Financial Accounting Standards and Practices

VerifiedAdded on 2020/11/23

|38

|3955

|272

Report

AI Summary

The assignment delves into the significance of regulations and principles in financial accounting. It examines various accounting standards such as IFRS and GAAP, highlighting their impact on financial statement preparation. The document emphasizes the importance of financial statements like balance sheets and income statements for understanding a company's financial position, growth, and profitability. It also analyzes the role of suspense and clearing accounts in facilitating accurate financial reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL ACCOUNTING

PRINCIPLES

PRINCIPLES

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Report related to financial accounting with its rules and regulations.........................................1

1. Defining financial accounting with its goal and objectives....................................................1

Drafting financial accounting regulations...................................................................................2

Accounting principles and rules for governing financial statements..........................................3

Elaborating various concepts of accounting which are disclosure, materiality and consistency4

CLIENT 1........................................................................................................................................4

1. Justifying its journal entries....................................................................................................4

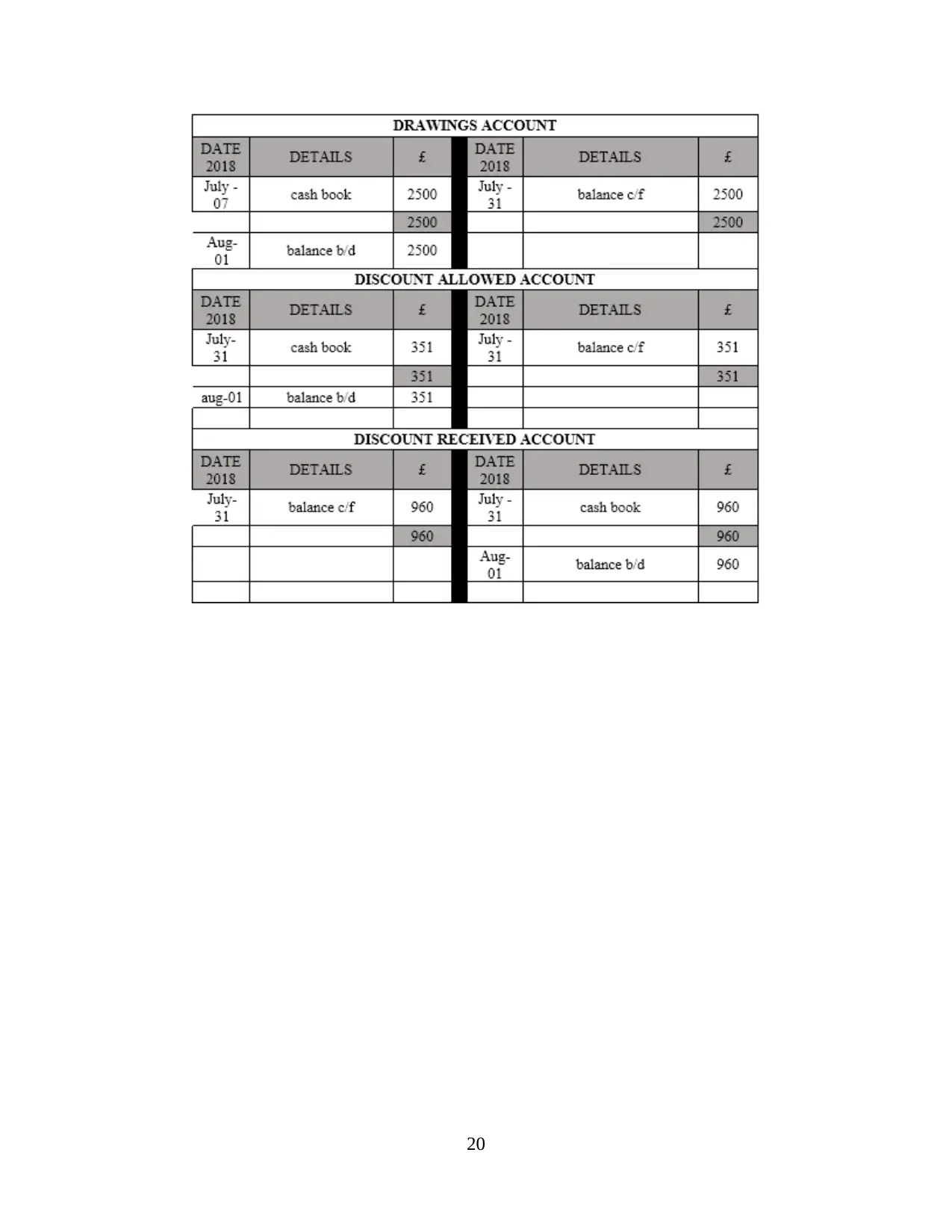

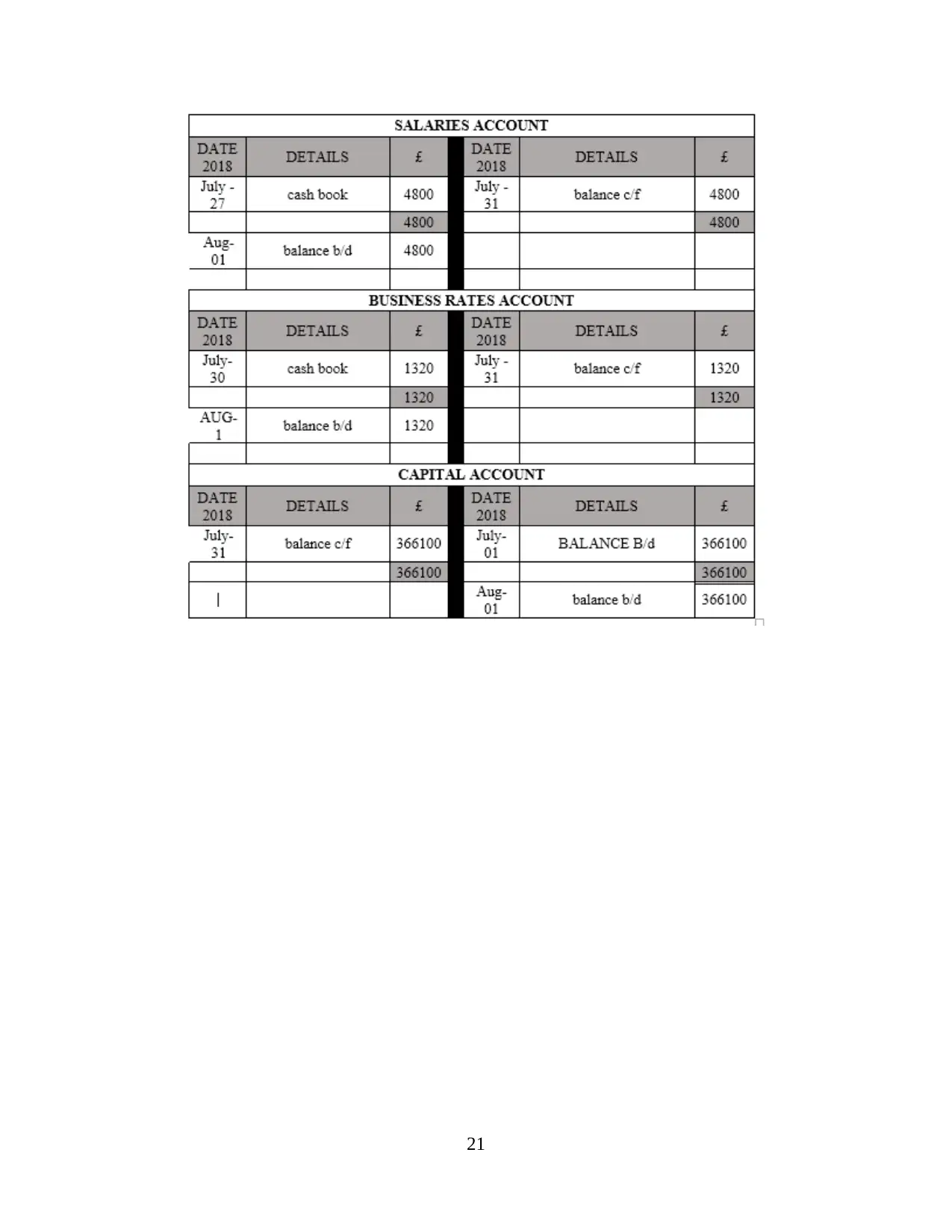

2. Representing its ledger accounts with reference to double entry recording...........................6

B. Ledger accounts......................................................................................................................7

3. Identifying accuracy level of trial balance............................................................................22

CLIENT 2......................................................................................................................................23

(a) Representing Income statement of July 2018 for Sierra Laurenmt.....................................23

(b) Representing Income statement for July 2018 for Sierra Laurent.......................................25

CLIENT 3......................................................................................................................................26

(a) Representing Profit and loss statement of July 31 for LMS Limited..................................26

(b) Representing balance sheet for July 2018 of LMS limited.................................................27

(c) Justifying prudence and consistence with reference to accounting concept .......................27

(d) Representing motive of depreciation for accounting aspect with reference to its each

method.......................................................................................................................................28

CLIENT 4......................................................................................................................................28

A. Representing objective of preparing Bank Reconciliation Statement (BRS)......................28

B. Representing entries which helps in creating variances with context of bank statements...29

C. Representing Cash book of Kendal with its Bank reconciliation statement........................30

CLIENT 5......................................................................................................................................32

(a) Representing Purchase and Sales Ledger account ..............................................................32

(b) Defining control account ....................................................................................................33

CLIENT 6......................................................................................................................................33

a. Representing features of suspense account...........................................................................33

b.c. Representing trial balance .................................................................................................34

d. Representing difference between suspense and clearing account ........................................34

CONCLUSION..............................................................................................................................35

REFERENCES..............................................................................................................................37

INTRODUCTION...........................................................................................................................1

Report related to financial accounting with its rules and regulations.........................................1

1. Defining financial accounting with its goal and objectives....................................................1

Drafting financial accounting regulations...................................................................................2

Accounting principles and rules for governing financial statements..........................................3

Elaborating various concepts of accounting which are disclosure, materiality and consistency4

CLIENT 1........................................................................................................................................4

1. Justifying its journal entries....................................................................................................4

2. Representing its ledger accounts with reference to double entry recording...........................6

B. Ledger accounts......................................................................................................................7

3. Identifying accuracy level of trial balance............................................................................22

CLIENT 2......................................................................................................................................23

(a) Representing Income statement of July 2018 for Sierra Laurenmt.....................................23

(b) Representing Income statement for July 2018 for Sierra Laurent.......................................25

CLIENT 3......................................................................................................................................26

(a) Representing Profit and loss statement of July 31 for LMS Limited..................................26

(b) Representing balance sheet for July 2018 of LMS limited.................................................27

(c) Justifying prudence and consistence with reference to accounting concept .......................27

(d) Representing motive of depreciation for accounting aspect with reference to its each

method.......................................................................................................................................28

CLIENT 4......................................................................................................................................28

A. Representing objective of preparing Bank Reconciliation Statement (BRS)......................28

B. Representing entries which helps in creating variances with context of bank statements...29

C. Representing Cash book of Kendal with its Bank reconciliation statement........................30

CLIENT 5......................................................................................................................................32

(a) Representing Purchase and Sales Ledger account ..............................................................32

(b) Defining control account ....................................................................................................33

CLIENT 6......................................................................................................................................33

a. Representing features of suspense account...........................................................................33

b.c. Representing trial balance .................................................................................................34

d. Representing difference between suspense and clearing account ........................................34

CONCLUSION..............................................................................................................................35

REFERENCES..............................................................................................................................37

INTRODUCTION

The principles of financial accounting are termed as very important for any business

entity as it helps in creating ease for perspective of understanding expenses of future. The main

objective is to control cost on basis of its operation which are held in premises. The present

report is giving brief discussion related to regulations and principles of accounting. In the same

series, it had represented its significance of accounting for attaining growth and profitability

which is followed by every industry along with business entity. There report is signifying

importance of depreciation with its both methods. It had also articulated different financial

statements like balance sheet, income statement, trial balance, bank reconciliation statements etc.

Further it had represented suspense account with its important features and it had been compared

with control account.

Report related to financial accounting with its rules and regulations

1. Defining financial accounting with its goal and objectives

It is considered as a particular accounting branch as it helps in tracking financial

statements of any organization in appropriate aspect. The main role of financial accounting has

been specified as measurement, reporting, gathering and recording of transactions related to

investors and shareholders. It is replicated as appropriate source for determining financial

performances of any organization along with its stability. The major concern is of representing it

in very consistent and fair aspect. The financial statement must be prepared by considering

financial standards which are Generally Accepted Accounting Principles and (IFRS)

International Financial reporting standards.

Its goals and objectives are defined with 4 classifications such as:

Reliability

Relevance

Comparability

Consistency

Reliability: The information which is given via statements of financial must be totally

reliable. In the same series, investors would be gaining difficulty for getting information which is

reliable and in its absence it also creates issues for decision making process. It had been justified

1

The principles of financial accounting are termed as very important for any business

entity as it helps in creating ease for perspective of understanding expenses of future. The main

objective is to control cost on basis of its operation which are held in premises. The present

report is giving brief discussion related to regulations and principles of accounting. In the same

series, it had represented its significance of accounting for attaining growth and profitability

which is followed by every industry along with business entity. There report is signifying

importance of depreciation with its both methods. It had also articulated different financial

statements like balance sheet, income statement, trial balance, bank reconciliation statements etc.

Further it had represented suspense account with its important features and it had been compared

with control account.

Report related to financial accounting with its rules and regulations

1. Defining financial accounting with its goal and objectives

It is considered as a particular accounting branch as it helps in tracking financial

statements of any organization in appropriate aspect. The main role of financial accounting has

been specified as measurement, reporting, gathering and recording of transactions related to

investors and shareholders. It is replicated as appropriate source for determining financial

performances of any organization along with its stability. The major concern is of representing it

in very consistent and fair aspect. The financial statement must be prepared by considering

financial standards which are Generally Accepted Accounting Principles and (IFRS)

International Financial reporting standards.

Its goals and objectives are defined with 4 classifications such as:

Reliability

Relevance

Comparability

Consistency

Reliability: The information which is given via statements of financial must be totally

reliable. In the same series, investors would be gaining difficulty for getting information which is

reliable and in its absence it also creates issues for decision making process. It had been justified

1

that information which is reliable does not mislead others because it had been framed by

ignoring bias and its verifications had been framed with ease.

Relevance: The financial information which had been provided must be relevant and

useful for its final users. It also creates ease for understanding and process of decision making

with context of organization's financial performance. The present information is known as very

relevant for giving outcome on yearly and quarterly aspect (Beatty and Liao, 2014).

Comparability: It also helps in creating ease for comparing statement of business entity

to other organization or from previous year statements It also signifies system which had formed

for purpose of financial statements for reporting and recording it in systematic aspect. In same

series, it would be making easy with perspective of investors according to date as it could be

adjusted with decision making process related to investments.

Consistency: There are various changes in standards as it would be creating lack for

process of preparing financial statements with consistence. It is considered as specific reason for

purpose of standards so it would represent its data with proper consistency and in decision

making process it could be used for comparison aspect.

Drafting financial accounting regulations

The information regarding finance must be fair, unbiased, understandable and

comparable. On this basis various regulations with context of financial statements are prepared,

presented and developed. In United Kingdom, the organizations which are listed under FTSE had

to work on standards of GAAP (Generally Accepted Accounting problems) for preparing

financial statements according to its principles. The organization could be expanded on basis of

global market international accounting as it has to follow specific regulations like IFRS and

IASB. Theses accounting regulations could be elaborated as below:

International financial reporting standards (IFRS): In the year 2005 in United

Kingdom it had directly constituted through contribution of financial reporting. It is prepared on

basis of setting different global standards for disclosure and preparation of financial statements.

If there is adaption of single accounting standard for different countries to provide financial

information in consistent aspect. It also creates ease for investors for comparing procedure. In the

same series, it provides guidance rather than setting regulations for financial reporting

(Mullinova, 2016).

2

ignoring bias and its verifications had been framed with ease.

Relevance: The financial information which had been provided must be relevant and

useful for its final users. It also creates ease for understanding and process of decision making

with context of organization's financial performance. The present information is known as very

relevant for giving outcome on yearly and quarterly aspect (Beatty and Liao, 2014).

Comparability: It also helps in creating ease for comparing statement of business entity

to other organization or from previous year statements It also signifies system which had formed

for purpose of financial statements for reporting and recording it in systematic aspect. In same

series, it would be making easy with perspective of investors according to date as it could be

adjusted with decision making process related to investments.

Consistency: There are various changes in standards as it would be creating lack for

process of preparing financial statements with consistence. It is considered as specific reason for

purpose of standards so it would represent its data with proper consistency and in decision

making process it could be used for comparison aspect.

Drafting financial accounting regulations

The information regarding finance must be fair, unbiased, understandable and

comparable. On this basis various regulations with context of financial statements are prepared,

presented and developed. In United Kingdom, the organizations which are listed under FTSE had

to work on standards of GAAP (Generally Accepted Accounting problems) for preparing

financial statements according to its principles. The organization could be expanded on basis of

global market international accounting as it has to follow specific regulations like IFRS and

IASB. Theses accounting regulations could be elaborated as below:

International financial reporting standards (IFRS): In the year 2005 in United

Kingdom it had directly constituted through contribution of financial reporting. It is prepared on

basis of setting different global standards for disclosure and preparation of financial statements.

If there is adaption of single accounting standard for different countries to provide financial

information in consistent aspect. It also creates ease for investors for comparing procedure. In the

same series, it provides guidance rather than setting regulations for financial reporting

(Mullinova, 2016).

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

International accounting standards board (IASB): The main goal of IASB is to

disclose each financial information to its professionals. It also helps in giving guidelines for

objective of preparing reports and database for preparing financial statements. The accounts

could be evaluated from this standard. There is presence of acceptance of legal structure through

stakeholders and for determining financial information which would directly influence investors

on basis of various countries.

Accounting principles and rules for governing financial statements

There is presence of various rules, principles and concepts for objective of financial

reports for application of accounting. There is presence of various rules and concepts which are

justified below:

Business Entity: In this concept, financial statements would not be using any personal

transactions with reference to owner. Business is referred as separate entity with its

particular owner.

Matching principle: All revenues and expenses must be similar in accounting duration

for extracting its earnings of actual concept.

Consistency: The process of accounting must be used for business perspective as it

should be similar and consistent with huge necessity of its changes.

Objectivity: There should be appropriate recording of its particular amount with context

of financial statements as it should also give proper evidence on impartial basis.

Materiality: In this principle, accounting process would be justifying impact on decision

of user for attaining significance and need for reporting in proper aspect.

Historical cost: The valuation of asset which is mentioned in financial statement with

reference to its original value but not recorded on its current value of market.

Monetary unit: The amount must be recorded on monetarism aspect and if its presence

in vice versa format then it would be not considered in financial statements.

Going concern:There is always an assumption with context of organization about its

continuity and it would be performed in specific indefinite duration (Pointer, Pointer Ivan

Andrew, 2011).

Accounting period: It would be signifying process of accounting in given duration on

basis of half year, quarterly and fiscal year.

3

disclose each financial information to its professionals. It also helps in giving guidelines for

objective of preparing reports and database for preparing financial statements. The accounts

could be evaluated from this standard. There is presence of acceptance of legal structure through

stakeholders and for determining financial information which would directly influence investors

on basis of various countries.

Accounting principles and rules for governing financial statements

There is presence of various rules, principles and concepts for objective of financial

reports for application of accounting. There is presence of various rules and concepts which are

justified below:

Business Entity: In this concept, financial statements would not be using any personal

transactions with reference to owner. Business is referred as separate entity with its

particular owner.

Matching principle: All revenues and expenses must be similar in accounting duration

for extracting its earnings of actual concept.

Consistency: The process of accounting must be used for business perspective as it

should be similar and consistent with huge necessity of its changes.

Objectivity: There should be appropriate recording of its particular amount with context

of financial statements as it should also give proper evidence on impartial basis.

Materiality: In this principle, accounting process would be justifying impact on decision

of user for attaining significance and need for reporting in proper aspect.

Historical cost: The valuation of asset which is mentioned in financial statement with

reference to its original value but not recorded on its current value of market.

Monetary unit: The amount must be recorded on monetarism aspect and if its presence

in vice versa format then it would be not considered in financial statements.

Going concern:There is always an assumption with context of organization about its

continuity and it would be performed in specific indefinite duration (Pointer, Pointer Ivan

Andrew, 2011).

Accounting period: It would be signifying process of accounting in given duration on

basis of half year, quarterly and fiscal year.

3

Conservatism: It would be signifying two particular amounts with reference to business

transaction as it would be directly considering its financial statements.

Elaborating various concepts of accounting which are disclosure, materiality and consistency

Full Disclosure principle: It is indirectly related to concept of materiality as it has huge

necessity for disclosing its every detail about financial like policies of accounting related

to its financial statements. There is attainment of knowledge with reference to its

creditors and investors as well with reference to business entity's operation on specific

accounting basis. It also helps in justifying changes of decision with reference to its user

on external basis related to particular business entity with its disclosure. It would be

directly ensuring about deficiency in information as it would not mislead any of financial

statements.

Materiality: The concept of accounting always signifies that it should always disclose

each thing as it creates very efficiency for its users. The business entity had gained

importance related to its items as it had gained importance to other business entity.

Different items had given significance to any other business entity which must be

avoided due to not providing any effect on its financials. This accounting concepts is

termed as very important as it helps accountants and auditors for decision making process

with reference to its classification about immaterial or material.

Consistency: It is known as very significant measure for purpose of accounting process

as it must be very consistent for specific financial duration to any other. If these

techniques could be altered, then it would justify its changes in techniques for disclosing

true performance related to financial statements. It is termed as very important measure

for comparison aspect from statement of past year. The policies of accounting must be

changed with techniques as it would directly replicate in stability and performance of any

business entity (Sharma and Panigrahi, 2013).

CLIENT 1

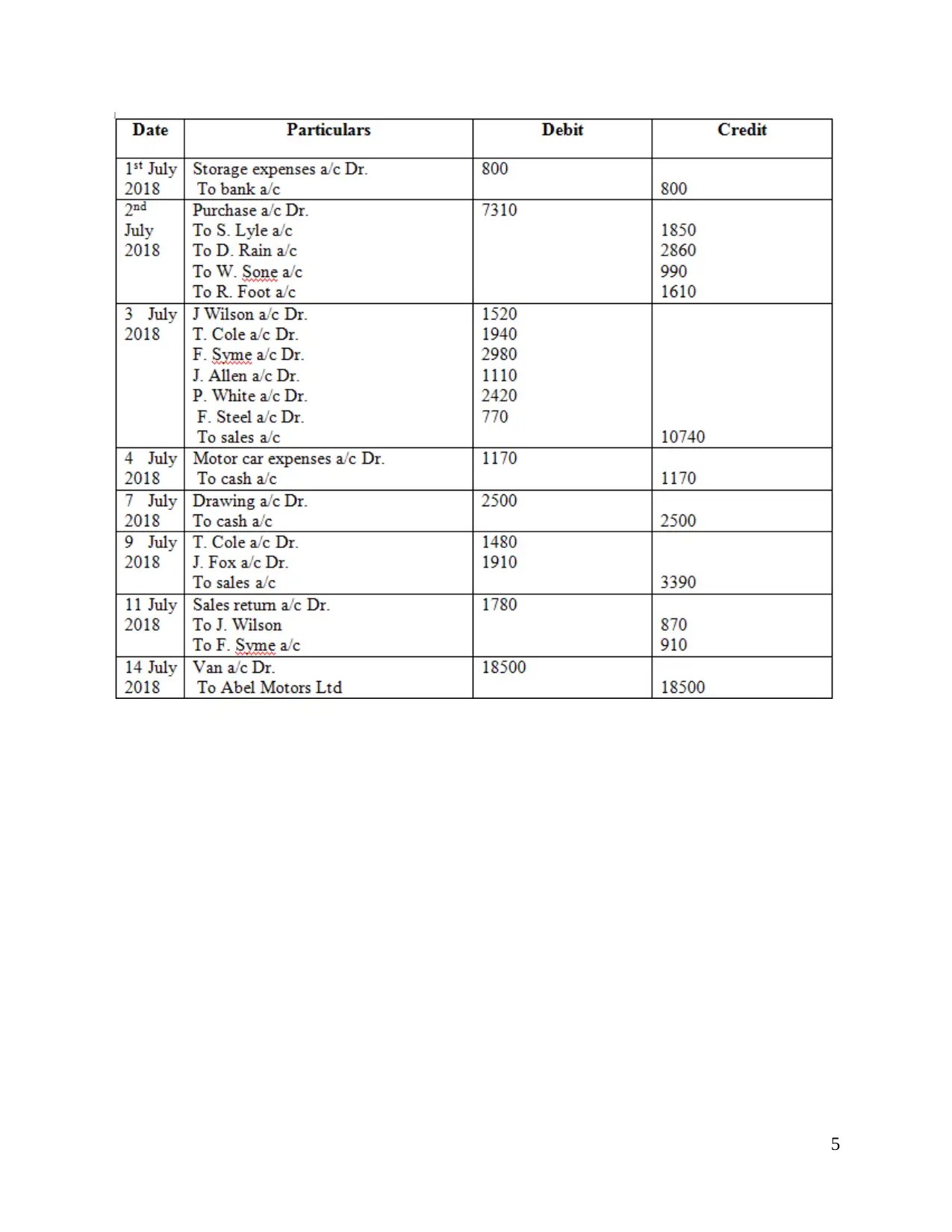

1. Justifying its journal entries

There is representation of journal entries with context of given transactions. It would be

altering its entries which are termed as very significant for business related to sales and purchase

are stated below:

4

transaction as it would be directly considering its financial statements.

Elaborating various concepts of accounting which are disclosure, materiality and consistency

Full Disclosure principle: It is indirectly related to concept of materiality as it has huge

necessity for disclosing its every detail about financial like policies of accounting related

to its financial statements. There is attainment of knowledge with reference to its

creditors and investors as well with reference to business entity's operation on specific

accounting basis. It also helps in justifying changes of decision with reference to its user

on external basis related to particular business entity with its disclosure. It would be

directly ensuring about deficiency in information as it would not mislead any of financial

statements.

Materiality: The concept of accounting always signifies that it should always disclose

each thing as it creates very efficiency for its users. The business entity had gained

importance related to its items as it had gained importance to other business entity.

Different items had given significance to any other business entity which must be

avoided due to not providing any effect on its financials. This accounting concepts is

termed as very important as it helps accountants and auditors for decision making process

with reference to its classification about immaterial or material.

Consistency: It is known as very significant measure for purpose of accounting process

as it must be very consistent for specific financial duration to any other. If these

techniques could be altered, then it would justify its changes in techniques for disclosing

true performance related to financial statements. It is termed as very important measure

for comparison aspect from statement of past year. The policies of accounting must be

changed with techniques as it would directly replicate in stability and performance of any

business entity (Sharma and Panigrahi, 2013).

CLIENT 1

1. Justifying its journal entries

There is representation of journal entries with context of given transactions. It would be

altering its entries which are termed as very significant for business related to sales and purchase

are stated below:

4

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

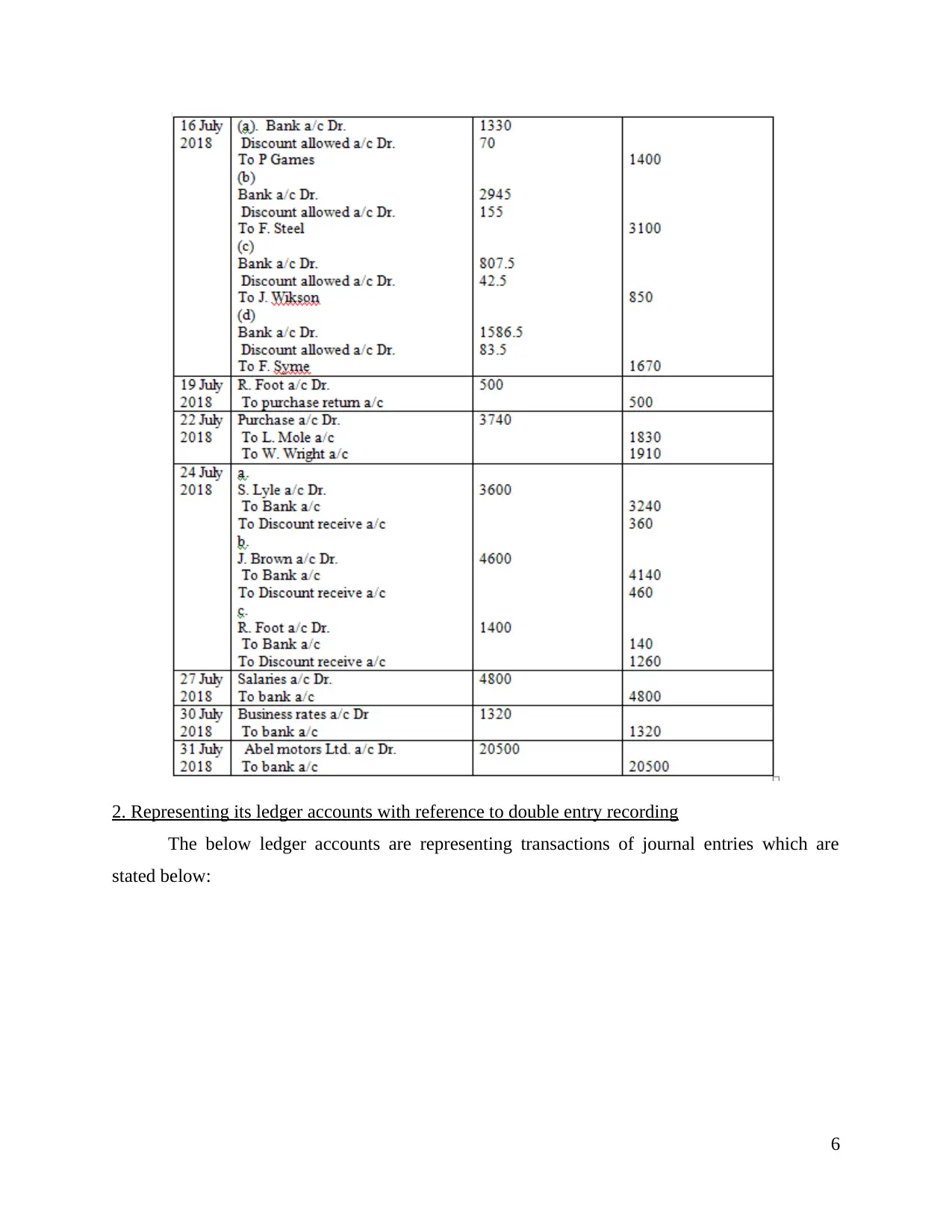

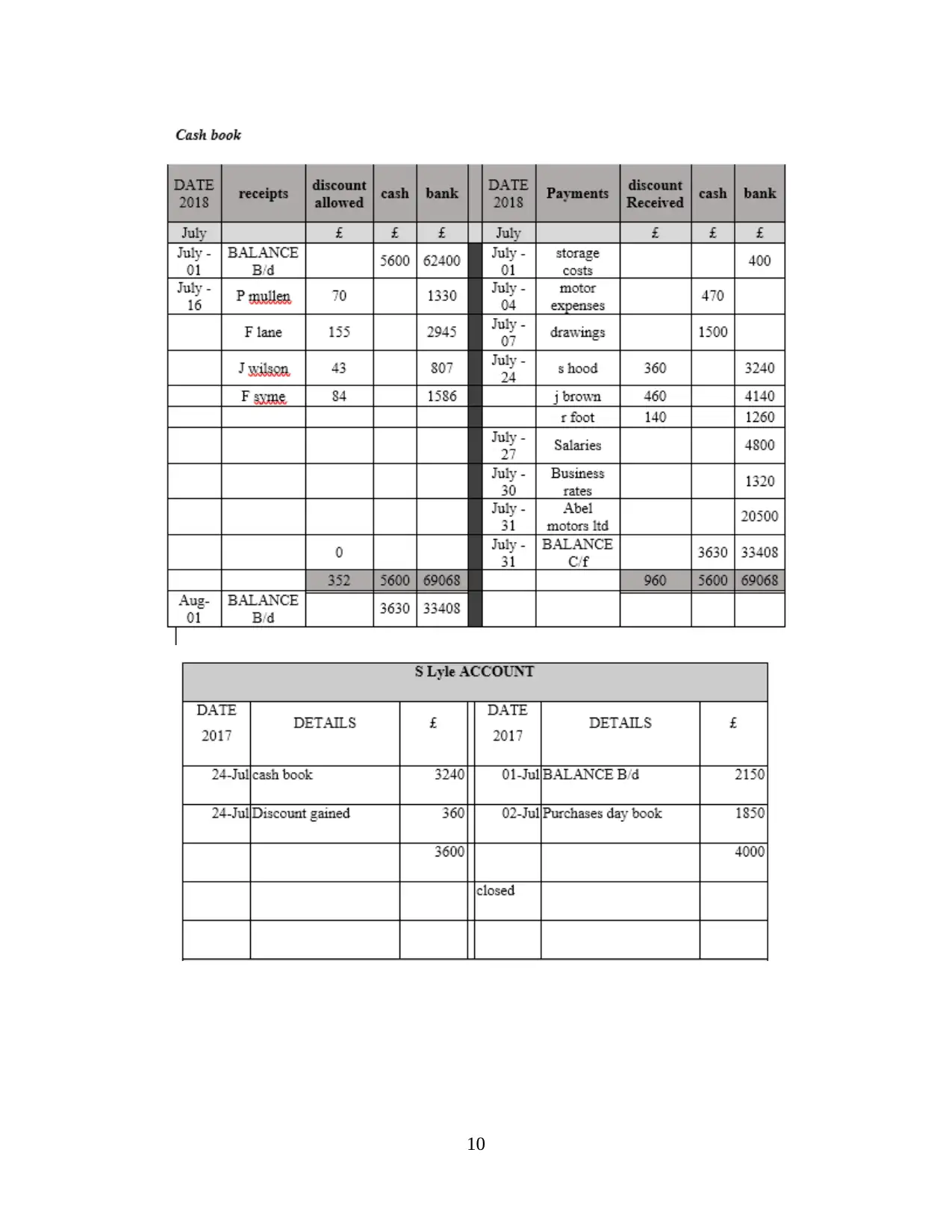

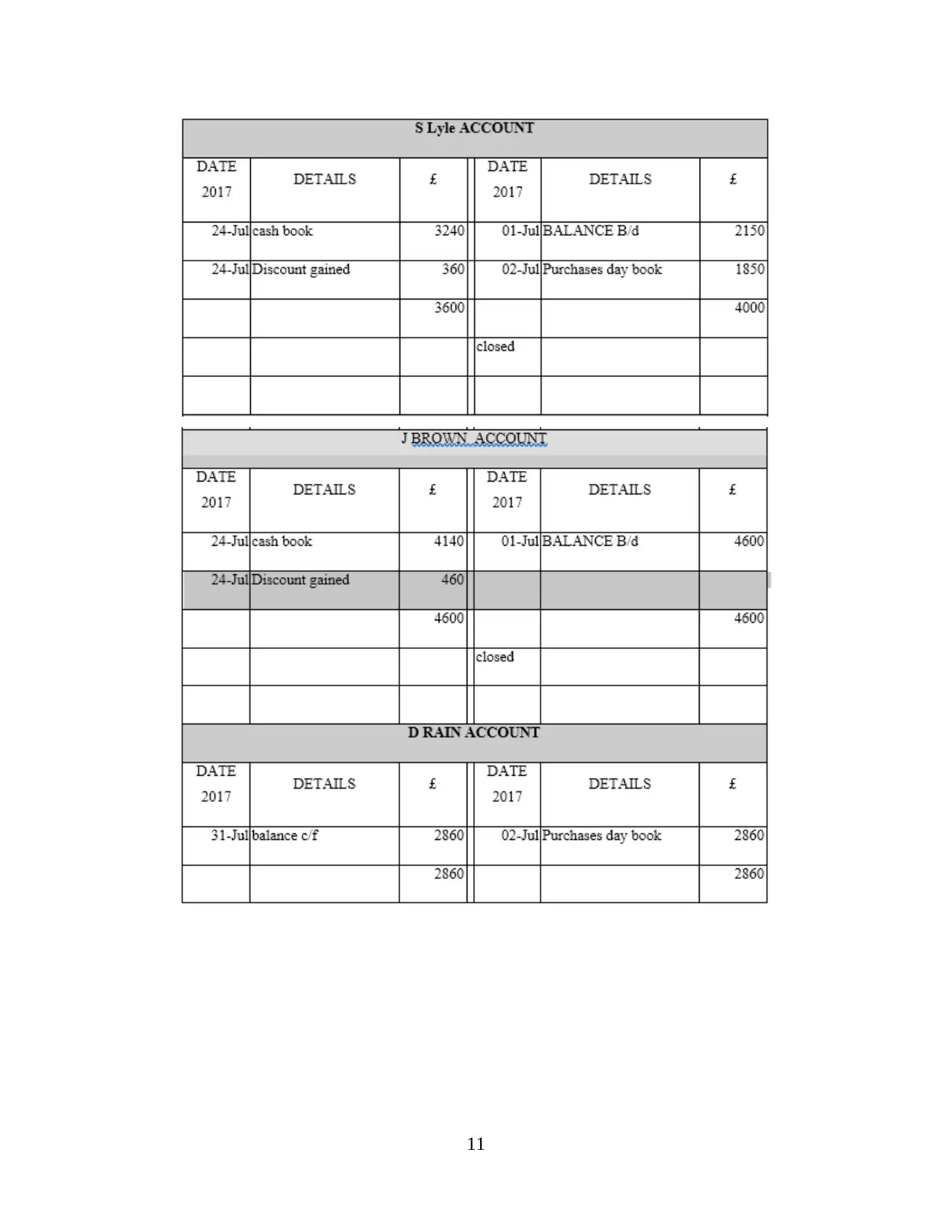

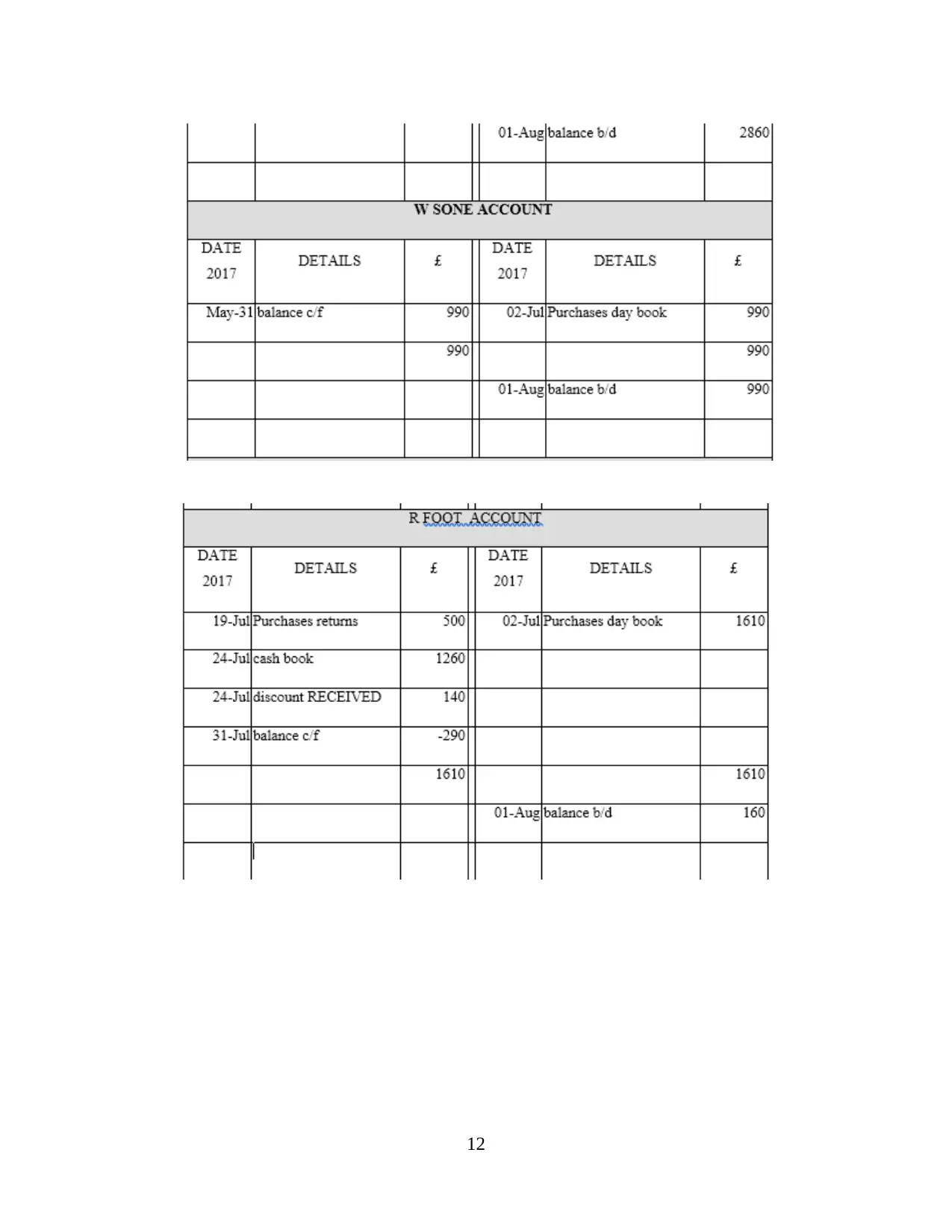

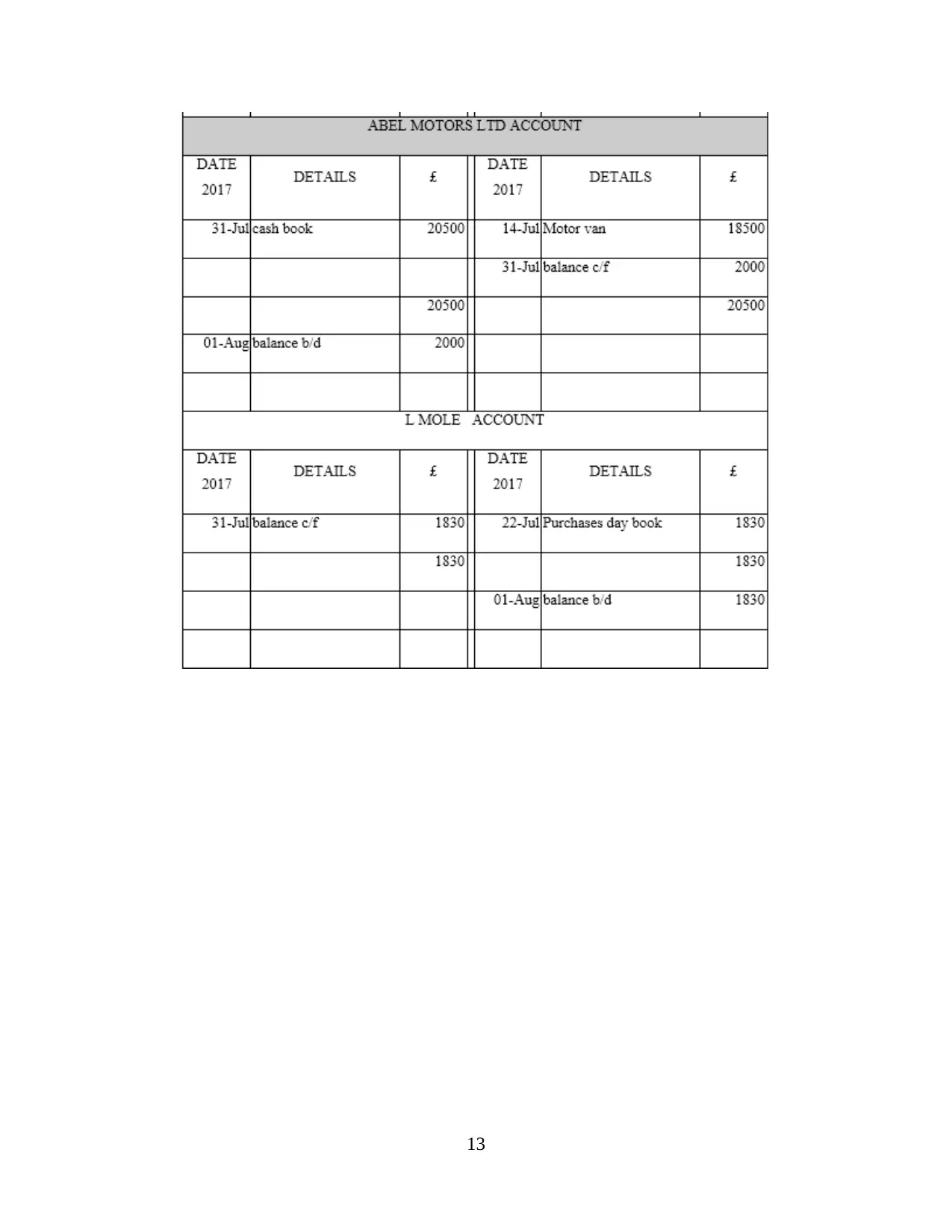

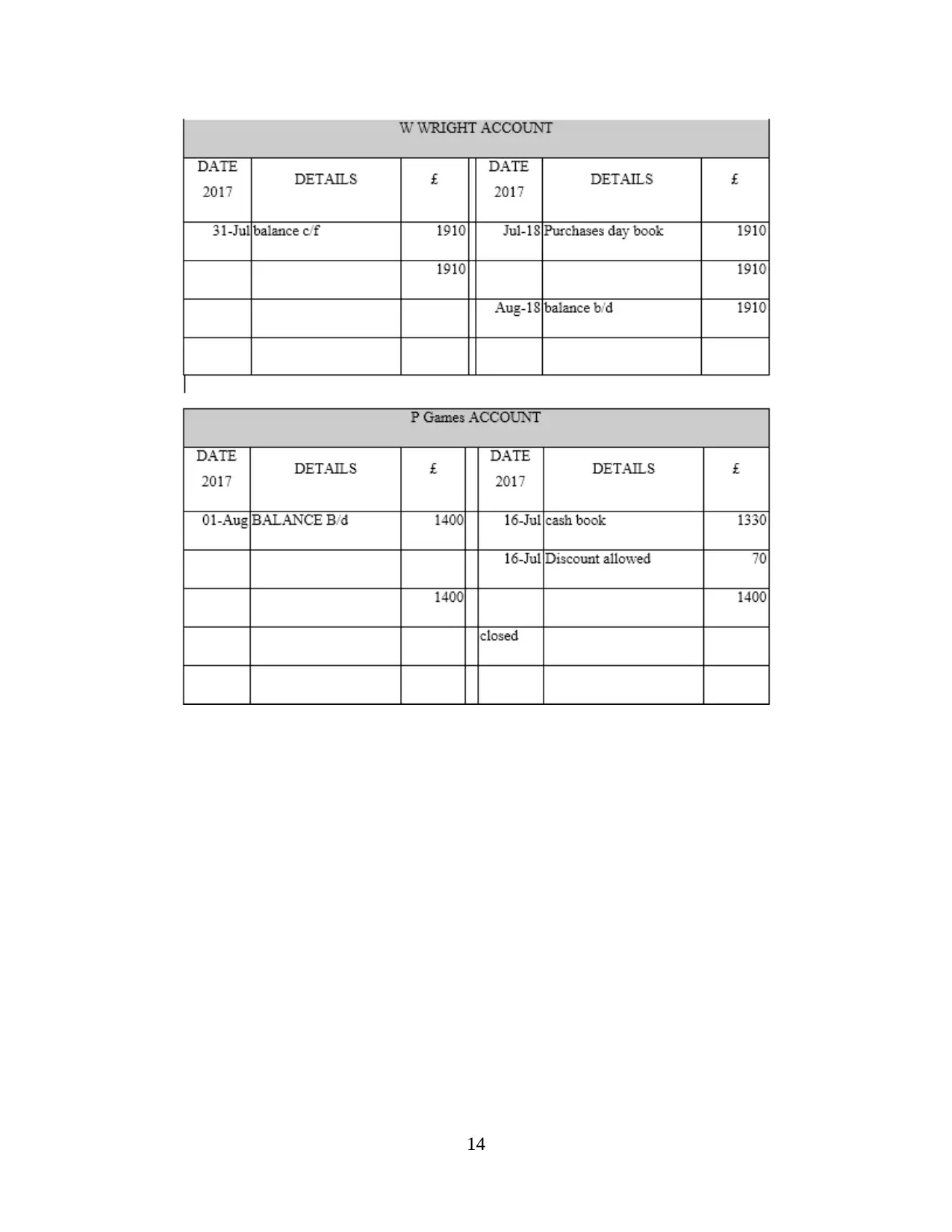

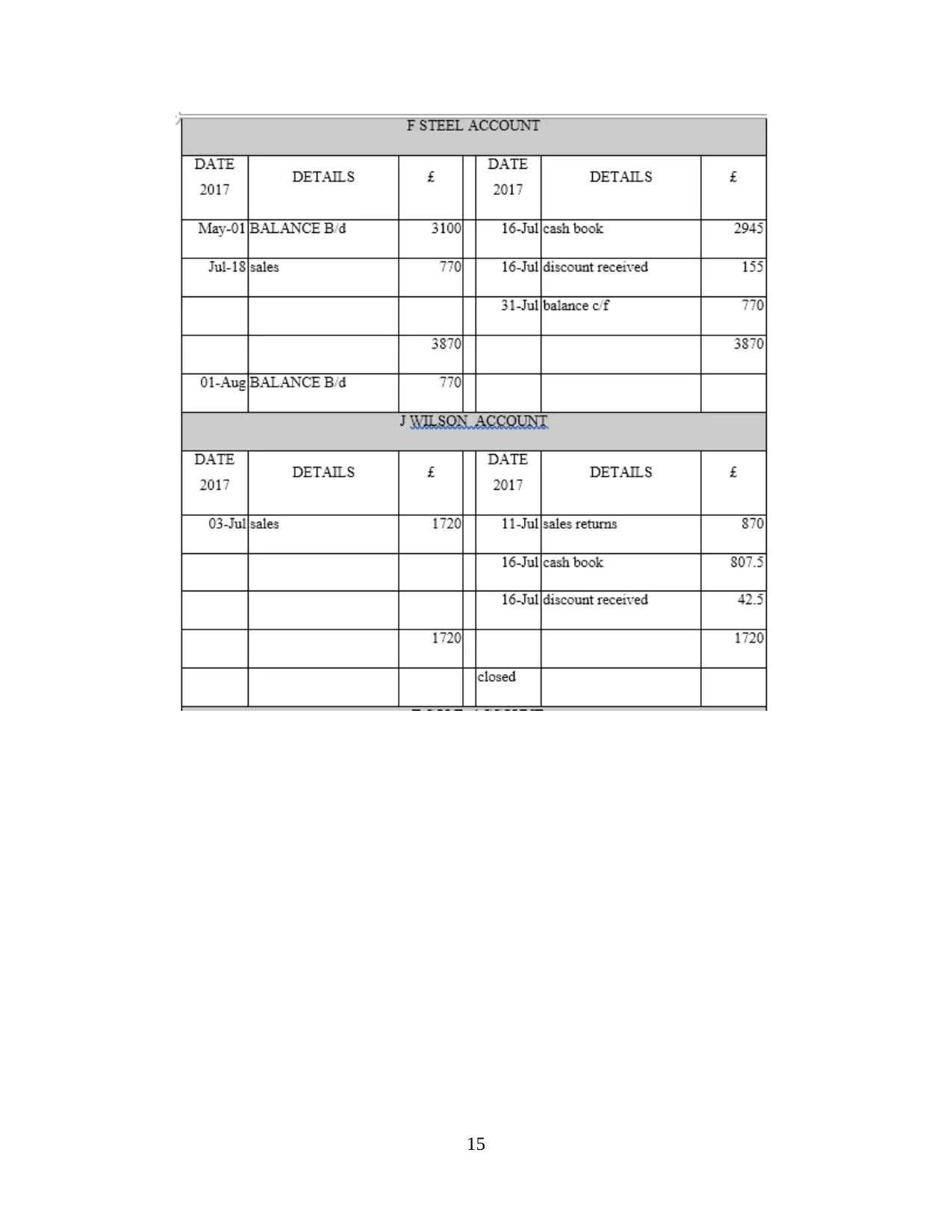

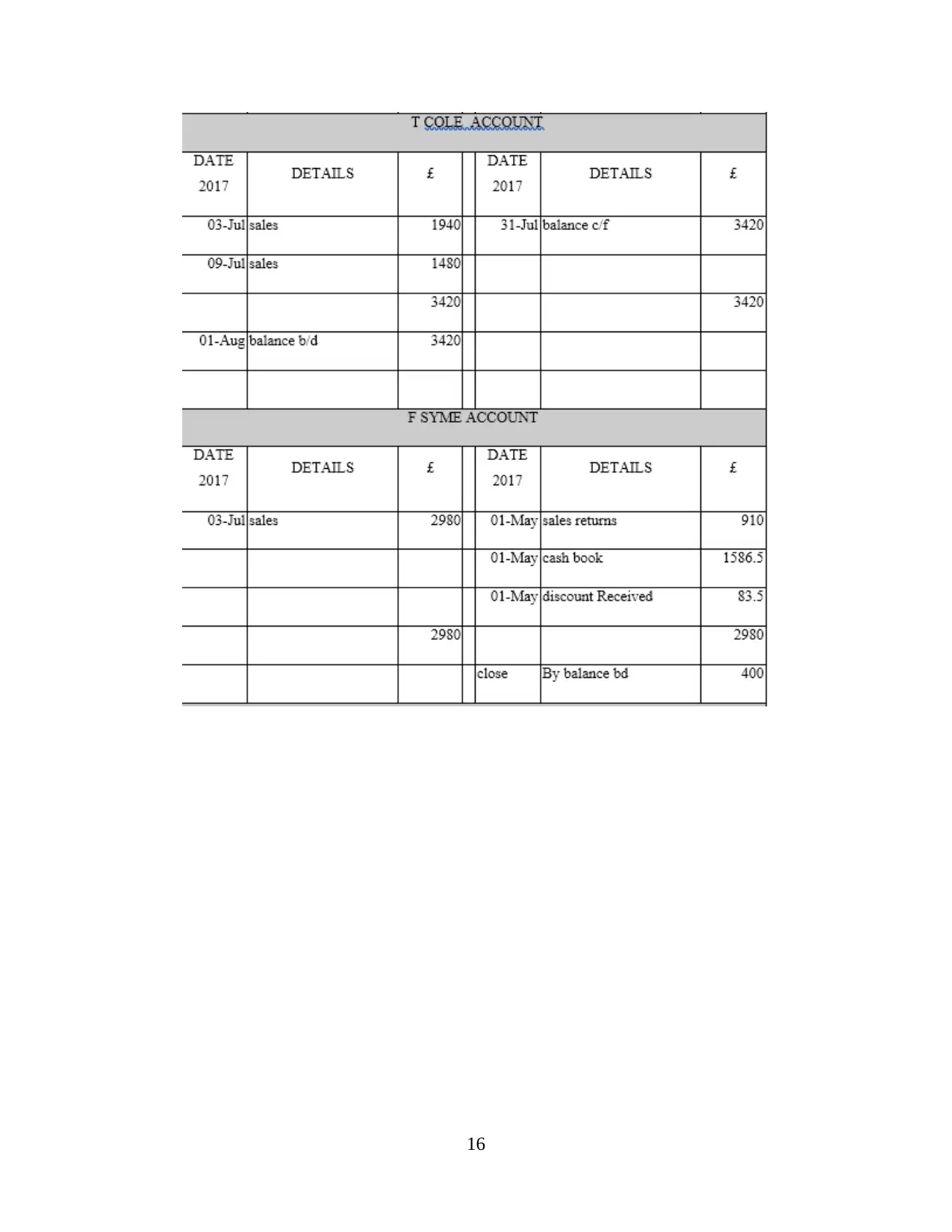

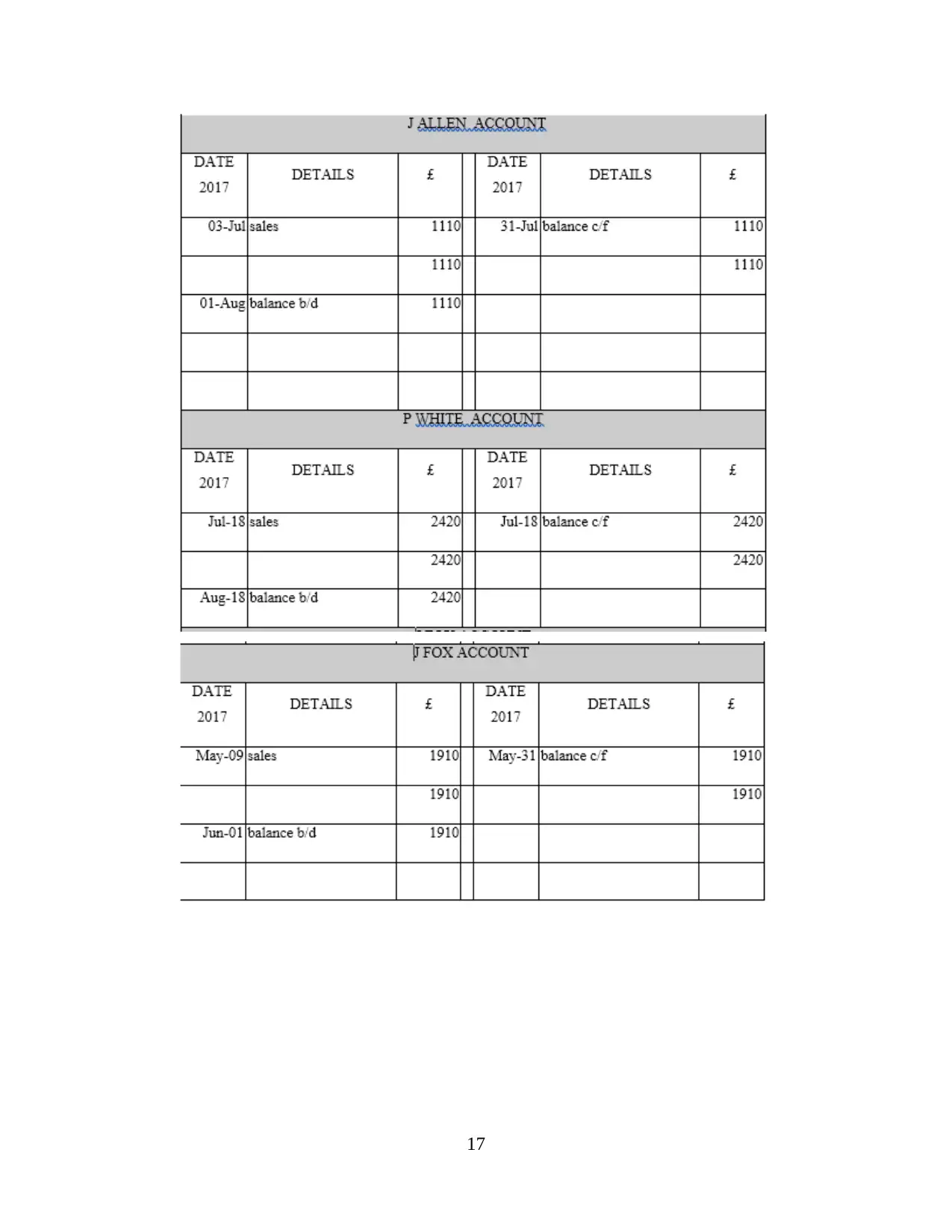

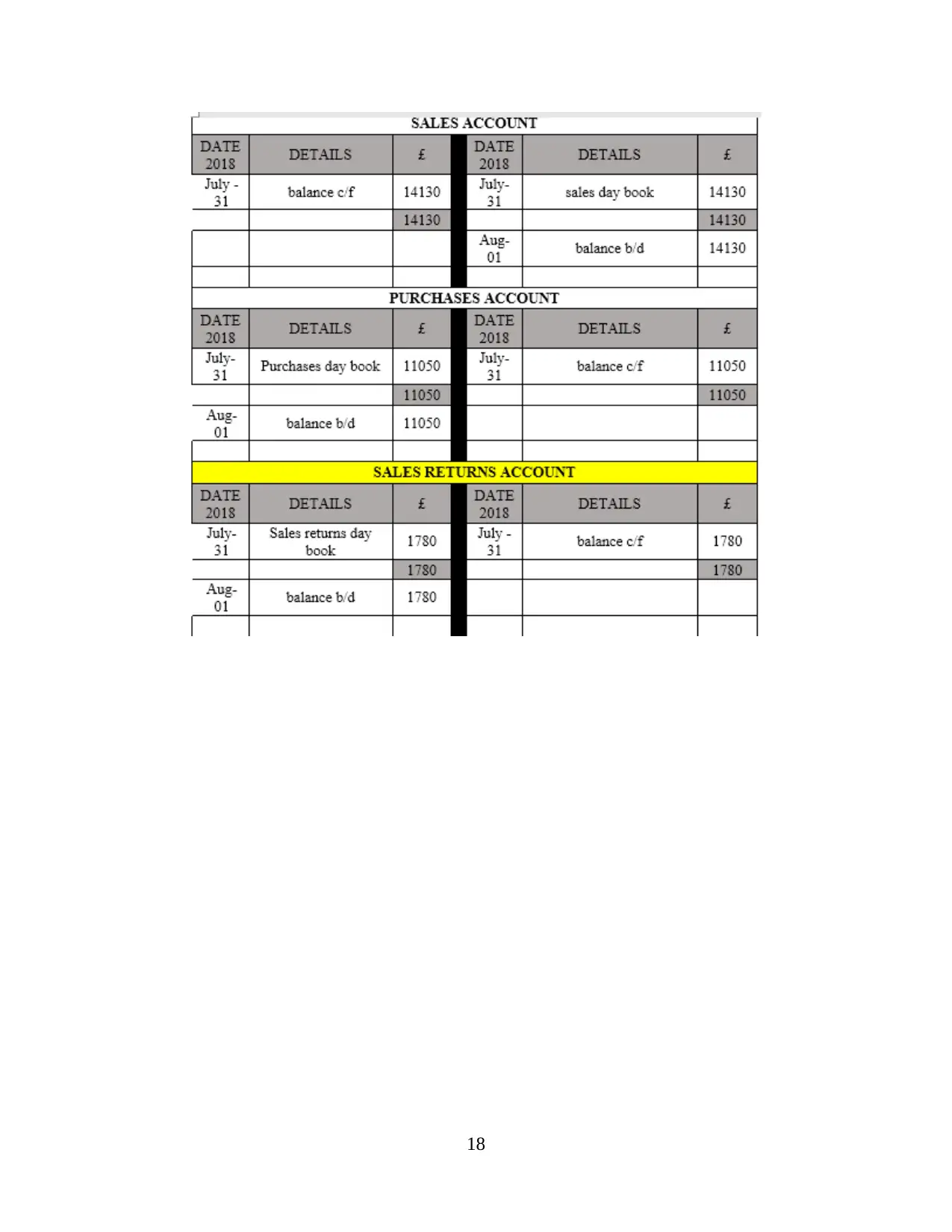

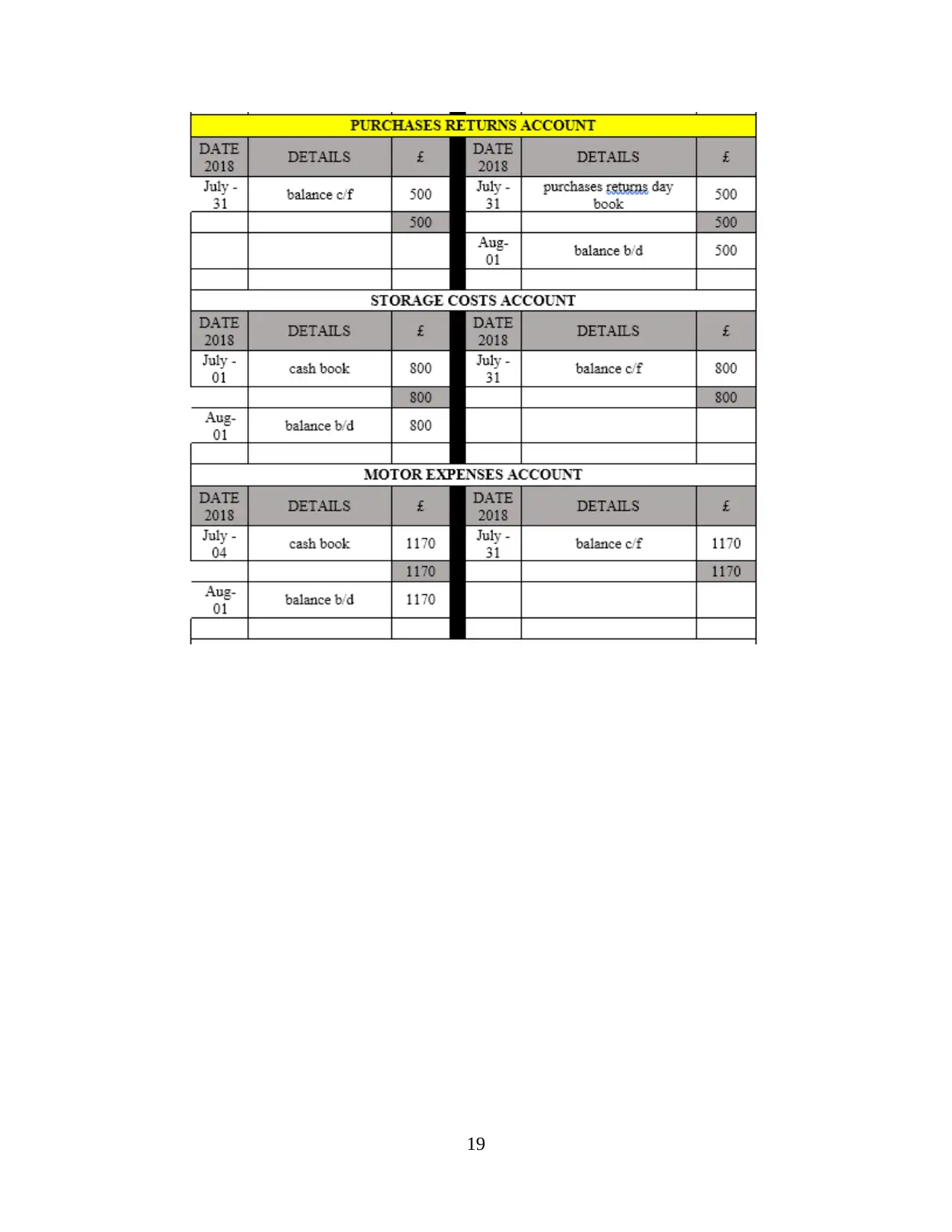

2. Representing its ledger accounts with reference to double entry recording

The below ledger accounts are representing transactions of journal entries which are

stated below:

6

The below ledger accounts are representing transactions of journal entries which are

stated below:

6

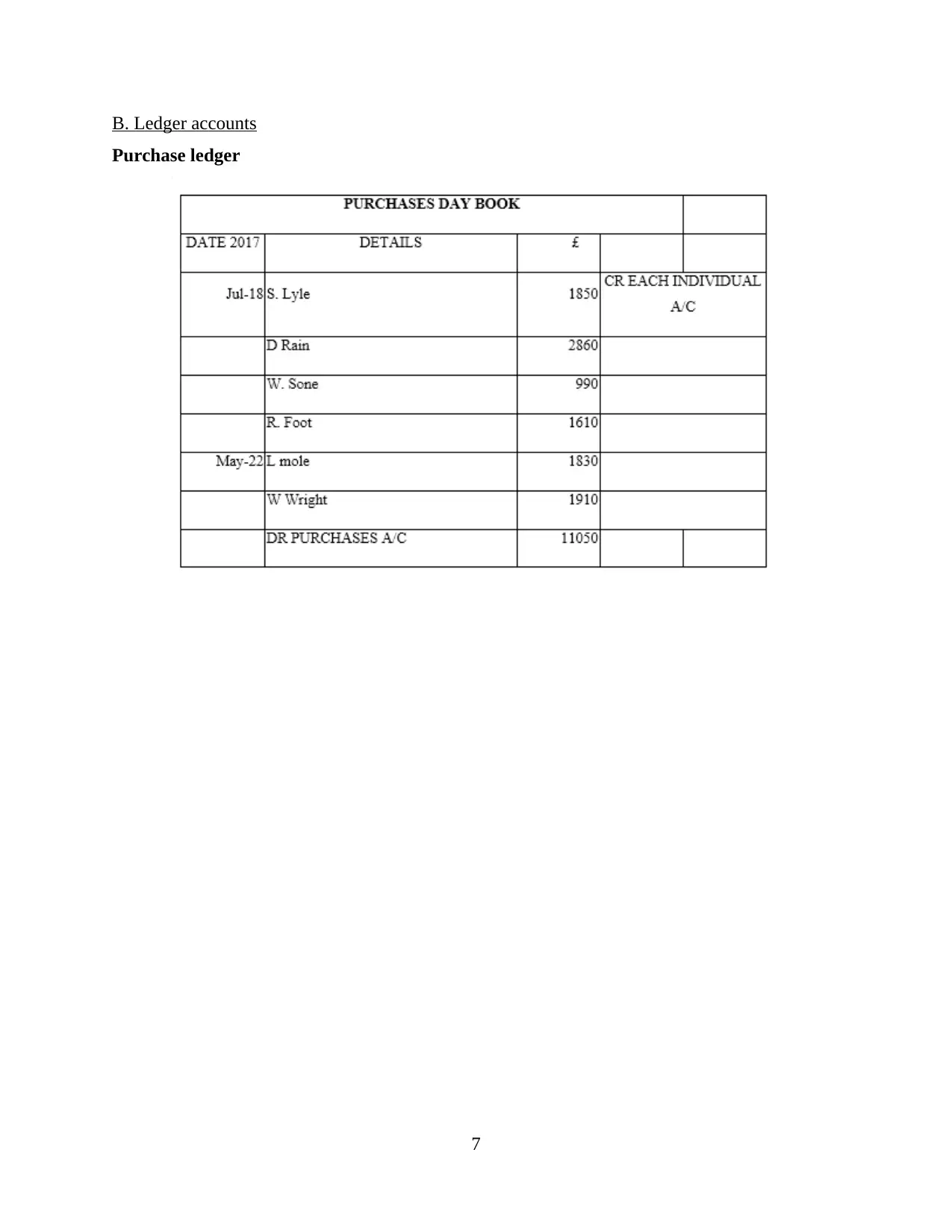

B. Ledger accounts

Purchase ledger

7

Purchase ledger

7

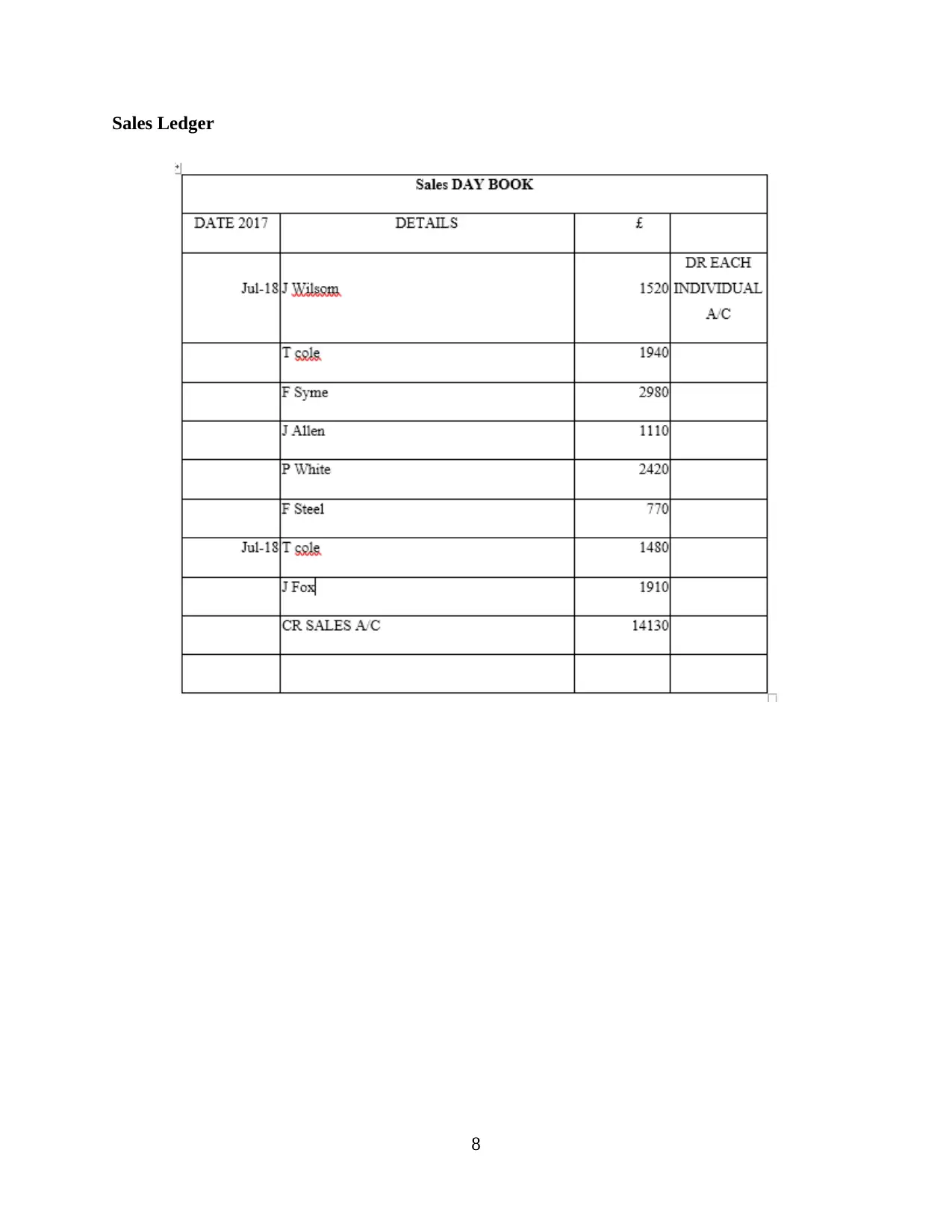

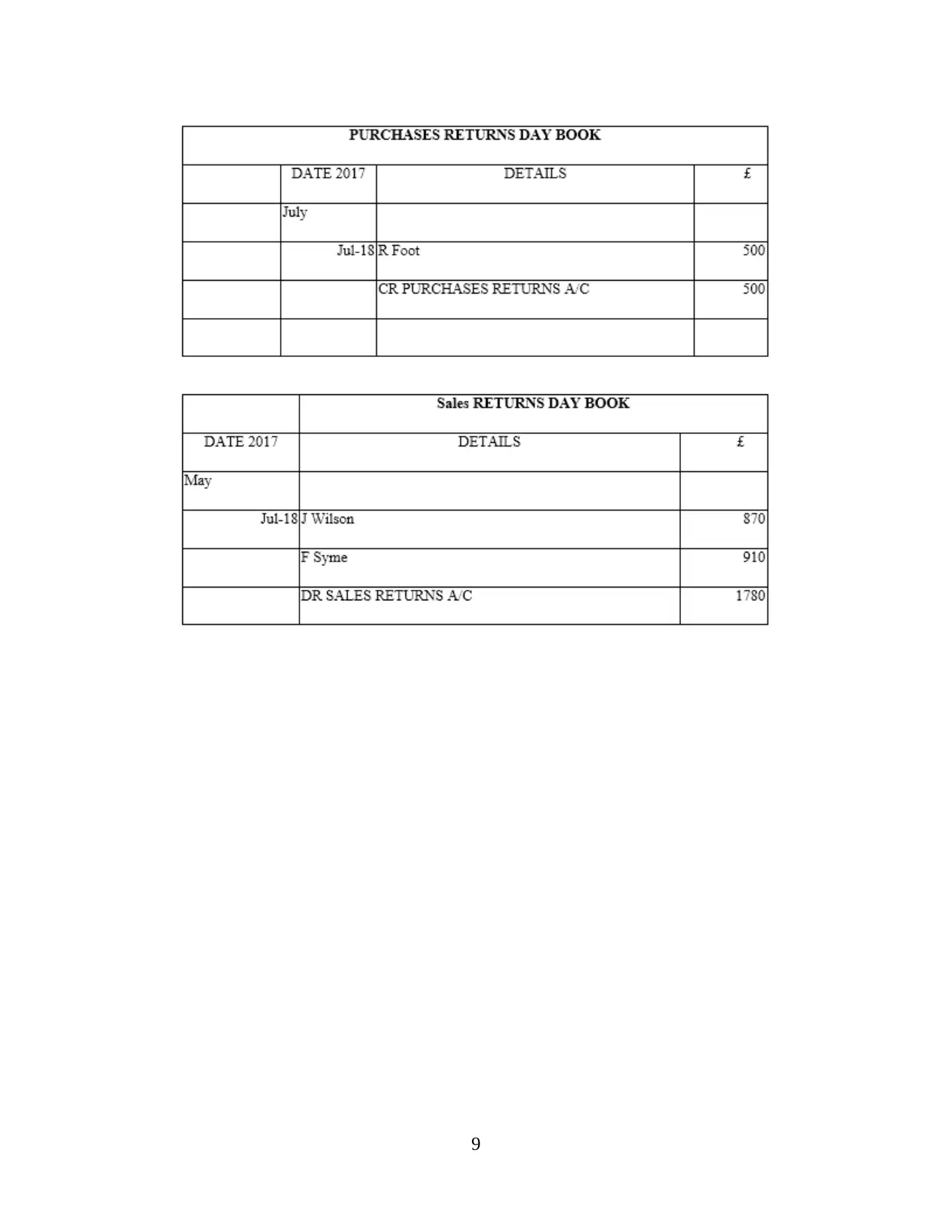

Sales Ledger

8

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

9

10

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

12

13

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

15

16

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

18

19

20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

21

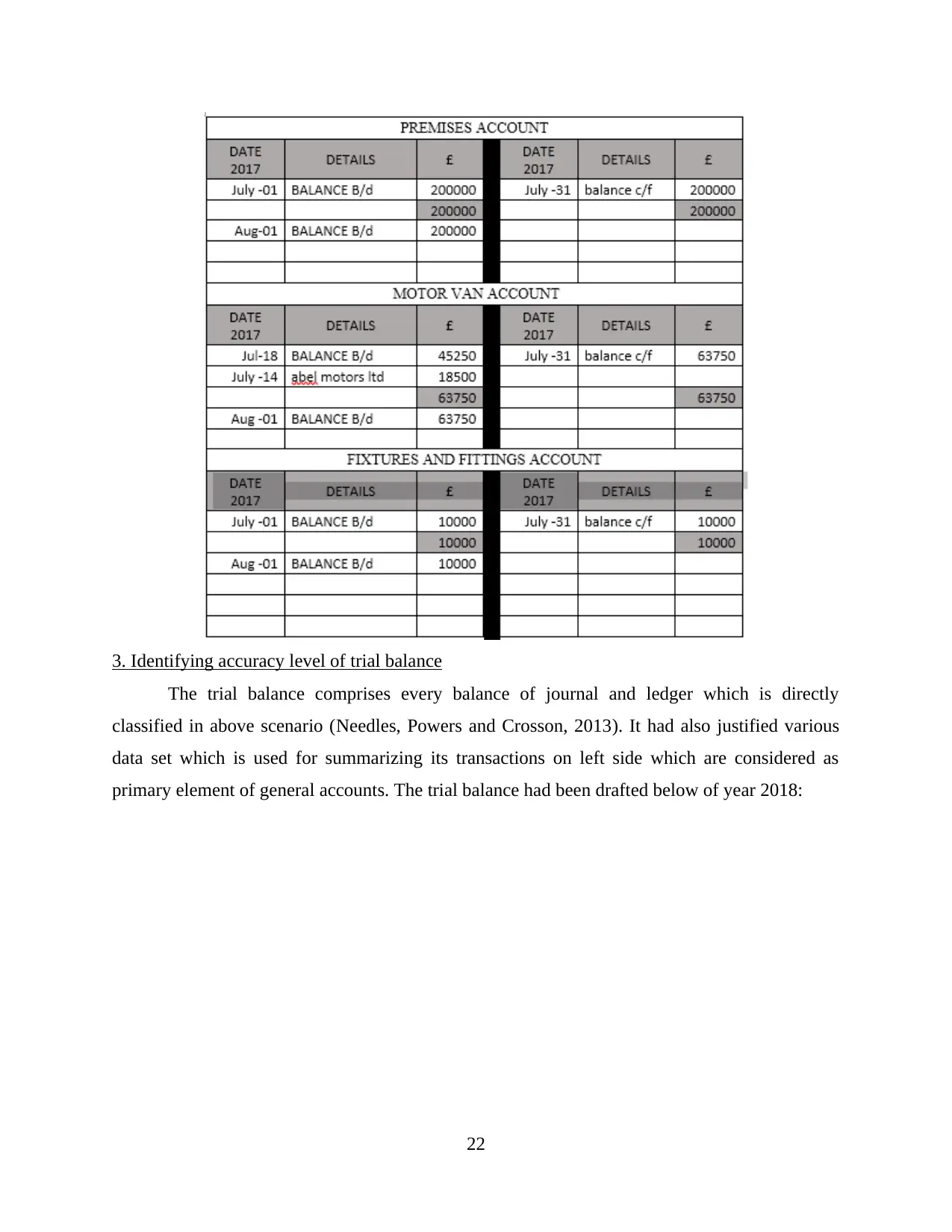

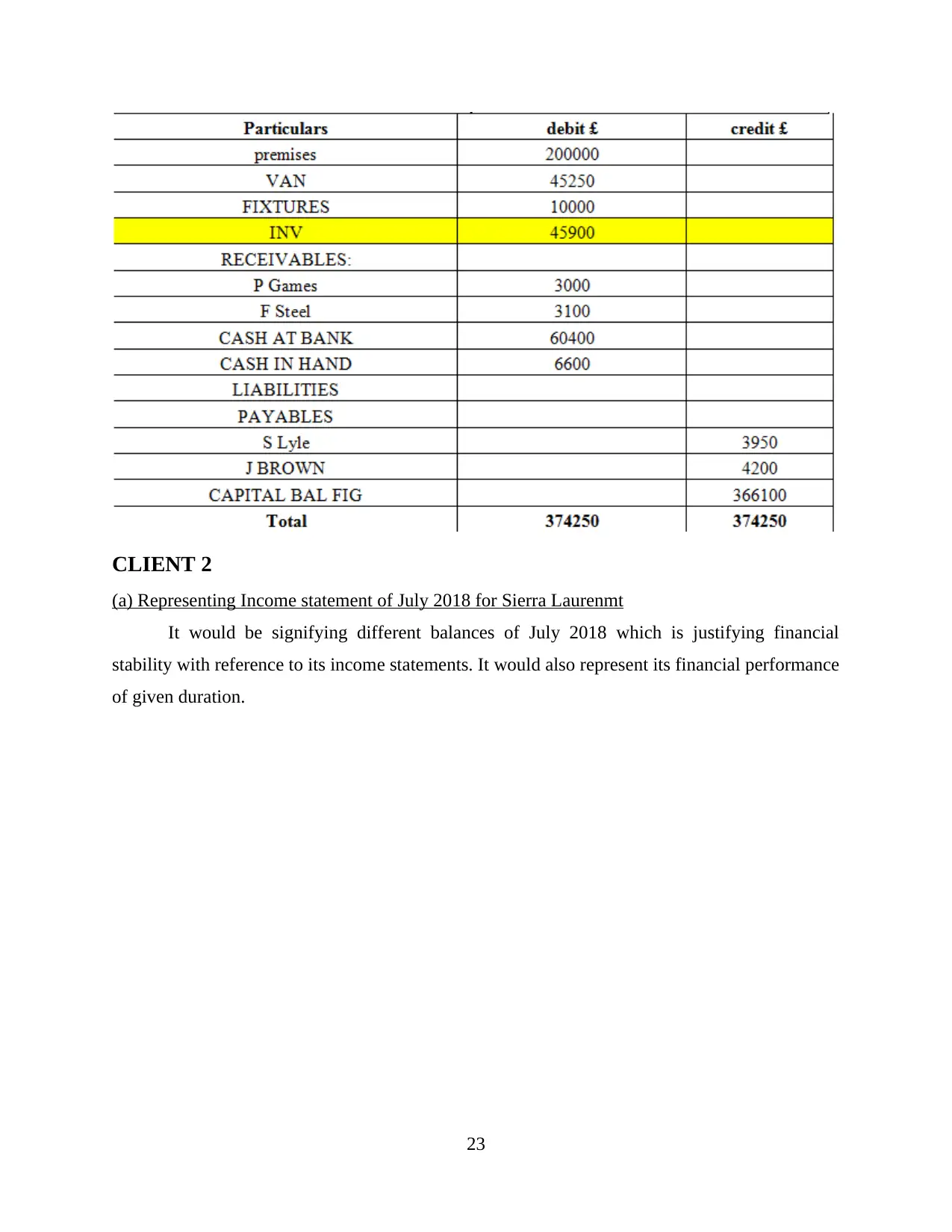

3. Identifying accuracy level of trial balance

The trial balance comprises every balance of journal and ledger which is directly

classified in above scenario (Needles, Powers and Crosson, 2013). It had also justified various

data set which is used for summarizing its transactions on left side which are considered as

primary element of general accounts. The trial balance had been drafted below of year 2018:

22

The trial balance comprises every balance of journal and ledger which is directly

classified in above scenario (Needles, Powers and Crosson, 2013). It had also justified various

data set which is used for summarizing its transactions on left side which are considered as

primary element of general accounts. The trial balance had been drafted below of year 2018:

22

CLIENT 2

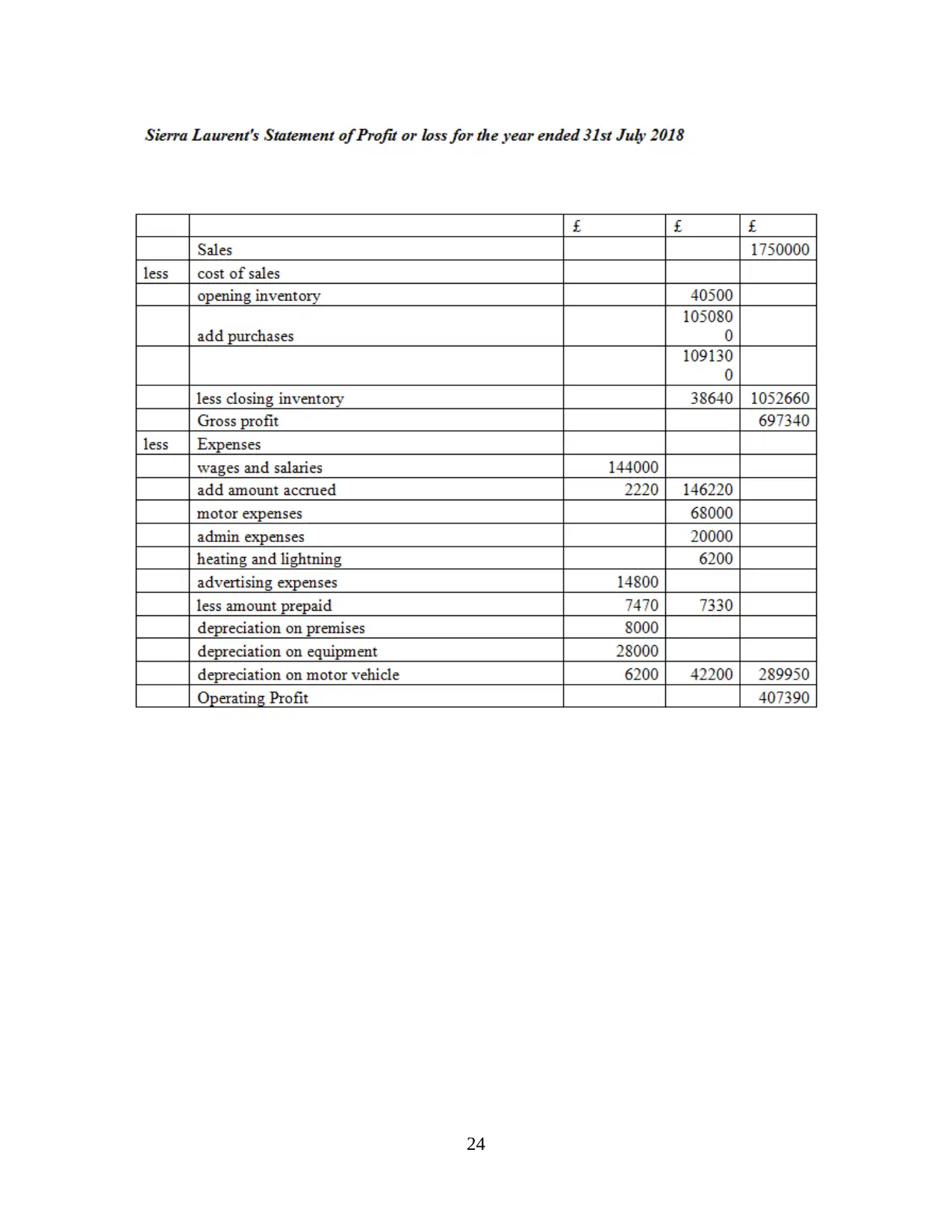

(a) Representing Income statement of July 2018 for Sierra Laurenmt

It would be signifying different balances of July 2018 which is justifying financial

stability with reference to its income statements. It would also represent its financial performance

of given duration.

23

(a) Representing Income statement of July 2018 for Sierra Laurenmt

It would be signifying different balances of July 2018 which is justifying financial

stability with reference to its income statements. It would also represent its financial performance

of given duration.

23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

24

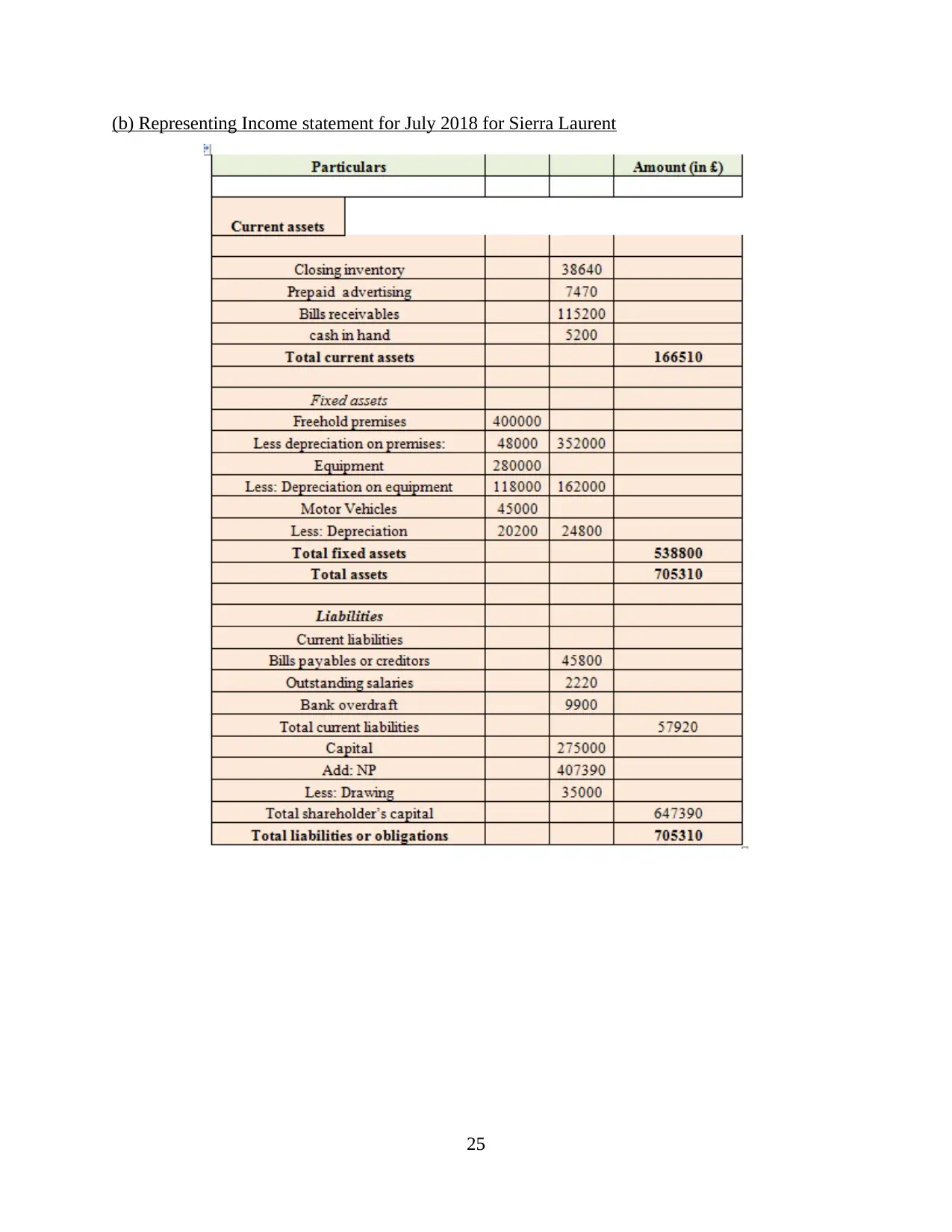

(b) Representing Income statement for July 2018 for Sierra Laurent

25

25

CLIENT 3

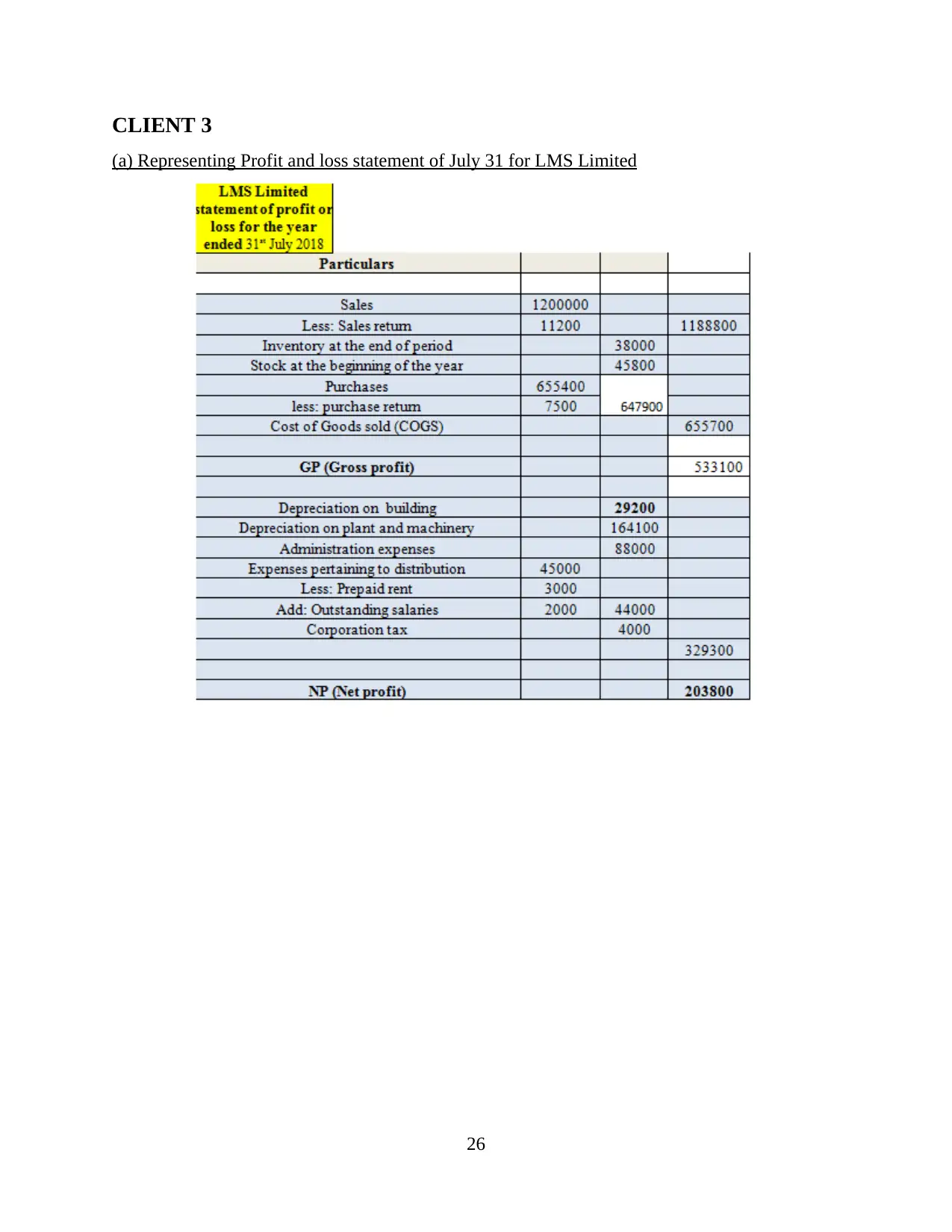

(a) Representing Profit and loss statement of July 31 for LMS Limited

26

(a) Representing Profit and loss statement of July 31 for LMS Limited

26

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

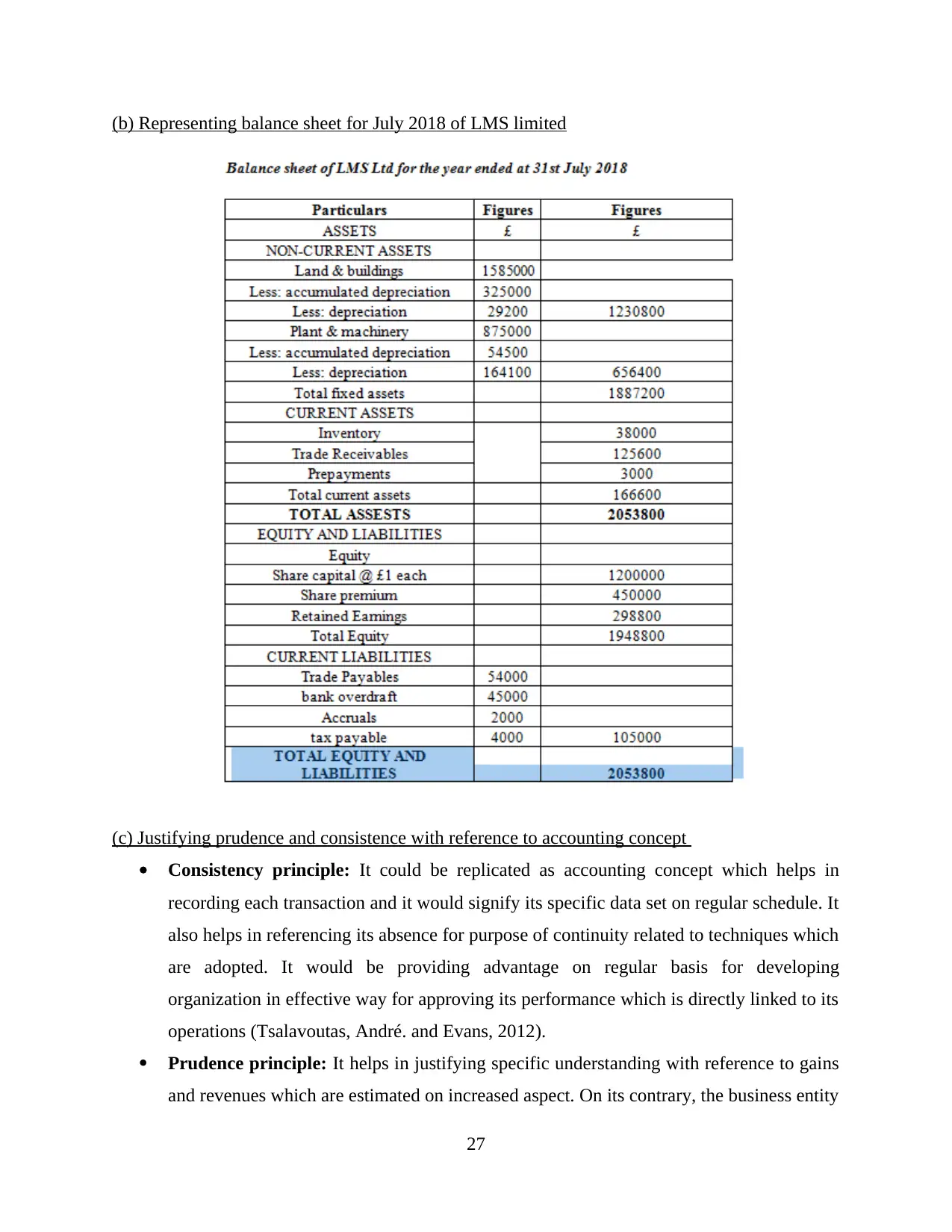

(b) Representing balance sheet for July 2018 of LMS limited

(c) Justifying prudence and consistence with reference to accounting concept

Consistency principle: It could be replicated as accounting concept which helps in

recording each transaction and it would signify its specific data set on regular schedule. It

also helps in referencing its absence for purpose of continuity related to techniques which

are adopted. It would be providing advantage on regular basis for developing

organization in effective way for approving its performance which is directly linked to its

operations (Tsalavoutas, André. and Evans, 2012).

Prudence principle: It helps in justifying specific understanding with reference to gains

and revenues which are estimated on increased aspect. On its contrary, the business entity

27

(c) Justifying prudence and consistence with reference to accounting concept

Consistency principle: It could be replicated as accounting concept which helps in

recording each transaction and it would signify its specific data set on regular schedule. It

also helps in referencing its absence for purpose of continuity related to techniques which

are adopted. It would be providing advantage on regular basis for developing

organization in effective way for approving its performance which is directly linked to its

operations (Tsalavoutas, André. and Evans, 2012).

Prudence principle: It helps in justifying specific understanding with reference to gains

and revenues which are estimated on increased aspect. On its contrary, the business entity

27

gives the least attention to its expenses along with its liability as well. In the same series,

if disclosures related to finance are represented then it would be performed via

conservatism as it gives relevancy factor. According to this technique, different

assumptions should be undertaken with context of specific level of increment along with

business entity's capacity and liabilities for attaining meetings with reference to debt of

particular business.

(d) Representing motive of depreciation for accounting aspect with reference to its each method

Depreciation has its major applications in every business entity. It could be stated as fall

in value of any particular asset. These assets could justify as computer, machinery or plant etc.

are purchased for duration of long term as it would help in extracting its net value for every year.

If there is consideration of any life span, then its value will decrease. This particular scenario is

replicated on mandatory aspect for tracing depreciation value with reference to its accounts. It

would be justifying its depreciation value of particular asset. In the same series, it would directly

exclude its salvage value from earned money with motive of selling asset from its actual cost.

The basic elements are useful life, historical cost and salvage value as it is extracted by methods

which are Straight line and Written down value method. It would signify its importance in below

stated manner:

The historical cost of specific asset had been reduced with uses of straight line method.

The original value of asset had been traced in end of each financial year.

While considering written down value it helps in comparing with loss and profit which

are estimated with context of sale.

There should be proper review about information for purpose of asset replacement with

context of written down value.

The business entity could not applicable method of depreciation as it would bear loss

during transaction which had been incurred for earning good profit with reference to

financial result (Dung, 2016).

CLIENT 4

A. Representing objective of preparing Bank Reconciliation Statement (BRS)

The statement of Bank Reconciliation is prepared for justifying differences in its bank

records and BRS. With reference to perspective of accounting, it is considered as very basic

28

if disclosures related to finance are represented then it would be performed via

conservatism as it gives relevancy factor. According to this technique, different

assumptions should be undertaken with context of specific level of increment along with

business entity's capacity and liabilities for attaining meetings with reference to debt of

particular business.

(d) Representing motive of depreciation for accounting aspect with reference to its each method

Depreciation has its major applications in every business entity. It could be stated as fall

in value of any particular asset. These assets could justify as computer, machinery or plant etc.

are purchased for duration of long term as it would help in extracting its net value for every year.

If there is consideration of any life span, then its value will decrease. This particular scenario is

replicated on mandatory aspect for tracing depreciation value with reference to its accounts. It

would be justifying its depreciation value of particular asset. In the same series, it would directly

exclude its salvage value from earned money with motive of selling asset from its actual cost.

The basic elements are useful life, historical cost and salvage value as it is extracted by methods

which are Straight line and Written down value method. It would signify its importance in below

stated manner:

The historical cost of specific asset had been reduced with uses of straight line method.

The original value of asset had been traced in end of each financial year.

While considering written down value it helps in comparing with loss and profit which

are estimated with context of sale.

There should be proper review about information for purpose of asset replacement with

context of written down value.

The business entity could not applicable method of depreciation as it would bear loss

during transaction which had been incurred for earning good profit with reference to

financial result (Dung, 2016).

CLIENT 4

A. Representing objective of preparing Bank Reconciliation Statement (BRS)

The statement of Bank Reconciliation is prepared for justifying differences in its bank

records and BRS. With reference to perspective of accounting, it is considered as very basic

28

document. On legal concern, this statement is not mandatory but in same series it justifies

different objectives which are:

Accuracy had been provided with reference to cash-book and passbook. Generally, its

accuracy level had been recorded on basis of transactions which are recorded in these

mentioned books.

The mistakes could be extracted from each book with reference to outflow and inflow of

cash as it should match to its cash-book and bank statement. It would be providing

special focus on its error and irregularities in books with context of business.

The business entity's balance could be provided which was initially rectified.

The cheque position could be gained for collection purpose is known with Bank

reconciliation statement.

It would be also creating level of convenience for issuing cheque with context of future

of knowing bank balance.

B. Representing entries which helps in creating variances with context of bank statements

There are different factors for creating variance in context of bank statements:

Each book gets overwrite for purpose of issuing cheque on immediate aspect to any of

particular party. In the same series, cheques must be absence for purpose of encashment

related to bank (Power, 2018).

There is presence of different mistakes due to server issue, in that scenario amount would

be transferred and information would be retained from depositor but books would be

maintained and on actual basis transfer would not be incur due to server problem.

There is presence of different services which are given by bank for purpose of cheque

issuance to its depositors, gathering bills and cheques so it would be charging

commission with penalty if irregularity of enough balance.

29

different objectives which are:

Accuracy had been provided with reference to cash-book and passbook. Generally, its

accuracy level had been recorded on basis of transactions which are recorded in these

mentioned books.

The mistakes could be extracted from each book with reference to outflow and inflow of

cash as it should match to its cash-book and bank statement. It would be providing

special focus on its error and irregularities in books with context of business.

The business entity's balance could be provided which was initially rectified.

The cheque position could be gained for collection purpose is known with Bank

reconciliation statement.

It would be also creating level of convenience for issuing cheque with context of future

of knowing bank balance.

B. Representing entries which helps in creating variances with context of bank statements

There are different factors for creating variance in context of bank statements:

Each book gets overwrite for purpose of issuing cheque on immediate aspect to any of

particular party. In the same series, cheques must be absence for purpose of encashment

related to bank (Power, 2018).

There is presence of different mistakes due to server issue, in that scenario amount would

be transferred and information would be retained from depositor but books would be

maintained and on actual basis transfer would not be incur due to server problem.

There is presence of different services which are given by bank for purpose of cheque

issuance to its depositors, gathering bills and cheques so it would be charging

commission with penalty if irregularity of enough balance.

29

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

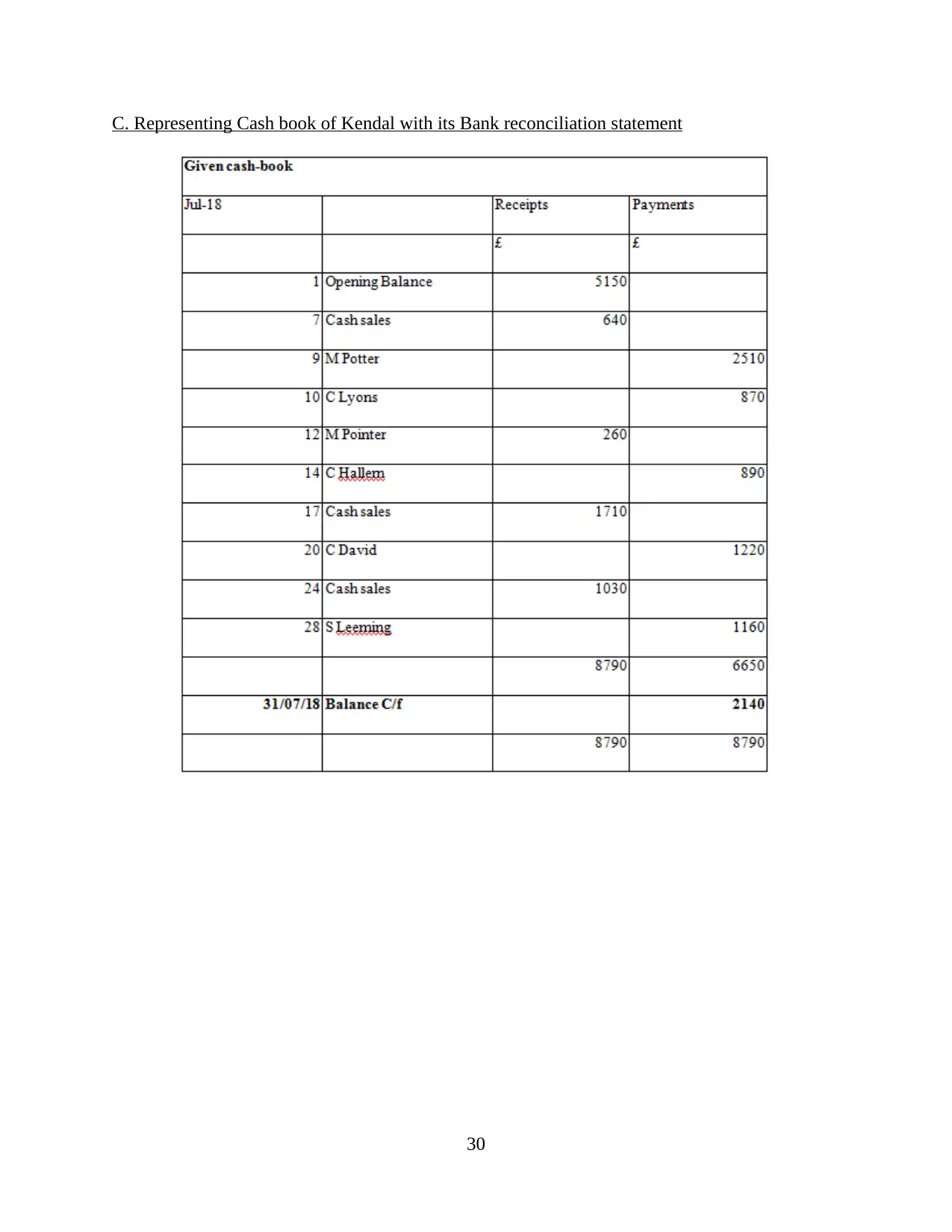

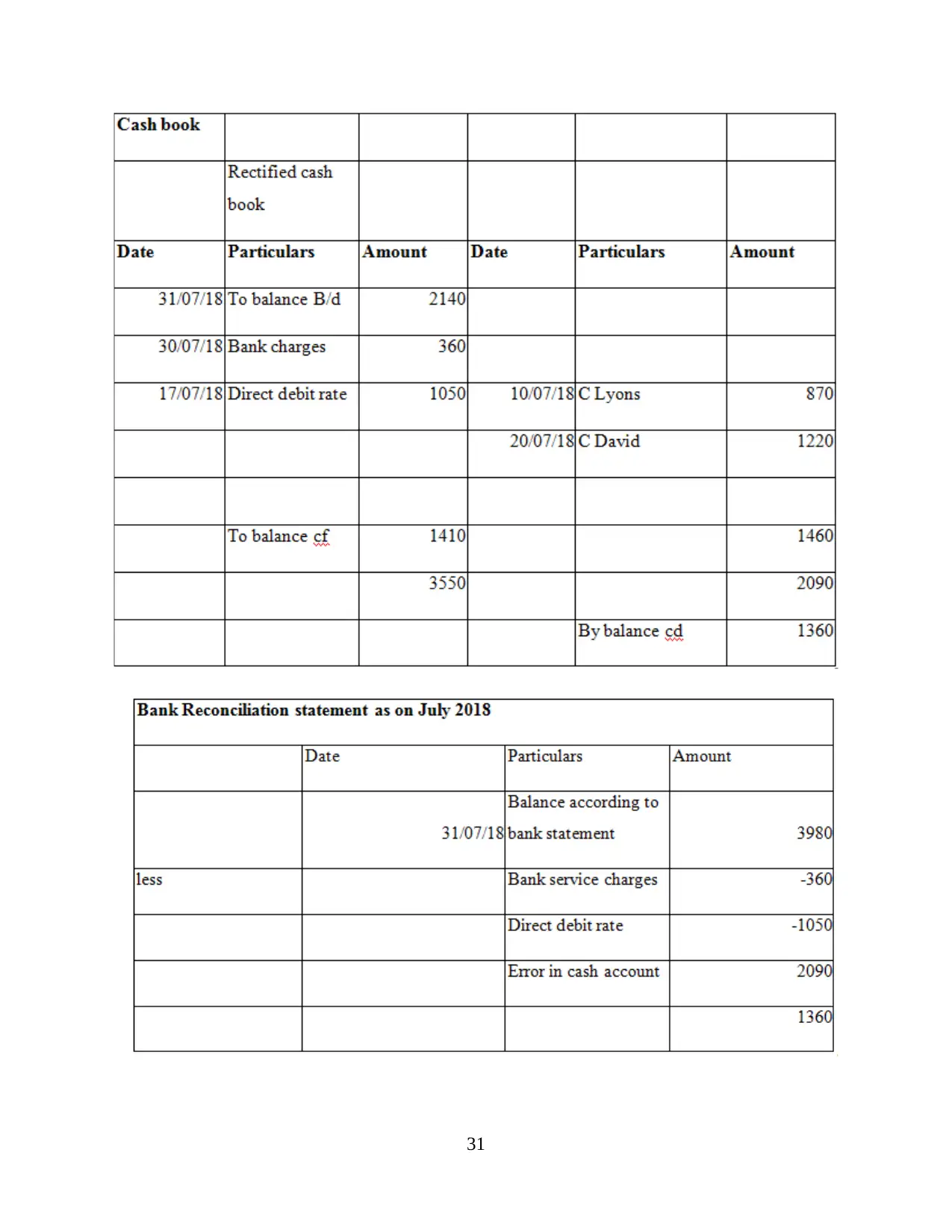

C. Representing Cash book of Kendal with its Bank reconciliation statement

30

30

31

CLIENT 5

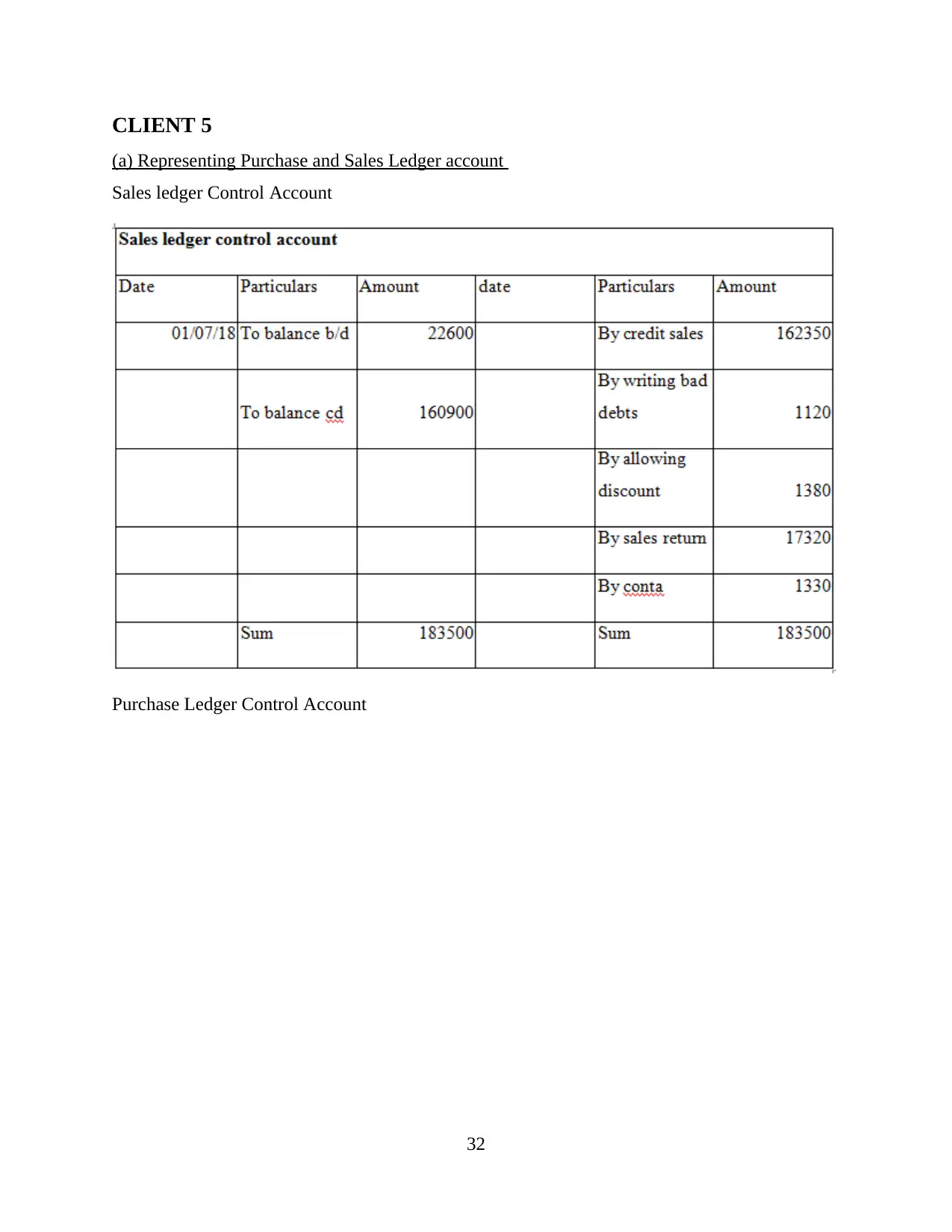

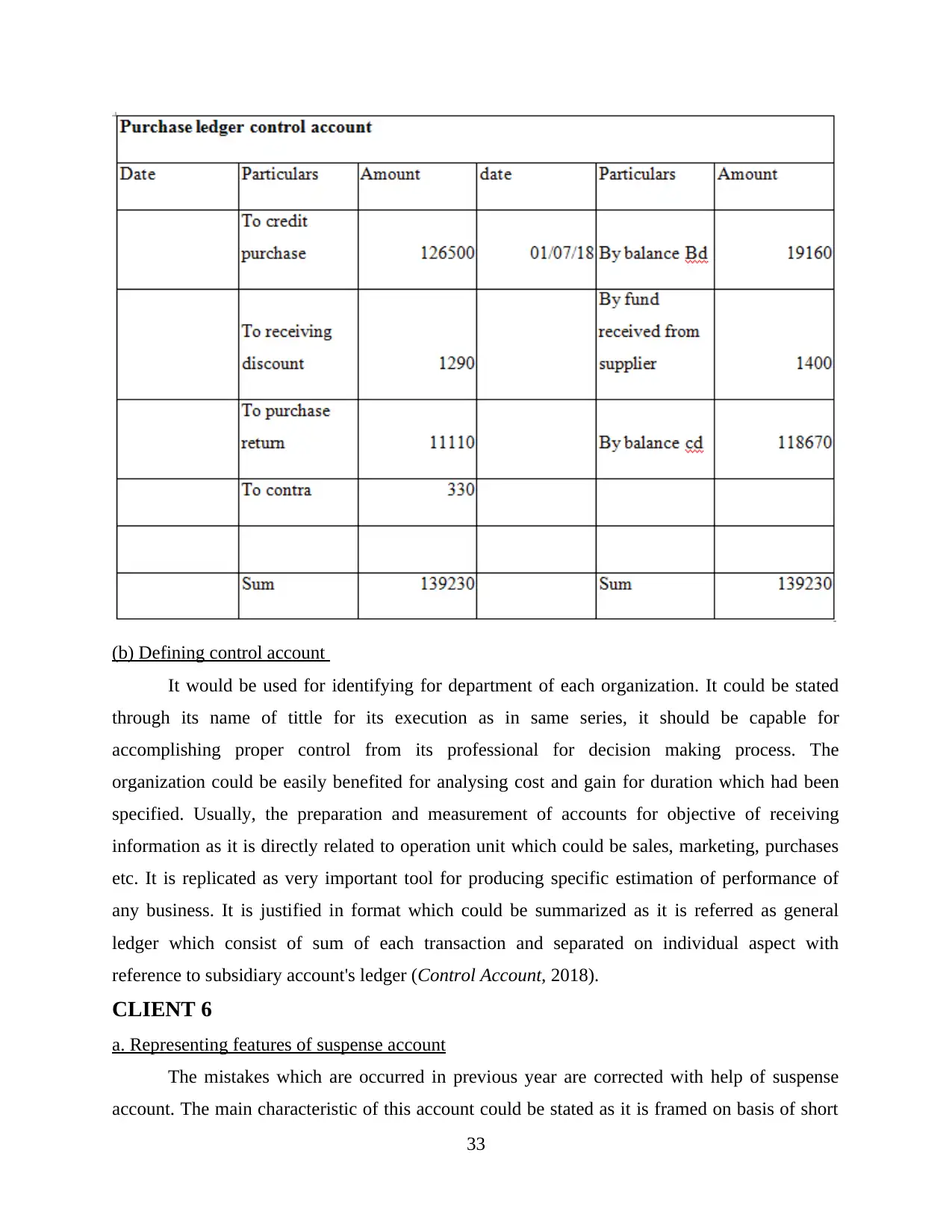

(a) Representing Purchase and Sales Ledger account

Sales ledger Control Account

Purchase Ledger Control Account

32

(a) Representing Purchase and Sales Ledger account

Sales ledger Control Account

Purchase Ledger Control Account

32

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(b) Defining control account

It would be used for identifying for department of each organization. It could be stated

through its name of tittle for its execution as in same series, it should be capable for

accomplishing proper control from its professional for decision making process. The

organization could be easily benefited for analysing cost and gain for duration which had been

specified. Usually, the preparation and measurement of accounts for objective of receiving

information as it is directly related to operation unit which could be sales, marketing, purchases

etc. It is replicated as very important tool for producing specific estimation of performance of

any business. It is justified in format which could be summarized as it is referred as general

ledger which consist of sum of each transaction and separated on individual aspect with

reference to subsidiary account's ledger (Control Account, 2018).

CLIENT 6

a. Representing features of suspense account

The mistakes which are occurred in previous year are corrected with help of suspense

account. The main characteristic of this account could be stated as it is framed on basis of short

33

It would be used for identifying for department of each organization. It could be stated

through its name of tittle for its execution as in same series, it should be capable for

accomplishing proper control from its professional for decision making process. The

organization could be easily benefited for analysing cost and gain for duration which had been

specified. Usually, the preparation and measurement of accounts for objective of receiving

information as it is directly related to operation unit which could be sales, marketing, purchases

etc. It is replicated as very important tool for producing specific estimation of performance of

any business. It is justified in format which could be summarized as it is referred as general

ledger which consist of sum of each transaction and separated on individual aspect with

reference to subsidiary account's ledger (Control Account, 2018).

CLIENT 6

a. Representing features of suspense account

The mistakes which are occurred in previous year are corrected with help of suspense

account. The main characteristic of this account could be stated as it is framed on basis of short

33

duration and temporary aspect. The main objective of this particular account for creating

promptness in its accounts with context of operation. This statement should be balanced if

belongingness is not determined. It should be capable for extracting its error which must be

resolved on earlier aspect. The most important feature could be stated as it should be zero before

preparation of final accounts.

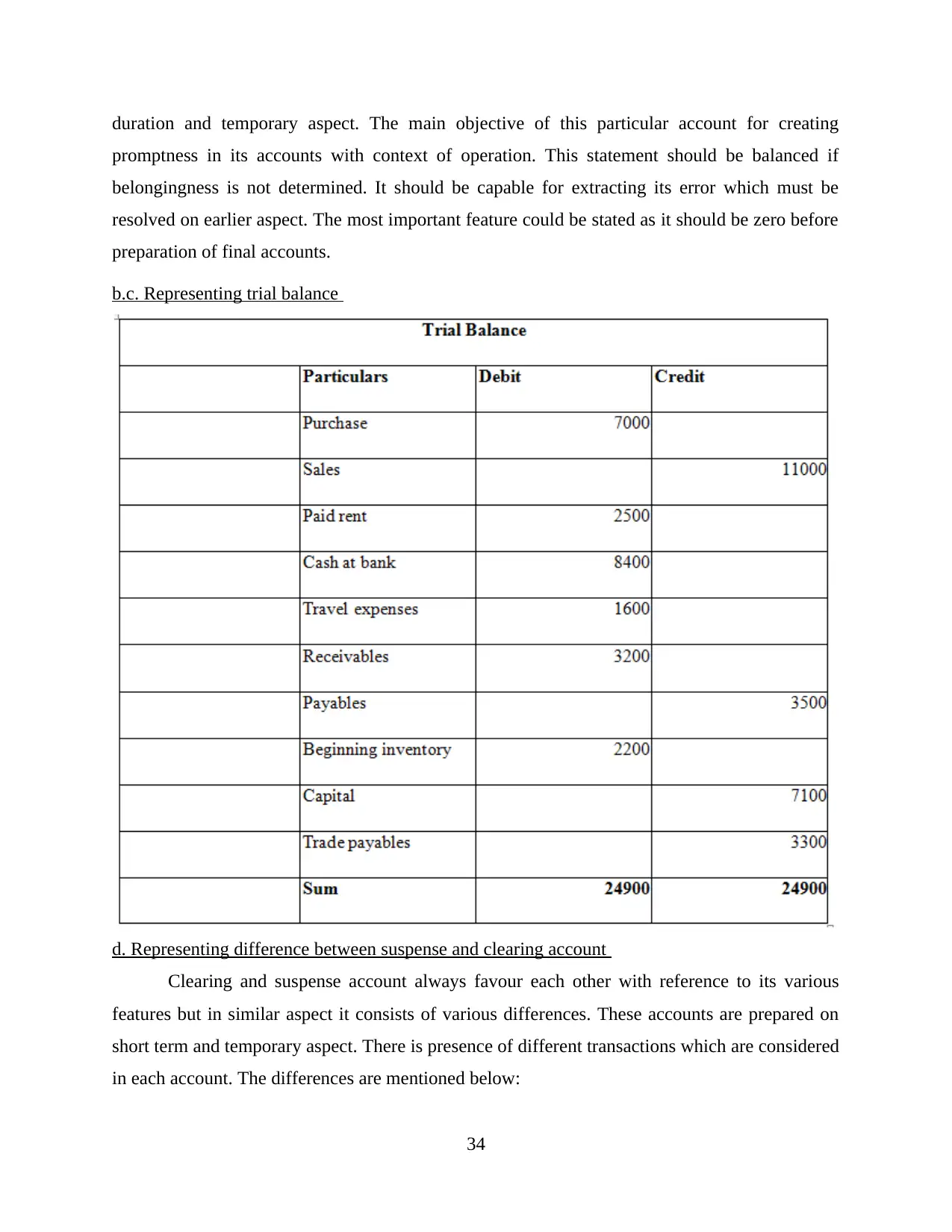

b.c. Representing trial balance

d. Representing difference between suspense and clearing account

Clearing and suspense account always favour each other with reference to its various

features but in similar aspect it consists of various differences. These accounts are prepared on

short term and temporary aspect. There is presence of different transactions which are considered

in each account. The differences are mentioned below:

34

promptness in its accounts with context of operation. This statement should be balanced if

belongingness is not determined. It should be capable for extracting its error which must be

resolved on earlier aspect. The most important feature could be stated as it should be zero before

preparation of final accounts.

b.c. Representing trial balance

d. Representing difference between suspense and clearing account

Clearing and suspense account always favour each other with reference to its various

features but in similar aspect it consists of various differences. These accounts are prepared on

short term and temporary aspect. There is presence of different transactions which are considered

in each account. The differences are mentioned below:

34

The information could be identified through clearing accounts which is recorded in

appropriate format and adjusted on later basis. On its contrary, preparation of suspense

account is during problem and at time of resolution it is balanced as zero.

The balance had been transferred in specific accounts but in clearing zero is moved in

final account and in suspense zero is transferred in correct account.

There is holding of uncertainties via suspense account and it considers only if there is any

existence of problem but in clearing account transactions are hold on temporary basis.

With the context of clearing account expenses of utility are hold and it may be closed in

end of month but on suspense account acts in unique aspect as amount has been recorded

when uncertainties are resolved.

The suspense account could be ended if fixed schedule is not present and on its contrary,

clearing account has specific closing time which is fixed (Cochran, 2018).

CONCLUSION

It could be concluded from above report that financial accounting is considered as very

important for each business organization with its industry. It had been articulated from this report

that financial stability and performance of organization could be determined by financial

accounting. There is presence of different rules, regulations and principles for the purpose of

preparation of financial statements. In the same series, different standards had been represented

such as IFRS, GAAP which are considered as very important aspect. It could be easily justified

from above report that different financial statements such as balance sheet, Income statement,

trial balance plays very important role as they are implied for gaining financial position. Further

it could be stated that growth and profitability could be accomplished by following these specific

regulations. It could be summed by analysing variances with reference to suspense and clearing

account with similarity of temporary aspect and vital for every business organization.

35

appropriate format and adjusted on later basis. On its contrary, preparation of suspense

account is during problem and at time of resolution it is balanced as zero.

The balance had been transferred in specific accounts but in clearing zero is moved in

final account and in suspense zero is transferred in correct account.

There is holding of uncertainties via suspense account and it considers only if there is any

existence of problem but in clearing account transactions are hold on temporary basis.

With the context of clearing account expenses of utility are hold and it may be closed in

end of month but on suspense account acts in unique aspect as amount has been recorded

when uncertainties are resolved.

The suspense account could be ended if fixed schedule is not present and on its contrary,

clearing account has specific closing time which is fixed (Cochran, 2018).

CONCLUSION

It could be concluded from above report that financial accounting is considered as very

important for each business organization with its industry. It had been articulated from this report

that financial stability and performance of organization could be determined by financial

accounting. There is presence of different rules, regulations and principles for the purpose of

preparation of financial statements. In the same series, different standards had been represented

such as IFRS, GAAP which are considered as very important aspect. It could be easily justified

from above report that different financial statements such as balance sheet, Income statement,

trial balance plays very important role as they are implied for gaining financial position. Further

it could be stated that growth and profitability could be accomplished by following these specific

regulations. It could be summed by analysing variances with reference to suspense and clearing

account with similarity of temporary aspect and vital for every business organization.

35

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2-3). pp.339-383.

Cochran, R. J., 2018. The Financial Accounting Standards Board’s Fair Value Mandate: Are

Level 3 Assets and Liabilities Being Measured Accurately? Accounting and Finance

Research. 7(2). p.33.

Dung, N. V., 2016. Value-relevance of financial statement information: A flexible application of

modern theories to the Vietnamese stock market. Quarterly Journal of Economics. 84.

pp.488-500.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches. (1). pp.60-

64.

Needles, B. E., Powers, M. and Crosson, S. V., 2013. Principles of accounting. Cengage

Learning.

Pointer, I. A., Pointer Ivan Andrew, 2011. Financial, account and ledger web application and

method for use on personal computers and internet capable mobile devices. U.S. Patent

Application 13/021,732.

Power, M., 2018. Accounting, boundary-making and organizational permeability. Research in

the Sociology of Organizations.57. pp.31-53.

Sharma, A. and Panigrahi, P. K., 2013. A review of financial accounting fraud detection based

on data mining techniques. arXiv preprint arXiv:1309.3944.

Tsalavoutas, I., André, P. and Evans, L., 2012. The transition to IFRS and the value relevance of

financial statements in Greece. The British Accounting Review. 44(4). pp.262-277.

Online

Control Accounts. 2018. [Online]. Available through:

<http://www.soofiainternational.org/control-accounts/>.

36

Books and Journals

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2-3). pp.339-383.

Cochran, R. J., 2018. The Financial Accounting Standards Board’s Fair Value Mandate: Are

Level 3 Assets and Liabilities Being Measured Accurately? Accounting and Finance

Research. 7(2). p.33.

Dung, N. V., 2016. Value-relevance of financial statement information: A flexible application of

modern theories to the Vietnamese stock market. Quarterly Journal of Economics. 84.

pp.488-500.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches. (1). pp.60-

64.

Needles, B. E., Powers, M. and Crosson, S. V., 2013. Principles of accounting. Cengage

Learning.

Pointer, I. A., Pointer Ivan Andrew, 2011. Financial, account and ledger web application and

method for use on personal computers and internet capable mobile devices. U.S. Patent

Application 13/021,732.

Power, M., 2018. Accounting, boundary-making and organizational permeability. Research in

the Sociology of Organizations.57. pp.31-53.

Sharma, A. and Panigrahi, P. K., 2013. A review of financial accounting fraud detection based

on data mining techniques. arXiv preprint arXiv:1309.3944.

Tsalavoutas, I., André, P. and Evans, L., 2012. The transition to IFRS and the value relevance of

financial statements in Greece. The British Accounting Review. 44(4). pp.262-277.

Online

Control Accounts. 2018. [Online]. Available through:

<http://www.soofiainternational.org/control-accounts/>.

36

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.