Financial Accounting - Taj Accountants

VerifiedAdded on 2021/02/21

|34

|5329

|41

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Part A...............................................................................................................................................1

1. Financial accounting and its purpose.......................................................................................1

2. External and internal stakeholders of large organization.........................................................3

PART B............................................................................................................................................5

CLIENT 1........................................................................................................................................5

CLIENT 2........................................................................................................................................5

c). Consistency and Prudence......................................................................................................5

d) Purpose of depreciation in financial statement........................................................................6

e)Difference between financial statements of sole trader and limited company........................7

CLIENT 3........................................................................................................................................8

A) Purpose of preparing Bank Reconciliation Statement ...........................................................8

B) Listing the areas that vary the record of bank and cash book................................................9

C) Imprest in petty cash system.................................................................................................10

CLIENT 4......................................................................................................................................10

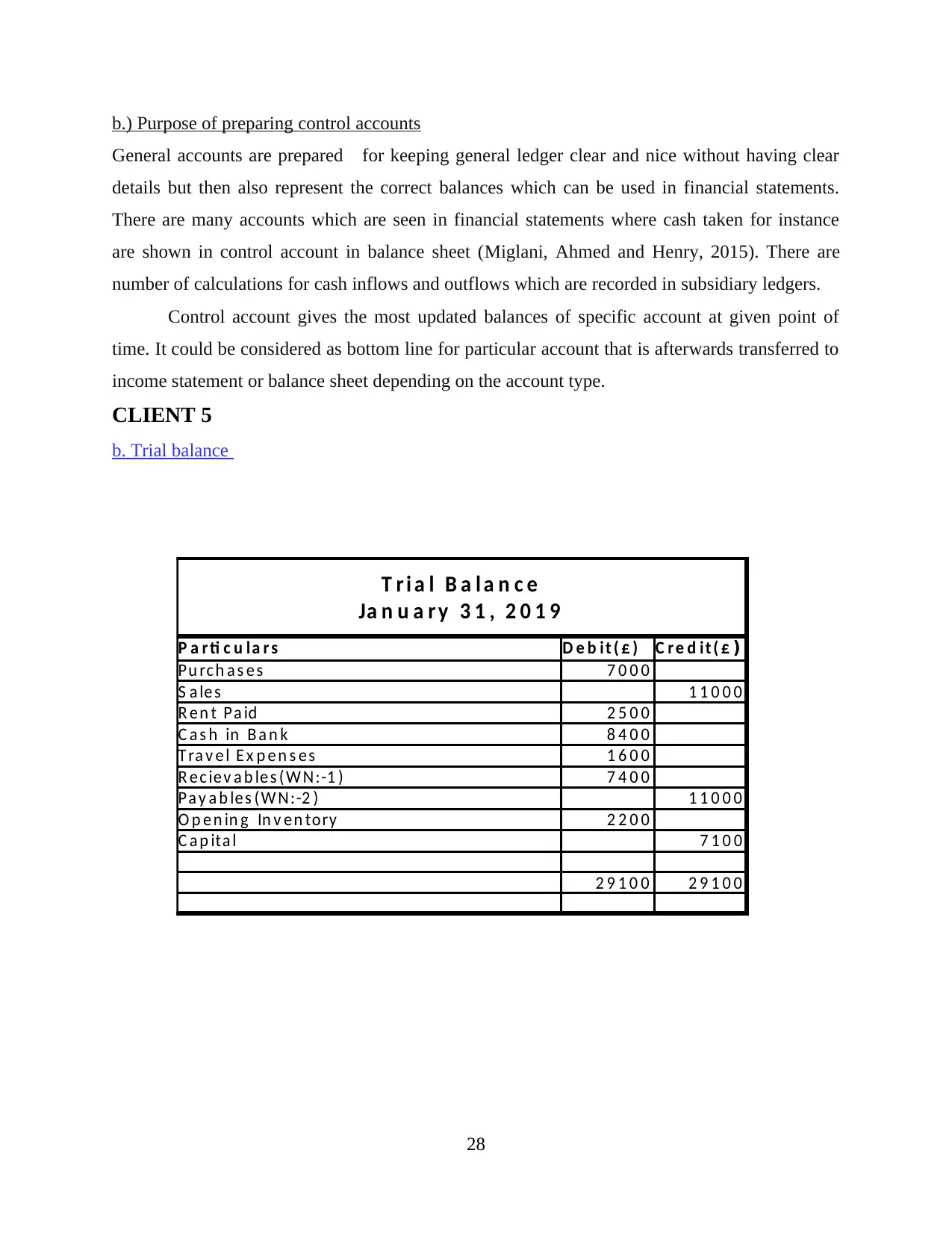

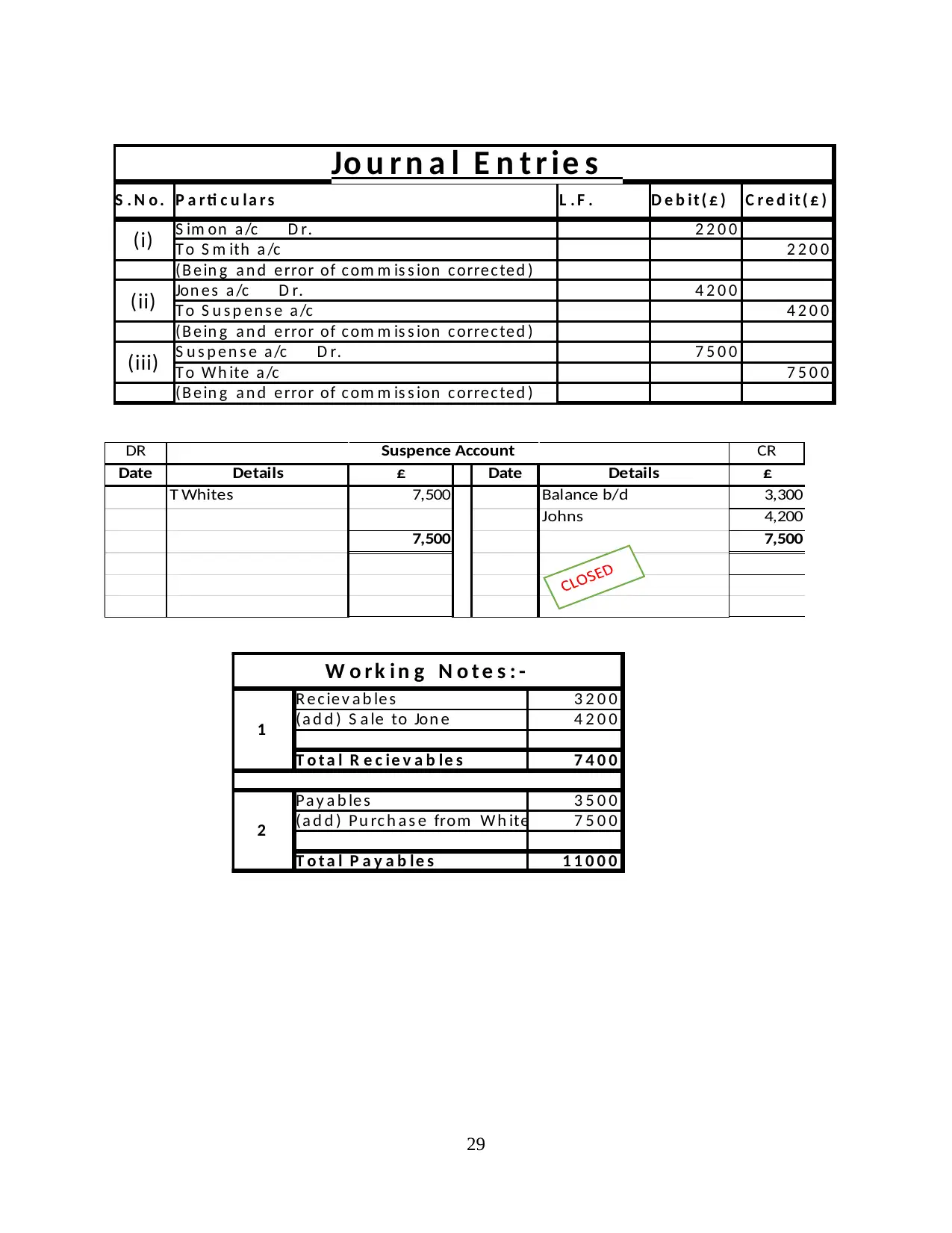

b.) Purpose of preparing control accounts.................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

Part A...............................................................................................................................................1

1. Financial accounting and its purpose.......................................................................................1

2. External and internal stakeholders of large organization.........................................................3

PART B............................................................................................................................................5

CLIENT 1........................................................................................................................................5

CLIENT 2........................................................................................................................................5

c). Consistency and Prudence......................................................................................................5

d) Purpose of depreciation in financial statement........................................................................6

e)Difference between financial statements of sole trader and limited company........................7

CLIENT 3........................................................................................................................................8

A) Purpose of preparing Bank Reconciliation Statement ...........................................................8

B) Listing the areas that vary the record of bank and cash book................................................9

C) Imprest in petty cash system.................................................................................................10

CLIENT 4......................................................................................................................................10

b.) Purpose of preparing control accounts.................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial accounting is one the most specialized branch of accounting which helps in

keeping complete track of various financial transactions. Such transactions are recorded by

effectively using standard guidelines in order to record, summarize and present transactions in

financial statements in a systematic and reliable manner.

This study will highlight on the key purpose of financial accounting. It will also

demonstrate internal and external stakeholders of the company and examine why they are

interested in the various financial statements of the organization. This study will record various

business transactions with the help of double entry book keeping and will also extract a trial

balance. Final accounts will be prepared for partnership, limited company and sole traders in

compliance with appropriate standards, conventions and principles. Furthermore, this study will

perform bank reconciliation system in order to ensure that the bank and company records are

correct. It will also reconcile control account and identify correct accounts for specific

transactions recorded in suspense account.

Taj Accountants is a small accountancy firm based in London, United Kingdom. It offers

one stop solution to customers regarding tax, business planning, accounts, payroll, bookkeeping,

advisory services to partnership, sole traders and limited company.

Part A

1. Financial accounting and its purpose.

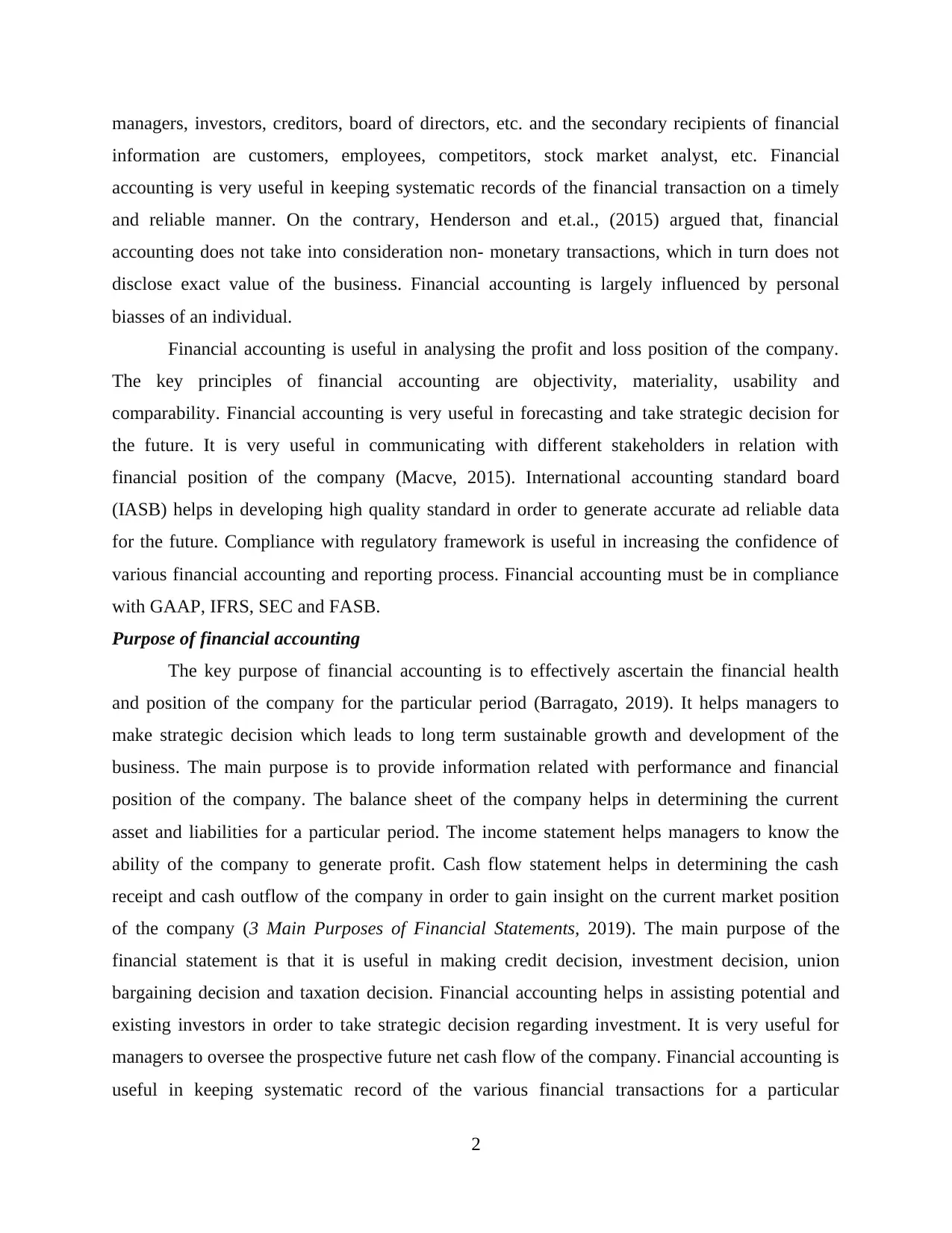

Schroeder, Clark and Cathey (2019) sought to establish the fact that, financial accounting

is one the most specialized branch of accounting which helps in keeping complete track of

various financial transactions. Financial accounting is useful in capturing the company's financial

position for the particular accounting period. Financial accounting is carried out by effectively

complying with various accounting standards, conventions and principles. Financial accounting

mainly generates four main financial statements which mainly includes income statement,

balance sheet, owner's equity statement and cash flow statement. Financial transactions are

recorded by effectively using standard guidelines in order to record, summarize and present

transactions in financial statements in a systematic and reliable manner. Furthermore, such

financial statements are useful for stakeholders in order to extract useful information and make

strategic decision (Financial Accounting – Introduction, Accounting Concepts, Preparation and

Presentation of Financial Statements, 2018). The primary recipients of financial statements are

1

Financial accounting is one the most specialized branch of accounting which helps in

keeping complete track of various financial transactions. Such transactions are recorded by

effectively using standard guidelines in order to record, summarize and present transactions in

financial statements in a systematic and reliable manner.

This study will highlight on the key purpose of financial accounting. It will also

demonstrate internal and external stakeholders of the company and examine why they are

interested in the various financial statements of the organization. This study will record various

business transactions with the help of double entry book keeping and will also extract a trial

balance. Final accounts will be prepared for partnership, limited company and sole traders in

compliance with appropriate standards, conventions and principles. Furthermore, this study will

perform bank reconciliation system in order to ensure that the bank and company records are

correct. It will also reconcile control account and identify correct accounts for specific

transactions recorded in suspense account.

Taj Accountants is a small accountancy firm based in London, United Kingdom. It offers

one stop solution to customers regarding tax, business planning, accounts, payroll, bookkeeping,

advisory services to partnership, sole traders and limited company.

Part A

1. Financial accounting and its purpose.

Schroeder, Clark and Cathey (2019) sought to establish the fact that, financial accounting

is one the most specialized branch of accounting which helps in keeping complete track of

various financial transactions. Financial accounting is useful in capturing the company's financial

position for the particular accounting period. Financial accounting is carried out by effectively

complying with various accounting standards, conventions and principles. Financial accounting

mainly generates four main financial statements which mainly includes income statement,

balance sheet, owner's equity statement and cash flow statement. Financial transactions are

recorded by effectively using standard guidelines in order to record, summarize and present

transactions in financial statements in a systematic and reliable manner. Furthermore, such

financial statements are useful for stakeholders in order to extract useful information and make

strategic decision (Financial Accounting – Introduction, Accounting Concepts, Preparation and

Presentation of Financial Statements, 2018). The primary recipients of financial statements are

1

managers, investors, creditors, board of directors, etc. and the secondary recipients of financial

information are customers, employees, competitors, stock market analyst, etc. Financial

accounting is very useful in keeping systematic records of the financial transaction on a timely

and reliable manner. On the contrary, Henderson and et.al., (2015) argued that, financial

accounting does not take into consideration non- monetary transactions, which in turn does not

disclose exact value of the business. Financial accounting is largely influenced by personal

biasses of an individual.

Financial accounting is useful in analysing the profit and loss position of the company.

The key principles of financial accounting are objectivity, materiality, usability and

comparability. Financial accounting is very useful in forecasting and take strategic decision for

the future. It is very useful in communicating with different stakeholders in relation with

financial position of the company (Macve, 2015). International accounting standard board

(IASB) helps in developing high quality standard in order to generate accurate ad reliable data

for the future. Compliance with regulatory framework is useful in increasing the confidence of

various financial accounting and reporting process. Financial accounting must be in compliance

with GAAP, IFRS, SEC and FASB.

Purpose of financial accounting

The key purpose of financial accounting is to effectively ascertain the financial health

and position of the company for the particular period (Barragato, 2019). It helps managers to

make strategic decision which leads to long term sustainable growth and development of the

business. The main purpose is to provide information related with performance and financial

position of the company. The balance sheet of the company helps in determining the current

asset and liabilities for a particular period. The income statement helps managers to know the

ability of the company to generate profit. Cash flow statement helps in determining the cash

receipt and cash outflow of the company in order to gain insight on the current market position

of the company (3 Main Purposes of Financial Statements, 2019). The main purpose of the

financial statement is that it is useful in making credit decision, investment decision, union

bargaining decision and taxation decision. Financial accounting helps in assisting potential and

existing investors in order to take strategic decision regarding investment. It is very useful for

managers to oversee the prospective future net cash flow of the company. Financial accounting is

useful in keeping systematic record of the various financial transactions for a particular

2

information are customers, employees, competitors, stock market analyst, etc. Financial

accounting is very useful in keeping systematic records of the financial transaction on a timely

and reliable manner. On the contrary, Henderson and et.al., (2015) argued that, financial

accounting does not take into consideration non- monetary transactions, which in turn does not

disclose exact value of the business. Financial accounting is largely influenced by personal

biasses of an individual.

Financial accounting is useful in analysing the profit and loss position of the company.

The key principles of financial accounting are objectivity, materiality, usability and

comparability. Financial accounting is very useful in forecasting and take strategic decision for

the future. It is very useful in communicating with different stakeholders in relation with

financial position of the company (Macve, 2015). International accounting standard board

(IASB) helps in developing high quality standard in order to generate accurate ad reliable data

for the future. Compliance with regulatory framework is useful in increasing the confidence of

various financial accounting and reporting process. Financial accounting must be in compliance

with GAAP, IFRS, SEC and FASB.

Purpose of financial accounting

The key purpose of financial accounting is to effectively ascertain the financial health

and position of the company for the particular period (Barragato, 2019). It helps managers to

make strategic decision which leads to long term sustainable growth and development of the

business. The main purpose is to provide information related with performance and financial

position of the company. The balance sheet of the company helps in determining the current

asset and liabilities for a particular period. The income statement helps managers to know the

ability of the company to generate profit. Cash flow statement helps in determining the cash

receipt and cash outflow of the company in order to gain insight on the current market position

of the company (3 Main Purposes of Financial Statements, 2019). The main purpose of the

financial statement is that it is useful in making credit decision, investment decision, union

bargaining decision and taxation decision. Financial accounting helps in assisting potential and

existing investors in order to take strategic decision regarding investment. It is very useful for

managers to oversee the prospective future net cash flow of the company. Financial accounting is

useful in keeping systematic record of the various financial transactions for a particular

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

accounting period. It is very useful in determining the best performing sector of the company. It

is very useful in controlling the cost of the company by attaining economies of scale (Tassadaq

and Malik, 2015). The key purpose of financial accounting is to provide timely information to

the stakeholders of the company in order to make strategic decision. It is very useful in allocating

the resources and results in determining the cash flow, operational efficiency and financial

position of the company.

2. External and internal stakeholders of large organization.

Internal stakeholders

Internal stakeholders i.e., employees, managers and owners of the company are directly

related with the organization (Nilsson and Stockenstrand, 2015). They are the people who are

serving the organization and gets directly influenced by the performance of the company.

Internal stakeholders focus on making strategic decision which in turn results in long term

sustainable growth and development of the business.

Managers

They are interested in the financial statements of the company because it focuses on

managing the various affairs of the company by ascertaining the financial position and

performance of the organisation. They focus on ascertaining the most profitable unit of the

company and also helps in determining the factors which leads to higher cost and expenses.

Financial statements helps managers in taking strategic decision which leads to higher

profitability and attainment of economies of scale. It helps managers in assessing and evaluating

the liquidity, operational efficiency and profitability of the business (HASLAM and et.al., 2015).

The managers set the benchmarking standards and strategy which helps in identifying areas of

competence and attain greater heights and growth in future. It also helps in managing various

risk factors which in turn results in smooth functioning of the business.

Employees

Employees assess the financial statements of the company because it will help them in

evaluating the future growth prospect of an individual upon the growth, performance and

financial position of the company. It helps in ascertaining he job security and future

remuneration of an individual. Financial statements helps employees in assessing the financial

stability of the company. Of the company is performing better, then there are higher chances of

career growth and opportunities for the employees of the organization. In case the profit of the

3

is very useful in controlling the cost of the company by attaining economies of scale (Tassadaq

and Malik, 2015). The key purpose of financial accounting is to provide timely information to

the stakeholders of the company in order to make strategic decision. It is very useful in allocating

the resources and results in determining the cash flow, operational efficiency and financial

position of the company.

2. External and internal stakeholders of large organization.

Internal stakeholders

Internal stakeholders i.e., employees, managers and owners of the company are directly

related with the organization (Nilsson and Stockenstrand, 2015). They are the people who are

serving the organization and gets directly influenced by the performance of the company.

Internal stakeholders focus on making strategic decision which in turn results in long term

sustainable growth and development of the business.

Managers

They are interested in the financial statements of the company because it focuses on

managing the various affairs of the company by ascertaining the financial position and

performance of the organisation. They focus on ascertaining the most profitable unit of the

company and also helps in determining the factors which leads to higher cost and expenses.

Financial statements helps managers in taking strategic decision which leads to higher

profitability and attainment of economies of scale. It helps managers in assessing and evaluating

the liquidity, operational efficiency and profitability of the business (HASLAM and et.al., 2015).

The managers set the benchmarking standards and strategy which helps in identifying areas of

competence and attain greater heights and growth in future. It also helps in managing various

risk factors which in turn results in smooth functioning of the business.

Employees

Employees assess the financial statements of the company because it will help them in

evaluating the future growth prospect of an individual upon the growth, performance and

financial position of the company. It helps in ascertaining he job security and future

remuneration of an individual. Financial statements helps employees in assessing the financial

stability of the company. Of the company is performing better, then there are higher chances of

career growth and opportunities for the employees of the organization. In case the profit of the

3

company are low and are no future prospect for growth, then employees will quit that job and

will not further invest any money and time in that organization (Chalmers, Hay and Khlif, 2019).

External stakeholders

It refers to the people that are working outside the organisation and are affected by the

actions and decisions of the company. There are various types of external stakeholders such as

customers that buy products or services of the firm, creditors from whom organisation owes

money, suppliers of raw materials etc. (Vracheva, Judge and Madden, 2016). External

stakeholders of Taj Accountants that may be interested in receiving financial information

regarding operations of the company are as follows -

Government :

Government bodies such as tax authorities etc. are interested in getting financial

information of the firm for the purpose of determining that whether the organisation is

complying all the regulatory requirements and for the purpose of determining tax liability of the

business. Tax is calculated on the basis of profits generated by the firm (Diouf and Boiral, 2017).

Therefore, financial information related with the operations of Taj Accountants will help the

Government to calculate the amount of tax to be paid by the firm. Further, financial information

will also help the authorities to determine whether company is charging fair rate for offering the

services to the customers.

Lenders and creditors :

Creditor is an institution or individual that provides permission to another entity to

borrow money which is to repaid by the firm in the future. Creditors charges interest on the

amount provided to another entity in the form of loan. Lenders will require financial information

of Taj Accountants to determine credit worthiness of the firm. On the basis of financial position

of the company, lenders and creditors offer credit facilities. If, the financial position of the firm

is good it will indicate that company is able to pay outstanding amount on time. In case liquidity

position of firm is poor it will indicate that company does not have sufficient assets to pay

liabilities back on time (Martin and Moser, 2016).

Customers :

It refers to the individual or firm that purchase product or service of the business. If, there

is long term involvement between Taj Accountants and its customers then, clients will be

interested to determine company's ability to maintain stability in the operations. Further,

4

will not further invest any money and time in that organization (Chalmers, Hay and Khlif, 2019).

External stakeholders

It refers to the people that are working outside the organisation and are affected by the

actions and decisions of the company. There are various types of external stakeholders such as

customers that buy products or services of the firm, creditors from whom organisation owes

money, suppliers of raw materials etc. (Vracheva, Judge and Madden, 2016). External

stakeholders of Taj Accountants that may be interested in receiving financial information

regarding operations of the company are as follows -

Government :

Government bodies such as tax authorities etc. are interested in getting financial

information of the firm for the purpose of determining that whether the organisation is

complying all the regulatory requirements and for the purpose of determining tax liability of the

business. Tax is calculated on the basis of profits generated by the firm (Diouf and Boiral, 2017).

Therefore, financial information related with the operations of Taj Accountants will help the

Government to calculate the amount of tax to be paid by the firm. Further, financial information

will also help the authorities to determine whether company is charging fair rate for offering the

services to the customers.

Lenders and creditors :

Creditor is an institution or individual that provides permission to another entity to

borrow money which is to repaid by the firm in the future. Creditors charges interest on the

amount provided to another entity in the form of loan. Lenders will require financial information

of Taj Accountants to determine credit worthiness of the firm. On the basis of financial position

of the company, lenders and creditors offer credit facilities. If, the financial position of the firm

is good it will indicate that company is able to pay outstanding amount on time. In case liquidity

position of firm is poor it will indicate that company does not have sufficient assets to pay

liabilities back on time (Martin and Moser, 2016).

Customers :

It refers to the individual or firm that purchase product or service of the business. If, there

is long term involvement between Taj Accountants and its customers then, clients will be

interested to determine company's ability to maintain stability in the operations. Further,

4

financial information will help clients of Taj Accountants to ensure whether company will be

able to continue its existence in the future or not. Moreover, financial statements will help

customers to determine that whether firm is providing services at fair rate or not.

Investors :

It refers to the individual or firm that commits funds in the business in the expectation of

getting better financial returns from the company. Financial information regarding operations of

Taj Accountants will help potential investors to determine the viability of investing funds in the

company. Financial statements like profit and loss statement help to forecast dividend that will

be paid by the firm in the future. Further, financial information will also assist the investors of

Taj Accountants to analyse the risk associated with investing funds in the organisation. For

example -If there is more fluctuations in the profit of firm it will indicate that there is high risk

in investing capital in organisation (Diouf and Boiral, 2017).

PART B

CLIENT 1

1. Recording and classification of the journal entries

5

able to continue its existence in the future or not. Moreover, financial statements will help

customers to determine that whether firm is providing services at fair rate or not.

Investors :

It refers to the individual or firm that commits funds in the business in the expectation of

getting better financial returns from the company. Financial information regarding operations of

Taj Accountants will help potential investors to determine the viability of investing funds in the

company. Financial statements like profit and loss statement help to forecast dividend that will

be paid by the firm in the future. Further, financial information will also assist the investors of

Taj Accountants to analyse the risk associated with investing funds in the organisation. For

example -If there is more fluctuations in the profit of firm it will indicate that there is high risk

in investing capital in organisation (Diouf and Boiral, 2017).

PART B

CLIENT 1

1. Recording and classification of the journal entries

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

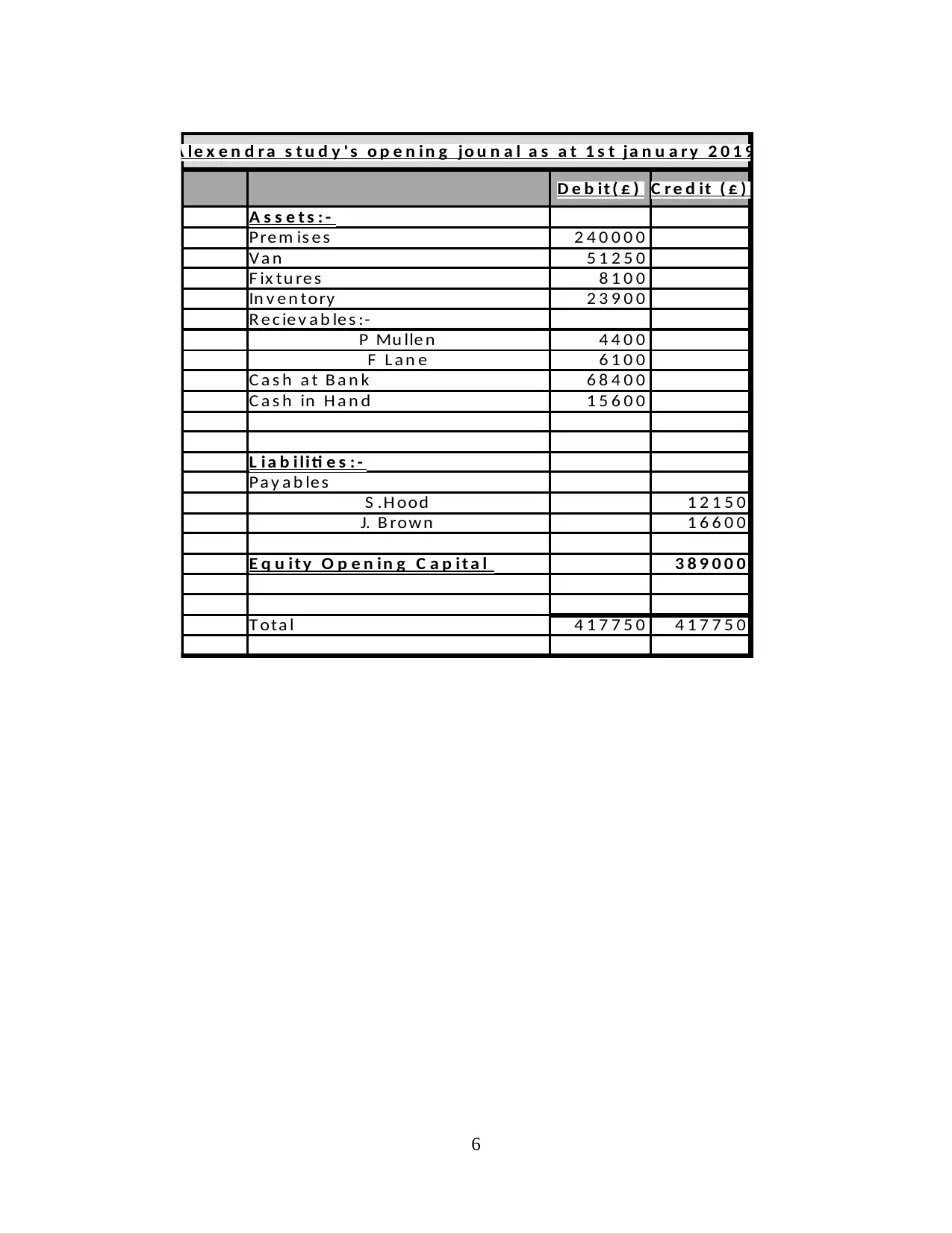

A le x e n d r a s t u d y ' s o p e n i n g jo u n a l a s a t 1 s t ja n u a r y 2 0 1 9

D e b i t ( £ ) C r e d it ( £ )

A s s e t s : -

Pre m is e s 2 4 0 0 0 0

V a n 5 1 2 5 0

F ix tu re s 8 1 0 0

In v e n tory 2 3 9 0 0

R e c ie v a b le s :-

P Mu lle n 4 4 0 0

F L a n e 6 1 0 0

C a s h a t B a n k 6 8 4 0 0

C a s h in H a n d 1 5 6 0 0

L i a b i li ti e s : -

Pa y a b le s

S .H ood 1 2 1 5 0

J. B rown 1 6 6 0 0

E q u it y O p e n in g C a p i t a l 3 8 9 0 0 0

T ota l 4 1 7 7 5 0 4 1 7 7 5 0

A le x e n d r a s t u d y ' s o p e n i n g jo u n a l a s a t 1 s t ja n u a r y 2 0 1 9

D e b i t ( £ ) C r e d it ( £ )

A s s e t s : -

Pre m is e s 2 4 0 0 0 0

V a n 5 1 2 5 0

F ix tu re s 8 1 0 0

In v e n tory 2 3 9 0 0

R e c ie v a b le s :-

P Mu lle n 4 4 0 0

F L a n e 6 1 0 0

C a s h a t B a n k 6 8 4 0 0

C a s h in H a n d 1 5 6 0 0

L i a b i li ti e s : -

Pa y a b le s

S .H ood 1 2 1 5 0

J. B rown 1 6 6 0 0

E q u it y O p e n in g C a p i t a l 3 8 9 0 0 0

T ota l 4 1 7 7 5 0 4 1 7 7 5 0

7

8

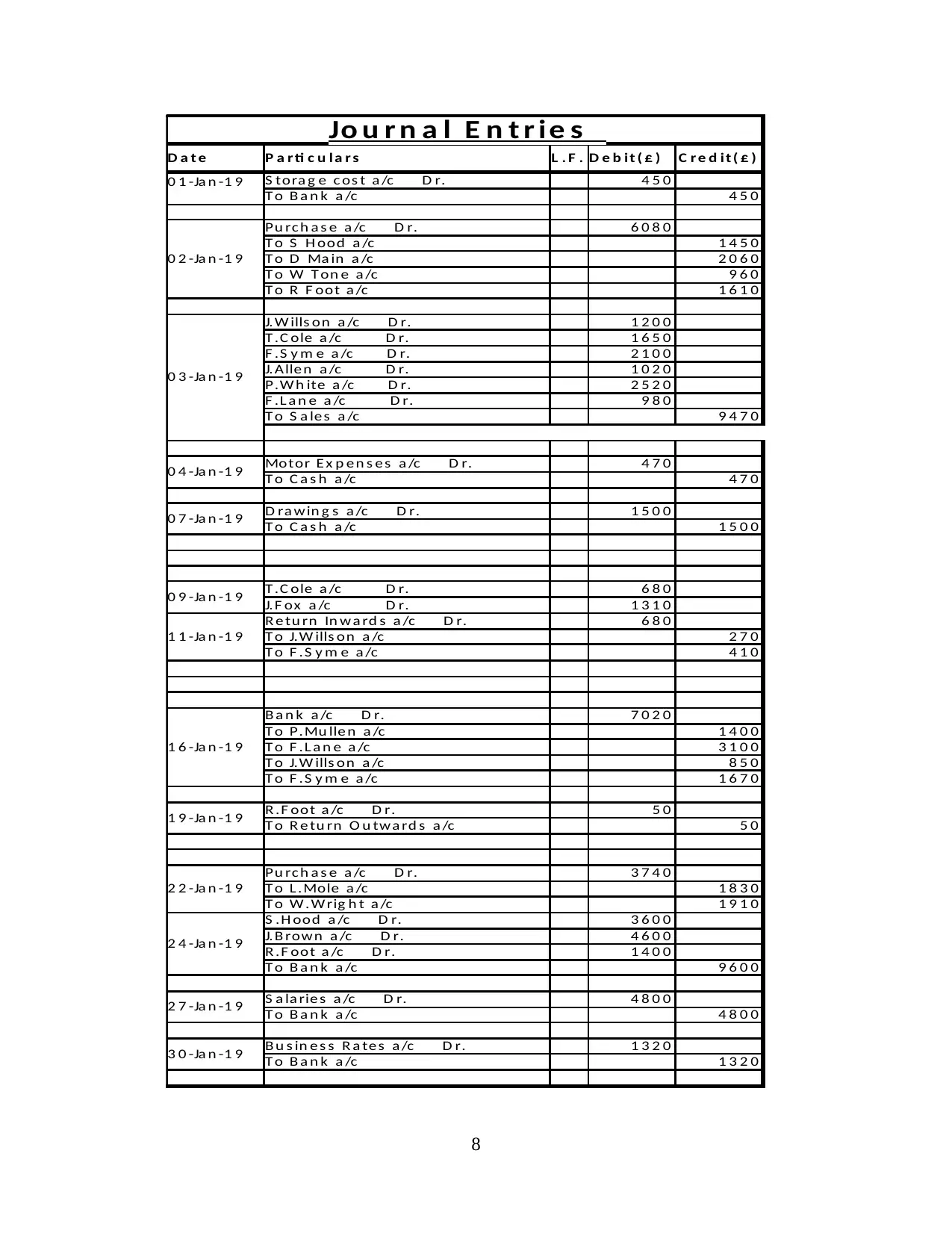

Jo u r n a l E n t r ie s

D a t e P a r ti c u la r s L . F . D e b it ( £ ) C r e d it ( £ )

0 1 -Ja n -1 9 S tora g e c os t a /c D r. 4 5 0

T o B a n k a /c 4 5 0

0 2 -Ja n -1 9

Pu rc h a s e a /c D r. 6 0 8 0

T o S H ood a /c 1 4 5 0

T o D Ma in a /c 2 0 6 0

T o W T on e a /c 9 6 0

T o R F oot a /c 1 6 1 0

0 3 -Ja n -1 9

J.W ills on a /c D r. 1 2 0 0

T .C ole a /c D r. 1 6 5 0

F .S y m e a /c D r. 2 1 0 0

J.Alle n a /c D r. 1 0 2 0

P.W h ite a /c D r. 2 5 2 0

F .L a n e a /c D r. 9 8 0

T o S a le s a /c 9 4 7 0

0 4 -Ja n -1 9 Motor E x p e n s e s a /c D r. 4 7 0

T o C a s h a /c 4 7 0

0 7 -Ja n -1 9 D ra w in g s a /c D r. 1 5 0 0

T o C a s h a /c 1 5 0 0

0 9 -Ja n -1 9 T .C ole a /c D r. 6 8 0

J.F ox a /c D r. 1 3 1 0

1 1 -Ja n -1 9

R e tu rn In w a rd s a /c D r. 6 8 0

T o J.W ills on a /c 2 7 0

T o F .S y m e a /c 4 1 0

1 6 -Ja n -1 9

B a n k a /c D r. 7 0 2 0

T o P.Mu lle n a /c 1 4 0 0

T o F .L a n e a /c 3 1 0 0

T o J.W ills on a /c 8 5 0

T o F .S y m e a /c 1 6 7 0

1 9 -Ja n -1 9 R .F oot a /c D r. 5 0

T o R e tu rn O u twa rd s a /c 5 0

2 2 -Ja n -1 9

Pu rc h a s e a /c D r. 3 7 4 0

T o L .Mole a /c 1 8 3 0

T o W .W rig h t a /c 1 9 1 0

2 4 -Ja n -1 9

S .H ood a /c D r. 3 6 0 0

J.B rown a /c D r. 4 6 0 0

R .F oot a /c D r. 1 4 0 0

T o B a n k a /c 9 6 0 0

2 7 -Ja n -1 9 S a la rie s a /c D r. 4 8 0 0

T o B a n k a /c 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s a /c D r. 1 3 2 0

T o B a n k a /c 1 3 2 0

Jo u r n a l E n t r ie s

D a t e P a r ti c u la r s L . F . D e b it ( £ ) C r e d it ( £ )

0 1 -Ja n -1 9 S tora g e c os t a /c D r. 4 5 0

T o B a n k a /c 4 5 0

0 2 -Ja n -1 9

Pu rc h a s e a /c D r. 6 0 8 0

T o S H ood a /c 1 4 5 0

T o D Ma in a /c 2 0 6 0

T o W T on e a /c 9 6 0

T o R F oot a /c 1 6 1 0

0 3 -Ja n -1 9

J.W ills on a /c D r. 1 2 0 0

T .C ole a /c D r. 1 6 5 0

F .S y m e a /c D r. 2 1 0 0

J.Alle n a /c D r. 1 0 2 0

P.W h ite a /c D r. 2 5 2 0

F .L a n e a /c D r. 9 8 0

T o S a le s a /c 9 4 7 0

0 4 -Ja n -1 9 Motor E x p e n s e s a /c D r. 4 7 0

T o C a s h a /c 4 7 0

0 7 -Ja n -1 9 D ra w in g s a /c D r. 1 5 0 0

T o C a s h a /c 1 5 0 0

0 9 -Ja n -1 9 T .C ole a /c D r. 6 8 0

J.F ox a /c D r. 1 3 1 0

1 1 -Ja n -1 9

R e tu rn In w a rd s a /c D r. 6 8 0

T o J.W ills on a /c 2 7 0

T o F .S y m e a /c 4 1 0

1 6 -Ja n -1 9

B a n k a /c D r. 7 0 2 0

T o P.Mu lle n a /c 1 4 0 0

T o F .L a n e a /c 3 1 0 0

T o J.W ills on a /c 8 5 0

T o F .S y m e a /c 1 6 7 0

1 9 -Ja n -1 9 R .F oot a /c D r. 5 0

T o R e tu rn O u twa rd s a /c 5 0

2 2 -Ja n -1 9

Pu rc h a s e a /c D r. 3 7 4 0

T o L .Mole a /c 1 8 3 0

T o W .W rig h t a /c 1 9 1 0

2 4 -Ja n -1 9

S .H ood a /c D r. 3 6 0 0

J.B rown a /c D r. 4 6 0 0

R .F oot a /c D r. 1 4 0 0

T o B a n k a /c 9 6 0 0

2 7 -Ja n -1 9 S a la rie s a /c D r. 4 8 0 0

T o B a n k a /c 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s a /c D r. 1 3 2 0

T o B a n k a /c 1 3 2 0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

9

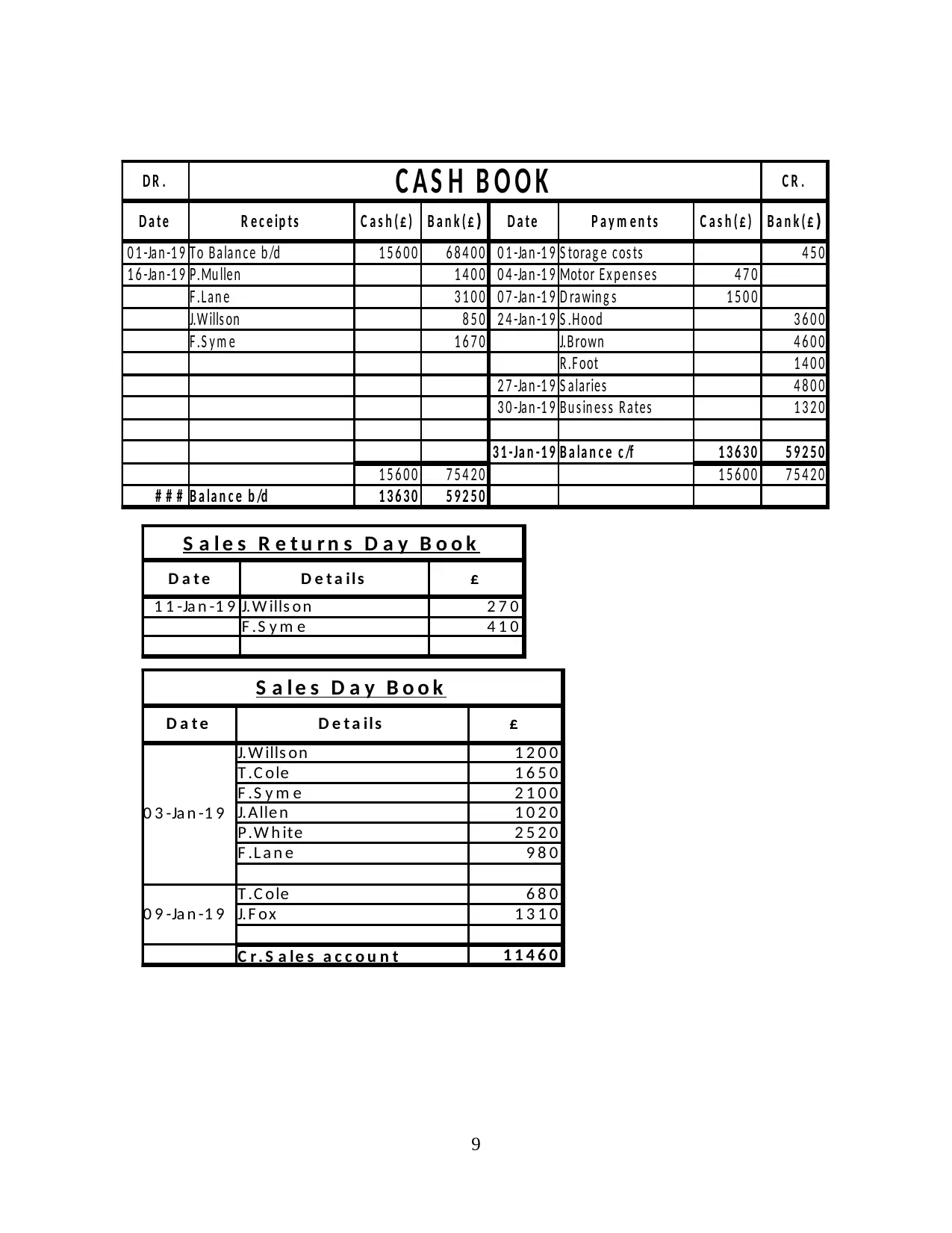

D R . C A S H B O O K C R .

D a t e R e c e ip t s C a s h ( £ ) D a t e P a y m e n t s C a s h ( £ )

0 1 -Ja n -1 9 T o B a la n c e b /d 1 5 6 0 0 6 8 4 0 0 0 1 -Ja n -1 9 S tora g e c os ts 4 5 0

1 6 -Ja n -1 9 P.Mu lle n 1 4 0 0 0 4 -Ja n -1 9 Motor E x p e n s e s 4 7 0

F .L a n e 3 1 0 0 0 7 -Ja n -1 9 D ra win g s 1 5 0 0

J.W ills on 8 5 0 2 4 -Ja n -1 9 S .H ood 3 6 0 0

F .S y m e 1 6 7 0 J.B rown 4 6 0 0

R .F oot 1 4 0 0

2 7 -Ja n -1 9 S a la rie s 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s 1 3 2 0

3 1 -Ja n - 1 9 B a la n c e c /f 1 3 6 3 0 5 9 2 5 0

1 5 6 0 0 7 5 4 2 0 1 5 6 0 0 7 5 4 2 0

# # # B a la n c e b /d 1 3 6 3 0 5 9 2 5 0

B a n k ( £ ) B a n k ( £ )

S a l e s D a y B o o k

D a t e D e t a ils £

0 3 -Ja n -1 9

J.W ills on 1 2 0 0

T .C ole 1 6 5 0

F .S y m e 2 1 0 0

J.Alle n 1 0 2 0

P.W h ite 2 5 2 0

F .L a n e 9 8 0

0 9 -Ja n -1 9

T .C ole 6 8 0

J.F ox 1 3 1 0

C r . S a le s a c c o u n t 1 1 4 6 0

S a l e s R e t u r n s D a y B o o k

D a t e D e t a ils £

1 1 -Ja n -1 9 J.W ills on 2 7 0

F .S y m e 4 1 0

D R . C A S H B O O K C R .

D a t e R e c e ip t s C a s h ( £ ) D a t e P a y m e n t s C a s h ( £ )

0 1 -Ja n -1 9 T o B a la n c e b /d 1 5 6 0 0 6 8 4 0 0 0 1 -Ja n -1 9 S tora g e c os ts 4 5 0

1 6 -Ja n -1 9 P.Mu lle n 1 4 0 0 0 4 -Ja n -1 9 Motor E x p e n s e s 4 7 0

F .L a n e 3 1 0 0 0 7 -Ja n -1 9 D ra win g s 1 5 0 0

J.W ills on 8 5 0 2 4 -Ja n -1 9 S .H ood 3 6 0 0

F .S y m e 1 6 7 0 J.B rown 4 6 0 0

R .F oot 1 4 0 0

2 7 -Ja n -1 9 S a la rie s 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s 1 3 2 0

3 1 -Ja n - 1 9 B a la n c e c /f 1 3 6 3 0 5 9 2 5 0

1 5 6 0 0 7 5 4 2 0 1 5 6 0 0 7 5 4 2 0

# # # B a la n c e b /d 1 3 6 3 0 5 9 2 5 0

B a n k ( £ ) B a n k ( £ )

S a l e s D a y B o o k

D a t e D e t a ils £

0 3 -Ja n -1 9

J.W ills on 1 2 0 0

T .C ole 1 6 5 0

F .S y m e 2 1 0 0

J.Alle n 1 0 2 0

P.W h ite 2 5 2 0

F .L a n e 9 8 0

0 9 -Ja n -1 9

T .C ole 6 8 0

J.F ox 1 3 1 0

C r . S a le s a c c o u n t 1 1 4 6 0

S a l e s R e t u r n s D a y B o o k

D a t e D e t a ils £

1 1 -Ja n -1 9 J.W ills on 2 7 0

F .S y m e 4 1 0

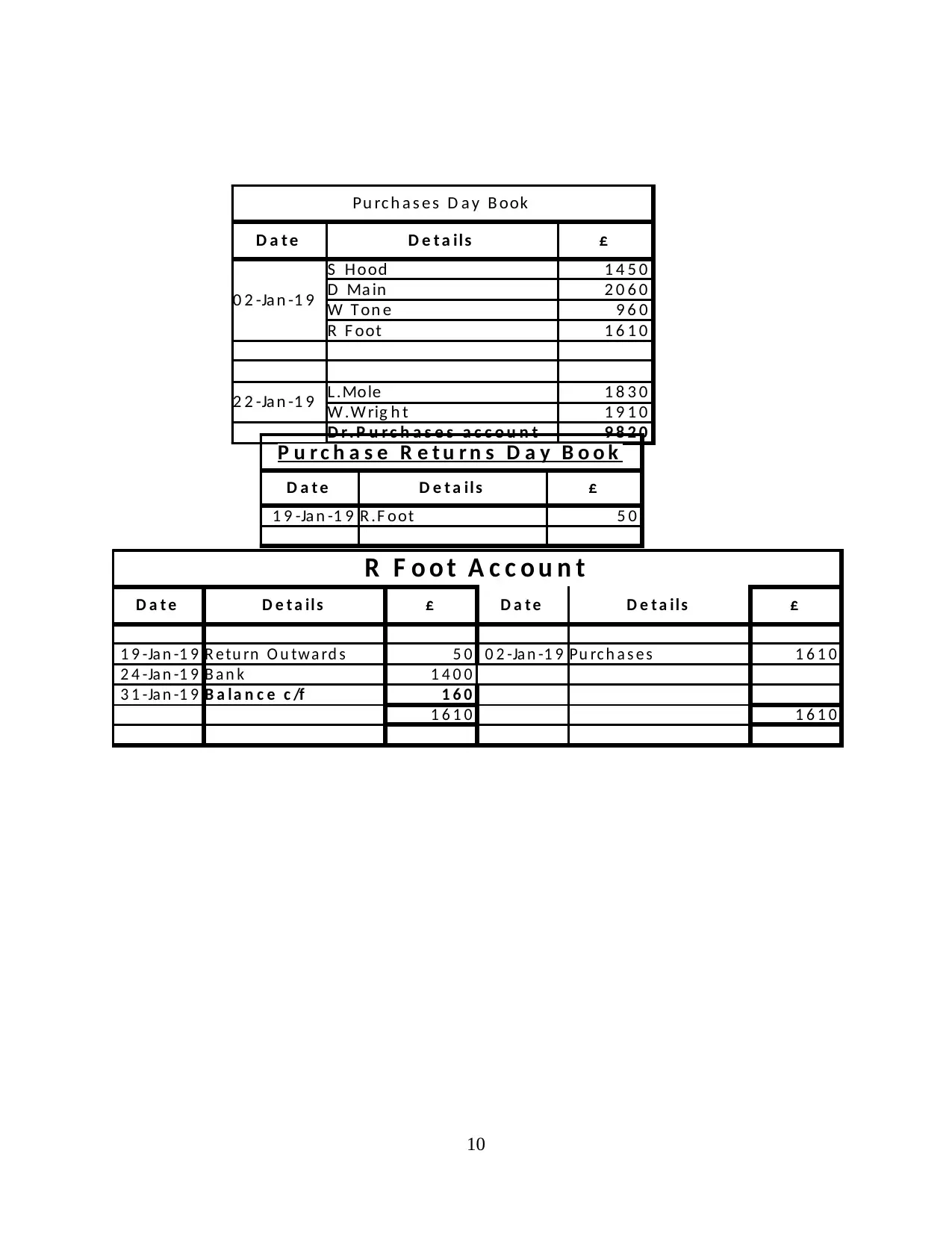

R F o o t A c c o u n t

D a t e D e t a il s £ D a t e D e t a il s £

1 9 -Ja n -1 9 R e tu rn O u tw a rd s 5 0 0 2 -Ja n -1 9 Pu rc h a s e s 1 6 1 0

2 4 -Ja n -1 9 B a n k 1 4 0 0

3 1 -Ja n -1 9 B a l a n c e c /f 1 6 0

1 6 1 0 1 6 1 0

10

Pu rc h a s e s D a y B ook

D a t e D e t a ils £

0 2 -Ja n -1 9

S H ood 1 4 5 0

D Ma in 2 0 6 0

W T on e 9 6 0

R F oot 1 6 1 0

2 2 -Ja n -1 9 L .Mole 1 8 3 0

W .W rig h t 1 9 1 0

D r . P u r c h a s e s a c c o u n t 9 8 2 0

P u r c h a s e R e t u r n s D a y B o o k

D a t e D e t a ils £

1 9 -Ja n -1 9 R .F oot 5 0

D a t e D e t a il s £ D a t e D e t a il s £

1 9 -Ja n -1 9 R e tu rn O u tw a rd s 5 0 0 2 -Ja n -1 9 Pu rc h a s e s 1 6 1 0

2 4 -Ja n -1 9 B a n k 1 4 0 0

3 1 -Ja n -1 9 B a l a n c e c /f 1 6 0

1 6 1 0 1 6 1 0

10

Pu rc h a s e s D a y B ook

D a t e D e t a ils £

0 2 -Ja n -1 9

S H ood 1 4 5 0

D Ma in 2 0 6 0

W T on e 9 6 0

R F oot 1 6 1 0

2 2 -Ja n -1 9 L .Mole 1 8 3 0

W .W rig h t 1 9 1 0

D r . P u r c h a s e s a c c o u n t 9 8 2 0

P u r c h a s e R e t u r n s D a y B o o k

D a t e D e t a ils £

1 9 -Ja n -1 9 R .F oot 5 0

11

T . C o le A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 3 -Ja n -1 9 S a le s 1 6 5 0

0 9 -Ja n -1 9 S a le s 6 8 0 3 1 -Ja n -1 9 B a la n c e c /f 2 3 3 0

2 3 3 0 2 3 3 0

F . S y m e A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 3 -Ja n -1 9 S a le s 2 1 0 0 1 1 -Ja n -1 9 R e tu rn In w a rd s 4 1 0

1 6 -Ja n -1 9 B a n k 1 6 7 0

3 1 -Ja n -1 9 B a la n c e c /f 2 0

2 1 0 0 2 1 0 0

J. A lle n A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 3 -Ja n -1 9 S a le s 1 0 2 0

3 1 -Ja n -1 9 B a la n c e c /f 1 0 2 0

1 0 2 0 1 0 2 0

S H o o d A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 1 -Ja n -1 9 B a la n c e b /d 1 2 1 5 0

2 4 -Ja n -1 9 B a n k 3 6 0 0 0 2 -Ja n -1 9 Pu rc h a s e s 1 4 5 0

3 1 -Ja n -1 9 B a la n c e c /f 1 0 0 0 0

1 3 6 0 0 1 3 6 0 0

J B r o w n A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 1 -Ja n -1 9 B a la n c e b /d 1 6 6 0 0

2 4 -Ja n -1 9 B a n k 4 6 0 0

3 1 -Ja n -1 9 B a la n c e c /f 1 2 0 0 0

1 6 6 0 0 1 6 6 0 0

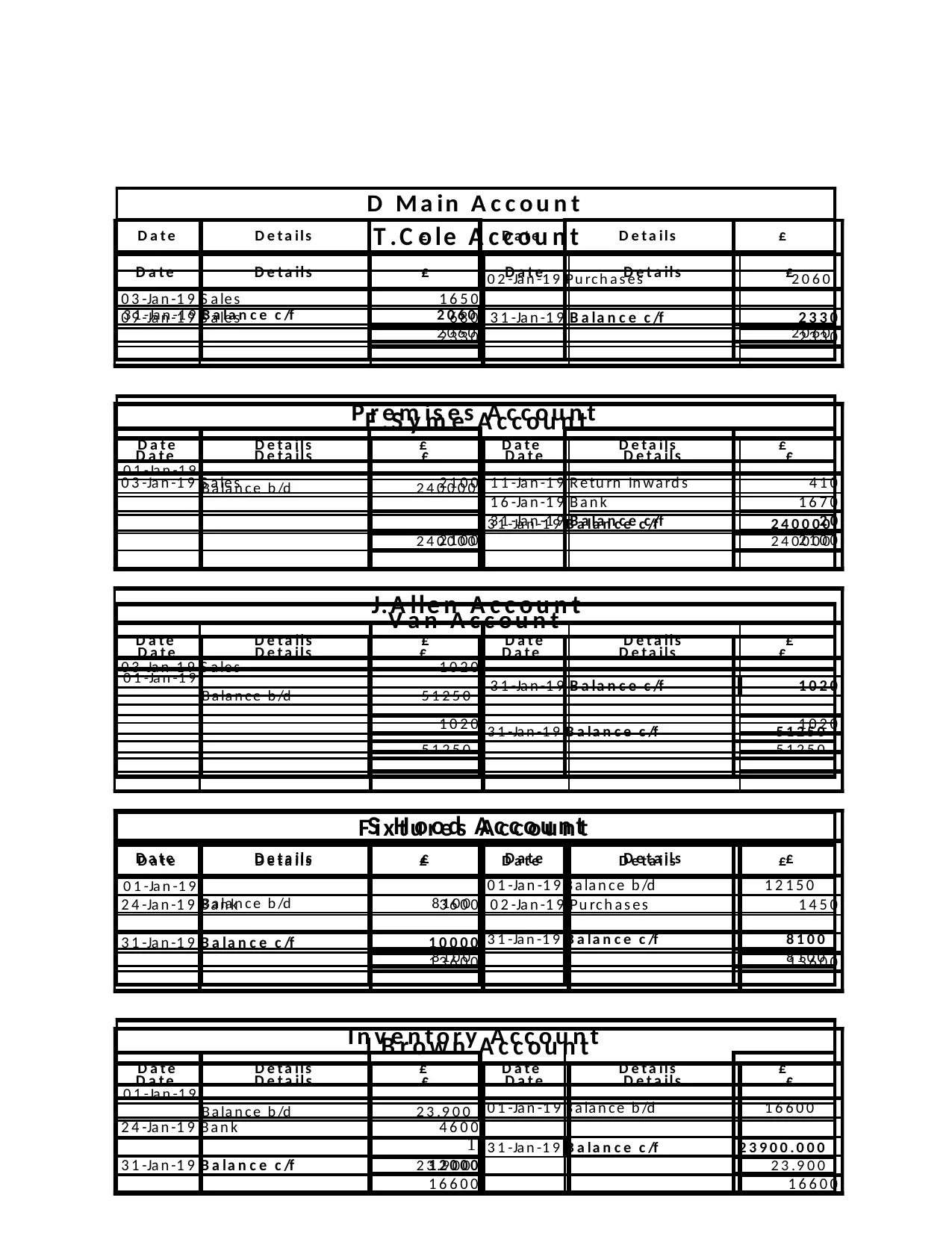

D M a in A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 2 -Ja n -1 9 Pu rc h a s e s 2 0 6 0

3 1 -Ja n -1 9 B a la n c e c /f 2 0 6 0

2 0 6 0 2 0 6 0

P r e m is e s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9

B a la n c e b /d 2 4 0 0 0 0

3 1 -Ja n -1 9 B a la n c e c /f 2 4 0 0 0 0

2 4 0 0 0 0 2 4 0 0 0 0

V a n A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9

B a la n c e b /d 5 1 2 5 0

3 1 -Ja n -1 9 B a la n c e c /f 5 1 2 5 0

5 1 2 5 0 5 1 2 5 0

F ix t u r e s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9

B a la n c e b /d 8 1 0 0

3 1 -Ja n -1 9 B a la n c e c /f 8 1 0 0

8 1 0 0 8 1 0 0

I n v e n t o r y A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9

B a la n c e b /d 2 3 .9 0 0

3 1 -Ja n -1 9 B a la n c e c /f 2 3 9 0 0 . 0 0 0

2 3 .9 0 0 2 3 .9 0 0

T . C o le A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 3 -Ja n -1 9 S a le s 1 6 5 0

0 9 -Ja n -1 9 S a le s 6 8 0 3 1 -Ja n -1 9 B a la n c e c /f 2 3 3 0

2 3 3 0 2 3 3 0

F . S y m e A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 3 -Ja n -1 9 S a le s 2 1 0 0 1 1 -Ja n -1 9 R e tu rn In w a rd s 4 1 0

1 6 -Ja n -1 9 B a n k 1 6 7 0

3 1 -Ja n -1 9 B a la n c e c /f 2 0

2 1 0 0 2 1 0 0

J. A lle n A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 3 -Ja n -1 9 S a le s 1 0 2 0

3 1 -Ja n -1 9 B a la n c e c /f 1 0 2 0

1 0 2 0 1 0 2 0

S H o o d A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 1 -Ja n -1 9 B a la n c e b /d 1 2 1 5 0

2 4 -Ja n -1 9 B a n k 3 6 0 0 0 2 -Ja n -1 9 Pu rc h a s e s 1 4 5 0

3 1 -Ja n -1 9 B a la n c e c /f 1 0 0 0 0

1 3 6 0 0 1 3 6 0 0

J B r o w n A c c o u n t

D a t e D e t a ils £ D a t e D e t a il s £

0 1 -Ja n -1 9 B a la n c e b /d 1 6 6 0 0

2 4 -Ja n -1 9 B a n k 4 6 0 0

3 1 -Ja n -1 9 B a la n c e c /f 1 2 0 0 0

1 6 6 0 0 1 6 6 0 0

D M a in A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 2 -Ja n -1 9 Pu rc h a s e s 2 0 6 0

3 1 -Ja n -1 9 B a la n c e c /f 2 0 6 0

2 0 6 0 2 0 6 0

P r e m is e s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9

B a la n c e b /d 2 4 0 0 0 0

3 1 -Ja n -1 9 B a la n c e c /f 2 4 0 0 0 0

2 4 0 0 0 0 2 4 0 0 0 0

V a n A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9

B a la n c e b /d 5 1 2 5 0

3 1 -Ja n -1 9 B a la n c e c /f 5 1 2 5 0

5 1 2 5 0 5 1 2 5 0

F ix t u r e s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9

B a la n c e b /d 8 1 0 0

3 1 -Ja n -1 9 B a la n c e c /f 8 1 0 0

8 1 0 0 8 1 0 0

I n v e n t o r y A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9

B a la n c e b /d 2 3 .9 0 0

3 1 -Ja n -1 9 B a la n c e c /f 2 3 9 0 0 . 0 0 0

2 3 .9 0 0 2 3 .9 0 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

12

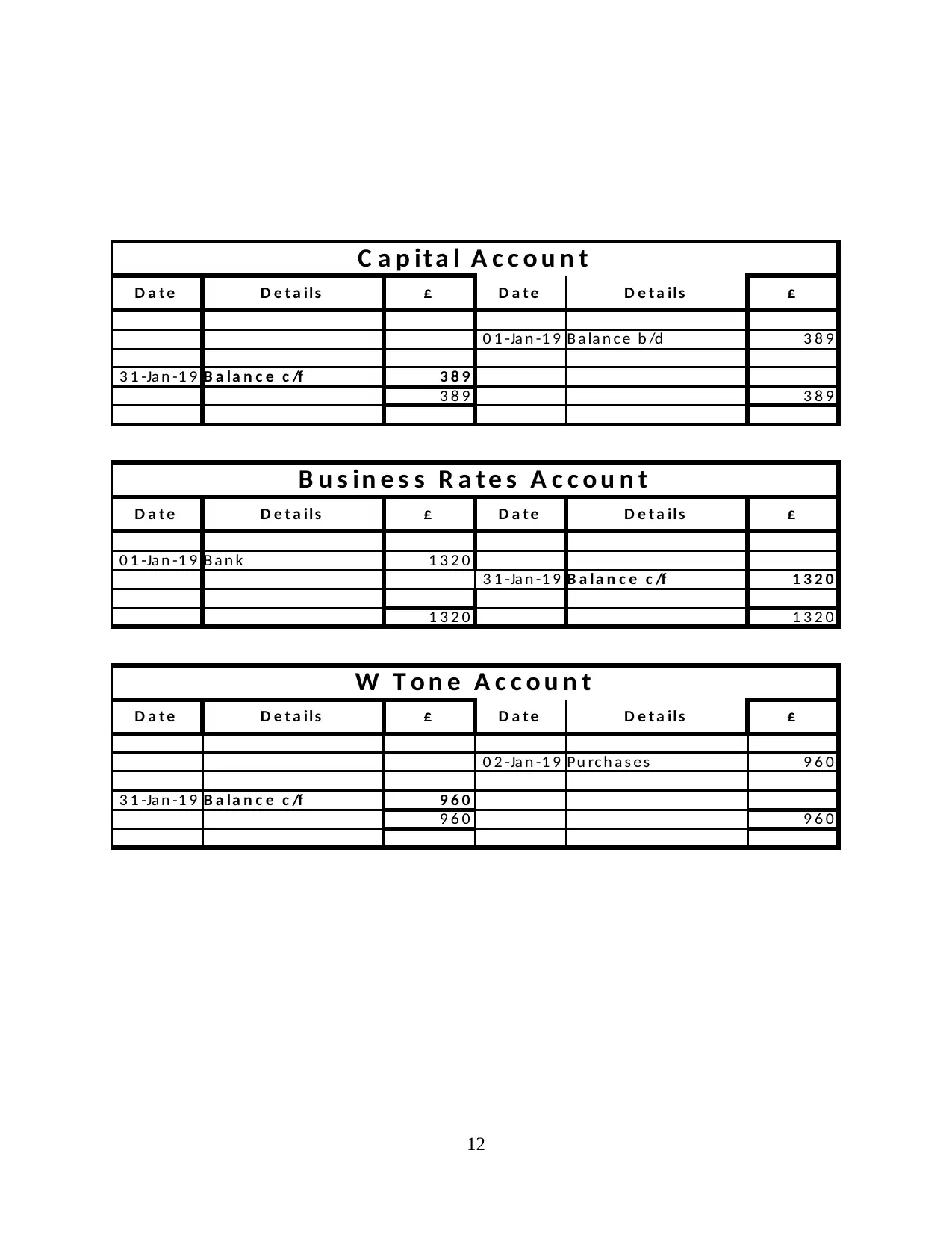

C a p it a l A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a la n c e b /d 3 8 9

3 1 -Ja n -1 9 B a la n c e c /f 3 8 9

3 8 9 3 8 9

B u s in e s s R a t e s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a n k 1 3 2 0

3 1 -Ja n -1 9 B a la n c e c /f 1 3 2 0

1 3 2 0 1 3 2 0

W T o n e A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 2 -Ja n -1 9 Pu rc h a s e s 9 6 0

3 1 -Ja n -1 9 B a la n c e c /f 9 6 0

9 6 0 9 6 0

C a p it a l A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a la n c e b /d 3 8 9

3 1 -Ja n -1 9 B a la n c e c /f 3 8 9

3 8 9 3 8 9

B u s in e s s R a t e s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a n k 1 3 2 0

3 1 -Ja n -1 9 B a la n c e c /f 1 3 2 0

1 3 2 0 1 3 2 0

W T o n e A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 2 -Ja n -1 9 Pu rc h a s e s 9 6 0

3 1 -Ja n -1 9 B a la n c e c /f 9 6 0

9 6 0 9 6 0

13

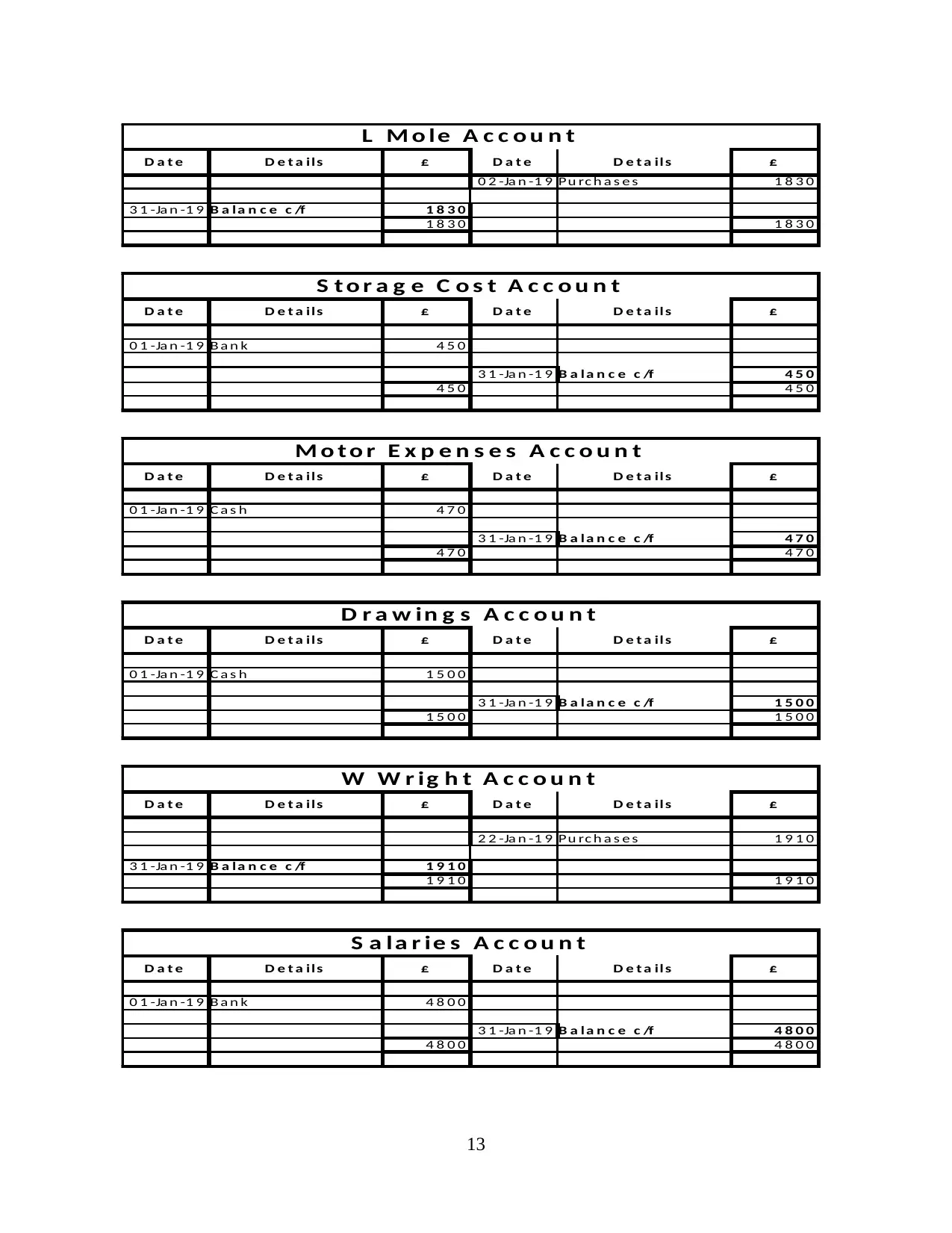

L M o le A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 2 -Ja n -1 9 Pu rc h a s e s 1 8 3 0

3 1 -Ja n -1 9 B a la n c e c /f 1 8 3 0

1 8 3 0 1 8 3 0

S t o r a g e C o s t A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a n k 4 5 0

3 1 -Ja n -1 9 B a la n c e c /f 4 5 0

4 5 0 4 5 0

M o t o r E x p e n s e s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 C a s h 4 7 0

3 1 -Ja n -1 9 B a la n c e c /f 4 7 0

4 7 0 4 7 0

D r a w in g s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 C a s h 1 5 0 0

3 1 -Ja n -1 9 B a la n c e c /f 1 5 0 0

1 5 0 0 1 5 0 0

W W r ig h t A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

2 2 -Ja n -1 9 Pu rc h a s e s 1 9 1 0

3 1 -Ja n -1 9 B a la n c e c /f 1 9 1 0

1 9 1 0 1 9 1 0

S a la r ie s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a n k 4 8 0 0

3 1 -Ja n -1 9 B a la n c e c /f 4 8 0 0

4 8 0 0 4 8 0 0

L M o le A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 2 -Ja n -1 9 Pu rc h a s e s 1 8 3 0

3 1 -Ja n -1 9 B a la n c e c /f 1 8 3 0

1 8 3 0 1 8 3 0

S t o r a g e C o s t A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a n k 4 5 0

3 1 -Ja n -1 9 B a la n c e c /f 4 5 0

4 5 0 4 5 0

M o t o r E x p e n s e s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 C a s h 4 7 0

3 1 -Ja n -1 9 B a la n c e c /f 4 7 0

4 7 0 4 7 0

D r a w in g s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 C a s h 1 5 0 0

3 1 -Ja n -1 9 B a la n c e c /f 1 5 0 0

1 5 0 0 1 5 0 0

W W r ig h t A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

2 2 -Ja n -1 9 Pu rc h a s e s 1 9 1 0

3 1 -Ja n -1 9 B a la n c e c /f 1 9 1 0

1 9 1 0 1 9 1 0

S a la r ie s A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a n k 4 8 0 0

3 1 -Ja n -1 9 B a la n c e c /f 4 8 0 0

4 8 0 0 4 8 0 0

14

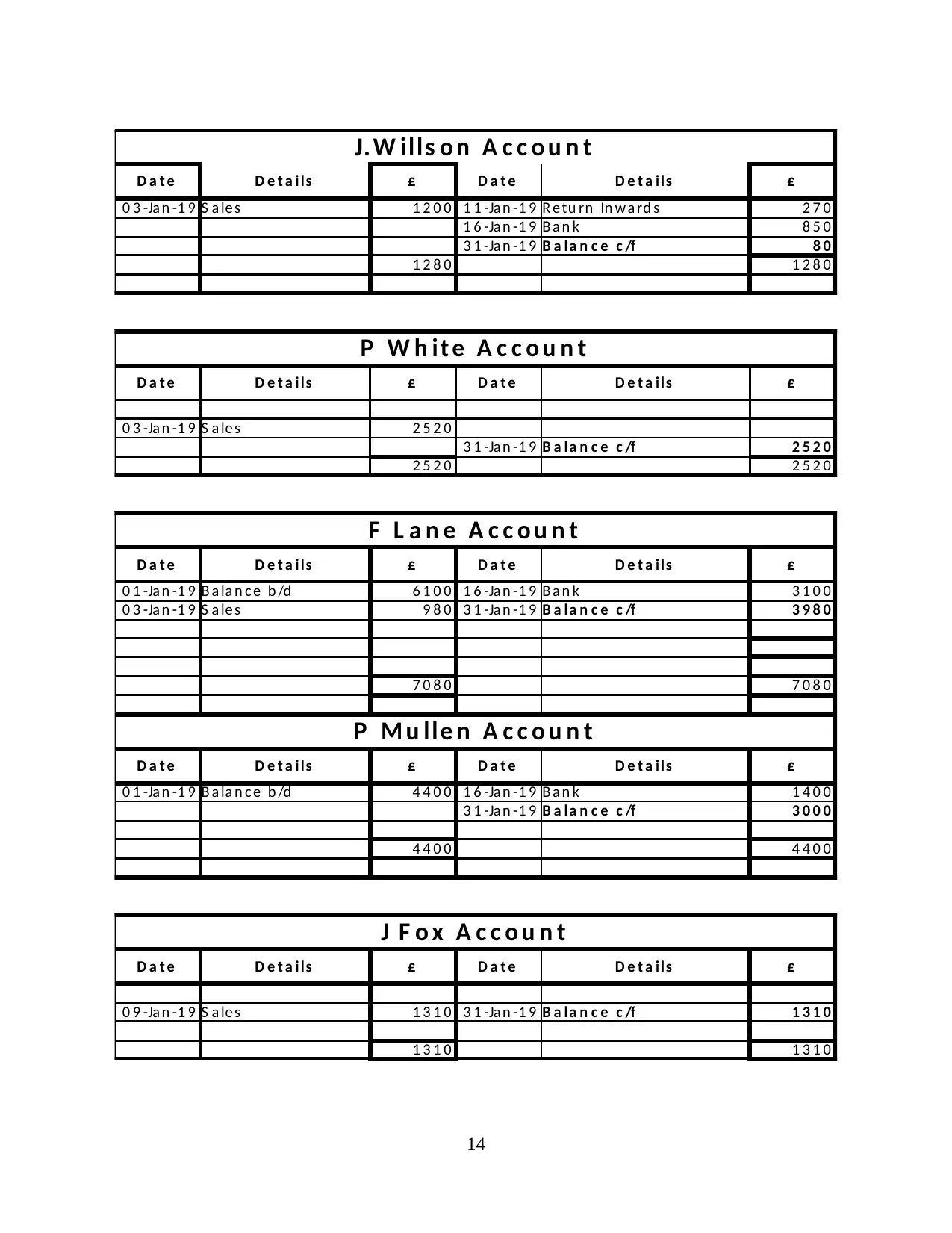

J. W ills o n A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 3 -Ja n -1 9 S a le s 1 2 0 0 1 1 -Ja n -1 9 R e tu rn In w a rd s 2 7 0

1 6 -Ja n -1 9 B a n k 8 5 0

3 1 -Ja n -1 9 B a la n c e c /f 8 0

1 2 8 0 1 2 8 0

P W h it e A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 3 -Ja n -1 9 S a le s 2 5 2 0

3 1 -Ja n -1 9 B a la n c e c /f 2 5 2 0

2 5 2 0 2 5 2 0

F L a n e A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a la n c e b /d 6 1 0 0 1 6 -Ja n -1 9 B a n k 3 1 0 0

0 3 -Ja n -1 9 S a le s 9 8 0 3 1 -Ja n -1 9 B a la n c e c /f 3 9 8 0

7 0 8 0 7 0 8 0

P M u lle n A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a la n c e b /d 4 4 0 0 1 6 -Ja n -1 9 B a n k 1 4 0 0

3 1 -Ja n -1 9 B a la n c e c /f 3 0 0 0

4 4 0 0 4 4 0 0

J F o x A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 9 -Ja n -1 9 S a le s 1 3 1 0 3 1 -Ja n -1 9 B a la n c e c /f 1 3 1 0

1 3 1 0 1 3 1 0

J. W ills o n A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 3 -Ja n -1 9 S a le s 1 2 0 0 1 1 -Ja n -1 9 R e tu rn In w a rd s 2 7 0

1 6 -Ja n -1 9 B a n k 8 5 0

3 1 -Ja n -1 9 B a la n c e c /f 8 0

1 2 8 0 1 2 8 0

P W h it e A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 3 -Ja n -1 9 S a le s 2 5 2 0

3 1 -Ja n -1 9 B a la n c e c /f 2 5 2 0

2 5 2 0 2 5 2 0

F L a n e A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a la n c e b /d 6 1 0 0 1 6 -Ja n -1 9 B a n k 3 1 0 0

0 3 -Ja n -1 9 S a le s 9 8 0 3 1 -Ja n -1 9 B a la n c e c /f 3 9 8 0

7 0 8 0 7 0 8 0

P M u lle n A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 1 -Ja n -1 9 B a la n c e b /d 4 4 0 0 1 6 -Ja n -1 9 B a n k 1 4 0 0

3 1 -Ja n -1 9 B a la n c e c /f 3 0 0 0

4 4 0 0 4 4 0 0

J F o x A c c o u n t

D a t e D e t a ils £ D a t e D e t a ils £

0 9 -Ja n -1 9 S a le s 1 3 1 0 3 1 -Ja n -1 9 B a la n c e c /f 1 3 1 0

1 3 1 0 1 3 1 0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

15

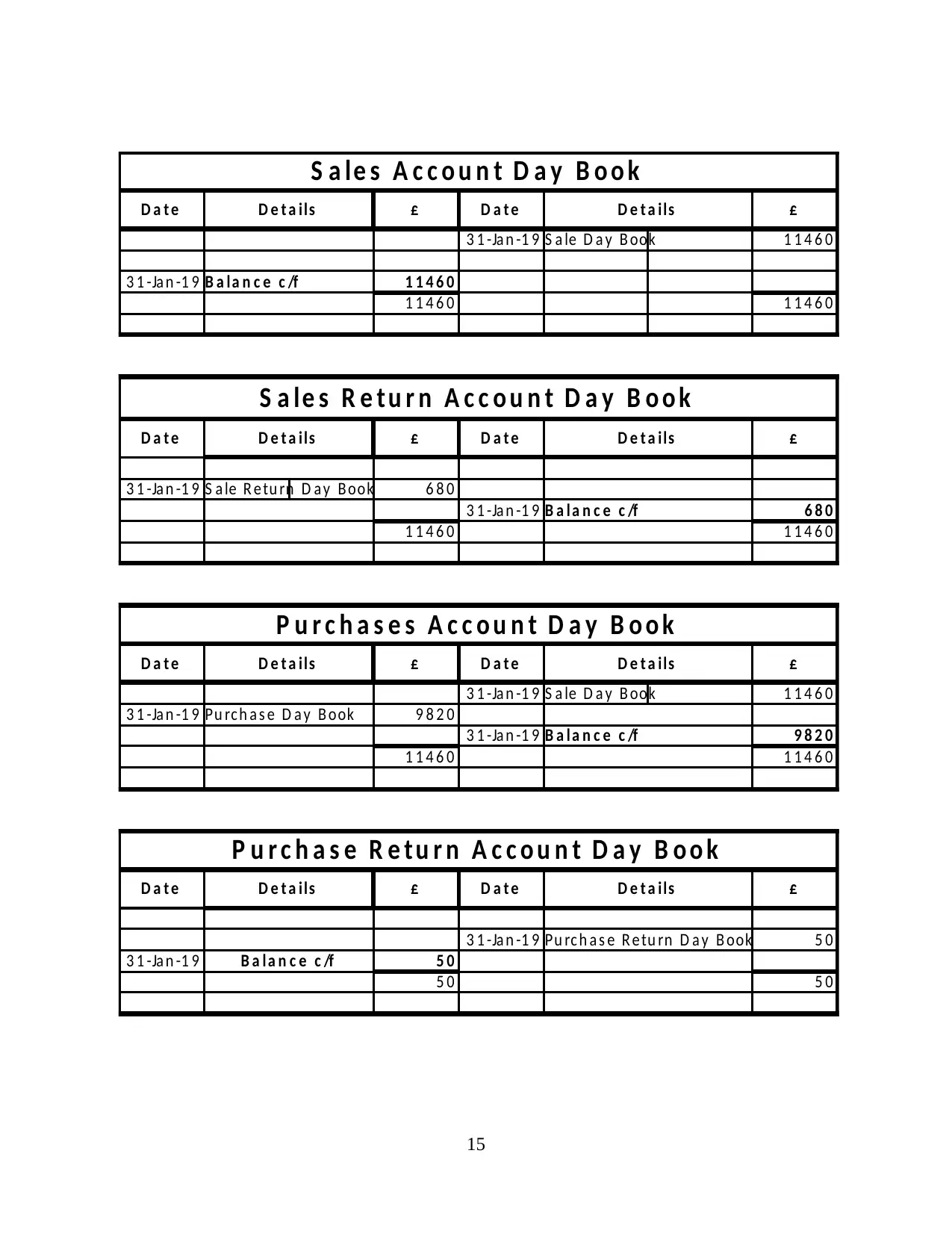

S a le s A c c o u n t D a y B o o k

D a t e D e t a i ls £ D a t e D e t a i ls £

3 1 -Ja n -1 9 S a le D a y B ook 1 1 4 6 0

3 1 -Ja n -1 9 B a la n c e c /f 1 1 4 6 0

1 1 4 6 0 1 1 4 6 0

S a le s R e t u r n A c c o u n t D a y B o o k

D a t e D e t a i ls £ D a t e D e t a i ls £

3 1 -Ja n -1 9 S a le R e tu rn D a y B ook 6 8 0

3 1 -Ja n -1 9 B a l a n c e c /f 6 8 0

1 1 4 6 0 1 1 4 6 0

P u r c h a s e s A c c o u n t D a y B o o k

D a t e D e t a i ls £ D a t e D e t a i ls £

3 1 -Ja n -1 9 S a le D a y B ook 1 1 4 6 0

3 1 -Ja n -1 9 Pu rc h a s e D a y B ook 9 8 2 0

3 1 -Ja n -1 9 B a l a n c e c /f 9 8 2 0

1 1 4 6 0 1 1 4 6 0

P u r c h a s e R e t u r n A c c o u n t D a y B o o k

D a t e D e t a i ls £ D a t e D e t a i ls £

3 1 -Ja n -1 9 Pu rc h a s e R e tu rn D a y B ook 5 0

3 1 -Ja n -1 9 B a l a n c e c /f 5 0

5 0 5 0

S a le s A c c o u n t D a y B o o k

D a t e D e t a i ls £ D a t e D e t a i ls £

3 1 -Ja n -1 9 S a le D a y B ook 1 1 4 6 0

3 1 -Ja n -1 9 B a la n c e c /f 1 1 4 6 0

1 1 4 6 0 1 1 4 6 0

S a le s R e t u r n A c c o u n t D a y B o o k

D a t e D e t a i ls £ D a t e D e t a i ls £

3 1 -Ja n -1 9 S a le R e tu rn D a y B ook 6 8 0

3 1 -Ja n -1 9 B a l a n c e c /f 6 8 0

1 1 4 6 0 1 1 4 6 0

P u r c h a s e s A c c o u n t D a y B o o k

D a t e D e t a i ls £ D a t e D e t a i ls £

3 1 -Ja n -1 9 S a le D a y B ook 1 1 4 6 0

3 1 -Ja n -1 9 Pu rc h a s e D a y B ook 9 8 2 0

3 1 -Ja n -1 9 B a l a n c e c /f 9 8 2 0

1 1 4 6 0 1 1 4 6 0

P u r c h a s e R e t u r n A c c o u n t D a y B o o k

D a t e D e t a i ls £ D a t e D e t a i ls £

3 1 -Ja n -1 9 Pu rc h a s e R e tu rn D a y B ook 5 0

3 1 -Ja n -1 9 B a l a n c e c /f 5 0

5 0 5 0

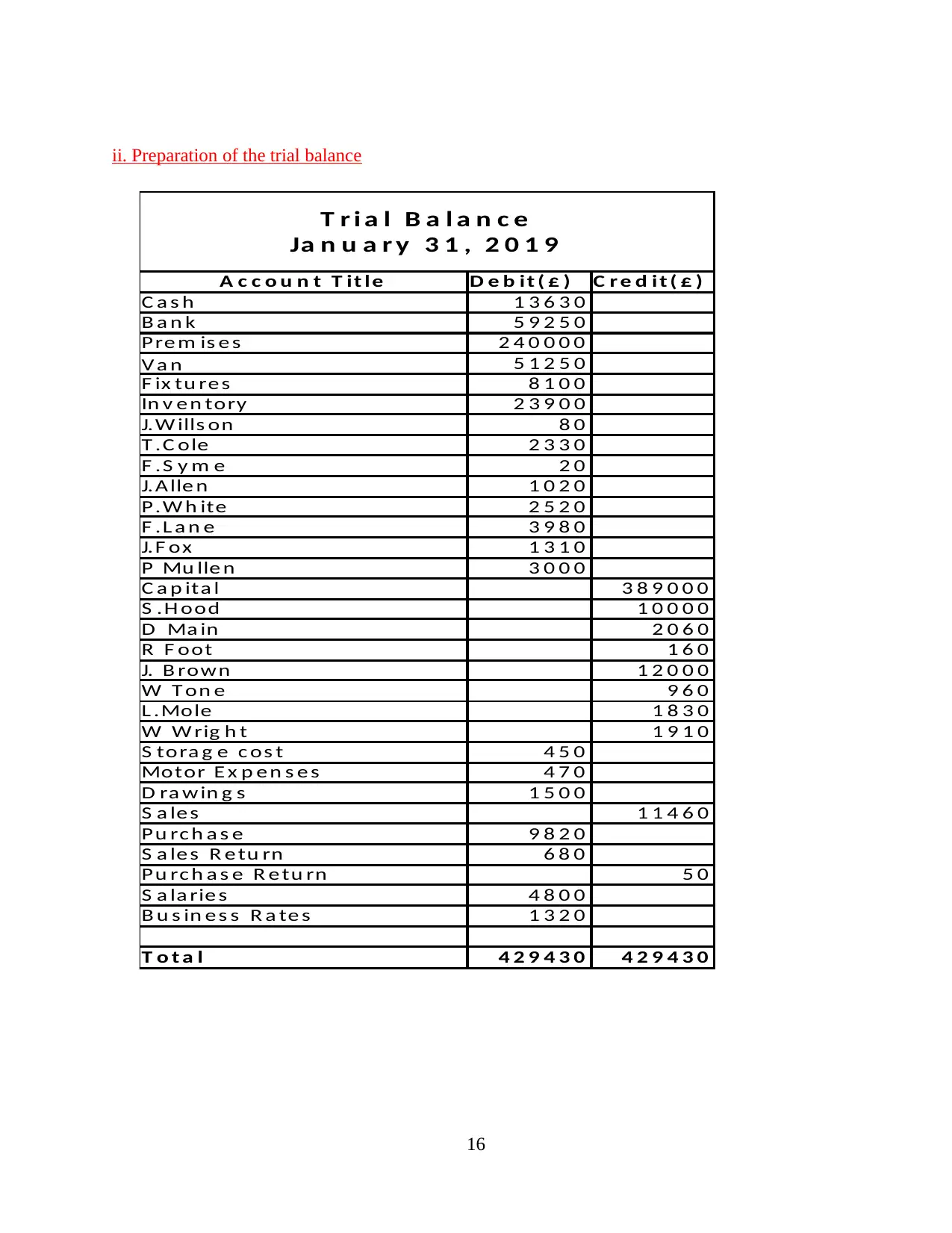

ii. Preparation of the trial balance

16

A c c o u n t T it le D e b it ( £ ) C r e d it ( £ )

C a s h 1 3 6 3 0

B a n k 5 9 2 5 0

Pre m is e s 2 4 0 0 0 0

V a n 5 1 2 5 0

F ix tu re s 8 1 0 0

In v e n tory 2 3 9 0 0

J.W ills on 8 0

T .C ole 2 3 3 0

F .S y m e 2 0

J.A lle n 1 0 2 0

P.W h ite 2 5 2 0

F .L a n e 3 9 8 0

J.F ox 1 3 1 0

P Mu lle n 3 0 0 0

C a p ita l 3 8 9 0 0 0

S .H ood 1 0 0 0 0

D Ma in 2 0 6 0

R F oot 1 6 0

J. B rown 1 2 0 0 0

W T on e 9 6 0

L .Mole 1 8 3 0

W W rig h t 1 9 1 0

S tora g e c os t 4 5 0

Motor E x p e n s e s 4 7 0

D ra w in g s 1 5 0 0

S a le s 1 1 4 6 0

Pu rc h a s e 9 8 2 0

S a le s R e tu rn 6 8 0

Pu rc h a s e R e tu rn 5 0

S a la rie s 4 8 0 0

B u s in e s s R a te s 1 3 2 0

T o t a l 4 2 9 4 3 0 4 2 9 4 3 0

T r i a l B a l a n c e

Ja n u a r y 3 1 , 2 0 1 9

16

A c c o u n t T it le D e b it ( £ ) C r e d it ( £ )

C a s h 1 3 6 3 0

B a n k 5 9 2 5 0

Pre m is e s 2 4 0 0 0 0

V a n 5 1 2 5 0

F ix tu re s 8 1 0 0

In v e n tory 2 3 9 0 0

J.W ills on 8 0

T .C ole 2 3 3 0

F .S y m e 2 0

J.A lle n 1 0 2 0

P.W h ite 2 5 2 0

F .L a n e 3 9 8 0

J.F ox 1 3 1 0

P Mu lle n 3 0 0 0

C a p ita l 3 8 9 0 0 0

S .H ood 1 0 0 0 0

D Ma in 2 0 6 0

R F oot 1 6 0

J. B rown 1 2 0 0 0

W T on e 9 6 0

L .Mole 1 8 3 0

W W rig h t 1 9 1 0

S tora g e c os t 4 5 0

Motor E x p e n s e s 4 7 0

D ra w in g s 1 5 0 0

S a le s 1 1 4 6 0

Pu rc h a s e 9 8 2 0

S a le s R e tu rn 6 8 0

Pu rc h a s e R e tu rn 5 0

S a la rie s 4 8 0 0

B u s in e s s R a te s 1 3 2 0

T o t a l 4 2 9 4 3 0 4 2 9 4 3 0

T r i a l B a l a n c e

Ja n u a r y 3 1 , 2 0 1 9

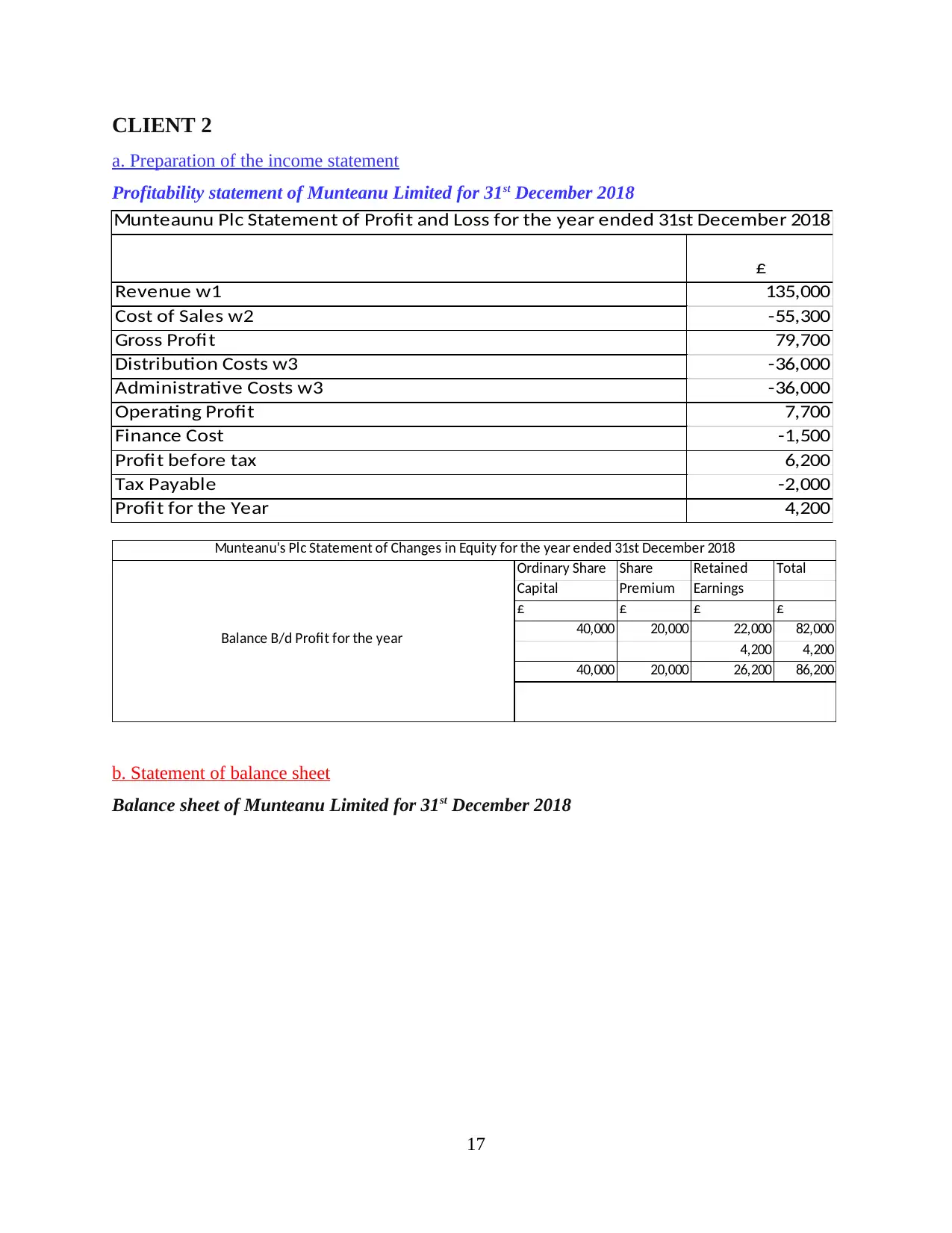

CLIENT 2

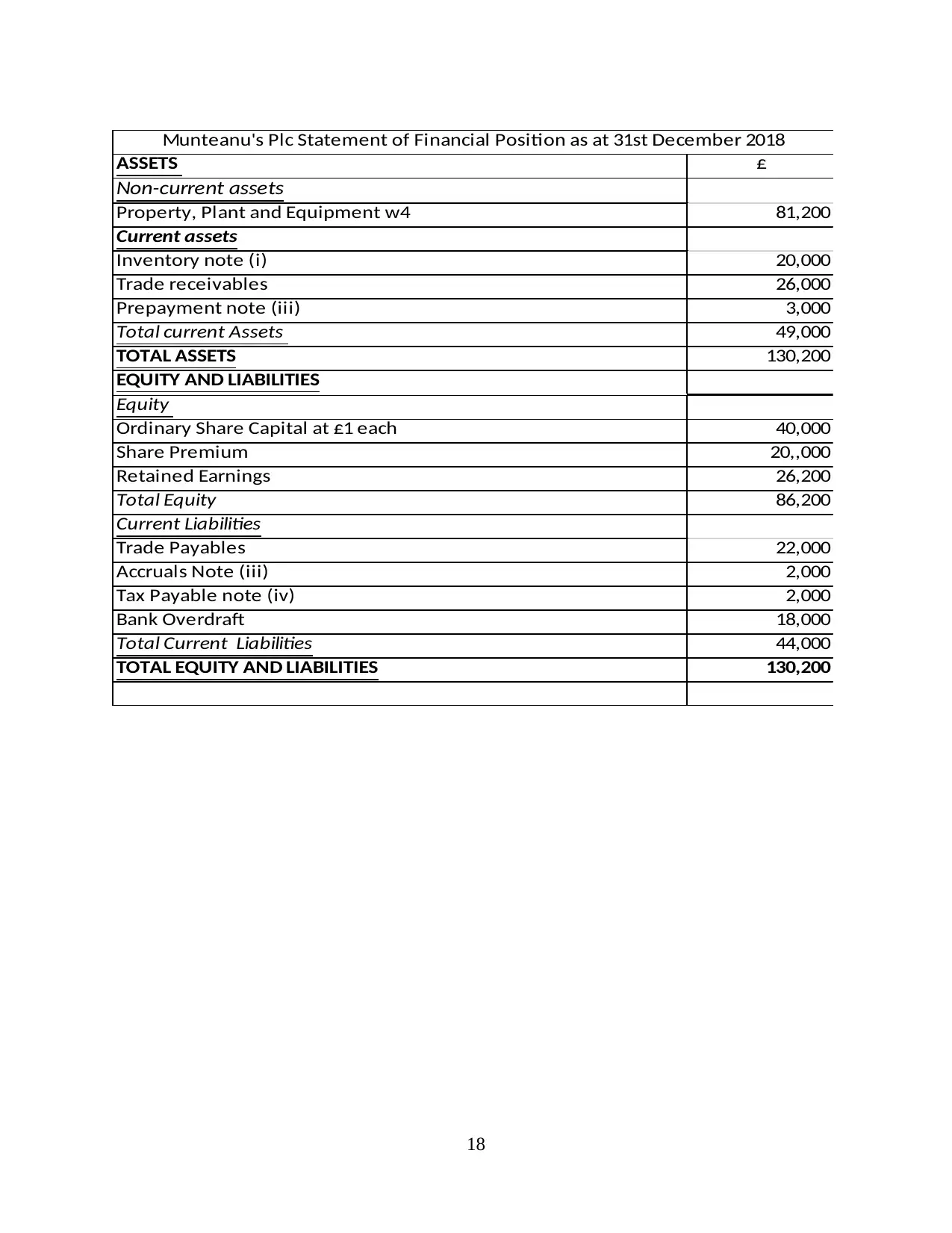

a. Preparation of the income statement

Profitability statement of Munteanu Limited for 31st December 2018

b. Statement of balance sheet

Balance sheet of Munteanu Limited for 31st December 2018

17

Revenue w1 135,000

Cost of Sales w2 -55,300

Gross Profit 79,700

Distribution Costs w3 -36,000

Administrative Costs w3 -36,000

Operating Profit 7,700

Finance Cost -1,500

Profit before tax 6,200

Tax Payable -2,000

Profit for the Year 4,200

Munteaunu Plc Statement of Profit and Loss for the year ended 31st December 2018

£

Ordinary Share Share Retained Total

Capital Premium Earnings

£ £ £ £

40,000 20,000 22,000 82,000

4,200 4,200

40,000 20,000 26,200 86,200

Munteanu's Plc Statement of Changes in Equity for the year ended 31st December 2018

Balance B/d Profit for the year

a. Preparation of the income statement

Profitability statement of Munteanu Limited for 31st December 2018

b. Statement of balance sheet

Balance sheet of Munteanu Limited for 31st December 2018

17

Revenue w1 135,000

Cost of Sales w2 -55,300

Gross Profit 79,700

Distribution Costs w3 -36,000

Administrative Costs w3 -36,000

Operating Profit 7,700

Finance Cost -1,500

Profit before tax 6,200

Tax Payable -2,000

Profit for the Year 4,200

Munteaunu Plc Statement of Profit and Loss for the year ended 31st December 2018

£

Ordinary Share Share Retained Total

Capital Premium Earnings

£ £ £ £

40,000 20,000 22,000 82,000

4,200 4,200

40,000 20,000 26,200 86,200

Munteanu's Plc Statement of Changes in Equity for the year ended 31st December 2018

Balance B/d Profit for the year

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

18

ASSETS £

Non-current assets

Property, Plant and Equipment w4 81,200

Current assets

Inventory note (i) 20,000

Trade receivables 26,000

Prepayment note (iii) 3,000

Total current Assets 49,000

TOTAL ASSETS 130,200

EQUITY AND LIABILITIES

Equity

Ordinary Share Capital at £1 each 40,000

Share Premium 20,,000

Retained Earnings 26,200

Total Equity 86,200

Current Liabilities

Trade Payables 22,000

Accruals Note (iii) 2,000

Tax Payable note (iv) 2,000

Bank Overdraft 18,000

Total Current Liabilities 44,000

TOTAL EQUITY AND LIABILITIES 130,200

Munteanu's Plc Statement of Financial Position as at 31st December 2018

ASSETS £

Non-current assets

Property, Plant and Equipment w4 81,200

Current assets

Inventory note (i) 20,000

Trade receivables 26,000

Prepayment note (iii) 3,000

Total current Assets 49,000

TOTAL ASSETS 130,200

EQUITY AND LIABILITIES

Equity

Ordinary Share Capital at £1 each 40,000

Share Premium 20,,000

Retained Earnings 26,200

Total Equity 86,200

Current Liabilities

Trade Payables 22,000

Accruals Note (iii) 2,000

Tax Payable note (iv) 2,000

Bank Overdraft 18,000

Total Current Liabilities 44,000

TOTAL EQUITY AND LIABILITIES 130,200

Munteanu's Plc Statement of Financial Position as at 31st December 2018

19

w1 REVENUE

SALES 138,000

Less returns Inwards -3,000

Revenue 135,000

w2 Cost of Sales

Opening Inventory 15000

Add Purchases 61000

Less returns Outwards -1500 59500

74500

Less closing Inventory note (i) -20000

54500

Dep on Buildings 800

Cost of Sales 55300

w3

ADMIN

costs DIST costs

TB 30000 35000

Dep on P and Machinery 4000 4000

admin salary accrued 2000

rent prepaid -3000

36000 36000

w4 PPE

L and B P and M

as per TB cost/valuation 60000 60000

acc dep at 1-Jan-18 -10000 -20000

note (ii) current year Depreciation -800 -8000

Carrying Value at 31-Dec 18

18 49200 32000 81200

w1 REVENUE

SALES 138,000

Less returns Inwards -3,000

Revenue 135,000

w2 Cost of Sales

Opening Inventory 15000

Add Purchases 61000

Less returns Outwards -1500 59500

74500

Less closing Inventory note (i) -20000

54500

Dep on Buildings 800

Cost of Sales 55300

w3

ADMIN

costs DIST costs

TB 30000 35000

Dep on P and Machinery 4000 4000

admin salary accrued 2000

rent prepaid -3000

36000 36000

w4 PPE

L and B P and M

as per TB cost/valuation 60000 60000

acc dep at 1-Jan-18 -10000 -20000

note (ii) current year Depreciation -800 -8000

Carrying Value at 31-Dec 18

18 49200 32000 81200

c). Consistency and Prudence

Consistency

Accounting information which facilitates comparison of financial reports of company

over different accounting years is known as principle of consistency. Consistency principle

requires that financial statements of the company should follow same accounting methods,

principles, practices, procedures and practices over the accounting years. This enables users of

financial statements in making meaningful and relevant comparison over the financial years.

Consistency principles allow companies to make changes in their accounting methods to more

preferred and effective method (Miglani, Ahmed and Henry, 2015). When the changes are made

to the methods of the accounting methods it is the responsibility of companies that they are

properly disclosed and highlighted in financial statements. It will enable the user to identify the

change and the effect of changes. As per Financial Accounting Standards Board consistency is

referred as quality and characteristic which makes financial information useful to the readers.

Objective behind consistency is of avoiding the intention from executive level

management of manipulating financial information for ensuring that accounting statement of

company look healthy. There are situations where management has to use inconsistency

principle in some of its accounting transactions or in its financial records. IFRS requires the

entities to use accounting policies consistently for reporting in financial statements.

This principle is important for viewer’s financial statements, experts, shareholders and

investors. When accounting principles and policies are used consistently it gives more reliability

and accuracy to the financial statements as decision making is highly dependent upon the

accuracy level of financial statements.

For Example: ABC used FIFO method of inventory valuation for valuing it stock of goods and to

determine COGS. Due to increase in material costs, company started using LIFO method for

valuing its inventory for appropriately reflecting its true profit (Nasseri, Yazdifar and Askarany,

2016). Change in method of accounting should be disclosed as break in consistency.

Prudence

Principle of prudence states that revenues, profits or assets should not be overestimated at

the same time losses, expenses and liabilities should also not underestimated by companies. It is

a fundamental accounting concept which is used for increasing trustworthiness of figures being

20

Consistency

Accounting information which facilitates comparison of financial reports of company

over different accounting years is known as principle of consistency. Consistency principle

requires that financial statements of the company should follow same accounting methods,

principles, practices, procedures and practices over the accounting years. This enables users of

financial statements in making meaningful and relevant comparison over the financial years.

Consistency principles allow companies to make changes in their accounting methods to more

preferred and effective method (Miglani, Ahmed and Henry, 2015). When the changes are made

to the methods of the accounting methods it is the responsibility of companies that they are

properly disclosed and highlighted in financial statements. It will enable the user to identify the

change and the effect of changes. As per Financial Accounting Standards Board consistency is

referred as quality and characteristic which makes financial information useful to the readers.

Objective behind consistency is of avoiding the intention from executive level

management of manipulating financial information for ensuring that accounting statement of

company look healthy. There are situations where management has to use inconsistency

principle in some of its accounting transactions or in its financial records. IFRS requires the

entities to use accounting policies consistently for reporting in financial statements.

This principle is important for viewer’s financial statements, experts, shareholders and

investors. When accounting principles and policies are used consistently it gives more reliability

and accuracy to the financial statements as decision making is highly dependent upon the

accuracy level of financial statements.

For Example: ABC used FIFO method of inventory valuation for valuing it stock of goods and to

determine COGS. Due to increase in material costs, company started using LIFO method for

valuing its inventory for appropriately reflecting its true profit (Nasseri, Yazdifar and Askarany,

2016). Change in method of accounting should be disclosed as break in consistency.

Prudence

Principle of prudence states that revenues, profits or assets should not be overestimated at

the same time losses, expenses and liabilities should also not underestimated by companies. It is

a fundamental accounting concept which is used for increasing trustworthiness of figures being

20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

reported in financial statement of business. Concept of prudence state that final accounts of

company should be cautious in reporting the transactions having significant impact over income

& expenses of business (Wells and Sinclair, 2016). While preparing reports conservative

approach should be shown by accountant so that revenues, assets and profits are recorded only

when actually realized by company. Similarly proactive approach should be used by company

for recognising the liabilities, expenses and losses. In brief profits and assets should not be

overvalued unless irrefutable evidences are obtained likewise expenses and losses must not be

overvalued and provisions should be made even if there is a possibility of occurrence. It is

assumed that concept of prudence requires that company should record every situation which is

less favourable to it but it is not the truth. The motive of prudence concept is that financial

statements should represent realistic perspective regarding every event that can influence the

decisions of readers of financial statements. Prudence concept was introduced over many

standards by International Accounting Standard.

d) Purpose of depreciation in financial statement.

Accounting has the responsibility to capture each kind of transactions occurring in

company. Depreciation is treated as an expense that is related to the fixed assets of company.

Depreciation is important because it represents how much of asset is used during an accounting

year. Different types of assets are there on which depreciation is charged. It represents specific

use of asset over an accounting year. Expensing items at time of purchase create distortion in net

income. Therefore it is preferred by accounting principles that items should be recorded as assets

along with corresponding expense when company is using each item. There are different

methods of depreciation which are available in accounting (Sivathaasan, 2016). Companies are

using depreciation for reporting the assets use to its stakeholders. It reduces historical value at

which asset was recorded. Although it is represented as non-cash expense over income

statement it reduces net income of company. Lower income of company will attract lower tax

liability. For reducing the tax liabilities companies usually use accelerated method of

depreciation.

There are different methods used for depreciation in which mainly there are two:

I) Straight Line method

It is the most commonly used method of depreciation which is also known as fixed

instalment method, original cost method and fix percentage method. In this method a fixed

21

company should be cautious in reporting the transactions having significant impact over income

& expenses of business (Wells and Sinclair, 2016). While preparing reports conservative

approach should be shown by accountant so that revenues, assets and profits are recorded only

when actually realized by company. Similarly proactive approach should be used by company

for recognising the liabilities, expenses and losses. In brief profits and assets should not be

overvalued unless irrefutable evidences are obtained likewise expenses and losses must not be

overvalued and provisions should be made even if there is a possibility of occurrence. It is

assumed that concept of prudence requires that company should record every situation which is

less favourable to it but it is not the truth. The motive of prudence concept is that financial

statements should represent realistic perspective regarding every event that can influence the

decisions of readers of financial statements. Prudence concept was introduced over many

standards by International Accounting Standard.

d) Purpose of depreciation in financial statement.

Accounting has the responsibility to capture each kind of transactions occurring in

company. Depreciation is treated as an expense that is related to the fixed assets of company.

Depreciation is important because it represents how much of asset is used during an accounting

year. Different types of assets are there on which depreciation is charged. It represents specific

use of asset over an accounting year. Expensing items at time of purchase create distortion in net

income. Therefore it is preferred by accounting principles that items should be recorded as assets

along with corresponding expense when company is using each item. There are different

methods of depreciation which are available in accounting (Sivathaasan, 2016). Companies are

using depreciation for reporting the assets use to its stakeholders. It reduces historical value at

which asset was recorded. Although it is represented as non-cash expense over income

statement it reduces net income of company. Lower income of company will attract lower tax

liability. For reducing the tax liabilities companies usually use accelerated method of

depreciation.

There are different methods used for depreciation in which mainly there are two:

I) Straight Line method

It is the most commonly used method of depreciation which is also known as fixed

instalment method, original cost method and fix percentage method. In this method a fixed

21

amount of depreciation is charged every accounting year throughout the life of asset.

Depreciation rate is reciprocal of its estimated useful life of the asset. It is useful for asset that do

not lose their value over short time and remains valuable for long time.

II) Reducing Balance Method

It is the second most used method by companies for charging depreciation on its assets. It is

also known as written down method, reducing instalment method. In this method depreciation

charges are reducing every accounting year but rate of depreciation is fixed throughout the life of

asset. It is charged over written down value of asset over the life of asset (Gamayuni, 2019). It is

useful for assets who lose its significant value in initial year so that company can claim

depreciation expenses of assets.

e) Difference between financial statements of sole trader and limited company.

Limited Company Sole Proprietorship

It is a legal entity which permits

individuals or group to apply for

creation of independent organisation of

shareholders.

Tax is imposed over limited company

as it represent separate legal entity

Shareholders fund has share capital,

retained earnings, revenues and capital

reserve.

Limited company is required to follow

proper accounting standards, rules,

principles, concepts and the regulatory

framework.

Financial statements of company are

required to be audited therefore

company has to follow accounting

principles, rules and concepts (Jermias,

2017).

This is simple business structure as

only owner is charged with

responsibility to control and run the

entire business.

Tax is imposed on income of owner or

sole proprietor.

There is only one account in owner's

equity that is equity account of owner.

A sole proprietor is not subject to

accounting standards, rules or

principles. It can also decide the form

of financial statements (Sivathaasan,

2016).

Accounts of sole proprietor are not

subject to audit unless revenues

exceeds the specified limit laid down.

A single owner entity is more prone to

risks as owner has the sole

22

Depreciation rate is reciprocal of its estimated useful life of the asset. It is useful for asset that do

not lose their value over short time and remains valuable for long time.

II) Reducing Balance Method

It is the second most used method by companies for charging depreciation on its assets. It is

also known as written down method, reducing instalment method. In this method depreciation

charges are reducing every accounting year but rate of depreciation is fixed throughout the life of

asset. It is charged over written down value of asset over the life of asset (Gamayuni, 2019). It is

useful for assets who lose its significant value in initial year so that company can claim

depreciation expenses of assets.

e) Difference between financial statements of sole trader and limited company.

Limited Company Sole Proprietorship

It is a legal entity which permits

individuals or group to apply for

creation of independent organisation of

shareholders.

Tax is imposed over limited company

as it represent separate legal entity

Shareholders fund has share capital,

retained earnings, revenues and capital

reserve.

Limited company is required to follow

proper accounting standards, rules,

principles, concepts and the regulatory

framework.

Financial statements of company are

required to be audited therefore

company has to follow accounting

principles, rules and concepts (Jermias,

2017).

This is simple business structure as

only owner is charged with

responsibility to control and run the

entire business.

Tax is imposed on income of owner or

sole proprietor.

There is only one account in owner's

equity that is equity account of owner.

A sole proprietor is not subject to

accounting standards, rules or

principles. It can also decide the form

of financial statements (Sivathaasan,

2016).

Accounts of sole proprietor are not

subject to audit unless revenues

exceeds the specified limit laid down.

A single owner entity is more prone to

risks as owner has the sole

22

In the case of company lenders could

initiate litigations and gain financial

recourse if the liabilities are not repaid

on time.

responsibility of repaying its liabilities.

CLIENT 3

A) Purpose of preparing Bank Reconciliation Statement

A reconciliation statement is prepared for comparing the records of business with that of its

bank for identifying the difference between the two records of cash transactions. Closing balance

of cash records prepared by business is known as book balance where the ending balance of bank

statement is known as bank balance. There would be differences between the 2 balances that are

required to be figured out by business and adjusted in the records. Ignoring the differences by

business will create substantial variances among the cash balances and the balance in bank

account. The reconciliation of statement is important so that it can identify the bounced cheques

of customers. Cheques that were issued and altered or stolen or cashed without knowledge of

the authorised business (Jermias, 2017). Detecting fraud is one of the key reason behind

preparation of bank reconciliation. When company is having fraudulent transactions it is

essential to reconcile its bank statements on monthly or even on weekly basis so that it can

identify and detect problems at instance.

Any standard method is not there for reconciling the statements but double entry system

of accounting is considered by GAAP. There are two methods of reconciliation which are double

entry reconciliation & account conversion. In double entry system which is generally used by

entities all transactions have dual effect in balance sheet. Whereas in method of account

conversion transaction record like cancelled cheques or receipts are only compared with ledger

entries (Purpose of preparing Bank Reconciliation Statements. 2019).

It is not mandatory for businesses to prepare bank reconciliation statement and also there

is no time frame or date within which it is to be prepared. But even than it is prepared on

periodical basis to check transactions relating to bank are properly recorded in bank column of

cash book. It will enable the company to detect errors occurred in recording the transactions so

that it can determine accurate bank balance on particular date (Gepp, Kumar and Bhattacharya,

23

initiate litigations and gain financial

recourse if the liabilities are not repaid

on time.

responsibility of repaying its liabilities.

CLIENT 3

A) Purpose of preparing Bank Reconciliation Statement

A reconciliation statement is prepared for comparing the records of business with that of its

bank for identifying the difference between the two records of cash transactions. Closing balance

of cash records prepared by business is known as book balance where the ending balance of bank

statement is known as bank balance. There would be differences between the 2 balances that are

required to be figured out by business and adjusted in the records. Ignoring the differences by

business will create substantial variances among the cash balances and the balance in bank

account. The reconciliation of statement is important so that it can identify the bounced cheques

of customers. Cheques that were issued and altered or stolen or cashed without knowledge of

the authorised business (Jermias, 2017). Detecting fraud is one of the key reason behind

preparation of bank reconciliation. When company is having fraudulent transactions it is

essential to reconcile its bank statements on monthly or even on weekly basis so that it can

identify and detect problems at instance.

Any standard method is not there for reconciling the statements but double entry system

of accounting is considered by GAAP. There are two methods of reconciliation which are double

entry reconciliation & account conversion. In double entry system which is generally used by

entities all transactions have dual effect in balance sheet. Whereas in method of account

conversion transaction record like cancelled cheques or receipts are only compared with ledger

entries (Purpose of preparing Bank Reconciliation Statements. 2019).

It is not mandatory for businesses to prepare bank reconciliation statement and also there

is no time frame or date within which it is to be prepared. But even than it is prepared on

periodical basis to check transactions relating to bank are properly recorded in bank column of

cash book. It will enable the company to detect errors occurred in recording the transactions so

that it can determine accurate bank balance on particular date (Gepp, Kumar and Bhattacharya,

23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2016). There are various benefits behind preparing BRS. It assists business in detecting frauds

and to reduce transaction risks that can lead to penalties and fines. Some of the benefits are:

Detection of Errors – BRS helps to spot out errors that are common in any business.

Mistakes under are defined as errors like additions, subtraction, miss payments or double

payments.

To track Interest and Fees - Sometimes banks add payments of interest, penalties and

fees in bank account which are to be adjusted in the books.

To detect frauds – Employees cannot be prevented from stealing the money once but

however could be prevented in future. Reconciliation help to detect and spot fraudulent

transaction in the business. It should be prepared by an independent employee so that employees

can be prevented from manipulating the books & reconciliation (Bay, 2018).

Tracking Receivables – It allows business in confirming all its receipts so that company

would not be required to face any default in payments due to payment issues.

B) Listing the areas that vary the record of bank and cash book.

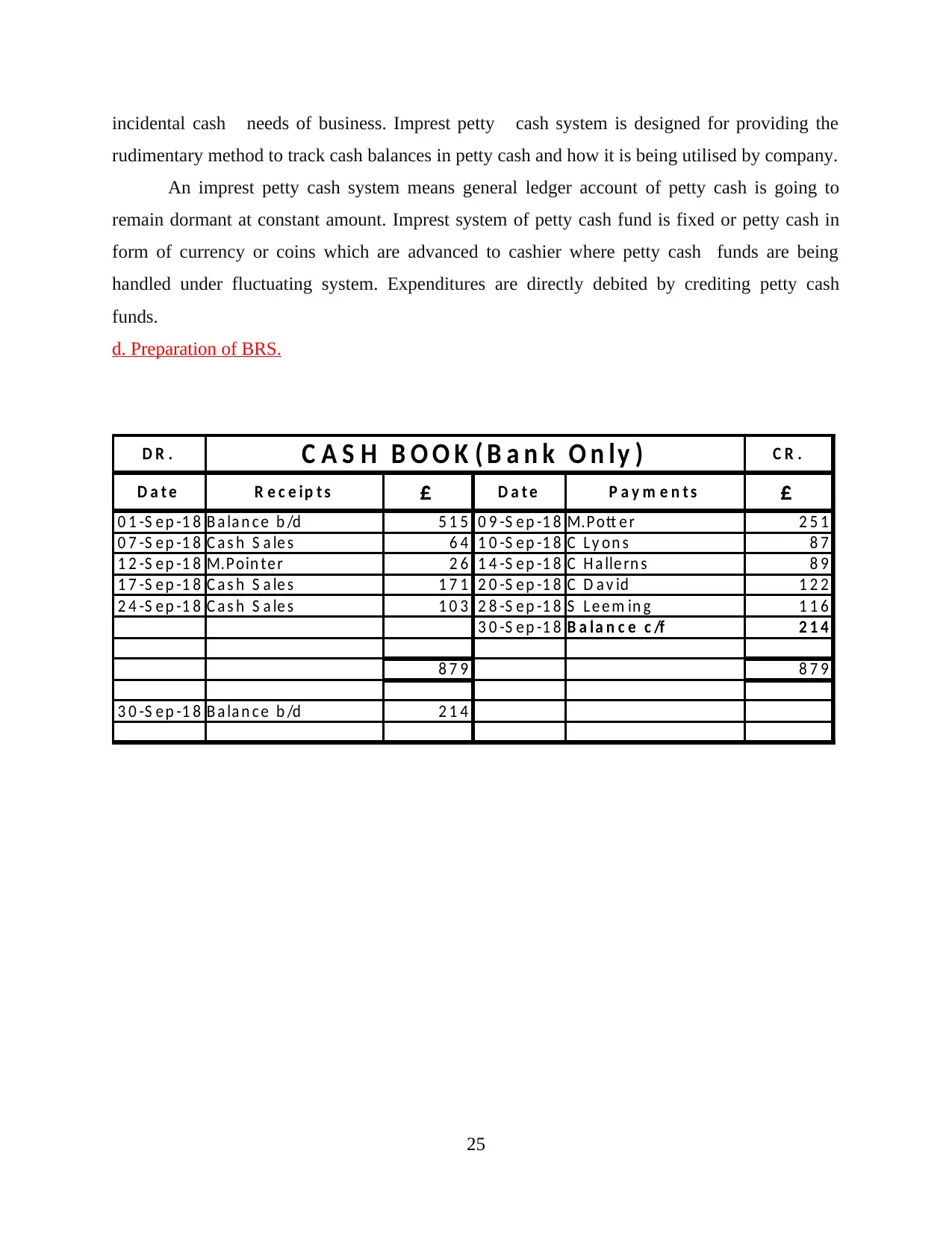

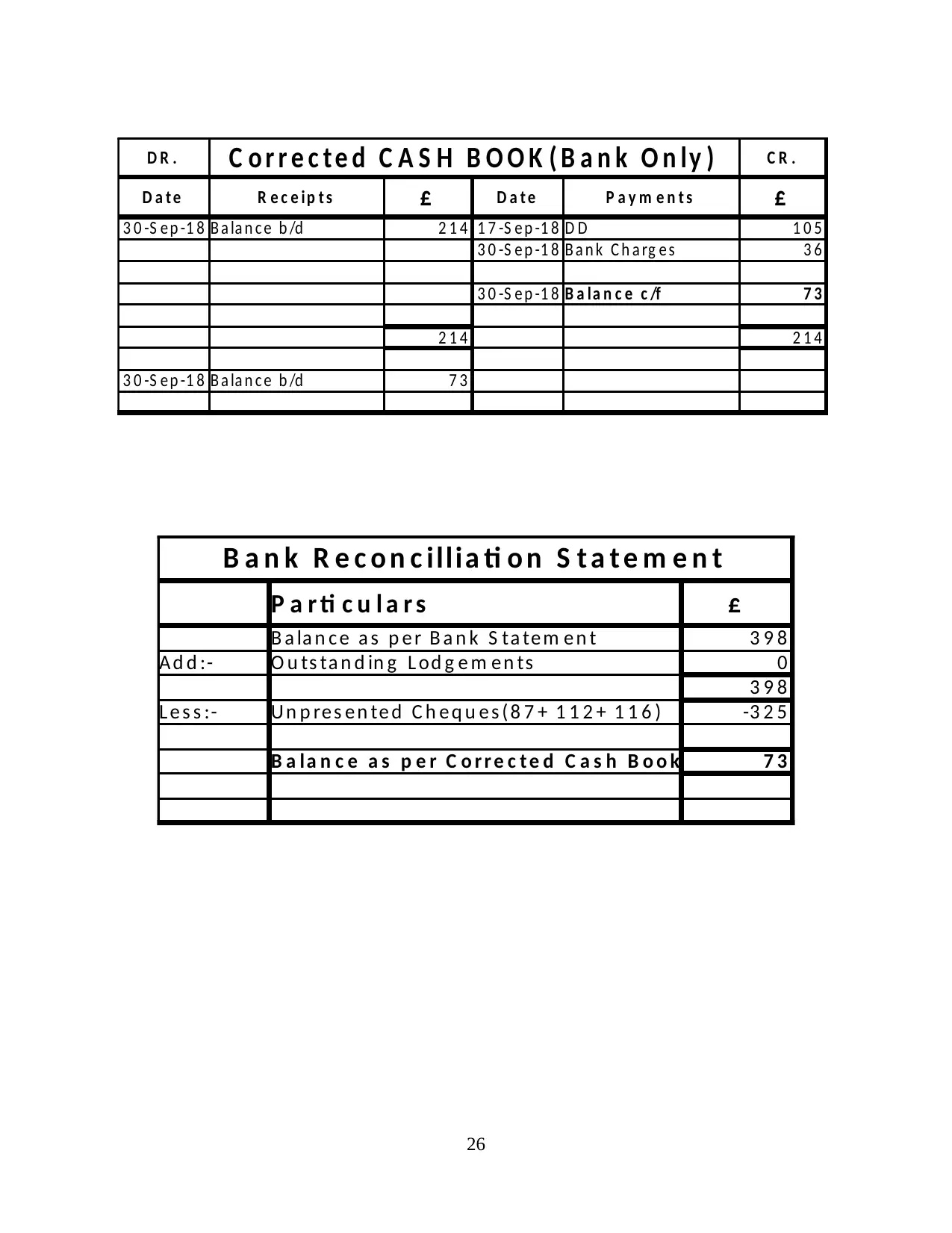

Where the cheques has been deposited but not credited in bank statements.

Where bank charges have been charged but not recorded in cash book.

When cheques are issued by company but are not cleared.