Financial Accounting: Communication & Reporting Analysis

VerifiedAdded on 2020/03/23

|20

|3470

|31

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting assignment. It begins with an analysis of financial reporting, focusing on communication and information effectiveness, and includes a letter to the IASB with recommendations for enhancing financial reports, particularly for investors. The solution then delves into share capital accounting, detailing journal entries for share applications, allotments, calls, forfeitures, and reissues. Finally, the assignment addresses current and deferred tax calculations, providing detailed worksheets and journal entries for income tax expense, refundable amounts, and deferred tax assets and liabilities. The analysis includes adjustments for temporary differences and their impact on taxable income and tax liabilities. This solution provides a complete overview of financial accounting principles and their practical application.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question No 1...........................................................................................................2

Answer to Question No 2...........................................................................................................6

Answer to Question No 3...........................................................................................................9

Requirement (i)......................................................................................................................9

Requirement (ii)...................................................................................................................10

Requirement (iii)..................................................................................................................11

Answer to Question No 4.........................................................................................................15

Answer to Question No 5.........................................................................................................17

Reference List..........................................................................................................................19

FINANCIAL ACCOUNTING

Table of Contents

Answer to Question No 1...........................................................................................................2

Answer to Question No 2...........................................................................................................6

Answer to Question No 3...........................................................................................................9

Requirement (i)......................................................................................................................9

Requirement (ii)...................................................................................................................10

Requirement (iii)..................................................................................................................11

Answer to Question No 4.........................................................................................................15

Answer to Question No 5.........................................................................................................17

Reference List..........................................................................................................................19

2

FINANCIAL ACCOUNTING

Answer to Question No 1

To,

The Chairperson

International Standard Accounting Board

35 Mayo Street, London- EX5CM 7HX, United Kingdom

Date: 17th September 2017

Subject: Guidance and recommendation for enhancing the communication and information

effectiveness in the financial report

Respected Sir,

Being an investor, I propose to construct certain plans in regards to the IASB

proposition in accordance to the efficiency of the information that is available within the

financial report. I have been looking to make certain investments in Westpac and ANZ,

which are two companies that are listed in the ASX. Due to this interest, I have assessed and

compared the annual report of the present accounting year of both the companies. During the

time of assessing the report, I have observed certain areas that can be developed for an

enhanced presentation and disclosure of the precise information. The construction of the

financial report is considered as intricate job by the one who prepares the report and in certain

cases it is considered by the users and the investors that this information may not have been

explained in a precise manner. There has been a development in the corporate reporting

quality even when there lays an opportunity for making additional developments. The

construction of a proper connection of information within the annual report has gone ahead of

FINANCIAL ACCOUNTING

Answer to Question No 1

To,

The Chairperson

International Standard Accounting Board

35 Mayo Street, London- EX5CM 7HX, United Kingdom

Date: 17th September 2017

Subject: Guidance and recommendation for enhancing the communication and information

effectiveness in the financial report

Respected Sir,

Being an investor, I propose to construct certain plans in regards to the IASB

proposition in accordance to the efficiency of the information that is available within the

financial report. I have been looking to make certain investments in Westpac and ANZ,

which are two companies that are listed in the ASX. Due to this interest, I have assessed and

compared the annual report of the present accounting year of both the companies. During the

time of assessing the report, I have observed certain areas that can be developed for an

enhanced presentation and disclosure of the precise information. The construction of the

financial report is considered as intricate job by the one who prepares the report and in certain

cases it is considered by the users and the investors that this information may not have been

explained in a precise manner. There has been a development in the corporate reporting

quality even when there lays an opportunity for making additional developments. The

construction of a proper connection of information within the annual report has gone ahead of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ACCOUNTING

any description with respect to the character of linkage and underlining the associated

disclosure region.

The improper disclosure of the financial information wipes out the information that is

valuable and which are contained within the annual report and this aspect in certain cases is

not understood properly by the investors. These are the factors that restrict the investors and

make it tough to undertake any financial decisions that are feasible. I have been able to

establish the requirement for making an efficient interpretation of the communication after

evaluating the annual report of Westpac and ANZ Bank. Conversely, there is an existence of

certain differences in the disclosure of the information of both the companies. It has been

revealed that with respect to the construction of the financial statements and the disclosure of

information of both the companies, there is a requirement for generalization. I have well

made myself well informed with respect to the seven principles available in Section 2 of the

explanation paper that associates simple and clear, comparable, entity distinct, in a suitable

format, independent from irrelevant replication and constructed to focus on the essential

matters (Pelger, 2016). It has been explained after assessment of the annual report for

Westpac and ANZ Bank that they are in compliance with certain principles but has certain

faults in most of the sections.

The banks being a part of the financial institutions are needed to undertake a precise liquidity

and credit risk disclosure and undertake the sectional evaluation for moderating the investors

to take decisions with respect to the investment. The well known and the reputed banks needs

to reveal their information in such a manner so that it provides a pure image of the financial

condition within a glance that can only be gained by implementing certain efficient principles

that are absent. There is no segmental evaluation undertaken by ANZ Bank within their

financial report. Furthermore, segmental evaluation has not been undertaken by Westpac by

sustainably explaining the segments. Segmental evaluation has not been undertaken by ANZ

FINANCIAL ACCOUNTING

any description with respect to the character of linkage and underlining the associated

disclosure region.

The improper disclosure of the financial information wipes out the information that is

valuable and which are contained within the annual report and this aspect in certain cases is

not understood properly by the investors. These are the factors that restrict the investors and

make it tough to undertake any financial decisions that are feasible. I have been able to

establish the requirement for making an efficient interpretation of the communication after

evaluating the annual report of Westpac and ANZ Bank. Conversely, there is an existence of

certain differences in the disclosure of the information of both the companies. It has been

revealed that with respect to the construction of the financial statements and the disclosure of

information of both the companies, there is a requirement for generalization. I have well

made myself well informed with respect to the seven principles available in Section 2 of the

explanation paper that associates simple and clear, comparable, entity distinct, in a suitable

format, independent from irrelevant replication and constructed to focus on the essential

matters (Pelger, 2016). It has been explained after assessment of the annual report for

Westpac and ANZ Bank that they are in compliance with certain principles but has certain

faults in most of the sections.

The banks being a part of the financial institutions are needed to undertake a precise liquidity

and credit risk disclosure and undertake the sectional evaluation for moderating the investors

to take decisions with respect to the investment. The well known and the reputed banks needs

to reveal their information in such a manner so that it provides a pure image of the financial

condition within a glance that can only be gained by implementing certain efficient principles

that are absent. There is no segmental evaluation undertaken by ANZ Bank within their

financial report. Furthermore, segmental evaluation has not been undertaken by Westpac by

sustainably explaining the segments. Segmental evaluation has not been undertaken by ANZ

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ACCOUNTING

Bank and there is no individual analysis. Additionally, for toughening the regulations of the

banking industry, Basel has been implemented which an inclusive tool for a measure of

transformations. I have observed that there are individual disclosures that are necessary.

Conversely, very less data with respect to the same was explained in the financial statement

notes. In accordance to Westpac, there has been suitable explanation of the information and

the requirements about Basel and the information with respect to risk in the banking industry.

On the other hand, the financial statement of ANZ Bank does not have any data in regards to

Tier I and Tier II. On the other hand, Westpac have revealed disclosures about both the Tiers.

The divisional enactment of Westpac has been presented accurately in their financial report in

comparison to ANZ Bank who has not revealed this distinct aspect.

The financial annual reports of the companies should utilise the graphical process for

revealing their financial information that would make the investors ease down during the

assessment of the performance. By making use of the graphs it would be suitable in spite of

exploiting some descriptive disclosures as in certain cases such data becomes outmoded.

After undertaking the assessment of the financial reports and in respect to all the information

in regards to the above recognised disclosures, it has been regarded that interpretation of the

data in the annual report needs key developments. Certain principles of efficient

communications that requires implementing most of them into action are competent of

making entity distinct and comparable (Jorissen et al., 2014).

For making sure that interpretation is highlighted, the companies in certain cases consider the

combination of the investors. The investors look to recognise the value entity distinct data

and giving effective and enhancement of every segment, nucleus range of products is of

specific assistance. The companies should implement the information that forward seeking

and quantitative targets for computing the performance against the constructed strategic aims.

The principle of being entity distinct and the process with the help of which the data are

FINANCIAL ACCOUNTING

Bank and there is no individual analysis. Additionally, for toughening the regulations of the

banking industry, Basel has been implemented which an inclusive tool for a measure of

transformations. I have observed that there are individual disclosures that are necessary.

Conversely, very less data with respect to the same was explained in the financial statement

notes. In accordance to Westpac, there has been suitable explanation of the information and

the requirements about Basel and the information with respect to risk in the banking industry.

On the other hand, the financial statement of ANZ Bank does not have any data in regards to

Tier I and Tier II. On the other hand, Westpac have revealed disclosures about both the Tiers.

The divisional enactment of Westpac has been presented accurately in their financial report in

comparison to ANZ Bank who has not revealed this distinct aspect.

The financial annual reports of the companies should utilise the graphical process for

revealing their financial information that would make the investors ease down during the

assessment of the performance. By making use of the graphs it would be suitable in spite of

exploiting some descriptive disclosures as in certain cases such data becomes outmoded.

After undertaking the assessment of the financial reports and in respect to all the information

in regards to the above recognised disclosures, it has been regarded that interpretation of the

data in the annual report needs key developments. Certain principles of efficient

communications that requires implementing most of them into action are competent of

making entity distinct and comparable (Jorissen et al., 2014).

For making sure that interpretation is highlighted, the companies in certain cases consider the

combination of the investors. The investors look to recognise the value entity distinct data

and giving effective and enhancement of every segment, nucleus range of products is of

specific assistance. The companies should implement the information that forward seeking

and quantitative targets for computing the performance against the constructed strategic aims.

The principle of being entity distinct and the process with the help of which the data are

5

FINANCIAL ACCOUNTING

disclosed should be implemented by the companies. The data presented in the annual report is

improved and enhanced with respect to the entity situations rather than being common by

implementing the entity specific principle. It would be preferred and ideal by the investors to

look at the distinct data as they can simply access the standard information about the firms

from sources that are external. Additionally, the disclosed financial data and other precise

data should be helpful in making simple comparison among various periods of reporting that

need not negotiate the effectiveness of the data in the process of decision making.

The usefulness of the communication of the data can be developed by making use of precise

formatting as recognized by various stakeholders. There are several reports that are disclosed

by the financial institutions with respect to the usage of the graphs and tables for the

disclosure of the financial information. Conversely, there are doubts that are existent with

regards to the use of formats and hence, I would suggest making use of efficient formatting

for an enhanced communication of the data. I think that the investors would have a simple

process in undertaking the financial decisions if they are capable of comparing the

information and evaluate the pattern of the financial performance over several periods. The

development of the formats should be dependent and reliable on the factors that are entity

distinct. The international standards are needed to be developed in an intense guidance on the

use of the suitable format.

I would advise being an investor those certain principles of undertaking efficient

communication, which should be implemented by the companies. After the precise evaluation

of the financial statement of both the companies, some of the most efficient principles that

require to be implemented have been making use of precise formatting and entity distinct.

Yours Sincerely,

Malcolm Johnson

FINANCIAL ACCOUNTING

disclosed should be implemented by the companies. The data presented in the annual report is

improved and enhanced with respect to the entity situations rather than being common by

implementing the entity specific principle. It would be preferred and ideal by the investors to

look at the distinct data as they can simply access the standard information about the firms

from sources that are external. Additionally, the disclosed financial data and other precise

data should be helpful in making simple comparison among various periods of reporting that

need not negotiate the effectiveness of the data in the process of decision making.

The usefulness of the communication of the data can be developed by making use of precise

formatting as recognized by various stakeholders. There are several reports that are disclosed

by the financial institutions with respect to the usage of the graphs and tables for the

disclosure of the financial information. Conversely, there are doubts that are existent with

regards to the use of formats and hence, I would suggest making use of efficient formatting

for an enhanced communication of the data. I think that the investors would have a simple

process in undertaking the financial decisions if they are capable of comparing the

information and evaluate the pattern of the financial performance over several periods. The

development of the formats should be dependent and reliable on the factors that are entity

distinct. The international standards are needed to be developed in an intense guidance on the

use of the suitable format.

I would advise being an investor those certain principles of undertaking efficient

communication, which should be implemented by the companies. After the precise evaluation

of the financial statement of both the companies, some of the most efficient principles that

require to be implemented have been making use of precise formatting and entity distinct.

Yours Sincerely,

Malcolm Johnson

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ACCOUNTING

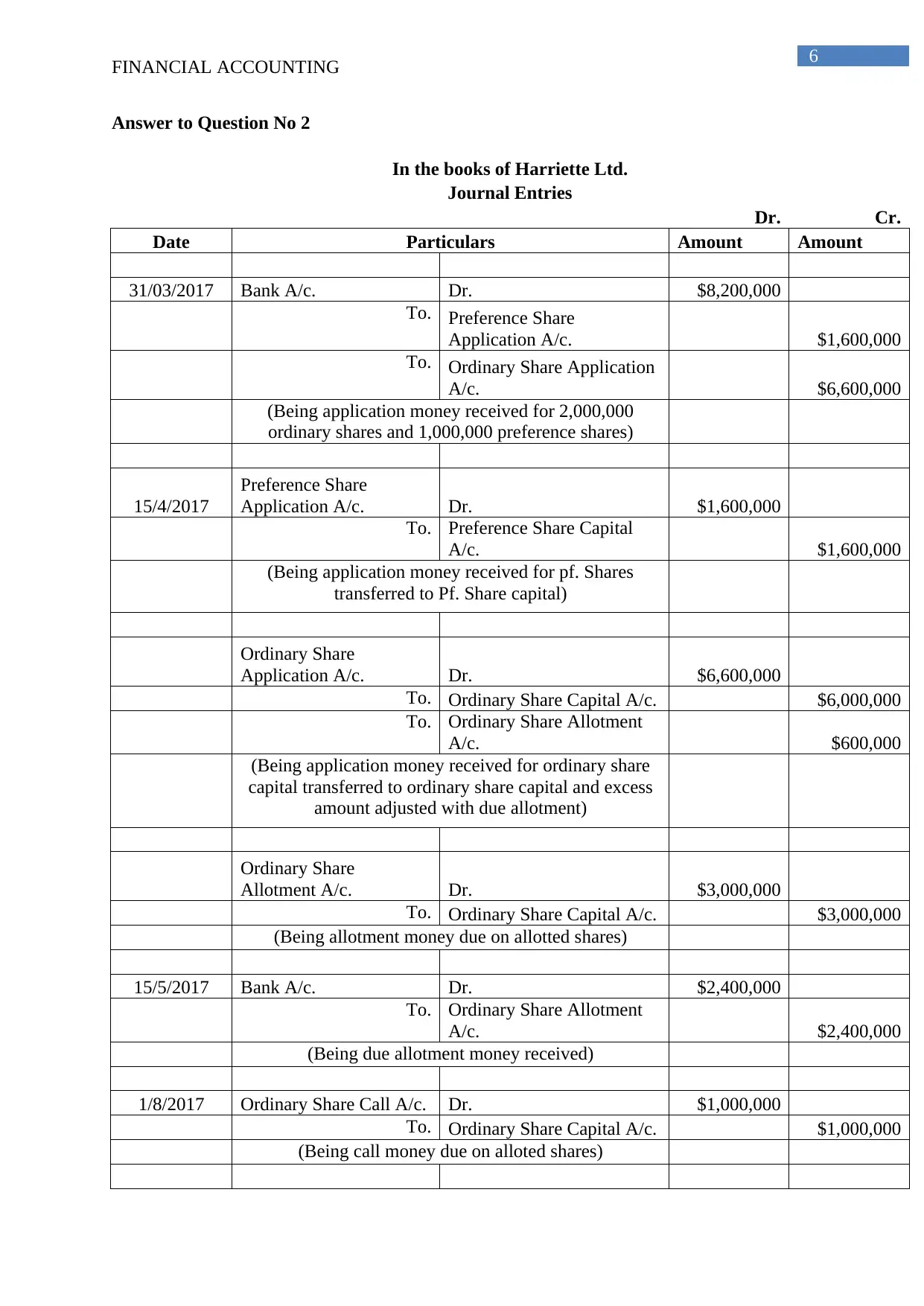

Answer to Question No 2

In the books of Harriette Ltd.

Journal Entries

Dr. Cr.

Date Particulars Amount Amount

31/03/2017 Bank A/c. Dr. $8,200,000

To. Preference Share

Application A/c. $1,600,000

To. Ordinary Share Application

A/c. $6,600,000

(Being application money received for 2,000,000

ordinary shares and 1,000,000 preference shares)

15/4/2017

Preference Share

Application A/c. Dr. $1,600,000

To. Preference Share Capital

A/c. $1,600,000

(Being application money received for pf. Shares

transferred to Pf. Share capital)

Ordinary Share

Application A/c. Dr. $6,600,000

To. Ordinary Share Capital A/c. $6,000,000

To. Ordinary Share Allotment

A/c. $600,000

(Being application money received for ordinary share

capital transferred to ordinary share capital and excess

amount adjusted with due allotment)

Ordinary Share

Allotment A/c. Dr. $3,000,000

To. Ordinary Share Capital A/c. $3,000,000

(Being allotment money due on allotted shares)

15/5/2017 Bank A/c. Dr. $2,400,000

To. Ordinary Share Allotment

A/c. $2,400,000

(Being due allotment money received)

1/8/2017 Ordinary Share Call A/c. Dr. $1,000,000

To. Ordinary Share Capital A/c. $1,000,000

(Being call money due on alloted shares)

FINANCIAL ACCOUNTING

Answer to Question No 2

In the books of Harriette Ltd.

Journal Entries

Dr. Cr.

Date Particulars Amount Amount

31/03/2017 Bank A/c. Dr. $8,200,000

To. Preference Share

Application A/c. $1,600,000

To. Ordinary Share Application

A/c. $6,600,000

(Being application money received for 2,000,000

ordinary shares and 1,000,000 preference shares)

15/4/2017

Preference Share

Application A/c. Dr. $1,600,000

To. Preference Share Capital

A/c. $1,600,000

(Being application money received for pf. Shares

transferred to Pf. Share capital)

Ordinary Share

Application A/c. Dr. $6,600,000

To. Ordinary Share Capital A/c. $6,000,000

To. Ordinary Share Allotment

A/c. $600,000

(Being application money received for ordinary share

capital transferred to ordinary share capital and excess

amount adjusted with due allotment)

Ordinary Share

Allotment A/c. Dr. $3,000,000

To. Ordinary Share Capital A/c. $3,000,000

(Being allotment money due on allotted shares)

15/5/2017 Bank A/c. Dr. $2,400,000

To. Ordinary Share Allotment

A/c. $2,400,000

(Being due allotment money received)

1/8/2017 Ordinary Share Call A/c. Dr. $1,000,000

To. Ordinary Share Capital A/c. $1,000,000

(Being call money due on alloted shares)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ACCOUNTING

1/9/2017 Bank A/c. Dr. $975,000

Calls-in-Arrear A/c. Dr. $25,000

To. Ordinary Share Call A/c. $1,000,000

(Being due call money received except for 50000

shares)

15/9/2017

Ordinary Share Capital

A/c. Dr. $250,000

To. Calls-in-Arrear A/c. $25,000

To. Ordinary Share Forfeiture

A/c. $225,000

(Being the 50000 shares, for which call money is due,

forfeited accordingly)

Bank A/c. Dr. $210,000

Ordinary Share

Forfeiture A/c. Dr. $40,000

To. Ordinary Share Capital A/c. $250,000

(Being the forfeited shares reissued for $4.20 per

shares)

Cost of Forfeiture &

Reissue A/c. Dr. $7,500

To. Bank A/c. $7,500

(Being cost of forfeiture and reissue of shares paid)

Ordinary Share

Forfeiture A/c. Dr. $185,000

To. Cost of Forfeiture &

Reissue A/c. $7,500

To. Capital Reserve A/c. $177,500

(Being the balance of share forfeiture a/c. after

adjusting with cost of forfeiture and reissue transferred

to capital reserve)

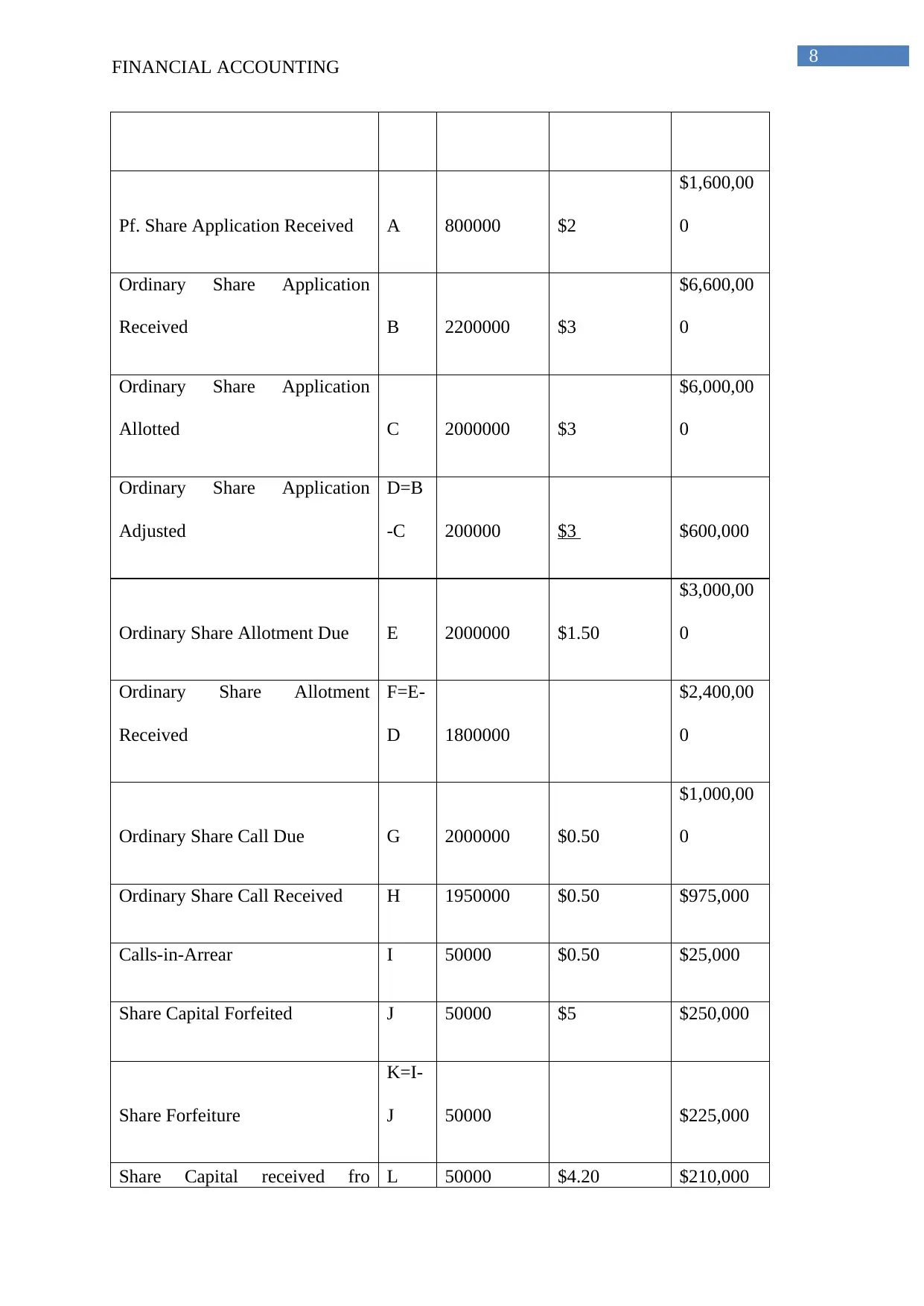

Workings:

Particulars

Nos. Of

Shares

Value per

Share Amount

FINANCIAL ACCOUNTING

1/9/2017 Bank A/c. Dr. $975,000

Calls-in-Arrear A/c. Dr. $25,000

To. Ordinary Share Call A/c. $1,000,000

(Being due call money received except for 50000

shares)

15/9/2017

Ordinary Share Capital

A/c. Dr. $250,000

To. Calls-in-Arrear A/c. $25,000

To. Ordinary Share Forfeiture

A/c. $225,000

(Being the 50000 shares, for which call money is due,

forfeited accordingly)

Bank A/c. Dr. $210,000

Ordinary Share

Forfeiture A/c. Dr. $40,000

To. Ordinary Share Capital A/c. $250,000

(Being the forfeited shares reissued for $4.20 per

shares)

Cost of Forfeiture &

Reissue A/c. Dr. $7,500

To. Bank A/c. $7,500

(Being cost of forfeiture and reissue of shares paid)

Ordinary Share

Forfeiture A/c. Dr. $185,000

To. Cost of Forfeiture &

Reissue A/c. $7,500

To. Capital Reserve A/c. $177,500

(Being the balance of share forfeiture a/c. after

adjusting with cost of forfeiture and reissue transferred

to capital reserve)

Workings:

Particulars

Nos. Of

Shares

Value per

Share Amount

8

FINANCIAL ACCOUNTING

Pf. Share Application Received A 800000 $2

$1,600,00

0

Ordinary Share Application

Received B 2200000 $3

$6,600,00

0

Ordinary Share Application

Allotted C 2000000 $3

$6,000,00

0

Ordinary Share Application

Adjusted

D=B

-C 200000 $3 $600,000

Ordinary Share Allotment Due E 2000000 $1.50

$3,000,00

0

Ordinary Share Allotment

Received

F=E-

D 1800000

$2,400,00

0

Ordinary Share Call Due G 2000000 $0.50

$1,000,00

0

Ordinary Share Call Received H 1950000 $0.50 $975,000

Calls-in-Arrear I 50000 $0.50 $25,000

Share Capital Forfeited J 50000 $5 $250,000

Share Forfeiture

K=I-

J 50000 $225,000

Share Capital received fro L 50000 $4.20 $210,000

FINANCIAL ACCOUNTING

Pf. Share Application Received A 800000 $2

$1,600,00

0

Ordinary Share Application

Received B 2200000 $3

$6,600,00

0

Ordinary Share Application

Allotted C 2000000 $3

$6,000,00

0

Ordinary Share Application

Adjusted

D=B

-C 200000 $3 $600,000

Ordinary Share Allotment Due E 2000000 $1.50

$3,000,00

0

Ordinary Share Allotment

Received

F=E-

D 1800000

$2,400,00

0

Ordinary Share Call Due G 2000000 $0.50

$1,000,00

0

Ordinary Share Call Received H 1950000 $0.50 $975,000

Calls-in-Arrear I 50000 $0.50 $25,000

Share Capital Forfeited J 50000 $5 $250,000

Share Forfeiture

K=I-

J 50000 $225,000

Share Capital received fro L 50000 $4.20 $210,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL ACCOUNTING

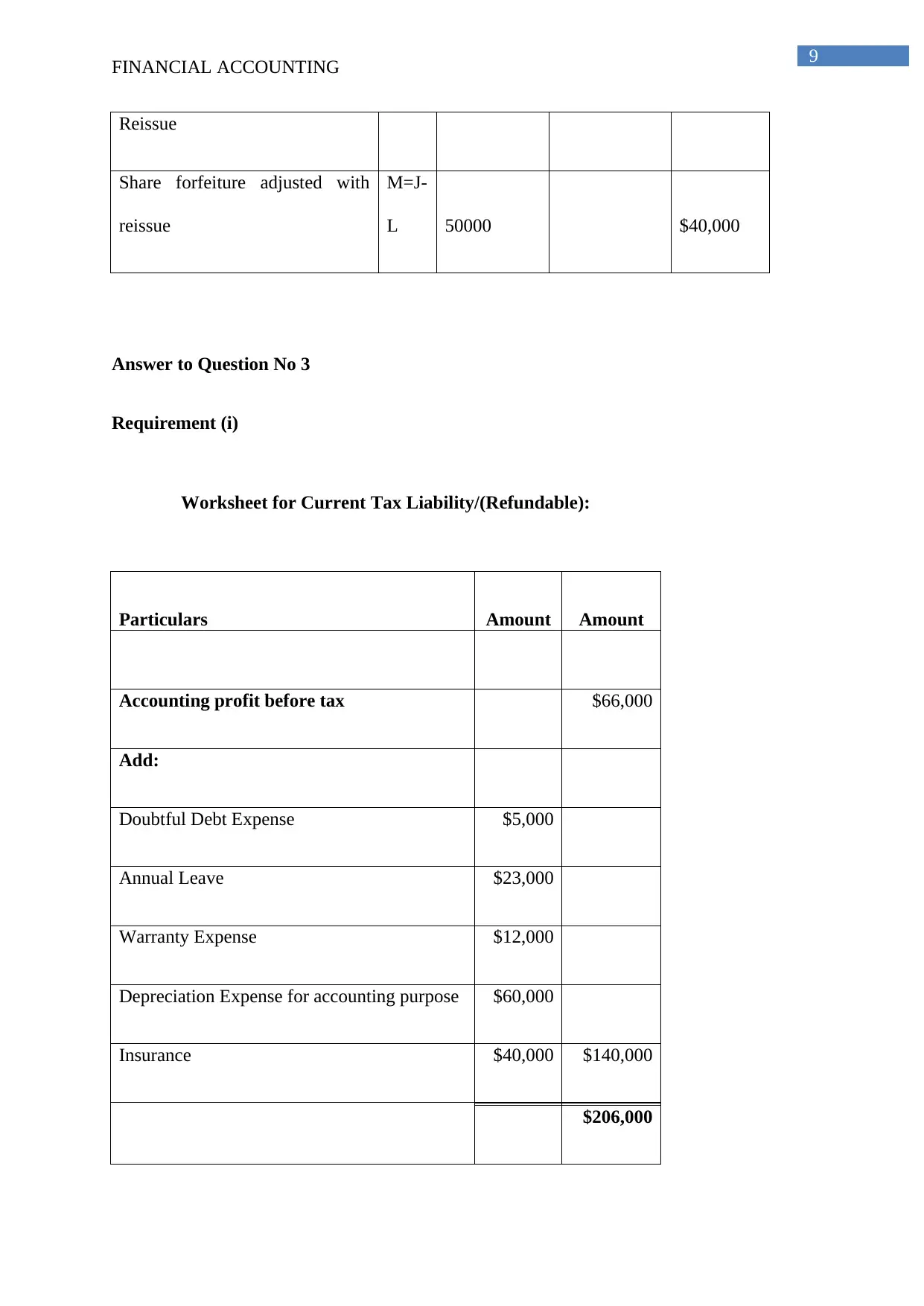

Reissue

Share forfeiture adjusted with

reissue

M=J-

L 50000 $40,000

Answer to Question No 3

Requirement (i)

Worksheet for Current Tax Liability/(Refundable):

Particulars Amount Amount

Accounting profit before tax $66,000

Add:

Doubtful Debt Expense $5,000

Annual Leave $23,000

Warranty Expense $12,000

Depreciation Expense for accounting purpose $60,000

Insurance $40,000 $140,000

$206,000

FINANCIAL ACCOUNTING

Reissue

Share forfeiture adjusted with

reissue

M=J-

L 50000 $40,000

Answer to Question No 3

Requirement (i)

Worksheet for Current Tax Liability/(Refundable):

Particulars Amount Amount

Accounting profit before tax $66,000

Add:

Doubtful Debt Expense $5,000

Annual Leave $23,000

Warranty Expense $12,000

Depreciation Expense for accounting purpose $60,000

Insurance $40,000 $140,000

$206,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

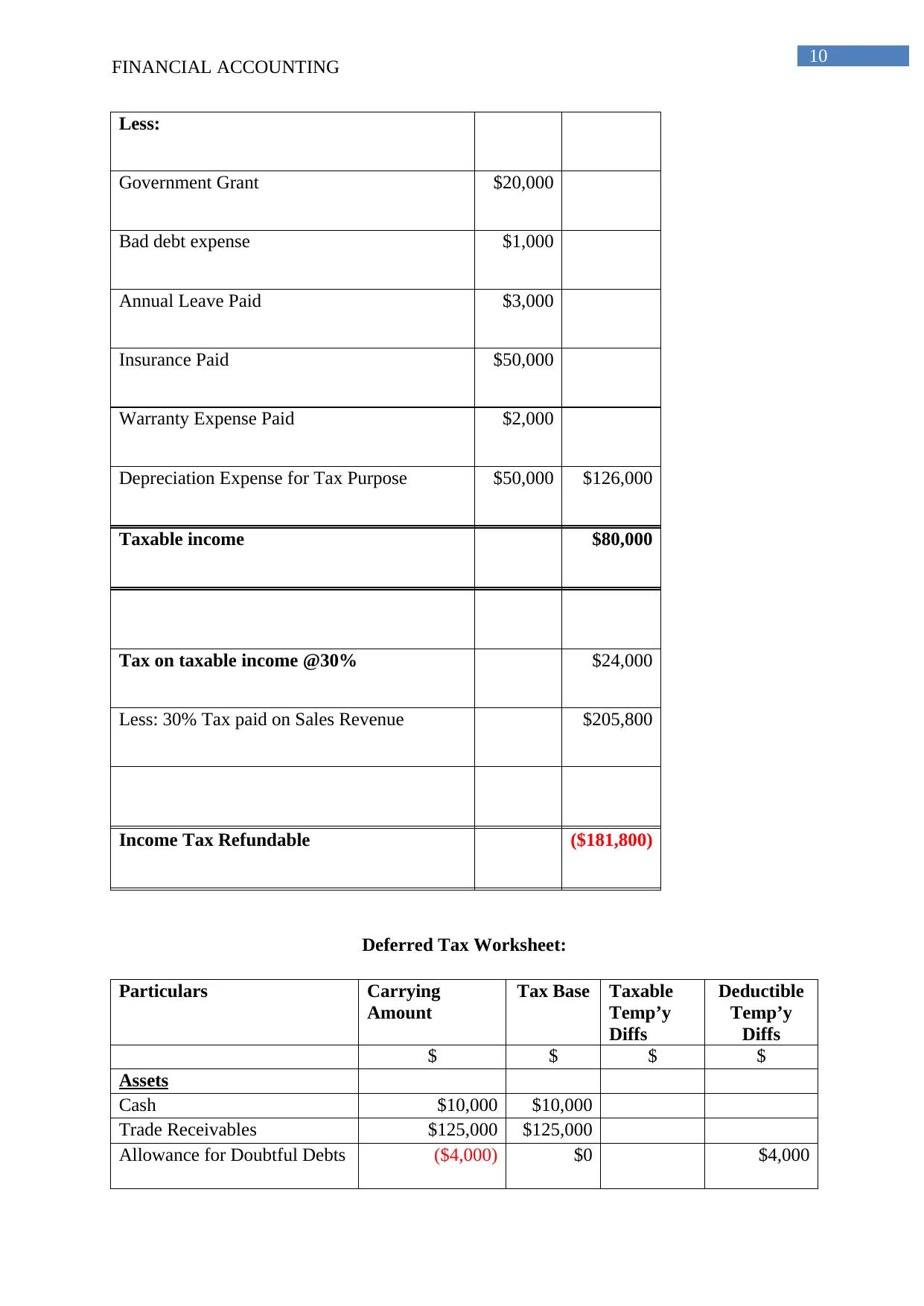

FINANCIAL ACCOUNTING

Less:

Government Grant $20,000

Bad debt expense $1,000

Annual Leave Paid $3,000

Insurance Paid $50,000

Warranty Expense Paid $2,000

Depreciation Expense for Tax Purpose $50,000 $126,000

Taxable income $80,000

Tax on taxable income @30% $24,000

Less: 30% Tax paid on Sales Revenue $205,800

Income Tax Refundable ($181,800)

Deferred Tax Worksheet:

Particulars Carrying

Amount

Tax Base Taxable

Temp’y

Diffs

Deductible

Temp’y

Diffs

$ $ $ $

Assets

Cash $10,000 $10,000

Trade Receivables $125,000 $125,000

Allowance for Doubtful Debts ($4,000) $0 $4,000

FINANCIAL ACCOUNTING

Less:

Government Grant $20,000

Bad debt expense $1,000

Annual Leave Paid $3,000

Insurance Paid $50,000

Warranty Expense Paid $2,000

Depreciation Expense for Tax Purpose $50,000 $126,000

Taxable income $80,000

Tax on taxable income @30% $24,000

Less: 30% Tax paid on Sales Revenue $205,800

Income Tax Refundable ($181,800)

Deferred Tax Worksheet:

Particulars Carrying

Amount

Tax Base Taxable

Temp’y

Diffs

Deductible

Temp’y

Diffs

$ $ $ $

Assets

Cash $10,000 $10,000

Trade Receivables $125,000 $125,000

Allowance for Doubtful Debts ($4,000) $0 $4,000

11

FINANCIAL ACCOUNTING

Inventories $60,000 $60,000

Prepaid Insurance $10,000 $10,000

Goodwill $20,000 $20,000

Equipment $300,000 $300,000

Accumulated Depreciation ($60,000) ($50,000) $10,000

Liabilities

Trade Payables $35,000 $35,000

Provision for Warranties $10,000 $10,000

Provision for Annual Leave $20,000 $20,000

Loan Payable $90,000 $90,000

Total Temporary differences $10,000 $44,000

Deferred tax liability (30%) $3,000

Deferred tax asset (30%) $13,200

Requirement (ii)

Dr. Cr.

Date Particulars Amount Amount

30/06/201

7 Income Tax Expense A/c. Dr. $24,000

Income Tax Refundable

A/c. Dr. $181,800

To, Advance Tax Paid A/c. $205,800

(Being Income tax expenses adjusterd with advance

tax paid and income tax refundable recorded)

$13,200

Deferred Tax Assets A/c. Dr. $3,000

To,

Deferred Tax Liability

A/c. $10,200

To,

Income Tax Expense

A/c.

(Being deferred tax assets and deferred tax liabilities

recorded)

Profit & loss A/c. $21,000

To,

Income Tax Expense

A/c. $21,000

(Being income tax expense transferred to P/L A/c.)

FINANCIAL ACCOUNTING

Inventories $60,000 $60,000

Prepaid Insurance $10,000 $10,000

Goodwill $20,000 $20,000

Equipment $300,000 $300,000

Accumulated Depreciation ($60,000) ($50,000) $10,000

Liabilities

Trade Payables $35,000 $35,000

Provision for Warranties $10,000 $10,000

Provision for Annual Leave $20,000 $20,000

Loan Payable $90,000 $90,000

Total Temporary differences $10,000 $44,000

Deferred tax liability (30%) $3,000

Deferred tax asset (30%) $13,200

Requirement (ii)

Dr. Cr.

Date Particulars Amount Amount

30/06/201

7 Income Tax Expense A/c. Dr. $24,000

Income Tax Refundable

A/c. Dr. $181,800

To, Advance Tax Paid A/c. $205,800

(Being Income tax expenses adjusterd with advance

tax paid and income tax refundable recorded)

$13,200

Deferred Tax Assets A/c. Dr. $3,000

To,

Deferred Tax Liability

A/c. $10,200

To,

Income Tax Expense

A/c.

(Being deferred tax assets and deferred tax liabilities

recorded)

Profit & loss A/c. $21,000

To,

Income Tax Expense

A/c. $21,000

(Being income tax expense transferred to P/L A/c.)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.