Financial Accounting Assignment: Financial Statements Analysis

VerifiedAdded on 2021/02/21

|34

|5329

|41

Homework Assignment

AI Summary

This financial accounting assignment solution provides a detailed overview of financial accounting, its purpose, and the stakeholders involved. It covers the recording and classification of journal entries, preparation of trial balances, income statements, and balance sheets. The assignment further delves into accounting principles like consistency and prudence, and explains the purpose of depreciation. It also explores the differences between financial statements of sole traders and limited companies. Furthermore, the solution includes the preparation of bank reconciliation statements, identifying variances between bank and cash book records, and the imprest system in petty cash. The assignment also covers the purpose of preparing control accounts. The solution is comprehensive, including references, and provides a solid foundation for understanding financial accounting principles and practices.

FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Part A...............................................................................................................................................1

1. Financial accounting and its purpose.......................................................................................1

2. External and internal stakeholders of large organization.........................................................3

PART B............................................................................................................................................5

CLIENT 1........................................................................................................................................5

CLIENT 2........................................................................................................................................5

c). Consistency and Prudence......................................................................................................5

d) Purpose of depreciation in financial statement........................................................................6

e)Difference between financial statements of sole trader and limited company........................7

CLIENT 3........................................................................................................................................8

A) Purpose of preparing Bank Reconciliation Statement ...........................................................8

B) Listing the areas that vary the record of bank and cash book................................................9

C) Imprest in petty cash system.................................................................................................10

CLIENT 4......................................................................................................................................10

b.) Purpose of preparing control accounts.................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

Part A...............................................................................................................................................1

1. Financial accounting and its purpose.......................................................................................1

2. External and internal stakeholders of large organization.........................................................3

PART B............................................................................................................................................5

CLIENT 1........................................................................................................................................5

CLIENT 2........................................................................................................................................5

c). Consistency and Prudence......................................................................................................5

d) Purpose of depreciation in financial statement........................................................................6

e)Difference between financial statements of sole trader and limited company........................7

CLIENT 3........................................................................................................................................8

A) Purpose of preparing Bank Reconciliation Statement ...........................................................8

B) Listing the areas that vary the record of bank and cash book................................................9

C) Imprest in petty cash system.................................................................................................10

CLIENT 4......................................................................................................................................10

b.) Purpose of preparing control accounts.................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial accounting is one the most specialized branch of accounting which helps in

keeping complete track of various financial transactions. Such transactions are recorded by

effectively using standard guidelines in order to record, summarize and present transactions in

financial statements in a systematic and reliable manner.

This study will highlight on the key purpose of financial accounting. It will also

demonstrate internal and external stakeholders of the company and examine why they are

interested in the various financial statements of the organization. This study will record various

business transactions with the help of double entry book keeping and will also extract a trial

balance. Final accounts will be prepared for partnership, limited company and sole traders in

compliance with appropriate standards, conventions and principles. Furthermore, this study will

perform bank reconciliation system in order to ensure that the bank and company records are

correct. It will also reconcile control account and identify correct accounts for specific

transactions recorded in suspense account.

Taj Accountants is a small accountancy firm based in London, United Kingdom. It offers

one stop solution to customers regarding tax, business planning, accounts, payroll, bookkeeping,

advisory services to partnership, sole traders and limited company.

Part A

1. Financial accounting and its purpose.

Schroeder, Clark and Cathey (2019) sought to establish the fact that, financial accounting

is one the most specialized branch of accounting which helps in keeping complete track of

various financial transactions. Financial accounting is useful in capturing the company's financial

position for the particular accounting period. Financial accounting is carried out by effectively

complying with various accounting standards, conventions and principles. Financial accounting

mainly generates four main financial statements which mainly includes income statement,

balance sheet, owner's equity statement and cash flow statement. Financial transactions are

recorded by effectively using standard guidelines in order to record, summarize and present

transactions in financial statements in a systematic and reliable manner. Furthermore, such

financial statements are useful for stakeholders in order to extract useful information and make

strategic decision (Financial Accounting – Introduction, Accounting Concepts, Preparation and

Presentation of Financial Statements, 2018). The primary recipients of financial statements are

1

Financial accounting is one the most specialized branch of accounting which helps in

keeping complete track of various financial transactions. Such transactions are recorded by

effectively using standard guidelines in order to record, summarize and present transactions in

financial statements in a systematic and reliable manner.

This study will highlight on the key purpose of financial accounting. It will also

demonstrate internal and external stakeholders of the company and examine why they are

interested in the various financial statements of the organization. This study will record various

business transactions with the help of double entry book keeping and will also extract a trial

balance. Final accounts will be prepared for partnership, limited company and sole traders in

compliance with appropriate standards, conventions and principles. Furthermore, this study will

perform bank reconciliation system in order to ensure that the bank and company records are

correct. It will also reconcile control account and identify correct accounts for specific

transactions recorded in suspense account.

Taj Accountants is a small accountancy firm based in London, United Kingdom. It offers

one stop solution to customers regarding tax, business planning, accounts, payroll, bookkeeping,

advisory services to partnership, sole traders and limited company.

Part A

1. Financial accounting and its purpose.

Schroeder, Clark and Cathey (2019) sought to establish the fact that, financial accounting

is one the most specialized branch of accounting which helps in keeping complete track of

various financial transactions. Financial accounting is useful in capturing the company's financial

position for the particular accounting period. Financial accounting is carried out by effectively

complying with various accounting standards, conventions and principles. Financial accounting

mainly generates four main financial statements which mainly includes income statement,

balance sheet, owner's equity statement and cash flow statement. Financial transactions are

recorded by effectively using standard guidelines in order to record, summarize and present

transactions in financial statements in a systematic and reliable manner. Furthermore, such

financial statements are useful for stakeholders in order to extract useful information and make

strategic decision (Financial Accounting – Introduction, Accounting Concepts, Preparation and

Presentation of Financial Statements, 2018). The primary recipients of financial statements are

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

managers, investors, creditors, board of directors, etc. and the secondary recipients of financial

information are customers, employees, competitors, stock market analyst, etc. Financial

accounting is very useful in keeping systematic records of the financial transaction on a timely

and reliable manner. On the contrary, Henderson and et.al., (2015) argued that, financial

accounting does not take into consideration non- monetary transactions, which in turn does not

disclose exact value of the business. Financial accounting is largely influenced by personal

biasses of an individual.

Financial accounting is useful in analysing the profit and loss position of the company.

The key principles of financial accounting are objectivity, materiality, usability and

comparability. Financial accounting is very useful in forecasting and take strategic decision for

the future. It is very useful in communicating with different stakeholders in relation with

financial position of the company (Macve, 2015). International accounting standard board

(IASB) helps in developing high quality standard in order to generate accurate ad reliable data

for the future. Compliance with regulatory framework is useful in increasing the confidence of

various financial accounting and reporting process. Financial accounting must be in compliance

with GAAP, IFRS, SEC and FASB.

Purpose of financial accounting

The key purpose of financial accounting is to effectively ascertain the financial health

and position of the company for the particular period (Barragato, 2019). It helps managers to

make strategic decision which leads to long term sustainable growth and development of the

business. The main purpose is to provide information related with performance and financial

position of the company. The balance sheet of the company helps in determining the current

asset and liabilities for a particular period. The income statement helps managers to know the

ability of the company to generate profit. Cash flow statement helps in determining the cash

receipt and cash outflow of the company in order to gain insight on the current market position

of the company (3 Main Purposes of Financial Statements, 2019). The main purpose of the

financial statement is that it is useful in making credit decision, investment decision, union

bargaining decision and taxation decision. Financial accounting helps in assisting potential and

existing investors in order to take strategic decision regarding investment. It is very useful for

managers to oversee the prospective future net cash flow of the company. Financial accounting is

useful in keeping systematic record of the various financial transactions for a particular

2

information are customers, employees, competitors, stock market analyst, etc. Financial

accounting is very useful in keeping systematic records of the financial transaction on a timely

and reliable manner. On the contrary, Henderson and et.al., (2015) argued that, financial

accounting does not take into consideration non- monetary transactions, which in turn does not

disclose exact value of the business. Financial accounting is largely influenced by personal

biasses of an individual.

Financial accounting is useful in analysing the profit and loss position of the company.

The key principles of financial accounting are objectivity, materiality, usability and

comparability. Financial accounting is very useful in forecasting and take strategic decision for

the future. It is very useful in communicating with different stakeholders in relation with

financial position of the company (Macve, 2015). International accounting standard board

(IASB) helps in developing high quality standard in order to generate accurate ad reliable data

for the future. Compliance with regulatory framework is useful in increasing the confidence of

various financial accounting and reporting process. Financial accounting must be in compliance

with GAAP, IFRS, SEC and FASB.

Purpose of financial accounting

The key purpose of financial accounting is to effectively ascertain the financial health

and position of the company for the particular period (Barragato, 2019). It helps managers to

make strategic decision which leads to long term sustainable growth and development of the

business. The main purpose is to provide information related with performance and financial

position of the company. The balance sheet of the company helps in determining the current

asset and liabilities for a particular period. The income statement helps managers to know the

ability of the company to generate profit. Cash flow statement helps in determining the cash

receipt and cash outflow of the company in order to gain insight on the current market position

of the company (3 Main Purposes of Financial Statements, 2019). The main purpose of the

financial statement is that it is useful in making credit decision, investment decision, union

bargaining decision and taxation decision. Financial accounting helps in assisting potential and

existing investors in order to take strategic decision regarding investment. It is very useful for

managers to oversee the prospective future net cash flow of the company. Financial accounting is

useful in keeping systematic record of the various financial transactions for a particular

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting period. It is very useful in determining the best performing sector of the company. It

is very useful in controlling the cost of the company by attaining economies of scale (Tassadaq

and Malik, 2015). The key purpose of financial accounting is to provide timely information to

the stakeholders of the company in order to make strategic decision. It is very useful in allocating

the resources and results in determining the cash flow, operational efficiency and financial

position of the company.

2. External and internal stakeholders of large organization.

Internal stakeholders

Internal stakeholders i.e., employees, managers and owners of the company are directly

related with the organization (Nilsson and Stockenstrand, 2015). They are the people who are

serving the organization and gets directly influenced by the performance of the company.

Internal stakeholders focus on making strategic decision which in turn results in long term

sustainable growth and development of the business.

Managers

They are interested in the financial statements of the company because it focuses on

managing the various affairs of the company by ascertaining the financial position and

performance of the organisation. They focus on ascertaining the most profitable unit of the

company and also helps in determining the factors which leads to higher cost and expenses.

Financial statements helps managers in taking strategic decision which leads to higher

profitability and attainment of economies of scale. It helps managers in assessing and evaluating

the liquidity, operational efficiency and profitability of the business (HASLAM and et.al., 2015).

The managers set the benchmarking standards and strategy which helps in identifying areas of

competence and attain greater heights and growth in future. It also helps in managing various

risk factors which in turn results in smooth functioning of the business.

Employees

Employees assess the financial statements of the company because it will help them in

evaluating the future growth prospect of an individual upon the growth, performance and

financial position of the company. It helps in ascertaining he job security and future

remuneration of an individual. Financial statements helps employees in assessing the financial

stability of the company. Of the company is performing better, then there are higher chances of

career growth and opportunities for the employees of the organization. In case the profit of the

3

is very useful in controlling the cost of the company by attaining economies of scale (Tassadaq

and Malik, 2015). The key purpose of financial accounting is to provide timely information to

the stakeholders of the company in order to make strategic decision. It is very useful in allocating

the resources and results in determining the cash flow, operational efficiency and financial

position of the company.

2. External and internal stakeholders of large organization.

Internal stakeholders

Internal stakeholders i.e., employees, managers and owners of the company are directly

related with the organization (Nilsson and Stockenstrand, 2015). They are the people who are

serving the organization and gets directly influenced by the performance of the company.

Internal stakeholders focus on making strategic decision which in turn results in long term

sustainable growth and development of the business.

Managers

They are interested in the financial statements of the company because it focuses on

managing the various affairs of the company by ascertaining the financial position and

performance of the organisation. They focus on ascertaining the most profitable unit of the

company and also helps in determining the factors which leads to higher cost and expenses.

Financial statements helps managers in taking strategic decision which leads to higher

profitability and attainment of economies of scale. It helps managers in assessing and evaluating

the liquidity, operational efficiency and profitability of the business (HASLAM and et.al., 2015).

The managers set the benchmarking standards and strategy which helps in identifying areas of

competence and attain greater heights and growth in future. It also helps in managing various

risk factors which in turn results in smooth functioning of the business.

Employees

Employees assess the financial statements of the company because it will help them in

evaluating the future growth prospect of an individual upon the growth, performance and

financial position of the company. It helps in ascertaining he job security and future

remuneration of an individual. Financial statements helps employees in assessing the financial

stability of the company. Of the company is performing better, then there are higher chances of

career growth and opportunities for the employees of the organization. In case the profit of the

3

company are low and are no future prospect for growth, then employees will quit that job and

will not further invest any money and time in that organization (Chalmers, Hay and Khlif, 2019).

External stakeholders

It refers to the people that are working outside the organisation and are affected by the

actions and decisions of the company. There are various types of external stakeholders such as

customers that buy products or services of the firm, creditors from whom organisation owes

money, suppliers of raw materials etc. (Vracheva, Judge and Madden, 2016). External

stakeholders of Taj Accountants that may be interested in receiving financial information

regarding operations of the company are as follows -

Government :

Government bodies such as tax authorities etc. are interested in getting financial

information of the firm for the purpose of determining that whether the organisation is

complying all the regulatory requirements and for the purpose of determining tax liability of the

business. Tax is calculated on the basis of profits generated by the firm (Diouf and Boiral, 2017).

Therefore, financial information related with the operations of Taj Accountants will help the

Government to calculate the amount of tax to be paid by the firm. Further, financial information

will also help the authorities to determine whether company is charging fair rate for offering the

services to the customers.

Lenders and creditors :

Creditor is an institution or individual that provides permission to another entity to

borrow money which is to repaid by the firm in the future. Creditors charges interest on the

amount provided to another entity in the form of loan. Lenders will require financial information

of Taj Accountants to determine credit worthiness of the firm. On the basis of financial position

of the company, lenders and creditors offer credit facilities. If, the financial position of the firm

is good it will indicate that company is able to pay outstanding amount on time. In case liquidity

position of firm is poor it will indicate that company does not have sufficient assets to pay

liabilities back on time (Martin and Moser, 2016).

Customers :

It refers to the individual or firm that purchase product or service of the business. If, there

is long term involvement between Taj Accountants and its customers then, clients will be

interested to determine company's ability to maintain stability in the operations. Further,

4

will not further invest any money and time in that organization (Chalmers, Hay and Khlif, 2019).

External stakeholders

It refers to the people that are working outside the organisation and are affected by the

actions and decisions of the company. There are various types of external stakeholders such as

customers that buy products or services of the firm, creditors from whom organisation owes

money, suppliers of raw materials etc. (Vracheva, Judge and Madden, 2016). External

stakeholders of Taj Accountants that may be interested in receiving financial information

regarding operations of the company are as follows -

Government :

Government bodies such as tax authorities etc. are interested in getting financial

information of the firm for the purpose of determining that whether the organisation is

complying all the regulatory requirements and for the purpose of determining tax liability of the

business. Tax is calculated on the basis of profits generated by the firm (Diouf and Boiral, 2017).

Therefore, financial information related with the operations of Taj Accountants will help the

Government to calculate the amount of tax to be paid by the firm. Further, financial information

will also help the authorities to determine whether company is charging fair rate for offering the

services to the customers.

Lenders and creditors :

Creditor is an institution or individual that provides permission to another entity to

borrow money which is to repaid by the firm in the future. Creditors charges interest on the

amount provided to another entity in the form of loan. Lenders will require financial information

of Taj Accountants to determine credit worthiness of the firm. On the basis of financial position

of the company, lenders and creditors offer credit facilities. If, the financial position of the firm

is good it will indicate that company is able to pay outstanding amount on time. In case liquidity

position of firm is poor it will indicate that company does not have sufficient assets to pay

liabilities back on time (Martin and Moser, 2016).

Customers :

It refers to the individual or firm that purchase product or service of the business. If, there

is long term involvement between Taj Accountants and its customers then, clients will be

interested to determine company's ability to maintain stability in the operations. Further,

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial information will help clients of Taj Accountants to ensure whether company will be

able to continue its existence in the future or not. Moreover, financial statements will help

customers to determine that whether firm is providing services at fair rate or not.

Investors :

It refers to the individual or firm that commits funds in the business in the expectation of

getting better financial returns from the company. Financial information regarding operations of

Taj Accountants will help potential investors to determine the viability of investing funds in the

company. Financial statements like profit and loss statement help to forecast dividend that will

be paid by the firm in the future. Further, financial information will also assist the investors of

Taj Accountants to analyse the risk associated with investing funds in the organisation. For

example -If there is more fluctuations in the profit of firm it will indicate that there is high risk

in investing capital in organisation (Diouf and Boiral, 2017).

PART B

CLIENT 1

1. Recording and classification of the journal entries

5

able to continue its existence in the future or not. Moreover, financial statements will help

customers to determine that whether firm is providing services at fair rate or not.

Investors :

It refers to the individual or firm that commits funds in the business in the expectation of

getting better financial returns from the company. Financial information regarding operations of

Taj Accountants will help potential investors to determine the viability of investing funds in the

company. Financial statements like profit and loss statement help to forecast dividend that will

be paid by the firm in the future. Further, financial information will also assist the investors of

Taj Accountants to analyse the risk associated with investing funds in the organisation. For

example -If there is more fluctuations in the profit of firm it will indicate that there is high risk

in investing capital in organisation (Diouf and Boiral, 2017).

PART B

CLIENT 1

1. Recording and classification of the journal entries

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

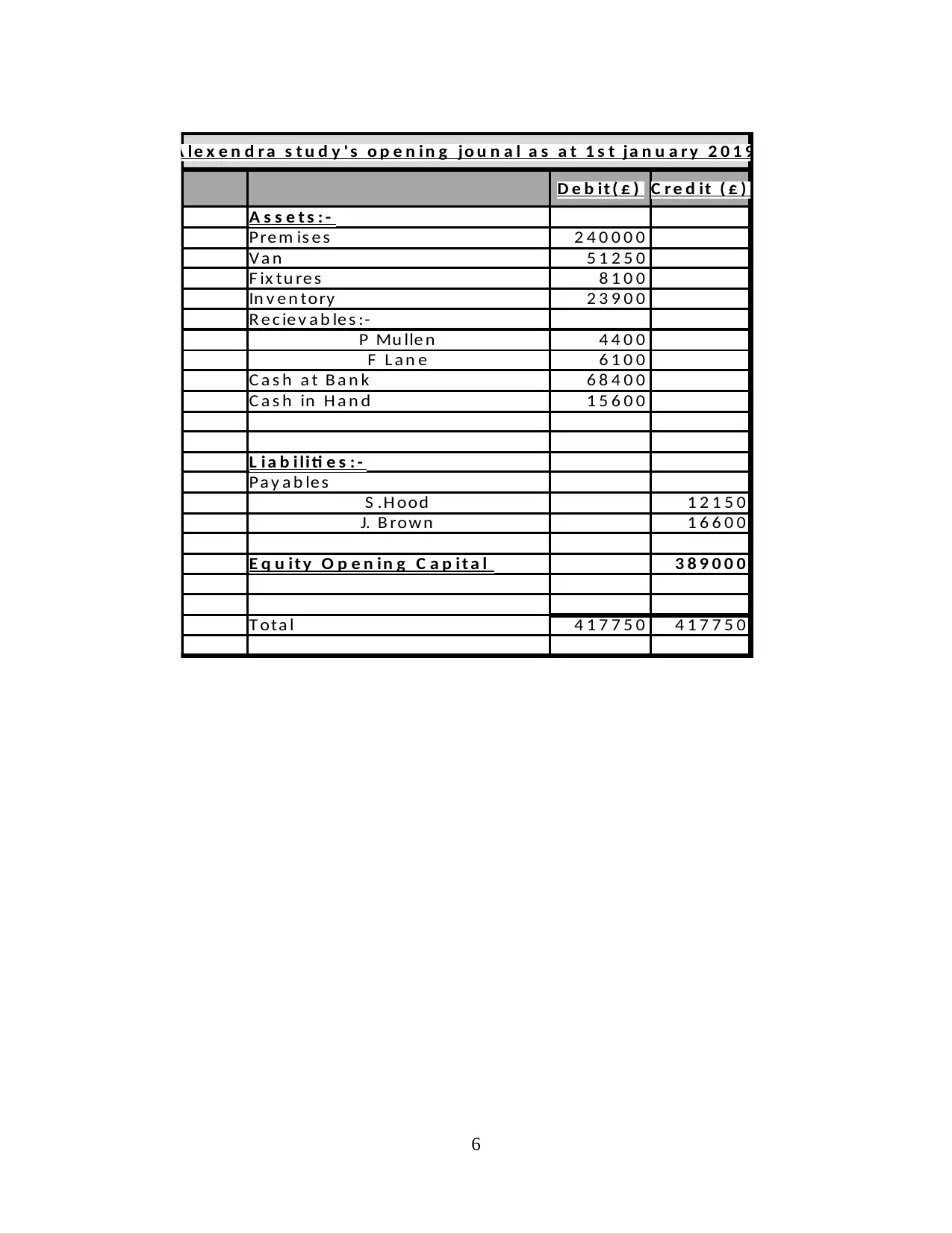

A le x e n d r a s t u d y ' s o p e n i n g jo u n a l a s a t 1 s t ja n u a r y 2 0 1 9

D e b i t ( £ ) C r e d it ( £ )

A s s e t s : -

Pre m is e s 2 4 0 0 0 0

V a n 5 1 2 5 0

F ix tu re s 8 1 0 0

In v e n tory 2 3 9 0 0

R e c ie v a b le s :-

P Mu lle n 4 4 0 0

F L a n e 6 1 0 0

C a s h a t B a n k 6 8 4 0 0

C a s h in H a n d 1 5 6 0 0

L i a b i li ti e s : -

Pa y a b le s

S .H ood 1 2 1 5 0

J. B rown 1 6 6 0 0

E q u it y O p e n in g C a p i t a l 3 8 9 0 0 0

T ota l 4 1 7 7 5 0 4 1 7 7 5 0

A le x e n d r a s t u d y ' s o p e n i n g jo u n a l a s a t 1 s t ja n u a r y 2 0 1 9

D e b i t ( £ ) C r e d it ( £ )

A s s e t s : -

Pre m is e s 2 4 0 0 0 0

V a n 5 1 2 5 0

F ix tu re s 8 1 0 0

In v e n tory 2 3 9 0 0

R e c ie v a b le s :-

P Mu lle n 4 4 0 0

F L a n e 6 1 0 0

C a s h a t B a n k 6 8 4 0 0

C a s h in H a n d 1 5 6 0 0

L i a b i li ti e s : -

Pa y a b le s

S .H ood 1 2 1 5 0

J. B rown 1 6 6 0 0

E q u it y O p e n in g C a p i t a l 3 8 9 0 0 0

T ota l 4 1 7 7 5 0 4 1 7 7 5 0

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

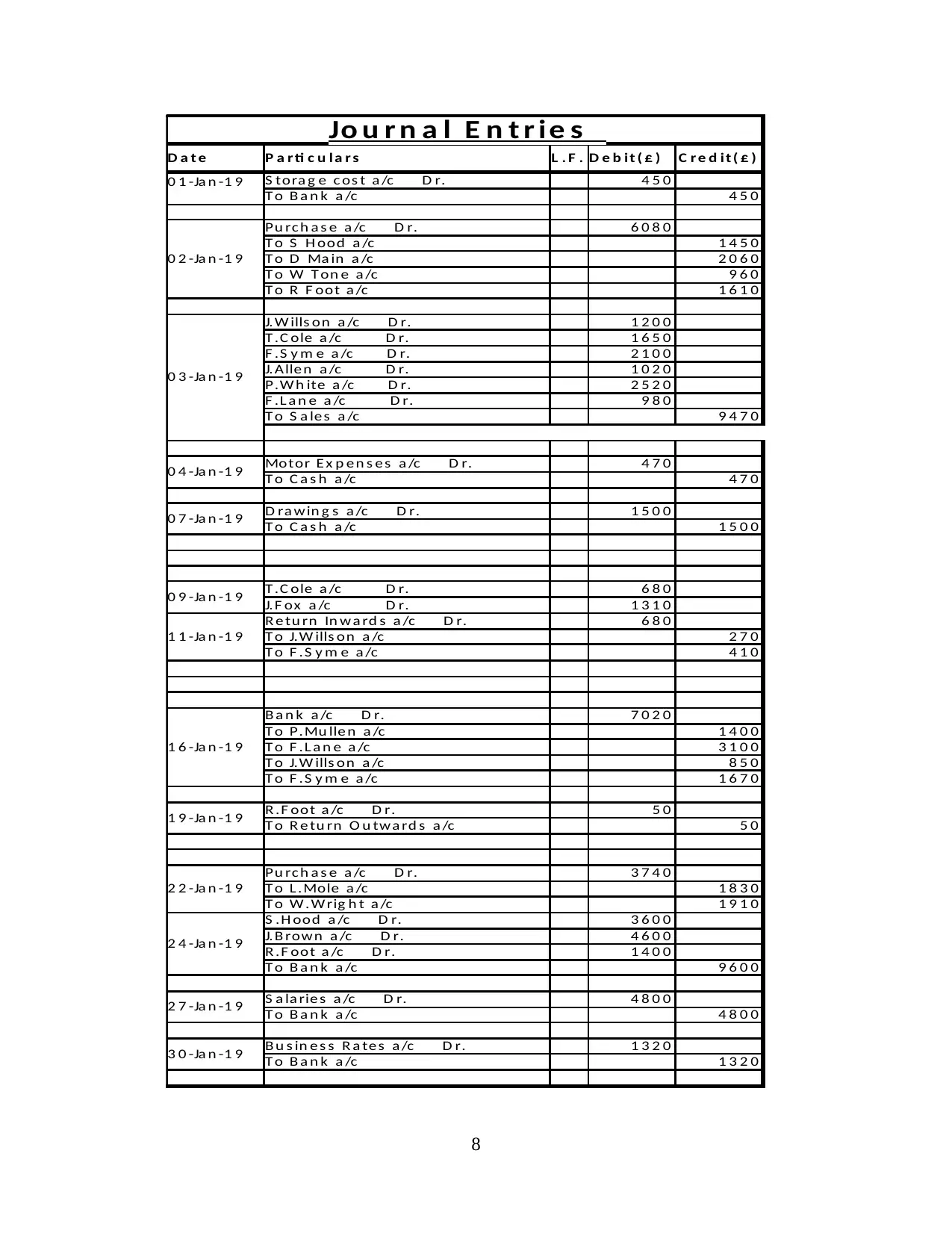

Jo u r n a l E n t r ie s

D a t e P a r ti c u la r s L . F . D e b it ( £ ) C r e d it ( £ )

0 1 -Ja n -1 9 S tora g e c os t a /c D r. 4 5 0

T o B a n k a /c 4 5 0

0 2 -Ja n -1 9

Pu rc h a s e a /c D r. 6 0 8 0

T o S H ood a /c 1 4 5 0

T o D Ma in a /c 2 0 6 0

T o W T on e a /c 9 6 0

T o R F oot a /c 1 6 1 0

0 3 -Ja n -1 9

J.W ills on a /c D r. 1 2 0 0

T .C ole a /c D r. 1 6 5 0

F .S y m e a /c D r. 2 1 0 0

J.Alle n a /c D r. 1 0 2 0

P.W h ite a /c D r. 2 5 2 0

F .L a n e a /c D r. 9 8 0

T o S a le s a /c 9 4 7 0

0 4 -Ja n -1 9 Motor E x p e n s e s a /c D r. 4 7 0

T o C a s h a /c 4 7 0

0 7 -Ja n -1 9 D ra w in g s a /c D r. 1 5 0 0

T o C a s h a /c 1 5 0 0

0 9 -Ja n -1 9 T .C ole a /c D r. 6 8 0

J.F ox a /c D r. 1 3 1 0

1 1 -Ja n -1 9

R e tu rn In w a rd s a /c D r. 6 8 0

T o J.W ills on a /c 2 7 0

T o F .S y m e a /c 4 1 0

1 6 -Ja n -1 9

B a n k a /c D r. 7 0 2 0

T o P.Mu lle n a /c 1 4 0 0

T o F .L a n e a /c 3 1 0 0

T o J.W ills on a /c 8 5 0

T o F .S y m e a /c 1 6 7 0

1 9 -Ja n -1 9 R .F oot a /c D r. 5 0

T o R e tu rn O u twa rd s a /c 5 0

2 2 -Ja n -1 9

Pu rc h a s e a /c D r. 3 7 4 0

T o L .Mole a /c 1 8 3 0

T o W .W rig h t a /c 1 9 1 0

2 4 -Ja n -1 9

S .H ood a /c D r. 3 6 0 0

J.B rown a /c D r. 4 6 0 0

R .F oot a /c D r. 1 4 0 0

T o B a n k a /c 9 6 0 0

2 7 -Ja n -1 9 S a la rie s a /c D r. 4 8 0 0

T o B a n k a /c 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s a /c D r. 1 3 2 0

T o B a n k a /c 1 3 2 0

Jo u r n a l E n t r ie s

D a t e P a r ti c u la r s L . F . D e b it ( £ ) C r e d it ( £ )

0 1 -Ja n -1 9 S tora g e c os t a /c D r. 4 5 0

T o B a n k a /c 4 5 0

0 2 -Ja n -1 9

Pu rc h a s e a /c D r. 6 0 8 0

T o S H ood a /c 1 4 5 0

T o D Ma in a /c 2 0 6 0

T o W T on e a /c 9 6 0

T o R F oot a /c 1 6 1 0

0 3 -Ja n -1 9

J.W ills on a /c D r. 1 2 0 0

T .C ole a /c D r. 1 6 5 0

F .S y m e a /c D r. 2 1 0 0

J.Alle n a /c D r. 1 0 2 0

P.W h ite a /c D r. 2 5 2 0

F .L a n e a /c D r. 9 8 0

T o S a le s a /c 9 4 7 0

0 4 -Ja n -1 9 Motor E x p e n s e s a /c D r. 4 7 0

T o C a s h a /c 4 7 0

0 7 -Ja n -1 9 D ra w in g s a /c D r. 1 5 0 0

T o C a s h a /c 1 5 0 0

0 9 -Ja n -1 9 T .C ole a /c D r. 6 8 0

J.F ox a /c D r. 1 3 1 0

1 1 -Ja n -1 9

R e tu rn In w a rd s a /c D r. 6 8 0

T o J.W ills on a /c 2 7 0

T o F .S y m e a /c 4 1 0

1 6 -Ja n -1 9

B a n k a /c D r. 7 0 2 0

T o P.Mu lle n a /c 1 4 0 0

T o F .L a n e a /c 3 1 0 0

T o J.W ills on a /c 8 5 0

T o F .S y m e a /c 1 6 7 0

1 9 -Ja n -1 9 R .F oot a /c D r. 5 0

T o R e tu rn O u twa rd s a /c 5 0

2 2 -Ja n -1 9

Pu rc h a s e a /c D r. 3 7 4 0

T o L .Mole a /c 1 8 3 0

T o W .W rig h t a /c 1 9 1 0

2 4 -Ja n -1 9

S .H ood a /c D r. 3 6 0 0

J.B rown a /c D r. 4 6 0 0

R .F oot a /c D r. 1 4 0 0

T o B a n k a /c 9 6 0 0

2 7 -Ja n -1 9 S a la rie s a /c D r. 4 8 0 0

T o B a n k a /c 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s a /c D r. 1 3 2 0

T o B a n k a /c 1 3 2 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

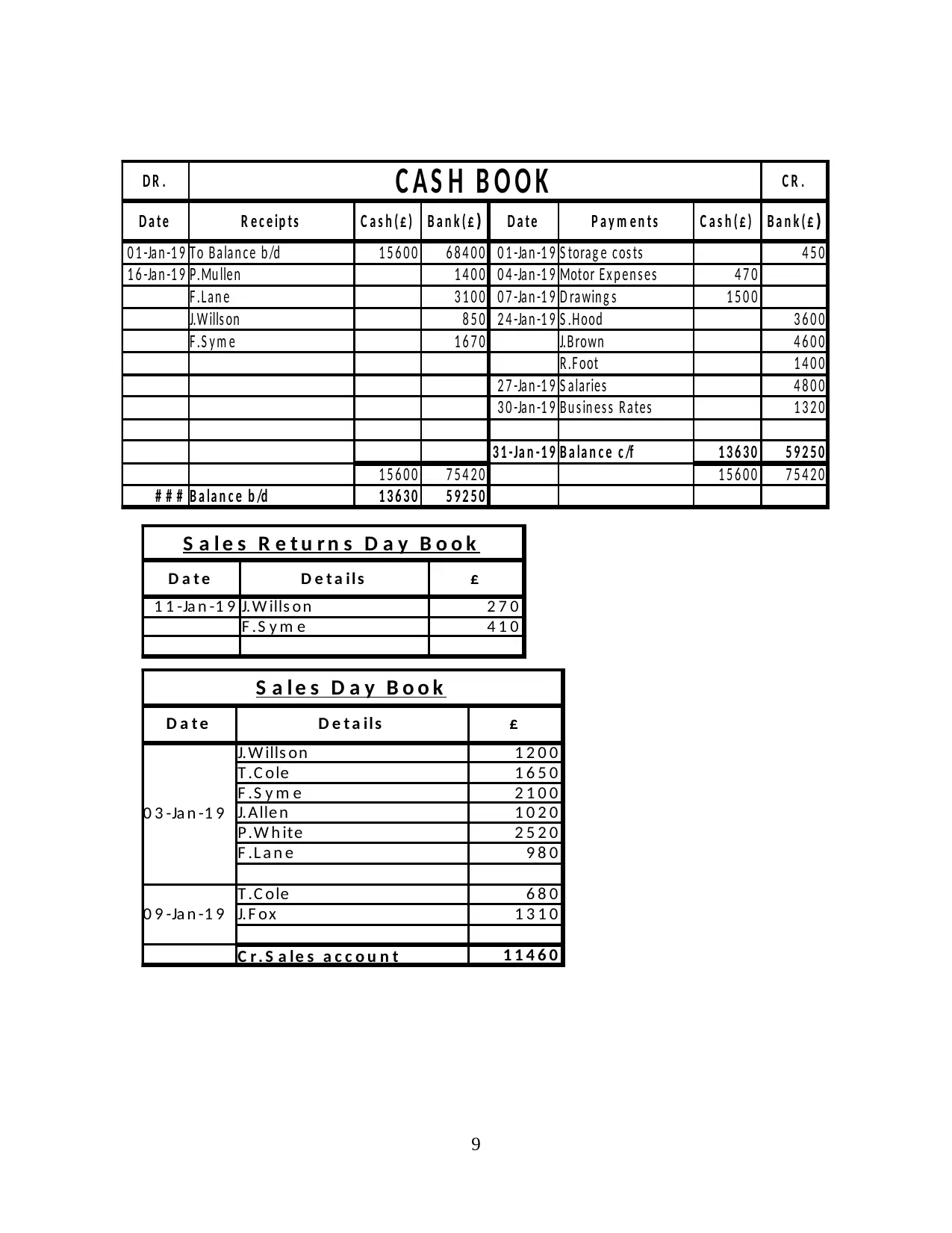

D R . C A S H B O O K C R .

D a t e R e c e ip t s C a s h ( £ ) D a t e P a y m e n t s C a s h ( £ )

0 1 -Ja n -1 9 T o B a la n c e b /d 1 5 6 0 0 6 8 4 0 0 0 1 -Ja n -1 9 S tora g e c os ts 4 5 0

1 6 -Ja n -1 9 P.Mu lle n 1 4 0 0 0 4 -Ja n -1 9 Motor E x p e n s e s 4 7 0

F .L a n e 3 1 0 0 0 7 -Ja n -1 9 D ra win g s 1 5 0 0

J.W ills on 8 5 0 2 4 -Ja n -1 9 S .H ood 3 6 0 0

F .S y m e 1 6 7 0 J.B rown 4 6 0 0

R .F oot 1 4 0 0

2 7 -Ja n -1 9 S a la rie s 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s 1 3 2 0

3 1 -Ja n - 1 9 B a la n c e c /f 1 3 6 3 0 5 9 2 5 0

1 5 6 0 0 7 5 4 2 0 1 5 6 0 0 7 5 4 2 0

# # # B a la n c e b /d 1 3 6 3 0 5 9 2 5 0

B a n k ( £ ) B a n k ( £ )

S a l e s D a y B o o k

D a t e D e t a ils £

0 3 -Ja n -1 9

J.W ills on 1 2 0 0

T .C ole 1 6 5 0

F .S y m e 2 1 0 0

J.Alle n 1 0 2 0

P.W h ite 2 5 2 0

F .L a n e 9 8 0

0 9 -Ja n -1 9

T .C ole 6 8 0

J.F ox 1 3 1 0

C r . S a le s a c c o u n t 1 1 4 6 0

S a l e s R e t u r n s D a y B o o k

D a t e D e t a ils £

1 1 -Ja n -1 9 J.W ills on 2 7 0

F .S y m e 4 1 0

D R . C A S H B O O K C R .

D a t e R e c e ip t s C a s h ( £ ) D a t e P a y m e n t s C a s h ( £ )

0 1 -Ja n -1 9 T o B a la n c e b /d 1 5 6 0 0 6 8 4 0 0 0 1 -Ja n -1 9 S tora g e c os ts 4 5 0

1 6 -Ja n -1 9 P.Mu lle n 1 4 0 0 0 4 -Ja n -1 9 Motor E x p e n s e s 4 7 0

F .L a n e 3 1 0 0 0 7 -Ja n -1 9 D ra win g s 1 5 0 0

J.W ills on 8 5 0 2 4 -Ja n -1 9 S .H ood 3 6 0 0

F .S y m e 1 6 7 0 J.B rown 4 6 0 0

R .F oot 1 4 0 0

2 7 -Ja n -1 9 S a la rie s 4 8 0 0

3 0 -Ja n -1 9 B u s in e s s R a te s 1 3 2 0

3 1 -Ja n - 1 9 B a la n c e c /f 1 3 6 3 0 5 9 2 5 0

1 5 6 0 0 7 5 4 2 0 1 5 6 0 0 7 5 4 2 0

# # # B a la n c e b /d 1 3 6 3 0 5 9 2 5 0

B a n k ( £ ) B a n k ( £ )

S a l e s D a y B o o k

D a t e D e t a ils £

0 3 -Ja n -1 9

J.W ills on 1 2 0 0

T .C ole 1 6 5 0

F .S y m e 2 1 0 0

J.Alle n 1 0 2 0

P.W h ite 2 5 2 0

F .L a n e 9 8 0

0 9 -Ja n -1 9

T .C ole 6 8 0

J.F ox 1 3 1 0

C r . S a le s a c c o u n t 1 1 4 6 0

S a l e s R e t u r n s D a y B o o k

D a t e D e t a ils £

1 1 -Ja n -1 9 J.W ills on 2 7 0

F .S y m e 4 1 0

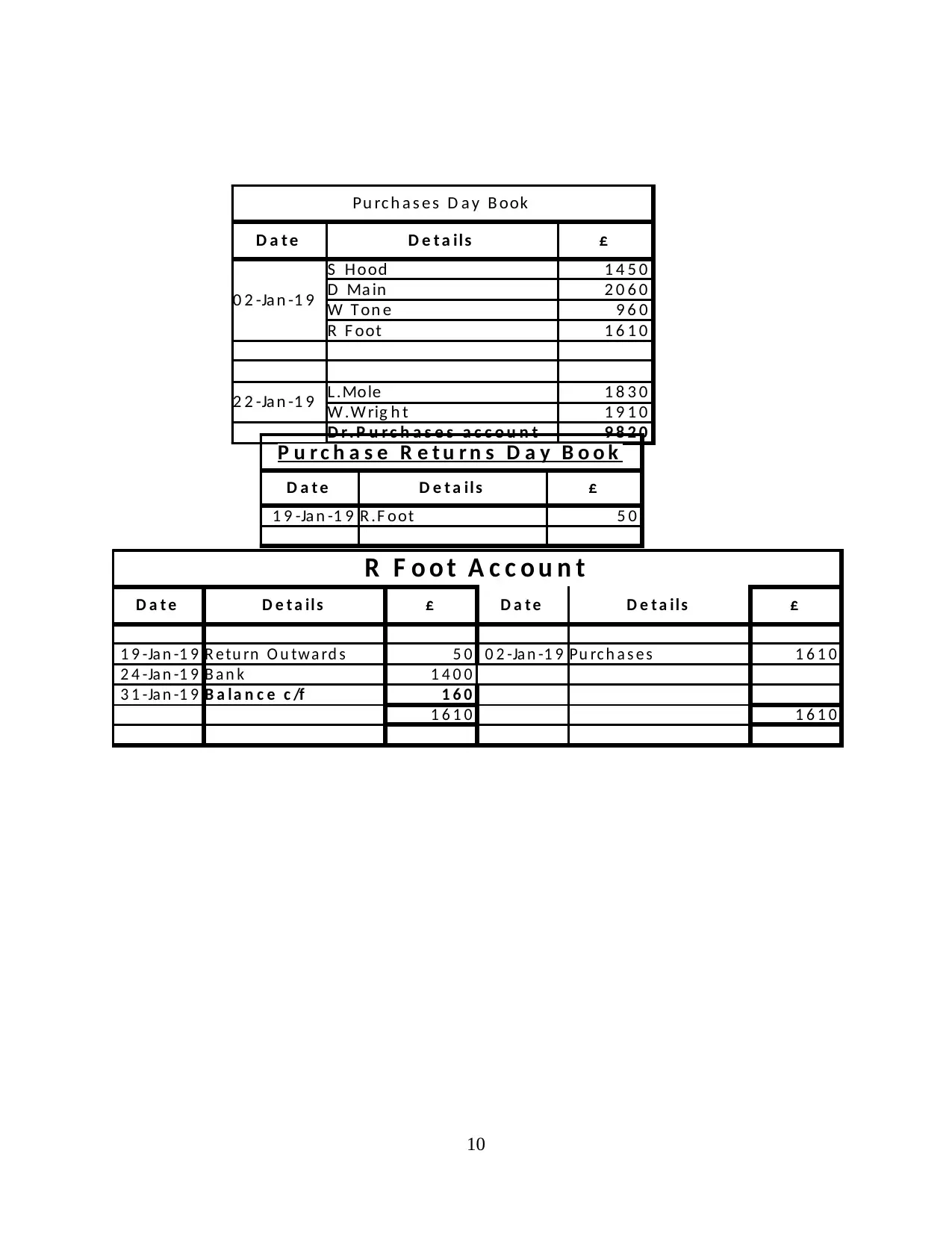

R F o o t A c c o u n t

D a t e D e t a il s £ D a t e D e t a il s £

1 9 -Ja n -1 9 R e tu rn O u tw a rd s 5 0 0 2 -Ja n -1 9 Pu rc h a s e s 1 6 1 0

2 4 -Ja n -1 9 B a n k 1 4 0 0

3 1 -Ja n -1 9 B a l a n c e c /f 1 6 0

1 6 1 0 1 6 1 0

10

Pu rc h a s e s D a y B ook

D a t e D e t a ils £

0 2 -Ja n -1 9

S H ood 1 4 5 0

D Ma in 2 0 6 0

W T on e 9 6 0

R F oot 1 6 1 0

2 2 -Ja n -1 9 L .Mole 1 8 3 0

W .W rig h t 1 9 1 0

D r . P u r c h a s e s a c c o u n t 9 8 2 0

P u r c h a s e R e t u r n s D a y B o o k

D a t e D e t a ils £

1 9 -Ja n -1 9 R .F oot 5 0

D a t e D e t a il s £ D a t e D e t a il s £

1 9 -Ja n -1 9 R e tu rn O u tw a rd s 5 0 0 2 -Ja n -1 9 Pu rc h a s e s 1 6 1 0

2 4 -Ja n -1 9 B a n k 1 4 0 0

3 1 -Ja n -1 9 B a l a n c e c /f 1 6 0

1 6 1 0 1 6 1 0

10

Pu rc h a s e s D a y B ook

D a t e D e t a ils £

0 2 -Ja n -1 9

S H ood 1 4 5 0

D Ma in 2 0 6 0

W T on e 9 6 0

R F oot 1 6 1 0

2 2 -Ja n -1 9 L .Mole 1 8 3 0

W .W rig h t 1 9 1 0

D r . P u r c h a s e s a c c o u n t 9 8 2 0

P u r c h a s e R e t u r n s D a y B o o k

D a t e D e t a ils £

1 9 -Ja n -1 9 R .F oot 5 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.