Financial Accounting and The Financial Statements

Added on 2023-01-18

10 Pages1838 Words33 Views

Financial Accounting

And

The Financial

Statements

And

The Financial

Statements

Contents

TASK A...........................................................................................................................................4

1. Annual Depreciation to be charged in income statement of Smilie Nyero for 30th

Sep. 2019:..................................................................................................................................4

2. Carrying amounts of the non-current assets that will be shown in the Statement of

Financial Position at 30 September 2019:............................................................................4

TASK B...........................................................................................................................................4

Operating Profit Ratio:..............................................................................................................4

Profit-after tax Ratio:.................................................................................................................5

TASK C...........................................................................................................................................6

Gearing Ratios:..........................................................................................................................6

Debt Ratio:.................................................................................................................................7

TASK D...........................................................................................................................................7

1. Cash Conversion Cycle (CCC):..........................................................................................7

2. Calculation of the Cash Conversion Cycle for Sainsbury’s Group Plc for the years

2019 and 2018:..........................................................................................................................8

3. Comment:...............................................................................................................................9

REFERENCES............................................................................................................................11

TASK A...........................................................................................................................................4

1. Annual Depreciation to be charged in income statement of Smilie Nyero for 30th

Sep. 2019:..................................................................................................................................4

2. Carrying amounts of the non-current assets that will be shown in the Statement of

Financial Position at 30 September 2019:............................................................................4

TASK B...........................................................................................................................................4

Operating Profit Ratio:..............................................................................................................4

Profit-after tax Ratio:.................................................................................................................5

TASK C...........................................................................................................................................6

Gearing Ratios:..........................................................................................................................6

Debt Ratio:.................................................................................................................................7

TASK D...........................................................................................................................................7

1. Cash Conversion Cycle (CCC):..........................................................................................7

2. Calculation of the Cash Conversion Cycle for Sainsbury’s Group Plc for the years

2019 and 2018:..........................................................................................................................8

3. Comment:...............................................................................................................................9

REFERENCES............................................................................................................................11

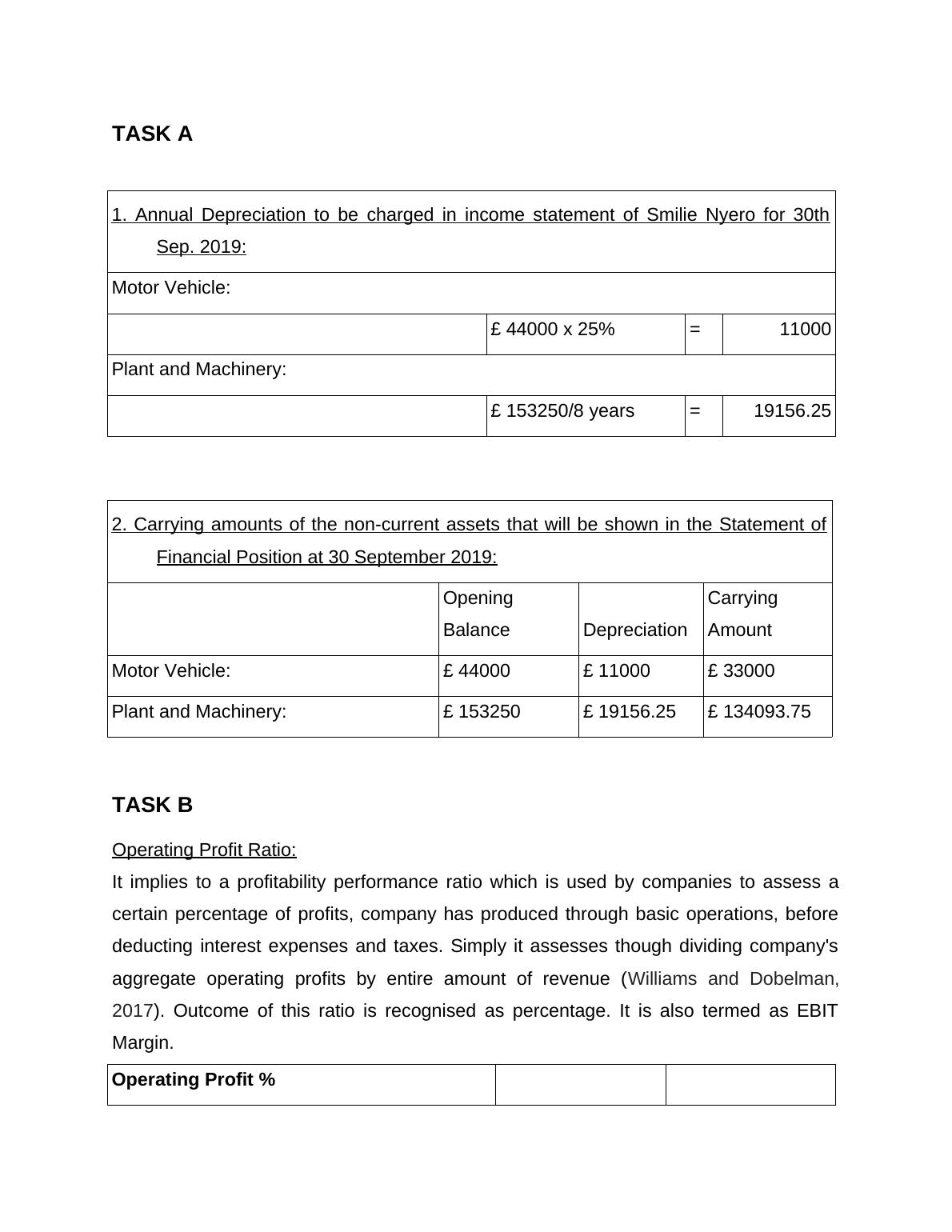

TASK A

1. Annual Depreciation to be charged in income statement of Smilie Nyero for 30th

Sep. 2019:

Motor Vehicle:

£ 44000 x 25% = 11000

Plant and Machinery:

£ 153250/8 years = 19156.25

2. Carrying amounts of the non-current assets that will be shown in the Statement of

Financial Position at 30 September 2019:

Opening

Balance Depreciation

Carrying

Amount

Motor Vehicle: £ 44000 £ 11000 £ 33000

Plant and Machinery: £ 153250 £ 19156.25 £ 134093.75

TASK B

Operating Profit Ratio:

It implies to a profitability performance ratio which is used by companies to assess a

certain percentage of profits, company has produced through basic operations, before

deducting interest expenses and taxes. Simply it assesses though dividing company's

aggregate operating profits by entire amount of revenue (Williams and Dobelman,

2017). Outcome of this ratio is recognised as percentage. It is also termed as EBIT

Margin.

Operating Profit %

1. Annual Depreciation to be charged in income statement of Smilie Nyero for 30th

Sep. 2019:

Motor Vehicle:

£ 44000 x 25% = 11000

Plant and Machinery:

£ 153250/8 years = 19156.25

2. Carrying amounts of the non-current assets that will be shown in the Statement of

Financial Position at 30 September 2019:

Opening

Balance Depreciation

Carrying

Amount

Motor Vehicle: £ 44000 £ 11000 £ 33000

Plant and Machinery: £ 153250 £ 19156.25 £ 134093.75

TASK B

Operating Profit Ratio:

It implies to a profitability performance ratio which is used by companies to assess a

certain percentage of profits, company has produced through basic operations, before

deducting interest expenses and taxes. Simply it assesses though dividing company's

aggregate operating profits by entire amount of revenue (Williams and Dobelman,

2017). Outcome of this ratio is recognised as percentage. It is also termed as EBIT

Margin.

Operating Profit %

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Economics - Statement of Profit and Loss Accountlg...

|7

|982

|28

Financial Analysis of Sainsbury and Tescolg...

|14

|3768

|47

Financial Performance Analysislg...

|17

|4331

|1

Comparison of Tesco and Sainsbury’s Financial Performance through Ratio Analysislg...

|17

|3984

|58

Accounting for Managers: Horizontal Analysis and Financial Ratios of Woolworthslg...

|16

|3238

|339