Financial Accounting Part 2

VerifiedAdded on 2020/12/24

|9

|1351

|328

Report

AI Summary

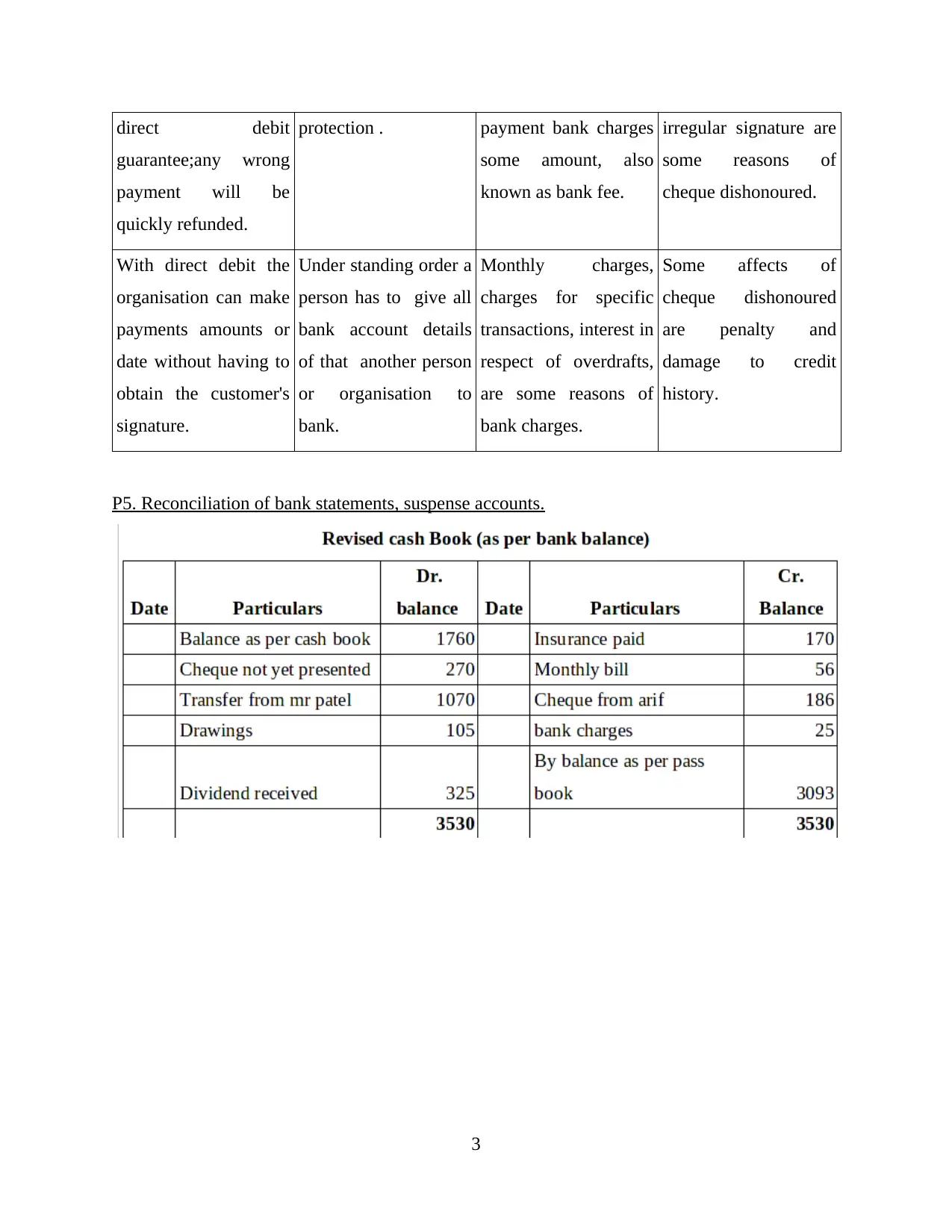

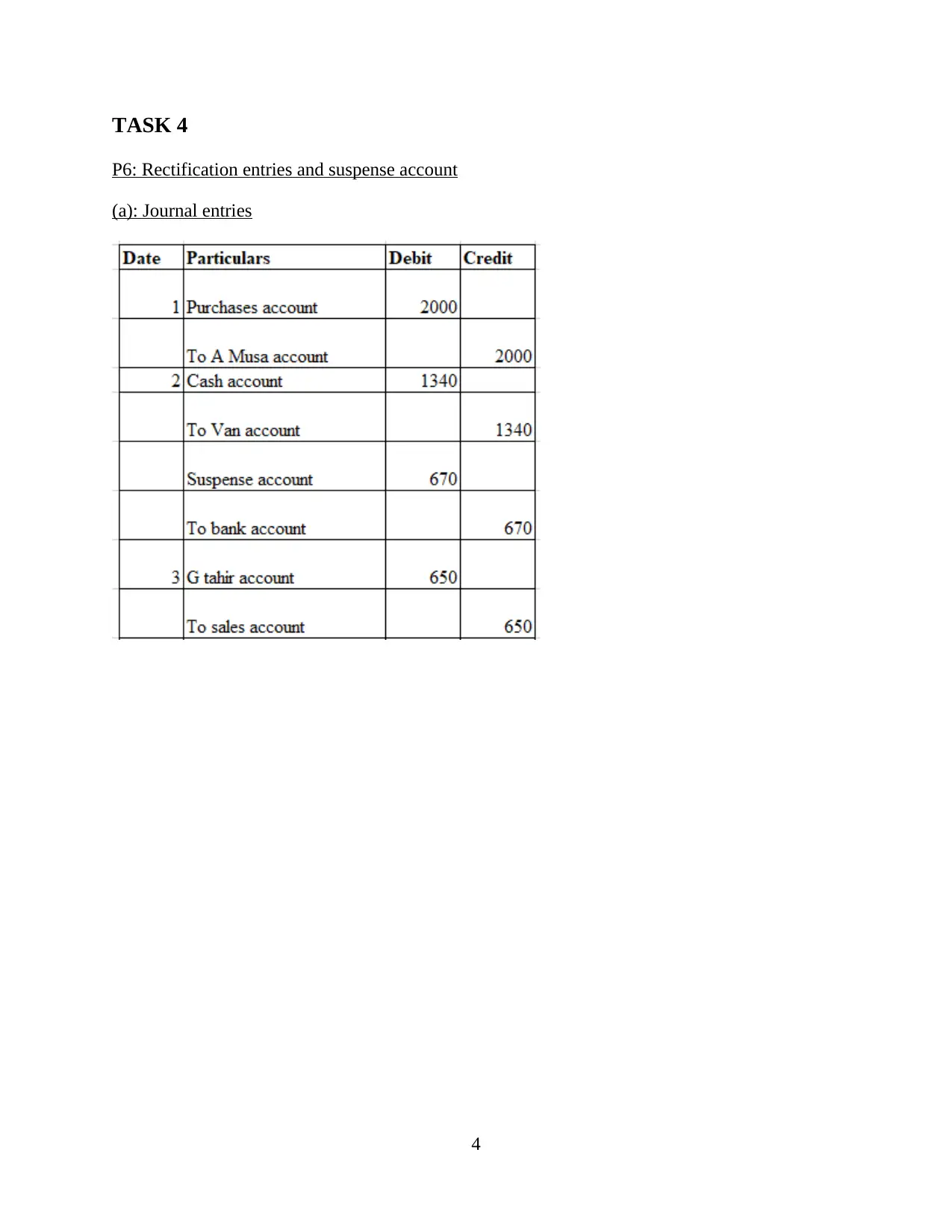

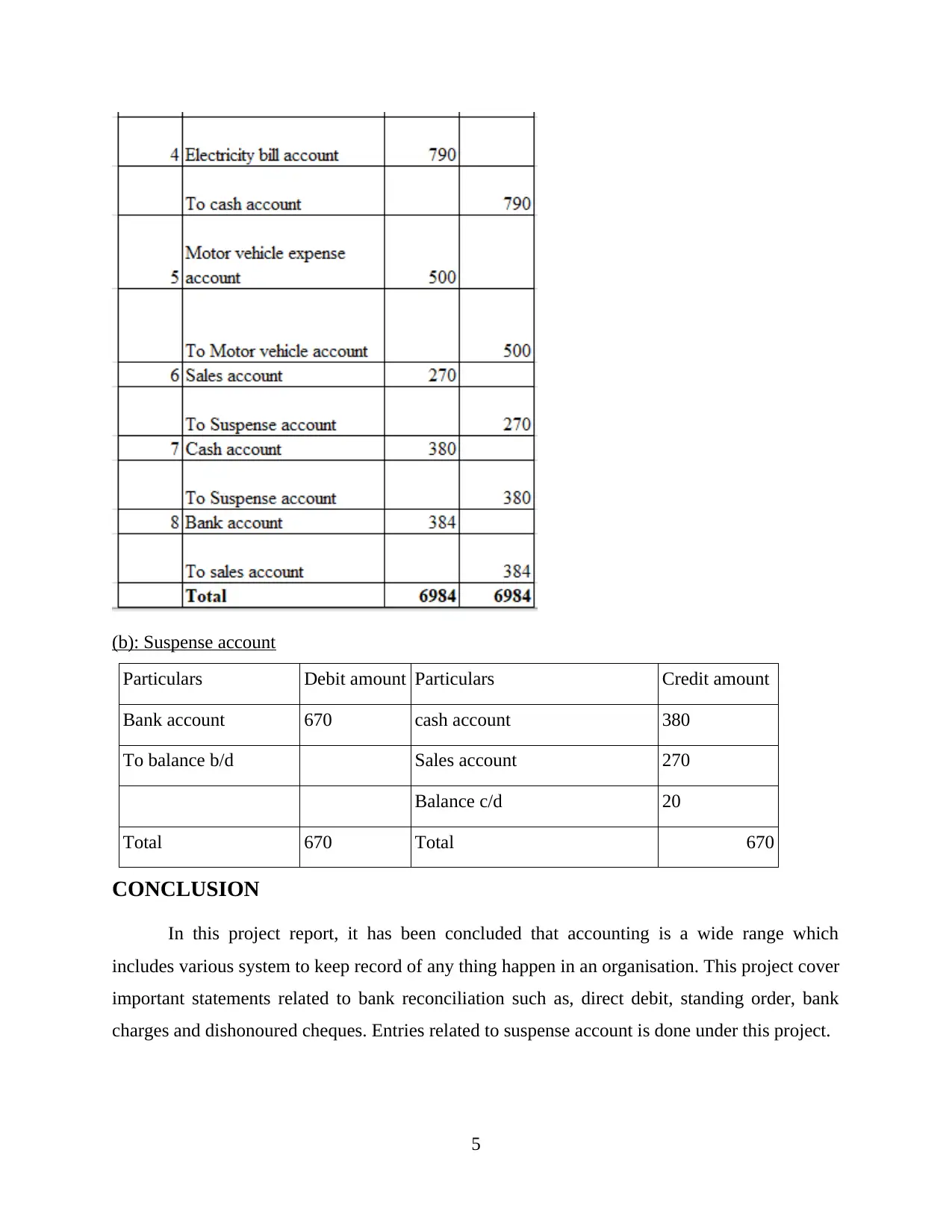

This report explores key concepts in financial accounting, including bank reconciliation, suspense accounts, and rectification entries. It examines the significance of bank statements for businesses, comparing different banking services and their impact on financial records. The report also provides a practical example of reconciling bank statements and demonstrates how to handle suspense accounts with journal entries.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.