Table of Contents Introduction to Financial Accounting

32 Pages3577 Words353 Views

Added on 2020-07-23

About This Document

Defining financial accounting In the current times, in UK, it is mandatory for business units listed on stock exchange to prepare and present financial statements at the end of accounting year. Defining financial accounting In the current times, in UK, it is mandatory for business units listed on stock exchange to prepare and present financial statements at the end of accounting year. Specifically, there are mainly three types of statements which are prepared by business organization such as: Income statement: In this statement, manager records revenue

Table of Contents Introduction to Financial Accounting

Added on 2020-07-23

ShareRelated Documents

Financial Accounting1

TABLE OF CONTENTSINTRODUCTION......................................................................................................................31. Defining financial accounting............................................................................................32. Presenting key regulations which are associated with financial accounting......................43. Stating concept of accounting rules and principles............................................................44. Explaining concept and convention of consistency and materiality..................................5CLIENT 1...................................................................................................................................5a. Journal entries.....................................................................................................................5b. Ledgers account.................................................................................................................7c. Trial balance.....................................................................................................................15CLIENT 2.................................................................................................................................15a. Income statement..............................................................................................................15b. Balance sheet....................................................................................................................16CLIENT 3.................................................................................................................................18a. Profitability statement of Raintree Ltd.............................................................................18b. Presenting statement of financial position for Raintree Ltd.............................................19c. Stating prudence and consistency concept of accounting................................................19d. Evaluating methods of depreciation.................................................................................20CLIENT 4.................................................................................................................................21A. Stating the purpose of bank reconciliation statement......................................................21B. Presenting reasons due to which balance of cash and pass book varies..........................22C. Bank reconciliation..........................................................................................................22CLIENT 5.................................................................................................................................24a. Preparing Henderson’s sales and purchase ledger...........................................................241............................................................................................................................................242............................................................................................................................................252

b. Defining control account..................................................................................................25CLIENT 6.................................................................................................................................26a. Presenting suspense account and its features...................................................................26b. Trial balance and usage of control accounts....................................................................27c. Rectification of accounting entries...................................................................................28d. Difference between suspense and clearing account.........................................................29CONCLUSION........................................................................................................................29REFERENCES.........................................................................................................................303

INTRODUCTION Financial accounting field lays high level of emphasis on summarizing, analyzing andreporting of monetary transactions. Tools and techniques of financial accounting help intracking business performance over the period. Now, from sole traders to publicly listedorganizations prepare financial statement for assessing the extent to which their performanceimproved over time frame. The present report is based on varied situation which will presenthow journal and ledger helps in preparing trial balance and thereby final accounts. Besidesthis, report will develop understanding regarding accounting concepts and principles. Further,report also depicts how bank reconciliation assists business unit in getting information aboutmonetary aspects. Further, concept of suspense, clearing and control account will also bedescribed related to FA. 1. Defining financial accounting In the current times, in UK, it is mandatory for business units listed on stock exchangeprepare and present financial statements at the end of accounting year. Besides this, soletraders tend to focus on the preparation of income statement to ascertain income generateover expenses. Hence, by recording all the business transactions business entities preparefinal account which in turn considered as financial accounting. Specifically, there are mainlythree types of statements which are prepared by business organization such as:Income statement: In this statement, manager records revenue and expenses related tofinancial year. The main motive behind the preparation of such statement to identifyincome generated over expenses. Income aspects of profitability statement includesales revenue, dividend and interest received (Warren and Jones, 2018). On the otherside, expenditures side of income statement includes both direct and indirect.Material, labour and overhead are recognized as direct expenses. In contrast to this,selling and distribution, administration etc are depicted as indirect expenses. Hence,by subtracting expenses from income generated one can determine net margin. Balance sheet: Statement of financial position furnishes information about the levelof assets, liability and shareholder’s equity. Hence, by making evaluation of balance4

sheet firm and its stakeholders can assess the extent to which liquidity and solvencyposition of company is good. Cash flow statement: This statement entails position of cash inflows under threedifferent categories such as operating, investing and financing activities. Byundertaking such statement, firm can assess its cash position at the end of accountingperiod.Hence, by undertaking accounting concept, principles, rules and regulations al the abovedepicted are prepared by business unit. 2. Presenting key regulations which are associated with financial accounting In UK, majority of the companies prepare financial statements by complying withrules of GAAP related to such country. In addition to this, there are several companies thatperform activities and functions internationally. Hence, now companies that have globaloperations lay focus on undertaking IASB and FRS for recording as well as presentingbusiness transactions (Larson, Lewis and Spilker, 2017). Hence, by preparing final accountson the basis of such globalized rules firm can satisfy information need of stakeholders to agreat extent. 3. Stating concept of accounting rules and principlesAccounting year concept: On the basis of such concept business unit should preparestatements for the specific time frame such as quarterly, half yearly and annually. Going concern concept: It may be served as a fundamental principle of accountingwhich believes that firm will continue its operations for longer time frame (GoingConcern Concept, 2017). Accrual concept: In financial accounting, accrual concept presents that expenses andincome needs to be recorded in the concerned period they occur irrespective of cashaspect. Hence, such approach helps in presenting fair view of financial aspects byreflecting all expenses associated with revenue with respect to specified time frame.Money measurement concept: Such accounting concept presents that onlyinformation which can be presented in monetary form included under final accounts(Narayanaswamy, 2017). Hence, non-financial information such as customer base,employee’s capabilities are not considered as part of final accounts due to itsqualitative nature. 5

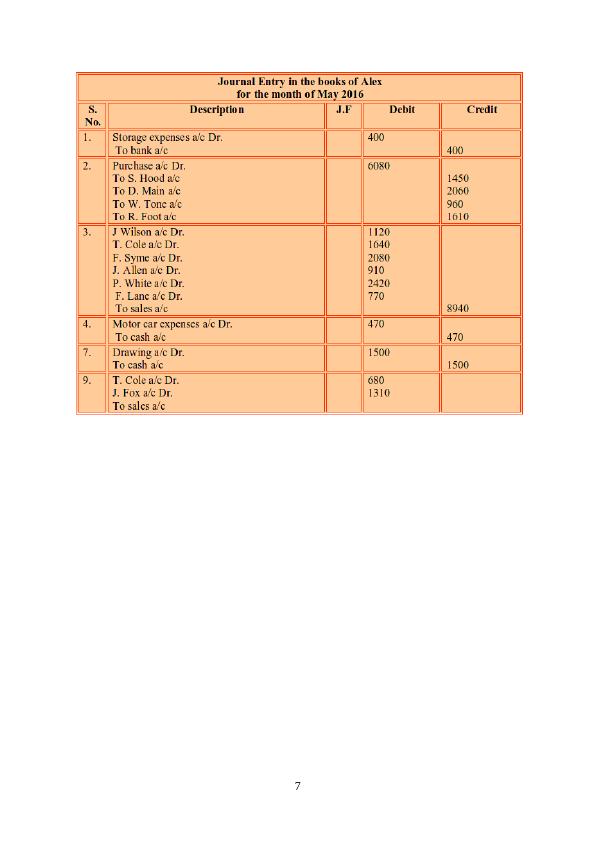

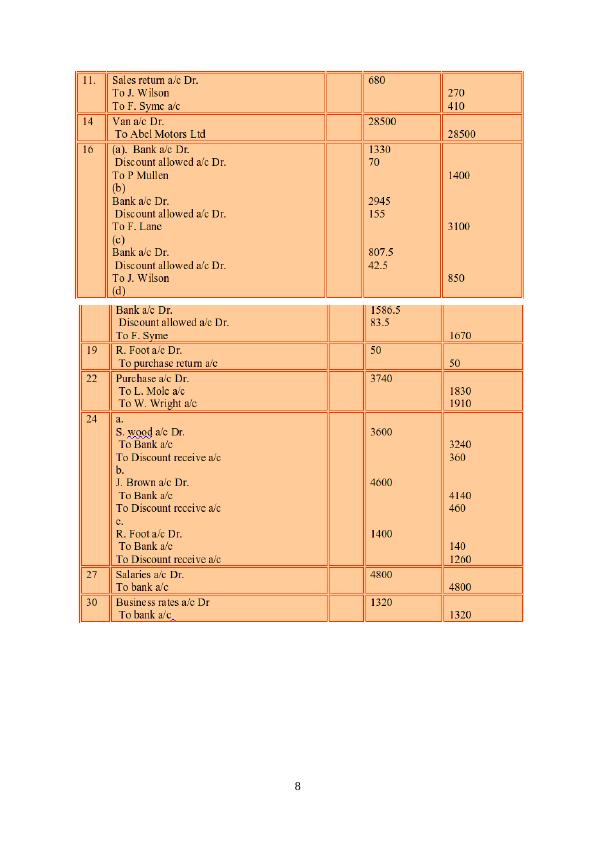

Dual aspect concept: According to such concept, each business transaction has dualeffect under financial statements in terms of debit and credit. For instance: Salesworth of £2000 made in against to cash. In this, two accounts will be affected such assales (credit) and cash (debit) with related figures. Assets: Liabilities + owner’s equity4. Explaining concept and convention of consistency and materiality Consistency principle: As per such concept, firm should focus on following similarrules in each accounting year that leads comparability. Further, such concept relies onthe aspect that firm needs to mention reason behind making changes in specificmethod and its impact on financial outcomes (Maynard, 2017). Materiality concept: This concept or principle entails that business unit should reflectall material information in its financial statements and notes that may have an impacton the decision making aspect of stakeholders. CLIENT 1a. Journal entries Journal of Alex Study’s for the period of 2017 is as follows: 6

7

8

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial accounting Field PDFlg...

|32

|3855

|370

Assignment on Financial Accounting pdflg...

|47

|5713

|177

Report on Accounting Conventions and Principleslg...

|34

|3968

|114

Financial Accounting Principles - Assignmentlg...

|37

|4664

|305

Importance of Accounting in Preparation of Financial Statements - Reportlg...

|34

|4240

|26

Financial Accounting: Assignment Samplelg...

|37

|5577

|390