Financial Analysis and Performance Report for Alam Plc (2017-2018)

VerifiedAdded on 2022/11/15

|15

|4264

|117

Report

AI Summary

This report presents a comprehensive financial analysis of Alam Plc, evaluating its performance over two years (2017-2018). The analysis begins with a detailed ratio analysis, examining profitability (operating margin, net income, return on equity), efficiency (fixed asset turnover, inventory turnover, accounts receivable and payable turnover), liquidity, and solvency ratios. The report also includes a break-even analysis to determine the point at which the company neither makes a profit nor incurs a loss, and a critical evaluation of the sources of funds. The report highlights areas of concern, such as declining profitability and efficiency, and suggests corrective actions for improvement. The financial analysis employs various techniques, including horizontal analysis and the calculation of key financial ratios to assess the company's financial health. The report includes income statements and balance sheets to support the analysis.

Running Head: FINANCIAL ANALYSIS 1

FINANCIAL ANALYSIS AND REPORT

FINANCIAL ANALYSIS AND REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 2

Table of Contents

PART A......................................................................................................................................3

Answer 2: Ratio analysis............................................................................................................3

Profitability.............................................................................................................................3

Efficiency...............................................................................................................................4

Liquidity.................................................................................................................................5

Solvency.................................................................................................................................6

Investing Ratios......................................................................................................................7

PART B......................................................................................................................................8

Answer 2: Break even Analysis.................................................................................................8

PART C......................................................................................................................................8

Answer 1....................................................................................................................................8

Answer 2: Critical Evaluation of the sources of the funds.......................................................12

Ownership Sources...................................................................................................................12

References................................................................................................................................14

Table of Contents

PART A......................................................................................................................................3

Answer 2: Ratio analysis............................................................................................................3

Profitability.............................................................................................................................3

Efficiency...............................................................................................................................4

Liquidity.................................................................................................................................5

Solvency.................................................................................................................................6

Investing Ratios......................................................................................................................7

PART B......................................................................................................................................8

Answer 2: Break even Analysis.................................................................................................8

PART C......................................................................................................................................8

Answer 1....................................................................................................................................8

Answer 2: Critical Evaluation of the sources of the funds.......................................................12

Ownership Sources...................................................................................................................12

References................................................................................................................................14

FINANCIAL ANALYSIS 3

PART A

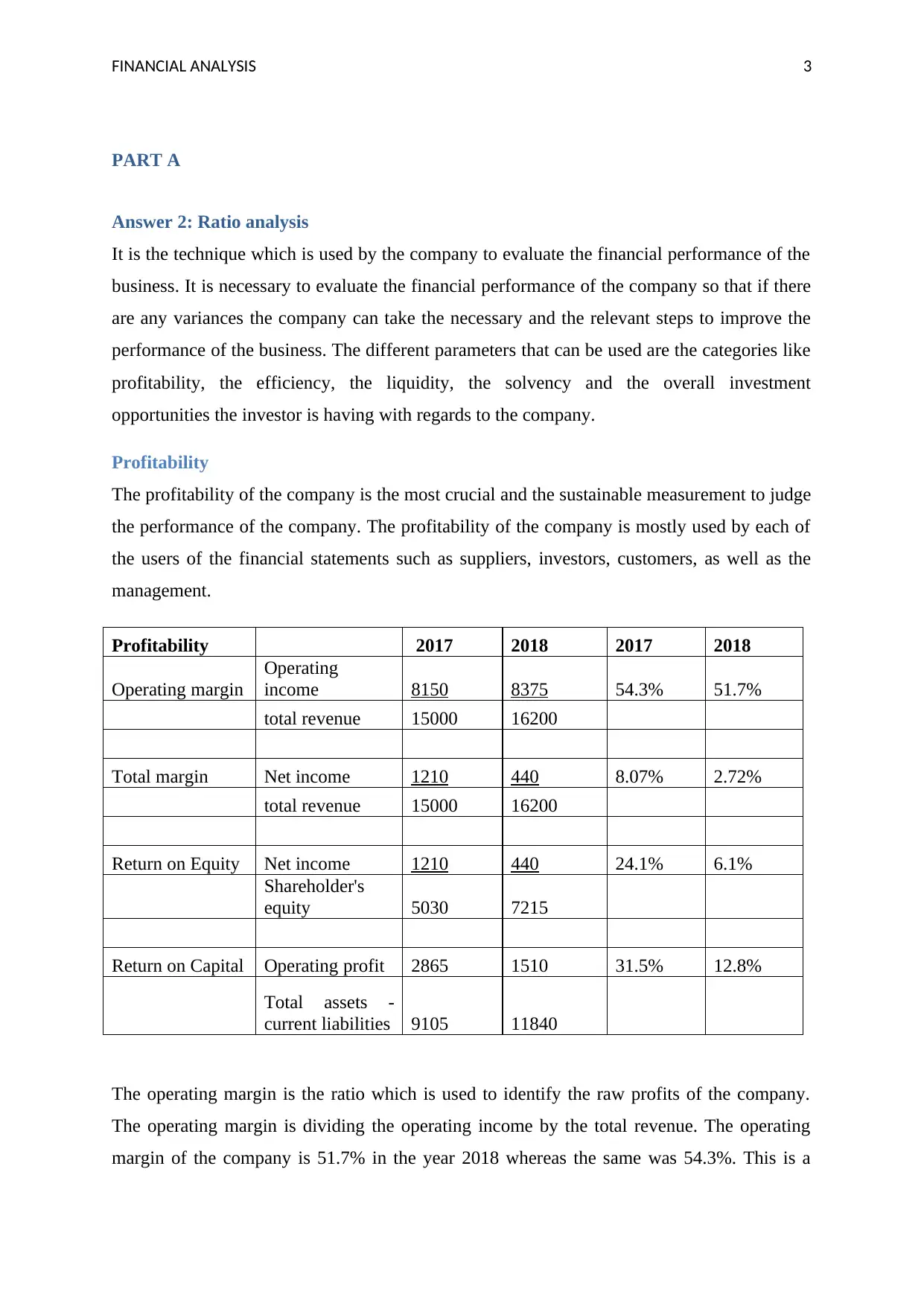

Answer 2: Ratio analysis

It is the technique which is used by the company to evaluate the financial performance of the

business. It is necessary to evaluate the financial performance of the company so that if there

are any variances the company can take the necessary and the relevant steps to improve the

performance of the business. The different parameters that can be used are the categories like

profitability, the efficiency, the liquidity, the solvency and the overall investment

opportunities the investor is having with regards to the company.

Profitability

The profitability of the company is the most crucial and the sustainable measurement to judge

the performance of the company. The profitability of the company is mostly used by each of

the users of the financial statements such as suppliers, investors, customers, as well as the

management.

Profitability 2017 2018 2017 2018

Operating margin

Operating

income 8150 8375 54.3% 51.7%

total revenue 15000 16200

Total margin Net income 1210 440 8.07% 2.72%

total revenue 15000 16200

Return on Equity Net income 1210 440 24.1% 6.1%

Shareholder's

equity 5030 7215

Return on Capital Operating profit 2865 1510 31.5% 12.8%

Total assets -

current liabilities 9105 11840

The operating margin is the ratio which is used to identify the raw profits of the company.

The operating margin is dividing the operating income by the total revenue. The operating

margin of the company is 51.7% in the year 2018 whereas the same was 54.3%. This is a

PART A

Answer 2: Ratio analysis

It is the technique which is used by the company to evaluate the financial performance of the

business. It is necessary to evaluate the financial performance of the company so that if there

are any variances the company can take the necessary and the relevant steps to improve the

performance of the business. The different parameters that can be used are the categories like

profitability, the efficiency, the liquidity, the solvency and the overall investment

opportunities the investor is having with regards to the company.

Profitability

The profitability of the company is the most crucial and the sustainable measurement to judge

the performance of the company. The profitability of the company is mostly used by each of

the users of the financial statements such as suppliers, investors, customers, as well as the

management.

Profitability 2017 2018 2017 2018

Operating margin

Operating

income 8150 8375 54.3% 51.7%

total revenue 15000 16200

Total margin Net income 1210 440 8.07% 2.72%

total revenue 15000 16200

Return on Equity Net income 1210 440 24.1% 6.1%

Shareholder's

equity 5030 7215

Return on Capital Operating profit 2865 1510 31.5% 12.8%

Total assets -

current liabilities 9105 11840

The operating margin is the ratio which is used to identify the raw profits of the company.

The operating margin is dividing the operating income by the total revenue. The operating

margin of the company is 51.7% in the year 2018 whereas the same was 54.3%. This is a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 4

negative indication and the company must improve immediately by cutting the costs such as

the cost of the sales and the raw materials (Robinson, Henry Pirie and Broihahn, 2015).

The total margin also known as the net profit is the ratio which is calculated by dividing the

net income by the total revenue. The net income in the previous year was $1040 whereas the

same declined to $250. This implies that the net income has been declined to a non-

acceptable level and the percentage of the net profit decreased from 14.7% to 2.7%. The net

income determines the ultimate results of the company and to improve the net profit margin

the company must reduce the labour charges and must keep the extra costs out (Zietlow,

Hankin, Seidner and O'Brien, 2018).

The return on equity of the Alam Plc. was 24.1% in the eyar 2017 and the same reduced to

6.1% in the year 2018. This indicates the investors are not getting enough returns against the

funds invested by them in the business. In order to improve the ratio the company must

distribute the idle cash if any left and shall focus on funding through debt (Ahmad, 2016).

Hence, the overall profitability of the company is not smooth and sound and the company

needs immediate actions by the company to improve and the profitability. Hence, the

profitability areas are not in the favour of the investors and the immediate corrective actions

are required (Williams and Dobelman, 2017). The overall profitability of the company needs

to be revised to grab the greater market share.

Efficiency

The efficiency of the company can be measured with the help of the turnover ratios. Basically

the efficiency determines how well, the company is able to realize the cash from the current

assets and how well they are able to pay back the current liabilities. In this case the

parameters used to calculate the efficiency of the company are the fixed asset turnover ratio,

the accounts receivable turnover ratio, the inventory turnover and the accounts payable

turnover ratio.

Activity Ratios 2017 2018 2017 2018

Fixed Asset Turnover Net sales 15000 16200 2.69 2.35

times Fixed Assets 5570 6890

Accounts payable

turnover

Accounts payable * 365 75555

0 784750

110.3

0

100.2

9

negative indication and the company must improve immediately by cutting the costs such as

the cost of the sales and the raw materials (Robinson, Henry Pirie and Broihahn, 2015).

The total margin also known as the net profit is the ratio which is calculated by dividing the

net income by the total revenue. The net income in the previous year was $1040 whereas the

same declined to $250. This implies that the net income has been declined to a non-

acceptable level and the percentage of the net profit decreased from 14.7% to 2.7%. The net

income determines the ultimate results of the company and to improve the net profit margin

the company must reduce the labour charges and must keep the extra costs out (Zietlow,

Hankin, Seidner and O'Brien, 2018).

The return on equity of the Alam Plc. was 24.1% in the eyar 2017 and the same reduced to

6.1% in the year 2018. This indicates the investors are not getting enough returns against the

funds invested by them in the business. In order to improve the ratio the company must

distribute the idle cash if any left and shall focus on funding through debt (Ahmad, 2016).

Hence, the overall profitability of the company is not smooth and sound and the company

needs immediate actions by the company to improve and the profitability. Hence, the

profitability areas are not in the favour of the investors and the immediate corrective actions

are required (Williams and Dobelman, 2017). The overall profitability of the company needs

to be revised to grab the greater market share.

Efficiency

The efficiency of the company can be measured with the help of the turnover ratios. Basically

the efficiency determines how well, the company is able to realize the cash from the current

assets and how well they are able to pay back the current liabilities. In this case the

parameters used to calculate the efficiency of the company are the fixed asset turnover ratio,

the accounts receivable turnover ratio, the inventory turnover and the accounts payable

turnover ratio.

Activity Ratios 2017 2018 2017 2018

Fixed Asset Turnover Net sales 15000 16200 2.69 2.35

times Fixed Assets 5570 6890

Accounts payable

turnover

Accounts payable * 365 75555

0 784750

110.3

0

100.2

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 5

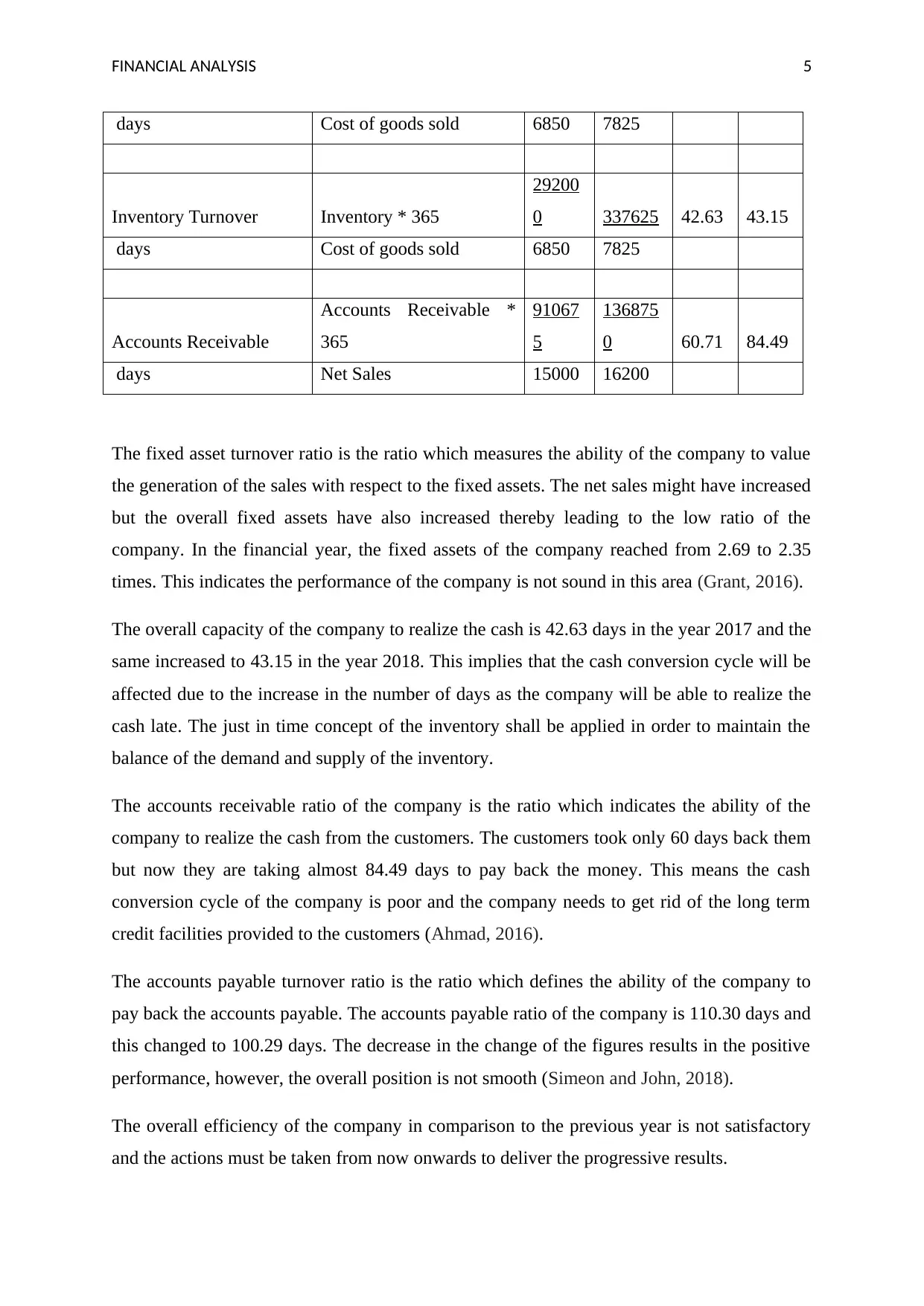

days Cost of goods sold 6850 7825

Inventory Turnover Inventory * 365

29200

0 337625 42.63 43.15

days Cost of goods sold 6850 7825

Accounts Receivable

Accounts Receivable *

365

91067

5

136875

0 60.71 84.49

days Net Sales 15000 16200

The fixed asset turnover ratio is the ratio which measures the ability of the company to value

the generation of the sales with respect to the fixed assets. The net sales might have increased

but the overall fixed assets have also increased thereby leading to the low ratio of the

company. In the financial year, the fixed assets of the company reached from 2.69 to 2.35

times. This indicates the performance of the company is not sound in this area (Grant, 2016).

The overall capacity of the company to realize the cash is 42.63 days in the year 2017 and the

same increased to 43.15 in the year 2018. This implies that the cash conversion cycle will be

affected due to the increase in the number of days as the company will be able to realize the

cash late. The just in time concept of the inventory shall be applied in order to maintain the

balance of the demand and supply of the inventory.

The accounts receivable ratio of the company is the ratio which indicates the ability of the

company to realize the cash from the customers. The customers took only 60 days back them

but now they are taking almost 84.49 days to pay back the money. This means the cash

conversion cycle of the company is poor and the company needs to get rid of the long term

credit facilities provided to the customers (Ahmad, 2016).

The accounts payable turnover ratio is the ratio which defines the ability of the company to

pay back the accounts payable. The accounts payable ratio of the company is 110.30 days and

this changed to 100.29 days. The decrease in the change of the figures results in the positive

performance, however, the overall position is not smooth (Simeon and John, 2018).

The overall efficiency of the company in comparison to the previous year is not satisfactory

and the actions must be taken from now onwards to deliver the progressive results.

days Cost of goods sold 6850 7825

Inventory Turnover Inventory * 365

29200

0 337625 42.63 43.15

days Cost of goods sold 6850 7825

Accounts Receivable

Accounts Receivable *

365

91067

5

136875

0 60.71 84.49

days Net Sales 15000 16200

The fixed asset turnover ratio is the ratio which measures the ability of the company to value

the generation of the sales with respect to the fixed assets. The net sales might have increased

but the overall fixed assets have also increased thereby leading to the low ratio of the

company. In the financial year, the fixed assets of the company reached from 2.69 to 2.35

times. This indicates the performance of the company is not sound in this area (Grant, 2016).

The overall capacity of the company to realize the cash is 42.63 days in the year 2017 and the

same increased to 43.15 in the year 2018. This implies that the cash conversion cycle will be

affected due to the increase in the number of days as the company will be able to realize the

cash late. The just in time concept of the inventory shall be applied in order to maintain the

balance of the demand and supply of the inventory.

The accounts receivable ratio of the company is the ratio which indicates the ability of the

company to realize the cash from the customers. The customers took only 60 days back them

but now they are taking almost 84.49 days to pay back the money. This means the cash

conversion cycle of the company is poor and the company needs to get rid of the long term

credit facilities provided to the customers (Ahmad, 2016).

The accounts payable turnover ratio is the ratio which defines the ability of the company to

pay back the accounts payable. The accounts payable ratio of the company is 110.30 days and

this changed to 100.29 days. The decrease in the change of the figures results in the positive

performance, however, the overall position is not smooth (Simeon and John, 2018).

The overall efficiency of the company in comparison to the previous year is not satisfactory

and the actions must be taken from now onwards to deliver the progressive results.

FINANCIAL ANALYSIS 6

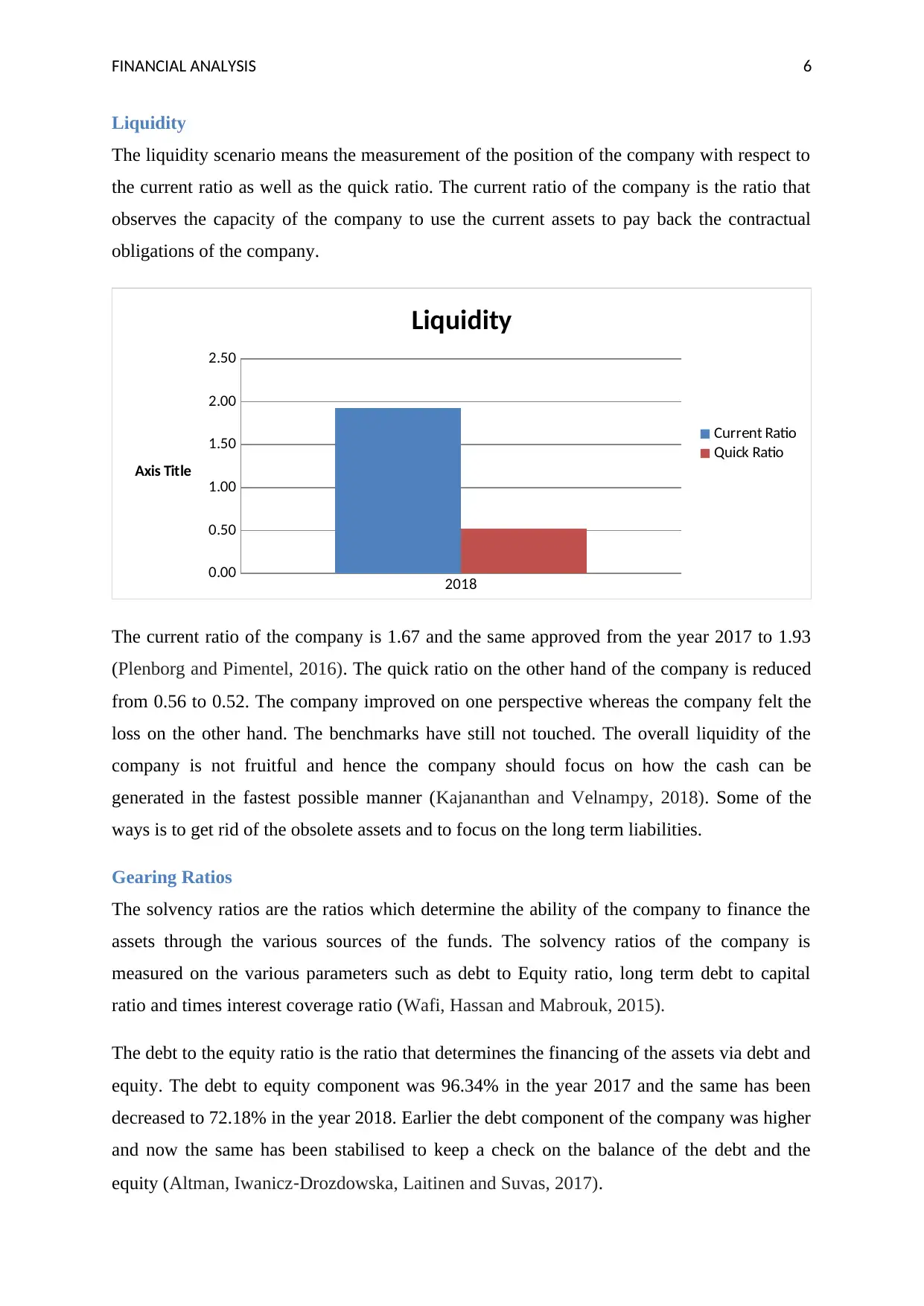

Liquidity

The liquidity scenario means the measurement of the position of the company with respect to

the current ratio as well as the quick ratio. The current ratio of the company is the ratio that

observes the capacity of the company to use the current assets to pay back the contractual

obligations of the company.

2018

0.00

0.50

1.00

1.50

2.00

2.50

Liquidity

Current Ratio

Quick Ratio

Axis Title

The current ratio of the company is 1.67 and the same approved from the year 2017 to 1.93

(Plenborg and Pimentel, 2016). The quick ratio on the other hand of the company is reduced

from 0.56 to 0.52. The company improved on one perspective whereas the company felt the

loss on the other hand. The benchmarks have still not touched. The overall liquidity of the

company is not fruitful and hence the company should focus on how the cash can be

generated in the fastest possible manner (Kajananthan and Velnampy, 2018). Some of the

ways is to get rid of the obsolete assets and to focus on the long term liabilities.

Gearing Ratios

The solvency ratios are the ratios which determine the ability of the company to finance the

assets through the various sources of the funds. The solvency ratios of the company is

measured on the various parameters such as debt to Equity ratio, long term debt to capital

ratio and times interest coverage ratio (Wafi, Hassan and Mabrouk, 2015).

The debt to the equity ratio is the ratio that determines the financing of the assets via debt and

equity. The debt to equity component was 96.34% in the year 2017 and the same has been

decreased to 72.18% in the year 2018. Earlier the debt component of the company was higher

and now the same has been stabilised to keep a check on the balance of the debt and the

equity (Altman, Iwanicz‐Drozdowska, Laitinen and Suvas, 2017).

Liquidity

The liquidity scenario means the measurement of the position of the company with respect to

the current ratio as well as the quick ratio. The current ratio of the company is the ratio that

observes the capacity of the company to use the current assets to pay back the contractual

obligations of the company.

2018

0.00

0.50

1.00

1.50

2.00

2.50

Liquidity

Current Ratio

Quick Ratio

Axis Title

The current ratio of the company is 1.67 and the same approved from the year 2017 to 1.93

(Plenborg and Pimentel, 2016). The quick ratio on the other hand of the company is reduced

from 0.56 to 0.52. The company improved on one perspective whereas the company felt the

loss on the other hand. The benchmarks have still not touched. The overall liquidity of the

company is not fruitful and hence the company should focus on how the cash can be

generated in the fastest possible manner (Kajananthan and Velnampy, 2018). Some of the

ways is to get rid of the obsolete assets and to focus on the long term liabilities.

Gearing Ratios

The solvency ratios are the ratios which determine the ability of the company to finance the

assets through the various sources of the funds. The solvency ratios of the company is

measured on the various parameters such as debt to Equity ratio, long term debt to capital

ratio and times interest coverage ratio (Wafi, Hassan and Mabrouk, 2015).

The debt to the equity ratio is the ratio that determines the financing of the assets via debt and

equity. The debt to equity component was 96.34% in the year 2017 and the same has been

decreased to 72.18% in the year 2018. Earlier the debt component of the company was higher

and now the same has been stabilised to keep a check on the balance of the debt and the

equity (Altman, Iwanicz‐Drozdowska, Laitinen and Suvas, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 7

2018

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Capital Structure

Long tern debt to capotal Ratio

Times interest coverage ratio

Axis Title

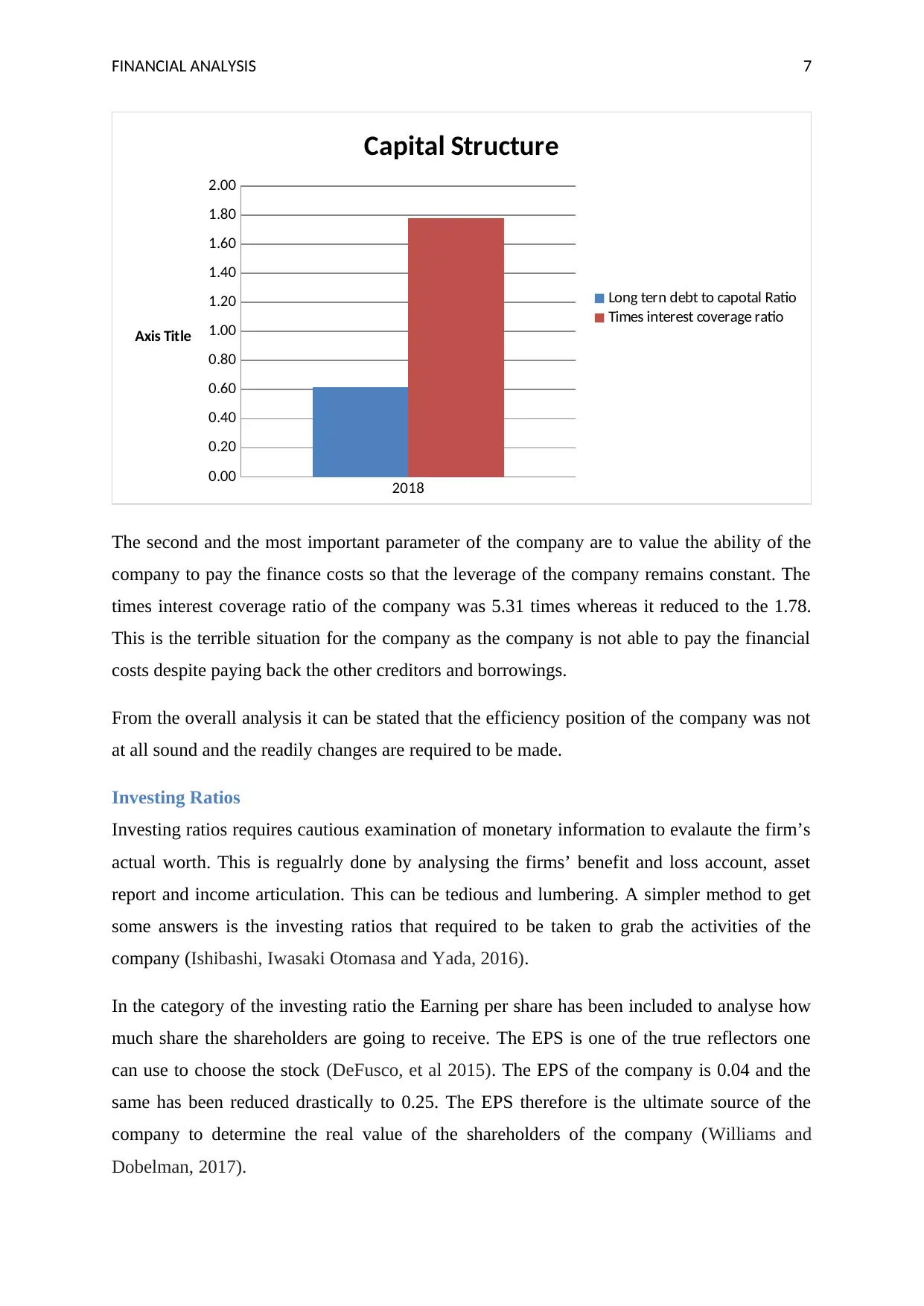

The second and the most important parameter of the company are to value the ability of the

company to pay the finance costs so that the leverage of the company remains constant. The

times interest coverage ratio of the company was 5.31 times whereas it reduced to the 1.78.

This is the terrible situation for the company as the company is not able to pay the financial

costs despite paying back the other creditors and borrowings.

From the overall analysis it can be stated that the efficiency position of the company was not

at all sound and the readily changes are required to be made.

Investing Ratios

Investing ratios requires cautious examination of monetary information to evalaute the firm’s

actual worth. This is regualrly done by analysing the firms’ benefit and loss account, asset

report and income articulation. This can be tedious and lumbering. A simpler method to get

some answers is the investing ratios that required to be taken to grab the activities of the

company (Ishibashi, Iwasaki Otomasa and Yada, 2016).

In the category of the investing ratio the Earning per share has been included to analyse how

much share the shareholders are going to receive. The EPS is one of the true reflectors one

can use to choose the stock (DeFusco, et al 2015). The EPS of the company is 0.04 and the

same has been reduced drastically to 0.25. The EPS therefore is the ultimate source of the

company to determine the real value of the shareholders of the company (Williams and

Dobelman, 2017).

2018

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Capital Structure

Long tern debt to capotal Ratio

Times interest coverage ratio

Axis Title

The second and the most important parameter of the company are to value the ability of the

company to pay the finance costs so that the leverage of the company remains constant. The

times interest coverage ratio of the company was 5.31 times whereas it reduced to the 1.78.

This is the terrible situation for the company as the company is not able to pay the financial

costs despite paying back the other creditors and borrowings.

From the overall analysis it can be stated that the efficiency position of the company was not

at all sound and the readily changes are required to be made.

Investing Ratios

Investing ratios requires cautious examination of monetary information to evalaute the firm’s

actual worth. This is regualrly done by analysing the firms’ benefit and loss account, asset

report and income articulation. This can be tedious and lumbering. A simpler method to get

some answers is the investing ratios that required to be taken to grab the activities of the

company (Ishibashi, Iwasaki Otomasa and Yada, 2016).

In the category of the investing ratio the Earning per share has been included to analyse how

much share the shareholders are going to receive. The EPS is one of the true reflectors one

can use to choose the stock (DeFusco, et al 2015). The EPS of the company is 0.04 and the

same has been reduced drastically to 0.25. The EPS therefore is the ultimate source of the

company to determine the real value of the shareholders of the company (Williams and

Dobelman, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 8

PART B

Answer 2: Break even Analysis

Break-even analysis is a technique which is utilised for the implementation of the cost

functions. The three major factors that are used by the concept of the breakeven are the sales,

profit and the cost. The major gaols of the methodology are to classify the relationship

between through various parameters (Tanco, Cat and Garat, 2019).

The key assumptions of the break even model, within the light of the reality of the today’s

business model are determined below.

The total costs are classified into the fixed and variable expenses. It ignores the semi

variable cost.

The functioning of the cost and the revenue remains linear.

The cost of the product will remain constant is also one of the most important feature

and the assumption.

The volume of the sales and the volume of the production are equivalent to each other

(Kabanov, 2019).

The zero improvement in the technology is also one of the most important factors.

The changes in the input prices are set off.

Where the firm deals with the multiple products the product mix is constant.

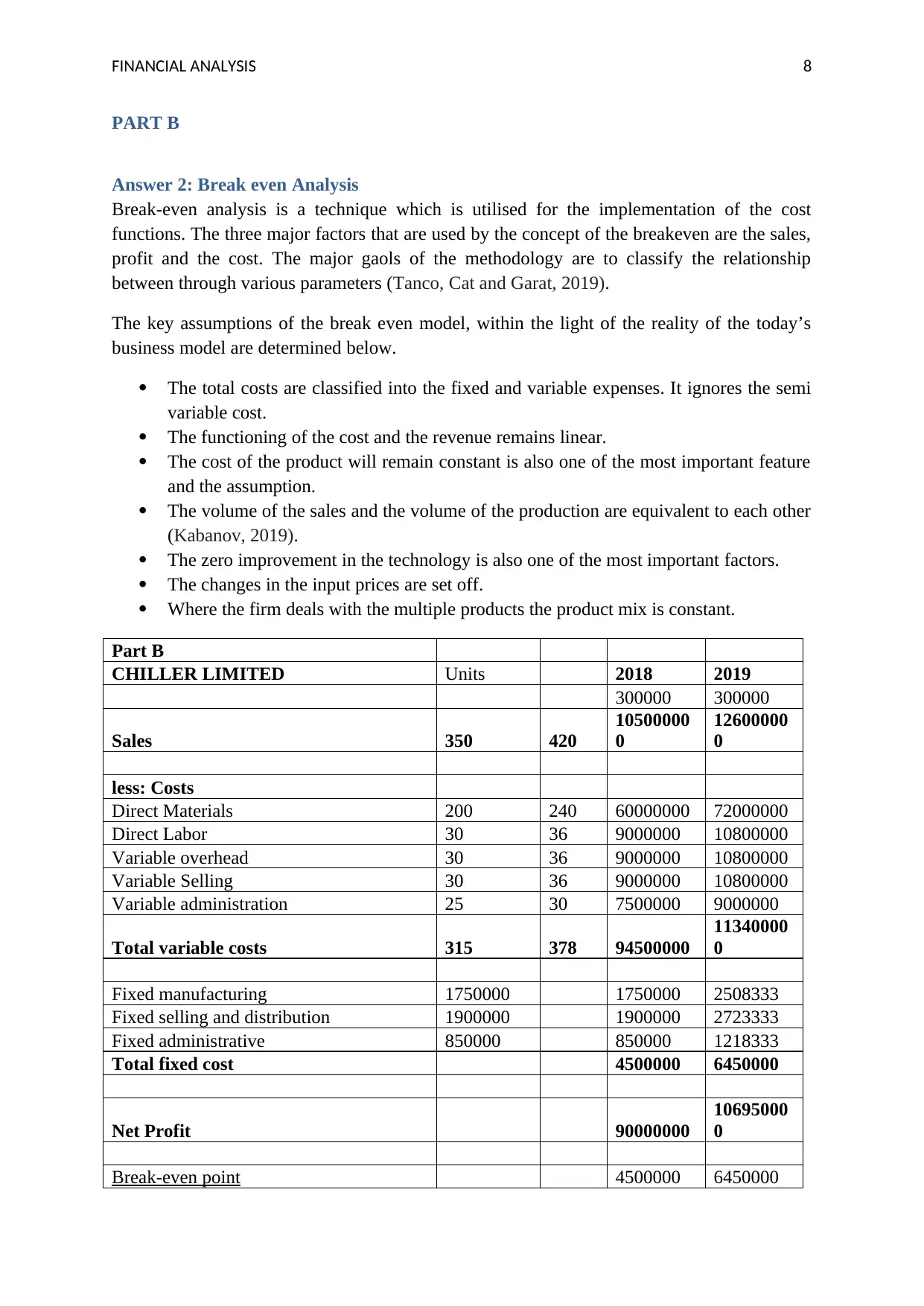

Part B

CHILLER LIMITED Units 2018 2019

300000 300000

Sales 350 420

10500000

0

12600000

0

less: Costs

Direct Materials 200 240 60000000 72000000

Direct Labor 30 36 9000000 10800000

Variable overhead 30 36 9000000 10800000

Variable Selling 30 36 9000000 10800000

Variable administration 25 30 7500000 9000000

Total variable costs 315 378 94500000

11340000

0

Fixed manufacturing 1750000 1750000 2508333

Fixed selling and distribution 1900000 1900000 2723333

Fixed administrative 850000 850000 1218333

Total fixed cost 4500000 6450000

Net Profit 90000000

10695000

0

Break-even point 4500000 6450000

PART B

Answer 2: Break even Analysis

Break-even analysis is a technique which is utilised for the implementation of the cost

functions. The three major factors that are used by the concept of the breakeven are the sales,

profit and the cost. The major gaols of the methodology are to classify the relationship

between through various parameters (Tanco, Cat and Garat, 2019).

The key assumptions of the break even model, within the light of the reality of the today’s

business model are determined below.

The total costs are classified into the fixed and variable expenses. It ignores the semi

variable cost.

The functioning of the cost and the revenue remains linear.

The cost of the product will remain constant is also one of the most important feature

and the assumption.

The volume of the sales and the volume of the production are equivalent to each other

(Kabanov, 2019).

The zero improvement in the technology is also one of the most important factors.

The changes in the input prices are set off.

Where the firm deals with the multiple products the product mix is constant.

Part B

CHILLER LIMITED Units 2018 2019

300000 300000

Sales 350 420

10500000

0

12600000

0

less: Costs

Direct Materials 200 240 60000000 72000000

Direct Labor 30 36 9000000 10800000

Variable overhead 30 36 9000000 10800000

Variable Selling 30 36 9000000 10800000

Variable administration 25 30 7500000 9000000

Total variable costs 315 378 94500000

11340000

0

Fixed manufacturing 1750000 1750000 2508333

Fixed selling and distribution 1900000 1900000 2723333

Fixed administrative 850000 850000 1218333

Total fixed cost 4500000 6450000

Net Profit 90000000

10695000

0

Break-even point 4500000 6450000

FINANCIAL ANALYSIS 9

Contribution margin per unit 35 42

Breakeven point (in units) 128571 153571

Breakeven point (in dollars)

Fixed costs/ contribution margin ratio 45000000 64500000

Margin of Safety (in units)

Actual units - Breakeven units 171429 146429

Margin of safety (in dollars)

Actual sales - Breakeven sales 60000000 61500000

The breakeven units are 128571 for the financial year 2018 and the same has been increased

in over the year 2019 to 153571. Overall the company needs to maintain the number of units

to be in a situation of no profit and no loss. Beyond that if the company keeps a record of low

units the losses will be incurred. The margin of safety on the other hand is 171429 and the

same has been reduced to 146429.

PART C

Answer 1

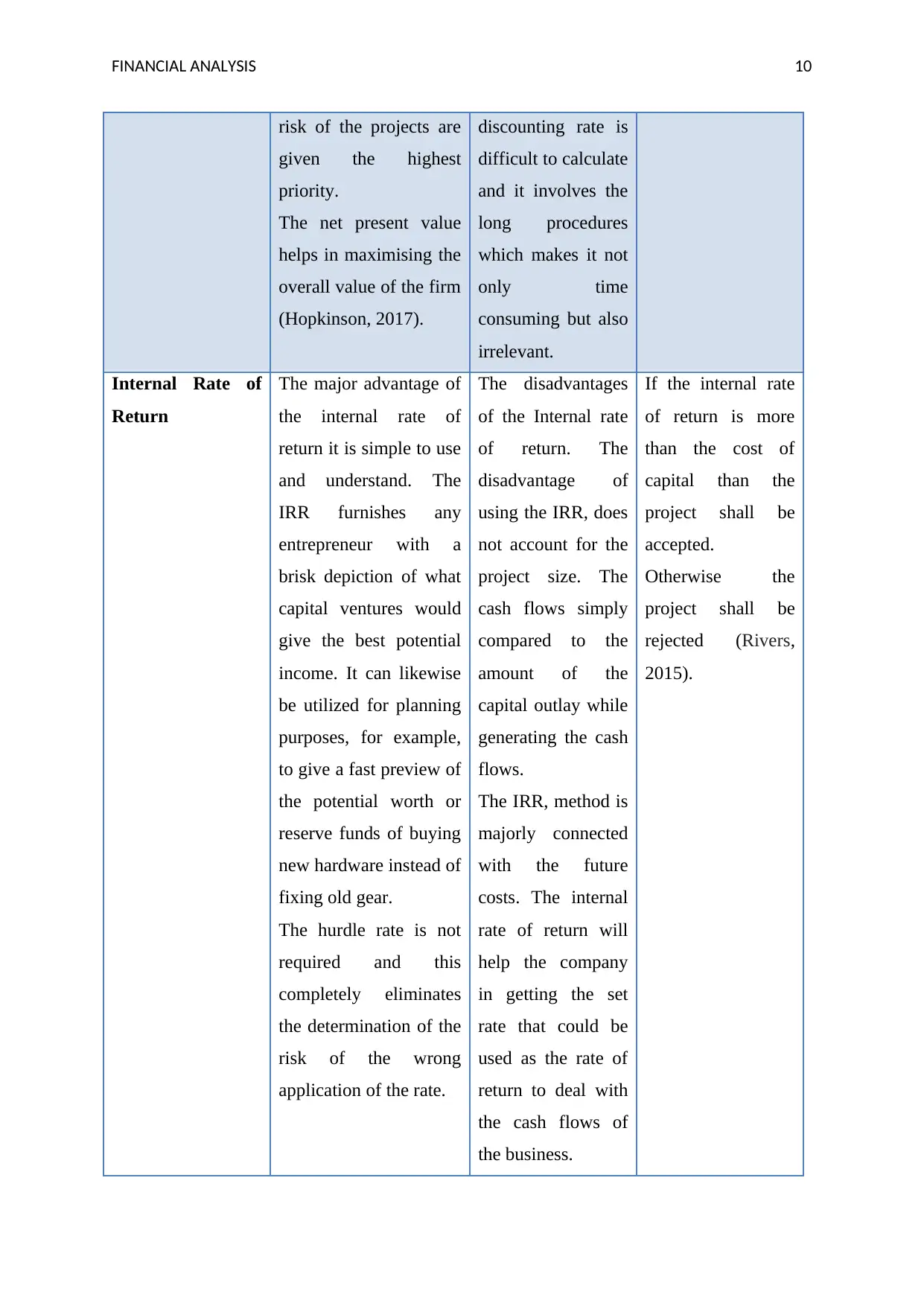

Basis Advantages Disadvantages Criteria to meet

Net Present Value The basic advantage of

the NPV is that it gives

the importance to the

time value of the

money.

The good part of the

NPV is that it considers

the cash flow before

and after the tax cash

flow to judge the

overall potential of the

project.

The profitability and the

The major

disadvantages of

the net present

value of the firm

are at times it

becomes difficult to

use and the

implement its

results while

deciding project

shall be accepted or

declined.

Sometimes the

A positive NPV

shows a positive

aspect whereas the

negative NPV

shows the project

shall be deducted.

Contribution margin per unit 35 42

Breakeven point (in units) 128571 153571

Breakeven point (in dollars)

Fixed costs/ contribution margin ratio 45000000 64500000

Margin of Safety (in units)

Actual units - Breakeven units 171429 146429

Margin of safety (in dollars)

Actual sales - Breakeven sales 60000000 61500000

The breakeven units are 128571 for the financial year 2018 and the same has been increased

in over the year 2019 to 153571. Overall the company needs to maintain the number of units

to be in a situation of no profit and no loss. Beyond that if the company keeps a record of low

units the losses will be incurred. The margin of safety on the other hand is 171429 and the

same has been reduced to 146429.

PART C

Answer 1

Basis Advantages Disadvantages Criteria to meet

Net Present Value The basic advantage of

the NPV is that it gives

the importance to the

time value of the

money.

The good part of the

NPV is that it considers

the cash flow before

and after the tax cash

flow to judge the

overall potential of the

project.

The profitability and the

The major

disadvantages of

the net present

value of the firm

are at times it

becomes difficult to

use and the

implement its

results while

deciding project

shall be accepted or

declined.

Sometimes the

A positive NPV

shows a positive

aspect whereas the

negative NPV

shows the project

shall be deducted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS 10

risk of the projects are

given the highest

priority.

The net present value

helps in maximising the

overall value of the firm

(Hopkinson, 2017).

discounting rate is

difficult to calculate

and it involves the

long procedures

which makes it not

only time

consuming but also

irrelevant.

Internal Rate of

Return

The major advantage of

the internal rate of

return it is simple to use

and understand. The

IRR furnishes any

entrepreneur with a

brisk depiction of what

capital ventures would

give the best potential

income. It can likewise

be utilized for planning

purposes, for example,

to give a fast preview of

the potential worth or

reserve funds of buying

new hardware instead of

fixing old gear.

The hurdle rate is not

required and this

completely eliminates

the determination of the

risk of the wrong

application of the rate.

The disadvantages

of the Internal rate

of return. The

disadvantage of

using the IRR, does

not account for the

project size. The

cash flows simply

compared to the

amount of the

capital outlay while

generating the cash

flows.

The IRR, method is

majorly connected

with the future

costs. The internal

rate of return will

help the company

in getting the set

rate that could be

used as the rate of

return to deal with

the cash flows of

the business.

If the internal rate

of return is more

than the cost of

capital than the

project shall be

accepted.

Otherwise the

project shall be

rejected (Rivers,

2015).

risk of the projects are

given the highest

priority.

The net present value

helps in maximising the

overall value of the firm

(Hopkinson, 2017).

discounting rate is

difficult to calculate

and it involves the

long procedures

which makes it not

only time

consuming but also

irrelevant.

Internal Rate of

Return

The major advantage of

the internal rate of

return it is simple to use

and understand. The

IRR furnishes any

entrepreneur with a

brisk depiction of what

capital ventures would

give the best potential

income. It can likewise

be utilized for planning

purposes, for example,

to give a fast preview of

the potential worth or

reserve funds of buying

new hardware instead of

fixing old gear.

The hurdle rate is not

required and this

completely eliminates

the determination of the

risk of the wrong

application of the rate.

The disadvantages

of the Internal rate

of return. The

disadvantage of

using the IRR, does

not account for the

project size. The

cash flows simply

compared to the

amount of the

capital outlay while

generating the cash

flows.

The IRR, method is

majorly connected

with the future

costs. The internal

rate of return will

help the company

in getting the set

rate that could be

used as the rate of

return to deal with

the cash flows of

the business.

If the internal rate

of return is more

than the cost of

capital than the

project shall be

accepted.

Otherwise the

project shall be

rejected (Rivers,

2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS 11

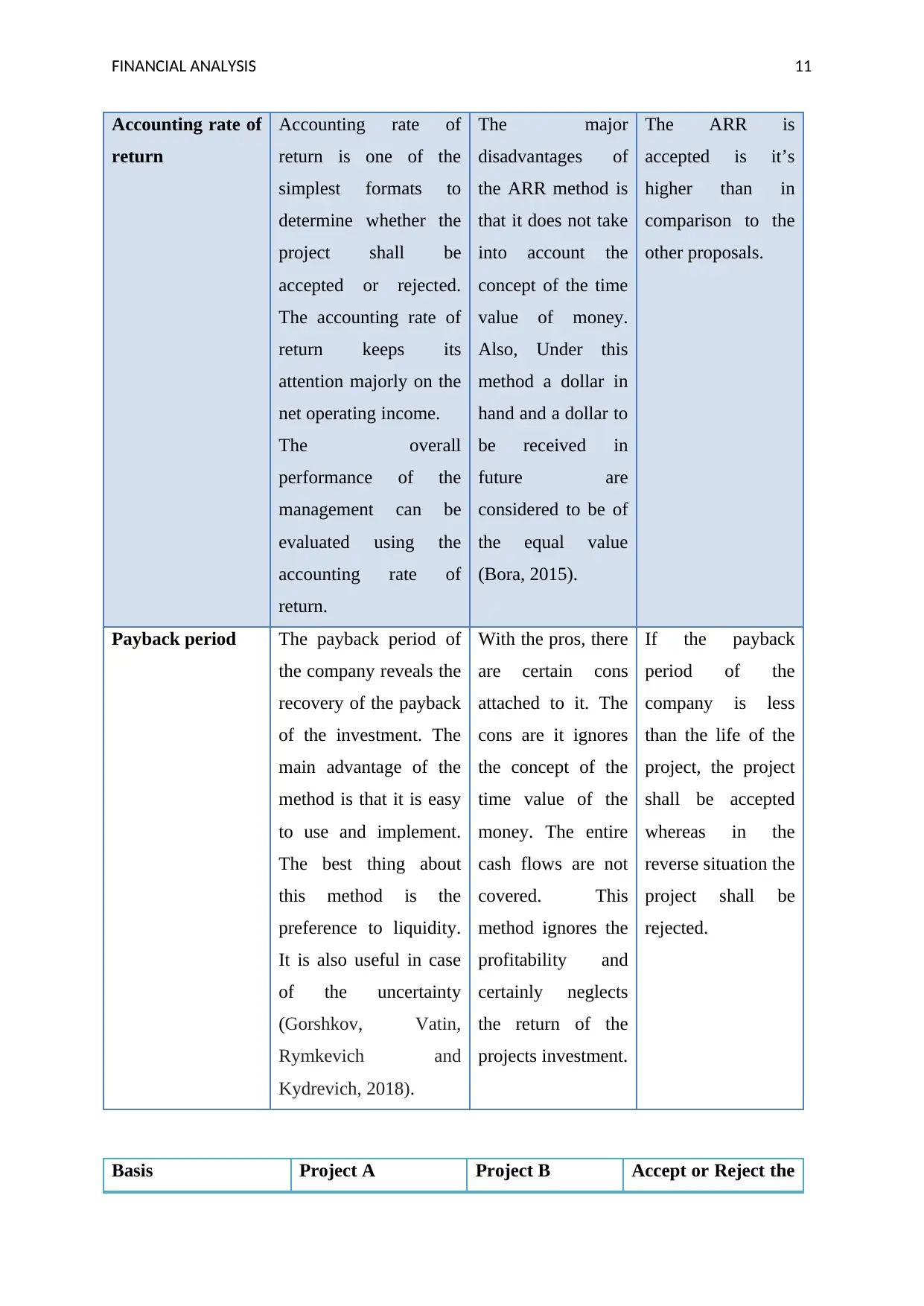

Accounting rate of

return

Accounting rate of

return is one of the

simplest formats to

determine whether the

project shall be

accepted or rejected.

The accounting rate of

return keeps its

attention majorly on the

net operating income.

The overall

performance of the

management can be

evaluated using the

accounting rate of

return.

The major

disadvantages of

the ARR method is

that it does not take

into account the

concept of the time

value of money.

Also, Under this

method a dollar in

hand and a dollar to

be received in

future are

considered to be of

the equal value

(Bora, 2015).

The ARR is

accepted is it’s

higher than in

comparison to the

other proposals.

Payback period The payback period of

the company reveals the

recovery of the payback

of the investment. The

main advantage of the

method is that it is easy

to use and implement.

The best thing about

this method is the

preference to liquidity.

It is also useful in case

of the uncertainty

(Gorshkov, Vatin,

Rymkevich and

Kydrevich, 2018).

With the pros, there

are certain cons

attached to it. The

cons are it ignores

the concept of the

time value of the

money. The entire

cash flows are not

covered. This

method ignores the

profitability and

certainly neglects

the return of the

projects investment.

If the payback

period of the

company is less

than the life of the

project, the project

shall be accepted

whereas in the

reverse situation the

project shall be

rejected.

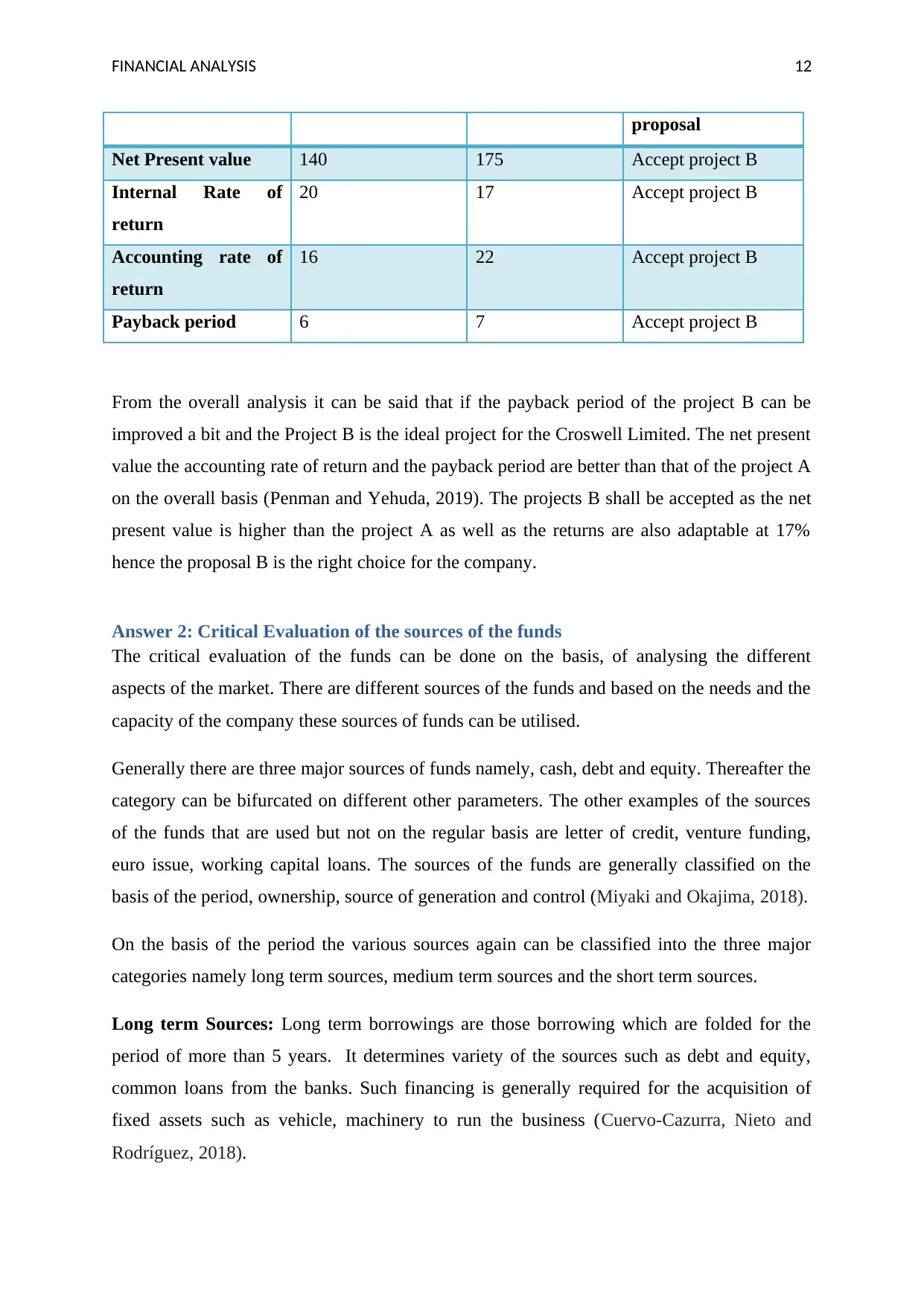

Basis Project A Project B Accept or Reject the

Accounting rate of

return

Accounting rate of

return is one of the

simplest formats to

determine whether the

project shall be

accepted or rejected.

The accounting rate of

return keeps its

attention majorly on the

net operating income.

The overall

performance of the

management can be

evaluated using the

accounting rate of

return.

The major

disadvantages of

the ARR method is

that it does not take

into account the

concept of the time

value of money.

Also, Under this

method a dollar in

hand and a dollar to

be received in

future are

considered to be of

the equal value

(Bora, 2015).

The ARR is

accepted is it’s

higher than in

comparison to the

other proposals.

Payback period The payback period of

the company reveals the

recovery of the payback

of the investment. The

main advantage of the

method is that it is easy

to use and implement.

The best thing about

this method is the

preference to liquidity.

It is also useful in case

of the uncertainty

(Gorshkov, Vatin,

Rymkevich and

Kydrevich, 2018).

With the pros, there

are certain cons

attached to it. The

cons are it ignores

the concept of the

time value of the

money. The entire

cash flows are not

covered. This

method ignores the

profitability and

certainly neglects

the return of the

projects investment.

If the payback

period of the

company is less

than the life of the

project, the project

shall be accepted

whereas in the

reverse situation the

project shall be

rejected.

Basis Project A Project B Accept or Reject the

FINANCIAL ANALYSIS 12

proposal

Net Present value 140 175 Accept project B

Internal Rate of

return

20 17 Accept project B

Accounting rate of

return

16 22 Accept project B

Payback period 6 7 Accept project B

From the overall analysis it can be said that if the payback period of the project B can be

improved a bit and the Project B is the ideal project for the Croswell Limited. The net present

value the accounting rate of return and the payback period are better than that of the project A

on the overall basis (Penman and Yehuda, 2019). The projects B shall be accepted as the net

present value is higher than the project A as well as the returns are also adaptable at 17%

hence the proposal B is the right choice for the company.

Answer 2: Critical Evaluation of the sources of the funds

The critical evaluation of the funds can be done on the basis, of analysing the different

aspects of the market. There are different sources of the funds and based on the needs and the

capacity of the company these sources of funds can be utilised.

Generally there are three major sources of funds namely, cash, debt and equity. Thereafter the

category can be bifurcated on different other parameters. The other examples of the sources

of the funds that are used but not on the regular basis are letter of credit, venture funding,

euro issue, working capital loans. The sources of the funds are generally classified on the

basis of the period, ownership, source of generation and control (Miyaki and Okajima, 2018).

On the basis of the period the various sources again can be classified into the three major

categories namely long term sources, medium term sources and the short term sources.

Long term Sources: Long term borrowings are those borrowing which are folded for the

period of more than 5 years. It determines variety of the sources such as debt and equity,

common loans from the banks. Such financing is generally required for the acquisition of

fixed assets such as vehicle, machinery to run the business (Cuervo-Cazurra, Nieto and

Rodríguez, 2018).

proposal

Net Present value 140 175 Accept project B

Internal Rate of

return

20 17 Accept project B

Accounting rate of

return

16 22 Accept project B

Payback period 6 7 Accept project B

From the overall analysis it can be said that if the payback period of the project B can be

improved a bit and the Project B is the ideal project for the Croswell Limited. The net present

value the accounting rate of return and the payback period are better than that of the project A

on the overall basis (Penman and Yehuda, 2019). The projects B shall be accepted as the net

present value is higher than the project A as well as the returns are also adaptable at 17%

hence the proposal B is the right choice for the company.

Answer 2: Critical Evaluation of the sources of the funds

The critical evaluation of the funds can be done on the basis, of analysing the different

aspects of the market. There are different sources of the funds and based on the needs and the

capacity of the company these sources of funds can be utilised.

Generally there are three major sources of funds namely, cash, debt and equity. Thereafter the

category can be bifurcated on different other parameters. The other examples of the sources

of the funds that are used but not on the regular basis are letter of credit, venture funding,

euro issue, working capital loans. The sources of the funds are generally classified on the

basis of the period, ownership, source of generation and control (Miyaki and Okajima, 2018).

On the basis of the period the various sources again can be classified into the three major

categories namely long term sources, medium term sources and the short term sources.

Long term Sources: Long term borrowings are those borrowing which are folded for the

period of more than 5 years. It determines variety of the sources such as debt and equity,

common loans from the banks. Such financing is generally required for the acquisition of

fixed assets such as vehicle, machinery to run the business (Cuervo-Cazurra, Nieto and

Rodríguez, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.