PDF - Financial Accounting Principles

Added on 2020-10-04

26 Pages4838 Words68 Views

Financial AccountingPrinciplesTable of Contents

INTRODUCTION...........................................................................................................................1PART A...........................................................................................................................................11. Concept of financial accounting ........................................................................................12. Legislation and rules that are use in accounting ................................................................13. Principles and accounts .....................................................................................................14. Convention and concepts of accounting ............................................................................2PART B............................................................................................................................................3CLIENT 1........................................................................................................................................3Journal entries.........................................................................................................................3Posting it into ledger...............................................................................................................8Trail balance.........................................................................................................................13CLIENT 2......................................................................................................................................14a): Statement of profit and loss for peter piper.....................................................................14b): Statement of balance sheet..............................................................................................15CLIENT 3......................................................................................................................................16c): Concept of accounting principles....................................................................................16d): Purpose of using depreciation in formulation of financial accounting...........................17CLIENT 4......................................................................................................................................18a): Purpose of Bank reconciliation statements and difficulties............................................18b): list of some records that are varies .................................................................................19c): Calculation......................................................................................................................19CLIENT 5.....................................................................................................................................20a): Ledger control accounts..................................................................................................201: Sales ledger control a/c.....................................................................................................202: Purchase ledger control a/c...............................................................................................21b): Advantage of using ledger control account ....................................................................21CLINET 6......................................................................................................................................22a): Suspense a/c....................................................................................................................22b): Trail balance....................................................................................................................22c): Journal entry....................................................................................................................22d): Comparison among suspense and clearing account .......................................................23

INTRODUCTIONFinancial accounting is a systematic recording of accounting data those are collectedfrom daily transactions of an organisation. It is essential aspects for every business organizationwhether small or large. There are require a perfect accounting system to manage there financialdata in perfect manner (Weil, Schipper and Francis, 2013). This project report include certainrule and regulation those are applicable in recording of entries into the books of account. There are certain principles and convention those are helpful in posting transactions intovarious statements those are made by the accountant. The primary objective of using financialaccounting is to prepare accurate and reliable information in order to increase profitability of thecompany. Certain statements that are use for the purpose of recording and analysing data areclearly utilise under this project.PART A1. Concept of financial accounting Financial accounting is systematic recording of financial transaction those are doneduring the time. This consists of recording, summarising and analysing performance of ancompany with these statements (Edmonds and et. al., 2013). While, it is use to prepare the samein order to determine materiality, comparability and reliability of the company.2. Legislation and rules that are use in accounting Accounting regulation are one of the important record which are issue by institution onregularly basis. Basically, it is disclosure of financial performance by using these statements.There some useful advantage of using regulation to improve credibility and reliability those arerelies on specific theory and concepts. Types of accounting regulation:Disclosure of statements.Content standards.Presentation standard. Privately set rules and practices.3. Principles and accounts It has been seen that to record financial transaction in more perfect manner they need touse more certain rules and procedure that are helpful in systematic record of data. It is known as1

measurement processing and evaluation of financial information regarding performance ofeconomic entity. Some of them are:Personal accounts: Debit the receiver and credit the giverReal a/c: Debit what comes in, credit what goes out.Nominal: Debit all expenses and losses or credit all income and profits.Principles: Accrual principles: It is refers to be the perfect concepts which is use to record all thoseinformation that must be recorded in a accounting time when they actual occur. Not at that timewhen cash-flows are incurred.Conservatism: According to this particular concepts, all those expenses and debts mustbe converted into one accounting period (Macve, 2015). This will be termed as a conservatism, iffinancial details are occur at very minimum gain for the company.4. Convention and concepts of accounting Every business entity need to follow some specific accounting practices which are helpfulfor the manager to record transaction into the books of accounts. Some conventions are: Convention: Money measurement: In every organisation, manager need to record every transactionwhich are incur only in terms of financial and non-financial terms. It involves workforces skills,market leadership and many more.Separate entity: As per this concepts, accountant must ensure that all transactionsperform by company's are require to be individually recorded. Materiality: It is known as important parts of convention that are profitable for thecompany in order to follow basic principles for the purpose of making valuable decision-making.Concepts: Going concern: Under this, managers make an assumption about the information untilthere is not any perfect evidence. It is a regular process which is being followed by the companyfor longer period of time.Cost basis: All those assets must be enter in the accounts books on its actual cost paid tothe company and not at current market value.Entity: It reflect the annual recording of activities of a particular business organization. 2

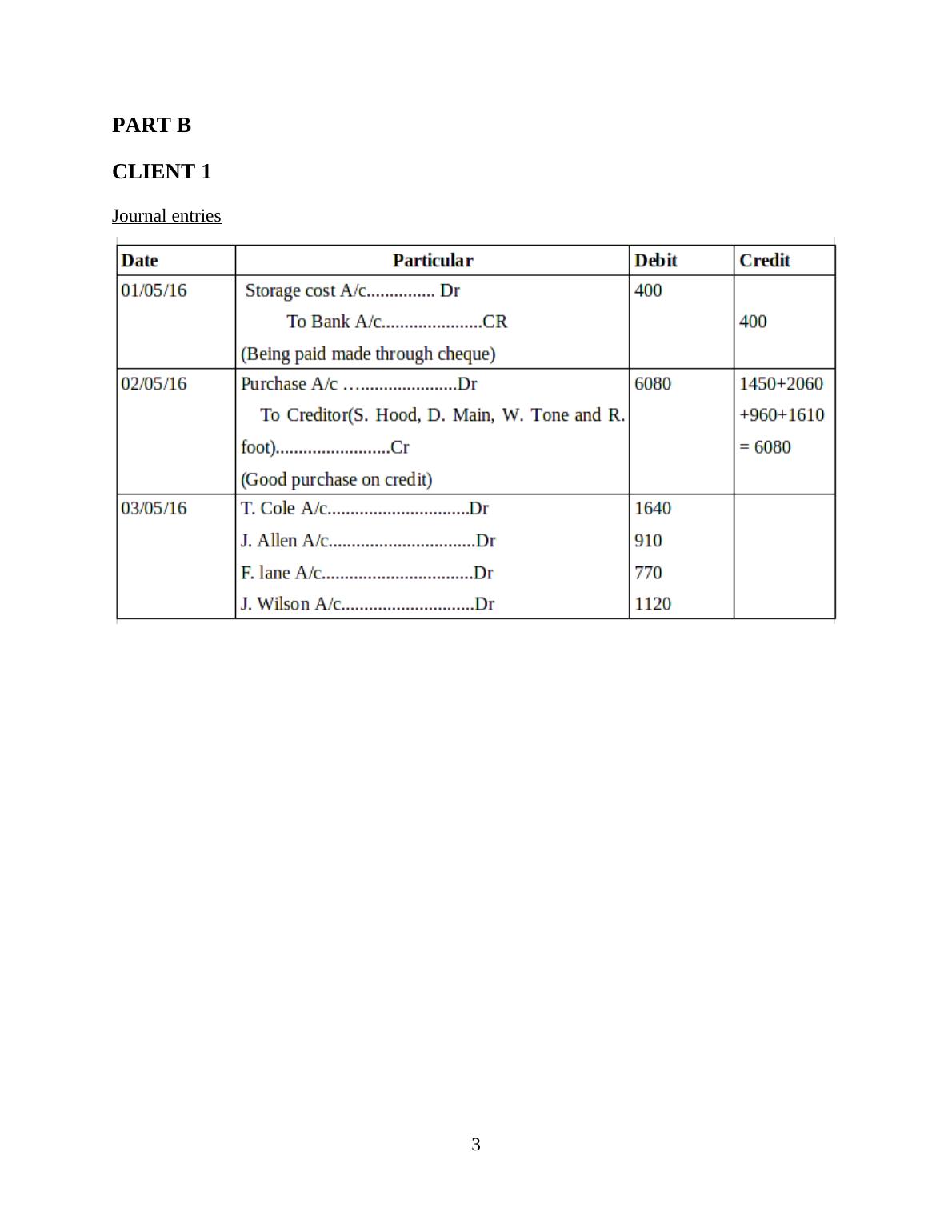

PART BCLIENT 1Journal entries3

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Introduction to Financial Accountinglg...

|30

|5105

|401

(solved) Financial Accounting PDFlg...

|29

|5463

|298

Principle, Concepts and Importance of Financial Accounting - Assignmentlg...

|36

|4351

|33

Financial Accounting Principles - PDFlg...

|27

|4346

|118

Financial Accounting Principles | Reportlg...

|41

|6450

|41

Assignment on Financial Accounting pdflg...

|47

|5713

|177