Accounting and Financial Reporting Standards

VerifiedAdded on 2020/10/22

|47

|5713

|177

AI Summary

This document provides a collection of studies and research papers related to accounting and financial reporting standards. It includes articles from various journals such as Journal of Accounting Research, Accounting, Organizations and Society, Critical Perspectives On Accounting, and more. The documents cover topics like market pricing of banks' fair value assets, internal information quality, and management accounting. This resource is useful for students and researchers looking for past papers and solved assignments on accounting and financial reporting standards.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. Produce a report to Line Manager for discussing accounting regulations........................1

Material disclosure and consistency concepts........................................................................4

CLIENT 1........................................................................................................................................5

A. Journal entries for the sole trader......................................................................................5

B. Producing ledger accounts for business...........................................................................10

C. Preparing trial balance for firm........................................................................................18

M1. Compiling trial balance by taking purchase and sale transactions...............................19

M2. Trial balance by considering accounting rules and regulations....................................20

CLIENT 2......................................................................................................................................20

A. Income statement for the sole trader................................................................................20

B. Balance sheet for firm......................................................................................................21

CLIENT 3......................................................................................................................................22

A. Profit and Loss account for organisation.........................................................................22

B. Balance sheet for Raintree Ltd.........................................................................................23

..............................................................................................................................................25

..............................................................................................................................................26

..............................................................................................................................................27

..............................................................................................................................................28

..............................................................................................................................................28

C. Outlining principles and concepts of accounting.............................................................28

D. Importance of measuring and presenting depreciation in financials...............................29

M2. Assessing P&L, balance sheet and cash flow statements.............................................29

D2. Accurate calculations in accounting for producing financial statements......................29

CLIENT 4......................................................................................................................................30

A. Preparation of bank reconciliation statement..................................................................30

B. Causes of recording transaction in bank reconciliation statement...................................30

C. Producing cash books......................................................................................................30

..............................................................................................................................................31

INTRODUCTION...........................................................................................................................1

A. Produce a report to Line Manager for discussing accounting regulations........................1

Material disclosure and consistency concepts........................................................................4

CLIENT 1........................................................................................................................................5

A. Journal entries for the sole trader......................................................................................5

B. Producing ledger accounts for business...........................................................................10

C. Preparing trial balance for firm........................................................................................18

M1. Compiling trial balance by taking purchase and sale transactions...............................19

M2. Trial balance by considering accounting rules and regulations....................................20

CLIENT 2......................................................................................................................................20

A. Income statement for the sole trader................................................................................20

B. Balance sheet for firm......................................................................................................21

CLIENT 3......................................................................................................................................22

A. Profit and Loss account for organisation.........................................................................22

B. Balance sheet for Raintree Ltd.........................................................................................23

..............................................................................................................................................25

..............................................................................................................................................26

..............................................................................................................................................27

..............................................................................................................................................28

..............................................................................................................................................28

C. Outlining principles and concepts of accounting.............................................................28

D. Importance of measuring and presenting depreciation in financials...............................29

M2. Assessing P&L, balance sheet and cash flow statements.............................................29

D2. Accurate calculations in accounting for producing financial statements......................29

CLIENT 4......................................................................................................................................30

A. Preparation of bank reconciliation statement..................................................................30

B. Causes of recording transaction in bank reconciliation statement...................................30

C. Producing cash books......................................................................................................30

..............................................................................................................................................31

..............................................................................................................................................31

M3. Reconciliation process and related accounting terms...................................................31

D3. Producing bank reconciliation statement.......................................................................32

CLIENT 5......................................................................................................................................32

A. Producing sales and purchase ledger account for the company......................................32

B. Explaining control account..............................................................................................33

CLIENT 6......................................................................................................................................33

A. Discussing suspense account and main features of suspense account.............................33

B. Preparation of trial balance..............................................................................................33

C. Producing journal entries.................................................................................................34

D. Distinguishing clearing and suspense account................................................................35

M4. Exploring types of accounts..........................................................................................35

D4. Providing accounting methods for organisation............................................................35

CONCLUSION..............................................................................................................................36

REFERENCES..............................................................................................................................37

M3. Reconciliation process and related accounting terms...................................................31

D3. Producing bank reconciliation statement.......................................................................32

CLIENT 5......................................................................................................................................32

A. Producing sales and purchase ledger account for the company......................................32

B. Explaining control account..............................................................................................33

CLIENT 6......................................................................................................................................33

A. Discussing suspense account and main features of suspense account.............................33

B. Preparation of trial balance..............................................................................................33

C. Producing journal entries.................................................................................................34

D. Distinguishing clearing and suspense account................................................................35

M4. Exploring types of accounts..........................................................................................35

D4. Providing accounting methods for organisation............................................................35

CONCLUSION..............................................................................................................................36

REFERENCES..............................................................................................................................37

INTRODUCTION

Financial accounting is crucial branch of accounting which is required for preparation of

financial statements in effective way. Present report deals with importance of accounting in the

business in order to record various transactions that occurs on day-to-day basis. The solutions for

various clients are provided by seeking information given and as a result, financials are prepared.

In accordance to this, journal entries are made, then entries are posted to general ledger accounts

in effective manner. From this, trial balance is formulated to check on errors if any that might

creep in posting entries into ledger. Finally, balance sheet and income statements are drawn.

Apart from this, bank reconciliation statement is prepared to rectify balances of bank and that

with records maintained by firm. Suspense account and control account is explained.

Furthermore, accounting regulations, principles and concepts are discussed which are provided

by various professional bodies. Thus, it can be said that accounting plays crucial role in the

business as it provides clarity regarding the transaction occurred in and classified into their

respective nature of accounts.

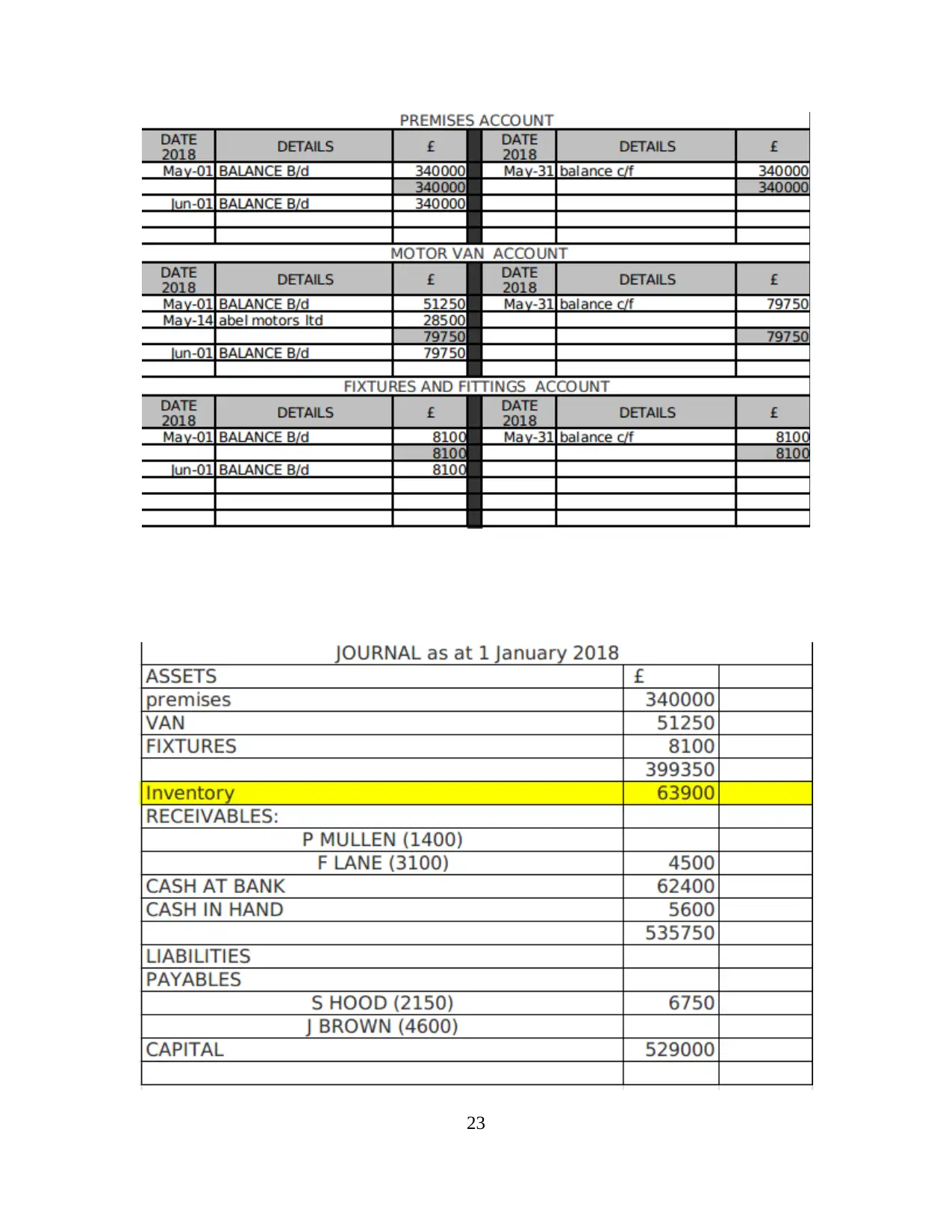

A. Produce a report to Line Manager for discussing accounting regulations

To: Line Manager

From: Junior Accountant

Subject: Accounting terms, regulations to be taken into account by organisation

Respected Sir,

Accounting is one of the important functions in the business so that day-to-day

transactions may be effectively recorded (Damodaran, 2016). It is essentially required because

without taking into account various transactions into account, financial statements cannot be

prepared in effectual manner. In carrying out this task, accounting principles and regulations

play a crucial role in preparing financials in the best possible manner. The financials such as

cash flow statement, balance sheet, income statement are important pillars of accounting which

is used to carry out proper financial health of the concern in effective way.

The balance sheet shows assets and liabilities of organisation for a particular period

usually one year. On the other side, cash flow statement effectively shows cash position

whether surplus or deficit exists. While, Profit and Loss account clarifies expenditures incurred

1

Financial accounting is crucial branch of accounting which is required for preparation of

financial statements in effective way. Present report deals with importance of accounting in the

business in order to record various transactions that occurs on day-to-day basis. The solutions for

various clients are provided by seeking information given and as a result, financials are prepared.

In accordance to this, journal entries are made, then entries are posted to general ledger accounts

in effective manner. From this, trial balance is formulated to check on errors if any that might

creep in posting entries into ledger. Finally, balance sheet and income statements are drawn.

Apart from this, bank reconciliation statement is prepared to rectify balances of bank and that

with records maintained by firm. Suspense account and control account is explained.

Furthermore, accounting regulations, principles and concepts are discussed which are provided

by various professional bodies. Thus, it can be said that accounting plays crucial role in the

business as it provides clarity regarding the transaction occurred in and classified into their

respective nature of accounts.

A. Produce a report to Line Manager for discussing accounting regulations

To: Line Manager

From: Junior Accountant

Subject: Accounting terms, regulations to be taken into account by organisation

Respected Sir,

Accounting is one of the important functions in the business so that day-to-day

transactions may be effectively recorded (Damodaran, 2016). It is essentially required because

without taking into account various transactions into account, financial statements cannot be

prepared in effectual manner. In carrying out this task, accounting principles and regulations

play a crucial role in preparing financials in the best possible manner. The financials such as

cash flow statement, balance sheet, income statement are important pillars of accounting which

is used to carry out proper financial health of the concern in effective way.

The balance sheet shows assets and liabilities of organisation for a particular period

usually one year. On the other side, cash flow statement effectively shows cash position

whether surplus or deficit exists. While, Profit and Loss account clarifies expenditures incurred

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

and income earned in particular financial year. Hence, all these statements are prepared by

relying on proper accounting practices by accountant so that clear position can be highlighted

regarding health in effective manner.

Accounting principles and regulations governed by the accounting professional bodies

are important because financials cannot be formulated in effective way without abiding by rules

and principles of accounting (Nash, 2018). This helps to effectively prepare proper financials

which highlights true and fair view of financials in the best possible manner. On the other hand,

if regulations are not properly followed, then organisation is not able to produce financials in

effective way. This affects fairness of accounts and as such, it is required that such regulations

and principles should be followed for producing financials with ease. The accounting

information derived through financials is quite useful for the organisation as it imparts to the

external users of financial information for taking enhanced decisions. Creditors' are benefited as

they seek financials and attain clarity about the solvency position of company. On the other

side, investors' are benefited as they analyse profitability aspect of organisation. Moreover,

other users also seek such information and then take decisions. Hence, accounting regulations

are important part in carrying out accounting as firm is benefited by following various requisites

and thus, authentic financials are formulated in effective way.

Financial Accounting

Financial Accounting is useful as past data is used to draw effective financials. In simple

words, monetary transactions which occur on daily basis are taken into account and thus,

financials are prepared with ease. It is required so that proper statements may be formulated and

it may impart necessary information to external users quite effectually (Busco and Quattrone,

2018). This is essentially required because external users rely on financials which serves them

the required information by which they are able to take enhanced decisions.

Apart from external parties, internal management is also benefited by seeking financial

statements because they make strategies and initiates improvement for strengthening internal

operations. It is required to strengthen organisation internally so that output may be produced

more and customers' satisfaction level is enhanced in a better way.

Creditors and investors are able to take better decisions and thus, financial accounting is

2

relying on proper accounting practices by accountant so that clear position can be highlighted

regarding health in effective manner.

Accounting principles and regulations governed by the accounting professional bodies

are important because financials cannot be formulated in effective way without abiding by rules

and principles of accounting (Nash, 2018). This helps to effectively prepare proper financials

which highlights true and fair view of financials in the best possible manner. On the other hand,

if regulations are not properly followed, then organisation is not able to produce financials in

effective way. This affects fairness of accounts and as such, it is required that such regulations

and principles should be followed for producing financials with ease. The accounting

information derived through financials is quite useful for the organisation as it imparts to the

external users of financial information for taking enhanced decisions. Creditors' are benefited as

they seek financials and attain clarity about the solvency position of company. On the other

side, investors' are benefited as they analyse profitability aspect of organisation. Moreover,

other users also seek such information and then take decisions. Hence, accounting regulations

are important part in carrying out accounting as firm is benefited by following various requisites

and thus, authentic financials are formulated in effective way.

Financial Accounting

Financial Accounting is useful as past data is used to draw effective financials. In simple

words, monetary transactions which occur on daily basis are taken into account and thus,

financials are prepared with ease. It is required so that proper statements may be formulated and

it may impart necessary information to external users quite effectually (Busco and Quattrone,

2018). This is essentially required because external users rely on financials which serves them

the required information by which they are able to take enhanced decisions.

Apart from external parties, internal management is also benefited by seeking financial

statements because they make strategies and initiates improvement for strengthening internal

operations. It is required to strengthen organisation internally so that output may be produced

more and customers' satisfaction level is enhanced in a better way.

Creditors and investors are able to take better decisions and thus, financial accounting is

2

the main element in producing authenticated financials of organisation highlighting health in

terms of financial performance. Moreover, profitability, efficiency, solvency and liquidity

aspects of firm are effectively attained which is possible by preparing financial statements by

information provided by such accounting. In relation to this, monetary transactions such

recording in books of prime entry and posting them into ledger and then constructing trial

balance are bases for effectively producing balance sheet, income and cash flow statements

(Constable and Kuasirikun, 2018). In addressing this, taxation authorities are benefited by

seeking financials as it serves them to effectively ascertain tax liability of organisation in the

best possible manner. Thus, it can be said that financial accounting gives clarity regarding

overall position of firm quite effectually.

Regulations of Financial Accounting

The financials are produced in order to gain useful insight with regards to overall

position of company in effective manner. In relation to this, for preparing adequate and

authenticated statements, it is required that accounting regulations must be properly followed by

the organisation so that reliability and transparency may not get diminished. This helps to

produce effective and better statements by relying on various accounting regulations imparted

by professional bodies entrusted to provide guidelines to accountants so that reliable financials

may be prepared in effective way.

In addressing this, financial statements may be manipulated by company which affects

reliability and as such, imparts wrong information to users. It adversely affects them as when

they rely on manipulated statements, decision-making is hampered badly. False information is

provided to them impacting on external parties up to a high extent (Heitzman and Huang,

2018). This should be alleviated in order to produce reliable financials and thus, financial

regulator of UK has given FRC guidelines which have to be effectively followed by

organisation and government also for preparing authenticated financials. The legal frameworks

are listed under-

FRC (Financial Reporting Council)- The body is entitled to foster development in the nation

and regulates organisations and government units as well. Hence, accounting practices are

adopted by accountants quite effectually.

3

terms of financial performance. Moreover, profitability, efficiency, solvency and liquidity

aspects of firm are effectively attained which is possible by preparing financial statements by

information provided by such accounting. In relation to this, monetary transactions such

recording in books of prime entry and posting them into ledger and then constructing trial

balance are bases for effectively producing balance sheet, income and cash flow statements

(Constable and Kuasirikun, 2018). In addressing this, taxation authorities are benefited by

seeking financials as it serves them to effectively ascertain tax liability of organisation in the

best possible manner. Thus, it can be said that financial accounting gives clarity regarding

overall position of firm quite effectually.

Regulations of Financial Accounting

The financials are produced in order to gain useful insight with regards to overall

position of company in effective manner. In relation to this, for preparing adequate and

authenticated statements, it is required that accounting regulations must be properly followed by

the organisation so that reliability and transparency may not get diminished. This helps to

produce effective and better statements by relying on various accounting regulations imparted

by professional bodies entrusted to provide guidelines to accountants so that reliable financials

may be prepared in effective way.

In addressing this, financial statements may be manipulated by company which affects

reliability and as such, imparts wrong information to users. It adversely affects them as when

they rely on manipulated statements, decision-making is hampered badly. False information is

provided to them impacting on external parties up to a high extent (Heitzman and Huang,

2018). This should be alleviated in order to produce reliable financials and thus, financial

regulator of UK has given FRC guidelines which have to be effectively followed by

organisation and government also for preparing authenticated financials. The legal frameworks

are listed under-

FRC (Financial Reporting Council)- The body is entitled to foster development in the nation

and regulates organisations and government units as well. Hence, accounting practices are

adopted by accountants quite effectually.

3

IASB (International Accounting Standards Board)- This body is entrusted to provide

guidelines to the company's accountant by which reliable and fair financials may be prepared.

This helps to effectively prepare statements and no false information is indulged in.

IFRS (International Financial Reporting Standards)- The accounting body also imparts

guidelines to the accountants in order to abide by legal framework so that adequate financials

may be formulated in the best possible manner.

Rules for accounting

GAAP (Generally Accepted Accounting Principles) which is another important body

has imparted guidelines for preparing financials in effective manner. The several principles and

rules are described below-

Economic assumption- This accounting rule postulates that organisation analyses economic

environment and as such, assumptions are made accordingly (Libby, 2017). In additional to

this, assumptions are made to estimate how economic environment will impact upon sales and

forthcoming project.

Principle of full disclosure- It states that firm should prepare financials by taking into account

all the monetary transactions. In simple words, to produce reliability, it is needed to compile

financials in single statements so that more transparency may be imparted in a better way.

Going concern principle- The accounting principle states that financial statements are produced

by taking into consideration this principle. It means that firm carries on business for long run

and will not shut down immediately. Observing this, financials are prepared.

Materiality principle- This principle postulates that only material information should be taken

into account which do not affect decision-making by external users. Hence, immaterial items

must be ignored. This is required so that material items are taken into account for producing

financials (Nitzl, 2018).

Monetary unit assumption- The principle is related to monetary value of currencies. The US

Dollar is universally applicable and accepted currency which can be used by organisation in

order to made business transactions in effective manner.

Material disclosure and consistency concepts

4

guidelines to the company's accountant by which reliable and fair financials may be prepared.

This helps to effectively prepare statements and no false information is indulged in.

IFRS (International Financial Reporting Standards)- The accounting body also imparts

guidelines to the accountants in order to abide by legal framework so that adequate financials

may be formulated in the best possible manner.

Rules for accounting

GAAP (Generally Accepted Accounting Principles) which is another important body

has imparted guidelines for preparing financials in effective manner. The several principles and

rules are described below-

Economic assumption- This accounting rule postulates that organisation analyses economic

environment and as such, assumptions are made accordingly (Libby, 2017). In additional to

this, assumptions are made to estimate how economic environment will impact upon sales and

forthcoming project.

Principle of full disclosure- It states that firm should prepare financials by taking into account

all the monetary transactions. In simple words, to produce reliability, it is needed to compile

financials in single statements so that more transparency may be imparted in a better way.

Going concern principle- The accounting principle states that financial statements are produced

by taking into consideration this principle. It means that firm carries on business for long run

and will not shut down immediately. Observing this, financials are prepared.

Materiality principle- This principle postulates that only material information should be taken

into account which do not affect decision-making by external users. Hence, immaterial items

must be ignored. This is required so that material items are taken into account for producing

financials (Nitzl, 2018).

Monetary unit assumption- The principle is related to monetary value of currencies. The US

Dollar is universally applicable and accepted currency which can be used by organisation in

order to made business transactions in effective manner.

Material disclosure and consistency concepts

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Concept of consistency- The accounting concept states that firm should take into account only

that accounting policies which it has used in previous year. In simple words, consistent methods

should be followed in order to produce reliability in the best possible manner. It can be said that

if consistent accounting methods are not taken into then transparency and reliability of

organisation is hampered. Hence, it is required to follow same policies. For instance, if straight

line method is followed by the organisation, then should be followed in forthcoming years in

order to produce reliable information.

Material disclosure- The concept states that material information should be taken into account

which affects financial statements up to a high extent. In other words, immaterial items or

information should be ignored which do not have impact on users of accounting information

and thus, reliability can be ascertained in a better way. The books of accounts should disclose

only material items which is effectively evaluated by external stakeholders and they are able to

take decisions in the best possible manner.

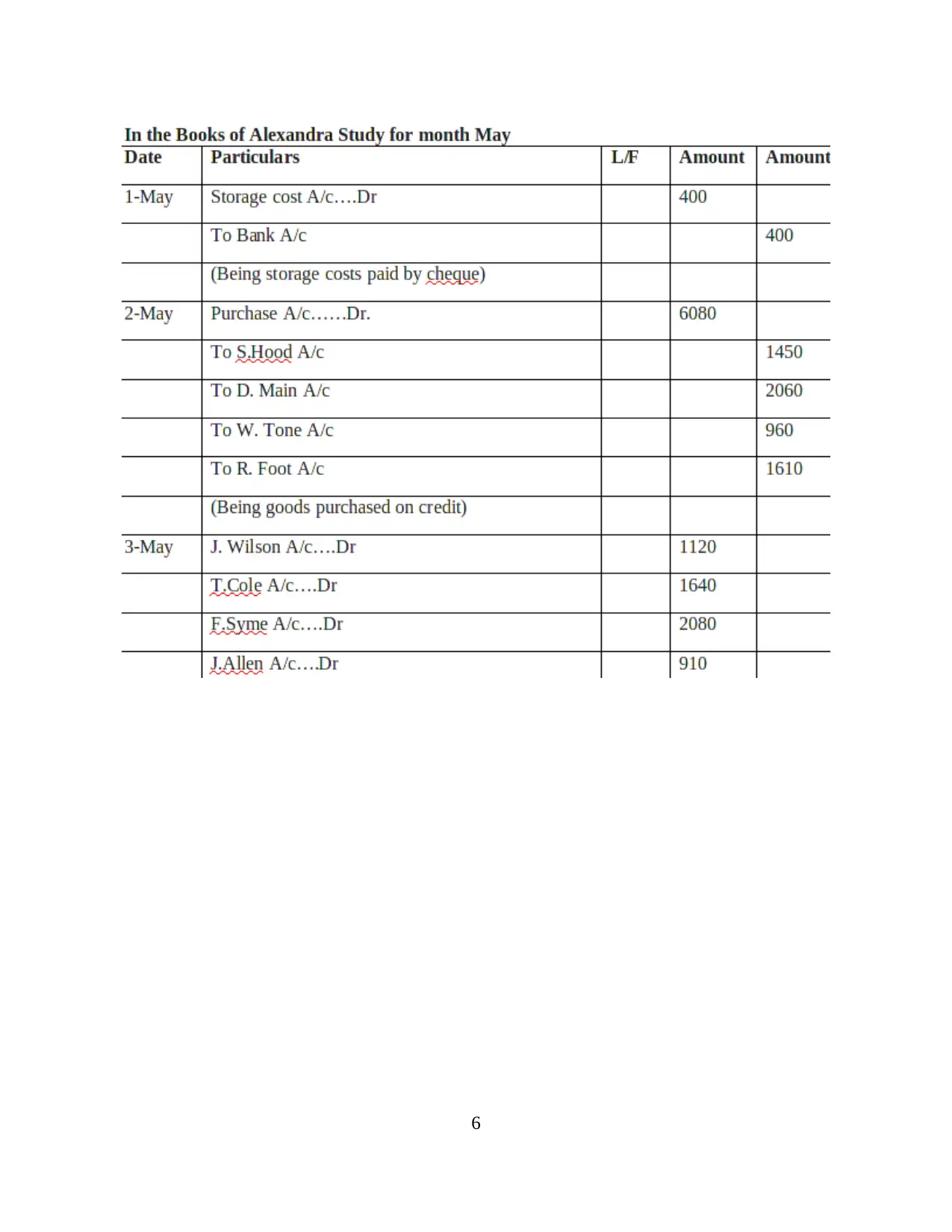

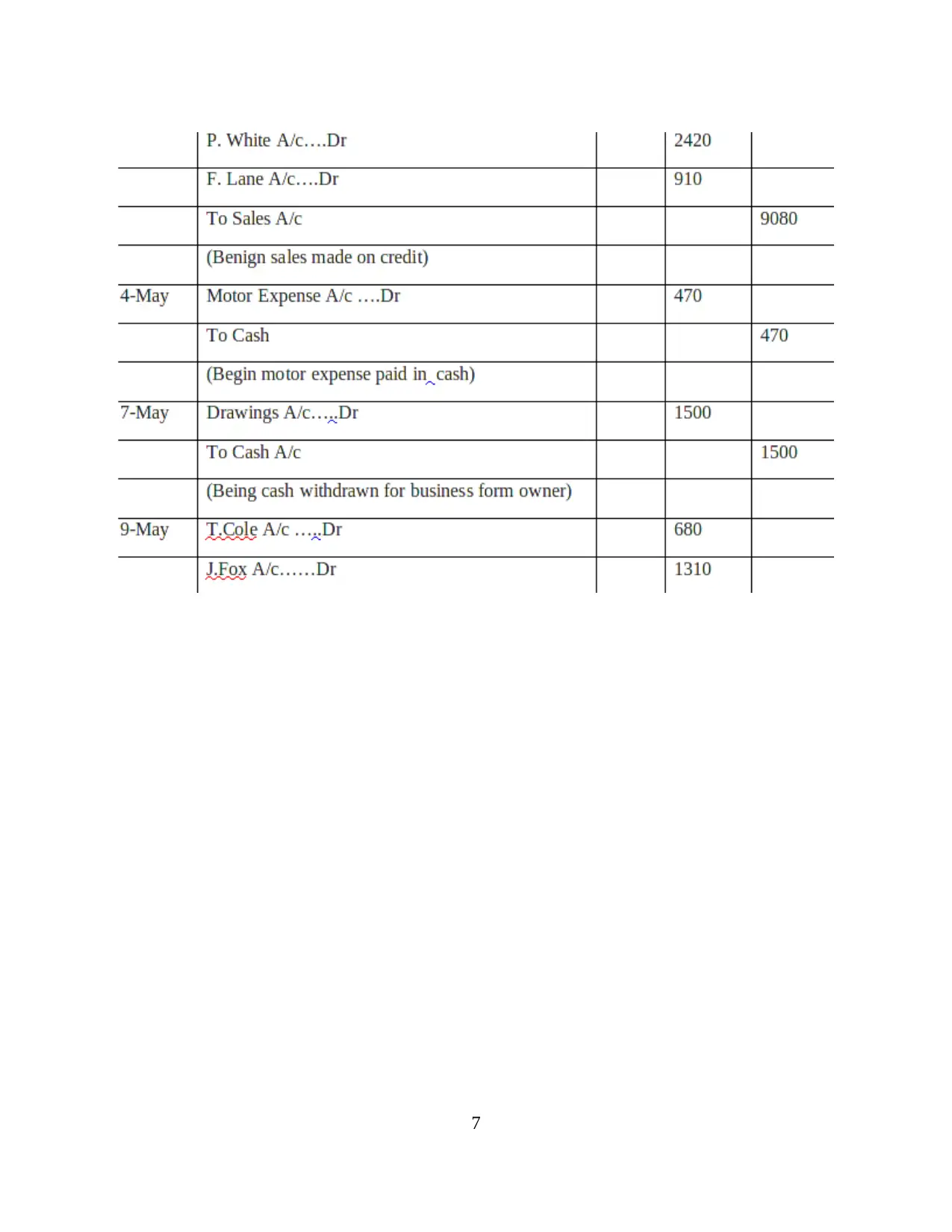

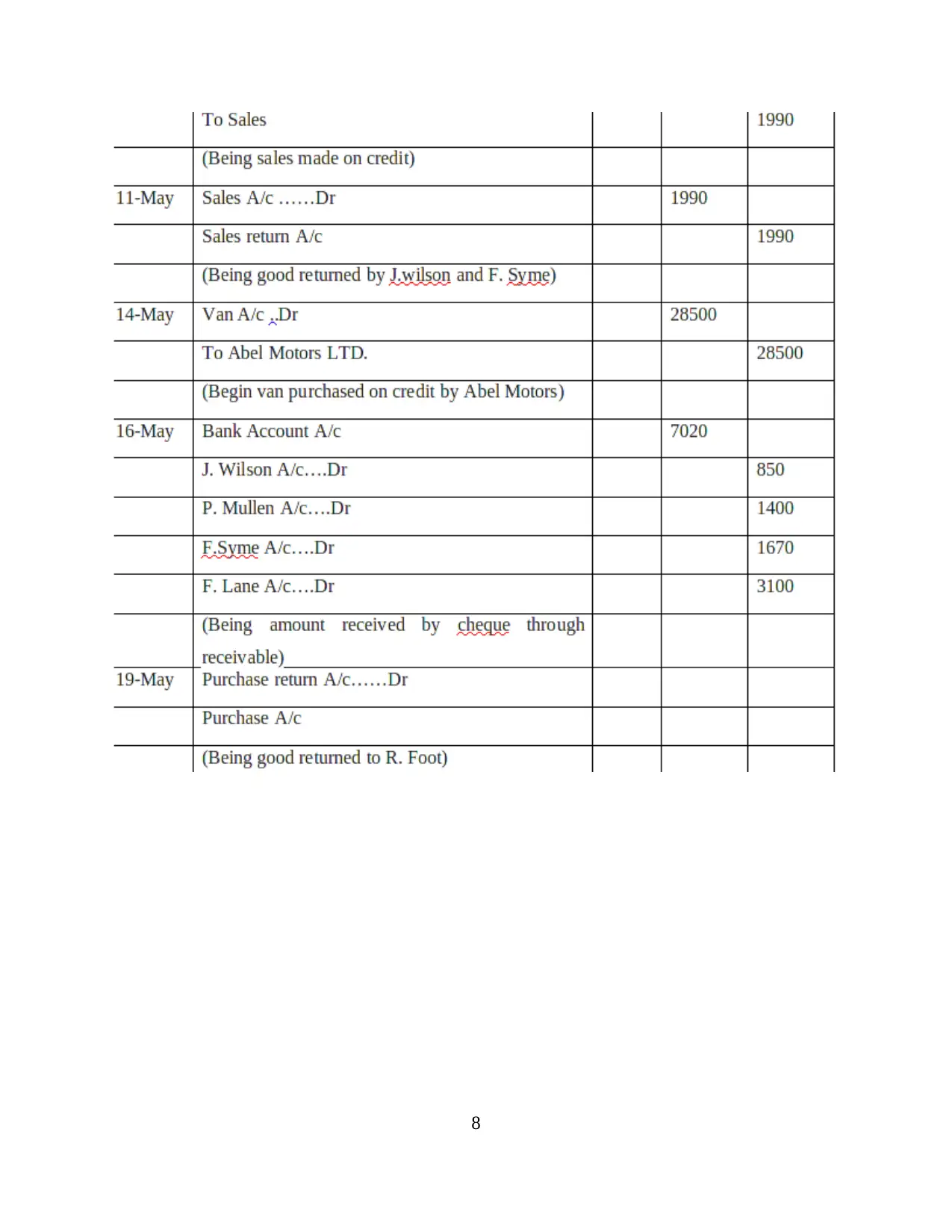

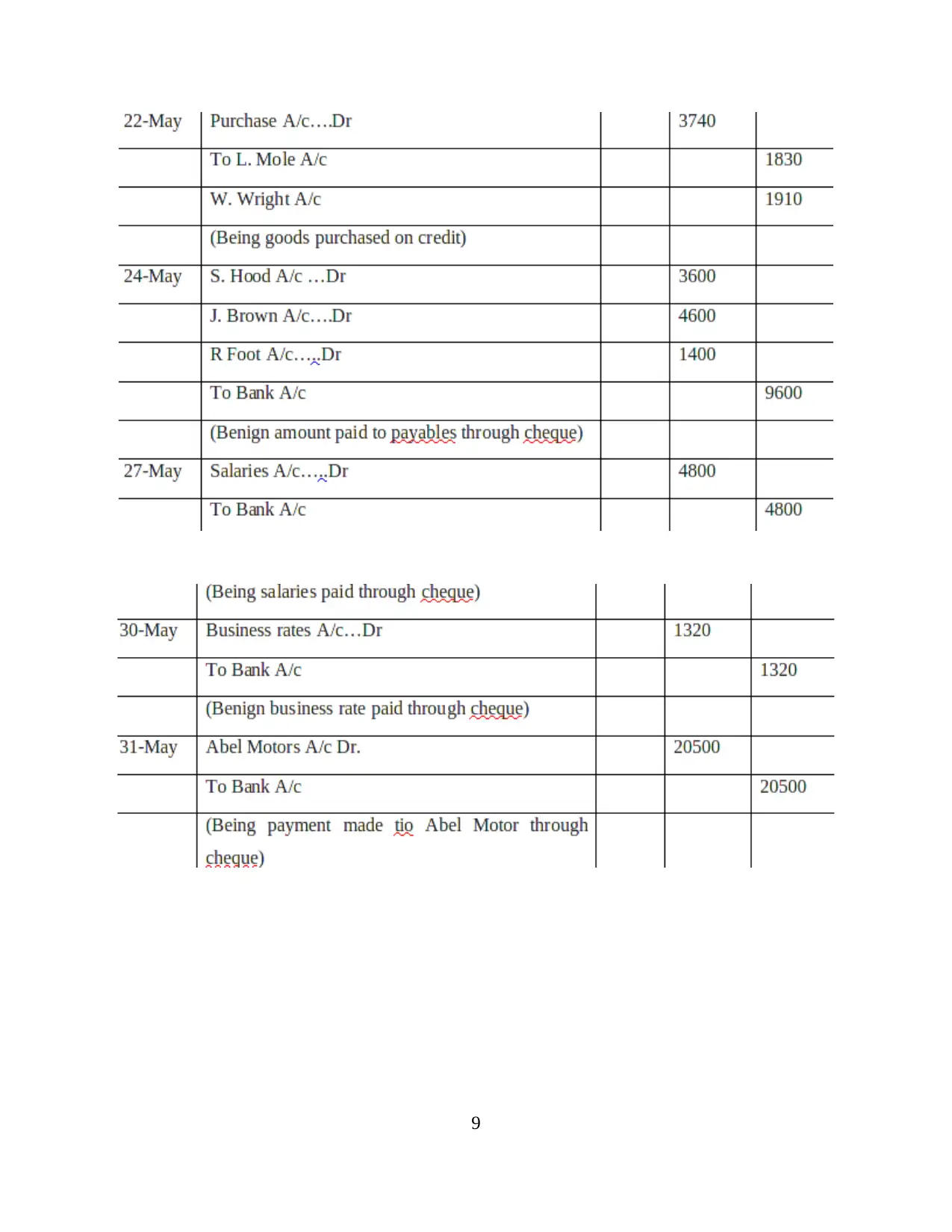

CLIENT 1

A. Journal entries for the sole trader

The transactions are to be recorded in a better way so that receipts and withdrawals may

be effectively ascertained (Schneider, 2018). For recording transactions, books of prime entry

also known as journal is made in the best possible manner. It can be said that for producing

financials, journal entries is the first step which is done by recording business transaction in

chronological order. This is made in chronological order so that every transaction occurred on a

particular date should be recorded on that date only for the purpose of reliability. Hence, entries

are posted in journal so that each and every transaction may be recorded and accounted for quite

effectually. The journal entries are produced for Alexandra firm below-

5

that accounting policies which it has used in previous year. In simple words, consistent methods

should be followed in order to produce reliability in the best possible manner. It can be said that

if consistent accounting methods are not taken into then transparency and reliability of

organisation is hampered. Hence, it is required to follow same policies. For instance, if straight

line method is followed by the organisation, then should be followed in forthcoming years in

order to produce reliable information.

Material disclosure- The concept states that material information should be taken into account

which affects financial statements up to a high extent. In other words, immaterial items or

information should be ignored which do not have impact on users of accounting information

and thus, reliability can be ascertained in a better way. The books of accounts should disclose

only material items which is effectively evaluated by external stakeholders and they are able to

take decisions in the best possible manner.

CLIENT 1

A. Journal entries for the sole trader

The transactions are to be recorded in a better way so that receipts and withdrawals may

be effectively ascertained (Schneider, 2018). For recording transactions, books of prime entry

also known as journal is made in the best possible manner. It can be said that for producing

financials, journal entries is the first step which is done by recording business transaction in

chronological order. This is made in chronological order so that every transaction occurred on a

particular date should be recorded on that date only for the purpose of reliability. Hence, entries

are posted in journal so that each and every transaction may be recorded and accounted for quite

effectually. The journal entries are produced for Alexandra firm below-

5

6

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

8

9

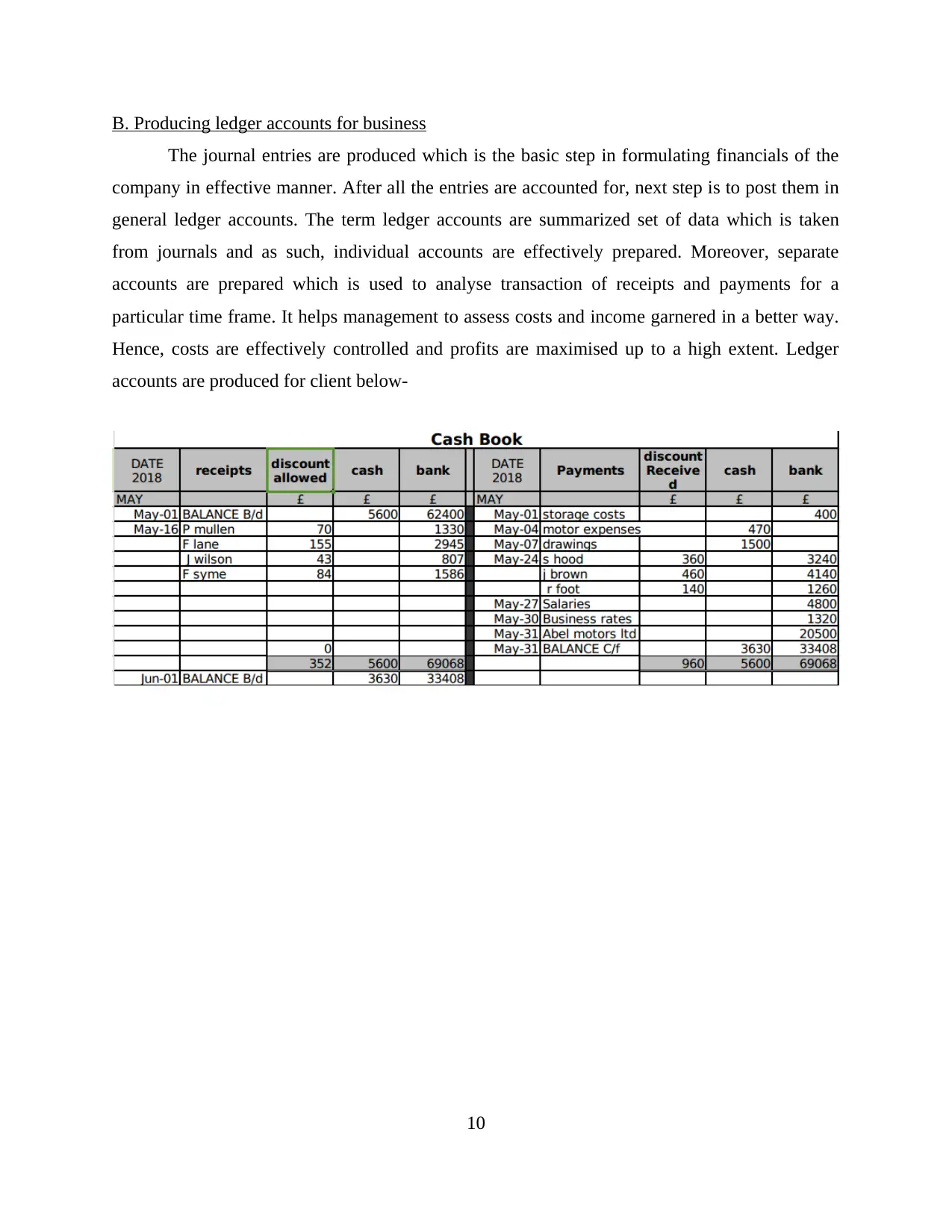

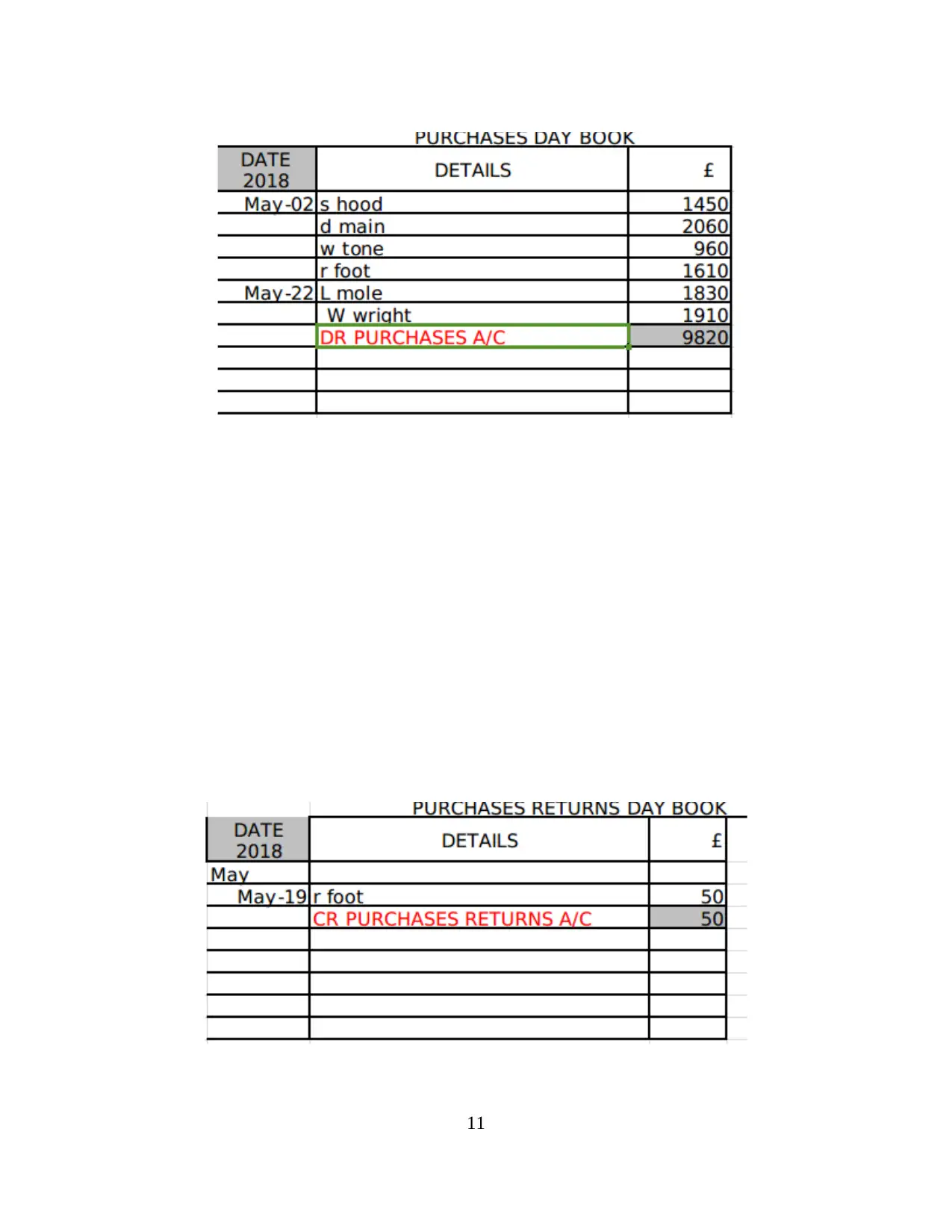

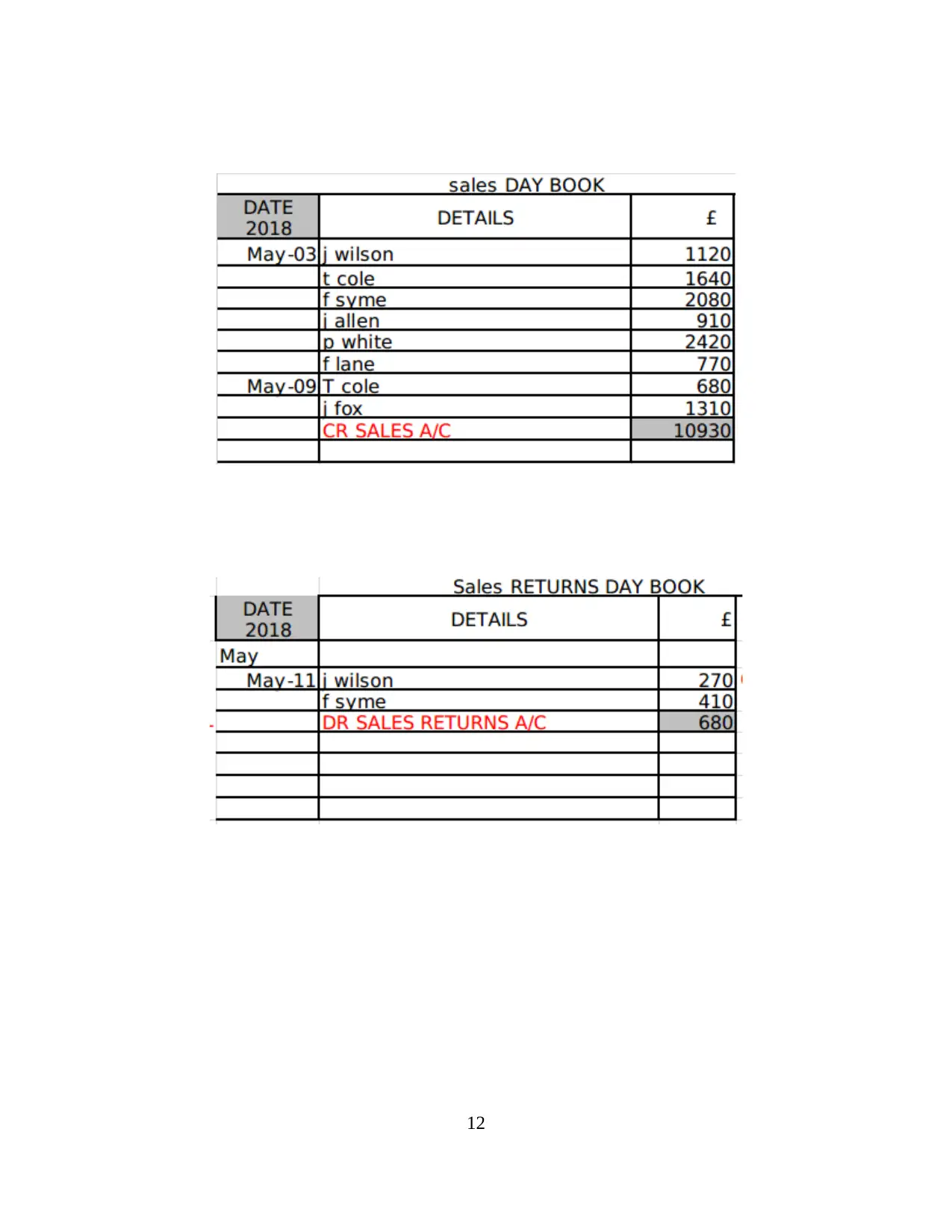

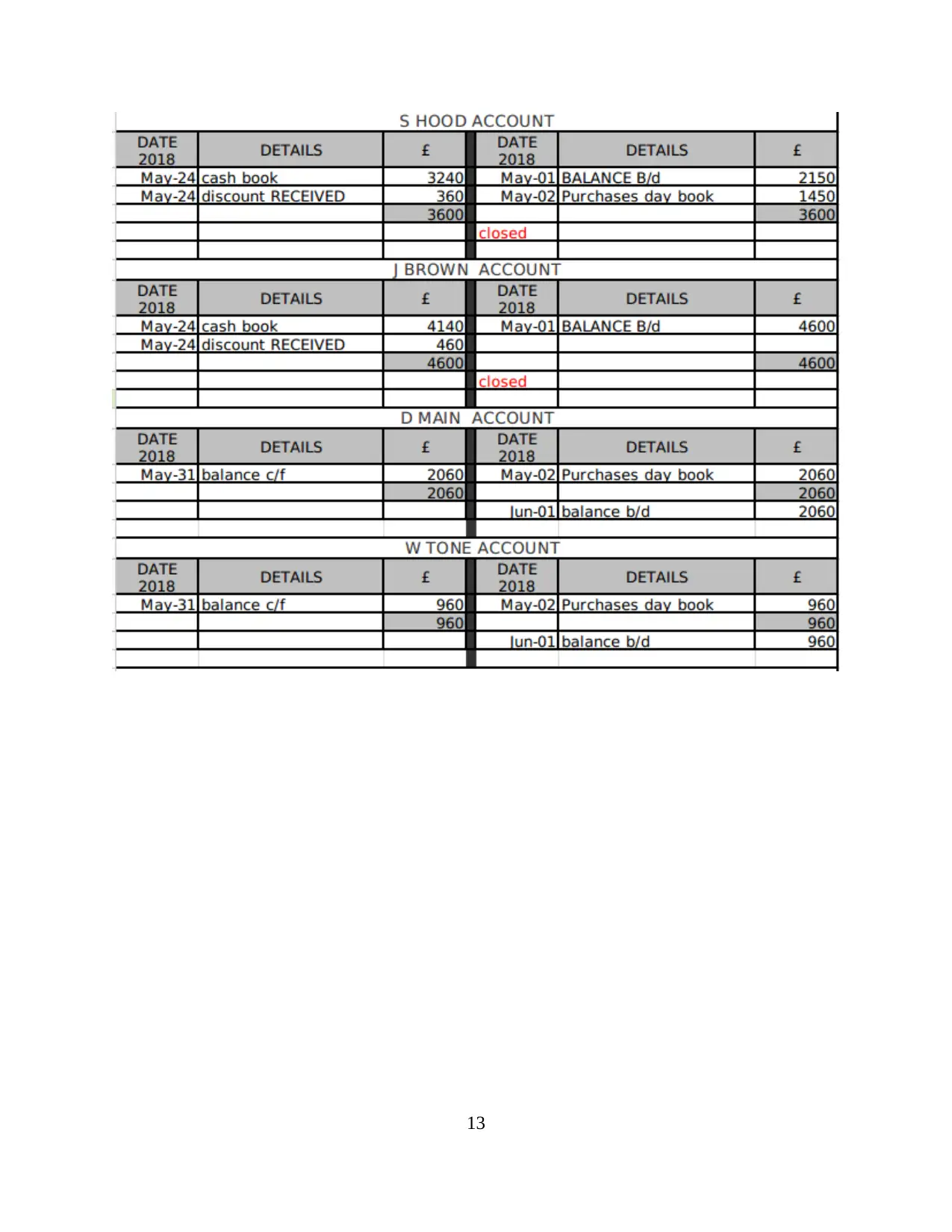

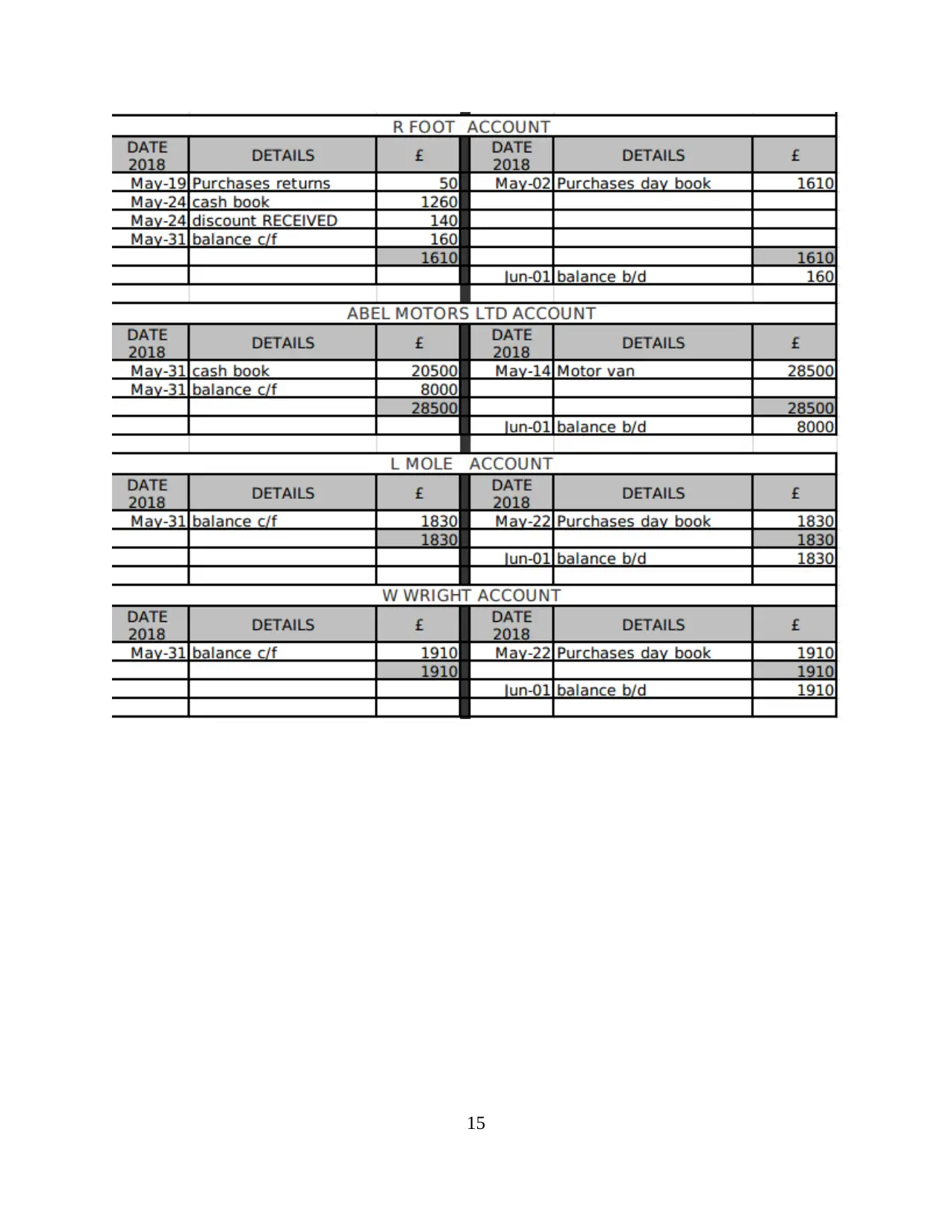

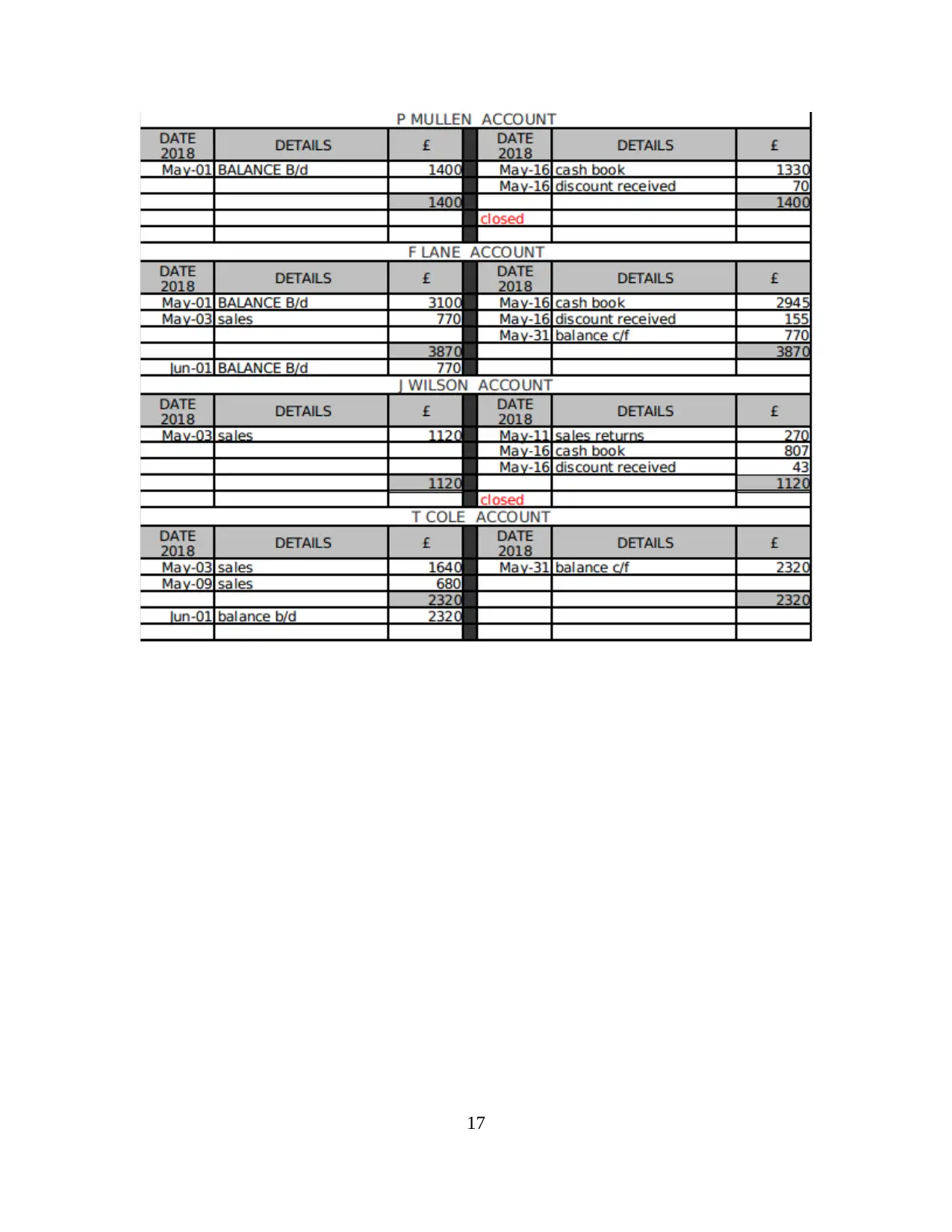

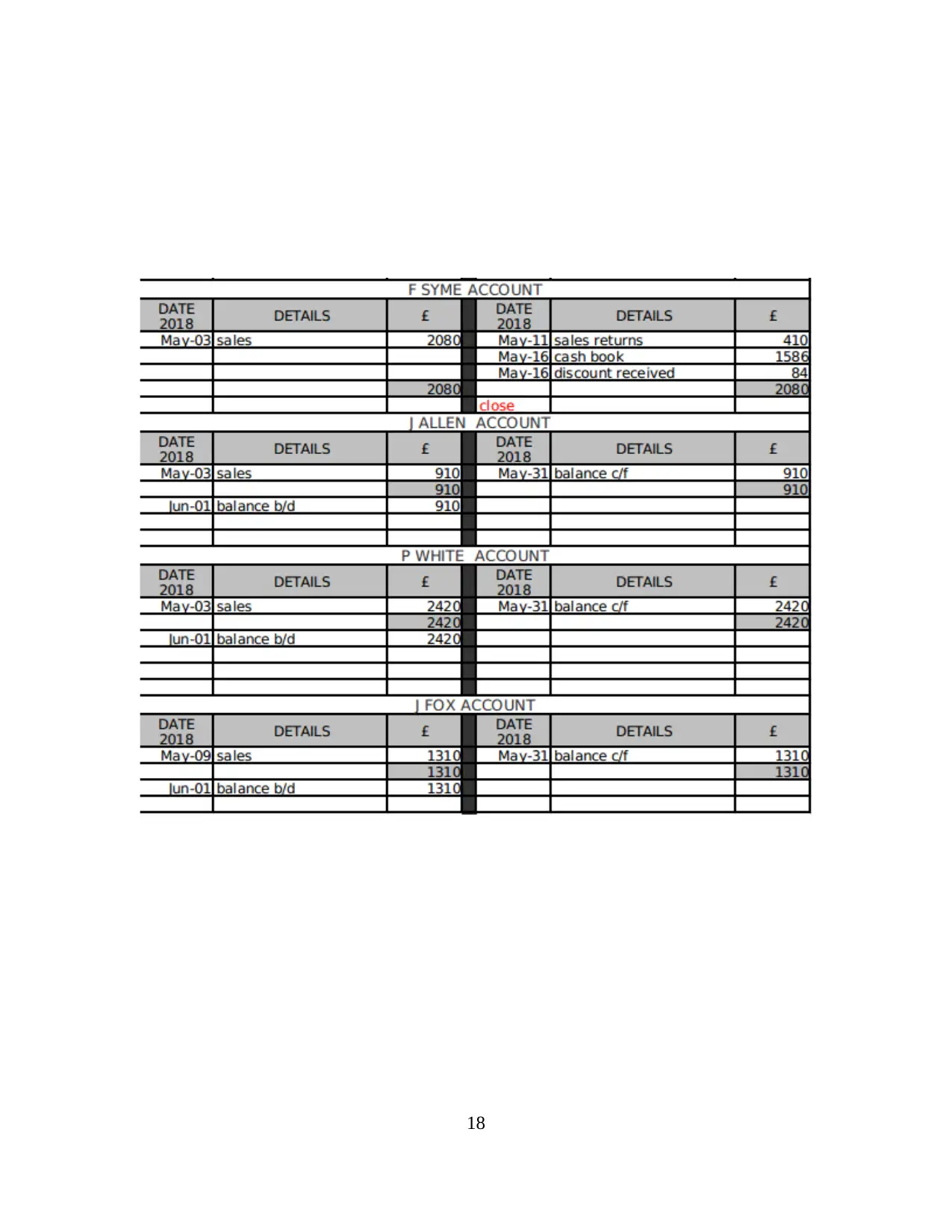

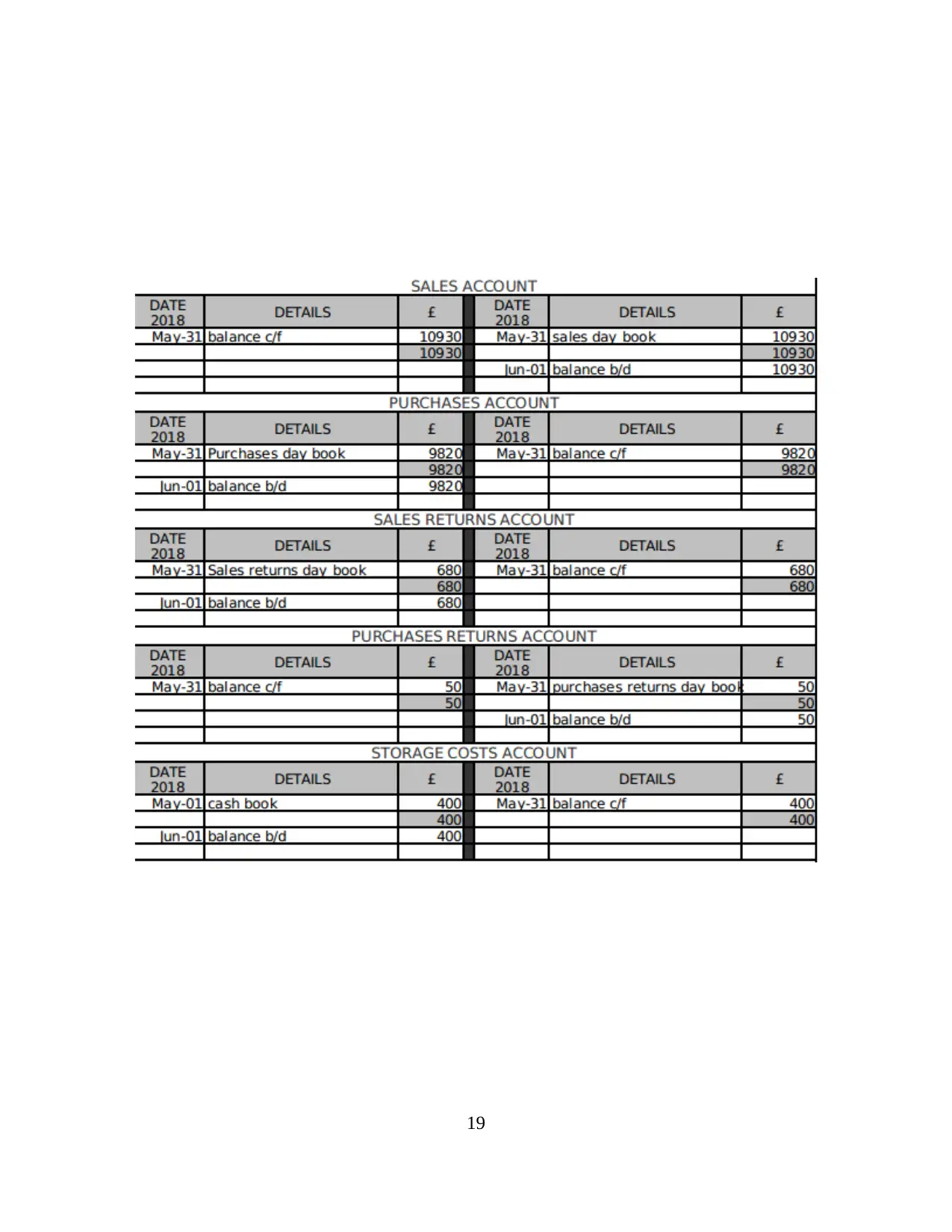

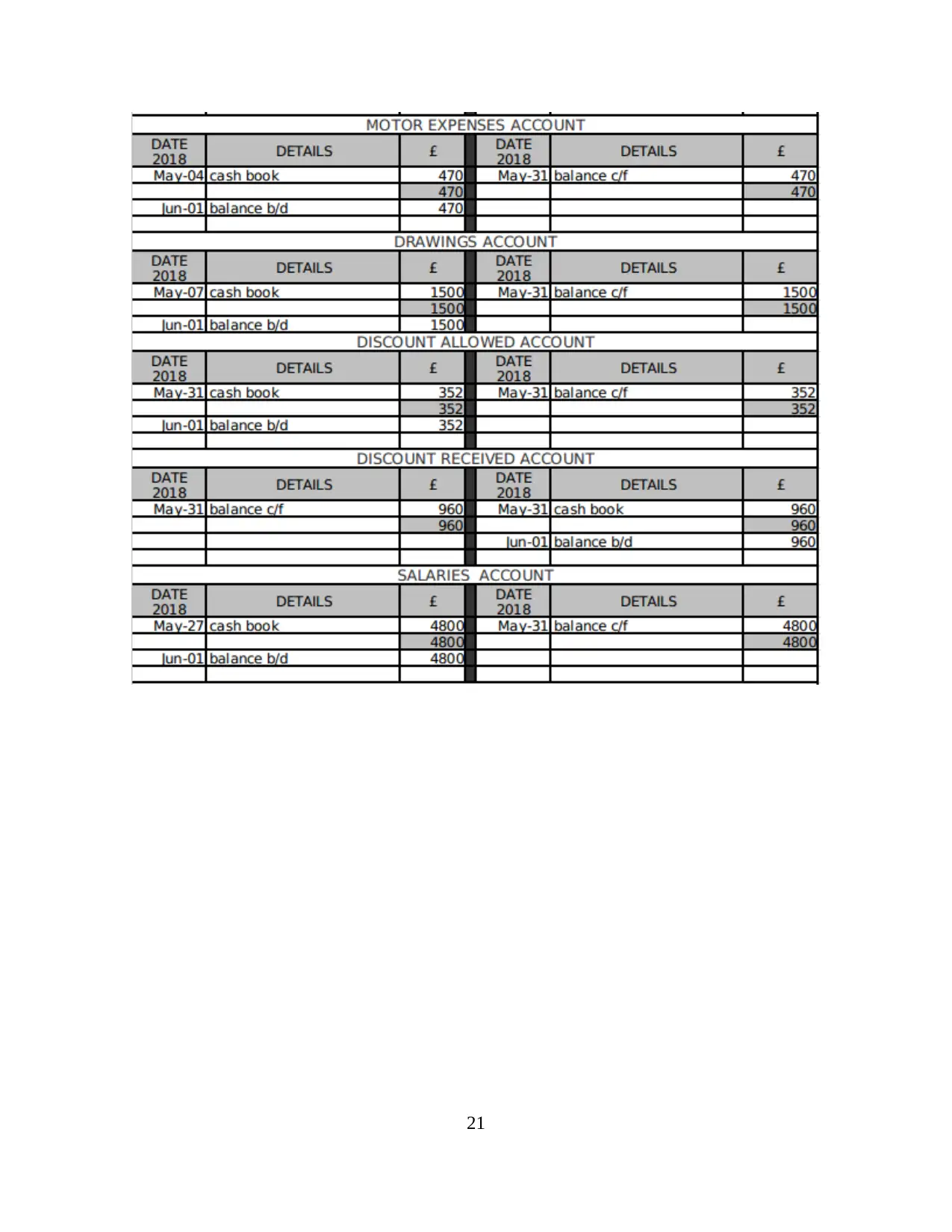

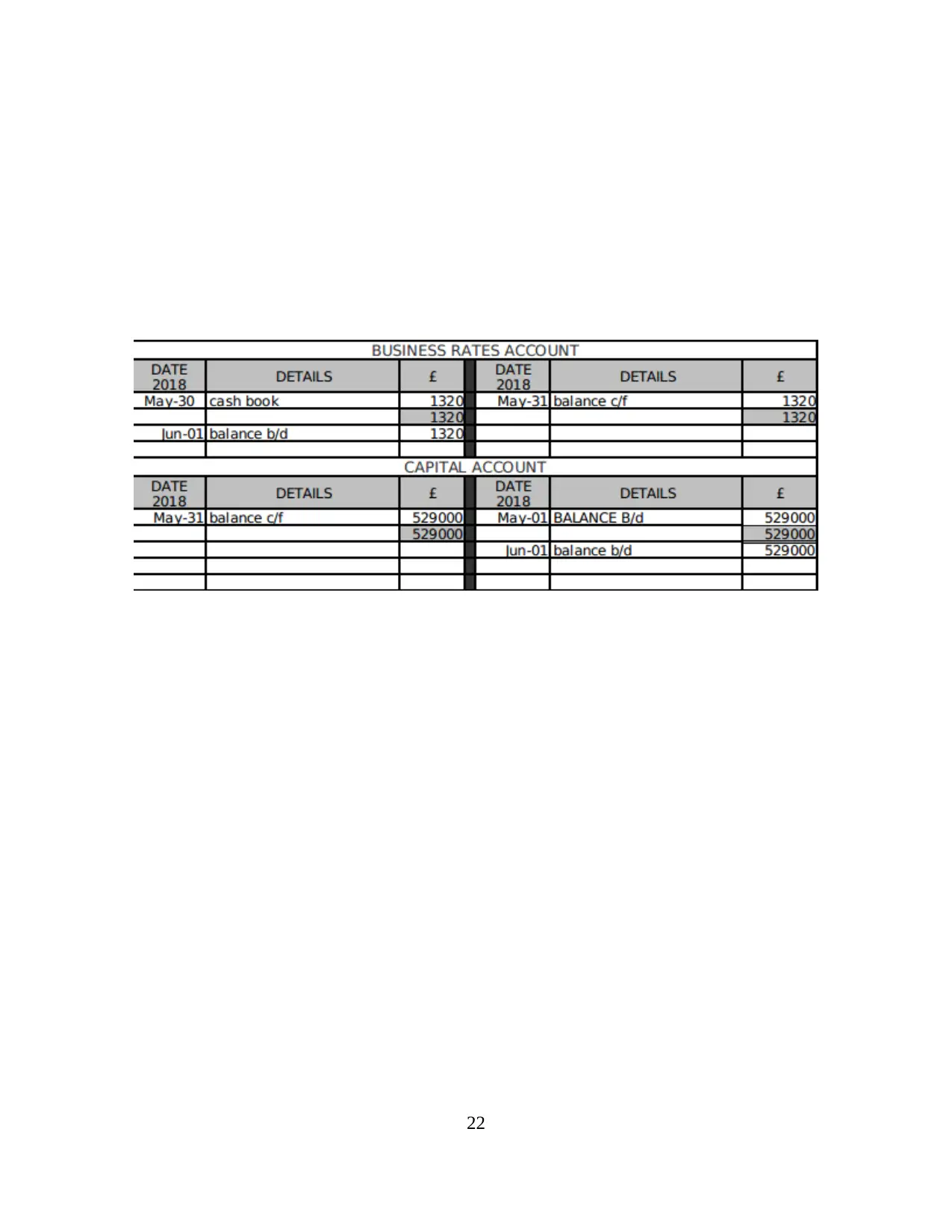

B. Producing ledger accounts for business

The journal entries are produced which is the basic step in formulating financials of the

company in effective manner. After all the entries are accounted for, next step is to post them in

general ledger accounts. The term ledger accounts are summarized set of data which is taken

from journals and as such, individual accounts are effectively prepared. Moreover, separate

accounts are prepared which is used to analyse transaction of receipts and payments for a

particular time frame. It helps management to assess costs and income garnered in a better way.

Hence, costs are effectively controlled and profits are maximised up to a high extent. Ledger

accounts are produced for client below-

10

The journal entries are produced which is the basic step in formulating financials of the

company in effective manner. After all the entries are accounted for, next step is to post them in

general ledger accounts. The term ledger accounts are summarized set of data which is taken

from journals and as such, individual accounts are effectively prepared. Moreover, separate

accounts are prepared which is used to analyse transaction of receipts and payments for a

particular time frame. It helps management to assess costs and income garnered in a better way.

Hence, costs are effectively controlled and profits are maximised up to a high extent. Ledger

accounts are produced for client below-

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

12

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

14

15

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

17

18

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

20

21

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

23

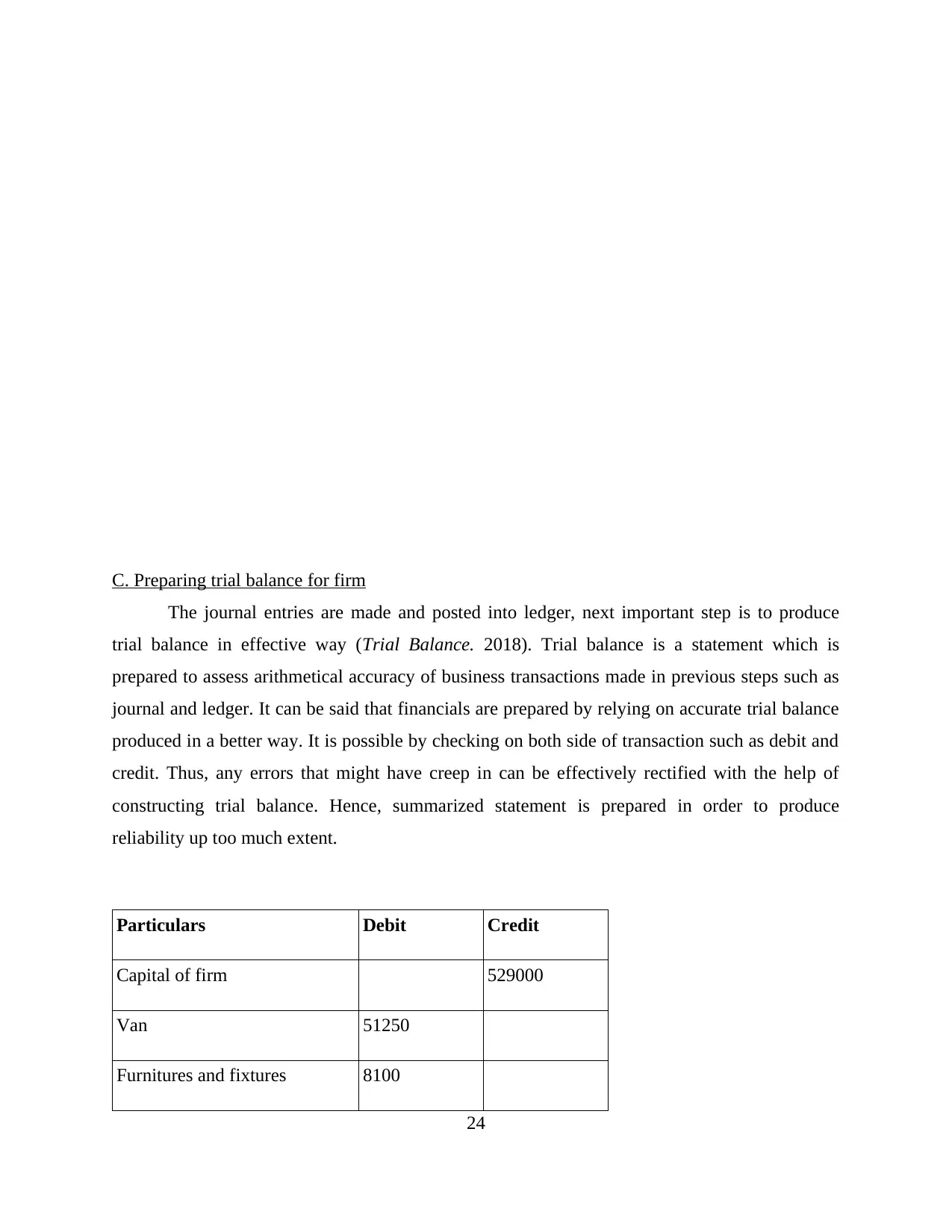

C. Preparing trial balance for firm

The journal entries are made and posted into ledger, next important step is to produce

trial balance in effective way (Trial Balance. 2018). Trial balance is a statement which is

prepared to assess arithmetical accuracy of business transactions made in previous steps such as

journal and ledger. It can be said that financials are prepared by relying on accurate trial balance

produced in a better way. It is possible by checking on both side of transaction such as debit and

credit. Thus, any errors that might have creep in can be effectively rectified with the help of

constructing trial balance. Hence, summarized statement is prepared in order to produce

reliability up too much extent.

Particulars Debit Credit

Capital of firm 529000

Van 51250

Furnitures and fixtures 8100

24

The journal entries are made and posted into ledger, next important step is to produce

trial balance in effective way (Trial Balance. 2018). Trial balance is a statement which is

prepared to assess arithmetical accuracy of business transactions made in previous steps such as

journal and ledger. It can be said that financials are prepared by relying on accurate trial balance

produced in a better way. It is possible by checking on both side of transaction such as debit and

credit. Thus, any errors that might have creep in can be effectively rectified with the help of

constructing trial balance. Hence, summarized statement is prepared in order to produce

reliability up too much extent.

Particulars Debit Credit

Capital of firm 529000

Van 51250

Furnitures and fixtures 8100

24

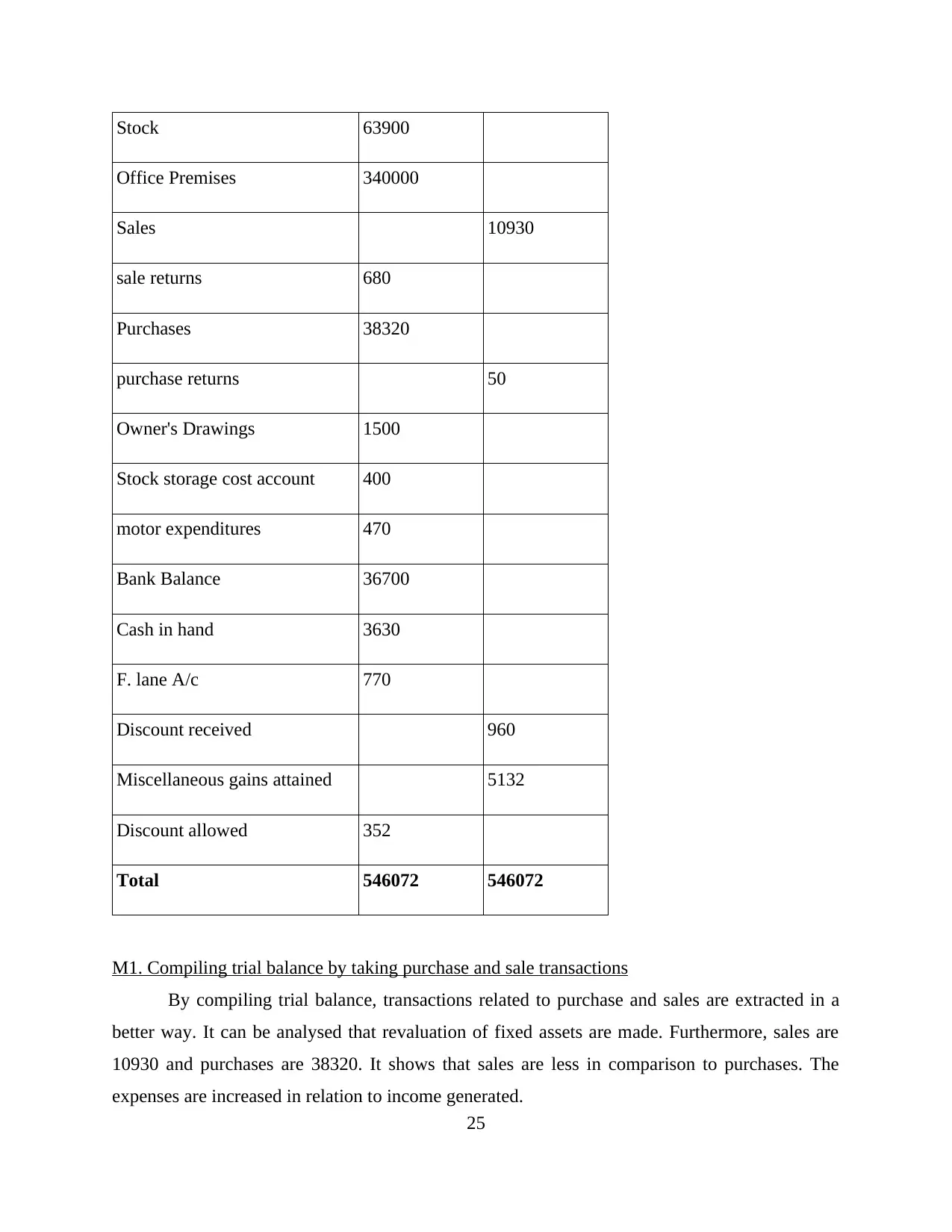

Stock 63900

Office Premises 340000

Sales 10930

sale returns 680

Purchases 38320

purchase returns 50

Owner's Drawings 1500

Stock storage cost account 400

motor expenditures 470

Bank Balance 36700

Cash in hand 3630

F. lane A/c 770

Discount received 960

Miscellaneous gains attained 5132

Discount allowed 352

Total 546072 546072

M1. Compiling trial balance by taking purchase and sale transactions

By compiling trial balance, transactions related to purchase and sales are extracted in a

better way. It can be analysed that revaluation of fixed assets are made. Furthermore, sales are

10930 and purchases are 38320. It shows that sales are less in comparison to purchases. The

expenses are increased in relation to income generated.

25

Office Premises 340000

Sales 10930

sale returns 680

Purchases 38320

purchase returns 50

Owner's Drawings 1500

Stock storage cost account 400

motor expenditures 470

Bank Balance 36700

Cash in hand 3630

F. lane A/c 770

Discount received 960

Miscellaneous gains attained 5132

Discount allowed 352

Total 546072 546072

M1. Compiling trial balance by taking purchase and sale transactions

By compiling trial balance, transactions related to purchase and sales are extracted in a

better way. It can be analysed that revaluation of fixed assets are made. Furthermore, sales are

10930 and purchases are 38320. It shows that sales are less in comparison to purchases. The

expenses are increased in relation to income generated.

25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

M2. Trial balance by considering accounting rules and regulations

Preparation of trial balance is made in accordance to the rules and guidelines provided by

various professional bodies such as IASB, GAAP and FRS. Mathematical accuracy is observed

by following guidelines in appropriate way (Adalı and Kızıl, 2017).

CLIENT 2

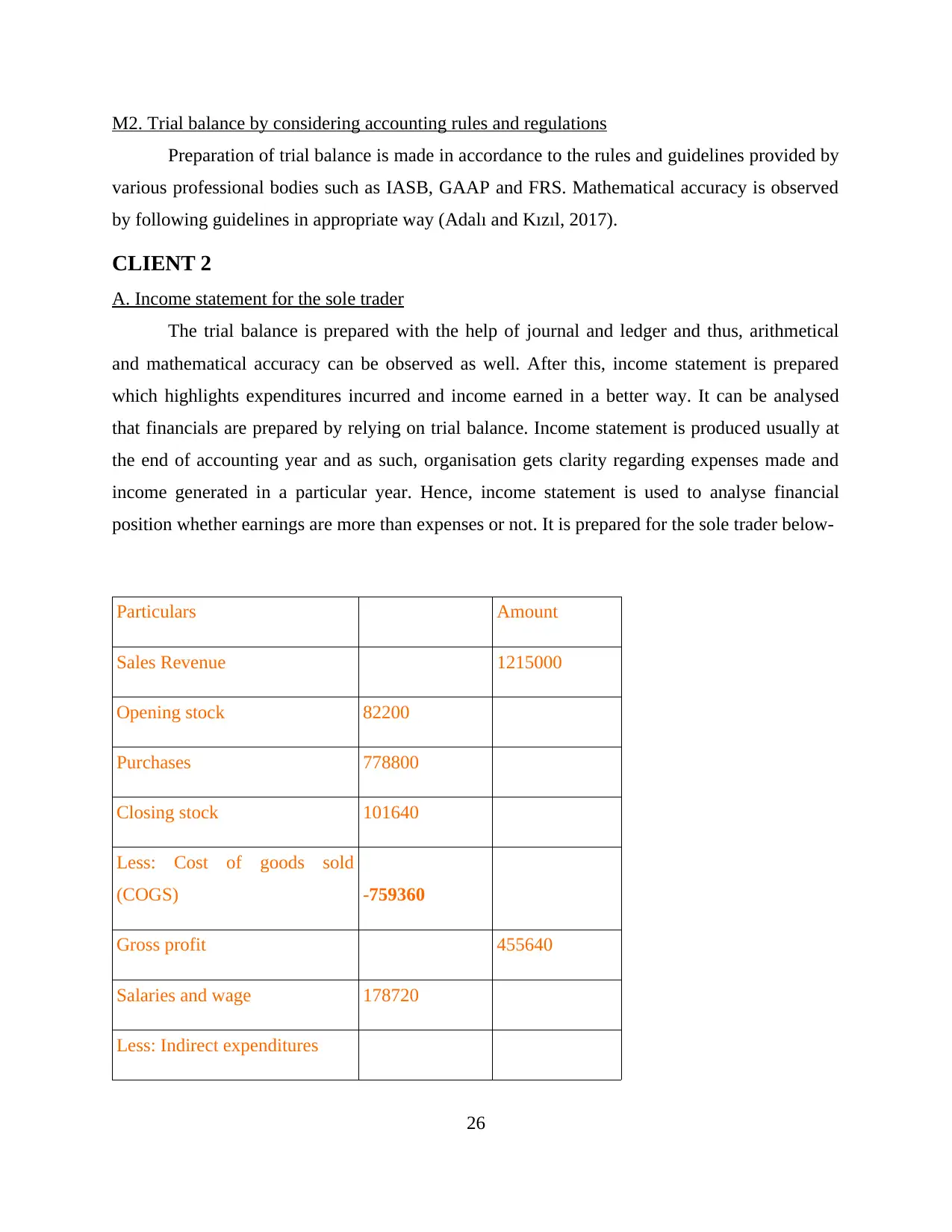

A. Income statement for the sole trader

The trial balance is prepared with the help of journal and ledger and thus, arithmetical

and mathematical accuracy can be observed as well. After this, income statement is prepared

which highlights expenditures incurred and income earned in a better way. It can be analysed

that financials are prepared by relying on trial balance. Income statement is produced usually at

the end of accounting year and as such, organisation gets clarity regarding expenses made and

income generated in a particular year. Hence, income statement is used to analyse financial

position whether earnings are more than expenses or not. It is prepared for the sole trader below-

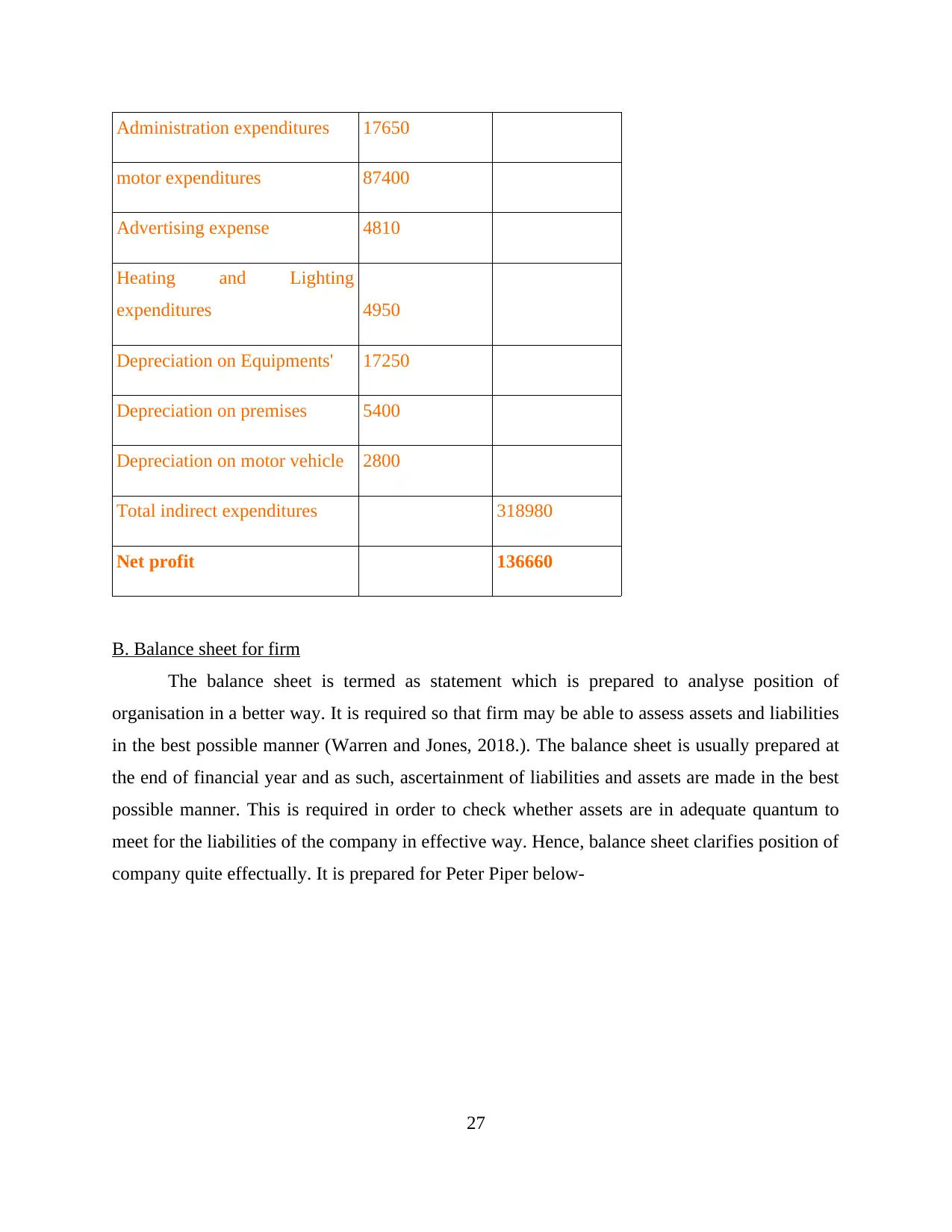

Particulars Amount

Sales Revenue 1215000

Opening stock 82200

Purchases 778800

Closing stock 101640

Less: Cost of goods sold

(COGS) -759360

Gross profit 455640

Salaries and wage 178720

Less: Indirect expenditures

26

Preparation of trial balance is made in accordance to the rules and guidelines provided by

various professional bodies such as IASB, GAAP and FRS. Mathematical accuracy is observed

by following guidelines in appropriate way (Adalı and Kızıl, 2017).

CLIENT 2

A. Income statement for the sole trader

The trial balance is prepared with the help of journal and ledger and thus, arithmetical

and mathematical accuracy can be observed as well. After this, income statement is prepared

which highlights expenditures incurred and income earned in a better way. It can be analysed

that financials are prepared by relying on trial balance. Income statement is produced usually at

the end of accounting year and as such, organisation gets clarity regarding expenses made and

income generated in a particular year. Hence, income statement is used to analyse financial

position whether earnings are more than expenses or not. It is prepared for the sole trader below-

Particulars Amount

Sales Revenue 1215000

Opening stock 82200

Purchases 778800

Closing stock 101640

Less: Cost of goods sold

(COGS) -759360

Gross profit 455640

Salaries and wage 178720

Less: Indirect expenditures

26

Administration expenditures 17650

motor expenditures 87400

Advertising expense 4810

Heating and Lighting

expenditures 4950

Depreciation on Equipments' 17250

Depreciation on premises 5400

Depreciation on motor vehicle 2800

Total indirect expenditures 318980

Net profit 136660

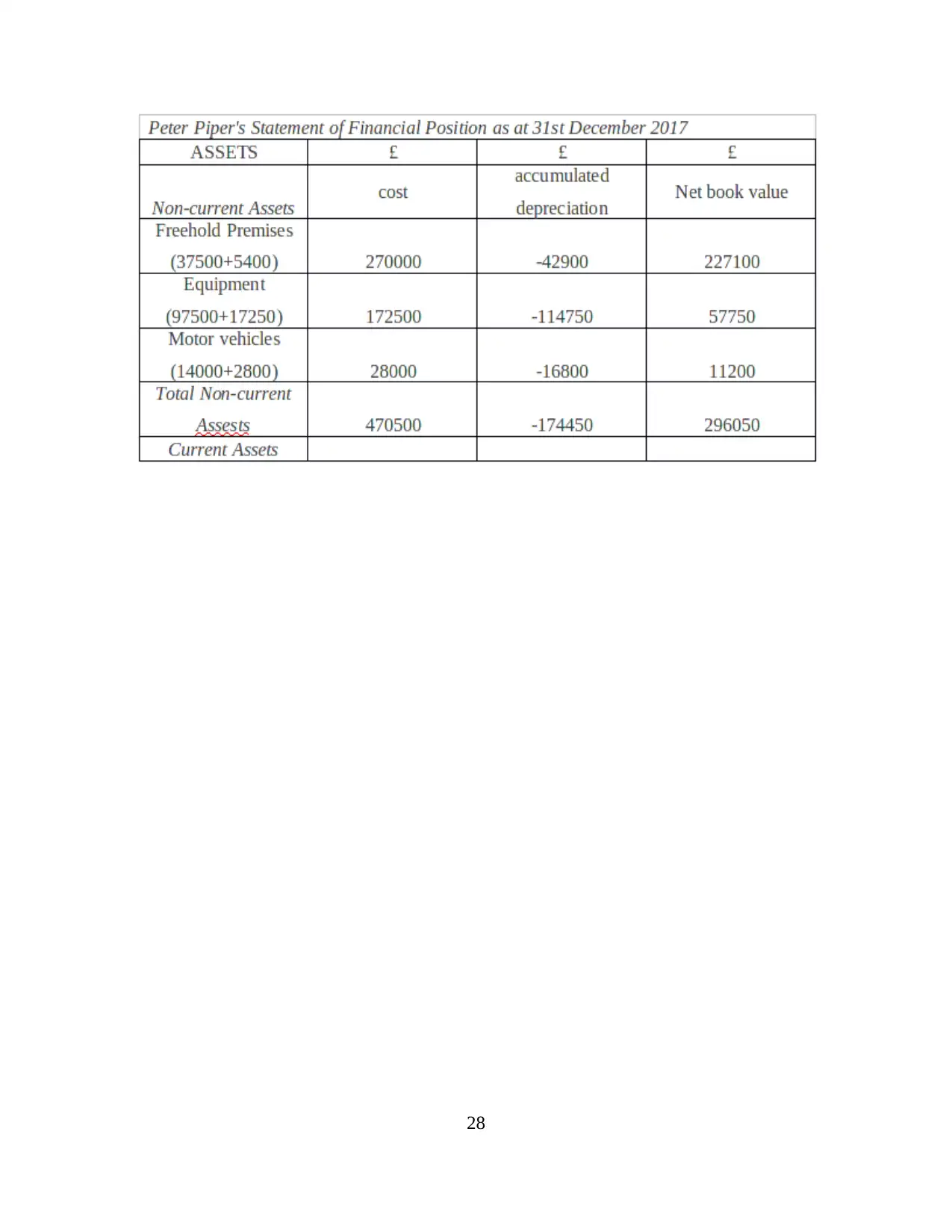

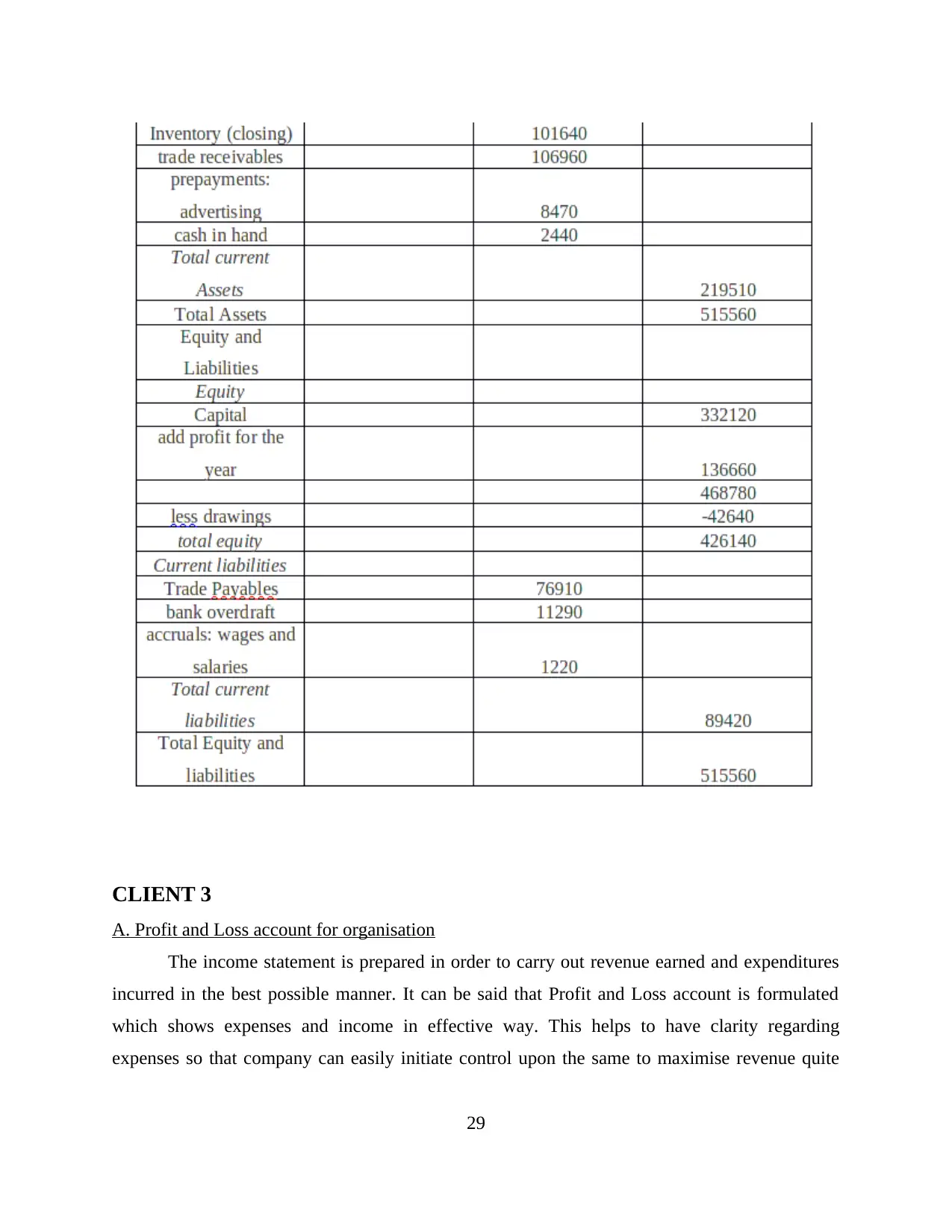

B. Balance sheet for firm

The balance sheet is termed as statement which is prepared to analyse position of

organisation in a better way. It is required so that firm may be able to assess assets and liabilities

in the best possible manner (Warren and Jones, 2018.). The balance sheet is usually prepared at

the end of financial year and as such, ascertainment of liabilities and assets are made in the best

possible manner. This is required in order to check whether assets are in adequate quantum to

meet for the liabilities of the company in effective way. Hence, balance sheet clarifies position of

company quite effectually. It is prepared for Peter Piper below-

27

motor expenditures 87400

Advertising expense 4810

Heating and Lighting

expenditures 4950

Depreciation on Equipments' 17250

Depreciation on premises 5400

Depreciation on motor vehicle 2800

Total indirect expenditures 318980

Net profit 136660

B. Balance sheet for firm

The balance sheet is termed as statement which is prepared to analyse position of

organisation in a better way. It is required so that firm may be able to assess assets and liabilities

in the best possible manner (Warren and Jones, 2018.). The balance sheet is usually prepared at

the end of financial year and as such, ascertainment of liabilities and assets are made in the best

possible manner. This is required in order to check whether assets are in adequate quantum to

meet for the liabilities of the company in effective way. Hence, balance sheet clarifies position of

company quite effectually. It is prepared for Peter Piper below-

27

28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CLIENT 3

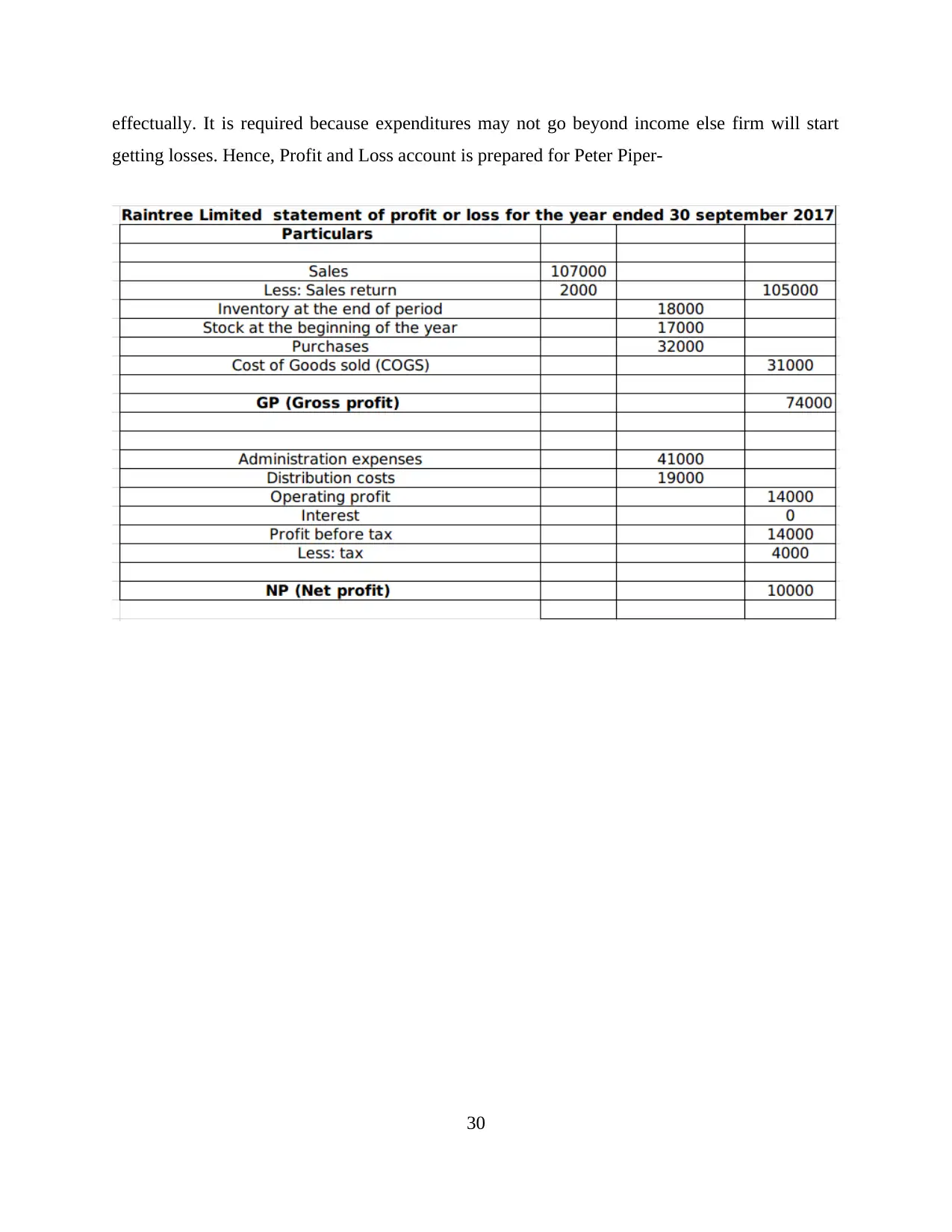

A. Profit and Loss account for organisation

The income statement is prepared in order to carry out revenue earned and expenditures

incurred in the best possible manner. It can be said that Profit and Loss account is formulated

which shows expenses and income in effective way. This helps to have clarity regarding

expenses so that company can easily initiate control upon the same to maximise revenue quite

29

A. Profit and Loss account for organisation

The income statement is prepared in order to carry out revenue earned and expenditures

incurred in the best possible manner. It can be said that Profit and Loss account is formulated

which shows expenses and income in effective way. This helps to have clarity regarding

expenses so that company can easily initiate control upon the same to maximise revenue quite

29

effectually. It is required because expenditures may not go beyond income else firm will start

getting losses. Hence, Profit and Loss account is prepared for Peter Piper-

30

getting losses. Hence, Profit and Loss account is prepared for Peter Piper-

30

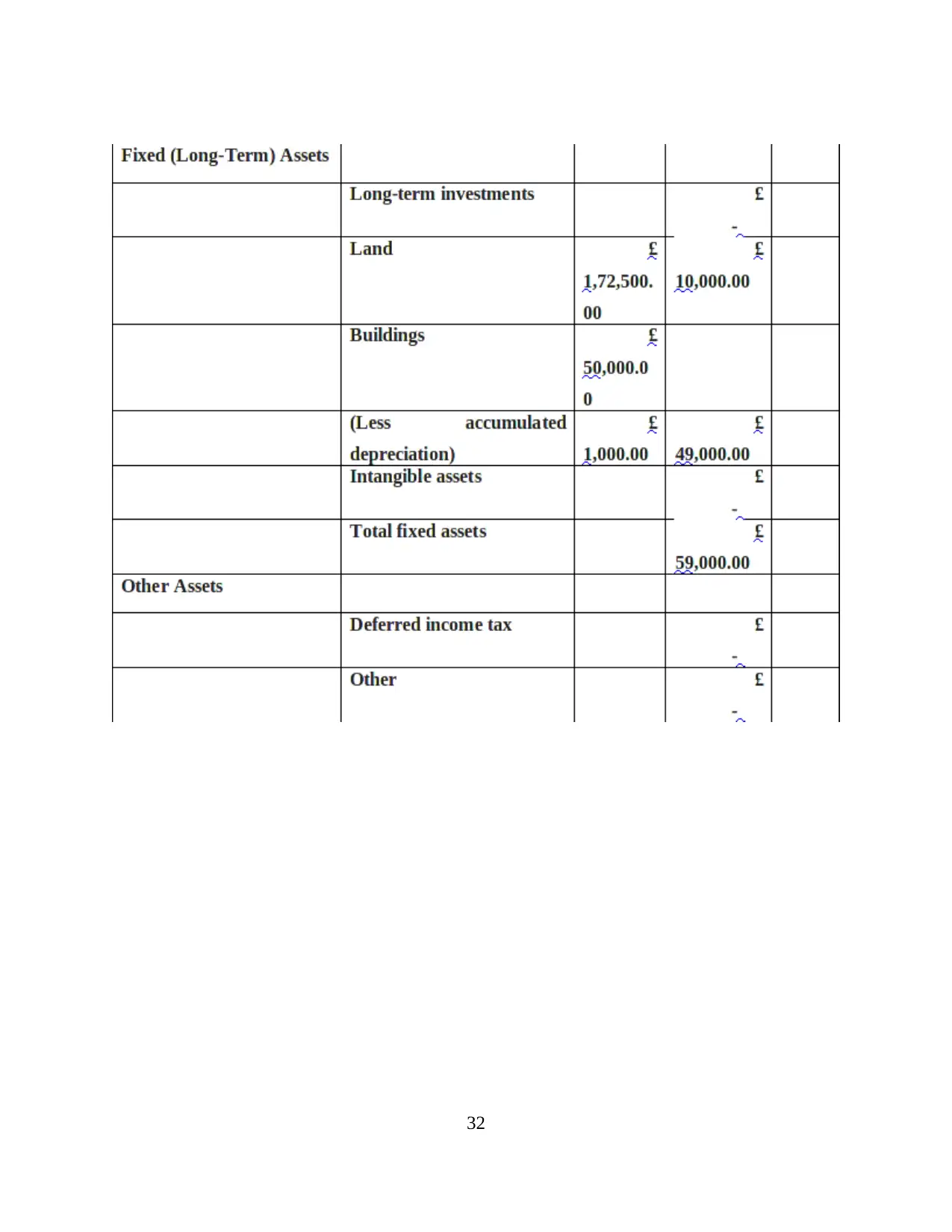

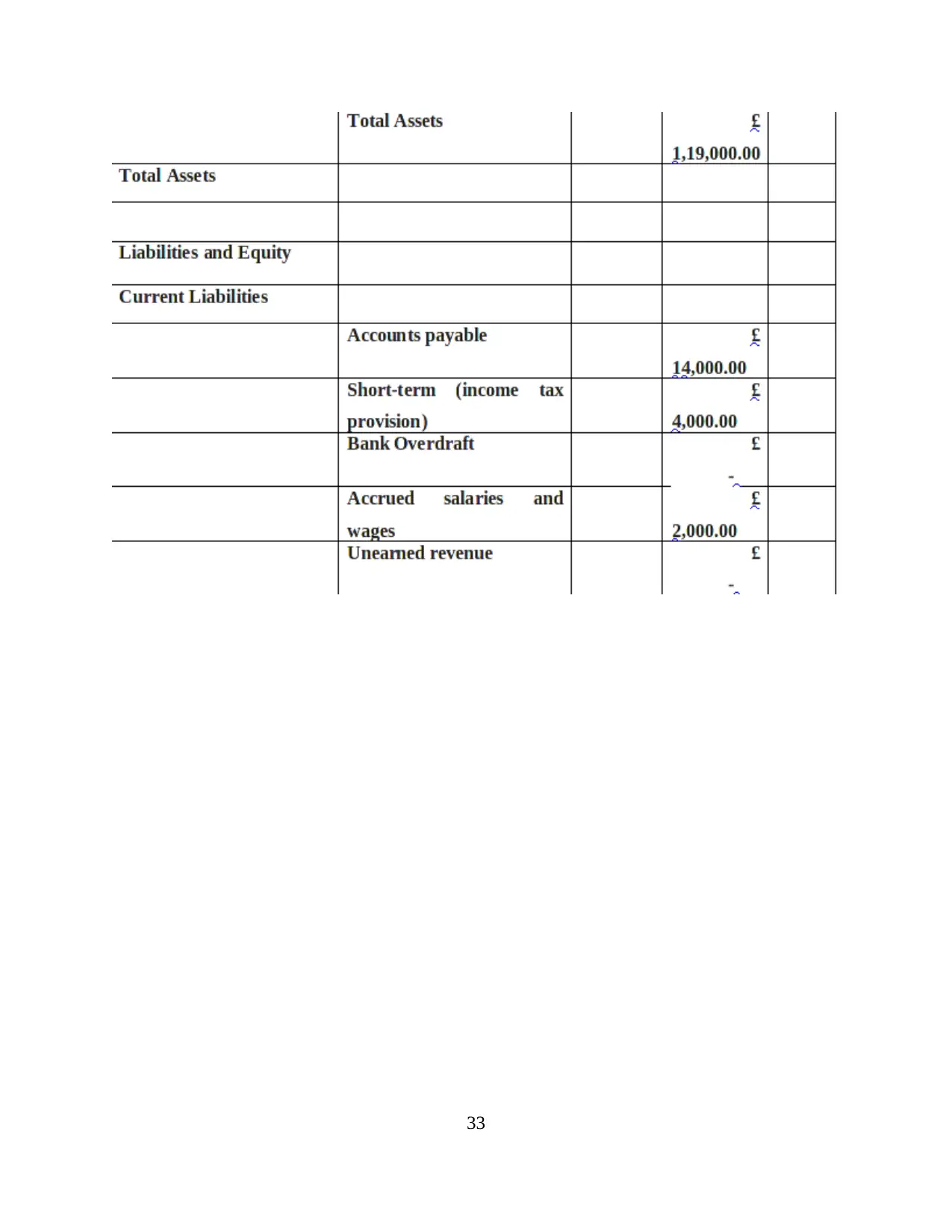

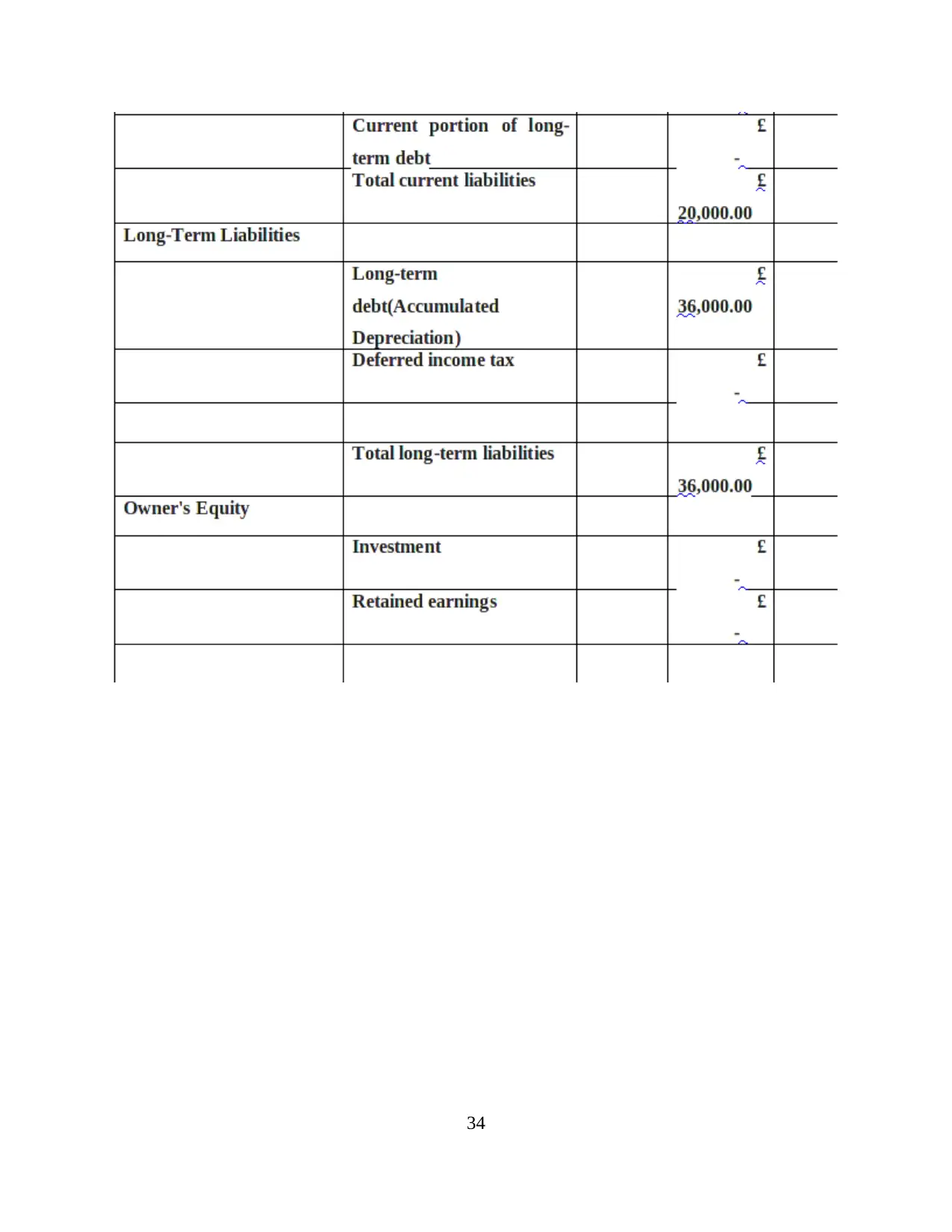

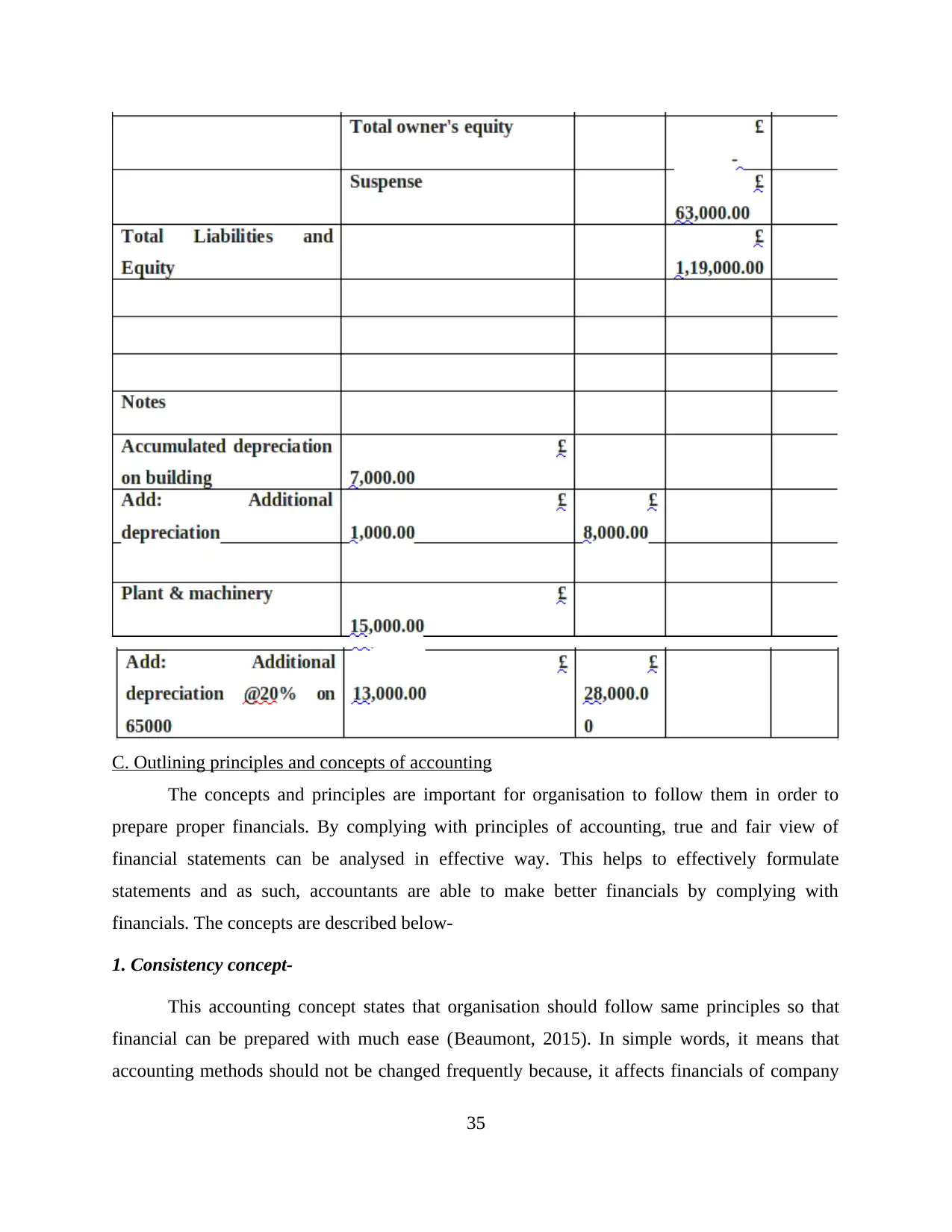

B. Balance sheet for Raintree Ltd

Balance sheet is a statement which is done in order to assess whether firm has enough

assests both current and fixed to meet liabilities in the best possible manner (Bloomfield and

et.al, 2017). This is required to be prepared as overall financial health is ascertained in a better

way. Furthermore, it is also called statement of financial position as it shows position at the end

of year quite effectually. The balance sheet is also useful as comparison can be easily made with

previous year data. The current year figure can also be matched with past data and thus, balance

sheet provides clarity regarding assets and liabilities of organisation in effectual manner. The

statement for Raintree Ltd is formulated under-

31

Balance sheet is a statement which is done in order to assess whether firm has enough

assests both current and fixed to meet liabilities in the best possible manner (Bloomfield and

et.al, 2017). This is required to be prepared as overall financial health is ascertained in a better

way. Furthermore, it is also called statement of financial position as it shows position at the end

of year quite effectually. The balance sheet is also useful as comparison can be easily made with

previous year data. The current year figure can also be matched with past data and thus, balance

sheet provides clarity regarding assets and liabilities of organisation in effectual manner. The

statement for Raintree Ltd is formulated under-

31

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

32

33

34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C. Outlining principles and concepts of accounting

The concepts and principles are important for organisation to follow them in order to

prepare proper financials. By complying with principles of accounting, true and fair view of

financial statements can be analysed in effective way. This helps to effectively formulate

statements and as such, accountants are able to make better financials by complying with

financials. The concepts are described below-

1. Consistency concept-

This accounting concept states that organisation should follow same principles so that

financial can be prepared with much ease (Beaumont, 2015). In simple words, it means that

accounting methods should not be changed frequently because, it affects financials of company

35

The concepts and principles are important for organisation to follow them in order to

prepare proper financials. By complying with principles of accounting, true and fair view of

financial statements can be analysed in effective way. This helps to effectively formulate

statements and as such, accountants are able to make better financials by complying with

financials. The concepts are described below-

1. Consistency concept-

This accounting concept states that organisation should follow same principles so that

financial can be prepared with much ease (Beaumont, 2015). In simple words, it means that

accounting methods should not be changed frequently because, it affects financials of company

35

in effective manner. It helps to attain clarity regarding accounting policies in the best possible

way. It helps to obtain reliability in effective way.

2. Prudence concept-

The prudence concept means that organisation should anticipate all losses and do not

count for gains. This is useful concept as business operates in an dynamic environment in which

changes are inevitable. Overestimation of assets should not be done and liabilities must be

underestimated.

D. Importance of measuring and presenting depreciation in financials

Depreciation is applied on fixed assets as they are useful life of asset gets reduced after

certain passage of time. It is charge on an asset because it is treated as an expense. However, it is

added back to net profit to ascertain cash flows (Dudin and et.al, 2015). There are two methods

of depreciation used in the business which are described below-

Straight line method :

The straight line method is quite useful method which charges depreciation on fixed rate

only. It means that company charges fixed rate of depreciation on yearly basis. It is charged till

life of asset becomes zero.

Written down method :

This method of depreciation is helpful as business charges depreciation which is based on

diminishing value. It is preferred by taxation authorities as it provides better view and correct

deprecation is measured through applying written down method.

M2. Assessing P&L, balance sheet and cash flow statements

The financials such as balance sheet, Profit and Loss account and cash flow statements

are used by external users to assess financial health of company. It can be said that without

preparation of these three financial statements, firm's overall position cannot be ascertained.

Hence, adequate information is imparted by them (Goh., Li, Ng and Yong, 2015).

D2. Accurate calculations in accounting for producing financial statements

The computations should be made accurately so that financials may be prepared without

any errors. The total assets 137000 and stockholders' equity were 102000 and thus, total

36

way. It helps to obtain reliability in effective way.

2. Prudence concept-

The prudence concept means that organisation should anticipate all losses and do not

count for gains. This is useful concept as business operates in an dynamic environment in which

changes are inevitable. Overestimation of assets should not be done and liabilities must be

underestimated.

D. Importance of measuring and presenting depreciation in financials

Depreciation is applied on fixed assets as they are useful life of asset gets reduced after

certain passage of time. It is charge on an asset because it is treated as an expense. However, it is

added back to net profit to ascertain cash flows (Dudin and et.al, 2015). There are two methods

of depreciation used in the business which are described below-

Straight line method :

The straight line method is quite useful method which charges depreciation on fixed rate

only. It means that company charges fixed rate of depreciation on yearly basis. It is charged till

life of asset becomes zero.

Written down method :

This method of depreciation is helpful as business charges depreciation which is based on

diminishing value. It is preferred by taxation authorities as it provides better view and correct

deprecation is measured through applying written down method.

M2. Assessing P&L, balance sheet and cash flow statements

The financials such as balance sheet, Profit and Loss account and cash flow statements

are used by external users to assess financial health of company. It can be said that without

preparation of these three financial statements, firm's overall position cannot be ascertained.

Hence, adequate information is imparted by them (Goh., Li, Ng and Yong, 2015).

D2. Accurate calculations in accounting for producing financial statements

The computations should be made accurately so that financials may be prepared without

any errors. The total assets 137000 and stockholders' equity were 102000 and thus, total

36

liabilities are 137000 which means that due to accurate calculations, both side of balance sheet is

matched.

CLIENT 4

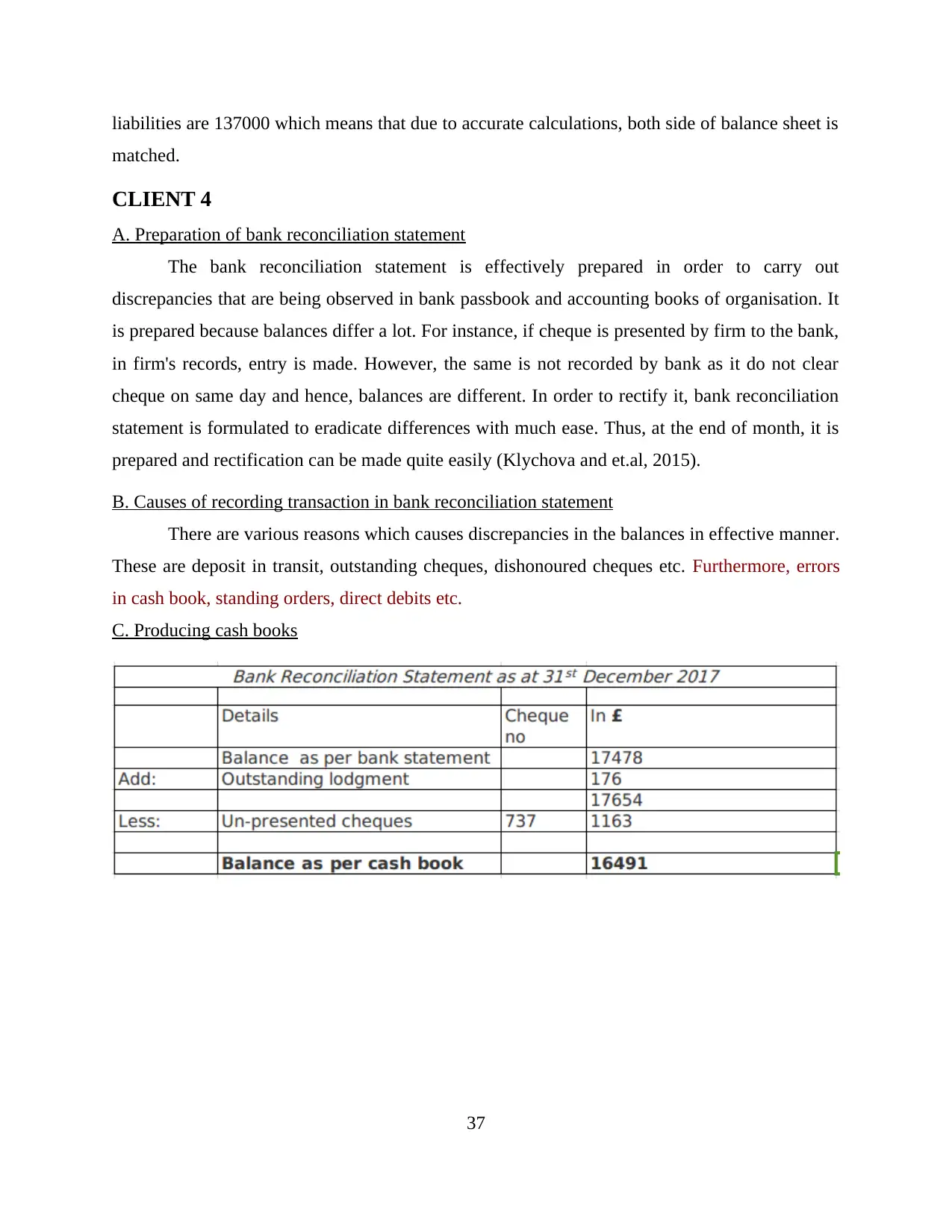

A. Preparation of bank reconciliation statement

The bank reconciliation statement is effectively prepared in order to carry out

discrepancies that are being observed in bank passbook and accounting books of organisation. It

is prepared because balances differ a lot. For instance, if cheque is presented by firm to the bank,

in firm's records, entry is made. However, the same is not recorded by bank as it do not clear

cheque on same day and hence, balances are different. In order to rectify it, bank reconciliation

statement is formulated to eradicate differences with much ease. Thus, at the end of month, it is

prepared and rectification can be made quite easily (Klychova and et.al, 2015).

B. Causes of recording transaction in bank reconciliation statement

There are various reasons which causes discrepancies in the balances in effective manner.

These are deposit in transit, outstanding cheques, dishonoured cheques etc. Furthermore, errors

in cash book, standing orders, direct debits etc.

C. Producing cash books

37

matched.

CLIENT 4

A. Preparation of bank reconciliation statement

The bank reconciliation statement is effectively prepared in order to carry out

discrepancies that are being observed in bank passbook and accounting books of organisation. It

is prepared because balances differ a lot. For instance, if cheque is presented by firm to the bank,

in firm's records, entry is made. However, the same is not recorded by bank as it do not clear

cheque on same day and hence, balances are different. In order to rectify it, bank reconciliation

statement is formulated to eradicate differences with much ease. Thus, at the end of month, it is

prepared and rectification can be made quite easily (Klychova and et.al, 2015).

B. Causes of recording transaction in bank reconciliation statement

There are various reasons which causes discrepancies in the balances in effective manner.

These are deposit in transit, outstanding cheques, dishonoured cheques etc. Furthermore, errors

in cash book, standing orders, direct debits etc.

C. Producing cash books

37

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

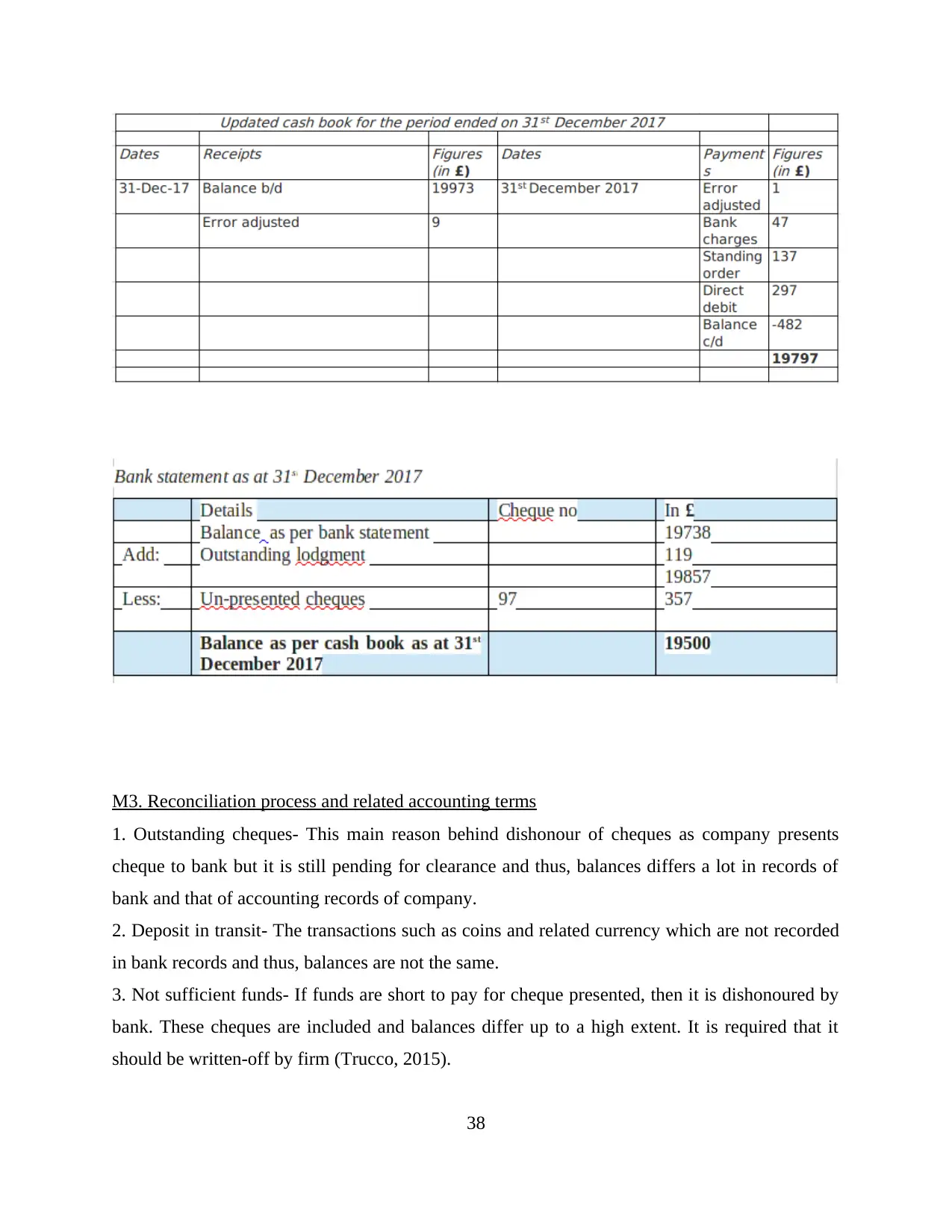

M3. Reconciliation process and related accounting terms

1. Outstanding cheques- This main reason behind dishonour of cheques as company presents

cheque to bank but it is still pending for clearance and thus, balances differs a lot in records of

bank and that of accounting records of company.

2. Deposit in transit- The transactions such as coins and related currency which are not recorded

in bank records and thus, balances are not the same.

3. Not sufficient funds- If funds are short to pay for cheque presented, then it is dishonoured by

bank. These cheques are included and balances differ up to a high extent. It is required that it

should be written-off by firm (Trucco, 2015).

38

1. Outstanding cheques- This main reason behind dishonour of cheques as company presents

cheque to bank but it is still pending for clearance and thus, balances differs a lot in records of

bank and that of accounting records of company.

2. Deposit in transit- The transactions such as coins and related currency which are not recorded

in bank records and thus, balances are not the same.

3. Not sufficient funds- If funds are short to pay for cheque presented, then it is dishonoured by

bank. These cheques are included and balances differ up to a high extent. It is required that it

should be written-off by firm (Trucco, 2015).

38

D3. Producing bank reconciliation statement

The concepts that are used in preparing bank statements are ratio analysis, trend analysis

etc.

CLIENT 5

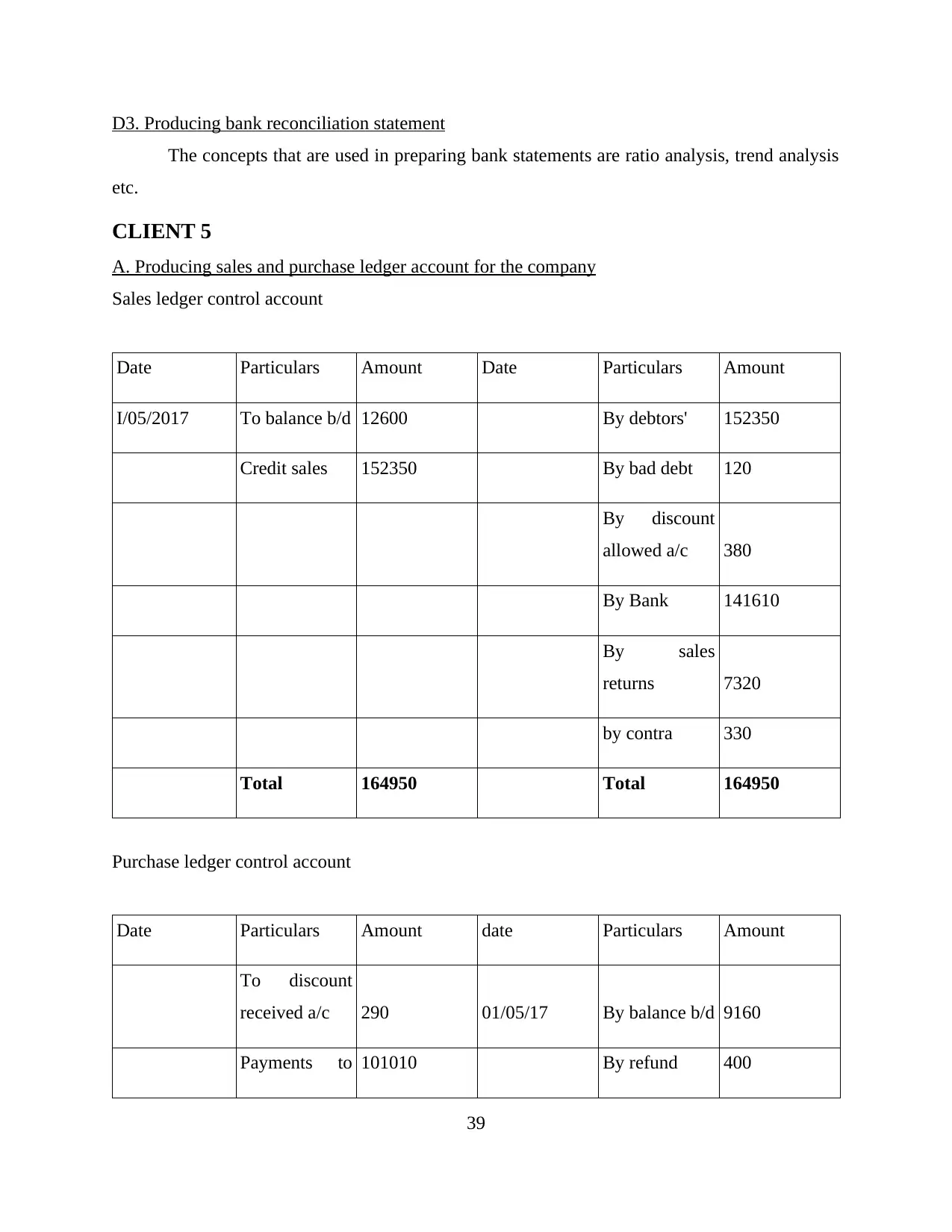

A. Producing sales and purchase ledger account for the company

Sales ledger control account

Date Particulars Amount Date Particulars Amount

I/05/2017 To balance b/d 12600 By debtors' 152350

Credit sales 152350 By bad debt 120

By discount

allowed a/c 380

By Bank 141610

By sales

returns 7320

by contra 330

Total 164950 Total 164950

Purchase ledger control account

Date Particulars Amount date Particulars Amount

To discount

received a/c 290 01/05/17 By balance b/d 9160

Payments to 101010 By refund 400

39

The concepts that are used in preparing bank statements are ratio analysis, trend analysis

etc.

CLIENT 5

A. Producing sales and purchase ledger account for the company

Sales ledger control account

Date Particulars Amount Date Particulars Amount

I/05/2017 To balance b/d 12600 By debtors' 152350

Credit sales 152350 By bad debt 120

By discount

allowed a/c 380

By Bank 141610

By sales

returns 7320

by contra 330

Total 164950 Total 164950

Purchase ledger control account

Date Particulars Amount date Particulars Amount

To discount

received a/c 290 01/05/17 By balance b/d 9160

Payments to 101010 By refund 400

39

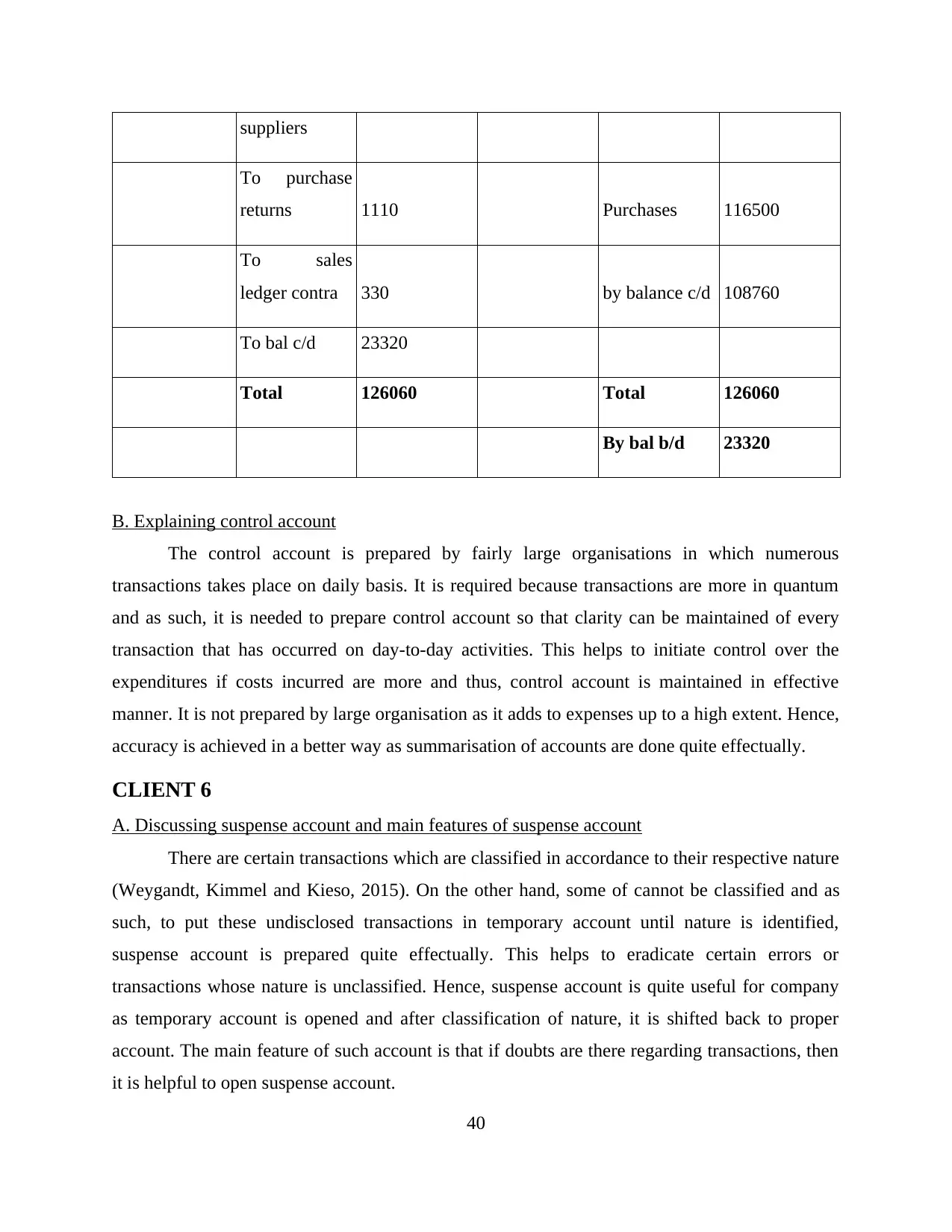

suppliers

To purchase

returns 1110 Purchases 116500

To sales

ledger contra 330 by balance c/d 108760

To bal c/d 23320

Total 126060 Total 126060

By bal b/d 23320

B. Explaining control account

The control account is prepared by fairly large organisations in which numerous

transactions takes place on daily basis. It is required because transactions are more in quantum

and as such, it is needed to prepare control account so that clarity can be maintained of every

transaction that has occurred on day-to-day activities. This helps to initiate control over the

expenditures if costs incurred are more and thus, control account is maintained in effective

manner. It is not prepared by large organisation as it adds to expenses up to a high extent. Hence,

accuracy is achieved in a better way as summarisation of accounts are done quite effectually.

CLIENT 6

A. Discussing suspense account and main features of suspense account

There are certain transactions which are classified in accordance to their respective nature

(Weygandt, Kimmel and Kieso, 2015). On the other hand, some of cannot be classified and as

such, to put these undisclosed transactions in temporary account until nature is identified,

suspense account is prepared quite effectually. This helps to eradicate certain errors or

transactions whose nature is unclassified. Hence, suspense account is quite useful for company

as temporary account is opened and after classification of nature, it is shifted back to proper

account. The main feature of such account is that if doubts are there regarding transactions, then

it is helpful to open suspense account.

40

To purchase

returns 1110 Purchases 116500

To sales

ledger contra 330 by balance c/d 108760

To bal c/d 23320

Total 126060 Total 126060

By bal b/d 23320

B. Explaining control account

The control account is prepared by fairly large organisations in which numerous

transactions takes place on daily basis. It is required because transactions are more in quantum

and as such, it is needed to prepare control account so that clarity can be maintained of every

transaction that has occurred on day-to-day activities. This helps to initiate control over the

expenditures if costs incurred are more and thus, control account is maintained in effective

manner. It is not prepared by large organisation as it adds to expenses up to a high extent. Hence,

accuracy is achieved in a better way as summarisation of accounts are done quite effectually.

CLIENT 6

A. Discussing suspense account and main features of suspense account

There are certain transactions which are classified in accordance to their respective nature

(Weygandt, Kimmel and Kieso, 2015). On the other hand, some of cannot be classified and as

such, to put these undisclosed transactions in temporary account until nature is identified,

suspense account is prepared quite effectually. This helps to eradicate certain errors or

transactions whose nature is unclassified. Hence, suspense account is quite useful for company

as temporary account is opened and after classification of nature, it is shifted back to proper

account. The main feature of such account is that if doubts are there regarding transactions, then

it is helpful to open suspense account.

40

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

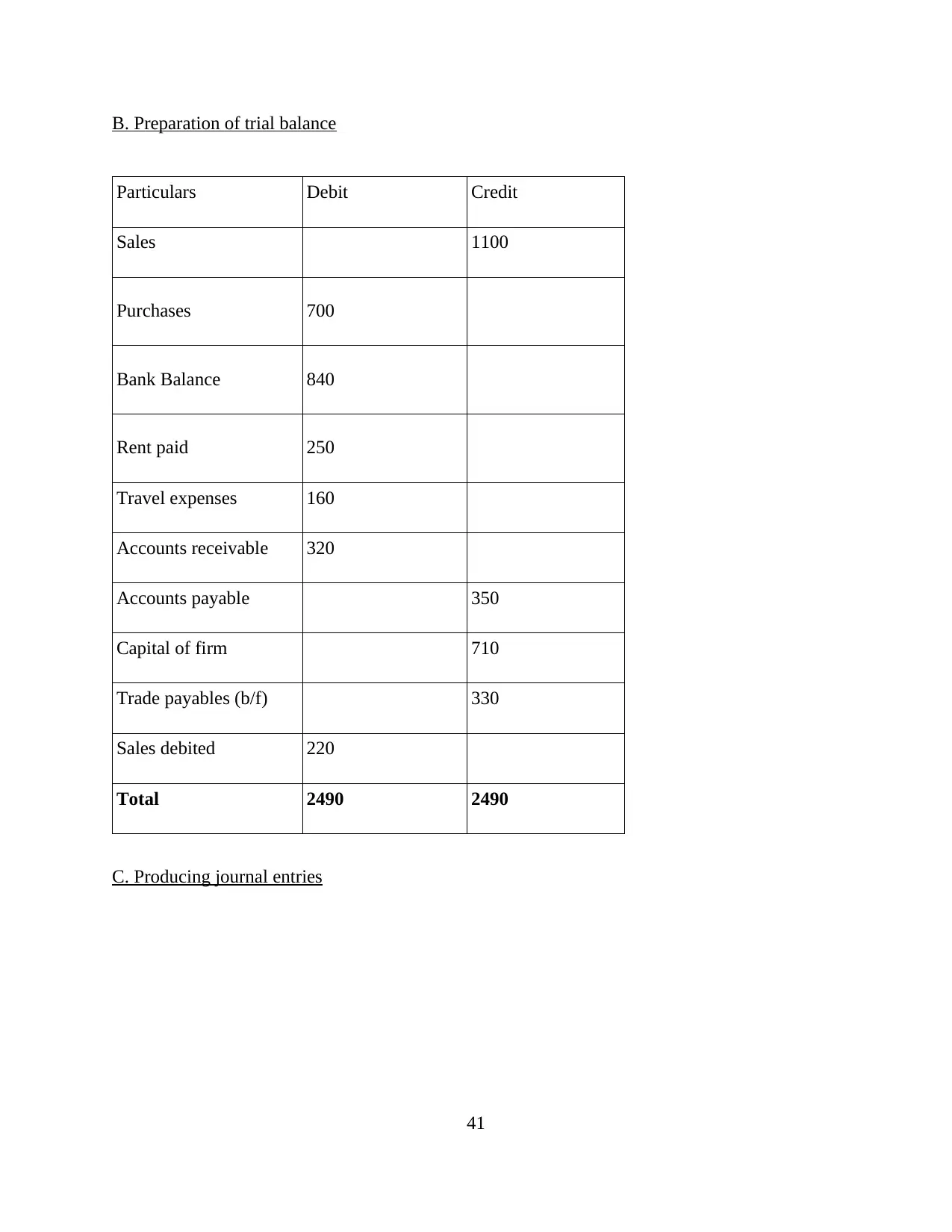

B. Preparation of trial balance

Particulars Debit Credit

Sales 1100

Purchases 700

Bank Balance 840

Rent paid 250

Travel expenses 160

Accounts receivable 320

Accounts payable 350

Capital of firm 710

Trade payables (b/f) 330

Sales debited 220

Total 2490 2490

C. Producing journal entries

41

Particulars Debit Credit

Sales 1100

Purchases 700

Bank Balance 840

Rent paid 250

Travel expenses 160

Accounts receivable 320

Accounts payable 350

Capital of firm 710

Trade payables (b/f) 330

Sales debited 220

Total 2490 2490

C. Producing journal entries

41

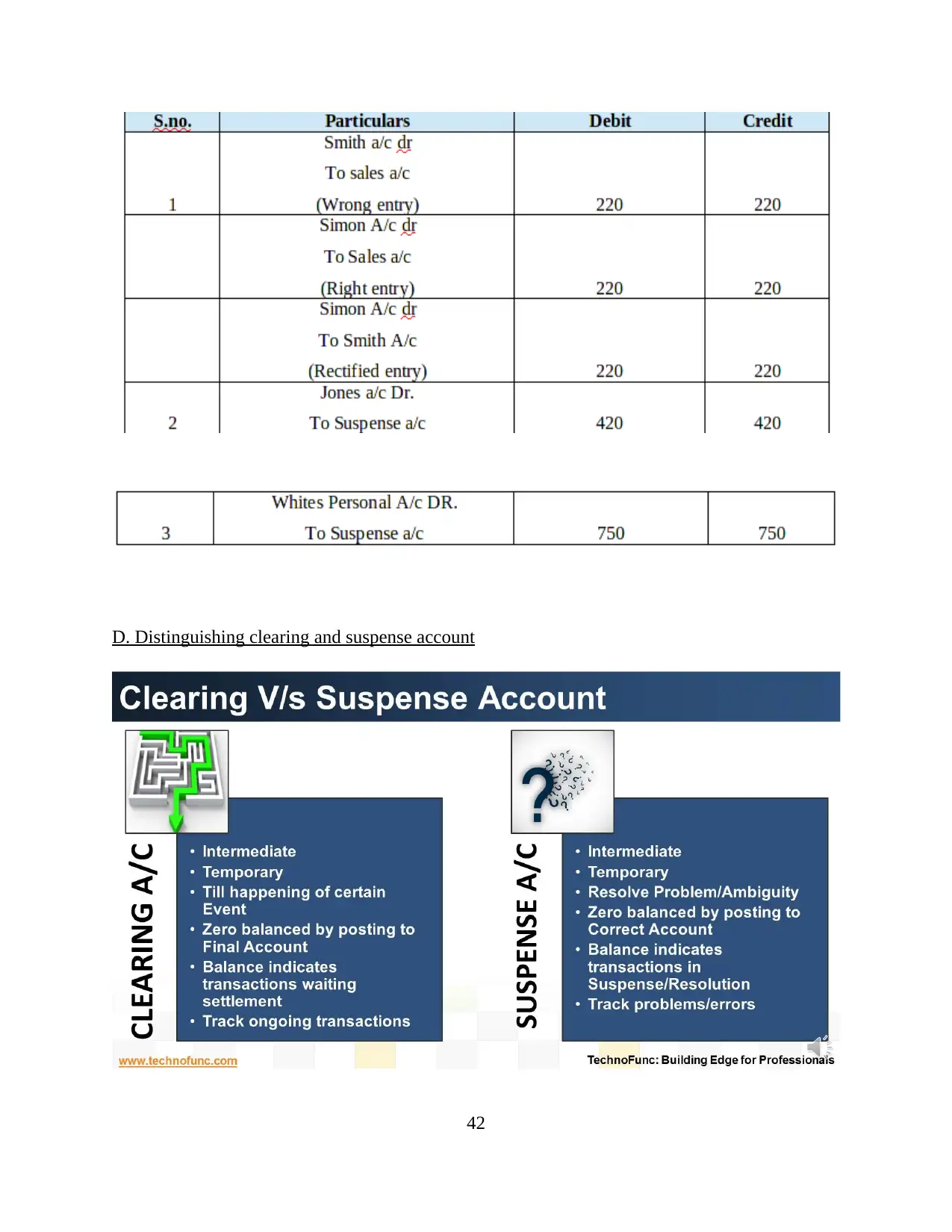

D. Distinguishing clearing and suspense account

42

42

M4. Exploring types of accounts

There are various statements which helps to effectively analyse financial position in

effectual manner. Basically, income statement is formulated which shows revenue earned and

expenditures incurred quite effectually. Furthermore, business reduces expenses so that it may

not exceed income in effective manner. On the other hand, balance sheet is prepared showing

assets and liabilities in the best possible manner (Warren Jr, Moffitt and Byrnes, 2015).

D4. Providing accounting methods for organisation

The accounting methods help to produce financial statements in effective manner. The

methods are required in order to prepare true and fair financials. Hence, by applying methods,

reliability and transparency can be effectively observed. This helps company to prepare

financials which are useful for external users to rely upon.

CONCLUSION

Hereby it can be concluded that business may be able to inject efficiency with the help of

accounting. It is required in order to attain clarity regarding operations of business. The

regulations imparted by professional bodies help accountants to construct financials in the best

possible manner. It can be said that firm is able to produce fair statements and thus, reliable

information is provided to stakeholders to take decisions. Moreover, financials such as balance

sheet, income statement and cash flow statement are pillars of financial statements and clarifies

overall position of company quite effectually. Thus, it can be said that by taking into account,

regulation and concepts, true and fair view of financials may be ascertained.

43

There are various statements which helps to effectively analyse financial position in

effectual manner. Basically, income statement is formulated which shows revenue earned and

expenditures incurred quite effectually. Furthermore, business reduces expenses so that it may

not exceed income in effective manner. On the other hand, balance sheet is prepared showing

assets and liabilities in the best possible manner (Warren Jr, Moffitt and Byrnes, 2015).

D4. Providing accounting methods for organisation

The accounting methods help to produce financial statements in effective manner. The

methods are required in order to prepare true and fair financials. Hence, by applying methods,

reliability and transparency can be effectively observed. This helps company to prepare

financials which are useful for external users to rely upon.

CONCLUSION

Hereby it can be concluded that business may be able to inject efficiency with the help of

accounting. It is required in order to attain clarity regarding operations of business. The

regulations imparted by professional bodies help accountants to construct financials in the best

possible manner. It can be said that firm is able to produce fair statements and thus, reliable

information is provided to stakeholders to take decisions. Moreover, financials such as balance

sheet, income statement and cash flow statement are pillars of financial statements and clarifies

overall position of company quite effectually. Thus, it can be said that by taking into account,

regulation and concepts, true and fair view of financials may be ascertained.

43

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Adalı, S. and Kızıl, C., 2017. A Research on the Responsibility of Accounting Professionals to

Determine and Prevent Accounting Errors and Frauds: Edirne Sample. EMAJ: Emerging

Markets Journal. 7(1). pp.53-64.

Beaumont, S. J., 2015. An investigation of the short‐and long‐run relations between executive

cash bonus payments and firm financial performance: a pitch. Accounting & Finance.

55(2). pp.337-343.

Bloomfield and et.al, 2017. The Effect of Regulatory Harmonization on Cross‐Border Labor

Migration: Evidence from the Accounting Profession. Journal of Accounting

Research. 55(1). pp.35-78.

Busco, C. and Quattrone, P., 2018. Performing business and social innovation through

accounting inscriptions: An introduction. Accounting, Organizations and Society.

Constable, P. and Kuasirikun, N., 2018. Gifting, Exchange and Reciprocity in Thai Annual

Reports: Towards a Buddhist Relational Theory of Thai Accounting Practice. Critical

Perspectives On Accounting.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Dudin, M. N. and et.al, 2015. International Practice of Generation of the National Budget Income

on the Basis of the Generally Accepted Financial Reporting Standards (IFRS).

Goh, B. W., Li, D., Ng, J. and Yong, K. O., 2015. Market pricing of banks’ fair value assets

reported under SFAS 157 since the 2008 financial crisis. Journal of Accounting and Public

Policy.34(2). pp.129-145.

44

Books and Journals

Adalı, S. and Kızıl, C., 2017. A Research on the Responsibility of Accounting Professionals to

Determine and Prevent Accounting Errors and Frauds: Edirne Sample. EMAJ: Emerging

Markets Journal. 7(1). pp.53-64.

Beaumont, S. J., 2015. An investigation of the short‐and long‐run relations between executive

cash bonus payments and firm financial performance: a pitch. Accounting & Finance.

55(2). pp.337-343.

Bloomfield and et.al, 2017. The Effect of Regulatory Harmonization on Cross‐Border Labor

Migration: Evidence from the Accounting Profession. Journal of Accounting

Research. 55(1). pp.35-78.

Busco, C. and Quattrone, P., 2018. Performing business and social innovation through

accounting inscriptions: An introduction. Accounting, Organizations and Society.

Constable, P. and Kuasirikun, N., 2018. Gifting, Exchange and Reciprocity in Thai Annual

Reports: Towards a Buddhist Relational Theory of Thai Accounting Practice. Critical

Perspectives On Accounting.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Dudin, M. N. and et.al, 2015. International Practice of Generation of the National Budget Income

on the Basis of the Generally Accepted Financial Reporting Standards (IFRS).

Goh, B. W., Li, D., Ng, J. and Yong, K. O., 2015. Market pricing of banks’ fair value assets

reported under SFAS 157 since the 2008 financial crisis. Journal of Accounting and Public

Policy.34(2). pp.129-145.

44

1 out of 47

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.