Financial Accounting of sole trader and the limited companies

VerifiedAdded on 2021/02/20

|30

|4643

|34

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

a. Explaining the meaning and the purpose of financial accounting...........................................2

Difference in between financial accounting and management accounting ................................3

b. Two internal stakeholder and four external stakeholders important in the organisation. ......4

Client 1.............................................................................................................................................6

I. Recording and classification of the journal entries..................................................................6

........................................................................................................................................................11

........................................................................................................................................................12

ii. Preparation of the trial balance.............................................................................................15

Client 2...........................................................................................................................................16

a. Preparation of the income statement.....................................................................................16

b. Statement of balance sheet....................................................................................................17

c. Explaining the consistency and the prudence concept..........................................................18

d. Describing purpose of the depreciation and its methods .....................................................18

e. Evaluating the difference in between the financial statements of the sole trader and the

limited companies.....................................................................................................................19

Client 3...........................................................................................................................................19

a. Explaining the meaning and the purpose of the bank reconciliation statement ...................19

b. Listing down the areas where bank records can vary from the cash statement....................20

c. Explaining the imprest under the system of petty cash.........................................................20

d. Preparation of bank reconciliation statement........................................................................21

Client 4...........................................................................................................................................22

a. Preparing sales and the purchase ledger account..................................................................22

...................................................................................................................................................22

b. Explaining the meaning of the control account.....................................................................22

Client 5...........................................................................................................................................23

a. Explaining the meaning of suspense account and its features...............................................23

b. Drafting a trial balance .........................................................................................................23

INTRODUCTION...........................................................................................................................1

a. Explaining the meaning and the purpose of financial accounting...........................................2

Difference in between financial accounting and management accounting ................................3

b. Two internal stakeholder and four external stakeholders important in the organisation. ......4

Client 1.............................................................................................................................................6

I. Recording and classification of the journal entries..................................................................6

........................................................................................................................................................11

........................................................................................................................................................12

ii. Preparation of the trial balance.............................................................................................15

Client 2...........................................................................................................................................16

a. Preparation of the income statement.....................................................................................16

b. Statement of balance sheet....................................................................................................17

c. Explaining the consistency and the prudence concept..........................................................18

d. Describing purpose of the depreciation and its methods .....................................................18

e. Evaluating the difference in between the financial statements of the sole trader and the

limited companies.....................................................................................................................19

Client 3...........................................................................................................................................19

a. Explaining the meaning and the purpose of the bank reconciliation statement ...................19

b. Listing down the areas where bank records can vary from the cash statement....................20

c. Explaining the imprest under the system of petty cash.........................................................20

d. Preparation of bank reconciliation statement........................................................................21

Client 4...........................................................................................................................................22

a. Preparing sales and the purchase ledger account..................................................................22

...................................................................................................................................................22

b. Explaining the meaning of the control account.....................................................................22

Client 5...........................................................................................................................................23

a. Explaining the meaning of suspense account and its features...............................................23

b. Drafting a trial balance .........................................................................................................23

c. Rectification of errors ...........................................................................................................24

CONCLUSION..............................................................................................................................24

REFERENCES..............................................................................................................................25

CONCLUSION..............................................................................................................................24

REFERENCES..............................................................................................................................25

INTRODUCTION

FA is a process which is used by company to keep a day to day record of company financial

activities. In this transaction are recorded, summarized and stipulated to examined the stability of

the company and also enhances the position to take risk in the business for some new projects

(Schaltegger and Burritt, 2017). The main purpose to prepared financial accounting is that to

helps company to take effective decision and also prepare the financial report which is to be

presented at the time when it is demanded by the stakeholders. Usually the financial statement

reflect the income and expenditure of an enterprise to maintain the b/s of the company in

summarized way. To prepared the financial accounting proper department is established to

analyse their financial transaction and also prepare their financial report and present them in

effective manner.

This report will incudes the meaning of FA and analysis of all the stakeholders within

the company. It includes the formulation of final accounts in respect of proprietors, partnership

and the limited liability organizations in context of its various principles, convention and

standards. It further includes the descriptive of bank reconciliation statement which ensure the

company and bank records. The report concludes with the matter to reconcile accounts which is

to be shifted in recorded transaction to establish the right accounts in the company.

1

FA is a process which is used by company to keep a day to day record of company financial

activities. In this transaction are recorded, summarized and stipulated to examined the stability of

the company and also enhances the position to take risk in the business for some new projects

(Schaltegger and Burritt, 2017). The main purpose to prepared financial accounting is that to

helps company to take effective decision and also prepare the financial report which is to be

presented at the time when it is demanded by the stakeholders. Usually the financial statement

reflect the income and expenditure of an enterprise to maintain the b/s of the company in

summarized way. To prepared the financial accounting proper department is established to

analyse their financial transaction and also prepare their financial report and present them in

effective manner.

This report will incudes the meaning of FA and analysis of all the stakeholders within

the company. It includes the formulation of final accounts in respect of proprietors, partnership

and the limited liability organizations in context of its various principles, convention and

standards. It further includes the descriptive of bank reconciliation statement which ensure the

company and bank records. The report concludes with the matter to reconcile accounts which is

to be shifted in recorded transaction to establish the right accounts in the company.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial accounting

It is the main branch categorised as of accounting in which, financial accounting assists

traces the financial transactions of a company. There are standard guidelines which are used in

recording, presenting and summarizing in a financial report which includes balance sheet or

income statements (Männasoo, Maripuu and Hazak, 2018). This accounting serves for interest of

stakeholders, owners, creditors, etc. Companies generally issue financial statements on a daily

basis for providing regular data and other related information to the interested people.

The standard format of financial accounting relates to double entry book keeping in

which the transaction are recorded under credit and debit side. Along with it, the accrual basis of

account concept is followed under financial accounting. This concept represents that the revenue

are recorded only when it has earned even amount is not received. The financial accounting

reports is prepared under the guidelines of GAAP. The financial reports comprise income

statements, cash flow & retained earning statements. These statements are framed under GAAP

and IFRS guidelines.

a. Explaining the meaning and the purpose of financial accounting

Purpose of financial accounting

Provide information to interested individuals - The main purpose for which financial

accounting is prepared under business is to gather financial report and offer important and

relevant information about the action taken by the firm to parties like creditors, taxation

authority, investors, etc. Also, these reports of financial accounting is helpful to ascertain cash

flows within a business (Persson, Radcliffe, and Stein, 2018.). The reports are prepared for the

purpose of providing guidelines for future investment for reaching to decision making and

increase the profitability of a business organisation.

Determining cash flows for future investments - It is the main purpose of financial

accounting for assisting the detail of cash flows under which cash inflows and cash outflows are

determined. Every statements of financial accounting is different from each other and contain

different information as well in relation to business operations. The purpose satisfies by

developing financial reports for the use of critical business decisions by owners or stock holders

of a company.

Act as an evidence in case of dispute - It is also prepared for the purpose for the use of

an evidence in which these records are taken as legal evidence in case of any dispute arises in the

It is the main branch categorised as of accounting in which, financial accounting assists

traces the financial transactions of a company. There are standard guidelines which are used in

recording, presenting and summarizing in a financial report which includes balance sheet or

income statements (Männasoo, Maripuu and Hazak, 2018). This accounting serves for interest of

stakeholders, owners, creditors, etc. Companies generally issue financial statements on a daily

basis for providing regular data and other related information to the interested people.

The standard format of financial accounting relates to double entry book keeping in

which the transaction are recorded under credit and debit side. Along with it, the accrual basis of

account concept is followed under financial accounting. This concept represents that the revenue

are recorded only when it has earned even amount is not received. The financial accounting

reports is prepared under the guidelines of GAAP. The financial reports comprise income

statements, cash flow & retained earning statements. These statements are framed under GAAP

and IFRS guidelines.

a. Explaining the meaning and the purpose of financial accounting

Purpose of financial accounting

Provide information to interested individuals - The main purpose for which financial

accounting is prepared under business is to gather financial report and offer important and

relevant information about the action taken by the firm to parties like creditors, taxation

authority, investors, etc. Also, these reports of financial accounting is helpful to ascertain cash

flows within a business (Persson, Radcliffe, and Stein, 2018.). The reports are prepared for the

purpose of providing guidelines for future investment for reaching to decision making and

increase the profitability of a business organisation.

Determining cash flows for future investments - It is the main purpose of financial

accounting for assisting the detail of cash flows under which cash inflows and cash outflows are

determined. Every statements of financial accounting is different from each other and contain

different information as well in relation to business operations. The purpose satisfies by

developing financial reports for the use of critical business decisions by owners or stock holders

of a company.

Act as an evidence in case of dispute - It is also prepared for the purpose for the use of

an evidence in which these records are taken as legal evidence in case of any dispute arises in the

company (Coyne, Coyne and Walker, 2018). Along with it, this also lay an appropriate financial

information which can facilitate company to avail facility of credit from lenders as good

financial records create goodwill of the company among creditors.

Profit comparison for determining actual position - At last, the financial statements are

developed for the purpose of comparison of profit which are well analysed by the maintained

records of current year with the previous year. This company is able to measure their

performance from the past year statements with that of current year statements. Theses figures

enables the company in ascertaining their positions.

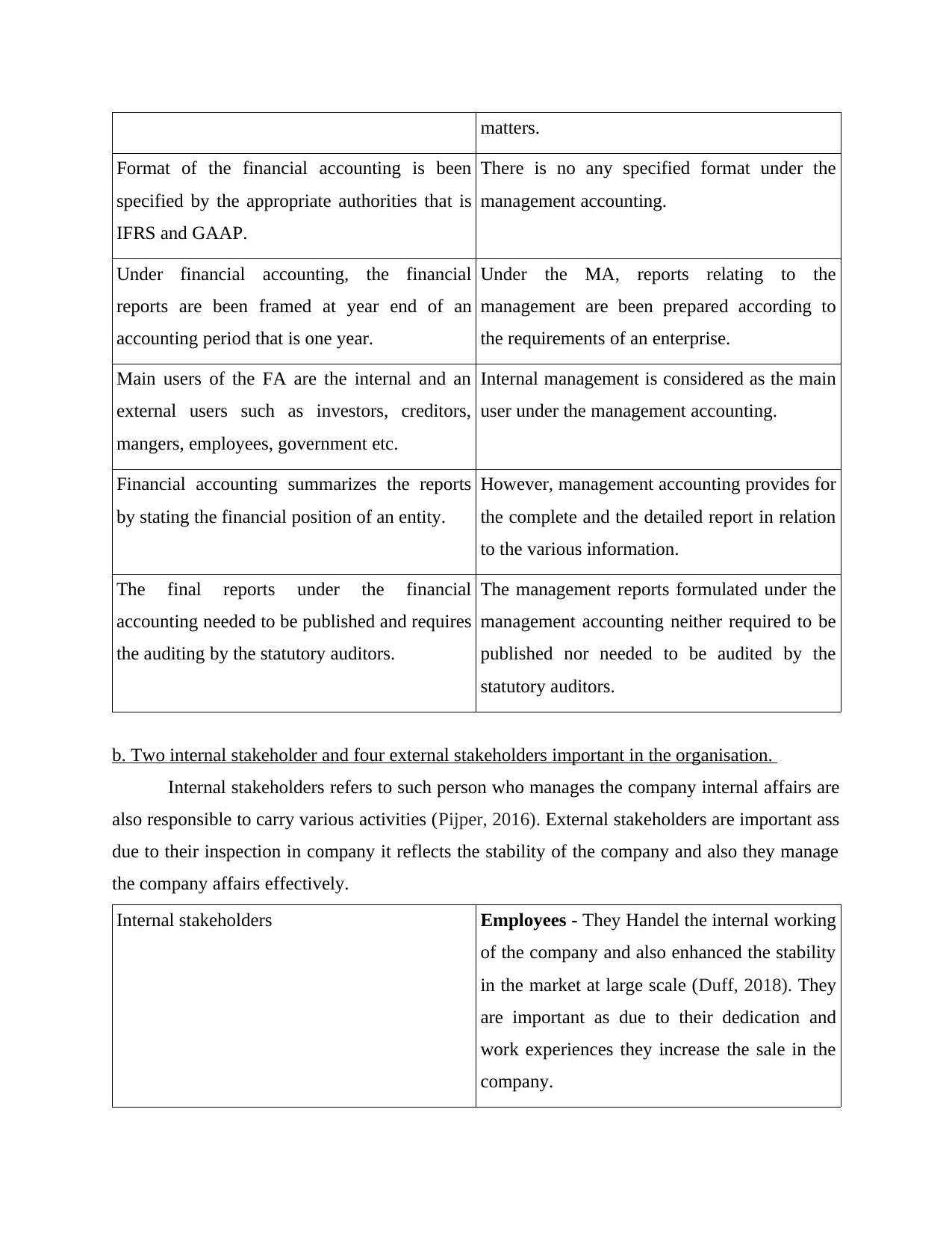

Difference in between financial accounting and management accounting

Financial accounting Management accounting

It refers to the accounting system that

emphasize on the formulation of the financial

statements in order to provide the financial

information to the users or the interested

parties.

It means the accounting system that provides

the relevant information to mangers in making

the policies, procedures and in developing the

strategies for the purpose of running the

business effectively and efficiently (Difference

Between Financial Accounting and

Management Accounting, 2019).

Financial accounting provides for only the

monetary information and does not accounts

for the non-monetary information.

It facilitates both monetary as well as the non-

monetary information.

It is compulsory for all the organization. It is not compulsory for each and every

organization to opt for management

accounting.

The main objective of the financial accounting

is to facilitate the financial information to the

outsiders.

The primary objective of MA to help the

management within the organization in respect

of planning and making suitable decisions by

facilitating the information on the several

information which can facilitate company to avail facility of credit from lenders as good

financial records create goodwill of the company among creditors.

Profit comparison for determining actual position - At last, the financial statements are

developed for the purpose of comparison of profit which are well analysed by the maintained

records of current year with the previous year. This company is able to measure their

performance from the past year statements with that of current year statements. Theses figures

enables the company in ascertaining their positions.

Difference in between financial accounting and management accounting

Financial accounting Management accounting

It refers to the accounting system that

emphasize on the formulation of the financial

statements in order to provide the financial

information to the users or the interested

parties.

It means the accounting system that provides

the relevant information to mangers in making

the policies, procedures and in developing the

strategies for the purpose of running the

business effectively and efficiently (Difference

Between Financial Accounting and

Management Accounting, 2019).

Financial accounting provides for only the

monetary information and does not accounts

for the non-monetary information.

It facilitates both monetary as well as the non-

monetary information.

It is compulsory for all the organization. It is not compulsory for each and every

organization to opt for management

accounting.

The main objective of the financial accounting

is to facilitate the financial information to the

outsiders.

The primary objective of MA to help the

management within the organization in respect

of planning and making suitable decisions by

facilitating the information on the several

matters.

Format of the financial accounting is been

specified by the appropriate authorities that is

IFRS and GAAP.

There is no any specified format under the

management accounting.

Under financial accounting, the financial

reports are been framed at year end of an

accounting period that is one year.

Under the MA, reports relating to the

management are been prepared according to

the requirements of an enterprise.

Main users of the FA are the internal and an

external users such as investors, creditors,

mangers, employees, government etc.

Internal management is considered as the main

user under the management accounting.

Financial accounting summarizes the reports

by stating the financial position of an entity.

However, management accounting provides for

the complete and the detailed report in relation

to the various information.

The final reports under the financial

accounting needed to be published and requires

the auditing by the statutory auditors.

The management reports formulated under the

management accounting neither required to be

published nor needed to be audited by the

statutory auditors.

b. Two internal stakeholder and four external stakeholders important in the organisation.

Internal stakeholders refers to such person who manages the company internal affairs are

also responsible to carry various activities (Pijper, 2016). External stakeholders are important ass

due to their inspection in company it reflects the stability of the company and also they manage

the company affairs effectively.

Internal stakeholders Employees - They Handel the internal working

of the company and also enhanced the stability

in the market at large scale (Duff, 2018). They

are important as due to their dedication and

work experiences they increase the sale in the

company.

Format of the financial accounting is been

specified by the appropriate authorities that is

IFRS and GAAP.

There is no any specified format under the

management accounting.

Under financial accounting, the financial

reports are been framed at year end of an

accounting period that is one year.

Under the MA, reports relating to the

management are been prepared according to

the requirements of an enterprise.

Main users of the FA are the internal and an

external users such as investors, creditors,

mangers, employees, government etc.

Internal management is considered as the main

user under the management accounting.

Financial accounting summarizes the reports

by stating the financial position of an entity.

However, management accounting provides for

the complete and the detailed report in relation

to the various information.

The final reports under the financial

accounting needed to be published and requires

the auditing by the statutory auditors.

The management reports formulated under the

management accounting neither required to be

published nor needed to be audited by the

statutory auditors.

b. Two internal stakeholder and four external stakeholders important in the organisation.

Internal stakeholders refers to such person who manages the company internal affairs are

also responsible to carry various activities (Pijper, 2016). External stakeholders are important ass

due to their inspection in company it reflects the stability of the company and also they manage

the company affairs effectively.

Internal stakeholders Employees - They Handel the internal working

of the company and also enhanced the stability

in the market at large scale (Duff, 2018). They

are important as due to their dedication and

work experiences they increase the sale in the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managers – They are the persons who

manages the overall activity of an entity and

also handle employees and assigned them day

to day actively which is to be completed within

the stipulated time. The manager's role are

important in internal management of the

company.

External stakeholders Consumers- They purchase goods from the

company. Thus, if the company position is

stable, they can attract more consumers

towards their business (Clatworthy and Peel,

2016).

Investors - They are also major stakeholders in

the company as they invest money in the

project to get good return. They can also verify

build trust in the company and can also

demand their financial report. So to maintain

the reputation in the market company had to

present the appropriate report so that there is

continuous cash flow in the company.

Government - Government imposed taxes to

company regarding their transaction and also

their dealing in goods from import to export

(Ullah and et.al., 2018). Thus, government also

sometimes invests money in the company and

they can examine the financial report of the

company at any time. Thus, it is the duty of the

company to keep an up-to-date report so that it

can be presentable at any time.

Supplier - these are those persons who

manages the overall activity of an entity and

also handle employees and assigned them day

to day actively which is to be completed within

the stipulated time. The manager's role are

important in internal management of the

company.

External stakeholders Consumers- They purchase goods from the

company. Thus, if the company position is

stable, they can attract more consumers

towards their business (Clatworthy and Peel,

2016).

Investors - They are also major stakeholders in

the company as they invest money in the

project to get good return. They can also verify

build trust in the company and can also

demand their financial report. So to maintain

the reputation in the market company had to

present the appropriate report so that there is

continuous cash flow in the company.

Government - Government imposed taxes to

company regarding their transaction and also

their dealing in goods from import to export

(Ullah and et.al., 2018). Thus, government also

sometimes invests money in the company and

they can examine the financial report of the

company at any time. Thus, it is the duty of the

company to keep an up-to-date report so that it

can be presentable at any time.

Supplier - these are those persons who

supplies goods to the company and also they

are important. As company manage their

transaction by viewing the supply of raw

material and resources in the company. Thus,

supplier provides finished goods to company at

bargain rates if company had good terms with

them (Weetman, 2019).

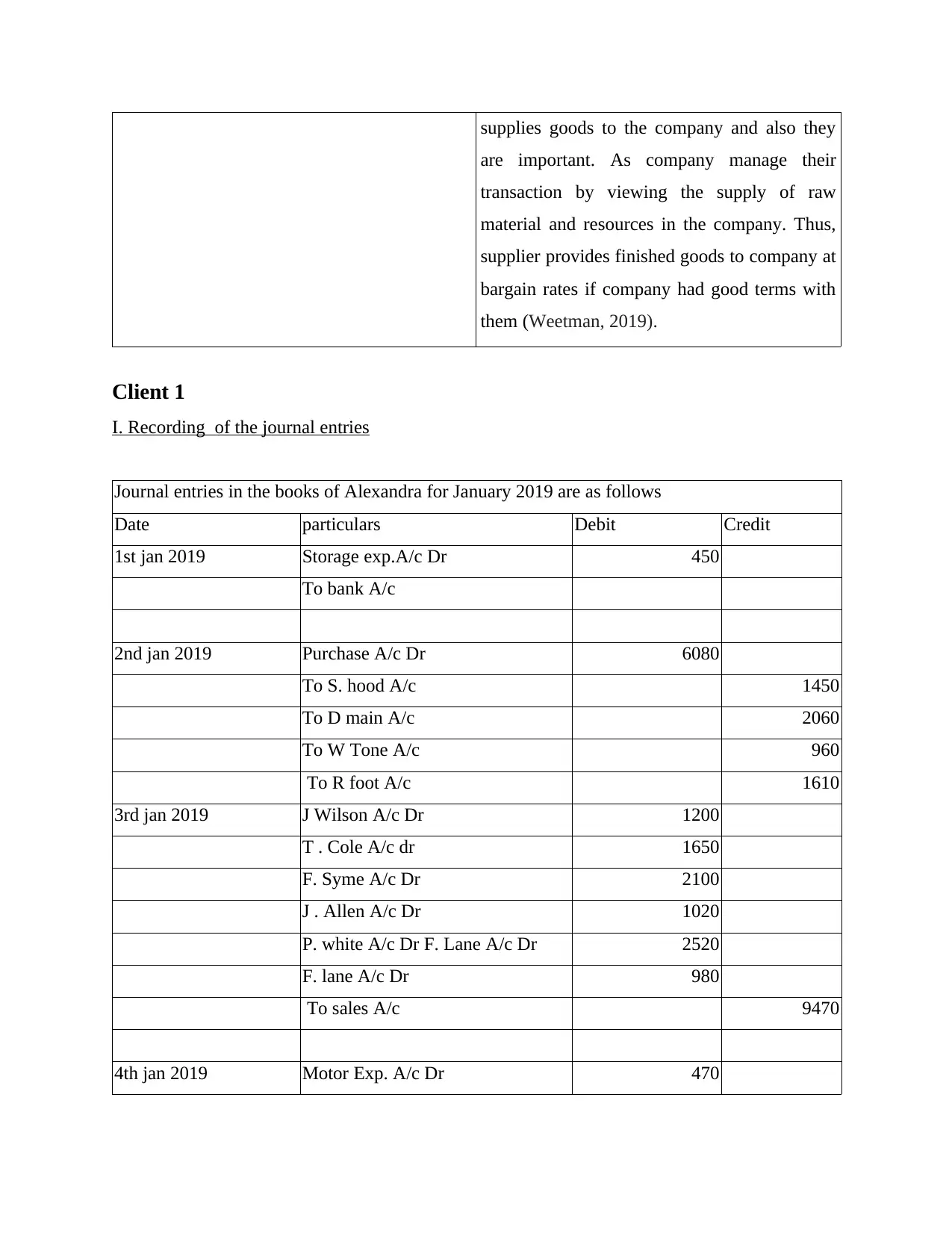

Client 1

I. Recording of the journal entries

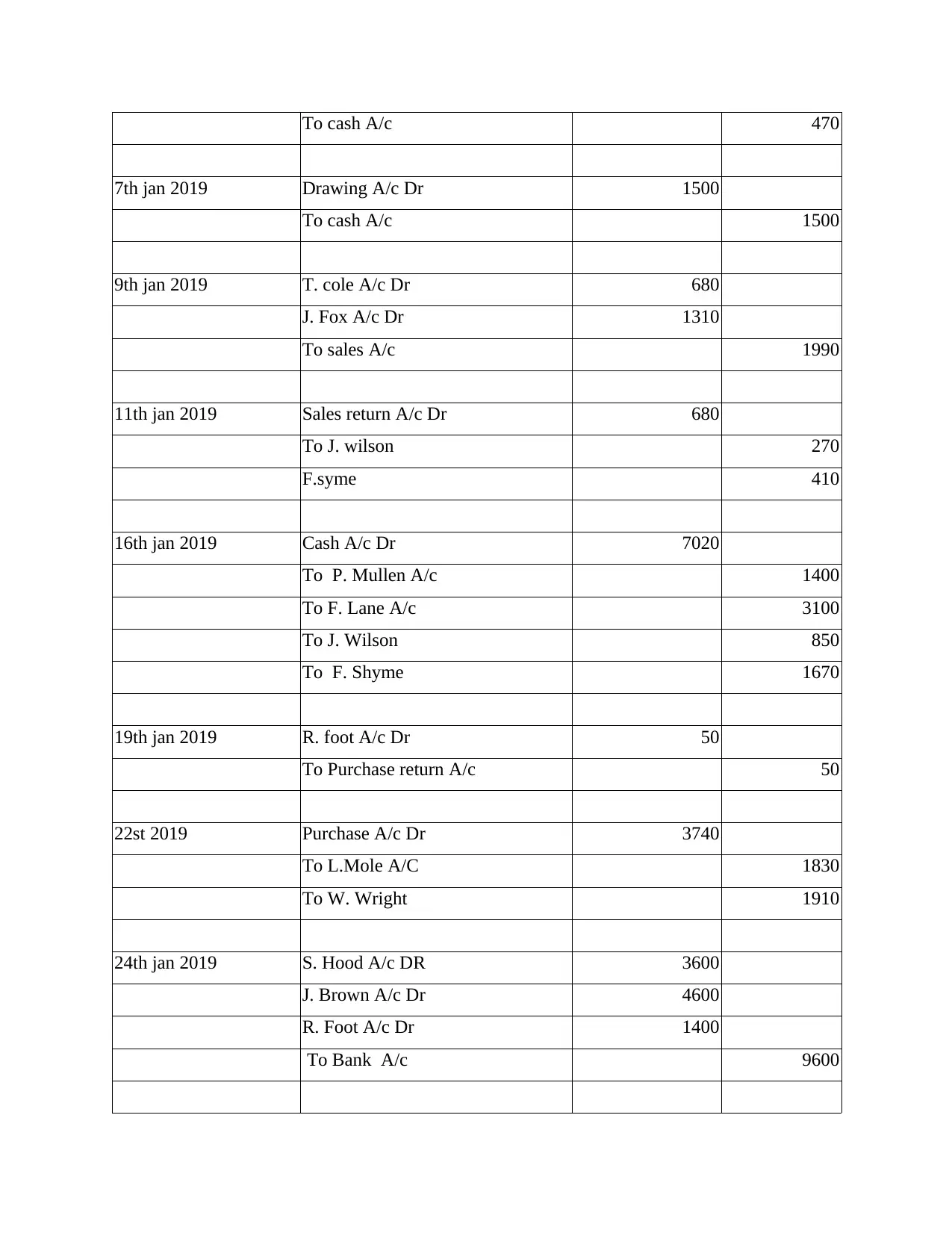

Journal entries in the books of Alexandra for January 2019 are as follows

Date particulars Debit Credit

1st jan 2019 Storage exp.A/c Dr 450

To bank A/c

2nd jan 2019 Purchase A/c Dr 6080

To S. hood A/c 1450

To D main A/c 2060

To W Tone A/c 960

To R foot A/c 1610

3rd jan 2019 J Wilson A/c Dr 1200

T . Cole A/c dr 1650

F. Syme A/c Dr 2100

J . Allen A/c Dr 1020

P. white A/c Dr F. Lane A/c Dr 2520

F. lane A/c Dr 980

To sales A/c 9470

4th jan 2019 Motor Exp. A/c Dr 470

are important. As company manage their

transaction by viewing the supply of raw

material and resources in the company. Thus,

supplier provides finished goods to company at

bargain rates if company had good terms with

them (Weetman, 2019).

Client 1

I. Recording of the journal entries

Journal entries in the books of Alexandra for January 2019 are as follows

Date particulars Debit Credit

1st jan 2019 Storage exp.A/c Dr 450

To bank A/c

2nd jan 2019 Purchase A/c Dr 6080

To S. hood A/c 1450

To D main A/c 2060

To W Tone A/c 960

To R foot A/c 1610

3rd jan 2019 J Wilson A/c Dr 1200

T . Cole A/c dr 1650

F. Syme A/c Dr 2100

J . Allen A/c Dr 1020

P. white A/c Dr F. Lane A/c Dr 2520

F. lane A/c Dr 980

To sales A/c 9470

4th jan 2019 Motor Exp. A/c Dr 470

To cash A/c 470

7th jan 2019 Drawing A/c Dr 1500

To cash A/c 1500

9th jan 2019 T. cole A/c Dr 680

J. Fox A/c Dr 1310

To sales A/c 1990

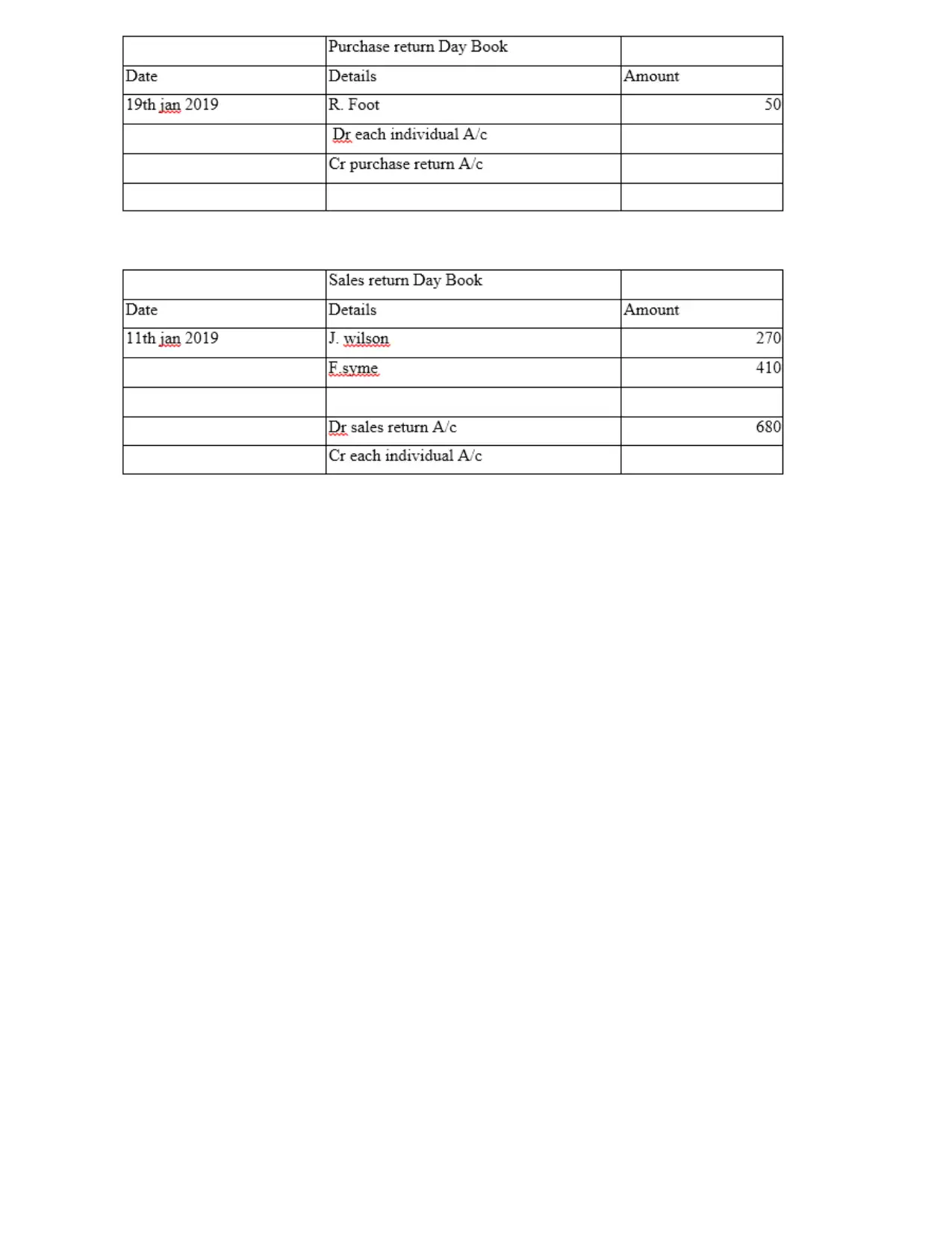

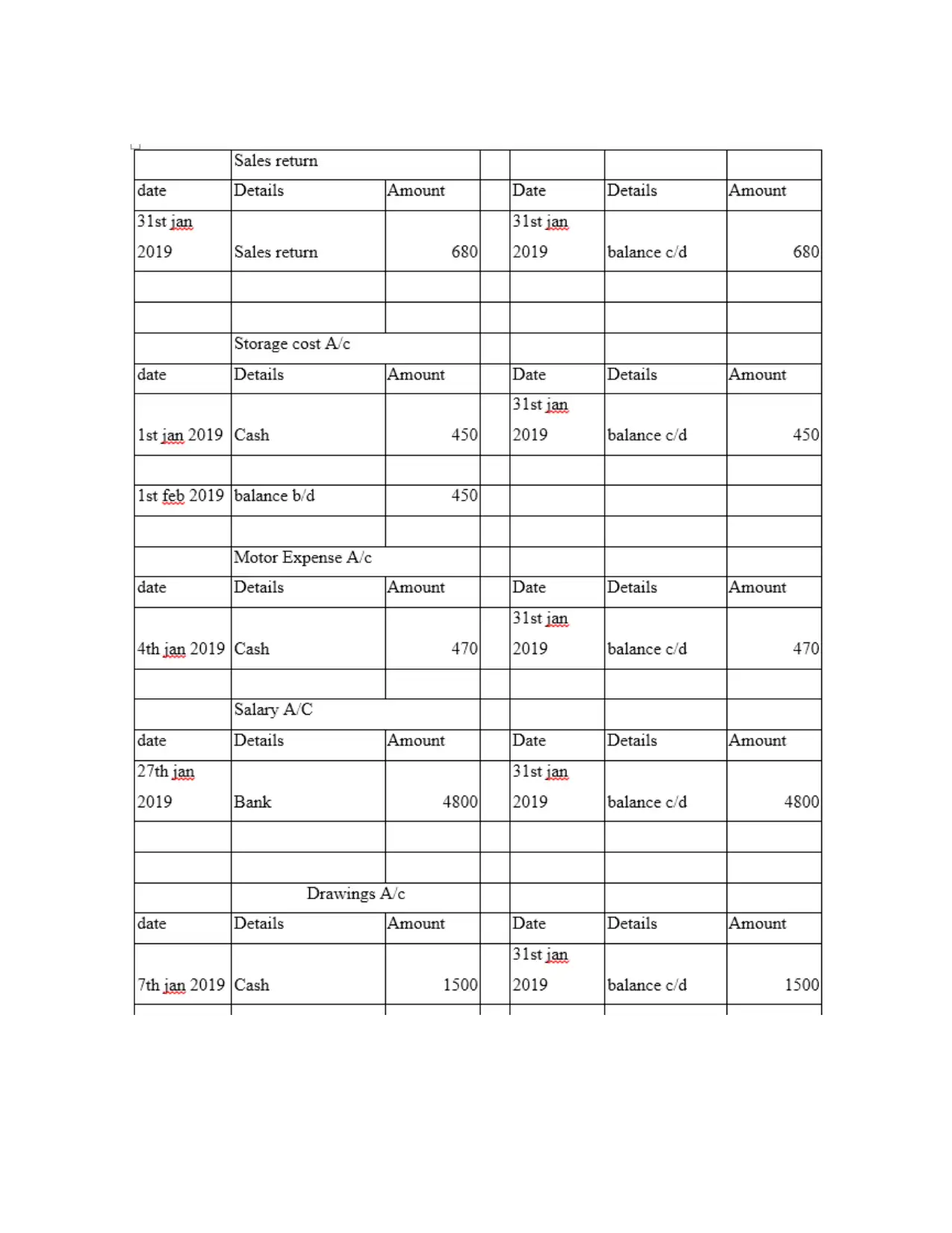

11th jan 2019 Sales return A/c Dr 680

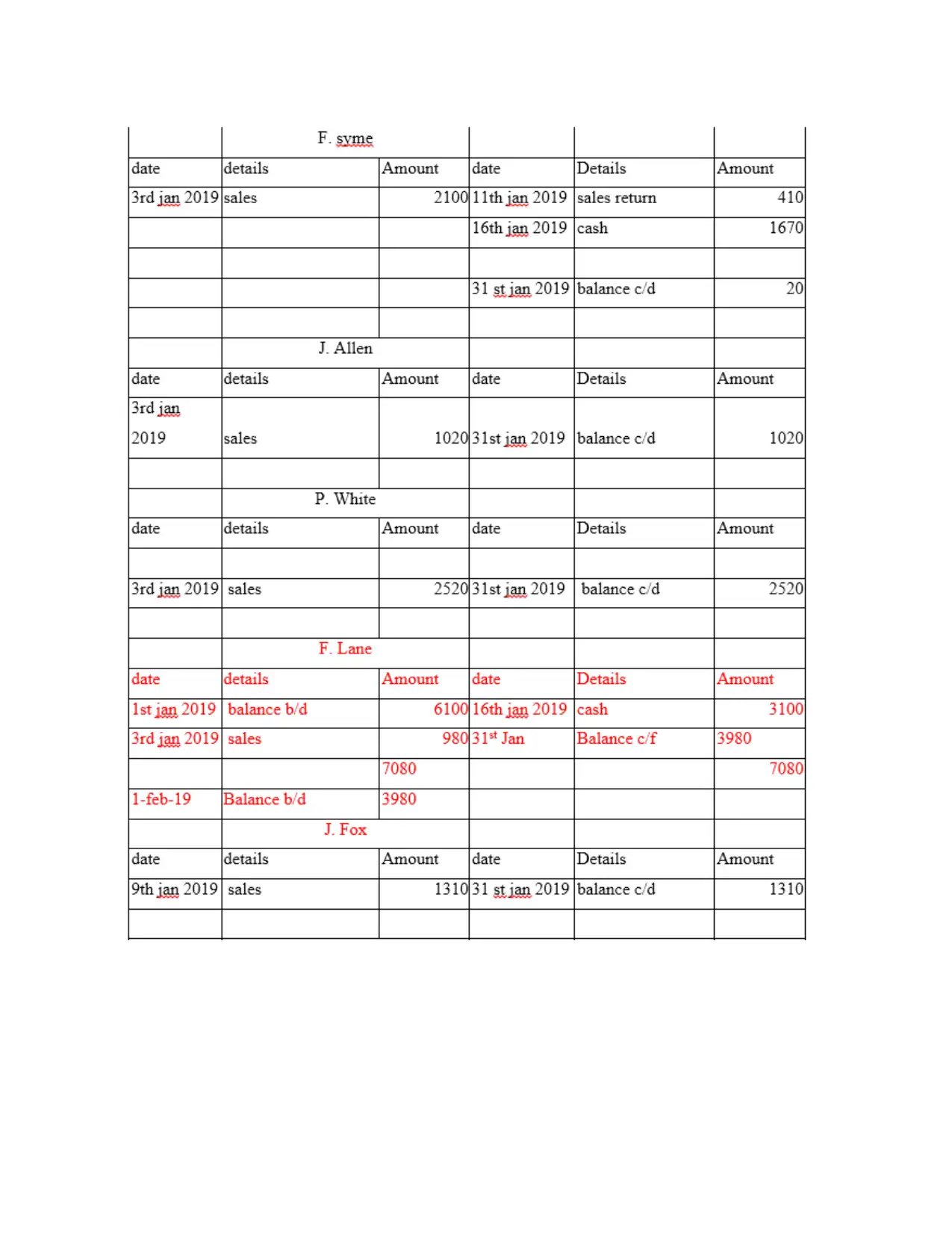

To J. wilson 270

F.syme 410

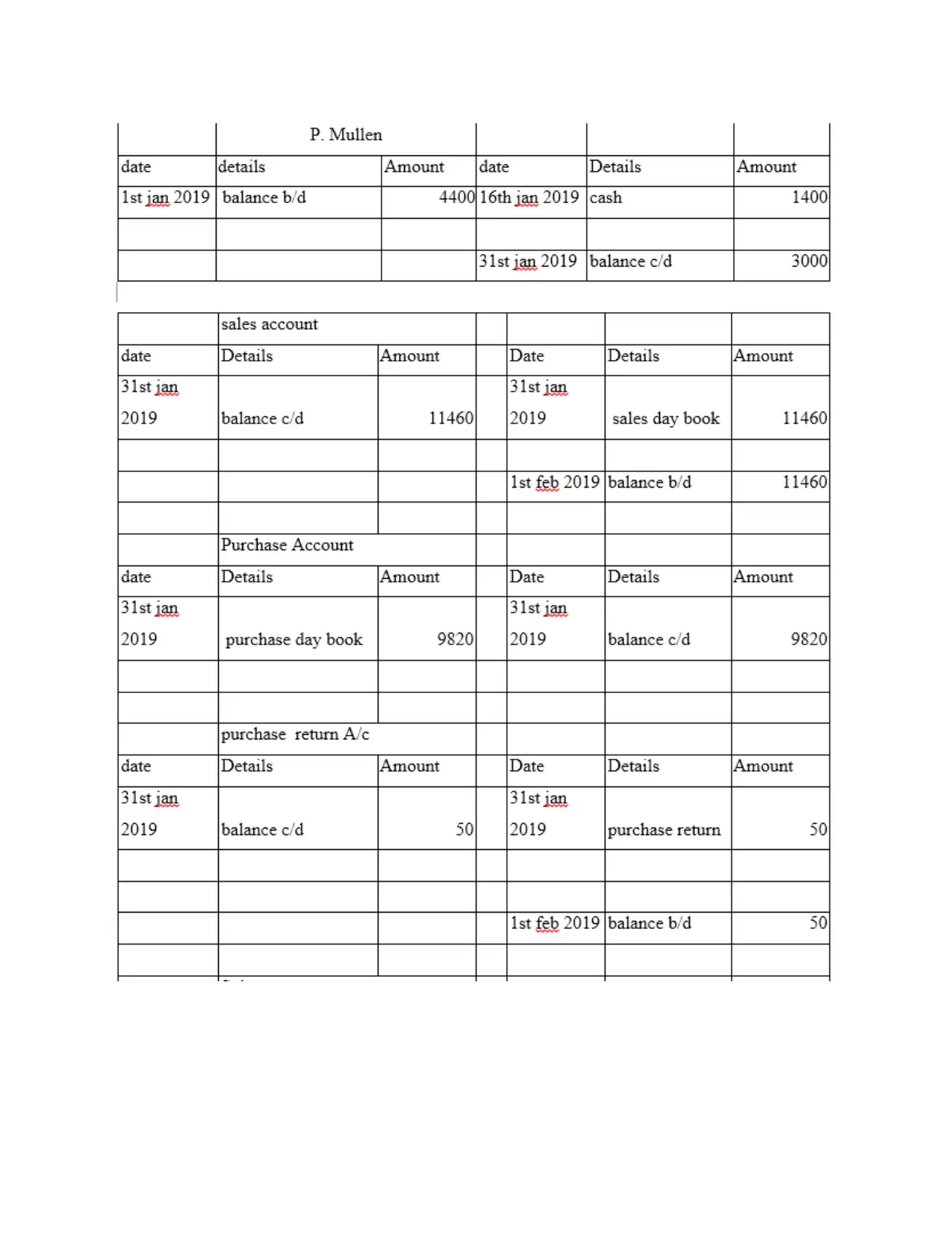

16th jan 2019 Cash A/c Dr 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson 850

To F. Shyme 1670

19th jan 2019 R. foot A/c Dr 50

To Purchase return A/c 50

22st 2019 Purchase A/c Dr 3740

To L.Mole A/C 1830

To W. Wright 1910

24th jan 2019 S. Hood A/c DR 3600

J. Brown A/c Dr 4600

R. Foot A/c Dr 1400

To Bank A/c 9600

7th jan 2019 Drawing A/c Dr 1500

To cash A/c 1500

9th jan 2019 T. cole A/c Dr 680

J. Fox A/c Dr 1310

To sales A/c 1990

11th jan 2019 Sales return A/c Dr 680

To J. wilson 270

F.syme 410

16th jan 2019 Cash A/c Dr 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson 850

To F. Shyme 1670

19th jan 2019 R. foot A/c Dr 50

To Purchase return A/c 50

22st 2019 Purchase A/c Dr 3740

To L.Mole A/C 1830

To W. Wright 1910

24th jan 2019 S. Hood A/c DR 3600

J. Brown A/c Dr 4600

R. Foot A/c Dr 1400

To Bank A/c 9600

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

27th jan 2019 Salary A/c Dr 4800

To bank A/c 4800

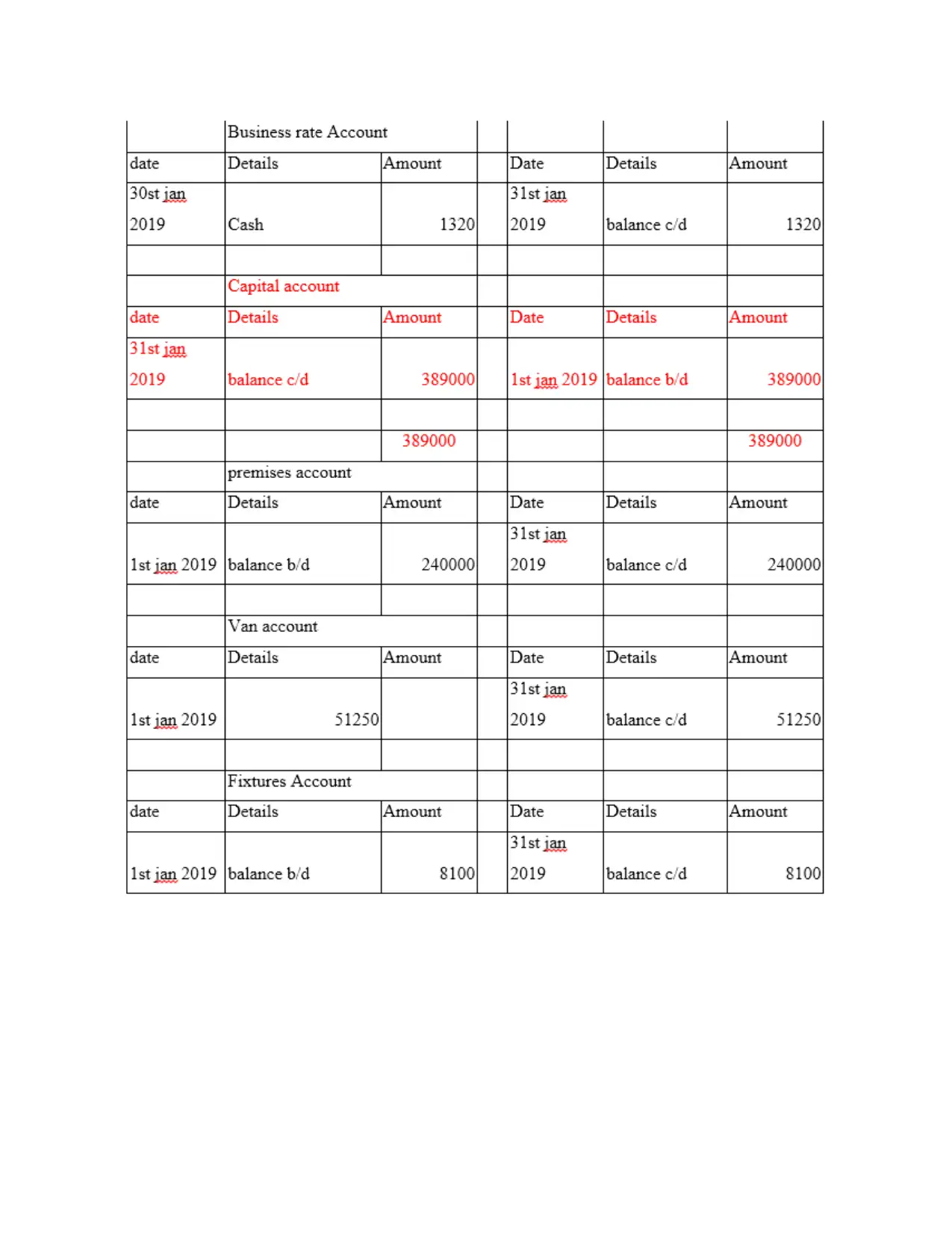

30th jan 2019 Business rates A/c Dr 1320

To bank A/c 1320

To bank A/c 4800

30th jan 2019 Business rates A/c Dr 1320

To bank A/c 1320

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

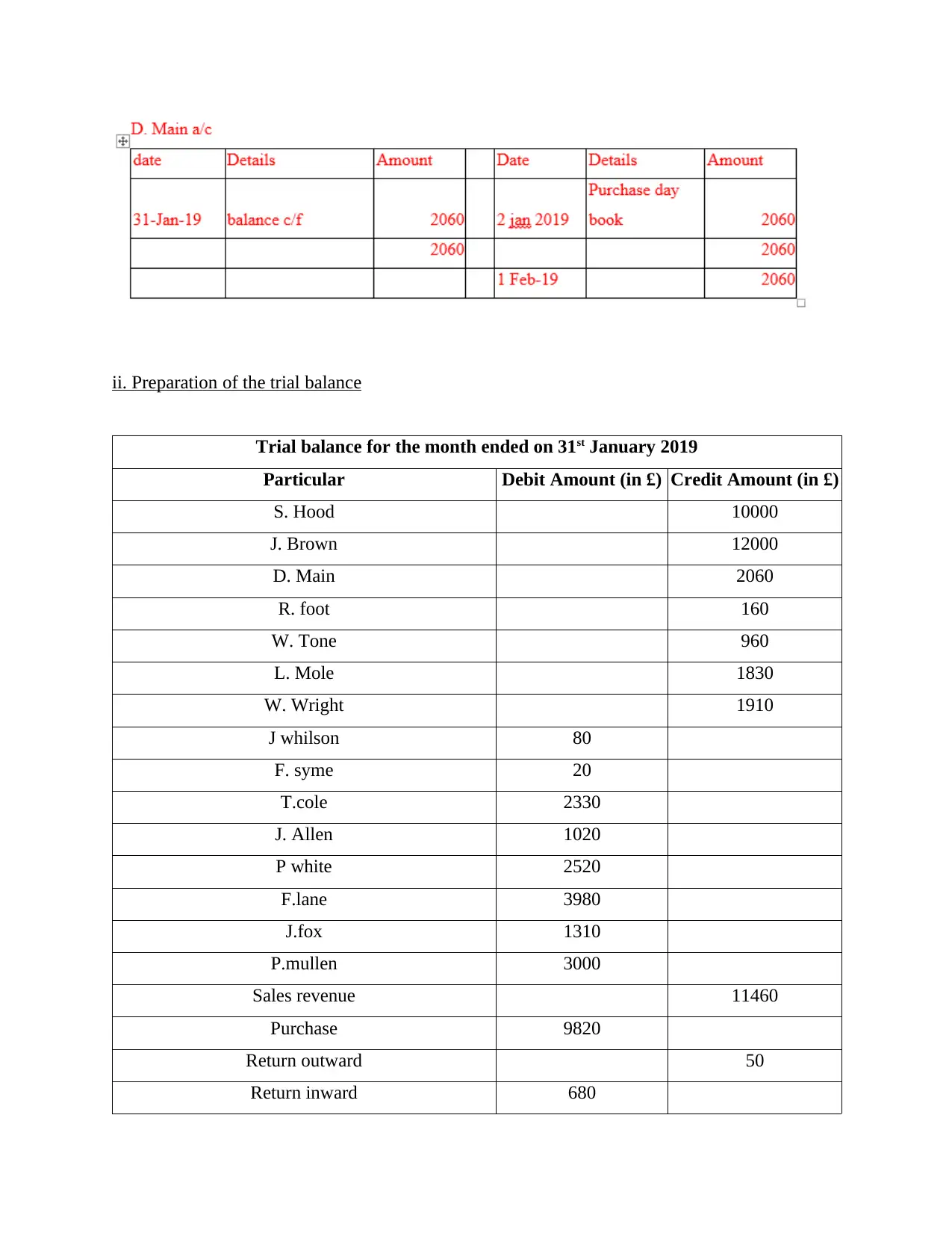

ii. Preparation of the trial balance

Trial balance for the month ended on 31st January 2019

Particular Debit Amount (in £) Credit Amount (in £)

S. Hood 10000

J. Brown 12000

D. Main 2060

R. foot 160

W. Tone 960

L. Mole 1830

W. Wright 1910

J whilson 80

F. syme 20

T.cole 2330

J. Allen 1020

P white 2520

F.lane 3980

J.fox 1310

P.mullen 3000

Sales revenue 11460

Purchase 9820

Return outward 50

Return inward 680

Trial balance for the month ended on 31st January 2019

Particular Debit Amount (in £) Credit Amount (in £)

S. Hood 10000

J. Brown 12000

D. Main 2060

R. foot 160

W. Tone 960

L. Mole 1830

W. Wright 1910

J whilson 80

F. syme 20

T.cole 2330

J. Allen 1020

P white 2520

F.lane 3980

J.fox 1310

P.mullen 3000

Sales revenue 11460

Purchase 9820

Return outward 50

Return inward 680

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

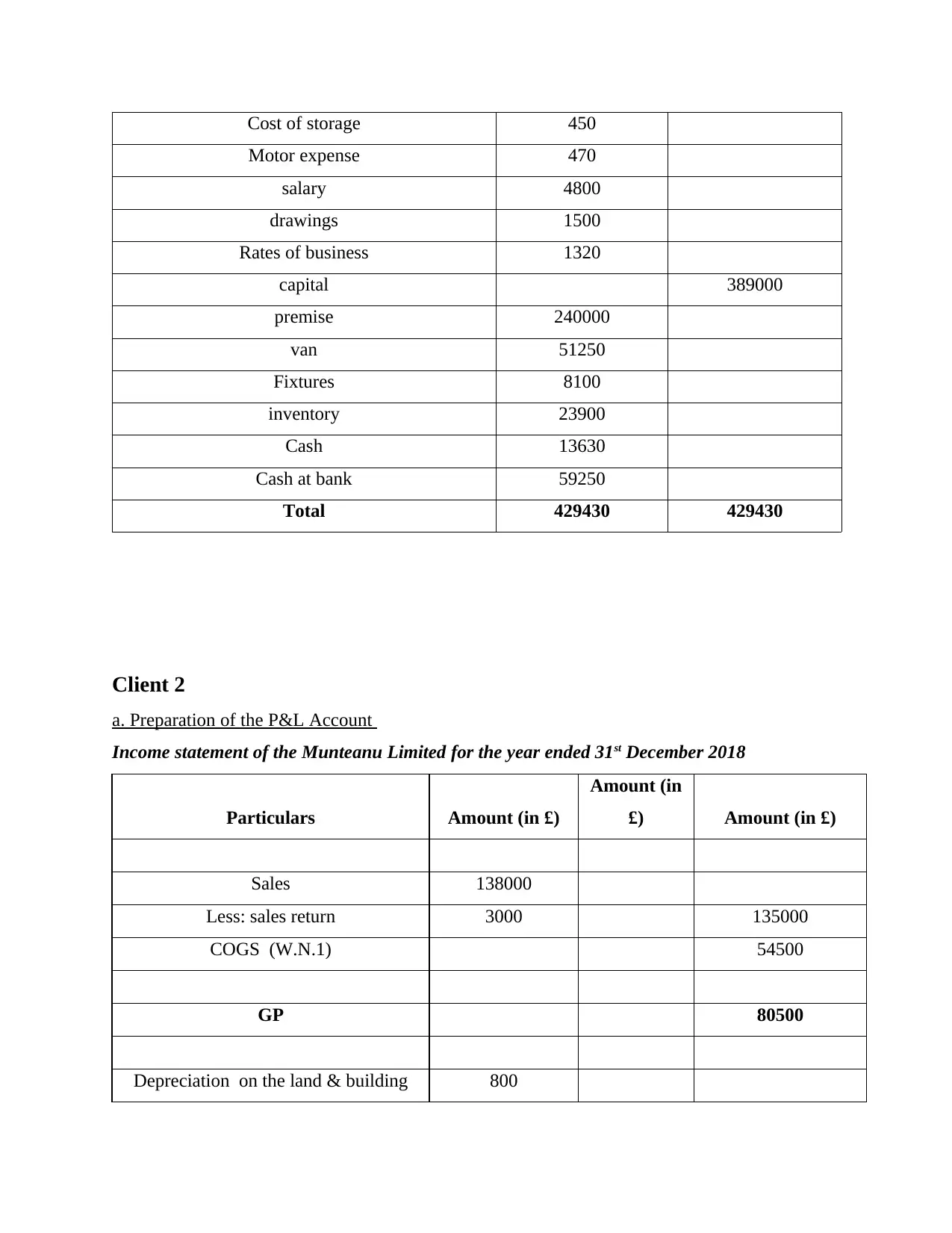

Cost of storage 450

Motor expense 470

salary 4800

drawings 1500

Rates of business 1320

capital 389000

premise 240000

van 51250

Fixtures 8100

inventory 23900

Cash 13630

Cash at bank 59250

Total 429430 429430

Client 2

a. Preparation of the P&L Account

Income statement of the Munteanu Limited for the year ended 31st December 2018

Particulars Amount (in £)

Amount (in

£) Amount (in £)

Sales 138000

Less: sales return 3000 135000

COGS (W.N.1) 54500

GP 80500

Depreciation on the land & building 800

Motor expense 470

salary 4800

drawings 1500

Rates of business 1320

capital 389000

premise 240000

van 51250

Fixtures 8100

inventory 23900

Cash 13630

Cash at bank 59250

Total 429430 429430

Client 2

a. Preparation of the P&L Account

Income statement of the Munteanu Limited for the year ended 31st December 2018

Particulars Amount (in £)

Amount (in

£) Amount (in £)

Sales 138000

Less: sales return 3000 135000

COGS (W.N.1) 54500

GP 80500

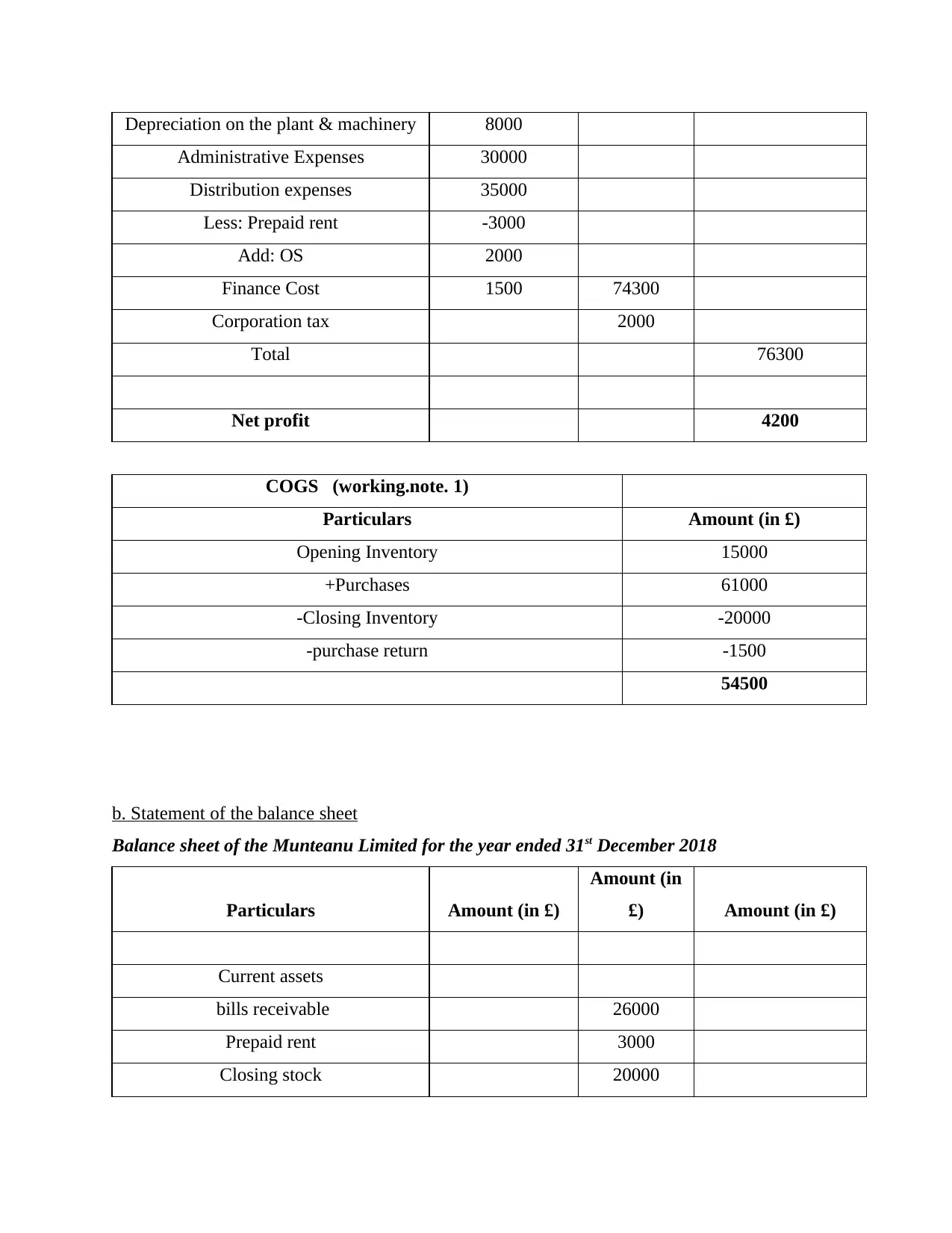

Depreciation on the land & building 800

Depreciation on the plant & machinery 8000

Administrative Expenses 30000

Distribution expenses 35000

Less: Prepaid rent -3000

Add: OS 2000

Finance Cost 1500 74300

Corporation tax 2000

Total 76300

Net profit 4200

COGS (working.note. 1)

Particulars Amount (in £)

Opening Inventory 15000

+Purchases 61000

-Closing Inventory -20000

-purchase return -1500

54500

b. Statement of the balance sheet

Balance sheet of the Munteanu Limited for the year ended 31st December 2018

Particulars Amount (in £)

Amount (in

£) Amount (in £)

Current assets

bills receivable 26000

Prepaid rent 3000

Closing stock 20000

Administrative Expenses 30000

Distribution expenses 35000

Less: Prepaid rent -3000

Add: OS 2000

Finance Cost 1500 74300

Corporation tax 2000

Total 76300

Net profit 4200

COGS (working.note. 1)

Particulars Amount (in £)

Opening Inventory 15000

+Purchases 61000

-Closing Inventory -20000

-purchase return -1500

54500

b. Statement of the balance sheet

Balance sheet of the Munteanu Limited for the year ended 31st December 2018

Particulars Amount (in £)

Amount (in

£) Amount (in £)

Current assets

bills receivable 26000

Prepaid rent 3000

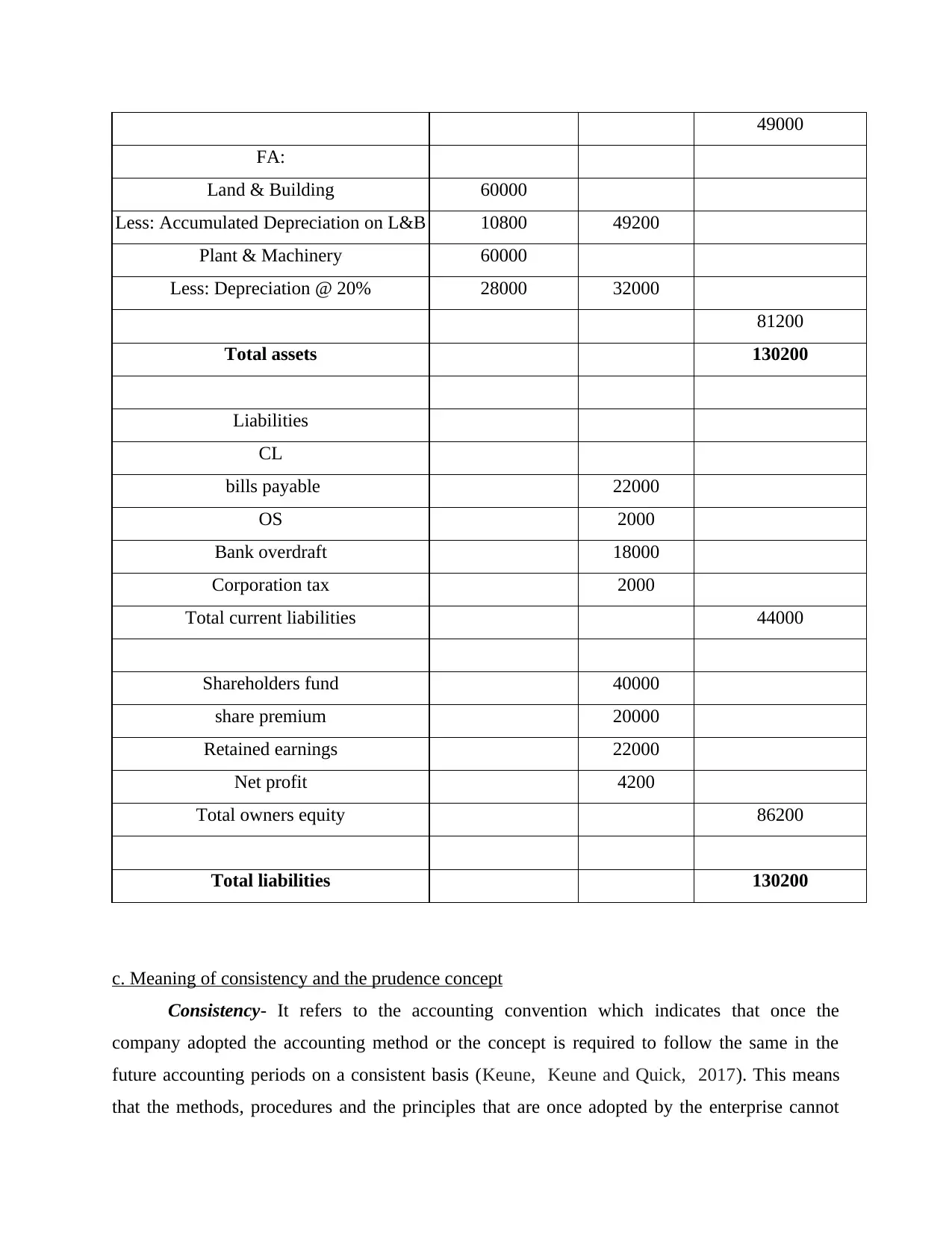

Closing stock 20000

49000

FA:

Land & Building 60000

Less: Accumulated Depreciation on L&B 10800 49200

Plant & Machinery 60000

Less: Depreciation @ 20% 28000 32000

81200

Total assets 130200

Liabilities

CL

bills payable 22000

OS 2000

Bank overdraft 18000

Corporation tax 2000

Total current liabilities 44000

Shareholders fund 40000

share premium 20000

Retained earnings 22000

Net profit 4200

Total owners equity 86200

Total liabilities 130200

c. Meaning of consistency and the prudence concept

Consistency- It refers to the accounting convention which indicates that once the

company adopted the accounting method or the concept is required to follow the same in the

future accounting periods on a consistent basis (Keune, Keune and Quick, 2017). This means

that the methods, procedures and the principles that are once adopted by the enterprise cannot

FA:

Land & Building 60000

Less: Accumulated Depreciation on L&B 10800 49200

Plant & Machinery 60000

Less: Depreciation @ 20% 28000 32000

81200

Total assets 130200

Liabilities

CL

bills payable 22000

OS 2000

Bank overdraft 18000

Corporation tax 2000

Total current liabilities 44000

Shareholders fund 40000

share premium 20000

Retained earnings 22000

Net profit 4200

Total owners equity 86200

Total liabilities 130200

c. Meaning of consistency and the prudence concept

Consistency- It refers to the accounting convention which indicates that once the

company adopted the accounting method or the concept is required to follow the same in the

future accounting periods on a consistent basis (Keune, Keune and Quick, 2017). This means

that the methods, procedures and the principles that are once adopted by the enterprise cannot

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

change in the future. It could change the accounting principle only in case of the introduction of

the new version which results in the improvement of the financial results. The information in

relation to the change is to be involved in the financial reports or the documentation. For

example- An organization is using FIFO method in making valuation of its inventory and in

identifying the COGS. However, because of the increasing material cost, it has concluded that

the LIFO will be considered as the better indicator as it states true profitability (Xu and Doupnik,

2016). Thus, it can change the method by making the appropriate disclosure relating to the break

in the consistency.

Prudence- An accounting principle which says that do not estimate for the sum of

revenues but provide for all the possible losses. In other words it means not overestimating the

recognized revenue amounts or underestimating amount of the expenses. It means that recording

the revenue transaction and the asset at the time it gets certain, however, entering transaction

relating to expense or the liability at the time it gets probable. For example- Provision of bad

debts, recording the inventory at its realizable value rather than on the expected sales price.

d. Describing the objectives of the depreciation and its techniques

Depreciation refers to the decline in value of fixed asset because of any obsolescence or

tear over4 the useful its useful life. It referred as the accounting method in allocating tangible

asset cost entire useful life span of an asset and is been used to account for the decline in value.

The objective of depreciation is achieving the matching principle of accounting that is an entity

charges the depreciation in order to match with historical cost of an productive asset with that of

the earning revenues with the use of that asset (Bailey and Sawers, 2018). Mainly the two

methods which is been utilise by an organization for computing the depreciation that are straight

line method and the written down value method.

SLM- It refers to the method of depreciation which is utilized for recognizing carrying of

the fixed asset over the asset life. This method is applied where there does not present any

specific pattern in a way the asset could be utilized (Küpper and Pedell, 2016). It is the highly

recommended method as it is counted as the easiest method in calculating the depreciation

amount with very less errors.

Written down value method- It is also known as reducing value method which is used in

determining the worth of previously purchased asset and is bee computed by reducing the

accumulated depreciation from the real value of an asset.

the new version which results in the improvement of the financial results. The information in

relation to the change is to be involved in the financial reports or the documentation. For

example- An organization is using FIFO method in making valuation of its inventory and in

identifying the COGS. However, because of the increasing material cost, it has concluded that

the LIFO will be considered as the better indicator as it states true profitability (Xu and Doupnik,

2016). Thus, it can change the method by making the appropriate disclosure relating to the break

in the consistency.

Prudence- An accounting principle which says that do not estimate for the sum of

revenues but provide for all the possible losses. In other words it means not overestimating the

recognized revenue amounts or underestimating amount of the expenses. It means that recording

the revenue transaction and the asset at the time it gets certain, however, entering transaction

relating to expense or the liability at the time it gets probable. For example- Provision of bad

debts, recording the inventory at its realizable value rather than on the expected sales price.

d. Describing the objectives of the depreciation and its techniques

Depreciation refers to the decline in value of fixed asset because of any obsolescence or

tear over4 the useful its useful life. It referred as the accounting method in allocating tangible

asset cost entire useful life span of an asset and is been used to account for the decline in value.

The objective of depreciation is achieving the matching principle of accounting that is an entity

charges the depreciation in order to match with historical cost of an productive asset with that of

the earning revenues with the use of that asset (Bailey and Sawers, 2018). Mainly the two

methods which is been utilise by an organization for computing the depreciation that are straight

line method and the written down value method.

SLM- It refers to the method of depreciation which is utilized for recognizing carrying of

the fixed asset over the asset life. This method is applied where there does not present any

specific pattern in a way the asset could be utilized (Küpper and Pedell, 2016). It is the highly

recommended method as it is counted as the easiest method in calculating the depreciation

amount with very less errors.

Written down value method- It is also known as reducing value method which is used in

determining the worth of previously purchased asset and is bee computed by reducing the

accumulated depreciation from the real value of an asset.

e. Evaluating the difference in between the financial statements of the sole trader and the limited

companies.

Sole trader Limited company

Owner's equity under sole trader contains only

single item which is an sole trader's equity

account.

However, the shareholders fund of the limited

company includes share capital, retained

earnings, other revenue, capital reserves etc.

Taxes are deducted from the owner's income

and the sole trader.

The tax is been imposed as it is considered as

the separate legal enterprise.

Sole proprietor is not been subjected to any of

the accounting standards or the GAAP, then

the owner could decide whether the financial

statement required to prepare or not (Del

Giudice, Manganelli and De Paola, 2016). The

decision regarding the form of financial reports

also depends upon an owner.

Limited company require to follow all the

appropriate accounting concepts, rules,

principles and the regulatory framework as

provided by IFRS and GAAP.

The financial statements of the sole trader are

not subjected to any audit.

It is compulsory for the limited company to get

auditing of its financial statements from the

statutory auditor in compliance with the

concepts and the regulatory guidelines.

Client 3

a. Explaining the meaning and the objectives of bank reconciliation statement

BRS is a document which represents the summary of the bank records and activities of

business as it reconciles bank account of an enterprise with its financial records. It is a statement

that highlights the deposits, other activities and the withdrawals that impacts bank account for

the specific period (Sunarya, Nurhaeni and Haris, 2017). This statement is useful for the

company in exercising internal control so that fraud is any could be detected. The main purpose

of BRS statement is to compare records of bank with the cash statement and if there any

differences occurs could be resolved with the preparation of this statement. It helps in verifying

integrity of the data in between the bank records and financial records of the company.

companies.

Sole trader Limited company

Owner's equity under sole trader contains only

single item which is an sole trader's equity

account.

However, the shareholders fund of the limited

company includes share capital, retained

earnings, other revenue, capital reserves etc.

Taxes are deducted from the owner's income

and the sole trader.

The tax is been imposed as it is considered as

the separate legal enterprise.

Sole proprietor is not been subjected to any of

the accounting standards or the GAAP, then

the owner could decide whether the financial

statement required to prepare or not (Del

Giudice, Manganelli and De Paola, 2016). The

decision regarding the form of financial reports

also depends upon an owner.

Limited company require to follow all the

appropriate accounting concepts, rules,

principles and the regulatory framework as

provided by IFRS and GAAP.

The financial statements of the sole trader are

not subjected to any audit.

It is compulsory for the limited company to get

auditing of its financial statements from the

statutory auditor in compliance with the

concepts and the regulatory guidelines.

Client 3

a. Explaining the meaning and the objectives of bank reconciliation statement

BRS is a document which represents the summary of the bank records and activities of

business as it reconciles bank account of an enterprise with its financial records. It is a statement

that highlights the deposits, other activities and the withdrawals that impacts bank account for

the specific period (Sunarya, Nurhaeni and Haris, 2017). This statement is useful for the

company in exercising internal control so that fraud is any could be detected. The main purpose

of BRS statement is to compare records of bank with the cash statement and if there any

differences occurs could be resolved with the preparation of this statement. It helps in verifying

integrity of the data in between the bank records and financial records of the company.

b. Listing down the areas where bank records can vary from the cash statement

Unpresented cheques- When the cheque is been issued by enterprise for making the payment, it

is been entered towards the credit side of the bank column but if the person who received the

cheque has not presented the cheque on that date then this results in the variation in between the

bank and the cash records.

Unrealized cheques- the cheques that are been deposited by firm is been immediately debited

and balance of their bank statement increases however the bank credits the account of the firm at

the time when the cheques are realized (Ahmed, 2016). This causes the difference till the

cheques get cleared.

Dishonour of the cheques- An enterprise credited its account at the time when it deposits the

cheque within bank. On the other hand, if the information relating to the dishonour of the cheque

is been received later to company (Abuhamdeh,Csikszentmihalyi and Jalal, 2015). This leads to

the difference till it is been debited back into the account.

Errors in entering the transaction- when recording the transactions in cash book, an entity may

make errors such as missing the sales entry, wrong balancing. This results to the differences in

between the cash and bank balance.

c. Meaning of imprest under the system of petty cash

Imprest system refers to the system of accounting which is been designed in tracing the

ways in which the cash is been spend. It is the method that accounts for the petty cash through

maintaining the balance into a fund which equates the receipts of the petty cash with the

additional cash into the fund (Jeppson, Ruddy and Salerno, 2016). It is important for every

organization to maintain the imprest system as it helps in managing the spending of the cash in

order to protect money from getting stolen. It is the accounting control system that protect the

organization from facing theft or the misuse of funds.

d. Preparation of bank reconciliation statement

Unpresented cheques- When the cheque is been issued by enterprise for making the payment, it

is been entered towards the credit side of the bank column but if the person who received the

cheque has not presented the cheque on that date then this results in the variation in between the

bank and the cash records.

Unrealized cheques- the cheques that are been deposited by firm is been immediately debited

and balance of their bank statement increases however the bank credits the account of the firm at

the time when the cheques are realized (Ahmed, 2016). This causes the difference till the

cheques get cleared.

Dishonour of the cheques- An enterprise credited its account at the time when it deposits the

cheque within bank. On the other hand, if the information relating to the dishonour of the cheque

is been received later to company (Abuhamdeh,Csikszentmihalyi and Jalal, 2015). This leads to

the difference till it is been debited back into the account.

Errors in entering the transaction- when recording the transactions in cash book, an entity may

make errors such as missing the sales entry, wrong balancing. This results to the differences in

between the cash and bank balance.

c. Meaning of imprest under the system of petty cash

Imprest system refers to the system of accounting which is been designed in tracing the

ways in which the cash is been spend. It is the method that accounts for the petty cash through

maintaining the balance into a fund which equates the receipts of the petty cash with the

additional cash into the fund (Jeppson, Ruddy and Salerno, 2016). It is important for every

organization to maintain the imprest system as it helps in managing the spending of the cash in

order to protect money from getting stolen. It is the accounting control system that protect the

organization from facing theft or the misuse of funds.

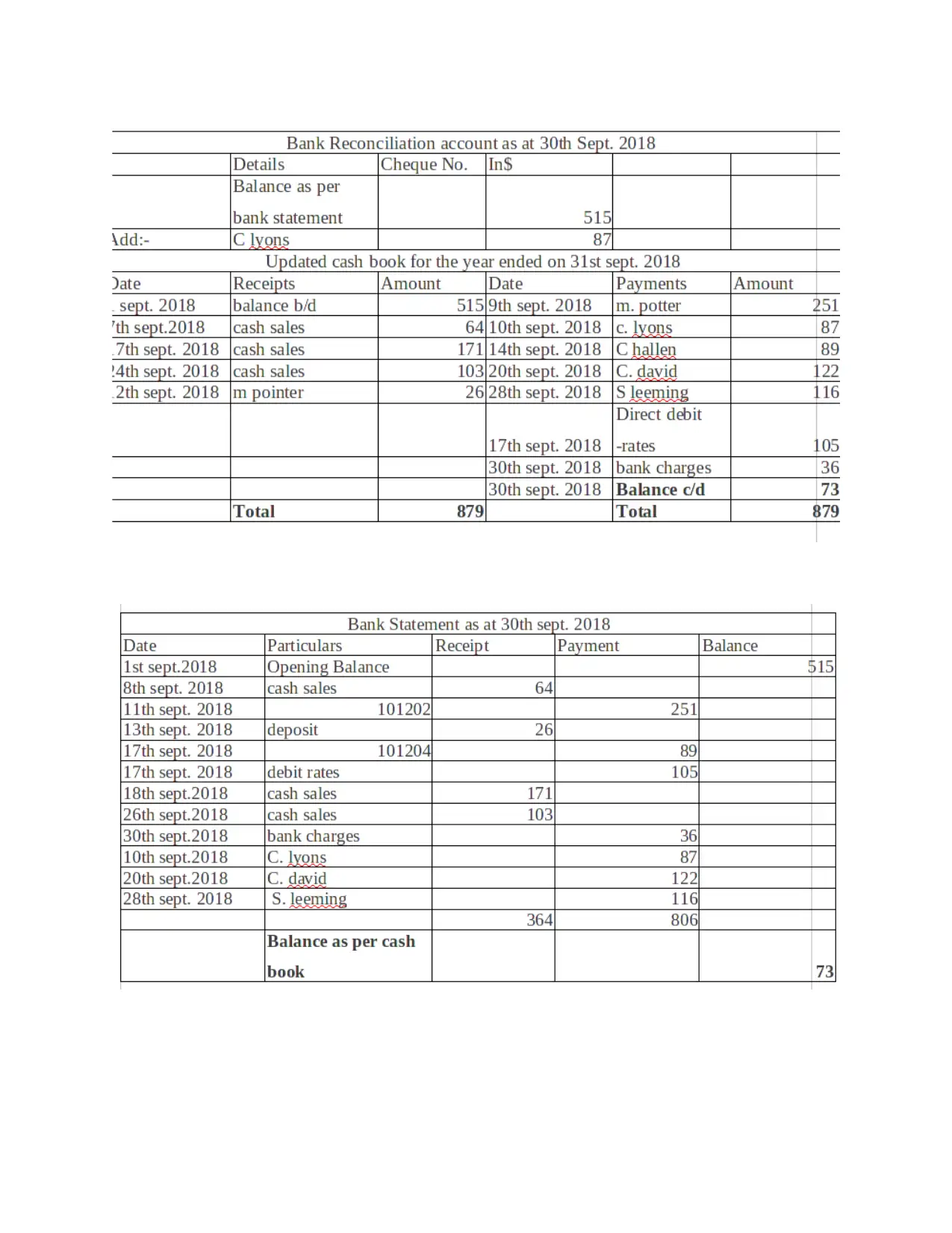

d. Preparation of bank reconciliation statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Client 4

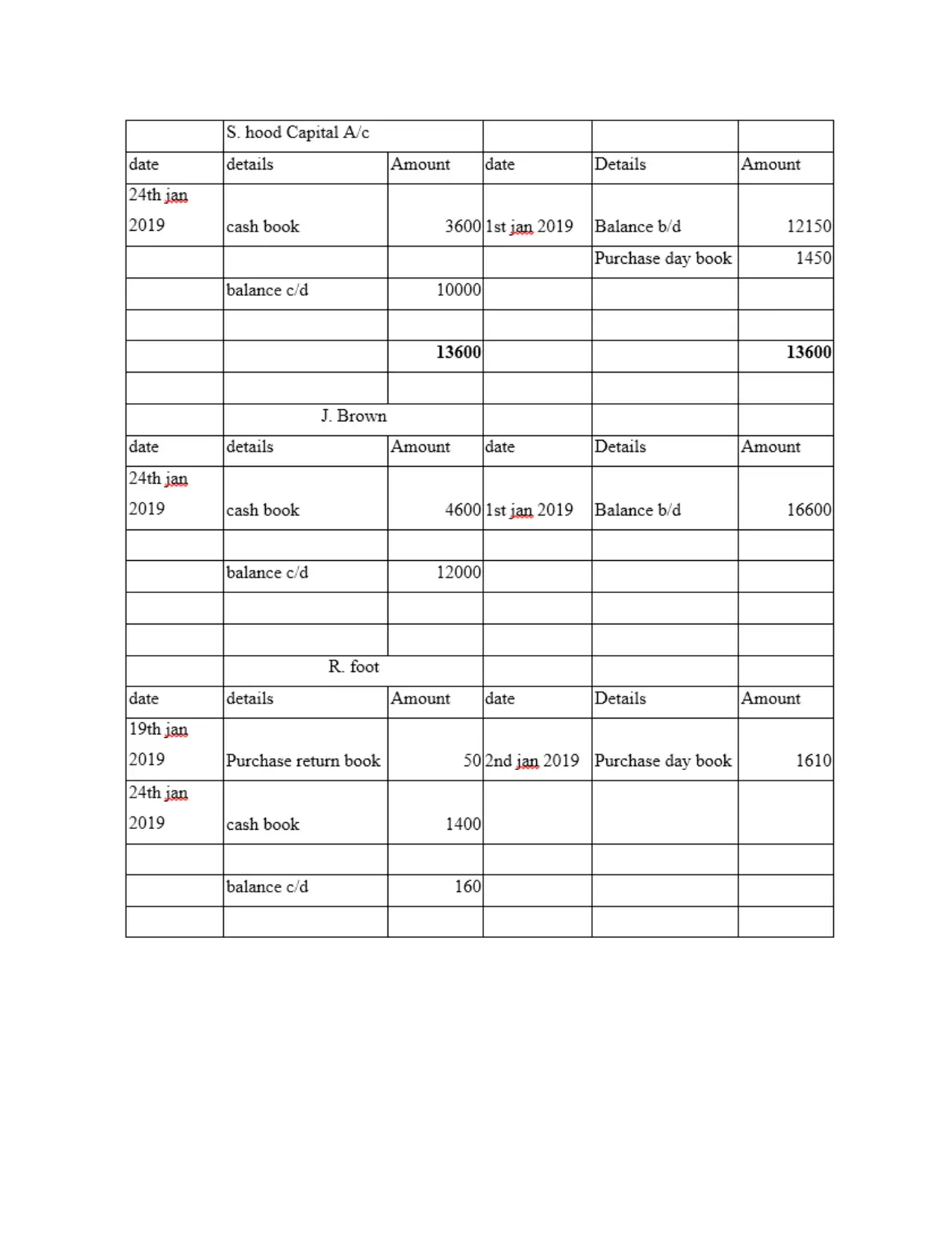

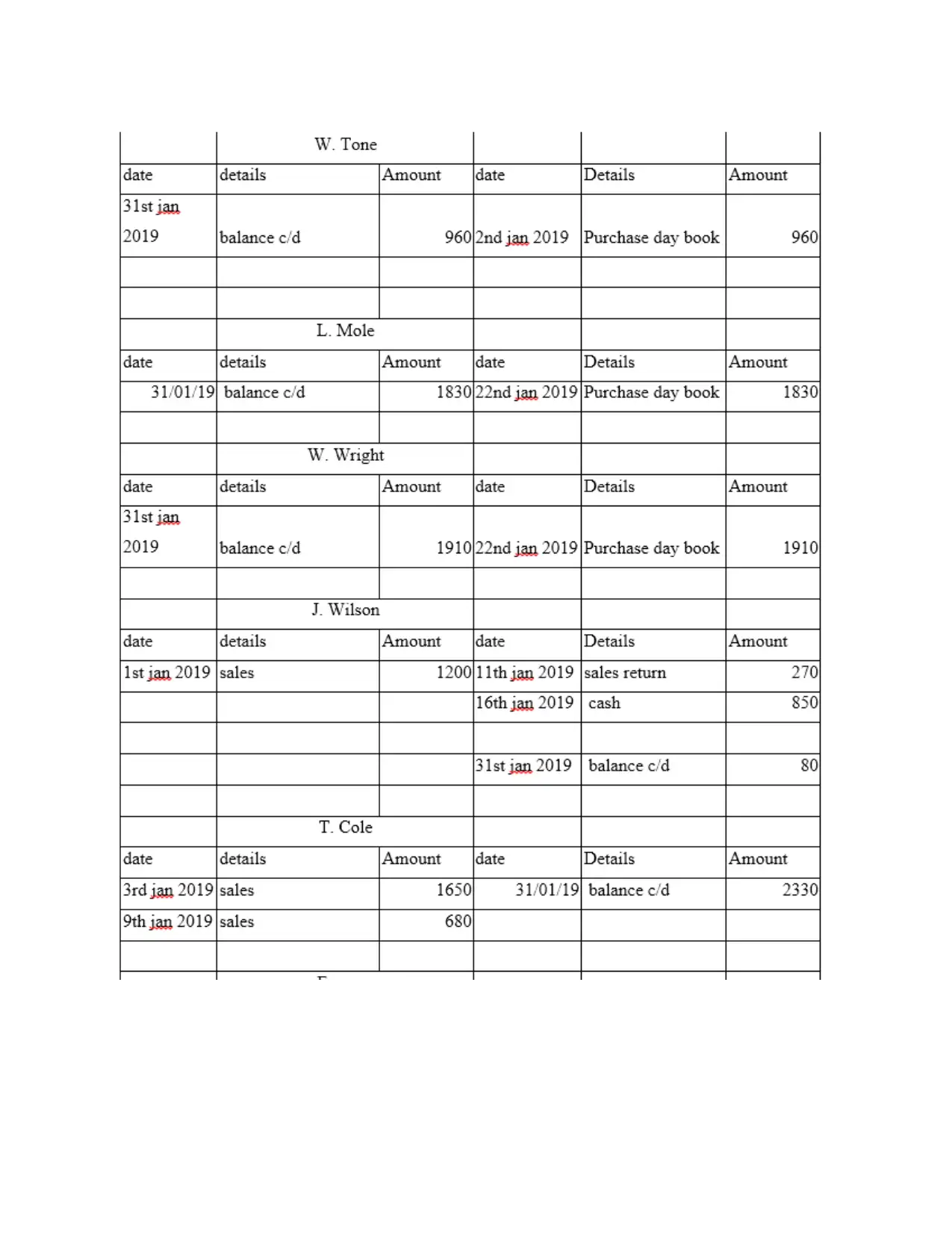

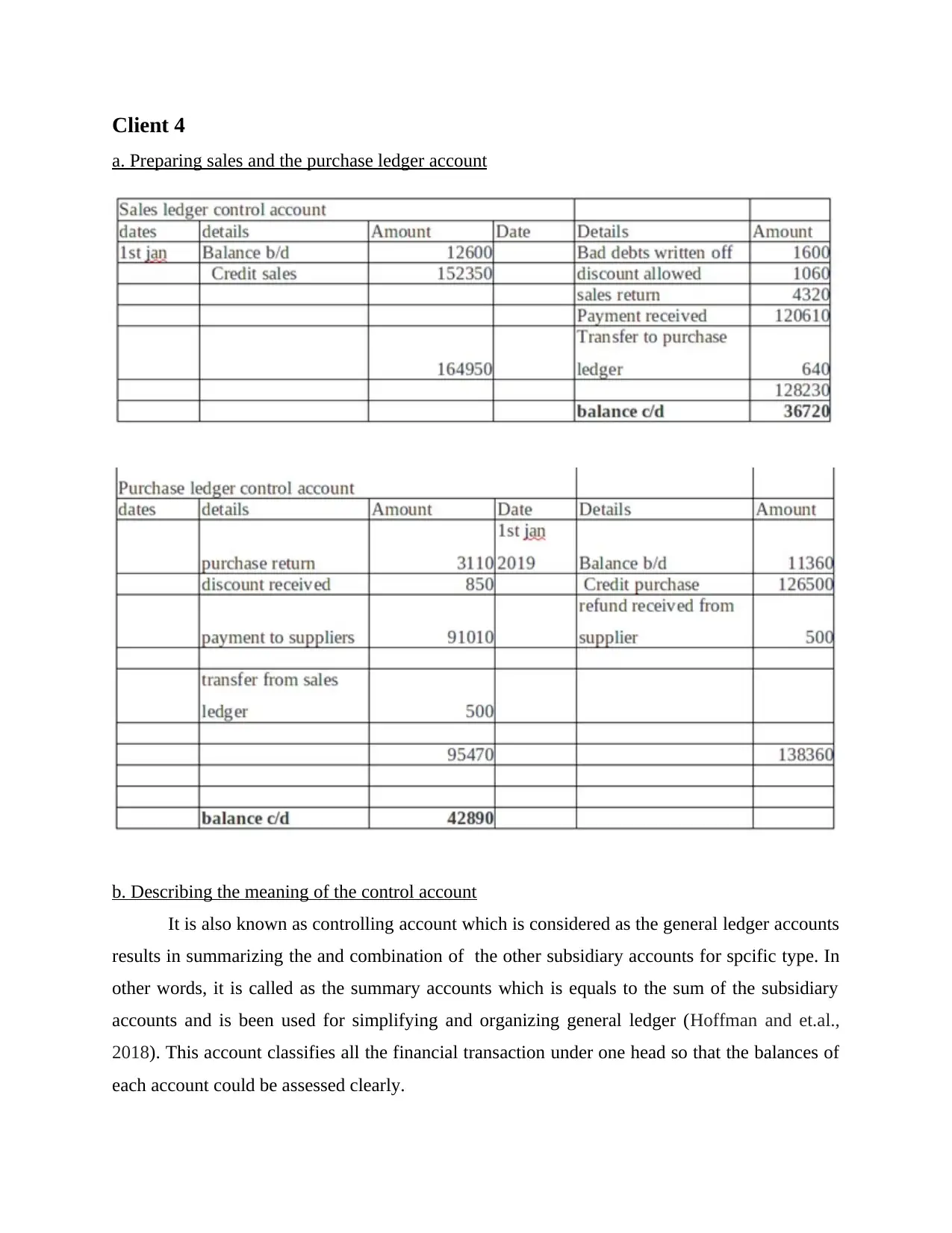

a. Preparing sales and the purchase ledger account

b. Describing the meaning of the control account

It is also known as controlling account which is considered as the general ledger accounts

results in summarizing the and combination of the other subsidiary accounts for spcific type. In

other words, it is called as the summary accounts which is equals to the sum of the subsidiary

accounts and is been used for simplifying and organizing general ledger (Hoffman and et.al.,

2018). This account classifies all the financial transaction under one head so that the balances of

each account could be assessed clearly.

a. Preparing sales and the purchase ledger account

b. Describing the meaning of the control account

It is also known as controlling account which is considered as the general ledger accounts

results in summarizing the and combination of the other subsidiary accounts for spcific type. In

other words, it is called as the summary accounts which is equals to the sum of the subsidiary

accounts and is been used for simplifying and organizing general ledger (Hoffman and et.al.,

2018). This account classifies all the financial transaction under one head so that the balances of

each account could be assessed clearly.

Client 5

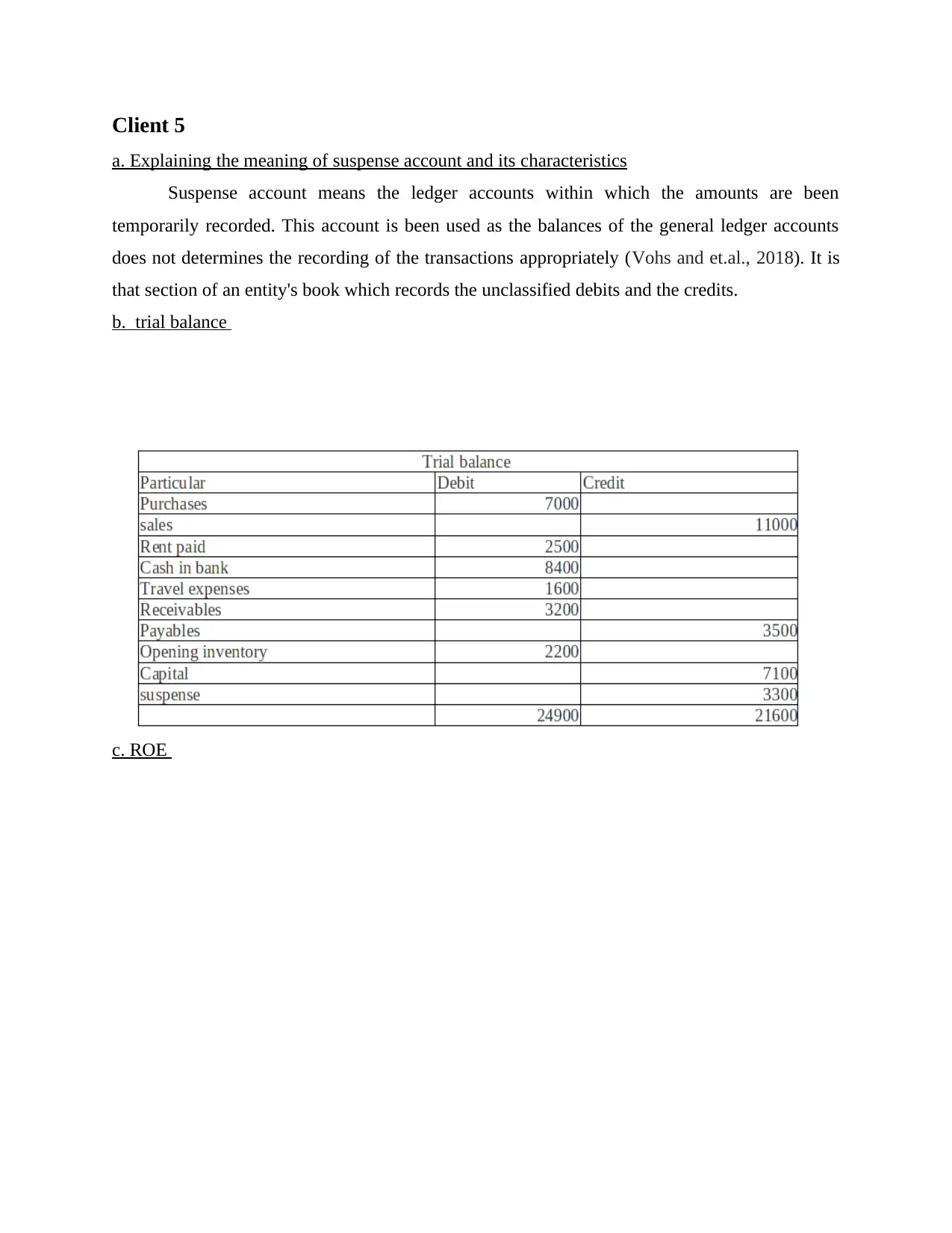

a. Explaining the meaning of suspense account and its characteristics

Suspense account means the ledger accounts within which the amounts are been

temporarily recorded. This account is been used as the balances of the general ledger accounts

does not determines the recording of the transactions appropriately (Vohs and et.al., 2018). It is

that section of an entity's book which records the unclassified debits and the credits.

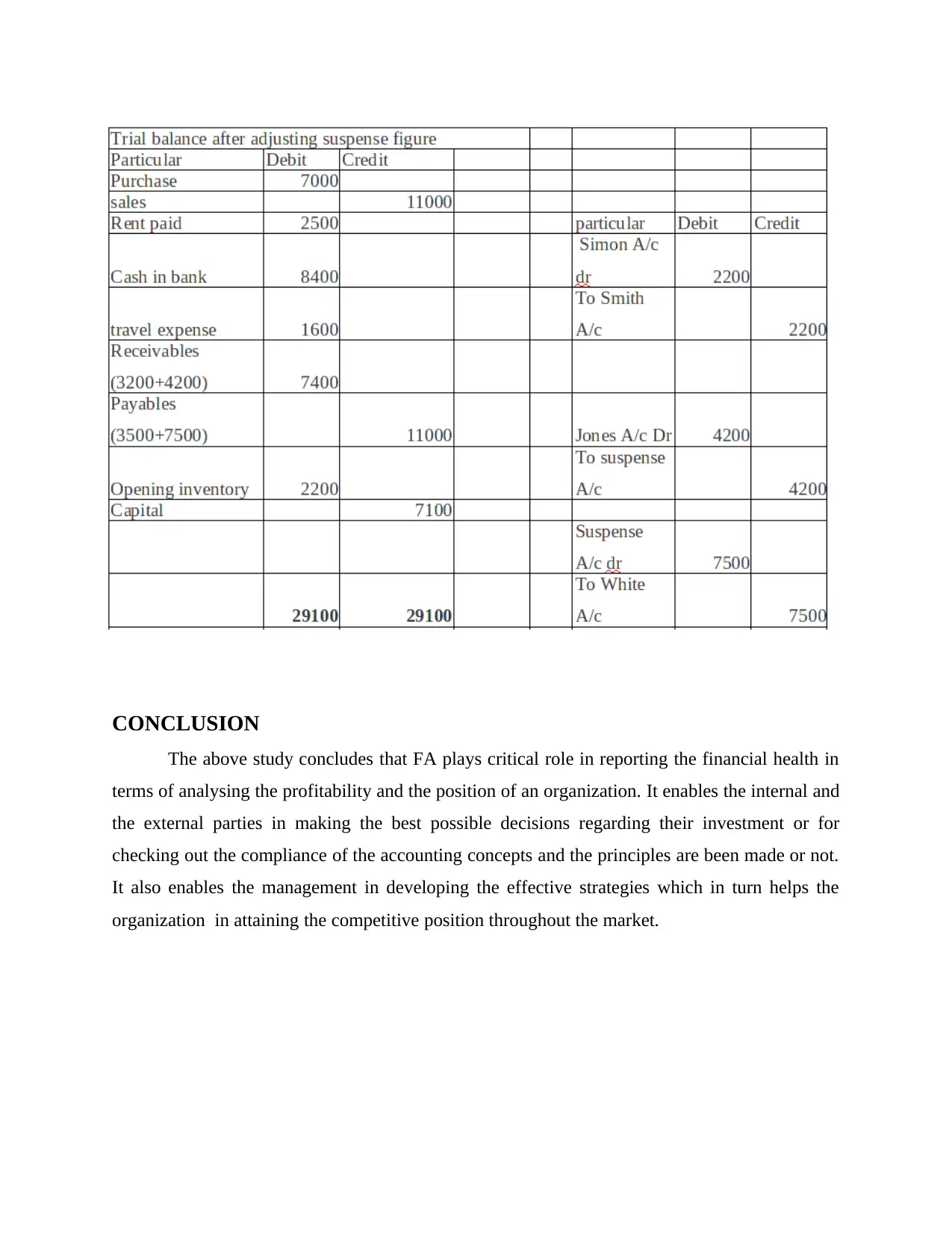

b. trial balance

c. ROE

a. Explaining the meaning of suspense account and its characteristics

Suspense account means the ledger accounts within which the amounts are been

temporarily recorded. This account is been used as the balances of the general ledger accounts

does not determines the recording of the transactions appropriately (Vohs and et.al., 2018). It is

that section of an entity's book which records the unclassified debits and the credits.

b. trial balance

c. ROE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

The above study concludes that FA plays critical role in reporting the financial health in

terms of analysing the profitability and the position of an organization. It enables the internal and

the external parties in making the best possible decisions regarding their investment or for

checking out the compliance of the accounting concepts and the principles are been made or not.

It also enables the management in developing the effective strategies which in turn helps the

organization in attaining the competitive position throughout the market.

The above study concludes that FA plays critical role in reporting the financial health in

terms of analysing the profitability and the position of an organization. It enables the internal and

the external parties in making the best possible decisions regarding their investment or for

checking out the compliance of the accounting concepts and the principles are been made or not.

It also enables the management in developing the effective strategies which in turn helps the

organization in attaining the competitive position throughout the market.

REFERENCES

Books and Journals

Books and Journals

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.