Finance for International Business

VerifiedAdded on 2023/03/23

|18

|3894

|68

AI Summary

Investment appraisal technique can be considered as an adequate measure that allows the organisations to identify the opportunity in an investment, which can eventually help them to improve the returns and generate higher revenue in the process.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE FOR INTERNATIONAL BUSINESS

Finance for International Business

Name of the Student:

Name of the University:

Authors Note:

Finance for International Business

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE FOR INTERNATIONAL BUSINESS 2

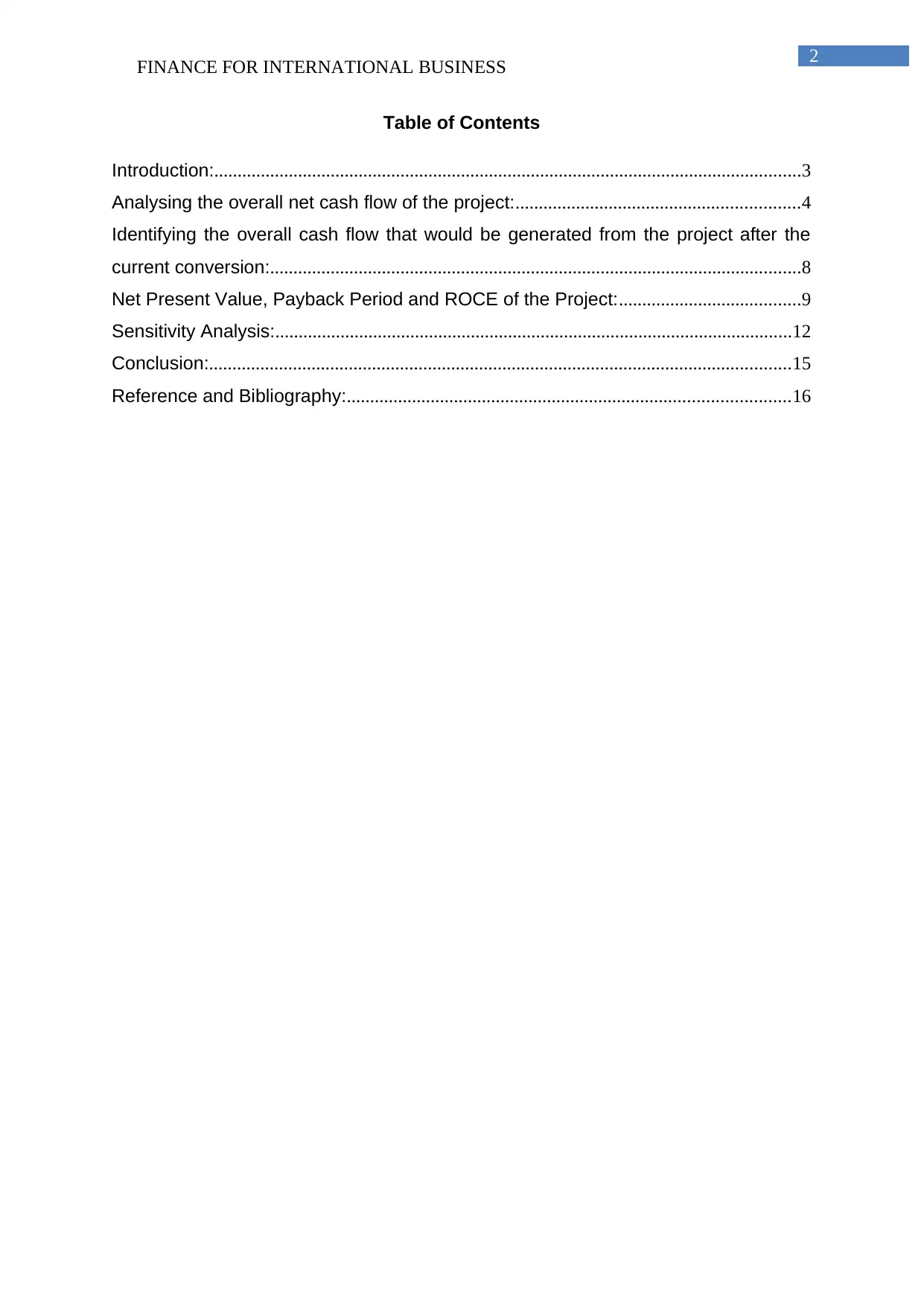

Table of Contents

Introduction:..............................................................................................................................3

Analysing the overall net cash flow of the project:.............................................................4

Identifying the overall cash flow that would be generated from the project after the

current conversion:..................................................................................................................8

Net Present Value, Payback Period and ROCE of the Project:.......................................9

Sensitivity Analysis:...............................................................................................................12

Conclusion:.............................................................................................................................15

Reference and Bibliography:...............................................................................................16

Table of Contents

Introduction:..............................................................................................................................3

Analysing the overall net cash flow of the project:.............................................................4

Identifying the overall cash flow that would be generated from the project after the

current conversion:..................................................................................................................8

Net Present Value, Payback Period and ROCE of the Project:.......................................9

Sensitivity Analysis:...............................................................................................................12

Conclusion:.............................................................................................................................15

Reference and Bibliography:...............................................................................................16

FINANCE FOR INTERNATIONAL BUSINESS 3

Introduction:

Investment appraisal technique can be considered as an adequate measure

that allows the organisations to identify the opportunity in an investment, which can

eventually help them to improve the returns and generate higher revenue in the

process. The assessment directly evaluates the project that was proposed to the

management of Organic Farm Foods Plc, which can improve their revenues in the

process. Moreover, the appraisal techniques such as net present value and payback

period has been utilised to detect whether the investment option is viable and could

generate the required rate of return in the process. Furthermore, the required rate of

return on capital employed is also calculated to determine the efficiency of the new

proposed project to improve the returns of Organic Farm Foods Plc.

Additionally, the project is situated with certain restrictions and limitation that

the has been followed to determine the level of changes in the company's overall

income and expenses in the long run. The relevant circumstances have been taken

into consideration to determine the overall of the company. Likewise, the currency

conversion rate has been taken into consideration to determine the level of free cash

flow that will be transferred to United Kingdom from Republic of Ireland. Moreover

adequate sensitivity analysis has been conducted to determine the level of changes

in the value of investment appraisal technique due to the alterations in fixed cost and

currency conversion rate.

Introduction:

Investment appraisal technique can be considered as an adequate measure

that allows the organisations to identify the opportunity in an investment, which can

eventually help them to improve the returns and generate higher revenue in the

process. The assessment directly evaluates the project that was proposed to the

management of Organic Farm Foods Plc, which can improve their revenues in the

process. Moreover, the appraisal techniques such as net present value and payback

period has been utilised to detect whether the investment option is viable and could

generate the required rate of return in the process. Furthermore, the required rate of

return on capital employed is also calculated to determine the efficiency of the new

proposed project to improve the returns of Organic Farm Foods Plc.

Additionally, the project is situated with certain restrictions and limitation that

the has been followed to determine the level of changes in the company's overall

income and expenses in the long run. The relevant circumstances have been taken

into consideration to determine the overall of the company. Likewise, the currency

conversion rate has been taken into consideration to determine the level of free cash

flow that will be transferred to United Kingdom from Republic of Ireland. Moreover

adequate sensitivity analysis has been conducted to determine the level of changes

in the value of investment appraisal technique due to the alterations in fixed cost and

currency conversion rate.

FINANCE FOR INTERNATIONAL BUSINESS 4

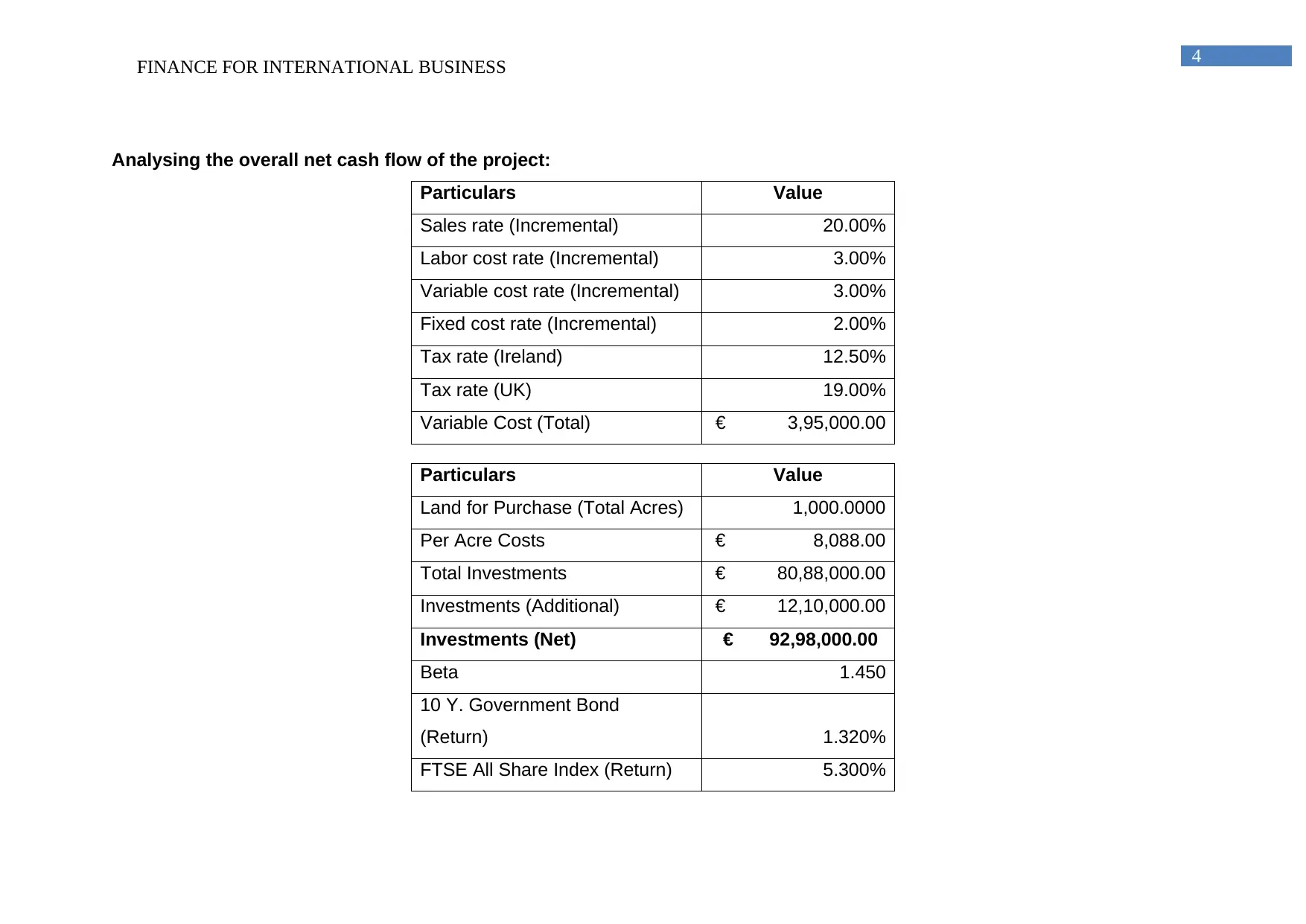

Analysing the overall net cash flow of the project:

Particulars Value

Sales rate (Incremental) 20.00%

Labor cost rate (Incremental) 3.00%

Variable cost rate (Incremental) 3.00%

Fixed cost rate (Incremental) 2.00%

Tax rate (Ireland) 12.50%

Tax rate (UK) 19.00%

Variable Cost (Total) € 3,95,000.00

Particulars Value

Land for Purchase (Total Acres) 1,000.0000

Per Acre Costs € 8,088.00

Total Investments € 80,88,000.00

Investments (Additional) € 12,10,000.00

Investments (Net) € 92,98,000.00

Beta 1.450

10 Y. Government Bond

(Return) 1.320%

FTSE All Share Index (Return) 5.300%

Analysing the overall net cash flow of the project:

Particulars Value

Sales rate (Incremental) 20.00%

Labor cost rate (Incremental) 3.00%

Variable cost rate (Incremental) 3.00%

Fixed cost rate (Incremental) 2.00%

Tax rate (Ireland) 12.50%

Tax rate (UK) 19.00%

Variable Cost (Total) € 3,95,000.00

Particulars Value

Land for Purchase (Total Acres) 1,000.0000

Per Acre Costs € 8,088.00

Total Investments € 80,88,000.00

Investments (Additional) € 12,10,000.00

Investments (Net) € 92,98,000.00

Beta 1.450

10 Y. Government Bond

(Return) 1.320%

FTSE All Share Index (Return) 5.300%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE FOR INTERNATIONAL BUSINESS 5

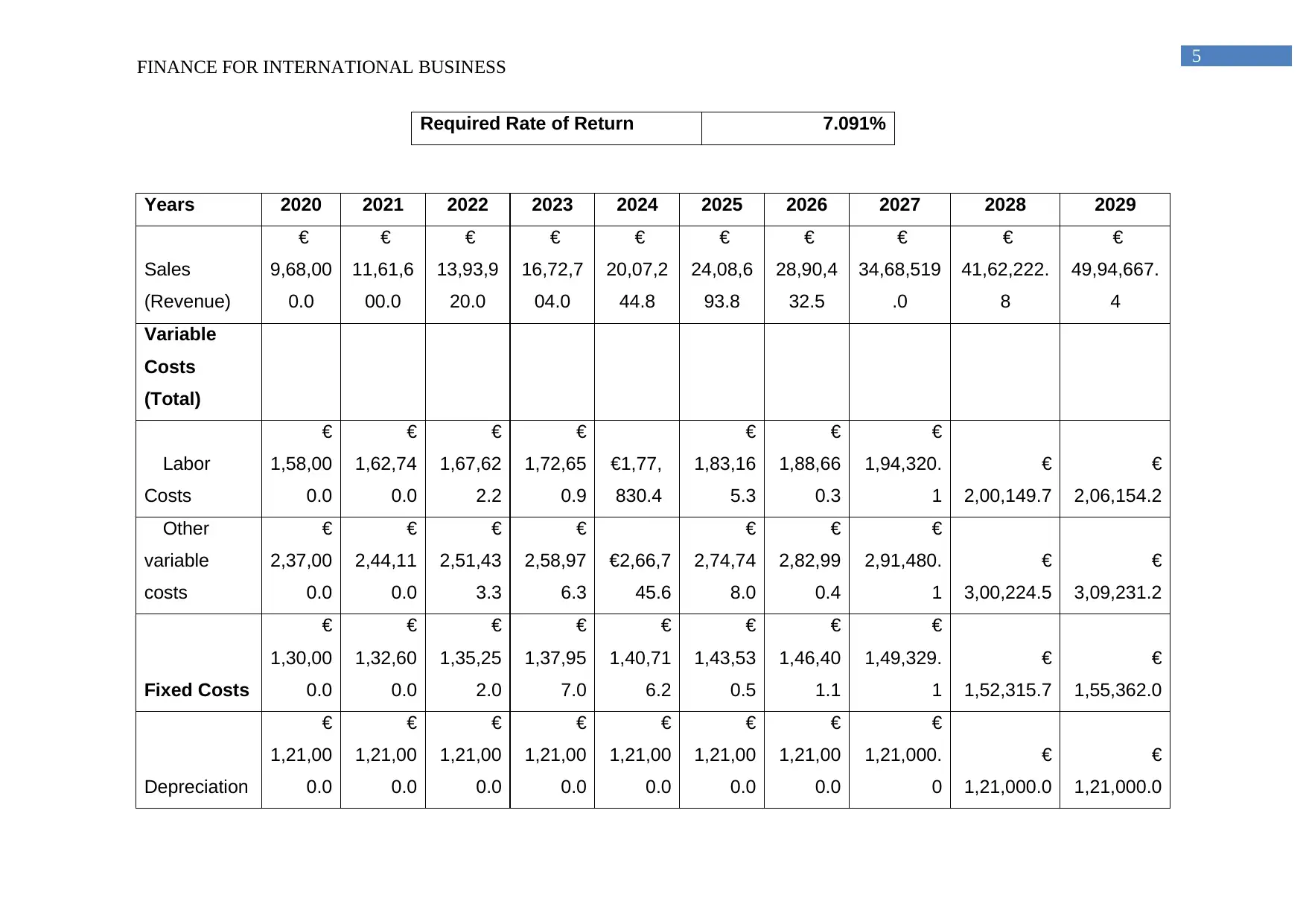

Required Rate of Return 7.091%

Years 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

Sales

(Revenue)

€

9,68,00

0.0

€

11,61,6

00.0

€

13,93,9

20.0

€

16,72,7

04.0

€

20,07,2

44.8

€

24,08,6

93.8

€

28,90,4

32.5

€

34,68,519

.0

€

41,62,222.

8

€

49,94,667.

4

Variable

Costs

(Total)

Labor

Costs

€

1,58,00

0.0

€

1,62,74

0.0

€

1,67,62

2.2

€

1,72,65

0.9

€1,77,

830.4

€

1,83,16

5.3

€

1,88,66

0.3

€

1,94,320.

1

€

2,00,149.7

€

2,06,154.2

Other

variable

costs

€

2,37,00

0.0

€

2,44,11

0.0

€

2,51,43

3.3

€

2,58,97

6.3

€2,66,7

45.6

€

2,74,74

8.0

€

2,82,99

0.4

€

2,91,480.

1

€

3,00,224.5

€

3,09,231.2

Fixed Costs

€

1,30,00

0.0

€

1,32,60

0.0

€

1,35,25

2.0

€

1,37,95

7.0

€

1,40,71

6.2

€

1,43,53

0.5

€

1,46,40

1.1

€

1,49,329.

1

€

1,52,315.7

€

1,55,362.0

Depreciation

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,000.

0

€

1,21,000.0

€

1,21,000.0

Required Rate of Return 7.091%

Years 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

Sales

(Revenue)

€

9,68,00

0.0

€

11,61,6

00.0

€

13,93,9

20.0

€

16,72,7

04.0

€

20,07,2

44.8

€

24,08,6

93.8

€

28,90,4

32.5

€

34,68,519

.0

€

41,62,222.

8

€

49,94,667.

4

Variable

Costs

(Total)

Labor

Costs

€

1,58,00

0.0

€

1,62,74

0.0

€

1,67,62

2.2

€

1,72,65

0.9

€1,77,

830.4

€

1,83,16

5.3

€

1,88,66

0.3

€

1,94,320.

1

€

2,00,149.7

€

2,06,154.2

Other

variable

costs

€

2,37,00

0.0

€

2,44,11

0.0

€

2,51,43

3.3

€

2,58,97

6.3

€2,66,7

45.6

€

2,74,74

8.0

€

2,82,99

0.4

€

2,91,480.

1

€

3,00,224.5

€

3,09,231.2

Fixed Costs

€

1,30,00

0.0

€

1,32,60

0.0

€

1,35,25

2.0

€

1,37,95

7.0

€

1,40,71

6.2

€

1,43,53

0.5

€

1,46,40

1.1

€

1,49,329.

1

€

1,52,315.7

€

1,55,362.0

Depreciation

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,000.

0

€

1,21,000.0

€

1,21,000.0

FINANCE FOR INTERNATIONAL BUSINESS 6

Total

Expenses

€

6,46,00

0.0

€

6,60,45

0.0

€

6,75,30

7.5

€

6,90,58

4.2

€

7,06,29

2.2

€

7,22,44

3.8

€

7,39,05

1.8

€

7,56,129.

3

€

7,73,689.9

€

7,91,747.4

PBT

€

3,22,00

0.0

€

5,01,15

0.0

€

7,18,61

2.5

€

9,82,11

9.8

€

13,00,9

52.6

€

16,86,2

50.0

€

21,51,3

80.7

€

27,12,389

.7

€

33,88,532.

9

€

42,02,919.

9

Tax

€

40,250.

0

€

62,643.

8

€

89,826.

6

€

1,22,76

5.0

€

1,62,61

9.1

€

2,10,78

1.2

€

2,68,92

2.6

€

3,39,048.

7

€

4,23,566.6

€

5,25,365.0

Net Profit

€

2,81,75

0.0

€

4,38,50

6.3

€

6,28,78

5.9

€

8,59,35

4.8

€

11,38,3

33.6

€

14,75,4

68.7

€

18,82,4

58.1

€

23,73,341

.0

€

29,64,966.

3

€

36,77,554.

9

Depreciation

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,000.

0

€

1,21,000.0

€

1,21,000.0

Net Cash

flow

€

4,02,75

0.0

€

5,59,50

6.3

€

7,49,78

5.9

€

9,80,35

4.8

€

12,59,3

33.6

€

15,96,4

68.7

€

20,03,4

58.1

€

24,94,341

.0

€

30,85,966.

3

€

37,98,554.

9

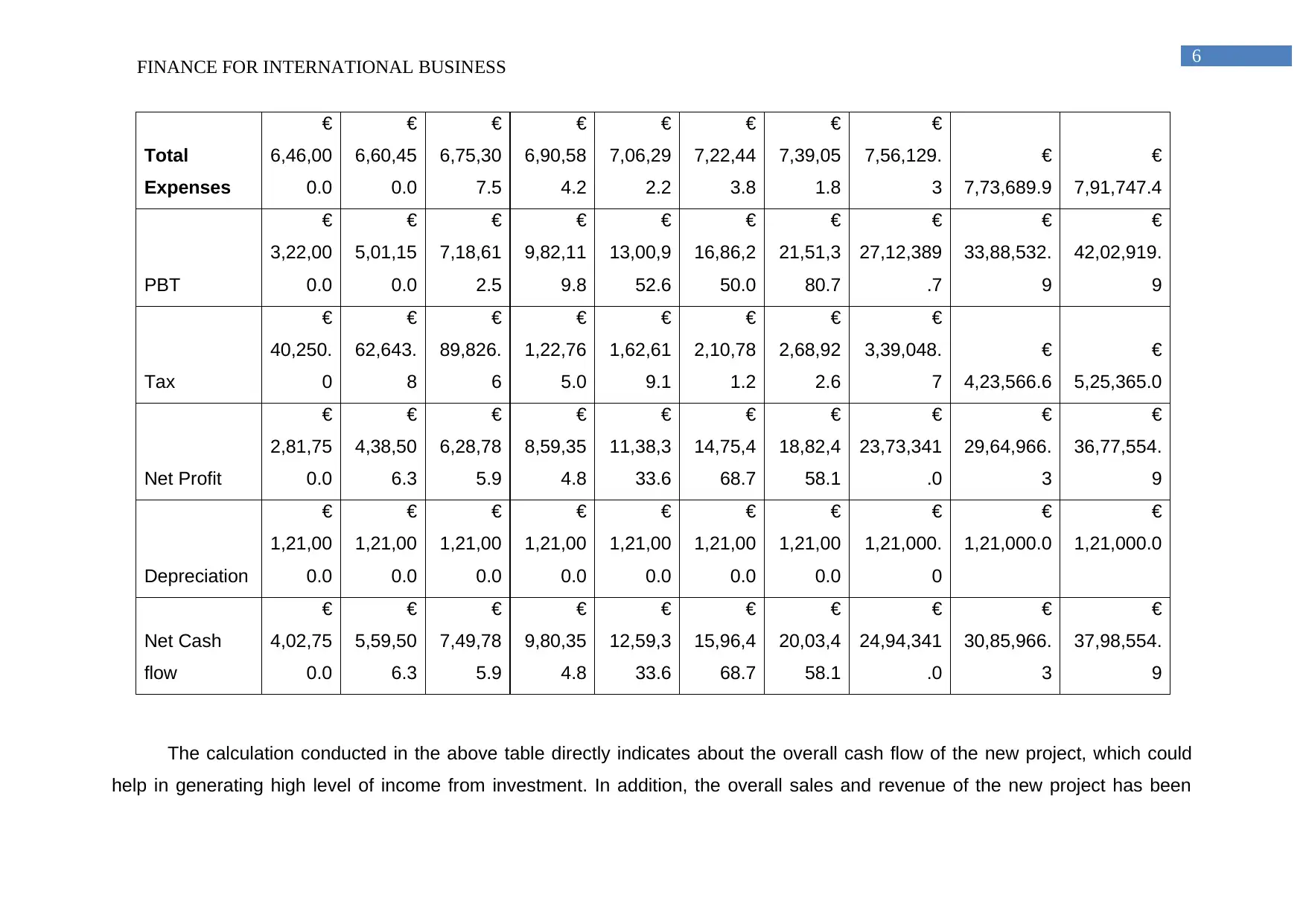

The calculation conducted in the above table directly indicates about the overall cash flow of the new project, which could

help in generating high level of income from investment. In addition, the overall sales and revenue of the new project has been

Total

Expenses

€

6,46,00

0.0

€

6,60,45

0.0

€

6,75,30

7.5

€

6,90,58

4.2

€

7,06,29

2.2

€

7,22,44

3.8

€

7,39,05

1.8

€

7,56,129.

3

€

7,73,689.9

€

7,91,747.4

PBT

€

3,22,00

0.0

€

5,01,15

0.0

€

7,18,61

2.5

€

9,82,11

9.8

€

13,00,9

52.6

€

16,86,2

50.0

€

21,51,3

80.7

€

27,12,389

.7

€

33,88,532.

9

€

42,02,919.

9

Tax

€

40,250.

0

€

62,643.

8

€

89,826.

6

€

1,22,76

5.0

€

1,62,61

9.1

€

2,10,78

1.2

€

2,68,92

2.6

€

3,39,048.

7

€

4,23,566.6

€

5,25,365.0

Net Profit

€

2,81,75

0.0

€

4,38,50

6.3

€

6,28,78

5.9

€

8,59,35

4.8

€

11,38,3

33.6

€

14,75,4

68.7

€

18,82,4

58.1

€

23,73,341

.0

€

29,64,966.

3

€

36,77,554.

9

Depreciation

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,00

0.0

€

1,21,000.

0

€

1,21,000.0

€

1,21,000.0

Net Cash

flow

€

4,02,75

0.0

€

5,59,50

6.3

€

7,49,78

5.9

€

9,80,35

4.8

€

12,59,3

33.6

€

15,96,4

68.7

€

20,03,4

58.1

€

24,94,341

.0

€

30,85,966.

3

€

37,98,554.

9

The calculation conducted in the above table directly indicates about the overall cash flow of the new project, which could

help in generating high level of income from investment. In addition, the overall sales and revenue of the new project has been

FINANCE FOR INTERNATIONAL BUSINESS 7

depicted in the above table, which is used for determining the free cash flow of the project. Moreover, the overall beta for the

organization, risk free rate of the country and market retune of the stock market is used for determine the cost of capital for the

organization, which is used for analyzing the net present value of the project. Moreover, the net cash flow of the organization has

been calculated on the basis elephant assumptions such as required rate of return, which has been calculated with the help of

Capital Asset pricing formula and is at 7.09%. This cost of capital is relatively been utilized for determining the level of present

value of future cash flows that would be generated from the project. Likewise, the net cash flow of the project is mainly derived by

deducting the relevant cost factors that would affect the overall income of new project. Besides, the overall sales revenue of the

project is detected to increase at the levels of 20% for the period of 9 years after the initial 1st year sales. In the similar instance,

the overall fixed cost and labor cost of the new project will be increased by 2% and 3% over the period of 9 years. The total variable

cost of the project is related derived by adding both the total labor cost and other variable cost incurred by the project. Therefore, it

could be understood that the overall variable cost has increased by the levels of 3% over the period of 9 years. On the other hand,

the fixed cost has increased by 2% in comparison to the values depicted in first year, which has helped in determining the accurate

level of net cash flows from the project (McLean and Zhao 2014).

The net cash flow has also evaluated adequate depreciation values to determine the Irish branch would conduct the level of

tax saving that. The inclusion of depreciation has relatively helped in increasing the level of net cash flows projected by the project

over the period of 10 years. Hence, the cash flows determined after the accommodation of depreciation section assertively help in

determining the overall amount that would be transferred from Ireland to United Kingdom. Shenkar, Luo and Chi (2014) Indicated

that with the help of investment appraisal techniques investors are able to determine the current and actual flow of cash that would

be generated from a project over the period of time.

depicted in the above table, which is used for determining the free cash flow of the project. Moreover, the overall beta for the

organization, risk free rate of the country and market retune of the stock market is used for determine the cost of capital for the

organization, which is used for analyzing the net present value of the project. Moreover, the net cash flow of the organization has

been calculated on the basis elephant assumptions such as required rate of return, which has been calculated with the help of

Capital Asset pricing formula and is at 7.09%. This cost of capital is relatively been utilized for determining the level of present

value of future cash flows that would be generated from the project. Likewise, the net cash flow of the project is mainly derived by

deducting the relevant cost factors that would affect the overall income of new project. Besides, the overall sales revenue of the

project is detected to increase at the levels of 20% for the period of 9 years after the initial 1st year sales. In the similar instance,

the overall fixed cost and labor cost of the new project will be increased by 2% and 3% over the period of 9 years. The total variable

cost of the project is related derived by adding both the total labor cost and other variable cost incurred by the project. Therefore, it

could be understood that the overall variable cost has increased by the levels of 3% over the period of 9 years. On the other hand,

the fixed cost has increased by 2% in comparison to the values depicted in first year, which has helped in determining the accurate

level of net cash flows from the project (McLean and Zhao 2014).

The net cash flow has also evaluated adequate depreciation values to determine the Irish branch would conduct the level of

tax saving that. The inclusion of depreciation has relatively helped in increasing the level of net cash flows projected by the project

over the period of 10 years. Hence, the cash flows determined after the accommodation of depreciation section assertively help in

determining the overall amount that would be transferred from Ireland to United Kingdom. Shenkar, Luo and Chi (2014) Indicated

that with the help of investment appraisal techniques investors are able to determine the current and actual flow of cash that would

be generated from a project over the period of time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR INTERNATIONAL BUSINESS 8

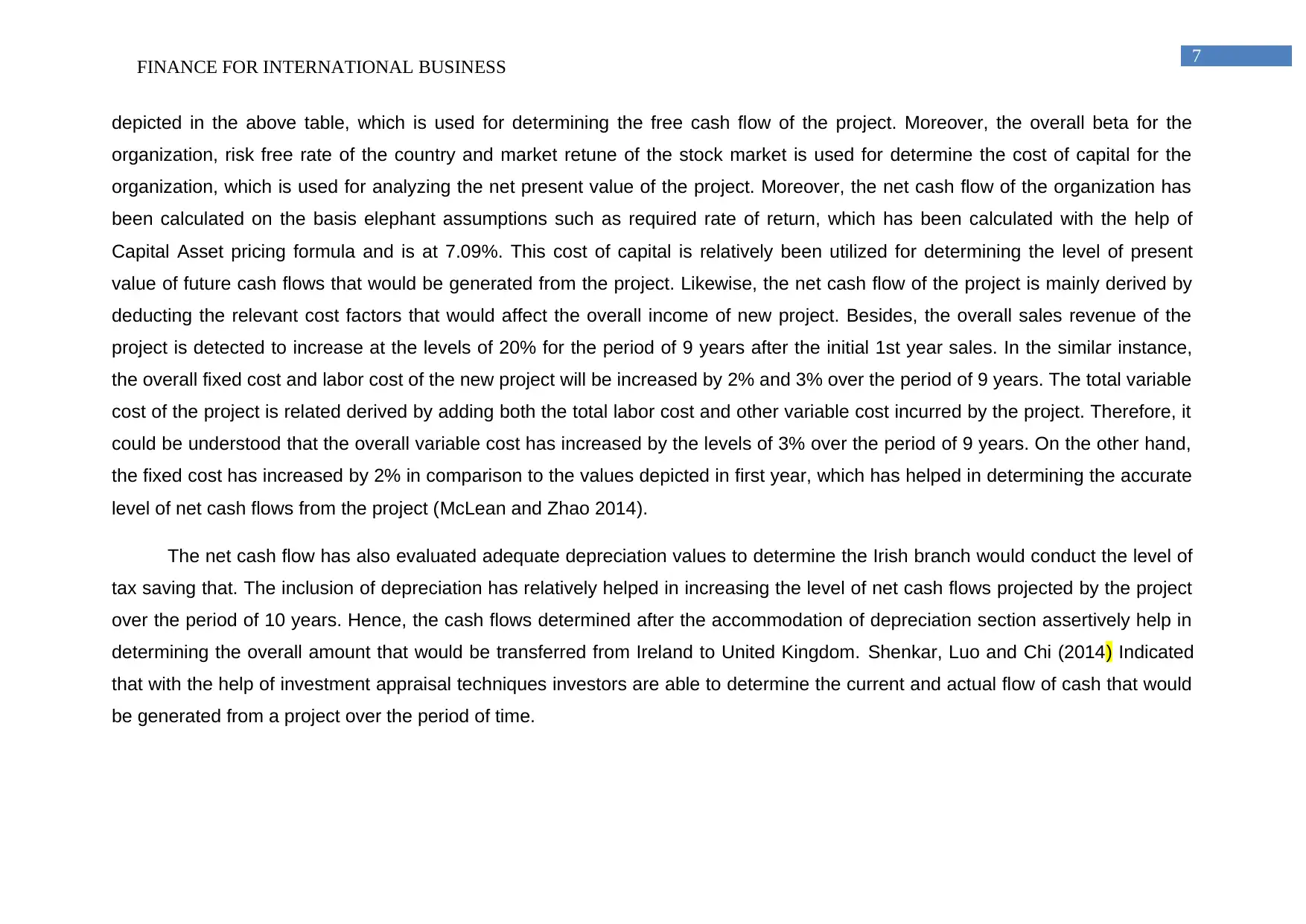

Identifying the overall cash flow that would be generated from the project after

the current conversion:

Years Net Cash flow

Additional Tax @

6.5% Estimated Cash flow

2020 £3,32,851.2 £21,635.3 £3,11,215.9

2021 £4,62,401.9 £30,056.1 £4,32,345.7

2022 £6,19,657.8 £40,277.8 £5,79,380.0

2023 £8,10,210.6 £52,663.7 £7,57,546.9

2024 £10,40,771.5 £67,650.1 £9,73,121.4

2025 £13,19,395.7 £85,760.7 £12,33,634.9

2026 £16,55,750.5 £1,07,623.8 £15,48,126.8

2027 £20,61,438.8 £1,33,993.5 £19,27,445.3

2028 £25,50,385.4 £1,65,775.0 £23,84,610.3

2029 £31,39,301.6 £2,04,054.6 £29,35,247.0

Exchange Rate (£1 = € 1.21) 0.826446281 1.21

The calculations conducted in the above table directly provide information

about the overall net cash flow that has been generated by the overall project after

converting it from euro to pound currency. The net cash flow of the overall project

has been determined in in British Pound to allow the organisation in United Kingdom

to determine the efficiency of the project and its profitability over the period of 10

years. From the relevant calculations, it could be understood that with the help of

currency conversion rate the overall net cash flow of the project is determined and

converted from Euro currency to British Pound currency. Moreover, additional tax of

6.5 % is added to the overall net cash flow of the project. This additional tax rate is

due to the higher tax charge in United Kingdom in comparison to Ireland. The tax

rate in Ireland is at the level of 12.5%, while the tax rate in UK is at 19%, where the

additional tax calculated for the project that needs to be paid in UK is 6.5%.

The additional tax that needs to be paid by the Organic Foods PLC is due to

the higher tax rate of United Kingdom and the Treaty that has been signed between

the European Union (Papadopoulos and Heslop 2014). The treaty relatively helps

and minimising the occurrence of double taxation among the countries such as

Identifying the overall cash flow that would be generated from the project after

the current conversion:

Years Net Cash flow

Additional Tax @

6.5% Estimated Cash flow

2020 £3,32,851.2 £21,635.3 £3,11,215.9

2021 £4,62,401.9 £30,056.1 £4,32,345.7

2022 £6,19,657.8 £40,277.8 £5,79,380.0

2023 £8,10,210.6 £52,663.7 £7,57,546.9

2024 £10,40,771.5 £67,650.1 £9,73,121.4

2025 £13,19,395.7 £85,760.7 £12,33,634.9

2026 £16,55,750.5 £1,07,623.8 £15,48,126.8

2027 £20,61,438.8 £1,33,993.5 £19,27,445.3

2028 £25,50,385.4 £1,65,775.0 £23,84,610.3

2029 £31,39,301.6 £2,04,054.6 £29,35,247.0

Exchange Rate (£1 = € 1.21) 0.826446281 1.21

The calculations conducted in the above table directly provide information

about the overall net cash flow that has been generated by the overall project after

converting it from euro to pound currency. The net cash flow of the overall project

has been determined in in British Pound to allow the organisation in United Kingdom

to determine the efficiency of the project and its profitability over the period of 10

years. From the relevant calculations, it could be understood that with the help of

currency conversion rate the overall net cash flow of the project is determined and

converted from Euro currency to British Pound currency. Moreover, additional tax of

6.5 % is added to the overall net cash flow of the project. This additional tax rate is

due to the higher tax charge in United Kingdom in comparison to Ireland. The tax

rate in Ireland is at the level of 12.5%, while the tax rate in UK is at 19%, where the

additional tax calculated for the project that needs to be paid in UK is 6.5%.

The additional tax that needs to be paid by the Organic Foods PLC is due to

the higher tax rate of United Kingdom and the Treaty that has been signed between

the European Union (Papadopoulos and Heslop 2014). The treaty relatively helps

and minimising the occurrence of double taxation among the countries such as

FINANCE FOR INTERNATIONAL BUSINESS 9

United Kingdom and Ireland. This is the main reason why the taxation rate of 19% in

United Kingdom has been reduced to the levels of 6.5%, as the overall 12.5% tax

rate has been paid in Ireland, which is not taxed in United Kingdom due to the

presence of double taxation policy. The case study directly provides information

about the exchange rate that converts British Pound to Euro currency, where

adequate calculations have been conducted to derive the inverted values of the

currencies. Hence, the (£1 = € 1.2) is converted into (€1= £0.826446281).This

derivation of the currency conversion rate has relatively helped in determining the

overall value of the euro that has been generated from Ireland in British pounds.

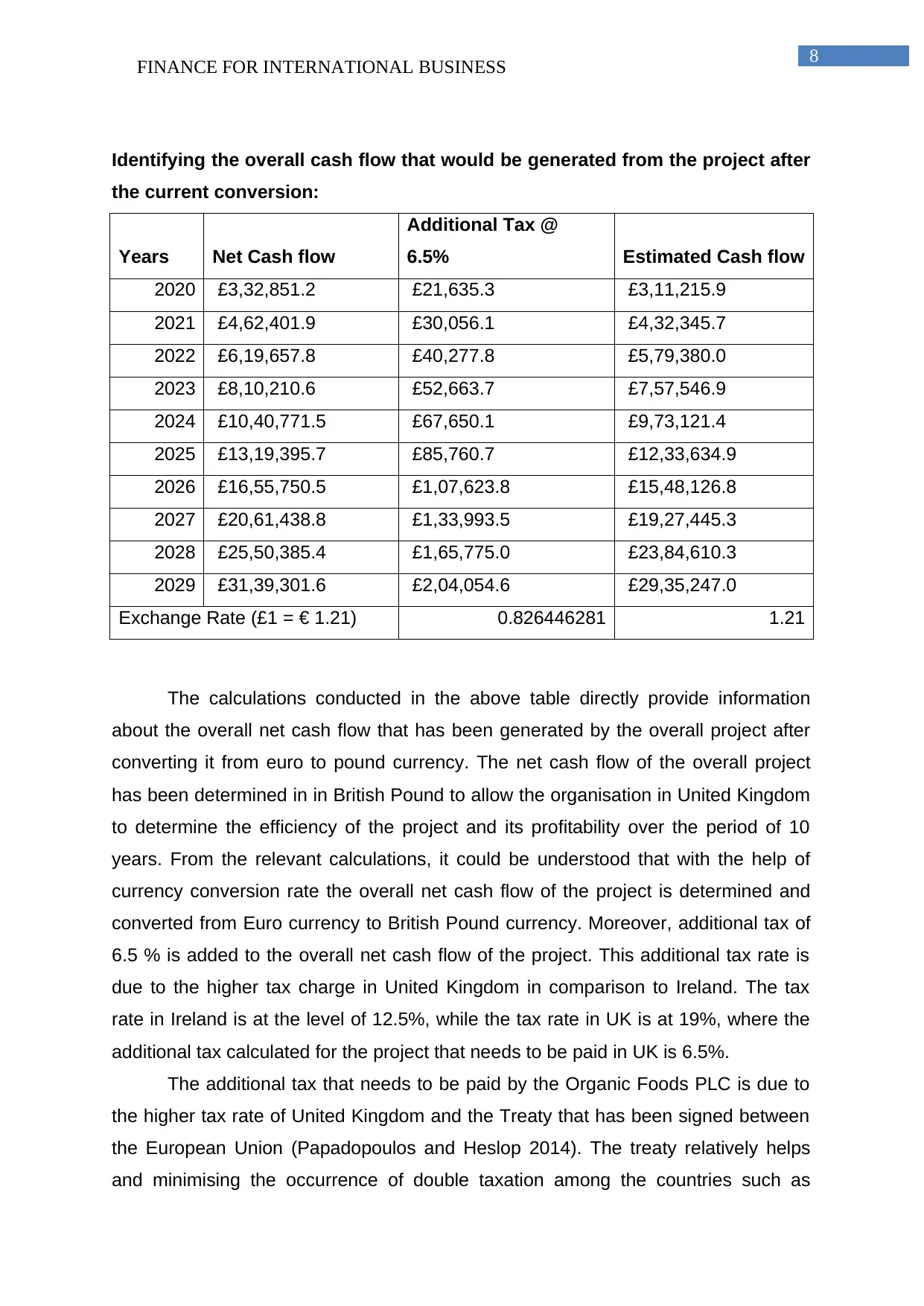

Net Present Value, Payback Period and ROCE of the Project:

Probabilit

y Change in Net cash flow

Normal trading terms 55.0% 0.0%

Favorable trading terms 30.0% 15.0%

Unfavorable trading terms 15.0% -30.0%

Year

202

0 2021 2022

202

3 2024

202

5

202

6

202

7

202

8

202

9

Norm

al

tradin

g

terms

£

3,11

,215

.9

£

4,32,345.7

£

5,79,

380.0

£

7,57

,546

.9

£

9,73,1

21.4

£

12,3

3,63

4.9

£

15,4

8,12

6.8

£

19,2

7,44

5.3

£

23,8

4,61

0.3

£

29,3

5,24

7.0

Favor

able

tradin

g

terms

£

3,57

,898

.3

£

4,97,197.6

£

6,66,

287.0

£

8,71

,178

.9

£

11,19,

089.6

£

14,1

8,68

0.2

£

17,8

0,34

5.8

£

22,1

6,56

2.1

£

27,4

2,30

1.9

£

33,7

5,53

4.1

Unfa

vorab

le

tradin

£

2,17

,851

£

3,02,642.0

£

4,05,

566.0

£

5,30

,282

£

6,81,1

85.0

£

8,63

,544

£

10,8

3,68

£

13,4

9,21

£

16,6

9,22

£

20,5

4,67

United Kingdom and Ireland. This is the main reason why the taxation rate of 19% in

United Kingdom has been reduced to the levels of 6.5%, as the overall 12.5% tax

rate has been paid in Ireland, which is not taxed in United Kingdom due to the

presence of double taxation policy. The case study directly provides information

about the exchange rate that converts British Pound to Euro currency, where

adequate calculations have been conducted to derive the inverted values of the

currencies. Hence, the (£1 = € 1.2) is converted into (€1= £0.826446281).This

derivation of the currency conversion rate has relatively helped in determining the

overall value of the euro that has been generated from Ireland in British pounds.

Net Present Value, Payback Period and ROCE of the Project:

Probabilit

y Change in Net cash flow

Normal trading terms 55.0% 0.0%

Favorable trading terms 30.0% 15.0%

Unfavorable trading terms 15.0% -30.0%

Year

202

0 2021 2022

202

3 2024

202

5

202

6

202

7

202

8

202

9

Norm

al

tradin

g

terms

£

3,11

,215

.9

£

4,32,345.7

£

5,79,

380.0

£

7,57

,546

.9

£

9,73,1

21.4

£

12,3

3,63

4.9

£

15,4

8,12

6.8

£

19,2

7,44

5.3

£

23,8

4,61

0.3

£

29,3

5,24

7.0

Favor

able

tradin

g

terms

£

3,57

,898

.3

£

4,97,197.6

£

6,66,

287.0

£

8,71

,178

.9

£

11,19,

089.6

£

14,1

8,68

0.2

£

17,8

0,34

5.8

£

22,1

6,56

2.1

£

27,4

2,30

1.9

£

33,7

5,53

4.1

Unfa

vorab

le

tradin

£

2,17

,851

£

3,02,642.0

£

4,05,

566.0

£

5,30

,282

£

6,81,1

85.0

£

8,63

,544

£

10,8

3,68

£

13,4

9,21

£

16,6

9,22

£

20,5

4,67

FINANCE FOR INTERNATIONAL BUSINESS 10

g

terms .1 .8 .5 8.7 1.7 7.2 2.9

Over

all

estim

ated

cash

flow

£

3,11

,215

.9

£

4,32,345.7

£

5,79,

380.0

£

7,57

,546

.9

£

9,73,1

21.4

£

12,3

3,63

4.9

£

15,4

8,12

6.8

£

19,2

7,44

5.3

£

23,8

4,61

0.3

£

29,3

5,24

7.0

Cum

ulativ

e

Cash

flow

-£

73,7

3,08

1.6

-£

69,40,735.

9

-£

63,61

,355.

8

-£

56,0

3,80

8.9

-£

46,30,

687.5

-£

33,9

7,05

2.6

-£

18,4

8,92

5.8

£

78,5

19.5

£

24,6

3,12

9.8

£

53,9

8,37

6.8

PV

factor

0.93

379 0.87195

0.814

22

0.76

031

0.709

96

0.66

295

0.61

905

0.57

806

0.53

979

0.50

405

Over

all

estim

ated

cash

flow

£

2,90

,608

.8

£

3,76,986.0

£

4,71,

742.1

£

5,75

,967

.0

£

6,90,8

79.2

£

8,17

,840

.9

£

9,58

,375

.5

£

11,1

4,18

7.5

£

12,8

7,18

4.1

£

14,7

9,49

9.8

Net Present Value £ 3,78,973.410

ROCE 1.04932

Payback period 7.95926 years

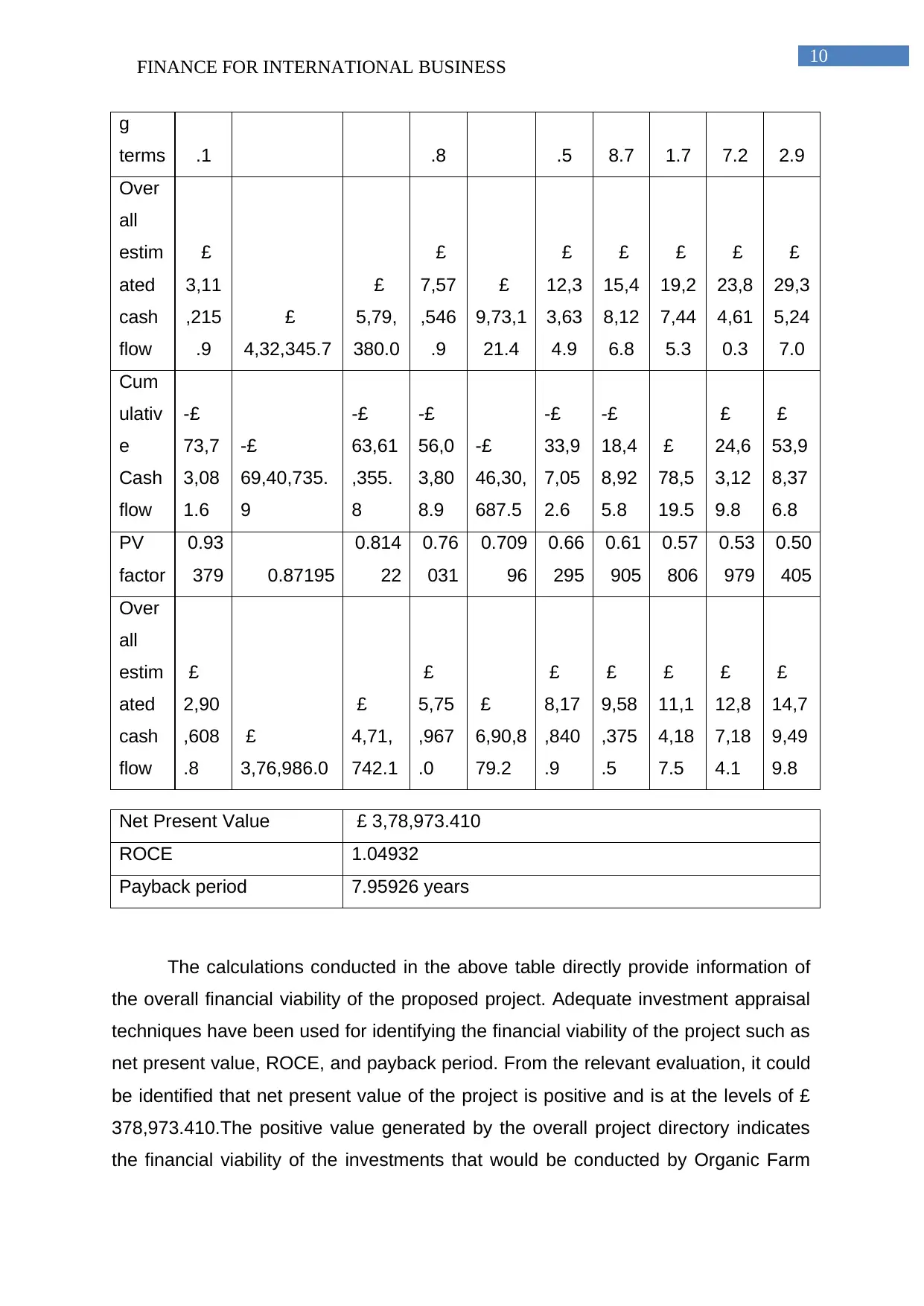

The calculations conducted in the above table directly provide information of

the overall financial viability of the proposed project. Adequate investment appraisal

techniques have been used for identifying the financial viability of the project such as

net present value, ROCE, and payback period. From the relevant evaluation, it could

be identified that net present value of the project is positive and is at the levels of £

378,973.410.The positive value generated by the overall project directory indicates

the financial viability of the investments that would be conducted by Organic Farm

g

terms .1 .8 .5 8.7 1.7 7.2 2.9

Over

all

estim

ated

cash

flow

£

3,11

,215

.9

£

4,32,345.7

£

5,79,

380.0

£

7,57

,546

.9

£

9,73,1

21.4

£

12,3

3,63

4.9

£

15,4

8,12

6.8

£

19,2

7,44

5.3

£

23,8

4,61

0.3

£

29,3

5,24

7.0

Cum

ulativ

e

Cash

flow

-£

73,7

3,08

1.6

-£

69,40,735.

9

-£

63,61

,355.

8

-£

56,0

3,80

8.9

-£

46,30,

687.5

-£

33,9

7,05

2.6

-£

18,4

8,92

5.8

£

78,5

19.5

£

24,6

3,12

9.8

£

53,9

8,37

6.8

PV

factor

0.93

379 0.87195

0.814

22

0.76

031

0.709

96

0.66

295

0.61

905

0.57

806

0.53

979

0.50

405

Over

all

estim

ated

cash

flow

£

2,90

,608

.8

£

3,76,986.0

£

4,71,

742.1

£

5,75

,967

.0

£

6,90,8

79.2

£

8,17

,840

.9

£

9,58

,375

.5

£

11,1

4,18

7.5

£

12,8

7,18

4.1

£

14,7

9,49

9.8

Net Present Value £ 3,78,973.410

ROCE 1.04932

Payback period 7.95926 years

The calculations conducted in the above table directly provide information of

the overall financial viability of the proposed project. Adequate investment appraisal

techniques have been used for identifying the financial viability of the project such as

net present value, ROCE, and payback period. From the relevant evaluation, it could

be identified that net present value of the project is positive and is at the levels of £

378,973.410.The positive value generated by the overall project directory indicates

the financial viability of the investments that would be conducted by Organic Farm

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE FOR INTERNATIONAL BUSINESS 11

Food PLC in Ireland (Sassen 2017). Furthermore, the calculations are also

conducted on return on capital employed, which is at the levels of 1.04932, which is

relatively adequate for investment purposes. However, Payback Period of the overall

project is at the levels of 7.9 years, which directly violates the requirements that are

needed by the management of Organic Farms Foods PLC.

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

£-

£500,000.0

£1,000,000.0

£1,500,000.0

£2,000,000.0

£2,500,000.0

£3,000,000.0

£3,500,000.0

£4,000,000.0

Cashflows in different scenario

Favourable trading terms Unfavourable trading terms

Overall estimated cash flow

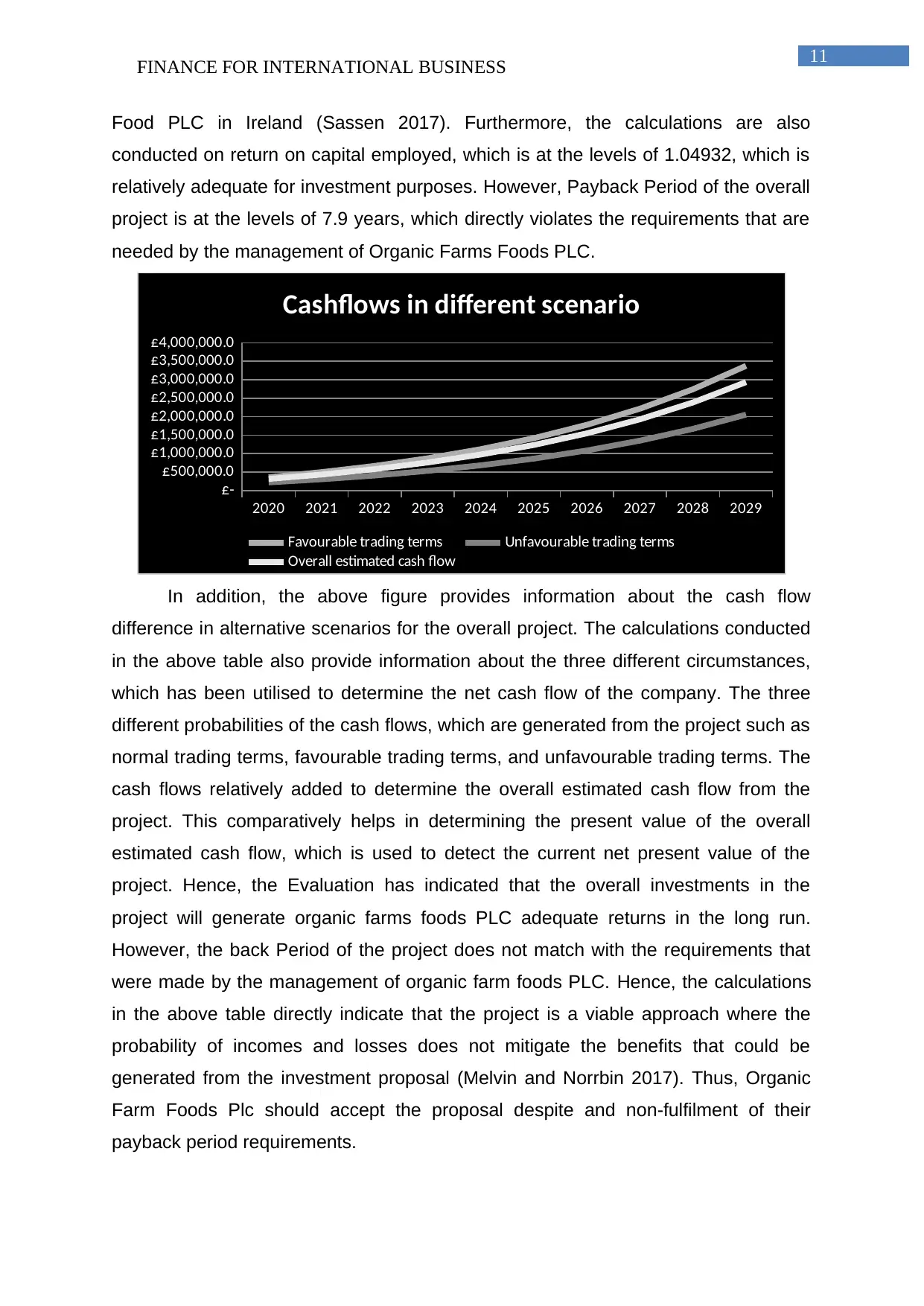

In addition, the above figure provides information about the cash flow

difference in alternative scenarios for the overall project. The calculations conducted

in the above table also provide information about the three different circumstances,

which has been utilised to determine the net cash flow of the company. The three

different probabilities of the cash flows, which are generated from the project such as

normal trading terms, favourable trading terms, and unfavourable trading terms. The

cash flows relatively added to determine the overall estimated cash flow from the

project. This comparatively helps in determining the present value of the overall

estimated cash flow, which is used to detect the current net present value of the

project. Hence, the Evaluation has indicated that the overall investments in the

project will generate organic farms foods PLC adequate returns in the long run.

However, the back Period of the project does not match with the requirements that

were made by the management of organic farm foods PLC. Hence, the calculations

in the above table directly indicate that the project is a viable approach where the

probability of incomes and losses does not mitigate the benefits that could be

generated from the investment proposal (Melvin and Norrbin 2017). Thus, Organic

Farm Foods Plc should accept the proposal despite and non-fulfilment of their

payback period requirements.

Food PLC in Ireland (Sassen 2017). Furthermore, the calculations are also

conducted on return on capital employed, which is at the levels of 1.04932, which is

relatively adequate for investment purposes. However, Payback Period of the overall

project is at the levels of 7.9 years, which directly violates the requirements that are

needed by the management of Organic Farms Foods PLC.

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

£-

£500,000.0

£1,000,000.0

£1,500,000.0

£2,000,000.0

£2,500,000.0

£3,000,000.0

£3,500,000.0

£4,000,000.0

Cashflows in different scenario

Favourable trading terms Unfavourable trading terms

Overall estimated cash flow

In addition, the above figure provides information about the cash flow

difference in alternative scenarios for the overall project. The calculations conducted

in the above table also provide information about the three different circumstances,

which has been utilised to determine the net cash flow of the company. The three

different probabilities of the cash flows, which are generated from the project such as

normal trading terms, favourable trading terms, and unfavourable trading terms. The

cash flows relatively added to determine the overall estimated cash flow from the

project. This comparatively helps in determining the present value of the overall

estimated cash flow, which is used to detect the current net present value of the

project. Hence, the Evaluation has indicated that the overall investments in the

project will generate organic farms foods PLC adequate returns in the long run.

However, the back Period of the project does not match with the requirements that

were made by the management of organic farm foods PLC. Hence, the calculations

in the above table directly indicate that the project is a viable approach where the

probability of incomes and losses does not mitigate the benefits that could be

generated from the investment proposal (Melvin and Norrbin 2017). Thus, Organic

Farm Foods Plc should accept the proposal despite and non-fulfilment of their

payback period requirements.

FINANCE FOR INTERNATIONAL BUSINESS 12

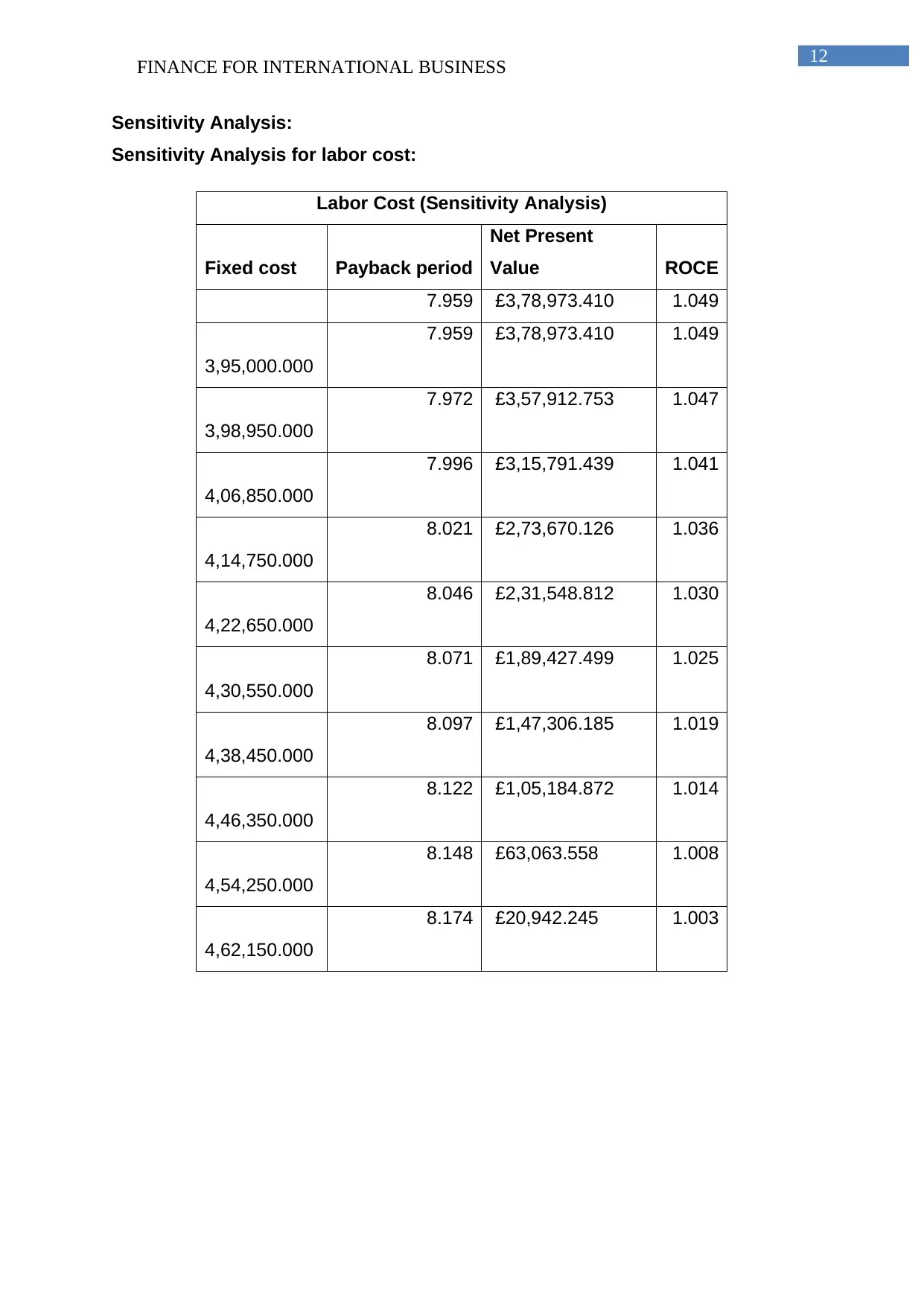

Sensitivity Analysis:

Sensitivity Analysis for labor cost:

Labor Cost (Sensitivity Analysis)

Fixed cost Payback period

Net Present

Value ROCE

7.959 £3,78,973.410 1.049

3,95,000.000

7.959 £3,78,973.410 1.049

3,98,950.000

7.972 £3,57,912.753 1.047

4,06,850.000

7.996 £3,15,791.439 1.041

4,14,750.000

8.021 £2,73,670.126 1.036

4,22,650.000

8.046 £2,31,548.812 1.030

4,30,550.000

8.071 £1,89,427.499 1.025

4,38,450.000

8.097 £1,47,306.185 1.019

4,46,350.000

8.122 £1,05,184.872 1.014

4,54,250.000

8.148 £63,063.558 1.008

4,62,150.000

8.174 £20,942.245 1.003

Sensitivity Analysis:

Sensitivity Analysis for labor cost:

Labor Cost (Sensitivity Analysis)

Fixed cost Payback period

Net Present

Value ROCE

7.959 £3,78,973.410 1.049

3,95,000.000

7.959 £3,78,973.410 1.049

3,98,950.000

7.972 £3,57,912.753 1.047

4,06,850.000

7.996 £3,15,791.439 1.041

4,14,750.000

8.021 £2,73,670.126 1.036

4,22,650.000

8.046 £2,31,548.812 1.030

4,30,550.000

8.071 £1,89,427.499 1.025

4,38,450.000

8.097 £1,47,306.185 1.019

4,46,350.000

8.122 £1,05,184.872 1.014

4,54,250.000

8.148 £63,063.558 1.008

4,62,150.000

8.174 £20,942.245 1.003

FINANCE FOR INTERNATIONAL BUSINESS 13

395000 398950 406850 414750 422650 430550 438450 446350 454250 462150

7.850

7.900

7.950

8.000

8.050

8.100

8.150

8.200

Payback Period

395000 398950 406850 414750 422650 430550 438450 446350 454250 462150

£-

£50,000.000

£100,000.000

£150,000.000

£200,000.000

£250,000.000

£300,000.000

£350,000.000

£400,000.000

Net Present Value

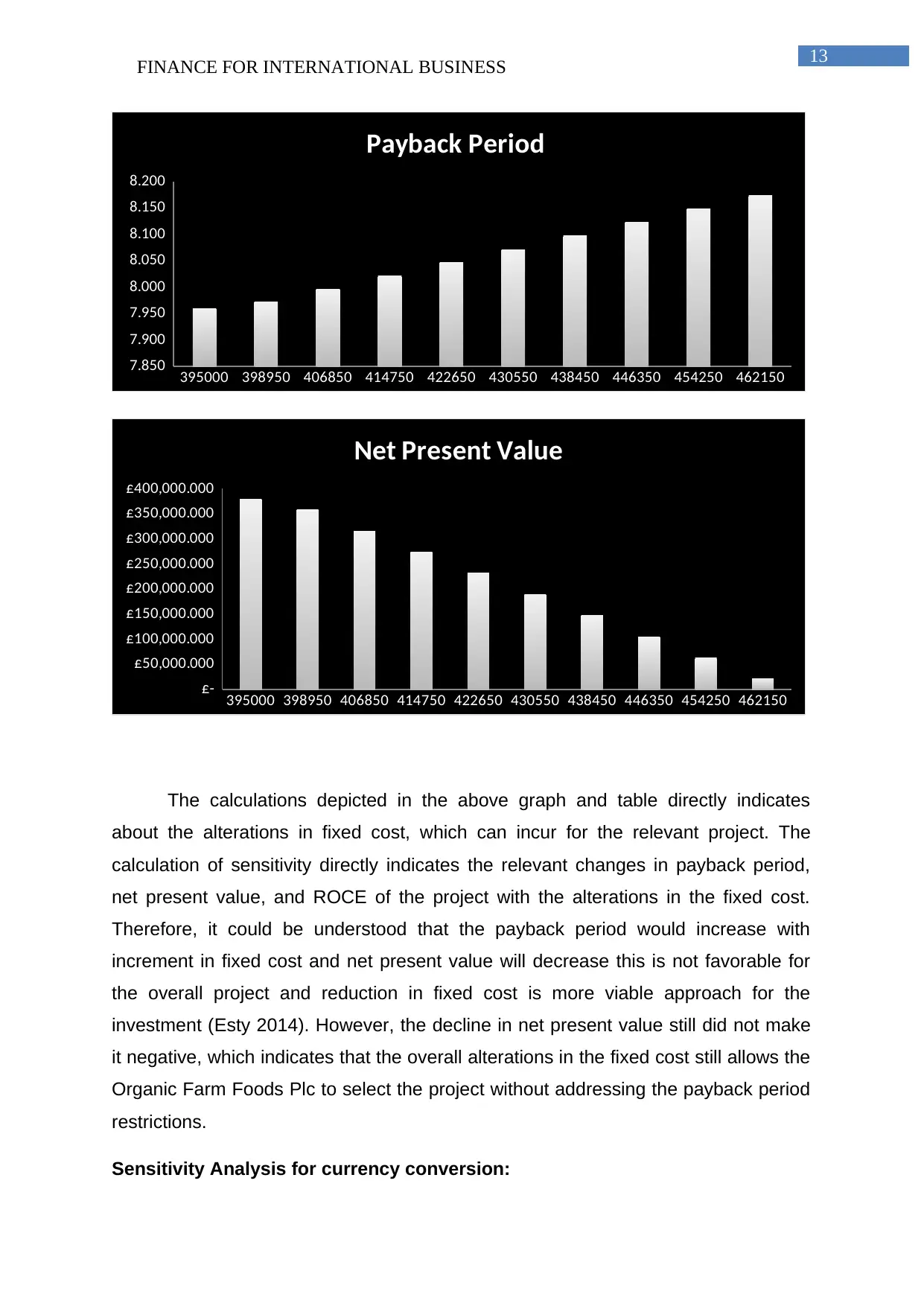

The calculations depicted in the above graph and table directly indicates

about the alterations in fixed cost, which can incur for the relevant project. The

calculation of sensitivity directly indicates the relevant changes in payback period,

net present value, and ROCE of the project with the alterations in the fixed cost.

Therefore, it could be understood that the payback period would increase with

increment in fixed cost and net present value will decrease this is not favorable for

the overall project and reduction in fixed cost is more viable approach for the

investment (Esty 2014). However, the decline in net present value still did not make

it negative, which indicates that the overall alterations in the fixed cost still allows the

Organic Farm Foods Plc to select the project without addressing the payback period

restrictions.

Sensitivity Analysis for currency conversion:

395000 398950 406850 414750 422650 430550 438450 446350 454250 462150

7.850

7.900

7.950

8.000

8.050

8.100

8.150

8.200

Payback Period

395000 398950 406850 414750 422650 430550 438450 446350 454250 462150

£-

£50,000.000

£100,000.000

£150,000.000

£200,000.000

£250,000.000

£300,000.000

£350,000.000

£400,000.000

Net Present Value

The calculations depicted in the above graph and table directly indicates

about the alterations in fixed cost, which can incur for the relevant project. The

calculation of sensitivity directly indicates the relevant changes in payback period,

net present value, and ROCE of the project with the alterations in the fixed cost.

Therefore, it could be understood that the payback period would increase with

increment in fixed cost and net present value will decrease this is not favorable for

the overall project and reduction in fixed cost is more viable approach for the

investment (Esty 2014). However, the decline in net present value still did not make

it negative, which indicates that the overall alterations in the fixed cost still allows the

Organic Farm Foods Plc to select the project without addressing the payback period

restrictions.

Sensitivity Analysis for currency conversion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR INTERNATIONAL BUSINESS 14

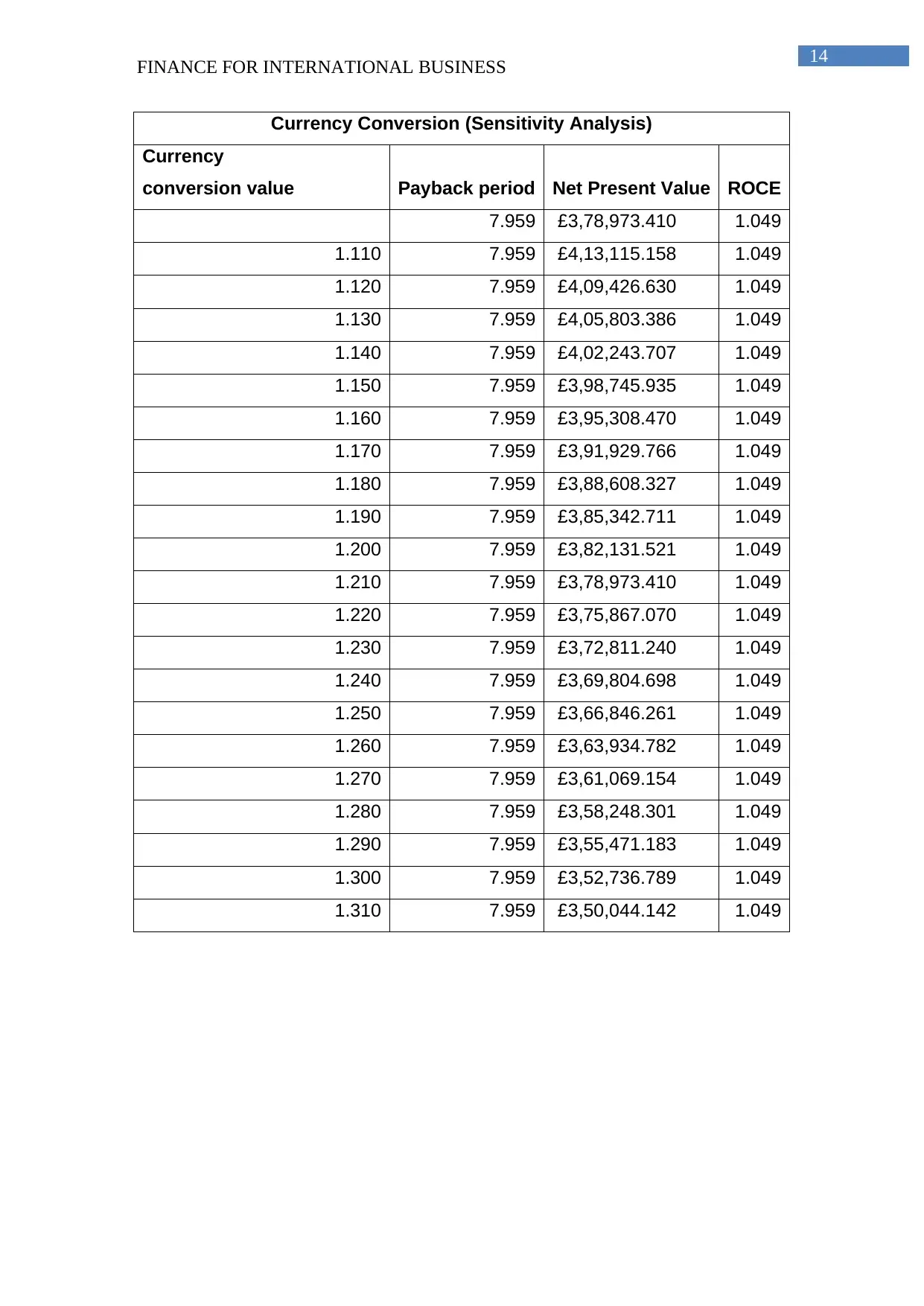

Currency Conversion (Sensitivity Analysis)

Currency

conversion value Payback period Net Present Value ROCE

7.959 £3,78,973.410 1.049

1.110 7.959 £4,13,115.158 1.049

1.120 7.959 £4,09,426.630 1.049

1.130 7.959 £4,05,803.386 1.049

1.140 7.959 £4,02,243.707 1.049

1.150 7.959 £3,98,745.935 1.049

1.160 7.959 £3,95,308.470 1.049

1.170 7.959 £3,91,929.766 1.049

1.180 7.959 £3,88,608.327 1.049

1.190 7.959 £3,85,342.711 1.049

1.200 7.959 £3,82,131.521 1.049

1.210 7.959 £3,78,973.410 1.049

1.220 7.959 £3,75,867.070 1.049

1.230 7.959 £3,72,811.240 1.049

1.240 7.959 £3,69,804.698 1.049

1.250 7.959 £3,66,846.261 1.049

1.260 7.959 £3,63,934.782 1.049

1.270 7.959 £3,61,069.154 1.049

1.280 7.959 £3,58,248.301 1.049

1.290 7.959 £3,55,471.183 1.049

1.300 7.959 £3,52,736.789 1.049

1.310 7.959 £3,50,044.142 1.049

Currency Conversion (Sensitivity Analysis)

Currency

conversion value Payback period Net Present Value ROCE

7.959 £3,78,973.410 1.049

1.110 7.959 £4,13,115.158 1.049

1.120 7.959 £4,09,426.630 1.049

1.130 7.959 £4,05,803.386 1.049

1.140 7.959 £4,02,243.707 1.049

1.150 7.959 £3,98,745.935 1.049

1.160 7.959 £3,95,308.470 1.049

1.170 7.959 £3,91,929.766 1.049

1.180 7.959 £3,88,608.327 1.049

1.190 7.959 £3,85,342.711 1.049

1.200 7.959 £3,82,131.521 1.049

1.210 7.959 £3,78,973.410 1.049

1.220 7.959 £3,75,867.070 1.049

1.230 7.959 £3,72,811.240 1.049

1.240 7.959 £3,69,804.698 1.049

1.250 7.959 £3,66,846.261 1.049

1.260 7.959 £3,63,934.782 1.049

1.270 7.959 £3,61,069.154 1.049

1.280 7.959 £3,58,248.301 1.049

1.290 7.959 £3,55,471.183 1.049

1.300 7.959 £3,52,736.789 1.049

1.310 7.959 £3,50,044.142 1.049

FINANCE FOR INTERNATIONAL BUSINESS 15

1.110

1.120

1.130

1.140

1.150

1.160

1.170

1.180

1.190

1.200

1.210

1.220

1.230

1.240

1.250

1.260

1.270

1.280

1.290

1.300

1.310

£300,000.000

£320,000.000

£340,000.000

£360,000.000

£380,000.000

£400,000.000

£420,000.000

Net Present Value

1.11 1.12 1.13 1.14 1.15 1.16 1.17 1.18 1.19 1.2 1.21 1.22 1.23 1.24 1.25 1.26 1.27 1.28 1.29 1.3 1.31

7.959

7.959

7.959

Payback Period

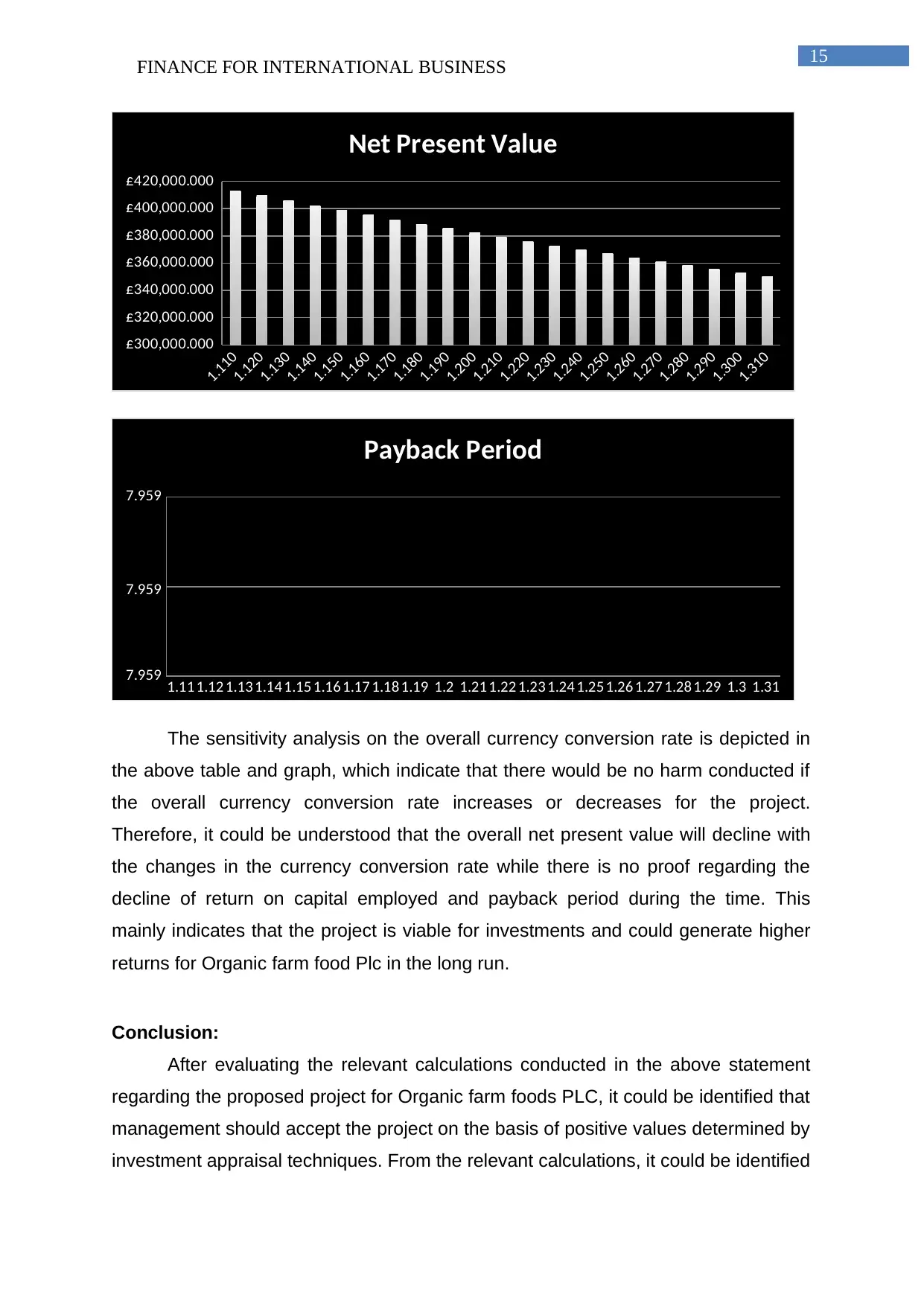

The sensitivity analysis on the overall currency conversion rate is depicted in

the above table and graph, which indicate that there would be no harm conducted if

the overall currency conversion rate increases or decreases for the project.

Therefore, it could be understood that the overall net present value will decline with

the changes in the currency conversion rate while there is no proof regarding the

decline of return on capital employed and payback period during the time. This

mainly indicates that the project is viable for investments and could generate higher

returns for Organic farm food Plc in the long run.

Conclusion:

After evaluating the relevant calculations conducted in the above statement

regarding the proposed project for Organic farm foods PLC, it could be identified that

management should accept the project on the basis of positive values determined by

investment appraisal techniques. From the relevant calculations, it could be identified

1.110

1.120

1.130

1.140

1.150

1.160

1.170

1.180

1.190

1.200

1.210

1.220

1.230

1.240

1.250

1.260

1.270

1.280

1.290

1.300

1.310

£300,000.000

£320,000.000

£340,000.000

£360,000.000

£380,000.000

£400,000.000

£420,000.000

Net Present Value

1.11 1.12 1.13 1.14 1.15 1.16 1.17 1.18 1.19 1.2 1.21 1.22 1.23 1.24 1.25 1.26 1.27 1.28 1.29 1.3 1.31

7.959

7.959

7.959

Payback Period

The sensitivity analysis on the overall currency conversion rate is depicted in

the above table and graph, which indicate that there would be no harm conducted if

the overall currency conversion rate increases or decreases for the project.

Therefore, it could be understood that the overall net present value will decline with

the changes in the currency conversion rate while there is no proof regarding the

decline of return on capital employed and payback period during the time. This

mainly indicates that the project is viable for investments and could generate higher

returns for Organic farm food Plc in the long run.

Conclusion:

After evaluating the relevant calculations conducted in the above statement

regarding the proposed project for Organic farm foods PLC, it could be identified that

management should accept the project on the basis of positive values determined by

investment appraisal techniques. From the relevant calculations, it could be identified

FINANCE FOR INTERNATIONAL BUSINESS 16

that the investments in in Ireland would allow organic farm foods to generate high

level of revenues while even if alternative circumstances occur. Hence, the

management should accept the overall proposal for open the business in Ireland and

generate adequate revenues in the process.

that the investments in in Ireland would allow organic farm foods to generate high

level of revenues while even if alternative circumstances occur. Hence, the

management should accept the overall proposal for open the business in Ireland and

generate adequate revenues in the process.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE FOR INTERNATIONAL BUSINESS 17

Reference and Bibliography:

Ajami, R. and Goddard, J.G., 2014. International business: Theory and practice.

Routledge.

Avdjiev, S., McCauley, R.N. and Shin, H.S., 2016. Breaking free of the triple

coincidence in international finance. Economic Policy, 31(87), pp.409-451.

Badarinza, C., Campbell, J.Y. and Ramadorai, T., 2016. International comparative

household finance. Annual Review of Economics, 8, pp.111-144.

Bräutigam, D. and Gallagher, K.P., 2014. Bartering Globalization: China's

Commodity‐backed Finance in Africa and Latin America. Global Policy, 5(3), pp.346-

352.

Cavusgil, S.T., Knight, G., Riesenberger, J.R., Rammal, H.G. and Rose, E.L.,

2014. International business. Pearson Australia.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and

access to finance. Strategic management journal, 35(1), pp.1-23.

Cumming, D.J. and Vismara, S., 2017. De-segmenting research in entrepreneurial

finance. Venture Capital, 19(1-2), pp.17-27.

Esty, B., 2014. An overview of project finance and infrastructure finance-2014

update. HBS Case, (214083).

Ferreira, M.P., Santos, J.C., de Almeida, M.I.R. and Reis, N.R., 2014. Mergers &

acquisitions research: A bibliometric study of top strategy and international business

journals, 1980–2010. Journal of Business Research, 67(12), pp.2550-2558.

Reference and Bibliography:

Ajami, R. and Goddard, J.G., 2014. International business: Theory and practice.

Routledge.

Avdjiev, S., McCauley, R.N. and Shin, H.S., 2016. Breaking free of the triple

coincidence in international finance. Economic Policy, 31(87), pp.409-451.

Badarinza, C., Campbell, J.Y. and Ramadorai, T., 2016. International comparative

household finance. Annual Review of Economics, 8, pp.111-144.

Bräutigam, D. and Gallagher, K.P., 2014. Bartering Globalization: China's

Commodity‐backed Finance in Africa and Latin America. Global Policy, 5(3), pp.346-

352.

Cavusgil, S.T., Knight, G., Riesenberger, J.R., Rammal, H.G. and Rose, E.L.,

2014. International business. Pearson Australia.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and

access to finance. Strategic management journal, 35(1), pp.1-23.

Cumming, D.J. and Vismara, S., 2017. De-segmenting research in entrepreneurial

finance. Venture Capital, 19(1-2), pp.17-27.

Esty, B., 2014. An overview of project finance and infrastructure finance-2014

update. HBS Case, (214083).

Ferreira, M.P., Santos, J.C., de Almeida, M.I.R. and Reis, N.R., 2014. Mergers &

acquisitions research: A bibliometric study of top strategy and international business

journals, 1980–2010. Journal of Business Research, 67(12), pp.2550-2558.

FINANCE FOR INTERNATIONAL BUSINESS 18

Finney, A., 2014. The international film business: A market guide beyond Hollywood.

Routledge.

Forsgren, M. and Johanson, J., 2014. Managing networks in international business.

Routledge.

Gelsomino, L.M., Mangiaracina, R., Perego, A. and Tumino, A., 2016. Supply chain

finance: a literature review. International Journal of Physical Distribution & Logistics

Management, 46(4), pp.348-366.

McLean, R.D. and Zhao, M., 2014. The business cycle, investor sentiment, and

costly external finance. The Journal of Finance, 69(3), pp.1377-1409.

Melvin, M. and Norrbin, S., 2017. International money and finance. Academic Press.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Papadopoulos, N. and Heslop, L.A., 2014. Product-country images: Impact and role

in international marketing. Routledge.

Picciotto, S. and Mayne, R. eds., 2016. Regulating international business: beyond

liberalization. Springer.

Sassen, S., 2017. Finance and business services in New York City: international

linkages and domestic effects. In Deindustrialization and Regional Economic

Transformation(pp. 132-290). Routledge.

Shenkar, O., Luo, Y. and Chi, T., 2014. International business. Routledge.

Zingales, L., 2015. Presidential address: Does finance benefit society?. The Journal

of Finance, 70(4), pp.1327-1363.

Finney, A., 2014. The international film business: A market guide beyond Hollywood.

Routledge.

Forsgren, M. and Johanson, J., 2014. Managing networks in international business.

Routledge.

Gelsomino, L.M., Mangiaracina, R., Perego, A. and Tumino, A., 2016. Supply chain

finance: a literature review. International Journal of Physical Distribution & Logistics

Management, 46(4), pp.348-366.

McLean, R.D. and Zhao, M., 2014. The business cycle, investor sentiment, and

costly external finance. The Journal of Finance, 69(3), pp.1377-1409.

Melvin, M. and Norrbin, S., 2017. International money and finance. Academic Press.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Papadopoulos, N. and Heslop, L.A., 2014. Product-country images: Impact and role

in international marketing. Routledge.

Picciotto, S. and Mayne, R. eds., 2016. Regulating international business: beyond

liberalization. Springer.

Sassen, S., 2017. Finance and business services in New York City: international

linkages and domestic effects. In Deindustrialization and Regional Economic

Transformation(pp. 132-290). Routledge.

Shenkar, O., Luo, Y. and Chi, T., 2014. International business. Routledge.

Zingales, L., 2015. Presidential address: Does finance benefit society?. The Journal

of Finance, 70(4), pp.1327-1363.

1 out of 18

Related Documents

![AUDITIZZ ELECTRONICS REPORT ON BUSINESS FINANCE [Enter YOUR name here]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fps%2Ff8b2265e530d4c6e9e0b7871ef3f5175.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.