Financial Analysis (Definition, Guide)

Added on 2022-08-26

35 Pages9194 Words20 Views

Running head: FINANCIAL ANALYSIS

Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

FINANCIAL ANALYSIS1

Table of Contents

1.0 Introduction.......................................................................................................... 2

1.1 Overview of Strategic Financial Analysis...........................................................2

1.2 Background of Companies................................................................................. 2

1.3 Purpose of the report........................................................................................ 2

1.4 Structure of the report...................................................................................... 2

Ratio Analysis....................................................................................................... 2

Common Size Statement...................................................................................... 3

DuPont................................................................................................................. 3

2.0 Strategic Financial Analysis..................................................................................3

2.1 Ratio analysis – 3-Year Trend, year on year trend analysis...............................3

2.1.1 Profitability.................................................................................................. 3

2.1.2 Liquidity...................................................................................................... 5

2.1.3 Solvency...................................................................................................... 7

2.1.4 Efficiency..................................................................................................... 8

2.1.5 Investor..................................................................................................... 10

2.2 Common Size statement................................................................................. 12

2.2.1 Vertical common size analysis..................................................................12

2.2.2 Horizontal common size analysis..............................................................12

2.3 DuPont............................................................................................................ 12

3.0 Analysis and Evaluation of Limitations and Strengths of Methods......................13

3.1 Ratio Analysis.................................................................................................. 13

3.1.1 Ratio Analysis – Limitations and Strengths................................................13

3.1.2. Contemporary Methods Proposed to Minimize Limitations of Ratio Analysis

........................................................................................................................... 13

3.2 Common Size Statement Analysis...................................................................14

3.2.1 Common Size Statement Analysis – Limitations and Strengths................14

3.2.2 Contemporary Methods Proposed to Minimize Common Size Statement

Analysis.............................................................................................................. 14

3.3 DuPont Analysis............................................................................................... 14

3.3.1 Common Size Statement Analysis – Limitations and Strengths................15

3.3.2 Contemporary Methods Proposed to Minimize DuPont Analysis................15

4.0 Conclusion and Recommendations.....................................................................15

6.0 Appendix............................................................................................................ 16

Table of Contents

1.0 Introduction.......................................................................................................... 2

1.1 Overview of Strategic Financial Analysis...........................................................2

1.2 Background of Companies................................................................................. 2

1.3 Purpose of the report........................................................................................ 2

1.4 Structure of the report...................................................................................... 2

Ratio Analysis....................................................................................................... 2

Common Size Statement...................................................................................... 3

DuPont................................................................................................................. 3

2.0 Strategic Financial Analysis..................................................................................3

2.1 Ratio analysis – 3-Year Trend, year on year trend analysis...............................3

2.1.1 Profitability.................................................................................................. 3

2.1.2 Liquidity...................................................................................................... 5

2.1.3 Solvency...................................................................................................... 7

2.1.4 Efficiency..................................................................................................... 8

2.1.5 Investor..................................................................................................... 10

2.2 Common Size statement................................................................................. 12

2.2.1 Vertical common size analysis..................................................................12

2.2.2 Horizontal common size analysis..............................................................12

2.3 DuPont............................................................................................................ 12

3.0 Analysis and Evaluation of Limitations and Strengths of Methods......................13

3.1 Ratio Analysis.................................................................................................. 13

3.1.1 Ratio Analysis – Limitations and Strengths................................................13

3.1.2. Contemporary Methods Proposed to Minimize Limitations of Ratio Analysis

........................................................................................................................... 13

3.2 Common Size Statement Analysis...................................................................14

3.2.1 Common Size Statement Analysis – Limitations and Strengths................14

3.2.2 Contemporary Methods Proposed to Minimize Common Size Statement

Analysis.............................................................................................................. 14

3.3 DuPont Analysis............................................................................................... 14

3.3.1 Common Size Statement Analysis – Limitations and Strengths................15

3.3.2 Contemporary Methods Proposed to Minimize DuPont Analysis................15

4.0 Conclusion and Recommendations.....................................................................15

6.0 Appendix............................................................................................................ 16

FINANCIAL ANALYSIS2

6.1 Vertical............................................................................................................ 16

6.2 Horizontal........................................................................................................ 20

References............................................................................................................... 26

6.1 Vertical............................................................................................................ 16

6.2 Horizontal........................................................................................................ 20

References............................................................................................................... 26

FINANCIAL ANALYSIS3

1.0 Introduction

1.1 Overview of Strategic Financial Analysis

Strategic financial analysis is the method of combination tool to interpret the financial

information to foresee whether the organization is moving towards in achieving the goals from

the financial perspective. Strategic financial analysis provides information and helps in assisting

the company and their stake holders to accomplish their mission. It helps to seek answers for

whether the company has performed successfully, comparatively to its own past performance

and to its competitors and helps to analyse future performance or the value of the company and

shares it issues. Strategic financial analysis uses data such as company’s annual report, financial

statements and notes, and management commentary (operating and financial review or

management’s discussion and analysis) to identify financial risks and key ratio is used to

calculate the financial health (Elaine Henry 2011 and Prager 2005).

1.2 Background of Companies

Wolseley was discovered in 1887 by Frederick York Wolseley started as Wolseley Sheep

Shearing Machine Company. The company then further extended to manufacture. During the

period 1901, the company started to sell car and machine tool business which became a part of

Morris Motors, BMC, British Leyland and Rover Group. On 31st July 2017 Wolseley plc

changed its name to Ferguson plc. Ferguson has over 1 million customers served by 35,000

associates in 2,280 locations (corporate.wolseley.co.uk).

Tate & Lyle was founded by Henry Tate & sons and Abram Lyle & Sons in 1921 where

the initially started as sugar refining business. After 1970’s they started to expanded to raw

materials such as corn and tapioca into ingredients that add taste, texture, and nutrients to food

and beverages. Now the Tate &Lyle is well known for the global supplier of food and beverage

ingredients to industrial market. Tate & Lyle started as a small factory in Liverpool to now

delivering from 30 countries from over 70 location (tateandlyle.com)

1.3 Purpose of the report

The purpose of the report is to analyse and compare the three statement which are;

income statement, balance sheet and cash flow statement of two companies (Wolseley and Tate

& Lyle). Ratio analysis will be computed between the two companies to evaluate the financial

decision which helps to foresee the financial performance or problems in the long term and short

term and take necessary decision or strategy to overcome and grow in the market.

1.4 Structure of the report

The two companies’ ratio (profitability, liquidity, solvency, efficiency, investor) will

computed then common size statement analysis (vertical and horizontal common is size analysis)

will be evaluated and analysed along with the DuPont analysis (net profit margin, asset turnover

and equity multiplier).

Ratio Analysis

Ratio analysis is a quantitative method of gaining insight of the company’s financial

performance to predict the future of the company’s performance and problems but however the

ratios are only the indicators of company’s performance giving us an idea of what happened but

not why it happened (Henry 2011).

1.0 Introduction

1.1 Overview of Strategic Financial Analysis

Strategic financial analysis is the method of combination tool to interpret the financial

information to foresee whether the organization is moving towards in achieving the goals from

the financial perspective. Strategic financial analysis provides information and helps in assisting

the company and their stake holders to accomplish their mission. It helps to seek answers for

whether the company has performed successfully, comparatively to its own past performance

and to its competitors and helps to analyse future performance or the value of the company and

shares it issues. Strategic financial analysis uses data such as company’s annual report, financial

statements and notes, and management commentary (operating and financial review or

management’s discussion and analysis) to identify financial risks and key ratio is used to

calculate the financial health (Elaine Henry 2011 and Prager 2005).

1.2 Background of Companies

Wolseley was discovered in 1887 by Frederick York Wolseley started as Wolseley Sheep

Shearing Machine Company. The company then further extended to manufacture. During the

period 1901, the company started to sell car and machine tool business which became a part of

Morris Motors, BMC, British Leyland and Rover Group. On 31st July 2017 Wolseley plc

changed its name to Ferguson plc. Ferguson has over 1 million customers served by 35,000

associates in 2,280 locations (corporate.wolseley.co.uk).

Tate & Lyle was founded by Henry Tate & sons and Abram Lyle & Sons in 1921 where

the initially started as sugar refining business. After 1970’s they started to expanded to raw

materials such as corn and tapioca into ingredients that add taste, texture, and nutrients to food

and beverages. Now the Tate &Lyle is well known for the global supplier of food and beverage

ingredients to industrial market. Tate & Lyle started as a small factory in Liverpool to now

delivering from 30 countries from over 70 location (tateandlyle.com)

1.3 Purpose of the report

The purpose of the report is to analyse and compare the three statement which are;

income statement, balance sheet and cash flow statement of two companies (Wolseley and Tate

& Lyle). Ratio analysis will be computed between the two companies to evaluate the financial

decision which helps to foresee the financial performance or problems in the long term and short

term and take necessary decision or strategy to overcome and grow in the market.

1.4 Structure of the report

The two companies’ ratio (profitability, liquidity, solvency, efficiency, investor) will

computed then common size statement analysis (vertical and horizontal common is size analysis)

will be evaluated and analysed along with the DuPont analysis (net profit margin, asset turnover

and equity multiplier).

Ratio Analysis

Ratio analysis is a quantitative method of gaining insight of the company’s financial

performance to predict the future of the company’s performance and problems but however the

ratios are only the indicators of company’s performance giving us an idea of what happened but

not why it happened (Henry 2011).

FINANCIAL ANALYSIS4

Common Size Statement

Common size statement is an income statement where each item in the income statement

is expressed as percentage of sales or revenue which is also known as vertical common analysis.

Common size statement can be divided into vertical and horizontal common size analysis (Ryan

2016). Horizontal analysis which is also knowns as the trend analysis is the method to analysis

the financial statement which shows the changes in the amounts of corresponding financial

statement items over a period of time (accountingformanagement.org).

DuPont

DuPont analysis is used evaluate the performance of the company such as the how well

the company assets are being used, to determine the profitability and to know the financial

position of the company. DuPont analysis uses profit margin, asset turnover and equity multiplier

ratio to analyse the company’s performance (Nurul 2018).

2.0 Strategic Financial Analysis

2.1 Ratio analysis – 3-Year Trend, year on year trend analysis

According to Myers, “Ratio analysis is a study of relationship among various financial

factors in a business” (Grewal 2016). Thus, it Is a method analysing the financial statement by

computing the ratio such as profitability, liquidity, solvency, efficiency and investors ratio. Ratio

analysis is to express the proportional relationship between the figures in the financial statement.

It is based on the balance sheet, income statement and cash flow (Sergio 2016).

2.1.1 Profitability

Profitability ratio is the measure that indicates of the ability of the company to earn profit.

Profitability of the company is analysed through Gross Profit Ratio (GPR), Operating Ratio (or),

Operating Profit Ratio (OPR), Net Profit Ratio (NPR) and Return on Investment or capital

Employed (ROI/ROCE) (Grewal 2016). Most of the organization uses Gross Profit Ratio

(GPR) and Net Profit Ratio (NPR) which will be used to calculate profitability ratio of

Wolseley and Tate & Lyle.

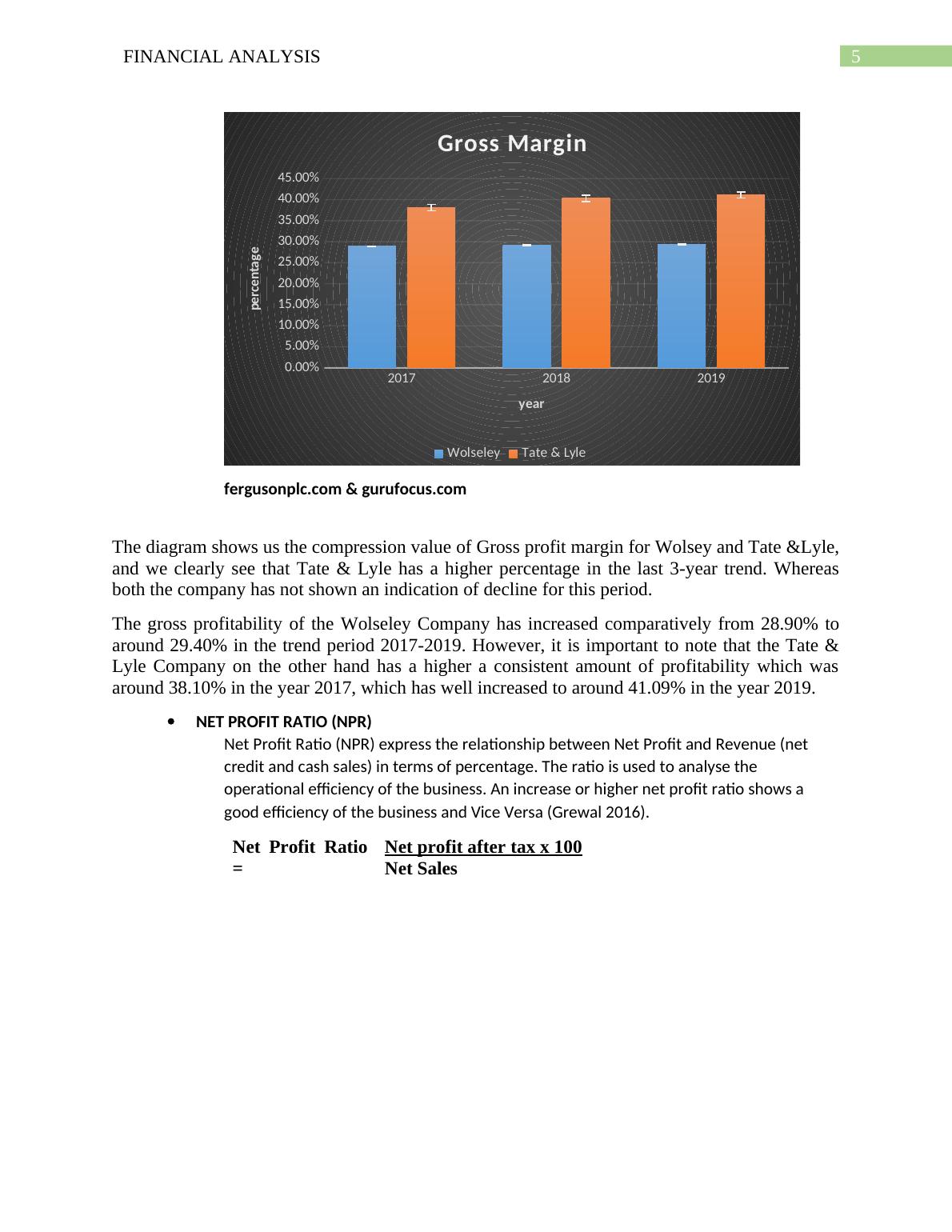

GROSS PROFIT RATIO (GPR)

Gross profit ratio (GPR) shows the connection between Gross Profit and

Revenue (net credit and cash sales) in terms of percentage. The ratio

is analysed to decide the efficiency with which production or purchase

operation and selling operations are carried on. A high Gross Profit

Ratio is sign of good management (Monica 2014).

Gross profit Gross profit

ratio =

Gross profit x 100

Net Sales

Common Size Statement

Common size statement is an income statement where each item in the income statement

is expressed as percentage of sales or revenue which is also known as vertical common analysis.

Common size statement can be divided into vertical and horizontal common size analysis (Ryan

2016). Horizontal analysis which is also knowns as the trend analysis is the method to analysis

the financial statement which shows the changes in the amounts of corresponding financial

statement items over a period of time (accountingformanagement.org).

DuPont

DuPont analysis is used evaluate the performance of the company such as the how well

the company assets are being used, to determine the profitability and to know the financial

position of the company. DuPont analysis uses profit margin, asset turnover and equity multiplier

ratio to analyse the company’s performance (Nurul 2018).

2.0 Strategic Financial Analysis

2.1 Ratio analysis – 3-Year Trend, year on year trend analysis

According to Myers, “Ratio analysis is a study of relationship among various financial

factors in a business” (Grewal 2016). Thus, it Is a method analysing the financial statement by

computing the ratio such as profitability, liquidity, solvency, efficiency and investors ratio. Ratio

analysis is to express the proportional relationship between the figures in the financial statement.

It is based on the balance sheet, income statement and cash flow (Sergio 2016).

2.1.1 Profitability

Profitability ratio is the measure that indicates of the ability of the company to earn profit.

Profitability of the company is analysed through Gross Profit Ratio (GPR), Operating Ratio (or),

Operating Profit Ratio (OPR), Net Profit Ratio (NPR) and Return on Investment or capital

Employed (ROI/ROCE) (Grewal 2016). Most of the organization uses Gross Profit Ratio

(GPR) and Net Profit Ratio (NPR) which will be used to calculate profitability ratio of

Wolseley and Tate & Lyle.

GROSS PROFIT RATIO (GPR)

Gross profit ratio (GPR) shows the connection between Gross Profit and

Revenue (net credit and cash sales) in terms of percentage. The ratio

is analysed to decide the efficiency with which production or purchase

operation and selling operations are carried on. A high Gross Profit

Ratio is sign of good management (Monica 2014).

Gross profit Gross profit

ratio =

Gross profit x 100

Net Sales

FINANCIAL ANALYSIS5

2017 2018 2019

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

Gross Margin

Wolseley Tate & Lyle

year

percentage

fergusonplc.com & gurufocus.com

The diagram shows us the compression value of Gross profit margin for Wolsey and Tate &Lyle,

and we clearly see that Tate & Lyle has a higher percentage in the last 3-year trend. Whereas

both the company has not shown an indication of decline for this period.

The gross profitability of the Wolseley Company has increased comparatively from 28.90% to

around 29.40% in the trend period 2017-2019. However, it is important to note that the Tate &

Lyle Company on the other hand has a higher a consistent amount of profitability which was

around 38.10% in the year 2017, which has well increased to around 41.09% in the year 2019.

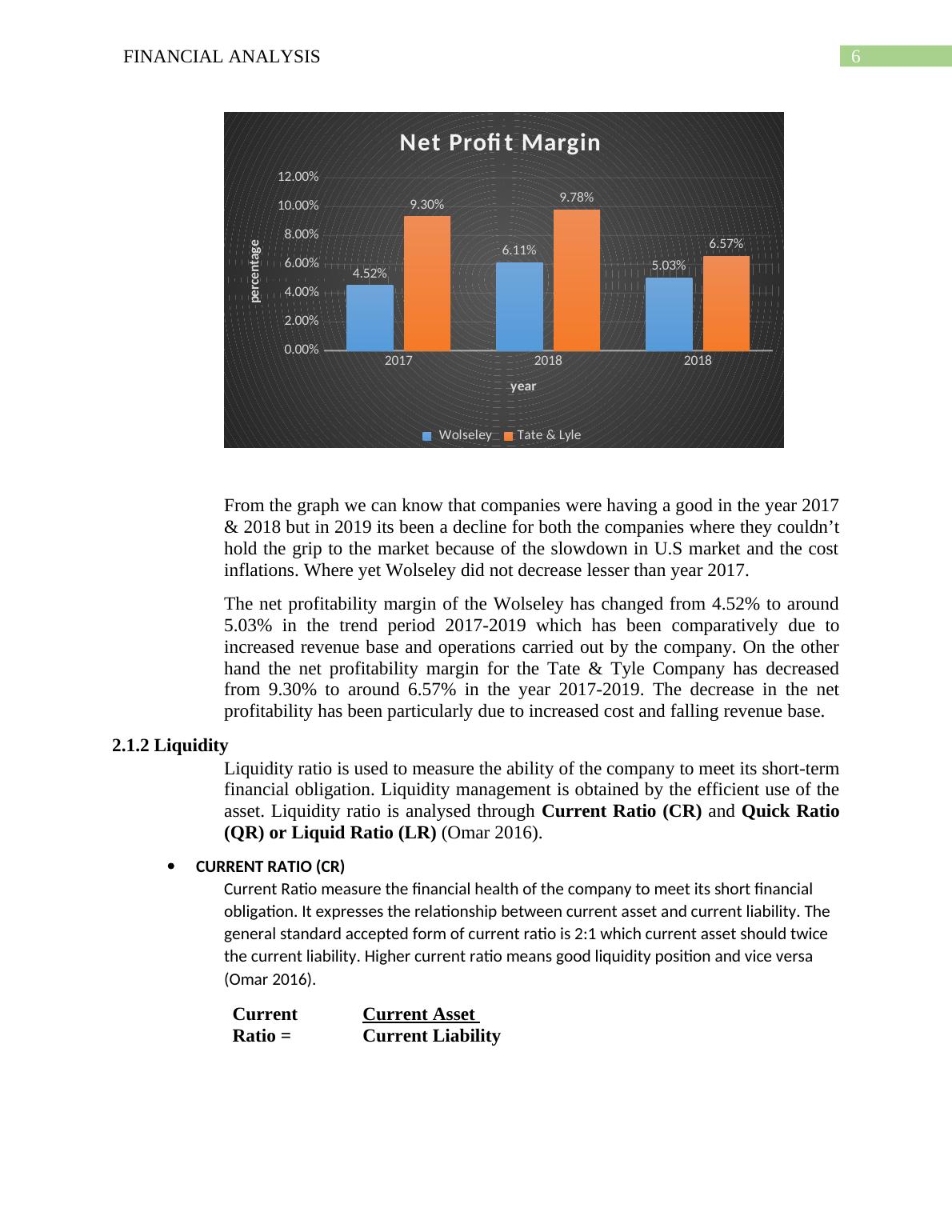

NET PROFIT RATIO (NPR)

Net Profit Ratio (NPR) express the relationship between Net Profit and

Revenue (net credit and cash sales) in terms of percentage. The ratio

is used to analyse the operational efficiency of the business. An

increase or higher net profit ratio shows a good efficiency of the

business and Vice Versa (Grewal 2016).

Net Profit Ratio

=

Net profit after tax x 100

Net Sales

2017 2018 2019

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

Gross Margin

Wolseley Tate & Lyle

year

percentage

fergusonplc.com & gurufocus.com

The diagram shows us the compression value of Gross profit margin for Wolsey and Tate &Lyle,

and we clearly see that Tate & Lyle has a higher percentage in the last 3-year trend. Whereas

both the company has not shown an indication of decline for this period.

The gross profitability of the Wolseley Company has increased comparatively from 28.90% to

around 29.40% in the trend period 2017-2019. However, it is important to note that the Tate &

Lyle Company on the other hand has a higher a consistent amount of profitability which was

around 38.10% in the year 2017, which has well increased to around 41.09% in the year 2019.

NET PROFIT RATIO (NPR)

Net Profit Ratio (NPR) express the relationship between Net Profit and

Revenue (net credit and cash sales) in terms of percentage. The ratio

is used to analyse the operational efficiency of the business. An

increase or higher net profit ratio shows a good efficiency of the

business and Vice Versa (Grewal 2016).

Net Profit Ratio

=

Net profit after tax x 100

Net Sales

FINANCIAL ANALYSIS6

2017 2018 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

4.52%

6.11%

5.03%

9.30% 9.78%

6.57%

Net Profi t Margin

Wolseley Tate & Lyle

year

percentage

From the graph we can know that companies were having a good in the year 2017

& 2018 but in 2019 its been a decline for both the companies where they couldn’t

hold the grip to the market because of the slowdown in U.S market and the cost

inflations. Where yet Wolseley did not decrease lesser than year 2017.

The net profitability margin of the Wolseley has changed from 4.52% to around

5.03% in the trend period 2017-2019 which has been comparatively due to

increased revenue base and operations carried out by the company. On the other

hand the net profitability margin for the Tate & Tyle Company has decreased

from 9.30% to around 6.57% in the year 2017-2019. The decrease in the net

profitability has been particularly due to increased cost and falling revenue base.

2.1.2 Liquidity

Liquidity ratio is used to measure the ability of the company to meet its short-term

financial obligation. Liquidity management is obtained by the efficient use of the

asset. Liquidity ratio is analysed through Current Ratio (CR) and Quick Ratio

(QR) or Liquid Ratio (LR) (Omar 2016).

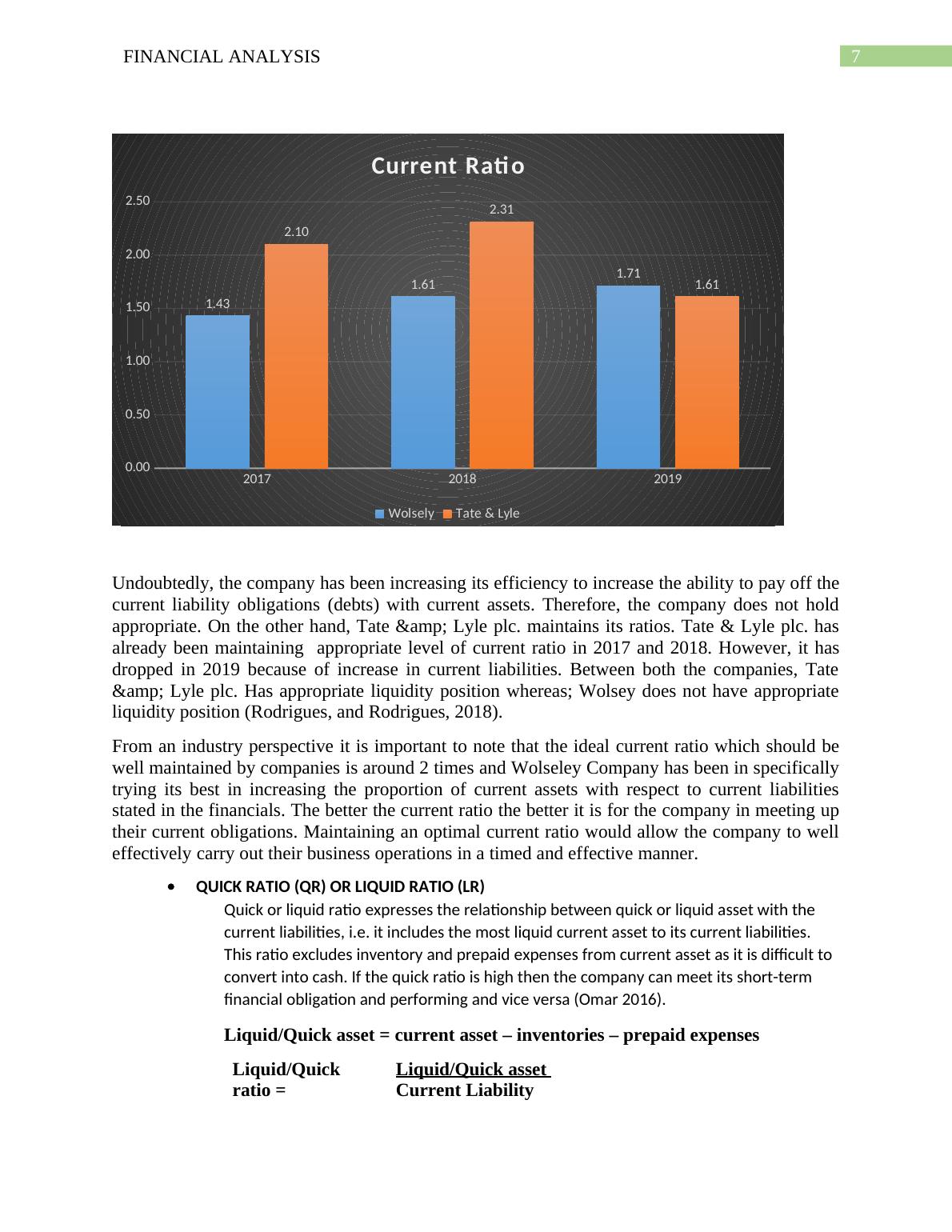

CURRENT RATIO (CR)

Current Ratio measure the financial health of the company to meet its

short financial obligation. It expresses the relationship between current

asset and current liability. The general standard accepted form of

current ratio is 2:1 which current asset should twice the current

liability. Higher current ratio means good liquidity position and vice

versa (Omar 2016).

Current

Ratio =

Current Asset

Current Liability

2017 2018 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

4.52%

6.11%

5.03%

9.30% 9.78%

6.57%

Net Profi t Margin

Wolseley Tate & Lyle

year

percentage

From the graph we can know that companies were having a good in the year 2017

& 2018 but in 2019 its been a decline for both the companies where they couldn’t

hold the grip to the market because of the slowdown in U.S market and the cost

inflations. Where yet Wolseley did not decrease lesser than year 2017.

The net profitability margin of the Wolseley has changed from 4.52% to around

5.03% in the trend period 2017-2019 which has been comparatively due to

increased revenue base and operations carried out by the company. On the other

hand the net profitability margin for the Tate & Tyle Company has decreased

from 9.30% to around 6.57% in the year 2017-2019. The decrease in the net

profitability has been particularly due to increased cost and falling revenue base.

2.1.2 Liquidity

Liquidity ratio is used to measure the ability of the company to meet its short-term

financial obligation. Liquidity management is obtained by the efficient use of the

asset. Liquidity ratio is analysed through Current Ratio (CR) and Quick Ratio

(QR) or Liquid Ratio (LR) (Omar 2016).

CURRENT RATIO (CR)

Current Ratio measure the financial health of the company to meet its

short financial obligation. It expresses the relationship between current

asset and current liability. The general standard accepted form of

current ratio is 2:1 which current asset should twice the current

liability. Higher current ratio means good liquidity position and vice

versa (Omar 2016).

Current

Ratio =

Current Asset

Current Liability

FINANCIAL ANALYSIS7

2017 2018 2019

0.00

0.50

1.00

1.50

2.00

2.50

1.43

1.61 1.71

2.10

2.31

1.61

Current Ratio

Wolsely Tate & Lyle

Undoubtedly, the company has been increasing its efficiency to increase the ability to pay off the

current liability obligations (debts) with current assets. Therefore, the company does not hold

appropriate. On the other hand, Tate & Lyle plc. maintains its ratios. Tate & Lyle plc. has

already been maintaining appropriate level of current ratio in 2017 and 2018. However, it has

dropped in 2019 because of increase in current liabilities. Between both the companies, Tate

& Lyle plc. Has appropriate liquidity position whereas; Wolsey does not have appropriate

liquidity position (Rodrigues, and Rodrigues, 2018).

From an industry perspective it is important to note that the ideal current ratio which should be

well maintained by companies is around 2 times and Wolseley Company has been in specifically

trying its best in increasing the proportion of current assets with respect to current liabilities

stated in the financials. The better the current ratio the better it is for the company in meeting up

their current obligations. Maintaining an optimal current ratio would allow the company to well

effectively carry out their business operations in a timed and effective manner.

QUICK RATIO (QR) OR LIQUID RATIO (LR)

Quick or liquid ratio expresses the relationship between quick or liquid

asset with the current liabilities, i.e. it includes the most liquid current

asset to its current liabilities. This ratio excludes inventory and

prepaid expenses from current asset as it is difficult to convert into

cash. If the quick ratio is high then the company can meet its short-

term financial obligation and performing and vice versa (Omar 2016).

Liquid/Quick asset = current asset – inventories – prepaid expenses

Liquid/Quick

ratio =

Liquid/Quick asset

Current Liability

2017 2018 2019

0.00

0.50

1.00

1.50

2.00

2.50

1.43

1.61 1.71

2.10

2.31

1.61

Current Ratio

Wolsely Tate & Lyle

Undoubtedly, the company has been increasing its efficiency to increase the ability to pay off the

current liability obligations (debts) with current assets. Therefore, the company does not hold

appropriate. On the other hand, Tate & Lyle plc. maintains its ratios. Tate & Lyle plc. has

already been maintaining appropriate level of current ratio in 2017 and 2018. However, it has

dropped in 2019 because of increase in current liabilities. Between both the companies, Tate

& Lyle plc. Has appropriate liquidity position whereas; Wolsey does not have appropriate

liquidity position (Rodrigues, and Rodrigues, 2018).

From an industry perspective it is important to note that the ideal current ratio which should be

well maintained by companies is around 2 times and Wolseley Company has been in specifically

trying its best in increasing the proportion of current assets with respect to current liabilities

stated in the financials. The better the current ratio the better it is for the company in meeting up

their current obligations. Maintaining an optimal current ratio would allow the company to well

effectively carry out their business operations in a timed and effective manner.

QUICK RATIO (QR) OR LIQUID RATIO (LR)

Quick or liquid ratio expresses the relationship between quick or liquid

asset with the current liabilities, i.e. it includes the most liquid current

asset to its current liabilities. This ratio excludes inventory and

prepaid expenses from current asset as it is difficult to convert into

cash. If the quick ratio is high then the company can meet its short-

term financial obligation and performing and vice versa (Omar 2016).

Liquid/Quick asset = current asset – inventories – prepaid expenses

Liquid/Quick

ratio =

Liquid/Quick asset

Current Liability

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Overview of Strategic Financial Analysislg...

|20

|4417

|17

Strategic Financial Analysislg...

|55

|8602

|68

Strategic Financial Analysis TABLE OF CONTENTSlg...

|57

|13738

|400

Strategic Financial Analysis - Assignmentlg...

|32

|4920

|422

(DOC) Complete Strategic Finance Assignmentlg...

|46

|10766

|192

Financial Statements Analysis Processlg...

|25

|4694

|27