Financial Accounting INTRODUCTION 1 (A.)

Added on 2020-06-03

24 Pages4530 Words345 Views

Financial accounting

Table of Contents

INTRODUCTION...........................................................................................................................1

(A). (i) Definition of financial accounting...................................................................................1

(A.) (ii) Explaining key regulations associated with financial accounting..................................1

(A). (iii) Presenting accounting rules and principles...................................................................2

(A). (iv) Consistency and material disclosure concepts...............................................................3

CLIENT 1........................................................................................................................................3

(i). Prime entry books...................................................................................................................3

(ii). Double entry booking keeping..............................................................................................5

CLIENT 2........................................................................................................................................8

(A). Profit and loss account..........................................................................................................8

(B). Statement of financial position.............................................................................................9

CLIENT 3......................................................................................................................................10

(A). Profitability statement of Raintree Ltd...............................................................................10

(B). Statement of financial position of Raintree Ltd..................................................................11

(C). ‘Consistency’ and ‘Prudence’ concept...............................................................................12

(D). Purpose of depreciation and its methods............................................................................12

CLIENT 4......................................................................................................................................13

(A). Purpose of Bank Reconciliation Statement........................................................................13

(B). Reasons which may distinguish cash book (bank column) and pass book balance...........13

(C) (i). BRS on 1st December 2016............................................................................................13

(C). (ii) BRS on 31st Dec. 2016..................................................................................................14

(C). (iii) Corrected cash book....................................................................................................15

CLIENT 5......................................................................................................................................15

(A). (i) Sales Ledger Control Account.......................................................................................15

(A). (ii) Purchase Ledger Control Account................................................................................16

(B). Explaining ‘control Account’.............................................................................................16

CLIENT 6......................................................................................................................................17

(A). Suspense account; definition and main features.................................................................17

(B). Drafting a trial balance.......................................................................................................17

(C). Journal entries to rectify the entries....................................................................................18

(D). Differentiate between Suspense and Clearing Account.....................................................18

INTRODUCTION...........................................................................................................................1

(A). (i) Definition of financial accounting...................................................................................1

(A.) (ii) Explaining key regulations associated with financial accounting..................................1

(A). (iii) Presenting accounting rules and principles...................................................................2

(A). (iv) Consistency and material disclosure concepts...............................................................3

CLIENT 1........................................................................................................................................3

(i). Prime entry books...................................................................................................................3

(ii). Double entry booking keeping..............................................................................................5

CLIENT 2........................................................................................................................................8

(A). Profit and loss account..........................................................................................................8

(B). Statement of financial position.............................................................................................9

CLIENT 3......................................................................................................................................10

(A). Profitability statement of Raintree Ltd...............................................................................10

(B). Statement of financial position of Raintree Ltd..................................................................11

(C). ‘Consistency’ and ‘Prudence’ concept...............................................................................12

(D). Purpose of depreciation and its methods............................................................................12

CLIENT 4......................................................................................................................................13

(A). Purpose of Bank Reconciliation Statement........................................................................13

(B). Reasons which may distinguish cash book (bank column) and pass book balance...........13

(C) (i). BRS on 1st December 2016............................................................................................13

(C). (ii) BRS on 31st Dec. 2016..................................................................................................14

(C). (iii) Corrected cash book....................................................................................................15

CLIENT 5......................................................................................................................................15

(A). (i) Sales Ledger Control Account.......................................................................................15

(A). (ii) Purchase Ledger Control Account................................................................................16

(B). Explaining ‘control Account’.............................................................................................16

CLIENT 6......................................................................................................................................17

(A). Suspense account; definition and main features.................................................................17

(B). Drafting a trial balance.......................................................................................................17

(C). Journal entries to rectify the entries....................................................................................18

(D). Differentiate between Suspense and Clearing Account.....................................................18

INTRODUCTION

Business merchandises number of trading functions and activities, which needs to be

recorded properly in the financial accounts complying with the accounting principles, accounting

standards and financial reporting standards as well. The research paper here emphasizes upon

examining main regulations and standards that are necessary to follow to record financial

transactions. The report will also provide practical illustrations to prepare bank reconciliation,

profit and loss account, and statement of financial position, control accounts and rectifying

entries as well.

(A). (i) Definition of financial accounting

It is a specialized field or branch of accounting that track organization’s financial

activities and events of a given period. This is concerned about keeping proper record of an

entity’s financial transactions and activities that are the result of organization’s operations for a

given time period. All the financial results are summarized in key accounts including balance

sheet, profitability statement and cash flow statement (Elliott, 2017). The main objective of it is

to measure financial performance and profitability result of the establishment. Such annual

reports do not only helps in assessing business performance but also convey it to the external

stakeholders like shareholders, suppliers, lenders, tax authorities and others who use such reports

for making rational decisions. Company Act 2006 necessarily obligates every public as well as

private establishment to audit their accounts before its publication to ensure that each and every

information presented in the financial accounts are free from any material misstatement and valid

and true. All these accounts are constructed complying with the principles, such as consistency,

monetary measurement, accrual and other key concepts (Rajendran, 2017). Transactions are

recorded following double-entry book keeping system which state that every trading function has

dual impact on both debit and credit side. Income statement present details about revenue and

expenses. However, balance sheet showcase assets and liabilities whereas cash flow statement

only display transactions that either generated cash into the business or result in its outflow.

(A.) (ii) Explaining key regulations associated with financial accounting

Financial Reporting Council (FRC) is the key regulatory authority who make accounting

rules and regulations. UK GAAP are the domestic accounting principles that presents key

conventions and concepts that are needs to be adhere with in financial account preparation.

1 | P a g e

Business merchandises number of trading functions and activities, which needs to be

recorded properly in the financial accounts complying with the accounting principles, accounting

standards and financial reporting standards as well. The research paper here emphasizes upon

examining main regulations and standards that are necessary to follow to record financial

transactions. The report will also provide practical illustrations to prepare bank reconciliation,

profit and loss account, and statement of financial position, control accounts and rectifying

entries as well.

(A). (i) Definition of financial accounting

It is a specialized field or branch of accounting that track organization’s financial

activities and events of a given period. This is concerned about keeping proper record of an

entity’s financial transactions and activities that are the result of organization’s operations for a

given time period. All the financial results are summarized in key accounts including balance

sheet, profitability statement and cash flow statement (Elliott, 2017). The main objective of it is

to measure financial performance and profitability result of the establishment. Such annual

reports do not only helps in assessing business performance but also convey it to the external

stakeholders like shareholders, suppliers, lenders, tax authorities and others who use such reports

for making rational decisions. Company Act 2006 necessarily obligates every public as well as

private establishment to audit their accounts before its publication to ensure that each and every

information presented in the financial accounts are free from any material misstatement and valid

and true. All these accounts are constructed complying with the principles, such as consistency,

monetary measurement, accrual and other key concepts (Rajendran, 2017). Transactions are

recorded following double-entry book keeping system which state that every trading function has

dual impact on both debit and credit side. Income statement present details about revenue and

expenses. However, balance sheet showcase assets and liabilities whereas cash flow statement

only display transactions that either generated cash into the business or result in its outflow.

(A.) (ii) Explaining key regulations associated with financial accounting

Financial Reporting Council (FRC) is the key regulatory authority who make accounting

rules and regulations. UK GAAP are the domestic accounting principles that presents key

conventions and concepts that are needs to be adhere with in financial account preparation.

1 | P a g e

Initially, as companies were just operate domestically, thus, UK GAAP was sufficient. However,

with the globalization as companies started overseas operations (Weil, Schipper and Francis,

2013). It became necessary to promote harmonize reporting so that different companies financial

health can be easily compared by stakeholders for good decision-making. Now-a-days,

multinational organizations need to follow international accounting standards and international

financial reporting standards as well. Moreover, listed companies on the stock exchange need to

publish their statement to convey their audited statement to all the stakeholders. It made it easier

for the investors to easily compare company’s accounts operating in distinctive land of the world

and build trust among them.

(A). (iii) Presenting accounting rules and principles

Principles are the guidelines that is necessary to abide by accountant. Some of the

important concepts are prepared here as follows:

Accrual concept: As per this, transaction should be reported in the year when they

actually take place regardless their impact on cash. Thus, all the outstanding balance of the

current year will be display in current year’s income statement, however, prepaid income

received in the current year that is related to following year should be disclosed next year.

Matching principle: As said earlier, that transactions are recorded following double-

entry book keeping system, thus, according to this principle, spending must be match with the

income received.

Going concern: As name itself, it expects that the enterprise will run their operation for a

long-lasting period and it will not go into liquidation in near future (Pratt, 2013). This principle

enable corporations to defer their expenditures like depreciation is amortized over the life of the

asset.

Monetary principle: Money measurement concept tells that financial accounts display

only such information that can be measured monetarily. In other words, qualitative

characteristics that exits in non-numerical or non-statistical form cannot be incorporated in

accounts like staff productivity, consumer satisfaction and others

Full disclosure: As its name, it states that all the information should be disclosed in the

annual accounts, so that, interested stakeholder can get any information whenever needed.

2 | P a g e

with the globalization as companies started overseas operations (Weil, Schipper and Francis,

2013). It became necessary to promote harmonize reporting so that different companies financial

health can be easily compared by stakeholders for good decision-making. Now-a-days,

multinational organizations need to follow international accounting standards and international

financial reporting standards as well. Moreover, listed companies on the stock exchange need to

publish their statement to convey their audited statement to all the stakeholders. It made it easier

for the investors to easily compare company’s accounts operating in distinctive land of the world

and build trust among them.

(A). (iii) Presenting accounting rules and principles

Principles are the guidelines that is necessary to abide by accountant. Some of the

important concepts are prepared here as follows:

Accrual concept: As per this, transaction should be reported in the year when they

actually take place regardless their impact on cash. Thus, all the outstanding balance of the

current year will be display in current year’s income statement, however, prepaid income

received in the current year that is related to following year should be disclosed next year.

Matching principle: As said earlier, that transactions are recorded following double-

entry book keeping system, thus, according to this principle, spending must be match with the

income received.

Going concern: As name itself, it expects that the enterprise will run their operation for a

long-lasting period and it will not go into liquidation in near future (Pratt, 2013). This principle

enable corporations to defer their expenditures like depreciation is amortized over the life of the

asset.

Monetary principle: Money measurement concept tells that financial accounts display

only such information that can be measured monetarily. In other words, qualitative

characteristics that exits in non-numerical or non-statistical form cannot be incorporated in

accounts like staff productivity, consumer satisfaction and others

Full disclosure: As its name, it states that all the information should be disclosed in the

annual accounts, so that, interested stakeholder can get any information whenever needed.

2 | P a g e

Auditors also check it and give their opinion whether company had given full details or present

true and fair position or not (Henderson and et.al., 2015).

(A). (iv) Consistency and material disclosure concepts

Consistency and materiality are the two different type of accounting concepts which

every accountant need to comply with, while preparing accounts. Former states that once

adopted principle will be followed throughout entire business life, until and unless any change in

the method promote its financial reporting. Auditors check that whether company had followed

the same principle followed in last year or not, if no, then auditor verify that whether newly

adopted system help to improve its reporting or not. This principle is useful to maintain

comparability of the results over different financial years (Elliott, 2017). On the other side,

materiality disclosure is about disclosure of all the materialistic information in the financial

accounts. In other words, it can be said that organizations must not withhold any critical dataset

from owners, investors, lender, suppliers, regulators and other stakeholders. Financial accounts

of the firm should deliver full details to the intended audience and it must be free from any

material error, can be assured through unqualified report of auditor.

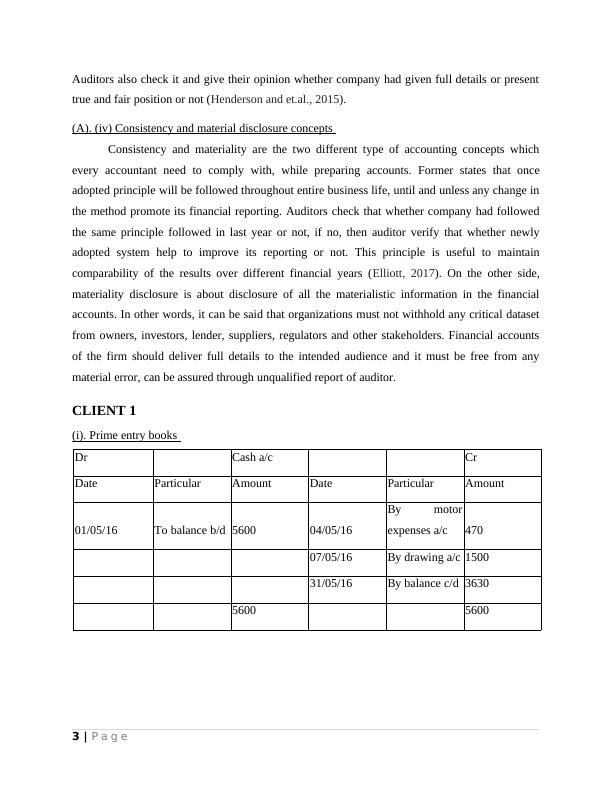

CLIENT 1

(i). Prime entry books

Dr Cash a/c Cr

Date Particular Amount Date Particular Amount

01/05/16 To balance b/d 5600 04/05/16

By motor

expenses a/c 470

07/05/16 By drawing a/c 1500

31/05/16 By balance c/d 3630

5600 5600

3 | P a g e

true and fair position or not (Henderson and et.al., 2015).

(A). (iv) Consistency and material disclosure concepts

Consistency and materiality are the two different type of accounting concepts which

every accountant need to comply with, while preparing accounts. Former states that once

adopted principle will be followed throughout entire business life, until and unless any change in

the method promote its financial reporting. Auditors check that whether company had followed

the same principle followed in last year or not, if no, then auditor verify that whether newly

adopted system help to improve its reporting or not. This principle is useful to maintain

comparability of the results over different financial years (Elliott, 2017). On the other side,

materiality disclosure is about disclosure of all the materialistic information in the financial

accounts. In other words, it can be said that organizations must not withhold any critical dataset

from owners, investors, lender, suppliers, regulators and other stakeholders. Financial accounts

of the firm should deliver full details to the intended audience and it must be free from any

material error, can be assured through unqualified report of auditor.

CLIENT 1

(i). Prime entry books

Dr Cash a/c Cr

Date Particular Amount Date Particular Amount

01/05/16 To balance b/d 5600 04/05/16

By motor

expenses a/c 470

07/05/16 By drawing a/c 1500

31/05/16 By balance c/d 3630

5600 5600

3 | P a g e

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Accounting Principles Assignment Solvedlg...

|37

|6580

|173

Financial Accounting Assignment Reportlg...

|20

|5085

|52

Financial Accounting: Assignment Samplelg...

|37

|5577

|390

Report on Accounting Conventions and Principleslg...

|34

|3968

|114

FINANCIAL ACCOUNTING INTRODUCTION 1lg...

|31

|2925

|245

Assignment on Financial Accounting pdflg...

|47

|5713

|177