Financial Accounting: Users of Accounting Information, Differences with Management Accounting, Fundamental Concepts, and Financial Statements

VerifiedAdded on 2023/06/10

|11

|2154

|190

AI Summary

This report discusses the uses of Sainsbury’s Accounting Information, differences between Financial Accounting and Management Accounting, fundamental concepts of accounting, and the two main types of Financial Statements with sample formats. It identifies four users of Sainsbury’s Accounting Information and why each needs the Accounting Information, explains four main differences between Financial Accounting and Management Accounting, and provides illustrations of four fundamental concepts of accounting. It also distinguishes between the two main types of Financial Statement by constructing sample formats from each.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Identify four users of Sainsbury’s Accounting Information and why each needs the

Accounting Information...............................................................................................................3

Identify and explain four main differences between Financial Accounting and Management

Accounting...................................................................................................................................4

Explain the following four fundamental concepts of accounting giving illustrations:................5

Distinguish between the two main types of Financial Statement by constructing sample

formats from each........................................................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Identify four users of Sainsbury’s Accounting Information and why each needs the

Accounting Information...............................................................................................................3

Identify and explain four main differences between Financial Accounting and Management

Accounting...................................................................................................................................4

Explain the following four fundamental concepts of accounting giving illustrations:................5

Distinguish between the two main types of Financial Statement by constructing sample

formats from each........................................................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial Accounting defines to be specified field of accounting that involves various

activities including recording, summarizing, and reporting the countless proceedings and

transactions resulting from a business concern and its working over a time period. The various

transactions are prepared in different financial statements that records the organisations

performance over a specific time period (Gómez-Villegas, 2021). In this report of financial

accounting we would be answering four different questions that relate to their individual

questioning. In the first question four different uses of Sainsbury’s Accounting Information and

why each one needs this would be identified. In the second question explanation of the

divergence between both the accounting terms financial and management would be answered.

The third question would provide the important concepts of accounting with the help of

examples. The fourth question will help to understand the two different types of financial

statements that are prepared with their respective samples.

MAIN BODY

Identify four users of Sainsbury’s Accounting Information and why each needs the Accounting

Information.

Financial statements prepared are used by different people and corporates in whatever way

they might feel fit for them. The four main uses of financial statements are: Administration: the management of the company is the chief user of the income

statements, balance sheets and cash flows statements, although management itself

prepares these statements still they need to refer those to identify growth and

advancement. It is used to have a look at the liquidity, profitability, cash flows, assets,

debts, finance requirements and various everyday operational activities. This analysis of

statements helps the team to make decisions about the business regarding budgets,

employees, etc. Investors: It being the owner of the companies, need to stay updated on the financial

performance of the company (Sheshukova, and Mukhina, 2018). It is crucial for them as

these statements provide detailed figures about the revenue, expenditure, profitability,

debt load and will aide in finding out the capacbility of the orgsanisation in respect to

Financial Accounting defines to be specified field of accounting that involves various

activities including recording, summarizing, and reporting the countless proceedings and

transactions resulting from a business concern and its working over a time period. The various

transactions are prepared in different financial statements that records the organisations

performance over a specific time period (Gómez-Villegas, 2021). In this report of financial

accounting we would be answering four different questions that relate to their individual

questioning. In the first question four different uses of Sainsbury’s Accounting Information and

why each one needs this would be identified. In the second question explanation of the

divergence between both the accounting terms financial and management would be answered.

The third question would provide the important concepts of accounting with the help of

examples. The fourth question will help to understand the two different types of financial

statements that are prepared with their respective samples.

MAIN BODY

Identify four users of Sainsbury’s Accounting Information and why each needs the Accounting

Information.

Financial statements prepared are used by different people and corporates in whatever way

they might feel fit for them. The four main uses of financial statements are: Administration: the management of the company is the chief user of the income

statements, balance sheets and cash flows statements, although management itself

prepares these statements still they need to refer those to identify growth and

advancement. It is used to have a look at the liquidity, profitability, cash flows, assets,

debts, finance requirements and various everyday operational activities. This analysis of

statements helps the team to make decisions about the business regarding budgets,

employees, etc. Investors: It being the owner of the companies, need to stay updated on the financial

performance of the company (Sheshukova, and Mukhina, 2018). It is crucial for them as

these statements provide detailed figures about the revenue, expenditure, profitability,

debt load and will aide in finding out the capacbility of the orgsanisation in respect to

meeting the short and long – term requirements. The most important for all statements is

the income statement as this statement provides information regarding the profit making

ability of the company. After analysing, these investors can decide whether to stay

invested or take an exit from the company. Competitors: The competitors need to read the financial statements to know the strengths,

weaknesses, opportunities and threats the company is facing. Taking advantage of the

competitor's position is what every company waits for. Additionally, the companies need

to sustain the competitive edge and hence want to comprehend the financial health. Also,

they can change the strategies they used in the past years by looking at the financial

background of other players in the market (Springer, Giner, and Mora, 2020).

Government and authorities: Authorities like sales tax department and income tax

department has to review the accounts to ensure that the company has paid taxes or not.

Moreover, they have to make plan for the future tax predictions which is based on the

performance of the company.

Identify and explain four main differences between Financial Accounting and Management

Accounting.

Financial Accounting is a specific type of accounting that comprises with the method of

abstracting the documents and maintenance of transactions in the businesses operations for a

specific period of time which are represented to the analysts so that they can take better decisions

for the company in terms of financial situation. Financial accounting focuses on revealing the net

profits and losses of a business in a financial year. The primary objective is to provide a fair and

true evaluation of a business.

Management accounting is a procedure to examine the cost of business and operations for

preparation of the internal financial report, records and helps in taking better decision making.

The primary objective is to provide both qualitative and quantitative information to the analysts

and managers, so that it can help them in better decision making and which results in increasing

the profit (Maradona, and Chand, 2018).

Basis Financial Accounting Management Accounting

Aim The main aim is to reduce the It aims for making informed

the income statement as this statement provides information regarding the profit making

ability of the company. After analysing, these investors can decide whether to stay

invested or take an exit from the company. Competitors: The competitors need to read the financial statements to know the strengths,

weaknesses, opportunities and threats the company is facing. Taking advantage of the

competitor's position is what every company waits for. Additionally, the companies need

to sustain the competitive edge and hence want to comprehend the financial health. Also,

they can change the strategies they used in the past years by looking at the financial

background of other players in the market (Springer, Giner, and Mora, 2020).

Government and authorities: Authorities like sales tax department and income tax

department has to review the accounts to ensure that the company has paid taxes or not.

Moreover, they have to make plan for the future tax predictions which is based on the

performance of the company.

Identify and explain four main differences between Financial Accounting and Management

Accounting.

Financial Accounting is a specific type of accounting that comprises with the method of

abstracting the documents and maintenance of transactions in the businesses operations for a

specific period of time which are represented to the analysts so that they can take better decisions

for the company in terms of financial situation. Financial accounting focuses on revealing the net

profits and losses of a business in a financial year. The primary objective is to provide a fair and

true evaluation of a business.

Management accounting is a procedure to examine the cost of business and operations for

preparation of the internal financial report, records and helps in taking better decision making.

The primary objective is to provide both qualitative and quantitative information to the analysts

and managers, so that it can help them in better decision making and which results in increasing

the profit (Maradona, and Chand, 2018).

Basis Financial Accounting Management Accounting

Aim The main aim is to reduce the It aims for making informed

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

cost of the finance and to ensure

sufficient funds to the company

for business operations.

business decisions for management.

Time Financial accounting focuses on

past transactions of an enterprise

and is generally done for one

accounting year.

These reports are maintained when

there is a need in the company for

taking any decision for the business

in terms of expansion and growth.

Format Financial accounts are

represented in a specific format

so that whenever there is need of

comparison with the other

organisations it can be easily

done.

The format of management

accoutring is informal and it is

prepared as per the need of the

management.

Audience It is prepared to provide

inforamtion which can be used

by external parties like

shareholders and lenders.

It is prepared to provide information

to the management of the

organisation and its employees.

Rules Rules of GAAP (Generally

accepted accounting principles)

are followed when preparing of

the financial accounting.

There are no fixed rules in

preparation of management

accounting.

Explain the following four fundamental concepts of accounting giving illustrations:

i) Business Entity: It is an organization setup by individual or a group of person to do

business. This is basically formed to do make income/profit. The type of business

structure decides how the business entity is to be taxed.

Type of business entity:

sole proprietorship- formed by an individual.

sufficient funds to the company

for business operations.

business decisions for management.

Time Financial accounting focuses on

past transactions of an enterprise

and is generally done for one

accounting year.

These reports are maintained when

there is a need in the company for

taking any decision for the business

in terms of expansion and growth.

Format Financial accounts are

represented in a specific format

so that whenever there is need of

comparison with the other

organisations it can be easily

done.

The format of management

accoutring is informal and it is

prepared as per the need of the

management.

Audience It is prepared to provide

inforamtion which can be used

by external parties like

shareholders and lenders.

It is prepared to provide information

to the management of the

organisation and its employees.

Rules Rules of GAAP (Generally

accepted accounting principles)

are followed when preparing of

the financial accounting.

There are no fixed rules in

preparation of management

accounting.

Explain the following four fundamental concepts of accounting giving illustrations:

i) Business Entity: It is an organization setup by individual or a group of person to do

business. This is basically formed to do make income/profit. The type of business

structure decides how the business entity is to be taxed.

Type of business entity:

sole proprietorship- formed by an individual.

Partnership- when two or more person come together to run a business.

LLP- a form of partnership where liability of person is limited.

Company – a separate legal entity created by company’s act formed by person.

ii) Going concern: It is an accounting term used to define continuation of an

organisation. It defines that company need financial resources and other resources to

do business in the market contrary to it may symbolize bankruptcy or discontinuation

of the business. It is one of the basis on which financial accounting is done. An

organisation is said to be going concern when sale of its assets does not implies its

discontinuation. For example: a business entity unable to pay its debt and liabilities,

also the business is continuously running losses therefore decides to shut down the

business such entity is not a going concern (Giner, and Mora, 2019).

iii) Consistency: It is an accounting principal which says that if particular method is

chosen for accounting it should be followed continuously. Such methods can be only

changed if required by law, if auditor required so, improving the financial records

consistency is required in accounting to be more accurate and understandable.

Sometimes director avoid consistency in order to manipulate records and hide

revenue and profit. For example: an organisation uses written down value method

(WDV) for depreciation, now it should not change to straight line method in the next

year.

iv) Monetary value: It is a good and service is a specific amount that market is willing to

pay in order to obtain the service and goods. Basically it is an amount that is given in

order to receive the product and service. Both tangible and intangible assets have a

pre-determined value for exchange in monetary terms. Monetary value makes

exchange easy and efficient. The modern economy has a price labelled for all the

services and goods available in the market. Monetary value is decided by the forces

of demand and supply in the market. For example: real estate, commodities, labour

and services all have a cash price.

LLP- a form of partnership where liability of person is limited.

Company – a separate legal entity created by company’s act formed by person.

ii) Going concern: It is an accounting term used to define continuation of an

organisation. It defines that company need financial resources and other resources to

do business in the market contrary to it may symbolize bankruptcy or discontinuation

of the business. It is one of the basis on which financial accounting is done. An

organisation is said to be going concern when sale of its assets does not implies its

discontinuation. For example: a business entity unable to pay its debt and liabilities,

also the business is continuously running losses therefore decides to shut down the

business such entity is not a going concern (Giner, and Mora, 2019).

iii) Consistency: It is an accounting principal which says that if particular method is

chosen for accounting it should be followed continuously. Such methods can be only

changed if required by law, if auditor required so, improving the financial records

consistency is required in accounting to be more accurate and understandable.

Sometimes director avoid consistency in order to manipulate records and hide

revenue and profit. For example: an organisation uses written down value method

(WDV) for depreciation, now it should not change to straight line method in the next

year.

iv) Monetary value: It is a good and service is a specific amount that market is willing to

pay in order to obtain the service and goods. Basically it is an amount that is given in

order to receive the product and service. Both tangible and intangible assets have a

pre-determined value for exchange in monetary terms. Monetary value makes

exchange easy and efficient. The modern economy has a price labelled for all the

services and goods available in the market. Monetary value is decided by the forces

of demand and supply in the market. For example: real estate, commodities, labour

and services all have a cash price.

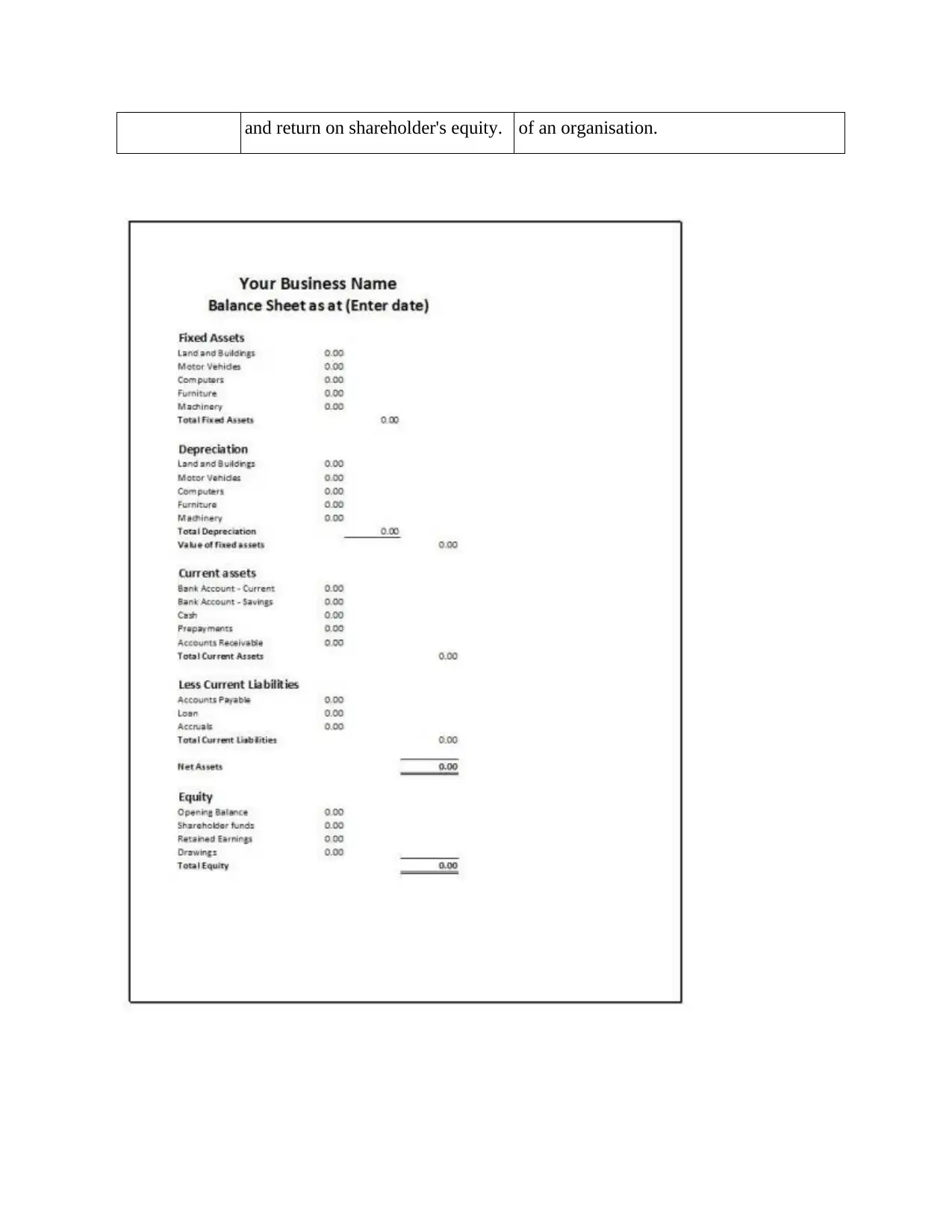

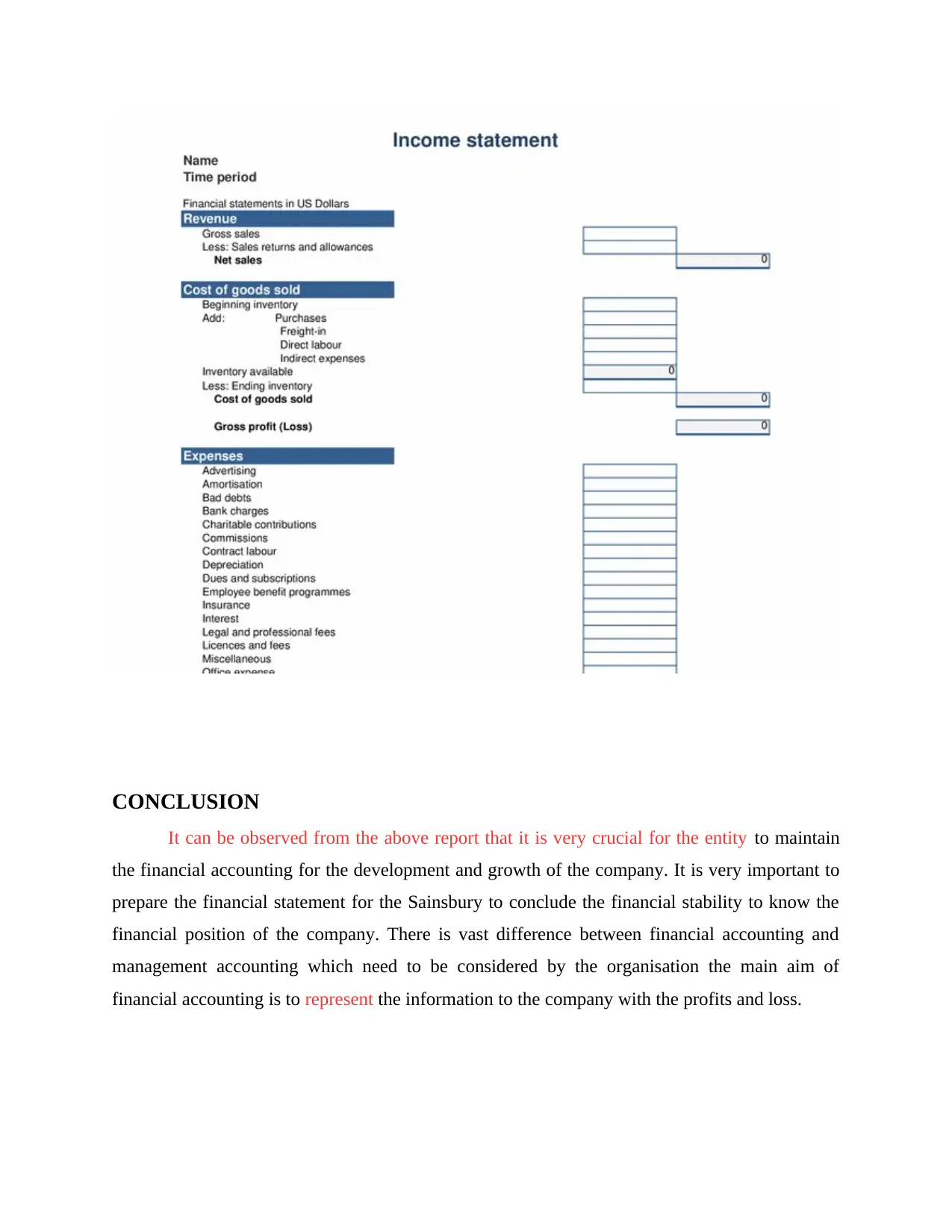

Distinguish between the two main types of Financial Statement by constructing sample formats

from each

Financial statements are an assemblage of concise reports of an entity's financial results, its

financial position and cash flows. These are an authorized record of financial position and results

of an entity, industry or individual person and it represents information in a well organised and

structured manner which makes it easier for its users to understand the organisation's position.

The two main types financial statements are:

Balance Sheet

Income Statement

The balance sheet and income statement supply essential or basic that provides a precis

summary about the financial results and position of the organisation. Major differences between

balance sheet and income statement of a company are tabulated below:

Basis Balance Sheet Income Statement

Meaning It is a financial statement which

evaluates company's financial

performance over a point of time.

It is a financial statement which provides

summary of organisations financial

performance over a specific period of

time. It is also termed as Profit and Loss

(P&L) statement (Lee, and et.al., 2018).

Time The balance sheet addresses the

financial position of an entity for a

one year.

The income statement summarises the

financial stability and performance of the

entity for a longer period of time.

Key items It consists of asset, liabilities and

shareholder's equity.

It comprises of revenue, expense and gains

and losses arising from sale of an asset.

Usage Investors and creditors used it to

ascertain trustworthiness and

availability of asset for pledge and

surety.

Management, investors and stakeholders

use it to determine the performance and

future expectation or anticipation of an

entity.

Financial

Analysis

It helps in determining the

financial position using ratios such

as current ratio, debt to equity ratio

Gross margin ratio, operating margin ratio,

interest coverage ratios are used in

income statement to analyse performance

from each

Financial statements are an assemblage of concise reports of an entity's financial results, its

financial position and cash flows. These are an authorized record of financial position and results

of an entity, industry or individual person and it represents information in a well organised and

structured manner which makes it easier for its users to understand the organisation's position.

The two main types financial statements are:

Balance Sheet

Income Statement

The balance sheet and income statement supply essential or basic that provides a precis

summary about the financial results and position of the organisation. Major differences between

balance sheet and income statement of a company are tabulated below:

Basis Balance Sheet Income Statement

Meaning It is a financial statement which

evaluates company's financial

performance over a point of time.

It is a financial statement which provides

summary of organisations financial

performance over a specific period of

time. It is also termed as Profit and Loss

(P&L) statement (Lee, and et.al., 2018).

Time The balance sheet addresses the

financial position of an entity for a

one year.

The income statement summarises the

financial stability and performance of the

entity for a longer period of time.

Key items It consists of asset, liabilities and

shareholder's equity.

It comprises of revenue, expense and gains

and losses arising from sale of an asset.

Usage Investors and creditors used it to

ascertain trustworthiness and

availability of asset for pledge and

surety.

Management, investors and stakeholders

use it to determine the performance and

future expectation or anticipation of an

entity.

Financial

Analysis

It helps in determining the

financial position using ratios such

as current ratio, debt to equity ratio

Gross margin ratio, operating margin ratio,

interest coverage ratios are used in

income statement to analyse performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and return on shareholder's equity. of an organisation.

CONCLUSION

It can be observed from the above report that it is very crucial for the entity to maintain

the financial accounting for the development and growth of the company. It is very important to

prepare the financial statement for the Sainsbury to conclude the financial stability to know the

financial position of the company. There is vast difference between financial accounting and

management accounting which need to be considered by the organisation the main aim of

financial accounting is to represent the information to the company with the profits and loss.

It can be observed from the above report that it is very crucial for the entity to maintain

the financial accounting for the development and growth of the company. It is very important to

prepare the financial statement for the Sainsbury to conclude the financial stability to know the

financial position of the company. There is vast difference between financial accounting and

management accounting which need to be considered by the organisation the main aim of

financial accounting is to represent the information to the company with the profits and loss.

REFERENCES

Books and Journals

Gómez-Villegas, M., 2021. Towards an accounting of socio-environmental conflicts in South

America. Routledge handbook of environmental accounting, pp.339-349.

Springer, Cham. Giner, B. and Mora, A., 2020. Political interference in private entities' financial

reporting and the public interest: evidence from the Spanish financial crisis. Accounting,

Auditing & Accountability Journal.

Maradona, A.F. and Chand, P., 2018. The pathway of transition to International Financial

Reporting Standards (IFRS) in developing countries: Evidence from Indonesia. Journal

of International Accounting, Auditing and Taxation, 30, pp.57-68.

Anders, S.B., 2020. Nonprofit accounting resources. The CPA Journal, 90(4), pp.64-65.

Giner, B. and Mora, A., 2019. Bank loan loss accounting and its contracting effects: the new

expected loss models. Accounting and Business Research, 49(6), pp.726-752.

Lee, S.M., and et.al., 2018. Material weaknesses in internal control in relation to derivatives and

hedge accounting. Journal of Corporate Accounting & Finance, 29(3), pp.24-31.

Sheshukova, T. and Mukhina, E., 2018, October. Environmental accounting in digital economy.

In The 2018 International Conference on Digital Science (pp. 64-70).

Books and Journals

Gómez-Villegas, M., 2021. Towards an accounting of socio-environmental conflicts in South

America. Routledge handbook of environmental accounting, pp.339-349.

Springer, Cham. Giner, B. and Mora, A., 2020. Political interference in private entities' financial

reporting and the public interest: evidence from the Spanish financial crisis. Accounting,

Auditing & Accountability Journal.

Maradona, A.F. and Chand, P., 2018. The pathway of transition to International Financial

Reporting Standards (IFRS) in developing countries: Evidence from Indonesia. Journal

of International Accounting, Auditing and Taxation, 30, pp.57-68.

Anders, S.B., 2020. Nonprofit accounting resources. The CPA Journal, 90(4), pp.64-65.

Giner, B. and Mora, A., 2019. Bank loan loss accounting and its contracting effects: the new

expected loss models. Accounting and Business Research, 49(6), pp.726-752.

Lee, S.M., and et.al., 2018. Material weaknesses in internal control in relation to derivatives and

hedge accounting. Journal of Corporate Accounting & Finance, 29(3), pp.24-31.

Sheshukova, T. and Mukhina, E., 2018, October. Environmental accounting in digital economy.

In The 2018 International Conference on Digital Science (pp. 64-70).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.