ACC514 Financial Accounting Assignment Solution, 2019

VerifiedAdded on 2023/01/04

|14

|464

|45

Homework Assignment

AI Summary

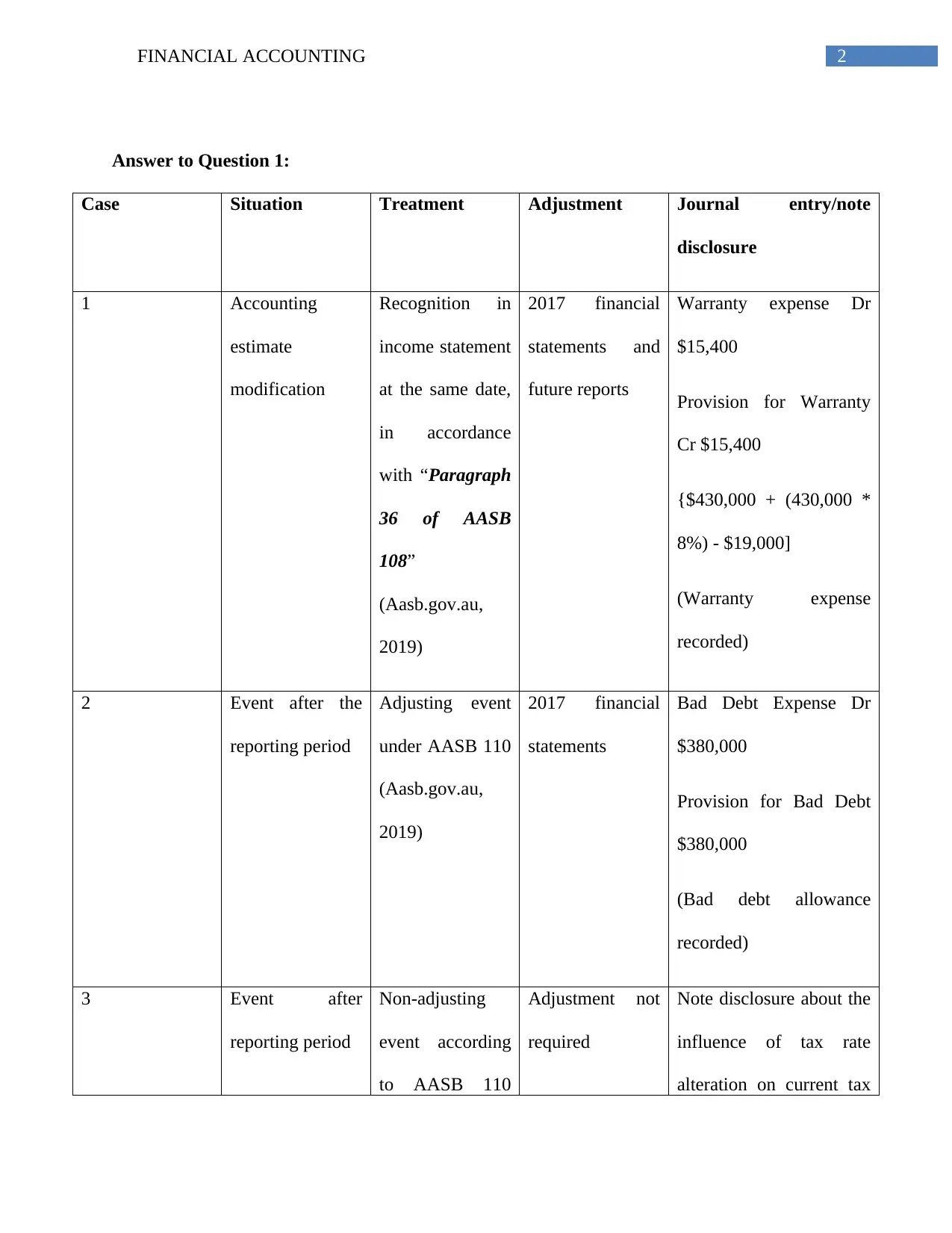

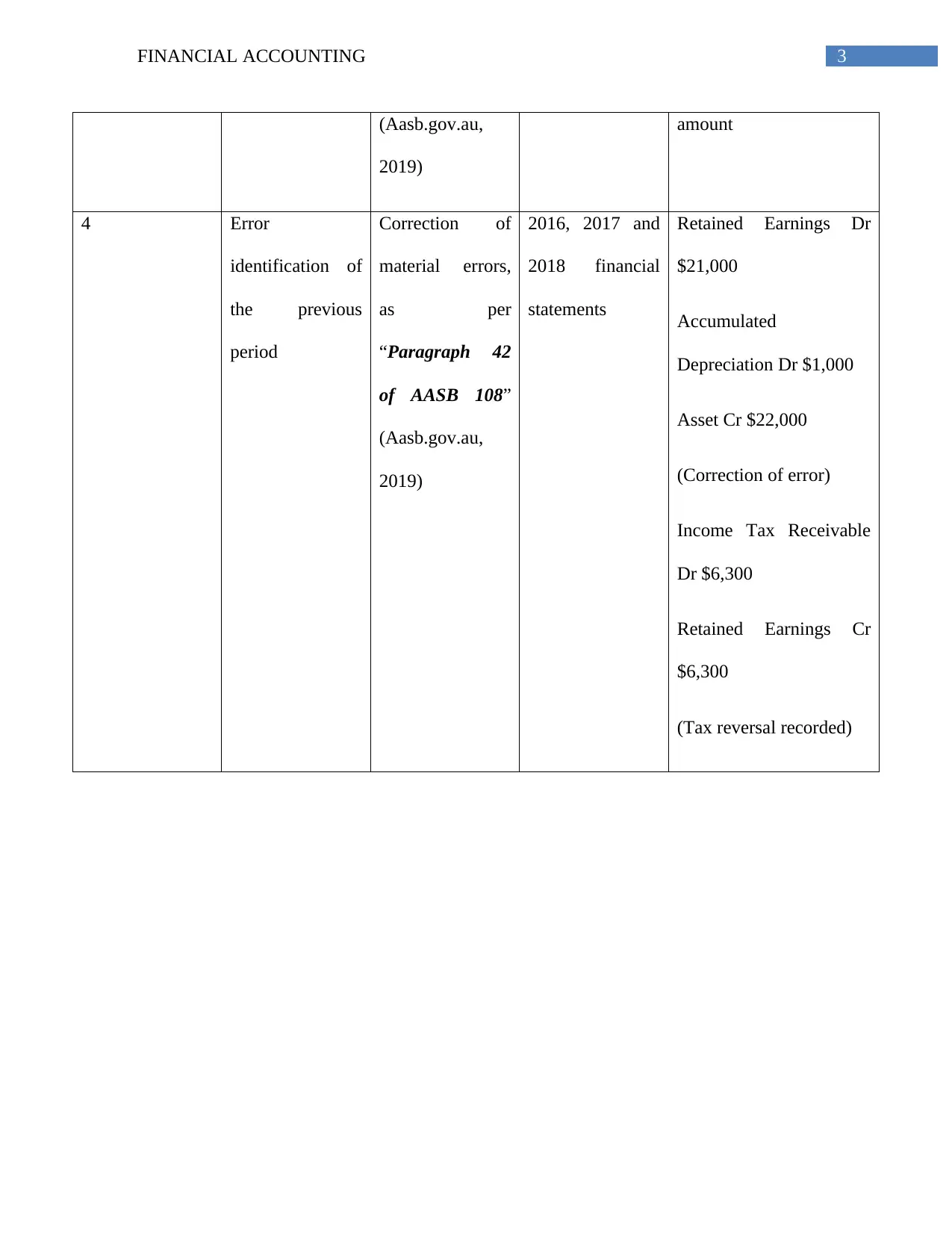

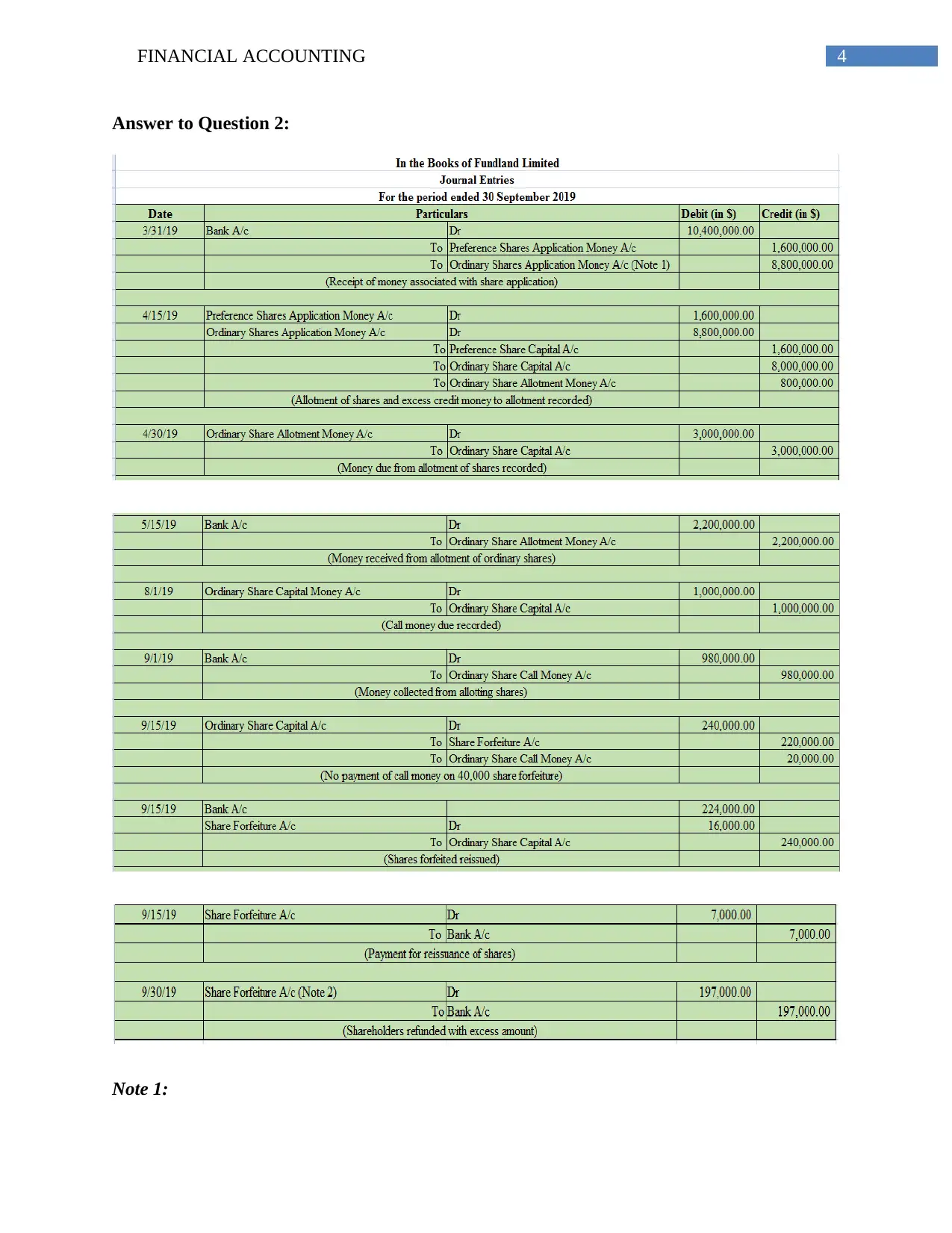

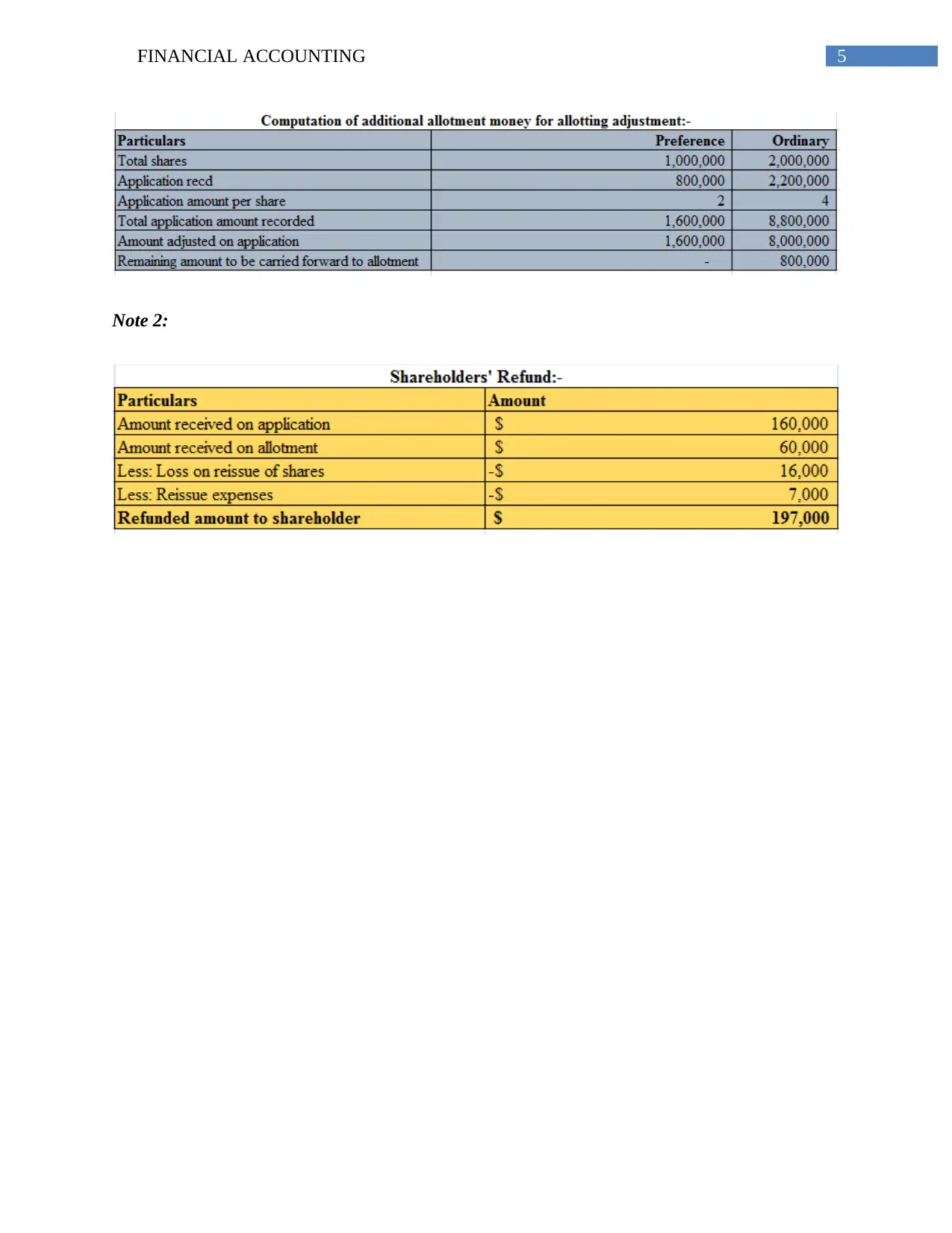

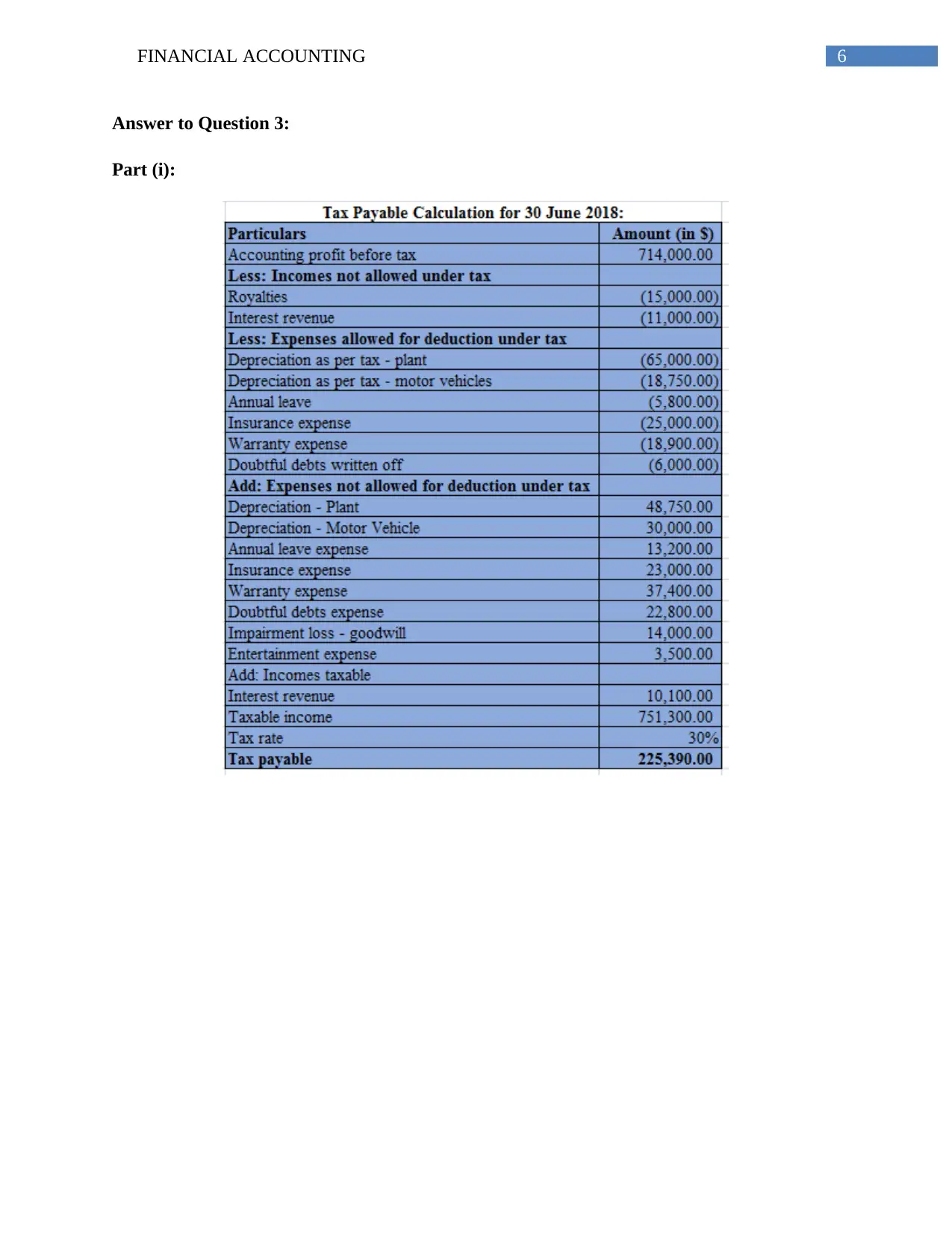

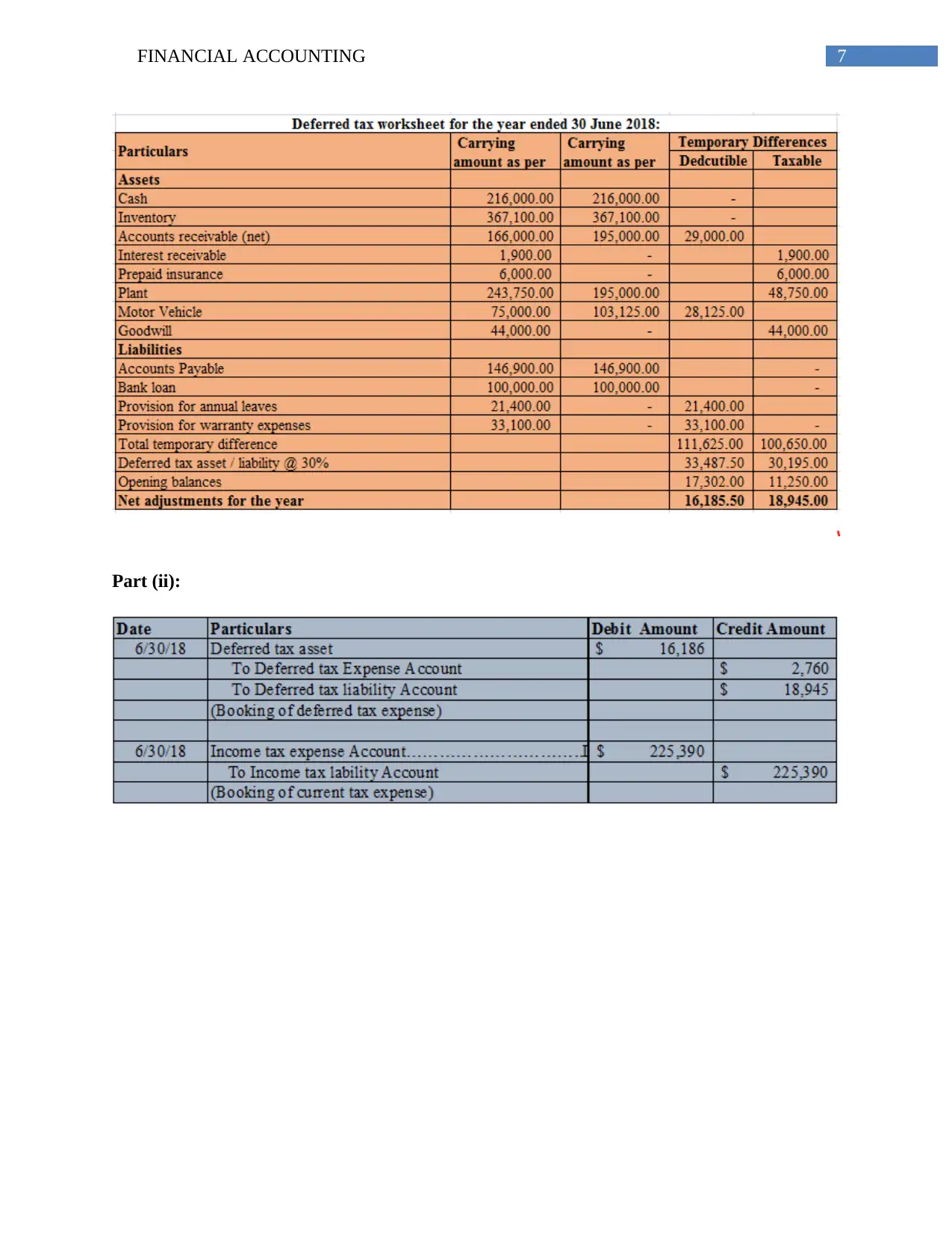

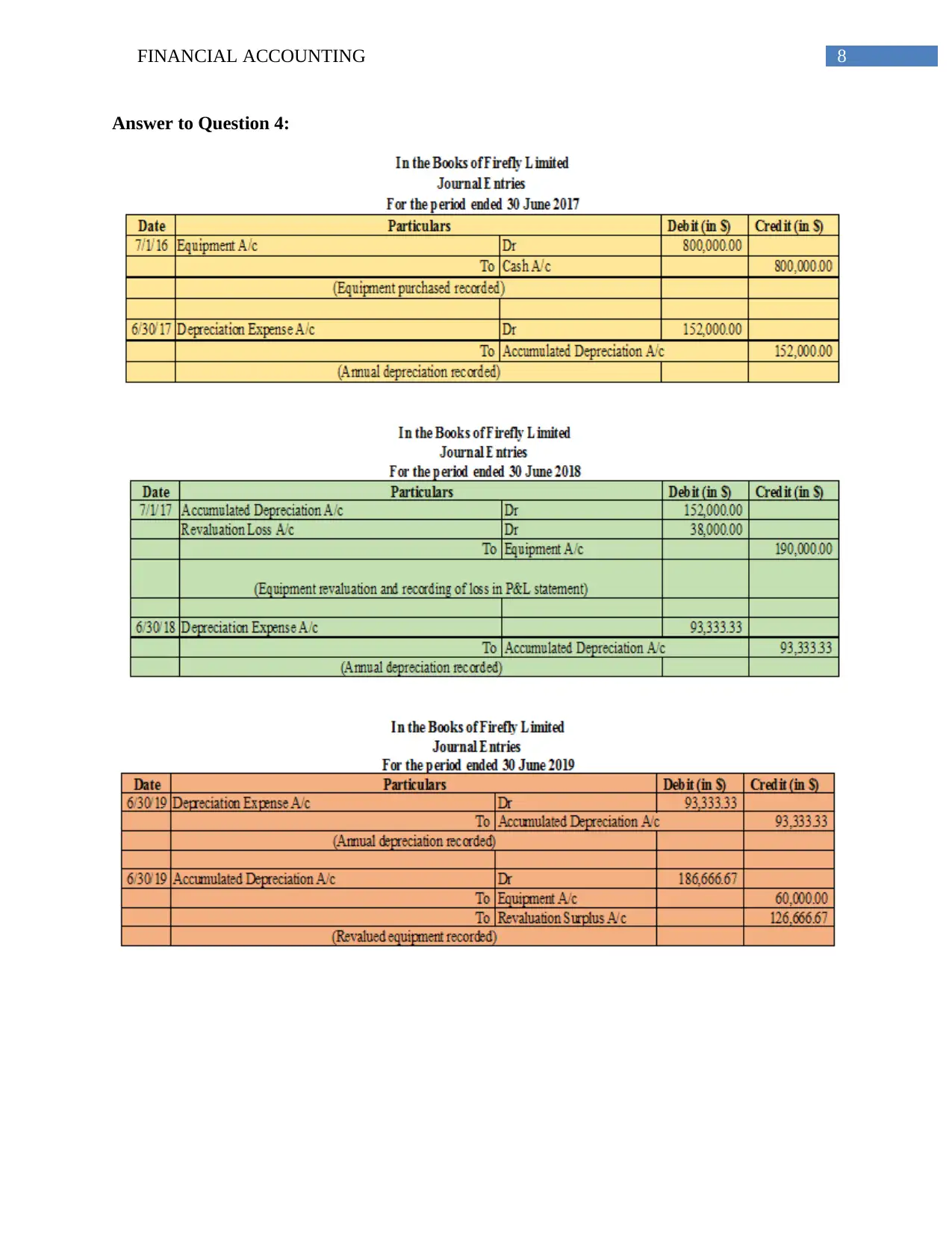

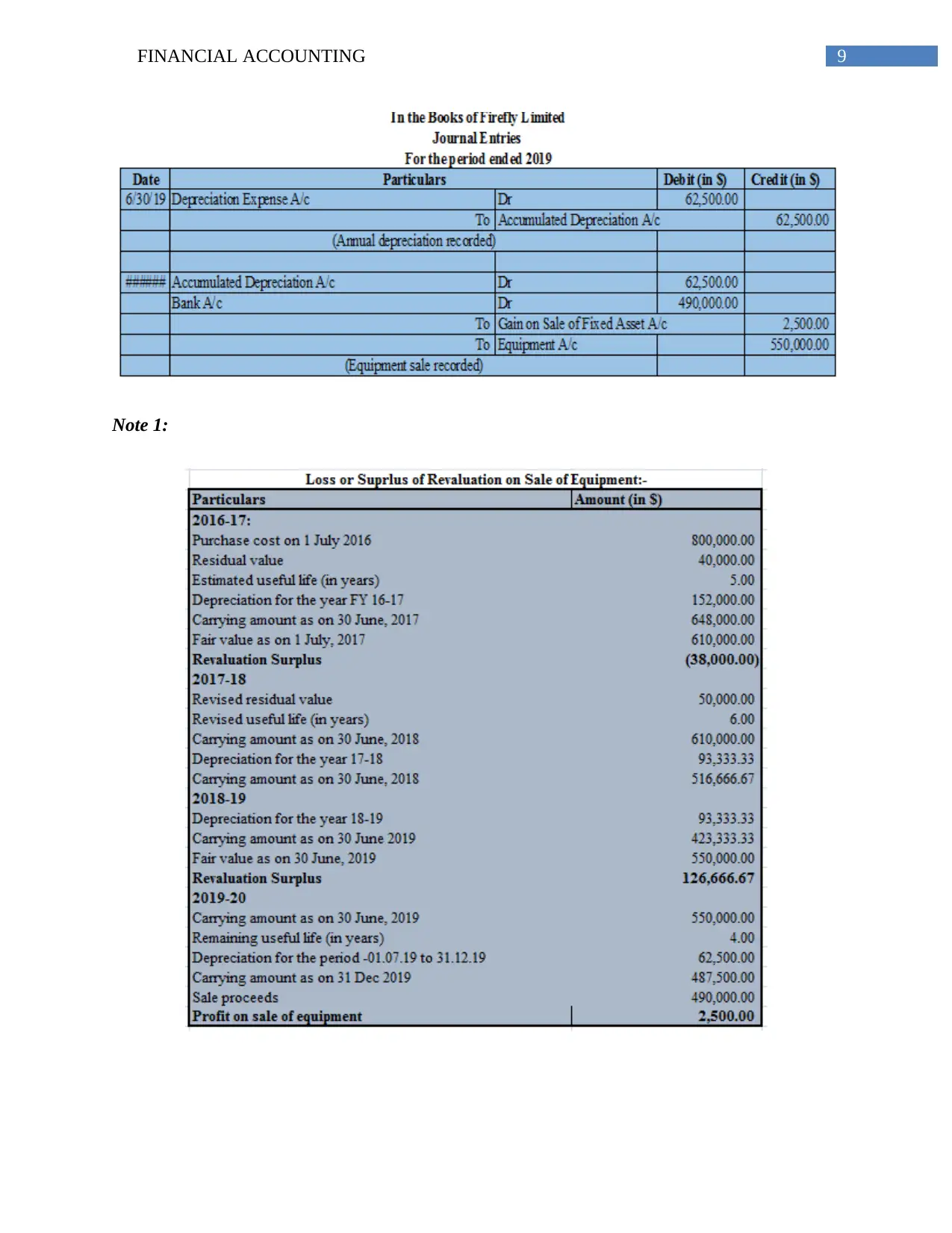

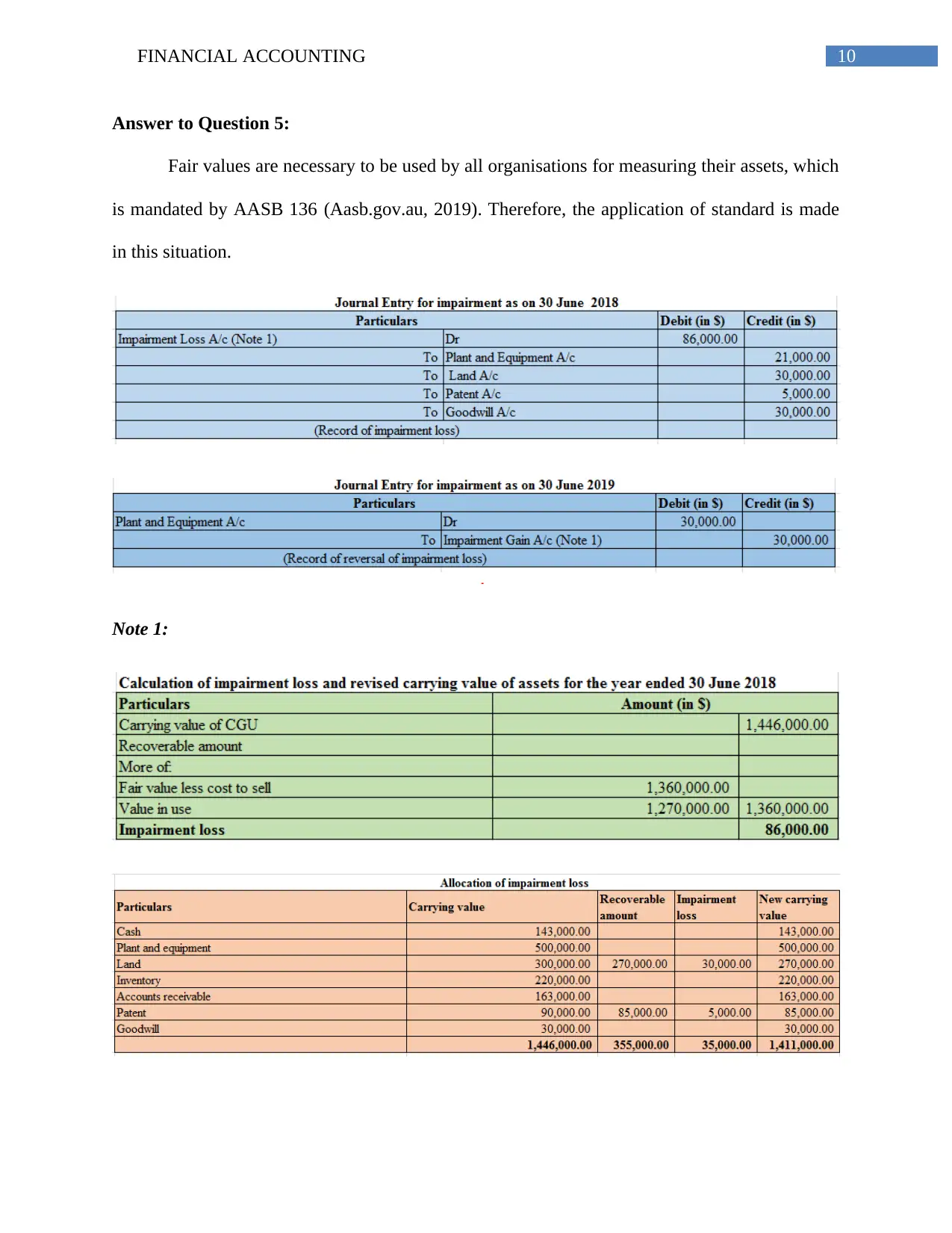

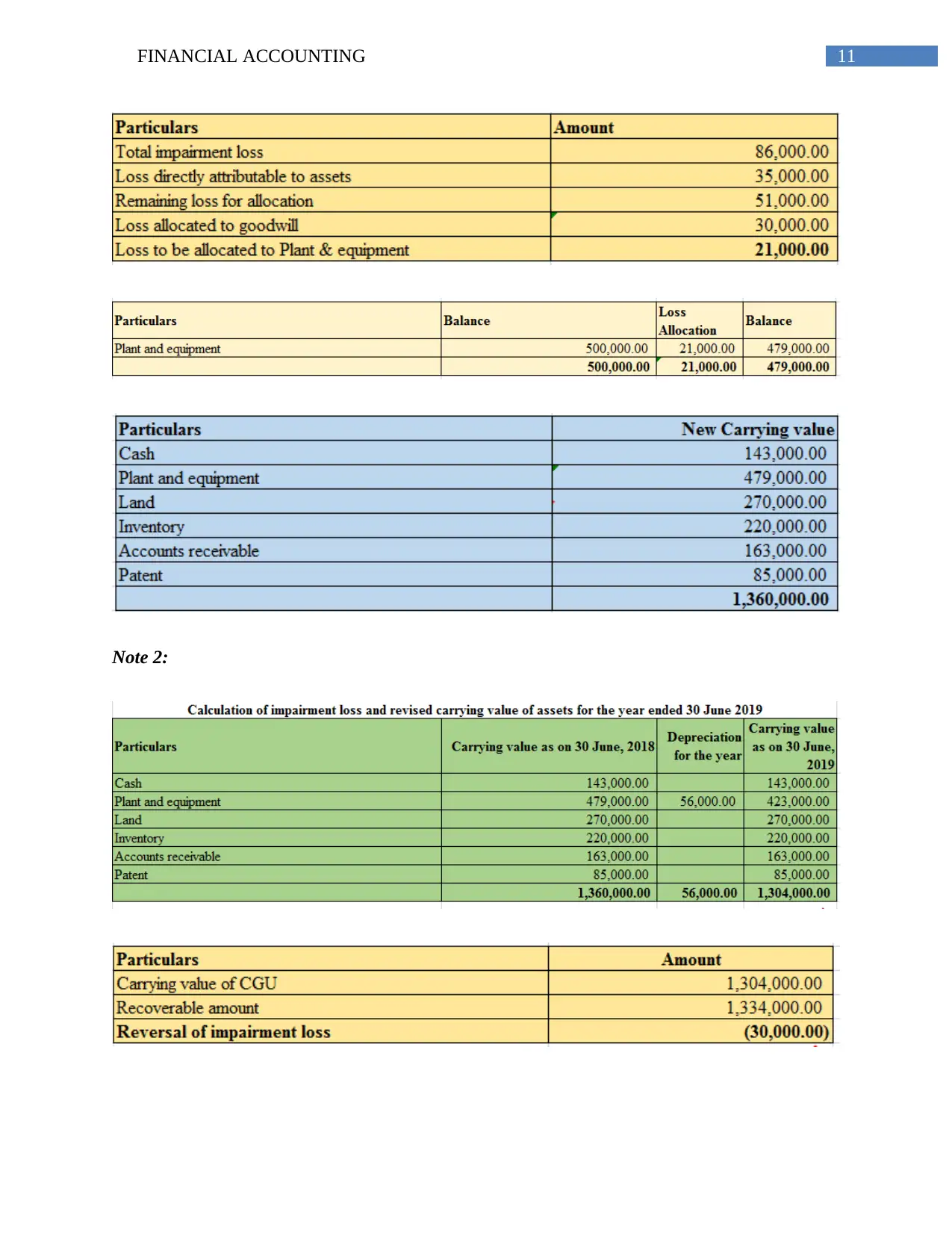

This document provides a comprehensive solution to a financial accounting assignment (ACC514) focusing on financial statement disclosures. The assignment addresses several scenarios, including warranty provisions, bad debt, and error corrections, all analyzed under relevant AASB standards. The solution includes journal entries, note disclosures, and explanations for each situation, demonstrating the application of accounting principles to real-world financial reporting problems. The document covers topics such as accounting recognition, adjusting events, and error correction, offering a detailed breakdown of the financial impact and appropriate accounting treatments. Furthermore, the solution refers to specific AASB standards, such as AASB 108, AASB 110, and AASB 136, to ensure accuracy and compliance. The assignment covers the preparation of financial statements and includes analysis of fair values and their application within the organization.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.