Financial Accounting Principles

VerifiedAdded on 2023/01/09

|24

|3907

|85

AI Summary

This document provides an overview of financial accounting principles and their significance in reporting corporate transactions. It discusses the types of internal and external stakeholders and their roles in the financial accounting process.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Principles

Principles

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

PART A..................................................................................................................................3

PART B..................................................................................................................................6

Client 1...................................................................................................................................6

Client 2.................................................................................................................................15

Client 3.................................................................................................................................19

Client 4.................................................................................................................................20

Client 5.................................................................................................................................22

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

PART A..................................................................................................................................3

PART B..................................................................................................................................6

Client 1...................................................................................................................................6

Client 2.................................................................................................................................15

Client 3.................................................................................................................................19

Client 4.................................................................................................................................20

Client 5.................................................................................................................................22

CONCLUSION..............................................................................................................................23

REFERENCES..............................................................................................................................24

INTRODUCTION

Financial accounting is a sector wherein financial data within financial reports are collected,

analysed and presented (Ebaid, 2016). The financial status of businesses can be seen by

customers and stakeholders in this reporting phase. Along with this financial accounting, the

work of all company operations in respect of profit or loss has a critical part to play. Essentially,

it includes several forms of accounting records and accounts such as P&L book, balance sheet,

revenue tax etc. This business offers small-scale accounting large variety of services. In addition,

in the project report, role of companies is best described in the phrase financial accounting. In

order to determine their value in the financial details, both various stakeholders are listed.

Similar activities are performed by five clients in perhaps a section of the survey.

TASK

PART A

1. Financial accounting with its main purpose for company.

In general terms, the phrase "financial statements" applies to the collection of financial

details in the context of financial reporting to diverse stakeholders (Nilsson and Stockenstrand

2015). This accounting is primarily designed to awaken corporations to produce shift in business

time over the course. Eventually, the annual statements shall be reported towards the close of the

fiscal cycle of the statutory reports. There will be several forms of difficulties in the lack of this

accounting method. Unlike other owners, the shareholder in the business would have little

impact. Moreover, the companies would have trouble understanding their current financial

position. Internal manager file different kinds of financial reports including a P&L report and the

balance sheet respectively within the consulting company. In addition, they provide complete

financial reports and make decisions based of that factors which impact business conditions.

In this respect, it is crucial to be aware of the financial accountability standards and rules.

This is how the annual results are found null in the lack of these reporting requirements. GAAP

is understood as the common accounting concept as the most basic characteristic of financial

performance. The accounts and analyses are defined under certain standards of financial

reporting. Below are listed other uses of financial accounting:

Advantageous in calculating cash flow: Financial reports aid to reliably predict working

capital on the impact of accounting reports. It is important because businesses will

Financial accounting is a sector wherein financial data within financial reports are collected,

analysed and presented (Ebaid, 2016). The financial status of businesses can be seen by

customers and stakeholders in this reporting phase. Along with this financial accounting, the

work of all company operations in respect of profit or loss has a critical part to play. Essentially,

it includes several forms of accounting records and accounts such as P&L book, balance sheet,

revenue tax etc. This business offers small-scale accounting large variety of services. In addition,

in the project report, role of companies is best described in the phrase financial accounting. In

order to determine their value in the financial details, both various stakeholders are listed.

Similar activities are performed by five clients in perhaps a section of the survey.

TASK

PART A

1. Financial accounting with its main purpose for company.

In general terms, the phrase "financial statements" applies to the collection of financial

details in the context of financial reporting to diverse stakeholders (Nilsson and Stockenstrand

2015). This accounting is primarily designed to awaken corporations to produce shift in business

time over the course. Eventually, the annual statements shall be reported towards the close of the

fiscal cycle of the statutory reports. There will be several forms of difficulties in the lack of this

accounting method. Unlike other owners, the shareholder in the business would have little

impact. Moreover, the companies would have trouble understanding their current financial

position. Internal manager file different kinds of financial reports including a P&L report and the

balance sheet respectively within the consulting company. In addition, they provide complete

financial reports and make decisions based of that factors which impact business conditions.

In this respect, it is crucial to be aware of the financial accountability standards and rules.

This is how the annual results are found null in the lack of these reporting requirements. GAAP

is understood as the common accounting concept as the most basic characteristic of financial

performance. The accounts and analyses are defined under certain standards of financial

reporting. Below are listed other uses of financial accounting:

Advantageous in calculating cash flow: Financial reports aid to reliably predict working

capital on the impact of accounting reports. It is important because businesses will

determine the operation that produces further cash and what is not, according to benefit

and loss report statistics. This allows the cash balance to be expected.

Assistance to taxes decision-making: Financial management for companies is also

effective when getting tax judgments (Burritt and Schaltegger 2014). That is why firms

can calculate a total tax payable on earnings with both the assistance of income

declarations.

Provide a basis for plans: In addition to the financial statements, successful and

strategic tactics are created. In the end, businesses will define means of generating

appropriate policies and proposals dependent on sales and investment.

Provide accurate information: It is observed that financial information for about their

numerous functions and processes can be provided by revenue recognition firms. It is

therefore connected all in all to the quantification of the real financial position.

Helpful in decision-making: Financial accounting is indeed helpful in making

appropriate decision, in addition to the above advantages for each sort of organisation.

For e.g. if the financial position of some business becomes stronger, they may plan to

grow the business. Therefore, for judgments, the financial statements are important.

Good for the groups concerned: The banking structure is beneficial for all internally

and externally players. Efficient policies and approaches may be drawn up based on

financial reports by the internal customers. The financial position is understood and

commitment rendered appropriately, as will other stakeholders.

Comparison benefit: It is among the most significant aspects of financial statements

as companies can monitor and correlate their previous accounts with their overall results

in the present accounting year with the support of financial system.

From the above all discussion, it has been stated that considerable usage in financial

statements is often related to as bookkeeping for reporting corporate transactions. The

accounting statements are used by company managers to list economic operations in the

corporate folders. Because each financial exchange involves a double entry scheme, two

accounts have an effect that reveals all sides of an exchange. For example, if the small

businessman is purchasing houses, a bank card to the real estate account is recorded to display

the value of the property receipt and then a cash-credit to demonstrate cash output. Financial

accounting may help owners to remind internal customers such as their staff of the successes and

and loss report statistics. This allows the cash balance to be expected.

Assistance to taxes decision-making: Financial management for companies is also

effective when getting tax judgments (Burritt and Schaltegger 2014). That is why firms

can calculate a total tax payable on earnings with both the assistance of income

declarations.

Provide a basis for plans: In addition to the financial statements, successful and

strategic tactics are created. In the end, businesses will define means of generating

appropriate policies and proposals dependent on sales and investment.

Provide accurate information: It is observed that financial information for about their

numerous functions and processes can be provided by revenue recognition firms. It is

therefore connected all in all to the quantification of the real financial position.

Helpful in decision-making: Financial accounting is indeed helpful in making

appropriate decision, in addition to the above advantages for each sort of organisation.

For e.g. if the financial position of some business becomes stronger, they may plan to

grow the business. Therefore, for judgments, the financial statements are important.

Good for the groups concerned: The banking structure is beneficial for all internally

and externally players. Efficient policies and approaches may be drawn up based on

financial reports by the internal customers. The financial position is understood and

commitment rendered appropriately, as will other stakeholders.

Comparison benefit: It is among the most significant aspects of financial statements

as companies can monitor and correlate their previous accounts with their overall results

in the present accounting year with the support of financial system.

From the above all discussion, it has been stated that considerable usage in financial

statements is often related to as bookkeeping for reporting corporate transactions. The

accounting statements are used by company managers to list economic operations in the

corporate folders. Because each financial exchange involves a double entry scheme, two

accounts have an effect that reveals all sides of an exchange. For example, if the small

businessman is purchasing houses, a bank card to the real estate account is recorded to display

the value of the property receipt and then a cash-credit to demonstrate cash output. Financial

accounting may help owners to remind internal customers such as their staff of the successes and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

limitations of the business. This detail may be utilized by organizations that include their

workers with income sharing or stock-based incentive schemes. For limited public firms, the

company's share price is a common indicator. In order to share the amount, and to promote

employee efficiency, small companies should balance their incentives and salary rates if

appropriate. These are the primary aims of financial accounting, because of this, are the

organizations' compulsory accounting systems.

2. Types of internal and external stakeholders.

Stakeholders: It is a collective of people involved in all company practices (McCarthy,

Shelmon and Mattie, 2012). Many stakeholders are concerned with earning income. The

stakeholders are usually categorized into two kinds:

• Internal interested parties

• External stakeholders

For enterprises, all of the shareholders are relevant since they have an involvement in market

practices. The following are listed and their specific meanings are elaborated underneath:

Internal interested parties: Local partners engage in regular market operations and learn about

the priorities. Such shareholders can be influenced by client strategies and policies. A few typical

examples involve staff, BOD (Director's Board), administrators, etc. The following parties are

listed in a specific sense: In this connection:

• Board of Directors: The BOD is a community of individuals who are obsessed about

laws and regulations are mindful that such laws are inferred within company process.

They are generally known as divisions at the upper level which make most of the crucial

decision within company. They demonstrate a role in the business's financial data, even

though they develop additional policies and tactics on this basis.

• Employees: These are seen as people or groups who carry out different activities and

tasks in order to get their salaries or salaries. Finally, workers play a significant part in

the organization's commitment to income. To the effect, they express a concern in the

financial state of the organization and assess if it has ample funds left to pay the

employees.

External stakeholders: These are individuals that are not involved in commercial practices but

have interest in each transaction. These parties' main aim is to put money the finance in the

workers with income sharing or stock-based incentive schemes. For limited public firms, the

company's share price is a common indicator. In order to share the amount, and to promote

employee efficiency, small companies should balance their incentives and salary rates if

appropriate. These are the primary aims of financial accounting, because of this, are the

organizations' compulsory accounting systems.

2. Types of internal and external stakeholders.

Stakeholders: It is a collective of people involved in all company practices (McCarthy,

Shelmon and Mattie, 2012). Many stakeholders are concerned with earning income. The

stakeholders are usually categorized into two kinds:

• Internal interested parties

• External stakeholders

For enterprises, all of the shareholders are relevant since they have an involvement in market

practices. The following are listed and their specific meanings are elaborated underneath:

Internal interested parties: Local partners engage in regular market operations and learn about

the priorities. Such shareholders can be influenced by client strategies and policies. A few typical

examples involve staff, BOD (Director's Board), administrators, etc. The following parties are

listed in a specific sense: In this connection:

• Board of Directors: The BOD is a community of individuals who are obsessed about

laws and regulations are mindful that such laws are inferred within company process.

They are generally known as divisions at the upper level which make most of the crucial

decision within company. They demonstrate a role in the business's financial data, even

though they develop additional policies and tactics on this basis.

• Employees: These are seen as people or groups who carry out different activities and

tasks in order to get their salaries or salaries. Finally, workers play a significant part in

the organization's commitment to income. To the effect, they express a concern in the

financial state of the organization and assess if it has ample funds left to pay the

employees.

External stakeholders: These are individuals that are not involved in commercial practices but

have interest in each transaction. These parties' main aim is to put money the finance in the

company with the assumption that they will receive the return. Consumers, suppliers, creditors

etc. are a prominent example. The following are the following stakeholders:

• The Supplier: Depending on their financial state, they render the payment exchange with

businesses. This is to suggest, manufacturers offer the requisite content on credit for

goodwill to businesses. In theory, for the cash contract the vendors demonstrate concern

in the company's financial position.

• Investor: These are the number of people that buy shares their financial resources in the

exchange share of organizations. They assess the financial condition of businesses before

allowing even expenditure. To them, however, financial knowledge is very helpful in

predicting potential returns on their savings.

• Creditors: The investors are those that demand another party's assets (Blake, 2013). In

other terms, the individual about whom income owes may be identified. Finally, in order

to decide whether or not to offer financial support with some individual business, they

show their concern in the firm’s financial position.

• Government: This is the last player to differentiate from the others. They contribute to

the creation of regulations, statutes and laws that are important for businesses to obey.

Both government and organizations receive the tax that enables them to run the specific

activities for the growth of nation or firm operation.

These are also the external customers of firms that demonstrate their own involvement in

businesses task and function in order to earn a subsequent amount over the investment.

PART B

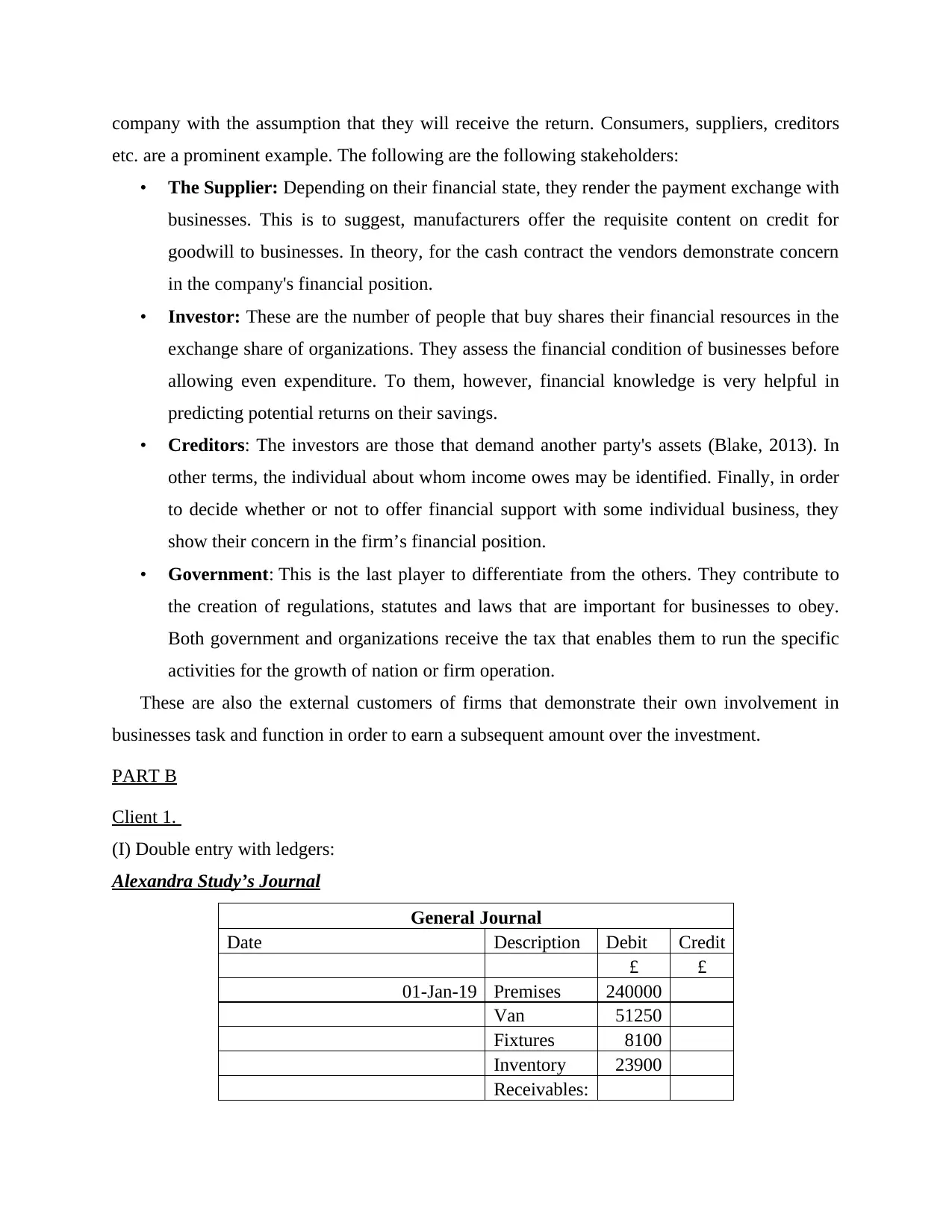

Client 1.

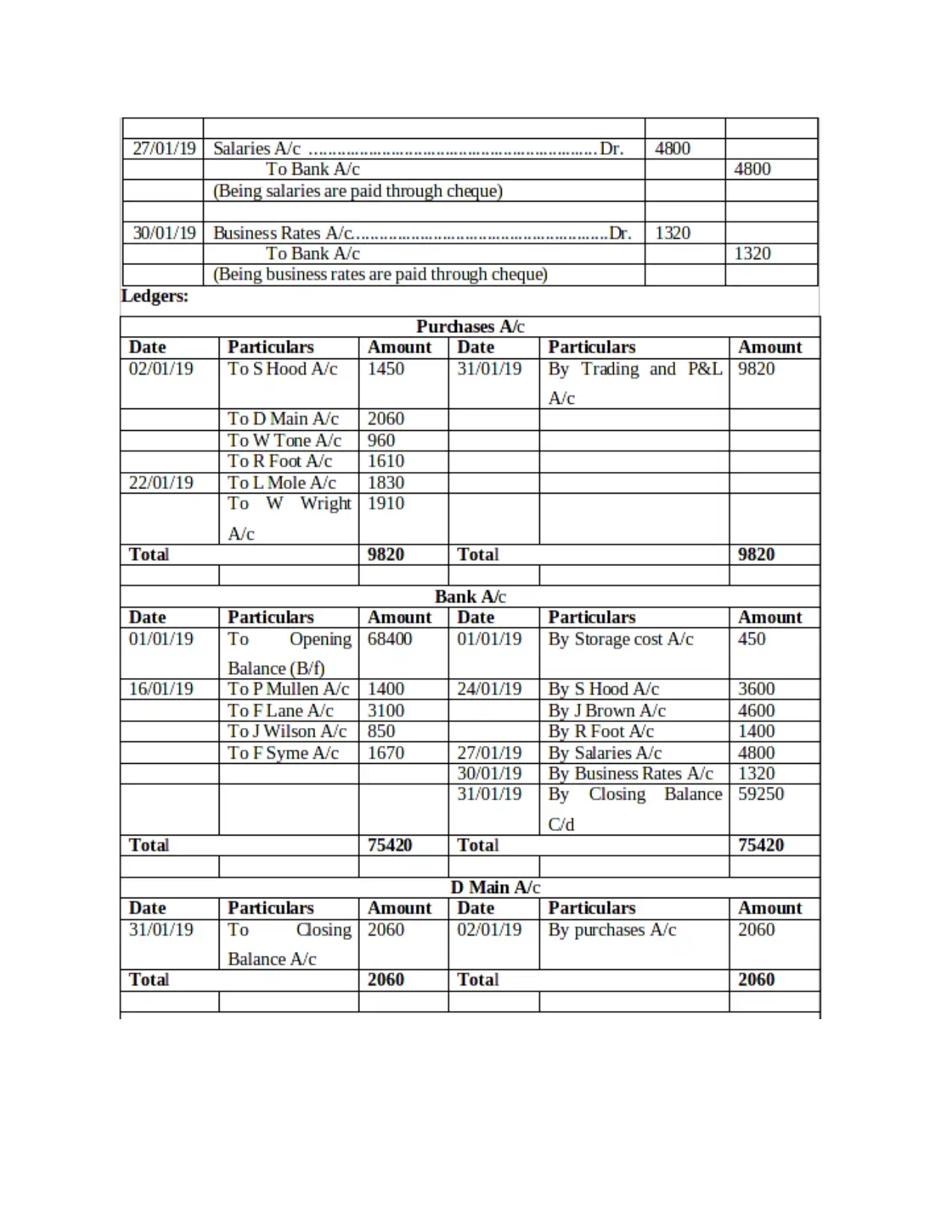

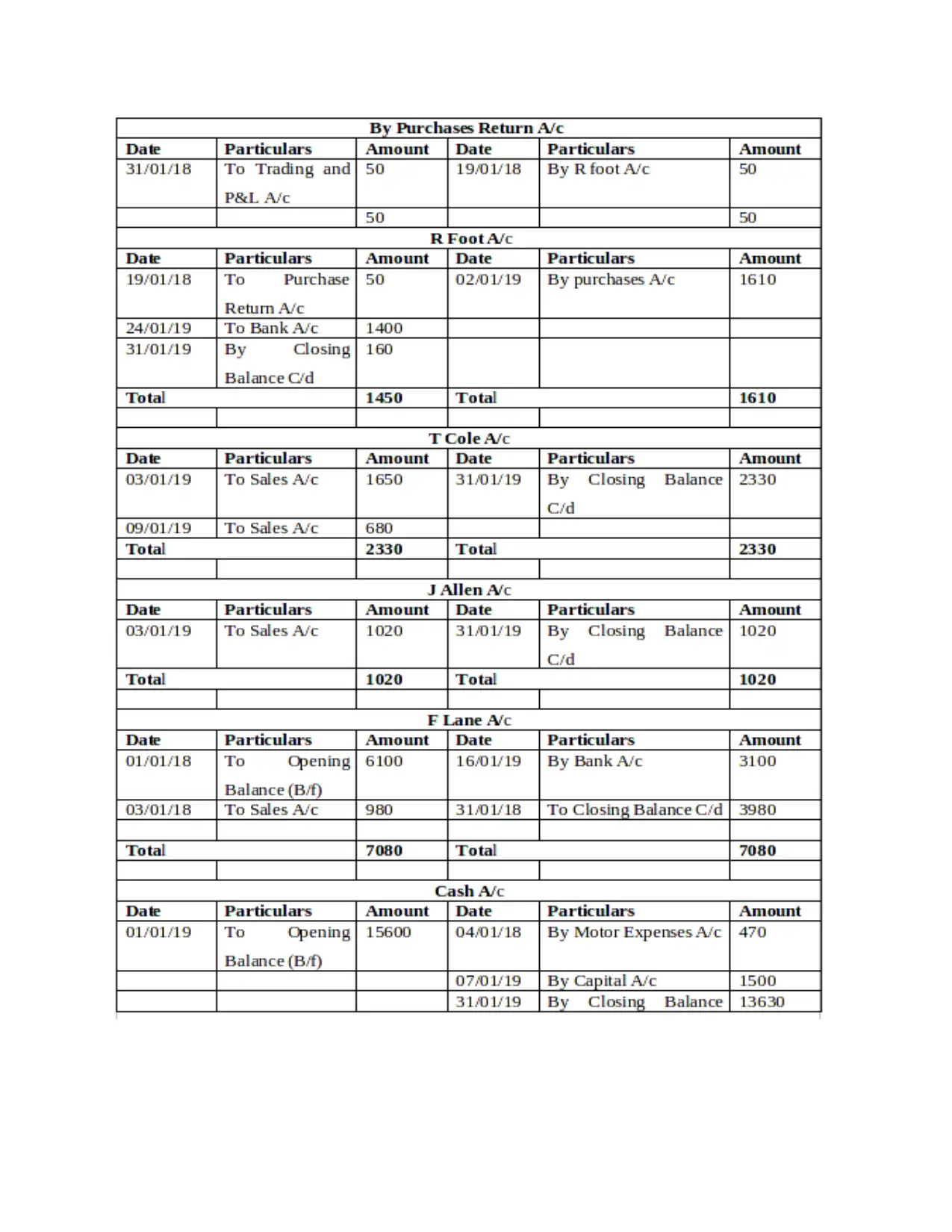

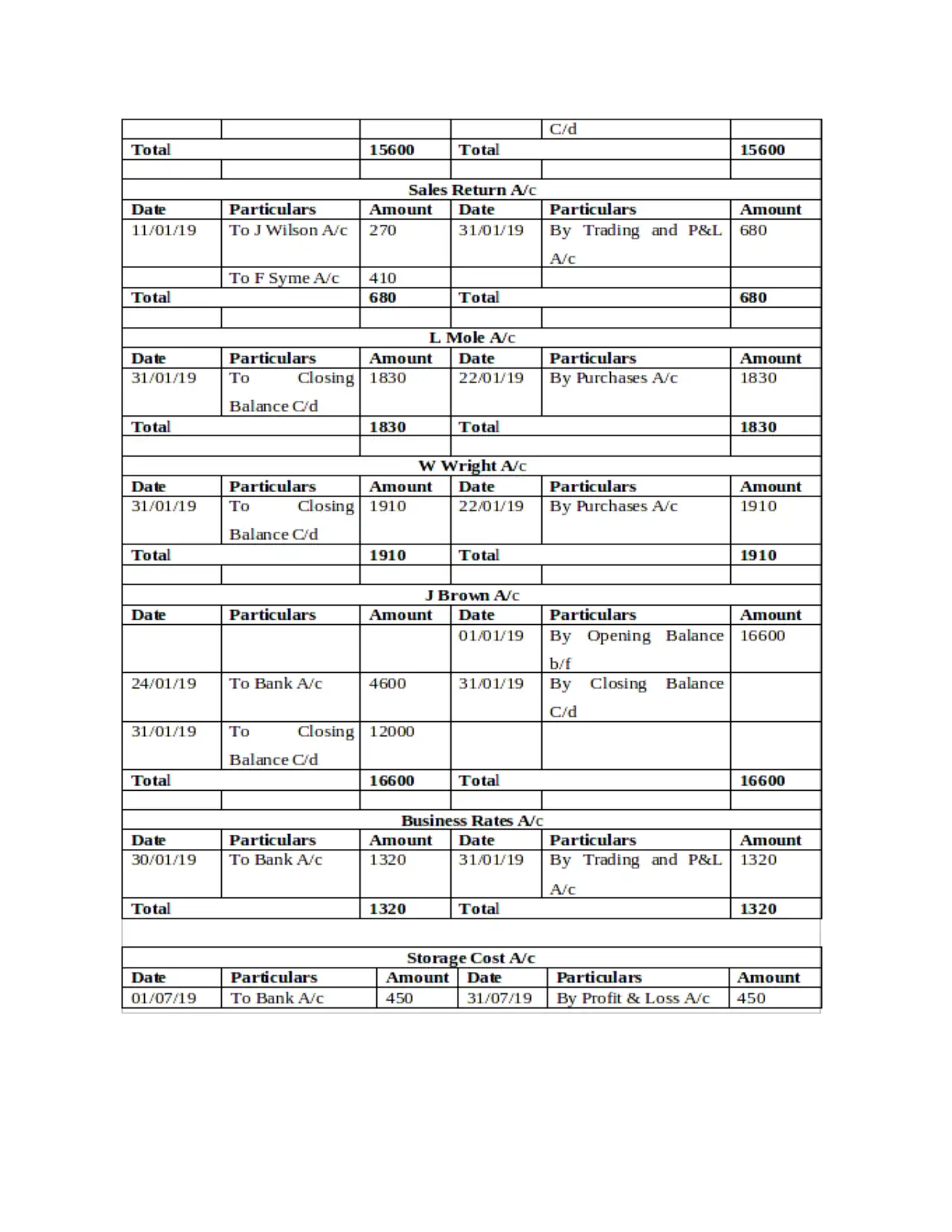

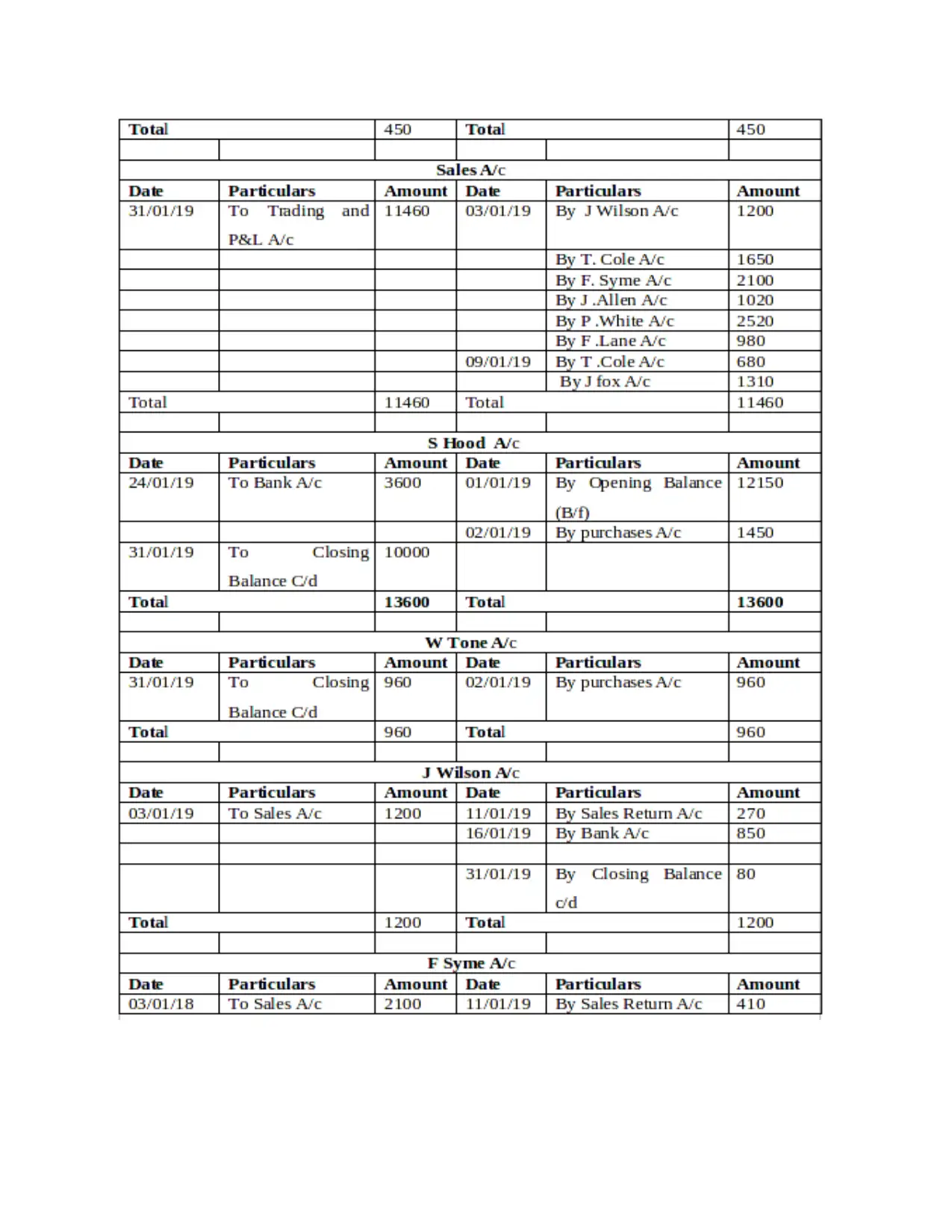

(I) Double entry with ledgers:

Alexandra Study’s Journal

General Journal

Date Description Debit Credit

£ £

01-Jan-19 Premises 240000

Van 51250

Fixtures 8100

Inventory 23900

Receivables:

etc. are a prominent example. The following are the following stakeholders:

• The Supplier: Depending on their financial state, they render the payment exchange with

businesses. This is to suggest, manufacturers offer the requisite content on credit for

goodwill to businesses. In theory, for the cash contract the vendors demonstrate concern

in the company's financial position.

• Investor: These are the number of people that buy shares their financial resources in the

exchange share of organizations. They assess the financial condition of businesses before

allowing even expenditure. To them, however, financial knowledge is very helpful in

predicting potential returns on their savings.

• Creditors: The investors are those that demand another party's assets (Blake, 2013). In

other terms, the individual about whom income owes may be identified. Finally, in order

to decide whether or not to offer financial support with some individual business, they

show their concern in the firm’s financial position.

• Government: This is the last player to differentiate from the others. They contribute to

the creation of regulations, statutes and laws that are important for businesses to obey.

Both government and organizations receive the tax that enables them to run the specific

activities for the growth of nation or firm operation.

These are also the external customers of firms that demonstrate their own involvement in

businesses task and function in order to earn a subsequent amount over the investment.

PART B

Client 1.

(I) Double entry with ledgers:

Alexandra Study’s Journal

General Journal

Date Description Debit Credit

£ £

01-Jan-19 Premises 240000

Van 51250

Fixtures 8100

Inventory 23900

Receivables:

P Mullen 4400

F Lane 6100

Cash at

Bank 68400

Cash in

hand 15600

Payable:

S. Hood 12150

J. Brown 16600

Total 417750 28750

In order to calculate Alexandra’s capital, the accounting equation has to be applied.

Assets = Capital + Liability

417 750 = Capital + 28 750

Therefore, her capital equals to £389 000 (417 750 – 28 750).

F Lane 6100

Cash at

Bank 68400

Cash in

hand 15600

Payable:

S. Hood 12150

J. Brown 16600

Total 417750 28750

In order to calculate Alexandra’s capital, the accounting equation has to be applied.

Assets = Capital + Liability

417 750 = Capital + 28 750

Therefore, her capital equals to £389 000 (417 750 – 28 750).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

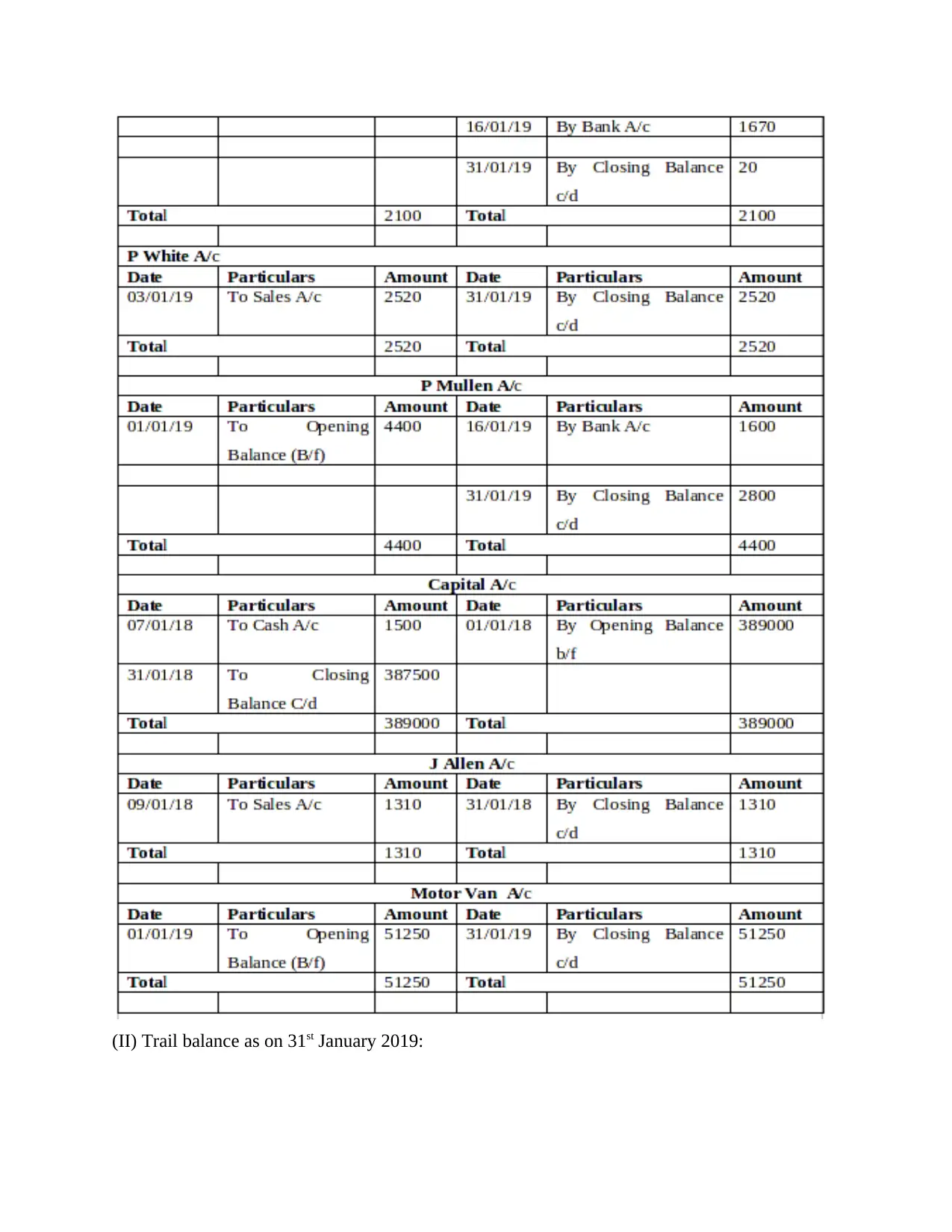

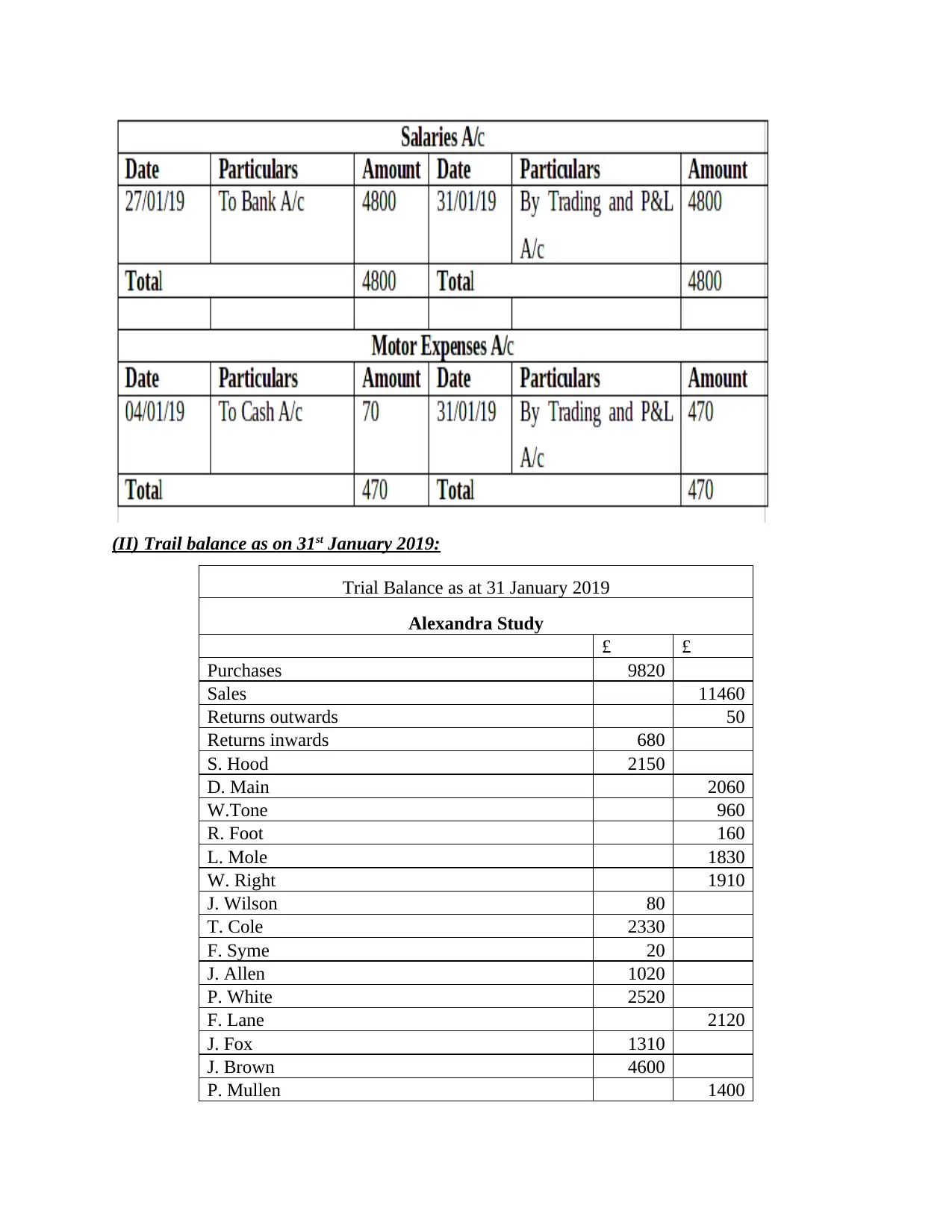

(II) Trail balance as on 31st January 2019:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(II) Trail balance as on 31st January 2019:

Trial Balance as at 31 January 2019

Alexandra Study

£ £

Purchases 9820

Sales 11460

Returns outwards 50

Returns inwards 680

S. Hood 2150

D. Main 2060

W.Tone 960

R. Foot 160

L. Mole 1830

W. Right 1910

J. Wilson 80

T. Cole 2330

F. Syme 20

J. Allen 1020

P. White 2520

F. Lane 2120

J. Fox 1310

J. Brown 4600

P. Mullen 1400

Trial Balance as at 31 January 2019

Alexandra Study

£ £

Purchases 9820

Sales 11460

Returns outwards 50

Returns inwards 680

S. Hood 2150

D. Main 2060

W.Tone 960

R. Foot 160

L. Mole 1830

W. Right 1910

J. Wilson 80

T. Cole 2330

F. Syme 20

J. Allen 1020

P. White 2520

F. Lane 2120

J. Fox 1310

J. Brown 4600

P. Mullen 1400

Storage Expense 450

Bank 9150

Motor Expense 470

Cash 1970

Drawings 1500

Salaries 4800

Business Rates 1320

Total 33070 33070

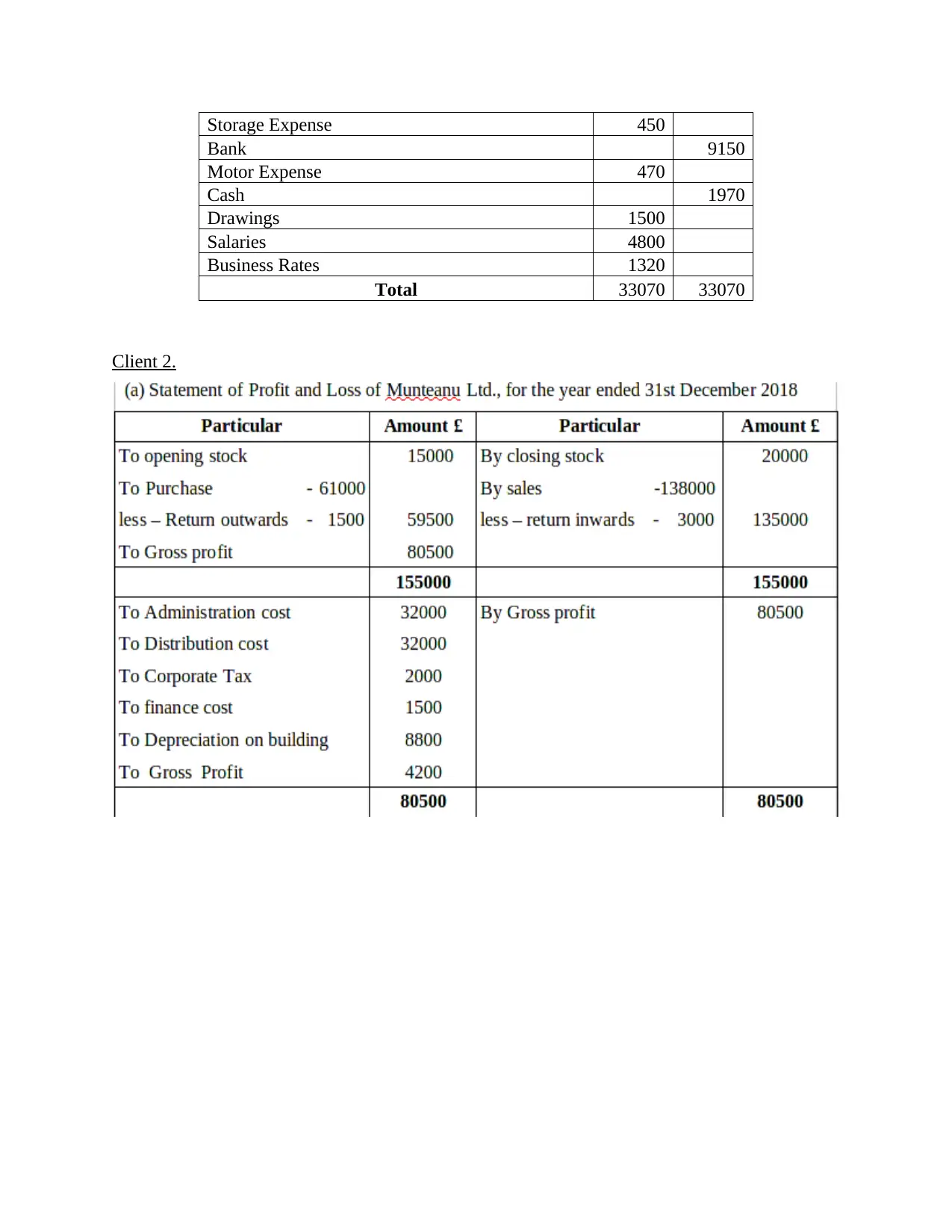

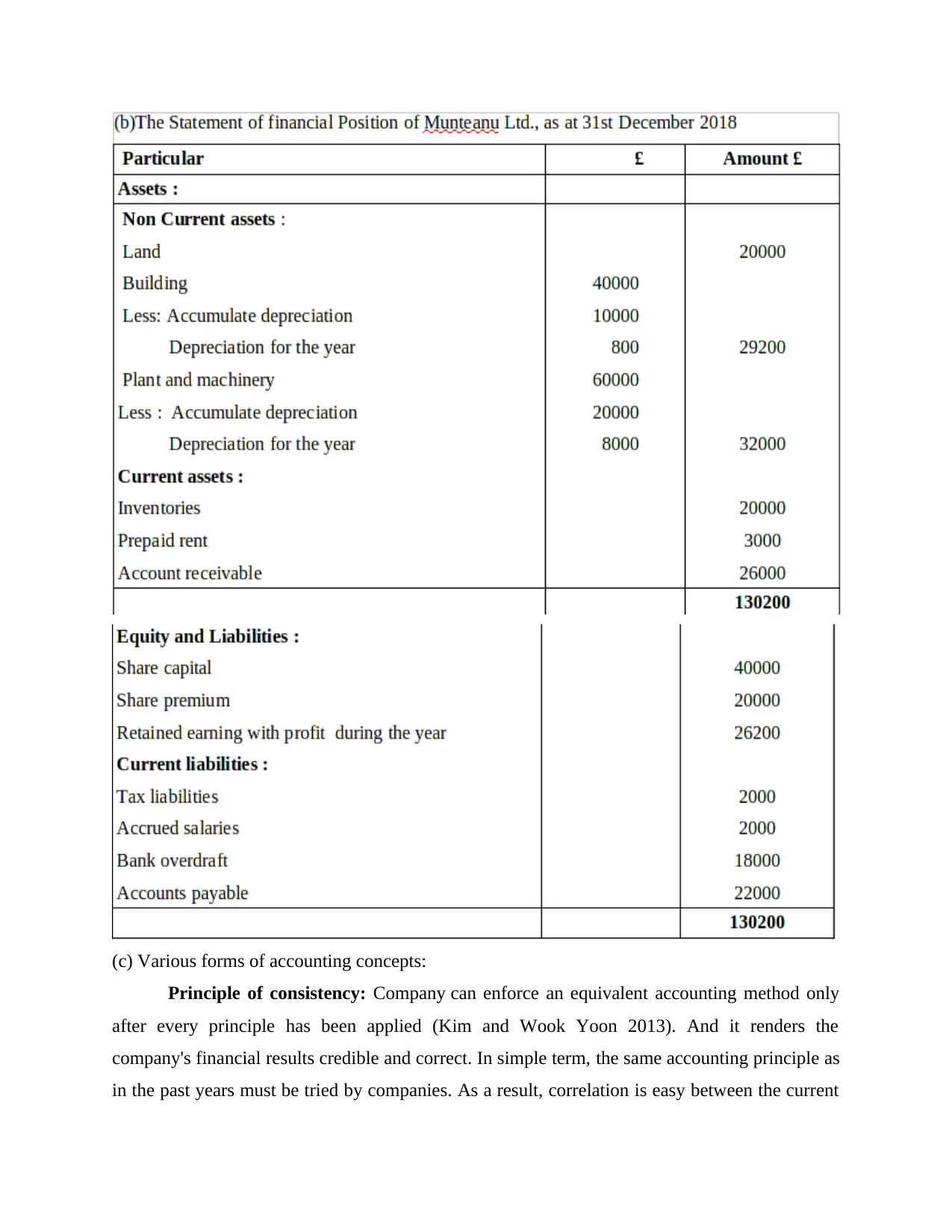

Client 2.

Bank 9150

Motor Expense 470

Cash 1970

Drawings 1500

Salaries 4800

Business Rates 1320

Total 33070 33070

Client 2.

(c) Various forms of accounting concepts:

Principle of consistency: Company can enforce an equivalent accounting method only

after every principle has been applied (Kim and Wook Yoon 2013). And it renders the

company's financial results credible and correct. In simple term, the same accounting principle as

in the past years must be tried by companies. As a result, correlation is easy between the current

Principle of consistency: Company can enforce an equivalent accounting method only

after every principle has been applied (Kim and Wook Yoon 2013). And it renders the

company's financial results credible and correct. In simple term, the same accounting principle as

in the past years must be tried by companies. As a result, correlation is easy between the current

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

year and the past year by these organizations. Finally, it would be impossible for the companies,

without this definition, to critically evaluate their income reports. In fact, the auditors also

recommend that certain customers follow a specific accounting term for all financial period. The

auditors will disregard suggesting the financial report in the lack of such an accounting principle.

Generally speaking, businesses disregard the quality principle of reporting to demonstrate the

greatest benefit from the income statements.

Prudence principle: This accounting framework definition applies to a corporation that

does not misjudge its income and overlook spending number. They are fundamental elements of

the financial statements that provide more reliable data to reflect the business for reporting.

Prudence principles usually refer to the establishment of the obsolete stock for questionable

commitments or reservations. The financial reports are defined by the international Accounting

Framework (IAS) as well as the GAAP, as described here. The financial report and interpretation

of the details and statistic stated in the accounting book using this approach are more accurate

and secure.

D) The intention of the asset value when the financial statements are formulated.

Depreciation: The quality of any specific assets could be described as a decrease as time

passes (Zeff, 2016). This is usually charged for actual damage over the investments. Further, the

decay becomes positive because asset losses are allocated over asset existence.

Objective of depreciation: The primary aim of depreciation is simply to assess the true

worth of the properties. Within this relation, the following is some purpose:

• The first goal of the deterioration is to determine the exact effects of the job.

• The measurement of the real value of properties is another objective of the depreciation

process.

• Business organizations can find the full financial situation and also depreciation and

amortization.

• To assess the profitability value of fixed assets induced by period as well as the

utilization of fixed assets.

Depreciation estimation technique: there have been various forms of depreciation

measurement processes. Some factors are given here below:

• Straight line method: A fixed installation process is also known (DeBerg and Chapman,

2012). It is a tool which is used over the entire lifespan to calculate the carrying value of

without this definition, to critically evaluate their income reports. In fact, the auditors also

recommend that certain customers follow a specific accounting term for all financial period. The

auditors will disregard suggesting the financial report in the lack of such an accounting principle.

Generally speaking, businesses disregard the quality principle of reporting to demonstrate the

greatest benefit from the income statements.

Prudence principle: This accounting framework definition applies to a corporation that

does not misjudge its income and overlook spending number. They are fundamental elements of

the financial statements that provide more reliable data to reflect the business for reporting.

Prudence principles usually refer to the establishment of the obsolete stock for questionable

commitments or reservations. The financial reports are defined by the international Accounting

Framework (IAS) as well as the GAAP, as described here. The financial report and interpretation

of the details and statistic stated in the accounting book using this approach are more accurate

and secure.

D) The intention of the asset value when the financial statements are formulated.

Depreciation: The quality of any specific assets could be described as a decrease as time

passes (Zeff, 2016). This is usually charged for actual damage over the investments. Further, the

decay becomes positive because asset losses are allocated over asset existence.

Objective of depreciation: The primary aim of depreciation is simply to assess the true

worth of the properties. Within this relation, the following is some purpose:

• The first goal of the deterioration is to determine the exact effects of the job.

• The measurement of the real value of properties is another objective of the depreciation

process.

• Business organizations can find the full financial situation and also depreciation and

amortization.

• To assess the profitability value of fixed assets induced by period as well as the

utilization of fixed assets.

Depreciation estimation technique: there have been various forms of depreciation

measurement processes. Some factors are given here below:

• Straight line method: A fixed installation process is also known (DeBerg and Chapman,

2012). It is a tool which is used over the entire lifespan to calculate the carrying value of

every fixed asset. This approach is generally used in depreciation estimation at long last.

The following steps are indicated in the calculation of depreciation:

Analysis of the capital asset initial expenses.

1. Then remove the replacement cost again from value of assets of fixed assets.

2. Approximately asset life determination.

3. The impairment levels and asset prices would then increase.

Here are the measures to measure the deterioration by this process of some real assets.

Finally, the depreciation estimation is calculated with the following formula:

Depreciation: (Cost of assets- scrap value)/ Life of assets.

• Reduction of the consistency method: This is a form of method of depreciation that is

determined on a fixed rate equal to the straight line depreciation (Giner, 2014). In

addition to the way of reducing stability, the percentage of the rate is not calculated based

on asset costs. This calculates the frequency on the fixed asset market value. This

approach is basically ideal for machines, generators, etc.

(e) Assessment of disparity between business owners and restricted corporations' financial

reports

Basis of

difference

Sole traders Limited company

Auditing There is no requirement to perform

the analysis of financial records in the

financial reports of the single traders.

From the other side, it is important

that the businesses perform the

examination mostly on financial

records of the general company in

order to determine the quality of the

documents prepared.

Equity Just one element in the financial

reports of the small businesses is the

wealth of the lender.

The shareholding of the shareholder

includes share value, surplus of cash,

retained profits, etc.

Preparation of

financial

statements

It involves the preparing of the annual

statements and audits for the company

owner.

Accountants write the annual report

for the firms.

The following steps are indicated in the calculation of depreciation:

Analysis of the capital asset initial expenses.

1. Then remove the replacement cost again from value of assets of fixed assets.

2. Approximately asset life determination.

3. The impairment levels and asset prices would then increase.

Here are the measures to measure the deterioration by this process of some real assets.

Finally, the depreciation estimation is calculated with the following formula:

Depreciation: (Cost of assets- scrap value)/ Life of assets.

• Reduction of the consistency method: This is a form of method of depreciation that is

determined on a fixed rate equal to the straight line depreciation (Giner, 2014). In

addition to the way of reducing stability, the percentage of the rate is not calculated based

on asset costs. This calculates the frequency on the fixed asset market value. This

approach is basically ideal for machines, generators, etc.

(e) Assessment of disparity between business owners and restricted corporations' financial

reports

Basis of

difference

Sole traders Limited company

Auditing There is no requirement to perform

the analysis of financial records in the

financial reports of the single traders.

From the other side, it is important

that the businesses perform the

examination mostly on financial

records of the general company in

order to determine the quality of the

documents prepared.

Equity Just one element in the financial

reports of the small businesses is the

wealth of the lender.

The shareholding of the shareholder

includes share value, surplus of cash,

retained profits, etc.

Preparation of

financial

statements

It involves the preparing of the annual

statements and audits for the company

owner.

Accountants write the annual report

for the firms.

Amount of

transaction

Finally, the volume of financial

transactions is smaller in the lone

traders owing to their limited business

scale.

At the other side, a number of non -

financial and financial activities occur

in the limited firms.

Mandatory The preparing of the financial report

is not mandatory for single traders

(Wang, 2014).

To order to assess the financial

condition, it is important for them to

review the financial accounts.

Client 3.

(A) Purpose of preparation of BRS

The system for bank reconciliation is the system being established to align the cash position

with the facts on the bank card. Finally, to monitor corporate transactions and company keeps a

cash register. This is a simple declaration and is intended to test the bank account on the

specified date according to the transfer bank as well as cash register. It indicates whether there

are any variations between them. The key aim is to find theft and mistakes in the account and

bank balance to explain the results. The following are, in this context, other reasons for planning

the BRS:

• Check for validity: The key aim of planning is to determine the correct and consistency

of the bank statement of the BR account.

• Prevention of theft: Bank recovery system other than that is meant to report frauds so

errors in cash accounts.

• Transparency: The BR statements often help explain the balance deposited in cash

records. This is the primary objective for all sizes of industries to prepare a BRS.

(B) Areas where bank statements as well as cash books are different:

• Failure to become conscious of bank costs: This is the key explanation that checking

statements vary from bank reports. For this reason, banks often pay a certain sum owing

to their operation. The bank will not ask the employee about this charge and this will be

the distinguishing factor.

• Direct debited mortgage interest: Another source of variance is the volume of

mortgage interest charged on the mortgage. It is not included in the cash journals

(Canziani, 2014), in the absence of facts.

transaction

Finally, the volume of financial

transactions is smaller in the lone

traders owing to their limited business

scale.

At the other side, a number of non -

financial and financial activities occur

in the limited firms.

Mandatory The preparing of the financial report

is not mandatory for single traders

(Wang, 2014).

To order to assess the financial

condition, it is important for them to

review the financial accounts.

Client 3.

(A) Purpose of preparation of BRS

The system for bank reconciliation is the system being established to align the cash position

with the facts on the bank card. Finally, to monitor corporate transactions and company keeps a

cash register. This is a simple declaration and is intended to test the bank account on the

specified date according to the transfer bank as well as cash register. It indicates whether there

are any variations between them. The key aim is to find theft and mistakes in the account and

bank balance to explain the results. The following are, in this context, other reasons for planning

the BRS:

• Check for validity: The key aim of planning is to determine the correct and consistency

of the bank statement of the BR account.

• Prevention of theft: Bank recovery system other than that is meant to report frauds so

errors in cash accounts.

• Transparency: The BR statements often help explain the balance deposited in cash

records. This is the primary objective for all sizes of industries to prepare a BRS.

(B) Areas where bank statements as well as cash books are different:

• Failure to become conscious of bank costs: This is the key explanation that checking

statements vary from bank reports. For this reason, banks often pay a certain sum owing

to their operation. The bank will not ask the employee about this charge and this will be

the distinguishing factor.

• Direct debited mortgage interest: Another source of variance is the volume of

mortgage interest charged on the mortgage. It is not included in the cash journals

(Canziani, 2014), in the absence of facts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(C) Imprest:

The imprest may usually be described as a form of fund used by organizations in the sense of

mini expenses. In fact, businesses are returned that volume of fund at a certain date. In addition,

it is applicable to financial transfers on a daily basis by businesses.

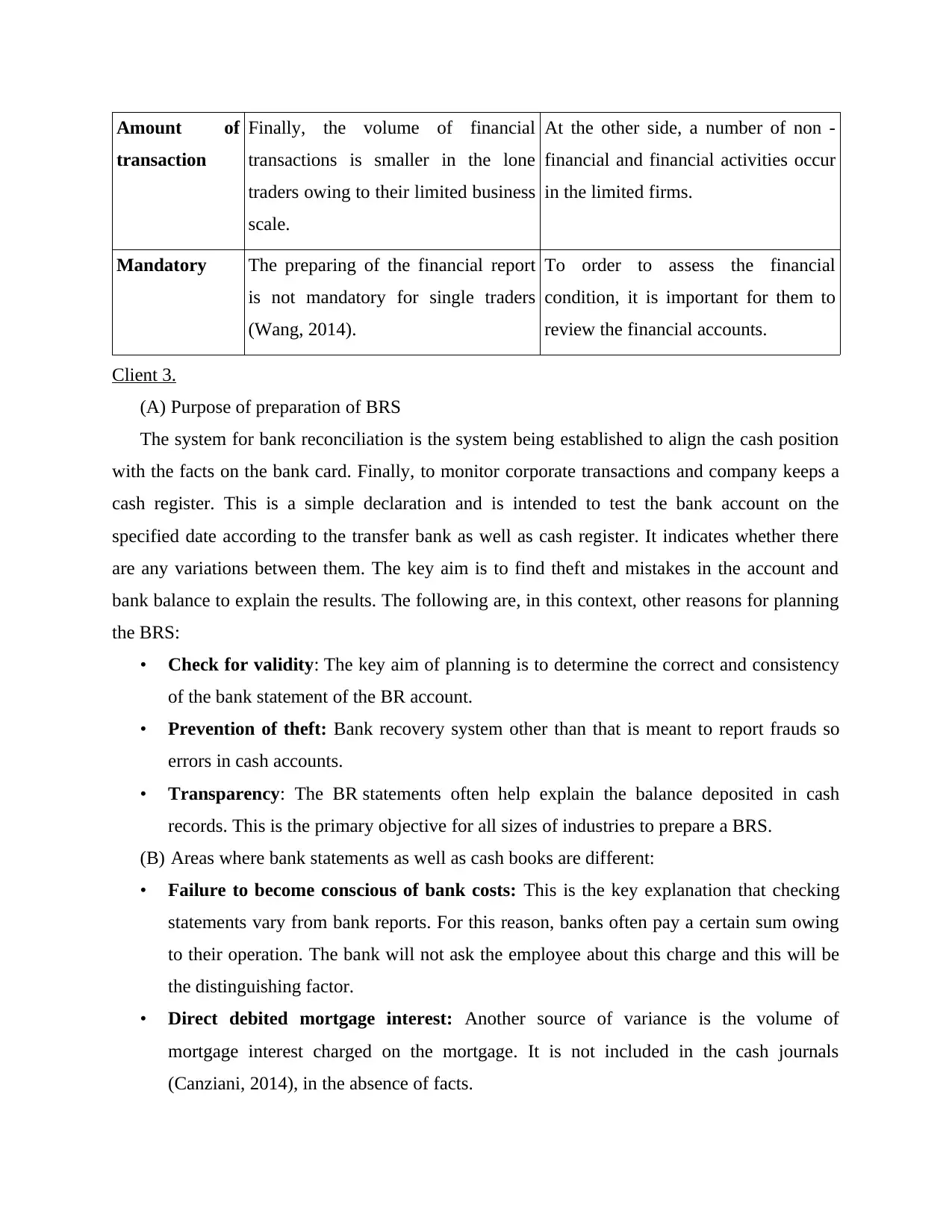

(D) Cash book for Burcu limited for september, 2018

Client 4

(a) Prepare and balance in the books of Hilly for January, 2018

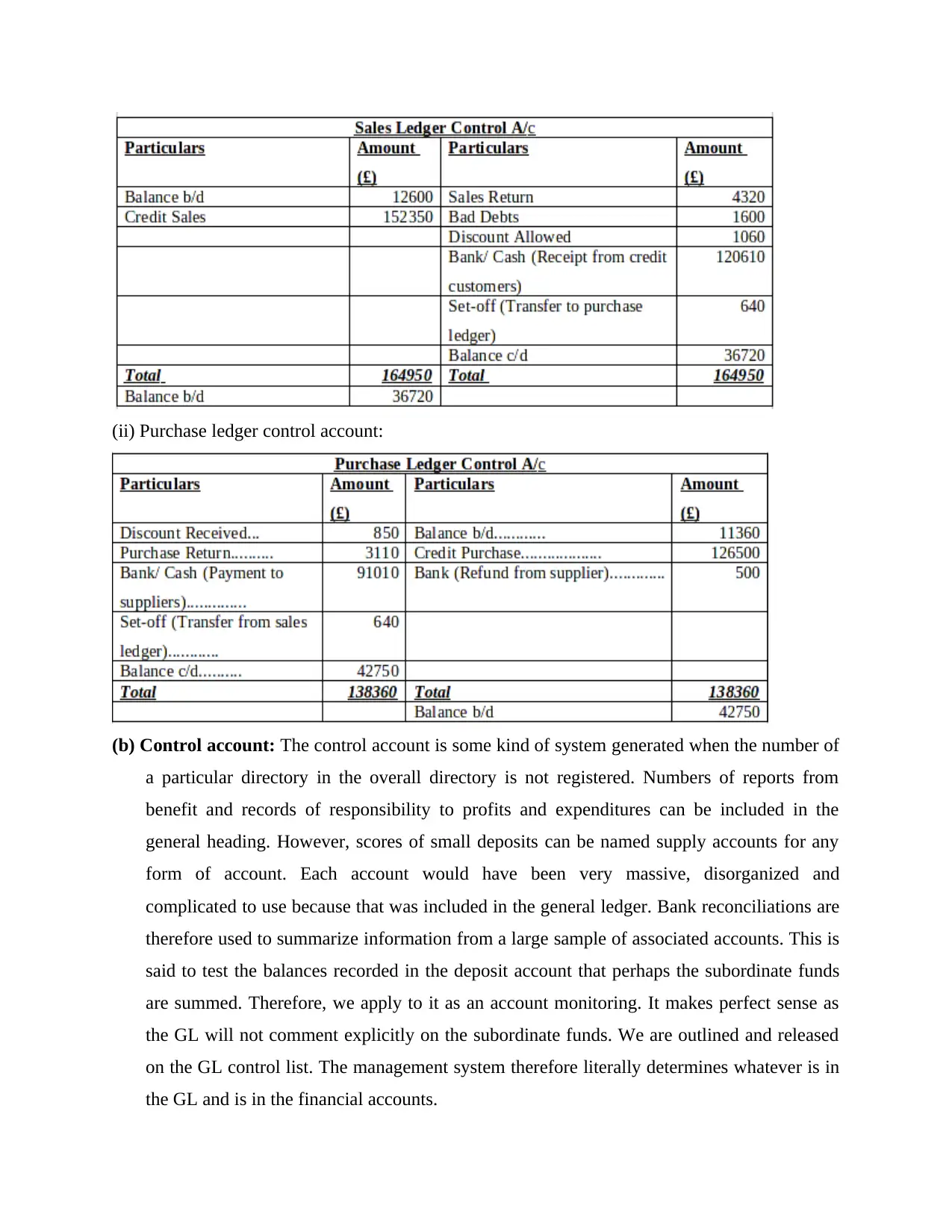

(I) Sales ledger control account:

The imprest may usually be described as a form of fund used by organizations in the sense of

mini expenses. In fact, businesses are returned that volume of fund at a certain date. In addition,

it is applicable to financial transfers on a daily basis by businesses.

(D) Cash book for Burcu limited for september, 2018

Client 4

(a) Prepare and balance in the books of Hilly for January, 2018

(I) Sales ledger control account:

(ii) Purchase ledger control account:

(b) Control account: The control account is some kind of system generated when the number of

a particular directory in the overall directory is not registered. Numbers of reports from

benefit and records of responsibility to profits and expenditures can be included in the

general heading. However, scores of small deposits can be named supply accounts for any

form of account. Each account would have been very massive, disorganized and

complicated to use because that was included in the general ledger. Bank reconciliations are

therefore used to summarize information from a large sample of associated accounts. This is

said to test the balances recorded in the deposit account that perhaps the subordinate funds

are summed. Therefore, we apply to it as an account monitoring. It makes perfect sense as

the GL will not comment explicitly on the subordinate funds. We are outlined and released

on the GL control list. The management system therefore literally determines whatever is in

the GL and is in the financial accounts.

(b) Control account: The control account is some kind of system generated when the number of

a particular directory in the overall directory is not registered. Numbers of reports from

benefit and records of responsibility to profits and expenditures can be included in the

general heading. However, scores of small deposits can be named supply accounts for any

form of account. Each account would have been very massive, disorganized and

complicated to use because that was included in the general ledger. Bank reconciliations are

therefore used to summarize information from a large sample of associated accounts. This is

said to test the balances recorded in the deposit account that perhaps the subordinate funds

are summed. Therefore, we apply to it as an account monitoring. It makes perfect sense as

the GL will not comment explicitly on the subordinate funds. We are outlined and released

on the GL control list. The management system therefore literally determines whatever is in

the GL and is in the financial accounts.

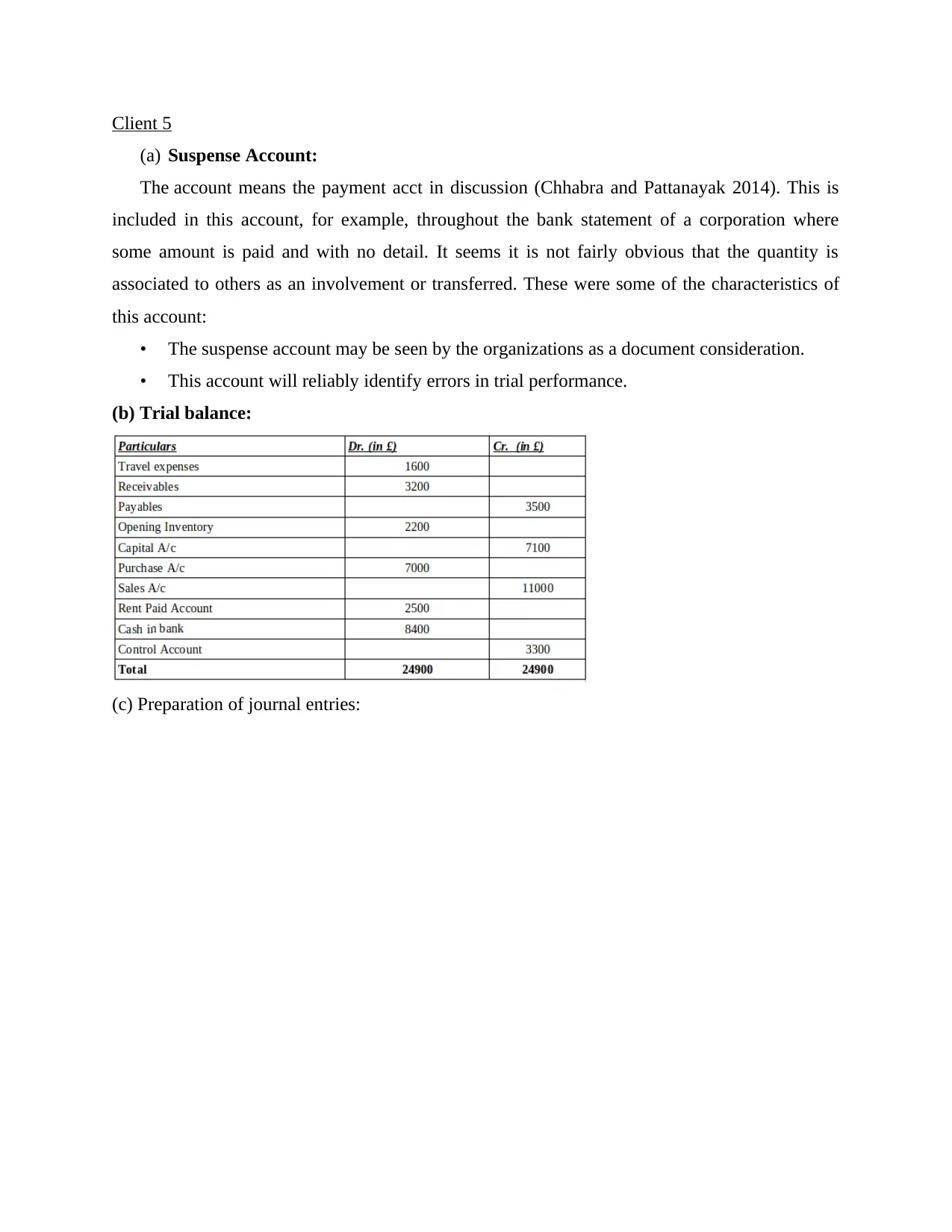

Client 5

(a) Suspense Account:

The account means the payment acct in discussion (Chhabra and Pattanayak 2014). This is

included in this account, for example, throughout the bank statement of a corporation where

some amount is paid and with no detail. It seems it is not fairly obvious that the quantity is

associated to others as an involvement or transferred. These were some of the characteristics of

this account:

• The suspense account may be seen by the organizations as a document consideration.

• This account will reliably identify errors in trial performance.

(b) Trial balance:

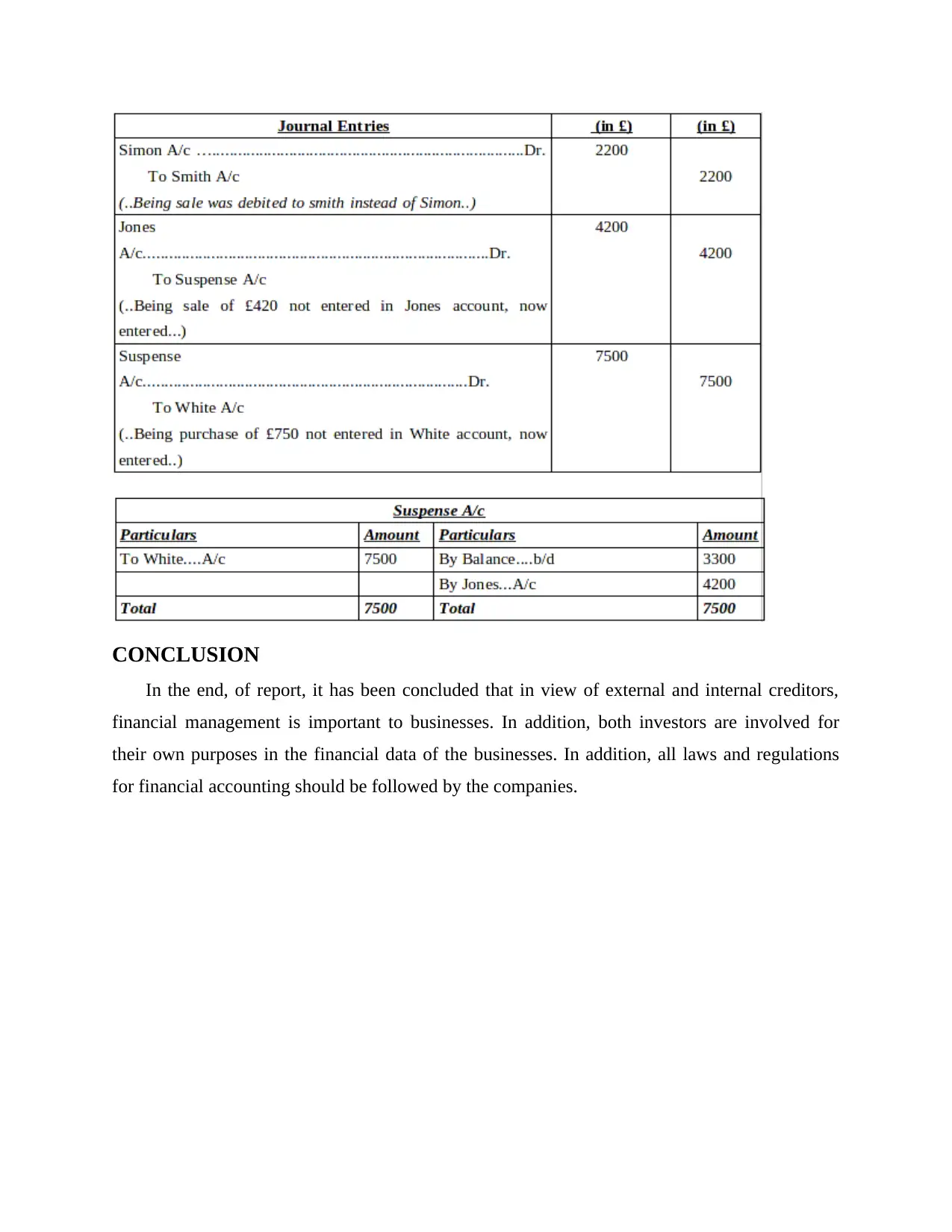

(c) Preparation of journal entries:

(a) Suspense Account:

The account means the payment acct in discussion (Chhabra and Pattanayak 2014). This is

included in this account, for example, throughout the bank statement of a corporation where

some amount is paid and with no detail. It seems it is not fairly obvious that the quantity is

associated to others as an involvement or transferred. These were some of the characteristics of

this account:

• The suspense account may be seen by the organizations as a document consideration.

• This account will reliably identify errors in trial performance.

(b) Trial balance:

(c) Preparation of journal entries:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

In the end, of report, it has been concluded that in view of external and internal creditors,

financial management is important to businesses. In addition, both investors are involved for

their own purposes in the financial data of the businesses. In addition, all laws and regulations

for financial accounting should be followed by the companies.

In the end, of report, it has been concluded that in view of external and internal creditors,

financial management is important to businesses. In addition, both investors are involved for

their own purposes in the financial data of the businesses. In addition, all laws and regulations

for financial accounting should be followed by the companies.

REFERENCES

Books and Journals

Blake, J. D., 2013. A Chinese perspective on international variations in accounting.

In Perspectives on Accounting and Finance in China (RLE Accounting). (pp. 15-34).

Routledge.

Burritt, R. and Schaltegger, S., 2014. Accounting towards sustainability in production and

supply chains. The British Accounting Review. 46(4). pp.327-343.

Canziani, A., 2014. Gino Zappa (1879-1960): accounting revolutionary. In Twentieth Century

Accounting Thinkers (RLE Accounting). (pp. 162-185). Routledge.

Chhabra, K. S. and Pattanayak, J. K., 2014. Financial accounting practices among small

enterprises: Issues and challenges. IUP Journal of Accounting Research & Audit

Practices. 13(3). p.37.

DeBerg, C. L. and Chapman, K. J., 2012. Assessing student performance and attitudes based on

common learning goals and alternative pedagogies: The case of principles of financial

accounting. Academy of Educational Leadership Journal. 16. p.63.

Ebaid, I. E. S., 2016. International accounting standards and accounting quality in code-law

countries: The case of Egypt. Journal of Financial Regulation and Compliance. 24(1).

pp.41-59.

Giner, B., 2014. Accounting for emission trading schemes: A still open debate. Social and

Environmental Accountability Journal. 34(1). pp.45-51.

Kim, S., Lee, C. and Wook Yoon, S., 2013. Goodwill accounting and asymmetric timeliness of

earnings. Review of Accounting and Finance. 12(2). pp.112-129.

McCarthy, J. H., Shelmon, N .E. and Mattie, J. A., 2012. Financial and accounting guide for

not-for-profit organizations(Vol. 6). John Wiley & Sons.

Nilsson, F. and Stockenstrand, A .K., 2015. Financial accounting and management control. The

tensions and conflicts between uniformity and uniqueness. Springer, Cham.

Wang, X., 2014. Research on the improvement of internal control under accounting

informationization environment. In Applied Mechanics and Materials. (Vol. 687, pp.

1962-1965). Trans Tech Publications.

Zeff, S. A., 2016. Forging accounting principles in five countries: A history and an analysis of

trends. Routledge.

Books and Journals

Blake, J. D., 2013. A Chinese perspective on international variations in accounting.

In Perspectives on Accounting and Finance in China (RLE Accounting). (pp. 15-34).

Routledge.

Burritt, R. and Schaltegger, S., 2014. Accounting towards sustainability in production and

supply chains. The British Accounting Review. 46(4). pp.327-343.

Canziani, A., 2014. Gino Zappa (1879-1960): accounting revolutionary. In Twentieth Century

Accounting Thinkers (RLE Accounting). (pp. 162-185). Routledge.

Chhabra, K. S. and Pattanayak, J. K., 2014. Financial accounting practices among small

enterprises: Issues and challenges. IUP Journal of Accounting Research & Audit

Practices. 13(3). p.37.

DeBerg, C. L. and Chapman, K. J., 2012. Assessing student performance and attitudes based on

common learning goals and alternative pedagogies: The case of principles of financial

accounting. Academy of Educational Leadership Journal. 16. p.63.

Ebaid, I. E. S., 2016. International accounting standards and accounting quality in code-law

countries: The case of Egypt. Journal of Financial Regulation and Compliance. 24(1).

pp.41-59.

Giner, B., 2014. Accounting for emission trading schemes: A still open debate. Social and

Environmental Accountability Journal. 34(1). pp.45-51.

Kim, S., Lee, C. and Wook Yoon, S., 2013. Goodwill accounting and asymmetric timeliness of

earnings. Review of Accounting and Finance. 12(2). pp.112-129.

McCarthy, J. H., Shelmon, N .E. and Mattie, J. A., 2012. Financial and accounting guide for

not-for-profit organizations(Vol. 6). John Wiley & Sons.

Nilsson, F. and Stockenstrand, A .K., 2015. Financial accounting and management control. The

tensions and conflicts between uniformity and uniqueness. Springer, Cham.

Wang, X., 2014. Research on the improvement of internal control under accounting

informationization environment. In Applied Mechanics and Materials. (Vol. 687, pp.

1962-1965). Trans Tech Publications.

Zeff, S. A., 2016. Forging accounting principles in five countries: A history and an analysis of

trends. Routledge.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.