

year 2016 to 1.84 but in the following year, it increased to 1.96 representing higher

borrowing instances. Considering the equity ratio, during the year 2015 the equity ratio stood

0.52 while it marginally fell to 0.46 in the year 2016 to 0.46. In the concluding year of 2017,

the equity ratio stood for BHP Billiton to 0.49. The debt to equity ratio on the other hand

stood 0.92 for the year ended 2015 while in the subsequent year of 2016 the debt to equity

ratio rose to 1.19 (Williams 2014). The rise in debt equity is because of the impairment and

expenditure of US $272 million.

Capital Structure Ratios 2015 2016 2017

Debt Ratio 2.08 1.84 1.96

Equity Ratio 0.52 0.46 0.49

8FINANCE FOR BUSINESS

Debt-Equity Ratio 0.92 1.19 1.04

Gearing Ratio 0.50 1.08 0.53

Debt Ratio Equity Ratio Debt-Equity Ratio Gearing Ratio

0.00

0.50

1.00

1.50

2.00

2.50

2.08

0.52

0.92

0.50

1.84

0.46

1.19 1.08

1.96

0.49

1.04

0.53

Capital Structure Ratios

2015 2016

2017 Linear (2017)

Figure 3: Figure representing Capital Structure Ratios

(Source: As Created by Author)

Efficiency ratios:

The efficiency ratio is used to measure the effectiveness of the organization in

determining whether the firm has been successfully making the use of assets and liabilities

(Edmonds et al. 2016). As evident that the accounts receivable ratios for BHP Billiton during

the year 2015 stood 8.96 whereas in the year of 2016 the accounts receivable ratio was 8.31.

In the recently concluded year of 2017 the accounts receivable ratio reportable by the firm

was 12.63 with a sharp rise from the previous year of 2016. The asset turnover ratio has been

somewhat low as the figure reported for the year ended 2015 and 2016 stood 0.36 and 0.26

respectively (Pratt 2016). Whereas in the year 2017 the asset turnover ratio reported by the

firm was 0.33. The inventory turnover ratio though reflects an improving trend as the time

taken by BHP Billiton to rotate its inventory has been gradually decreasing.

Debt-Equity Ratio 0.92 1.19 1.04

Gearing Ratio 0.50 1.08 0.53

Debt Ratio Equity Ratio Debt-Equity Ratio Gearing Ratio

0.00

0.50

1.00

1.50

2.00

2.50

2.08

0.52

0.92

0.50

1.84

0.46

1.19 1.08

1.96

0.49

1.04

0.53

Capital Structure Ratios

2015 2016

2017 Linear (2017)

Figure 3: Figure representing Capital Structure Ratios

(Source: As Created by Author)

Efficiency ratios:

The efficiency ratio is used to measure the effectiveness of the organization in

determining whether the firm has been successfully making the use of assets and liabilities

(Edmonds et al. 2016). As evident that the accounts receivable ratios for BHP Billiton during

the year 2015 stood 8.96 whereas in the year of 2016 the accounts receivable ratio was 8.31.

In the recently concluded year of 2017 the accounts receivable ratio reportable by the firm

was 12.63 with a sharp rise from the previous year of 2016. The asset turnover ratio has been

somewhat low as the figure reported for the year ended 2015 and 2016 stood 0.36 and 0.26

respectively (Pratt 2016). Whereas in the year 2017 the asset turnover ratio reported by the

firm was 0.33. The inventory turnover ratio though reflects an improving trend as the time

taken by BHP Billiton to rotate its inventory has been gradually decreasing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

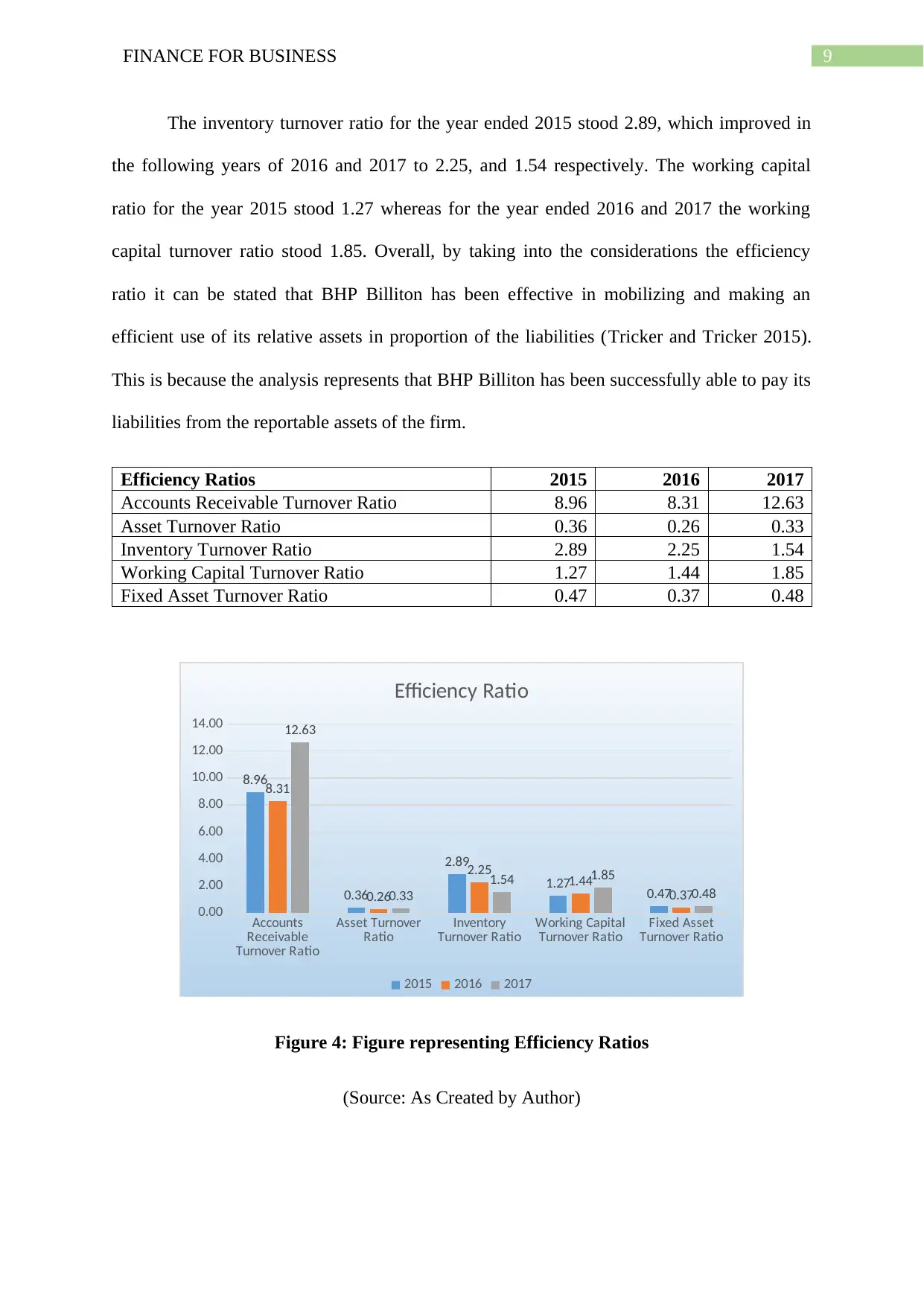

9FINANCE FOR BUSINESS

The inventory turnover ratio for the year ended 2015 stood 2.89, which improved in

the following years of 2016 and 2017 to 2.25, and 1.54 respectively. The working capital

ratio for the year 2015 stood 1.27 whereas for the year ended 2016 and 2017 the working

capital turnover ratio stood 1.85. Overall, by taking into the considerations the efficiency

ratio it can be stated that BHP Billiton has been effective in mobilizing and making an

efficient use of its relative assets in proportion of the liabilities (Tricker and Tricker 2015).

This is because the analysis represents that BHP Billiton has been successfully able to pay its

liabilities from the reportable assets of the firm.

Efficiency Ratios 2015 2016 2017

Accounts Receivable Turnover Ratio 8.96 8.31 12.63

Asset Turnover Ratio 0.36 0.26 0.33

Inventory Turnover Ratio 2.89 2.25 1.54

Working Capital Turnover Ratio 1.27 1.44 1.85

Fixed Asset Turnover Ratio 0.47 0.37 0.48

Accounts

Receivable

Turnover Ratio

Asset Turnover

Ratio Inventory

Turnover Ratio Working Capital

Turnover Ratio Fixed Asset

Turnover Ratio

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

8.96

0.36

2.89

1.27 0.47

8.31

0.26

2.25 1.44

0.37

12.63

0.33

1.54 1.85

0.48

Efficiency Ratio

2015 2016 2017

Figure 4: Figure representing Efficiency Ratios

(Source: As Created by Author)

The inventory turnover ratio for the year ended 2015 stood 2.89, which improved in

the following years of 2016 and 2017 to 2.25, and 1.54 respectively. The working capital

ratio for the year 2015 stood 1.27 whereas for the year ended 2016 and 2017 the working

capital turnover ratio stood 1.85. Overall, by taking into the considerations the efficiency

ratio it can be stated that BHP Billiton has been effective in mobilizing and making an

efficient use of its relative assets in proportion of the liabilities (Tricker and Tricker 2015).

This is because the analysis represents that BHP Billiton has been successfully able to pay its

liabilities from the reportable assets of the firm.

Efficiency Ratios 2015 2016 2017

Accounts Receivable Turnover Ratio 8.96 8.31 12.63

Asset Turnover Ratio 0.36 0.26 0.33

Inventory Turnover Ratio 2.89 2.25 1.54

Working Capital Turnover Ratio 1.27 1.44 1.85

Fixed Asset Turnover Ratio 0.47 0.37 0.48

Accounts

Receivable

Turnover Ratio

Asset Turnover

Ratio Inventory

Turnover Ratio Working Capital

Turnover Ratio Fixed Asset

Turnover Ratio

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

8.96

0.36

2.89

1.27 0.47

8.31

0.26

2.25 1.44

0.37

12.63

0.33

1.54 1.85

0.48

Efficiency Ratio

2015 2016 2017

Figure 4: Figure representing Efficiency Ratios

(Source: As Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR BUSINESS

Conclusion:

On a decisive note the study, suggest that the general performance of the BHP Billiton

has been growing as the business has made advancement in technologies and constant

innovation so that it can reshape the operational strategy and market overall. The company

has been able to change the customer expectation with segmented goods from corner to

corner to its zone of processes. The financial analysis signifies that the corporation has

performed well in the marketplace by improving its proceeds from operations.

Conclusion:

On a decisive note the study, suggest that the general performance of the BHP Billiton

has been growing as the business has made advancement in technologies and constant

innovation so that it can reshape the operational strategy and market overall. The company

has been able to change the customer expectation with segmented goods from corner to

corner to its zone of processes. The financial analysis signifies that the corporation has

performed well in the marketplace by improving its proceeds from operations.

11FINANCE FOR BUSINESS

Reference List:

Asquith, P. and Weiss, L.A., 2016. Determining a Firm's Financial Health (PIPES‐

A). Lessons in Corporate Finance: A Case Studies Approach to Financial Tools, Financial

Policies, and Valuation, pp.7-25.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2), pp.339-383.

BHP Billiton. (2018). Financial results and operational reviews. [online] Available at:

https://www.bhp.com/investor-centre/financial-results-and-operational-reviews [Accessed 11

Jan. 2018].

BHP. (2018). BHP Billiton | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 11 Jan. 2018].

Board, A.P., 2015. Tetranormalization and the Accounting Standard-Setting

Process. Organizational Change and Global Standardization: Solutions to Standards and

Norms Overwhelming Organizations, p.69.

Cadden, D.T. and Schneider, G.P., 2014, January. Accounting and Entrepreneurship students:

Scope and delivery issues. In Allied Academies International Conference. Academy of

Entrepreneurship. Proceedings (Vol. 20, No. 1, p. 3). Jordan Whitney Enterprises, Inc.

Deegan, C., 2016. Financial accounting. McGraw-Hill Education Australia.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Reference List:

Asquith, P. and Weiss, L.A., 2016. Determining a Firm's Financial Health (PIPES‐

A). Lessons in Corporate Finance: A Case Studies Approach to Financial Tools, Financial

Policies, and Valuation, pp.7-25.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2), pp.339-383.

BHP Billiton. (2018). Financial results and operational reviews. [online] Available at:

https://www.bhp.com/investor-centre/financial-results-and-operational-reviews [Accessed 11

Jan. 2018].

BHP. (2018). BHP Billiton | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 11 Jan. 2018].

Board, A.P., 2015. Tetranormalization and the Accounting Standard-Setting

Process. Organizational Change and Global Standardization: Solutions to Standards and

Norms Overwhelming Organizations, p.69.

Cadden, D.T. and Schneider, G.P., 2014, January. Accounting and Entrepreneurship students:

Scope and delivery issues. In Allied Academies International Conference. Academy of

Entrepreneurship. Proceedings (Vol. 20, No. 1, p. 3). Jordan Whitney Enterprises, Inc.

Deegan, C., 2016. Financial accounting. McGraw-Hill Education Australia.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.