Financial Accounting Report: Concepts, Statements, and Stakeholders

VerifiedAdded on 2020/12/24

|18

|4328

|273

Report

AI Summary

This report delves into the realm of financial accounting, focusing on its core principles and practical applications within a business context, specifically using Airdri Limited as a case study. It explores the purposes of financial accounting, including the preparation of income statements, cash flow statements, and financial position statements. The report outlines key regulations, principles, and conventions that govern financial reporting, such as ethical and measurement rules, going concern, matching principle, and convention consistency. It further examines the roles of internal and external stakeholders, providing examples of each. The report includes journal entries and discusses areas that can cause organizational records to vary from banker's records. The report provides an understanding of financial accounting and its importance in decision-making.

FINANCIAL

ACCOUTING

ACCOUTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

a. BUSINESS REPORT..................................................................................................................3

CLIENT 1........................................................................................................................................7

Client 2...........................................................................................................................................11

c. Accounting concepts..............................................................................................................12

d. Types and purposes of depreciation in formulating financial statements..............................13

CLIENT 3......................................................................................................................................13

(B). Areas which cause the organizational records to vary from banker's record.....................14

(c) Imprest in petty cash book...................................................................................................14

CLIENT 4......................................................................................................................................15

CLIENT 5......................................................................................................................................16

REFERENCES..............................................................................................................................19

Contents...........................................................................................................................................2

a. BUSINESS REPORT..................................................................................................................3

CLIENT 1........................................................................................................................................7

Client 2...........................................................................................................................................11

c. Accounting concepts..............................................................................................................12

d. Types and purposes of depreciation in formulating financial statements..............................13

CLIENT 3......................................................................................................................................13

(B). Areas which cause the organizational records to vary from banker's record.....................14

(c) Imprest in petty cash book...................................................................................................14

CLIENT 4......................................................................................................................................15

CLIENT 5......................................................................................................................................16

REFERENCES..............................................................................................................................19

INTRODUCTION

Financial accounting is the field of bookkeeping worried about the deprived, examination

and announcing of monetary exchanges relating to a business (Arvidsson, 2011). All enterprises

need to plan fiscal reports for a particular timeframe and money related reports have present

before partners. It is useful for the association to take viable choices seeing speculation just as

extension. Fiscal reports demonstrates the money related position of the company. To more

readily comprehend this idea Airdri Limited has been chosen which bargains in electronic

segments and it has a place with United Kingdom. In this report, there are following subjects are

secured, for example, budgetary bookkeeping and its motivations, examination of inward and

outside partners, trail balance , asset report, last records for sole dealers, bookkeeping ideas

identified with consistency and prudency. Aside from this it also talk about reasons for getting

ready bank compromise articulations and deals and buy control record.

FINANCIAL ACCOUNTING

Financial accounting is a part of accounting which helps in tracking the financial

transactions of any organisation for operating and managing its operations in a systematic

manner. It helps in recording, summarizing and presenting all the transactions to prepare the

financial statements. The purpose of preparing such statement is to provide information related to

the operations, performance and cash flows to the managers for taking effective decisions

(Edwards and et. al., 2013). All the organisations are required to maintain their financial

transactions in effective manner so that information be able to usable for stakeholders and

owners. This report includes book keeping system, ledger posting system and the reconciliation

statements. Accounting rules, principles, consistency and importance of financial accounts are

also defined in this context.

Financial accounting is the field of bookkeeping worried about the deprived, examination

and announcing of monetary exchanges relating to a business (Arvidsson, 2011). All enterprises

need to plan fiscal reports for a particular timeframe and money related reports have present

before partners. It is useful for the association to take viable choices seeing speculation just as

extension. Fiscal reports demonstrates the money related position of the company. To more

readily comprehend this idea Airdri Limited has been chosen which bargains in electronic

segments and it has a place with United Kingdom. In this report, there are following subjects are

secured, for example, budgetary bookkeeping and its motivations, examination of inward and

outside partners, trail balance , asset report, last records for sole dealers, bookkeeping ideas

identified with consistency and prudency. Aside from this it also talk about reasons for getting

ready bank compromise articulations and deals and buy control record.

FINANCIAL ACCOUNTING

Financial accounting is a part of accounting which helps in tracking the financial

transactions of any organisation for operating and managing its operations in a systematic

manner. It helps in recording, summarizing and presenting all the transactions to prepare the

financial statements. The purpose of preparing such statement is to provide information related to

the operations, performance and cash flows to the managers for taking effective decisions

(Edwards and et. al., 2013). All the organisations are required to maintain their financial

transactions in effective manner so that information be able to usable for stakeholders and

owners. This report includes book keeping system, ledger posting system and the reconciliation

statements. Accounting rules, principles, consistency and importance of financial accounts are

also defined in this context.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a. BUSINESS REPORT

1. Financial Accounting: Financial accounting is a process recording financial transactions to

provide information related to financial performance and position of the organization. All the

financial statements are prepared by considering the local as well as international standards

prescribed. Such accounting helps in collecting and summarizing financial data for the

preparation of statements, such as, income statement, cash flow statement and financial position

statements. All such statements are described below:

Income Statement: Income statements also known as profit & loss statements are

prepared to show the profits and losses of an organization over a period. Such

statements are used to display the organizational revenues, selling and administrative

expenses, incomes and expenses, costs, taxes paid, gross profit, net profit in a systematic

and logical manner. With the help of such statements owners, directors and stakeholders

are able to determine the profitability of the organisation.

Cash flow statement: Cash flow statements are those statements includes transactions

related to the inflows and outflows of an organization during an accounting period. Such

statements provides important information related to the cash requirements and needs

for execution of the functions and operations of business in smooth manner. It reflects

the liquidity position of any organisation.

Financial position statement: Financial position statements are the written records

which conveys the activities and financial performance of any organization. These

statements are inspected by the government agencies, accountants to ensure accuracy in

the operations. Such statements are also known as balance sheet which includes the

details related to assets and liabilities. These are majorly used to take financial and

investing decisions for current as well as future time period.

Regulations related to financial accounting: There are various rules and regulations which are

mandatory to follow in an organization while preparing financial statements in order to

effectively manage the financial transactions by the management for better execution of financial

operations (Francis and et. al., 2013). In order to present the financial information, various

regulations are formed and these are described as :

Financial Reporting Council (FRC): FRC has provided various provisions in specific

and descriptive format. FRC Board is responsible for overall governance and setting

1. Financial Accounting: Financial accounting is a process recording financial transactions to

provide information related to financial performance and position of the organization. All the

financial statements are prepared by considering the local as well as international standards

prescribed. Such accounting helps in collecting and summarizing financial data for the

preparation of statements, such as, income statement, cash flow statement and financial position

statements. All such statements are described below:

Income Statement: Income statements also known as profit & loss statements are

prepared to show the profits and losses of an organization over a period. Such

statements are used to display the organizational revenues, selling and administrative

expenses, incomes and expenses, costs, taxes paid, gross profit, net profit in a systematic

and logical manner. With the help of such statements owners, directors and stakeholders

are able to determine the profitability of the organisation.

Cash flow statement: Cash flow statements are those statements includes transactions

related to the inflows and outflows of an organization during an accounting period. Such

statements provides important information related to the cash requirements and needs

for execution of the functions and operations of business in smooth manner. It reflects

the liquidity position of any organisation.

Financial position statement: Financial position statements are the written records

which conveys the activities and financial performance of any organization. These

statements are inspected by the government agencies, accountants to ensure accuracy in

the operations. Such statements are also known as balance sheet which includes the

details related to assets and liabilities. These are majorly used to take financial and

investing decisions for current as well as future time period.

Regulations related to financial accounting: There are various rules and regulations which are

mandatory to follow in an organization while preparing financial statements in order to

effectively manage the financial transactions by the management for better execution of financial

operations (Francis and et. al., 2013). In order to present the financial information, various

regulations are formed and these are described as :

Financial Reporting Council (FRC): FRC has provided various provisions in specific

and descriptive format. FRC Board is responsible for overall governance and setting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

strategies along with standards and approval of all codes. Such council helps in

promoting integrity and transparency in the day to day transactions of any organization.

Financial Accounting Standards Board ( FASB): FASB is a private, standard setting

authority which provides principles, legislations and rules related to preparation of

financial statements. It is the responsibility of FASB to establish and time to time update

reporting standards which are used by the financial professionals by the organizations.

The standards prescribed by such authority majorly helps managers and accountants to

present and disclose the financial information and accounting policies.

Financial accounting principles and rules: There are various financial accounting rules and

principles which all organizations must follow. Some of them are as follows:

Accounting rules: Some of the accounting rules are:

Ethical rules: Ethical rules are concerned with what is right and what is wrong. Some

guidelines are defined by various associations to feature the fundamental target and logical

reasons which are mandatory to follow by any organization (Horngren and et. al., 2012).

Financial ethics are related to general ethics which are essential for maintaining stability and

harmony in any organisation.

Measurement rules: Measurement rules are related to the money measurement in any

organization. Money measurement defines that an organisation should only record those

transactions which are expressed in terms of money. It helps in focusing only quantitative

information. Such rules are prescribed to measure the transactions and formulating policies for

future.

Boundary rules: Boundary rules are prepared to set future strengths of any organization.

Such rules defines what an organization should do and what not. These helps in establishing the

final documents on regular basis at the end of financial period. Such helps in recording the

transaction along with assumptions where the firm must go as well as various projects to be

accomplish at the end of the accounting year (Liao and et. al., 2014).

Accounting principles: Some of the accounting standards are as follows:

Going Concern: Going concern concept is a fundamental concept in financial

accounting. All organizations work on the principle that they will continue their operation in the

next accounting period and will not discontinue its operations due to any reason. Such concept is

applicable in all the organizations as whole.

promoting integrity and transparency in the day to day transactions of any organization.

Financial Accounting Standards Board ( FASB): FASB is a private, standard setting

authority which provides principles, legislations and rules related to preparation of

financial statements. It is the responsibility of FASB to establish and time to time update

reporting standards which are used by the financial professionals by the organizations.

The standards prescribed by such authority majorly helps managers and accountants to

present and disclose the financial information and accounting policies.

Financial accounting principles and rules: There are various financial accounting rules and

principles which all organizations must follow. Some of them are as follows:

Accounting rules: Some of the accounting rules are:

Ethical rules: Ethical rules are concerned with what is right and what is wrong. Some

guidelines are defined by various associations to feature the fundamental target and logical

reasons which are mandatory to follow by any organization (Horngren and et. al., 2012).

Financial ethics are related to general ethics which are essential for maintaining stability and

harmony in any organisation.

Measurement rules: Measurement rules are related to the money measurement in any

organization. Money measurement defines that an organisation should only record those

transactions which are expressed in terms of money. It helps in focusing only quantitative

information. Such rules are prescribed to measure the transactions and formulating policies for

future.

Boundary rules: Boundary rules are prepared to set future strengths of any organization.

Such rules defines what an organization should do and what not. These helps in establishing the

final documents on regular basis at the end of financial period. Such helps in recording the

transaction along with assumptions where the firm must go as well as various projects to be

accomplish at the end of the accounting year (Liao and et. al., 2014).

Accounting principles: Some of the accounting standards are as follows:

Going Concern: Going concern concept is a fundamental concept in financial

accounting. All organizations work on the principle that they will continue their operation in the

next accounting period and will not discontinue its operations due to any reason. Such concept is

applicable in all the organizations as whole.

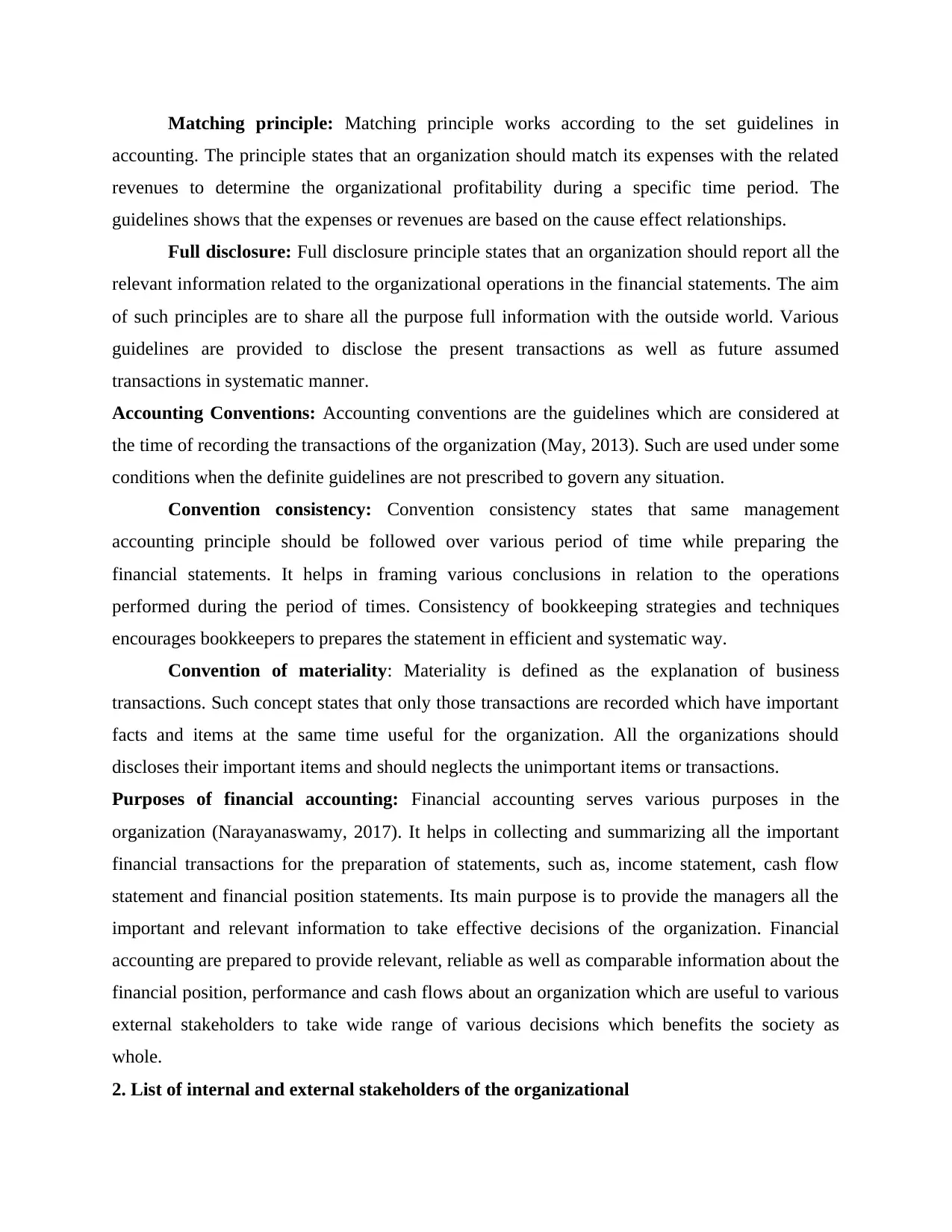

Matching principle: Matching principle works according to the set guidelines in

accounting. The principle states that an organization should match its expenses with the related

revenues to determine the organizational profitability during a specific time period. The

guidelines shows that the expenses or revenues are based on the cause effect relationships.

Full disclosure: Full disclosure principle states that an organization should report all the

relevant information related to the organizational operations in the financial statements. The aim

of such principles are to share all the purpose full information with the outside world. Various

guidelines are provided to disclose the present transactions as well as future assumed

transactions in systematic manner.

Accounting Conventions: Accounting conventions are the guidelines which are considered at

the time of recording the transactions of the organization (May, 2013). Such are used under some

conditions when the definite guidelines are not prescribed to govern any situation.

Convention consistency: Convention consistency states that same management

accounting principle should be followed over various period of time while preparing the

financial statements. It helps in framing various conclusions in relation to the operations

performed during the period of times. Consistency of bookkeeping strategies and techniques

encourages bookkeepers to prepares the statement in efficient and systematic way.

Convention of materiality: Materiality is defined as the explanation of business

transactions. Such concept states that only those transactions are recorded which have important

facts and items at the same time useful for the organization. All the organizations should

discloses their important items and should neglects the unimportant items or transactions.

Purposes of financial accounting: Financial accounting serves various purposes in the

organization (Narayanaswamy, 2017). It helps in collecting and summarizing all the important

financial transactions for the preparation of statements, such as, income statement, cash flow

statement and financial position statements. Its main purpose is to provide the managers all the

important and relevant information to take effective decisions of the organization. Financial

accounting are prepared to provide relevant, reliable as well as comparable information about the

financial position, performance and cash flows about an organization which are useful to various

external stakeholders to take wide range of various decisions which benefits the society as

whole.

2. List of internal and external stakeholders of the organizational

accounting. The principle states that an organization should match its expenses with the related

revenues to determine the organizational profitability during a specific time period. The

guidelines shows that the expenses or revenues are based on the cause effect relationships.

Full disclosure: Full disclosure principle states that an organization should report all the

relevant information related to the organizational operations in the financial statements. The aim

of such principles are to share all the purpose full information with the outside world. Various

guidelines are provided to disclose the present transactions as well as future assumed

transactions in systematic manner.

Accounting Conventions: Accounting conventions are the guidelines which are considered at

the time of recording the transactions of the organization (May, 2013). Such are used under some

conditions when the definite guidelines are not prescribed to govern any situation.

Convention consistency: Convention consistency states that same management

accounting principle should be followed over various period of time while preparing the

financial statements. It helps in framing various conclusions in relation to the operations

performed during the period of times. Consistency of bookkeeping strategies and techniques

encourages bookkeepers to prepares the statement in efficient and systematic way.

Convention of materiality: Materiality is defined as the explanation of business

transactions. Such concept states that only those transactions are recorded which have important

facts and items at the same time useful for the organization. All the organizations should

discloses their important items and should neglects the unimportant items or transactions.

Purposes of financial accounting: Financial accounting serves various purposes in the

organization (Narayanaswamy, 2017). It helps in collecting and summarizing all the important

financial transactions for the preparation of statements, such as, income statement, cash flow

statement and financial position statements. Its main purpose is to provide the managers all the

important and relevant information to take effective decisions of the organization. Financial

accounting are prepared to provide relevant, reliable as well as comparable information about the

financial position, performance and cash flows about an organization which are useful to various

external stakeholders to take wide range of various decisions which benefits the society as

whole.

2. List of internal and external stakeholders of the organizational

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

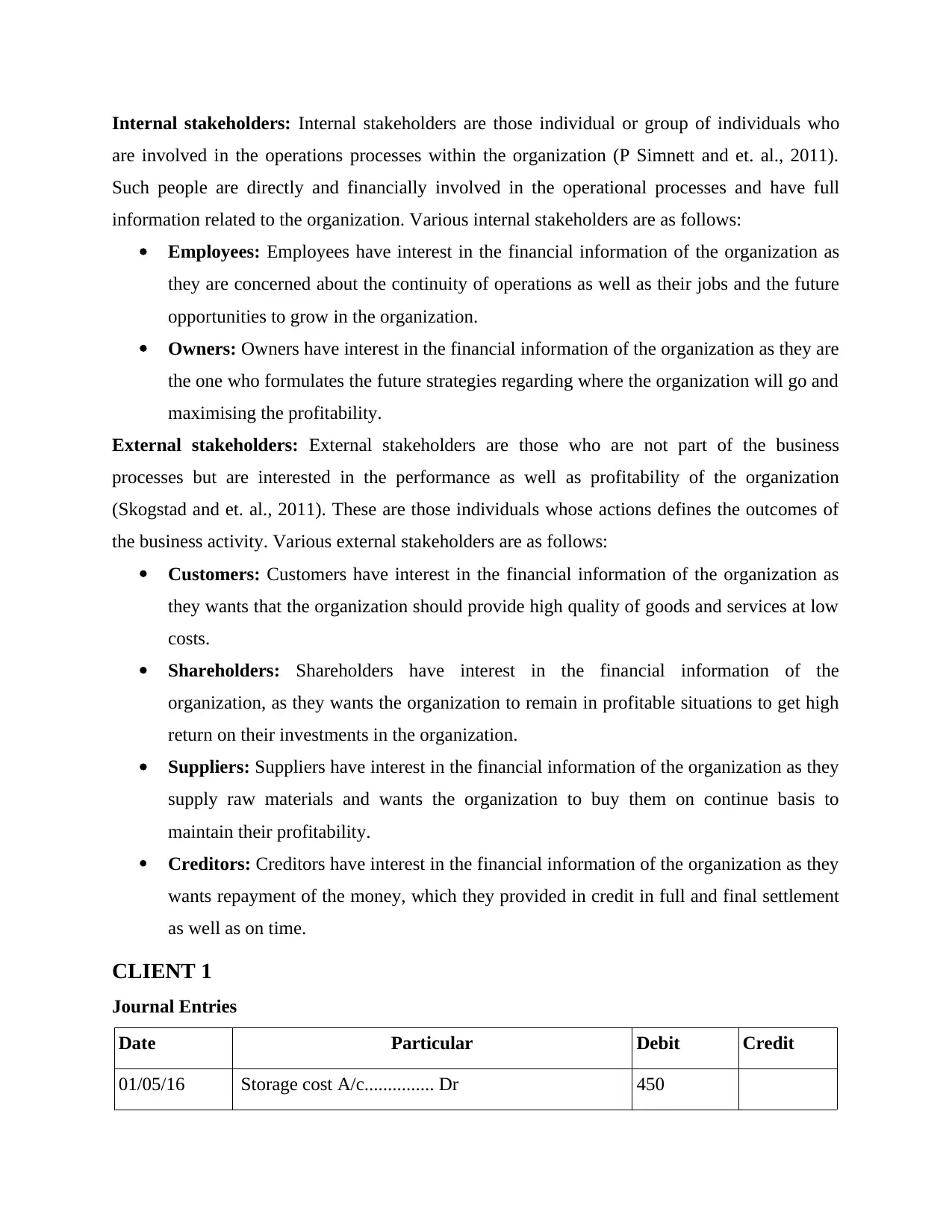

Internal stakeholders: Internal stakeholders are those individual or group of individuals who

are involved in the operations processes within the organization (P Simnett and et. al., 2011).

Such people are directly and financially involved in the operational processes and have full

information related to the organization. Various internal stakeholders are as follows:

Employees: Employees have interest in the financial information of the organization as

they are concerned about the continuity of operations as well as their jobs and the future

opportunities to grow in the organization.

Owners: Owners have interest in the financial information of the organization as they are

the one who formulates the future strategies regarding where the organization will go and

maximising the profitability.

External stakeholders: External stakeholders are those who are not part of the business

processes but are interested in the performance as well as profitability of the organization

(Skogstad and et. al., 2011). These are those individuals whose actions defines the outcomes of

the business activity. Various external stakeholders are as follows:

Customers: Customers have interest in the financial information of the organization as

they wants that the organization should provide high quality of goods and services at low

costs.

Shareholders: Shareholders have interest in the financial information of the

organization, as they wants the organization to remain in profitable situations to get high

return on their investments in the organization.

Suppliers: Suppliers have interest in the financial information of the organization as they

supply raw materials and wants the organization to buy them on continue basis to

maintain their profitability.

Creditors: Creditors have interest in the financial information of the organization as they

wants repayment of the money, which they provided in credit in full and final settlement

as well as on time.

CLIENT 1

Journal Entries

Date Particular Debit Credit

01/05/16 Storage cost A/c............... Dr 450

are involved in the operations processes within the organization (P Simnett and et. al., 2011).

Such people are directly and financially involved in the operational processes and have full

information related to the organization. Various internal stakeholders are as follows:

Employees: Employees have interest in the financial information of the organization as

they are concerned about the continuity of operations as well as their jobs and the future

opportunities to grow in the organization.

Owners: Owners have interest in the financial information of the organization as they are

the one who formulates the future strategies regarding where the organization will go and

maximising the profitability.

External stakeholders: External stakeholders are those who are not part of the business

processes but are interested in the performance as well as profitability of the organization

(Skogstad and et. al., 2011). These are those individuals whose actions defines the outcomes of

the business activity. Various external stakeholders are as follows:

Customers: Customers have interest in the financial information of the organization as

they wants that the organization should provide high quality of goods and services at low

costs.

Shareholders: Shareholders have interest in the financial information of the

organization, as they wants the organization to remain in profitable situations to get high

return on their investments in the organization.

Suppliers: Suppliers have interest in the financial information of the organization as they

supply raw materials and wants the organization to buy them on continue basis to

maintain their profitability.

Creditors: Creditors have interest in the financial information of the organization as they

wants repayment of the money, which they provided in credit in full and final settlement

as well as on time.

CLIENT 1

Journal Entries

Date Particular Debit Credit

01/05/16 Storage cost A/c............... Dr 450

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

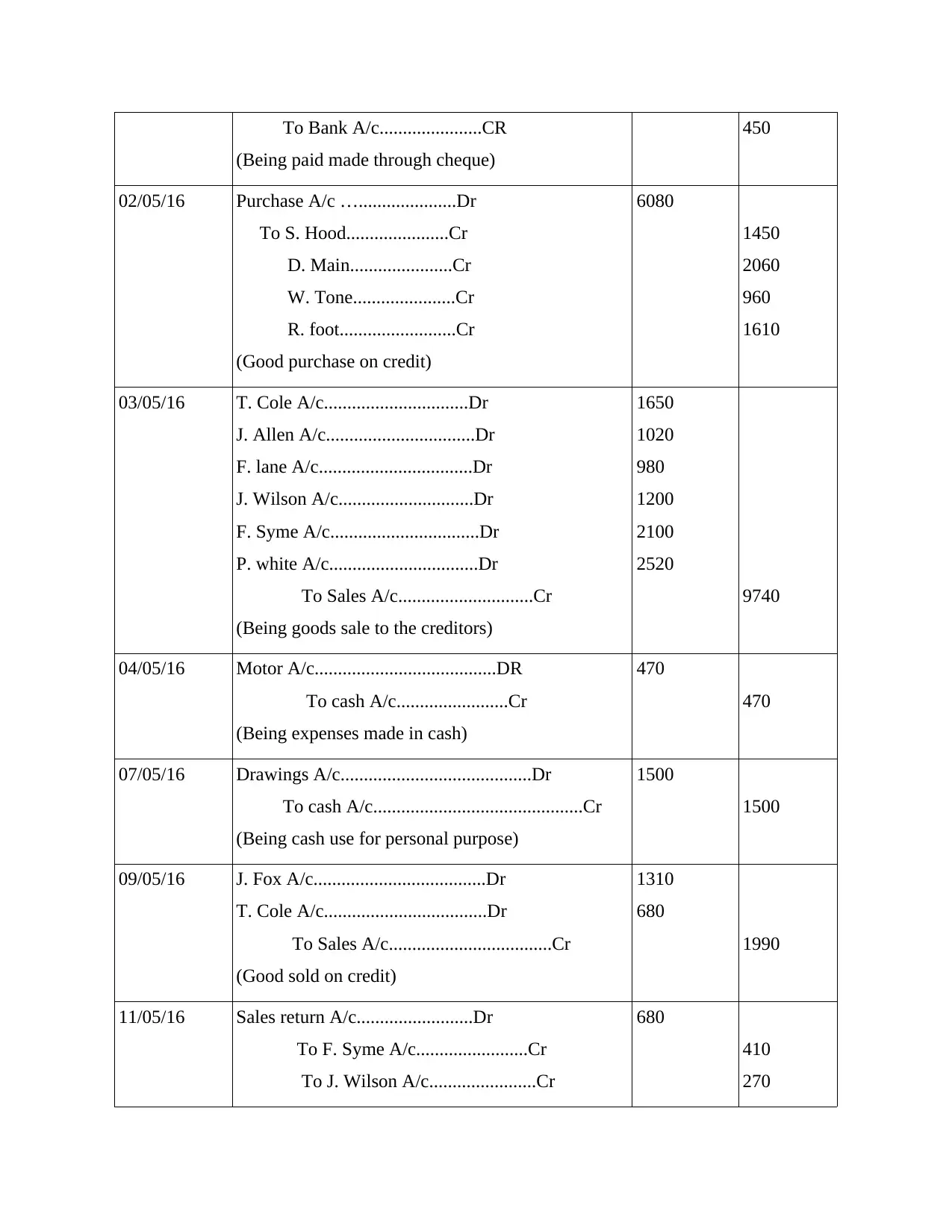

To Bank A/c......................CR

(Being paid made through cheque)

450

02/05/16 Purchase A/c ….....................Dr

To S. Hood......................Cr

D. Main......................Cr

W. Tone......................Cr

R. foot.........................Cr

(Good purchase on credit)

6080

1450

2060

960

1610

03/05/16 T. Cole A/c...............................Dr

J. Allen A/c................................Dr

F. lane A/c.................................Dr

J. Wilson A/c.............................Dr

F. Syme A/c................................Dr

P. white A/c................................Dr

To Sales A/c.............................Cr

(Being goods sale to the creditors)

1650

1020

980

1200

2100

2520

9740

04/05/16 Motor A/c.......................................DR

To cash A/c........................Cr

(Being expenses made in cash)

470

470

07/05/16 Drawings A/c.........................................Dr

To cash A/c.............................................Cr

(Being cash use for personal purpose)

1500

1500

09/05/16 J. Fox A/c.....................................Dr

T. Cole A/c...................................Dr

To Sales A/c...................................Cr

(Good sold on credit)

1310

680

1990

11/05/16 Sales return A/c.........................Dr

To F. Syme A/c........................Cr

To J. Wilson A/c.......................Cr

680

410

270

(Being paid made through cheque)

450

02/05/16 Purchase A/c ….....................Dr

To S. Hood......................Cr

D. Main......................Cr

W. Tone......................Cr

R. foot.........................Cr

(Good purchase on credit)

6080

1450

2060

960

1610

03/05/16 T. Cole A/c...............................Dr

J. Allen A/c................................Dr

F. lane A/c.................................Dr

J. Wilson A/c.............................Dr

F. Syme A/c................................Dr

P. white A/c................................Dr

To Sales A/c.............................Cr

(Being goods sale to the creditors)

1650

1020

980

1200

2100

2520

9740

04/05/16 Motor A/c.......................................DR

To cash A/c........................Cr

(Being expenses made in cash)

470

470

07/05/16 Drawings A/c.........................................Dr

To cash A/c.............................................Cr

(Being cash use for personal purpose)

1500

1500

09/05/16 J. Fox A/c.....................................Dr

T. Cole A/c...................................Dr

To Sales A/c...................................Cr

(Good sold on credit)

1310

680

1990

11/05/16 Sales return A/c.........................Dr

To F. Syme A/c........................Cr

To J. Wilson A/c.......................Cr

680

410

270

(Being goods return to creditors)

16/05/16 Bank A/c.............................Dr

To F. Lane A/c.............................Cr

To P. Mullen A/c.........................Cr

To J. Wilson A/c..........................Cr

To F. Syme A/c.............................Cr

(Being payment received from debtors)

7020

3100

1400

850

1670

19/05/16 R. Foot A/c.............................Dr

To Purchase Return A/c............................Cr

(Goods return to R. foot)

50

50

22/05/16 Purchase A/c.................................Dr

To W. Wright.................................Cr

L. Mole......................................Cr

(Being good brought on credit)

3740

1910

1830

24/05/16 J. Brown A/c.....................................Dr

S. Hood A/c.......................................Dr

R. Foot A/c........................................Dr

To Bank A/c.....................................Cr

(Being payment made to creditors)

4600

3600

1400

9600

27/05/16 Salary A/c.....................Dr

To Bank A/c..................Cr

(Being Salary made through cheque)

4800

4800

30/05/16 Business Rate A/c..........................Dr

To bank A/c...................................Cr

(Rate paid through cheques)

1320

1320

Ledger posting

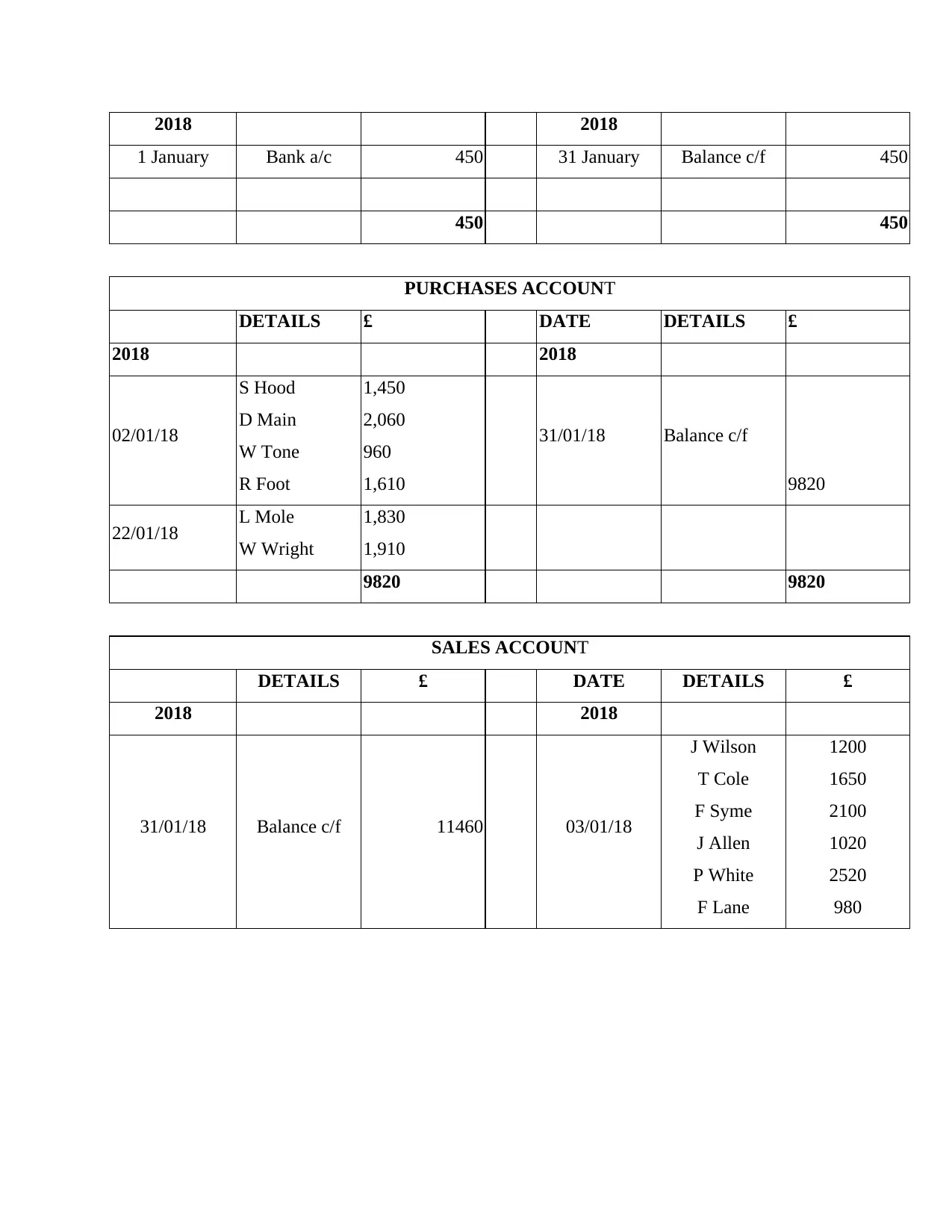

STORAGE COSTS ACCOUNT

DETAILS £ DATE DETAILS £

16/05/16 Bank A/c.............................Dr

To F. Lane A/c.............................Cr

To P. Mullen A/c.........................Cr

To J. Wilson A/c..........................Cr

To F. Syme A/c.............................Cr

(Being payment received from debtors)

7020

3100

1400

850

1670

19/05/16 R. Foot A/c.............................Dr

To Purchase Return A/c............................Cr

(Goods return to R. foot)

50

50

22/05/16 Purchase A/c.................................Dr

To W. Wright.................................Cr

L. Mole......................................Cr

(Being good brought on credit)

3740

1910

1830

24/05/16 J. Brown A/c.....................................Dr

S. Hood A/c.......................................Dr

R. Foot A/c........................................Dr

To Bank A/c.....................................Cr

(Being payment made to creditors)

4600

3600

1400

9600

27/05/16 Salary A/c.....................Dr

To Bank A/c..................Cr

(Being Salary made through cheque)

4800

4800

30/05/16 Business Rate A/c..........................Dr

To bank A/c...................................Cr

(Rate paid through cheques)

1320

1320

Ledger posting

STORAGE COSTS ACCOUNT

DETAILS £ DATE DETAILS £

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018 2018

1 January Bank a/c 450 31 January Balance c/f 450

450 450

PURCHASES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

02/01/18

S Hood

D Main

W Tone

R Foot

1,450

2,060

960

1,610

31/01/18 Balance c/f

9820

22/01/18 L Mole

W Wright

1,830

1,910

9820 9820

SALES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31/01/18 Balance c/f 11460 03/01/18

J Wilson

T Cole

F Syme

J Allen

P White

F Lane

1200

1650

2100

1020

2520

980

1 January Bank a/c 450 31 January Balance c/f 450

450 450

PURCHASES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

02/01/18

S Hood

D Main

W Tone

R Foot

1,450

2,060

960

1,610

31/01/18 Balance c/f

9820

22/01/18 L Mole

W Wright

1,830

1,910

9820 9820

SALES ACCOUNT

DETAILS £ DATE DETAILS £

2018 2018

31/01/18 Balance c/f 11460 03/01/18

J Wilson

T Cole

F Syme

J Allen

P White

F Lane

1200

1650

2100

1020

2520

980

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

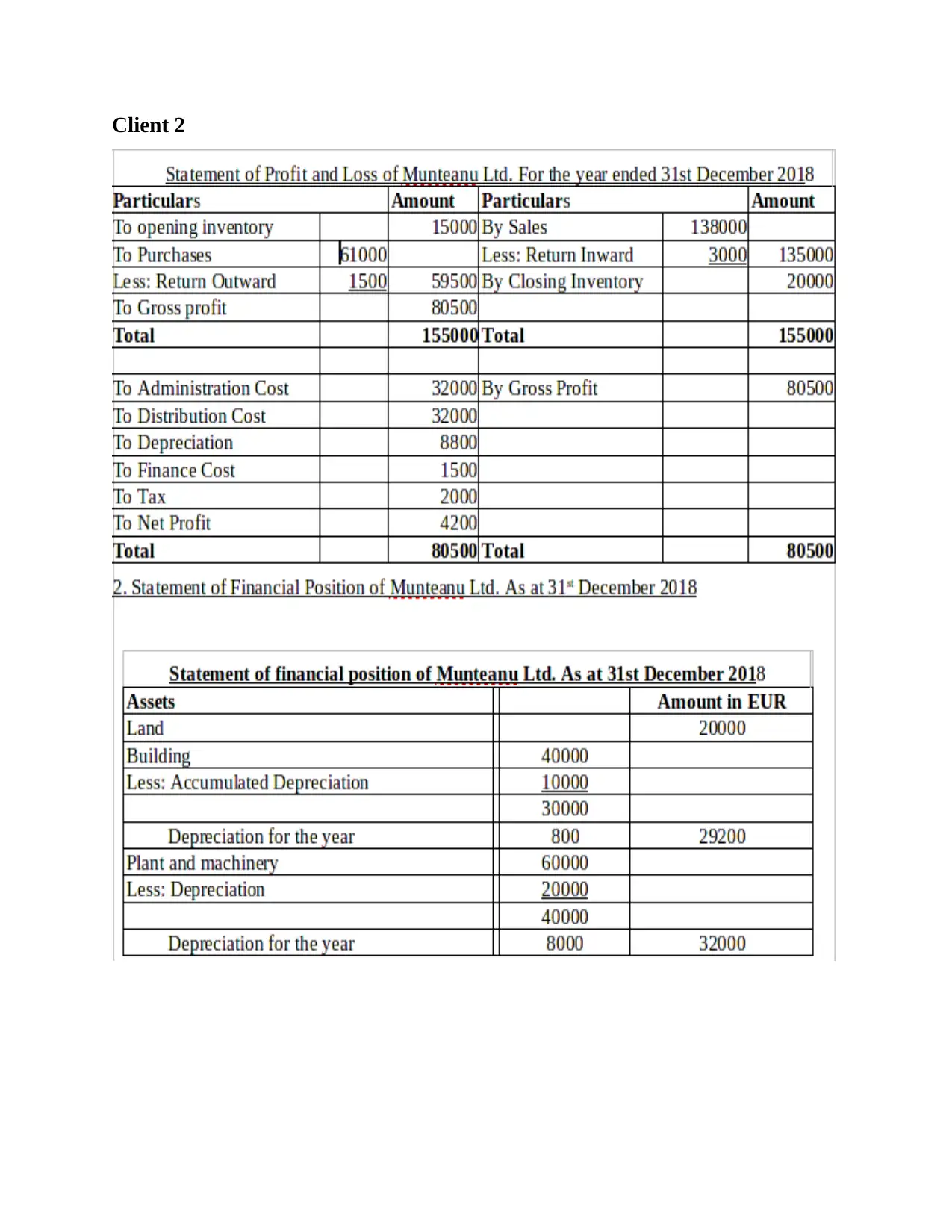

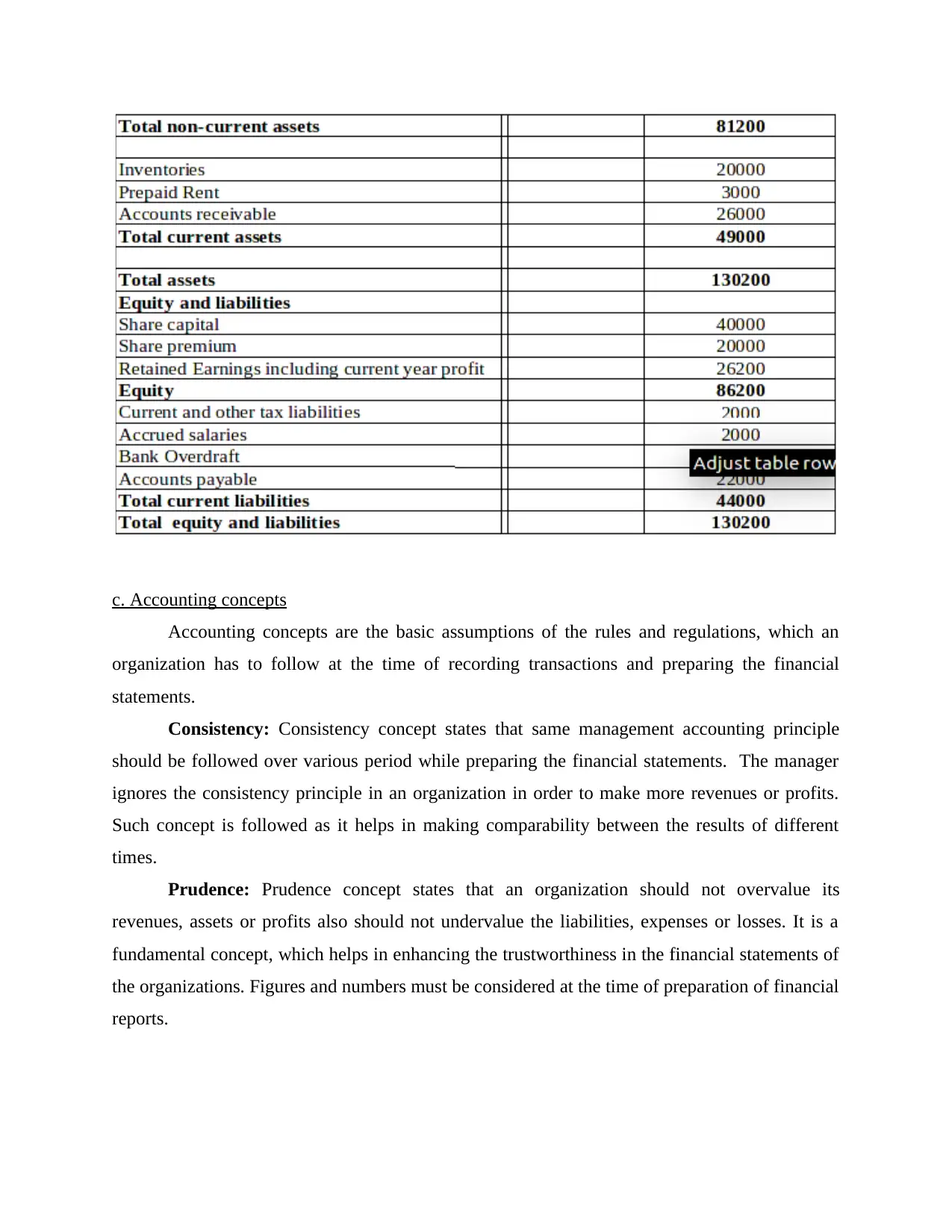

Client 2

c. Accounting concepts

Accounting concepts are the basic assumptions of the rules and regulations, which an

organization has to follow at the time of recording transactions and preparing the financial

statements.

Consistency: Consistency concept states that same management accounting principle

should be followed over various period while preparing the financial statements. The manager

ignores the consistency principle in an organization in order to make more revenues or profits.

Such concept is followed as it helps in making comparability between the results of different

times.

Prudence: Prudence concept states that an organization should not overvalue its

revenues, assets or profits also should not undervalue the liabilities, expenses or losses. It is a

fundamental concept, which helps in enhancing the trustworthiness in the financial statements of

the organizations. Figures and numbers must be considered at the time of preparation of financial

reports.

Accounting concepts are the basic assumptions of the rules and regulations, which an

organization has to follow at the time of recording transactions and preparing the financial

statements.

Consistency: Consistency concept states that same management accounting principle

should be followed over various period while preparing the financial statements. The manager

ignores the consistency principle in an organization in order to make more revenues or profits.

Such concept is followed as it helps in making comparability between the results of different

times.

Prudence: Prudence concept states that an organization should not overvalue its

revenues, assets or profits also should not undervalue the liabilities, expenses or losses. It is a

fundamental concept, which helps in enhancing the trustworthiness in the financial statements of

the organizations. Figures and numbers must be considered at the time of preparation of financial

reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.