Investment Appraisal Techniques: Doc

12 Pages3005 Words89 Views

Added on 2021-02-21

Investment Appraisal Techniques: Doc

Added on 2021-02-21

ShareRelated Documents

InvestmentAppraisal

Table of ContentsINTRODUCTION...........................................................................................................................3TASK...............................................................................................................................................35.1. .........................................................................................................................................32.1. .........................................................................................................................................45.2. .........................................................................................................................................92.2 ..........................................................................................................................................92.2.........................................................................................................................................10CONCLUSION..............................................................................................................................11REFERENCES..............................................................................................................................12

INTRODUCTIONInvestment Appraisal relates to set of procedures used to assess an investment'sattractiveness. In the framework of a business, the main aim of the it is to value advantages orbenefits in order to justify overall business expenses (Li and Trutnevyte, 2017). The study coversdiscussion upon major methods of investment appraisal, evaluation and recommendation abouteach specific projects provided and efficient manner though which company may obtain fundsfor financing projects. TASK5.1. Financial appraisal methods to analyse competing investment projects in the public andprivate sector:In modern era, different business organisations are applying various short of methods ofinvestment appraisal. Use of these facilitates selection of appropriate investment, project orproposal. Before applying such different methods managerial personnels should analyse the coreuse of such methods and asses which is most suitable method for given investment proposals andprojects. Major investment appraisals are Accounting-rate of return, IRR, Net-present value,payback period etc (Hoesli and MacGregor, 2014). Following is discussion on such differentmethods, as follows: Payback Period: One of the quickest tools of investment appraisal is payback-period.Payback method demonstrates how long it would take for any project or investmentproposal to produce enough cash-flow to compensate the project's original price. Accounting Rate of Return: ARR implies to method which defines expected amount ofprofit from any proposal or investment. It exhibits net-accounting profit generating fromdifferent investment proposals as specific percent of investment made in project. Thistechniques also called as return on capital or investment return. Net Present Value: This is most commonly applied technique of investment-appraisal.NPV is simply aggregate amount of PV-discounted future outflow and inflow of cashassociated with proposal or project. Normally weighted-average capital cost( WACC ) isregarded as PV-discounting factor with respect to future expected cash-flows under net-present value technique.

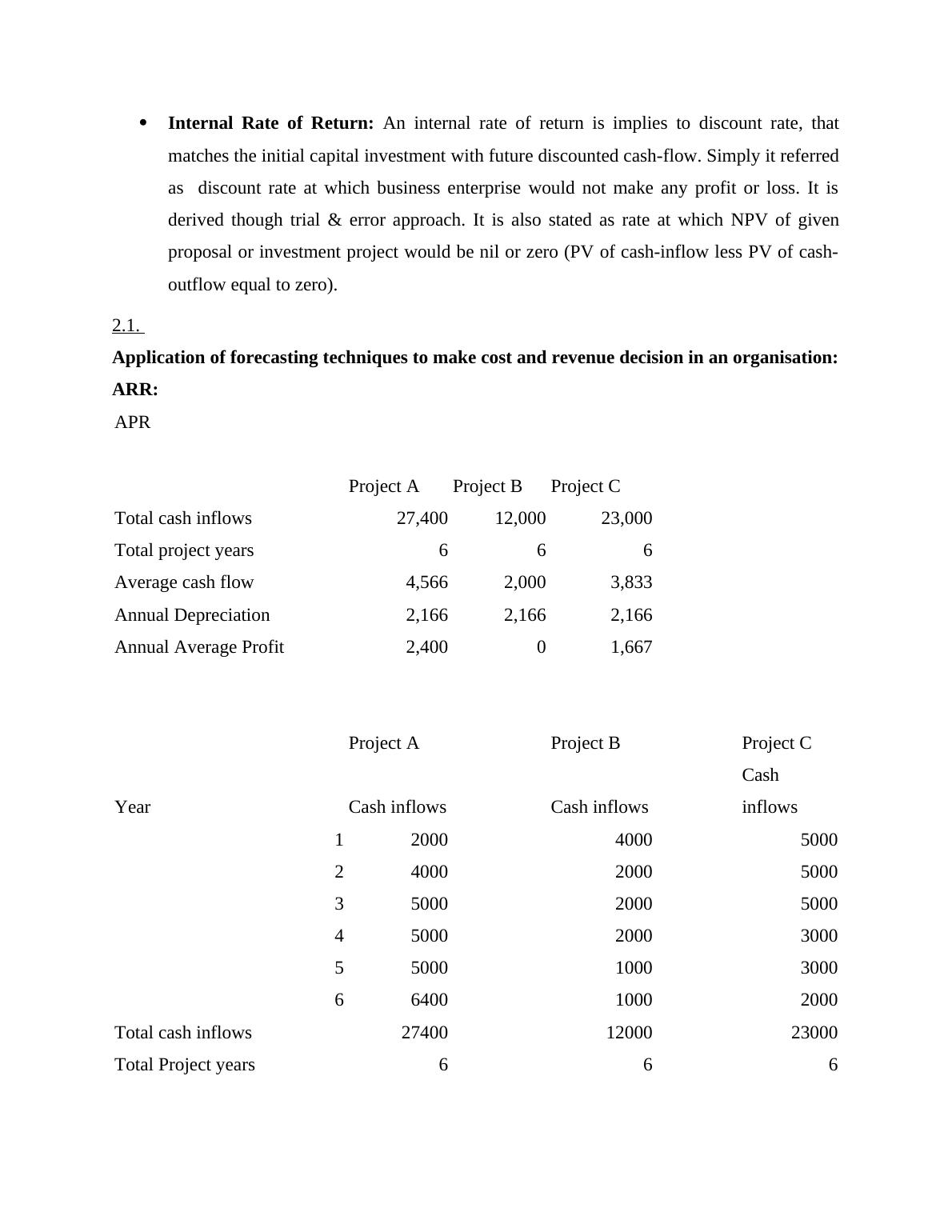

Internal Rate of Return: An internal rate of return is implies to discount rate, thatmatches the initial capital investment with future discounted cash-flow. Simply it referredas discount rate at which business enterprise would not make any profit or loss. It isderived though trial & error approach. It is also stated as rate at which NPV of givenproposal or investment project would be nil or zero (PV of cash-inflow less PV of cash-outflow equal to zero). 2.1. Application of forecasting techniques to make cost and revenue decision in an organisation:ARR:APRProject AProject BProject CTotal cash inflows27,40012,00023,000Total project years666Average cash flow4,5662,0003,833Annual Depreciation2,1662,1662,166Annual Average Profit2,40001,667Project AProject BProject CYearCash inflowsCash inflowsCash inflows120004000500024000200050003500020005000450002000300055000100030006640010002000Total cash inflows274001200023000Total Project years666Working for Project A :Average cash flows = Total cash inflows/ Total project years = 27400/6 = 4566Annual Depreciation = Total investment/total project years = 13000/6 = 2166

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Investment Appraisal Techniques and Risk Assessment using Accounting Ratioslg...

|11

|2205

|75

International Financial Management: Investment Appraisal Techniqueslg...

|9

|1808

|71

APC308 Financial Management: Investment Appraisal Techniques and Merger & Takeoverslg...

|13

|3832

|276

Business Decision Makinglg...

|7

|1412

|119

Comprehensive Report of Goodfellow PLClg...

|9

|1425

|67

Capital Budgeting Techniques for Investment Appraisallg...

|11

|2353

|295