Financial Accounting Principles and Concepts

VerifiedAdded on 2023/03/16

|38

|3915

|73

AI Summary

This document provides an overview of financial accounting principles and concepts. It discusses the importance of accounting regulations and concepts in the business and various concepts for achieving growth of the company. It also explores the preparation of financial statements, journal entries, ledger accounts, trial balance, income statement, balance sheet, and more. The document covers topics such as accounting rules and principles, regulations relating to financial accounting, conventions and concepts relating to consistency and material disclosure, and case studies of clients.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Account Principle

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

Report to Line Manager...............................................................................................................4

Client 1.............................................................................................................................................7

A. Preparation of Journal entries.................................................................................................7

B. Ledger accounts......................................................................................................................9

C. Trial balance..........................................................................................................................18

Client 2...........................................................................................................................................19

A. Statement of Profit and Loss.................................................................................................19

B. Preparing balance sheet of Peter piper..................................................................................20

Client 3...........................................................................................................................................22

A. Producing Income statement.................................................................................................22

B. Preparing Statement of Financial Position............................................................................23

C. Consistency and Prudency concepts.....................................................................................28

D. Outlining purpose of depreciation........................................................................................29

Client 4...........................................................................................................................................30

A. Preparation of Bank Reconciliation Statement.....................................................................30

B. Causes of varying bank records with accounting books.......................................................31

C. Producing Bank Reconciliation Statement...........................................................................31

Client 5...........................................................................................................................................31

A. Sales ledger control account and Purchase ledger control account......................................31

B. Explaining meaning of control account................................................................................32

Client 6...........................................................................................................................................33

A. Meaning and features of suspense account...........................................................................33

INTRODUCTION...........................................................................................................................3

Report to Line Manager...............................................................................................................4

Client 1.............................................................................................................................................7

A. Preparation of Journal entries.................................................................................................7

B. Ledger accounts......................................................................................................................9

C. Trial balance..........................................................................................................................18

Client 2...........................................................................................................................................19

A. Statement of Profit and Loss.................................................................................................19

B. Preparing balance sheet of Peter piper..................................................................................20

Client 3...........................................................................................................................................22

A. Producing Income statement.................................................................................................22

B. Preparing Statement of Financial Position............................................................................23

C. Consistency and Prudency concepts.....................................................................................28

D. Outlining purpose of depreciation........................................................................................29

Client 4...........................................................................................................................................30

A. Preparation of Bank Reconciliation Statement.....................................................................30

B. Causes of varying bank records with accounting books.......................................................31

C. Producing Bank Reconciliation Statement...........................................................................31

Client 5...........................................................................................................................................31

A. Sales ledger control account and Purchase ledger control account......................................31

B. Explaining meaning of control account................................................................................32

Client 6...........................................................................................................................................33

A. Meaning and features of suspense account...........................................................................33

B. Drafting trial balance............................................................................................................33

C. Preparing journal entries.......................................................................................................34

D. Differentiating suspense and clearing account.....................................................................34

CONCLUSION..............................................................................................................................34

REFERENCES..............................................................................................................................36

INTRODUCTION

Accounting plays crucial role in the company to prepare final accounts in effective

manner. Present report deals with preparation of financial statements of 6 clients and showing

financial position. Moreover, accounting principles and concepts are discussed in the report.

Accounting guidelines issued by various professional bodies are explained as well. Furthermore,

trial balance and ledger accounts are prepared for the clients. Moreover, sales and purchase

ledger control both are produced. Thus, it can be said that financial accounting principles

provides way to produce correct financial statements of the business.

C. Preparing journal entries.......................................................................................................34

D. Differentiating suspense and clearing account.....................................................................34

CONCLUSION..............................................................................................................................34

REFERENCES..............................................................................................................................36

INTRODUCTION

Accounting plays crucial role in the company to prepare final accounts in effective

manner. Present report deals with preparation of financial statements of 6 clients and showing

financial position. Moreover, accounting principles and concepts are discussed in the report.

Accounting guidelines issued by various professional bodies are explained as well. Furthermore,

trial balance and ledger accounts are prepared for the clients. Moreover, sales and purchase

ledger control both are produced. Thus, it can be said that financial accounting principles

provides way to produce correct financial statements of the business.

Report to Line Manager

To: Line Manager

Subject: Importance of accounting regulations and concepts in the business and various

concepts for achieving growth of company.

Define financial accounting: - Financial accounting is a financial statement of a company. In

financial statement we include income statement and balance sheet of the company. It is the

process of recording, summarising, classifying and interpreting the financial statement of a

company. Financial accounting is the accounting activities of the company and it’s a

preparation of profit and loss accounts and balance sheet of a company. Company issue their

financial statement time to time and assess the statement regularly (Warren and Jones, 2018).

The main purpose of financial accounting is to forecast for the company, how to earn more

profits in future. Financial statement include cash flow, income statement, balance sheet,

retained earnings. In income statements include revenue and expenses of the company. Cash

flow include operating, investing and financing activities of the company. Balance sheet is a

statement of financial year it include assets, liabilities, capital equity etc. Financial statement

also shows the financial condition of a company. There are some principle regarding financial

accounting that is company report should be easy to understand and credible and comparable.

Financial accounting follow the common rules which is accounting standards. Financial

accounting is differ from managerial accounting and its forecast the financial reports of the

company and this reports shows to the stakeholders, regulators of the company. The IASB

(International Accounting Standards Board) objective is to provide financial information to

investor, shareholders and lenders. And then decision involves buying, selling, or holding

equity and to provide loans from credit.

Explain regulation relating to financial accounting: - The main purpose of financial

accounting is to forecast for the company. In the financial accounting prepared profit and loss

statement and statement of financial position of partnership to examine. The accounting

standards are designed for betterment of financial accounting. In accounting standards include

what transaction should be shown in financial statement (Mullinova, 2016). The main purpose

of creating accounts standards is to define proper accounting practice with in legal framework.

The necessity of accounting regulation is when an individual choose to start a business. The

need for accounting standards only becomes apparent when the key characteristics of the

To: Line Manager

Subject: Importance of accounting regulations and concepts in the business and various

concepts for achieving growth of company.

Define financial accounting: - Financial accounting is a financial statement of a company. In

financial statement we include income statement and balance sheet of the company. It is the

process of recording, summarising, classifying and interpreting the financial statement of a

company. Financial accounting is the accounting activities of the company and it’s a

preparation of profit and loss accounts and balance sheet of a company. Company issue their

financial statement time to time and assess the statement regularly (Warren and Jones, 2018).

The main purpose of financial accounting is to forecast for the company, how to earn more

profits in future. Financial statement include cash flow, income statement, balance sheet,

retained earnings. In income statements include revenue and expenses of the company. Cash

flow include operating, investing and financing activities of the company. Balance sheet is a

statement of financial year it include assets, liabilities, capital equity etc. Financial statement

also shows the financial condition of a company. There are some principle regarding financial

accounting that is company report should be easy to understand and credible and comparable.

Financial accounting follow the common rules which is accounting standards. Financial

accounting is differ from managerial accounting and its forecast the financial reports of the

company and this reports shows to the stakeholders, regulators of the company. The IASB

(International Accounting Standards Board) objective is to provide financial information to

investor, shareholders and lenders. And then decision involves buying, selling, or holding

equity and to provide loans from credit.

Explain regulation relating to financial accounting: - The main purpose of financial

accounting is to forecast for the company. In the financial accounting prepared profit and loss

statement and statement of financial position of partnership to examine. The accounting

standards are designed for betterment of financial accounting. In accounting standards include

what transaction should be shown in financial statement (Mullinova, 2016). The main purpose

of creating accounts standards is to define proper accounting practice with in legal framework.

The necessity of accounting regulation is when an individual choose to start a business. The

need for accounting standards only becomes apparent when the key characteristics of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

various mediums through which business venture can be carried. Financial accounting

focusses on the following areas that is identification and recording of financial information. In

financial accounting the activities should be reported. In this include clarity, accuracy

materialistic data which helps in better to judge a report. Financial statement are prepared

under regulatory framework. First is professional regulation, in this its outline that

recommended methods that can be used to value inventory and to provide guidance on when

inventory should be recognised. The next international regulation, in this the main aim of the

IASC was to promote the company worldwide and compare consistency in financial

statements with other companies. ISAB main aim is to establish open participatory and

transparent due process, collaborate globally for standard setting community and to connect

with investors, regulators, business leaders and the global accountancy profession at every

stage of process. The ISAB has full control on developing and set its own technical aspects.

Describe accounting rules and principles: - The rules and concepts that govern in

accounting. The main purpose of accounting principle is the accounting is based on legalistic

accounting which is detailed or complicated. If any company distribute their financial

statements to the shareholder or to the public so its required to follow generally accepted

accounting principle for preparing financial statements (Libby, 2017). Some basic accounting

principle are:-

The business as a single entity concept:- The business is a single entity . Business all

activities are treated separately .A business can run long after the existence of its owner.

The specific currency principle: - All country have their own currency. Some companies

who conduct business in foreign currencies ant then convert the currencies in prevalent

exchange rate of currency.

The specific time period principle: - Financial statement prepare in a specific time period. In

income statement there is start date and end date. And balance sheet is prepare on a certain

date.

The Historical Cost Principle: - The prices which is items were bought and sold its

valuation is done in financial statements. The real value may changes in inflation and

recession time.

focusses on the following areas that is identification and recording of financial information. In

financial accounting the activities should be reported. In this include clarity, accuracy

materialistic data which helps in better to judge a report. Financial statement are prepared

under regulatory framework. First is professional regulation, in this its outline that

recommended methods that can be used to value inventory and to provide guidance on when

inventory should be recognised. The next international regulation, in this the main aim of the

IASC was to promote the company worldwide and compare consistency in financial

statements with other companies. ISAB main aim is to establish open participatory and

transparent due process, collaborate globally for standard setting community and to connect

with investors, regulators, business leaders and the global accountancy profession at every

stage of process. The ISAB has full control on developing and set its own technical aspects.

Describe accounting rules and principles: - The rules and concepts that govern in

accounting. The main purpose of accounting principle is the accounting is based on legalistic

accounting which is detailed or complicated. If any company distribute their financial

statements to the shareholder or to the public so its required to follow generally accepted

accounting principle for preparing financial statements (Libby, 2017). Some basic accounting

principle are:-

The business as a single entity concept:- The business is a single entity . Business all

activities are treated separately .A business can run long after the existence of its owner.

The specific currency principle: - All country have their own currency. Some companies

who conduct business in foreign currencies ant then convert the currencies in prevalent

exchange rate of currency.

The specific time period principle: - Financial statement prepare in a specific time period. In

income statement there is start date and end date. And balance sheet is prepare on a certain

date.

The Historical Cost Principle: - The prices which is items were bought and sold its

valuation is done in financial statements. The real value may changes in inflation and

recession time.

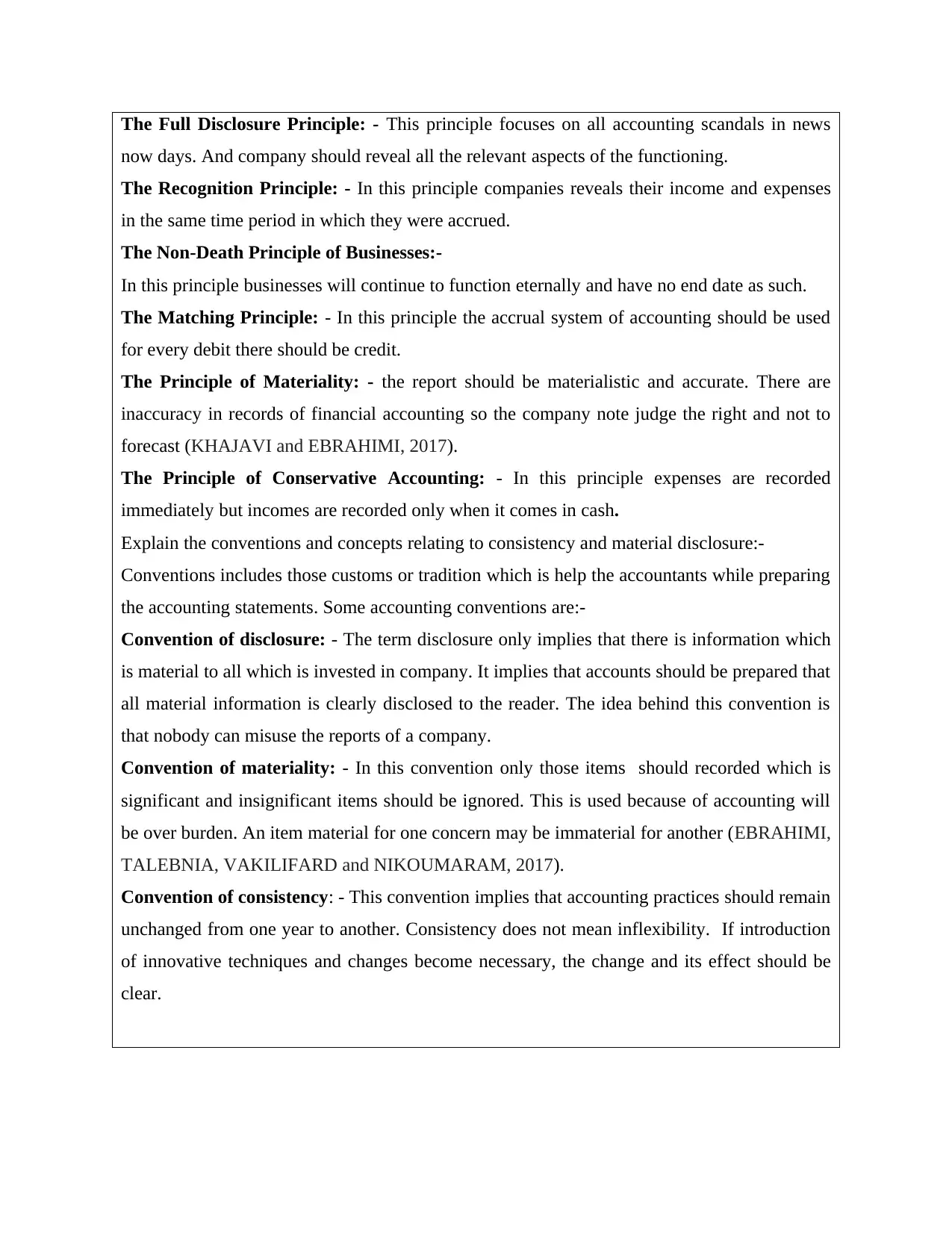

The Full Disclosure Principle: - This principle focuses on all accounting scandals in news

now days. And company should reveal all the relevant aspects of the functioning.

The Recognition Principle: - In this principle companies reveals their income and expenses

in the same time period in which they were accrued.

The Non-Death Principle of Businesses:-

In this principle businesses will continue to function eternally and have no end date as such.

The Matching Principle: - In this principle the accrual system of accounting should be used

for every debit there should be credit.

The Principle of Materiality: - the report should be materialistic and accurate. There are

inaccuracy in records of financial accounting so the company note judge the right and not to

forecast (KHAJAVI and EBRAHIMI, 2017).

The Principle of Conservative Accounting: - In this principle expenses are recorded

immediately but incomes are recorded only when it comes in cash.

Explain the conventions and concepts relating to consistency and material disclosure:-

Conventions includes those customs or tradition which is help the accountants while preparing

the accounting statements. Some accounting conventions are:-

Convention of disclosure: - The term disclosure only implies that there is information which

is material to all which is invested in company. It implies that accounts should be prepared that

all material information is clearly disclosed to the reader. The idea behind this convention is

that nobody can misuse the reports of a company.

Convention of materiality: - In this convention only those items should recorded which is

significant and insignificant items should be ignored. This is used because of accounting will

be over burden. An item material for one concern may be immaterial for another (EBRAHIMI,

TALEBNIA, VAKILIFARD and NIKOUMARAM, 2017).

Convention of consistency: - This convention implies that accounting practices should remain

unchanged from one year to another. Consistency does not mean inflexibility. If introduction

of innovative techniques and changes become necessary, the change and its effect should be

clear.

now days. And company should reveal all the relevant aspects of the functioning.

The Recognition Principle: - In this principle companies reveals their income and expenses

in the same time period in which they were accrued.

The Non-Death Principle of Businesses:-

In this principle businesses will continue to function eternally and have no end date as such.

The Matching Principle: - In this principle the accrual system of accounting should be used

for every debit there should be credit.

The Principle of Materiality: - the report should be materialistic and accurate. There are

inaccuracy in records of financial accounting so the company note judge the right and not to

forecast (KHAJAVI and EBRAHIMI, 2017).

The Principle of Conservative Accounting: - In this principle expenses are recorded

immediately but incomes are recorded only when it comes in cash.

Explain the conventions and concepts relating to consistency and material disclosure:-

Conventions includes those customs or tradition which is help the accountants while preparing

the accounting statements. Some accounting conventions are:-

Convention of disclosure: - The term disclosure only implies that there is information which

is material to all which is invested in company. It implies that accounts should be prepared that

all material information is clearly disclosed to the reader. The idea behind this convention is

that nobody can misuse the reports of a company.

Convention of materiality: - In this convention only those items should recorded which is

significant and insignificant items should be ignored. This is used because of accounting will

be over burden. An item material for one concern may be immaterial for another (EBRAHIMI,

TALEBNIA, VAKILIFARD and NIKOUMARAM, 2017).

Convention of consistency: - This convention implies that accounting practices should remain

unchanged from one year to another. Consistency does not mean inflexibility. If introduction

of innovative techniques and changes become necessary, the change and its effect should be

clear.

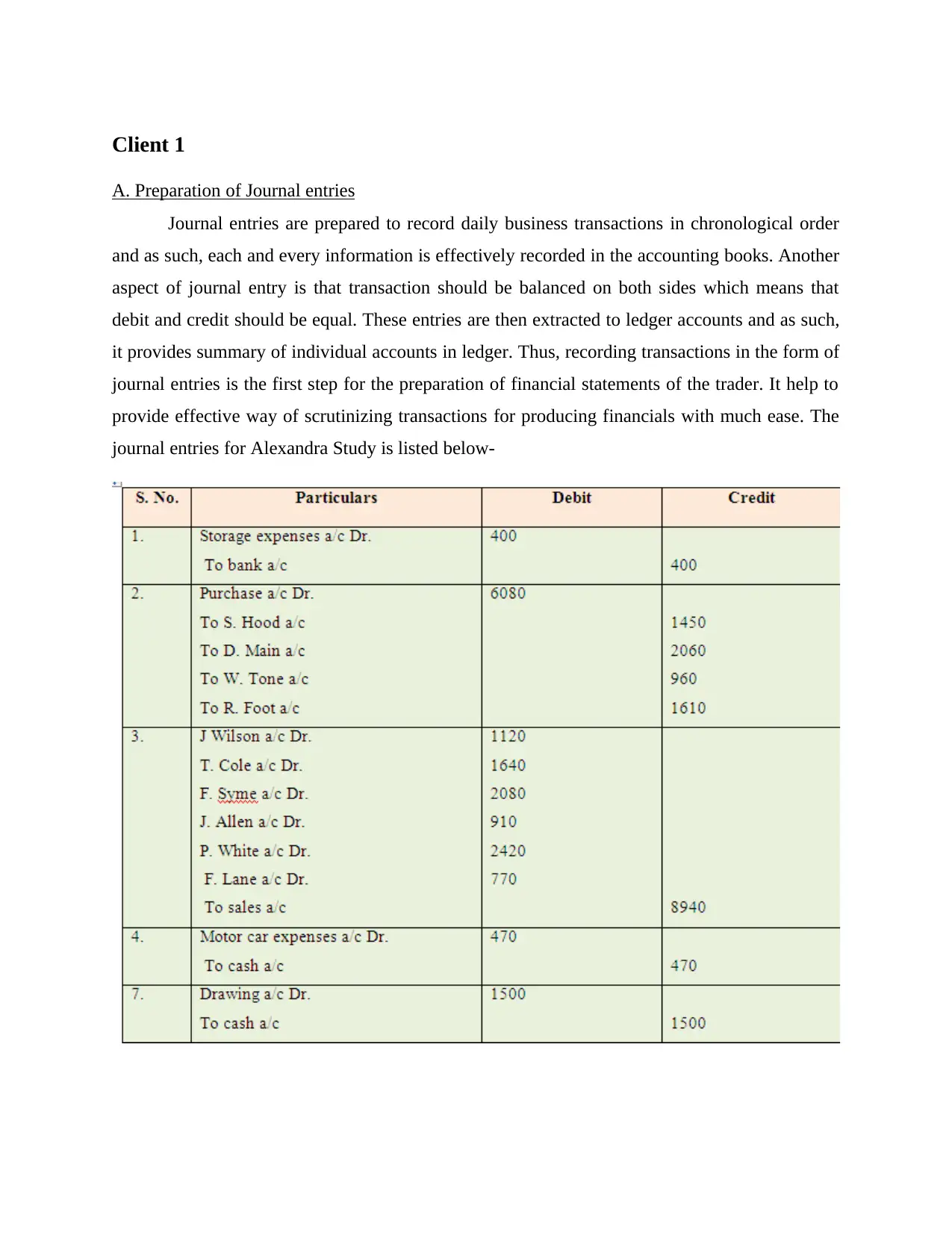

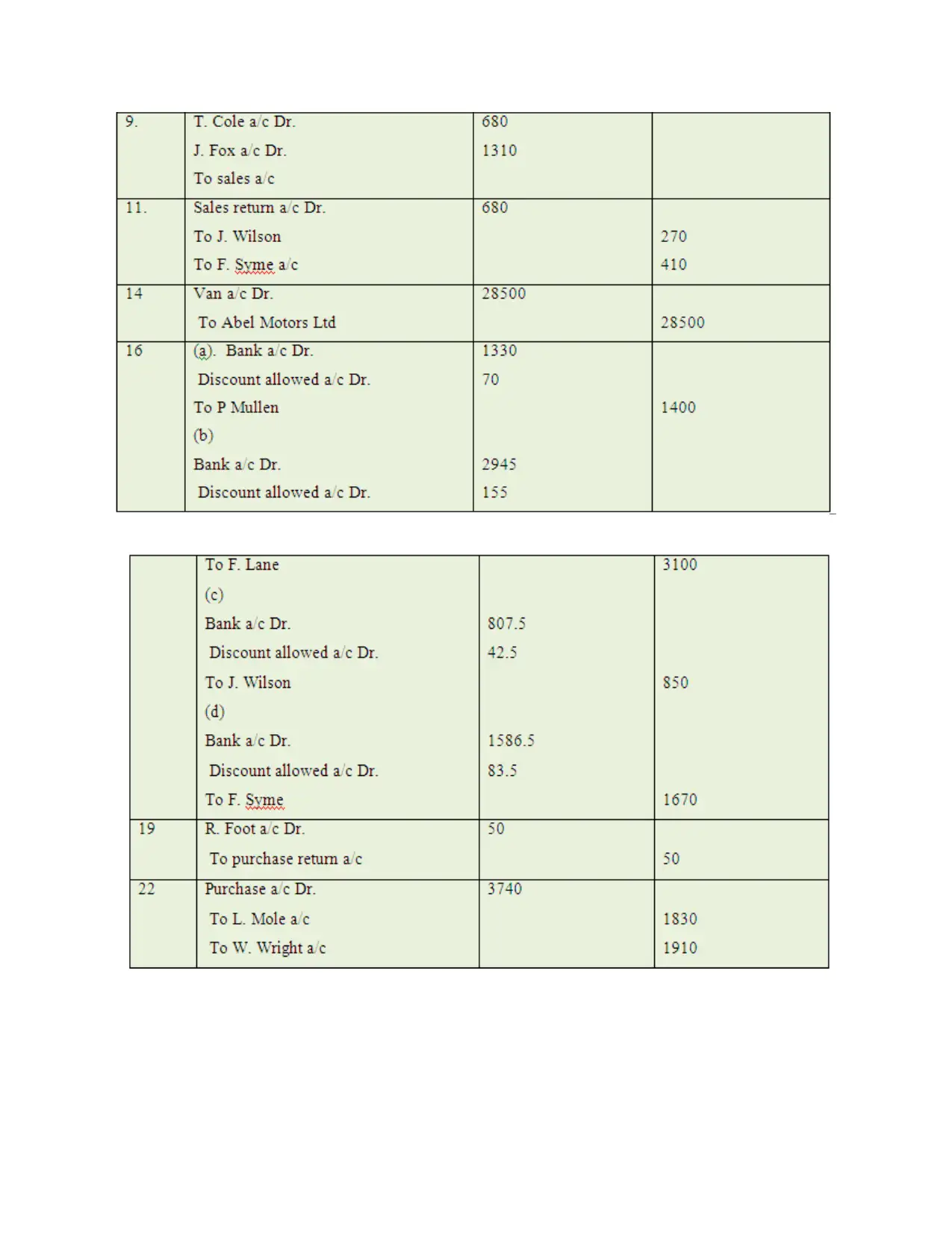

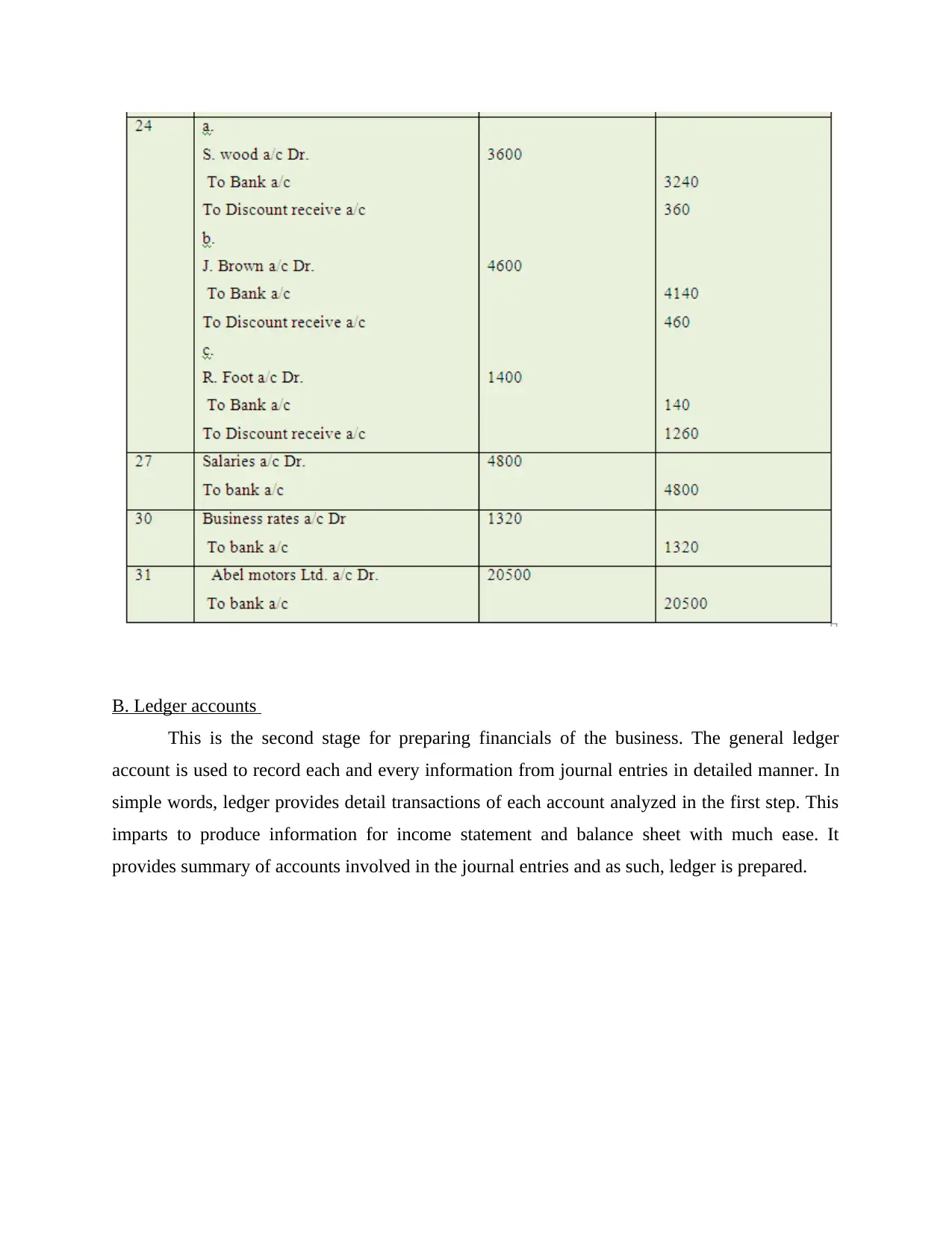

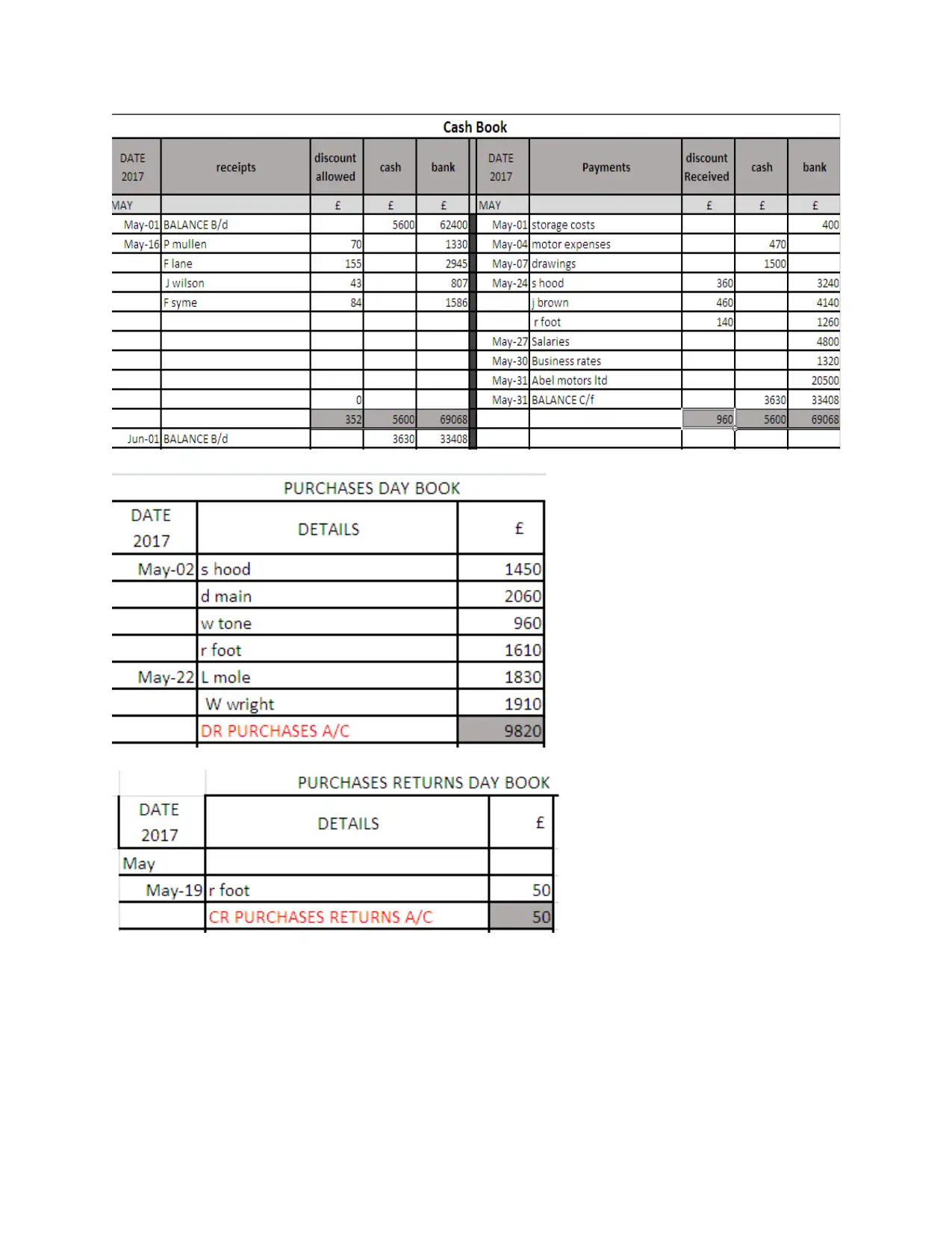

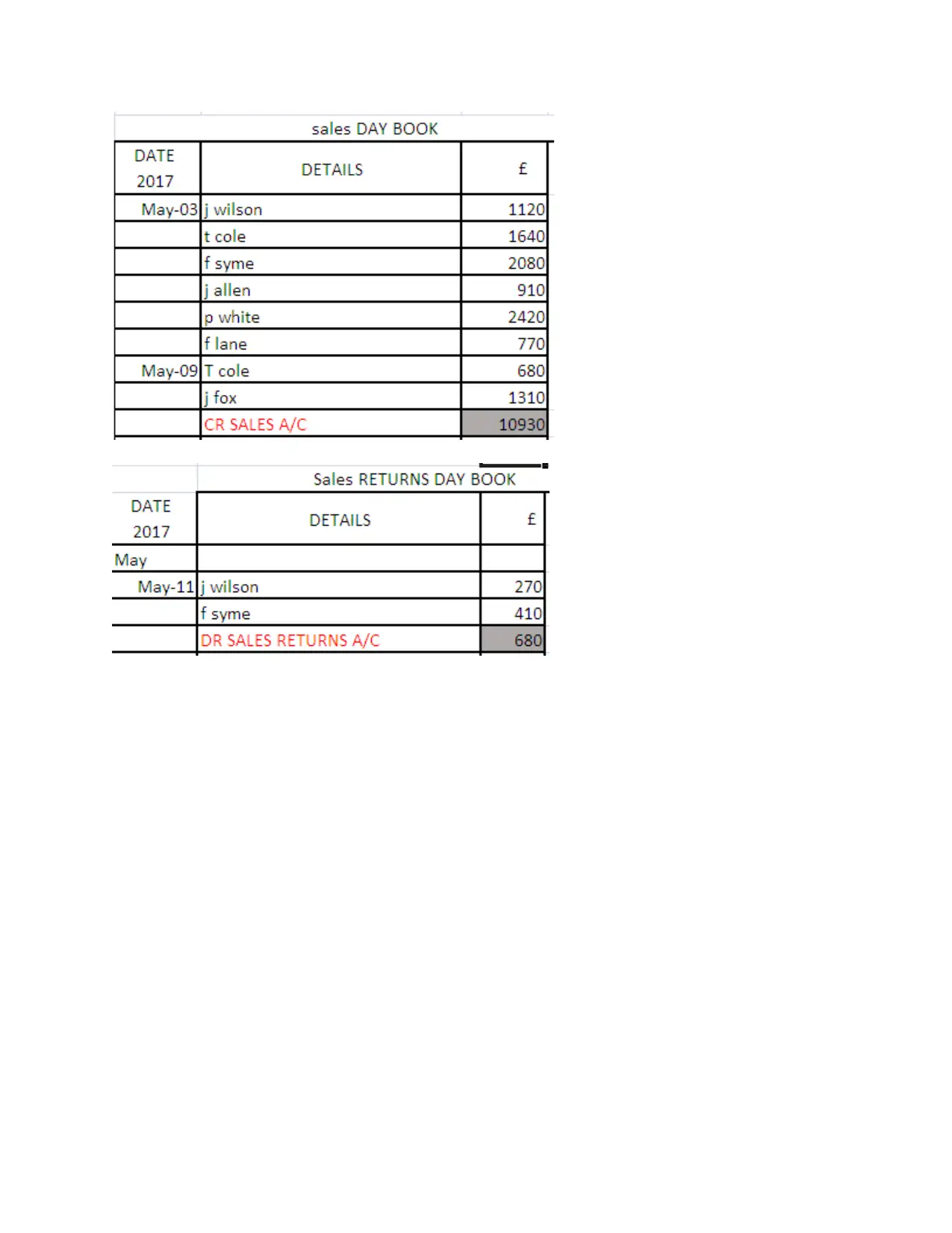

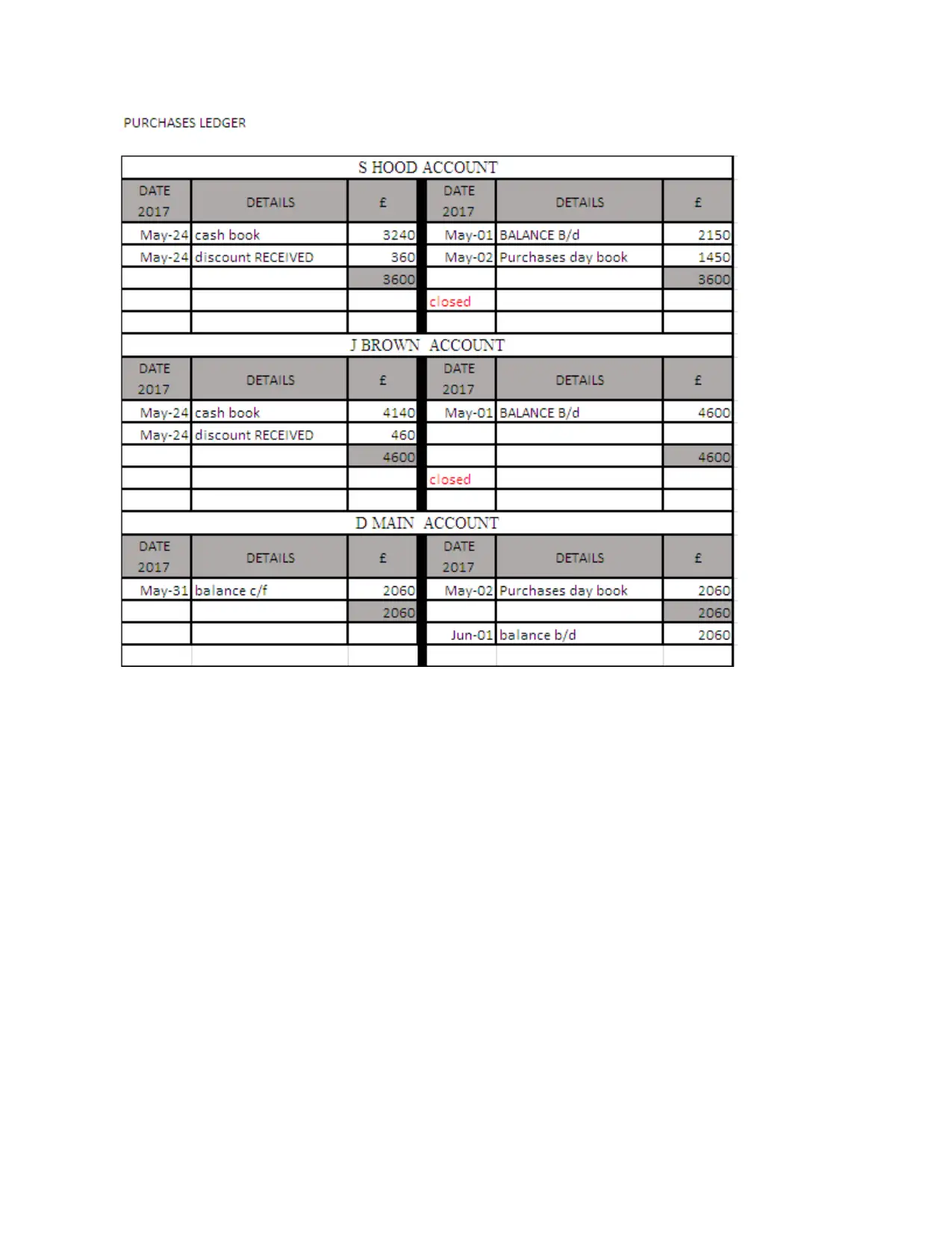

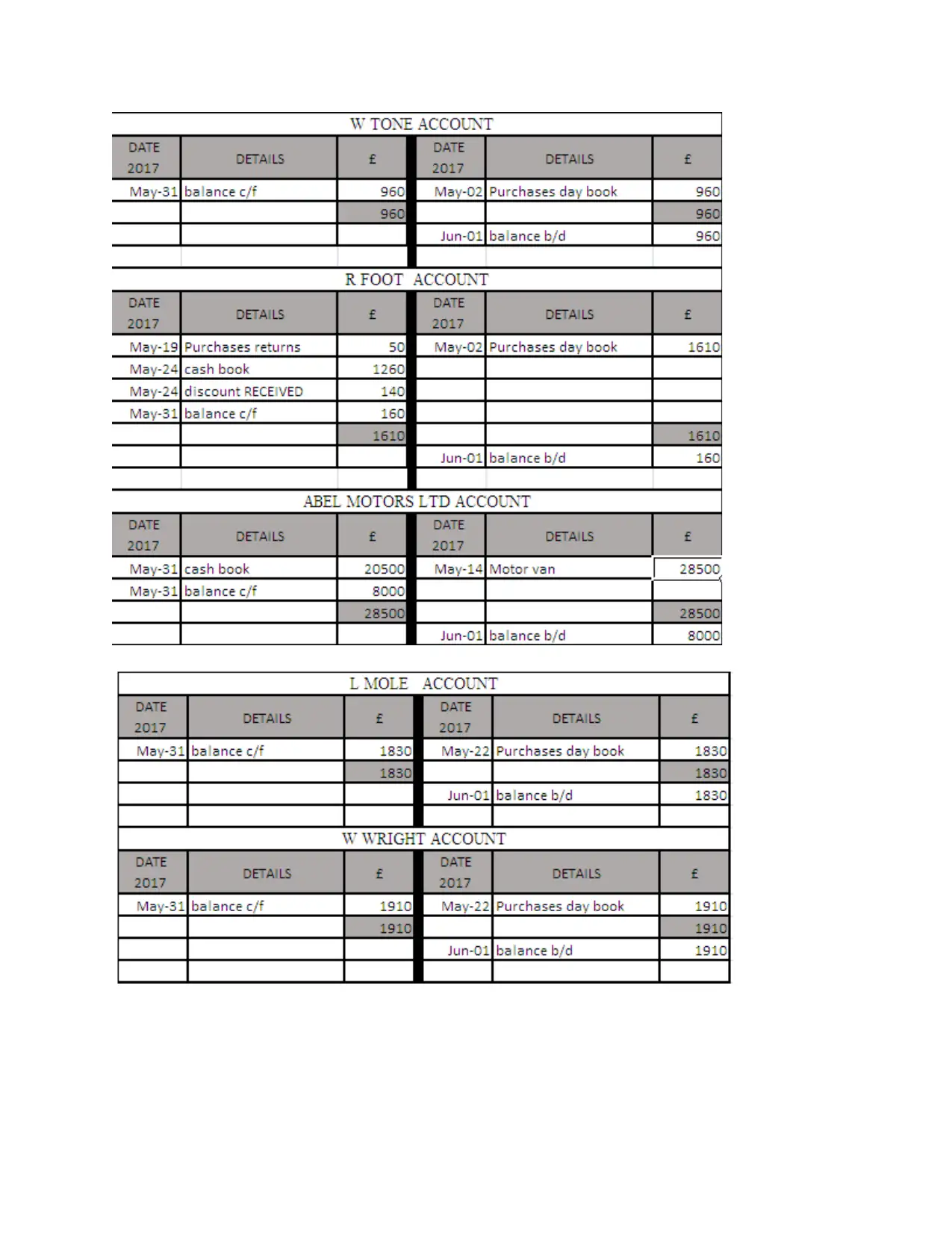

Client 1

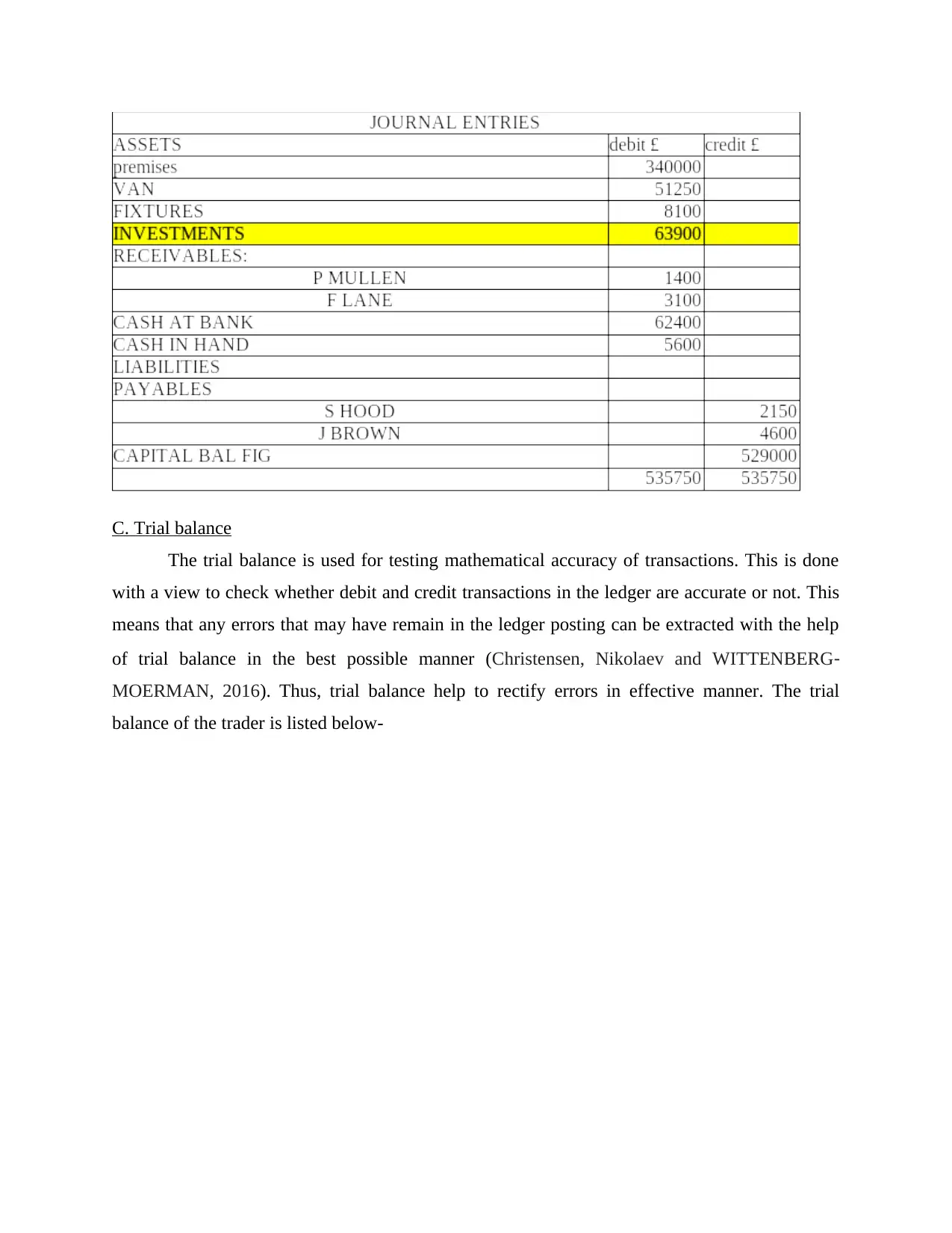

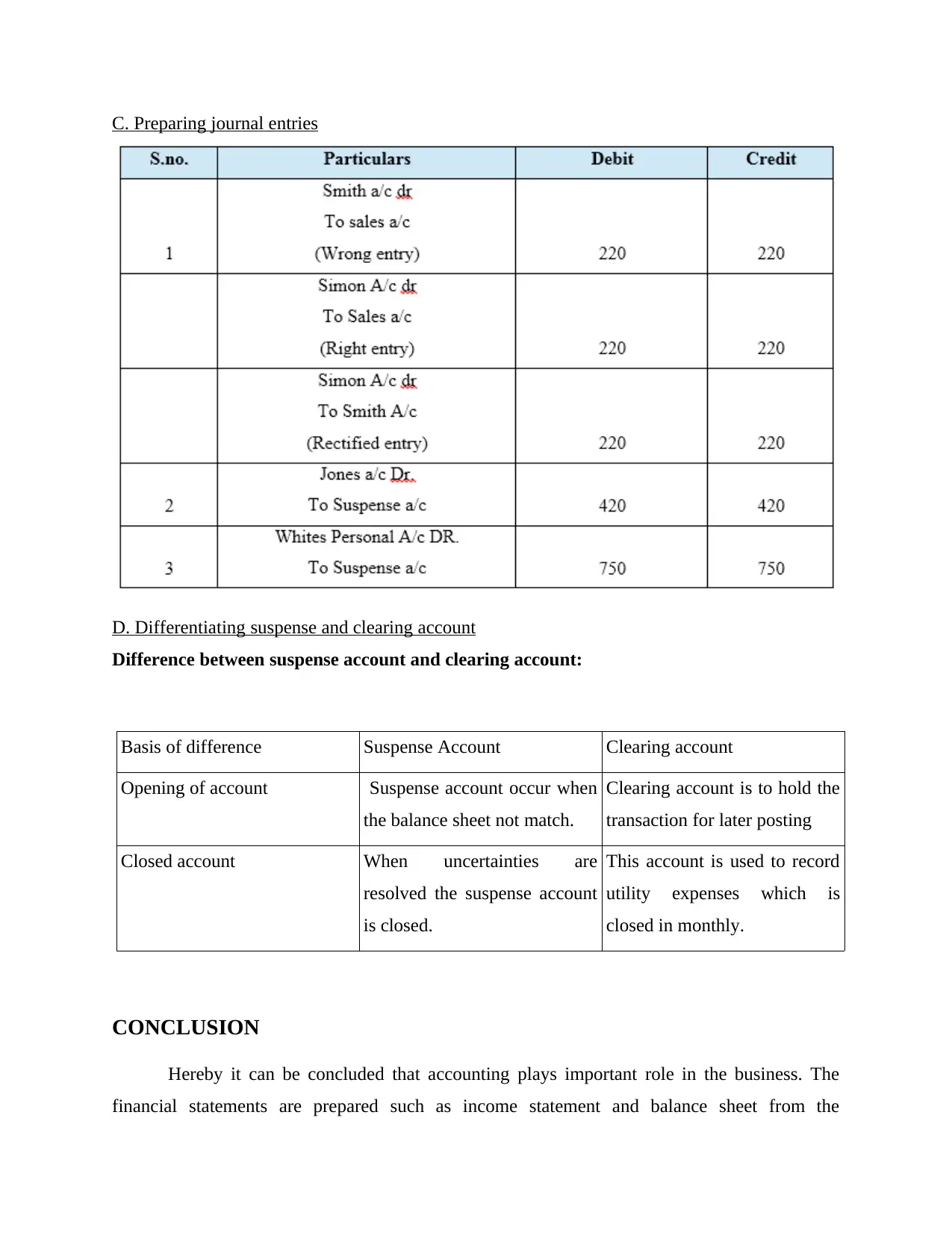

A. Preparation of Journal entries

Journal entries are prepared to record daily business transactions in chronological order

and as such, each and every information is effectively recorded in the accounting books. Another

aspect of journal entry is that transaction should be balanced on both sides which means that

debit and credit should be equal. These entries are then extracted to ledger accounts and as such,

it provides summary of individual accounts in ledger. Thus, recording transactions in the form of

journal entries is the first step for the preparation of financial statements of the trader. It help to

provide effective way of scrutinizing transactions for producing financials with much ease. The

journal entries for Alexandra Study is listed below-

A. Preparation of Journal entries

Journal entries are prepared to record daily business transactions in chronological order

and as such, each and every information is effectively recorded in the accounting books. Another

aspect of journal entry is that transaction should be balanced on both sides which means that

debit and credit should be equal. These entries are then extracted to ledger accounts and as such,

it provides summary of individual accounts in ledger. Thus, recording transactions in the form of

journal entries is the first step for the preparation of financial statements of the trader. It help to

provide effective way of scrutinizing transactions for producing financials with much ease. The

journal entries for Alexandra Study is listed below-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

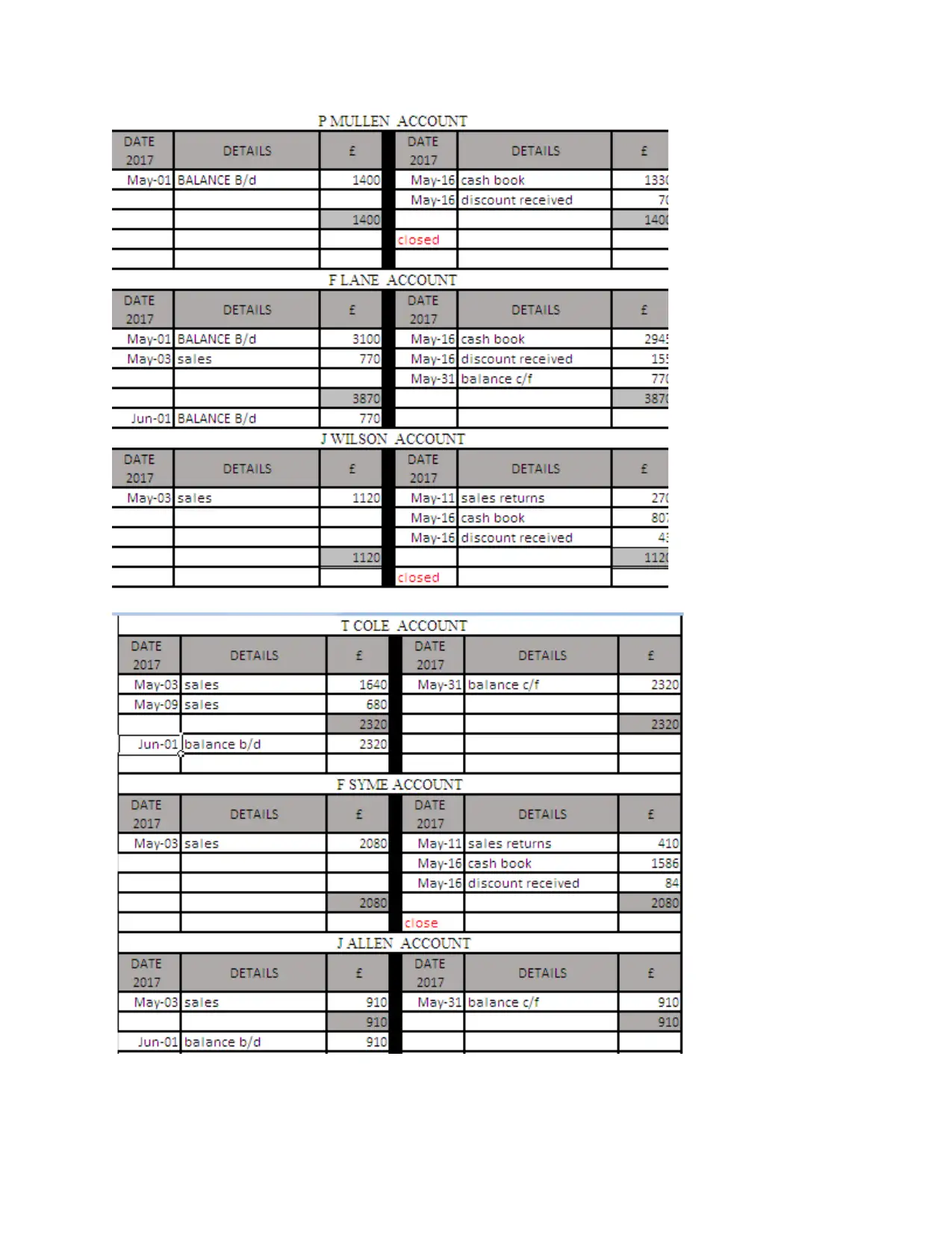

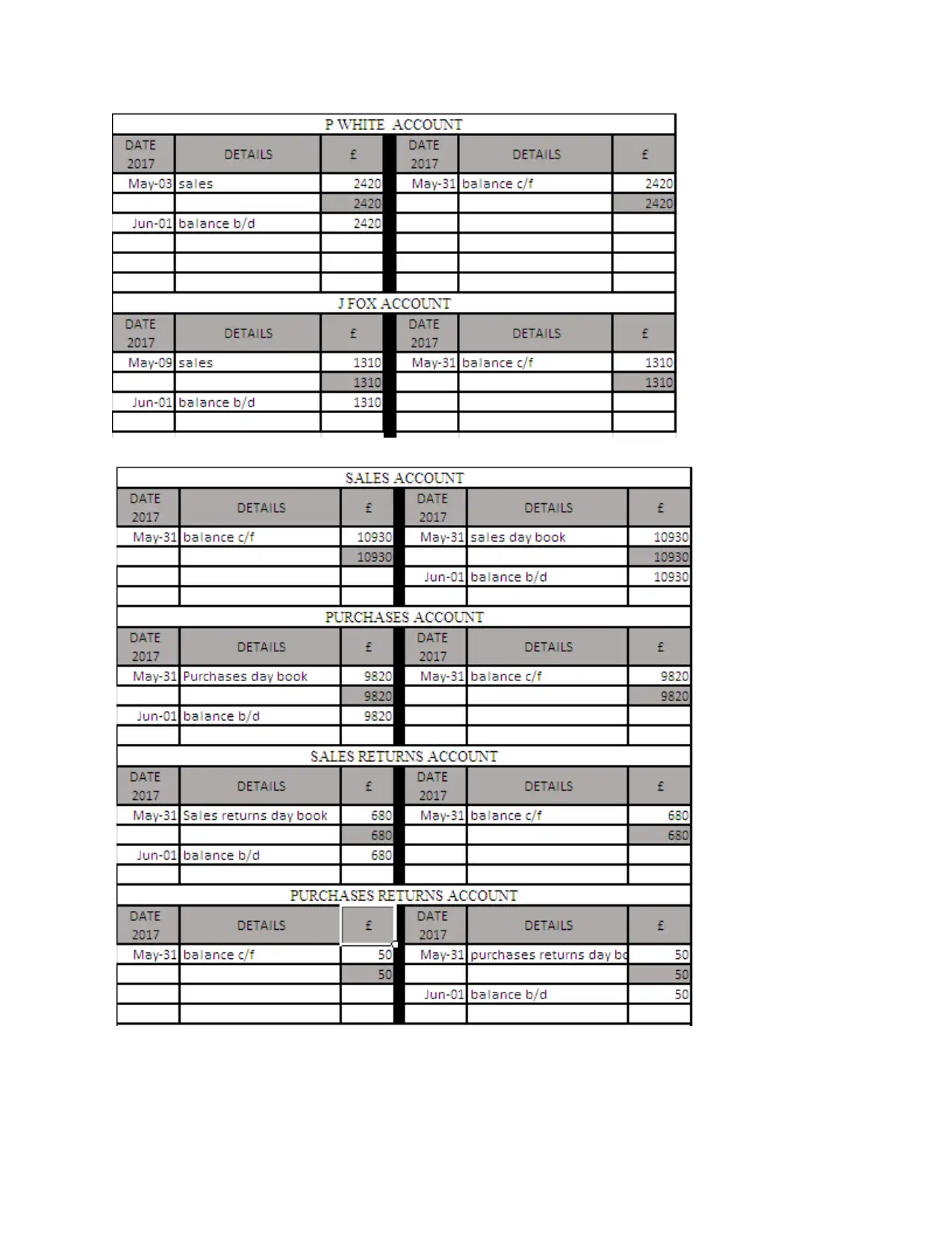

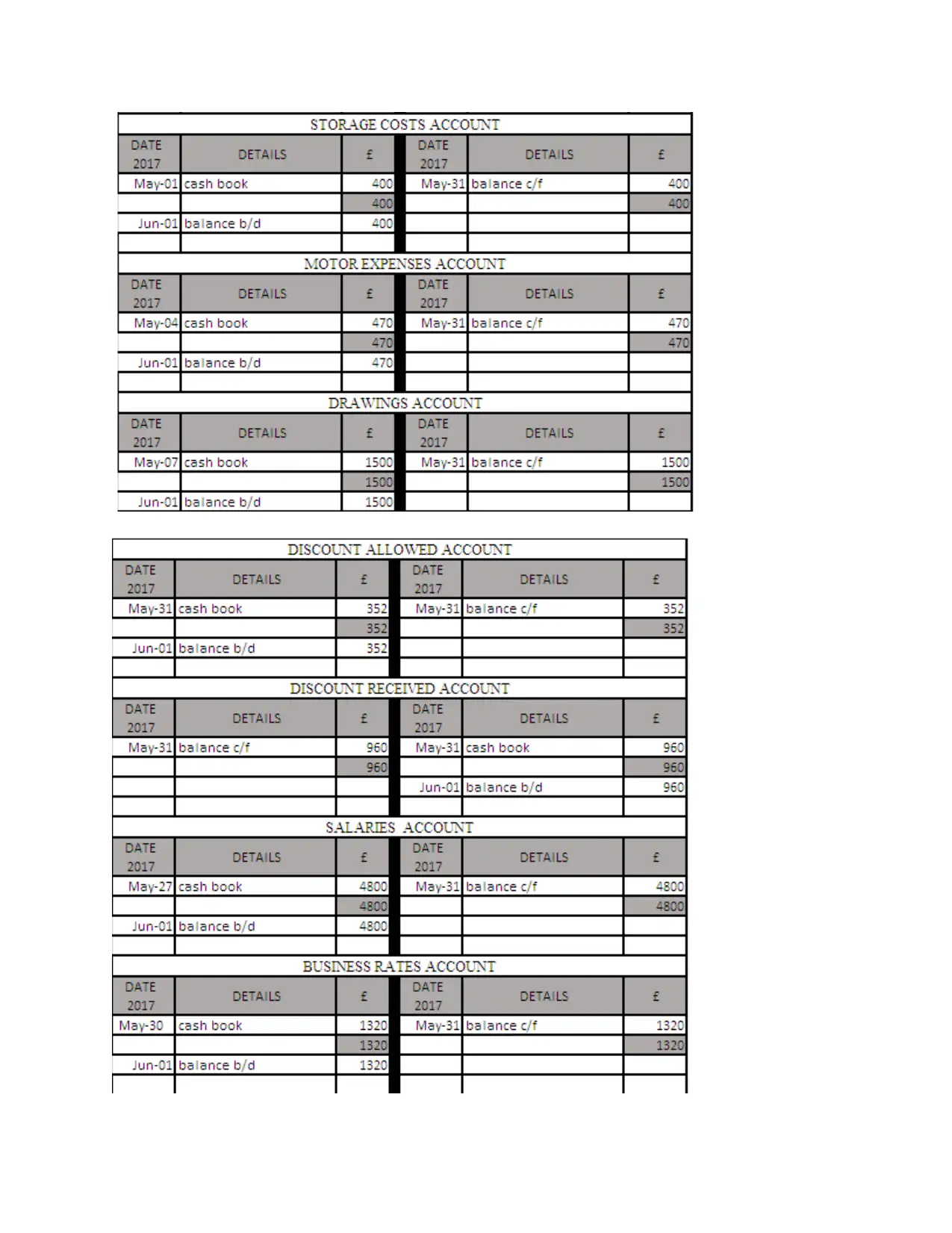

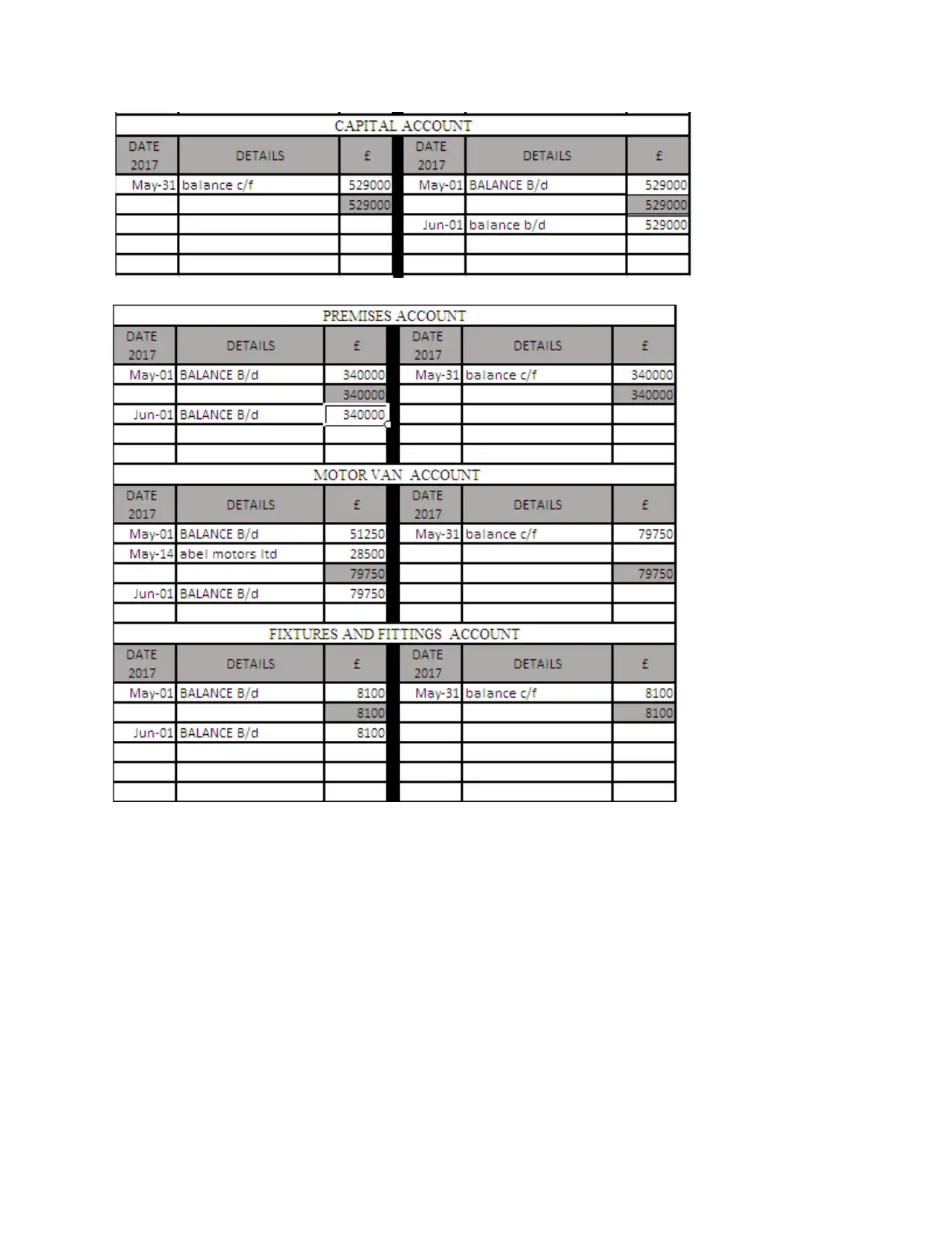

B. Ledger accounts

This is the second stage for preparing financials of the business. The general ledger

account is used to record each and every information from journal entries in detailed manner. In

simple words, ledger provides detail transactions of each account analyzed in the first step. This

imparts to produce information for income statement and balance sheet with much ease. It

provides summary of accounts involved in the journal entries and as such, ledger is prepared.

This is the second stage for preparing financials of the business. The general ledger

account is used to record each and every information from journal entries in detailed manner. In

simple words, ledger provides detail transactions of each account analyzed in the first step. This

imparts to produce information for income statement and balance sheet with much ease. It

provides summary of accounts involved in the journal entries and as such, ledger is prepared.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

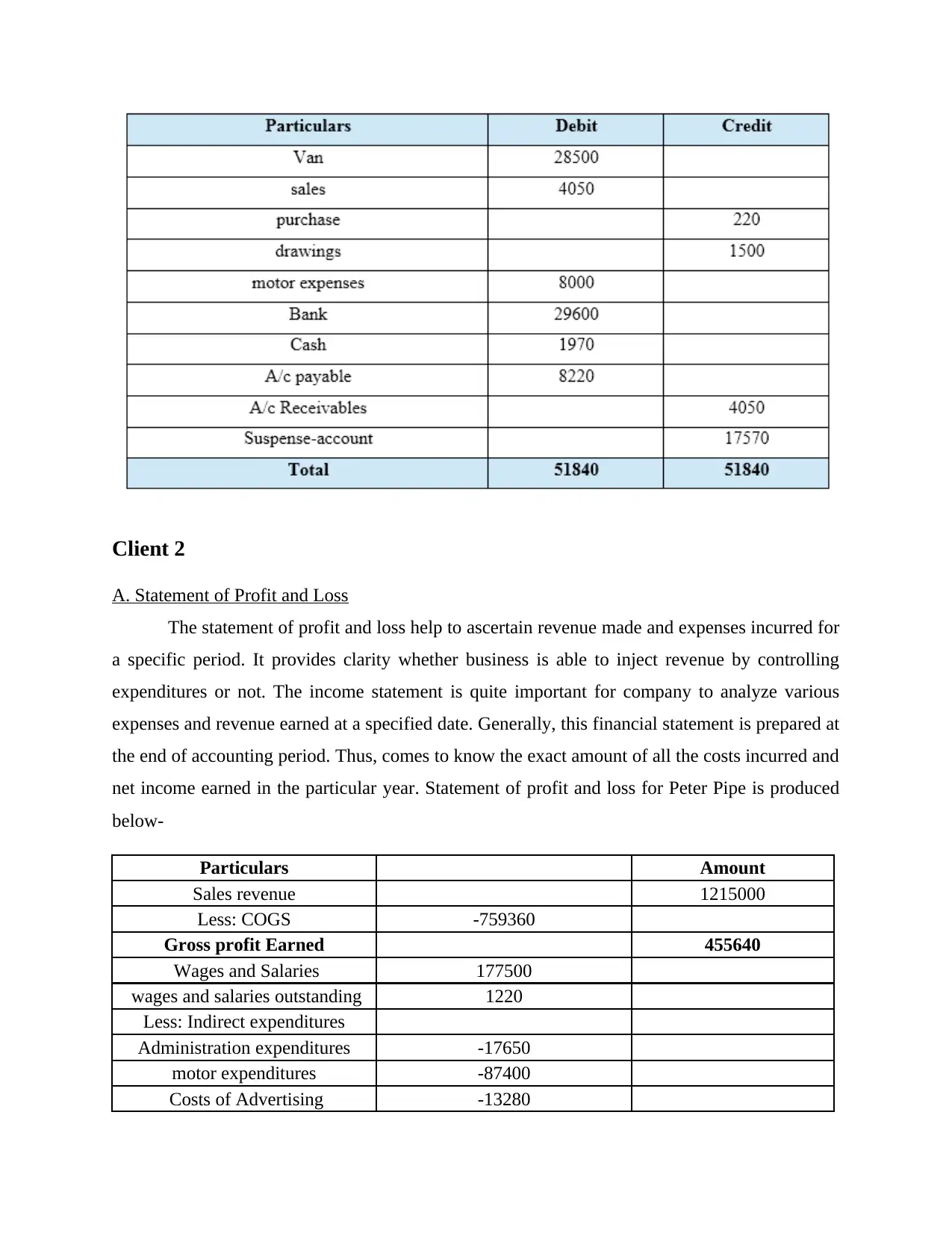

C. Trial balance

The trial balance is used for testing mathematical accuracy of transactions. This is done

with a view to check whether debit and credit transactions in the ledger are accurate or not. This

means that any errors that may have remain in the ledger posting can be extracted with the help

of trial balance in the best possible manner (Christensen, Nikolaev and WITTENBERG‐

MOERMAN, 2016). Thus, trial balance help to rectify errors in effective manner. The trial

balance of the trader is listed below-

The trial balance is used for testing mathematical accuracy of transactions. This is done

with a view to check whether debit and credit transactions in the ledger are accurate or not. This

means that any errors that may have remain in the ledger posting can be extracted with the help

of trial balance in the best possible manner (Christensen, Nikolaev and WITTENBERG‐

MOERMAN, 2016). Thus, trial balance help to rectify errors in effective manner. The trial

balance of the trader is listed below-

Client 2

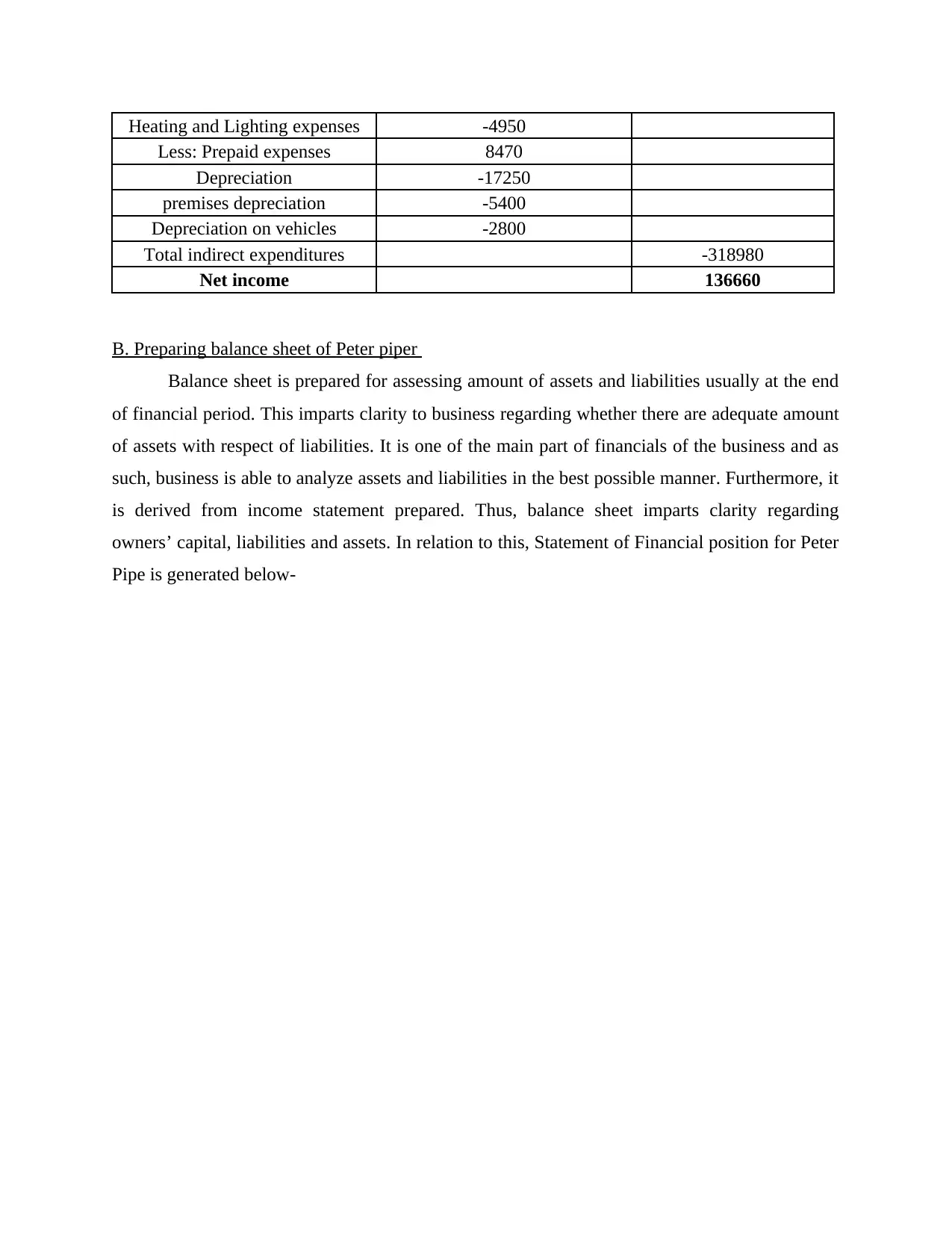

A. Statement of Profit and Loss

The statement of profit and loss help to ascertain revenue made and expenses incurred for

a specific period. It provides clarity whether business is able to inject revenue by controlling

expenditures or not. The income statement is quite important for company to analyze various

expenses and revenue earned at a specified date. Generally, this financial statement is prepared at

the end of accounting period. Thus, comes to know the exact amount of all the costs incurred and

net income earned in the particular year. Statement of profit and loss for Peter Pipe is produced

below-

Particulars Amount

Sales revenue 1215000

Less: COGS -759360

Gross profit Earned 455640

Wages and Salaries 177500

wages and salaries outstanding 1220

Less: Indirect expenditures

Administration expenditures -17650

motor expenditures -87400

Costs of Advertising -13280

A. Statement of Profit and Loss

The statement of profit and loss help to ascertain revenue made and expenses incurred for

a specific period. It provides clarity whether business is able to inject revenue by controlling

expenditures or not. The income statement is quite important for company to analyze various

expenses and revenue earned at a specified date. Generally, this financial statement is prepared at

the end of accounting period. Thus, comes to know the exact amount of all the costs incurred and

net income earned in the particular year. Statement of profit and loss for Peter Pipe is produced

below-

Particulars Amount

Sales revenue 1215000

Less: COGS -759360

Gross profit Earned 455640

Wages and Salaries 177500

wages and salaries outstanding 1220

Less: Indirect expenditures

Administration expenditures -17650

motor expenditures -87400

Costs of Advertising -13280

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Heating and Lighting expenses -4950

Less: Prepaid expenses 8470

Depreciation -17250

premises depreciation -5400

Depreciation on vehicles -2800

Total indirect expenditures -318980

Net income 136660

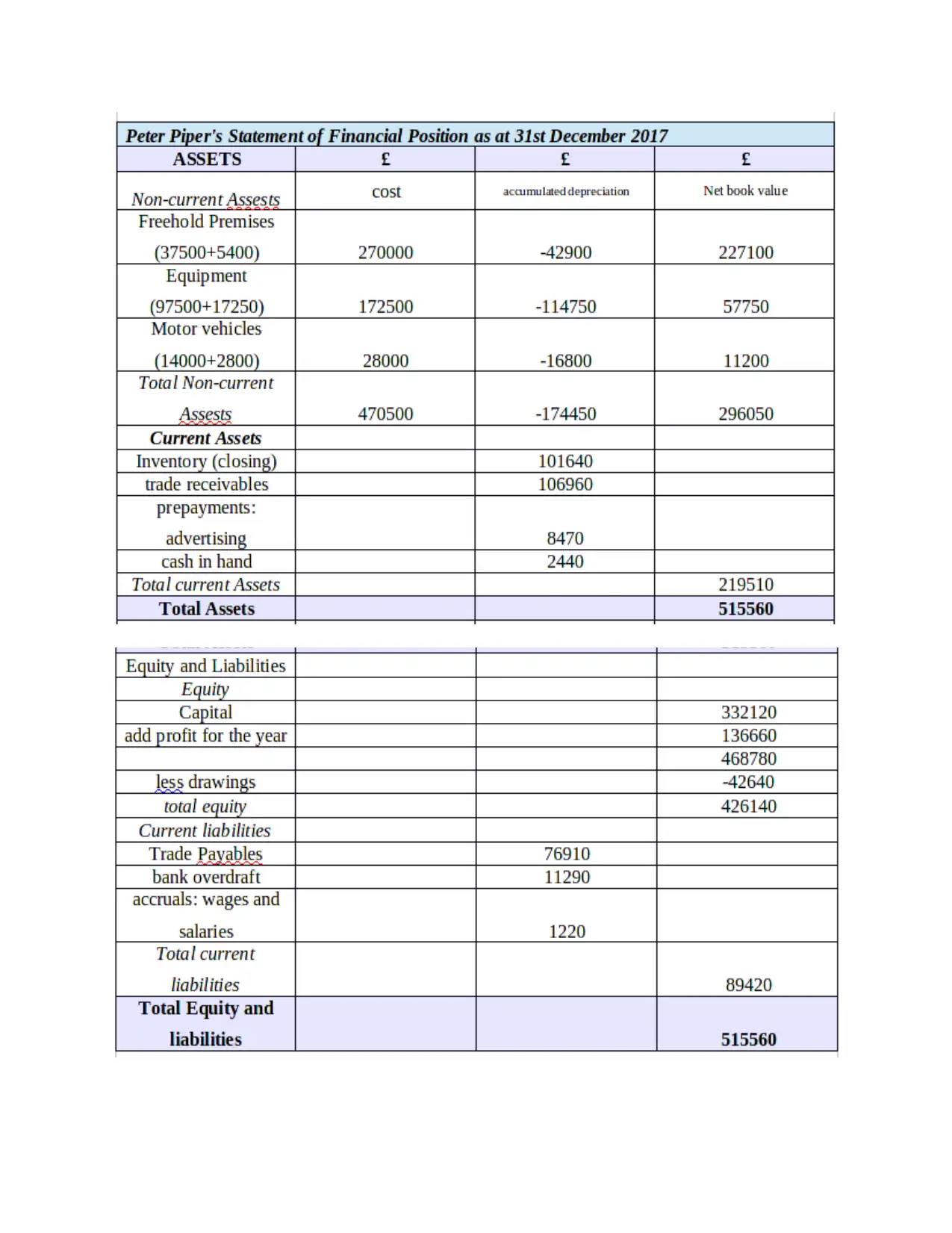

B. Preparing balance sheet of Peter piper

Balance sheet is prepared for assessing amount of assets and liabilities usually at the end

of financial period. This imparts clarity to business regarding whether there are adequate amount

of assets with respect of liabilities. It is one of the main part of financials of the business and as

such, business is able to analyze assets and liabilities in the best possible manner. Furthermore, it

is derived from income statement prepared. Thus, balance sheet imparts clarity regarding

owners’ capital, liabilities and assets. In relation to this, Statement of Financial position for Peter

Pipe is generated below-

Less: Prepaid expenses 8470

Depreciation -17250

premises depreciation -5400

Depreciation on vehicles -2800

Total indirect expenditures -318980

Net income 136660

B. Preparing balance sheet of Peter piper

Balance sheet is prepared for assessing amount of assets and liabilities usually at the end

of financial period. This imparts clarity to business regarding whether there are adequate amount

of assets with respect of liabilities. It is one of the main part of financials of the business and as

such, business is able to analyze assets and liabilities in the best possible manner. Furthermore, it

is derived from income statement prepared. Thus, balance sheet imparts clarity regarding

owners’ capital, liabilities and assets. In relation to this, Statement of Financial position for Peter

Pipe is generated below-

Client 3

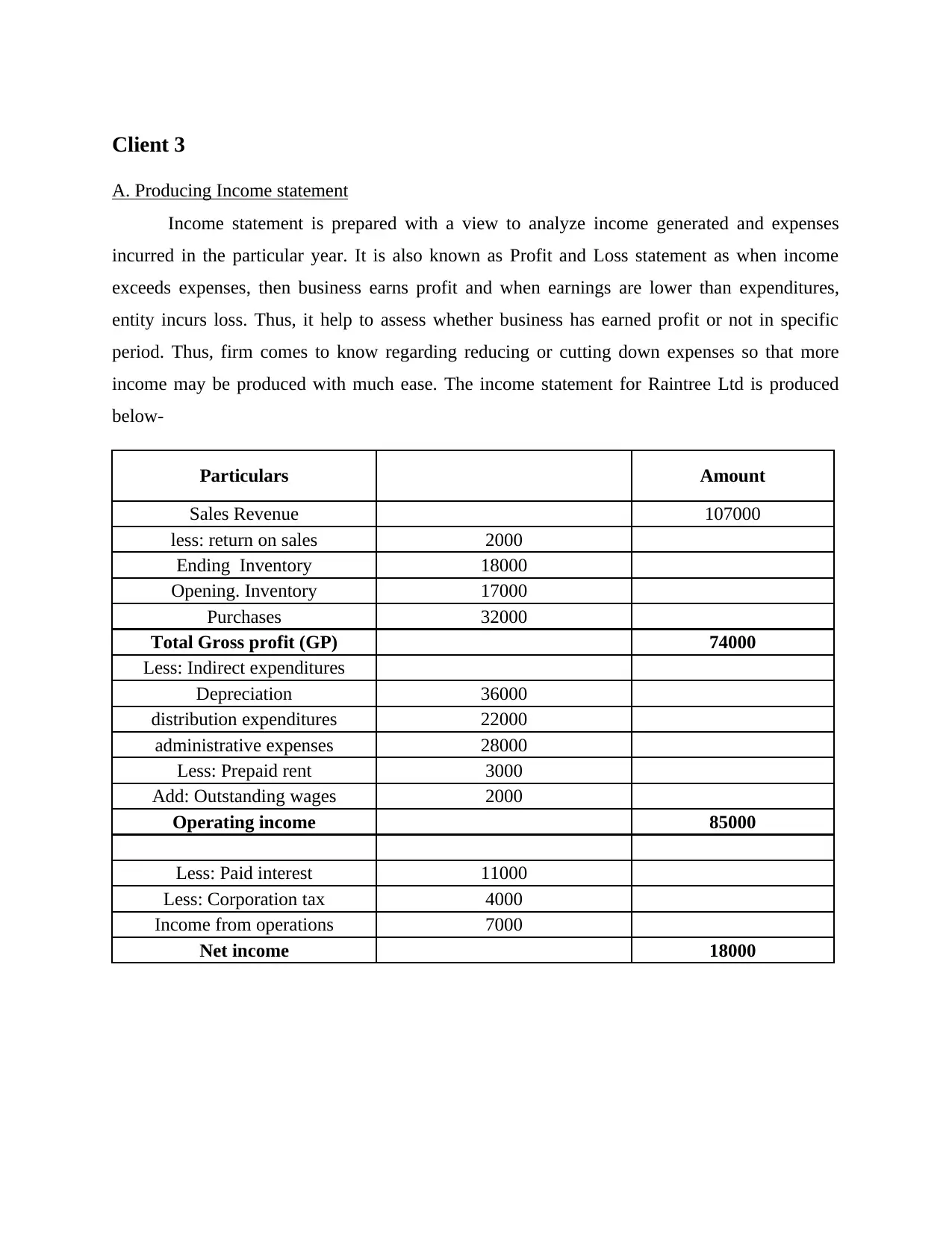

A. Producing Income statement

Income statement is prepared with a view to analyze income generated and expenses

incurred in the particular year. It is also known as Profit and Loss statement as when income

exceeds expenses, then business earns profit and when earnings are lower than expenditures,

entity incurs loss. Thus, it help to assess whether business has earned profit or not in specific

period. Thus, firm comes to know regarding reducing or cutting down expenses so that more

income may be produced with much ease. The income statement for Raintree Ltd is produced

below-

Particulars Amount

Sales Revenue 107000

less: return on sales 2000

Ending Inventory 18000

Opening. Inventory 17000

Purchases 32000

Total Gross profit (GP) 74000

Less: Indirect expenditures

Depreciation 36000

distribution expenditures 22000

administrative expenses 28000

Less: Prepaid rent 3000

Add: Outstanding wages 2000

Operating income 85000

Less: Paid interest 11000

Less: Corporation tax 4000

Income from operations 7000

Net income 18000

A. Producing Income statement

Income statement is prepared with a view to analyze income generated and expenses

incurred in the particular year. It is also known as Profit and Loss statement as when income

exceeds expenses, then business earns profit and when earnings are lower than expenditures,

entity incurs loss. Thus, it help to assess whether business has earned profit or not in specific

period. Thus, firm comes to know regarding reducing or cutting down expenses so that more

income may be produced with much ease. The income statement for Raintree Ltd is produced

below-

Particulars Amount

Sales Revenue 107000

less: return on sales 2000

Ending Inventory 18000

Opening. Inventory 17000

Purchases 32000

Total Gross profit (GP) 74000

Less: Indirect expenditures

Depreciation 36000

distribution expenditures 22000

administrative expenses 28000

Less: Prepaid rent 3000

Add: Outstanding wages 2000

Operating income 85000

Less: Paid interest 11000

Less: Corporation tax 4000

Income from operations 7000

Net income 18000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

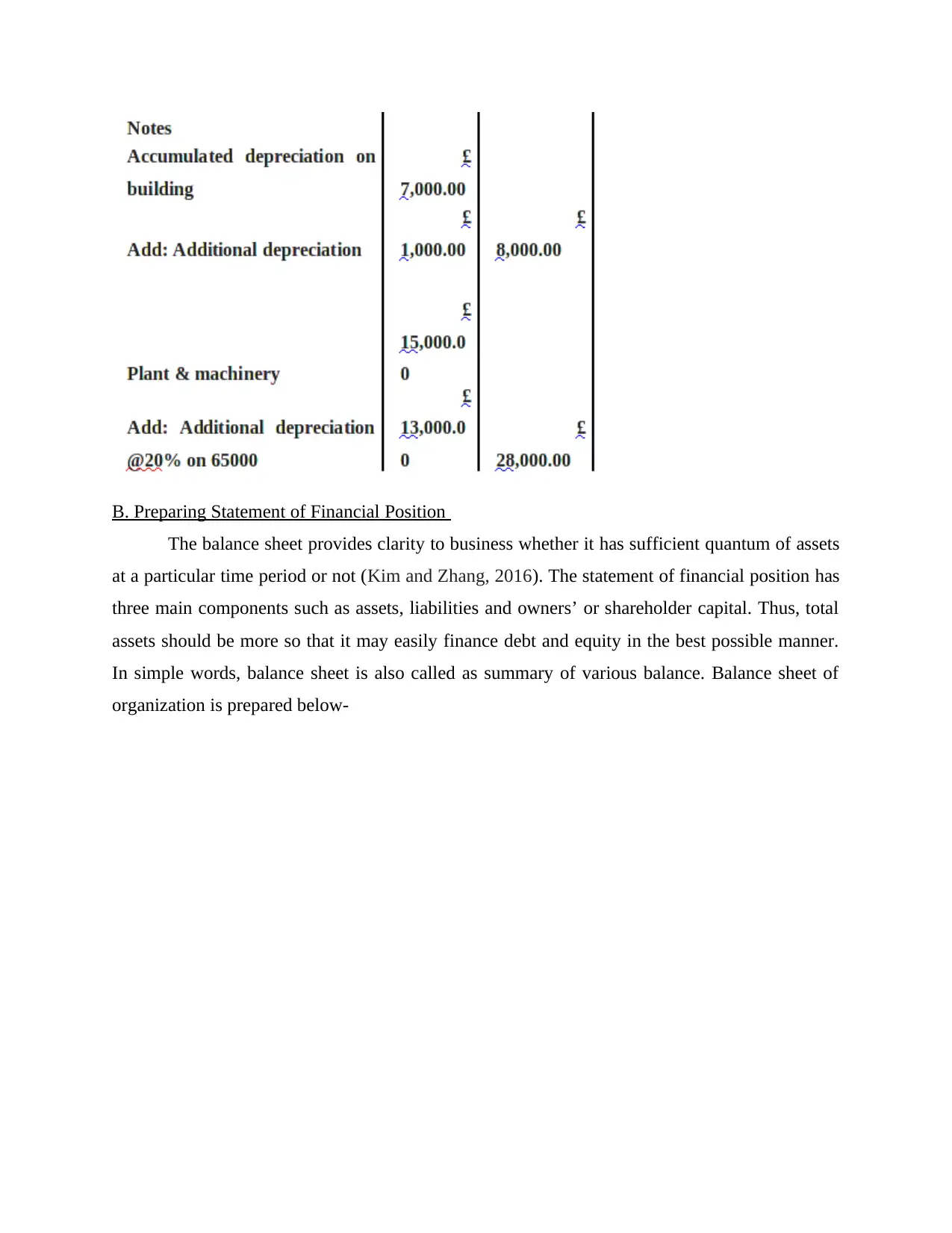

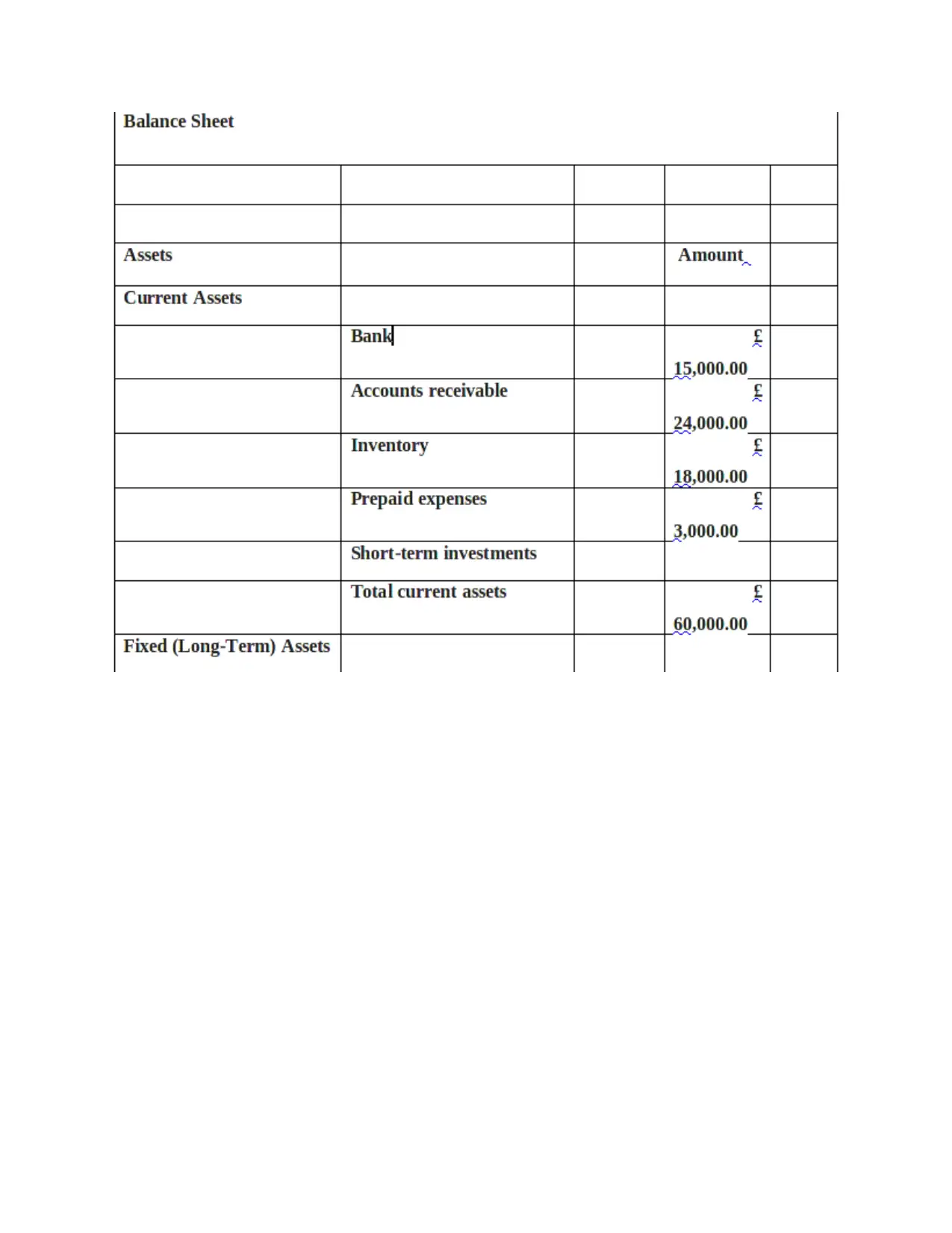

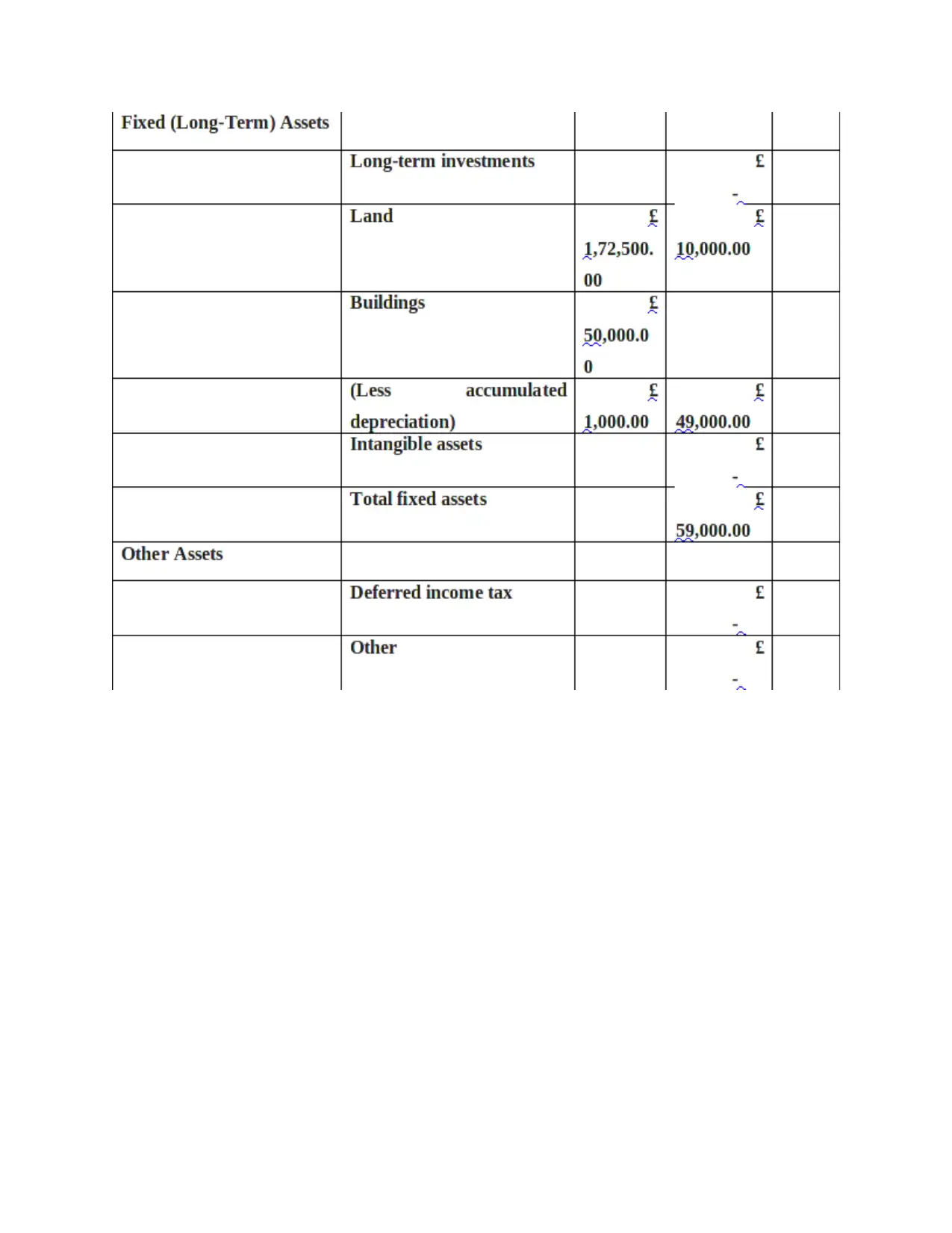

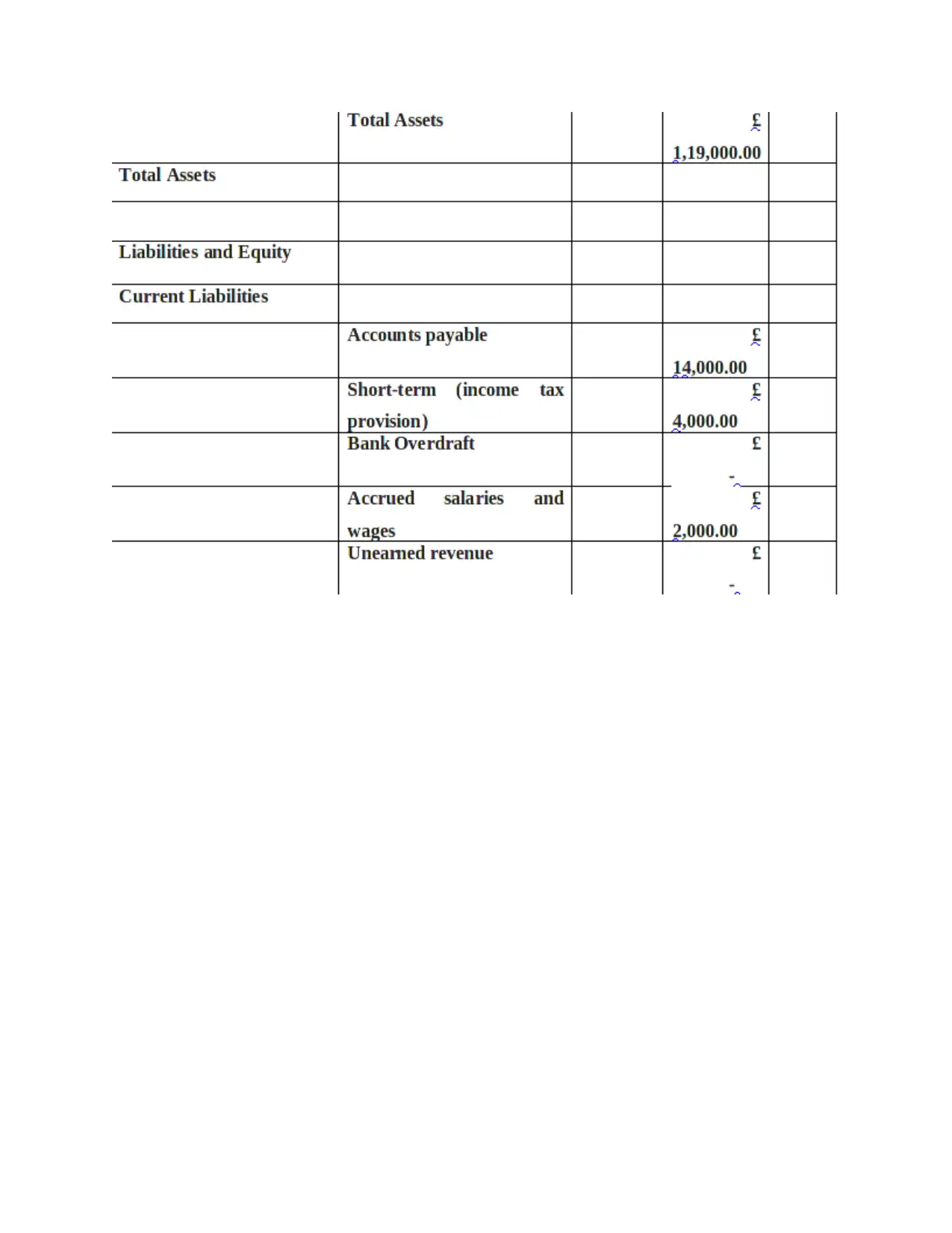

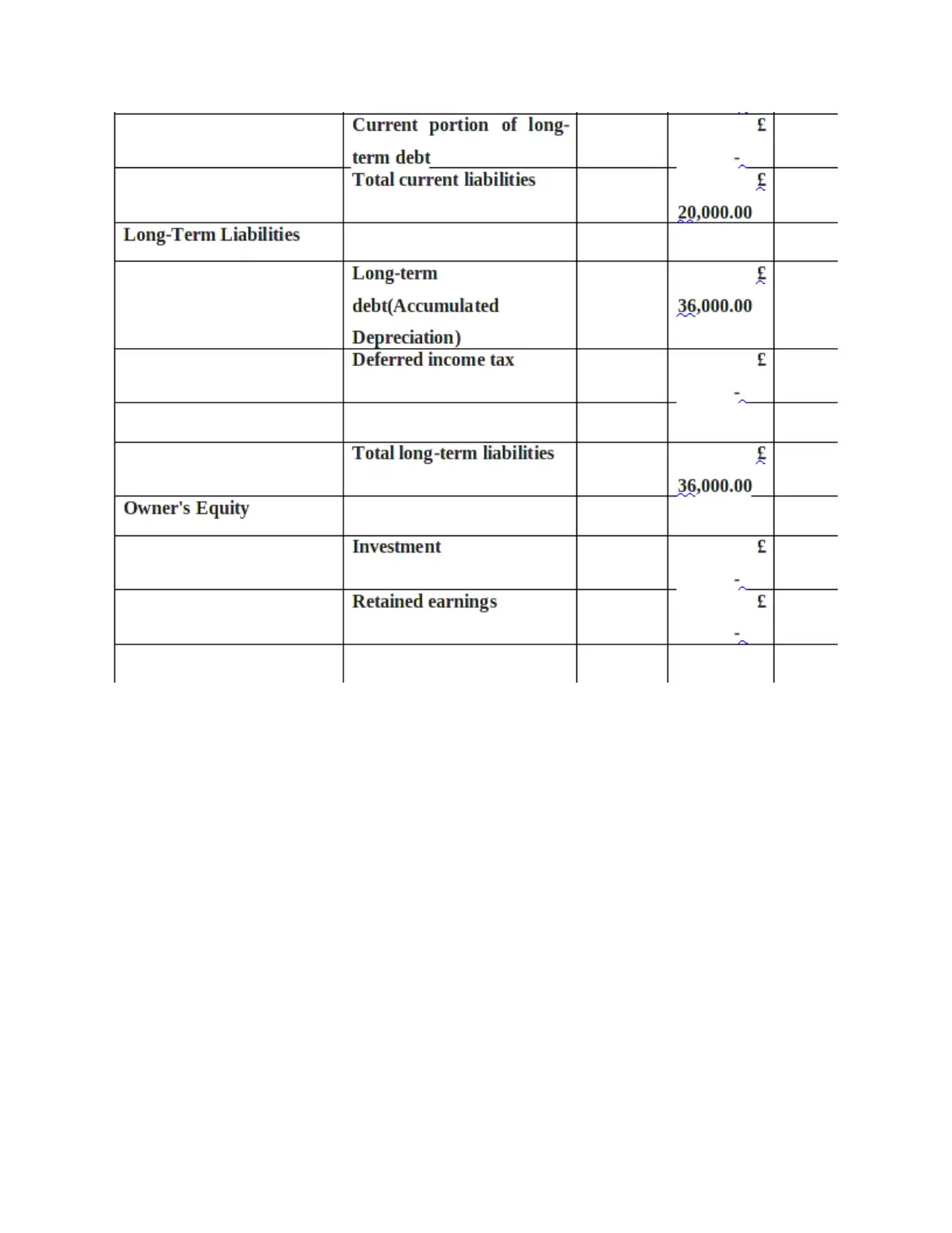

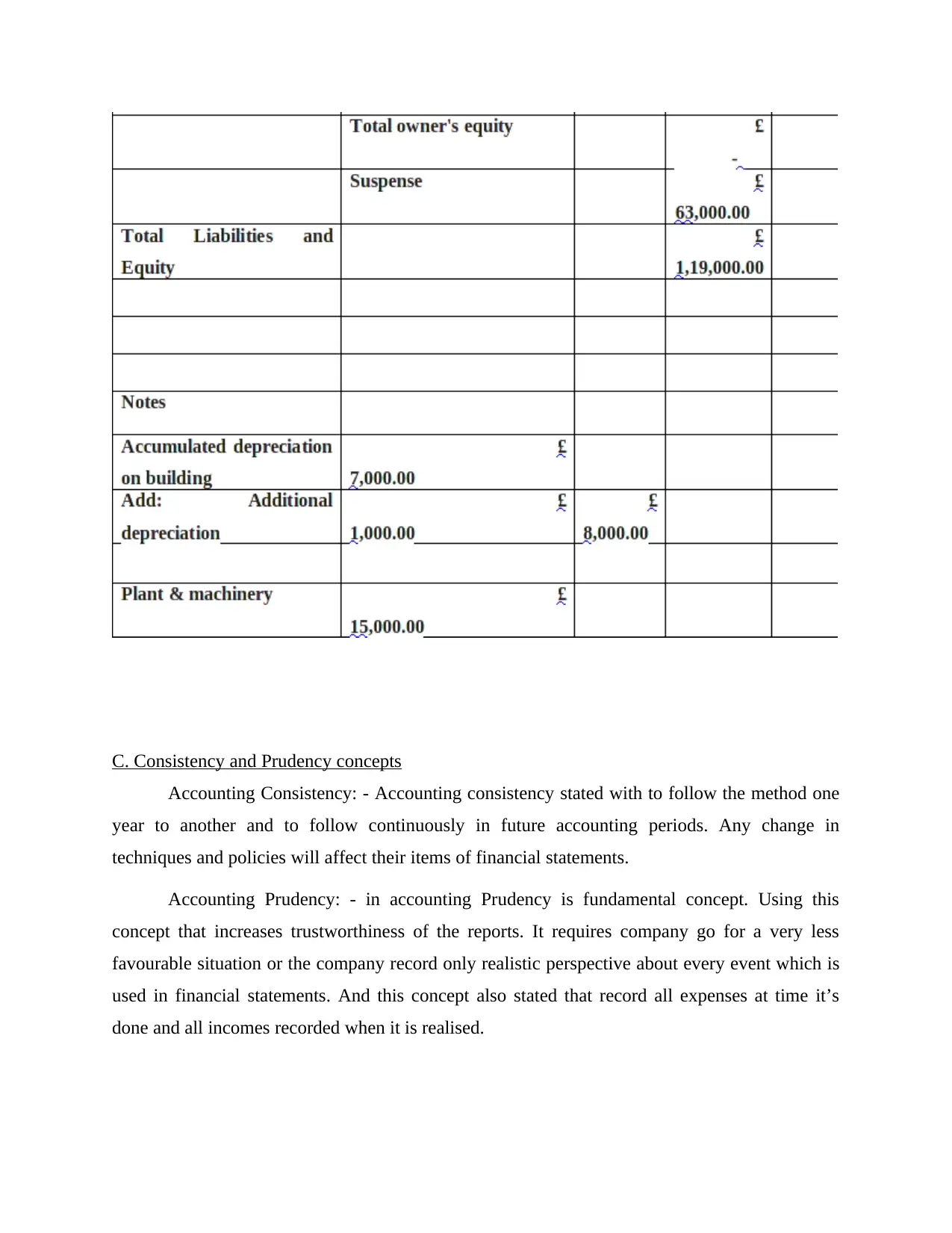

B. Preparing Statement of Financial Position

The balance sheet provides clarity to business whether it has sufficient quantum of assets

at a particular time period or not (Kim and Zhang, 2016). The statement of financial position has

three main components such as assets, liabilities and owners’ or shareholder capital. Thus, total

assets should be more so that it may easily finance debt and equity in the best possible manner.

In simple words, balance sheet is also called as summary of various balance. Balance sheet of

organization is prepared below-

The balance sheet provides clarity to business whether it has sufficient quantum of assets

at a particular time period or not (Kim and Zhang, 2016). The statement of financial position has

three main components such as assets, liabilities and owners’ or shareholder capital. Thus, total

assets should be more so that it may easily finance debt and equity in the best possible manner.

In simple words, balance sheet is also called as summary of various balance. Balance sheet of

organization is prepared below-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C. Consistency and Prudency concepts

Accounting Consistency: - Accounting consistency stated with to follow the method one

year to another and to follow continuously in future accounting periods. Any change in

techniques and policies will affect their items of financial statements.

Accounting Prudency: - in accounting Prudency is fundamental concept. Using this

concept that increases trustworthiness of the reports. It requires company go for a very less

favourable situation or the company record only realistic perspective about every event which is

used in financial statements. And this concept also stated that record all expenses at time it’s

done and all incomes recorded when it is realised.

Accounting Consistency: - Accounting consistency stated with to follow the method one

year to another and to follow continuously in future accounting periods. Any change in

techniques and policies will affect their items of financial statements.

Accounting Prudency: - in accounting Prudency is fundamental concept. Using this

concept that increases trustworthiness of the reports. It requires company go for a very less

favourable situation or the company record only realistic perspective about every event which is

used in financial statements. And this concept also stated that record all expenses at time it’s

done and all incomes recorded when it is realised.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

D. Outlining purpose of depreciation

If a company make a large purchase and its items shows in balance sheet as assets. Assets

is long term investment by the company. Depreciation is related to company fixed assets.

Because fixed assets is used in a year and depreciation expenses is lying on it. Vehicle and

equipment are most common assets which is depreciated. Depreciation is a reduction in value of

any assets. The main purpose of depreciation is to match the cost of an assets to the revenue

earned from using this assets (Balakrishnan, Watts and Zuo, 2016).

Types of depreciation:-

1. Straight line method

2. Written down value method

3. units of production

4. sum of year digits

Mostly used method of depreciation is Straight line method and written down value method. In

straight line method the same amount is used in calculating for each accounting period. The

formula is using for calculating depreciation in straight line method is

Depreciation amount= (cost of assets- salvage value)/useful life of assets in a year

For example: - Assets value=100000

Depreciation rate=20%

1st year =100000*20/100=20000

2nd year=100000*20/100=20000

In Written down value method depreciation is charged on reducing balance of an assets and a

fixed rate. The formula is used in

D=1-n/ r/c

r= residual value of assets

n= useful life assets in a year

c= cost of assets

If a company make a large purchase and its items shows in balance sheet as assets. Assets

is long term investment by the company. Depreciation is related to company fixed assets.

Because fixed assets is used in a year and depreciation expenses is lying on it. Vehicle and

equipment are most common assets which is depreciated. Depreciation is a reduction in value of

any assets. The main purpose of depreciation is to match the cost of an assets to the revenue

earned from using this assets (Balakrishnan, Watts and Zuo, 2016).

Types of depreciation:-

1. Straight line method

2. Written down value method

3. units of production

4. sum of year digits

Mostly used method of depreciation is Straight line method and written down value method. In

straight line method the same amount is used in calculating for each accounting period. The

formula is using for calculating depreciation in straight line method is

Depreciation amount= (cost of assets- salvage value)/useful life of assets in a year

For example: - Assets value=100000

Depreciation rate=20%

1st year =100000*20/100=20000

2nd year=100000*20/100=20000

In Written down value method depreciation is charged on reducing balance of an assets and a

fixed rate. The formula is used in

D=1-n/ r/c

r= residual value of assets

n= useful life assets in a year

c= cost of assets

1st year =100000*20/100=20000

2nd year =80000*20/100=16000

Written down value method is appropriate for calculating depreciation because we get the

residual amount of an assets year by year at the time of sold the assets we get the scrap value of

this assets. And, in straight line method there is no residual value so we don't get scrap value.

Client 4

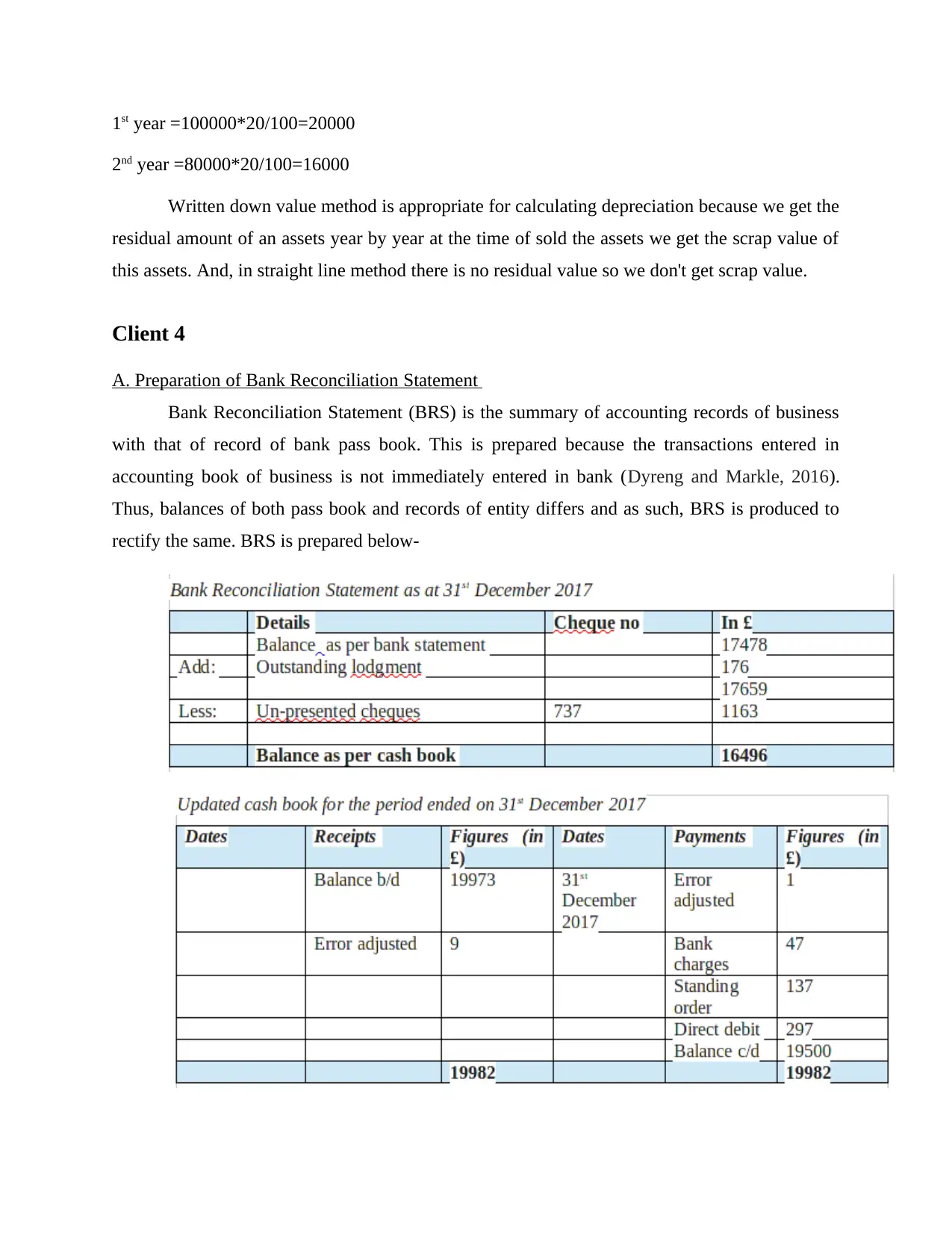

A. Preparation of Bank Reconciliation Statement

Bank Reconciliation Statement (BRS) is the summary of accounting records of business

with that of record of bank pass book. This is prepared because the transactions entered in

accounting book of business is not immediately entered in bank (Dyreng and Markle, 2016).

Thus, balances of both pass book and records of entity differs and as such, BRS is produced to

rectify the same. BRS is prepared below-

2nd year =80000*20/100=16000

Written down value method is appropriate for calculating depreciation because we get the

residual amount of an assets year by year at the time of sold the assets we get the scrap value of

this assets. And, in straight line method there is no residual value so we don't get scrap value.

Client 4

A. Preparation of Bank Reconciliation Statement

Bank Reconciliation Statement (BRS) is the summary of accounting records of business

with that of record of bank pass book. This is prepared because the transactions entered in

accounting book of business is not immediately entered in bank (Dyreng and Markle, 2016).

Thus, balances of both pass book and records of entity differs and as such, BRS is produced to

rectify the same. BRS is prepared below-

B. Causes of varying bank records with accounting books

The causes for varying business records with bank pass book are numerous. The balances

of bank and entity differs at the end of period. It includes cheque dishonored, deposits made but

not recorded in bank pass book. Interest charges and many other factors led to influence both

balances. Thus, through preparation of BRS, business may be able to analyze actual balance left

after carrying out expenditures.

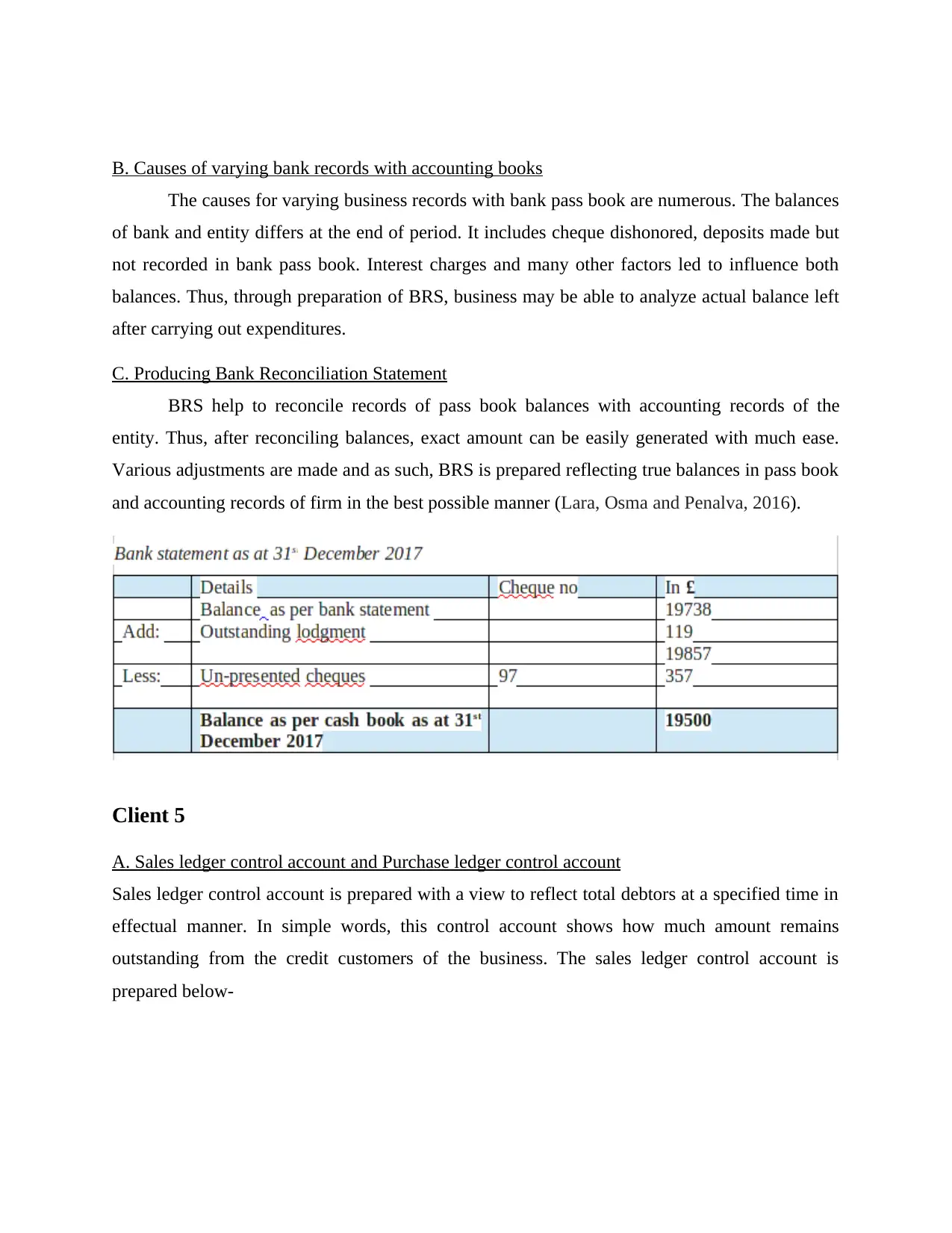

C. Producing Bank Reconciliation Statement

BRS help to reconcile records of pass book balances with accounting records of the

entity. Thus, after reconciling balances, exact amount can be easily generated with much ease.

Various adjustments are made and as such, BRS is prepared reflecting true balances in pass book

and accounting records of firm in the best possible manner (Lara, Osma and Penalva, 2016).

Client 5

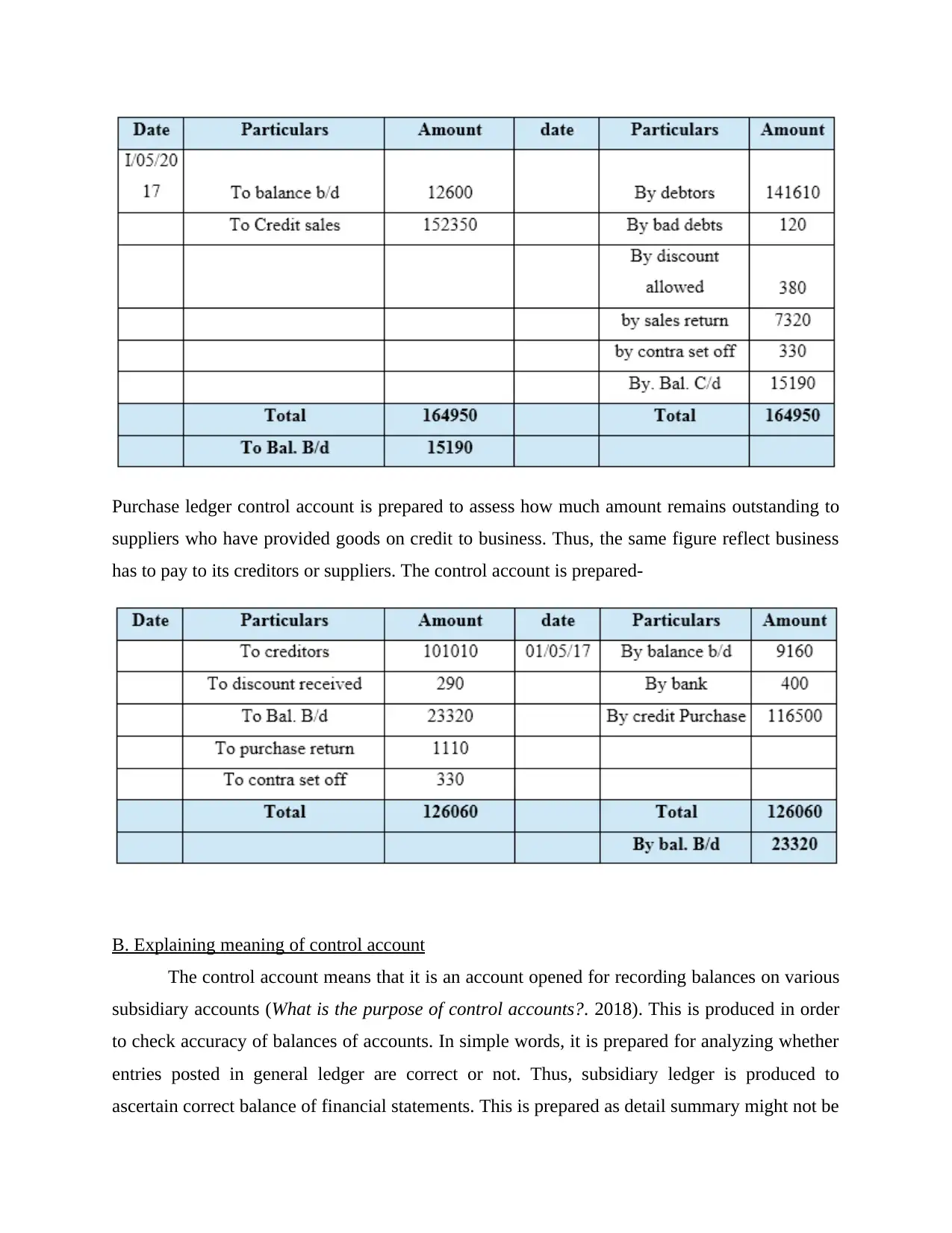

A. Sales ledger control account and Purchase ledger control account

Sales ledger control account is prepared with a view to reflect total debtors at a specified time in

effectual manner. In simple words, this control account shows how much amount remains

outstanding from the credit customers of the business. The sales ledger control account is

prepared below-

The causes for varying business records with bank pass book are numerous. The balances

of bank and entity differs at the end of period. It includes cheque dishonored, deposits made but

not recorded in bank pass book. Interest charges and many other factors led to influence both

balances. Thus, through preparation of BRS, business may be able to analyze actual balance left

after carrying out expenditures.

C. Producing Bank Reconciliation Statement

BRS help to reconcile records of pass book balances with accounting records of the

entity. Thus, after reconciling balances, exact amount can be easily generated with much ease.

Various adjustments are made and as such, BRS is prepared reflecting true balances in pass book

and accounting records of firm in the best possible manner (Lara, Osma and Penalva, 2016).

Client 5

A. Sales ledger control account and Purchase ledger control account

Sales ledger control account is prepared with a view to reflect total debtors at a specified time in

effectual manner. In simple words, this control account shows how much amount remains

outstanding from the credit customers of the business. The sales ledger control account is

prepared below-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Purchase ledger control account is prepared to assess how much amount remains outstanding to

suppliers who have provided goods on credit to business. Thus, the same figure reflect business

has to pay to its creditors or suppliers. The control account is prepared-

B. Explaining meaning of control account

The control account means that it is an account opened for recording balances on various

subsidiary accounts (What is the purpose of control accounts?. 2018). This is produced in order

to check accuracy of balances of accounts. In simple words, it is prepared for analyzing whether

entries posted in general ledger are correct or not. Thus, subsidiary ledger is produced to

ascertain correct balance of financial statements. This is prepared as detail summary might not be

suppliers who have provided goods on credit to business. Thus, the same figure reflect business

has to pay to its creditors or suppliers. The control account is prepared-

B. Explaining meaning of control account

The control account means that it is an account opened for recording balances on various

subsidiary accounts (What is the purpose of control accounts?. 2018). This is produced in order

to check accuracy of balances of accounts. In simple words, it is prepared for analyzing whether

entries posted in general ledger are correct or not. Thus, subsidiary ledger is produced to

ascertain correct balance of financial statements. This is prepared as detail summary might not be

provided in accounts receivable or payables and as such, firm is able to ascertain accurate

balances.

Client 6

A. Meaning and features of suspense account

Suspense account: - Suspense account is an account which is open when in balance sheet the

proper amount could not be determined at the time that the transaction was recorded. The amount

which is shows in suspense account its only temporary basis. And after the amount should be

investigated and posted to the correct amount (Legenzova, 2016).

Features of suspense account:

It is used on a temporary basis

it is closed when the transaction should be match and correct entry should be posted

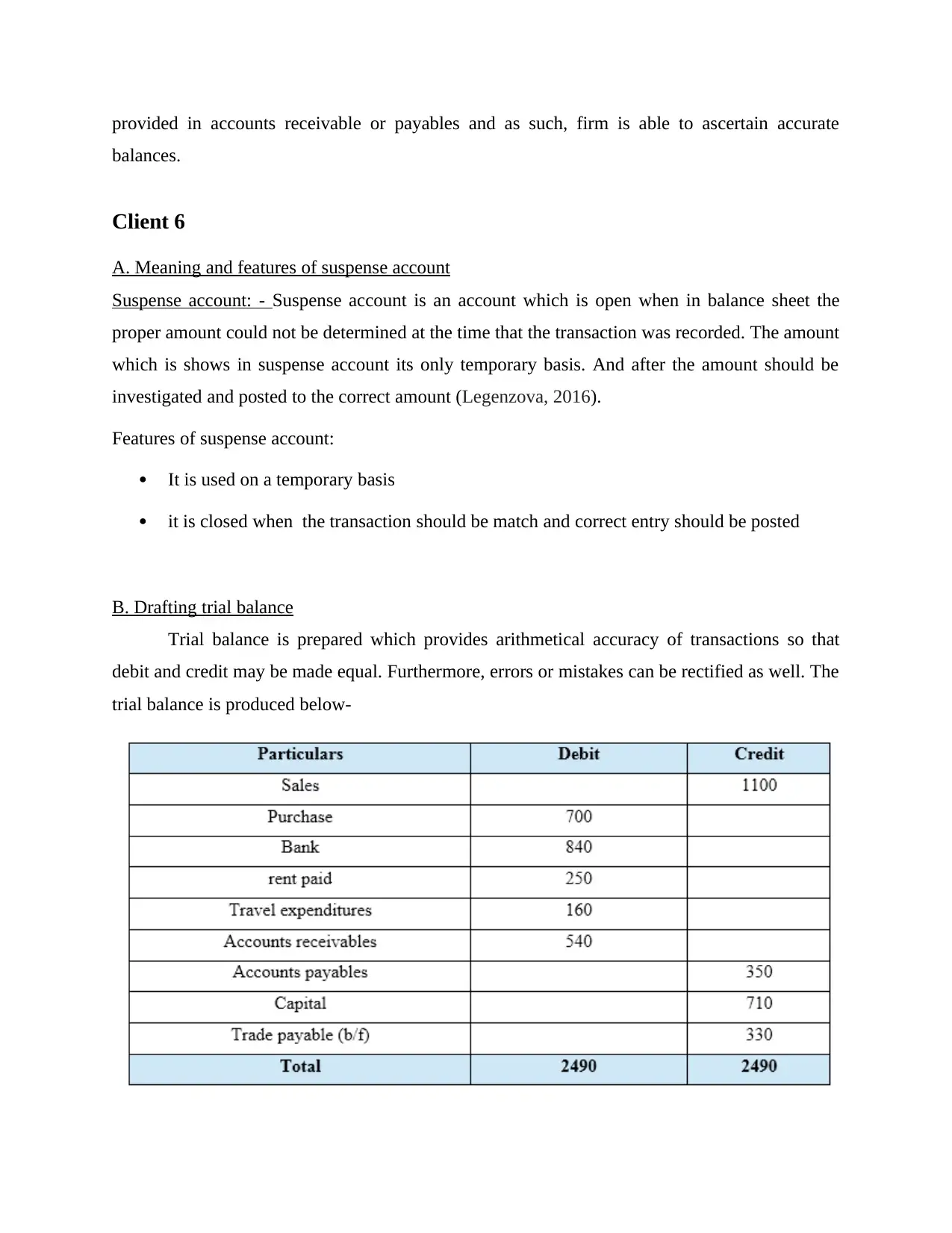

B. Drafting trial balance

Trial balance is prepared which provides arithmetical accuracy of transactions so that

debit and credit may be made equal. Furthermore, errors or mistakes can be rectified as well. The

trial balance is produced below-

balances.

Client 6

A. Meaning and features of suspense account

Suspense account: - Suspense account is an account which is open when in balance sheet the

proper amount could not be determined at the time that the transaction was recorded. The amount

which is shows in suspense account its only temporary basis. And after the amount should be

investigated and posted to the correct amount (Legenzova, 2016).

Features of suspense account:

It is used on a temporary basis

it is closed when the transaction should be match and correct entry should be posted

B. Drafting trial balance

Trial balance is prepared which provides arithmetical accuracy of transactions so that

debit and credit may be made equal. Furthermore, errors or mistakes can be rectified as well. The

trial balance is produced below-

C. Preparing journal entries

D. Differentiating suspense and clearing account

Difference between suspense account and clearing account:

Basis of difference Suspense Account Clearing account

Opening of account Suspense account occur when

the balance sheet not match.

Clearing account is to hold the

transaction for later posting

Closed account When uncertainties are

resolved the suspense account

is closed.

This account is used to record

utility expenses which is

closed in monthly.

CONCLUSION

Hereby it can be concluded that accounting plays important role in the business. The

financial statements are prepared such as income statement and balance sheet from the

D. Differentiating suspense and clearing account

Difference between suspense account and clearing account:

Basis of difference Suspense Account Clearing account

Opening of account Suspense account occur when

the balance sheet not match.

Clearing account is to hold the

transaction for later posting

Closed account When uncertainties are

resolved the suspense account

is closed.

This account is used to record

utility expenses which is

closed in monthly.

CONCLUSION

Hereby it can be concluded that accounting plays important role in the business. The

financial statements are prepared such as income statement and balance sheet from the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

accounting records maintained in the books of accounts. Moreover, financial accounting is quite

useful as all the transactions entered in and as such, business is able to prepare final accounts

with much ease.. The accounting concepts and rules also help accountants to prepare correct

financials.

useful as all the transactions entered in and as such, business is able to prepare final accounts

with much ease.. The accounting concepts and rules also help accountants to prepare correct

financials.

REFERENCES

Books and Journals

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting. 43(5-6). pp.513-542.

Christensen, H. B., Nikolaev, V. V. and WITTENBERG‐MOERMAN, R.E.G.I.N.A., 2016.

Accounting information in financial contracting: The incomplete contract theory

perspective. Journal of accounting research. 54(2). pp.397-435.

Dyreng, S. D. and Markle, K. S., 2016. The effect of financial constraints on income shifting by

US multinationals. The Accounting Review. 91(6). pp.1601-1627.

EBRAHIMI, M., TALEBNIA, G.A., VAKILIFARD, H. and NIKOUMARAM, H., 2017. THE

EXPLAINING WORKING CAPITAL MANAGEMENT STRATEGY BY MARKOV

CHAIN MONTE CARLO.

KHAJAVI, S. and EBRAHIMI, M., 2017. MODELLING THE EFFECTIVE VARIABLES FOR

OF FINANCIAL STATEMENTS FRAUD DETECTION USING DATA MINING

TECHNIQUES.

Kim, J. B. and Zhang, L., 2016. Accounting conservatism and stock price crash risk: Firm‐level

evidence. Contemporary Accounting Research. 33(1). pp.412-441.

Lara, J.M.G., Osma, B. G. and Penalva, F., 2016. Accounting conservatism and firm investment

efficiency. Journal of Accounting and Economics. 61(1). pp.221-238.

Legenzova, R., 2016. A concept of accounting quality from accounting harmonisation

perspective. Economics and Business. 28(1). pp.33-37.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion

to Behavioural Accounting Research (pp. 42-54). Routledge.

Books and Journals

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting. 43(5-6). pp.513-542.

Christensen, H. B., Nikolaev, V. V. and WITTENBERG‐MOERMAN, R.E.G.I.N.A., 2016.

Accounting information in financial contracting: The incomplete contract theory

perspective. Journal of accounting research. 54(2). pp.397-435.

Dyreng, S. D. and Markle, K. S., 2016. The effect of financial constraints on income shifting by

US multinationals. The Accounting Review. 91(6). pp.1601-1627.

EBRAHIMI, M., TALEBNIA, G.A., VAKILIFARD, H. and NIKOUMARAM, H., 2017. THE

EXPLAINING WORKING CAPITAL MANAGEMENT STRATEGY BY MARKOV

CHAIN MONTE CARLO.

KHAJAVI, S. and EBRAHIMI, M., 2017. MODELLING THE EFFECTIVE VARIABLES FOR

OF FINANCIAL STATEMENTS FRAUD DETECTION USING DATA MINING

TECHNIQUES.

Kim, J. B. and Zhang, L., 2016. Accounting conservatism and stock price crash risk: Firm‐level

evidence. Contemporary Accounting Research. 33(1). pp.412-441.

Lara, J.M.G., Osma, B. G. and Penalva, F., 2016. Accounting conservatism and firm investment

efficiency. Journal of Accounting and Economics. 61(1). pp.221-238.

Legenzova, R., 2016. A concept of accounting quality from accounting harmonisation

perspective. Economics and Business. 28(1). pp.33-37.

Libby, R., 2017. Accounting and human information processing. In The Routledge Companion

to Behavioural Accounting Research (pp. 42-54). Routledge.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches. (1). pp.60-64.

Warren, C. S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Online

What is the purpose of control accounts?. 2018 [Online] Available Through:

<https://www.accountingcoach.com/blog/accounts-receivable-control-account-subsidiary-

ledger>

and assessment" for bank financial accounting. Modern European Researches. (1). pp.60-64.

Warren, C. S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Online

What is the purpose of control accounts?. 2018 [Online] Available Through:

<https://www.accountingcoach.com/blog/accounts-receivable-control-account-subsidiary-

ledger>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.