Financial Accounting

VerifiedAdded on 2023/01/11

|19

|4404

|22

AI Summary

\nI want to ask if these 3500 words include calculations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Formulation of trial balance as on 31st March 2020..............................................................1

1.2 Recording business transactions in the books of Catherine...................................................3

1.3 Applying the trial balance figures and showing the statement in which, they will be shows

.....................................................................................................................................................7

TASK 2............................................................................................................................................8

2.1 Description of the financial accounting statements prepared by business entities and

discussion of the type of information presented through each....................................................8

2.2 Preparation of statement of profit and loss in accordance with International Accounting

Standards for Italian Wines Ltd. As on 31st March 2020..........................................................10

2.3 Preparation of statement of financial position in accordance with International Accounting

Standards for Italian Wines Ltd. As on 31st March 2020..........................................................11

2.4 Calculation of different ratios..............................................................................................11

TASK 3..........................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Formulation of trial balance as on 31st March 2020..............................................................1

1.2 Recording business transactions in the books of Catherine...................................................3

1.3 Applying the trial balance figures and showing the statement in which, they will be shows

.....................................................................................................................................................7

TASK 2............................................................................................................................................8

2.1 Description of the financial accounting statements prepared by business entities and

discussion of the type of information presented through each....................................................8

2.2 Preparation of statement of profit and loss in accordance with International Accounting

Standards for Italian Wines Ltd. As on 31st March 2020..........................................................10

2.3 Preparation of statement of financial position in accordance with International Accounting

Standards for Italian Wines Ltd. As on 31st March 2020..........................................................11

2.4 Calculation of different ratios..............................................................................................11

TASK 3..........................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial accounting can be defined as the process of formulating final accounts in

appropriate manner so that actual position of the company could be determined. The accounts

that are generated with the help of it are profit and loss account, balance sheet and cash flow

statement (Biddle, Ma and Song, 2019). It is very important for all the organisation to make sure

that they are able to conduct financial accounting every year as it leaves impact upon

stakeholders. On the other hand, all the results that are created with the help of it, are assessed by

shareholders and investors so that they can determine that entity will be able to provide them

good returns or not. If an enterprise will not be able to deliver appropriate information of

position and performance of business to the external as well as internal parties then it may lead

the business towards failure. It can also affect the market image as well as the long-term

objectives such as higher profits, revenues etc. Main aim of this assignment is to understand the

way in which financial accounting should be conducted and the key factors which should be

focused to generate final accounts. For this purpose, different topics are covered in this report.

These are formulation of trial balance, application of double entry system and generation of

ledgers, creating financial statements on the basis of trial balance and the notes that are shows

below it. Apart from this, bank reconciliation statement and key elements that are related to it are

also discussed in this project.

TASK 1

1.1 Formulation of trial balance as on 31st March 2020

Trial balance is a statement which is generated after the formulation of different types of

ledger accounts. While creating it, it is very important or the accounting professionals to make

sure that they are able to understand all the business transactions properly. If they are not aware

of their nature then it may result in wrong formulation of trial balance (Dauderies and Annand,

2019). There are several types of business transactions which are as follows:

Sales: When an entity or individual sale the goods which are used for carrying out

operations then it is known as sales. The balance of it is considered as credit as all the receipts

are recorded in credit side. It is shown in the profit and loss account of the financial statements.

Purchase: When an enterprise buys material or goods to perform the operations then it is

known as purchase. The balance of it is debit as it results in outflow of monetary resources and

1

Financial accounting can be defined as the process of formulating final accounts in

appropriate manner so that actual position of the company could be determined. The accounts

that are generated with the help of it are profit and loss account, balance sheet and cash flow

statement (Biddle, Ma and Song, 2019). It is very important for all the organisation to make sure

that they are able to conduct financial accounting every year as it leaves impact upon

stakeholders. On the other hand, all the results that are created with the help of it, are assessed by

shareholders and investors so that they can determine that entity will be able to provide them

good returns or not. If an enterprise will not be able to deliver appropriate information of

position and performance of business to the external as well as internal parties then it may lead

the business towards failure. It can also affect the market image as well as the long-term

objectives such as higher profits, revenues etc. Main aim of this assignment is to understand the

way in which financial accounting should be conducted and the key factors which should be

focused to generate final accounts. For this purpose, different topics are covered in this report.

These are formulation of trial balance, application of double entry system and generation of

ledgers, creating financial statements on the basis of trial balance and the notes that are shows

below it. Apart from this, bank reconciliation statement and key elements that are related to it are

also discussed in this project.

TASK 1

1.1 Formulation of trial balance as on 31st March 2020

Trial balance is a statement which is generated after the formulation of different types of

ledger accounts. While creating it, it is very important or the accounting professionals to make

sure that they are able to understand all the business transactions properly. If they are not aware

of their nature then it may result in wrong formulation of trial balance (Dauderies and Annand,

2019). There are several types of business transactions which are as follows:

Sales: When an entity or individual sale the goods which are used for carrying out

operations then it is known as sales. The balance of it is considered as credit as all the receipts

are recorded in credit side. It is shown in the profit and loss account of the financial statements.

Purchase: When an enterprise buys material or goods to perform the operations then it is

known as purchase. The balance of it is debit as it results in outflow of monetary resources and

1

every thing which goes out of the business or the expenses have debit balance. It is reflected in

the profit and loss account of final accounts (Flesher, Flesher and Previts, 2018).

Receipts: When a business entity sale its goods on credit then the amount of it will be

recovered after a few days or months on a due date. The amount which is related to the credit

sales then it will be considered as receipts for the business. If the amount of it is not received by

the organisation then it will be treated as bad debts.

Payments: When an organisation purchases stock on credit then the amount which will

be required to be paid by the business after the due date will be considered as the payment. It is

reflected in the liabilities side of balance sheet which is a financial statement (Hanif and

Mukherjee, 2018).

There are various types of regulations which are applied to the financial accounting. All

of them are as follows:

Accounting standards: These are the main regulations that are required to be followed

by all the organisations in order to generate financial statements in proper manner. There are

various types of IAS and IFRS which are required to be complied in order to reduce possibility

of legal actions.

Accounting principles: While conducting financial accounting it is very important for

all the accounting professionals to make sure that they are following all the principles as it is

essential to generate the records (Kimmel, Weygandt and Kieso, 2018).

Accounting concepts: For all the business entities IAS have developed different types of

accounting concepts, such as going concern, separate business entity etc. In order to formulate

final accounts properly all of them are required to be followed properly.

There are various types of manual and electronic systems to formulate trial balance. In

earlier years manual systems were used by the companies but in modern era different types of

software are used to generate the trial balance. One of them is Tally.

Trial balance helps to understand the concept of errors. When it is generated and the total

of debit and credit side is not matched then the balanced amount shows that the accounting

professionals have made mistakes to generate the accounts (Maynard, 2017). If the total of both

the sides is matched then it is considered that no error was made while formulating it. Trial

balance is very important for all the organisations as it helps to analyse the errors which were

made while generating journals or ledgers.

2

the profit and loss account of final accounts (Flesher, Flesher and Previts, 2018).

Receipts: When a business entity sale its goods on credit then the amount of it will be

recovered after a few days or months on a due date. The amount which is related to the credit

sales then it will be considered as receipts for the business. If the amount of it is not received by

the organisation then it will be treated as bad debts.

Payments: When an organisation purchases stock on credit then the amount which will

be required to be paid by the business after the due date will be considered as the payment. It is

reflected in the liabilities side of balance sheet which is a financial statement (Hanif and

Mukherjee, 2018).

There are various types of regulations which are applied to the financial accounting. All

of them are as follows:

Accounting standards: These are the main regulations that are required to be followed

by all the organisations in order to generate financial statements in proper manner. There are

various types of IAS and IFRS which are required to be complied in order to reduce possibility

of legal actions.

Accounting principles: While conducting financial accounting it is very important for

all the accounting professionals to make sure that they are following all the principles as it is

essential to generate the records (Kimmel, Weygandt and Kieso, 2018).

Accounting concepts: For all the business entities IAS have developed different types of

accounting concepts, such as going concern, separate business entity etc. In order to formulate

final accounts properly all of them are required to be followed properly.

There are various types of manual and electronic systems to formulate trial balance. In

earlier years manual systems were used by the companies but in modern era different types of

software are used to generate the trial balance. One of them is Tally.

Trial balance helps to understand the concept of errors. When it is generated and the total

of debit and credit side is not matched then the balanced amount shows that the accounting

professionals have made mistakes to generate the accounts (Maynard, 2017). If the total of both

the sides is matched then it is considered that no error was made while formulating it. Trial

balance is very important for all the organisations as it helps to analyse the errors which were

made while generating journals or ledgers.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

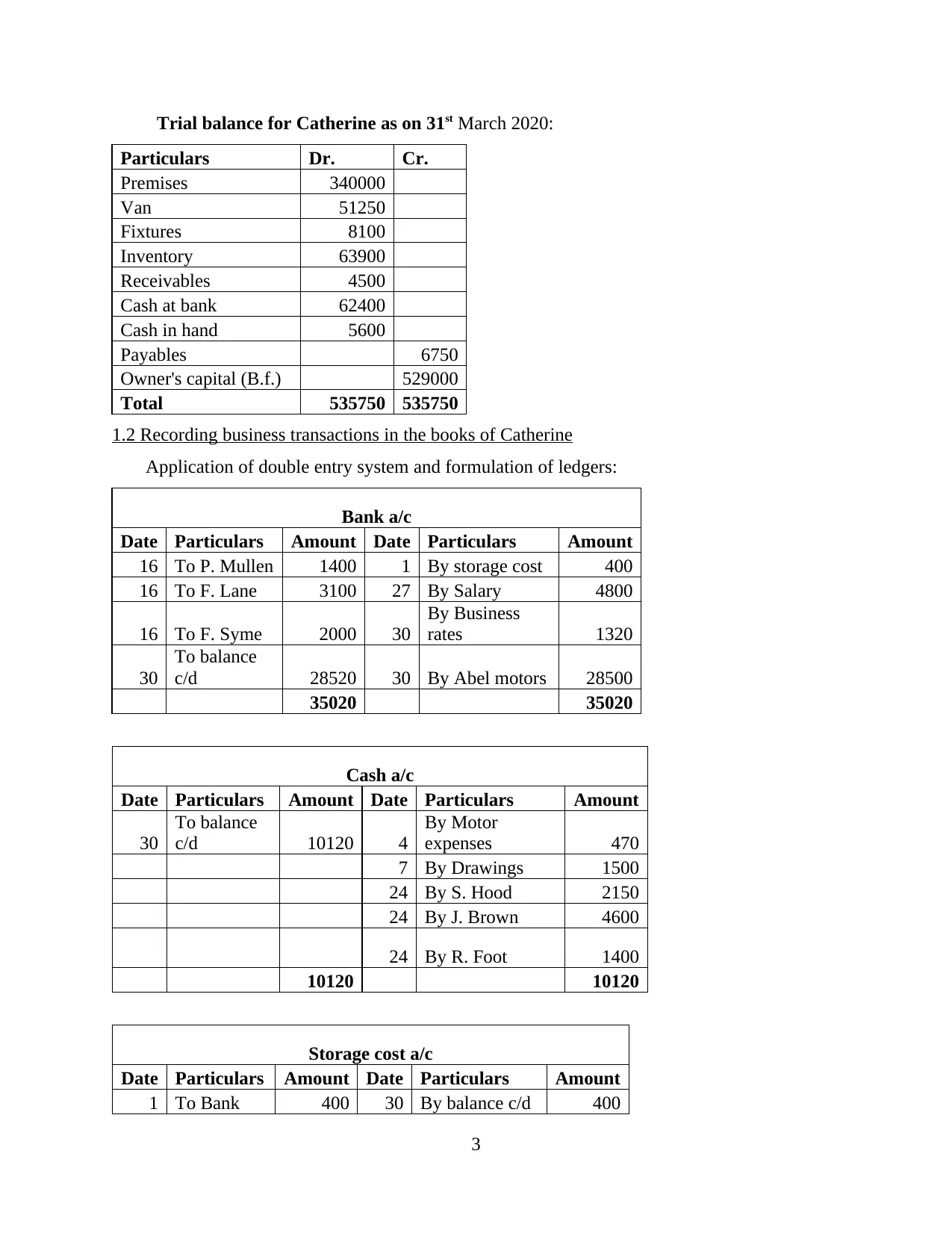

Trial balance for Catherine as on 31st March 2020:

Particulars Dr. Cr.

Premises 340000

Van 51250

Fixtures 8100

Inventory 63900

Receivables 4500

Cash at bank 62400

Cash in hand 5600

Payables 6750

Owner's capital (B.f.) 529000

Total 535750 535750

1.2 Recording business transactions in the books of Catherine

Application of double entry system and formulation of ledgers:

Bank a/c

Date Particulars Amount Date Particulars Amount

16 To P. Mullen 1400 1 By storage cost 400

16 To F. Lane 3100 27 By Salary 4800

16 To F. Syme 2000 30

By Business

rates 1320

30

To balance

c/d 28520 30 By Abel motors 28500

35020 35020

Cash a/c

Date Particulars Amount Date Particulars Amount

30

To balance

c/d 10120 4

By Motor

expenses 470

7 By Drawings 1500

24 By S. Hood 2150

24 By J. Brown 4600

24 By R. Foot 1400

10120 10120

Storage cost a/c

Date Particulars Amount Date Particulars Amount

1 To Bank 400 30 By balance c/d 400

3

Particulars Dr. Cr.

Premises 340000

Van 51250

Fixtures 8100

Inventory 63900

Receivables 4500

Cash at bank 62400

Cash in hand 5600

Payables 6750

Owner's capital (B.f.) 529000

Total 535750 535750

1.2 Recording business transactions in the books of Catherine

Application of double entry system and formulation of ledgers:

Bank a/c

Date Particulars Amount Date Particulars Amount

16 To P. Mullen 1400 1 By storage cost 400

16 To F. Lane 3100 27 By Salary 4800

16 To F. Syme 2000 30

By Business

rates 1320

30

To balance

c/d 28520 30 By Abel motors 28500

35020 35020

Cash a/c

Date Particulars Amount Date Particulars Amount

30

To balance

c/d 10120 4

By Motor

expenses 470

7 By Drawings 1500

24 By S. Hood 2150

24 By J. Brown 4600

24 By R. Foot 1400

10120 10120

Storage cost a/c

Date Particulars Amount Date Particulars Amount

1 To Bank 400 30 By balance c/d 400

3

400 400

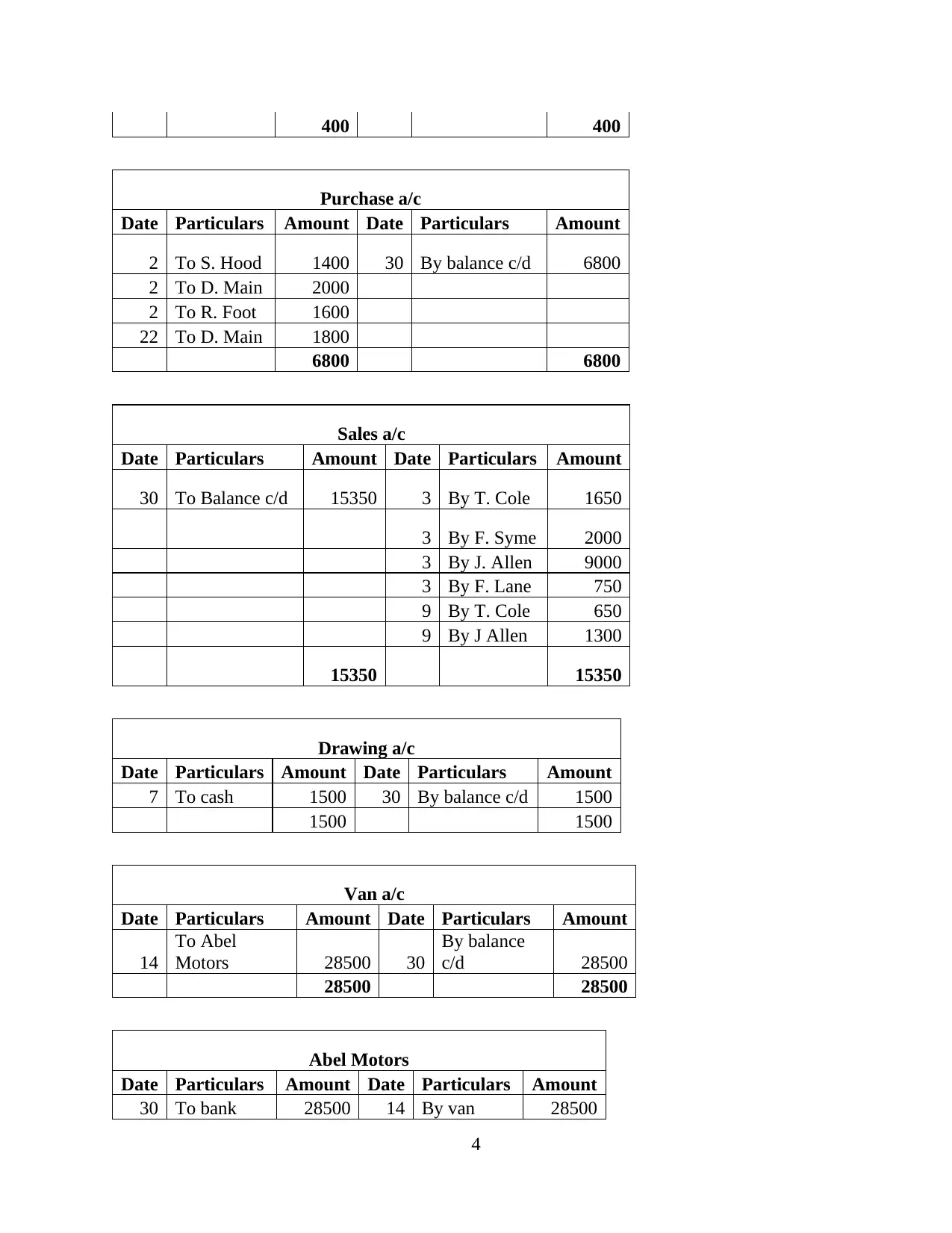

Purchase a/c

Date Particulars Amount Date Particulars Amount

2 To S. Hood 1400 30 By balance c/d 6800

2 To D. Main 2000

2 To R. Foot 1600

22 To D. Main 1800

6800 6800

Sales a/c

Date Particulars Amount Date Particulars Amount

30 To Balance c/d 15350 3 By T. Cole 1650

3 By F. Syme 2000

3 By J. Allen 9000

3 By F. Lane 750

9 By T. Cole 650

9 By J Allen 1300

15350 15350

Drawing a/c

Date Particulars Amount Date Particulars Amount

7 To cash 1500 30 By balance c/d 1500

1500 1500

Van a/c

Date Particulars Amount Date Particulars Amount

14

To Abel

Motors 28500 30

By balance

c/d 28500

28500 28500

Abel Motors

Date Particulars Amount Date Particulars Amount

30 To bank 28500 14 By van 28500

4

Purchase a/c

Date Particulars Amount Date Particulars Amount

2 To S. Hood 1400 30 By balance c/d 6800

2 To D. Main 2000

2 To R. Foot 1600

22 To D. Main 1800

6800 6800

Sales a/c

Date Particulars Amount Date Particulars Amount

30 To Balance c/d 15350 3 By T. Cole 1650

3 By F. Syme 2000

3 By J. Allen 9000

3 By F. Lane 750

9 By T. Cole 650

9 By J Allen 1300

15350 15350

Drawing a/c

Date Particulars Amount Date Particulars Amount

7 To cash 1500 30 By balance c/d 1500

1500 1500

Van a/c

Date Particulars Amount Date Particulars Amount

14

To Abel

Motors 28500 30

By balance

c/d 28500

28500 28500

Abel Motors

Date Particulars Amount Date Particulars Amount

30 To bank 28500 14 By van 28500

4

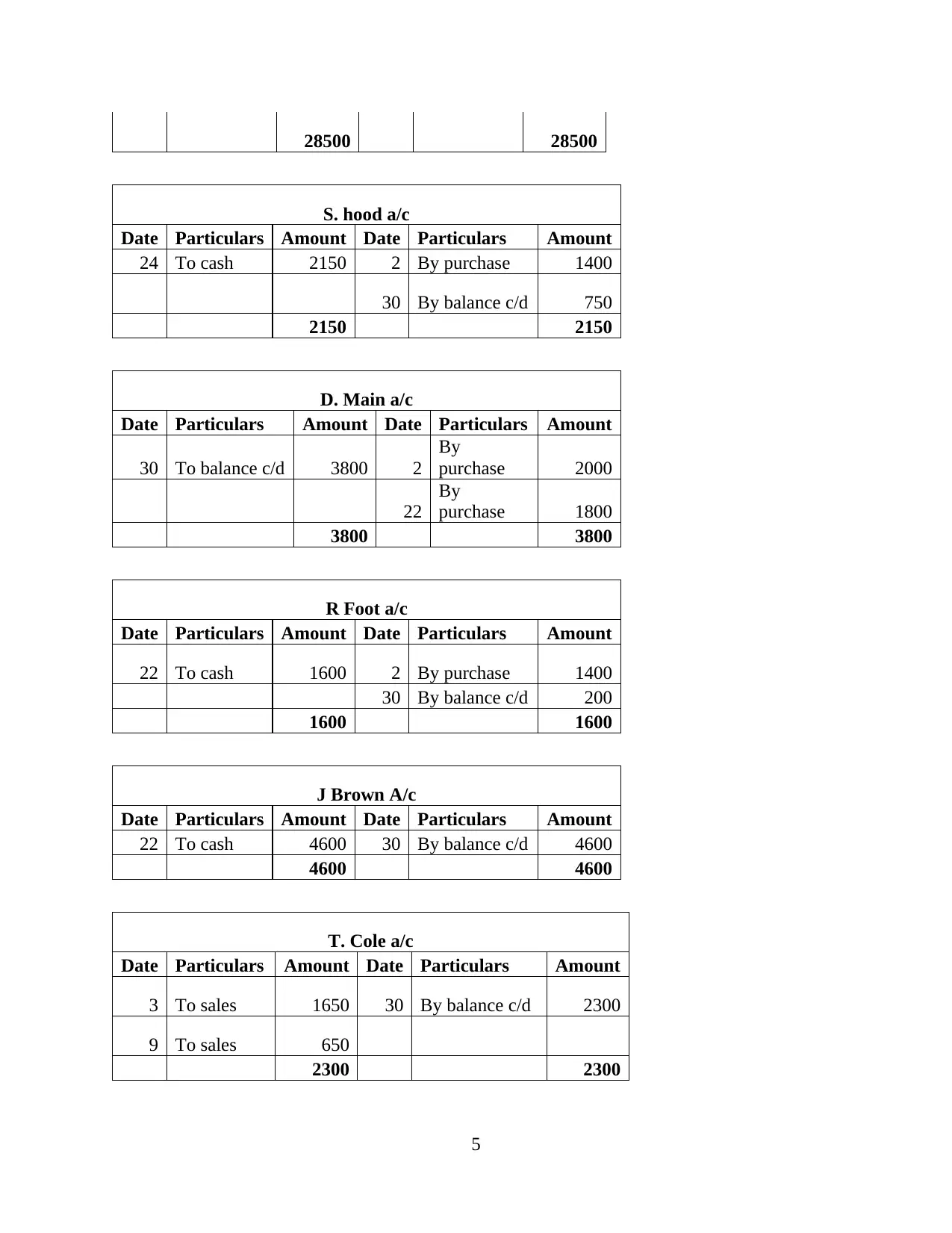

28500 28500

S. hood a/c

Date Particulars Amount Date Particulars Amount

24 To cash 2150 2 By purchase 1400

30 By balance c/d 750

2150 2150

D. Main a/c

Date Particulars Amount Date Particulars Amount

30 To balance c/d 3800 2

By

purchase 2000

22

By

purchase 1800

3800 3800

R Foot a/c

Date Particulars Amount Date Particulars Amount

22 To cash 1600 2 By purchase 1400

30 By balance c/d 200

1600 1600

J Brown A/c

Date Particulars Amount Date Particulars Amount

22 To cash 4600 30 By balance c/d 4600

4600 4600

T. Cole a/c

Date Particulars Amount Date Particulars Amount

3 To sales 1650 30 By balance c/d 2300

9 To sales 650

2300 2300

5

S. hood a/c

Date Particulars Amount Date Particulars Amount

24 To cash 2150 2 By purchase 1400

30 By balance c/d 750

2150 2150

D. Main a/c

Date Particulars Amount Date Particulars Amount

30 To balance c/d 3800 2

By

purchase 2000

22

By

purchase 1800

3800 3800

R Foot a/c

Date Particulars Amount Date Particulars Amount

22 To cash 1600 2 By purchase 1400

30 By balance c/d 200

1600 1600

J Brown A/c

Date Particulars Amount Date Particulars Amount

22 To cash 4600 30 By balance c/d 4600

4600 4600

T. Cole a/c

Date Particulars Amount Date Particulars Amount

3 To sales 1650 30 By balance c/d 2300

9 To sales 650

2300 2300

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

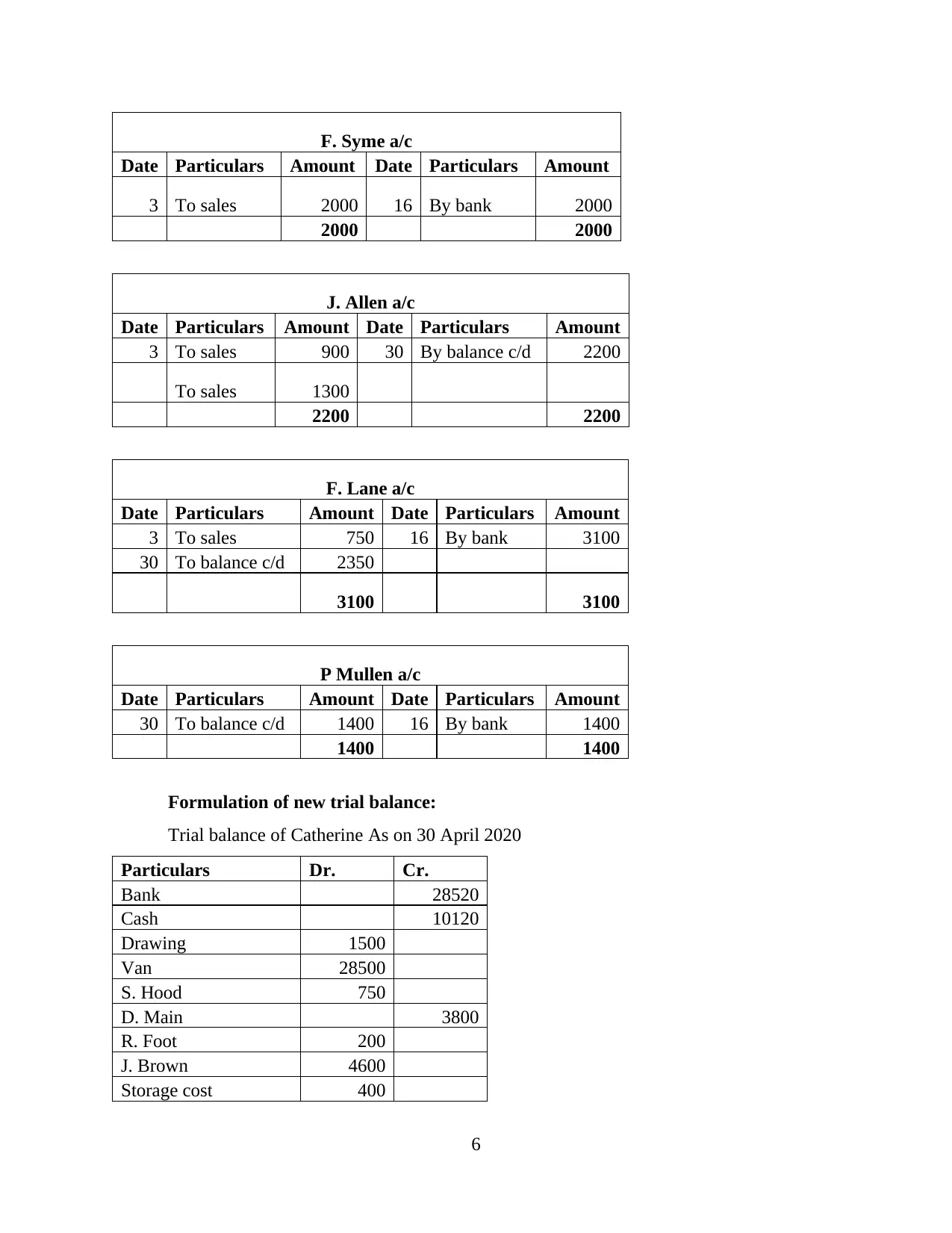

F. Syme a/c

Date Particulars Amount Date Particulars Amount

3 To sales 2000 16 By bank 2000

2000 2000

J. Allen a/c

Date Particulars Amount Date Particulars Amount

3 To sales 900 30 By balance c/d 2200

To sales 1300

2200 2200

F. Lane a/c

Date Particulars Amount Date Particulars Amount

3 To sales 750 16 By bank 3100

30 To balance c/d 2350

3100 3100

P Mullen a/c

Date Particulars Amount Date Particulars Amount

30 To balance c/d 1400 16 By bank 1400

1400 1400

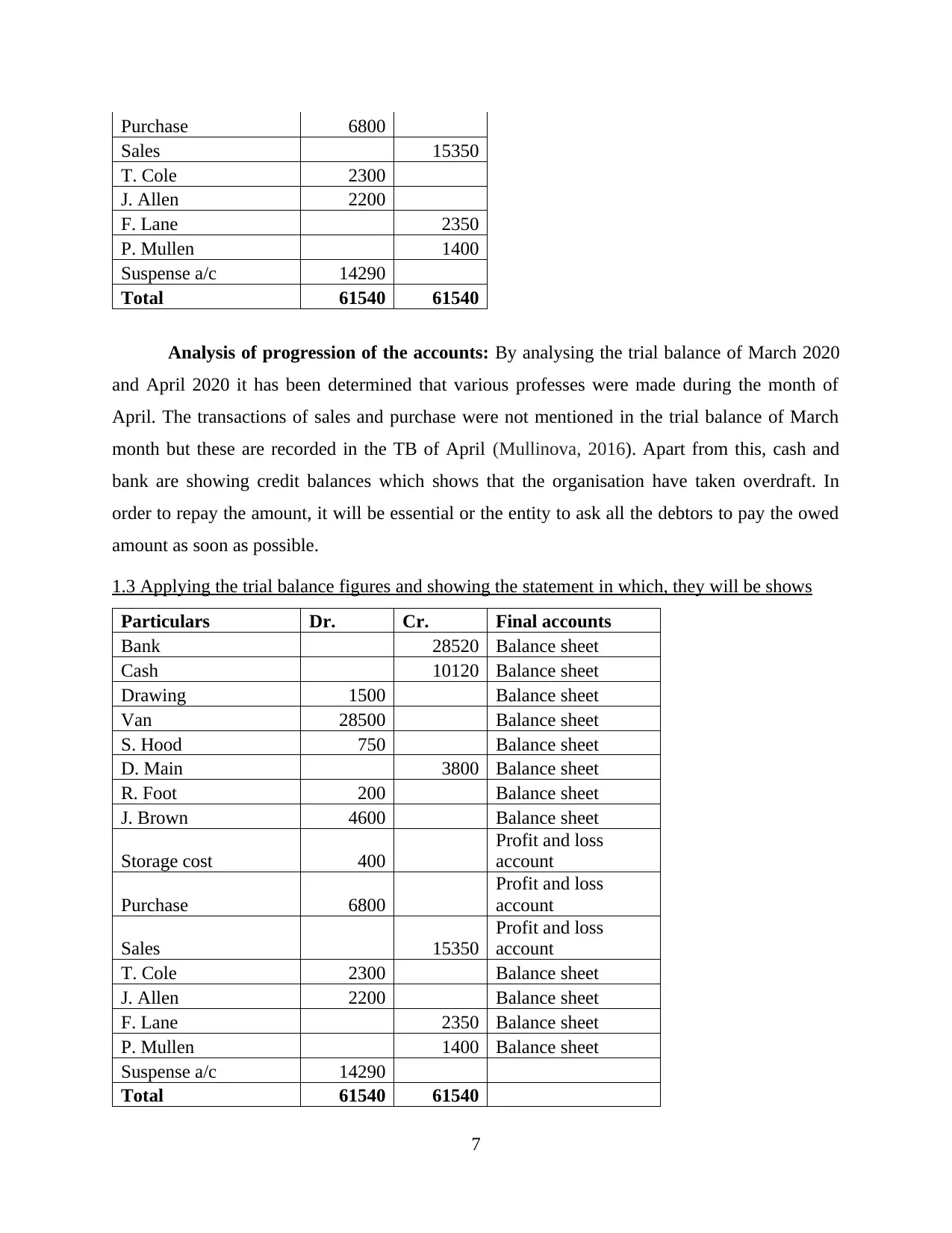

Formulation of new trial balance:

Trial balance of Catherine As on 30 April 2020

Particulars Dr. Cr.

Bank 28520

Cash 10120

Drawing 1500

Van 28500

S. Hood 750

D. Main 3800

R. Foot 200

J. Brown 4600

Storage cost 400

6

Date Particulars Amount Date Particulars Amount

3 To sales 2000 16 By bank 2000

2000 2000

J. Allen a/c

Date Particulars Amount Date Particulars Amount

3 To sales 900 30 By balance c/d 2200

To sales 1300

2200 2200

F. Lane a/c

Date Particulars Amount Date Particulars Amount

3 To sales 750 16 By bank 3100

30 To balance c/d 2350

3100 3100

P Mullen a/c

Date Particulars Amount Date Particulars Amount

30 To balance c/d 1400 16 By bank 1400

1400 1400

Formulation of new trial balance:

Trial balance of Catherine As on 30 April 2020

Particulars Dr. Cr.

Bank 28520

Cash 10120

Drawing 1500

Van 28500

S. Hood 750

D. Main 3800

R. Foot 200

J. Brown 4600

Storage cost 400

6

Purchase 6800

Sales 15350

T. Cole 2300

J. Allen 2200

F. Lane 2350

P. Mullen 1400

Suspense a/c 14290

Total 61540 61540

Analysis of progression of the accounts: By analysing the trial balance of March 2020

and April 2020 it has been determined that various professes were made during the month of

April. The transactions of sales and purchase were not mentioned in the trial balance of March

month but these are recorded in the TB of April (Mullinova, 2016). Apart from this, cash and

bank are showing credit balances which shows that the organisation have taken overdraft. In

order to repay the amount, it will be essential or the entity to ask all the debtors to pay the owed

amount as soon as possible.

1.3 Applying the trial balance figures and showing the statement in which, they will be shows

Particulars Dr. Cr. Final accounts

Bank 28520 Balance sheet

Cash 10120 Balance sheet

Drawing 1500 Balance sheet

Van 28500 Balance sheet

S. Hood 750 Balance sheet

D. Main 3800 Balance sheet

R. Foot 200 Balance sheet

J. Brown 4600 Balance sheet

Storage cost 400

Profit and loss

account

Purchase 6800

Profit and loss

account

Sales 15350

Profit and loss

account

T. Cole 2300 Balance sheet

J. Allen 2200 Balance sheet

F. Lane 2350 Balance sheet

P. Mullen 1400 Balance sheet

Suspense a/c 14290

Total 61540 61540

7

Sales 15350

T. Cole 2300

J. Allen 2200

F. Lane 2350

P. Mullen 1400

Suspense a/c 14290

Total 61540 61540

Analysis of progression of the accounts: By analysing the trial balance of March 2020

and April 2020 it has been determined that various professes were made during the month of

April. The transactions of sales and purchase were not mentioned in the trial balance of March

month but these are recorded in the TB of April (Mullinova, 2016). Apart from this, cash and

bank are showing credit balances which shows that the organisation have taken overdraft. In

order to repay the amount, it will be essential or the entity to ask all the debtors to pay the owed

amount as soon as possible.

1.3 Applying the trial balance figures and showing the statement in which, they will be shows

Particulars Dr. Cr. Final accounts

Bank 28520 Balance sheet

Cash 10120 Balance sheet

Drawing 1500 Balance sheet

Van 28500 Balance sheet

S. Hood 750 Balance sheet

D. Main 3800 Balance sheet

R. Foot 200 Balance sheet

J. Brown 4600 Balance sheet

Storage cost 400

Profit and loss

account

Purchase 6800

Profit and loss

account

Sales 15350

Profit and loss

account

T. Cole 2300 Balance sheet

J. Allen 2200 Balance sheet

F. Lane 2350 Balance sheet

P. Mullen 1400 Balance sheet

Suspense a/c 14290

Total 61540 61540

7

TASK 2

2.1 Description of the financial accounting statements prepared by business entities and

discussion of the type of information presented through each

Financial reports: All the reports that are generated by an organisation to keep track

record of all the monetary transactions are known as financial reports. It can also be defined as

the report which is created to keep detailed data of all the transaction which are leaving financial

effect upon a business. Some of its examples are final accounts, audit report, annual report etc. It

is a wide term and financial statement is a part of it (Narayanaswamy, 2017).

Financial statements: All the organisations create specific accounts on yearly basis so

that information of actual position and performance of business could be shared with internal as

well as external stakeholders. There are three main types of statements which are profit and loss

account, balance sheet and cash flow statement. With the help of all of them an entity tries to

maintain interest of shareholders and other stakeholders so that all the operations could be

carried out systematically.

Difference between financial report and statements:

Basis Financial reports Financial statements

Definition All the reports that are

related to financial

information of the

organisation are the financial

report.

Specific accounts that are

generated for specific

purposes are the financial

statements.

Types Annual report, all financial

statements, audit report and

all the other reports that are

keeping track record of

financial impact of

transactions made by an

organisation.

Profit and loss account,

balance sheet, cash flow

statement etc. are the types

of financial statements that

are created by all the

companies on yearly basis

for specific purposes

(Oulasvirta and Bailey,

8

2.1 Description of the financial accounting statements prepared by business entities and

discussion of the type of information presented through each

Financial reports: All the reports that are generated by an organisation to keep track

record of all the monetary transactions are known as financial reports. It can also be defined as

the report which is created to keep detailed data of all the transaction which are leaving financial

effect upon a business. Some of its examples are final accounts, audit report, annual report etc. It

is a wide term and financial statement is a part of it (Narayanaswamy, 2017).

Financial statements: All the organisations create specific accounts on yearly basis so

that information of actual position and performance of business could be shared with internal as

well as external stakeholders. There are three main types of statements which are profit and loss

account, balance sheet and cash flow statement. With the help of all of them an entity tries to

maintain interest of shareholders and other stakeholders so that all the operations could be

carried out systematically.

Difference between financial report and statements:

Basis Financial reports Financial statements

Definition All the reports that are

related to financial

information of the

organisation are the financial

report.

Specific accounts that are

generated for specific

purposes are the financial

statements.

Types Annual report, all financial

statements, audit report and

all the other reports that are

keeping track record of

financial impact of

transactions made by an

organisation.

Profit and loss account,

balance sheet, cash flow

statement etc. are the types

of financial statements that

are created by all the

companies on yearly basis

for specific purposes

(Oulasvirta and Bailey,

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2016).

Various types of financial statements: There are different types of financial statements

which are created by companies on yearly basis. All of them are as follows:

Profit and loss account: All the expenses and incomes that are faced by a business

during an accounting year are recorded in it. Some of them are salaries, rent, insurance, postage,

legal expenses etc.

Balance sheet: It is mainly generated to analyse the financial position of company. All

the assets and liabilities of a firm are recorded in it. With the help of it, actual position of

business in the market could be analysed (Pratt, 2016).

Cash flow statement: It is mainly generated for the purpose of recording all the cash

transactions in a separate statement. It guides to analyse liquid strength of an organisation.

Difference between all of them:

Basis Profit and loss

account

Balance sheet Cash flow statement

Purpose Main purpose of this

statement is to analyse

the profitability of the

organisation. It can help

the investors and

shareholders to analyse

that the company is able

to generate appropriate

profits to provide them

good returns on their

invested funds

(Schroeder, Clark and

Cathey, 2019).

Purpose of creating

balance sheet on yearly

basis is to analyse

financial position of

business so that it could

be determined that the

company will be able to

sustain in the market or

not. It also helps to

analyse competitive

advantage of business.

Cash flow statement is

formulated on yealy

basis by all the

companies in order to

analyse that they are

having sufficient funds

to meet all the future

obligation or not. With

the help of it, liquidity of

business could be

analysed.

Structure The structure of it is

very easy as it is

formulated in the

account format.

It is also formulated in

accounts format but the

structure of it is slightly

different first of all, all

It is generated in vertical

formal in which all the

details are mentioned on

the basis of different

9

Various types of financial statements: There are different types of financial statements

which are created by companies on yearly basis. All of them are as follows:

Profit and loss account: All the expenses and incomes that are faced by a business

during an accounting year are recorded in it. Some of them are salaries, rent, insurance, postage,

legal expenses etc.

Balance sheet: It is mainly generated to analyse the financial position of company. All

the assets and liabilities of a firm are recorded in it. With the help of it, actual position of

business in the market could be analysed (Pratt, 2016).

Cash flow statement: It is mainly generated for the purpose of recording all the cash

transactions in a separate statement. It guides to analyse liquid strength of an organisation.

Difference between all of them:

Basis Profit and loss

account

Balance sheet Cash flow statement

Purpose Main purpose of this

statement is to analyse

the profitability of the

organisation. It can help

the investors and

shareholders to analyse

that the company is able

to generate appropriate

profits to provide them

good returns on their

invested funds

(Schroeder, Clark and

Cathey, 2019).

Purpose of creating

balance sheet on yearly

basis is to analyse

financial position of

business so that it could

be determined that the

company will be able to

sustain in the market or

not. It also helps to

analyse competitive

advantage of business.

Cash flow statement is

formulated on yealy

basis by all the

companies in order to

analyse that they are

having sufficient funds

to meet all the future

obligation or not. With

the help of it, liquidity of

business could be

analysed.

Structure The structure of it is

very easy as it is

formulated in the

account format.

It is also formulated in

accounts format but the

structure of it is slightly

different first of all, all

It is generated in vertical

formal in which all the

details are mentioned on

the basis of different

9

the equities are

recorded in liabilities

side then debts are

recorded in the same

side (Sorensen and

Miller, 2017). On the

other hand, in assets

side first of all, all the

short-term assets are

recorded and then fixed

and fictitious assets are

recorded.

activities which are

operating, investing and

financing.

Content All the incomes,

expenses, losses and

gains are the content of

this statement.

All the assets, liabilities

and equities are the

content of balance

sheet.

All the transactions that

are related to cash are the

content of this statement

and recorded under

different activities.

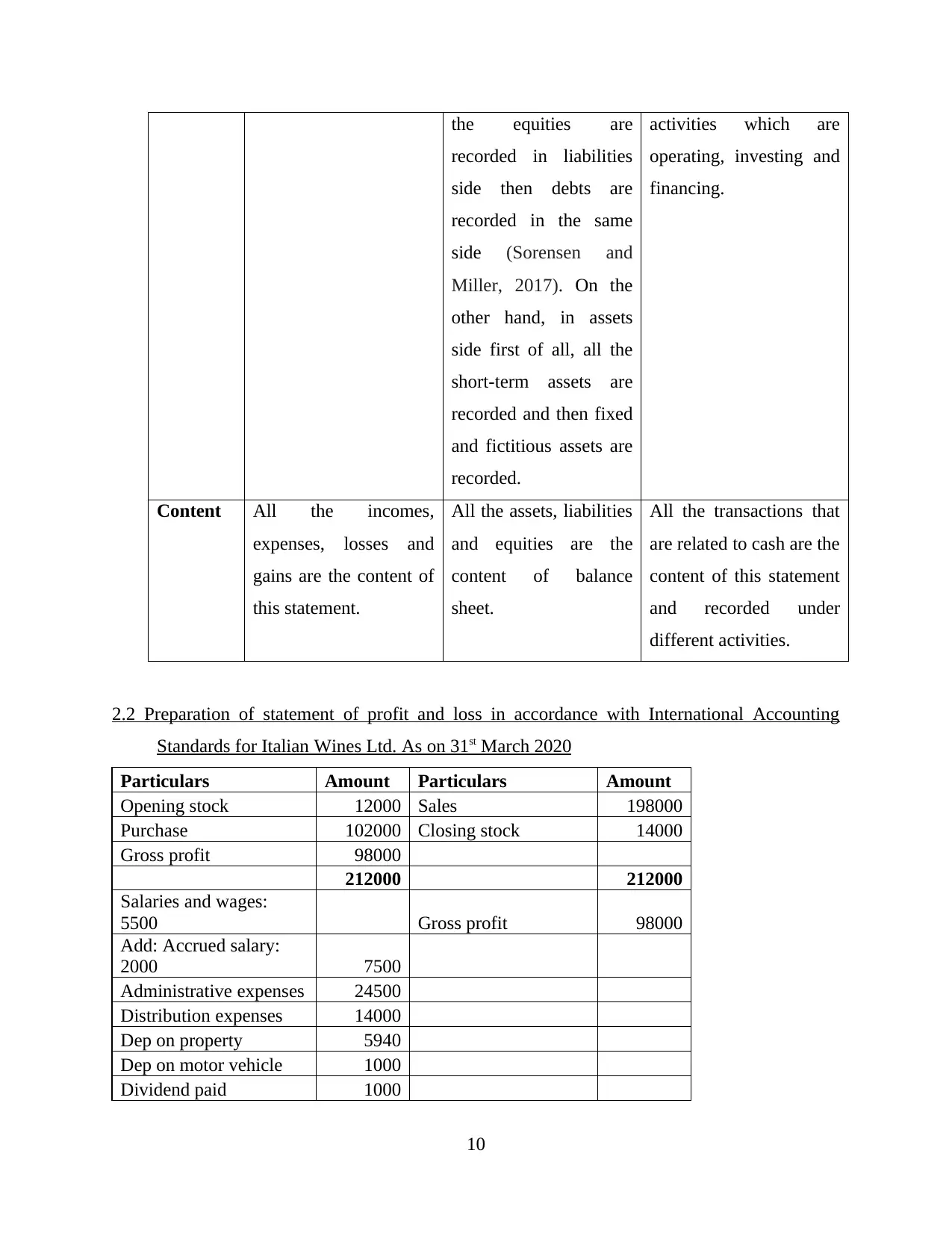

2.2 Preparation of statement of profit and loss in accordance with International Accounting

Standards for Italian Wines Ltd. As on 31st March 2020

Particulars Amount Particulars Amount

Opening stock 12000 Sales 198000

Purchase 102000 Closing stock 14000

Gross profit 98000

212000 212000

Salaries and wages:

5500 Gross profit 98000

Add: Accrued salary:

2000 7500

Administrative expenses 24500

Distribution expenses 14000

Dep on property 5940

Dep on motor vehicle 1000

Dividend paid 1000

10

recorded in liabilities

side then debts are

recorded in the same

side (Sorensen and

Miller, 2017). On the

other hand, in assets

side first of all, all the

short-term assets are

recorded and then fixed

and fictitious assets are

recorded.

activities which are

operating, investing and

financing.

Content All the incomes,

expenses, losses and

gains are the content of

this statement.

All the assets, liabilities

and equities are the

content of balance

sheet.

All the transactions that

are related to cash are the

content of this statement

and recorded under

different activities.

2.2 Preparation of statement of profit and loss in accordance with International Accounting

Standards for Italian Wines Ltd. As on 31st March 2020

Particulars Amount Particulars Amount

Opening stock 12000 Sales 198000

Purchase 102000 Closing stock 14000

Gross profit 98000

212000 212000

Salaries and wages:

5500 Gross profit 98000

Add: Accrued salary:

2000 7500

Administrative expenses 24500

Distribution expenses 14000

Dep on property 5940

Dep on motor vehicle 1000

Dividend paid 1000

10

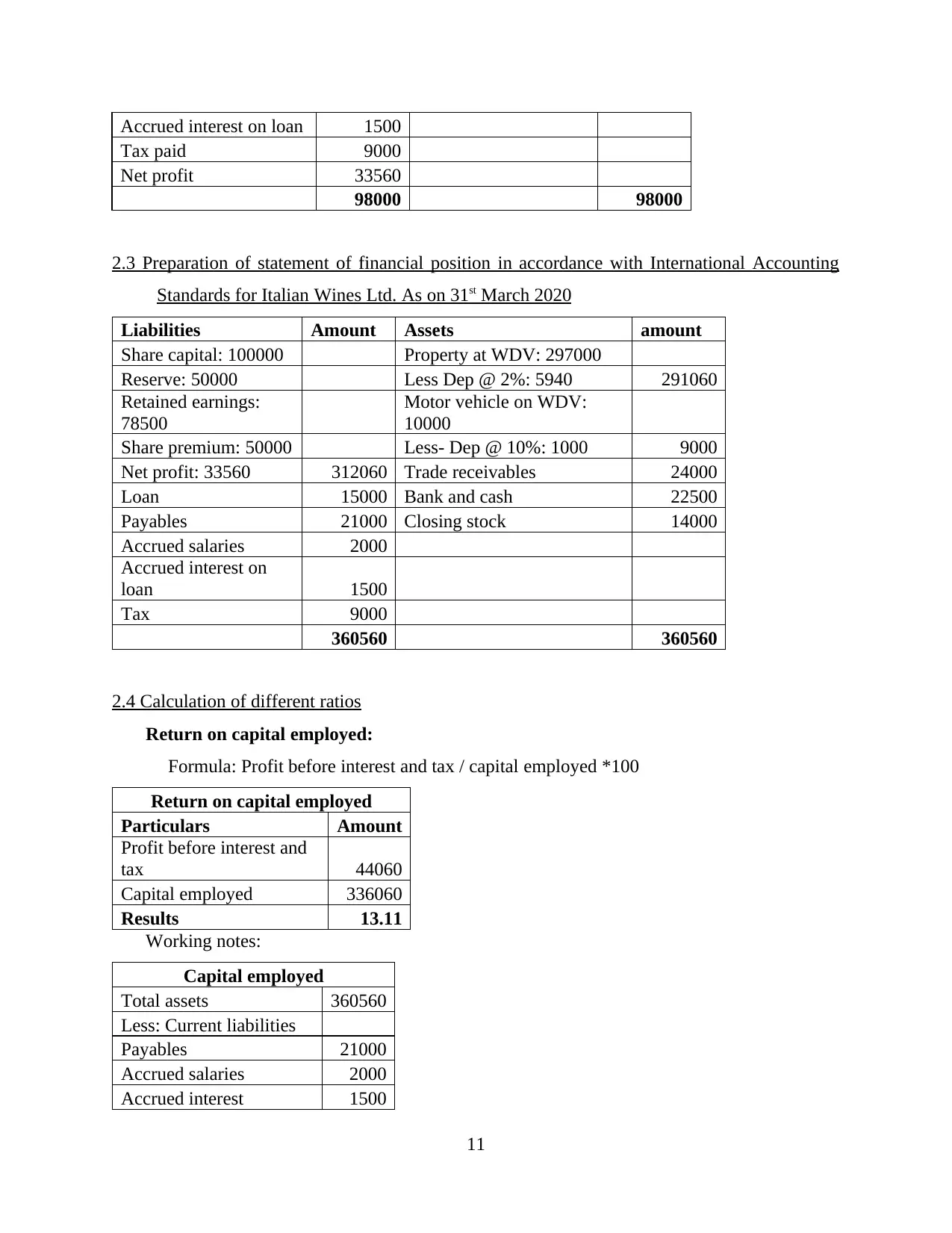

Accrued interest on loan 1500

Tax paid 9000

Net profit 33560

98000 98000

2.3 Preparation of statement of financial position in accordance with International Accounting

Standards for Italian Wines Ltd. As on 31st March 2020

Liabilities Amount Assets amount

Share capital: 100000 Property at WDV: 297000

Reserve: 50000 Less Dep @ 2%: 5940 291060

Retained earnings:

78500

Motor vehicle on WDV:

10000

Share premium: 50000 Less- Dep @ 10%: 1000 9000

Net profit: 33560 312060 Trade receivables 24000

Loan 15000 Bank and cash 22500

Payables 21000 Closing stock 14000

Accrued salaries 2000

Accrued interest on

loan 1500

Tax 9000

360560 360560

2.4 Calculation of different ratios

Return on capital employed:

Formula: Profit before interest and tax / capital employed *100

Return on capital employed

Particulars Amount

Profit before interest and

tax 44060

Capital employed 336060

Results 13.11

Working notes:

Capital employed

Total assets 360560

Less: Current liabilities

Payables 21000

Accrued salaries 2000

Accrued interest 1500

11

Tax paid 9000

Net profit 33560

98000 98000

2.3 Preparation of statement of financial position in accordance with International Accounting

Standards for Italian Wines Ltd. As on 31st March 2020

Liabilities Amount Assets amount

Share capital: 100000 Property at WDV: 297000

Reserve: 50000 Less Dep @ 2%: 5940 291060

Retained earnings:

78500

Motor vehicle on WDV:

10000

Share premium: 50000 Less- Dep @ 10%: 1000 9000

Net profit: 33560 312060 Trade receivables 24000

Loan 15000 Bank and cash 22500

Payables 21000 Closing stock 14000

Accrued salaries 2000

Accrued interest on

loan 1500

Tax 9000

360560 360560

2.4 Calculation of different ratios

Return on capital employed:

Formula: Profit before interest and tax / capital employed *100

Return on capital employed

Particulars Amount

Profit before interest and

tax 44060

Capital employed 336060

Results 13.11

Working notes:

Capital employed

Total assets 360560

Less: Current liabilities

Payables 21000

Accrued salaries 2000

Accrued interest 1500

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

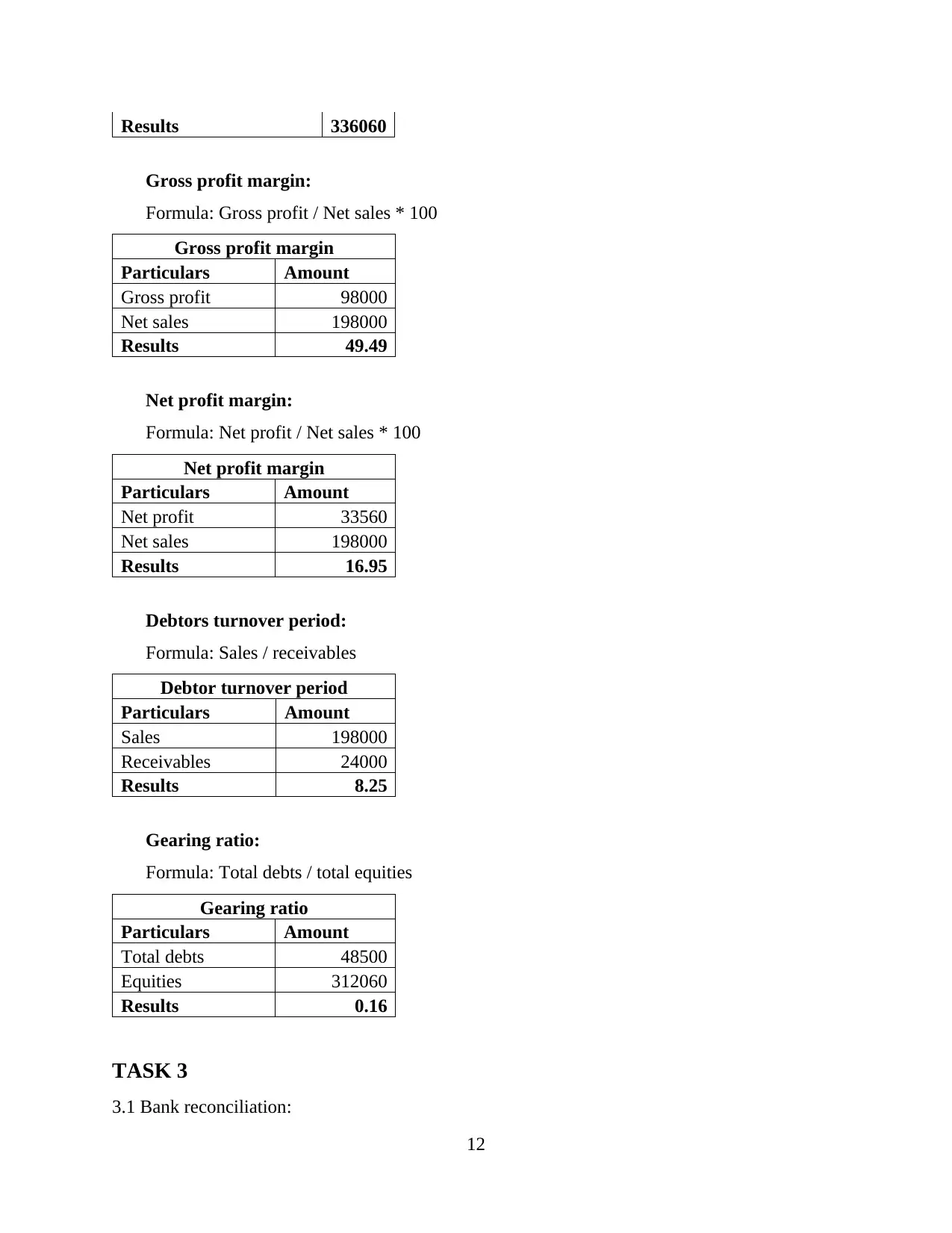

Results 336060

Gross profit margin:

Formula: Gross profit / Net sales * 100

Gross profit margin

Particulars Amount

Gross profit 98000

Net sales 198000

Results 49.49

Net profit margin:

Formula: Net profit / Net sales * 100

Net profit margin

Particulars Amount

Net profit 33560

Net sales 198000

Results 16.95

Debtors turnover period:

Formula: Sales / receivables

Debtor turnover period

Particulars Amount

Sales 198000

Receivables 24000

Results 8.25

Gearing ratio:

Formula: Total debts / total equities

Gearing ratio

Particulars Amount

Total debts 48500

Equities 312060

Results 0.16

TASK 3

3.1 Bank reconciliation:

12

Gross profit margin:

Formula: Gross profit / Net sales * 100

Gross profit margin

Particulars Amount

Gross profit 98000

Net sales 198000

Results 49.49

Net profit margin:

Formula: Net profit / Net sales * 100

Net profit margin

Particulars Amount

Net profit 33560

Net sales 198000

Results 16.95

Debtors turnover period:

Formula: Sales / receivables

Debtor turnover period

Particulars Amount

Sales 198000

Receivables 24000

Results 8.25

Gearing ratio:

Formula: Total debts / total equities

Gearing ratio

Particulars Amount

Total debts 48500

Equities 312060

Results 0.16

TASK 3

3.1 Bank reconciliation:

12

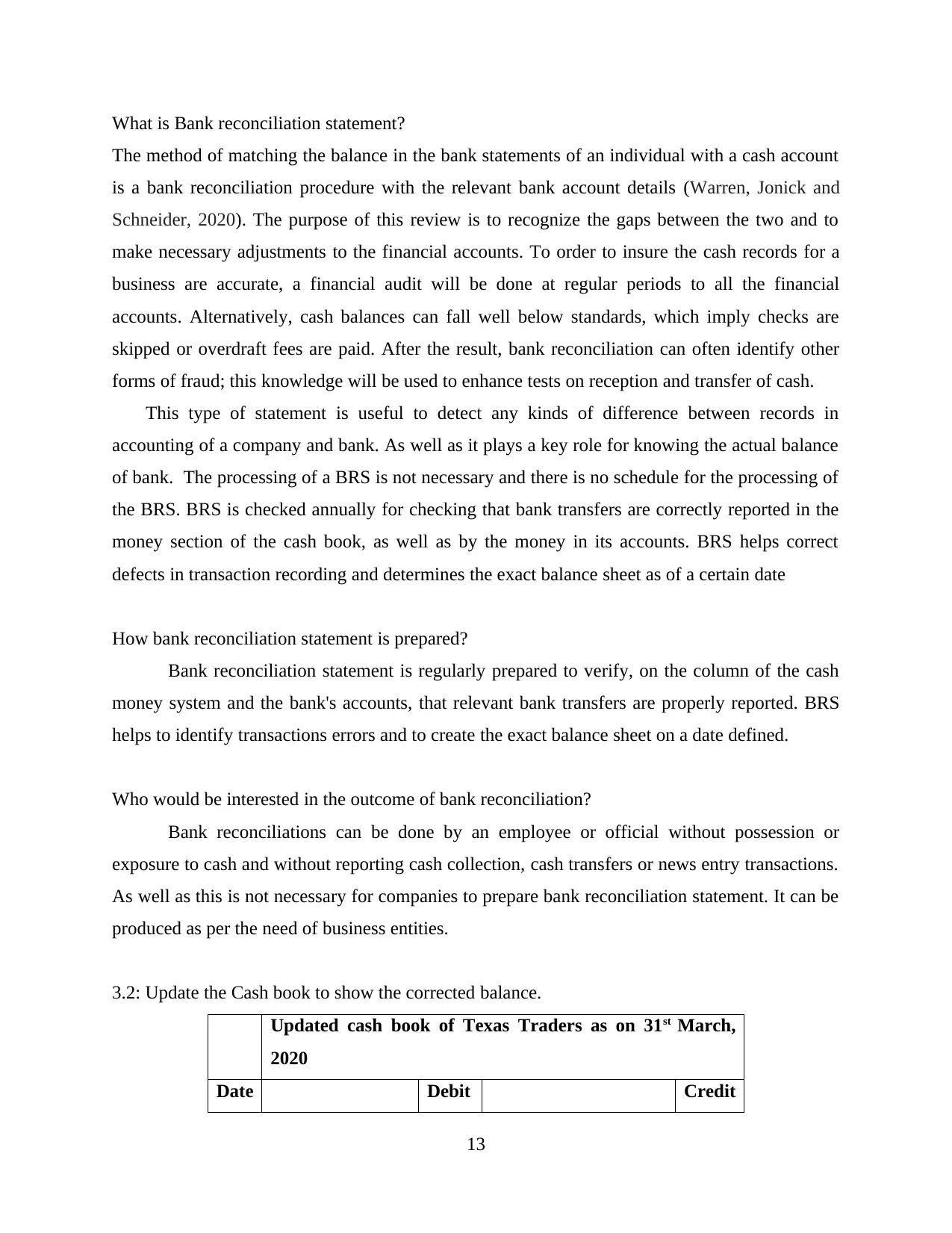

What is Bank reconciliation statement?

The method of matching the balance in the bank statements of an individual with a cash account

is a bank reconciliation procedure with the relevant bank account details (Warren, Jonick and

Schneider, 2020). The purpose of this review is to recognize the gaps between the two and to

make necessary adjustments to the financial accounts. To order to insure the cash records for a

business are accurate, a financial audit will be done at regular periods to all the financial

accounts. Alternatively, cash balances can fall well below standards, which imply checks are

skipped or overdraft fees are paid. After the result, bank reconciliation can often identify other

forms of fraud; this knowledge will be used to enhance tests on reception and transfer of cash.

This type of statement is useful to detect any kinds of difference between records in

accounting of a company and bank. As well as it plays a key role for knowing the actual balance

of bank. The processing of a BRS is not necessary and there is no schedule for the processing of

the BRS. BRS is checked annually for checking that bank transfers are correctly reported in the

money section of the cash book, as well as by the money in its accounts. BRS helps correct

defects in transaction recording and determines the exact balance sheet as of a certain date

How bank reconciliation statement is prepared?

Bank reconciliation statement is regularly prepared to verify, on the column of the cash

money system and the bank's accounts, that relevant bank transfers are properly reported. BRS

helps to identify transactions errors and to create the exact balance sheet on a date defined.

Who would be interested in the outcome of bank reconciliation?

Bank reconciliations can be done by an employee or official without possession or

exposure to cash and without reporting cash collection, cash transfers or news entry transactions.

As well as this is not necessary for companies to prepare bank reconciliation statement. It can be

produced as per the need of business entities.

3.2: Update the Cash book to show the corrected balance.

Updated cash book of Texas Traders as on 31st March,

2020

Date Debit Credit

13

The method of matching the balance in the bank statements of an individual with a cash account

is a bank reconciliation procedure with the relevant bank account details (Warren, Jonick and

Schneider, 2020). The purpose of this review is to recognize the gaps between the two and to

make necessary adjustments to the financial accounts. To order to insure the cash records for a

business are accurate, a financial audit will be done at regular periods to all the financial

accounts. Alternatively, cash balances can fall well below standards, which imply checks are

skipped or overdraft fees are paid. After the result, bank reconciliation can often identify other

forms of fraud; this knowledge will be used to enhance tests on reception and transfer of cash.

This type of statement is useful to detect any kinds of difference between records in

accounting of a company and bank. As well as it plays a key role for knowing the actual balance

of bank. The processing of a BRS is not necessary and there is no schedule for the processing of

the BRS. BRS is checked annually for checking that bank transfers are correctly reported in the

money section of the cash book, as well as by the money in its accounts. BRS helps correct

defects in transaction recording and determines the exact balance sheet as of a certain date

How bank reconciliation statement is prepared?

Bank reconciliation statement is regularly prepared to verify, on the column of the cash

money system and the bank's accounts, that relevant bank transfers are properly reported. BRS

helps to identify transactions errors and to create the exact balance sheet on a date defined.

Who would be interested in the outcome of bank reconciliation?

Bank reconciliations can be done by an employee or official without possession or

exposure to cash and without reporting cash collection, cash transfers or news entry transactions.

As well as this is not necessary for companies to prepare bank reconciliation statement. It can be

produced as per the need of business entities.

3.2: Update the Cash book to show the corrected balance.

Updated cash book of Texas Traders as on 31st March,

2020

Date Debit Credit

13

£ £

1 Bal b/d 5000

2 Rent Mrs Miller 5000

5 Spenser Ltd. 2500

8 Interest on debentures 2500

9 Cash 1500

14

Capital introduced

Mr. white 5000

15 PC World purchase 6000

20 Insurance claim 15000 Electricity 1800

21 Repayment of loan 9200

22 Legal fees 4000

23 Cash 8000

28 North Wings Ltd. 5000

29 Salary:

Amber 2000

Oshun 2500

Baker 2800

30 Bal c/d 6200

42000 42000

3.3: Prepare a bank reconciliation statement.

Bank Reconciliation Statement of Texas Traders as

on 31st March, 2020

Particulars £ + £ -

Balance as per cash book 6200

Salary:

Amber (not deducted from bank) 2000

Baker (not deducted from bank) 2800

14

1 Bal b/d 5000

2 Rent Mrs Miller 5000

5 Spenser Ltd. 2500

8 Interest on debentures 2500

9 Cash 1500

14

Capital introduced

Mr. white 5000

15 PC World purchase 6000

20 Insurance claim 15000 Electricity 1800

21 Repayment of loan 9200

22 Legal fees 4000

23 Cash 8000

28 North Wings Ltd. 5000

29 Salary:

Amber 2000

Oshun 2500

Baker 2800

30 Bal c/d 6200

42000 42000

3.3: Prepare a bank reconciliation statement.

Bank Reconciliation Statement of Texas Traders as

on 31st March, 2020

Particulars £ + £ -

Balance as per cash book 6200

Salary:

Amber (not deducted from bank) 2000

Baker (not deducted from bank) 2800

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

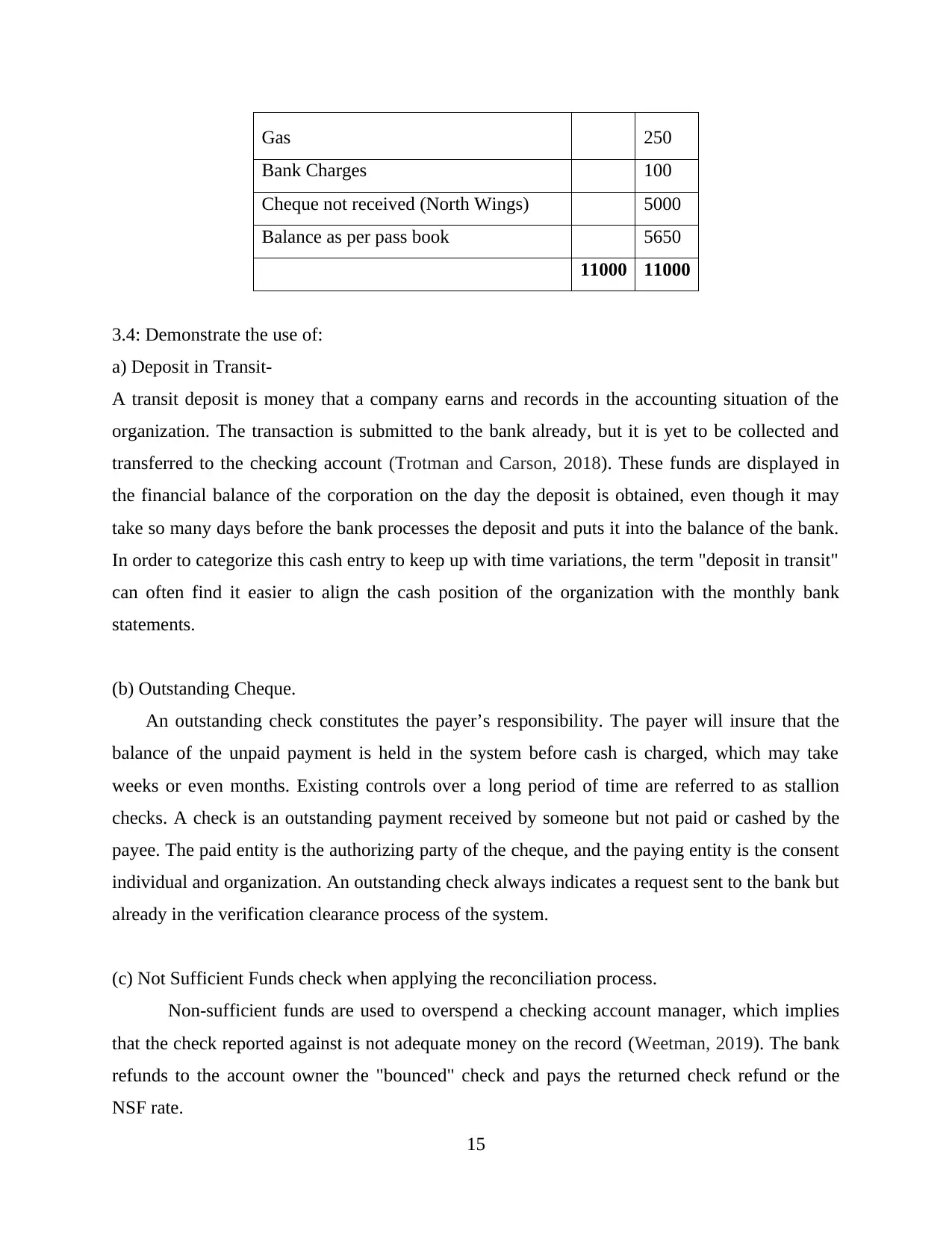

Gas 250

Bank Charges 100

Cheque not received (North Wings) 5000

Balance as per pass book 5650

11000 11000

3.4: Demonstrate the use of:

a) Deposit in Transit-

A transit deposit is money that a company earns and records in the accounting situation of the

organization. The transaction is submitted to the bank already, but it is yet to be collected and

transferred to the checking account (Trotman and Carson, 2018). These funds are displayed in

the financial balance of the corporation on the day the deposit is obtained, even though it may

take so many days before the bank processes the deposit and puts it into the balance of the bank.

In order to categorize this cash entry to keep up with time variations, the term "deposit in transit"

can often find it easier to align the cash position of the organization with the monthly bank

statements.

(b) Outstanding Cheque.

An outstanding check constitutes the payer’s responsibility. The payer will insure that the

balance of the unpaid payment is held in the system before cash is charged, which may take

weeks or even months. Existing controls over a long period of time are referred to as stallion

checks. A check is an outstanding payment received by someone but not paid or cashed by the

payee. The paid entity is the authorizing party of the cheque, and the paying entity is the consent

individual and organization. An outstanding check always indicates a request sent to the bank but

already in the verification clearance process of the system.

(c) Not Sufficient Funds check when applying the reconciliation process.

Non-sufficient funds are used to overspend a checking account manager, which implies

that the check reported against is not adequate money on the record (Weetman, 2019). The bank

refunds to the account owner the "bounced" check and pays the returned check refund or the

NSF rate.

15

Bank Charges 100

Cheque not received (North Wings) 5000

Balance as per pass book 5650

11000 11000

3.4: Demonstrate the use of:

a) Deposit in Transit-

A transit deposit is money that a company earns and records in the accounting situation of the

organization. The transaction is submitted to the bank already, but it is yet to be collected and

transferred to the checking account (Trotman and Carson, 2018). These funds are displayed in

the financial balance of the corporation on the day the deposit is obtained, even though it may

take so many days before the bank processes the deposit and puts it into the balance of the bank.

In order to categorize this cash entry to keep up with time variations, the term "deposit in transit"

can often find it easier to align the cash position of the organization with the monthly bank

statements.

(b) Outstanding Cheque.

An outstanding check constitutes the payer’s responsibility. The payer will insure that the

balance of the unpaid payment is held in the system before cash is charged, which may take

weeks or even months. Existing controls over a long period of time are referred to as stallion

checks. A check is an outstanding payment received by someone but not paid or cashed by the

payee. The paid entity is the authorizing party of the cheque, and the paying entity is the consent

individual and organization. An outstanding check always indicates a request sent to the bank but

already in the verification clearance process of the system.

(c) Not Sufficient Funds check when applying the reconciliation process.

Non-sufficient funds are used to overspend a checking account manager, which implies

that the check reported against is not adequate money on the record (Weetman, 2019). The bank

refunds to the account owner the "bounced" check and pays the returned check refund or the

NSF rate.

15

CONCLUSION

From the above project report it has been concluded that financial accounting is the

procedure which is followed to generate financial statements such as profit and loss account,

balance sheet and cash flow statement. While generating all of them it is very important or

accounting professionals to make sure that they are able to follow all the accounting rules such as

accounting concepts, principles and standards. Ignorance of them may result in improper

formulation of statements. While checking accuracy of cash book bank reconciliation statement

if generated which helps to differentiate cash and bank book.

16

From the above project report it has been concluded that financial accounting is the

procedure which is followed to generate financial statements such as profit and loss account,

balance sheet and cash flow statement. While generating all of them it is very important or

accounting professionals to make sure that they are able to follow all the accounting rules such as

accounting concepts, principles and standards. Ignorance of them may result in improper

formulation of statements. While checking accuracy of cash book bank reconciliation statement

if generated which helps to differentiate cash and bank book.

16

REFERENCES

Books and Journals:

Biddle, G. C., Ma, M. L. and Song, F. M., 2019. Accounting conservatism and bankruptcy

risk. Available at SSRN 1621272.

Dauderies, H. and Annand, D., 2019. Introduction to Financial Accounting. Lyryx.

Flesher, D. L., Flesher, T. K. and Previts, G. J., 2018. The Financial Accounting Standards

Board: Profiles of seven leaders. Research in Accounting Regulation. 30(1). pp.38-48.

Hanif, M. and Mukherjee, A., 2018. Financial Accounting-I. McGraw-Hill Education.

Kimmel, P. D., Weygandt, J. J. and Kieso, D. E., 2018. Financial accounting: tools for business

decision making. John Wiley & Sons.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches. (1).

pp.60-64.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Oulasvirta, L. O. and Bailey, S. J., 2016. Evolution of EU public sector financial accounting

standardisation: critical events that opened the window for attempted policy

change. Journal of European Integration. 38(6). pp.653-669.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Sorensen, D. P. and Miller, S. E., 2017. Financial accounting scandals and the reform of

corporate governance in the United States and in Italy. Corporate Governance: The

International Journal of Business in Society.

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage AU.

Warren, C., Jonick, C. and Schneider, J., 2020. Financial accounting. Cengage Learning.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

17

Books and Journals:

Biddle, G. C., Ma, M. L. and Song, F. M., 2019. Accounting conservatism and bankruptcy

risk. Available at SSRN 1621272.

Dauderies, H. and Annand, D., 2019. Introduction to Financial Accounting. Lyryx.

Flesher, D. L., Flesher, T. K. and Previts, G. J., 2018. The Financial Accounting Standards

Board: Profiles of seven leaders. Research in Accounting Regulation. 30(1). pp.38-48.

Hanif, M. and Mukherjee, A., 2018. Financial Accounting-I. McGraw-Hill Education.

Kimmel, P. D., Weygandt, J. J. and Kieso, D. E., 2018. Financial accounting: tools for business

decision making. John Wiley & Sons.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches. (1).

pp.60-64.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Oulasvirta, L. O. and Bailey, S. J., 2016. Evolution of EU public sector financial accounting

standardisation: critical events that opened the window for attempted policy

change. Journal of European Integration. 38(6). pp.653-669.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Sorensen, D. P. and Miller, S. E., 2017. Financial accounting scandals and the reform of

corporate governance in the United States and in Italy. Corporate Governance: The

International Journal of Business in Society.

Trotman, K. and Carson, E., 2018. Financial accounting: an integrated approach. Cengage AU.

Warren, C., Jonick, C. and Schneider, J., 2020. Financial accounting. Cengage Learning.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

17

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.