Financial Accounting: Consolidated Financial Statement and Qualitative Characteristics of Financial Information

VerifiedAdded on 2023/06/14

|14

|3985

|320

AI Summary

This report covers the preparation of consolidated financial statement for a group of companies, characteristics of financial statements, financial and non-financial analysis, and importance of professional ethics in accounting. It includes a sample consolidated statement of financial position, calculation of goodwill and non-controlling interest, and discussion on relevance, reliability, and comparability of financial information. The report also evaluates the financial performance of Patrick financial services based on financial and non-financial information.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

UG221 FINANCIAL

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

(a)................................................................................................................................................3

(b)................................................................................................................................................5

Question: 2.......................................................................................................................................7

a. Financial and non-financial analysis.......................................................................................7

b. Importance of professional ethics in accounting and fundamental principles of professional

ethics for accountants..................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

(a)................................................................................................................................................3

(b)................................................................................................................................................5

Question: 2.......................................................................................................................................7

a. Financial and non-financial analysis.......................................................................................7

b. Importance of professional ethics in accounting and fundamental principles of professional

ethics for accountants..................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial accounting provides a base for recording business transaction write from

preparing journal entries till the preparation of final accounts that is, income statement and

statement of financial position (Saura, Palos-Sanchez and Grilo, 2019). So that, summarizing,

analysis and reporting of financial performance and financial position of a concern could be done

at the end of financial period. Financial accounting can be done for all kind of business

organizations whether it is a sole proprietorship, partnership or a company. The present report is

based on preparation of consolidated financial statement for a group of companies by combining

the financial results of a parent and a subsidiary company and accordingly, a consolidated

statement of financial position will be prepared. Also, the characteristics of financial statements

or financial information exhibited by financial statements such as relevance, comparability and

reliability will be discussed in this report. Furthermore, the financial performance of the business

will be evaluated on the basis of both financial and non – financial information and accordingly,

comments will be given on how non – financial information proves to be better than financial

information in indicating the likely future success of the business. At last, discussion will be

done on the importance of professional ethics in accounting along with highlighting the

fundamental principles of the same.

MAIN BODY

Question 1

(a)

Consolidated financial statement means the statement of a group where assets, equity,

liabilities, income, expenses etc. of parent company as well as all of its subsidiaries are combined

or integrate together. This is done in order to reflect the overall financial performance of a group.

The requirement of preparation of consolidated financial statement arises in the situation when

any company acquire more than 50% shares holdings of another company. In that case, the

acquirer is known as parent company while acquire is known as subsidiary (Dewi, Azam and

Yusoff 2019). As per International Financial Reporting Framework, every company who have

subsidiary need to prepare the consolidated financial statement.

Consolidated Statement of Financial Position for the Pee group

Financial accounting provides a base for recording business transaction write from

preparing journal entries till the preparation of final accounts that is, income statement and

statement of financial position (Saura, Palos-Sanchez and Grilo, 2019). So that, summarizing,

analysis and reporting of financial performance and financial position of a concern could be done

at the end of financial period. Financial accounting can be done for all kind of business

organizations whether it is a sole proprietorship, partnership or a company. The present report is

based on preparation of consolidated financial statement for a group of companies by combining

the financial results of a parent and a subsidiary company and accordingly, a consolidated

statement of financial position will be prepared. Also, the characteristics of financial statements

or financial information exhibited by financial statements such as relevance, comparability and

reliability will be discussed in this report. Furthermore, the financial performance of the business

will be evaluated on the basis of both financial and non – financial information and accordingly,

comments will be given on how non – financial information proves to be better than financial

information in indicating the likely future success of the business. At last, discussion will be

done on the importance of professional ethics in accounting along with highlighting the

fundamental principles of the same.

MAIN BODY

Question 1

(a)

Consolidated financial statement means the statement of a group where assets, equity,

liabilities, income, expenses etc. of parent company as well as all of its subsidiaries are combined

or integrate together. This is done in order to reflect the overall financial performance of a group.

The requirement of preparation of consolidated financial statement arises in the situation when

any company acquire more than 50% shares holdings of another company. In that case, the

acquirer is known as parent company while acquire is known as subsidiary (Dewi, Azam and

Yusoff 2019). As per International Financial Reporting Framework, every company who have

subsidiary need to prepare the consolidated financial statement.

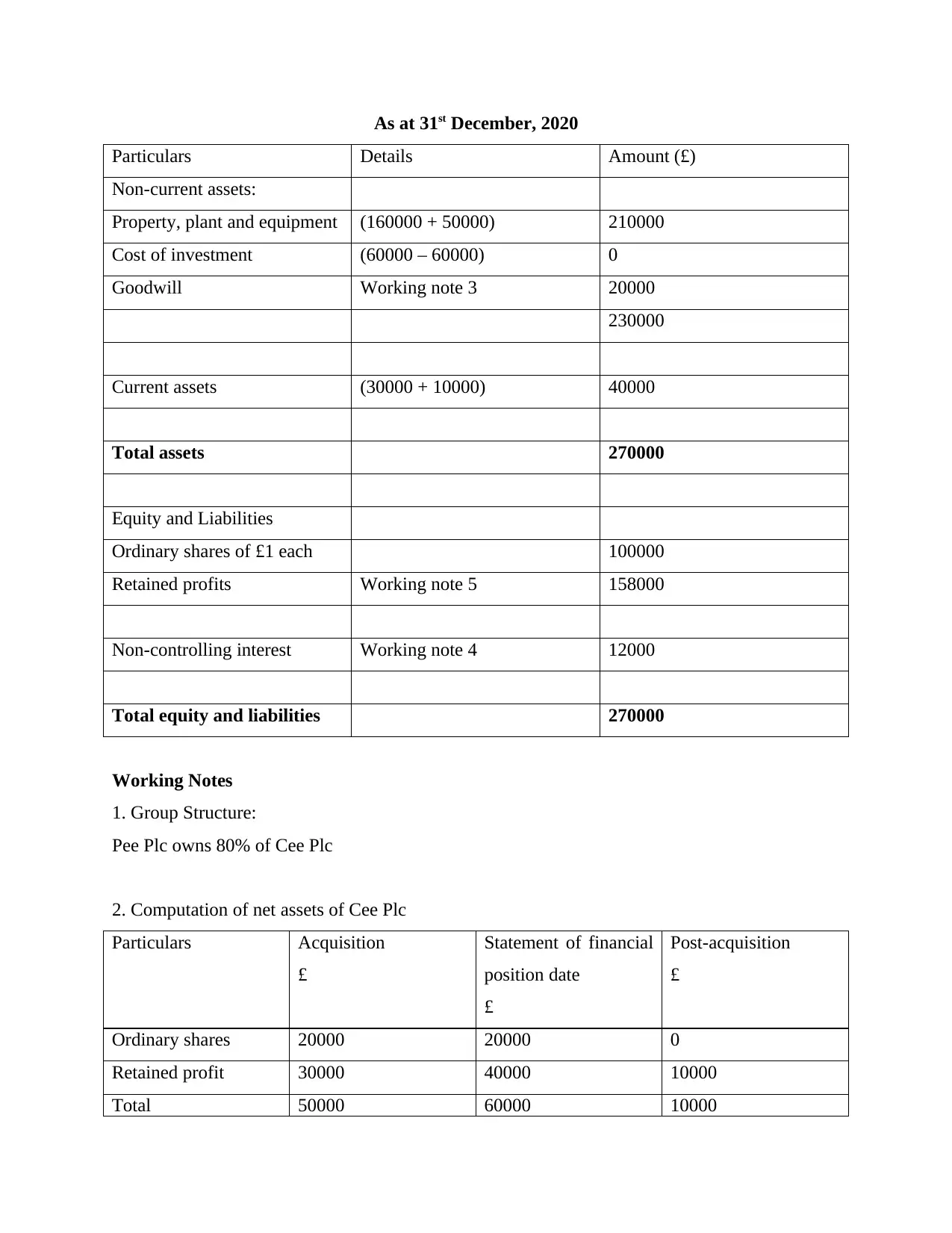

Consolidated Statement of Financial Position for the Pee group

As at 31st December, 2020

Particulars Details Amount (£)

Non-current assets:

Property, plant and equipment (160000 + 50000) 210000

Cost of investment (60000 – 60000) 0

Goodwill Working note 3 20000

230000

Current assets (30000 + 10000) 40000

Total assets 270000

Equity and Liabilities

Ordinary shares of £1 each 100000

Retained profits Working note 5 158000

Non-controlling interest Working note 4 12000

Total equity and liabilities 270000

Working Notes

1. Group Structure:

Pee Plc owns 80% of Cee Plc

2. Computation of net assets of Cee Plc

Particulars Acquisition

£

Statement of financial

position date

£

Post-acquisition

£

Ordinary shares 20000 20000 0

Retained profit 30000 40000 10000

Total 50000 60000 10000

Particulars Details Amount (£)

Non-current assets:

Property, plant and equipment (160000 + 50000) 210000

Cost of investment (60000 – 60000) 0

Goodwill Working note 3 20000

230000

Current assets (30000 + 10000) 40000

Total assets 270000

Equity and Liabilities

Ordinary shares of £1 each 100000

Retained profits Working note 5 158000

Non-controlling interest Working note 4 12000

Total equity and liabilities 270000

Working Notes

1. Group Structure:

Pee Plc owns 80% of Cee Plc

2. Computation of net assets of Cee Plc

Particulars Acquisition

£

Statement of financial

position date

£

Post-acquisition

£

Ordinary shares 20000 20000 0

Retained profit 30000 40000 10000

Total 50000 60000 10000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

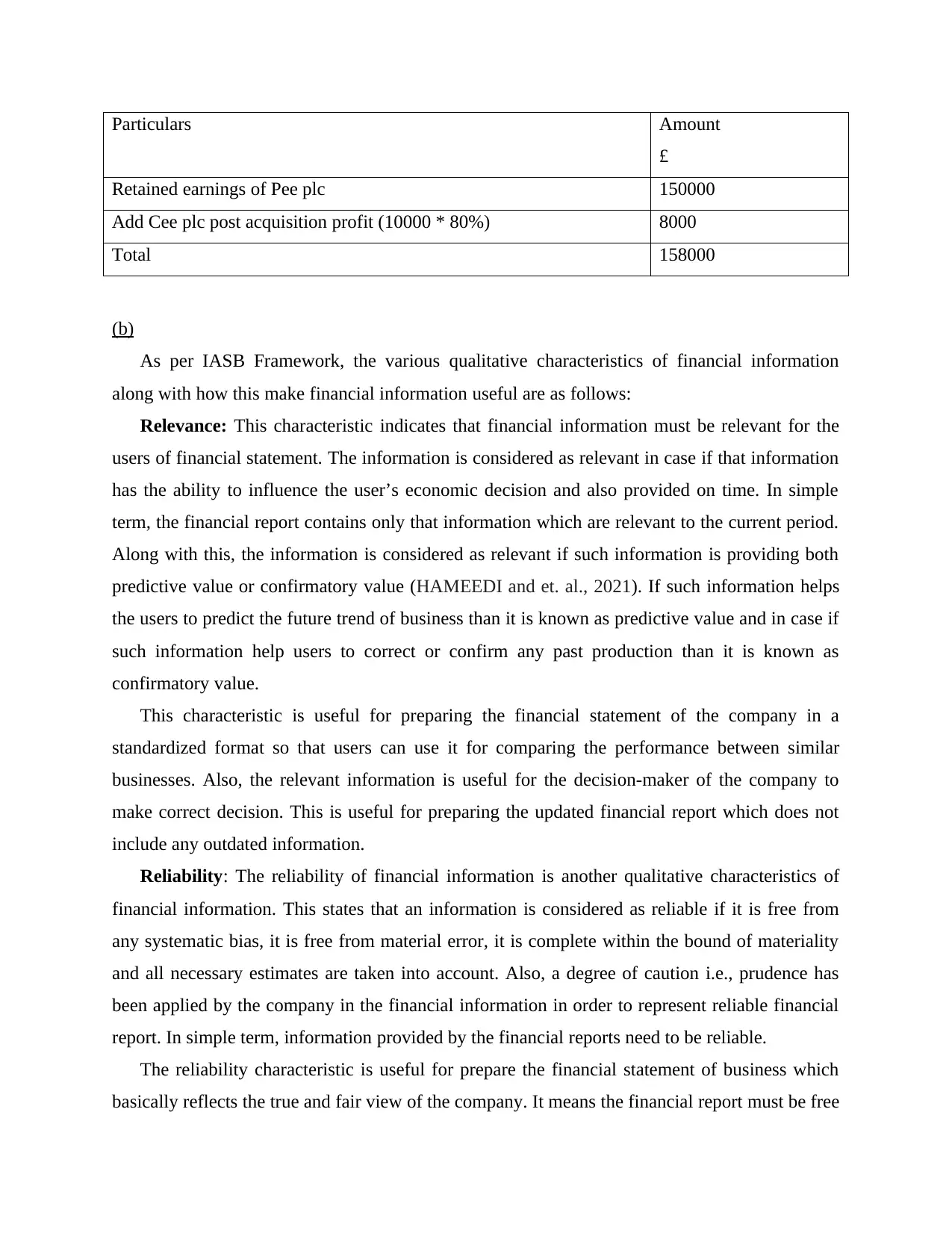

3. Computation of Goodwill

Goodwill is basically an intangible asset which is created at the situation when one

company acquire another company holding for a price greater than its net assets fair value. It

means if the consideration paid plus non-controlling interest of the company is higher than the

fair value of net assets of acquire company in that case goodwill arises. This is recorded on the

non-current assets of the company.

Particulars Amount

£

Consideration transferred 60000

Add Non-controlling interest (50000 * 20%) 10000

Total 70000

Less Fair value of net assets at acquisition -50000

Goodwill at acquisition 20000

4. Computation of Non-controlling interest

Non-controlling interest which is also known as minority interest is a proportion of the

subsidiary corporation stocks which is not owned by the parent corporation. For example, in the

present question Pee plc has acquire or own 80% shares of Cee Plc which is known as

controlling interest and the remaining 20% of Cee Plc shares which is own by general public is

known as non-controlling interest (Daskalov, 2020). The non-controlling interest is recorded on

the non-current liability section or equity section of the consolidated balance sheet of parent

company i.e., Pee group.

Particulars Amount

£

Non-controlling interest at acquisition 10000

Add NCI% of Cee Plc post acquisition (10000 * 20%) 2000

Total 12000

5. Calculation of consolidated retained earnings

Goodwill is basically an intangible asset which is created at the situation when one

company acquire another company holding for a price greater than its net assets fair value. It

means if the consideration paid plus non-controlling interest of the company is higher than the

fair value of net assets of acquire company in that case goodwill arises. This is recorded on the

non-current assets of the company.

Particulars Amount

£

Consideration transferred 60000

Add Non-controlling interest (50000 * 20%) 10000

Total 70000

Less Fair value of net assets at acquisition -50000

Goodwill at acquisition 20000

4. Computation of Non-controlling interest

Non-controlling interest which is also known as minority interest is a proportion of the

subsidiary corporation stocks which is not owned by the parent corporation. For example, in the

present question Pee plc has acquire or own 80% shares of Cee Plc which is known as

controlling interest and the remaining 20% of Cee Plc shares which is own by general public is

known as non-controlling interest (Daskalov, 2020). The non-controlling interest is recorded on

the non-current liability section or equity section of the consolidated balance sheet of parent

company i.e., Pee group.

Particulars Amount

£

Non-controlling interest at acquisition 10000

Add NCI% of Cee Plc post acquisition (10000 * 20%) 2000

Total 12000

5. Calculation of consolidated retained earnings

Particulars Amount

£

Retained earnings of Pee plc 150000

Add Cee plc post acquisition profit (10000 * 80%) 8000

Total 158000

(b)

As per IASB Framework, the various qualitative characteristics of financial information

along with how this make financial information useful are as follows:

Relevance: This characteristic indicates that financial information must be relevant for the

users of financial statement. The information is considered as relevant in case if that information

has the ability to influence the user’s economic decision and also provided on time. In simple

term, the financial report contains only that information which are relevant to the current period.

Along with this, the information is considered as relevant if such information is providing both

predictive value or confirmatory value (HAMEEDI and et. al., 2021). If such information helps

the users to predict the future trend of business than it is known as predictive value and in case if

such information help users to correct or confirm any past production than it is known as

confirmatory value.

This characteristic is useful for preparing the financial statement of the company in a

standardized format so that users can use it for comparing the performance between similar

businesses. Also, the relevant information is useful for the decision-maker of the company to

make correct decision. This is useful for preparing the updated financial report which does not

include any outdated information.

Reliability: The reliability of financial information is another qualitative characteristics of

financial information. This states that an information is considered as reliable if it is free from

any systematic bias, it is free from material error, it is complete within the bound of materiality

and all necessary estimates are taken into account. Also, a degree of caution i.e., prudence has

been applied by the company in the financial information in order to represent reliable financial

report. In simple term, information provided by the financial reports need to be reliable.

The reliability characteristic is useful for prepare the financial statement of business which

basically reflects the true and fair view of the company. It means the financial report must be free

£

Retained earnings of Pee plc 150000

Add Cee plc post acquisition profit (10000 * 80%) 8000

Total 158000

(b)

As per IASB Framework, the various qualitative characteristics of financial information

along with how this make financial information useful are as follows:

Relevance: This characteristic indicates that financial information must be relevant for the

users of financial statement. The information is considered as relevant in case if that information

has the ability to influence the user’s economic decision and also provided on time. In simple

term, the financial report contains only that information which are relevant to the current period.

Along with this, the information is considered as relevant if such information is providing both

predictive value or confirmatory value (HAMEEDI and et. al., 2021). If such information helps

the users to predict the future trend of business than it is known as predictive value and in case if

such information help users to correct or confirm any past production than it is known as

confirmatory value.

This characteristic is useful for preparing the financial statement of the company in a

standardized format so that users can use it for comparing the performance between similar

businesses. Also, the relevant information is useful for the decision-maker of the company to

make correct decision. This is useful for preparing the updated financial report which does not

include any outdated information.

Reliability: The reliability of financial information is another qualitative characteristics of

financial information. This states that an information is considered as reliable if it is free from

any systematic bias, it is free from material error, it is complete within the bound of materiality

and all necessary estimates are taken into account. Also, a degree of caution i.e., prudence has

been applied by the company in the financial information in order to represent reliable financial

report. In simple term, information provided by the financial reports need to be reliable.

The reliability characteristic is useful for prepare the financial statement of business which

basically reflects the true and fair view of the company. It means the financial report must be free

from any fraud, error or omission (Krupka and Muzyka, 2019). Also, the company need to

consider the unfavourable event and avoid biasness to ensure neutrality information while

preparing financial statement.

Comparability: One of the main qualitative characteristics of financial information includes

comparability. It means that information in the financial statement must be present in such way

that it can be easily compared with the similar information of the other entity. For example, the

closing inventory information on financial statement must be present by all companies of single

sector or industry at cost or net realizable value whichever is lower. With the help of this

characteristics, the users of financial statement are able to compare the financial data in order to

identify trend of business and also compare own business health with its competitors.

The comparability characteristics of the financial statement is useful for the both company as

well as users of the financial statement in comparing the profitability, liquidity, efficiency and

solvency position of the company (Zhang, 2018). Further, it is useful for comparing the current

performance of business with the past trends and also useful for comparison of current

information of the company with the competitor’s performance.

Question: 2

a. Financial and non-financial analysis

I. Commenting on the financial performance on the basis of financial information

The financial analysis of Patrick financial services will be done by using financial

parameters to describe different aspects such as the growth, profitability & credit management of

the business.

Growth: The turnover of the business has increased by 5% in the current year as compared to

previous year which is indicating a sign of business growth (Hosaka, 2019). Also, this increase is

greater than the inflation and thus, showing a real growth of the business. However, a negative

sign of growth can be seen through the net profit margin which was 20% in previous year and

19.8% in current year. This is may be due to the rise in costs or reduction in fee levels charged

for professional services to compete in the market. Further, a higher cash balance by 5% in the

current year shows improvement or growth in liquidity.

consider the unfavourable event and avoid biasness to ensure neutrality information while

preparing financial statement.

Comparability: One of the main qualitative characteristics of financial information includes

comparability. It means that information in the financial statement must be present in such way

that it can be easily compared with the similar information of the other entity. For example, the

closing inventory information on financial statement must be present by all companies of single

sector or industry at cost or net realizable value whichever is lower. With the help of this

characteristics, the users of financial statement are able to compare the financial data in order to

identify trend of business and also compare own business health with its competitors.

The comparability characteristics of the financial statement is useful for the both company as

well as users of the financial statement in comparing the profitability, liquidity, efficiency and

solvency position of the company (Zhang, 2018). Further, it is useful for comparing the current

performance of business with the past trends and also useful for comparison of current

information of the company with the competitor’s performance.

Question: 2

a. Financial and non-financial analysis

I. Commenting on the financial performance on the basis of financial information

The financial analysis of Patrick financial services will be done by using financial

parameters to describe different aspects such as the growth, profitability & credit management of

the business.

Growth: The turnover of the business has increased by 5% in the current year as compared to

previous year which is indicating a sign of business growth (Hosaka, 2019). Also, this increase is

greater than the inflation and thus, showing a real growth of the business. However, a negative

sign of growth can be seen through the net profit margin which was 20% in previous year and

19.8% in current year. This is may be due to the rise in costs or reduction in fee levels charged

for professional services to compete in the market. Further, a higher cash balance by 5% in the

current year shows improvement or growth in liquidity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profitability: Net profit is higher by 3.9% in current year as compared to previous year which

indicates that the overall profitability of the business has improved and the reason for this

increase can be credited to the higher turnover of the business.

Credit management: This aspect of the business can be explained through average trade

receivables days which has reduced by 3 days in current year indicating better credit policies

along with improvement in efficiency of recovering outstanding debts. Also, Patrick's

receivables days are less than that of industry average which reflects better working capital

management within the firm (Fernando, Li and Hou, 2020).

On the basis of financial analysis done through financial information, it could be said that

there could be possible concern for Patrick's regarding their low growth and margins, however

overall performance of the business seems to be quite good and indicates healthy future.

II. Comparison between financial and non-financial information

Financial information generally give insight of the past performance of the business

which is not sufficient for making it sure that the a better performance in the past will remains

the same in future as there may be higher costs or losing clients which may render the business

into losses. However, non-financial information are regarded as indicators of future performance

and accordingly, if it is showing good results, then it could be said that future financial

performance would be better (Maama and Mkhize, 2020). For instance, by delivering good

quality products to the customers, the business can have more customers in future also at higher

prices. The non-financial information can be obtained through business's balanced scorecard.

Within the balanced scorecard, internal processes indicates current cost efficiency which

is helpful in securing better profitability in future results. Also, a good performance in terms of

customer knowledge is helpful in getting more customers in the future. At last, measures such as

learning and innovation indicates the way in which the business is developing in terms of staff

retention, new products, etc. which are quite future focused measures and thus indicates the

likely future successes of the business better than financial information that is based on past

performance.

Accordingly, non-financial measures of business performance gives better view of

business success in the upcoming period than financial measures (Chen and Zhao, 2021).

III.Commenting on the financial performance on the basis of non-financial information

indicates that the overall profitability of the business has improved and the reason for this

increase can be credited to the higher turnover of the business.

Credit management: This aspect of the business can be explained through average trade

receivables days which has reduced by 3 days in current year indicating better credit policies

along with improvement in efficiency of recovering outstanding debts. Also, Patrick's

receivables days are less than that of industry average which reflects better working capital

management within the firm (Fernando, Li and Hou, 2020).

On the basis of financial analysis done through financial information, it could be said that

there could be possible concern for Patrick's regarding their low growth and margins, however

overall performance of the business seems to be quite good and indicates healthy future.

II. Comparison between financial and non-financial information

Financial information generally give insight of the past performance of the business

which is not sufficient for making it sure that the a better performance in the past will remains

the same in future as there may be higher costs or losing clients which may render the business

into losses. However, non-financial information are regarded as indicators of future performance

and accordingly, if it is showing good results, then it could be said that future financial

performance would be better (Maama and Mkhize, 2020). For instance, by delivering good

quality products to the customers, the business can have more customers in future also at higher

prices. The non-financial information can be obtained through business's balanced scorecard.

Within the balanced scorecard, internal processes indicates current cost efficiency which

is helpful in securing better profitability in future results. Also, a good performance in terms of

customer knowledge is helpful in getting more customers in the future. At last, measures such as

learning and innovation indicates the way in which the business is developing in terms of staff

retention, new products, etc. which are quite future focused measures and thus indicates the

likely future successes of the business better than financial information that is based on past

performance.

Accordingly, non-financial measures of business performance gives better view of

business success in the upcoming period than financial measures (Chen and Zhao, 2021).

III.Commenting on the financial performance on the basis of non-financial information

The non-financial information as stated within the balanced scorecard will be used for analysing

the business performance which gives better insights over operational issues and accordingly,

facilitates better picture of the future.

Internal business processes: It indicates the internal efficiency of the business. Here, efficiency

can be explained through error rate which has increased from 10 to 16% in the current year

which is may be due to the reduction in turnaround times in an attempt to make delivery on time.

Being in accounting and taxation field, such errors could lead clients into difficulties and even

they may be sued due to such errors (Mysaka, Derun and Skliaruk, 2021).

Customer Knowledge: It can be determined through the number of customers for two years

which has reduced in the current year indicating poor client retention which may be due to high

level of dissatisfaction among customers. Moreover, accounting firm generally expects repeated

work from clients every year and if the quality of service is not appropriate, then existing client

may move to competitors.

Also, there is an increase of 29% in average fees in the current year and on this basis it

can be said that increase in revenues within the current year is due to high fees charged from

clients and not due to getting extra clients (Maama and Mkhize, 2020). This may lead to losing

clients as well because Patrick's have less number of customers in the current year.

Due to both the above two reasons that is, higher fees charged and less number of

customer retained in the current year, there is a reduction in market share of around 6% for

Patrick in current year, however, the size of the market has grown from $4.5 m to the total

market revenue in the current of $6.75 m which indicates an increase of 50% in the size of the

market. Accordingly, in the scenario of greater size of market, the position of Patrick's is quite

worrying. Therefore, efforts are needed from Patrick to do much better and look forward to left

behind their competitors (Mysaka, Derun and Skliaruk, 2021).

Learning & Growth: As compared to competitors, Patrick is offering very fewer services apart

from their core services. The industry average is much higher in terms of offering non – core

services as a percentage of their revenues which is given 25% for previous and 30% for the

current year indicating a rise in revenue from non-core activities. However, Patrick's revenue has

reduced from 5% to 4% in the current which is its biggest weaknesses in terms of inability to

derive revenue from non-core business activities (Hosaka, 2019). Also, it can be said that Patrick

the business performance which gives better insights over operational issues and accordingly,

facilitates better picture of the future.

Internal business processes: It indicates the internal efficiency of the business. Here, efficiency

can be explained through error rate which has increased from 10 to 16% in the current year

which is may be due to the reduction in turnaround times in an attempt to make delivery on time.

Being in accounting and taxation field, such errors could lead clients into difficulties and even

they may be sued due to such errors (Mysaka, Derun and Skliaruk, 2021).

Customer Knowledge: It can be determined through the number of customers for two years

which has reduced in the current year indicating poor client retention which may be due to high

level of dissatisfaction among customers. Moreover, accounting firm generally expects repeated

work from clients every year and if the quality of service is not appropriate, then existing client

may move to competitors.

Also, there is an increase of 29% in average fees in the current year and on this basis it

can be said that increase in revenues within the current year is due to high fees charged from

clients and not due to getting extra clients (Maama and Mkhize, 2020). This may lead to losing

clients as well because Patrick's have less number of customers in the current year.

Due to both the above two reasons that is, higher fees charged and less number of

customer retained in the current year, there is a reduction in market share of around 6% for

Patrick in current year, however, the size of the market has grown from $4.5 m to the total

market revenue in the current of $6.75 m which indicates an increase of 50% in the size of the

market. Accordingly, in the scenario of greater size of market, the position of Patrick's is quite

worrying. Therefore, efforts are needed from Patrick to do much better and look forward to left

behind their competitors (Mysaka, Derun and Skliaruk, 2021).

Learning & Growth: As compared to competitors, Patrick is offering very fewer services apart

from their core services. The industry average is much higher in terms of offering non – core

services as a percentage of their revenues which is given 25% for previous and 30% for the

current year indicating a rise in revenue from non-core activities. However, Patrick's revenue has

reduced from 5% to 4% in the current which is its biggest weaknesses in terms of inability to

derive revenue from non-core business activities (Hosaka, 2019). Also, it can be said that Patrick

is ignoring the fact that they may get more clients who are expecting wider range of services

from accountants of Patrick.

In addition to this, there is low employee retention rate which shows that there is high

employee turnover due dissatisfaction among staff. In a business like accounting services, there

is a necessity to ensure staff continuity for the provision of better quality services because in case

of conservative clients, there may be resentment among them in sharing their confidential details

to a new person every time (Chen and Zhao, 2021). The reason behind high staff turnover could

be extra work pressure in completing their jobs in quick manner without satisfying themselves

that the job has been performed well. Along with this, the reason of low staff retention rate could

be less scope of gaining experience and ensure growth oriented career paths as the business is

offering less number of services apart from services associated with their core business activities.

b. Importance of professional ethics in accounting and fundamental principles of professional

ethics for accountants

With the existence of professional ethics, accountants resort to compliance with the laws

& regulations which is meant for governing their bodies of work and their respective

jurisdictions. In the absence of such ethics for professionals like accountants, there would be

negative effect on the reputation of that profession. To ensure ethical behaviour of professionals,

there are five fundamental principles established for professional accountant which indicates a

standard behaviour expected from them.

Another reason due to which professional ethics are important is that it promotes loyal

relationship and build trust with that of the users of accounting information (Bafghi, 2021). The

professional ethics are helpful in protecting the interests of various users of accounting

information such as investors and creditors who are directly affected by the conduct of

accountant as their decisions are based on the financial results indicates through financial

statements prepared by accountants. Also, the importance of professional ethics can be seen

through necessity of exhibiting required level of skills, knowledge and expertise while

performing accounting and preparing financial statements of the company. At last, it could be

said that ethical code of professional accountant is necessary as number of people rely upon their

expertise in measuring business performance and position along with ensuring that there is no

disclosure of confidential or sensitive information of the company in an unauthorized hand.

Fundamental principles of professional ethics for accountants

from accountants of Patrick.

In addition to this, there is low employee retention rate which shows that there is high

employee turnover due dissatisfaction among staff. In a business like accounting services, there

is a necessity to ensure staff continuity for the provision of better quality services because in case

of conservative clients, there may be resentment among them in sharing their confidential details

to a new person every time (Chen and Zhao, 2021). The reason behind high staff turnover could

be extra work pressure in completing their jobs in quick manner without satisfying themselves

that the job has been performed well. Along with this, the reason of low staff retention rate could

be less scope of gaining experience and ensure growth oriented career paths as the business is

offering less number of services apart from services associated with their core business activities.

b. Importance of professional ethics in accounting and fundamental principles of professional

ethics for accountants

With the existence of professional ethics, accountants resort to compliance with the laws

& regulations which is meant for governing their bodies of work and their respective

jurisdictions. In the absence of such ethics for professionals like accountants, there would be

negative effect on the reputation of that profession. To ensure ethical behaviour of professionals,

there are five fundamental principles established for professional accountant which indicates a

standard behaviour expected from them.

Another reason due to which professional ethics are important is that it promotes loyal

relationship and build trust with that of the users of accounting information (Bafghi, 2021). The

professional ethics are helpful in protecting the interests of various users of accounting

information such as investors and creditors who are directly affected by the conduct of

accountant as their decisions are based on the financial results indicates through financial

statements prepared by accountants. Also, the importance of professional ethics can be seen

through necessity of exhibiting required level of skills, knowledge and expertise while

performing accounting and preparing financial statements of the company. At last, it could be

said that ethical code of professional accountant is necessary as number of people rely upon their

expertise in measuring business performance and position along with ensuring that there is no

disclosure of confidential or sensitive information of the company in an unauthorized hand.

Fundamental principles of professional ethics for accountants

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

There are five fundamental principles that a professional accountant is required to

complied with, such as the following:

Integrity: It is necessary for a professional accountant to be straightforward & honest in carrying

out or satisfying all of their business & professional relationships. It also implies that members of

the professional association must not get associated with any kind of professional information

intentionally (Onumah, Simpson and Kwarteng, 2021).

Objectivity: A member of professional association should not allow any kind of compromise

while making business or professional judgement as a result of conflict of interest, biasses and

undue influence of any third party. Also, at the time of assurance engagement, it necessary for

members to be independent.

Professional competence & due care: It is necessary for a professional accountant to maintain

or even attain the level of skills & knowledge that is required to be make sure that whatever

professional service has been provided to a client or organization is up to the mark of

competency level required and thus the employing organization or client will receive competent

services. Also, the services and act of professional accountant should be based on the standards

& relevant legislation applicable on a particular professional body.

Confidentiality: A professional accountant should ensure and take necessary steps in

maintaining the confidentiality of information that they receive during their professional or

business course and accordingly, must not disclose such confidential or sensitive information to

external parties without having proper authority (Ilemona and Nwite, 2021). Therefore,

disclosure of information can be done only in the event when there is legal duty or right to do so.

Also, such confidential information acquired by professional accountant should not be used for

their own or third party's personal benefits.

Professional behaviour: Professional accountant is necessarily required to follow all the

applicable laws and regulations. Accordingly, they must avoid such actions that are intended to

disgrace their professional.

CONCLUSION

After summing up the above information, it is concluded from the report that financial

statement of the company must represent the reliable, relevant and comparable information to

users of financial statement. Further, the report has also computed the consolidated balance sheet

of Pee group as Pee plc has acquire 80% shares of Cee plc. In addition to this, the report has also

complied with, such as the following:

Integrity: It is necessary for a professional accountant to be straightforward & honest in carrying

out or satisfying all of their business & professional relationships. It also implies that members of

the professional association must not get associated with any kind of professional information

intentionally (Onumah, Simpson and Kwarteng, 2021).

Objectivity: A member of professional association should not allow any kind of compromise

while making business or professional judgement as a result of conflict of interest, biasses and

undue influence of any third party. Also, at the time of assurance engagement, it necessary for

members to be independent.

Professional competence & due care: It is necessary for a professional accountant to maintain

or even attain the level of skills & knowledge that is required to be make sure that whatever

professional service has been provided to a client or organization is up to the mark of

competency level required and thus the employing organization or client will receive competent

services. Also, the services and act of professional accountant should be based on the standards

& relevant legislation applicable on a particular professional body.

Confidentiality: A professional accountant should ensure and take necessary steps in

maintaining the confidentiality of information that they receive during their professional or

business course and accordingly, must not disclose such confidential or sensitive information to

external parties without having proper authority (Ilemona and Nwite, 2021). Therefore,

disclosure of information can be done only in the event when there is legal duty or right to do so.

Also, such confidential information acquired by professional accountant should not be used for

their own or third party's personal benefits.

Professional behaviour: Professional accountant is necessarily required to follow all the

applicable laws and regulations. Accordingly, they must avoid such actions that are intended to

disgrace their professional.

CONCLUSION

After summing up the above information, it is concluded from the report that financial

statement of the company must represent the reliable, relevant and comparable information to

users of financial statement. Further, the report has also computed the consolidated balance sheet

of Pee group as Pee plc has acquire 80% shares of Cee plc. In addition to this, the report has also

concluded why non-financial information give better indication of future success of business as

compared to financial information. Lastly, the report has briefly discussed the importance of

professional ethics along with the five fundamental principles of professional ethics need to be

follow by accountant.

compared to financial information. Lastly, the report has briefly discussed the importance of

professional ethics along with the five fundamental principles of professional ethics need to be

follow by accountant.

REFERENCES

Bafghi, A. A. T., 2021. Professional Ethics and Behavior in Accounting. International Journal of

Multicultural and Multireligious Understanding. 8(1). pp.545-555.

Chen, G. and Zhao, W., 2021, February. Application Research of Non-financial Indicators in the

Evaluation of Enterprise Performance. In 2020 International Conference on Modern

Education Management, Innovation and Entrepreneurship and Social Science

(MEMIESS 2020) (pp. 103-108). Atlantis Press.

Daskalov, Y., 2020. Qualitative Characteristics of the Information Presented in the Financial

Statements Prepared on the Basis of the International Public Sector Accounting

Standards. Nauchni trudove. (1). pp.89-97.

Dewi, N., Azam, S. and Yusoff, S., 2019. Factors influencing the information quality of local

government financial statement and financial accountability. Management Science

Letters. 9(9). pp.1373-1384.

Fernando, J. M. R., Li, L. and Hou, G. , 2020. Financial versus non-financial information for

default prediction: evidence from Sri Lanka and the USA. Emerging Markets Finance

and Trade. 56(3). pp.673-692.

HAMEEDI, K. S. and et. al., 2021. Financial performance reporting, IFRS implementation, and

accounting information: Evidence from Iraqi banking sector. The Journal of Asian

Finance, Economics and Business. 8(3). pp.1083-1094.

Hosaka, T. , 2019. Bankruptcy prediction using imaged financial ratios and convolutional neural

networks. Expert systems with applications. 117.pp.287-299.

Ilemona, A. S. and Nwite, S., 2021. Accounting Code of Ethics: Severity Analysis of Threats to

Compliance of Auditors in Nigerian Business Environment. Journal of Finance and

Accounting”. 9(1). pp.16-22.

Krupka, Y. and Muzyka, M., 2019. On qualitative characteristics of financial reporting. Herald

of Ternopil National Economic University, (3 (85)), pp.97-106.

Maama, H. and Mkhize, M. , 2020. Integration of non-financial information into corporate

reporting: a theoretical perspective. Academy of Accounting and Financial Studies

Journal. 24(2). pp.1-15.

Bafghi, A. A. T., 2021. Professional Ethics and Behavior in Accounting. International Journal of

Multicultural and Multireligious Understanding. 8(1). pp.545-555.

Chen, G. and Zhao, W., 2021, February. Application Research of Non-financial Indicators in the

Evaluation of Enterprise Performance. In 2020 International Conference on Modern

Education Management, Innovation and Entrepreneurship and Social Science

(MEMIESS 2020) (pp. 103-108). Atlantis Press.

Daskalov, Y., 2020. Qualitative Characteristics of the Information Presented in the Financial

Statements Prepared on the Basis of the International Public Sector Accounting

Standards. Nauchni trudove. (1). pp.89-97.

Dewi, N., Azam, S. and Yusoff, S., 2019. Factors influencing the information quality of local

government financial statement and financial accountability. Management Science

Letters. 9(9). pp.1373-1384.

Fernando, J. M. R., Li, L. and Hou, G. , 2020. Financial versus non-financial information for

default prediction: evidence from Sri Lanka and the USA. Emerging Markets Finance

and Trade. 56(3). pp.673-692.

HAMEEDI, K. S. and et. al., 2021. Financial performance reporting, IFRS implementation, and

accounting information: Evidence from Iraqi banking sector. The Journal of Asian

Finance, Economics and Business. 8(3). pp.1083-1094.

Hosaka, T. , 2019. Bankruptcy prediction using imaged financial ratios and convolutional neural

networks. Expert systems with applications. 117.pp.287-299.

Ilemona, A. S. and Nwite, S., 2021. Accounting Code of Ethics: Severity Analysis of Threats to

Compliance of Auditors in Nigerian Business Environment. Journal of Finance and

Accounting”. 9(1). pp.16-22.

Krupka, Y. and Muzyka, M., 2019. On qualitative characteristics of financial reporting. Herald

of Ternopil National Economic University, (3 (85)), pp.97-106.

Maama, H. and Mkhize, M. , 2020. Integration of non-financial information into corporate

reporting: a theoretical perspective. Academy of Accounting and Financial Studies

Journal. 24(2). pp.1-15.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mysaka, H., Derun, I. and Skliaruk, I., 2021. The role of non-financial reporting in modern

ecological problems updating and solving. Journal of Environmental Management &

Tourism. 12(1). pp.18-29.

Onumah, R. M., Simpson, S. N. Y. and Kwarteng, A., 2021. The effects of ethics education

interventions on ethical attitudes of professional accountants: evidence from

Ghana. Accounting Education. 30(4). pp.413-437.

Saura, J. R., Palos-Sanchez, P. and Grilo, A., 2019. Detecting indicators for startup business

success: Sentiment analysis using text data mining. Sustainability. 11(3). p.917.

Zhang, J. H., 2018. Accounting comparability, audit effort, and audit outcomes. Contemporary

Accounting Research. 35(1). pp.245-276.

ecological problems updating and solving. Journal of Environmental Management &

Tourism. 12(1). pp.18-29.

Onumah, R. M., Simpson, S. N. Y. and Kwarteng, A., 2021. The effects of ethics education

interventions on ethical attitudes of professional accountants: evidence from

Ghana. Accounting Education. 30(4). pp.413-437.

Saura, J. R., Palos-Sanchez, P. and Grilo, A., 2019. Detecting indicators for startup business

success: Sentiment analysis using text data mining. Sustainability. 11(3). p.917.

Zhang, J. H., 2018. Accounting comparability, audit effort, and audit outcomes. Contemporary

Accounting Research. 35(1). pp.245-276.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.