Financial Accounting INTRODUCTION 1

21 Pages5682 Words262 Views

Added on 2020-10-05

About This Document

Financial Accounting INTRODUCTION 1 1.1 Debit and credits 1 1.2 System of double-entry book keeping 1 1.3 Cash-book 1 1.4 Ledger 1 1.5 Trial balance 2 1.6 Accruals 2 1.7 Depreciation 2 1.8 Profit and loss Account 2 1.9 Balance sheet3 1.10 Cash Flow Statement 3 1.11 Financial Statements 3 1.12 Bad debts3 1.13 Bank reconciliation 4 1.14 Control accounts 4 1.15 Suspense accounts 4 TASK 24 2.14 2.29 2.410 2.511 TASK 312 TASK

Financial Accounting INTRODUCTION 1

Added on 2020-10-05

ShareRelated Documents

Financial Accounting

Table of ContentsINTRODUCTION...........................................................................................................................11.1 Debit and credits...................................................................................................................11.2 System of double-entry book keeping...................................................................................11.3 Cash-book.............................................................................................................................11.4 Ledger...................................................................................................................................11.5 Trial balance..........................................................................................................................21.6 Accruals.................................................................................................................................21.7 Depreciation..........................................................................................................................21.8 Profit and loss Account.........................................................................................................21.9 Balance sheet.........................................................................................................................31.10 Cash Flow Statement...........................................................................................................31.11 Financial Statements ..........................................................................................................31.12 Bad debts.............................................................................................................................31.13 Bank reconciliation.............................................................................................................41.14 Control accounts .................................................................................................................41.15 Suspense accounts...............................................................................................................4TASK 2............................................................................................................................................42.1................................................................................................................................................42.2................................................................................................................................................92.4..............................................................................................................................................102.5..............................................................................................................................................11TASK 3..........................................................................................................................................12TASK 4..........................................................................................................................................134.1 Explaining the process used to reconcile the control accounts and clearing the suspenseaccount. ....................................................................................................................................134.2 General entry for the suspense and preparation of control account ...................................14CONCLUSION..............................................................................................................................16REFERENCES..............................................................................................................................17

INTRODUCTIONFinancial accounting is the process of formulating the financial statements by recording,classifying, summarizing interpreting and communicating the results to the users. It is counted asthe most specialized branch of the accounting that traces the financial transactions of thecompany's business. The present study describes various concept of the accounting,understanding of which plays a crucial role in preparing and maintaining the businesstransactions of an entity. The report also includes the preparation of the financial statements ofthe J&J Ltd. Bank reconciliation statements are also formulated of the ABC Ltd. TASK 11.1 Debit and creditsDebit- It refers to the accounting entry which lets to either increases the asset or theexpense account and decreases the liability or the equity account (Zeff, 2016). Debit ispositioned towards the left side in accounting entry. Credits- It is the accounting entry which results in increasing the liability or the equityaccount and decreases the asset or the expense account. Credit is positioned to right side whenthe accounting entry is made. 1.2 System of double-entry book keepingDouble entry book keeping system states that for every transaction in the business, theamounts has to be recorded in minimum two accounts (Bailey and Samuels, 2018). It alsorequires for the amount of all the transactions must be entered as the debits with the equalamount to the credit side. It basically reflects that each business transaction contains both theaspects that is debit and the credit. 1.3 Cash-bookIt is the financial journal that records for all the cash receipts and the expenditures withthe inclusion of bank deposits and the withdrawals. Entries made in cash book are posted to thegeneral ledger (Chychyla, Leone and Minutti-Meza, 2019). It is set upprepared as the ledgerwhere all the cash transaction are entered in a logical order as per the date. It is the book ofthe final and the original entry. 1.4 LedgerIt is the written or the computerized record of the business transactions that are made inan accounting year. Different accounts are prepared for recording all the transactions in the1

ledger. The list of the accounts framed are called as the accounts chart. Classification of therecording made is known as the ledger (Martin and Davari, 2018). It is also called as thesecondary books of accounts. 1.5 Trial balanceIt is the accounting or the book-keeping report that list down the balances in each of thegeneral ledger accounts of an entity. It facilitates the preparation of the financial statements ofthe organization (Orlova and et.al., 2015). The total of the debit side must be equal to the total ofthe credit side in accordance with the trial balance account. 1.6 AccrualsIt refers to the adjustments that are made before the financial statements of the companyare issued. It includes two kinds of the business transactions that are as follows-Such losses, liabilities and the expenses that has been incurred but are not recorded in thebooks of accounts.Assets and the revenues that has been earned but are not recorded in the accountingbooks.1.7 DepreciationIt indicates the fall in the monetary value of an asset over its useful life, due to any wearand the tear or the obsolescence (Smieliauskas and et.al., 2018). Decrease in the value mayincurred because of various factors like unfavorable conditions in the market etc. The assets thatare been depreciated are machinery, currency and the equipment.1.8 Profit and loss AccountIt is thean statement accountthat shows the profit earned and the losses incurred by thecompany in its business during a particular accounting or time period. It allows in viewing thenet profit or the net loss of the business during the year after the deduction of all the income andthe expenditure (de Aguiar, 2018). This statement account summarizes all the costs, expensesand the revenues incurred in a specified period. This statementaccounthelps the firm in knowingits ability or the inability in generating the profits by the increase in the revenue or reducing thecost. It states the financial performance of an entity. 1.9 Balance sheetIt refers to the statement that includes the liabilities, equity capital and the assets of thecorporate at one point of time (Bay, 2018). It depicts the financial position of the enterprise in2

the overall market. It equates the assets and the liabilities of the firm and reflects the truefinancial health of the company. It illustrates the net worth of the business. It is useful for bothinternal and the external users as their decisions are based on the financial information in termsof their investment made in the business. 1.10 Cash Flow StatementIt is a statement that shows the changes in the financial position of the enterprise on thecash basis (Porter, 2019). It reveals about the net effects of all the transactions of the business interms of the cash during a specific accounting period. It records for all the inflows and theoutflows of cash in the business. It enables the firm in knowing the cash position of theircompany in the market. 1.11 Financial Statements Financial statements refer to the reports that are prepared by the management of theorganization for presenting the financial performance and the position of the entity at a point oftime. Financial statements are the set that includes the income statements, balance sheets and thecash flows report (Gordon, 2019). These reports are formulated to facilitate useful informationto the outsiders such as creditors, investors, government and tax authorities. Such statements areconsidered as the major source of evaluating the financial information for the decision makers.Reporting of such information places high focus on the relevance, reliability and the accuracy. Itprovides the true and fair view of the company's overall standing in the market. 1.12 Bad debtsThese are the due receivable that are not paid by the customers and the debtors. It ariseswhen the organization extends too much of the credit to its customers, who are incapable ofmeeting their liability or meeting their debt (Hsieh, Ma and Novoselov, 2019). It occurs due tothe reduced, missing and the delayed payments from the customers. Moreover, when thecustomer misrepresents himself in relation to obtaining the sale on the credit and purchases theproduct with no intention of paying seller. This resulted as the fraud from the side of thecustomers. The bad debts that are attached with the account receivable are reported in the incomestatement as the bad debt expenses or the non-recovered expense account. Two method are usedfor recording the bad debt such as direct write-off method and the allowance method. 3

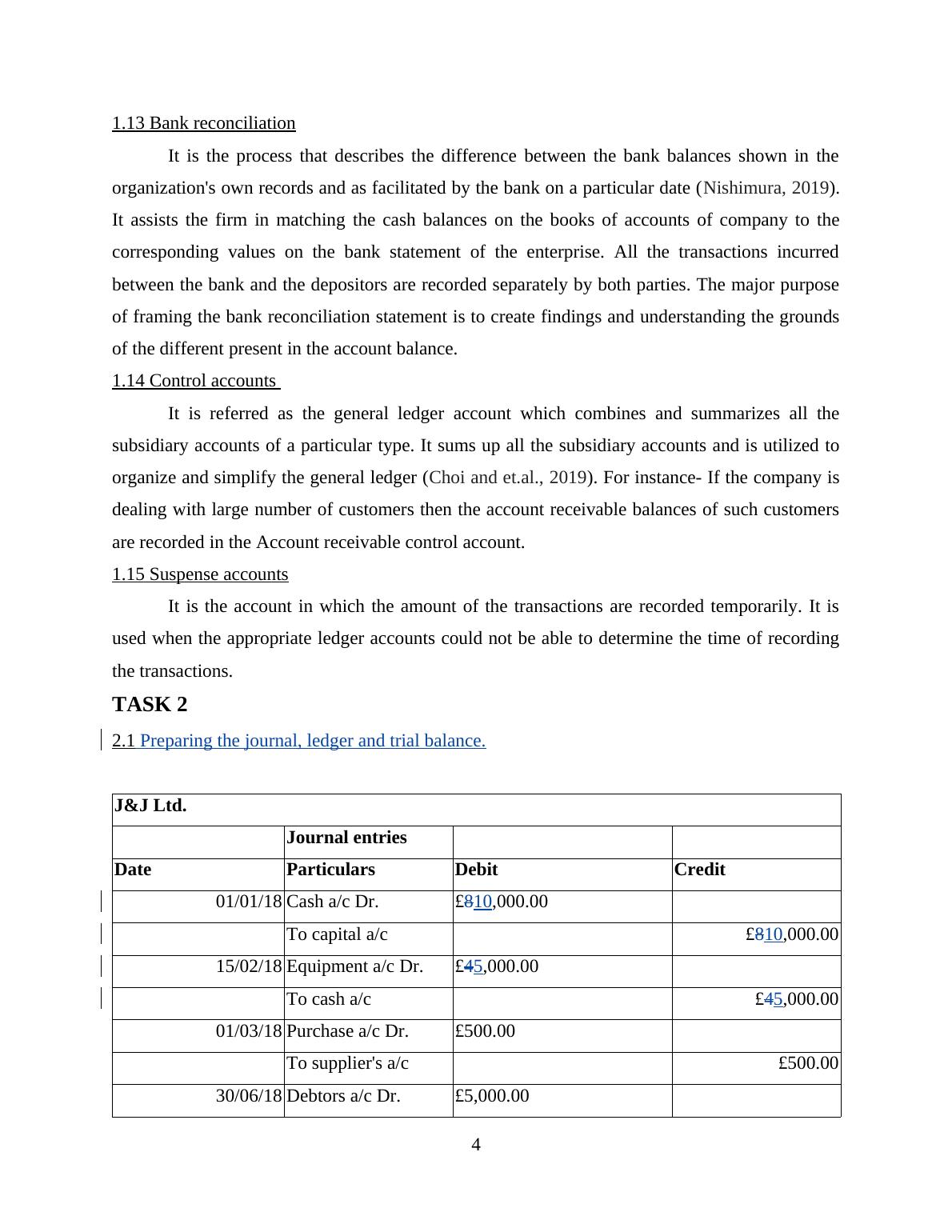

1.13 Bank reconciliationIt is the process that describes the difference between the bank balances shown in theorganization's own records and as facilitated by the bank on a particular date (Nishimura, 2019).It assists the firm in matching the cash balances on the books of accounts of company to thecorresponding values on the bank statement of the enterprise. All the transactions incurredbetween the bank and the depositors are recorded separately by both parties. The major purposeof framing the bank reconciliation statement is to create findings and understanding the groundsof the different present in the account balance. 1.14 Control accounts It is referred as the general ledger account which combines and summarizes all thesubsidiary accounts of a particular type. It sums up all the subsidiary accounts and is utilized toorganize and simplify the general ledger (Choi and et.al., 2019). For instance- If the company isdealing with large number of customers then the account receivable balances of such customersare recorded in the Account receivable control account. 1.15 Suspense accountsIt is the account in which the amount of the transactions are recorded temporarily. It isused when the appropriate ledger accounts could not be able to determine the time of recordingthe transactions. TASK 22.1Preparing the journal, ledger and trial balance.J&J Ltd.Journal entriesDateParticularsDebit Credit01/01/18Cash a/c Dr.£810,000.00To capital a/c£810,000.0015/02/18Equipment a/c Dr.£45,000.00To cash a/c£45,000.0001/03/18Purchase a/c Dr. £500.00To supplier's a/c£500.0030/06/18Debtors a/c Dr.£5,000.00To sales a/c£5,000.0001/07/18Account payable a/c Dr.£400.00To bank a/c£400.004

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Recording Financial Transactionslg...

|18

|4145

|147

Financial Accounting Principles: Book-keeping, Journals, Ledgers, and Control Reconciliation Statementlg...

|13

|3410

|247

Financial Accountinglg...

|20

|4294

|65

Financial Accounting INTRODUCTION 1 TASK 11 Question 1 2 7 TASK 29 Question 1 2 7 CONCLUSION 11 REFERENCES 12 INTRODUCTIONlg...

|14

|1243

|343

Financial Accounting: Concepts and Techniqueslg...

|21

|4301

|64

Financial Accounting: Types of Transactions, Principles, Statementslg...

|17

|4168

|441