Financial Analysis Report: Vodafone vs. Deutsche Telekom (2016-2017)

VerifiedAdded on 2022/11/14

|14

|2428

|226

Report

AI Summary

This report presents a comprehensive financial analysis of Vodafone Group PLC, evaluating its performance for the fiscal years 2016 and 2017. The analysis includes the calculation and interpretation of various financial ratios, such as profitability ratios (gross profit margin, return on equity, return on sales), liquidity ratios (current ratio, quick ratio), asset utilization ratios, gearing ratio, and interest coverage ratio. The report also compares Vodafone's financial performance with its competitor, Deutsche Telekom, highlighting key differences in their financial strategies and outcomes. The analysis explores reasons for these differences, considering factors like consumer demand, cost leadership, and investment strategies. The impact of competitors on Vodafone's financial position is also discussed, focusing on revenue reduction and asset investment. The report concludes with an assessment of Vodafone's overall financial health, emphasizing the importance of strategic adjustments to maintain competitiveness and improve financial performance. The report is based on the Vodafone Group Plc Annual Report 2017 and financial data from Deutsche Telekom.

FINANCIAL ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 1

Contents

Introduction...........................................................................................................................................2

Overview of the organisation.................................................................................................................2

Task 1....................................................................................................................................................3

Task 2: Financial Analysis....................................................................................................................6

Compare to Deutsche Telekom..........................................................................................................6

Reasons of differences.......................................................................................................................7

Impact of competitors........................................................................................................................8

Conclusion.............................................................................................................................................9

Bibliography........................................................................................................................................11

Contents

Introduction...........................................................................................................................................2

Overview of the organisation.................................................................................................................2

Task 1....................................................................................................................................................3

Task 2: Financial Analysis....................................................................................................................6

Compare to Deutsche Telekom..........................................................................................................6

Reasons of differences.......................................................................................................................7

Impact of competitors........................................................................................................................8

Conclusion.............................................................................................................................................9

Bibliography........................................................................................................................................11

FINANCIAL ANALYSIS 2

Introduction

Financial analysis is the process of evaluating the financial data to assess the performance of

an organisation. The position of the company is also analysed in order to expand the business

or to beat the competitors. There are different ways in which the company analyse its

financial performance such as vertical, leverage, growth, valuation, profitability, liquidity, etc

(CFI, 2019). The process helps the company to evaluate the growth rates in order to extend

the business in the different countries.

The main aim of this report is to understand the evaluation of financial ratio. In this report,

Vodafone has been taken into consideration in order to analyse the financial position of the

company. In this report, the financial ratio has been evaluated of the years of 2017 and 2016.

Deutsche Telekom has been taken into consideration in order to compare the financial

performance of Vodafone in the market.

Overview of the organisation

Vodafone Group plc is a British multinational company in England. The company operates in

the region of Asia, Europe, Africa and Oceania. The company have its own networks in the

different 25 countries and it also has the partner networks in 47 further countries. As the

company is operates in the different countries and have large business that is why; it is

required to evaluate the financial performance (Vodafone, 2018a). The company also have

the large number of competitors in the market. It is requires for the company to evaluate the

performance of Deutsche Telekom in order to evaluate the high threat of competition.

Deutsche Telekom is also a telecommunication company in German. It is one of the largest

telecommunication providers in the country of Europe (Deutsche Telekom, 2018). Deutsche

Introduction

Financial analysis is the process of evaluating the financial data to assess the performance of

an organisation. The position of the company is also analysed in order to expand the business

or to beat the competitors. There are different ways in which the company analyse its

financial performance such as vertical, leverage, growth, valuation, profitability, liquidity, etc

(CFI, 2019). The process helps the company to evaluate the growth rates in order to extend

the business in the different countries.

The main aim of this report is to understand the evaluation of financial ratio. In this report,

Vodafone has been taken into consideration in order to analyse the financial position of the

company. In this report, the financial ratio has been evaluated of the years of 2017 and 2016.

Deutsche Telekom has been taken into consideration in order to compare the financial

performance of Vodafone in the market.

Overview of the organisation

Vodafone Group plc is a British multinational company in England. The company operates in

the region of Asia, Europe, Africa and Oceania. The company have its own networks in the

different 25 countries and it also has the partner networks in 47 further countries. As the

company is operates in the different countries and have large business that is why; it is

required to evaluate the financial performance (Vodafone, 2018a). The company also have

the large number of competitors in the market. It is requires for the company to evaluate the

performance of Deutsche Telekom in order to evaluate the high threat of competition.

Deutsche Telekom is also a telecommunication company in German. It is one of the largest

telecommunication providers in the country of Europe (Deutsche Telekom, 2018). Deutsche

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 3

Telekom can beat the company with the high competition that is why; it is selected to

evaluate the position of Vodafone in the industry.

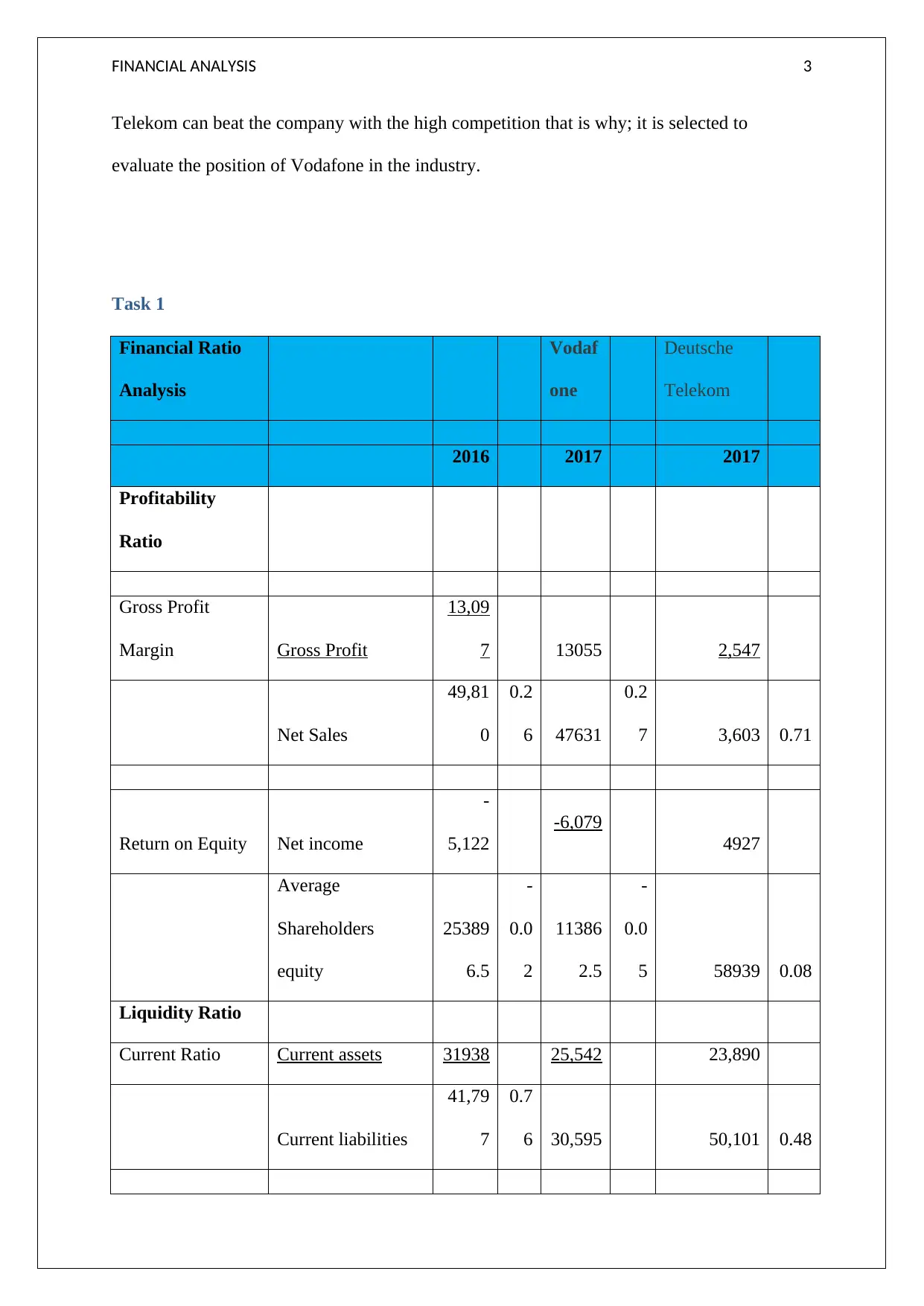

Task 1

Financial Ratio

Analysis

Vodaf

one

Deutsche

Telekom

2016 2017 2017

Profitability

Ratio

Gross Profit

Margin Gross Profit

13,09

7 13055 2,547

Net Sales

49,81

0

0.2

6 47631

0.2

7 3,603 0.71

Return on Equity Net income

-

5,122

-6,079

4927

Average

Shareholders

equity

25389

6.5

-

0.0

2

11386

2.5

-

0.0

5 58939 0.08

Liquidity Ratio

Current Ratio Current assets 31938 25,542 23,890

Current liabilities

41,79

7

0.7

6 30,595 50,101 0.48

Telekom can beat the company with the high competition that is why; it is selected to

evaluate the position of Vodafone in the industry.

Task 1

Financial Ratio

Analysis

Vodaf

one

Deutsche

Telekom

2016 2017 2017

Profitability

Ratio

Gross Profit

Margin Gross Profit

13,09

7 13055 2,547

Net Sales

49,81

0

0.2

6 47631

0.2

7 3,603 0.71

Return on Equity Net income

-

5,122

-6,079

4927

Average

Shareholders

equity

25389

6.5

-

0.0

2

11386

2.5

-

0.0

5 58939 0.08

Liquidity Ratio

Current Ratio Current assets 31938 25,542 23,890

Current liabilities

41,79

7

0.7

6 30,595 50,101 0.48

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 4

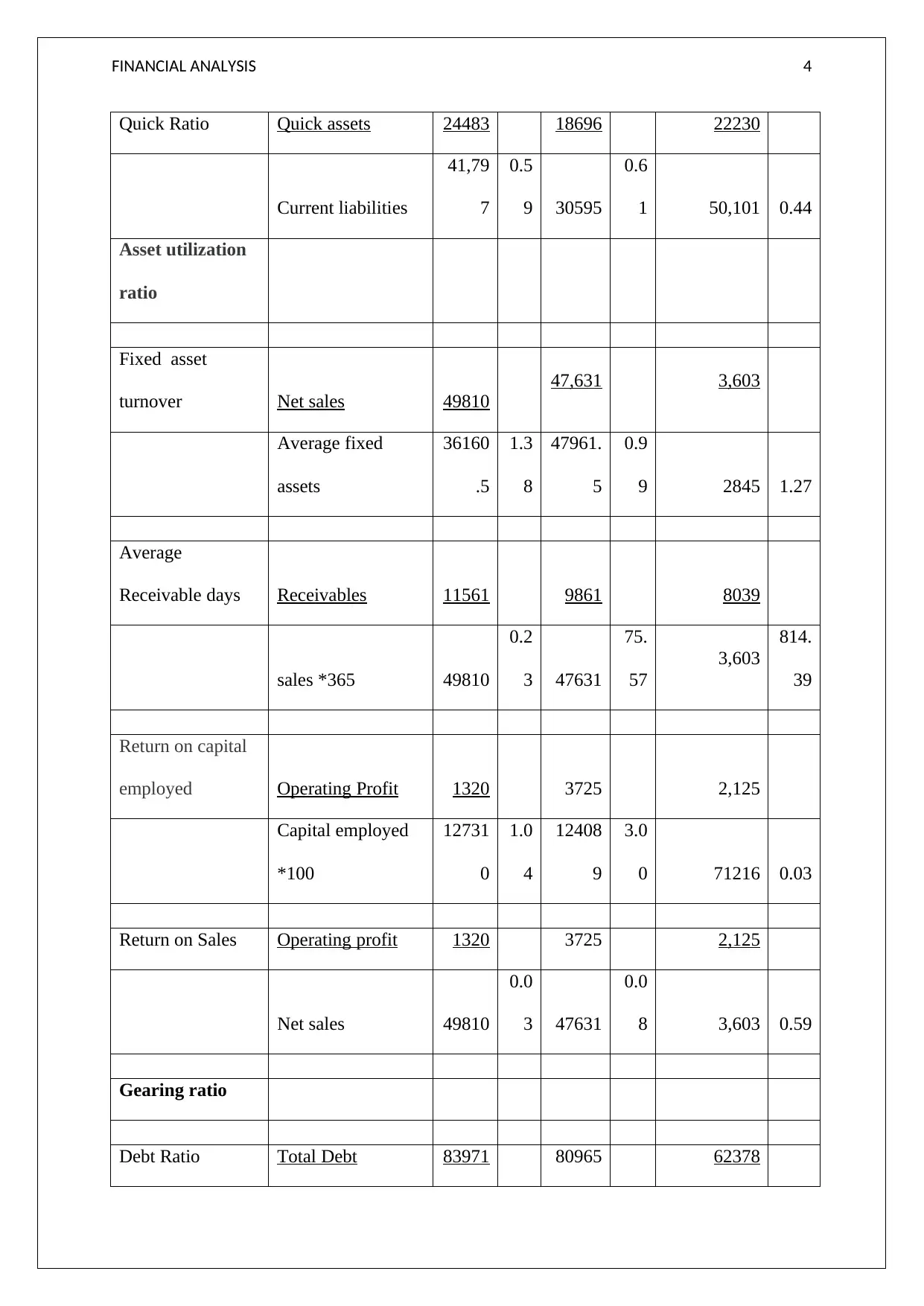

Quick Ratio Quick assets 24483 18696 22230

Current liabilities

41,79

7

0.5

9 30595

0.6

1 50,101 0.44

Asset utilization

ratio

Fixed asset

turnover Net sales 49810

47,631 3,603

Average fixed

assets

36160

.5

1.3

8

47961.

5

0.9

9 2845 1.27

Average

Receivable days Receivables 11561 9861 8039

sales *365 49810

0.2

3 47631

75.

57

3,603

814.

39

Return on capital

employed Operating Profit 1320 3725 2,125

Capital employed

*100

12731

0

1.0

4

12408

9

3.0

0 71216 0.03

Return on Sales Operating profit 1320 3725 2,125

Net sales 49810

0.0

3 47631

0.0

8 3,603 0.59

Gearing ratio

Debt Ratio Total Debt 83971 80965 62378

Quick Ratio Quick assets 24483 18696 22230

Current liabilities

41,79

7

0.5

9 30595

0.6

1 50,101 0.44

Asset utilization

ratio

Fixed asset

turnover Net sales 49810

47,631 3,603

Average fixed

assets

36160

.5

1.3

8

47961.

5

0.9

9 2845 1.27

Average

Receivable days Receivables 11561 9861 8039

sales *365 49810

0.2

3 47631

75.

57

3,603

814.

39

Return on capital

employed Operating Profit 1320 3725 2,125

Capital employed

*100

12731

0

1.0

4

12408

9

3.0

0 71216 0.03

Return on Sales Operating profit 1320 3725 2,125

Net sales 49810

0.0

3 47631

0.0

8 3,603 0.59

Gearing ratio

Debt Ratio Total Debt 83971 80965 62378

FINANCIAL ANALYSIS 5

Total Asset

1,69,1

07

0.5

0

15468

4

0.5

2 121317 0.51

Debt-to-Equity Ra

tio Total Debt 83971 80965 62378

Total Equity

83,32

5

1.0

1 73,719

1.1

0 583939 0.11

Interest coverage

ratio EBIT -190 2,792 7151

Interest Expenses 2046

-

0.0

9 -1406

-

1.9

9 2517 2.84

stock days

Stock turnover

days Average Stock 691.5 934 1120.5

Cost of Goods Sold

*365

-

36,71

3

-

6.8

7

34,576 0.0

3 190201 2.15

(Source: Vodafone, 2017)

Task 2: Financial Analysis

The financial ratio of the company is evaluated of the year 2016 and 2017. As per the

evaluation, it has been seen that the liquidity ratio of the company is decreasing from the year

2016 and 2017 (Vodafone, 2017b). It is observed that the current asset and current liabilities

Total Asset

1,69,1

07

0.5

0

15468

4

0.5

2 121317 0.51

Debt-to-Equity Ra

tio Total Debt 83971 80965 62378

Total Equity

83,32

5

1.0

1 73,719

1.1

0 583939 0.11

Interest coverage

ratio EBIT -190 2,792 7151

Interest Expenses 2046

-

0.0

9 -1406

-

1.9

9 2517 2.84

stock days

Stock turnover

days Average Stock 691.5 934 1120.5

Cost of Goods Sold

*365

-

36,71

3

-

6.8

7

34,576 0.0

3 190201 2.15

(Source: Vodafone, 2017)

Task 2: Financial Analysis

The financial ratio of the company is evaluated of the year 2016 and 2017. As per the

evaluation, it has been seen that the liquidity ratio of the company is decreasing from the year

2016 and 2017 (Vodafone, 2017b). It is observed that the current asset and current liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 6

of the company is reduces as compare to the last year. The liquidity ratio reflects that the

company is not able to pay its liabilities with the current assets amount. The debt of the

company is increases due to increasing the current liabilities (Robinson, Henry, Pirie, and

Broihahn, 2015).

The profitability ratio helps to evaluate the position of the company in terms of finance. It is

required to evaluate the profit to analyse the financial performance. In the case of Vodafone,

the gross profit margin ratio is evaluated in order to evaluate the financial capabilities. It is

the difference between the cost of goods sold and revenue. The ratio of the company is 0.26

to 0.27 that states the company net sales is decreases due to which net profit margin is also

decreases (Vodafone, 2017b). The increasing expenses is the major reason behind the

decreasing the profitability ratio of the company (Shpak, 2018).

Asset utilisation ratio defines the capability of an organisation to utilise the asset to attain the

success in the business. It is observed that the ratio of asset utilisation is decreases as the

efficiency to utilise the asset is reduces (Accounting tools, 2018b). The value of net sales is

reduces from 2016 to 2017 as 49810 to 47631respectively. The inappropriate use of asset

reduces to capability of the company to expand the business or invest in the other areas.

Compare to Deutsche Telekom

Vodafone and Deutsche Telekom are operated in the same industry due to which the

company face the challenges. Deutsche Telekom is the top competitor of the company that is

why, the financial performance is also evaluated. As per the evaluation, it has been seen that

the current profitability ratio of Deutsche Telekom is high as compare to Vodafone as its cost

of goods sold id less as compare to sale. In the year 2017, it is observed that the Deutsche

Telekom has 0.71 profitability ratio and Vodafone has 0.27 (Deutsche Telekom, 2017).

of the company is reduces as compare to the last year. The liquidity ratio reflects that the

company is not able to pay its liabilities with the current assets amount. The debt of the

company is increases due to increasing the current liabilities (Robinson, Henry, Pirie, and

Broihahn, 2015).

The profitability ratio helps to evaluate the position of the company in terms of finance. It is

required to evaluate the profit to analyse the financial performance. In the case of Vodafone,

the gross profit margin ratio is evaluated in order to evaluate the financial capabilities. It is

the difference between the cost of goods sold and revenue. The ratio of the company is 0.26

to 0.27 that states the company net sales is decreases due to which net profit margin is also

decreases (Vodafone, 2017b). The increasing expenses is the major reason behind the

decreasing the profitability ratio of the company (Shpak, 2018).

Asset utilisation ratio defines the capability of an organisation to utilise the asset to attain the

success in the business. It is observed that the ratio of asset utilisation is decreases as the

efficiency to utilise the asset is reduces (Accounting tools, 2018b). The value of net sales is

reduces from 2016 to 2017 as 49810 to 47631respectively. The inappropriate use of asset

reduces to capability of the company to expand the business or invest in the other areas.

Compare to Deutsche Telekom

Vodafone and Deutsche Telekom are operated in the same industry due to which the

company face the challenges. Deutsche Telekom is the top competitor of the company that is

why, the financial performance is also evaluated. As per the evaluation, it has been seen that

the current profitability ratio of Deutsche Telekom is high as compare to Vodafone as its cost

of goods sold id less as compare to sale. In the year 2017, it is observed that the Deutsche

Telekom has 0.71 profitability ratio and Vodafone has 0.27 (Deutsche Telekom, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 7

The liquidity ratio of the companies states that the Vodafone is more capable in order to pay

its liabilities as compare to Deutsche Telekom (The balance small business, 2019). Deutsche

Telekom has the large amount of current liabilities as compare to current asset and the

difference between the borrowing and investment is high. Deutsche Telekom has 0.48 as a

liquidity ratio and the Vodafone has 0.76 (Deutsche Telekom, 2017). The difference between

current asset and current liabilities is less and it can be said that the company have a chance

to improve its services.

The average receivable days reflects the collecting in which the organisation can collect its

credit amount (Accounting tools, 2018a). It is observed that the Vodafone provides the

services on credit amount as compare to Deutsche Telekom. Vodafone can collect its credit

amount in 75.57 days even it has a large amount credit to collect (Vodafone, 2017b). In the

case of Deutsche Telekom, the company provides the fewer amounts of services on credit and

it also receive the credit in large number of days. As per average receivable days, it is

observed that the Deutsche Telekom is more effective as they do not provide the large

amount of services on credit (Deutsche Telekom, 2017).

Reasons of differences

Deutsche Telekom and Vodafone have a huge difference in financial terms. Although, both

the companies are operating under the same industry and provide the similar services to

consumers but the companies have different techniques to operate the business.

It has been seen that both the companies implements the different approaches to operate the

business. In the case of Vodafone, the company provides the services on credit to consumers

due to which the current asset is decreases and current liabilities are increases. But the

Deutsche Telekom provides the fewer amounts of services on credit (Tough Nickel, 2016).

The liquidity ratio of the companies states that the Vodafone is more capable in order to pay

its liabilities as compare to Deutsche Telekom (The balance small business, 2019). Deutsche

Telekom has the large amount of current liabilities as compare to current asset and the

difference between the borrowing and investment is high. Deutsche Telekom has 0.48 as a

liquidity ratio and the Vodafone has 0.76 (Deutsche Telekom, 2017). The difference between

current asset and current liabilities is less and it can be said that the company have a chance

to improve its services.

The average receivable days reflects the collecting in which the organisation can collect its

credit amount (Accounting tools, 2018a). It is observed that the Vodafone provides the

services on credit amount as compare to Deutsche Telekom. Vodafone can collect its credit

amount in 75.57 days even it has a large amount credit to collect (Vodafone, 2017b). In the

case of Deutsche Telekom, the company provides the fewer amounts of services on credit and

it also receive the credit in large number of days. As per average receivable days, it is

observed that the Deutsche Telekom is more effective as they do not provide the large

amount of services on credit (Deutsche Telekom, 2017).

Reasons of differences

Deutsche Telekom and Vodafone have a huge difference in financial terms. Although, both

the companies are operating under the same industry and provide the similar services to

consumers but the companies have different techniques to operate the business.

It has been seen that both the companies implements the different approaches to operate the

business. In the case of Vodafone, the company provides the services on credit to consumers

due to which the current asset is decreases and current liabilities are increases. But the

Deutsche Telekom provides the fewer amounts of services on credit (Tough Nickel, 2016).

FINANCIAL ANALYSIS 8

The difference between the companies that affects their financial performance is the demand

of consumers. The demand of consumers is high towards the Vodafone as it has high sales.

Deutsche Telekom has less sales but the revenue is high that is why; its profitability ratio is

more effective than the Vodafone. The difference between the gross profit and cost of goods

sold is high in the case of Vodafone due to which they face the challenges of less revenue

(Winkinson, 2013). It can be said that the company adopts the cost leadership strategy to

attract the consumers. As per the strategy, it provides the services in fewer amounts as

compare to its competitors so that the large number of consumer attracts towards it. The

company face the challenges because revenue is reduced.

As per the analysis, it has been seen that the Deutsche Telekom consume the large amount in

expenses. According to the annual report of 2017, Deutsche Telekom invests the large

amount of 190201 in providing the services to consumer. It is observed that the Vodafone

consume less amount in producing the goods and services as compare to Deutsche Telekom.

In this analysis, it can be said that the Deutsche Telekom are more effective as they maintain

the stock. That is why; Deutsche Telekom is more appropriate in terms of stock turnover

days.

Impact of competitors

Affect Financial Position

Deutsche Telekom attracts the consumers by providing the similar nature of services with

high quality of goods. Attracting the large consumer towards the services of the company

affects the financial position as the sales of product is fluctuated. The revenue of the company

is reduces that affects the financial position in the industry (Info entrepreneurs, 2018).

Reducing revenue

The difference between the companies that affects their financial performance is the demand

of consumers. The demand of consumers is high towards the Vodafone as it has high sales.

Deutsche Telekom has less sales but the revenue is high that is why; its profitability ratio is

more effective than the Vodafone. The difference between the gross profit and cost of goods

sold is high in the case of Vodafone due to which they face the challenges of less revenue

(Winkinson, 2013). It can be said that the company adopts the cost leadership strategy to

attract the consumers. As per the strategy, it provides the services in fewer amounts as

compare to its competitors so that the large number of consumer attracts towards it. The

company face the challenges because revenue is reduced.

As per the analysis, it has been seen that the Deutsche Telekom consume the large amount in

expenses. According to the annual report of 2017, Deutsche Telekom invests the large

amount of 190201 in providing the services to consumer. It is observed that the Vodafone

consume less amount in producing the goods and services as compare to Deutsche Telekom.

In this analysis, it can be said that the Deutsche Telekom are more effective as they maintain

the stock. That is why; Deutsche Telekom is more appropriate in terms of stock turnover

days.

Impact of competitors

Affect Financial Position

Deutsche Telekom attracts the consumers by providing the similar nature of services with

high quality of goods. Attracting the large consumer towards the services of the company

affects the financial position as the sales of product is fluctuated. The revenue of the company

is reduces that affects the financial position in the industry (Info entrepreneurs, 2018).

Reducing revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 9

It is observed that the revenue of the company is reduces. Deutsche Telekom attracts the

consumer by implementing the premium quality of services. Premium quality of services

attracts the consumers due to which the sale is decreases. Competitors of the company affects

the revenue of Vodafone as the sales of Deutsche Telekom is increases.

Investment in Assets

It has been seen that reducing the revenue affects the asset. The company can invest the

profit amount in asset so that they can expand the business at the international level (Gitman,

Juchau, and Flanagan, 2015). But due to reducing revenue, the asset of the company is also

reduces due to which the Vodafone faces the issues.

Conclusion

At the end, it is concluded that the Vodafone has to be take care of services in order to beat

the competitors. The competitors of the company give the high competition by adopting the

different techniques and strategies. Vodafone should be concerned about the Deutsche

Telekom as it affects the growth and revenue. As per the financial analysis, it is observed that

the financial performance of the company is decreases year by year. Vodafone is more stable

as compare to Deutsche Telekom in terms of financial condition. The financial position of the

company is also affected due to its competitors. The liability of the company is reduces from

the year 2016 to 2017 which is effective for the success. Current asset of the company is less

than the current liabilities due to which it cannot expand the business at the international level

(Economic Times, 2018). The competitors of the company have negative effects on the

performance of Vodafone in financial terms such as reducing revenue, investment in assets,

and affect the financial performance. Although, both the companies are performing well in

their financial condition but they has to improve their financial performance.

It is observed that the revenue of the company is reduces. Deutsche Telekom attracts the

consumer by implementing the premium quality of services. Premium quality of services

attracts the consumers due to which the sale is decreases. Competitors of the company affects

the revenue of Vodafone as the sales of Deutsche Telekom is increases.

Investment in Assets

It has been seen that reducing the revenue affects the asset. The company can invest the

profit amount in asset so that they can expand the business at the international level (Gitman,

Juchau, and Flanagan, 2015). But due to reducing revenue, the asset of the company is also

reduces due to which the Vodafone faces the issues.

Conclusion

At the end, it is concluded that the Vodafone has to be take care of services in order to beat

the competitors. The competitors of the company give the high competition by adopting the

different techniques and strategies. Vodafone should be concerned about the Deutsche

Telekom as it affects the growth and revenue. As per the financial analysis, it is observed that

the financial performance of the company is decreases year by year. Vodafone is more stable

as compare to Deutsche Telekom in terms of financial condition. The financial position of the

company is also affected due to its competitors. The liability of the company is reduces from

the year 2016 to 2017 which is effective for the success. Current asset of the company is less

than the current liabilities due to which it cannot expand the business at the international level

(Economic Times, 2018). The competitors of the company have negative effects on the

performance of Vodafone in financial terms such as reducing revenue, investment in assets,

and affect the financial performance. Although, both the companies are performing well in

their financial condition but they has to improve their financial performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 10

FINANCIAL ANALYSIS 11

Bibliography

Websites

Accounting tools. (2018a) Accounts receivable collection period | Days sales

outstanding. [online] Available from:

https://www.accountingtools.com/articles/2017/5/13/accounts-receivable-collection-

period-days-sales-outstanding [Accessed 23/05/12].

Accounting tools. (2018b). Efficiency ratios. [online] Available from:

https://www.accountingtools.com/articles/efficiency-ratios.html [Accessed 23/05/12].

CFI. (2019) Types of Financial Analysis. [online] Available from:

https://corporatefinanceinstitute.com/resources/knowledge/finance/types-of-financial-

analysis/ [Accessed 23/05/12].

Deutsche Telekom. (2017) The 2017 Financial Year. [online] Available from:

file:///C:/Users/SYSTEM~1/AppData/Local/Temp/dl-180222-q4-allinone-1.pdf

[Accessed 23/05/12].

Deutsche Telekom. (2018) Company. [online] Available from:

https://www.telekom.com/en/company [Accessed 23/05/12].

Economic Times. (2018) Definition of 'Return On Equity'. [online] Available from:

https://economictimes.indiatimes.com/definition/return-on-equity [Accessed 23/05/12].

Info entrepreneurs. (2018) Understand your competitors. [online] Available from:

https://www.infoentrepreneurs.org/en/guides/understand-your-competitors/ [Accessed

23/05/12].

Bibliography

Websites

Accounting tools. (2018a) Accounts receivable collection period | Days sales

outstanding. [online] Available from:

https://www.accountingtools.com/articles/2017/5/13/accounts-receivable-collection-

period-days-sales-outstanding [Accessed 23/05/12].

Accounting tools. (2018b). Efficiency ratios. [online] Available from:

https://www.accountingtools.com/articles/efficiency-ratios.html [Accessed 23/05/12].

CFI. (2019) Types of Financial Analysis. [online] Available from:

https://corporatefinanceinstitute.com/resources/knowledge/finance/types-of-financial-

analysis/ [Accessed 23/05/12].

Deutsche Telekom. (2017) The 2017 Financial Year. [online] Available from:

file:///C:/Users/SYSTEM~1/AppData/Local/Temp/dl-180222-q4-allinone-1.pdf

[Accessed 23/05/12].

Deutsche Telekom. (2018) Company. [online] Available from:

https://www.telekom.com/en/company [Accessed 23/05/12].

Economic Times. (2018) Definition of 'Return On Equity'. [online] Available from:

https://economictimes.indiatimes.com/definition/return-on-equity [Accessed 23/05/12].

Info entrepreneurs. (2018) Understand your competitors. [online] Available from:

https://www.infoentrepreneurs.org/en/guides/understand-your-competitors/ [Accessed

23/05/12].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.