Financial Analysis of Gulf Hotels: ECM05EKM Assignment, Oman

VerifiedAdded on 2023/01/18

|17

|4201

|38

Homework Assignment

AI Summary

This assignment provides a comprehensive financial analysis of Gulf Hotels (Oman) Company Limited SAOG, a company listed on the Muscat Securities Market. The analysis utilizes both horizontal and vertical analysis techniques applied to the income statement and balance sheet for the years 2016-2018. The assignment evaluates the company's profitability and financial position, identifying trends and providing recommendations for improvement. It examines revenue, operating costs, and net profit to assess profitability, and analyzes assets, liabilities, and equity to determine financial health. The analysis reveals a decline in profitability due to falling revenue and a weakening liquidity position. Recommendations are provided to improve performance, including cross-promotional sales strategies and guest reward programs.

Running head: FINANCIAL ANALYSIS FOR MANAGERS

Financial Analysis for Managers

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Analysis for Managers

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS FOR MANAGERS

Table of Contents

Introduction:....................................................................................................................................2

Question 1:.......................................................................................................................................2

Introduction:................................................................................................................................2

Task A:.........................................................................................................................................2

Task B:.........................................................................................................................................6

Analysis of profitability position and financial position of Gulf Hotels (Oman) Company

Limited SAOG:............................................................................................................................7

Question 2:.....................................................................................................................................10

Task A:.......................................................................................................................................10

Task B:.......................................................................................................................................11

Task C:.......................................................................................................................................12

Question 3:.....................................................................................................................................12

Task A:.......................................................................................................................................12

Task B:.......................................................................................................................................13

Task C:.......................................................................................................................................14

References:....................................................................................................................................15

Table of Contents

Introduction:....................................................................................................................................2

Question 1:.......................................................................................................................................2

Introduction:................................................................................................................................2

Task A:.........................................................................................................................................2

Task B:.........................................................................................................................................6

Analysis of profitability position and financial position of Gulf Hotels (Oman) Company

Limited SAOG:............................................................................................................................7

Question 2:.....................................................................................................................................10

Task A:.......................................................................................................................................10

Task B:.......................................................................................................................................11

Task C:.......................................................................................................................................12

Question 3:.....................................................................................................................................12

Task A:.......................................................................................................................................12

Task B:.......................................................................................................................................13

Task C:.......................................................................................................................................14

References:....................................................................................................................................15

2FINANCIAL ANALYSIS FOR MANAGERS

Introduction:

The current assignment would provide a brief overview of the financial performance of

an organisation listed in Muscat Securities Exchange. The evaluation would be conducted with

the help of vertical analysis and horizontal analysis, which would assist in identifying the trends

in particular line items of the financial statements of the chosen organisation. Based on such

analysis, appropriate recommendations would be provided to the organisation so that it could

improve its financial performance in future. The second section of the assignment would deal

with undertaking suitable investment decision based on the provided alternatives with the help of

internal rate of return. Finally, the assignment would shed light on identifying the most profitable

scenario for the fertiliser manufacturer based on CVP analysis.

Question 1:

Introduction:

For this section, the organisation that has been selected is Gulf Hotels (Oman) Company

Limited SAOG. It owns and operates the Crowne Plaza Hotel in Muscat, the Sultanate of Oman

and it is listed in Muscat Securities Market (Bloomberg.com 2019). In this section, critical

analysis has been made in terms of evaluating the financial standing of the hotel in the Oman

market. The techniques used vertical analysis and horizontal analysis of the income statement

and balance sheet statement of the hotel for the past three years, which have assisted in gaining a

clear insight of its performance in the hospitality industry of Oman.

Task A:

Income statement (Profitability position):

Introduction:

The current assignment would provide a brief overview of the financial performance of

an organisation listed in Muscat Securities Exchange. The evaluation would be conducted with

the help of vertical analysis and horizontal analysis, which would assist in identifying the trends

in particular line items of the financial statements of the chosen organisation. Based on such

analysis, appropriate recommendations would be provided to the organisation so that it could

improve its financial performance in future. The second section of the assignment would deal

with undertaking suitable investment decision based on the provided alternatives with the help of

internal rate of return. Finally, the assignment would shed light on identifying the most profitable

scenario for the fertiliser manufacturer based on CVP analysis.

Question 1:

Introduction:

For this section, the organisation that has been selected is Gulf Hotels (Oman) Company

Limited SAOG. It owns and operates the Crowne Plaza Hotel in Muscat, the Sultanate of Oman

and it is listed in Muscat Securities Market (Bloomberg.com 2019). In this section, critical

analysis has been made in terms of evaluating the financial standing of the hotel in the Oman

market. The techniques used vertical analysis and horizontal analysis of the income statement

and balance sheet statement of the hotel for the past three years, which have assisted in gaining a

clear insight of its performance in the hospitality industry of Oman.

Task A:

Income statement (Profitability position):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS FOR MANAGERS

Vertical analysis of income statement for the years 2016-2018:

Particulars 2016 (in RO,000) Percentage 2017 (in RO,000) Percentage 2018 (in RO,000) Percentage

Revenue 8,186 100.00% 8,175 100.00% 6,342 100.00%

Operating costs 5,865- 71.65% 5,821- 71.20% 5,273- 83.14%

Management and licence fees 225- 2.75% 227- 2.78% 153- 2.41%

Reservation and market assessment fees 120- 1.47% 120- 1.47% 92- 1.45%

Operating profit 1,976 24.14% 2,007 24.55% 824 12.99%

Finance income 5 0.06% 7 0.09% 7 0.11%

Finance costs - 0.00% - 0.00% 28- 0.44%

Other income - 0.00% - 0.00% 35 -0.55%

Fair value loss on financial assets at fair value through profit or loss-

unrealised - 0.00% 24- 0.29% - 0.00%

Profit before taxation 1,981 24.20% 1,990 24.34% 838 13.21%

Taxation 246- 3.01% 373- 4.56% 127- 2.00%

Net profit for the year 1,735 21.19% 1,617 19.78% 711 11.21%

Horizontal analysis of income statement for the years 2016-2018:

Vertical analysis of income statement for the years 2016-2018:

Particulars 2016 (in RO,000) Percentage 2017 (in RO,000) Percentage 2018 (in RO,000) Percentage

Revenue 8,186 100.00% 8,175 100.00% 6,342 100.00%

Operating costs 5,865- 71.65% 5,821- 71.20% 5,273- 83.14%

Management and licence fees 225- 2.75% 227- 2.78% 153- 2.41%

Reservation and market assessment fees 120- 1.47% 120- 1.47% 92- 1.45%

Operating profit 1,976 24.14% 2,007 24.55% 824 12.99%

Finance income 5 0.06% 7 0.09% 7 0.11%

Finance costs - 0.00% - 0.00% 28- 0.44%

Other income - 0.00% - 0.00% 35 -0.55%

Fair value loss on financial assets at fair value through profit or loss-

unrealised - 0.00% 24- 0.29% - 0.00%

Profit before taxation 1,981 24.20% 1,990 24.34% 838 13.21%

Taxation 246- 3.01% 373- 4.56% 127- 2.00%

Net profit for the year 1,735 21.19% 1,617 19.78% 711 11.21%

Horizontal analysis of income statement for the years 2016-2018:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS FOR MANAGERS

Vertical analysis of balance sheet statement for the years 2016-2018:

Particulars 2016 (in RO,000) Percentage 2017 (in RO,000) Percentage 2018 (in RO,000) Percentage

Assets:

Non-current assets:

Property, plant and equipment 32,008 100.00% 31,834 100.00% 34,753 100.00%

Total non-current assets 32,008 95.15% 31,834 91.63% 34,753 94.85%

Current assets:

Inventories 36 2.20% 60 2.06% 50 2.65%

Other current assets - 0.00% 127 4.37% 176 9.32%

Trade receivables 717 43.91% 558 19.19% 532 28.18%

Other financial assets at amortised cost - 0.00% 17 0.58% 45 2.38%

Financial assets at fair value through profit or loss 25 1.53% 1 0.03% 1 0.05%

Cash and cash equivalents 855 52.36% 2,145 73.76% 1,084 57.42%

Total current assets 1,633 4.85% 2,908 8.37% 1,888 5.15%

Total assets 33,641 100.00% 34,742 100.00% 36,641 100.00%

Equity and liabiltiies:

Equity:

Share capital 3,428 11.99% 3,428 12.00% 3,428 12.12%

Share premium 58 0.20% 58 0.20% 58 0.21%

Legal reserve 1,143 4.00% 1,143 4.00% 1,143 4.04%

Revaluation reserve 22,796 79.76% 22,020 77.08% 22,020 77.86%

Retained earnings 1,157 4.05% 1,917 6.71% 1,631 5.77%

Total equity 28,582 84.96% 28,566 82.22% 28,280 77.18%

Liabilities:

Non-current liabilities:

Borrowings - 0.00% - 0.00% 1,912 29.40%

Provision for employees' end of service benefits 284 7.76% 315 6.94% 348 5.35%

Deferred taxation 3,376 92.24% 4,221 93.06% 4,243 65.25%

Total non-current liabilties 3,660 72.35% 4,536 73.45% 6,503 77.78%

Current liabilities:

Borrowings - - 338

Trade and other payables 1,147 81.99% 1,319 80.43% 1,399 75.30%

Taxation 252 18.01% 321 19.57% 121 6.51%

Total current liabilities 1,399 27.65% 1,640 26.55% 1,858 22.22%

Total liabilities 5,059 15.04% 6,176 17.78% 8,361 22.82%

Total equity and liabilities 33,641 100.00% 34,742 100.00% 36,641 100.00%

Vertical Analysis of Balance Sheet Statement:-

Horizontal analysis of balance sheet statement for the years 2016-2018:

Vertical analysis of balance sheet statement for the years 2016-2018:

Particulars 2016 (in RO,000) Percentage 2017 (in RO,000) Percentage 2018 (in RO,000) Percentage

Assets:

Non-current assets:

Property, plant and equipment 32,008 100.00% 31,834 100.00% 34,753 100.00%

Total non-current assets 32,008 95.15% 31,834 91.63% 34,753 94.85%

Current assets:

Inventories 36 2.20% 60 2.06% 50 2.65%

Other current assets - 0.00% 127 4.37% 176 9.32%

Trade receivables 717 43.91% 558 19.19% 532 28.18%

Other financial assets at amortised cost - 0.00% 17 0.58% 45 2.38%

Financial assets at fair value through profit or loss 25 1.53% 1 0.03% 1 0.05%

Cash and cash equivalents 855 52.36% 2,145 73.76% 1,084 57.42%

Total current assets 1,633 4.85% 2,908 8.37% 1,888 5.15%

Total assets 33,641 100.00% 34,742 100.00% 36,641 100.00%

Equity and liabiltiies:

Equity:

Share capital 3,428 11.99% 3,428 12.00% 3,428 12.12%

Share premium 58 0.20% 58 0.20% 58 0.21%

Legal reserve 1,143 4.00% 1,143 4.00% 1,143 4.04%

Revaluation reserve 22,796 79.76% 22,020 77.08% 22,020 77.86%

Retained earnings 1,157 4.05% 1,917 6.71% 1,631 5.77%

Total equity 28,582 84.96% 28,566 82.22% 28,280 77.18%

Liabilities:

Non-current liabilities:

Borrowings - 0.00% - 0.00% 1,912 29.40%

Provision for employees' end of service benefits 284 7.76% 315 6.94% 348 5.35%

Deferred taxation 3,376 92.24% 4,221 93.06% 4,243 65.25%

Total non-current liabilties 3,660 72.35% 4,536 73.45% 6,503 77.78%

Current liabilities:

Borrowings - - 338

Trade and other payables 1,147 81.99% 1,319 80.43% 1,399 75.30%

Taxation 252 18.01% 321 19.57% 121 6.51%

Total current liabilities 1,399 27.65% 1,640 26.55% 1,858 22.22%

Total liabilities 5,059 15.04% 6,176 17.78% 8,361 22.82%

Total equity and liabilities 33,641 100.00% 34,742 100.00% 36,641 100.00%

Vertical Analysis of Balance Sheet Statement:-

Horizontal analysis of balance sheet statement for the years 2016-2018:

5FINANCIAL ANALYSIS FOR MANAGERS

Particulars 2016 (in RO,000) 2017 (in RO,000) Percent Change

Assets:

Non-current assets:

Property, plant and equipment 32,008 31,834 -0.54%

Total non-current assets 32,008 31,834 -0.54%

Current assets:

Inventories 36 60 66.67%

Other current assets - 127 0.00%

Trade receivables 717 558 -22.18%

Other financial assets at amortised cost - 17 0.00%

Financial assets at fair value through profit or loss 25 1 -96.00%

Cash and cash equivalents 855 2,145 150.88%

Total current assets 1,633 2,908 78.08%

Total assets 33,641 34,742 3.27%

Equity and liabiltiies:

Equity:

Share capital 3,428 3,428 0.00%

Share premium 58 58 0.00%

Legal reserve 1,143 1,143 0.00%

Revaluation reserve 22,796 22,020 -3.40%

Retained earnings 1,157 1,917 65.69%

Total equity 28,582 28,566 -0.06%

Liabilities:

Non-current liabilities:

Borrowings - - 0.00%

Provision for employees' end of service benefits 284 315 10.92%

Deferred taxation 3,376 4,221 25.03%

Total non-current liabilties 3,660 4,536 23.93%

Current liabilities:

Borrowings - -

Trade and other payables 1,147 1,319 15.00%

Taxation 252 321 27.38%

Total current liabilities 1,399 1,640 17.23%

Total liabilities 5,059 6,176 22.08%

Total equity and liabilities 33,641 34,742 3.27%

Particulars 2016 (in RO,000) 2017 (in RO,000) Percent Change

Assets:

Non-current assets:

Property, plant and equipment 32,008 31,834 -0.54%

Total non-current assets 32,008 31,834 -0.54%

Current assets:

Inventories 36 60 66.67%

Other current assets - 127 0.00%

Trade receivables 717 558 -22.18%

Other financial assets at amortised cost - 17 0.00%

Financial assets at fair value through profit or loss 25 1 -96.00%

Cash and cash equivalents 855 2,145 150.88%

Total current assets 1,633 2,908 78.08%

Total assets 33,641 34,742 3.27%

Equity and liabiltiies:

Equity:

Share capital 3,428 3,428 0.00%

Share premium 58 58 0.00%

Legal reserve 1,143 1,143 0.00%

Revaluation reserve 22,796 22,020 -3.40%

Retained earnings 1,157 1,917 65.69%

Total equity 28,582 28,566 -0.06%

Liabilities:

Non-current liabilities:

Borrowings - - 0.00%

Provision for employees' end of service benefits 284 315 10.92%

Deferred taxation 3,376 4,221 25.03%

Total non-current liabilties 3,660 4,536 23.93%

Current liabilities:

Borrowings - -

Trade and other payables 1,147 1,319 15.00%

Taxation 252 321 27.38%

Total current liabilities 1,399 1,640 17.23%

Total liabilities 5,059 6,176 22.08%

Total equity and liabilities 33,641 34,742 3.27%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS FOR MANAGERS

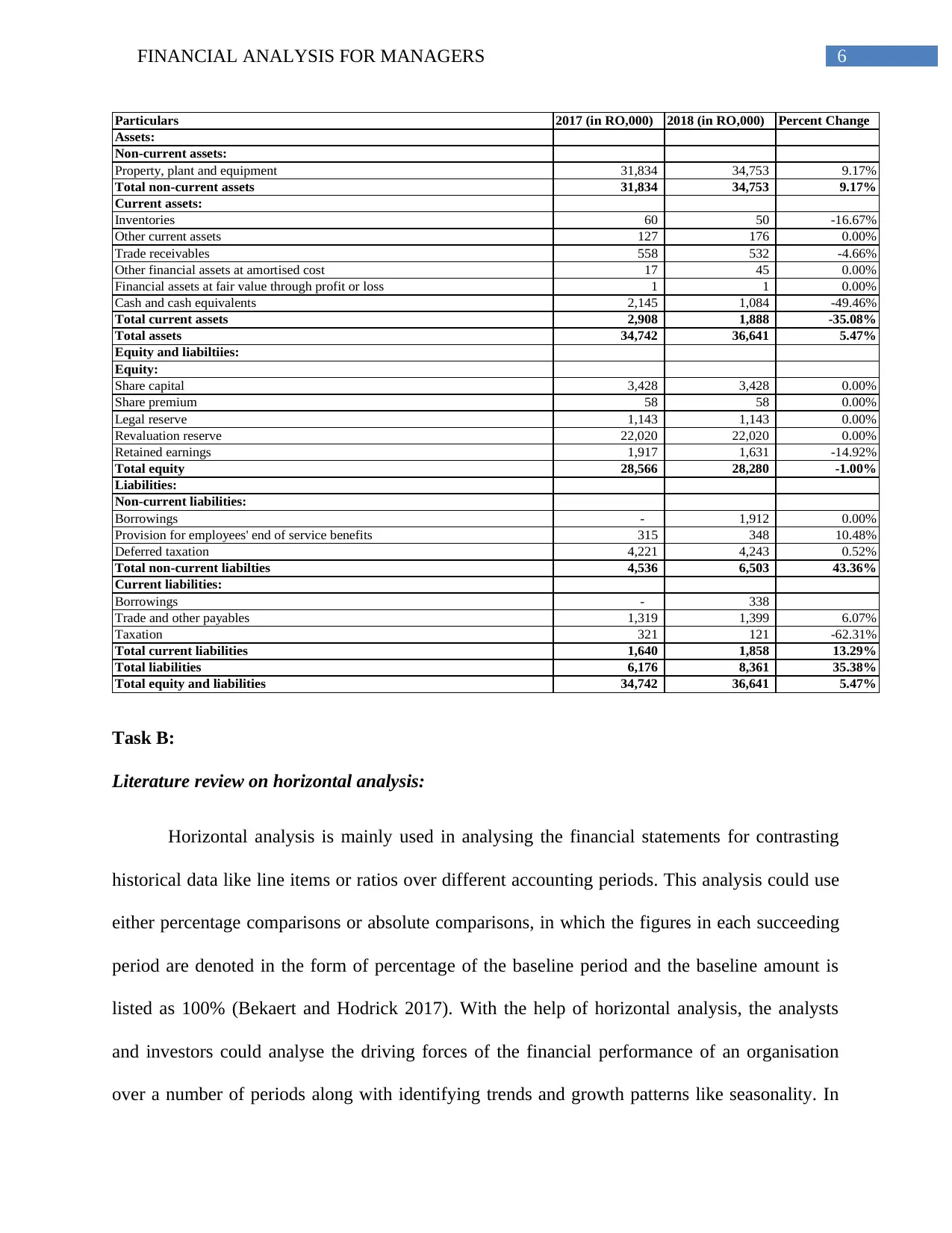

Particulars 2017 (in RO,000) 2018 (in RO,000) Percent Change

Assets:

Non-current assets:

Property, plant and equipment 31,834 34,753 9.17%

Total non-current assets 31,834 34,753 9.17%

Current assets:

Inventories 60 50 -16.67%

Other current assets 127 176 0.00%

Trade receivables 558 532 -4.66%

Other financial assets at amortised cost 17 45 0.00%

Financial assets at fair value through profit or loss 1 1 0.00%

Cash and cash equivalents 2,145 1,084 -49.46%

Total current assets 2,908 1,888 -35.08%

Total assets 34,742 36,641 5.47%

Equity and liabiltiies:

Equity:

Share capital 3,428 3,428 0.00%

Share premium 58 58 0.00%

Legal reserve 1,143 1,143 0.00%

Revaluation reserve 22,020 22,020 0.00%

Retained earnings 1,917 1,631 -14.92%

Total equity 28,566 28,280 -1.00%

Liabilities:

Non-current liabilities:

Borrowings - 1,912 0.00%

Provision for employees' end of service benefits 315 348 10.48%

Deferred taxation 4,221 4,243 0.52%

Total non-current liabilties 4,536 6,503 43.36%

Current liabilities:

Borrowings - 338

Trade and other payables 1,319 1,399 6.07%

Taxation 321 121 -62.31%

Total current liabilities 1,640 1,858 13.29%

Total liabilities 6,176 8,361 35.38%

Total equity and liabilities 34,742 36,641 5.47%

Task B:

Literature review on horizontal analysis:

Horizontal analysis is mainly used in analysing the financial statements for contrasting

historical data like line items or ratios over different accounting periods. This analysis could use

either percentage comparisons or absolute comparisons, in which the figures in each succeeding

period are denoted in the form of percentage of the baseline period and the baseline amount is

listed as 100% (Bekaert and Hodrick 2017). With the help of horizontal analysis, the analysts

and investors could analyse the driving forces of the financial performance of an organisation

over a number of periods along with identifying trends and growth patterns like seasonality. In

Particulars 2017 (in RO,000) 2018 (in RO,000) Percent Change

Assets:

Non-current assets:

Property, plant and equipment 31,834 34,753 9.17%

Total non-current assets 31,834 34,753 9.17%

Current assets:

Inventories 60 50 -16.67%

Other current assets 127 176 0.00%

Trade receivables 558 532 -4.66%

Other financial assets at amortised cost 17 45 0.00%

Financial assets at fair value through profit or loss 1 1 0.00%

Cash and cash equivalents 2,145 1,084 -49.46%

Total current assets 2,908 1,888 -35.08%

Total assets 34,742 36,641 5.47%

Equity and liabiltiies:

Equity:

Share capital 3,428 3,428 0.00%

Share premium 58 58 0.00%

Legal reserve 1,143 1,143 0.00%

Revaluation reserve 22,020 22,020 0.00%

Retained earnings 1,917 1,631 -14.92%

Total equity 28,566 28,280 -1.00%

Liabilities:

Non-current liabilities:

Borrowings - 1,912 0.00%

Provision for employees' end of service benefits 315 348 10.48%

Deferred taxation 4,221 4,243 0.52%

Total non-current liabilties 4,536 6,503 43.36%

Current liabilities:

Borrowings - 338

Trade and other payables 1,319 1,399 6.07%

Taxation 321 121 -62.31%

Total current liabilities 1,640 1,858 13.29%

Total liabilities 6,176 8,361 35.38%

Total equity and liabilities 34,742 36,641 5.47%

Task B:

Literature review on horizontal analysis:

Horizontal analysis is mainly used in analysing the financial statements for contrasting

historical data like line items or ratios over different accounting periods. This analysis could use

either percentage comparisons or absolute comparisons, in which the figures in each succeeding

period are denoted in the form of percentage of the baseline period and the baseline amount is

listed as 100% (Bekaert and Hodrick 2017). With the help of horizontal analysis, the analysts

and investors could analyse the driving forces of the financial performance of an organisation

over a number of periods along with identifying trends and growth patterns like seasonality. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS FOR MANAGERS

addition, the analysts could be able to analyse relative changes in various line items over the

years and accordingly, it is possible to make projections (Churet and Eccles 2014).

Literature review on vertical analysis:

Vertical analysis is a technique of analysing the financial statements where each line item

is listed as a number of a base figure within the statement. Therefore, the line items on the

income statement could be represented as percentage of sales revenue, while the line items on the

balance sheet statement could be expressed as percentage of total assets or total liabilities

(Ehrhardt and Brigham 2016). This analysis assists in easy understanding and comparing the

financial statements of one organisation with another and across industrial sectors. The reason is

that it is possible to see the relative proportions related to account balances. Thus, vertical

analysis assists in gaining an insight of whether there has been improvement or deterioration in

performance metrics (Fernandes 2014).

Analysis of profitability position and financial position of Gulf Hotels (Oman) Company

Limited SAOG:

Profitability position:

From the horizontal analysis of the income statement, it could be seen that Gulf Hotels

has experienced a slight fall in revenue by 0.13% in 2017 and the decline is significant by

22.42% in 2018. Although the organisation has managed to minimise its operating expenses over

the year, it has not been enough to offset the fall in revenue. As a result, the operating profit of

Gulf Hotels has fallen by 58.94% in 2018. Finally, even though there has been fall in tax expense

by 65.95% in 2018, net profit of the hotel is observed to decline by 56.03% in 2018.

addition, the analysts could be able to analyse relative changes in various line items over the

years and accordingly, it is possible to make projections (Churet and Eccles 2014).

Literature review on vertical analysis:

Vertical analysis is a technique of analysing the financial statements where each line item

is listed as a number of a base figure within the statement. Therefore, the line items on the

income statement could be represented as percentage of sales revenue, while the line items on the

balance sheet statement could be expressed as percentage of total assets or total liabilities

(Ehrhardt and Brigham 2016). This analysis assists in easy understanding and comparing the

financial statements of one organisation with another and across industrial sectors. The reason is

that it is possible to see the relative proportions related to account balances. Thus, vertical

analysis assists in gaining an insight of whether there has been improvement or deterioration in

performance metrics (Fernandes 2014).

Analysis of profitability position and financial position of Gulf Hotels (Oman) Company

Limited SAOG:

Profitability position:

From the horizontal analysis of the income statement, it could be seen that Gulf Hotels

has experienced a slight fall in revenue by 0.13% in 2017 and the decline is significant by

22.42% in 2018. Although the organisation has managed to minimise its operating expenses over

the year, it has not been enough to offset the fall in revenue. As a result, the operating profit of

Gulf Hotels has fallen by 58.94% in 2018. Finally, even though there has been fall in tax expense

by 65.95% in 2018, net profit of the hotel is observed to decline by 56.03% in 2018.

8FINANCIAL ANALYSIS FOR MANAGERS

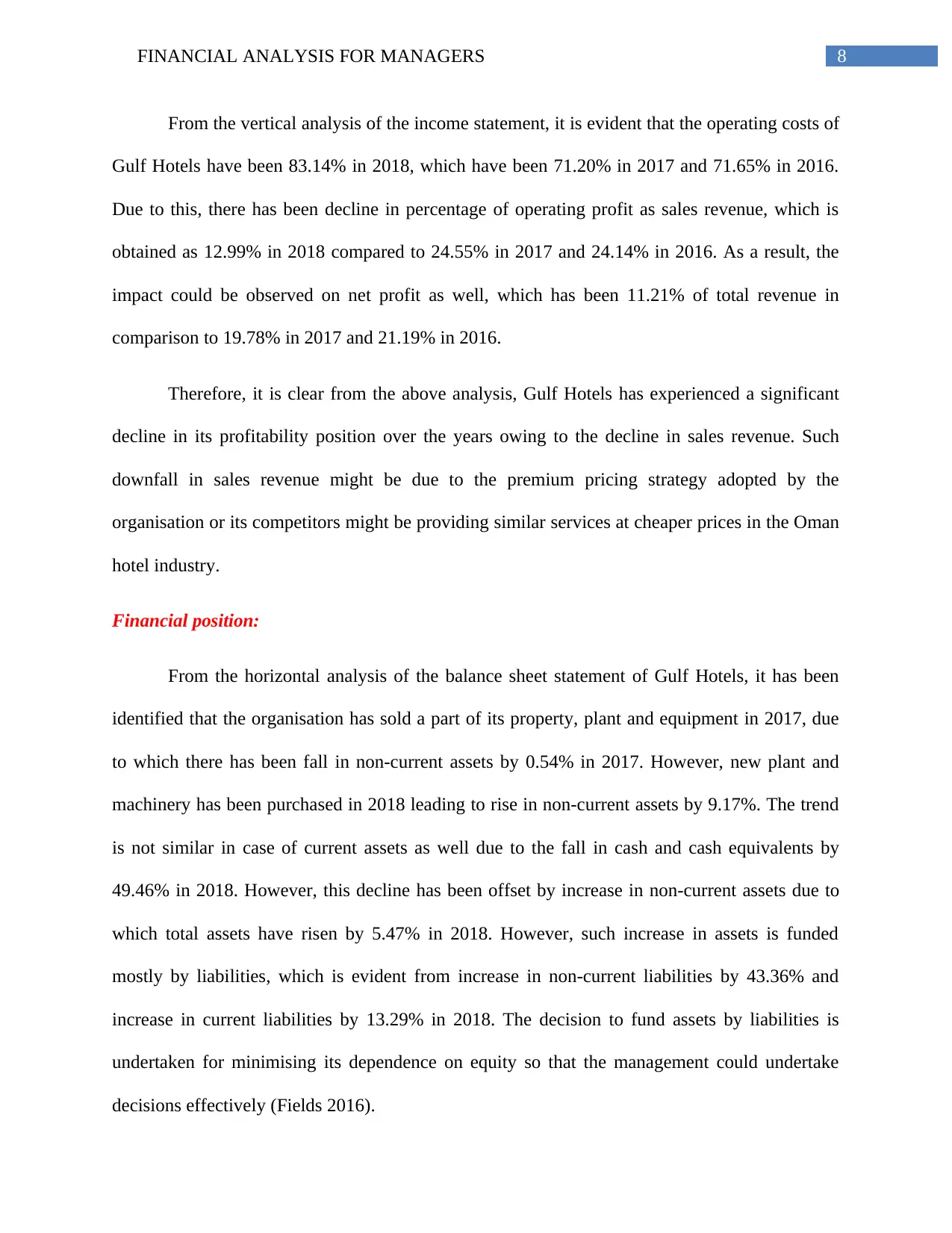

From the vertical analysis of the income statement, it is evident that the operating costs of

Gulf Hotels have been 83.14% in 2018, which have been 71.20% in 2017 and 71.65% in 2016.

Due to this, there has been decline in percentage of operating profit as sales revenue, which is

obtained as 12.99% in 2018 compared to 24.55% in 2017 and 24.14% in 2016. As a result, the

impact could be observed on net profit as well, which has been 11.21% of total revenue in

comparison to 19.78% in 2017 and 21.19% in 2016.

Therefore, it is clear from the above analysis, Gulf Hotels has experienced a significant

decline in its profitability position over the years owing to the decline in sales revenue. Such

downfall in sales revenue might be due to the premium pricing strategy adopted by the

organisation or its competitors might be providing similar services at cheaper prices in the Oman

hotel industry.

Financial position:

From the horizontal analysis of the balance sheet statement of Gulf Hotels, it has been

identified that the organisation has sold a part of its property, plant and equipment in 2017, due

to which there has been fall in non-current assets by 0.54% in 2017. However, new plant and

machinery has been purchased in 2018 leading to rise in non-current assets by 9.17%. The trend

is not similar in case of current assets as well due to the fall in cash and cash equivalents by

49.46% in 2018. However, this decline has been offset by increase in non-current assets due to

which total assets have risen by 5.47% in 2018. However, such increase in assets is funded

mostly by liabilities, which is evident from increase in non-current liabilities by 43.36% and

increase in current liabilities by 13.29% in 2018. The decision to fund assets by liabilities is

undertaken for minimising its dependence on equity so that the management could undertake

decisions effectively (Fields 2016).

From the vertical analysis of the income statement, it is evident that the operating costs of

Gulf Hotels have been 83.14% in 2018, which have been 71.20% in 2017 and 71.65% in 2016.

Due to this, there has been decline in percentage of operating profit as sales revenue, which is

obtained as 12.99% in 2018 compared to 24.55% in 2017 and 24.14% in 2016. As a result, the

impact could be observed on net profit as well, which has been 11.21% of total revenue in

comparison to 19.78% in 2017 and 21.19% in 2016.

Therefore, it is clear from the above analysis, Gulf Hotels has experienced a significant

decline in its profitability position over the years owing to the decline in sales revenue. Such

downfall in sales revenue might be due to the premium pricing strategy adopted by the

organisation or its competitors might be providing similar services at cheaper prices in the Oman

hotel industry.

Financial position:

From the horizontal analysis of the balance sheet statement of Gulf Hotels, it has been

identified that the organisation has sold a part of its property, plant and equipment in 2017, due

to which there has been fall in non-current assets by 0.54% in 2017. However, new plant and

machinery has been purchased in 2018 leading to rise in non-current assets by 9.17%. The trend

is not similar in case of current assets as well due to the fall in cash and cash equivalents by

49.46% in 2018. However, this decline has been offset by increase in non-current assets due to

which total assets have risen by 5.47% in 2018. However, such increase in assets is funded

mostly by liabilities, which is evident from increase in non-current liabilities by 43.36% and

increase in current liabilities by 13.29% in 2018. The decision to fund assets by liabilities is

undertaken for minimising its dependence on equity so that the management could undertake

decisions effectively (Fields 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS FOR MANAGERS

According to the vertical analysis of the balance sheet statement of Gulf Hotels, it could

be witnessed that Gulf Hotels has experienced a fall in cash and cash equivalents as percentage

of current assets from 73.76% in 2017 to 57.42% in 2018. On the other hand, there has been

significant increase in long-term borrowings, deferred taxation and trade payables and thus, it

could be stated that the organisation is suffering from poor liquidity position in the Oman

market.

Recommendations:

From the above analysis, it has been identified that Gulf Hotels is suffering from poor

profitability and liquidity positions in the Oman hotel industry. Hence, for improving these

positions, the hotel is required to undertake certain measures, which are discussed briefly as

follows:

The managers of Gulf Hotels need to adopt cross promotional sales strategy for

identifying and analysing big events to be taking place in the local region across the

period. After this, the hotel operators have to devise with a promotional strategy having

the potential; of coinciding with the event (Floyd and List 2016).

Gulf Hotels could implement guest rewards sales strategy as well, in which the operators

of the hotel would formulate a system for rewarding those guests staying frequently with

the hotel or buying upgrades or referring their acquaintances or family members. This, in

turn, would lead to repeat bookings for the Gulf Hotels, which would assist in increasing

its sales revenue (Gippel, Smith and Zhu 2015).

In addition, Gulf Hotels is required to minimise its operating costs and other fees so that

it could ensure higher profitability.

According to the vertical analysis of the balance sheet statement of Gulf Hotels, it could

be witnessed that Gulf Hotels has experienced a fall in cash and cash equivalents as percentage

of current assets from 73.76% in 2017 to 57.42% in 2018. On the other hand, there has been

significant increase in long-term borrowings, deferred taxation and trade payables and thus, it

could be stated that the organisation is suffering from poor liquidity position in the Oman

market.

Recommendations:

From the above analysis, it has been identified that Gulf Hotels is suffering from poor

profitability and liquidity positions in the Oman hotel industry. Hence, for improving these

positions, the hotel is required to undertake certain measures, which are discussed briefly as

follows:

The managers of Gulf Hotels need to adopt cross promotional sales strategy for

identifying and analysing big events to be taking place in the local region across the

period. After this, the hotel operators have to devise with a promotional strategy having

the potential; of coinciding with the event (Floyd and List 2016).

Gulf Hotels could implement guest rewards sales strategy as well, in which the operators

of the hotel would formulate a system for rewarding those guests staying frequently with

the hotel or buying upgrades or referring their acquaintances or family members. This, in

turn, would lead to repeat bookings for the Gulf Hotels, which would assist in increasing

its sales revenue (Gippel, Smith and Zhu 2015).

In addition, Gulf Hotels is required to minimise its operating costs and other fees so that

it could ensure higher profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS FOR MANAGERS

Gulf Hotels needs to emphasise more on aging accounts along with working hard to settle

due payments from the customers. This would assist the hotel in increasing its availability

of working capital (Gitman, Juchau and Flanagan 2015).

Finally, Gulf Hotels is needed to control its overhead costs on professional costs, rent,

labour, marketing and others. By cutting these expenses, the organisation would be able

to retain more cash in the business (Baños-Caballero, García-Teruel and Martínez-Solano

2014).

Question 2:

Task A:

Gulf Hotels needs to emphasise more on aging accounts along with working hard to settle

due payments from the customers. This would assist the hotel in increasing its availability

of working capital (Gitman, Juchau and Flanagan 2015).

Finally, Gulf Hotels is needed to control its overhead costs on professional costs, rent,

labour, marketing and others. By cutting these expenses, the organisation would be able

to retain more cash in the business (Baños-Caballero, García-Teruel and Martínez-Solano

2014).

Question 2:

Task A:

11FINANCIAL ANALYSIS FOR MANAGERS

In case of City Cinemas, if it starts a new cinema at Sohar, the internal rate of return is

computed as 20.93%. On the other hand, if the organisation acquires the existing cinema, the

internal rate of return for the project would be 23.06%. An investor should select Take-over

existing cinema at Nizwa because it offers a relatively higher rate of 23% as compared to new

cinema at Sohar that provides a return of 21% in the same period. Hence, on the basis of internal

rate of return, City Cinemas should acquire the existing cinema; however, the non-financial

factors are not taken into consideration for undertaking this decision.

Task B:

Internal rate of return (IRR) is a method, which is utilised in capital budgeting, for

projecting the profitability of potential investments. In other words, it is the rate of return that

makes the net present value equal to zero (Hillier et al. 2014). From the general perspective, the

more the internal rate of return of a project, it is always desirable to undertake the project. This

method is uniform for investments of different types and therefore, it could be utilised for

ranking numerous prospective projects on relative basis. By assuming that the investment costs

are identical among different projects, the project having the highest IRR would be chosen

(Karadag 2015).

There are certain non-financial factors that have to be considered before undertaking the

final investment decision. In case of City Cinemas, some of those factors include the population

growth, consumer trends and competition level in the industry. If the organisation starts a new

cinema at Sohar, the population is expected to increase by 12%. However, if it takes over an

existing cinema at Nizwa, the population growth is expected to increase by 5%, which is lower

than the other option. When the consumer trends are taken into consideration, the same is

expected to grow by 10%, while in Nizwa, it would remain stagnated. Thus, there would not be

In case of City Cinemas, if it starts a new cinema at Sohar, the internal rate of return is

computed as 20.93%. On the other hand, if the organisation acquires the existing cinema, the

internal rate of return for the project would be 23.06%. An investor should select Take-over

existing cinema at Nizwa because it offers a relatively higher rate of 23% as compared to new

cinema at Sohar that provides a return of 21% in the same period. Hence, on the basis of internal

rate of return, City Cinemas should acquire the existing cinema; however, the non-financial

factors are not taken into consideration for undertaking this decision.

Task B:

Internal rate of return (IRR) is a method, which is utilised in capital budgeting, for

projecting the profitability of potential investments. In other words, it is the rate of return that

makes the net present value equal to zero (Hillier et al. 2014). From the general perspective, the

more the internal rate of return of a project, it is always desirable to undertake the project. This

method is uniform for investments of different types and therefore, it could be utilised for

ranking numerous prospective projects on relative basis. By assuming that the investment costs

are identical among different projects, the project having the highest IRR would be chosen

(Karadag 2015).

There are certain non-financial factors that have to be considered before undertaking the

final investment decision. In case of City Cinemas, some of those factors include the population

growth, consumer trends and competition level in the industry. If the organisation starts a new

cinema at Sohar, the population is expected to increase by 12%. However, if it takes over an

existing cinema at Nizwa, the population growth is expected to increase by 5%, which is lower

than the other option. When the consumer trends are taken into consideration, the same is

expected to grow by 10%, while in Nizwa, it would remain stagnated. Thus, there would not be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.