Financial Accounting Principles | Report

Added on 2020-02-03

41 Pages6450 Words41 Views

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a) Meaning of financial accounting, regulation, rules and principles with effective concept

relating to consistency and material disclosure......................................................................1

(B) PORTFOLIO FOR A CLIENT.................................................................................................5

CLIENT 1........................................................................................................................................5

(i) The book of primary entry.................................................................................................5

(ii) Complete double entry system.........................................................................................6

..............................................................................................................................................11

..............................................................................................................................................12

..............................................................................................................................................13

..............................................................................................................................................15

..............................................................................................................................................17

..............................................................................................................................................17

(iii) Close accounts with drawing the trail balance..............................................................17

CLIENT 2......................................................................................................................................18

(a) Statement of profit and loss for Peter Pipe ....................................................................18

(b) Statement of financial position for Peter Pipe................................................................20

CLIENT 3......................................................................................................................................21

(a) Prepare the statement of profit and loss of Rain tree Ltd................................................21

(b) The statement of financial position ................................................................................21

(c) Explains the accounting concept of consistency and prudence......................................22

(d) Describes the purposes of depreciation in formulates accounting statements................23

CLIENT 4......................................................................................................................................24

(i) Prepare a bank reconciliation statement..........................................................................24

(ii)Prepare Kundal Ltd.'s updated cash book .......................................................................24

(iii) Prepare a bank reconciliation statement........................................................................24

CLIENT 5......................................................................................................................................26

(a) Prepare and balance in books of Henderson...................................................................26

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(a) Meaning of financial accounting, regulation, rules and principles with effective concept

relating to consistency and material disclosure......................................................................1

(B) PORTFOLIO FOR A CLIENT.................................................................................................5

CLIENT 1........................................................................................................................................5

(i) The book of primary entry.................................................................................................5

(ii) Complete double entry system.........................................................................................6

..............................................................................................................................................11

..............................................................................................................................................12

..............................................................................................................................................13

..............................................................................................................................................15

..............................................................................................................................................17

..............................................................................................................................................17

(iii) Close accounts with drawing the trail balance..............................................................17

CLIENT 2......................................................................................................................................18

(a) Statement of profit and loss for Peter Pipe ....................................................................18

(b) Statement of financial position for Peter Pipe................................................................20

CLIENT 3......................................................................................................................................21

(a) Prepare the statement of profit and loss of Rain tree Ltd................................................21

(b) The statement of financial position ................................................................................21

(c) Explains the accounting concept of consistency and prudence......................................22

(d) Describes the purposes of depreciation in formulates accounting statements................23

CLIENT 4......................................................................................................................................24

(i) Prepare a bank reconciliation statement..........................................................................24

(ii)Prepare Kundal Ltd.'s updated cash book .......................................................................24

(iii) Prepare a bank reconciliation statement........................................................................24

CLIENT 5......................................................................................................................................26

(a) Prepare and balance in books of Henderson...................................................................26

(i) Sales ledger control account ...........................................................................................26

(ii) Purchase ledger control account ....................................................................................27

(b) Control account ..............................................................................................................27

CLIENT 6......................................................................................................................................28

(a) Describes suspense account and main features of it.......................................................28

(b) Trial balance ..................................................................................................................29

(c) Journals entries with corrections.....................................................................................30

(d) Differentiate between suspense account and clearing account.......................................30

CONCLUSION..............................................................................................................................33

REFERENCES..............................................................................................................................34

(ii) Purchase ledger control account ....................................................................................27

(b) Control account ..............................................................................................................27

CLIENT 6......................................................................................................................................28

(a) Describes suspense account and main features of it.......................................................28

(b) Trial balance ..................................................................................................................29

(c) Journals entries with corrections.....................................................................................30

(d) Differentiate between suspense account and clearing account.......................................30

CONCLUSION..............................................................................................................................33

REFERENCES..............................................................................................................................34

INTRODUCTION

In recent years, role of accounting is continuously increases which also enhance market

complexity. It includes generally accepted accounting principles which is common set of rules

and standards which indicates financial statements (Carmona, Ezzamel and Gutiérrez, 2016).

There are different types of companies exist in market which require financial statements as per

guidance of GAAP. Main aim to considering rules and regulation of GAAP to create standard

and uniform results that are based on financial outcomes and performances. With applying in

non profit organisation, transparency can be accomplish in easy way. It covers key areas such as

recognition, measurement, presentation and disclosure. These elements assist to minimize risk

from financial erroneous with reporting that assist to check and making safeguards in a place

(Michelon, Pilonato and Ricceri, 2015).

In this context, report is based on different clients of accounting firm who requires

prepares journal, ledger, profit and loss account, balance sheet and many other financial

statements. In addition to this, it is also induces rectification of errors which considers

rectification for accomplish transactions. With the help of following transactions, business can

revealed their conclusion towards decision and outcomes (Engel, 2016). Moreover, it stresses on

find out mistakes which occur in the enterprise to do transactions. In this aspect, different types

of objectives can be achieve by the company for ascertain financial statements at workplace.

TASK 1

(a) Meaning of financial accounting, regulation, rules and principles with effective concept

relating to consistency and material disclosure

Meaning of financial accounting: Financial accounting is special branch which keep all records

of financial transactions. It assists to using standardized principles and guidelines that are

recorded and summarized within financial report and statements. For example, income

statements and balance sheet (Rinaldi, Unerman and Tilt, 2014). In addition to this, financial

accounting is a crucial element which helpful to make routine schedule for solve company

issues. Statements considering externally because it can be given outside the firm such charted

accountant, etc.

Regulation that are related to financial accounting: In this aspect, principles are derived that

prepare for matching the concept. In a report of financial statements such as audit, compilation

1

In recent years, role of accounting is continuously increases which also enhance market

complexity. It includes generally accepted accounting principles which is common set of rules

and standards which indicates financial statements (Carmona, Ezzamel and Gutiérrez, 2016).

There are different types of companies exist in market which require financial statements as per

guidance of GAAP. Main aim to considering rules and regulation of GAAP to create standard

and uniform results that are based on financial outcomes and performances. With applying in

non profit organisation, transparency can be accomplish in easy way. It covers key areas such as

recognition, measurement, presentation and disclosure. These elements assist to minimize risk

from financial erroneous with reporting that assist to check and making safeguards in a place

(Michelon, Pilonato and Ricceri, 2015).

In this context, report is based on different clients of accounting firm who requires

prepares journal, ledger, profit and loss account, balance sheet and many other financial

statements. In addition to this, it is also induces rectification of errors which considers

rectification for accomplish transactions. With the help of following transactions, business can

revealed their conclusion towards decision and outcomes (Engel, 2016). Moreover, it stresses on

find out mistakes which occur in the enterprise to do transactions. In this aspect, different types

of objectives can be achieve by the company for ascertain financial statements at workplace.

TASK 1

(a) Meaning of financial accounting, regulation, rules and principles with effective concept

relating to consistency and material disclosure

Meaning of financial accounting: Financial accounting is special branch which keep all records

of financial transactions. It assists to using standardized principles and guidelines that are

recorded and summarized within financial report and statements. For example, income

statements and balance sheet (Rinaldi, Unerman and Tilt, 2014). In addition to this, financial

accounting is a crucial element which helpful to make routine schedule for solve company

issues. Statements considering externally because it can be given outside the firm such charted

accountant, etc.

Regulation that are related to financial accounting: In this aspect, principles are derived that

prepare for matching the concept. In a report of financial statements such as audit, compilation

1

and review, etc. (Spence and Rinaldi, 2014). must be demonstrate information that are related to

contained statements of GAAP. There are certain regulation frames that are related to financial

accounting. They are as follows:

Principle of regularity: This principle is determines conformity with ensure rules and

laws.

Principle of consistency: It is states that what businesses fixed for treatment for

accounting, it regularly runs in same way every year (Colasse and Durand, 2014).

Principles of non-compensation: In this aspect, business should follows all details of

the financial information which seek to compensate a debt with an asset, revenue and

expenses, etc.

Principle of sincerity: This accounting principle is based on accounting unit which

reflect to good faith as per reality of financial status of company.

Principles of permanence of methods: This principle has aim to allowing and

comparing information that are related to finance part and also published by the

enterprise (Ahmad and Leftesi, 2014).

Principle of prudence: This principle has aim to show reality to make things look good

than they exist. In addition to this, revenue need to be recorded only when it covered in

certain provision with including for an expense.

Principle of continuity: In order to stating financial information, one person need to be

assume that enterprise cannot be interrupted. This principle ensures that assets have not

been accounted as disposable value which continually accounted which accepted on

historical value. For example, deprecation is considering as going concern (Miller and

Shawver, 2016).

Principle of periodicity: In respect to states financial information, accounting entry

allocating within a given period. It could be split as per covering various periods. In

addition to this, revenue also need to be split in the entire time span which not counted

for entire date of transaction.

Principle of full disclosure/materiality: With the help of information and value, it has

been pertaining that financial position in organisation need to be disclosed as records (de

Villiers, Rinaldi and Unerman, 2014).

2

contained statements of GAAP. There are certain regulation frames that are related to financial

accounting. They are as follows:

Principle of regularity: This principle is determines conformity with ensure rules and

laws.

Principle of consistency: It is states that what businesses fixed for treatment for

accounting, it regularly runs in same way every year (Colasse and Durand, 2014).

Principles of non-compensation: In this aspect, business should follows all details of

the financial information which seek to compensate a debt with an asset, revenue and

expenses, etc.

Principle of sincerity: This accounting principle is based on accounting unit which

reflect to good faith as per reality of financial status of company.

Principles of permanence of methods: This principle has aim to allowing and

comparing information that are related to finance part and also published by the

enterprise (Ahmad and Leftesi, 2014).

Principle of prudence: This principle has aim to show reality to make things look good

than they exist. In addition to this, revenue need to be recorded only when it covered in

certain provision with including for an expense.

Principle of continuity: In order to stating financial information, one person need to be

assume that enterprise cannot be interrupted. This principle ensures that assets have not

been accounted as disposable value which continually accounted which accepted on

historical value. For example, deprecation is considering as going concern (Miller and

Shawver, 2016).

Principle of periodicity: In respect to states financial information, accounting entry

allocating within a given period. It could be split as per covering various periods. In

addition to this, revenue also need to be split in the entire time span which not counted

for entire date of transaction.

Principle of full disclosure/materiality: With the help of information and value, it has

been pertaining that financial position in organisation need to be disclosed as records (de

Villiers, Rinaldi and Unerman, 2014).

2

Principle of utmost good faith: All essential information that are related to the

enterprise also disclosed for insurer before taking policy.

Accounting rules and principles: Accounting principles are accepted in basically three

concepts such as basic accounting principles and guidelines, detailed rules and standards and

accepted rules by the industry (Vogel, 2014). Below are such accounting principles and

guidelines which is frames in GAAP: Economic entity assumption: This accounting principle keeps transaction of all

businesses ahead from owner of enterprise. The both are different entities which

considered in the market. Monetary unit assumption: Economic activity within the business is measuring in pound

and transaction are expressed in pound only (Pijper, 2016). The period assumption: This accounting principle determines complex activities in short

and distinctive term within a specific time interval. Cost principle: Cost is refers as amount which spent as cash or equivalent of it. In

addition to this, it demonstrates whether purchase has been happened last year of many

years ago (Ismail, Ramli and Darus, 2014). Full disclosure principle: In this principle, certain information need to be keep safe that

is important for an investor or lender. These types of informations need to be disclosed in

a statement in numerous financial attachments. Going concern principle: This accounting principle determines that the enterprise will

continue exist for long time that carry objectives and commitments that not liquidate in

foreseeable future (Dillard and Vinnari, 2017). Matching principle: This accounting principle is essential for the enterprises to using

accrual system. In this aspect, expenses are need to be match with revenue. For instance,

commission expense need to be reported within a period of sales is made. Wages of

employee is also reported as the expenses (Carmona, Ezzamel and Gutiérrez, 2016). Revenue recognition principles: As per the accrual basis accounting, revenue has been

recognized has been sold and services also performed with money that actually received. Materiality: This accounting principle is frame basic guidelines which need to be

followed by accountant. Professional judgement is also needed to demonstrate significant

amount (Laughlin, 2014).

3

enterprise also disclosed for insurer before taking policy.

Accounting rules and principles: Accounting principles are accepted in basically three

concepts such as basic accounting principles and guidelines, detailed rules and standards and

accepted rules by the industry (Vogel, 2014). Below are such accounting principles and

guidelines which is frames in GAAP: Economic entity assumption: This accounting principle keeps transaction of all

businesses ahead from owner of enterprise. The both are different entities which

considered in the market. Monetary unit assumption: Economic activity within the business is measuring in pound

and transaction are expressed in pound only (Pijper, 2016). The period assumption: This accounting principle determines complex activities in short

and distinctive term within a specific time interval. Cost principle: Cost is refers as amount which spent as cash or equivalent of it. In

addition to this, it demonstrates whether purchase has been happened last year of many

years ago (Ismail, Ramli and Darus, 2014). Full disclosure principle: In this principle, certain information need to be keep safe that

is important for an investor or lender. These types of informations need to be disclosed in

a statement in numerous financial attachments. Going concern principle: This accounting principle determines that the enterprise will

continue exist for long time that carry objectives and commitments that not liquidate in

foreseeable future (Dillard and Vinnari, 2017). Matching principle: This accounting principle is essential for the enterprises to using

accrual system. In this aspect, expenses are need to be match with revenue. For instance,

commission expense need to be reported within a period of sales is made. Wages of

employee is also reported as the expenses (Carmona, Ezzamel and Gutiérrez, 2016). Revenue recognition principles: As per the accrual basis accounting, revenue has been

recognized has been sold and services also performed with money that actually received. Materiality: This accounting principle is frame basic guidelines which need to be

followed by accountant. Professional judgement is also needed to demonstrate significant

amount (Laughlin, 2014).

3

Conservatism: With this regard, two acceptable alternatives are exists within the

enterprise. Conservatism directs accountant for choosing the best alternative that take less

amount.

Conventions and concept relating to consistency and material disclosure: The term

convention includes costumes and tradition that guide accountant to prepare statements. There

are certain important accounting conventions: Convention of disclosure: In order to disclosure of all significant information, it is the

important accounting conventions (Zadek, Evans and Pruzan, 2013). It implies on

accounts which need to be prepare in a way which includes material information that is

clearly disclosed to the reader. Convention of materiality: Convention of materiality is refers as relative importance for

an item. In this convention, those events and items are recorded that possess significance

and other will be ignored. This is because, there is not any way which determines

difference between material and immaterial events (Youssef, 2015). Convention of consistency: This convention determines accounting practices which need

to be remains not charged from one time to another. For instance, stock is valued either

cost or market price whichever is less. Mainly this is follows after one year (Carmona,

Ezzamel and Gutiérrez, 2016).

Convention of conservatism: This element is based on caution approach that making

safe. It will ensure that uncertainties and risk element inherent in organisation activities

that has to be given in proper aspect (Ahmad, 2013).

4

enterprise. Conservatism directs accountant for choosing the best alternative that take less

amount.

Conventions and concept relating to consistency and material disclosure: The term

convention includes costumes and tradition that guide accountant to prepare statements. There

are certain important accounting conventions: Convention of disclosure: In order to disclosure of all significant information, it is the

important accounting conventions (Zadek, Evans and Pruzan, 2013). It implies on

accounts which need to be prepare in a way which includes material information that is

clearly disclosed to the reader. Convention of materiality: Convention of materiality is refers as relative importance for

an item. In this convention, those events and items are recorded that possess significance

and other will be ignored. This is because, there is not any way which determines

difference between material and immaterial events (Youssef, 2015). Convention of consistency: This convention determines accounting practices which need

to be remains not charged from one time to another. For instance, stock is valued either

cost or market price whichever is less. Mainly this is follows after one year (Carmona,

Ezzamel and Gutiérrez, 2016).

Convention of conservatism: This element is based on caution approach that making

safe. It will ensure that uncertainties and risk element inherent in organisation activities

that has to be given in proper aspect (Ahmad, 2013).

4

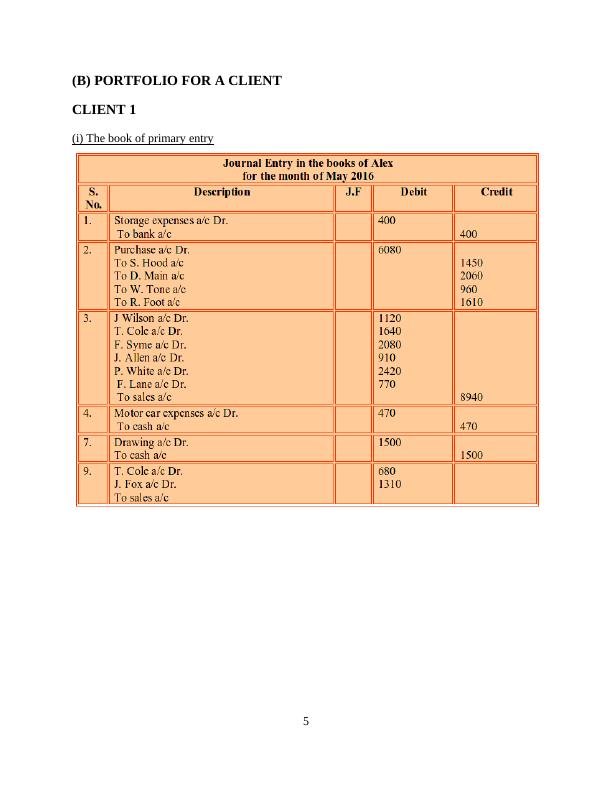

(B) PORTFOLIO FOR A CLIENT

CLIENT 1

(i) The book of primary entry

5

CLIENT 1

(i) The book of primary entry

5

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

FINANCIAL ACCOUNTING INTRODUCTION 3 A. (A) Statement of financial position 20 (B)lg...

|30

|3307

|315

Introduction to Financial Accountinglg...

|30

|5105

|401

Financial Accounting Principles Assignment - Doclg...

|30

|7212

|286

Financial Accounting Assignment - Zync Solutionslg...

|29

|5360

|97

Financial Accounting Principles Assignment - RBS Accountants Ltdlg...

|26

|7021

|485

Accounting Principles Assignment | Financial Accounting Assignmentlg...

|32

|4628

|54