Financial Accounting Principles and Applications Report, UK

VerifiedAdded on 2020/12/24

|36

|9395

|326

Report

AI Summary

This report provides a detailed exploration of financial accounting principles and their practical applications. It begins with an introduction to financial accounting, its purposes, and the relevant regulations, including IFRS and IASB. The report then describes key accounting rules and principles such as the business entity concept, dual aspect concept, and money measurement concept. It also covers the conventions of consistency and material disclosure. Part B of the report applies double-entry bookkeeping, analyzes transactions, and prepares financial statements for various clients, including profit and loss statements, balance sheets, and cash flow statements. The report also includes bank reconciliation processes and control account procedures. The conclusion summarizes the key findings and concepts discussed throughout the report.

FINANCIAL

ACCOUNTING

PRINCIPLE

ACCOUNTING

PRINCIPLE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

BUSINESS REPORT......................................................................................................................1

Financial accounting and its purposes....................................................................................1

The regulations relating to financial accounting....................................................................2

Describe accounting rules and principles...............................................................................3

Explain the convections and concepts relating to consistency and material disclosure.........5

PART B............................................................................................................................................6

CLIENT 1........................................................................................................................................6

P1 Apply the double entry book keeping system of debits and credit and record sales and

purchases transactions in a general ledger..............................................................................6

M1 Analyse the transactions to show the progression from a previous trial balance to the next

one using double entry book keeping...................................................................................21

D1 Apply trial balance figures to show which statement of financial accounts they will end up

..............................................................................................................................................22

CLIENT 2......................................................................................................................................22

P3 Financial accounts from given trial balance figures adjusting, depreciation and preparation

..............................................................................................................................................22

P4 Financial accounts subject to sole traders, partnerships or limited companies...............23

M2 Evaluation of profit and loss account, balance sheet and cash flow statement..............24

D2 Compare the essential features of each financial statement to analyse the differences

between them in terms purpose, structure and content.........................................................24

CLIENT 3......................................................................................................................................26

a) Profit and loss statement of Ltd. For the year ended 31st July 2018..............................26

(b) Statement of financial statement of Bowling Ltd...........................................................26

(c) Accounting Concepts:.....................................................................................................27

(d) Purpose of Depreciation in formulating Accounting statements and the methods used for

calculation of Depreciation:.................................................................................................28

CLIENT 4......................................................................................................................................28

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

BUSINESS REPORT......................................................................................................................1

Financial accounting and its purposes....................................................................................1

The regulations relating to financial accounting....................................................................2

Describe accounting rules and principles...............................................................................3

Explain the convections and concepts relating to consistency and material disclosure.........5

PART B............................................................................................................................................6

CLIENT 1........................................................................................................................................6

P1 Apply the double entry book keeping system of debits and credit and record sales and

purchases transactions in a general ledger..............................................................................6

M1 Analyse the transactions to show the progression from a previous trial balance to the next

one using double entry book keeping...................................................................................21

D1 Apply trial balance figures to show which statement of financial accounts they will end up

..............................................................................................................................................22

CLIENT 2......................................................................................................................................22

P3 Financial accounts from given trial balance figures adjusting, depreciation and preparation

..............................................................................................................................................22

P4 Financial accounts subject to sole traders, partnerships or limited companies...............23

M2 Evaluation of profit and loss account, balance sheet and cash flow statement..............24

D2 Compare the essential features of each financial statement to analyse the differences

between them in terms purpose, structure and content.........................................................24

CLIENT 3......................................................................................................................................26

a) Profit and loss statement of Ltd. For the year ended 31st July 2018..............................26

(b) Statement of financial statement of Bowling Ltd...........................................................26

(c) Accounting Concepts:.....................................................................................................27

(d) Purpose of Depreciation in formulating Accounting statements and the methods used for

calculation of Depreciation:.................................................................................................28

CLIENT 4......................................................................................................................................28

P5 Apply the bank reconciliation process to make a number of a reconciliation................28

(a) Need and Importance of Bank Reconciliation Statements:............................................28

M3 Apply the reconciliation process demonstrating the use of deposit in transit................29

D3 Accurate bank reconciliation statement..........................................................................29

CLIENT 5......................................................................................................................................30

(a) Control account...............................................................................................................30

(b) Ledger control accounts..................................................................................................30

CLIENT 6......................................................................................................................................31

P6 Process to be taken to reconcile control accounts and clear suspense account...............31

M4 Understanding of the type of accounts and how and why these accounts need to

reconciled.............................................................................................................................31

CONCLUSION..............................................................................................................................32

REFERENCES..............................................................................................................................33

(a) Need and Importance of Bank Reconciliation Statements:............................................28

M3 Apply the reconciliation process demonstrating the use of deposit in transit................29

D3 Accurate bank reconciliation statement..........................................................................29

CLIENT 5......................................................................................................................................30

(a) Control account...............................................................................................................30

(b) Ledger control accounts..................................................................................................30

CLIENT 6......................................................................................................................................31

P6 Process to be taken to reconcile control accounts and clear suspense account...............31

M4 Understanding of the type of accounts and how and why these accounts need to

reconciled.............................................................................................................................31

CONCLUSION..............................................................................................................................32

REFERENCES..............................................................................................................................33

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting is the process of recording, summarizing and reporting the

transaction in final report or statement such as cash flow, income statement and balance sheet

(Tassadaq and Malik, 2015). The final reports are prepared through accounting standards that are

followed by every organisation. These standards help to prepare financial statement in

appropriate format and show performance of the company in front of creditors, suppliers and

customers. Purpose of financial accounting is to provide accurate information about company to

existing and potential stakeholders regarding investment decisions. Oktra, a small organization

which based on UK has been chosen for this project.

This project report focused on double entry book keeping system and extract a trial

balance. There is statement of financial accounts according to sole traders, partnership and

limited companies. Creating a bank reconciliation statement, use of suspense account and way in

which it can help to ignore errors in trial balance.

PART A

BUSINESS REPORT

Financial accounting and its purposes

Financial accounting is a specialized branch of accounting that is used by several

companies to record, analyse, monitor and control various transaction of business. With the help

of this the company can track all records and create a detailed summary related to its financial

transactions. In the company when accounts are produced and displayed of financial information

in reports and presented in front of customers, creditor, suppliers of an organisation. Financial

accounting consists of different statements such as trading account to ascertain gross profit/loss,

Income statement account for net profit/net loss, cash flow to know different activities of

business relating to investment, operation and financial and balance sheet for present

performance of company (Maskell, Baggaley and Grasso, 2016). Oktra can attract more

investors by providing them reliable financial information of their organisational operational

activities. It is very essential for Oktra since it provides all the necessary information that is

needed by public for investment purposes. With the help of these statements the investors know

about financial strength of the business and an analysis of weak points that need to be contained.

It provides help to Oktra's top management to take effective and appropriate decisions regarding

1

Financial accounting is the process of recording, summarizing and reporting the

transaction in final report or statement such as cash flow, income statement and balance sheet

(Tassadaq and Malik, 2015). The final reports are prepared through accounting standards that are

followed by every organisation. These standards help to prepare financial statement in

appropriate format and show performance of the company in front of creditors, suppliers and

customers. Purpose of financial accounting is to provide accurate information about company to

existing and potential stakeholders regarding investment decisions. Oktra, a small organization

which based on UK has been chosen for this project.

This project report focused on double entry book keeping system and extract a trial

balance. There is statement of financial accounts according to sole traders, partnership and

limited companies. Creating a bank reconciliation statement, use of suspense account and way in

which it can help to ignore errors in trial balance.

PART A

BUSINESS REPORT

Financial accounting and its purposes

Financial accounting is a specialized branch of accounting that is used by several

companies to record, analyse, monitor and control various transaction of business. With the help

of this the company can track all records and create a detailed summary related to its financial

transactions. In the company when accounts are produced and displayed of financial information

in reports and presented in front of customers, creditor, suppliers of an organisation. Financial

accounting consists of different statements such as trading account to ascertain gross profit/loss,

Income statement account for net profit/net loss, cash flow to know different activities of

business relating to investment, operation and financial and balance sheet for present

performance of company (Maskell, Baggaley and Grasso, 2016). Oktra can attract more

investors by providing them reliable financial information of their organisational operational

activities. It is very essential for Oktra since it provides all the necessary information that is

needed by public for investment purposes. With the help of these statements the investors know

about financial strength of the business and an analysis of weak points that need to be contained.

It provides help to Oktra's top management to take effective and appropriate decisions regarding

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company in order to achieve their set objectives and goals. Different types of financial

statements are prepared that are important for a business, they are as follows -

Profit and loss statement - The statement of profit and loss is one of the company's core

financial statements that present their profit and loss for a specific time period. There is

calculated net profit and loss after determination of all revenues, incomes and other operating

and non-operating activities. It is an essential part of one of three statements that is used by Oktra

to present their performance. On an income statement, Revenues – Expenses = Net income. The

statement is prepared according to time period and follow operations of company. It is very

important for a business to keep a detailed information of its revenues to pay different expenses

such as taxes, interest, commission etc. (Francis, and et. Al, 2015).

Balance sheet – A balance sheet is a statement of the financial status of a company

which refers to the assets, liabilities and owners’ equity at a specific time. In additional way, it

represents the net worth of a business. With the help of balance sheet the financial position of

Oktra can be provided to its shareholders, customers, suppliers, investors and other external

activities. On a balance sheet, Assets = Liabilities + Stockholders' equity. It is divided into two

sections, left side of the balance sheet outlines all assets and in right side outlines all liabilities

and shareholders' equity.

Cash flow statement – It is a statement which is used to measure all transactions related

to cash that are done by business in a particular financial year. Cash flow statement is divided

into three categories– cash flow from operating activities, cash flow from investing activities and

cash flow from financing activities. It is important to know that cash flow is not the same as net

income because it does not involve actual transfer of money (Collins, Pasewark and Riley, 2012)

.

Purpose of financial accounting -

It is providing financial information about the performance, cash flows and financial

position of the company.

This financial information helps to take investment, credit and taxation decisions

regarding to company.

The regulations relating to financial accounting

For better understanding, different types rules, regulations and principles have been

developed for proper formulation of organization's financial statements. These regulations are

2

statements are prepared that are important for a business, they are as follows -

Profit and loss statement - The statement of profit and loss is one of the company's core

financial statements that present their profit and loss for a specific time period. There is

calculated net profit and loss after determination of all revenues, incomes and other operating

and non-operating activities. It is an essential part of one of three statements that is used by Oktra

to present their performance. On an income statement, Revenues – Expenses = Net income. The

statement is prepared according to time period and follow operations of company. It is very

important for a business to keep a detailed information of its revenues to pay different expenses

such as taxes, interest, commission etc. (Francis, and et. Al, 2015).

Balance sheet – A balance sheet is a statement of the financial status of a company

which refers to the assets, liabilities and owners’ equity at a specific time. In additional way, it

represents the net worth of a business. With the help of balance sheet the financial position of

Oktra can be provided to its shareholders, customers, suppliers, investors and other external

activities. On a balance sheet, Assets = Liabilities + Stockholders' equity. It is divided into two

sections, left side of the balance sheet outlines all assets and in right side outlines all liabilities

and shareholders' equity.

Cash flow statement – It is a statement which is used to measure all transactions related

to cash that are done by business in a particular financial year. Cash flow statement is divided

into three categories– cash flow from operating activities, cash flow from investing activities and

cash flow from financing activities. It is important to know that cash flow is not the same as net

income because it does not involve actual transfer of money (Collins, Pasewark and Riley, 2012)

.

Purpose of financial accounting -

It is providing financial information about the performance, cash flows and financial

position of the company.

This financial information helps to take investment, credit and taxation decisions

regarding to company.

The regulations relating to financial accounting

For better understanding, different types rules, regulations and principles have been

developed for proper formulation of organization's financial statements. These regulations are

2

help to maintain their financial account in an accurate way. All companies including Oktra

follow particular rules and regulations of financial accounting applicable to it. These regulations

provide guidance to investor for analysis of income statements, balance sheet and cash flow

statement. These regulations are introduced by regulatory authority of a country for recording

information in financial statement in appropriate way (Watrin, Pott and Ullmann, 2012). It is

possible to get reliable information from various statement. There are following reliable

regulations -

IFRS – International financial reporting standard was introduced a set of world wide

language. The businesses are using standards for their accounts and mangers apply them to

expand their business globally. There is continuous application of different accounting standards

according to different transactions.

IASB – International accounting standard board is a regularity authority who is liable to

introduce and develop several international financial accounting standards. It has been

introduced by IFRS that are formulated to guide organisations while preparing financial

accounts. At time when organisations are recording transactions in books they follow their rules

and regulations.

IFRS 9 – It is applied in financial accounting instruments for different financial

statements. With the help of this regulation the company can easily measure and identify their

financial assets.

IFRS 10 – It provides a guideline to combined businesses who formulate their financial

statements in consolidated form. It is mainly developed for parent entity which is responsible for

their subsidiaries.

Describe accounting rules and principles

Accounting principles are a set of rules and guidelines followed by companies while

preparing a financial report. The principles of accounting define particular criteria under which

all companies have to maintain their economic transactions in accounting books. There are

following accounting principles -

Business entity concept –

The business entity concept defines that entity of a business are presented as separate

legal entity distinct from its members (Lobo and Zhao, 2013). It means Oktra has a personal

identification on the basis of which it can carry out transactions in its own name, sue or be sued

3

follow particular rules and regulations of financial accounting applicable to it. These regulations

provide guidance to investor for analysis of income statements, balance sheet and cash flow

statement. These regulations are introduced by regulatory authority of a country for recording

information in financial statement in appropriate way (Watrin, Pott and Ullmann, 2012). It is

possible to get reliable information from various statement. There are following reliable

regulations -

IFRS – International financial reporting standard was introduced a set of world wide

language. The businesses are using standards for their accounts and mangers apply them to

expand their business globally. There is continuous application of different accounting standards

according to different transactions.

IASB – International accounting standard board is a regularity authority who is liable to

introduce and develop several international financial accounting standards. It has been

introduced by IFRS that are formulated to guide organisations while preparing financial

accounts. At time when organisations are recording transactions in books they follow their rules

and regulations.

IFRS 9 – It is applied in financial accounting instruments for different financial

statements. With the help of this regulation the company can easily measure and identify their

financial assets.

IFRS 10 – It provides a guideline to combined businesses who formulate their financial

statements in consolidated form. It is mainly developed for parent entity which is responsible for

their subsidiaries.

Describe accounting rules and principles

Accounting principles are a set of rules and guidelines followed by companies while

preparing a financial report. The principles of accounting define particular criteria under which

all companies have to maintain their economic transactions in accounting books. There are

following accounting principles -

Business entity concept –

The business entity concept defines that entity of a business are presented as separate

legal entity distinct from its members (Lobo and Zhao, 2013). It means Oktra has a personal

identification on the basis of which it can carry out transactions in its own name, sue or be sued

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and open account in bank. If all members leave the company there will be no impact seen on the

existence of Oktra, it will exist regardless.

Dual aspect concept –

According to this concept most of the companies follow this principle to show accurate

amount of particular transaction by recording it twice. If Oktra selects a single entry system it

would lead to irrelevant information since only one aspect of every transaction would be

recorded in its books. Therefore, to avoid this problem, financial accounting assure that every

single transaction has two aspects- debit side and credit side.

Money measurement concept –

The principle of money measurement is based on money value, it means only those

transactions shall be recorded in the books of Oktra that can be measured in money.

Cost principle –

From an accounting point of view, the term cost refers to the amount expended to

acquire an asset for business purposes. According to this principle, amounts are recorded at their

acquisition cost at the time of its purchase or acquisition in a financial year with an appropriation

for depreciation thereafter (Brief and Peasnell, 2013).

Going concern concept –

In this principle of accounting the business has expected to continue for long time as an

entity. This concept does not concern members of the company since it is a separate identity

expected to continue business perpetually.

Financial accounting year –

According to this principle, each business follows a particular financial year to prepare

their accounting books for quarterly, monthly or yearly basis. Generally, accounting period

adopted by companies is 1 April to 31 march as financial year.

Matching principle -

According to this principle, all expenses must be matched with their related revenues

generated in same accounting period. It means expenses and revenues are recorded in books of

same accounting year.

Accounting rules -

4

existence of Oktra, it will exist regardless.

Dual aspect concept –

According to this concept most of the companies follow this principle to show accurate

amount of particular transaction by recording it twice. If Oktra selects a single entry system it

would lead to irrelevant information since only one aspect of every transaction would be

recorded in its books. Therefore, to avoid this problem, financial accounting assure that every

single transaction has two aspects- debit side and credit side.

Money measurement concept –

The principle of money measurement is based on money value, it means only those

transactions shall be recorded in the books of Oktra that can be measured in money.

Cost principle –

From an accounting point of view, the term cost refers to the amount expended to

acquire an asset for business purposes. According to this principle, amounts are recorded at their

acquisition cost at the time of its purchase or acquisition in a financial year with an appropriation

for depreciation thereafter (Brief and Peasnell, 2013).

Going concern concept –

In this principle of accounting the business has expected to continue for long time as an

entity. This concept does not concern members of the company since it is a separate identity

expected to continue business perpetually.

Financial accounting year –

According to this principle, each business follows a particular financial year to prepare

their accounting books for quarterly, monthly or yearly basis. Generally, accounting period

adopted by companies is 1 April to 31 march as financial year.

Matching principle -

According to this principle, all expenses must be matched with their related revenues

generated in same accounting period. It means expenses and revenues are recorded in books of

same accounting year.

Accounting rules -

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For recording transaction in accounting books, we follow 'Three Golden Rules'. Double

entry system is followed to show dual effect of each transaction. The Three Golden Rules relate

to personal account, real account and nominal account. Basic rules are as follows -

1. Debit the receiver and credit the giver : This rule is applicable on Personal Account,

which is related to any individual, company or firm. Since in eyes of law, companies and

firms are legal entities considered as legal person (Nilsson and Stockenstrand, 2015).

This rule means, a person who receives something on behalf of Oktra is called Receiver

and amount is posted in debit column of their account, and same as if any person paid

something on behalf of Oktra is called Giver and amount will be posted in credit column

of their account.

2. Debit what comes in and credit what goes out : This principle is used for Real Account,

which includes all assets of organisation like machinery, building , land etc. And those

assets which come in business through purchase they will be debited in it's account and

anything going from business through sales will be credited in it's account.

3. Debit all expenses and credit all incomes : This principle is used for Nominal Account, it

includes all expenses and all incomes and gains of organisation. In this rule, we debit all

expenses and credit all incomes and gains incurred/received in organisation at the time of

production or sale respectively.

Explain the convections and concepts relating to consistency and material disclosure

Consistency convections – This convection of accounting states that it is used to

maintain a record with the same concept that was followed in previous years. Oktra will continue

to use it in same sequence in financial periods. To show effects in accounting results appropriate

methods should be adopted in case changes are made in accounting policies. Hence, the concept

of consistency assures that policies, method and practices of preparing the financial statements

remains same (Kirsch, 2012). This will help to easily analyse financial information from past

years. For investment decisions, internal and external shareholders analyse financial information

from past activities. Business consistency needs to be maintained for smooth auditing processes.

This concept helps in effortless comparison of financial performance from one period to another.

Material disclosure convention - The Convection of full material disclosure requires

revelation of all information, both favourable and non-favourable regarding to a business

enterprise. These material value are fully disclosed in annual report regarding to debtors and

5

entry system is followed to show dual effect of each transaction. The Three Golden Rules relate

to personal account, real account and nominal account. Basic rules are as follows -

1. Debit the receiver and credit the giver : This rule is applicable on Personal Account,

which is related to any individual, company or firm. Since in eyes of law, companies and

firms are legal entities considered as legal person (Nilsson and Stockenstrand, 2015).

This rule means, a person who receives something on behalf of Oktra is called Receiver

and amount is posted in debit column of their account, and same as if any person paid

something on behalf of Oktra is called Giver and amount will be posted in credit column

of their account.

2. Debit what comes in and credit what goes out : This principle is used for Real Account,

which includes all assets of organisation like machinery, building , land etc. And those

assets which come in business through purchase they will be debited in it's account and

anything going from business through sales will be credited in it's account.

3. Debit all expenses and credit all incomes : This principle is used for Nominal Account, it

includes all expenses and all incomes and gains of organisation. In this rule, we debit all

expenses and credit all incomes and gains incurred/received in organisation at the time of

production or sale respectively.

Explain the convections and concepts relating to consistency and material disclosure

Consistency convections – This convection of accounting states that it is used to

maintain a record with the same concept that was followed in previous years. Oktra will continue

to use it in same sequence in financial periods. To show effects in accounting results appropriate

methods should be adopted in case changes are made in accounting policies. Hence, the concept

of consistency assures that policies, method and practices of preparing the financial statements

remains same (Kirsch, 2012). This will help to easily analyse financial information from past

years. For investment decisions, internal and external shareholders analyse financial information

from past activities. Business consistency needs to be maintained for smooth auditing processes.

This concept helps in effortless comparison of financial performance from one period to another.

Material disclosure convention - The Convection of full material disclosure requires

revelation of all information, both favourable and non-favourable regarding to a business

enterprise. These material value are fully disclosed in annual report regarding to debtors and

5

creditors. IFRS 7 also states that financial information of preceding financial year must be

disclosed in front of its users. Users include both internal and external user. External users

concern suppliers, financial institutions that provide loans for industrial growth, tax authorities

and potential investors and many more. Internal users include top-level managers, middle-level

managers, lower-lever managers and board of directors (Bryer, 2013).

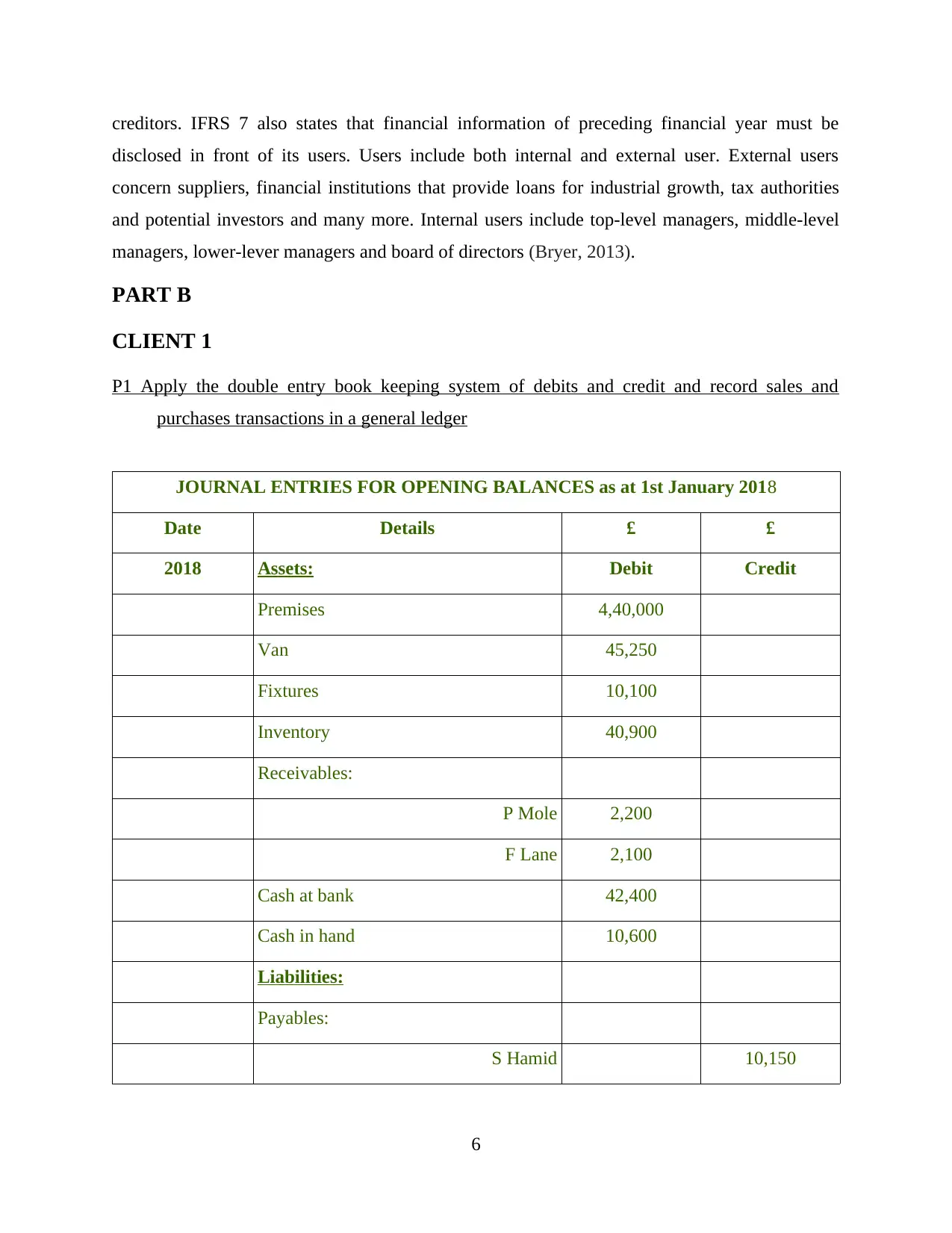

PART B

CLIENT 1

P1 Apply the double entry book keeping system of debits and credit and record sales and

purchases transactions in a general ledger

JOURNAL ENTRIES FOR OPENING BALANCES as at 1st January 2018

Date Details £ £

2018 Assets: Debit Credit

Premises 4,40,000

Van 45,250

Fixtures 10,100

Inventory 40,900

Receivables:

P Mole 2,200

F Lane 2,100

Cash at bank 42,400

Cash in hand 10,600

Liabilities:

Payables:

S Hamid 10,150

6

disclosed in front of its users. Users include both internal and external user. External users

concern suppliers, financial institutions that provide loans for industrial growth, tax authorities

and potential investors and many more. Internal users include top-level managers, middle-level

managers, lower-lever managers and board of directors (Bryer, 2013).

PART B

CLIENT 1

P1 Apply the double entry book keeping system of debits and credit and record sales and

purchases transactions in a general ledger

JOURNAL ENTRIES FOR OPENING BALANCES as at 1st January 2018

Date Details £ £

2018 Assets: Debit Credit

Premises 4,40,000

Van 45,250

Fixtures 10,100

Inventory 40,900

Receivables:

P Mole 2,200

F Lane 2,100

Cash at bank 42,400

Cash in hand 10,600

Liabilities:

Payables:

S Hamid 10,150

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

J Brown 9,600

Equity:

Opening capital at 1st January 2018 5,73,800

5,93,550 5,93,550

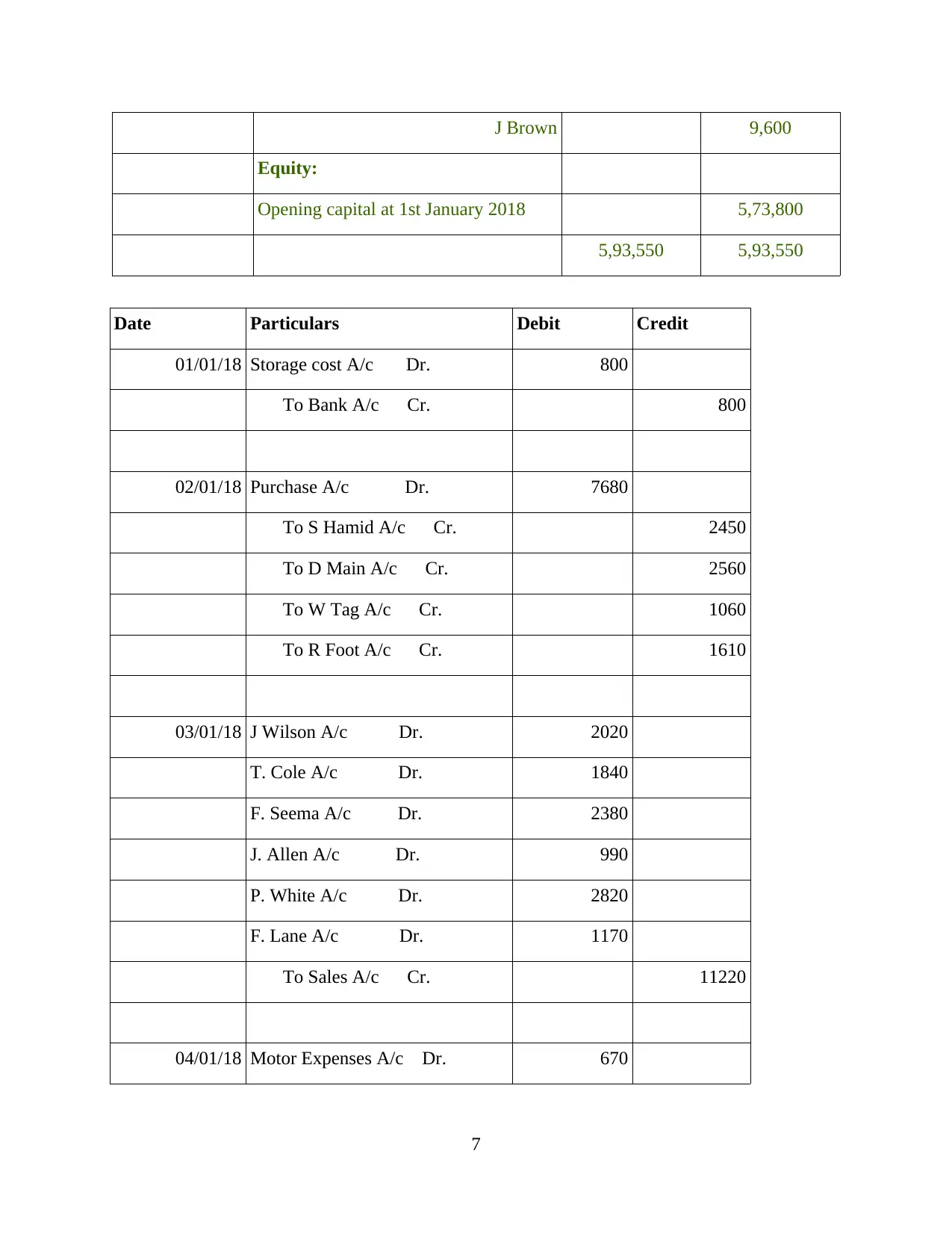

Date Particulars Debit Credit

01/01/18 Storage cost A/c Dr. 800

To Bank A/c Cr. 800

02/01/18 Purchase A/c Dr. 7680

To S Hamid A/c Cr. 2450

To D Main A/c Cr. 2560

To W Tag A/c Cr. 1060

To R Foot A/c Cr. 1610

03/01/18 J Wilson A/c Dr. 2020

T. Cole A/c Dr. 1840

F. Seema A/c Dr. 2380

J. Allen A/c Dr. 990

P. White A/c Dr. 2820

F. Lane A/c Dr. 1170

To Sales A/c Cr. 11220

04/01/18 Motor Expenses A/c Dr. 670

7

Equity:

Opening capital at 1st January 2018 5,73,800

5,93,550 5,93,550

Date Particulars Debit Credit

01/01/18 Storage cost A/c Dr. 800

To Bank A/c Cr. 800

02/01/18 Purchase A/c Dr. 7680

To S Hamid A/c Cr. 2450

To D Main A/c Cr. 2560

To W Tag A/c Cr. 1060

To R Foot A/c Cr. 1610

03/01/18 J Wilson A/c Dr. 2020

T. Cole A/c Dr. 1840

F. Seema A/c Dr. 2380

J. Allen A/c Dr. 990

P. White A/c Dr. 2820

F. Lane A/c Dr. 1170

To Sales A/c Cr. 11220

04/01/18 Motor Expenses A/c Dr. 670

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

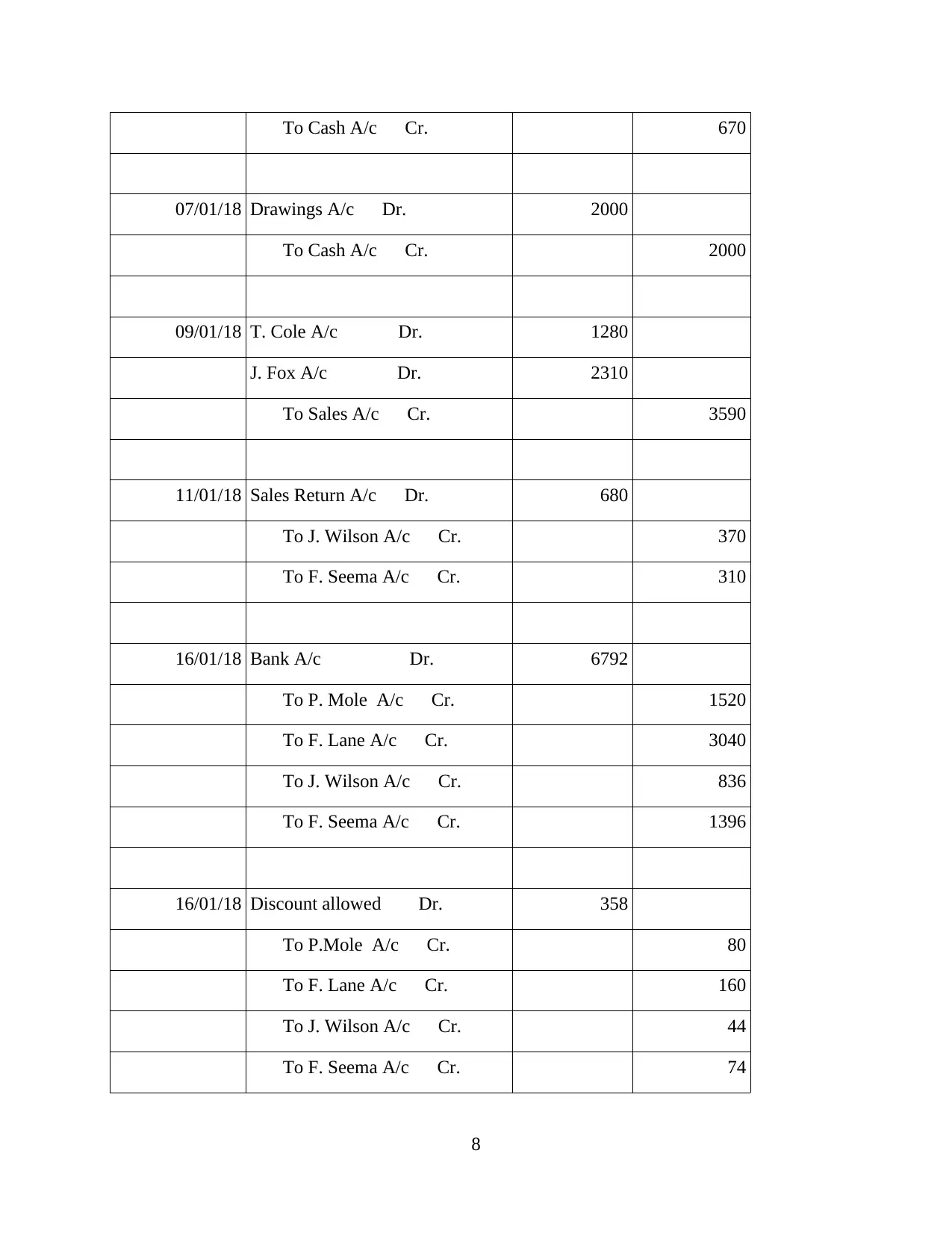

To Cash A/c Cr. 670

07/01/18 Drawings A/c Dr. 2000

To Cash A/c Cr. 2000

09/01/18 T. Cole A/c Dr. 1280

J. Fox A/c Dr. 2310

To Sales A/c Cr. 3590

11/01/18 Sales Return A/c Dr. 680

To J. Wilson A/c Cr. 370

To F. Seema A/c Cr. 310

16/01/18 Bank A/c Dr. 6792

To P. Mole A/c Cr. 1520

To F. Lane A/c Cr. 3040

To J. Wilson A/c Cr. 836

To F. Seema A/c Cr. 1396

16/01/18 Discount allowed Dr. 358

To P.Mole A/c Cr. 80

To F. Lane A/c Cr. 160

To J. Wilson A/c Cr. 44

To F. Seema A/c Cr. 74

8

07/01/18 Drawings A/c Dr. 2000

To Cash A/c Cr. 2000

09/01/18 T. Cole A/c Dr. 1280

J. Fox A/c Dr. 2310

To Sales A/c Cr. 3590

11/01/18 Sales Return A/c Dr. 680

To J. Wilson A/c Cr. 370

To F. Seema A/c Cr. 310

16/01/18 Bank A/c Dr. 6792

To P. Mole A/c Cr. 1520

To F. Lane A/c Cr. 3040

To J. Wilson A/c Cr. 836

To F. Seema A/c Cr. 1396

16/01/18 Discount allowed Dr. 358

To P.Mole A/c Cr. 80

To F. Lane A/c Cr. 160

To J. Wilson A/c Cr. 44

To F. Seema A/c Cr. 74

8

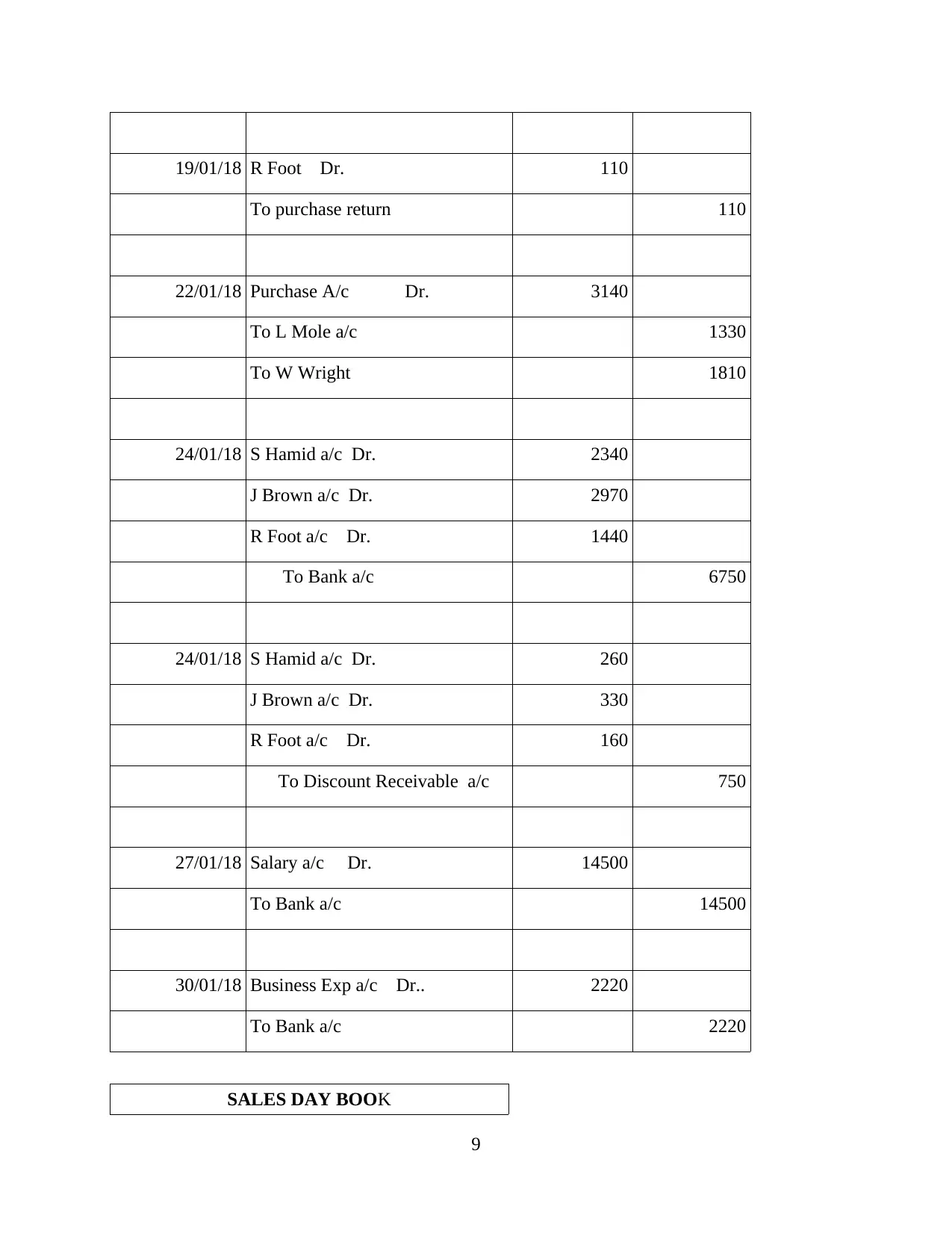

19/01/18 R Foot Dr. 110

To purchase return 110

22/01/18 Purchase A/c Dr. 3140

To L Mole a/c 1330

To W Wright 1810

24/01/18 S Hamid a/c Dr. 2340

J Brown a/c Dr. 2970

R Foot a/c Dr. 1440

To Bank a/c 6750

24/01/18 S Hamid a/c Dr. 260

J Brown a/c Dr. 330

R Foot a/c Dr. 160

To Discount Receivable a/c 750

27/01/18 Salary a/c Dr. 14500

To Bank a/c 14500

30/01/18 Business Exp a/c Dr.. 2220

To Bank a/c 2220

SALES DAY BOOK

9

To purchase return 110

22/01/18 Purchase A/c Dr. 3140

To L Mole a/c 1330

To W Wright 1810

24/01/18 S Hamid a/c Dr. 2340

J Brown a/c Dr. 2970

R Foot a/c Dr. 1440

To Bank a/c 6750

24/01/18 S Hamid a/c Dr. 260

J Brown a/c Dr. 330

R Foot a/c Dr. 160

To Discount Receivable a/c 750

27/01/18 Salary a/c Dr. 14500

To Bank a/c 14500

30/01/18 Business Exp a/c Dr.. 2220

To Bank a/c 2220

SALES DAY BOOK

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.