Financial Accounting Newsletter: Reporting and Standard Updates

VerifiedAdded on 2023/01/19

|12

|1428

|42

Report

AI Summary

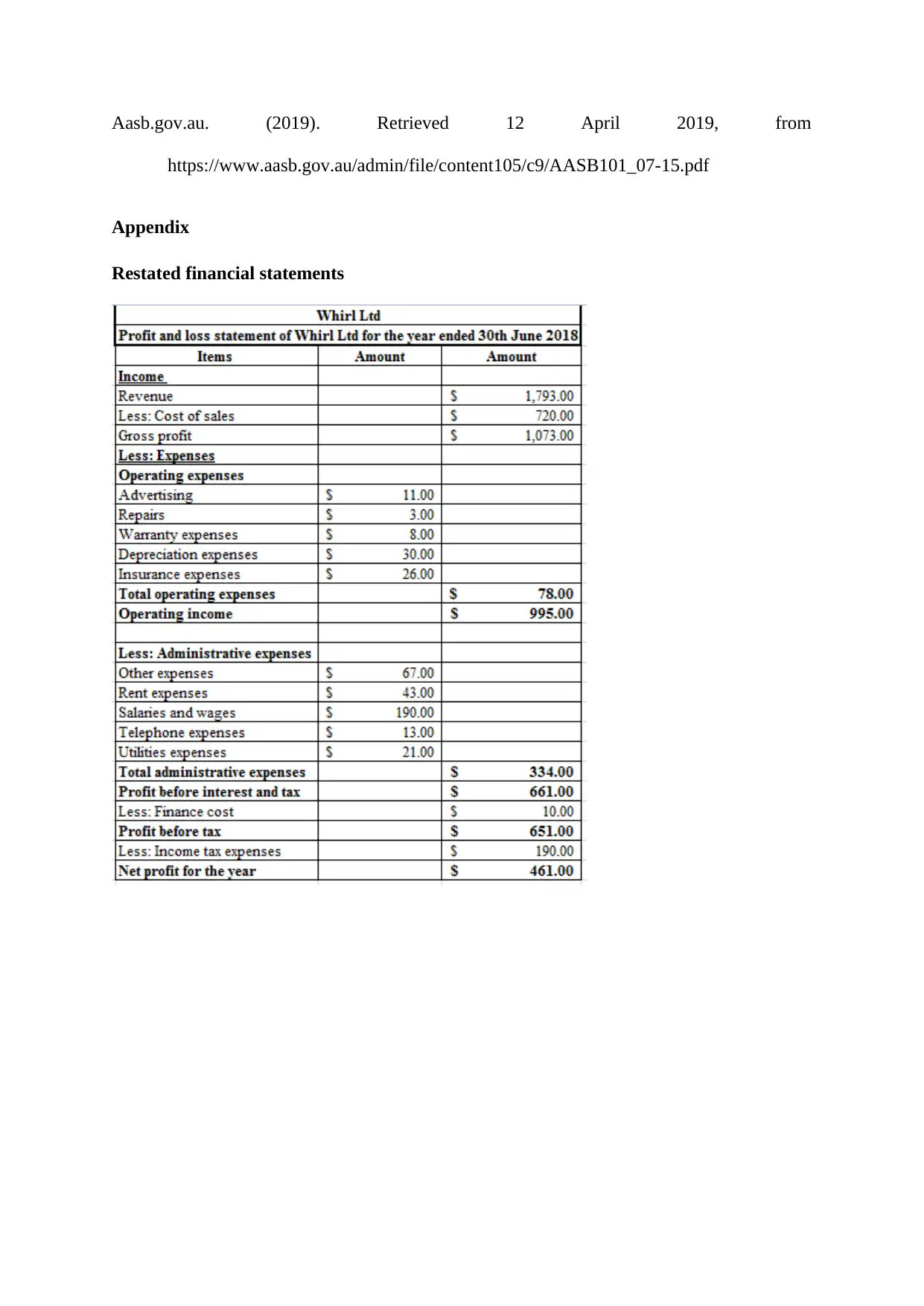

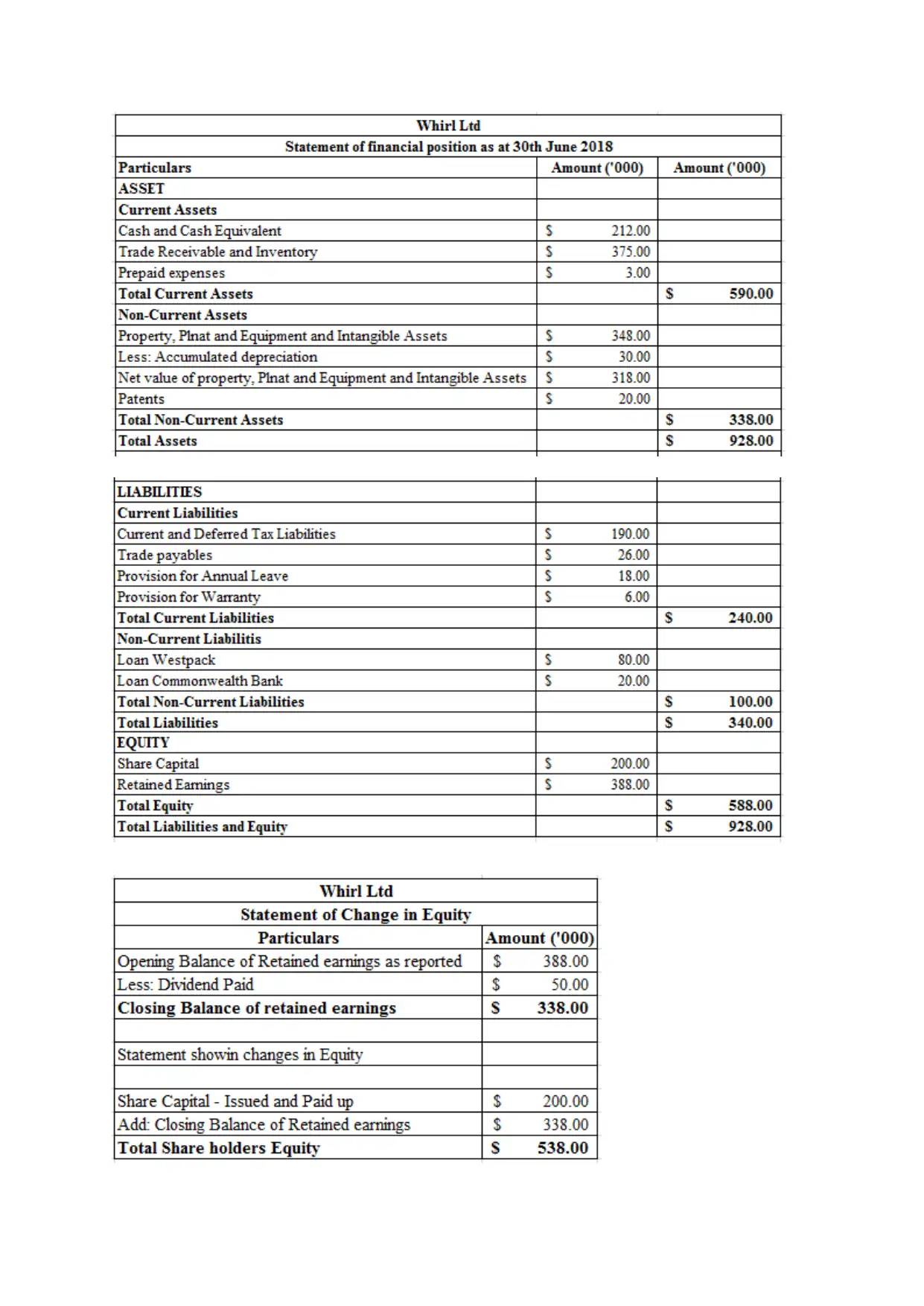

This financial accounting newsletter covers the period from December 1, 2018, to March 31, 2019, and addresses key developments in financial reporting. It highlights the new accounting standard AASB 2018-8 regarding Right-of-Use assets for not-for-profit organizations, clarifying definitions and providing temporary options for measurement. The newsletter also discusses AASB 137 on onerous contracts and updates from the IASB, including decisions on IFRS for SMEs and amendments to IFRS 17 on insurance contracts. Additionally, it covers proposed amendments for standard AASB 2019-X concerning the conceptual framework. The second part of the document analyzes financial statements prepared by a trainee accountant, identifying errors and non-compliance with AASB 101, providing detailed error corrections and references to the relevant accounting standards. It also includes a list of references used for the newsletter.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.