Financial Accounting Report: Client Accounts and Principles

VerifiedAdded on 2020/11/23

|38

|4842

|66

Report

AI Summary

This report provides a comprehensive overview of financial accounting, beginning with an introduction to financial accounting principles and regulations, including GAAP and IFRS. It details the importance of financial statements and their role in decision-making. The report then analyzes various accounting concepts like consistency and material disclosures. Several client case studies are presented, demonstrating the practical application of accounting principles. These cases include journal entries, ledger accounts, trial balances, profit and loss calculations, balance sheet preparation, bank reconciliation, and the formation of control accounts. The report also discusses suspense accounts and their characteristics. Finally, the report concludes with a summary of the key concepts and principles discussed, providing a valuable resource for students studying financial accounting. The report emphasizes the importance of accurate financial reporting for stakeholders and the significance of adhering to accounting standards.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

A. Reporting accounting regulations to the firm........................................................................1

Description of financial accounting.............................................................................................1

Various Regulations related to financial accounting...................................................................2

Various accounting rules and principles......................................................................................3

Concepts related to consistency and material disclosures...........................................................4

CLIENT 1........................................................................................................................................5

1. Draft of Journal for Client 1 as on May 1st 2017\....................................................................5

2. Preparation of ledger accounts for journal entries...................................................................7

3. Preparation of trial balance for Client 1................................................................................17

CLIENT 2......................................................................................................................................17

A. Computation of Profit and Loss Account for the year ending December 31st 2017.............17

B. Computation of balance Sheet for the year ending December 31st 2017..............................18

CLIENT 3......................................................................................................................................20

A. Computation of Profit and Loss Account for Rain Tree Ltd. for the year ending September

30th 2017.....................................................................................................................................20

B. Ascertaining financial position of Raintree Ltd....................................................................21

C. Analysing various concepts and principles of accounting....................................................26

D. Analysing the significance of measuring and representing depreciation.............................27

CLIENT 4......................................................................................................................................27

A. Assessment of aim for preparing bank statement.................................................................27

B. Identification of reasons for preparing bank statements.......................................................28

C. Preparation of Client’s Cash Book........................................................................................28

CLIENT 5......................................................................................................................................29

A. Formation of Sales Ledger Control and Purchase ledger Control of Henderson for the year

2017...........................................................................................................................................29

B. Defining Control Accounts...................................................................................................30

CLIENT 6......................................................................................................................................30

A. Analysis of Suspense Accounts and its characteristics.........................................................30

B. Preparation of trial balance...................................................................................................31

INTRODUCTION...........................................................................................................................1

A. Reporting accounting regulations to the firm........................................................................1

Description of financial accounting.............................................................................................1

Various Regulations related to financial accounting...................................................................2

Various accounting rules and principles......................................................................................3

Concepts related to consistency and material disclosures...........................................................4

CLIENT 1........................................................................................................................................5

1. Draft of Journal for Client 1 as on May 1st 2017\....................................................................5

2. Preparation of ledger accounts for journal entries...................................................................7

3. Preparation of trial balance for Client 1................................................................................17

CLIENT 2......................................................................................................................................17

A. Computation of Profit and Loss Account for the year ending December 31st 2017.............17

B. Computation of balance Sheet for the year ending December 31st 2017..............................18

CLIENT 3......................................................................................................................................20

A. Computation of Profit and Loss Account for Rain Tree Ltd. for the year ending September

30th 2017.....................................................................................................................................20

B. Ascertaining financial position of Raintree Ltd....................................................................21

C. Analysing various concepts and principles of accounting....................................................26

D. Analysing the significance of measuring and representing depreciation.............................27

CLIENT 4......................................................................................................................................27

A. Assessment of aim for preparing bank statement.................................................................27

B. Identification of reasons for preparing bank statements.......................................................28

C. Preparation of Client’s Cash Book........................................................................................28

CLIENT 5......................................................................................................................................29

A. Formation of Sales Ledger Control and Purchase ledger Control of Henderson for the year

2017...........................................................................................................................................29

B. Defining Control Accounts...................................................................................................30

CLIENT 6......................................................................................................................................30

A. Analysis of Suspense Accounts and its characteristics.........................................................30

B. Preparation of trial balance...................................................................................................31

C. Conducting Journal Entries...................................................................................................31

D. Assessment of difference between Clearing Account and Suspense Account.....................32

CONCLUSION..............................................................................................................................32

REFERENCES..............................................................................................................................33

D. Assessment of difference between Clearing Account and Suspense Account.....................32

CONCLUSION..............................................................................................................................32

REFERENCES..............................................................................................................................33

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management helps in ensuring that proper concepts and principles are being

followed by the organization while preparing presentation of various books of accounts. The

report is responsible for making comprehensive discussion regarding various accounting

principles that have been issued by GAAP. It will also help in spotting depreciation methods that

can be used by the companies while preparing their financial statements. The report then

discusses regarding trial balance and importance of maintain Bank reconciliation statements for

the organization so as to find out difference between pass book and cash book. In the end,

control account, clearing account and suspense account will be discussed in the report.

A. Reporting accounting regulations to the firm

To

Line manager

From: Junior Accountant

Subject: Analysing terminologies related to accounting and making the management aware of

various accounting principles

Sir

In order to improve the overall functioning of organization, it is important to prepare an

assessment of the rules and regulations that are required to be followed by management for its

effective operations. It helps in bringing the overall improvement in business transactions in

such a manner that it can help in improving overall transactional activities of business. There

are various accounting techniques that can be adopted by the managers that can further play an

important role in budgeting, costing and forecasting various operational tasks in an

organizational set up.

Description of financial accounting

Financial accounting is one of the most important fields of accounting that is concerned

towards preparation of summarized books of accounting that can further be used for analysis

and reporting purposes. It also helps in disclosing various financial transactions of company.

These financial statements can be utilized for public consumption as well. It is generally

presented in the format of Profit and Loss Account, Statement of Stockholder’s equity Cash

Flow Statement and Statement of financial position. It plays a substantial role in analysing the

1

Financial management helps in ensuring that proper concepts and principles are being

followed by the organization while preparing presentation of various books of accounts. The

report is responsible for making comprehensive discussion regarding various accounting

principles that have been issued by GAAP. It will also help in spotting depreciation methods that

can be used by the companies while preparing their financial statements. The report then

discusses regarding trial balance and importance of maintain Bank reconciliation statements for

the organization so as to find out difference between pass book and cash book. In the end,

control account, clearing account and suspense account will be discussed in the report.

A. Reporting accounting regulations to the firm

To

Line manager

From: Junior Accountant

Subject: Analysing terminologies related to accounting and making the management aware of

various accounting principles

Sir

In order to improve the overall functioning of organization, it is important to prepare an

assessment of the rules and regulations that are required to be followed by management for its

effective operations. It helps in bringing the overall improvement in business transactions in

such a manner that it can help in improving overall transactional activities of business. There

are various accounting techniques that can be adopted by the managers that can further play an

important role in budgeting, costing and forecasting various operational tasks in an

organizational set up.

Description of financial accounting

Financial accounting is one of the most important fields of accounting that is concerned

towards preparation of summarized books of accounting that can further be used for analysis

and reporting purposes. It also helps in disclosing various financial transactions of company.

These financial statements can be utilized for public consumption as well. It is generally

presented in the format of Profit and Loss Account, Statement of Stockholder’s equity Cash

Flow Statement and Statement of financial position. It plays a substantial role in analysing the

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance of operations of the company over a specific period of time. The main objective

behind disclosure of financial information is that it helps in giving information regarding

valuation of company that can help investors to decide that whether they want to invest in a

particular company or not (Brewer, 2013). Hence, it can be stated that financial accounting

helps in taking various investment decisions. Financial statements are then circulated to all the

stakeholders so that they can be made aware regarding performance of company for a

particular period.

Financial accounting is not only beneficial for outsiders to make investment decisions,

but it also plays a substantial role for insiders, that is management, so as to take decisions for

company. It helps in evaluating entity’s financial performance which are important to not to be

underestimated that can lead the management to make wrong decisions and thereby, leading

organization to generate losses.

Various Regulations related to financial accounting

There are various rules and regulations that are required to be followed by the

organization as it helps in providing legal framework to overall accounting operations. UK has

its own government regulations called as Financial Reporting Council (FRC). It helps in

disclosing various methods of financial reporting that are required to be followed by the

organization for its effective operations and thereby, presenting true and fair view of financial

stakeholders to shareholders. Some other regulations that have been accepted as universal

framework are mentioned as under:

International Financial Reporting Standards (IFRS): Standards that are being included

in IFRS helps in providing global language for the business so that companies can follow

similar method of financial reporting that is understandable and even comparable in

international boundaries. It helps in initiating proper disclosure of facts and figures which

can help in attracting a large number of investors towards it, based on its overall financial

condition. It helps in initiating proper treatment of cost, expenses and other operational

activities of the business (Dutta and Patatoukas, 2016).

International Accounting Standards (IAS): There is specific International Accounting

Standards Board that is responsible to guide regarding various aspects of financial

reporting. It helps in preparing an assessment that how particular types of transactions

must be reported in financial statements. Main aim of IASB is to bring transparency,

2

behind disclosure of financial information is that it helps in giving information regarding

valuation of company that can help investors to decide that whether they want to invest in a

particular company or not (Brewer, 2013). Hence, it can be stated that financial accounting

helps in taking various investment decisions. Financial statements are then circulated to all the

stakeholders so that they can be made aware regarding performance of company for a

particular period.

Financial accounting is not only beneficial for outsiders to make investment decisions,

but it also plays a substantial role for insiders, that is management, so as to take decisions for

company. It helps in evaluating entity’s financial performance which are important to not to be

underestimated that can lead the management to make wrong decisions and thereby, leading

organization to generate losses.

Various Regulations related to financial accounting

There are various rules and regulations that are required to be followed by the

organization as it helps in providing legal framework to overall accounting operations. UK has

its own government regulations called as Financial Reporting Council (FRC). It helps in

disclosing various methods of financial reporting that are required to be followed by the

organization for its effective operations and thereby, presenting true and fair view of financial

stakeholders to shareholders. Some other regulations that have been accepted as universal

framework are mentioned as under:

International Financial Reporting Standards (IFRS): Standards that are being included

in IFRS helps in providing global language for the business so that companies can follow

similar method of financial reporting that is understandable and even comparable in

international boundaries. It helps in initiating proper disclosure of facts and figures which

can help in attracting a large number of investors towards it, based on its overall financial

condition. It helps in initiating proper treatment of cost, expenses and other operational

activities of the business (Dutta and Patatoukas, 2016).

International Accounting Standards (IAS): There is specific International Accounting

Standards Board that is responsible to guide regarding various aspects of financial

reporting. It helps in preparing an assessment that how particular types of transactions

must be reported in financial statements. Main aim of IASB is to bring transparency,

2

efficiency and accountability in the worldwide financial reporting. Decisions that are taken

after considering financial statements, that have been prepared by IASC, are comparatively

more effective then through any other standards. It helps in bringing overall long term

financial stability to the organization (Pratt, 2016). Implementing the same as governance

process also proves to be quite effective for decision making aspects of organization.

Various accounting rules and principles

There are various accounting rules and principles which are mandatory to be followed

by the organization for its long-term success. Some of the Generally Accepted Accounting

Principles (GAAP) are mentioned as below:

Going Concern principle: It is required to be assumed by any type of organization that it

will exist forever. All the aims, objectives and commitment decided by the entity must

ensure that it is not going to be liquidated in near future and will go on forever. Hence, all

actions and steps taken by company will ensure that it will be able to gain adequate

amount of growth and all facts as well as figures that are being disclosed in financial

statements will be able to serve requirements business in near future. Full Disclosure principle: It is the duty of management of any organization to ensure that

all the important information, that can alter the decisions of stakeholders, has been

presented to them (Zeff, 2016). It must be initiated in such a manner that full disclosure

about the company has been initiated. It is due to this reason, the information that has not

been disclosed in the statements is then shared in form of footnotes, endnotes and working

notes. It is important for the management to disclose methods used and assumptions made

with respect to financial statements of the company. Materiality: It is a substantial principle of accounting which helps in ensuring that all the

material information must be disclosed to the stakeholders in such a manner that effective

decisions regarding investments can be made by them. It also helps in disclosing

authenticated sources. It also helps in disclosing the perspectives that is relevant material

facts to the ultimate stakeholders (Wong and Joshi, 2015). Matching Principle: Matching concept of accounting practice is related to recognizing

revenues and other related expenses of the organization within specific accounting period.

It helps in preparation of report revenues which helps in jotting down the expenses which

has been incurred by the firm in specific period. The main aim of this matching concept is

3

after considering financial statements, that have been prepared by IASC, are comparatively

more effective then through any other standards. It helps in bringing overall long term

financial stability to the organization (Pratt, 2016). Implementing the same as governance

process also proves to be quite effective for decision making aspects of organization.

Various accounting rules and principles

There are various accounting rules and principles which are mandatory to be followed

by the organization for its long-term success. Some of the Generally Accepted Accounting

Principles (GAAP) are mentioned as below:

Going Concern principle: It is required to be assumed by any type of organization that it

will exist forever. All the aims, objectives and commitment decided by the entity must

ensure that it is not going to be liquidated in near future and will go on forever. Hence, all

actions and steps taken by company will ensure that it will be able to gain adequate

amount of growth and all facts as well as figures that are being disclosed in financial

statements will be able to serve requirements business in near future. Full Disclosure principle: It is the duty of management of any organization to ensure that

all the important information, that can alter the decisions of stakeholders, has been

presented to them (Zeff, 2016). It must be initiated in such a manner that full disclosure

about the company has been initiated. It is due to this reason, the information that has not

been disclosed in the statements is then shared in form of footnotes, endnotes and working

notes. It is important for the management to disclose methods used and assumptions made

with respect to financial statements of the company. Materiality: It is a substantial principle of accounting which helps in ensuring that all the

material information must be disclosed to the stakeholders in such a manner that effective

decisions regarding investments can be made by them. It also helps in disclosing

authenticated sources. It also helps in disclosing the perspectives that is relevant material

facts to the ultimate stakeholders (Wong and Joshi, 2015). Matching Principle: Matching concept of accounting practice is related to recognizing

revenues and other related expenses of the organization within specific accounting period.

It helps in preparation of report revenues which helps in jotting down the expenses which

has been incurred by the firm in specific period. The main aim of this matching concept is

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to avoid any type of misstating mistakes with respect to earning which there by can affect

overall results as well. Economic identity assumption: It is one of the substantial assumption that can be noticed

in the principles issued in GAAP. Almost every organization tend to carry certain

economic identity. These economic entities can be in the form of companies, hospitals,

federal agencies and municipalities. It also helps in informing regarding decisions of the

organization. Moreover, it must also be ensuring that each organization is separate from

one another and hence accounting purposes of the same may also have substantial

difference in it. Monetary Unit Assumption: These are certain business transactions which have direct

relationship to the business. However, it is important that all the transactions that have

been initiated are in valid currency format. For instance, conducting transactions in dollar,

which is accepted worldwide and have a stable exchange rate can help in representing the

transactions in monetary unit (Huang and Vlady, 2012).

Concepts related to consistency and material disclosures

There are various concepts and conventions that are related to financial accounting. Out of all,

the most important accounting concepts are, consistency and material disclosure. The concepts

can be understood in the following manner:

Material disclosure: It is mandatory for the management to disclose all the financial accounts

related information in its financial statement so that it helps in presenting true and fair view of

the organization. All the operations that are directly or indirectly related to business can help

in finding out profits for the organization which is trusted enough for decision making aspects.

It helps in keeping and presenting the records of profits and loss in a well-defined manner.

Consistency: There are various consistent related trade practices that are required to be

followed by the organization. It is important that all the methods that are taken into

consideration while calculating profits must be consistent and no changes in the methods must

be brought without communicating the same to people (Guthrie and Pang, 2013). It also helps

in making calculations of profits specific enough.

4

overall results as well. Economic identity assumption: It is one of the substantial assumption that can be noticed

in the principles issued in GAAP. Almost every organization tend to carry certain

economic identity. These economic entities can be in the form of companies, hospitals,

federal agencies and municipalities. It also helps in informing regarding decisions of the

organization. Moreover, it must also be ensuring that each organization is separate from

one another and hence accounting purposes of the same may also have substantial

difference in it. Monetary Unit Assumption: These are certain business transactions which have direct

relationship to the business. However, it is important that all the transactions that have

been initiated are in valid currency format. For instance, conducting transactions in dollar,

which is accepted worldwide and have a stable exchange rate can help in representing the

transactions in monetary unit (Huang and Vlady, 2012).

Concepts related to consistency and material disclosures

There are various concepts and conventions that are related to financial accounting. Out of all,

the most important accounting concepts are, consistency and material disclosure. The concepts

can be understood in the following manner:

Material disclosure: It is mandatory for the management to disclose all the financial accounts

related information in its financial statement so that it helps in presenting true and fair view of

the organization. All the operations that are directly or indirectly related to business can help

in finding out profits for the organization which is trusted enough for decision making aspects.

It helps in keeping and presenting the records of profits and loss in a well-defined manner.

Consistency: There are various consistent related trade practices that are required to be

followed by the organization. It is important that all the methods that are taken into

consideration while calculating profits must be consistent and no changes in the methods must

be brought without communicating the same to people (Guthrie and Pang, 2013). It also helps

in making calculations of profits specific enough.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CLIENT 1

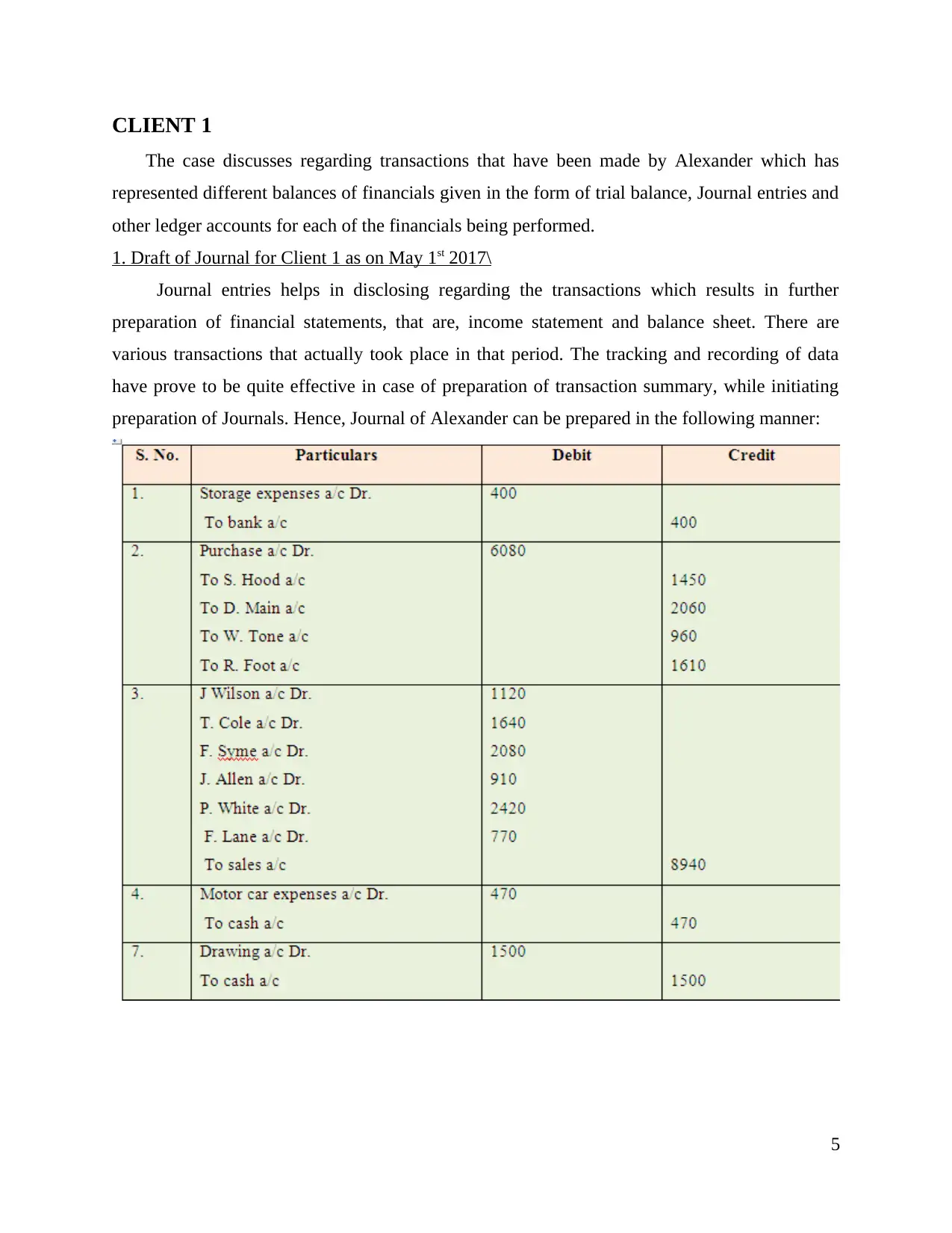

The case discusses regarding transactions that have been made by Alexander which has

represented different balances of financials given in the form of trial balance, Journal entries and

other ledger accounts for each of the financials being performed.

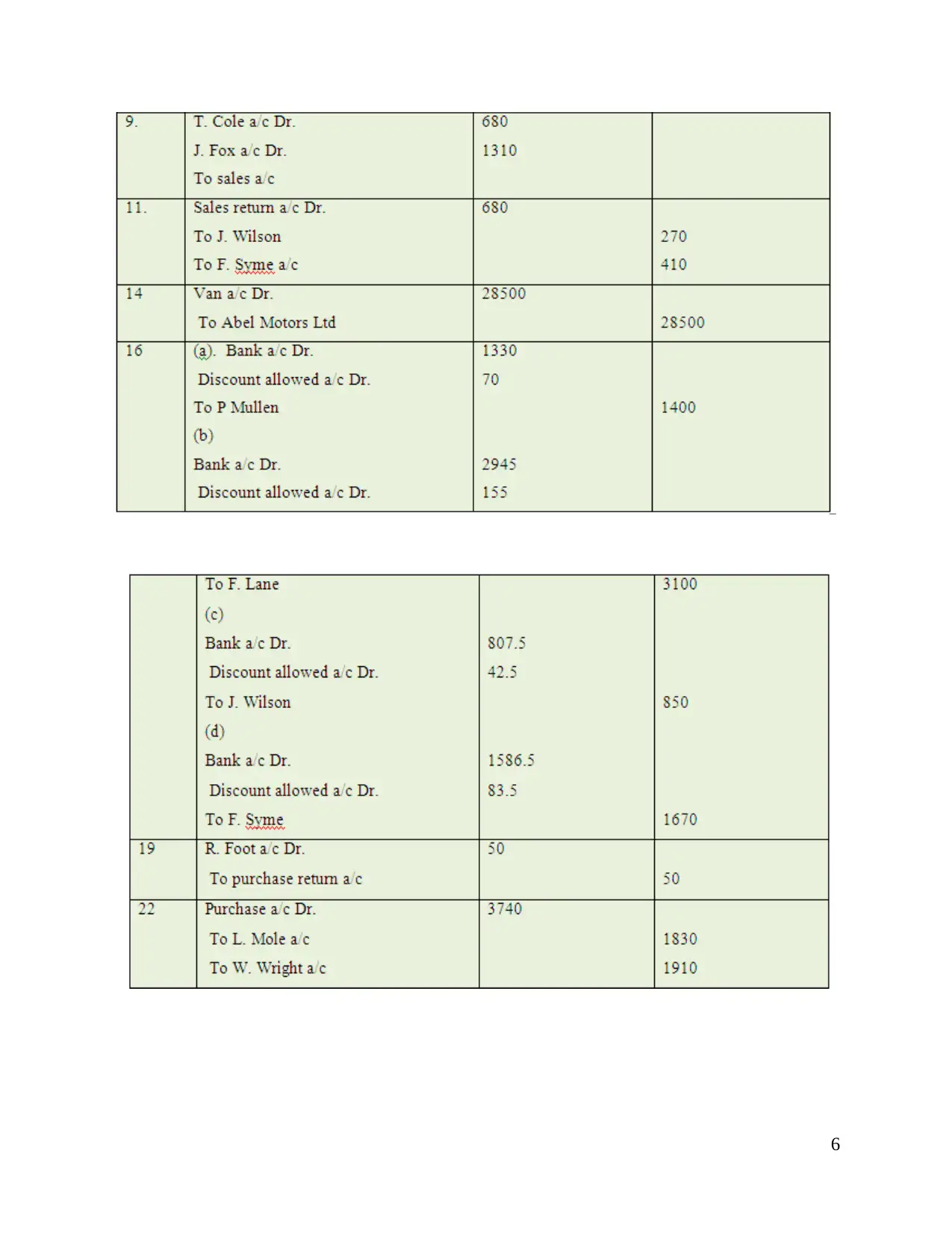

1. Draft of Journal for Client 1 as on May 1st 2017\

Journal entries helps in disclosing regarding the transactions which results in further

preparation of financial statements, that are, income statement and balance sheet. There are

various transactions that actually took place in that period. The tracking and recording of data

have prove to be quite effective in case of preparation of transaction summary, while initiating

preparation of Journals. Hence, Journal of Alexander can be prepared in the following manner:

5

The case discusses regarding transactions that have been made by Alexander which has

represented different balances of financials given in the form of trial balance, Journal entries and

other ledger accounts for each of the financials being performed.

1. Draft of Journal for Client 1 as on May 1st 2017\

Journal entries helps in disclosing regarding the transactions which results in further

preparation of financial statements, that are, income statement and balance sheet. There are

various transactions that actually took place in that period. The tracking and recording of data

have prove to be quite effective in case of preparation of transaction summary, while initiating

preparation of Journals. Hence, Journal of Alexander can be prepared in the following manner:

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

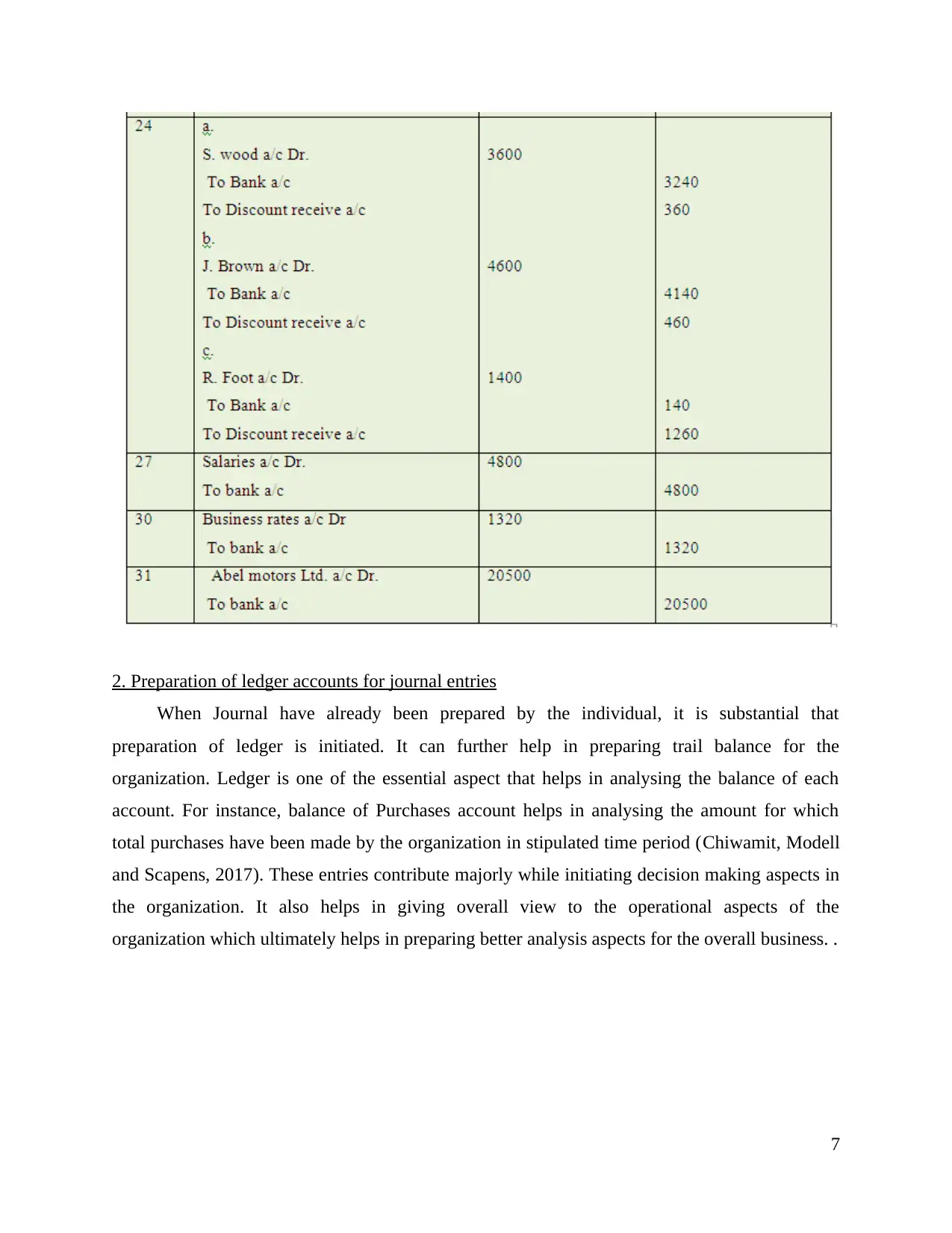

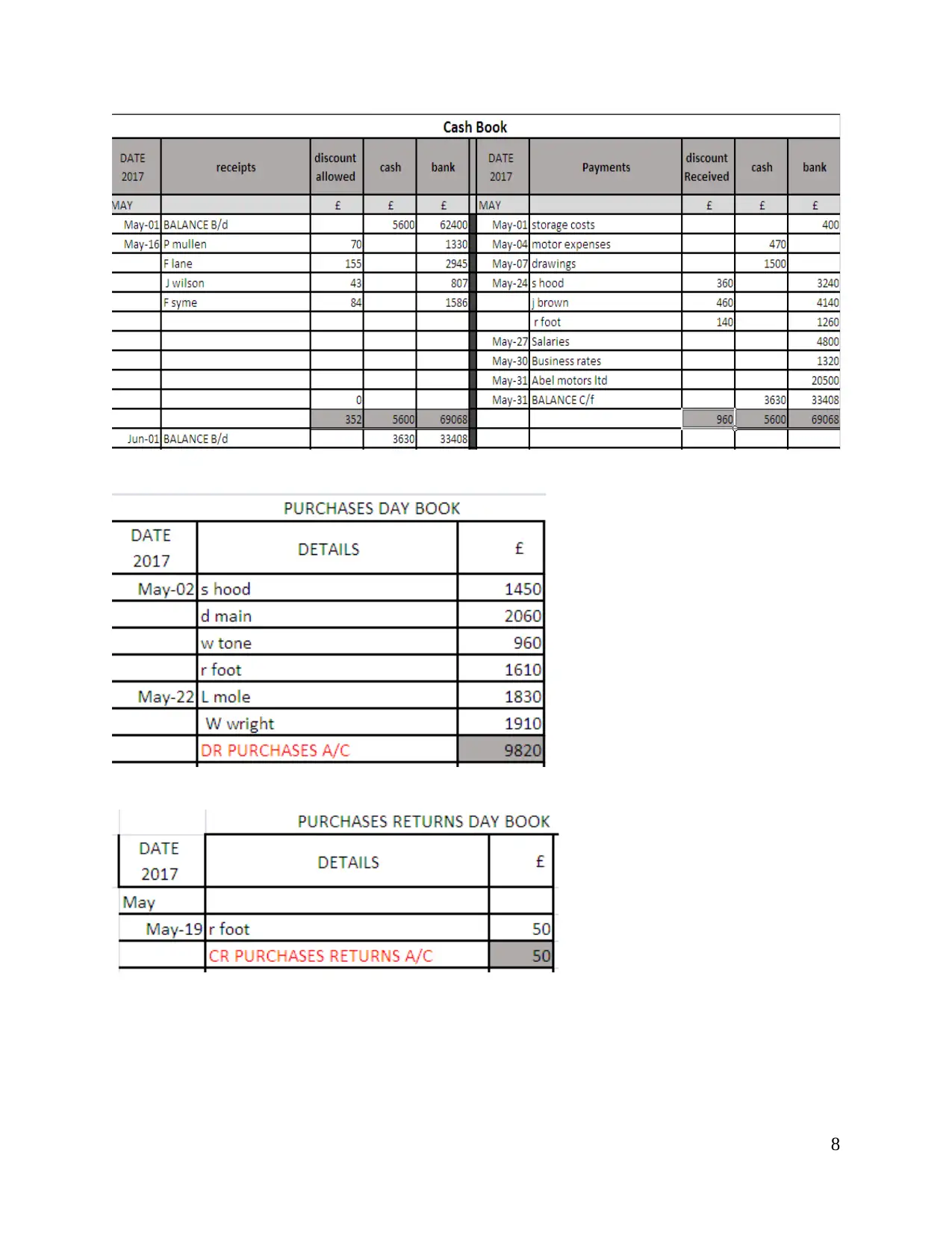

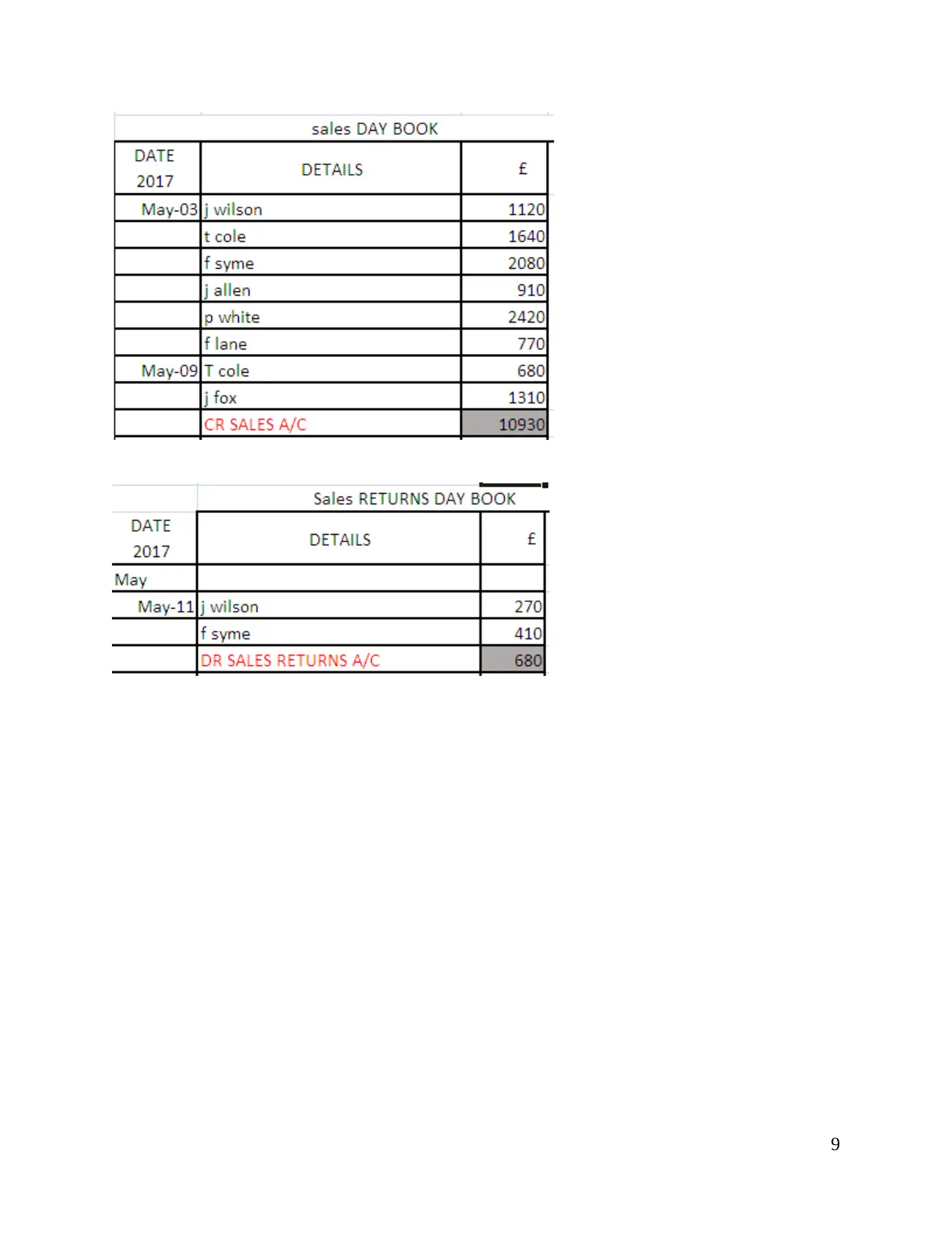

2. Preparation of ledger accounts for journal entries

When Journal have already been prepared by the individual, it is substantial that

preparation of ledger is initiated. It can further help in preparing trail balance for the

organization. Ledger is one of the essential aspect that helps in analysing the balance of each

account. For instance, balance of Purchases account helps in analysing the amount for which

total purchases have been made by the organization in stipulated time period (Chiwamit, Modell

and Scapens, 2017). These entries contribute majorly while initiating decision making aspects in

the organization. It also helps in giving overall view to the operational aspects of the

organization which ultimately helps in preparing better analysis aspects for the overall business. .

7

When Journal have already been prepared by the individual, it is substantial that

preparation of ledger is initiated. It can further help in preparing trail balance for the

organization. Ledger is one of the essential aspect that helps in analysing the balance of each

account. For instance, balance of Purchases account helps in analysing the amount for which

total purchases have been made by the organization in stipulated time period (Chiwamit, Modell

and Scapens, 2017). These entries contribute majorly while initiating decision making aspects in

the organization. It also helps in giving overall view to the operational aspects of the

organization which ultimately helps in preparing better analysis aspects for the overall business. .

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.