Environmental Management and Islamic CSR

VerifiedAdded on 2020/02/03

|41

|6450

|41

Literature Review

AI Summary

This assignment examines the relationship between environmental management accounting practices within companies adhering to the ISO 14001 standard and their compliance with Islamic corporate social responsibility. It delves into empirical research and case studies to understand how these practices contribute to ethical and sustainable business operations within the framework of Islamic principles.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a) Meaning of financial accounting, regulation, rules and principles with effective concept

relating to consistency and material disclosure......................................................................1

(B) PORTFOLIO FOR A CLIENT.................................................................................................5

CLIENT 1........................................................................................................................................5

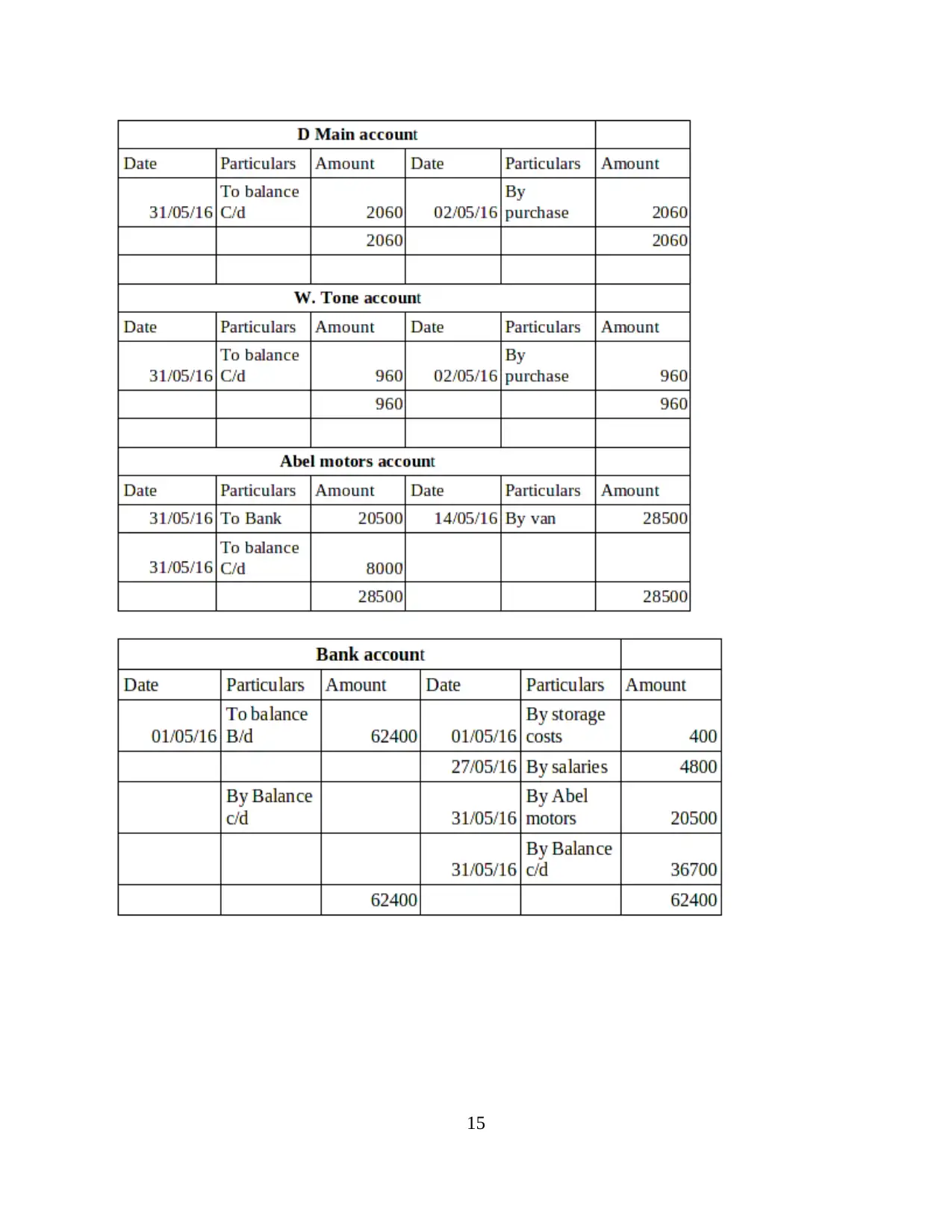

(i) The book of primary entry.................................................................................................5

(ii) Complete double entry system.........................................................................................6

..............................................................................................................................................11

..............................................................................................................................................12

..............................................................................................................................................13

..............................................................................................................................................15

..............................................................................................................................................17

..............................................................................................................................................17

(iii) Close accounts with drawing the trail balance..............................................................17

CLIENT 2......................................................................................................................................18

(a) Statement of profit and loss for Peter Pipe ....................................................................18

(b) Statement of financial position for Peter Pipe................................................................20

CLIENT 3......................................................................................................................................21

(a) Prepare the statement of profit and loss of Rain tree Ltd................................................21

(b) The statement of financial position ................................................................................21

(c) Explains the accounting concept of consistency and prudence......................................22

(d) Describes the purposes of depreciation in formulates accounting statements................23

CLIENT 4......................................................................................................................................24

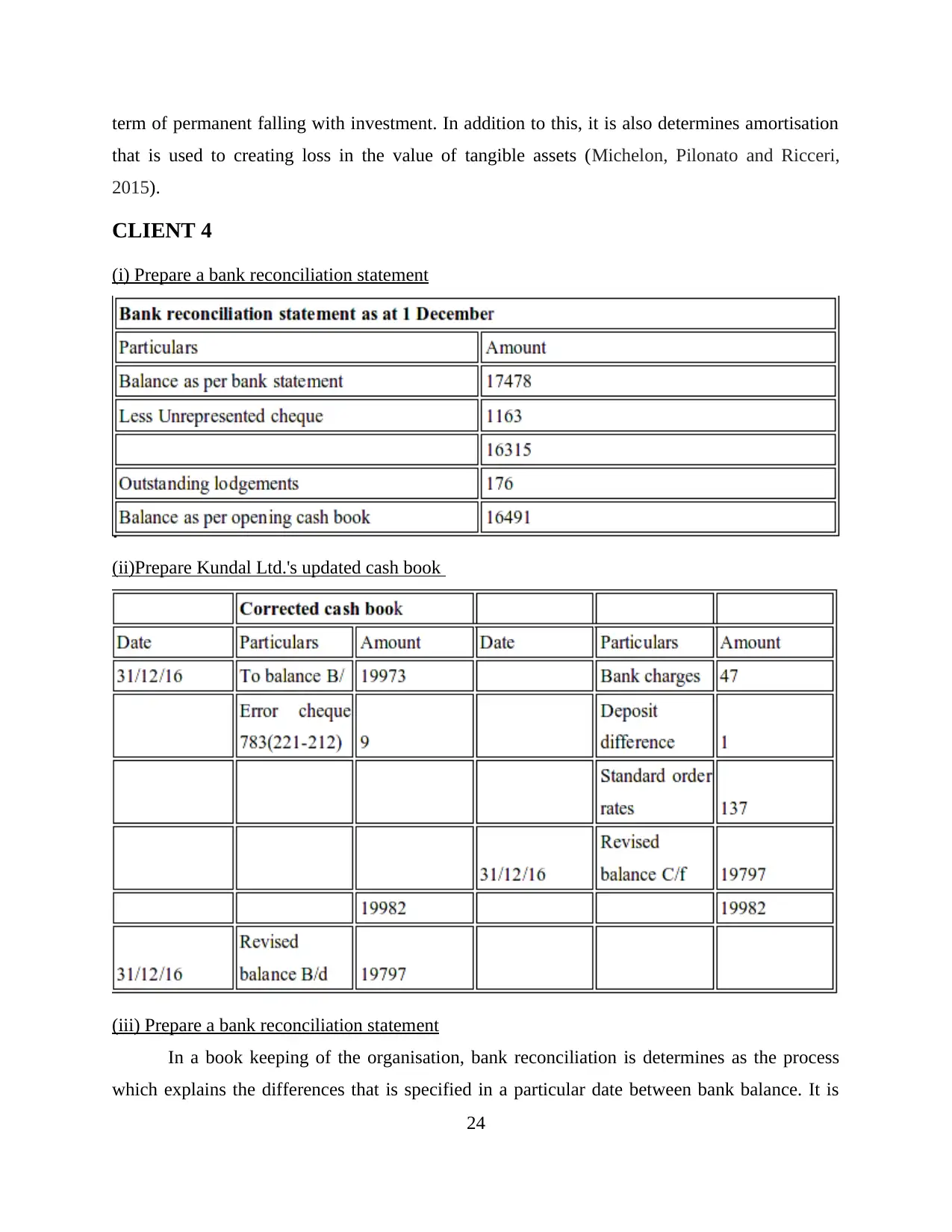

(i) Prepare a bank reconciliation statement..........................................................................24

(ii)Prepare Kundal Ltd.'s updated cash book .......................................................................24

(iii) Prepare a bank reconciliation statement........................................................................24

CLIENT 5......................................................................................................................................26

(a) Prepare and balance in books of Henderson...................................................................26

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a) Meaning of financial accounting, regulation, rules and principles with effective concept

relating to consistency and material disclosure......................................................................1

(B) PORTFOLIO FOR A CLIENT.................................................................................................5

CLIENT 1........................................................................................................................................5

(i) The book of primary entry.................................................................................................5

(ii) Complete double entry system.........................................................................................6

..............................................................................................................................................11

..............................................................................................................................................12

..............................................................................................................................................13

..............................................................................................................................................15

..............................................................................................................................................17

..............................................................................................................................................17

(iii) Close accounts with drawing the trail balance..............................................................17

CLIENT 2......................................................................................................................................18

(a) Statement of profit and loss for Peter Pipe ....................................................................18

(b) Statement of financial position for Peter Pipe................................................................20

CLIENT 3......................................................................................................................................21

(a) Prepare the statement of profit and loss of Rain tree Ltd................................................21

(b) The statement of financial position ................................................................................21

(c) Explains the accounting concept of consistency and prudence......................................22

(d) Describes the purposes of depreciation in formulates accounting statements................23

CLIENT 4......................................................................................................................................24

(i) Prepare a bank reconciliation statement..........................................................................24

(ii)Prepare Kundal Ltd.'s updated cash book .......................................................................24

(iii) Prepare a bank reconciliation statement........................................................................24

CLIENT 5......................................................................................................................................26

(a) Prepare and balance in books of Henderson...................................................................26

(i) Sales ledger control account ...........................................................................................26

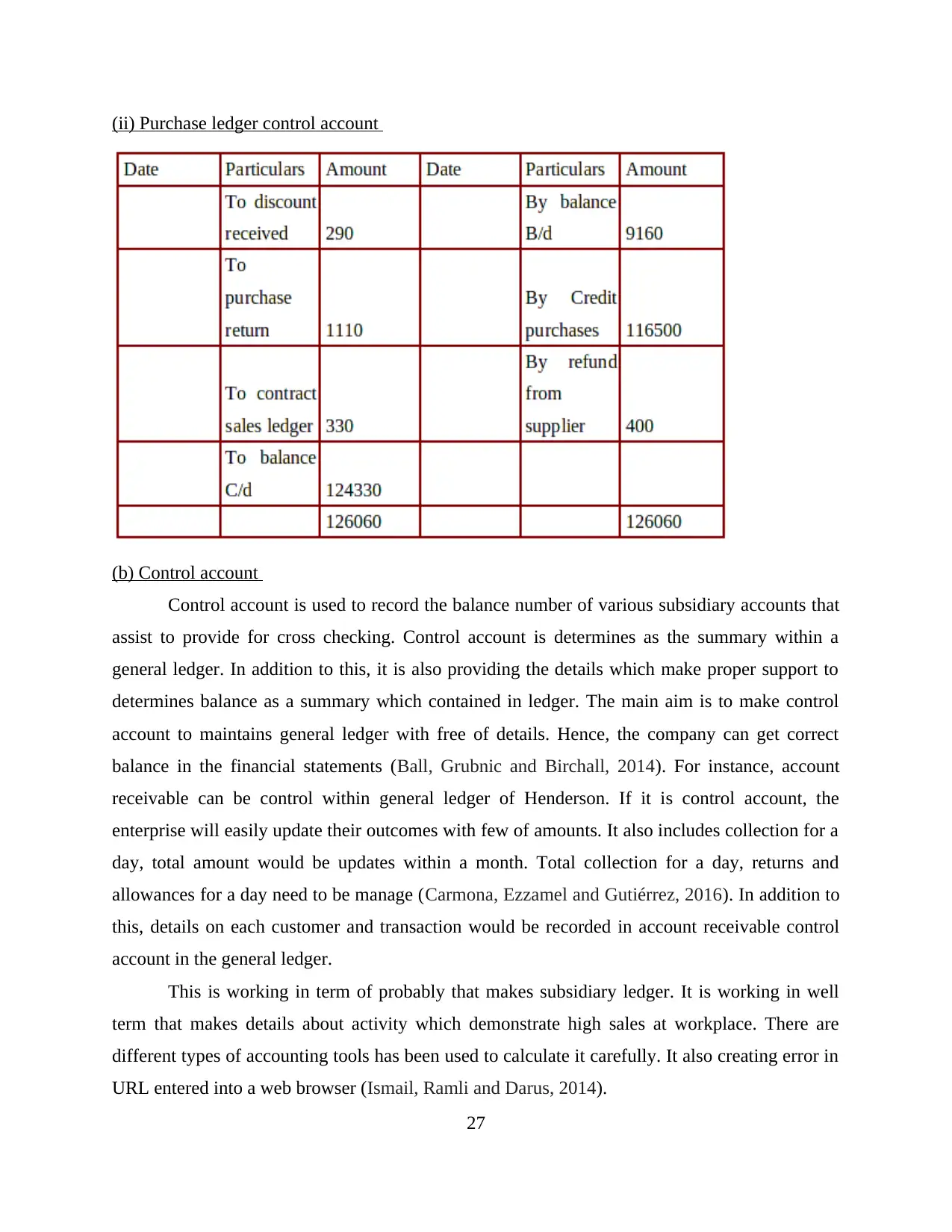

(ii) Purchase ledger control account ....................................................................................27

(b) Control account ..............................................................................................................27

CLIENT 6......................................................................................................................................28

(a) Describes suspense account and main features of it.......................................................28

(b) Trial balance ..................................................................................................................29

(c) Journals entries with corrections.....................................................................................30

(d) Differentiate between suspense account and clearing account.......................................30

CONCLUSION..............................................................................................................................33

REFERENCES..............................................................................................................................34

(ii) Purchase ledger control account ....................................................................................27

(b) Control account ..............................................................................................................27

CLIENT 6......................................................................................................................................28

(a) Describes suspense account and main features of it.......................................................28

(b) Trial balance ..................................................................................................................29

(c) Journals entries with corrections.....................................................................................30

(d) Differentiate between suspense account and clearing account.......................................30

CONCLUSION..............................................................................................................................33

REFERENCES..............................................................................................................................34

INTRODUCTION

In recent years, role of accounting is continuously increases which also enhance market

complexity. It includes generally accepted accounting principles which is common set of rules

and standards which indicates financial statements (Carmona, Ezzamel and Gutiérrez, 2016).

There are different types of companies exist in market which require financial statements as per

guidance of GAAP. Main aim to considering rules and regulation of GAAP to create standard

and uniform results that are based on financial outcomes and performances. With applying in

non profit organisation, transparency can be accomplish in easy way. It covers key areas such as

recognition, measurement, presentation and disclosure. These elements assist to minimize risk

from financial erroneous with reporting that assist to check and making safeguards in a place

(Michelon, Pilonato and Ricceri, 2015).

In this context, report is based on different clients of accounting firm who requires

prepares journal, ledger, profit and loss account, balance sheet and many other financial

statements. In addition to this, it is also induces rectification of errors which considers

rectification for accomplish transactions. With the help of following transactions, business can

revealed their conclusion towards decision and outcomes (Engel, 2016). Moreover, it stresses on

find out mistakes which occur in the enterprise to do transactions. In this aspect, different types

of objectives can be achieve by the company for ascertain financial statements at workplace.

TASK 1

(a) Meaning of financial accounting, regulation, rules and principles with effective concept

relating to consistency and material disclosure

Meaning of financial accounting: Financial accounting is special branch which keep all records

of financial transactions. It assists to using standardized principles and guidelines that are

recorded and summarized within financial report and statements. For example, income

statements and balance sheet (Rinaldi, Unerman and Tilt, 2014). In addition to this, financial

accounting is a crucial element which helpful to make routine schedule for solve company

issues. Statements considering externally because it can be given outside the firm such charted

accountant, etc.

Regulation that are related to financial accounting: In this aspect, principles are derived that

prepare for matching the concept. In a report of financial statements such as audit, compilation

1

In recent years, role of accounting is continuously increases which also enhance market

complexity. It includes generally accepted accounting principles which is common set of rules

and standards which indicates financial statements (Carmona, Ezzamel and Gutiérrez, 2016).

There are different types of companies exist in market which require financial statements as per

guidance of GAAP. Main aim to considering rules and regulation of GAAP to create standard

and uniform results that are based on financial outcomes and performances. With applying in

non profit organisation, transparency can be accomplish in easy way. It covers key areas such as

recognition, measurement, presentation and disclosure. These elements assist to minimize risk

from financial erroneous with reporting that assist to check and making safeguards in a place

(Michelon, Pilonato and Ricceri, 2015).

In this context, report is based on different clients of accounting firm who requires

prepares journal, ledger, profit and loss account, balance sheet and many other financial

statements. In addition to this, it is also induces rectification of errors which considers

rectification for accomplish transactions. With the help of following transactions, business can

revealed their conclusion towards decision and outcomes (Engel, 2016). Moreover, it stresses on

find out mistakes which occur in the enterprise to do transactions. In this aspect, different types

of objectives can be achieve by the company for ascertain financial statements at workplace.

TASK 1

(a) Meaning of financial accounting, regulation, rules and principles with effective concept

relating to consistency and material disclosure

Meaning of financial accounting: Financial accounting is special branch which keep all records

of financial transactions. It assists to using standardized principles and guidelines that are

recorded and summarized within financial report and statements. For example, income

statements and balance sheet (Rinaldi, Unerman and Tilt, 2014). In addition to this, financial

accounting is a crucial element which helpful to make routine schedule for solve company

issues. Statements considering externally because it can be given outside the firm such charted

accountant, etc.

Regulation that are related to financial accounting: In this aspect, principles are derived that

prepare for matching the concept. In a report of financial statements such as audit, compilation

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

and review, etc. (Spence and Rinaldi, 2014). must be demonstrate information that are related to

contained statements of GAAP. There are certain regulation frames that are related to financial

accounting. They are as follows:

Principle of regularity: This principle is determines conformity with ensure rules and

laws.

Principle of consistency: It is states that what businesses fixed for treatment for

accounting, it regularly runs in same way every year (Colasse and Durand, 2014).

Principles of non-compensation: In this aspect, business should follows all details of

the financial information which seek to compensate a debt with an asset, revenue and

expenses, etc.

Principle of sincerity: This accounting principle is based on accounting unit which

reflect to good faith as per reality of financial status of company.

Principles of permanence of methods: This principle has aim to allowing and

comparing information that are related to finance part and also published by the

enterprise (Ahmad and Leftesi, 2014).

Principle of prudence: This principle has aim to show reality to make things look good

than they exist. In addition to this, revenue need to be recorded only when it covered in

certain provision with including for an expense.

Principle of continuity: In order to stating financial information, one person need to be

assume that enterprise cannot be interrupted. This principle ensures that assets have not

been accounted as disposable value which continually accounted which accepted on

historical value. For example, deprecation is considering as going concern (Miller and

Shawver, 2016).

Principle of periodicity: In respect to states financial information, accounting entry

allocating within a given period. It could be split as per covering various periods. In

addition to this, revenue also need to be split in the entire time span which not counted

for entire date of transaction.

Principle of full disclosure/materiality: With the help of information and value, it has

been pertaining that financial position in organisation need to be disclosed as records (de

Villiers, Rinaldi and Unerman, 2014).

2

contained statements of GAAP. There are certain regulation frames that are related to financial

accounting. They are as follows:

Principle of regularity: This principle is determines conformity with ensure rules and

laws.

Principle of consistency: It is states that what businesses fixed for treatment for

accounting, it regularly runs in same way every year (Colasse and Durand, 2014).

Principles of non-compensation: In this aspect, business should follows all details of

the financial information which seek to compensate a debt with an asset, revenue and

expenses, etc.

Principle of sincerity: This accounting principle is based on accounting unit which

reflect to good faith as per reality of financial status of company.

Principles of permanence of methods: This principle has aim to allowing and

comparing information that are related to finance part and also published by the

enterprise (Ahmad and Leftesi, 2014).

Principle of prudence: This principle has aim to show reality to make things look good

than they exist. In addition to this, revenue need to be recorded only when it covered in

certain provision with including for an expense.

Principle of continuity: In order to stating financial information, one person need to be

assume that enterprise cannot be interrupted. This principle ensures that assets have not

been accounted as disposable value which continually accounted which accepted on

historical value. For example, deprecation is considering as going concern (Miller and

Shawver, 2016).

Principle of periodicity: In respect to states financial information, accounting entry

allocating within a given period. It could be split as per covering various periods. In

addition to this, revenue also need to be split in the entire time span which not counted

for entire date of transaction.

Principle of full disclosure/materiality: With the help of information and value, it has

been pertaining that financial position in organisation need to be disclosed as records (de

Villiers, Rinaldi and Unerman, 2014).

2

Principle of utmost good faith: All essential information that are related to the

enterprise also disclosed for insurer before taking policy.

Accounting rules and principles: Accounting principles are accepted in basically three

concepts such as basic accounting principles and guidelines, detailed rules and standards and

accepted rules by the industry (Vogel, 2014). Below are such accounting principles and

guidelines which is frames in GAAP: Economic entity assumption: This accounting principle keeps transaction of all

businesses ahead from owner of enterprise. The both are different entities which

considered in the market. Monetary unit assumption: Economic activity within the business is measuring in pound

and transaction are expressed in pound only (Pijper, 2016). The period assumption: This accounting principle determines complex activities in short

and distinctive term within a specific time interval. Cost principle: Cost is refers as amount which spent as cash or equivalent of it. In

addition to this, it demonstrates whether purchase has been happened last year of many

years ago (Ismail, Ramli and Darus, 2014). Full disclosure principle: In this principle, certain information need to be keep safe that

is important for an investor or lender. These types of informations need to be disclosed in

a statement in numerous financial attachments. Going concern principle: This accounting principle determines that the enterprise will

continue exist for long time that carry objectives and commitments that not liquidate in

foreseeable future (Dillard and Vinnari, 2017). Matching principle: This accounting principle is essential for the enterprises to using

accrual system. In this aspect, expenses are need to be match with revenue. For instance,

commission expense need to be reported within a period of sales is made. Wages of

employee is also reported as the expenses (Carmona, Ezzamel and Gutiérrez, 2016). Revenue recognition principles: As per the accrual basis accounting, revenue has been

recognized has been sold and services also performed with money that actually received. Materiality: This accounting principle is frame basic guidelines which need to be

followed by accountant. Professional judgement is also needed to demonstrate significant

amount (Laughlin, 2014).

3

enterprise also disclosed for insurer before taking policy.

Accounting rules and principles: Accounting principles are accepted in basically three

concepts such as basic accounting principles and guidelines, detailed rules and standards and

accepted rules by the industry (Vogel, 2014). Below are such accounting principles and

guidelines which is frames in GAAP: Economic entity assumption: This accounting principle keeps transaction of all

businesses ahead from owner of enterprise. The both are different entities which

considered in the market. Monetary unit assumption: Economic activity within the business is measuring in pound

and transaction are expressed in pound only (Pijper, 2016). The period assumption: This accounting principle determines complex activities in short

and distinctive term within a specific time interval. Cost principle: Cost is refers as amount which spent as cash or equivalent of it. In

addition to this, it demonstrates whether purchase has been happened last year of many

years ago (Ismail, Ramli and Darus, 2014). Full disclosure principle: In this principle, certain information need to be keep safe that

is important for an investor or lender. These types of informations need to be disclosed in

a statement in numerous financial attachments. Going concern principle: This accounting principle determines that the enterprise will

continue exist for long time that carry objectives and commitments that not liquidate in

foreseeable future (Dillard and Vinnari, 2017). Matching principle: This accounting principle is essential for the enterprises to using

accrual system. In this aspect, expenses are need to be match with revenue. For instance,

commission expense need to be reported within a period of sales is made. Wages of

employee is also reported as the expenses (Carmona, Ezzamel and Gutiérrez, 2016). Revenue recognition principles: As per the accrual basis accounting, revenue has been

recognized has been sold and services also performed with money that actually received. Materiality: This accounting principle is frame basic guidelines which need to be

followed by accountant. Professional judgement is also needed to demonstrate significant

amount (Laughlin, 2014).

3

Conservatism: With this regard, two acceptable alternatives are exists within the

enterprise. Conservatism directs accountant for choosing the best alternative that take less

amount.

Conventions and concept relating to consistency and material disclosure: The term

convention includes costumes and tradition that guide accountant to prepare statements. There

are certain important accounting conventions: Convention of disclosure: In order to disclosure of all significant information, it is the

important accounting conventions (Zadek, Evans and Pruzan, 2013). It implies on

accounts which need to be prepare in a way which includes material information that is

clearly disclosed to the reader. Convention of materiality: Convention of materiality is refers as relative importance for

an item. In this convention, those events and items are recorded that possess significance

and other will be ignored. This is because, there is not any way which determines

difference between material and immaterial events (Youssef, 2015). Convention of consistency: This convention determines accounting practices which need

to be remains not charged from one time to another. For instance, stock is valued either

cost or market price whichever is less. Mainly this is follows after one year (Carmona,

Ezzamel and Gutiérrez, 2016).

Convention of conservatism: This element is based on caution approach that making

safe. It will ensure that uncertainties and risk element inherent in organisation activities

that has to be given in proper aspect (Ahmad, 2013).

4

enterprise. Conservatism directs accountant for choosing the best alternative that take less

amount.

Conventions and concept relating to consistency and material disclosure: The term

convention includes costumes and tradition that guide accountant to prepare statements. There

are certain important accounting conventions: Convention of disclosure: In order to disclosure of all significant information, it is the

important accounting conventions (Zadek, Evans and Pruzan, 2013). It implies on

accounts which need to be prepare in a way which includes material information that is

clearly disclosed to the reader. Convention of materiality: Convention of materiality is refers as relative importance for

an item. In this convention, those events and items are recorded that possess significance

and other will be ignored. This is because, there is not any way which determines

difference between material and immaterial events (Youssef, 2015). Convention of consistency: This convention determines accounting practices which need

to be remains not charged from one time to another. For instance, stock is valued either

cost or market price whichever is less. Mainly this is follows after one year (Carmona,

Ezzamel and Gutiérrez, 2016).

Convention of conservatism: This element is based on caution approach that making

safe. It will ensure that uncertainties and risk element inherent in organisation activities

that has to be given in proper aspect (Ahmad, 2013).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

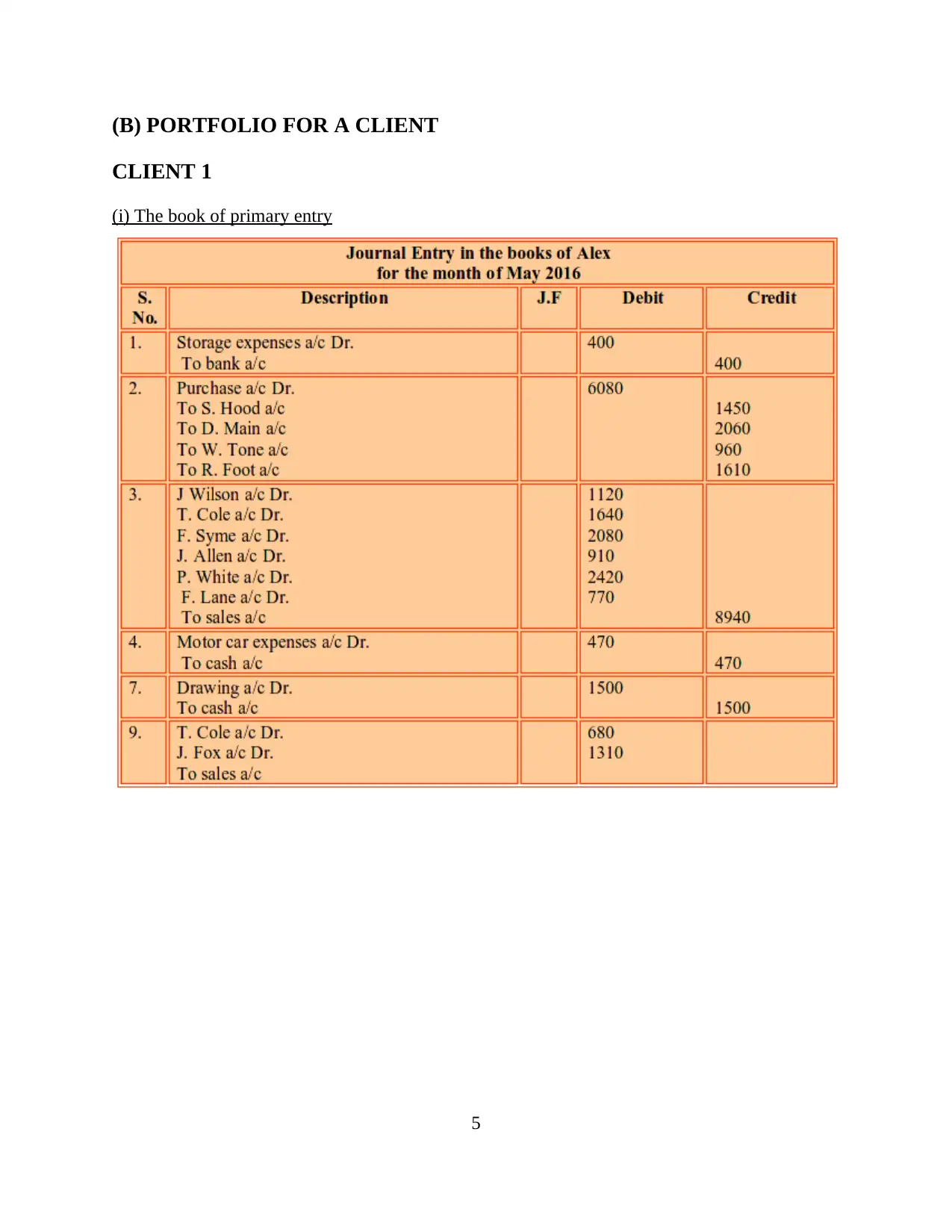

(B) PORTFOLIO FOR A CLIENT

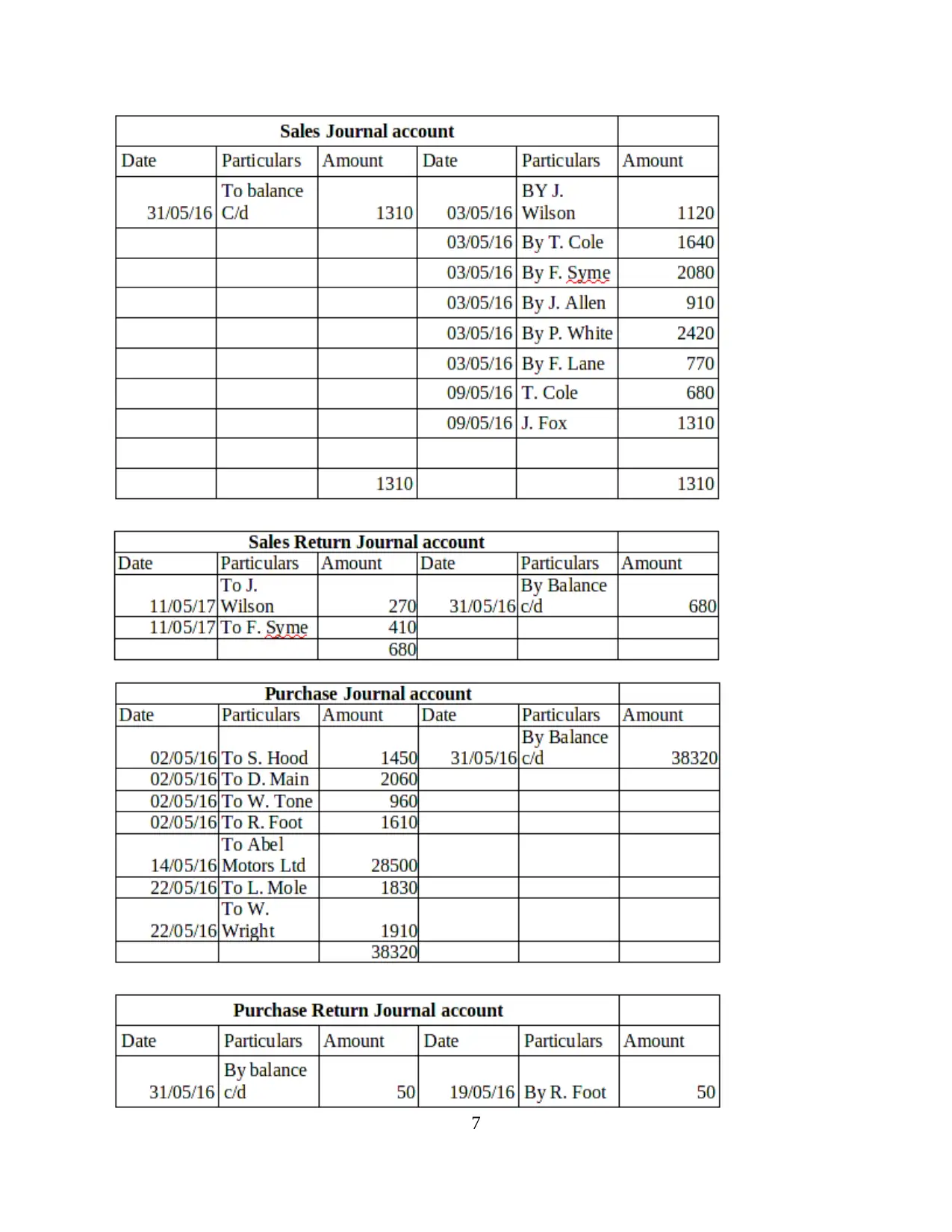

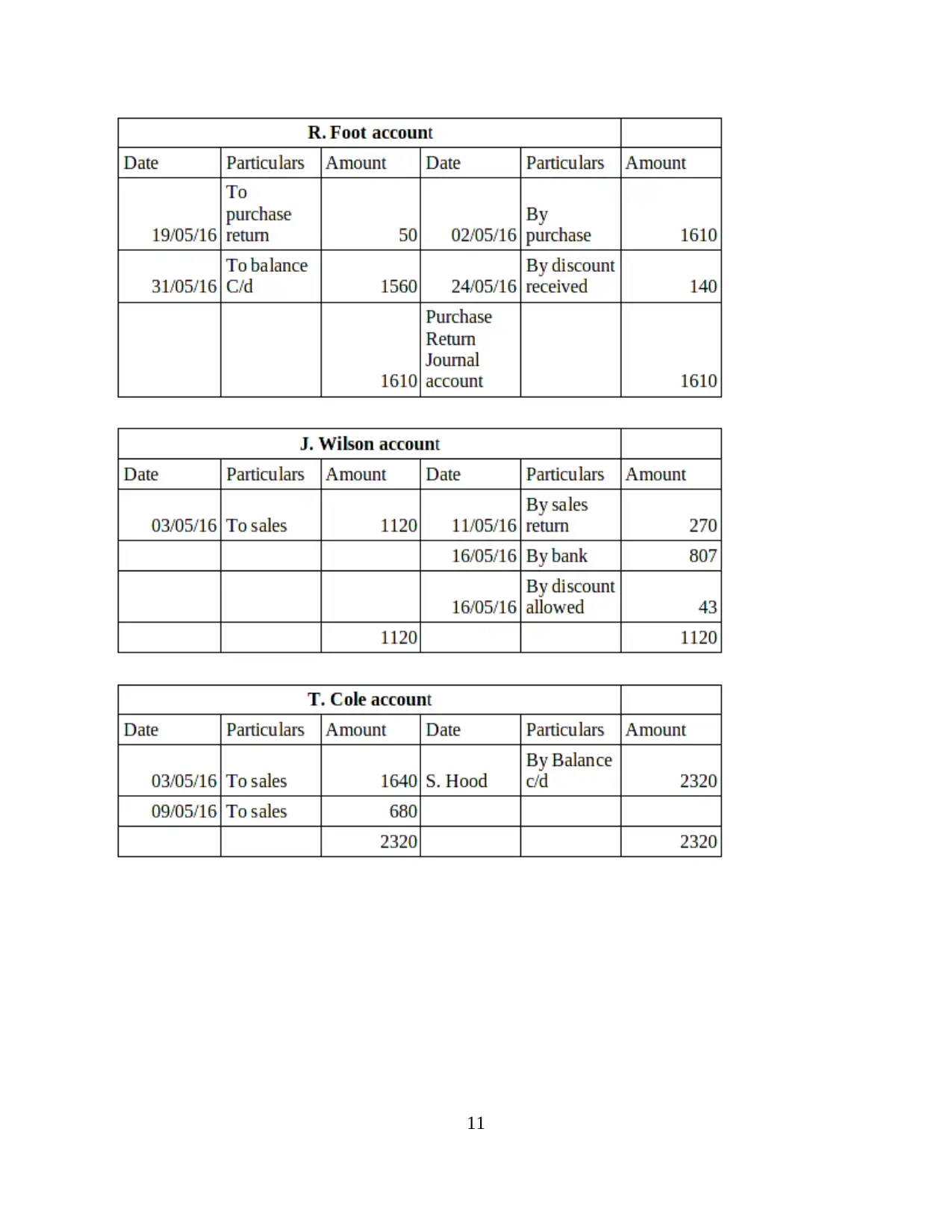

CLIENT 1

(i) The book of primary entry

5

CLIENT 1

(i) The book of primary entry

5

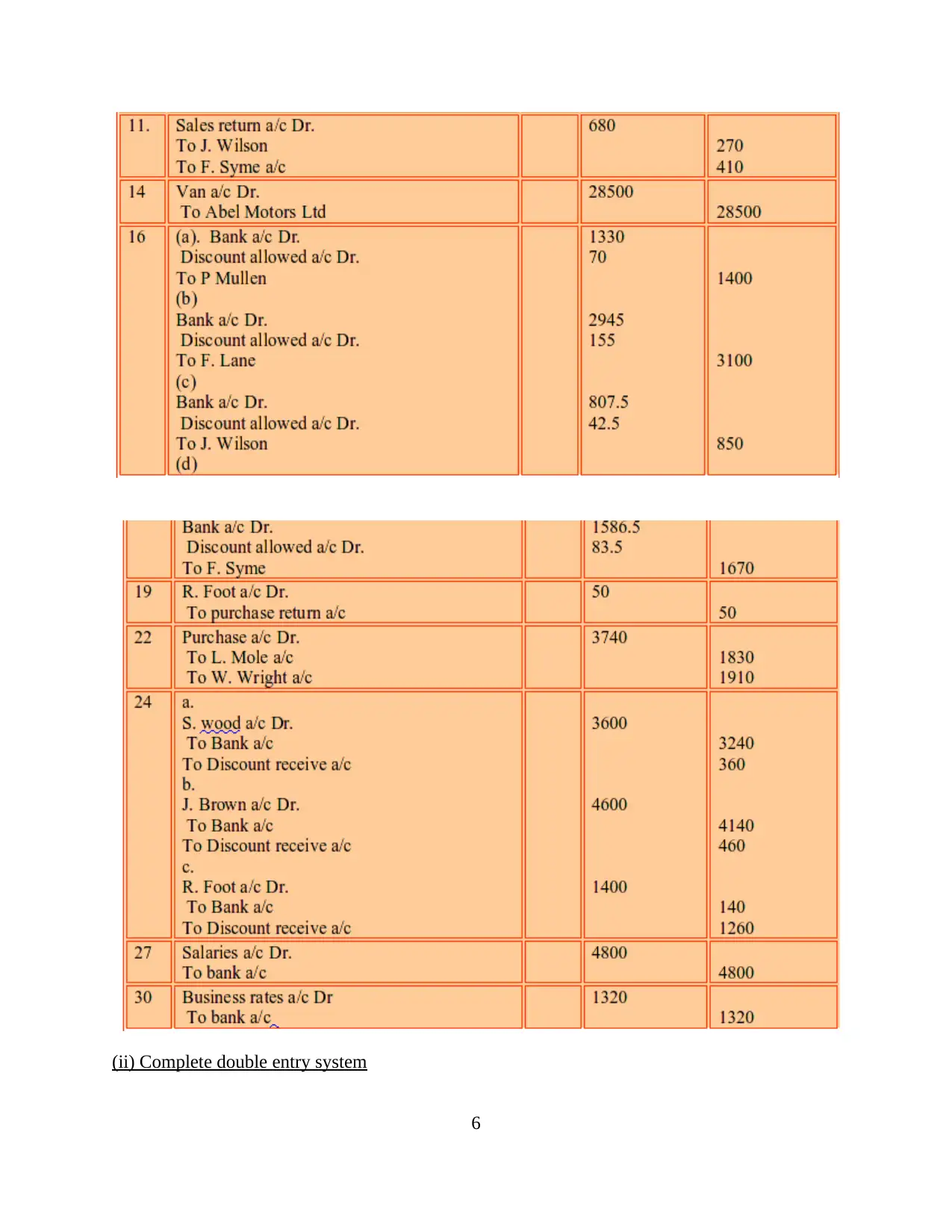

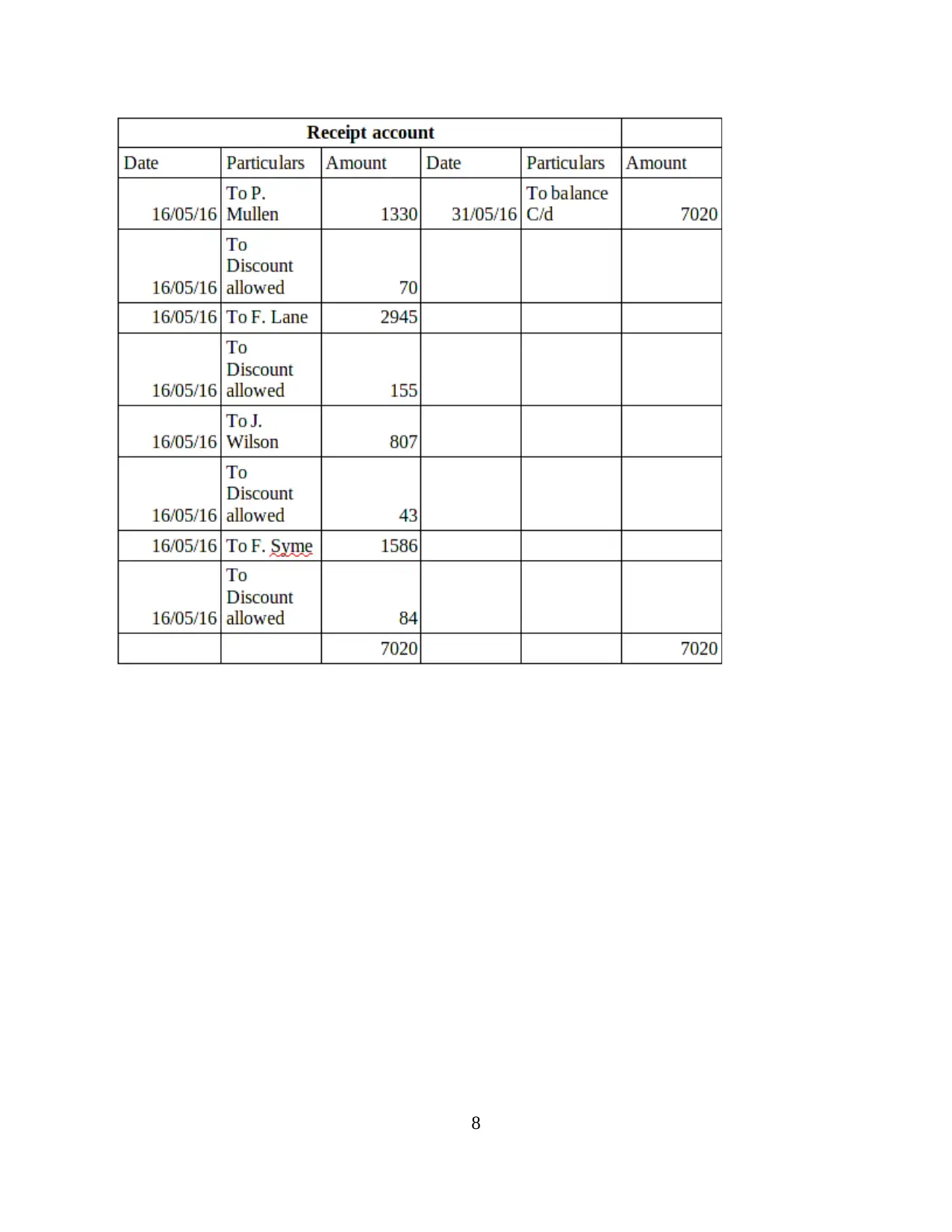

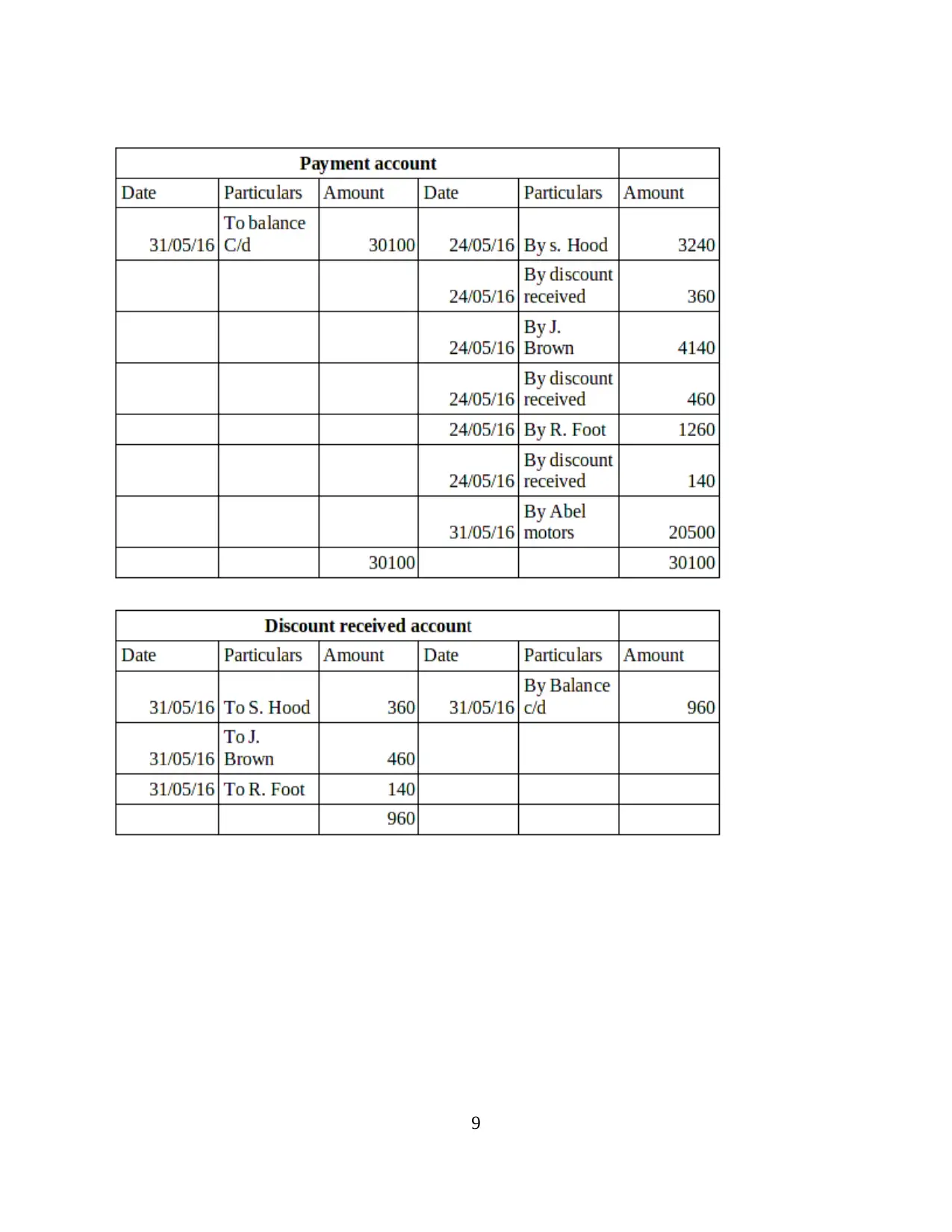

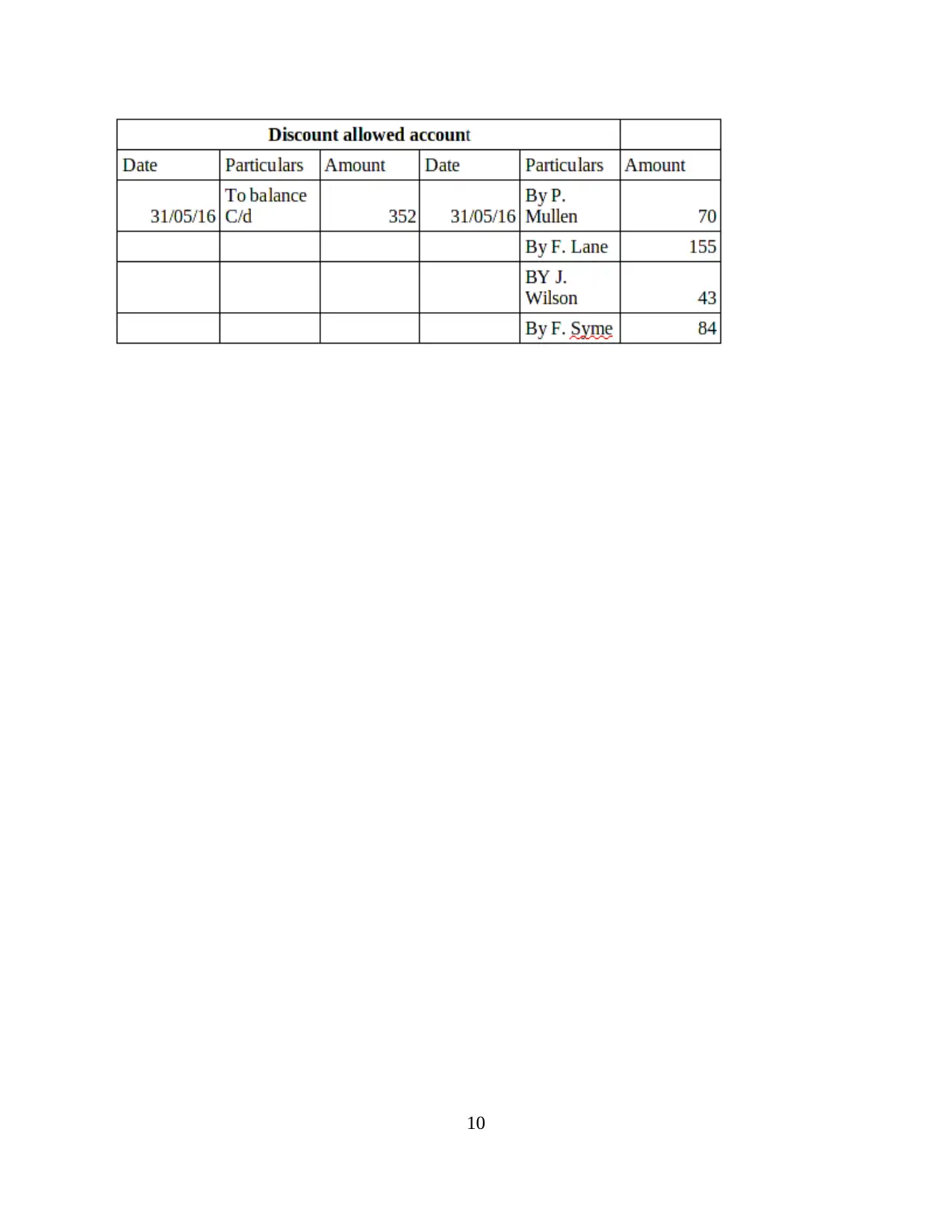

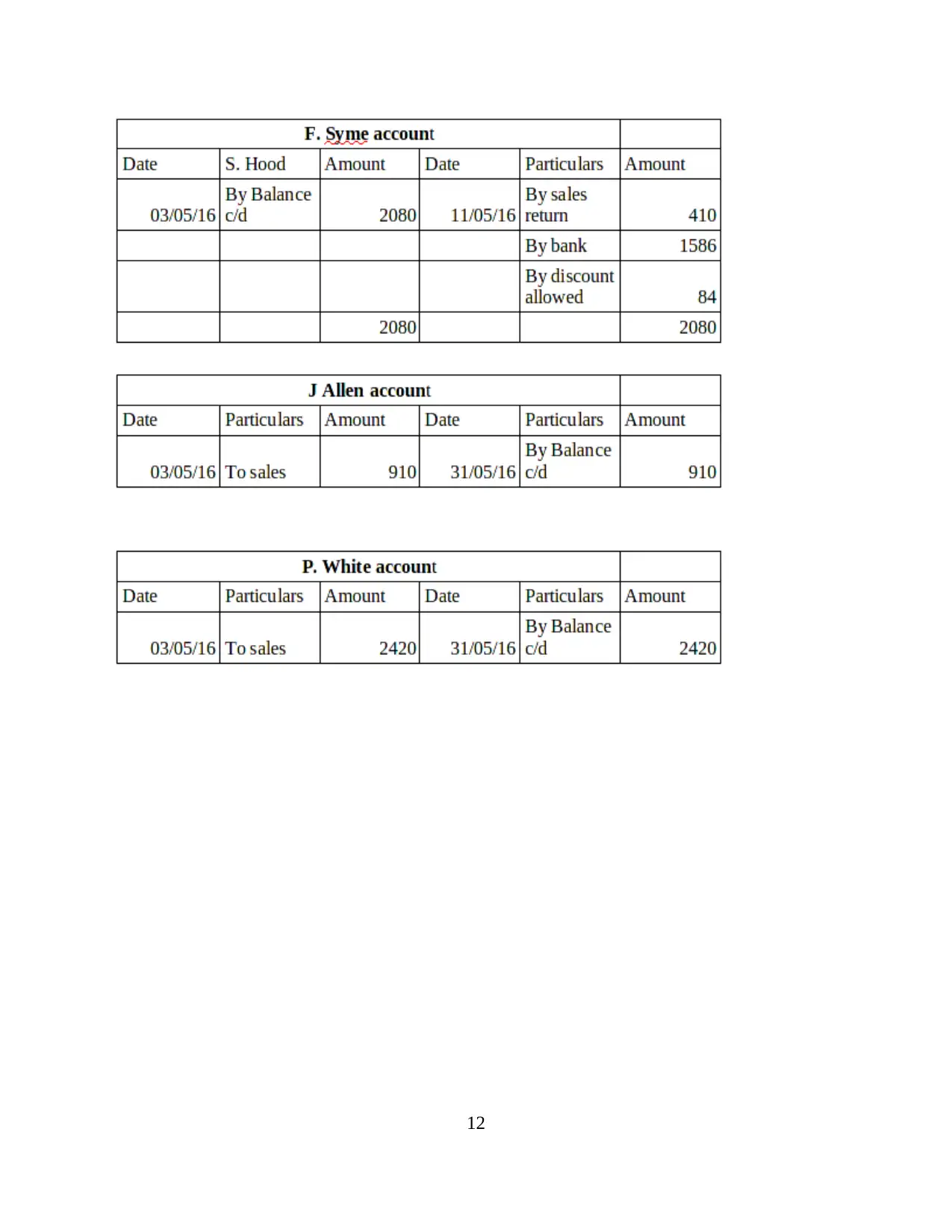

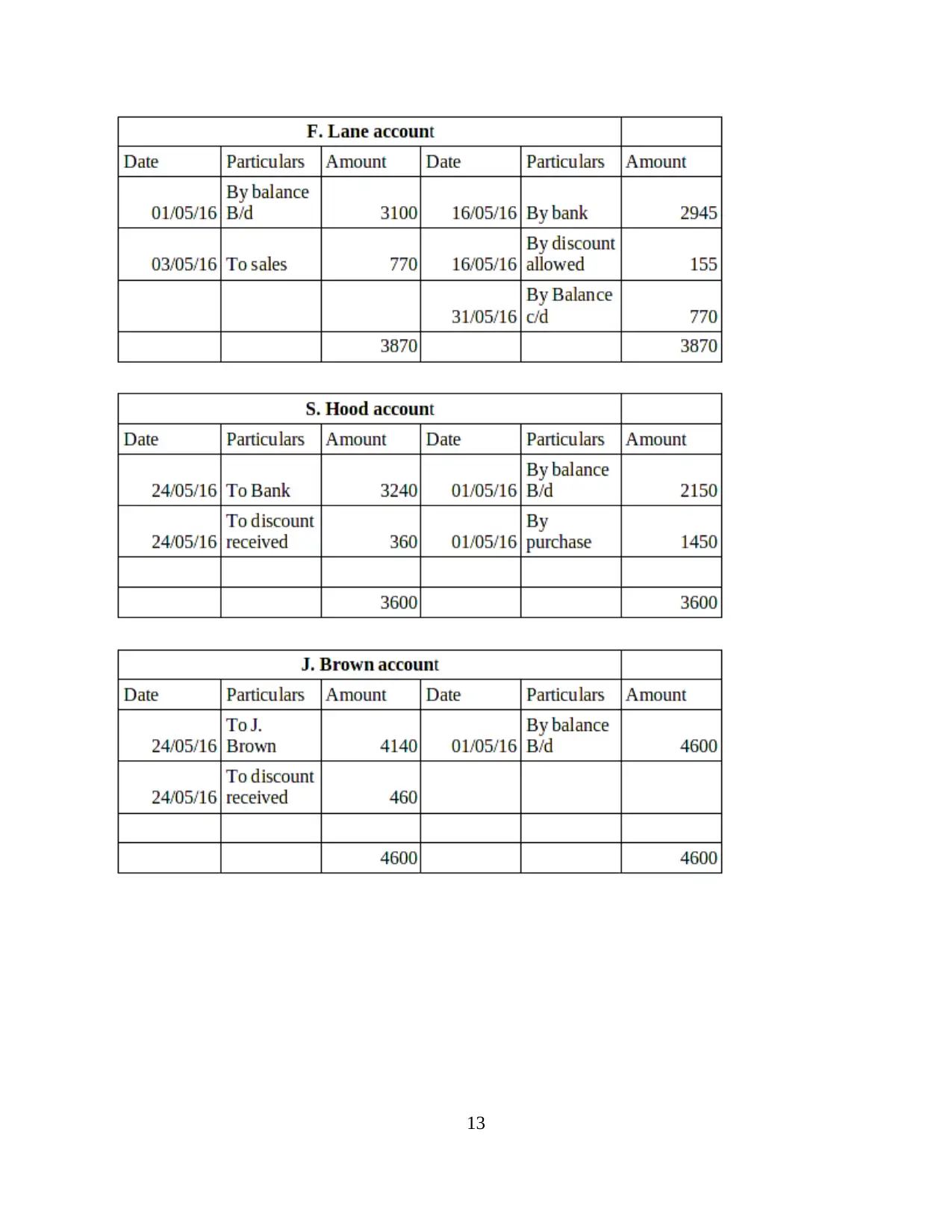

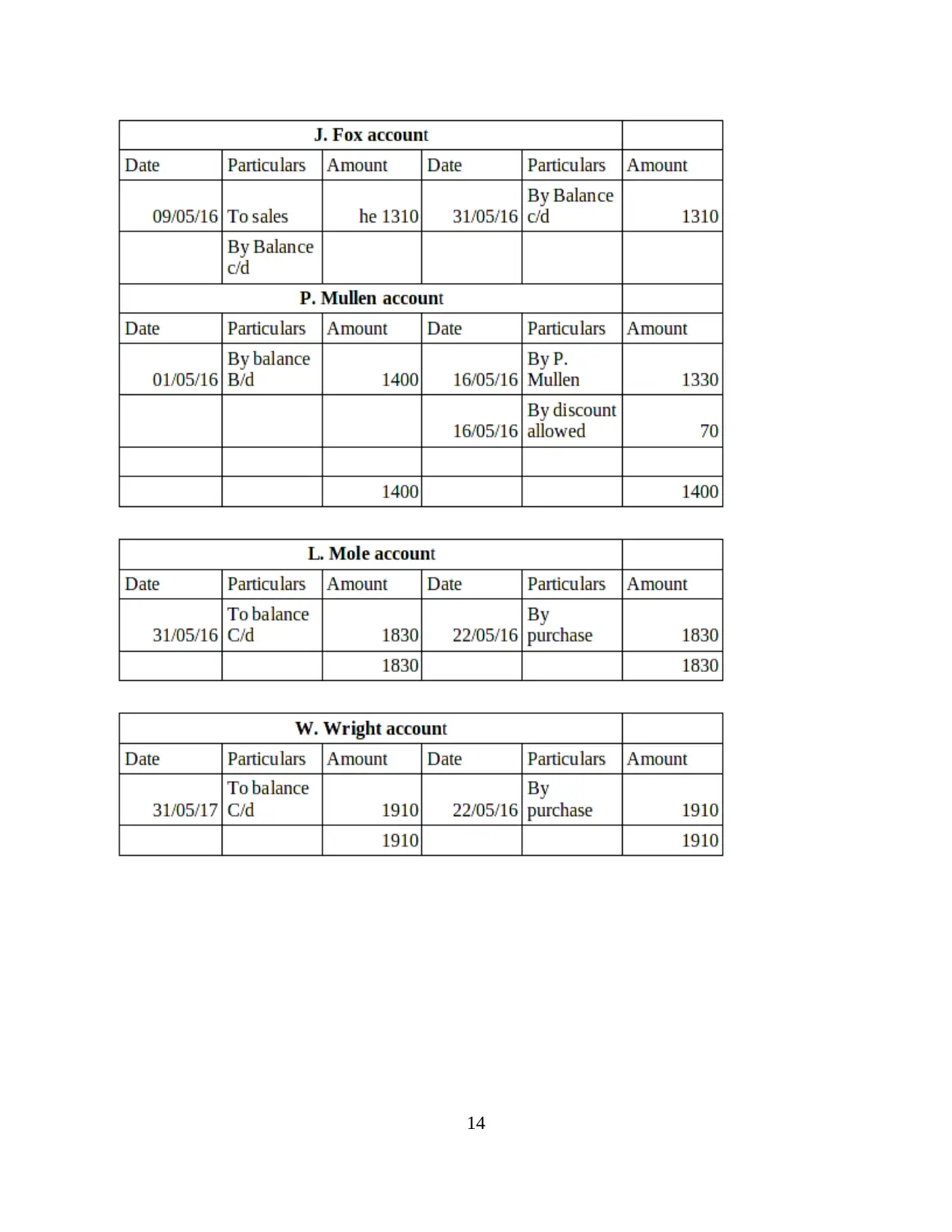

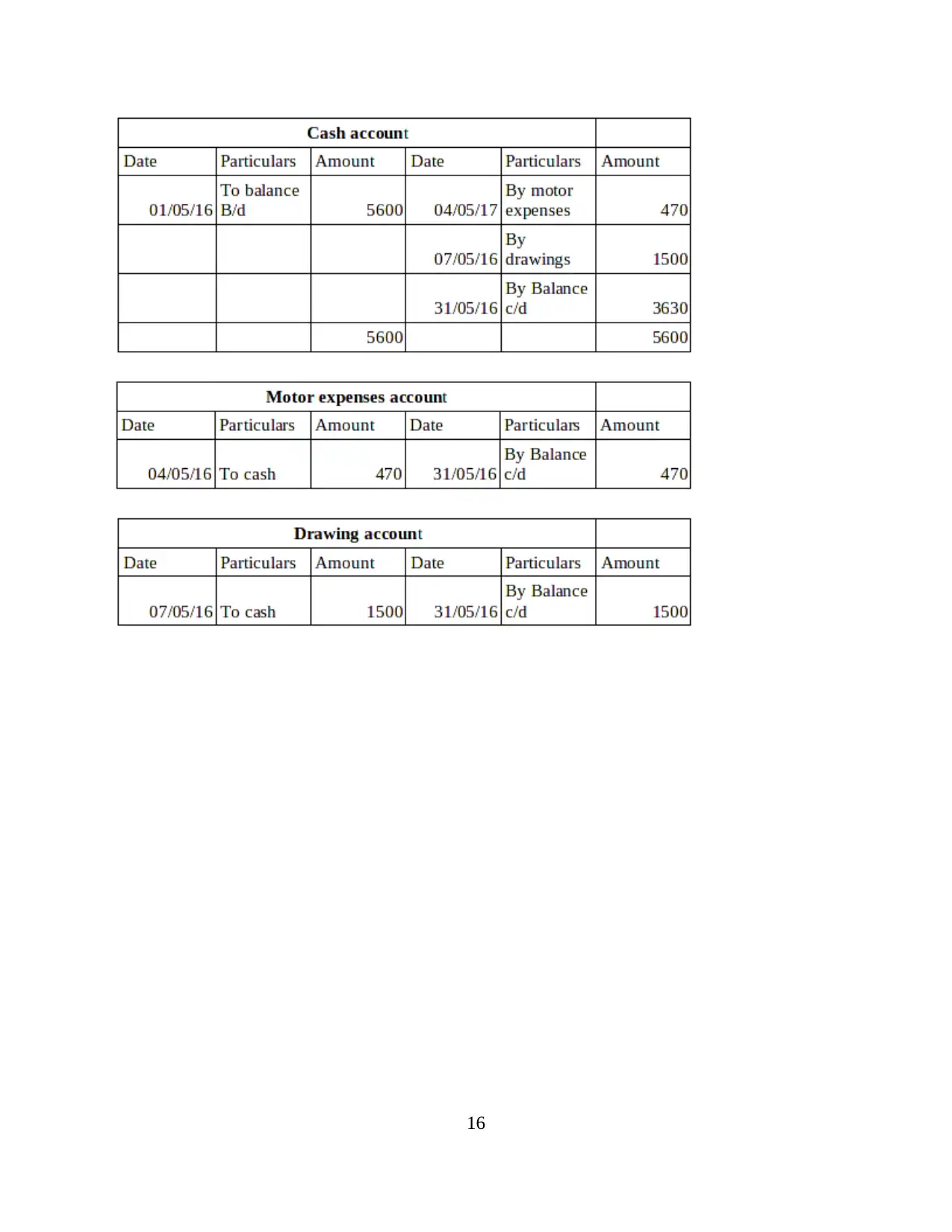

(ii) Complete double entry system

6

6

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

8

9

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

12

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

14

15

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

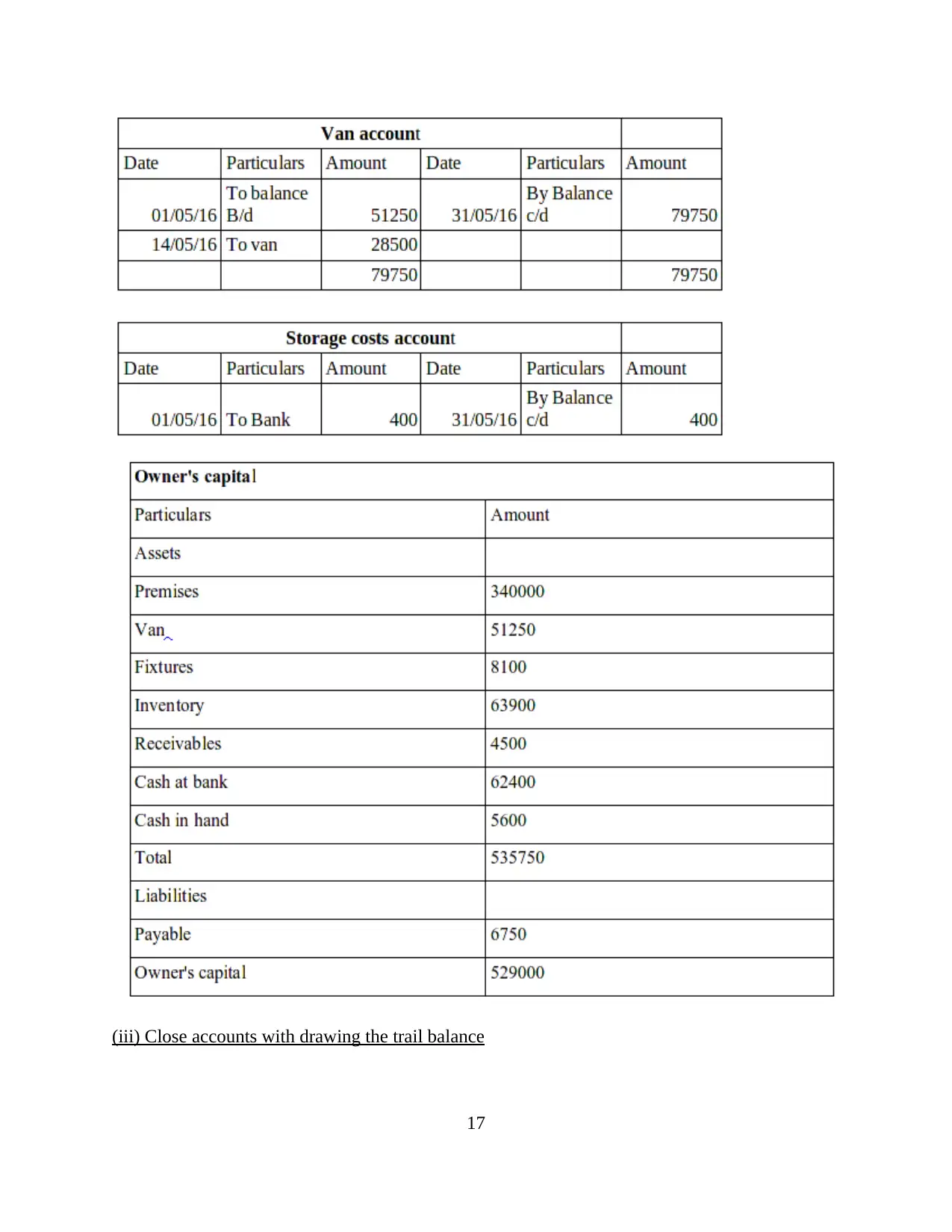

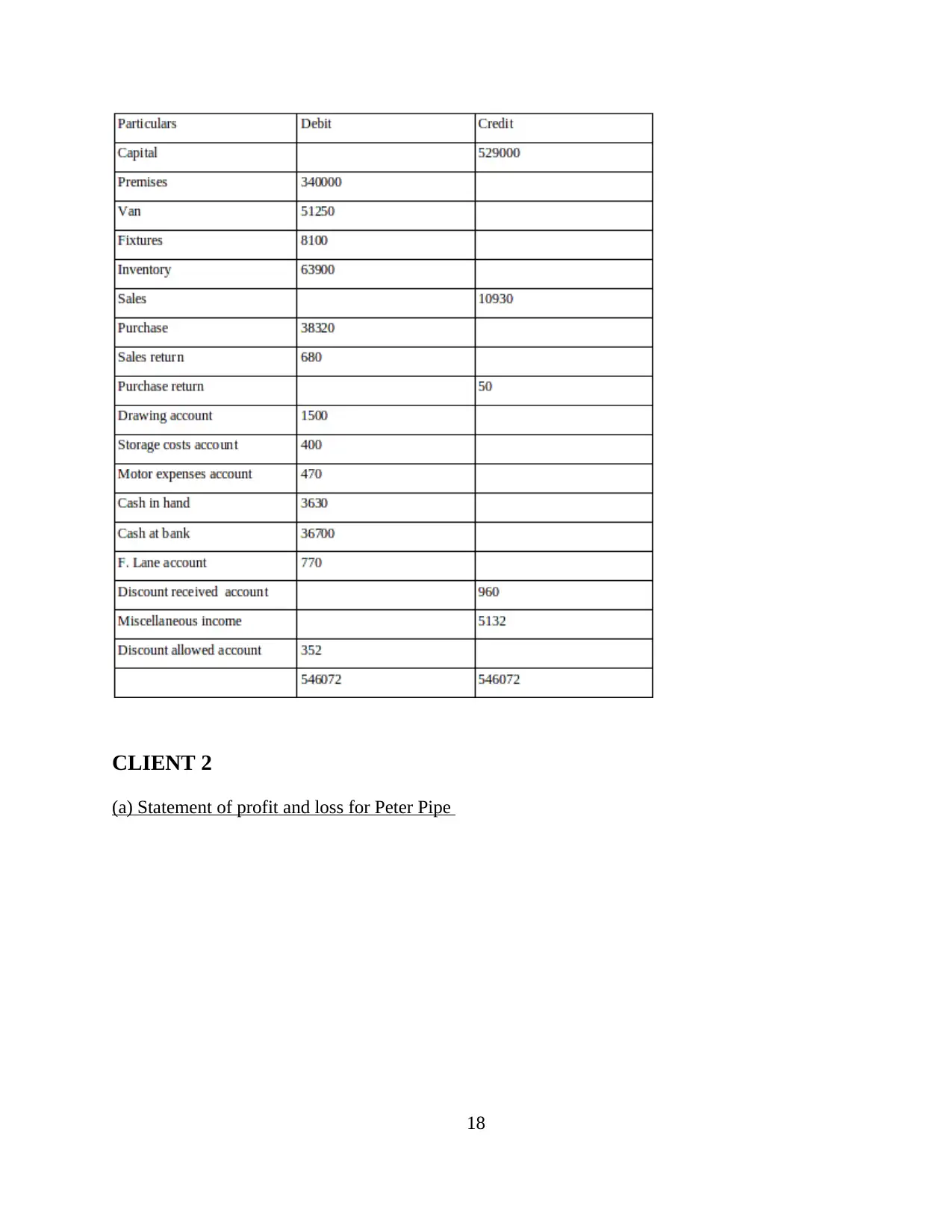

(iii) Close accounts with drawing the trail balance

17

17

CLIENT 2

(a) Statement of profit and loss for Peter Pipe

18

(a) Statement of profit and loss for Peter Pipe

18

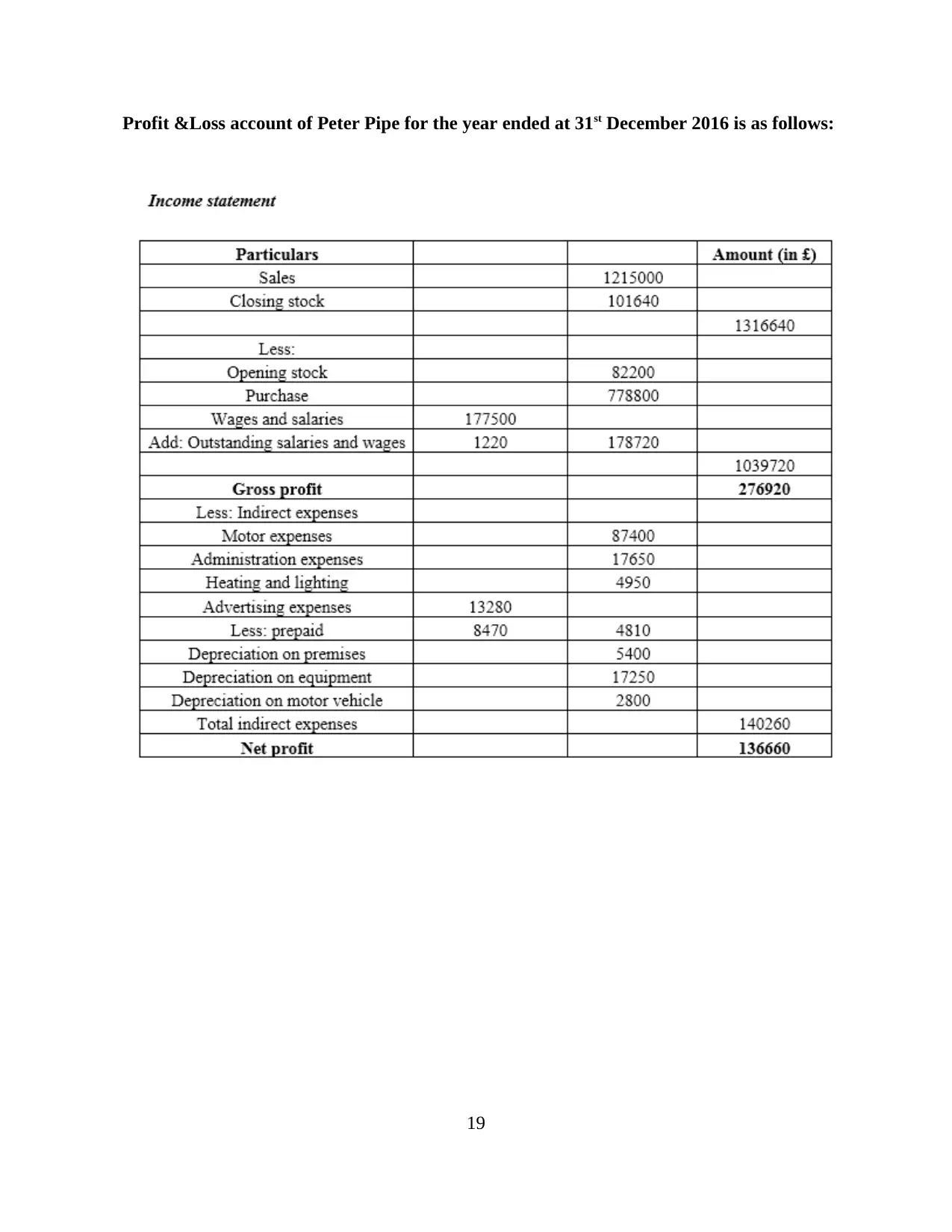

Profit &Loss account of Peter Pipe for the year ended at 31st December 2016 is as follows:

19

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

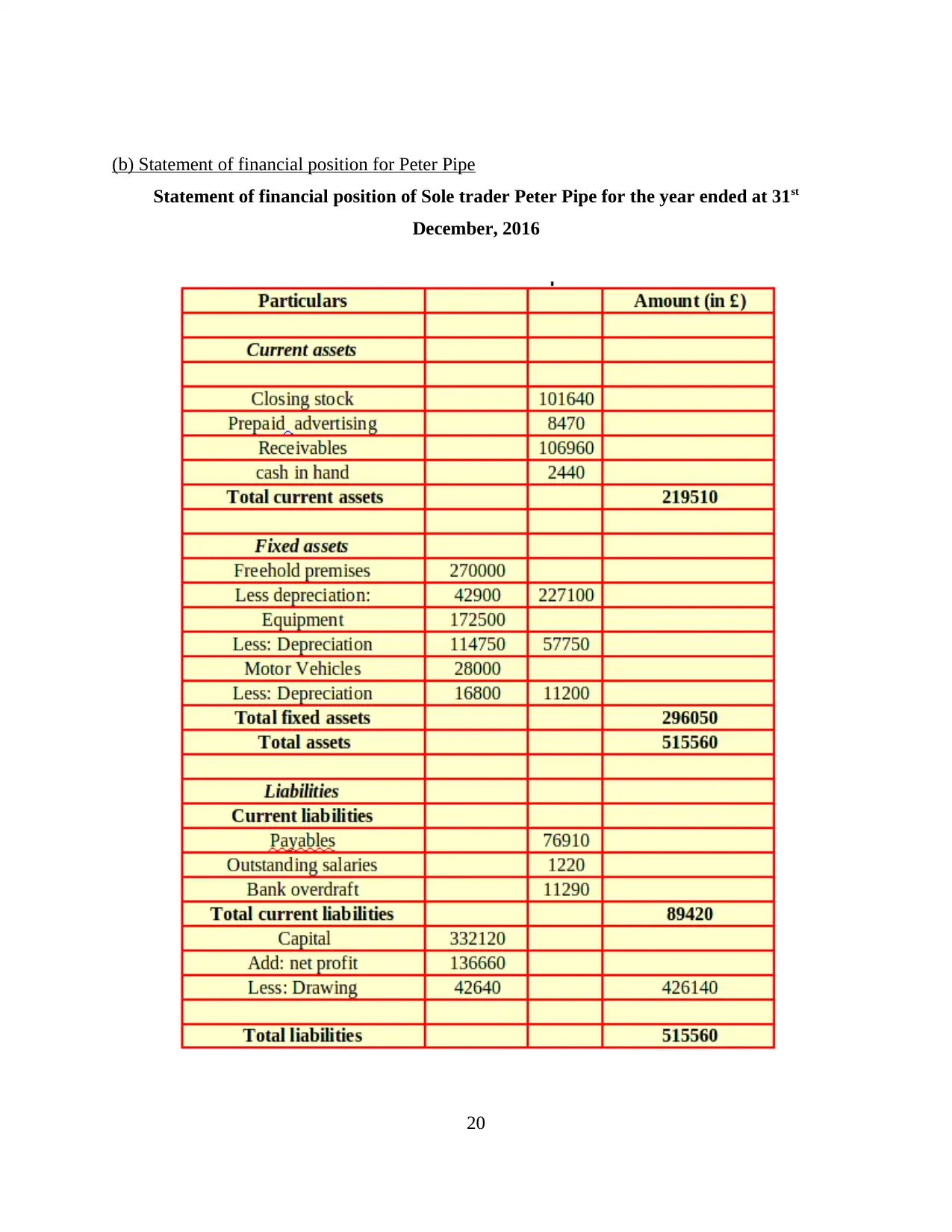

(b) Statement of financial position for Peter Pipe

Statement of financial position of Sole trader Peter Pipe for the year ended at 31st

December, 2016

20

Statement of financial position of Sole trader Peter Pipe for the year ended at 31st

December, 2016

20

CLIENT 3

(a) Prepare the statement of profit and loss of Rain tree Ltd.

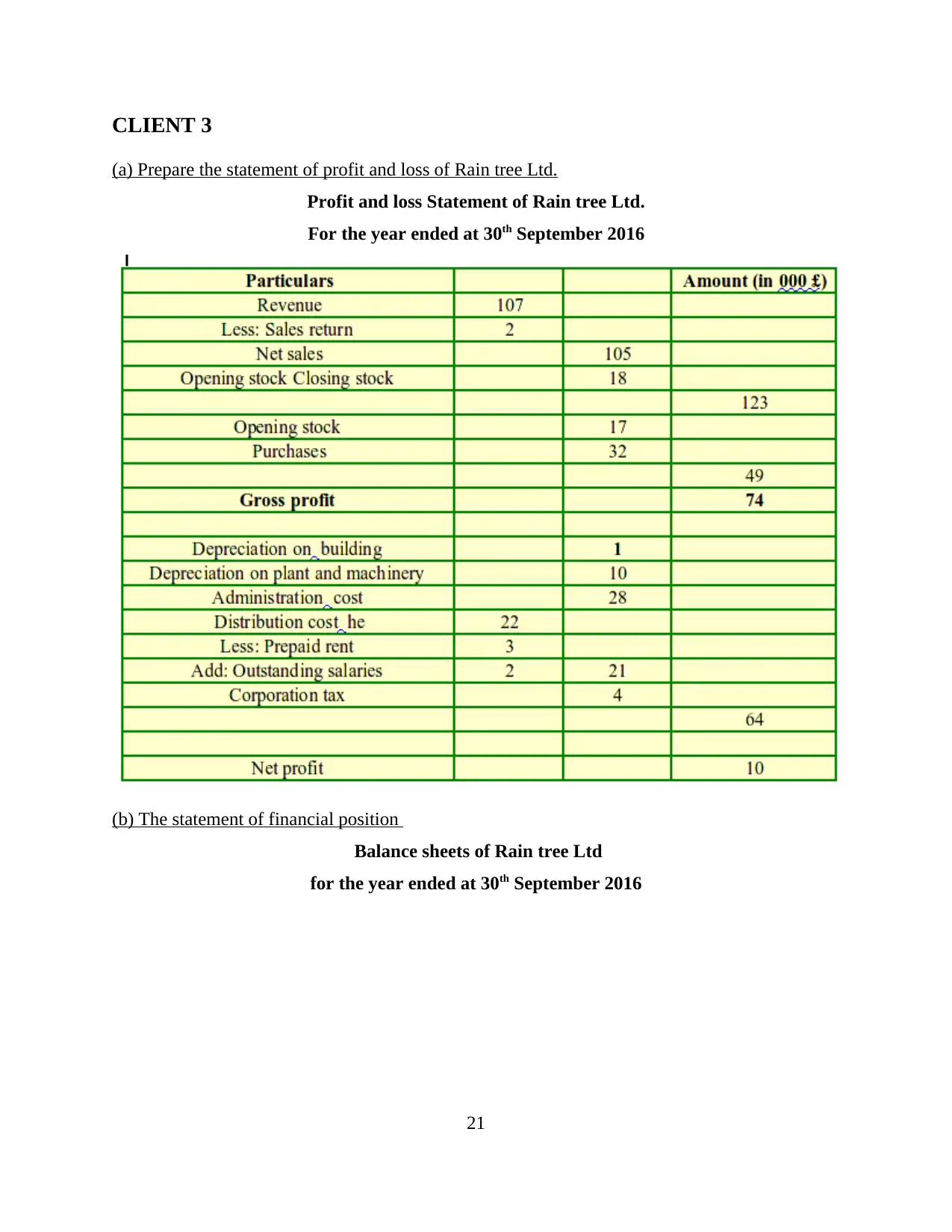

Profit and loss Statement of Rain tree Ltd.

For the year ended at 30th September 2016

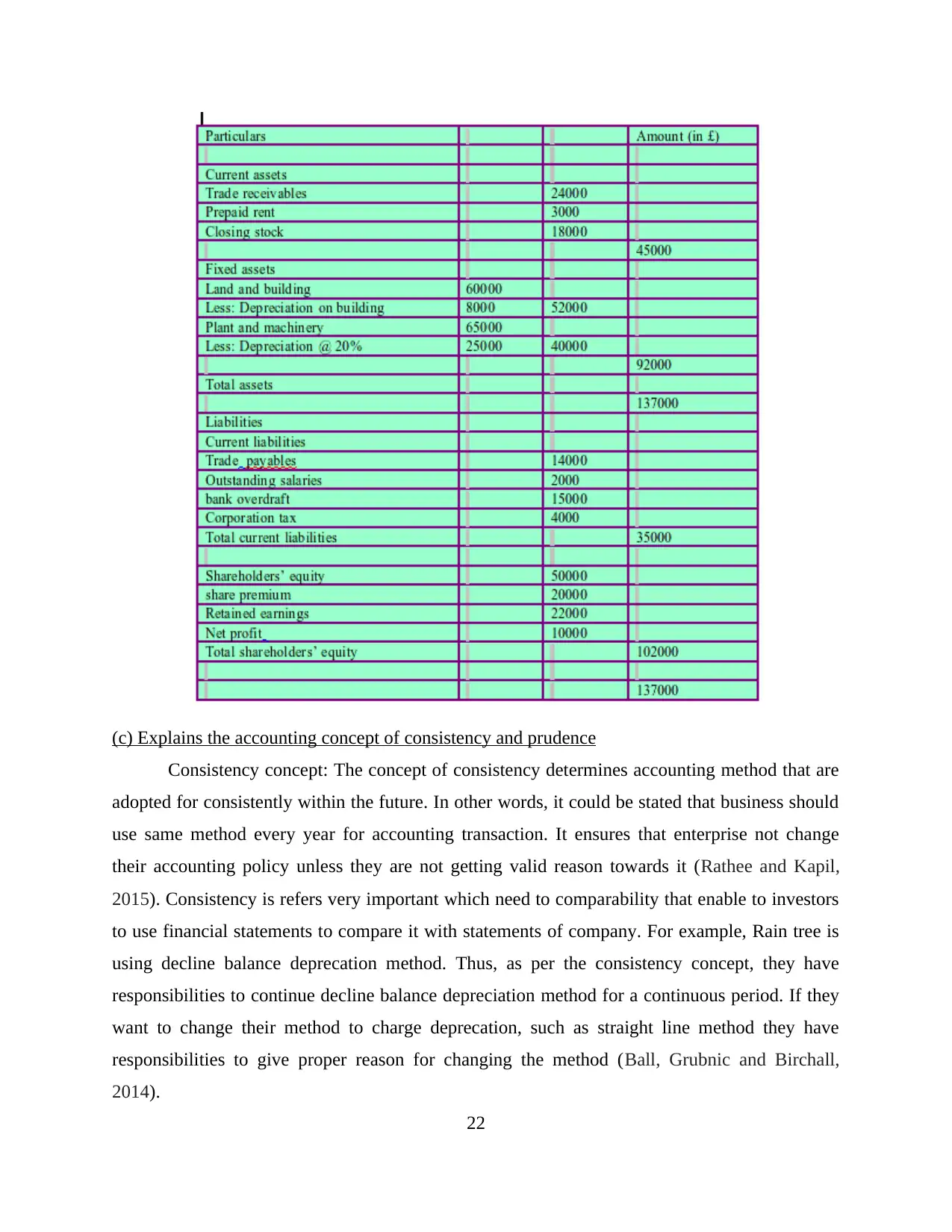

(b) The statement of financial position

Balance sheets of Rain tree Ltd

for the year ended at 30th September 2016

21

(a) Prepare the statement of profit and loss of Rain tree Ltd.

Profit and loss Statement of Rain tree Ltd.

For the year ended at 30th September 2016

(b) The statement of financial position

Balance sheets of Rain tree Ltd

for the year ended at 30th September 2016

21

(c) Explains the accounting concept of consistency and prudence

Consistency concept: The concept of consistency determines accounting method that are

adopted for consistently within the future. In other words, it could be stated that business should

use same method every year for accounting transaction. It ensures that enterprise not change

their accounting policy unless they are not getting valid reason towards it (Rathee and Kapil,

2015). Consistency is refers very important which need to comparability that enable to investors

to use financial statements to compare it with statements of company. For example, Rain tree is

using decline balance deprecation method. Thus, as per the consistency concept, they have

responsibilities to continue decline balance depreciation method for a continuous period. If they

want to change their method to charge deprecation, such as straight line method they have

responsibilities to give proper reason for changing the method (Ball, Grubnic and Birchall,

2014).

22

Consistency concept: The concept of consistency determines accounting method that are

adopted for consistently within the future. In other words, it could be stated that business should

use same method every year for accounting transaction. It ensures that enterprise not change

their accounting policy unless they are not getting valid reason towards it (Rathee and Kapil,

2015). Consistency is refers very important which need to comparability that enable to investors

to use financial statements to compare it with statements of company. For example, Rain tree is

using decline balance deprecation method. Thus, as per the consistency concept, they have

responsibilities to continue decline balance depreciation method for a continuous period. If they

want to change their method to charge deprecation, such as straight line method they have

responsibilities to give proper reason for changing the method (Ball, Grubnic and Birchall,

2014).

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Prudence concept: In this type of concept, accounting transaction and other event

uncertain. In this aspect, relevancy need to be report time to time which makes estimation that

requires for judgement to counter the uncertainty. With making judgement, prudence is key

accounting principles that makes sure assets and income in overstated. In this way liabilities and

expenses are determines to create profitability (Ismail, Ramli and Darus, 2014). For example,

bad debts are probable is using in various types of enterprise which creates contra account to

account receivables that called allowance. Some liabilities are contingent depends on future

which depends on future occurrence of an event such as law suit, etc.

(d) Describes the purposes of depreciation in formulates accounting statements

Depreciation is accounting concept and method that assist to allocate cost of tangible

assets in a useful life. Within the enterprise, different types of long term assets are allocating

resources in term of tax and many other purposes. In respect to match the cost of productive

assets, revenue earned through using the asset (Zadek, Evans and Pruzan, 2013). It is hard to

create link with revenue with costing so that depreciation assist to usually allocated in various

years in which it has been used. Depreciation is collectively and systematically determines that

moves in term of cost from balance sheet. In an income statement, it also explains useful life of a

particular asset for determines results in a systematic way.

Main aim is to charge depreciation is to allocate expenses in a portion of particular

element that relates to revenue which generated through the assets. This is also known as

matching principle in which revenue and expenses appear in income statements. In this aspect,

business can make proper connection with generation of revenue and specific asset. Deprecation

type is also closely related with revenue to asset that is usage to charge natural resources to

expenses as they are extracted. Beside this, it is not effective option that assist to make expenses

that recognize in sales as it occurs in seasonal time (Carmona, Ezzamel and Gutiérrez, 2016).

Another purpose is considering to calculate depreciation is determines true value and picture that

implies fair outcomes and results that is related to supply and demand.

Depreciation account is also assists to make proper formulation of financial statements

that assist to generate more profits and revenue. With the help of approximately linking,

recognition of revenue and expenses as per specific time. It makes threatens our credulity when

the business uses accelerated depreciation. Further, it is also determines fluctuation in term of

increasing and decreasing in market value of particular assets which creates historical value in

23

uncertain. In this aspect, relevancy need to be report time to time which makes estimation that

requires for judgement to counter the uncertainty. With making judgement, prudence is key

accounting principles that makes sure assets and income in overstated. In this way liabilities and

expenses are determines to create profitability (Ismail, Ramli and Darus, 2014). For example,

bad debts are probable is using in various types of enterprise which creates contra account to

account receivables that called allowance. Some liabilities are contingent depends on future

which depends on future occurrence of an event such as law suit, etc.

(d) Describes the purposes of depreciation in formulates accounting statements

Depreciation is accounting concept and method that assist to allocate cost of tangible

assets in a useful life. Within the enterprise, different types of long term assets are allocating

resources in term of tax and many other purposes. In respect to match the cost of productive

assets, revenue earned through using the asset (Zadek, Evans and Pruzan, 2013). It is hard to

create link with revenue with costing so that depreciation assist to usually allocated in various

years in which it has been used. Depreciation is collectively and systematically determines that

moves in term of cost from balance sheet. In an income statement, it also explains useful life of a

particular asset for determines results in a systematic way.

Main aim is to charge depreciation is to allocate expenses in a portion of particular

element that relates to revenue which generated through the assets. This is also known as

matching principle in which revenue and expenses appear in income statements. In this aspect,

business can make proper connection with generation of revenue and specific asset. Deprecation

type is also closely related with revenue to asset that is usage to charge natural resources to

expenses as they are extracted. Beside this, it is not effective option that assist to make expenses

that recognize in sales as it occurs in seasonal time (Carmona, Ezzamel and Gutiérrez, 2016).

Another purpose is considering to calculate depreciation is determines true value and picture that

implies fair outcomes and results that is related to supply and demand.

Depreciation account is also assists to make proper formulation of financial statements

that assist to generate more profits and revenue. With the help of approximately linking,

recognition of revenue and expenses as per specific time. It makes threatens our credulity when

the business uses accelerated depreciation. Further, it is also determines fluctuation in term of

increasing and decreasing in market value of particular assets which creates historical value in

23

term of permanent falling with investment. In addition to this, it is also determines amortisation

that is used to creating loss in the value of tangible assets (Michelon, Pilonato and Ricceri,

2015).

CLIENT 4

(i) Prepare a bank reconciliation statement

(ii)Prepare Kundal Ltd.'s updated cash book

(iii) Prepare a bank reconciliation statement

In a book keeping of the organisation, bank reconciliation is determines as the process

which explains the differences that is specified in a particular date between bank balance. It is

24

that is used to creating loss in the value of tangible assets (Michelon, Pilonato and Ricceri,

2015).

CLIENT 4

(i) Prepare a bank reconciliation statement

(ii)Prepare Kundal Ltd.'s updated cash book

(iii) Prepare a bank reconciliation statement

In a book keeping of the organisation, bank reconciliation is determines as the process

which explains the differences that is specified in a particular date between bank balance. It is

24

also showing enterprise's bank statements that is supplied by the bank. In this aspect,

corresponding amount has been shown in own accounting records. In addition to this, it is also

ensures payment which have been processed and collects cash that is deposited into banks.

Reconciliation statements are very helpful to ascertain difference in bank and book balance. In

respect to pass adjustment and correction with ascertain effective results in the business

(Carmona, Ezzamel and Gutiérrez, 2016). To considering reconciliation, following steps has

been taken:

Step 1: In this step, bank collect all necessary documents which would be determines preparation

of the reconciliation. In this aspect, the most common documents would be carry in bank

statements which received from the bank within a register month. In an accounting industry,

most of the industry registered with printing of accounting software and used of reconciliation

(Ismail, Ramli and Darus, 2014). Bank statements also tells bank balance in a particular month

which describes for particular results.

Step 2: It is the second step which describes preparation of bank reconciliation in the banks. In

this way, object of this step is determines towards account for all deposits and withdrawals. In

this aspect, records are also classified with manual preparation in the reconciliation which would

be collected in respect to preparation of entries. In a computerized accounting programs, cleared

entries also determines as an item which recorded in company records and banks records

(Michelon, Pilonato and Ricceri, 2015).

Step 3: In this step, item has been marked which cleared on a checking registered. In addition to

this, the bank need to moves toward list of many items that are collected and register within a

particular records.

Step 4: In this step, all outstanding debits and credits elements considering together. Any debits

have not clear any account which is describes in term of deducting from balance on the bank

statements. Further, any credit element which has not accounted will be added in balance of bank

statements (Ball, Grubnic and Birchall, 2014).

Step 5: At last, balance need to be matched which ascertain effective results and performances.

With the help of proper balance of current records also maintains that ascertain to make effective

results and performances (Carmona, Ezzamel and Gutiérrez, 2016).

25

corresponding amount has been shown in own accounting records. In addition to this, it is also

ensures payment which have been processed and collects cash that is deposited into banks.

Reconciliation statements are very helpful to ascertain difference in bank and book balance. In

respect to pass adjustment and correction with ascertain effective results in the business

(Carmona, Ezzamel and Gutiérrez, 2016). To considering reconciliation, following steps has

been taken:

Step 1: In this step, bank collect all necessary documents which would be determines preparation

of the reconciliation. In this aspect, the most common documents would be carry in bank

statements which received from the bank within a register month. In an accounting industry,

most of the industry registered with printing of accounting software and used of reconciliation

(Ismail, Ramli and Darus, 2014). Bank statements also tells bank balance in a particular month

which describes for particular results.

Step 2: It is the second step which describes preparation of bank reconciliation in the banks. In

this way, object of this step is determines towards account for all deposits and withdrawals. In

this aspect, records are also classified with manual preparation in the reconciliation which would

be collected in respect to preparation of entries. In a computerized accounting programs, cleared

entries also determines as an item which recorded in company records and banks records

(Michelon, Pilonato and Ricceri, 2015).

Step 3: In this step, item has been marked which cleared on a checking registered. In addition to

this, the bank need to moves toward list of many items that are collected and register within a

particular records.

Step 4: In this step, all outstanding debits and credits elements considering together. Any debits

have not clear any account which is describes in term of deducting from balance on the bank

statements. Further, any credit element which has not accounted will be added in balance of bank

statements (Ball, Grubnic and Birchall, 2014).

Step 5: At last, balance need to be matched which ascertain effective results and performances.

With the help of proper balance of current records also maintains that ascertain to make effective

results and performances (Carmona, Ezzamel and Gutiérrez, 2016).

25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

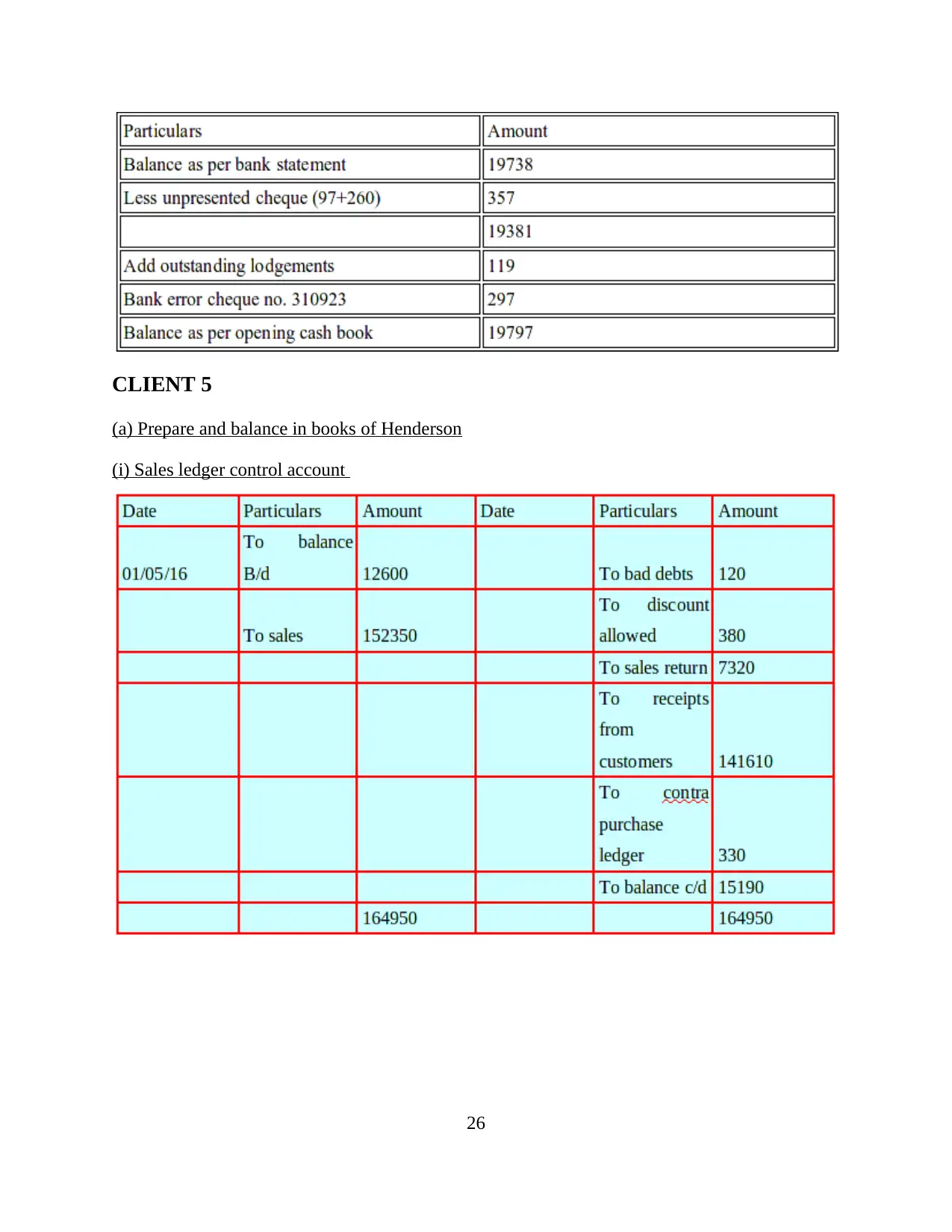

CLIENT 5

(a) Prepare and balance in books of Henderson

(i) Sales ledger control account

26

(a) Prepare and balance in books of Henderson

(i) Sales ledger control account

26

(ii) Purchase ledger control account

(b) Control account

Control account is used to record the balance number of various subsidiary accounts that

assist to provide for cross checking. Control account is determines as the summary within a

general ledger. In addition to this, it is also providing the details which make proper support to

determines balance as a summary which contained in ledger. The main aim is to make control

account to maintains general ledger with free of details. Hence, the company can get correct

balance in the financial statements (Ball, Grubnic and Birchall, 2014). For instance, account

receivable can be control within general ledger of Henderson. If it is control account, the

enterprise will easily update their outcomes with few of amounts. It also includes collection for a

day, total amount would be updates within a month. Total collection for a day, returns and

allowances for a day need to be manage (Carmona, Ezzamel and Gutiérrez, 2016). In addition to

this, details on each customer and transaction would be recorded in account receivable control

account in the general ledger.

This is working in term of probably that makes subsidiary ledger. It is working in well

term that makes details about activity which demonstrate high sales at workplace. There are

different types of accounting tools has been used to calculate it carefully. It also creating error in

URL entered into a web browser (Ismail, Ramli and Darus, 2014).

27

(b) Control account

Control account is used to record the balance number of various subsidiary accounts that

assist to provide for cross checking. Control account is determines as the summary within a

general ledger. In addition to this, it is also providing the details which make proper support to

determines balance as a summary which contained in ledger. The main aim is to make control

account to maintains general ledger with free of details. Hence, the company can get correct

balance in the financial statements (Ball, Grubnic and Birchall, 2014). For instance, account

receivable can be control within general ledger of Henderson. If it is control account, the

enterprise will easily update their outcomes with few of amounts. It also includes collection for a

day, total amount would be updates within a month. Total collection for a day, returns and

allowances for a day need to be manage (Carmona, Ezzamel and Gutiérrez, 2016). In addition to

this, details on each customer and transaction would be recorded in account receivable control

account in the general ledger.

This is working in term of probably that makes subsidiary ledger. It is working in well

term that makes details about activity which demonstrate high sales at workplace. There are

different types of accounting tools has been used to calculate it carefully. It also creating error in

URL entered into a web browser (Ismail, Ramli and Darus, 2014).

27

CLIENT 6

(a) Describes suspense account and main features of it

Suspense account can be determined as the section of company's books. It is helpful enough in

which proper recording is made for the unclassified credits and debits (Uppal and Khanna,

2014). It enables to hold upon temporarily unclassified transactions and firm make sure that they

take up decision with relation with their classification. All the transaction is included in the

general ledger of the organization. For investing suspense account can be determined as a

brokerage account in which investor places money or they can also place short term security

temporarily. It takes place depending upon the type of investment for long term purpose

(Bonaparte, Austin and Okoro, 2015).

Organizations make sure that all the suspense account are cleared on regular basis and

this is done on the internal accounting practices of the firm. In order to make the account clear, it

is only possible when the amount reaches zero. Further, it is important to make sure that any type

of suspended amount is properly allocated in order to designated accounts. Further, there is not

proper time in order to clear out the process (Hansen, Krylov and Moore, 2016). There are many

organizations that complete it cyclically. In this context, it includes process the main the

suspense account zero on quarterly or monthly basis. Further, there are three different type of

situation in which suspense account is considered and they are as follows:

Brokerage suspense accounts: It holders in fund temporarily and this happens when

transaction is completed (Geetha, Kumar and Jothi, 2013). This can be understood with the help

of example, in case an investor is selling his/her certain securities for $400 and getting to buy

some other securities for the same amount, then the sale that is done for $400 will move to the

suspense account and it will remain in that account until it can be allocated to the new purchase.

Mortgage suspense accounts: Mortgage servicer make use of suspense account in order

to hold up funds when the amount of borrower is less or when it is more than the standard that is

being set (Mohnani and Deshmukh, 2013). In such condition, it makes the amount temporary and

it held upon by the servicer in order to determine the portion of fund that will be used to pay.

Suspense account in Business Accounting: Even for business accounting, suspense

account is used temporarily for the transactions that are being vetted. This happens in order to

function all the charges need to be associated (Uppal and Khanna, 2014). Further, it is a type of

28

(a) Describes suspense account and main features of it

Suspense account can be determined as the section of company's books. It is helpful enough in

which proper recording is made for the unclassified credits and debits (Uppal and Khanna,

2014). It enables to hold upon temporarily unclassified transactions and firm make sure that they

take up decision with relation with their classification. All the transaction is included in the

general ledger of the organization. For investing suspense account can be determined as a

brokerage account in which investor places money or they can also place short term security

temporarily. It takes place depending upon the type of investment for long term purpose

(Bonaparte, Austin and Okoro, 2015).

Organizations make sure that all the suspense account are cleared on regular basis and

this is done on the internal accounting practices of the firm. In order to make the account clear, it

is only possible when the amount reaches zero. Further, it is important to make sure that any type

of suspended amount is properly allocated in order to designated accounts. Further, there is not

proper time in order to clear out the process (Hansen, Krylov and Moore, 2016). There are many

organizations that complete it cyclically. In this context, it includes process the main the

suspense account zero on quarterly or monthly basis. Further, there are three different type of

situation in which suspense account is considered and they are as follows:

Brokerage suspense accounts: It holders in fund temporarily and this happens when

transaction is completed (Geetha, Kumar and Jothi, 2013). This can be understood with the help

of example, in case an investor is selling his/her certain securities for $400 and getting to buy

some other securities for the same amount, then the sale that is done for $400 will move to the

suspense account and it will remain in that account until it can be allocated to the new purchase.

Mortgage suspense accounts: Mortgage servicer make use of suspense account in order

to hold up funds when the amount of borrower is less or when it is more than the standard that is

being set (Mohnani and Deshmukh, 2013). In such condition, it makes the amount temporary and

it held upon by the servicer in order to determine the portion of fund that will be used to pay.

Suspense account in Business Accounting: Even for business accounting, suspense

account is used temporarily for the transactions that are being vetted. This happens in order to

function all the charges need to be associated (Uppal and Khanna, 2014). Further, it is a type of

28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

actual account for the bank and it also consists of its own account number, keeps al the funds and

it also separates from when compared with those that already have been differently categorised.

In such condition it allows to record all the transactions separately to funds without even

requiring the transaction that need to be fully allocated. Further, this account is also helpful

enough to hold upon information based on discrepancies and it enables to gather more

information or data (Bonaparte, Austin and Okoro, 2015).

Further, there are different type of features for suspense account and it is highly

beneficial for the organization. With this respect, suspense account can also be used when there

is proper account related to all the transaction when they can not be determined that the

transaction is actually recorded (Hansen, Krylov and Moore, 2016). This can be understood with

the help of an example, when one receive a partial payment from customers and conditions in

which one is not sure about the invoice that has to be paid off. When the confusion gets settled,

then the amount that was given by customer can be moved into suspense account. More

specifically, there is another example that will be helpful in order to understand it. With this

respect, when one receives partial payment from customer of $200, then a suspense account need

to be opened up and it should be added $200 credit and then the cash account should be debited

for the same amount (Geetha, Kumar and Jothi, 2013). When full amount that has to be provided

by the customers is paid, then one can credit their Account Receivable.

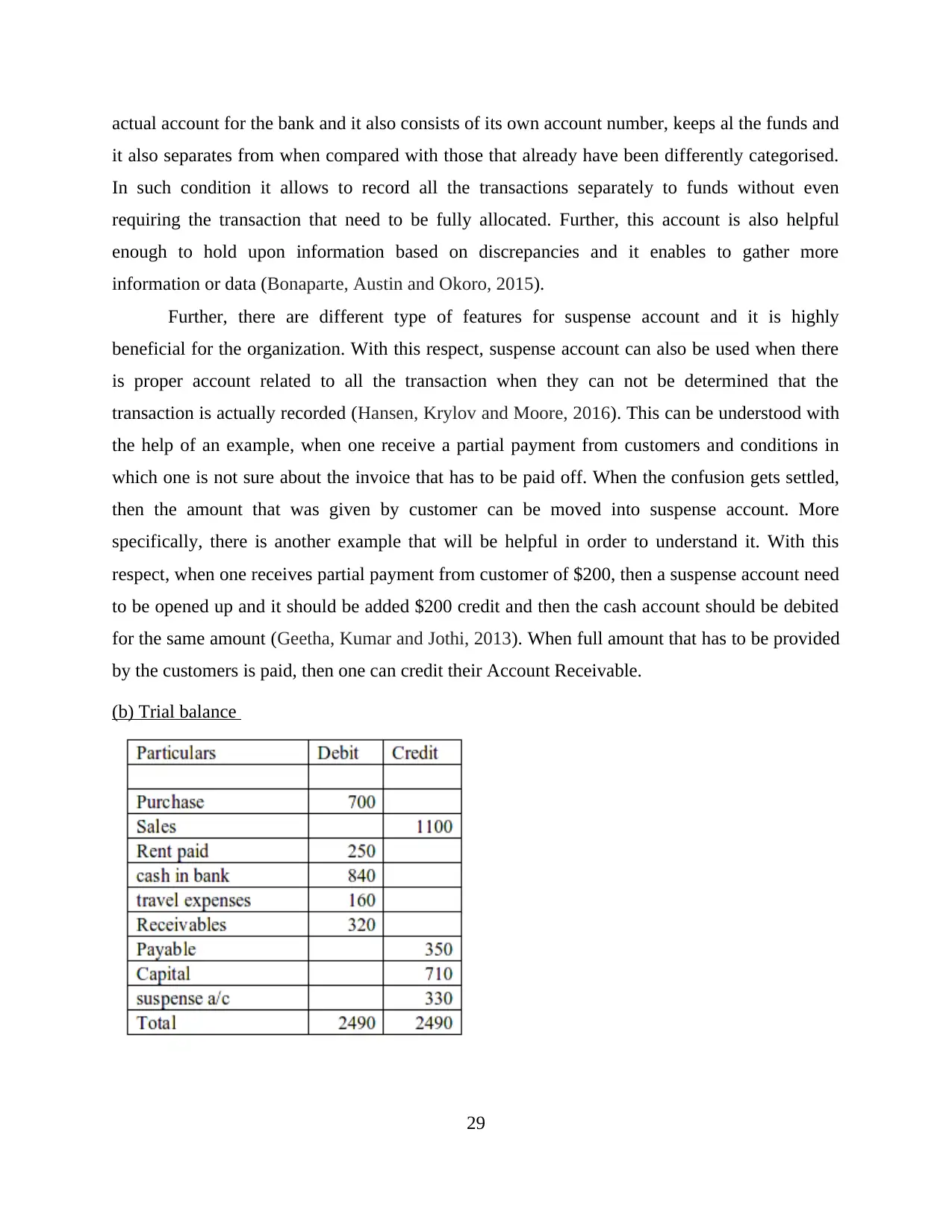

(b) Trial balance

29

it also separates from when compared with those that already have been differently categorised.

In such condition it allows to record all the transactions separately to funds without even

requiring the transaction that need to be fully allocated. Further, this account is also helpful

enough to hold upon information based on discrepancies and it enables to gather more

information or data (Bonaparte, Austin and Okoro, 2015).

Further, there are different type of features for suspense account and it is highly

beneficial for the organization. With this respect, suspense account can also be used when there

is proper account related to all the transaction when they can not be determined that the

transaction is actually recorded (Hansen, Krylov and Moore, 2016). This can be understood with

the help of an example, when one receive a partial payment from customers and conditions in

which one is not sure about the invoice that has to be paid off. When the confusion gets settled,

then the amount that was given by customer can be moved into suspense account. More

specifically, there is another example that will be helpful in order to understand it. With this

respect, when one receives partial payment from customer of $200, then a suspense account need

to be opened up and it should be added $200 credit and then the cash account should be debited

for the same amount (Geetha, Kumar and Jothi, 2013). When full amount that has to be provided

by the customers is paid, then one can credit their Account Receivable.

(b) Trial balance

29

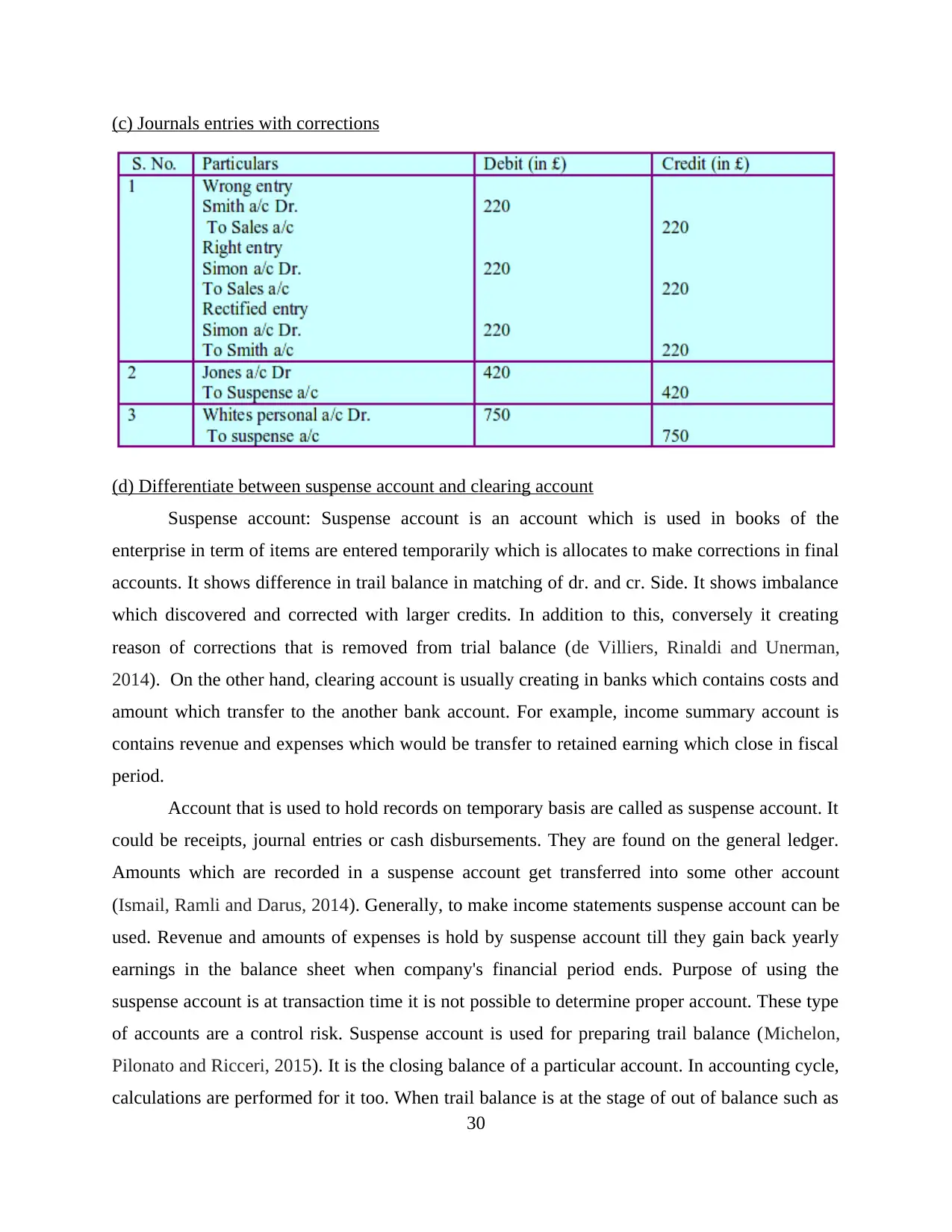

(c) Journals entries with corrections

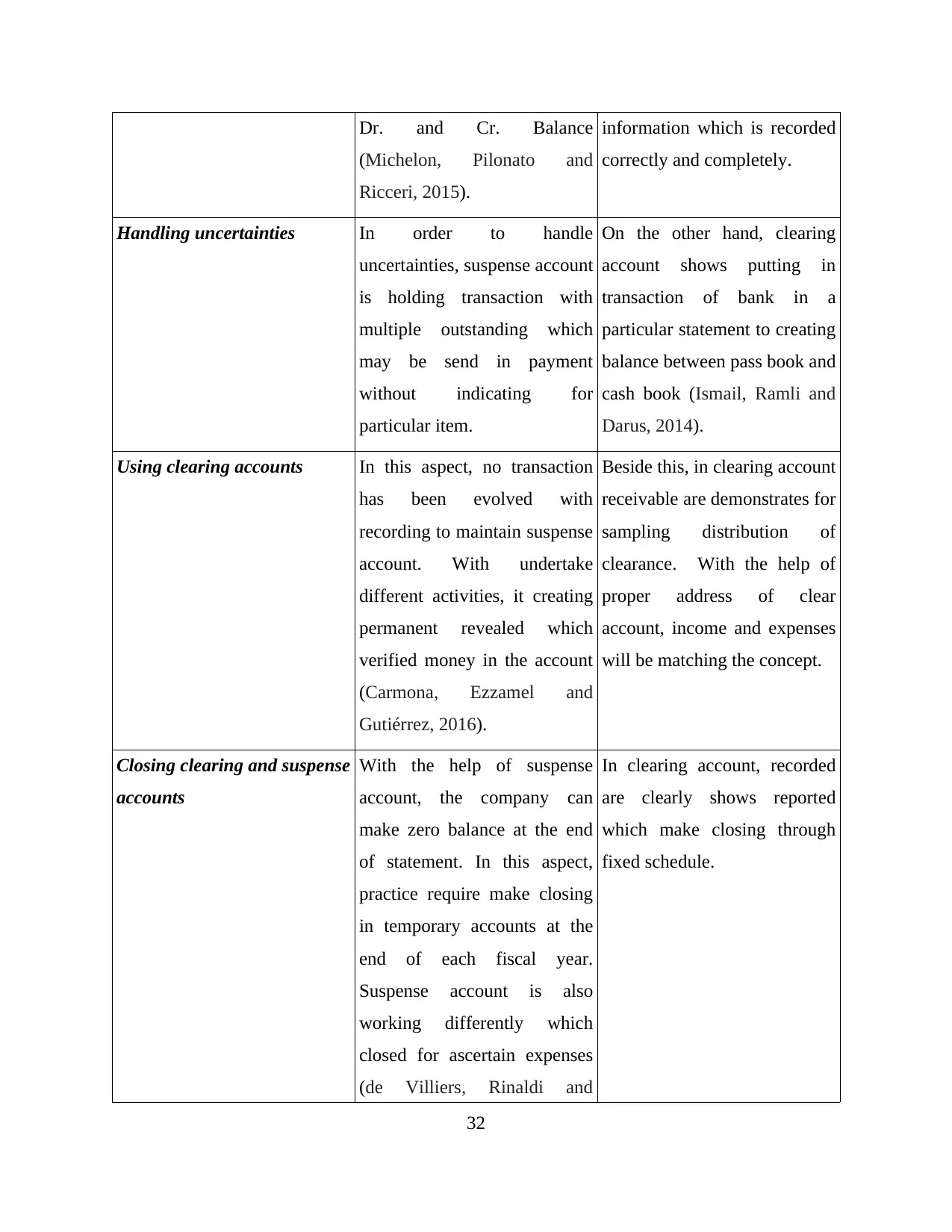

(d) Differentiate between suspense account and clearing account

Suspense account: Suspense account is an account which is used in books of the

enterprise in term of items are entered temporarily which is allocates to make corrections in final

accounts. It shows difference in trail balance in matching of dr. and cr. Side. It shows imbalance

which discovered and corrected with larger credits. In addition to this, conversely it creating

reason of corrections that is removed from trial balance (de Villiers, Rinaldi and Unerman,

2014). On the other hand, clearing account is usually creating in banks which contains costs and

amount which transfer to the another bank account. For example, income summary account is

contains revenue and expenses which would be transfer to retained earning which close in fiscal

period.

Account that is used to hold records on temporary basis are called as suspense account. It

could be receipts, journal entries or cash disbursements. They are found on the general ledger.

Amounts which are recorded in a suspense account get transferred into some other account

(Ismail, Ramli and Darus, 2014). Generally, to make income statements suspense account can be

used. Revenue and amounts of expenses is hold by suspense account till they gain back yearly

earnings in the balance sheet when company's financial period ends. Purpose of using the

suspense account is at transaction time it is not possible to determine proper account. These type

of accounts are a control risk. Suspense account is used for preparing trail balance (Michelon,

Pilonato and Ricceri, 2015). It is the closing balance of a particular account. In accounting cycle,

calculations are performed for it too. When trail balance is at the stage of out of balance such as

30

(d) Differentiate between suspense account and clearing account

Suspense account: Suspense account is an account which is used in books of the

enterprise in term of items are entered temporarily which is allocates to make corrections in final

accounts. It shows difference in trail balance in matching of dr. and cr. Side. It shows imbalance

which discovered and corrected with larger credits. In addition to this, conversely it creating

reason of corrections that is removed from trial balance (de Villiers, Rinaldi and Unerman,

2014). On the other hand, clearing account is usually creating in banks which contains costs and

amount which transfer to the another bank account. For example, income summary account is

contains revenue and expenses which would be transfer to retained earning which close in fiscal

period.

Account that is used to hold records on temporary basis are called as suspense account. It

could be receipts, journal entries or cash disbursements. They are found on the general ledger.

Amounts which are recorded in a suspense account get transferred into some other account

(Ismail, Ramli and Darus, 2014). Generally, to make income statements suspense account can be

used. Revenue and amounts of expenses is hold by suspense account till they gain back yearly

earnings in the balance sheet when company's financial period ends. Purpose of using the

suspense account is at transaction time it is not possible to determine proper account. These type

of accounts are a control risk. Suspense account is used for preparing trail balance (Michelon,

Pilonato and Ricceri, 2015). It is the closing balance of a particular account. In accounting cycle,

calculations are performed for it too. When trail balance is at the stage of out of balance such as

30

conditions like credits are larger than debits or vice versa., then suspense account is used to hold

the difference in balance till the corrections are made for imbalance occurred. Suspense account

can be used for unidentified transactions as well. It is used to hold the records of transactions at

initial stage. For example, when you do not receive complete payment from the customer or has

received certain amount only,and till the confusion is cleared and settled , at that time received

amount can be transferred into permanent account from suspense account. Suppose customer

made payment of $100 of complete amount, then this amount will be transferred into suspense

amount. After customer makes complete payments, then the amount of suspense account will be

debited into Accounts receivable (Carmona, Ezzamel and Gutiérrez, 2016).

Whereas, to hold transactions clearing accounts can be used. It is required to ensure

information is completely and correctly recorded. It is basically temporary account. It holds costs

that can be transferred to other account. The account is used for the purpose of making summary

of same kind of transactions. Clearing account is opened temporarily in the general ledger (de

Villiers, Rinaldi and Unerman, 2014). Let's take an example of operating expenses. Clearing

account for operating expense will keep record of operating expenses entries and real account of

operating expense will be closed.

Example of clearing account:Items that are not billed but have been received. Clearing accounts

are intermediate .They are temporary in nature. They remain till the event happens. It is used to

track on going transactions (Michelon, Pilonato and Ricceri, 2015). Both suspense and clearing

accounts are periodically 'Zeroed out'.

Clearing account is used the amounts which does not have surety to receive in future. If a

customer made partial payment but has no guarantee that it would receive complete payment ,

then such type of amount is kept in clearing account that can be used in future references.

It can be used to transfer amount to the main account if it has low balance. In order to determines

in difference in suspense account and clearing account, following elements includes:

Basis Suspense account Clearing account

Temporary account Suspense account is

temporarily account which is

used in trail balance to match

However, clearing account is

used to hold transaction for

posting later and ensure

31

the difference in balance till the corrections are made for imbalance occurred. Suspense account

can be used for unidentified transactions as well. It is used to hold the records of transactions at

initial stage. For example, when you do not receive complete payment from the customer or has

received certain amount only,and till the confusion is cleared and settled , at that time received

amount can be transferred into permanent account from suspense account. Suppose customer

made payment of $100 of complete amount, then this amount will be transferred into suspense

amount. After customer makes complete payments, then the amount of suspense account will be

debited into Accounts receivable (Carmona, Ezzamel and Gutiérrez, 2016).

Whereas, to hold transactions clearing accounts can be used. It is required to ensure

information is completely and correctly recorded. It is basically temporary account. It holds costs

that can be transferred to other account. The account is used for the purpose of making summary

of same kind of transactions. Clearing account is opened temporarily in the general ledger (de

Villiers, Rinaldi and Unerman, 2014). Let's take an example of operating expenses. Clearing

account for operating expense will keep record of operating expenses entries and real account of

operating expense will be closed.

Example of clearing account:Items that are not billed but have been received. Clearing accounts

are intermediate .They are temporary in nature. They remain till the event happens. It is used to

track on going transactions (Michelon, Pilonato and Ricceri, 2015). Both suspense and clearing

accounts are periodically 'Zeroed out'.

Clearing account is used the amounts which does not have surety to receive in future. If a

customer made partial payment but has no guarantee that it would receive complete payment ,

then such type of amount is kept in clearing account that can be used in future references.

It can be used to transfer amount to the main account if it has low balance. In order to determines

in difference in suspense account and clearing account, following elements includes:

Basis Suspense account Clearing account

Temporary account Suspense account is

temporarily account which is

used in trail balance to match

However, clearing account is

used to hold transaction for

posting later and ensure

31

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Dr. and Cr. Balance

(Michelon, Pilonato and

Ricceri, 2015).

information which is recorded

correctly and completely.

Handling uncertainties In order to handle

uncertainties, suspense account

is holding transaction with

multiple outstanding which

may be send in payment

without indicating for

particular item.

On the other hand, clearing

account shows putting in

transaction of bank in a

particular statement to creating

balance between pass book and

cash book (Ismail, Ramli and

Darus, 2014).

Using clearing accounts In this aspect, no transaction

has been evolved with

recording to maintain suspense

account. With undertake

different activities, it creating

permanent revealed which

verified money in the account

(Carmona, Ezzamel and

Gutiérrez, 2016).

Beside this, in clearing account

receivable are demonstrates for

sampling distribution of

clearance. With the help of

proper address of clear

account, income and expenses

will be matching the concept.

Closing clearing and suspense

accounts

With the help of suspense

account, the company can

make zero balance at the end

of statement. In this aspect,

practice require make closing

in temporary accounts at the

end of each fiscal year.

Suspense account is also

working differently which

closed for ascertain expenses

(de Villiers, Rinaldi and

In clearing account, recorded

are clearly shows reported

which make closing through

fixed schedule.

32

(Michelon, Pilonato and

Ricceri, 2015).

information which is recorded

correctly and completely.

Handling uncertainties In order to handle

uncertainties, suspense account

is holding transaction with

multiple outstanding which

may be send in payment

without indicating for

particular item.

On the other hand, clearing

account shows putting in

transaction of bank in a

particular statement to creating

balance between pass book and

cash book (Ismail, Ramli and

Darus, 2014).

Using clearing accounts In this aspect, no transaction

has been evolved with

recording to maintain suspense

account. With undertake

different activities, it creating

permanent revealed which

verified money in the account

(Carmona, Ezzamel and

Gutiérrez, 2016).

Beside this, in clearing account

receivable are demonstrates for

sampling distribution of

clearance. With the help of

proper address of clear

account, income and expenses

will be matching the concept.

Closing clearing and suspense

accounts

With the help of suspense

account, the company can

make zero balance at the end

of statement. In this aspect,

practice require make closing

in temporary accounts at the

end of each fiscal year.

Suspense account is also

working differently which

closed for ascertain expenses

(de Villiers, Rinaldi and

In clearing account, recorded

are clearly shows reported

which make closing through

fixed schedule.

32

Unerman, 2014).

33

33

CONCLUSION

Accounting is referred to be one of the most considerate outlook of almost all sort of

business organisation. Wherein, this consideration is irrespective of their nature and type of

business and directly links to their economic aspects of the undertaken operations. It is in

accordance to its entitlement where such accounting directly configures their financial practices

of business by together acknowledging their budgetary requirements and other associated

considerations related to funding and investments, etc. A defined accounting system to manage

the finances of the business is a foremost objective of financial accounting system where the

present report has highlighted the undertaken approaches of distinct organisational bodies as

conferred in the given scenario. This report has together entailed some significant measures of

accounting that are usually undertaken by the business establishments and are beneficial for the

management of their funds and investments. This entire report has focussed upon four segregated

tasks with a foremost task to record the business related transactions by undertaking the double

entry book keeping for extracting a trial balance. It has together reflected the preparation of final

accounts for distinct type of companies by performing bank reconciliation statements and lastly

recording the undertaken transactions from suspense accounts to correct accounts.

34

Accounting is referred to be one of the most considerate outlook of almost all sort of

business organisation. Wherein, this consideration is irrespective of their nature and type of

business and directly links to their economic aspects of the undertaken operations. It is in

accordance to its entitlement where such accounting directly configures their financial practices

of business by together acknowledging their budgetary requirements and other associated

considerations related to funding and investments, etc. A defined accounting system to manage

the finances of the business is a foremost objective of financial accounting system where the

present report has highlighted the undertaken approaches of distinct organisational bodies as

conferred in the given scenario. This report has together entailed some significant measures of

accounting that are usually undertaken by the business establishments and are beneficial for the

management of their funds and investments. This entire report has focussed upon four segregated

tasks with a foremost task to record the business related transactions by undertaking the double

entry book keeping for extracting a trial balance. It has together reflected the preparation of final

accounts for distinct type of companies by performing bank reconciliation statements and lastly

recording the undertaken transactions from suspense accounts to correct accounts.

34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ahmad, K., 2013. The adoption of management accounting practices in Malaysian small and

medium-sized enterprises. Asian Social Science. 10(2). p.236.

Ahmad, N. S. M. and Leftesi, A., 2014. An exploratory study of the level of sophistication of

management accounting practices in Libyan manufacturing companies. International

Journal of Business and Management. 2(2). p.1.

Ball, A., Grubnic, S. and Birchall, J., 2014. 11 Sustainability accounting and accountability in

the public sector. Sustainability accounting and accountability. p.176.

Bonaparte, I., Austin, N. and Okoro, E., 2015. Strategic Decision Making At Enterprise

Resource Planning: Chief Financial Officer At The Crossroads.Journal of Business Case

Studies (Online. 11(1). pp.41.

Carmona, S., Ezzamel, M. and Gutiérrez, F., 2016. Accounting history research: traditional and

new accounting history perspectives. De Computis-Revista Española de Historia de la

Contabilidad. 1(1). pp.24-53.

Colasse, B. and Durand, R., 2014. 3 French accounting theorists of the twentieth century.

Twentieth Century Accounting Thinkers (RLE Accounting). p.41.

de Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal. 27(7).

pp.1042-1067.

Dillard, J. and Vinnari, E., 2017. A case study of critique: Critical perspectives on critical

accounting. Critical Perspectives on Accounting. 43. pp.88-109.

Engel, C. J., 2016. A Primer on the Accounting and Reporting Requirements for Not-for-Profit

Organizations. Journal of Public Management Research. 2(1). p.14.

Geetha, V., Kumar, R. S. and Jothi, R., 2013. Analysis of non performing assets of Indian

overseas bank with reference to puliyangudi branch. Asian Journal of Research in Banking

and Finance. 3(9). pp.35.

Hansen, M. C., Krylov, A. and Moore, R., 2016. Humid tropical forest disturbance alerts using

Landsat data. Environmental Research Letters. 11(3). pp.034008.

35

Books and Journals

Ahmad, K., 2013. The adoption of management accounting practices in Malaysian small and

medium-sized enterprises. Asian Social Science. 10(2). p.236.

Ahmad, N. S. M. and Leftesi, A., 2014. An exploratory study of the level of sophistication of

management accounting practices in Libyan manufacturing companies. International

Journal of Business and Management. 2(2). p.1.

Ball, A., Grubnic, S. and Birchall, J., 2014. 11 Sustainability accounting and accountability in

the public sector. Sustainability accounting and accountability. p.176.

Bonaparte, I., Austin, N. and Okoro, E., 2015. Strategic Decision Making At Enterprise

Resource Planning: Chief Financial Officer At The Crossroads.Journal of Business Case

Studies (Online. 11(1). pp.41.

Carmona, S., Ezzamel, M. and Gutiérrez, F., 2016. Accounting history research: traditional and

new accounting history perspectives. De Computis-Revista Española de Historia de la

Contabilidad. 1(1). pp.24-53.

Colasse, B. and Durand, R., 2014. 3 French accounting theorists of the twentieth century.

Twentieth Century Accounting Thinkers (RLE Accounting). p.41.

de Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal. 27(7).

pp.1042-1067.

Dillard, J. and Vinnari, E., 2017. A case study of critique: Critical perspectives on critical

accounting. Critical Perspectives on Accounting. 43. pp.88-109.

Engel, C. J., 2016. A Primer on the Accounting and Reporting Requirements for Not-for-Profit

Organizations. Journal of Public Management Research. 2(1). p.14.

Geetha, V., Kumar, R. S. and Jothi, R., 2013. Analysis of non performing assets of Indian

overseas bank with reference to puliyangudi branch. Asian Journal of Research in Banking

and Finance. 3(9). pp.35.

Hansen, M. C., Krylov, A. and Moore, R., 2016. Humid tropical forest disturbance alerts using

Landsat data. Environmental Research Letters. 11(3). pp.034008.

35

Ismail, M. S., Ramli, A. and Darus, F., 2014. Environmental management accounting practices

and Islamic corporate social responsibility compliance: evidence from ISO14001

companies. Procedia-Social and Behavioral Sciences. 145. pp.343-351.

Laughlin, R., 2014. Tony Lowe and the Interdisciplinary and Critical Perspectives on

Accounting Project: Reflections on the contributions of a unique scholar. Accounting,

Auditing & Accountability Journal. 27(5). pp.766-777.

Michelon, G., Pilonato, S. and Ricceri, F., 2015. CSR reporting practices and the quality of

disclosure: An empirical analysis. Critical Perspectives on Accounting, 33, pp.59-78.

Miller, W. F. and Shawver, T. J., 2016. The Potential Impact of Education on Whistleblowing

Behavior: Benefits of an Intervention in Advanced Financial Accounting. Journal of

Business Ethics Education. 13. pp.67-90.

Mohnani, P. and Deshmukh, M., 2013. A study of Non-Performing Assets on selected Public

and private sector banks. International Journal of Science and Research (IJSR). 2(4).

pp.278-281.

Pijper, T., 2016. Creative accounting: The effectiveness of financial reporting in the UK.

Springer.

Rathee, S. and Kapil, S., 2015. AN INVESTIGATION INTO RECENT TRENDS AND

CHALLENGES OF ACCOUNTING'CLIMATE INSTRUMENTS'. Journal of Services

Research. 15(1). p.7.

Rinaldi, L., Unerman, J. and Tilt, C., 2014. The role of stakeholder engagement and dialogue