Financial Accounting: Scenario Analysis and Journal Entries

VerifiedAdded on 2024/06/28

|16

|1749

|349

AI Summary

This document presents a comprehensive analysis of financial accounting scenarios, including journal entries, ledger accounts, trial balances, trading and profit & loss accounts, balance sheets, bank reconciliations, and error rectifications. The scenarios cover various transactions, including capital introduction, purchases, sales, expenses, and adjustments. The document provides detailed explanations and calculations for each scenario, demonstrating the application of fundamental accounting principles.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Scenario 1........................................................................................................................................3

Question 1.................................................................................................................................... 3

Question 2.................................................................................................................................... 9

Scenario - 2.................................................................................................................................... 11

Question 1.................................................................................................................................. 11

Question 2.................................................................................................................................. 13

References –...................................................................................................................................15

2

Scenario 1........................................................................................................................................3

Question 1.................................................................................................................................... 3

Question 2.................................................................................................................................... 9

Scenario - 2.................................................................................................................................... 11

Question 1.................................................................................................................................. 11

Question 2.................................................................................................................................. 13

References –...................................................................................................................................15

2

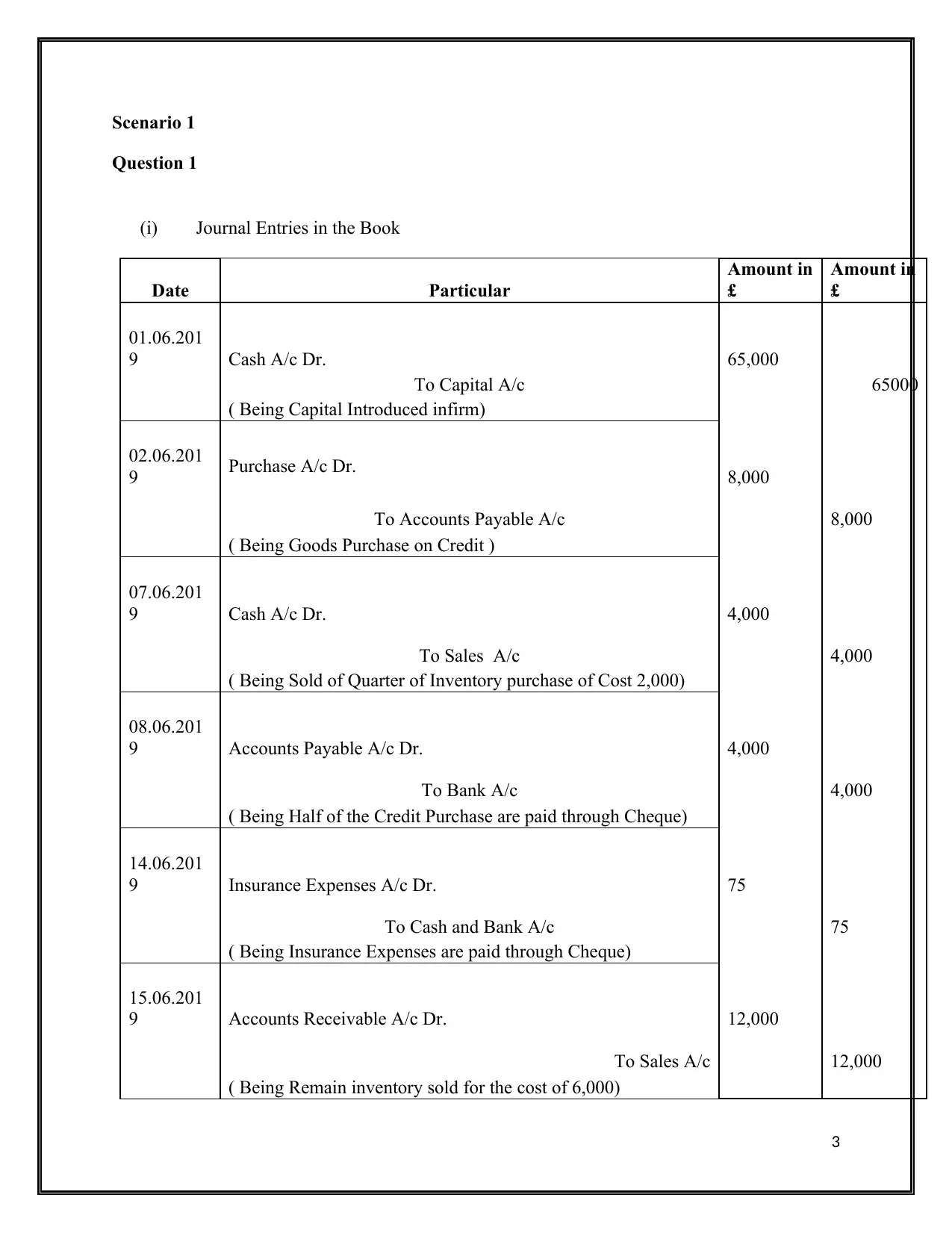

Scenario 1

Question 1

(i) Journal Entries in the Book

Date Particular

Amount in

£

Amount in

£

01.06.201

9 Cash A/c Dr. 65,000

To Capital A/c 65000

( Being Capital Introduced infirm)

02.06.201

9 Purchase A/c Dr. 8,000

To Accounts Payable A/c 8,000

( Being Goods Purchase on Credit )

07.06.201

9 Cash A/c Dr. 4,000

To Sales A/c 4,000

( Being Sold of Quarter of Inventory purchase of Cost 2,000)

08.06.201

9 Accounts Payable A/c Dr. 4,000

To Bank A/c 4,000

( Being Half of the Credit Purchase are paid through Cheque)

14.06.201

9 Insurance Expenses A/c Dr. 75

To Cash and Bank A/c 75

( Being Insurance Expenses are paid through Cheque)

15.06.201

9 Accounts Receivable A/c Dr. 12,000

To Sales A/c 12,000

( Being Remain inventory sold for the cost of 6,000)

3

Question 1

(i) Journal Entries in the Book

Date Particular

Amount in

£

Amount in

£

01.06.201

9 Cash A/c Dr. 65,000

To Capital A/c 65000

( Being Capital Introduced infirm)

02.06.201

9 Purchase A/c Dr. 8,000

To Accounts Payable A/c 8,000

( Being Goods Purchase on Credit )

07.06.201

9 Cash A/c Dr. 4,000

To Sales A/c 4,000

( Being Sold of Quarter of Inventory purchase of Cost 2,000)

08.06.201

9 Accounts Payable A/c Dr. 4,000

To Bank A/c 4,000

( Being Half of the Credit Purchase are paid through Cheque)

14.06.201

9 Insurance Expenses A/c Dr. 75

To Cash and Bank A/c 75

( Being Insurance Expenses are paid through Cheque)

15.06.201

9 Accounts Receivable A/c Dr. 12,000

To Sales A/c 12,000

( Being Remain inventory sold for the cost of 6,000)

3

16.06.201

9 Purchase A/c Dr. 10,000

To Accounts Payable A/c 10,000

( Being Goods Purchase on Credit )

18.06.201

9 Computer A/c Dr. 3,000

To Cash A/c 3,000

( Being computer equipment are purchased on cash )

20.06.201

9 Rent Expenses A/c Dr. 150

To Cash and Bank A/c 150

(Being Rent Paid through Cheque for the month )

21.06.201

9 Cash A/c Dr. 10,000

To Sales A/c 10,000

( Being half of the inventory of worth 5,000 sold on cash)

25.06.201

9 Petty Cash A/c Dr. 100

To Bank A/c 100

( Being Cash Withdrawn from the bank )

30.06.201

9 Stationary Expenses A/c Dr. 3,000

To Petty Cash A/c 2,800

(Being stationary Expenses are paid from Petty Cash of

Company)

4

9 Purchase A/c Dr. 10,000

To Accounts Payable A/c 10,000

( Being Goods Purchase on Credit )

18.06.201

9 Computer A/c Dr. 3,000

To Cash A/c 3,000

( Being computer equipment are purchased on cash )

20.06.201

9 Rent Expenses A/c Dr. 150

To Cash and Bank A/c 150

(Being Rent Paid through Cheque for the month )

21.06.201

9 Cash A/c Dr. 10,000

To Sales A/c 10,000

( Being half of the inventory of worth 5,000 sold on cash)

25.06.201

9 Petty Cash A/c Dr. 100

To Bank A/c 100

( Being Cash Withdrawn from the bank )

30.06.201

9 Stationary Expenses A/c Dr. 3,000

To Petty Cash A/c 2,800

(Being stationary Expenses are paid from Petty Cash of

Company)

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

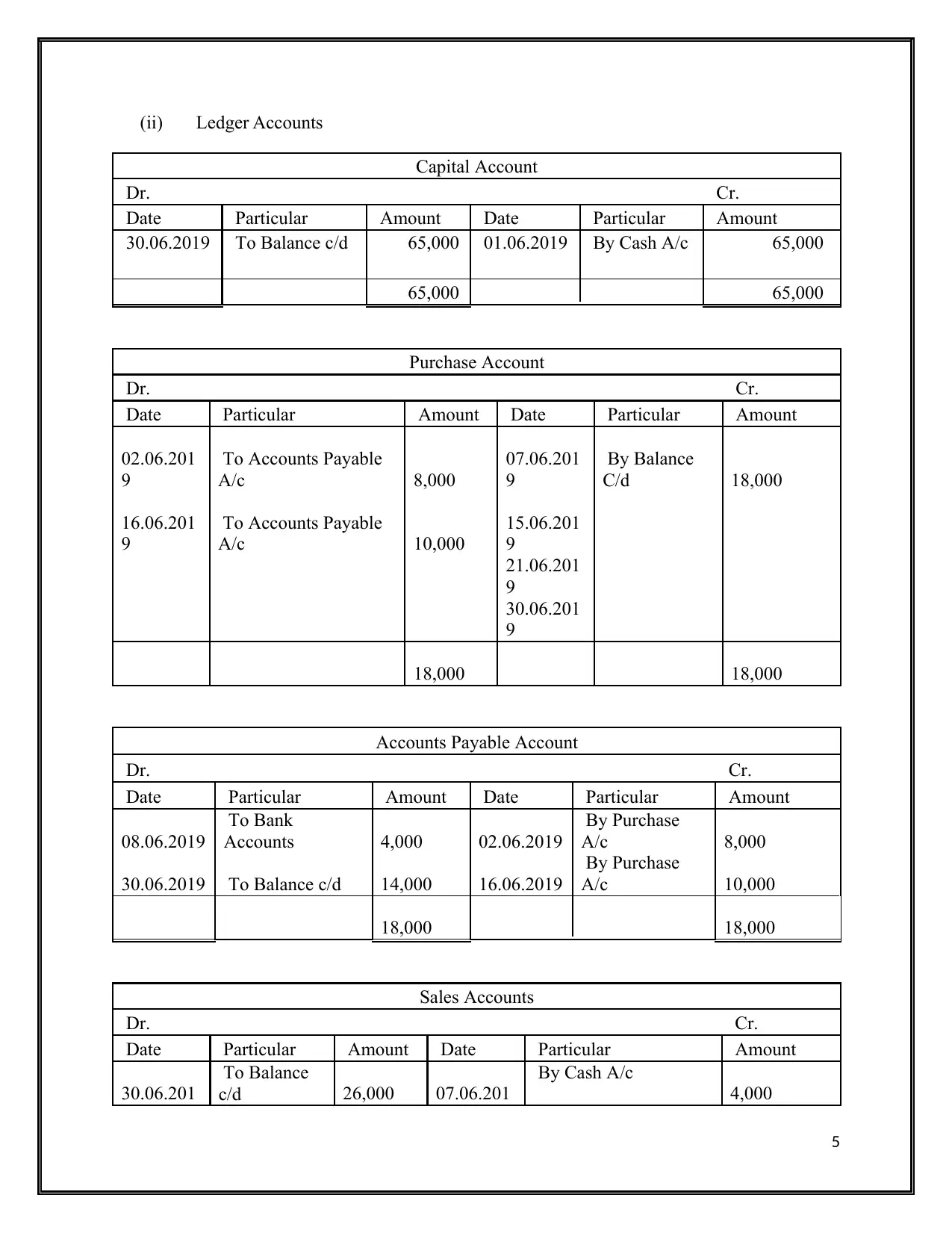

(ii) Ledger Accounts

Capital Account

Dr. Cr.

Date Particular Amount Date Particular Amount

30.06.2019 To Balance c/d 65,000 01.06.2019 By Cash A/c 65,000

65,000 65,000

Purchase Account

Dr. Cr.

Date Particular Amount Date Particular Amount

02.06.201

9

To Accounts Payable

A/c 8,000

07.06.201

9

By Balance

C/d 18,000

16.06.201

9

To Accounts Payable

A/c 10,000

15.06.201

9

21.06.201

9

30.06.201

9

18,000 18,000

Accounts Payable Account

Dr. Cr.

Date Particular Amount Date Particular Amount

08.06.2019

To Bank

Accounts 4,000 02.06.2019

By Purchase

A/c 8,000

30.06.2019 To Balance c/d 14,000 16.06.2019

By Purchase

A/c 10,000

18,000 18,000

Sales Accounts

Dr. Cr.

Date Particular Amount Date Particular Amount

30.06.201

To Balance

c/d 26,000 07.06.201

By Cash A/c

4,000

5

Capital Account

Dr. Cr.

Date Particular Amount Date Particular Amount

30.06.2019 To Balance c/d 65,000 01.06.2019 By Cash A/c 65,000

65,000 65,000

Purchase Account

Dr. Cr.

Date Particular Amount Date Particular Amount

02.06.201

9

To Accounts Payable

A/c 8,000

07.06.201

9

By Balance

C/d 18,000

16.06.201

9

To Accounts Payable

A/c 10,000

15.06.201

9

21.06.201

9

30.06.201

9

18,000 18,000

Accounts Payable Account

Dr. Cr.

Date Particular Amount Date Particular Amount

08.06.2019

To Bank

Accounts 4,000 02.06.2019

By Purchase

A/c 8,000

30.06.2019 To Balance c/d 14,000 16.06.2019

By Purchase

A/c 10,000

18,000 18,000

Sales Accounts

Dr. Cr.

Date Particular Amount Date Particular Amount

30.06.201

To Balance

c/d 26,000 07.06.201

By Cash A/c

4,000

5

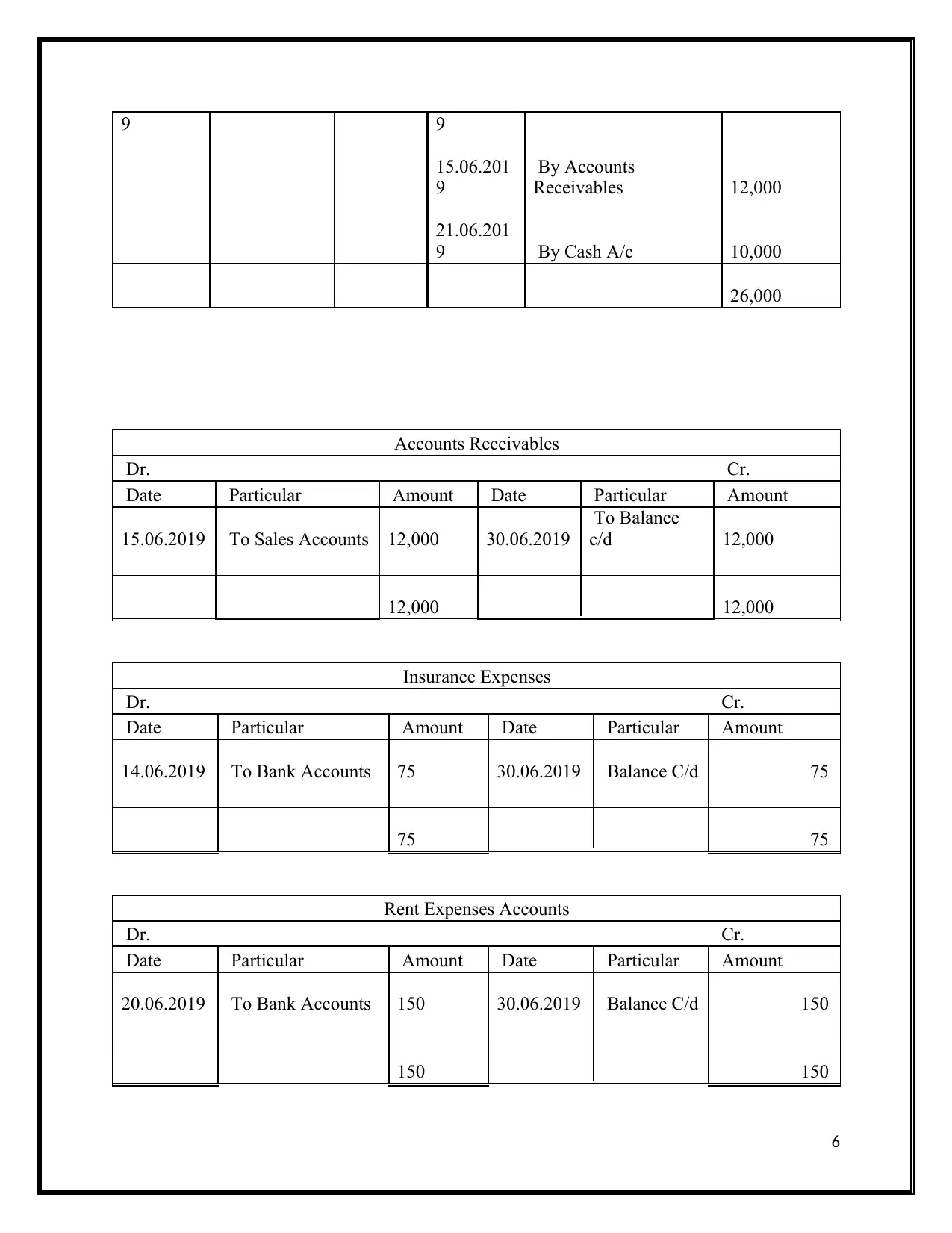

9 9

15.06.201

9

By Accounts

Receivables 12,000

21.06.201

9 By Cash A/c 10,000

26,000

Accounts Receivables

Dr. Cr.

Date Particular Amount Date Particular Amount

15.06.2019 To Sales Accounts 12,000 30.06.2019

To Balance

c/d 12,000

12,000 12,000

Insurance Expenses

Dr. Cr.

Date Particular Amount Date Particular Amount

14.06.2019 To Bank Accounts 75 30.06.2019 Balance C/d 75

75 75

Rent Expenses Accounts

Dr. Cr.

Date Particular Amount Date Particular Amount

20.06.2019 To Bank Accounts 150 30.06.2019 Balance C/d 150

150 150

6

15.06.201

9

By Accounts

Receivables 12,000

21.06.201

9 By Cash A/c 10,000

26,000

Accounts Receivables

Dr. Cr.

Date Particular Amount Date Particular Amount

15.06.2019 To Sales Accounts 12,000 30.06.2019

To Balance

c/d 12,000

12,000 12,000

Insurance Expenses

Dr. Cr.

Date Particular Amount Date Particular Amount

14.06.2019 To Bank Accounts 75 30.06.2019 Balance C/d 75

75 75

Rent Expenses Accounts

Dr. Cr.

Date Particular Amount Date Particular Amount

20.06.2019 To Bank Accounts 150 30.06.2019 Balance C/d 150

150 150

6

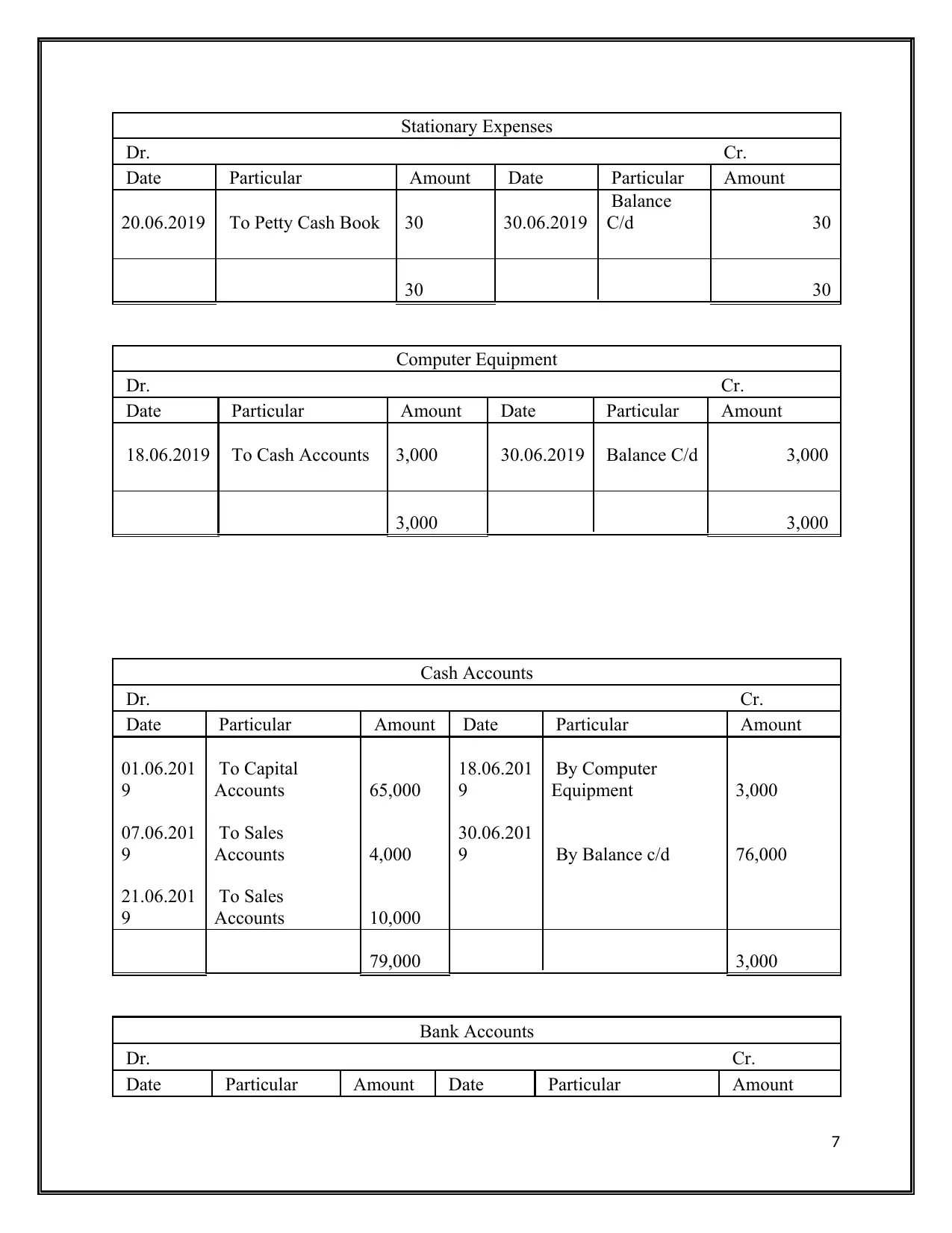

Stationary Expenses

Dr. Cr.

Date Particular Amount Date Particular Amount

20.06.2019 To Petty Cash Book 30 30.06.2019

Balance

C/d 30

30 30

Computer Equipment

Dr. Cr.

Date Particular Amount Date Particular Amount

18.06.2019 To Cash Accounts 3,000 30.06.2019 Balance C/d 3,000

3,000 3,000

Cash Accounts

Dr. Cr.

Date Particular Amount Date Particular Amount

01.06.201

9

To Capital

Accounts 65,000

18.06.201

9

By Computer

Equipment 3,000

07.06.201

9

To Sales

Accounts 4,000

30.06.201

9 By Balance c/d 76,000

21.06.201

9

To Sales

Accounts 10,000

79,000 3,000

Bank Accounts

Dr. Cr.

Date Particular Amount Date Particular Amount

7

Dr. Cr.

Date Particular Amount Date Particular Amount

20.06.2019 To Petty Cash Book 30 30.06.2019

Balance

C/d 30

30 30

Computer Equipment

Dr. Cr.

Date Particular Amount Date Particular Amount

18.06.2019 To Cash Accounts 3,000 30.06.2019 Balance C/d 3,000

3,000 3,000

Cash Accounts

Dr. Cr.

Date Particular Amount Date Particular Amount

01.06.201

9

To Capital

Accounts 65,000

18.06.201

9

By Computer

Equipment 3,000

07.06.201

9

To Sales

Accounts 4,000

30.06.201

9 By Balance c/d 76,000

21.06.201

9

To Sales

Accounts 10,000

79,000 3,000

Bank Accounts

Dr. Cr.

Date Particular Amount Date Particular Amount

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

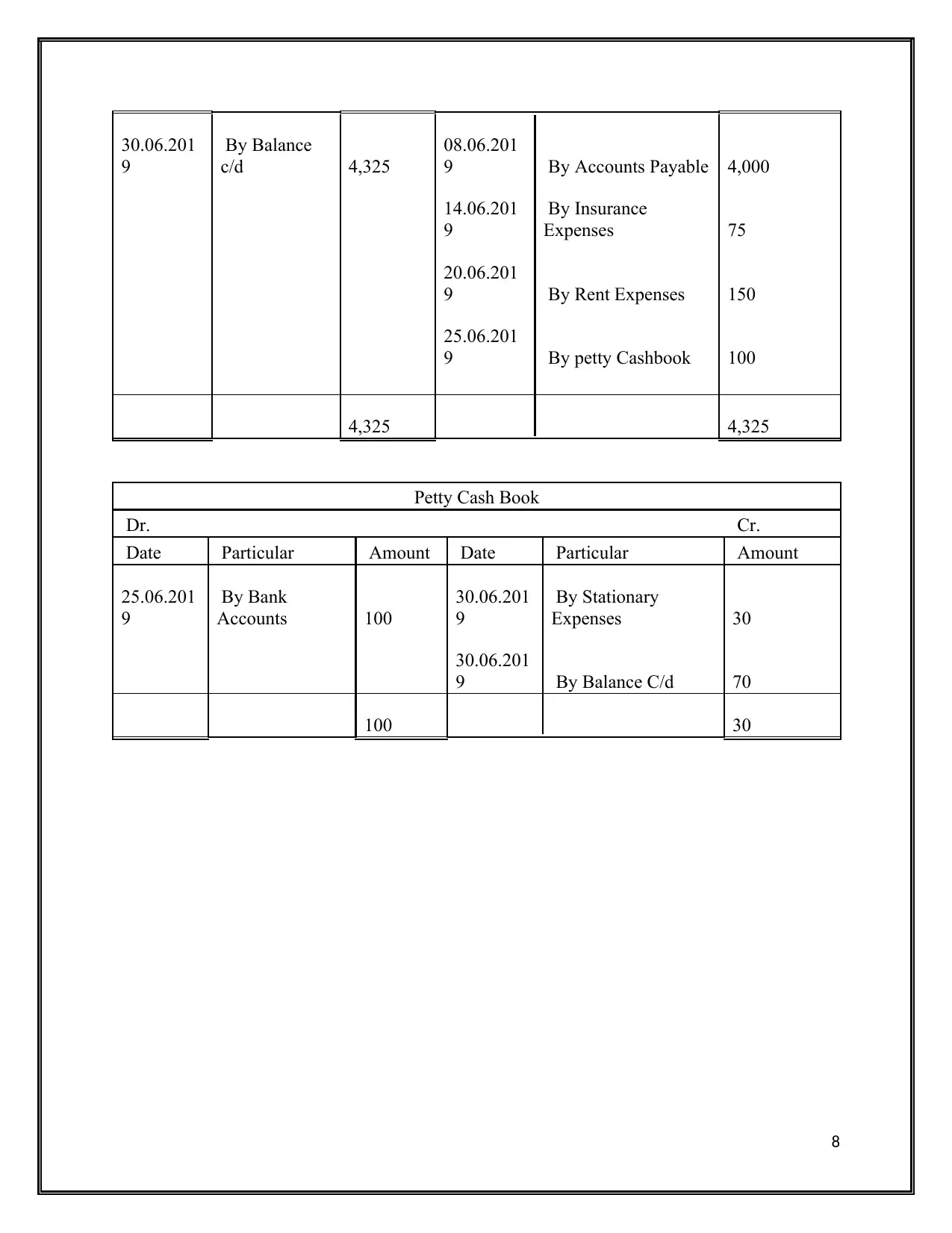

30.06.201

9

By Balance

c/d 4,325

08.06.201

9 By Accounts Payable 4,000

14.06.201

9

By Insurance

Expenses 75

20.06.201

9 By Rent Expenses 150

25.06.201

9 By petty Cashbook 100

4,325 4,325

Petty Cash Book

Dr. Cr.

Date Particular Amount Date Particular Amount

25.06.201

9

By Bank

Accounts 100

30.06.201

9

By Stationary

Expenses 30

30.06.201

9 By Balance C/d 70

100 30

8

9

By Balance

c/d 4,325

08.06.201

9 By Accounts Payable 4,000

14.06.201

9

By Insurance

Expenses 75

20.06.201

9 By Rent Expenses 150

25.06.201

9 By petty Cashbook 100

4,325 4,325

Petty Cash Book

Dr. Cr.

Date Particular Amount Date Particular Amount

25.06.201

9

By Bank

Accounts 100

30.06.201

9

By Stationary

Expenses 30

30.06.201

9 By Balance C/d 70

100 30

8

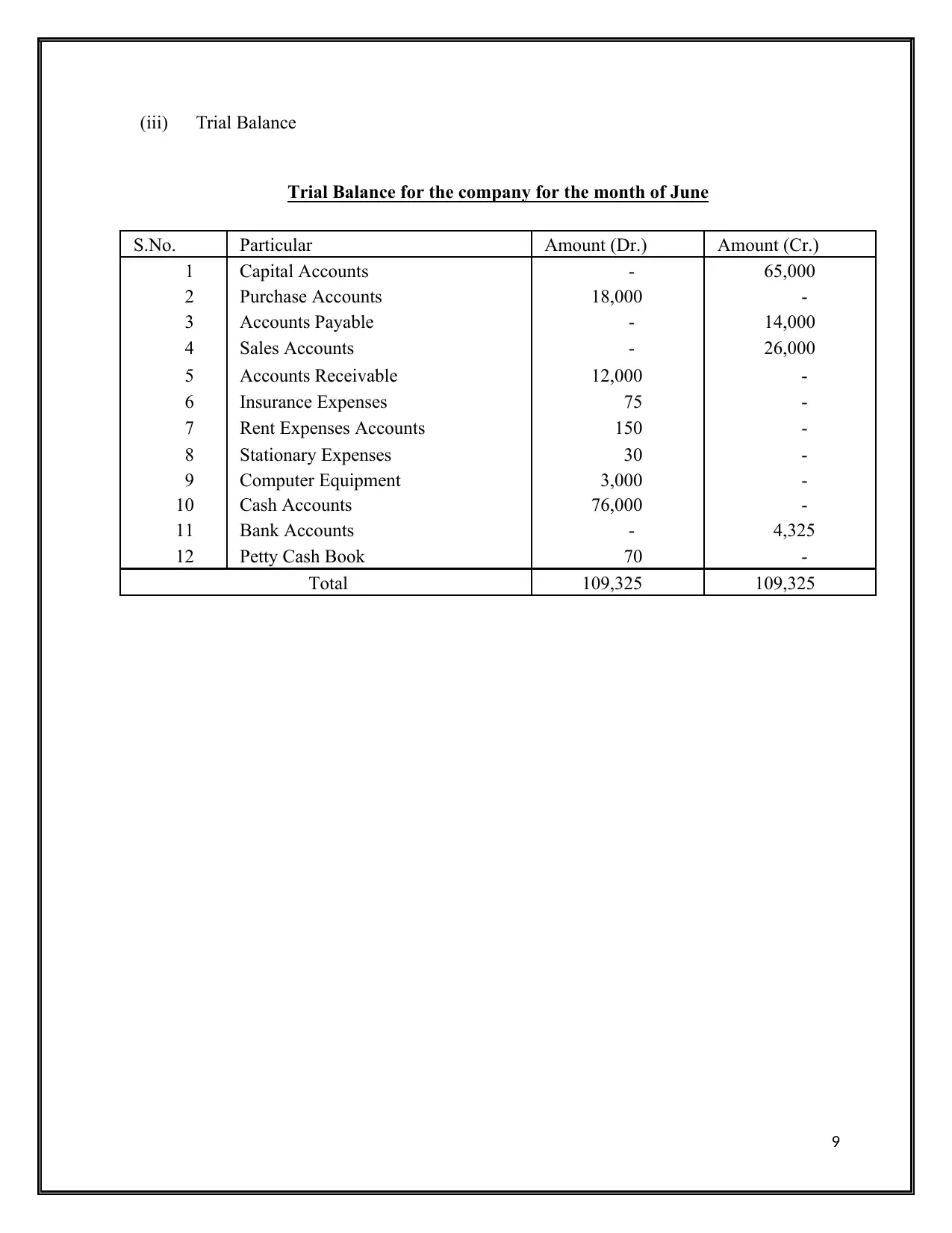

(iii) Trial Balance

Trial Balance for the company for the month of June

S.No. Particular Amount (Dr.) Amount (Cr.)

1 Capital Accounts - 65,000

2 Purchase Accounts 18,000 -

3 Accounts Payable - 14,000

4 Sales Accounts - 26,000

5 Accounts Receivable 12,000 -

6 Insurance Expenses 75 -

7 Rent Expenses Accounts 150 -

8 Stationary Expenses 30 -

9 Computer Equipment 3,000 -

10 Cash Accounts 76,000 -

11 Bank Accounts - 4,325

12 Petty Cash Book 70 -

Total 109,325 109,325

9

Trial Balance for the company for the month of June

S.No. Particular Amount (Dr.) Amount (Cr.)

1 Capital Accounts - 65,000

2 Purchase Accounts 18,000 -

3 Accounts Payable - 14,000

4 Sales Accounts - 26,000

5 Accounts Receivable 12,000 -

6 Insurance Expenses 75 -

7 Rent Expenses Accounts 150 -

8 Stationary Expenses 30 -

9 Computer Equipment 3,000 -

10 Cash Accounts 76,000 -

11 Bank Accounts - 4,325

12 Petty Cash Book 70 -

Total 109,325 109,325

9

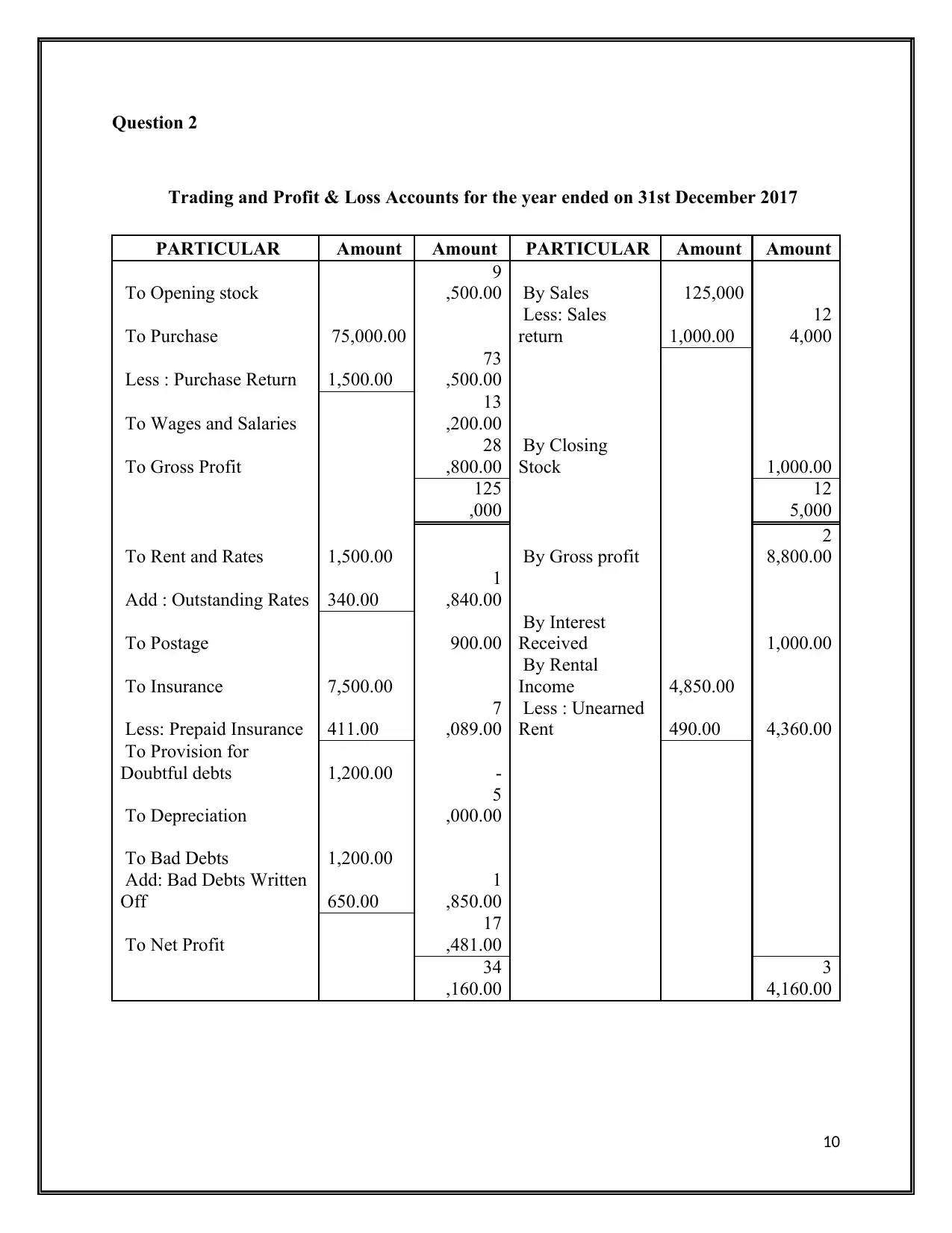

Question 2

Trading and Profit & Loss Accounts for the year ended on 31st December 2017

PARTICULAR Amount Amount PARTICULAR Amount Amount

To Opening stock

9

,500.00 By Sales 125,000

To Purchase 75,000.00

Less: Sales

return 1,000.00

12

4,000

Less : Purchase Return 1,500.00

73

,500.00

To Wages and Salaries

13

,200.00

To Gross Profit

28

,800.00

By Closing

Stock 1,000.00

125

,000

12

5,000

To Rent and Rates 1,500.00 By Gross profit

2

8,800.00

Add : Outstanding Rates 340.00

1

,840.00

To Postage 900.00

By Interest

Received 1,000.00

To Insurance 7,500.00

By Rental

Income 4,850.00

Less: Prepaid Insurance 411.00

7

,089.00

Less : Unearned

Rent 490.00 4,360.00

To Provision for

Doubtful debts 1,200.00 -

To Depreciation

5

,000.00

To Bad Debts 1,200.00

Add: Bad Debts Written

Off 650.00

1

,850.00

To Net Profit

17

,481.00

34

,160.00

3

4,160.00

10

Trading and Profit & Loss Accounts for the year ended on 31st December 2017

PARTICULAR Amount Amount PARTICULAR Amount Amount

To Opening stock

9

,500.00 By Sales 125,000

To Purchase 75,000.00

Less: Sales

return 1,000.00

12

4,000

Less : Purchase Return 1,500.00

73

,500.00

To Wages and Salaries

13

,200.00

To Gross Profit

28

,800.00

By Closing

Stock 1,000.00

125

,000

12

5,000

To Rent and Rates 1,500.00 By Gross profit

2

8,800.00

Add : Outstanding Rates 340.00

1

,840.00

To Postage 900.00

By Interest

Received 1,000.00

To Insurance 7,500.00

By Rental

Income 4,850.00

Less: Prepaid Insurance 411.00

7

,089.00

Less : Unearned

Rent 490.00 4,360.00

To Provision for

Doubtful debts 1,200.00 -

To Depreciation

5

,000.00

To Bad Debts 1,200.00

Add: Bad Debts Written

Off 650.00

1

,850.00

To Net Profit

17

,481.00

34

,160.00

3

4,160.00

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

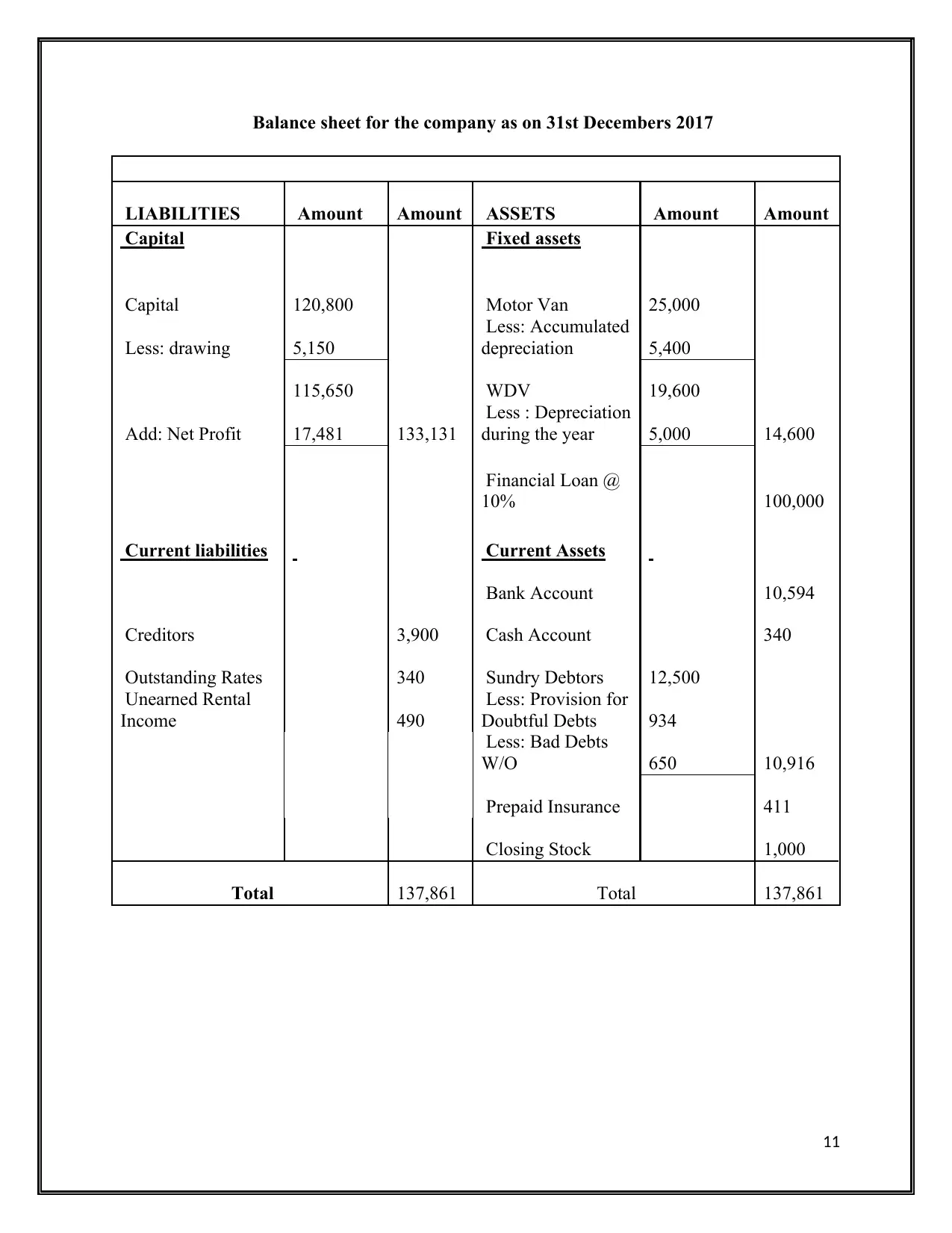

Balance sheet for the company as on 31st Decembers 2017

LIABILITIES Amount Amount ASSETS Amount Amount

Capital Fixed assets

Capital 120,800 Motor Van 25,000

Less: drawing 5,150

Less: Accumulated

depreciation 5,400

115,650 WDV 19,600

Add: Net Profit 17,481 133,131

Less : Depreciation

during the year 5,000 14,600

Financial Loan @

10% 100,000

Current liabilities Current Assets

Bank Account 10,594

Creditors 3,900 Cash Account 340

Outstanding Rates 340 Sundry Debtors 12,500

Unearned Rental

Income 490

Less: Provision for

Doubtful Debts 934

Less: Bad Debts

W/O 650 10,916

Prepaid Insurance 411

Closing Stock 1,000

Total 137,861 Total 137,861

11

LIABILITIES Amount Amount ASSETS Amount Amount

Capital Fixed assets

Capital 120,800 Motor Van 25,000

Less: drawing 5,150

Less: Accumulated

depreciation 5,400

115,650 WDV 19,600

Add: Net Profit 17,481 133,131

Less : Depreciation

during the year 5,000 14,600

Financial Loan @

10% 100,000

Current liabilities Current Assets

Bank Account 10,594

Creditors 3,900 Cash Account 340

Outstanding Rates 340 Sundry Debtors 12,500

Unearned Rental

Income 490

Less: Provision for

Doubtful Debts 934

Less: Bad Debts

W/O 650 10,916

Prepaid Insurance 411

Closing Stock 1,000

Total 137,861 Total 137,861

11

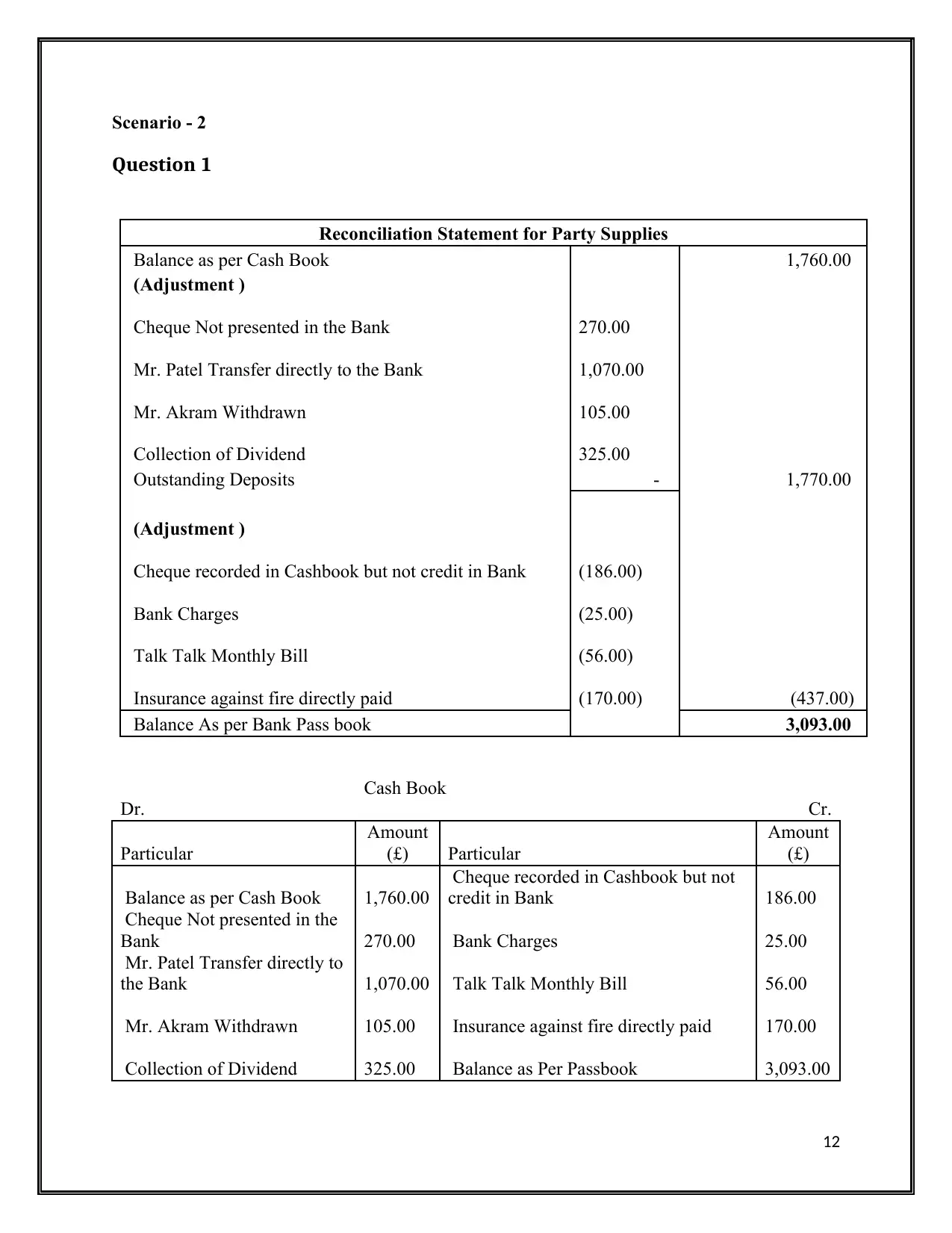

Scenario - 2

Question 1

Reconciliation Statement for Party Supplies

Balance as per Cash Book 1,760.00

(Adjustment )

Cheque Not presented in the Bank 270.00

Mr. Patel Transfer directly to the Bank 1,070.00

Mr. Akram Withdrawn 105.00

Collection of Dividend 325.00

Outstanding Deposits - 1,770.00

(Adjustment )

Cheque recorded in Cashbook but not credit in Bank (186.00)

Bank Charges (25.00)

Talk Talk Monthly Bill (56.00)

Insurance against fire directly paid (170.00) (437.00)

Balance As per Bank Pass book 3,093.00

Dr.

Cash Book

Cr.

Particular

Amount

(£) Particular

Amount

(£)

Balance as per Cash Book 1,760.00

Cheque recorded in Cashbook but not

credit in Bank 186.00

Cheque Not presented in the

Bank 270.00 Bank Charges 25.00

Mr. Patel Transfer directly to

the Bank 1,070.00 Talk Talk Monthly Bill 56.00

Mr. Akram Withdrawn 105.00 Insurance against fire directly paid 170.00

Collection of Dividend 325.00 Balance as Per Passbook 3,093.00

12

Question 1

Reconciliation Statement for Party Supplies

Balance as per Cash Book 1,760.00

(Adjustment )

Cheque Not presented in the Bank 270.00

Mr. Patel Transfer directly to the Bank 1,070.00

Mr. Akram Withdrawn 105.00

Collection of Dividend 325.00

Outstanding Deposits - 1,770.00

(Adjustment )

Cheque recorded in Cashbook but not credit in Bank (186.00)

Bank Charges (25.00)

Talk Talk Monthly Bill (56.00)

Insurance against fire directly paid (170.00) (437.00)

Balance As per Bank Pass book 3,093.00

Dr.

Cash Book

Cr.

Particular

Amount

(£) Particular

Amount

(£)

Balance as per Cash Book 1,760.00

Cheque recorded in Cashbook but not

credit in Bank 186.00

Cheque Not presented in the

Bank 270.00 Bank Charges 25.00

Mr. Patel Transfer directly to

the Bank 1,070.00 Talk Talk Monthly Bill 56.00

Mr. Akram Withdrawn 105.00 Insurance against fire directly paid 170.00

Collection of Dividend 325.00 Balance as Per Passbook 3,093.00

12

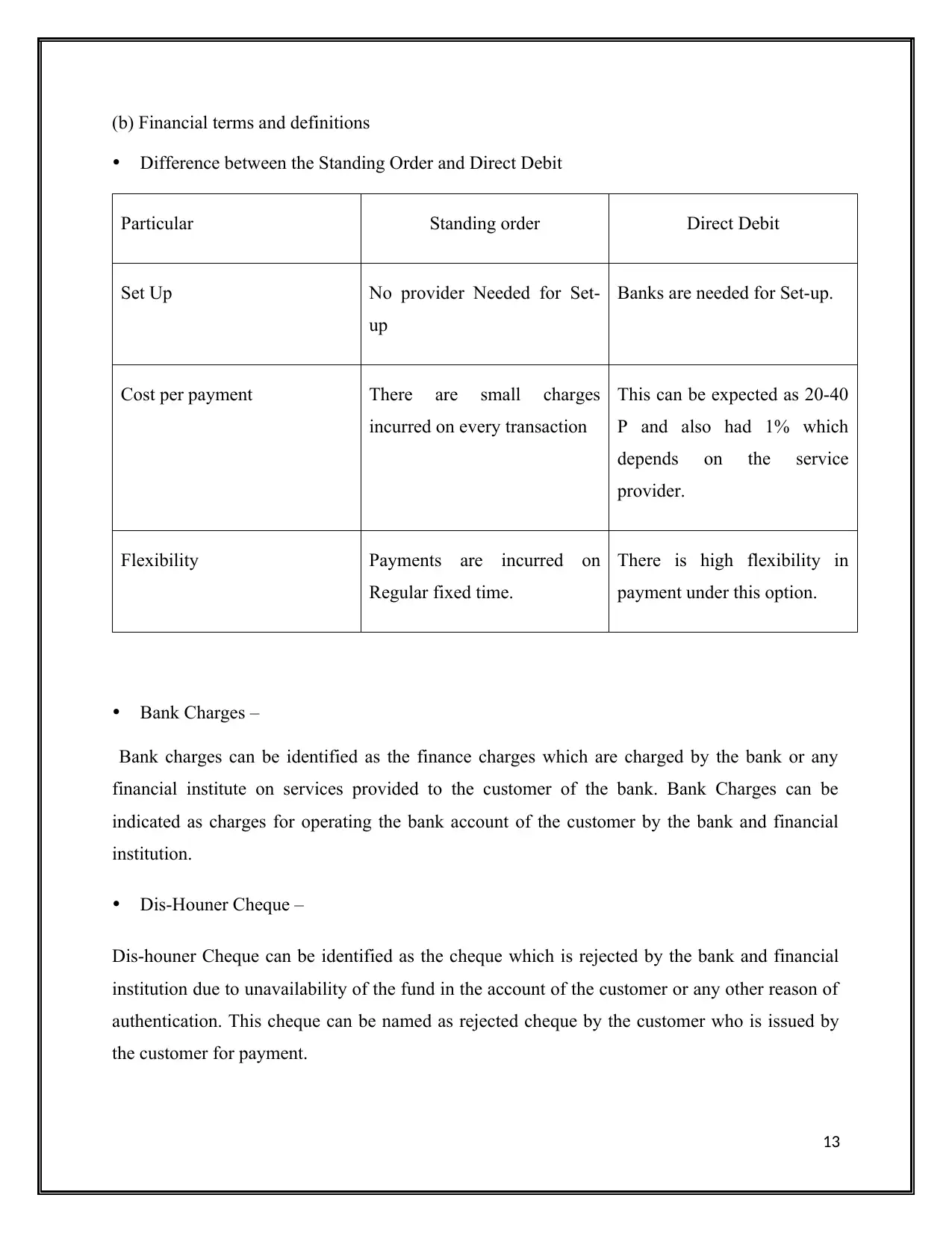

(b) Financial terms and definitions

Difference between the Standing Order and Direct Debit

Particular Standing order Direct Debit

Set Up No provider Needed for Set-

up

Banks are needed for Set-up.

Cost per payment There are small charges

incurred on every transaction

This can be expected as 20-40

P and also had 1% which

depends on the service

provider.

Flexibility Payments are incurred on

Regular fixed time.

There is high flexibility in

payment under this option.

Bank Charges –

Bank charges can be identified as the finance charges which are charged by the bank or any

financial institute on services provided to the customer of the bank. Bank Charges can be

indicated as charges for operating the bank account of the customer by the bank and financial

institution.

Dis-Houner Cheque –

Dis-houner Cheque can be identified as the cheque which is rejected by the bank and financial

institution due to unavailability of the fund in the account of the customer or any other reason of

authentication. This cheque can be named as rejected cheque by the customer who is issued by

the customer for payment.

13

Difference between the Standing Order and Direct Debit

Particular Standing order Direct Debit

Set Up No provider Needed for Set-

up

Banks are needed for Set-up.

Cost per payment There are small charges

incurred on every transaction

This can be expected as 20-40

P and also had 1% which

depends on the service

provider.

Flexibility Payments are incurred on

Regular fixed time.

There is high flexibility in

payment under this option.

Bank Charges –

Bank charges can be identified as the finance charges which are charged by the bank or any

financial institute on services provided to the customer of the bank. Bank Charges can be

indicated as charges for operating the bank account of the customer by the bank and financial

institution.

Dis-Houner Cheque –

Dis-houner Cheque can be identified as the cheque which is rejected by the bank and financial

institution due to unavailability of the fund in the account of the customer or any other reason of

authentication. This cheque can be named as rejected cheque by the customer who is issued by

the customer for payment.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

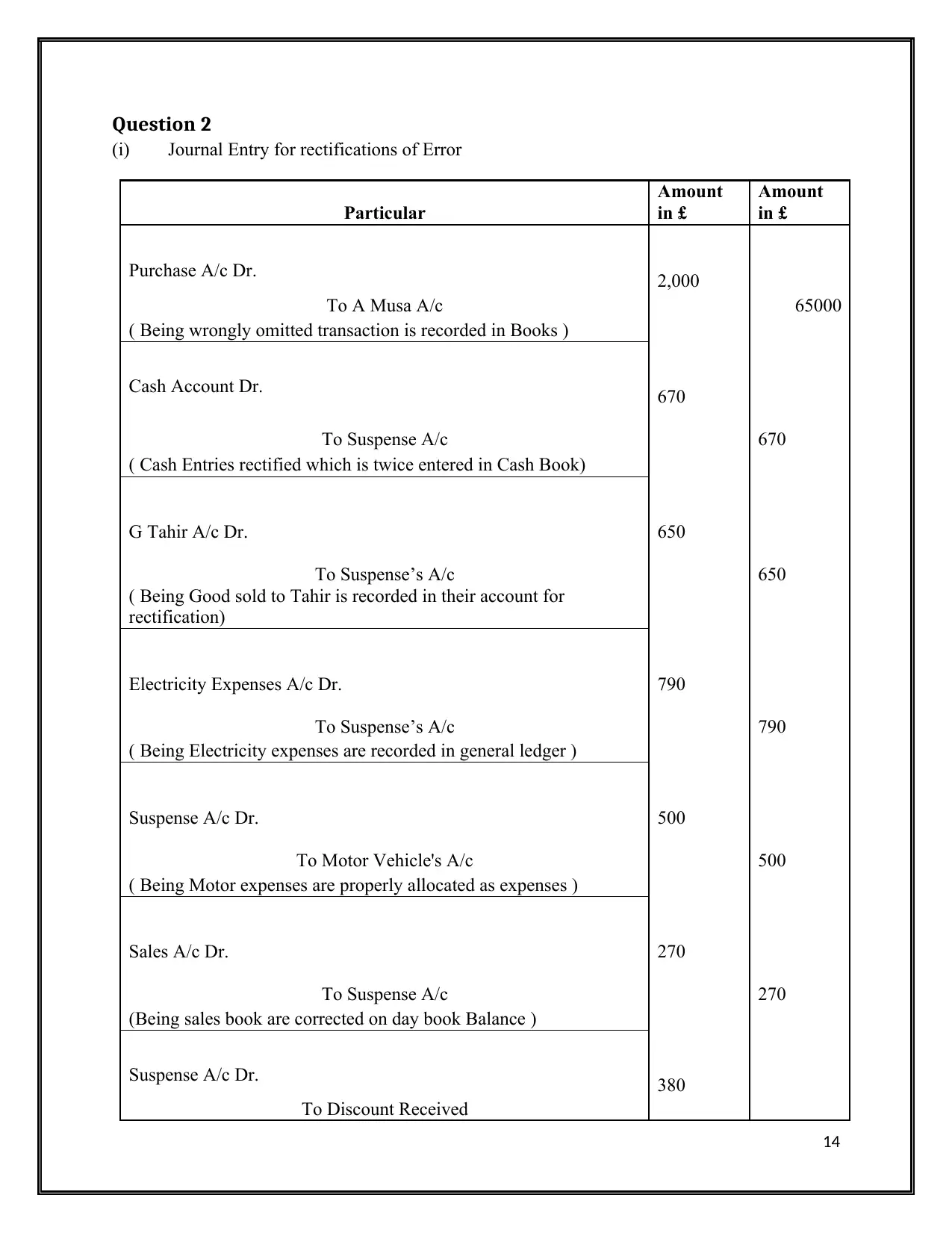

Question 2

(i) Journal Entry for rectifications of Error

Particular

Amount

in £

Amount

in £

Purchase A/c Dr. 2,000

To A Musa A/c 65000

( Being wrongly omitted transaction is recorded in Books )

Cash Account Dr. 670

To Suspense A/c 670

( Cash Entries rectified which is twice entered in Cash Book)

G Tahir A/c Dr. 650

To Suspense’s A/c 650

( Being Good sold to Tahir is recorded in their account for

rectification)

Electricity Expenses A/c Dr. 790

To Suspense’s A/c 790

( Being Electricity expenses are recorded in general ledger )

Suspense A/c Dr. 500

To Motor Vehicle's A/c 500

( Being Motor expenses are properly allocated as expenses )

Sales A/c Dr. 270

To Suspense A/c 270

(Being sales book are corrected on day book Balance )

Suspense A/c Dr. 380

To Discount Received

14

(i) Journal Entry for rectifications of Error

Particular

Amount

in £

Amount

in £

Purchase A/c Dr. 2,000

To A Musa A/c 65000

( Being wrongly omitted transaction is recorded in Books )

Cash Account Dr. 670

To Suspense A/c 670

( Cash Entries rectified which is twice entered in Cash Book)

G Tahir A/c Dr. 650

To Suspense’s A/c 650

( Being Good sold to Tahir is recorded in their account for

rectification)

Electricity Expenses A/c Dr. 790

To Suspense’s A/c 790

( Being Electricity expenses are recorded in general ledger )

Suspense A/c Dr. 500

To Motor Vehicle's A/c 500

( Being Motor expenses are properly allocated as expenses )

Sales A/c Dr. 270

To Suspense A/c 270

(Being sales book are corrected on day book Balance )

Suspense A/c Dr. 380

To Discount Received

14

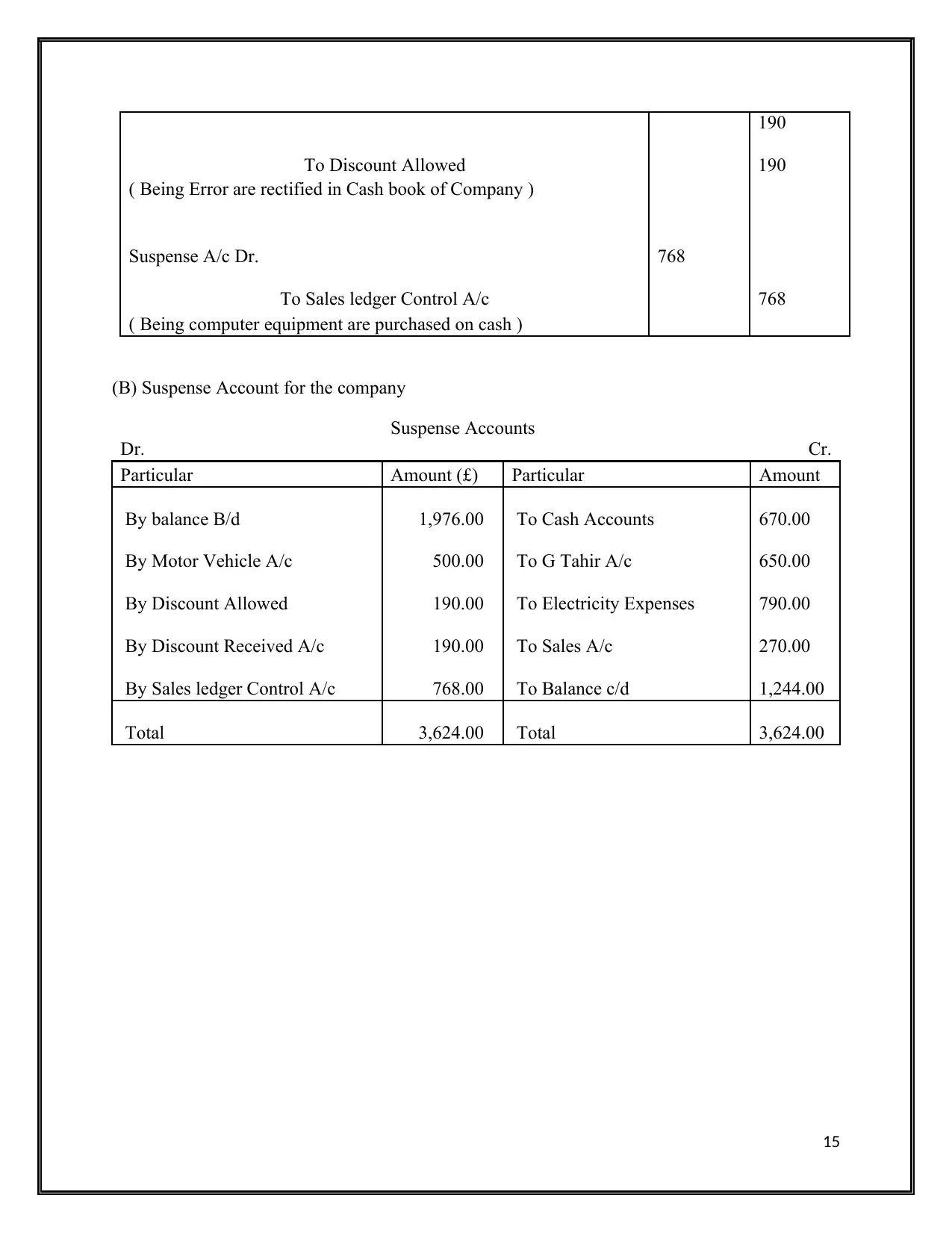

190

To Discount Allowed 190

( Being Error are rectified in Cash book of Company )

Suspense A/c Dr. 768

To Sales ledger Control A/c 768

( Being computer equipment are purchased on cash )

(B) Suspense Account for the company

Dr.

Suspense Accounts

Cr.

Particular Amount (£) Particular Amount

By balance B/d 1,976.00 To Cash Accounts 670.00

By Motor Vehicle A/c 500.00 To G Tahir A/c 650.00

By Discount Allowed 190.00 To Electricity Expenses 790.00

By Discount Received A/c 190.00 To Sales A/c 270.00

By Sales ledger Control A/c 768.00 To Balance c/d 1,244.00

Total 3,624.00 Total 3,624.00

15

To Discount Allowed 190

( Being Error are rectified in Cash book of Company )

Suspense A/c Dr. 768

To Sales ledger Control A/c 768

( Being computer equipment are purchased on cash )

(B) Suspense Account for the company

Dr.

Suspense Accounts

Cr.

Particular Amount (£) Particular Amount

By balance B/d 1,976.00 To Cash Accounts 670.00

By Motor Vehicle A/c 500.00 To G Tahir A/c 650.00

By Discount Allowed 190.00 To Electricity Expenses 790.00

By Discount Received A/c 190.00 To Sales A/c 270.00

By Sales ledger Control A/c 768.00 To Balance c/d 1,244.00

Total 3,624.00 Total 3,624.00

15

References –

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting, Binder

Ready Version. John Wiley & Sons.

Ainsworth, P. and Deines, D., 2019. Introduction to accounting: An integrated approach.

Wiley.

Accountingcoach, 2019, What is a suspense account?, [Online], Accountingcoach, Available

at: https://www.accountingcoach.com/blog/suspense-account [Accessed on 08.06.2019]

Corporatefinanceinstitute, 2019, What is Bank Reconciliation?, [Online],

Corporatefinanceinstitute, Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/bank-reconciliation/

[Accessed on 08.06.2019]

16

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting, Binder

Ready Version. John Wiley & Sons.

Ainsworth, P. and Deines, D., 2019. Introduction to accounting: An integrated approach.

Wiley.

Accountingcoach, 2019, What is a suspense account?, [Online], Accountingcoach, Available

at: https://www.accountingcoach.com/blog/suspense-account [Accessed on 08.06.2019]

Corporatefinanceinstitute, 2019, What is Bank Reconciliation?, [Online],

Corporatefinanceinstitute, Available at:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/bank-reconciliation/

[Accessed on 08.06.2019]

16

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.