Financial Reporting Newsletter: AASB, IASB, and Whirl Ltd Financials

VerifiedAdded on 2023/05/27

|12

|2802

|442

Report

AI Summary

This financial reporting newsletter provides a comprehensive overview of key developments in accounting standards and financial reporting practices. The report begins with an analysis of proposed amendments to the Australian Accounting Standards (AASB) concerning the conceptual framework, including its application to for-profit private sector companies. It then delves into specific standards, such as AASB 137 on onerous contracts, clarifying the inclusion of costs directly related to the contract. The newsletter also covers updates from the IASB, highlighting preliminary decisions and topics discussed in board meetings, including IFRS for SMEs and IBOR reform. Furthermore, the report examines a new accounting standard on right-of-use assets for not-for-profit organizations and the removal of RHCCA forms by ASX. The newsletter also defines business and materiality through new amending standards. The report then addresses the presentation of financial statements in accordance with AASB 101, emphasizing the requirements for fair representation and the handling of non-compliance with accounting standards. Finally, the report includes a detailed analysis of Whirl Ltd's financial statements, identifying and correcting errors in the profit and loss statement and statement of financial position, ensuring compliance with accounting standards.

Financial Accounting

News Letter

News Letter

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Name of the student

Name of the university

Student ID

Author note

Name of the university

Student ID

Author note

NEWS LETTER

Proposed standard AASB 2019-X Amendments to the

Australian Accounting Standards with reference to

conceptual framework

Consequential amendments for supporting AASB issuing

conceptual framework for the financial reporting those are set out

in proposed standard AASB 2019-X. At this level, application

for Conceptual Framework will be restricted to for –profit private

sector companies those have public accountability and those are

required by legislation for complying with the AAS and other

for-profit companies those opt to apply conceptual framework

voluntarily. The proposed standard will make amendments to the

AAS, interpretation and various other pronouncements of AASB

for permitting other companies to continue using framework for

the purpose of preparing and presenting the financial statements

as adopted by AASB in the year 2004. Further, some of the AAS,

interpretation and various other pronouncements of AASB

contain the reference to or the quotation from framework for

preparing and presenting the financial statements. The proposed

standard will update quotation and references while required so

that it may refer the conceptual framework and may make the

related other amendments for clarifying which version of

conceptual framework has been referred for the particular

pronouncement (Aasb.gov.au, 2019).

AASB 137 – Onerous contracts – cot of fulfilling the contract

As per the standard the onerous contract is the contract where the

unavoidable costs for meeting contractual obligation is more than

the expected economic benefit that is to be received from it. The

unavoidable cost is the lower of cost for fulfilling the same and

any penalties or compensation created from failure for fulfilling

it. As per the amendment cost for fulfilling the contract also

includes the costs directly related to contract (Aasb.gov.au,

2019). Example for the costs directly related to contract includes

direct material, direct labour, costs those are chargeable

explicitly to counterparty under contract. Allocation of the costs

directly related to the contract activities and other costs incurred

as the entity entered into contract. However, the general as well

as the administrative cost is not directly related to the contract

unless those are chargeable explicitly to counterparty under the

contract.

Summary of the news and development in context of financial

reporting

Period covered: 1st December 2018 to 31st March 2019

IASB Update on February 2019

IASB update highlighted the

preliminary decisions of IASB.

Final decision of the board on the

IFRS standards, IFRIC and

amendments were formally

balloted as the set forth in Due

Process Handbook of IFRS.

Topics discussed in the board

were related to IFRS for the SMEs

Standards –review and update,

primary financial statements,

management commentary,

amendment to the IFRS 17 –

Insurance contracts and IBOR

Reform and effects on the

financial reporting. In the meeting

all the 14 board members were

agreed with the decision, board

also decided which of the topics

will be discussed in the next board

meeting and all the 14 board

members were agreed with this

(Iasplus.com, 2019).

Proposed standard AASB 2019-X Amendments to the

Australian Accounting Standards with reference to

conceptual framework

Consequential amendments for supporting AASB issuing

conceptual framework for the financial reporting those are set out

in proposed standard AASB 2019-X. At this level, application

for Conceptual Framework will be restricted to for –profit private

sector companies those have public accountability and those are

required by legislation for complying with the AAS and other

for-profit companies those opt to apply conceptual framework

voluntarily. The proposed standard will make amendments to the

AAS, interpretation and various other pronouncements of AASB

for permitting other companies to continue using framework for

the purpose of preparing and presenting the financial statements

as adopted by AASB in the year 2004. Further, some of the AAS,

interpretation and various other pronouncements of AASB

contain the reference to or the quotation from framework for

preparing and presenting the financial statements. The proposed

standard will update quotation and references while required so

that it may refer the conceptual framework and may make the

related other amendments for clarifying which version of

conceptual framework has been referred for the particular

pronouncement (Aasb.gov.au, 2019).

AASB 137 – Onerous contracts – cot of fulfilling the contract

As per the standard the onerous contract is the contract where the

unavoidable costs for meeting contractual obligation is more than

the expected economic benefit that is to be received from it. The

unavoidable cost is the lower of cost for fulfilling the same and

any penalties or compensation created from failure for fulfilling

it. As per the amendment cost for fulfilling the contract also

includes the costs directly related to contract (Aasb.gov.au,

2019). Example for the costs directly related to contract includes

direct material, direct labour, costs those are chargeable

explicitly to counterparty under contract. Allocation of the costs

directly related to the contract activities and other costs incurred

as the entity entered into contract. However, the general as well

as the administrative cost is not directly related to the contract

unless those are chargeable explicitly to counterparty under the

contract.

Summary of the news and development in context of financial

reporting

Period covered: 1st December 2018 to 31st March 2019

IASB Update on February 2019

IASB update highlighted the

preliminary decisions of IASB.

Final decision of the board on the

IFRS standards, IFRIC and

amendments were formally

balloted as the set forth in Due

Process Handbook of IFRS.

Topics discussed in the board

were related to IFRS for the SMEs

Standards –review and update,

primary financial statements,

management commentary,

amendment to the IFRS 17 –

Insurance contracts and IBOR

Reform and effects on the

financial reporting. In the meeting

all the 14 board members were

agreed with the decision, board

also decided which of the topics

will be discussed in the next board

meeting and all the 14 board

members were agreed with this

(Iasplus.com, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

New Accounting Standard: Right-of-Use assets for Not-for-

profit organisations

AASB issued the AASB 2018-8 Amendments to the AAS –

Right-of-use Assets of Not-for-profit organisations for providing

temporary option for the non-for-profit lessees for selecting to

measure the class or classes of right-of-use assets generated from

‘concessionary leases’ at the initial recognition, either – at the

cost in compliance with AASB 16 Leases Para 23-25 that

incorporates amount of initial recognition of lease liability or at

the fair values in compliance with the AASB 16, Para Aus25.1.

In this aspect the concessionary leases are those are the leases

that have considerably below market terms and the conditions

principally will enable the organisation further to its objective. 2

key changes incorporated by the standard are – allowing

temporary option required to be applied to right-of-use assets on

basis of class by class and amending the AASB 1049 Whole of

Government and General Government Sector Financial

Reporting for allowing the government to measure the right-of-

use assets at the cost instead of fair values (Aasb.gov.au, 2019).

Removal of the Registered Holder Collateral Cover

Authorisation forms for the Client Accounts

ASX obtained the regulatory clearance for implementing

amendments to ASX Settlement Operating Rules and ASX Clear

Operating Rules and Procedures outlined under Response to

Consultation in context of removal of the RHCCA forms. The

amendment removed RHCCA form for the clients accounts and

further enable the 3rd party in taking the security interest over the

collateral and the excess cash where the prescribed condition are

fulfilled. Among other things, the amendment further assure that

where the accounts if client is transferred to the new clearing

participant, registered holder are not required to execute and to

provide the RHCCA form ahead of transfer and collateral that is

linked with the client account will secure the obligation

automatically (Aasb.gov.au, 2019).

New Australian Accounting

Standard for definition

AASB clarified definition of

business and material through 2 new

amending standards as follows –

AASB 2018-6 defines business

as integrated set of the activities

and the assets that is capable of

being managed and conducted

with the purpose of delivering

the services or goods to the

customers for generating

investment income

(Aasb.gov.au, 2019).

AASB 2018-7 defines that the

information will be considered

material if obscuring, misstating

or omitting the same could

reasonably be likely to influence

the decision that primary users

of GPFS make based on the

financial statement that provide

the financial information

regarding particular reporting

entity (Aasb.gov.au, 2019).

profit organisations

AASB issued the AASB 2018-8 Amendments to the AAS –

Right-of-use Assets of Not-for-profit organisations for providing

temporary option for the non-for-profit lessees for selecting to

measure the class or classes of right-of-use assets generated from

‘concessionary leases’ at the initial recognition, either – at the

cost in compliance with AASB 16 Leases Para 23-25 that

incorporates amount of initial recognition of lease liability or at

the fair values in compliance with the AASB 16, Para Aus25.1.

In this aspect the concessionary leases are those are the leases

that have considerably below market terms and the conditions

principally will enable the organisation further to its objective. 2

key changes incorporated by the standard are – allowing

temporary option required to be applied to right-of-use assets on

basis of class by class and amending the AASB 1049 Whole of

Government and General Government Sector Financial

Reporting for allowing the government to measure the right-of-

use assets at the cost instead of fair values (Aasb.gov.au, 2019).

Removal of the Registered Holder Collateral Cover

Authorisation forms for the Client Accounts

ASX obtained the regulatory clearance for implementing

amendments to ASX Settlement Operating Rules and ASX Clear

Operating Rules and Procedures outlined under Response to

Consultation in context of removal of the RHCCA forms. The

amendment removed RHCCA form for the clients accounts and

further enable the 3rd party in taking the security interest over the

collateral and the excess cash where the prescribed condition are

fulfilled. Among other things, the amendment further assure that

where the accounts if client is transferred to the new clearing

participant, registered holder are not required to execute and to

provide the RHCCA form ahead of transfer and collateral that is

linked with the client account will secure the obligation

automatically (Aasb.gov.au, 2019).

New Australian Accounting

Standard for definition

AASB clarified definition of

business and material through 2 new

amending standards as follows –

AASB 2018-6 defines business

as integrated set of the activities

and the assets that is capable of

being managed and conducted

with the purpose of delivering

the services or goods to the

customers for generating

investment income

(Aasb.gov.au, 2019).

AASB 2018-7 defines that the

information will be considered

material if obscuring, misstating

or omitting the same could

reasonably be likely to influence

the decision that primary users

of GPFS make based on the

financial statement that provide

the financial information

regarding particular reporting

entity (Aasb.gov.au, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer to Question 2:

As per the requirement of AASB 101 any entity shall present the financial statement

and the information represented in the financial statement regarding the entity’s financial

performance, cash flow position and financial position in true and fair manner. Fair

representation requires the faithful representation of the transaction taken place during the

period under consideration with reporting and disclosing impact for each of the transactions

(Aasb.gov.au, 2019). Further, the items reported in the financial statements including the

assets, equity, liabilities, revenues and expenses must meet the recognition criteria as per the

requirement of the conceptual framework. Further, the financial statement shall include the

additional disclosures, if necessary in accordance with the requirement of AAS. Requirement

of fair representation obliges to –

Provide additional disclosures if any particular AAS is not enough to enable the user

to understand the effect of particular transaction, other events as well as conditions in

context of financial performance and financial position of the entity (Aasb.gov.au,

2019).

Deliver the information for the accounting policies in such way that the information is

comparable, understandable, reliable and relevant.

Select and apply appropriate accounting policies in compliance with AASB 108 for

the accounting policies, errors and the changes in the estimates associated with

accounting (Aasb.gov.au, 2019).

However, it is notable that any entity is not in a position to rectify any accounting

policies used by it which is not appropriate through the disclosures, explanatory materials or

explanatory notes. Hence, in any scenario if the management concludes that the compliance

with any particular AAS will mislead the users and it will have conflicts with the preparation

As per the requirement of AASB 101 any entity shall present the financial statement

and the information represented in the financial statement regarding the entity’s financial

performance, cash flow position and financial position in true and fair manner. Fair

representation requires the faithful representation of the transaction taken place during the

period under consideration with reporting and disclosing impact for each of the transactions

(Aasb.gov.au, 2019). Further, the items reported in the financial statements including the

assets, equity, liabilities, revenues and expenses must meet the recognition criteria as per the

requirement of the conceptual framework. Further, the financial statement shall include the

additional disclosures, if necessary in accordance with the requirement of AAS. Requirement

of fair representation obliges to –

Provide additional disclosures if any particular AAS is not enough to enable the user

to understand the effect of particular transaction, other events as well as conditions in

context of financial performance and financial position of the entity (Aasb.gov.au,

2019).

Deliver the information for the accounting policies in such way that the information is

comparable, understandable, reliable and relevant.

Select and apply appropriate accounting policies in compliance with AASB 108 for

the accounting policies, errors and the changes in the estimates associated with

accounting (Aasb.gov.au, 2019).

However, it is notable that any entity is not in a position to rectify any accounting

policies used by it which is not appropriate through the disclosures, explanatory materials or

explanatory notes. Hence, in any scenario if the management concludes that the compliance

with any particular AAS will mislead the users and it will have conflicts with the preparation

of financial statement in compliance with the framework, entity shall not apply the same

(Aasb.gov.au, 2019). However, in accordance to AASB101, Para 21, if any entity does not

follow any particular requirement of AAS in the previous period and the non-compliance has

an impact on the amount reported in the financial statement, the entity shall disclose it

through making appropriate disclosures. Disclosures required for the same are as follows –

The organisation has been complied with all other requirement of AAS except the one

that has not been complied with for representing the statement fairly (Aasb.gov.au,

2019).

Management opined that all the information associated to cash flows, financial

performance and financial position has been fairly presented for preparation of

financial statement.

Title for the AAS that has not been complied with by the management, nature of non-

application, treatment required by AAS for the same, reason why the same has not

been complied and the reason why the compliance will mislead the users of financial

statement.

For each presented period, financial effect on each of the items owing to non-

compliance will be disclosed in the financial statement as per the requirement

(Aasb.gov.au, 2019).

Financial statement is the structured representation for representing the financial

performance and financial position of the entity. Main objective of financial statement is

delivering the information regarding the financial position as well as performance and cash

flows of the entity those are useful in making different economic decisions. For achieving the

objective the financial statement delivers the information regarding the assets, liabilities,

equities, revenues and expenses including the losses and gains, distribution to and

contributions by the owners in the capacity of owners and cash flows (Aasb.gov.au, 2019).

(Aasb.gov.au, 2019). However, in accordance to AASB101, Para 21, if any entity does not

follow any particular requirement of AAS in the previous period and the non-compliance has

an impact on the amount reported in the financial statement, the entity shall disclose it

through making appropriate disclosures. Disclosures required for the same are as follows –

The organisation has been complied with all other requirement of AAS except the one

that has not been complied with for representing the statement fairly (Aasb.gov.au,

2019).

Management opined that all the information associated to cash flows, financial

performance and financial position has been fairly presented for preparation of

financial statement.

Title for the AAS that has not been complied with by the management, nature of non-

application, treatment required by AAS for the same, reason why the same has not

been complied and the reason why the compliance will mislead the users of financial

statement.

For each presented period, financial effect on each of the items owing to non-

compliance will be disclosed in the financial statement as per the requirement

(Aasb.gov.au, 2019).

Financial statement is the structured representation for representing the financial

performance and financial position of the entity. Main objective of financial statement is

delivering the information regarding the financial position as well as performance and cash

flows of the entity those are useful in making different economic decisions. For achieving the

objective the financial statement delivers the information regarding the assets, liabilities,

equities, revenues and expenses including the losses and gains, distribution to and

contributions by the owners in the capacity of owners and cash flows (Aasb.gov.au, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The complete set of financial statement includes statement of the financial position as at the

closing of the period, statement of profit and loss and other comprehensive income for the

concerned period, statement of changes in the equity, statement of cash flows, notes including

the significant accounting policies and associated other explanatory information

(Aasb.gov.au, 2019).

In the given case, of Whirl Ltd, one of its trainee accountants prepared the profit and

loss statement, other comprehensive income, statement of changes in equity and statement of

financial position. The entity uses single statement format for preparing the profit and loss

statements and other comprehensive income, however the directors want to present the

analysis of the expenses by function rather than single statement format.

Going through the presented financial statements of Whirl Ltd various mistakes have

been found in context of presentation of the financial items as follows –

Profit and loss statement –

Cost of sales shall be deducted from the revenues and shall be presented below the

revenues to obtain the figure of gross profit

Expenses including the operating expenses and administrative expenses shall be

recorded below the gross profit and the total amount shall be deducted from gross

profit to obtain the figure of operating profit (Standard, 2015).

Finance cost shall be recorded below the operating profit and deducted from the

operating profit to obtain at the figure of net profit after tax

Income tax expenses shall be recorded under net profit after tax and shall be deducted

to obtain the figure of net profit.

closing of the period, statement of profit and loss and other comprehensive income for the

concerned period, statement of changes in the equity, statement of cash flows, notes including

the significant accounting policies and associated other explanatory information

(Aasb.gov.au, 2019).

In the given case, of Whirl Ltd, one of its trainee accountants prepared the profit and

loss statement, other comprehensive income, statement of changes in equity and statement of

financial position. The entity uses single statement format for preparing the profit and loss

statements and other comprehensive income, however the directors want to present the

analysis of the expenses by function rather than single statement format.

Going through the presented financial statements of Whirl Ltd various mistakes have

been found in context of presentation of the financial items as follows –

Profit and loss statement –

Cost of sales shall be deducted from the revenues and shall be presented below the

revenues to obtain the figure of gross profit

Expenses including the operating expenses and administrative expenses shall be

recorded below the gross profit and the total amount shall be deducted from gross

profit to obtain the figure of operating profit (Standard, 2015).

Finance cost shall be recorded below the operating profit and deducted from the

operating profit to obtain at the figure of net profit after tax

Income tax expenses shall be recorded under net profit after tax and shall be deducted

to obtain the figure of net profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

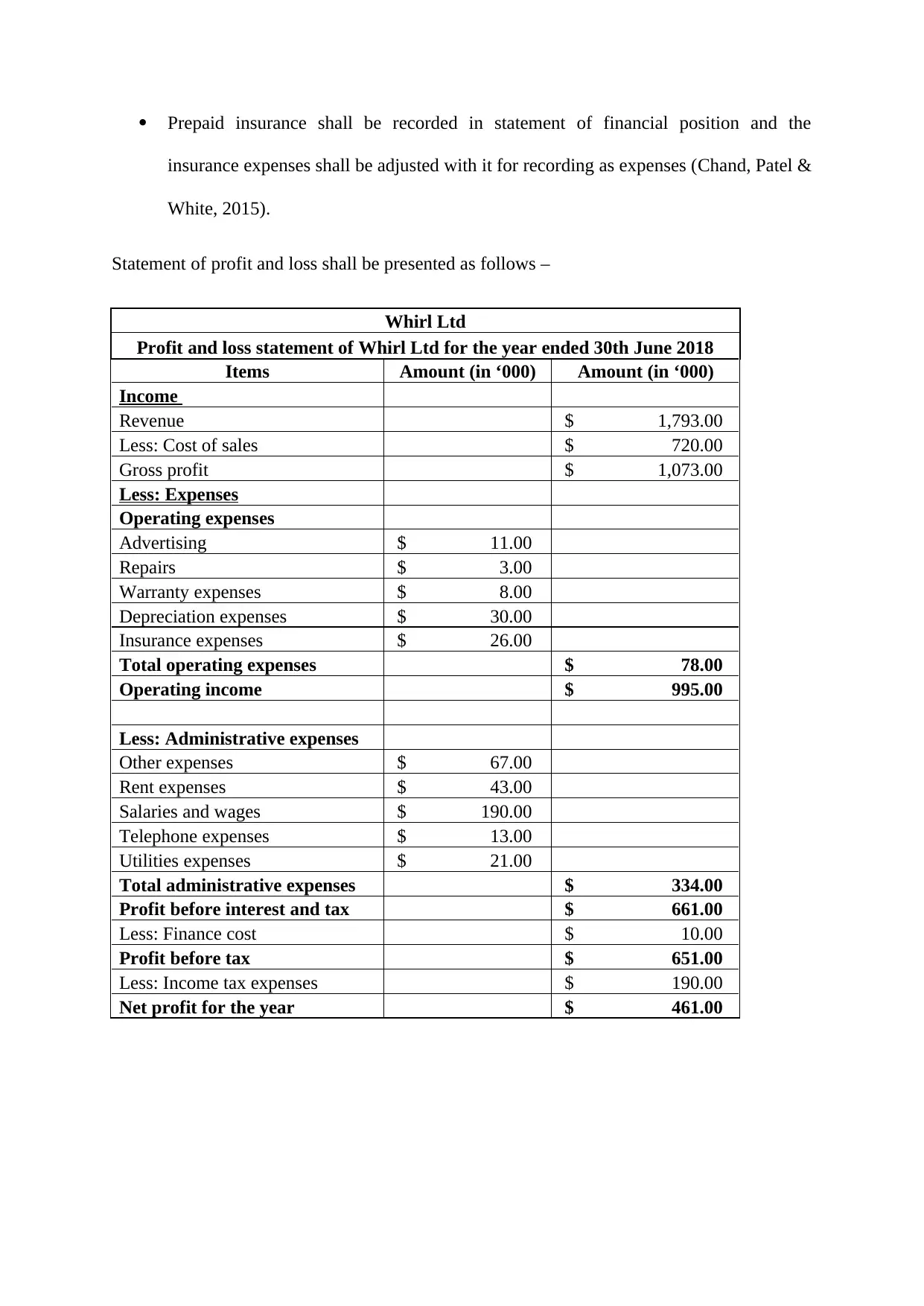

Prepaid insurance shall be recorded in statement of financial position and the

insurance expenses shall be adjusted with it for recording as expenses (Chand, Patel &

White, 2015).

Statement of profit and loss shall be presented as follows –

Whirl Ltd

Profit and loss statement of Whirl Ltd for the year ended 30th June 2018

Items Amount (in ‘000) Amount (in ‘000)

Income

Revenue $ 1,793.00

Less: Cost of sales $ 720.00

Gross profit $ 1,073.00

Less: Expenses

Operating expenses

Advertising $ 11.00

Repairs $ 3.00

Warranty expenses $ 8.00

Depreciation expenses $ 30.00

Insurance expenses $ 26.00

Total operating expenses $ 78.00

Operating income $ 995.00

Less: Administrative expenses

Other expenses $ 67.00

Rent expenses $ 43.00

Salaries and wages $ 190.00

Telephone expenses $ 13.00

Utilities expenses $ 21.00

Total administrative expenses $ 334.00

Profit before interest and tax $ 661.00

Less: Finance cost $ 10.00

Profit before tax $ 651.00

Less: Income tax expenses $ 190.00

Net profit for the year $ 461.00

insurance expenses shall be adjusted with it for recording as expenses (Chand, Patel &

White, 2015).

Statement of profit and loss shall be presented as follows –

Whirl Ltd

Profit and loss statement of Whirl Ltd for the year ended 30th June 2018

Items Amount (in ‘000) Amount (in ‘000)

Income

Revenue $ 1,793.00

Less: Cost of sales $ 720.00

Gross profit $ 1,073.00

Less: Expenses

Operating expenses

Advertising $ 11.00

Repairs $ 3.00

Warranty expenses $ 8.00

Depreciation expenses $ 30.00

Insurance expenses $ 26.00

Total operating expenses $ 78.00

Operating income $ 995.00

Less: Administrative expenses

Other expenses $ 67.00

Rent expenses $ 43.00

Salaries and wages $ 190.00

Telephone expenses $ 13.00

Utilities expenses $ 21.00

Total administrative expenses $ 334.00

Profit before interest and tax $ 661.00

Less: Finance cost $ 10.00

Profit before tax $ 651.00

Less: Income tax expenses $ 190.00

Net profit for the year $ 461.00

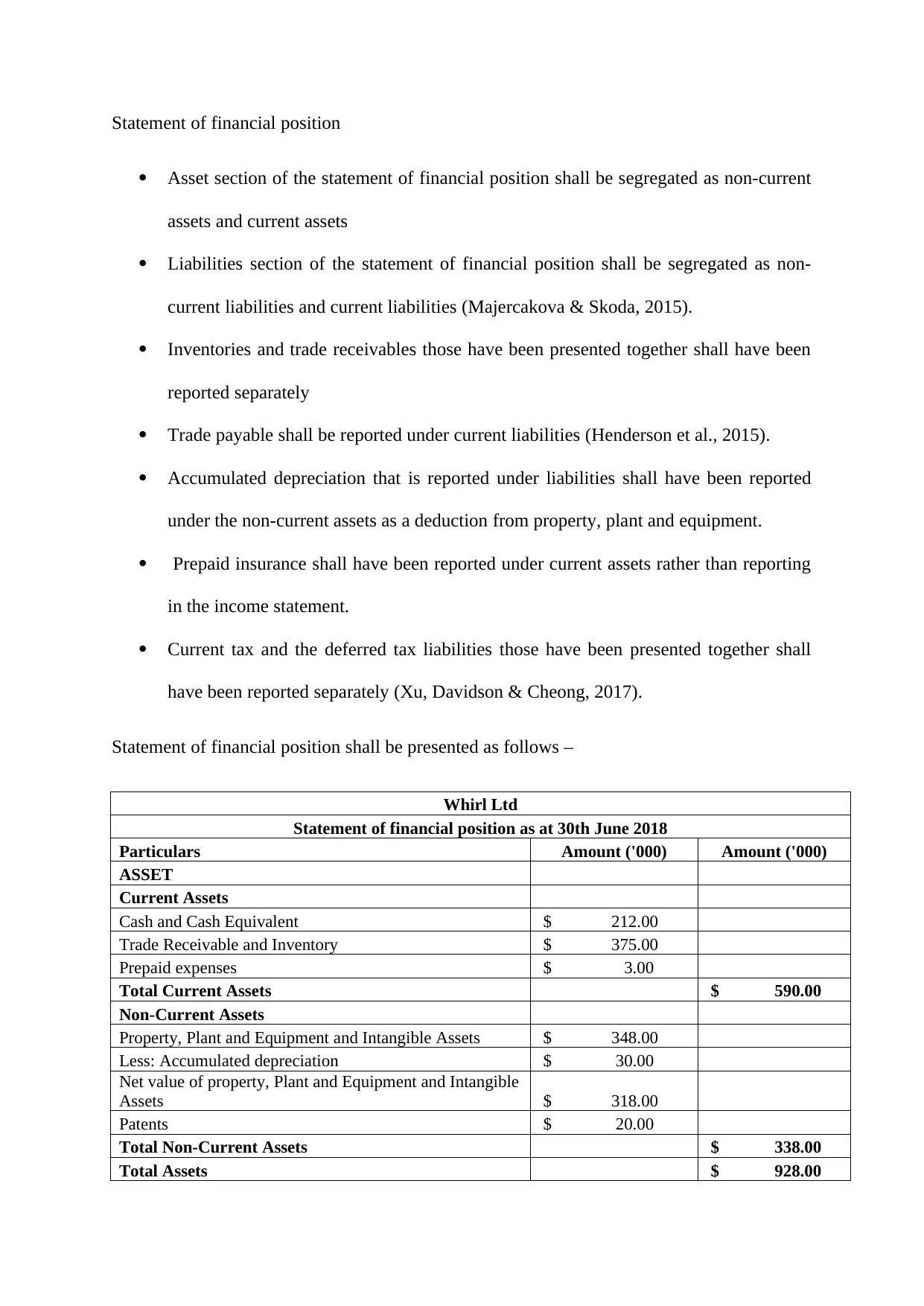

Statement of financial position

Asset section of the statement of financial position shall be segregated as non-current

assets and current assets

Liabilities section of the statement of financial position shall be segregated as non-

current liabilities and current liabilities (Majercakova & Skoda, 2015).

Inventories and trade receivables those have been presented together shall have been

reported separately

Trade payable shall be reported under current liabilities (Henderson et al., 2015).

Accumulated depreciation that is reported under liabilities shall have been reported

under the non-current assets as a deduction from property, plant and equipment.

Prepaid insurance shall have been reported under current assets rather than reporting

in the income statement.

Current tax and the deferred tax liabilities those have been presented together shall

have been reported separately (Xu, Davidson & Cheong, 2017).

Statement of financial position shall be presented as follows –

Whirl Ltd

Statement of financial position as at 30th June 2018

Particulars Amount ('000) Amount ('000)

ASSET

Current Assets

Cash and Cash Equivalent $ 212.00

Trade Receivable and Inventory $ 375.00

Prepaid expenses $ 3.00

Total Current Assets $ 590.00

Non-Current Assets

Property, Plant and Equipment and Intangible Assets $ 348.00

Less: Accumulated depreciation $ 30.00

Net value of property, Plant and Equipment and Intangible

Assets $ 318.00

Patents $ 20.00

Total Non-Current Assets $ 338.00

Total Assets $ 928.00

Asset section of the statement of financial position shall be segregated as non-current

assets and current assets

Liabilities section of the statement of financial position shall be segregated as non-

current liabilities and current liabilities (Majercakova & Skoda, 2015).

Inventories and trade receivables those have been presented together shall have been

reported separately

Trade payable shall be reported under current liabilities (Henderson et al., 2015).

Accumulated depreciation that is reported under liabilities shall have been reported

under the non-current assets as a deduction from property, plant and equipment.

Prepaid insurance shall have been reported under current assets rather than reporting

in the income statement.

Current tax and the deferred tax liabilities those have been presented together shall

have been reported separately (Xu, Davidson & Cheong, 2017).

Statement of financial position shall be presented as follows –

Whirl Ltd

Statement of financial position as at 30th June 2018

Particulars Amount ('000) Amount ('000)

ASSET

Current Assets

Cash and Cash Equivalent $ 212.00

Trade Receivable and Inventory $ 375.00

Prepaid expenses $ 3.00

Total Current Assets $ 590.00

Non-Current Assets

Property, Plant and Equipment and Intangible Assets $ 348.00

Less: Accumulated depreciation $ 30.00

Net value of property, Plant and Equipment and Intangible

Assets $ 318.00

Patents $ 20.00

Total Non-Current Assets $ 338.00

Total Assets $ 928.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

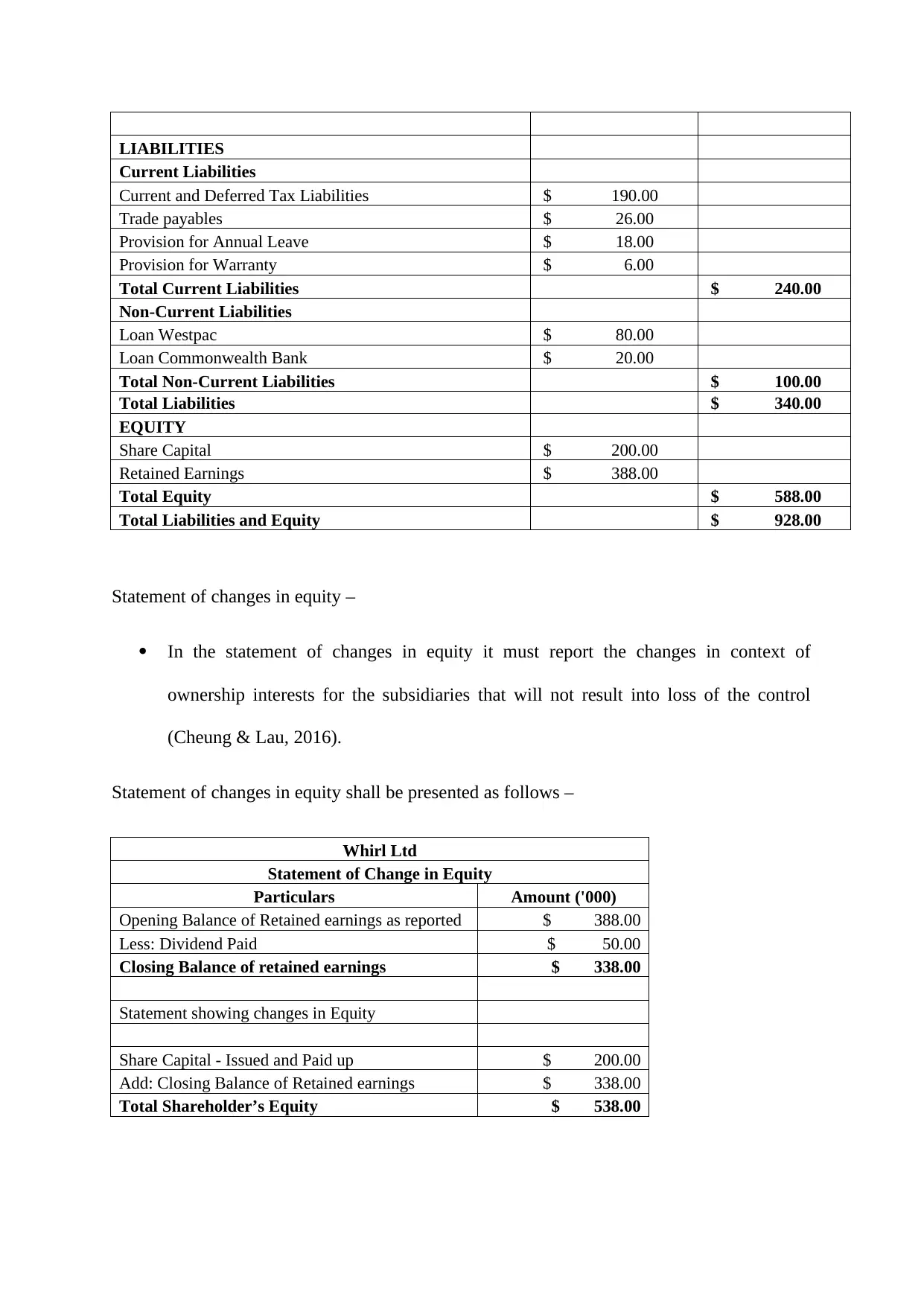

LIABILITIES

Current Liabilities

Current and Deferred Tax Liabilities $ 190.00

Trade payables $ 26.00

Provision for Annual Leave $ 18.00

Provision for Warranty $ 6.00

Total Current Liabilities $ 240.00

Non-Current Liabilities

Loan Westpac $ 80.00

Loan Commonwealth Bank $ 20.00

Total Non-Current Liabilities $ 100.00

Total Liabilities $ 340.00

EQUITY

Share Capital $ 200.00

Retained Earnings $ 388.00

Total Equity $ 588.00

Total Liabilities and Equity $ 928.00

Statement of changes in equity –

In the statement of changes in equity it must report the changes in context of

ownership interests for the subsidiaries that will not result into loss of the control

(Cheung & Lau, 2016).

Statement of changes in equity shall be presented as follows –

Whirl Ltd

Statement of Change in Equity

Particulars Amount ('000)

Opening Balance of Retained earnings as reported $ 388.00

Less: Dividend Paid $ 50.00

Closing Balance of retained earnings $ 338.00

Statement showing changes in Equity

Share Capital - Issued and Paid up $ 200.00

Add: Closing Balance of Retained earnings $ 338.00

Total Shareholder’s Equity $ 538.00

Current Liabilities

Current and Deferred Tax Liabilities $ 190.00

Trade payables $ 26.00

Provision for Annual Leave $ 18.00

Provision for Warranty $ 6.00

Total Current Liabilities $ 240.00

Non-Current Liabilities

Loan Westpac $ 80.00

Loan Commonwealth Bank $ 20.00

Total Non-Current Liabilities $ 100.00

Total Liabilities $ 340.00

EQUITY

Share Capital $ 200.00

Retained Earnings $ 388.00

Total Equity $ 588.00

Total Liabilities and Equity $ 928.00

Statement of changes in equity –

In the statement of changes in equity it must report the changes in context of

ownership interests for the subsidiaries that will not result into loss of the control

(Cheung & Lau, 2016).

Statement of changes in equity shall be presented as follows –

Whirl Ltd

Statement of Change in Equity

Particulars Amount ('000)

Opening Balance of Retained earnings as reported $ 388.00

Less: Dividend Paid $ 50.00

Closing Balance of retained earnings $ 338.00

Statement showing changes in Equity

Share Capital - Issued and Paid up $ 200.00

Add: Closing Balance of Retained earnings $ 338.00

Total Shareholder’s Equity $ 538.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reference

Aasb.gov.au. (2019). Retrieved 6 April 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/Framework_07-

04_COMPjun14_07-14.pdf

Aasb.gov.au. (2019). Retrieved 6 April 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf

Aasb.gov.au. (2019). Australian Accounting Standards Board (AASB) - Home . Retrieved 6

April 2019, from https://www.aasb.gov.au/

Chand, P., Patel, A., & White, M. (2015). Adopting international financial reporting

standards for small and medium‐sized enterprises. Australian Accounting

Review, 25(2), 139-154.

Cheung, E., & Lau, J. (2016). Readability of Notes to the Financial Statements and the

Adoption of IFRS. Australian Accounting Review, 26(2), 162-176.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hodgson, A., & Russell, M. (2014). Comprehending comprehensive income. Australian

Accounting Review, 24(2), 100-110.

Iasplus.com. (2019). International Accounting Standards Board (IASB). Retrieved 6 April

2019, from https://www.iasplus.com/en/resources/ifrsf/iasb-ifrs-ic/iasb

Majercakova, D., & Skoda, M. (2015). Fair value in financial statements after financial

crisis. Journal of Applied Accounting Research, 16(3), 312-332.

Standard, I. A. (2015). Presentation of Financial Statements. Balance Sheet, 54, 80A.

Aasb.gov.au. (2019). Retrieved 6 April 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/Framework_07-

04_COMPjun14_07-14.pdf

Aasb.gov.au. (2019). Retrieved 6 April 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf

Aasb.gov.au. (2019). Australian Accounting Standards Board (AASB) - Home . Retrieved 6

April 2019, from https://www.aasb.gov.au/

Chand, P., Patel, A., & White, M. (2015). Adopting international financial reporting

standards for small and medium‐sized enterprises. Australian Accounting

Review, 25(2), 139-154.

Cheung, E., & Lau, J. (2016). Readability of Notes to the Financial Statements and the

Adoption of IFRS. Australian Accounting Review, 26(2), 162-176.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hodgson, A., & Russell, M. (2014). Comprehending comprehensive income. Australian

Accounting Review, 24(2), 100-110.

Iasplus.com. (2019). International Accounting Standards Board (IASB). Retrieved 6 April

2019, from https://www.iasplus.com/en/resources/ifrsf/iasb-ifrs-ic/iasb

Majercakova, D., & Skoda, M. (2015). Fair value in financial statements after financial

crisis. Journal of Applied Accounting Research, 16(3), 312-332.

Standard, I. A. (2015). Presentation of Financial Statements. Balance Sheet, 54, 80A.

Xu, W., Davidson, R. A., & Cheong, C. S. (2017). Converting financial statements: operating

to capitalised leases. Pacific accounting review, 29(1), 34-54.

to capitalised leases. Pacific accounting review, 29(1), 34-54.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.