Financial Analysis Report: AACL's Financial Performance and Position

VerifiedAdded on 2023/01/19

|15

|2803

|81

Report

AI Summary

This report provides a comprehensive financial analysis of Australian Agricultural Projects Limited (AACL). It begins with an introduction to the company, followed by an analysis of its risk and profit potential, including an examination of industry dynamics using Porter's Five Forces and an assessment of the company's competitive strategies. The report then delves into accounting analysis, covering the nature of financial statements, performance analysis, and notes to the financial statements. An evaluation of accounting strategies is presented, followed by a section on recasting the financial statements. The analysis reveals a decline in revenue and profitability, although the company has improved its ability to meet short-term obligations. The report concludes with a summary of key findings and insights into AACL's financial performance and position.

Running head: FINANCIAL ANALYSIS

Financial analysis

Name of the student

Name of the university

Student ID

Author note

Financial analysis

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS

Table of Contents

1. Introduction..............................................................................................................................2

2.1 Risk and profit potential of the company..................................................................................3

2.1 Industry analysis....................................................................................................................3

2.2 Competitive strategy analysis................................................................................................5

3. Accounting analysis.................................................................................................................6

3.1 Nature of financial statements...............................................................................................6

3.2 Performance analysis.............................................................................................................8

3.3 Notes to financial statement...................................................................................................8

4. Accounting strategy evaluation................................................................................................9

5. Recasting the financial statements.........................................................................................10

6. Conclusion..............................................................................................................................11

Reference.......................................................................................................................................13

Table of Contents

1. Introduction..............................................................................................................................2

2.1 Risk and profit potential of the company..................................................................................3

2.1 Industry analysis....................................................................................................................3

2.2 Competitive strategy analysis................................................................................................5

3. Accounting analysis.................................................................................................................6

3.1 Nature of financial statements...............................................................................................6

3.2 Performance analysis.............................................................................................................8

3.3 Notes to financial statement...................................................................................................8

4. Accounting strategy evaluation................................................................................................9

5. Recasting the financial statements.........................................................................................10

6. Conclusion..............................................................................................................................11

Reference.......................................................................................................................................13

2FINANCIAL ANALYSIS

1. Introduction

Australian Agricultural Projects Limited (AACL) is the ASX listed entity that is engaged

in operation of olive grove and is located in Boort, Victoria. The entity further engaged in

operation of the managed investment schemes and serves Peppercorn Estate Limited, Victorian

Olive Oil Project and Victorian Olive Oil Project II. The company started its business during the

year 2004 with establishment of various olive oil brands. The entity has the leading technical

teams and developed its capacity in establishing new olive grove projects and manages other

groves to expand in other markets (Voopl.com.au, 2019).

1. Introduction

Australian Agricultural Projects Limited (AACL) is the ASX listed entity that is engaged

in operation of olive grove and is located in Boort, Victoria. The entity further engaged in

operation of the managed investment schemes and serves Peppercorn Estate Limited, Victorian

Olive Oil Project and Victorian Olive Oil Project II. The company started its business during the

year 2004 with establishment of various olive oil brands. The entity has the leading technical

teams and developed its capacity in establishing new olive grove projects and manages other

groves to expand in other markets (Voopl.com.au, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS

2.1 Risk and profit potential of the company

2.1 Industry analysis

Porter’s 5 forces is the holistic strategic framework that takes the strategic decision

beyond just analysing present competition. It will focus on how the Australian Agricultural

Company Limited may build the sustainable competitive advantages in beverage, tobacco and

food industry.

Threat from the new entrants

New entrants in the beverage, tobacco and food industry brings new ways to do the

things, innovation that put on pressure on the company through reduced costs, strategy of lower

2.1 Risk and profit potential of the company

2.1 Industry analysis

Porter’s 5 forces is the holistic strategic framework that takes the strategic decision

beyond just analysing present competition. It will focus on how the Australian Agricultural

Company Limited may build the sustainable competitive advantages in beverage, tobacco and

food industry.

Threat from the new entrants

New entrants in the beverage, tobacco and food industry brings new ways to do the

things, innovation that put on pressure on the company through reduced costs, strategy of lower

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS

pricing and offering value propositions to customers. Hence, the entity shall manage all the

challenges and construct the effective barriers for safeguarding the competitive edge. AACL

manages the risk through (i) innovating the new services and products. New products not only

attract the new customers but also provide a reason to the existing customers to buy product from

AACL (ii) through building the economies of scale that will enable it to lower the per unit fixed

cost (Engel, 2016).

Bargaining power of the suppliers

Most of the entities from beverage, tobacco and food industry purchase raw materials

from different suppliers. Dominant position of the suppliers may decreases margin of AACL

from market. Further, the powerful suppliers may use their negotiating power for extracting the

higher prices from the buyers. Hence, the higher bargaining power of the suppliers will lower the

overall profitability. Supplier’s bargaining power are tackled by AACL through (i) building the

proficient supply chain engaging multiple suppliers (ii) through experimenting the products

designs using various materials so that in case where the prices increases for one raw material the

entity can reallocate to another (iii) developing the dedicated suppliers whose business will be

solely dependent on the firm (Kupka & Thomas, 2014).

Bargaining power of the buyers

Generally, the buyers are demanding and want to buy best available offerings through

paying possible minimum price. This will in turn put pressure on AACL’s profitability over the

long term. Small and more powerful customer base of the entity will enable it to achieve higher

bargaining power and will increase the ability to seek offers and discounts. AACL tackles the

buyer’s bargaining power through (i) building large customer base that will help to reduce

pricing and offering value propositions to customers. Hence, the entity shall manage all the

challenges and construct the effective barriers for safeguarding the competitive edge. AACL

manages the risk through (i) innovating the new services and products. New products not only

attract the new customers but also provide a reason to the existing customers to buy product from

AACL (ii) through building the economies of scale that will enable it to lower the per unit fixed

cost (Engel, 2016).

Bargaining power of the suppliers

Most of the entities from beverage, tobacco and food industry purchase raw materials

from different suppliers. Dominant position of the suppliers may decreases margin of AACL

from market. Further, the powerful suppliers may use their negotiating power for extracting the

higher prices from the buyers. Hence, the higher bargaining power of the suppliers will lower the

overall profitability. Supplier’s bargaining power are tackled by AACL through (i) building the

proficient supply chain engaging multiple suppliers (ii) through experimenting the products

designs using various materials so that in case where the prices increases for one raw material the

entity can reallocate to another (iii) developing the dedicated suppliers whose business will be

solely dependent on the firm (Kupka & Thomas, 2014).

Bargaining power of the buyers

Generally, the buyers are demanding and want to buy best available offerings through

paying possible minimum price. This will in turn put pressure on AACL’s profitability over the

long term. Small and more powerful customer base of the entity will enable it to achieve higher

bargaining power and will increase the ability to seek offers and discounts. AACL tackles the

buyer’s bargaining power through (i) building large customer base that will help to reduce

5FINANCIAL ANALYSIS

bargaining power of buyers and will deliver the opportunity to streamline the production and

sales process (ii) through innovating new products as it is unlikely that the customers will seek

offerings and discounts on new products (Pérez-Pérez et al., 2019).

Threats from substitute service or products

When any new service or product fulfils the requirement of a customer in different way,

profitability of the industry suffers. For instance, the services provided by Google Drive and

Dropbox replaced drives for storage hardware. Further, the threat from substitute product is high

if it provides value proposition that is exceptionally different from the industry’s present

offerings. This threat is managed by AACL through (i) being the service oriented and not just

the product oriented (ii) through understanding core requirement of customer rather than the

purchasing habits of the customers (iii) through increasing switching cost for customers

(Voopl.com.au, 2019).

Rivalry from existing competitors

If rivalry among existing industry players is intense it will lower the prices and will

reduce the overall profitability of industry. AACL operates in the competitive beverage, tobacco

and food industry that has impact on the profitability of the entity. This is managed by the entity

through (i) building the sustainable differentiation (ii) through building the scale with which it

can compete in better way (iii) collaborating with the competitors for increasing market size

rather than only competing for the small market (Voopl.com.au, 2019).

2.2 Competitive strategy analysis

AACL is doing better and different things from the competitors and it is targeting the

countries with better economies. In market, it is positioned as innovators for agribusiness.

bargaining power of buyers and will deliver the opportunity to streamline the production and

sales process (ii) through innovating new products as it is unlikely that the customers will seek

offerings and discounts on new products (Pérez-Pérez et al., 2019).

Threats from substitute service or products

When any new service or product fulfils the requirement of a customer in different way,

profitability of the industry suffers. For instance, the services provided by Google Drive and

Dropbox replaced drives for storage hardware. Further, the threat from substitute product is high

if it provides value proposition that is exceptionally different from the industry’s present

offerings. This threat is managed by AACL through (i) being the service oriented and not just

the product oriented (ii) through understanding core requirement of customer rather than the

purchasing habits of the customers (iii) through increasing switching cost for customers

(Voopl.com.au, 2019).

Rivalry from existing competitors

If rivalry among existing industry players is intense it will lower the prices and will

reduce the overall profitability of industry. AACL operates in the competitive beverage, tobacco

and food industry that has impact on the profitability of the entity. This is managed by the entity

through (i) building the sustainable differentiation (ii) through building the scale with which it

can compete in better way (iii) collaborating with the competitors for increasing market size

rather than only competing for the small market (Voopl.com.au, 2019).

2.2 Competitive strategy analysis

AACL is doing better and different things from the competitors and it is targeting the

countries with better economies. In market, it is positioned as innovators for agribusiness.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS

Implementation of the cost leadership and product differentiation strategies will be beneficial for

the entity under the stable and predictable environment. In case there is a change in economic

scenario, it will lead to diseconomies for the entity as well as for overall agricultural industry in

implementing cost leadership strategy (Member.afraccess.com, 2019). Major strategy of the

entity is focusing on marketing and branding of luxury branded beef products. Through the

people who love eating beef are not concerned regarding the cost of the same. However, AACL

is still able to achieve the competitive advantage through delivering different products and low

cost service through serving the individual market segment. Further, the entity launched value

added and luxury products for attracting target customers. The company has been identified as

leading provider for cattle, beef and the agricultural products (Member.afraccess.com, 2019).

3. Accounting analysis

3.1 Nature of financial statements

AACL reports the consolidated income statement, consolidated financial position

statement, consolidated statement for changes in the equity and consolidated statement of the

cash flows.

Consolidated income statement – it combines the expenses, revenues and income from the

parent entity and the subsidiaries. It represents the aggregated picture of entire organization

rather than presenting only the individual parts. Consolidated income statement represents

revenues, COGS, selling and the administrative expenses, other expenses, interest expenses,

taxes paid and net profit. AACL’s income statement is divided into the time periods that follows

the operation of the entity logically. The report is prepared for 12 months period closed on 31st

Implementation of the cost leadership and product differentiation strategies will be beneficial for

the entity under the stable and predictable environment. In case there is a change in economic

scenario, it will lead to diseconomies for the entity as well as for overall agricultural industry in

implementing cost leadership strategy (Member.afraccess.com, 2019). Major strategy of the

entity is focusing on marketing and branding of luxury branded beef products. Through the

people who love eating beef are not concerned regarding the cost of the same. However, AACL

is still able to achieve the competitive advantage through delivering different products and low

cost service through serving the individual market segment. Further, the entity launched value

added and luxury products for attracting target customers. The company has been identified as

leading provider for cattle, beef and the agricultural products (Member.afraccess.com, 2019).

3. Accounting analysis

3.1 Nature of financial statements

AACL reports the consolidated income statement, consolidated financial position

statement, consolidated statement for changes in the equity and consolidated statement of the

cash flows.

Consolidated income statement – it combines the expenses, revenues and income from the

parent entity and the subsidiaries. It represents the aggregated picture of entire organization

rather than presenting only the individual parts. Consolidated income statement represents

revenues, COGS, selling and the administrative expenses, other expenses, interest expenses,

taxes paid and net profit. AACL’s income statement is divided into the time periods that follows

the operation of the entity logically. The report is prepared for 12 months period closed on 31st

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS

March 2018. 2 sections of the income statement include revenues and expenses (Wahlen,

Baginski & Bradshaw, 2014).

Consolidated financial position statement – it represents the total asset of the entity and how the

assets are financed through debt or through equity. Balance sheet is generally based on the

fundamental equation of “Assets = Liabilities + equity”. Consolidated statement of financial

position of AACL is segregated into assets, liabilities and equity. Total asset is further segregated

into current assets and non-current assets and total liabilities are separated into current liabilities

and non-current liabilities. Current assets includes the assets those can be quickly converted into

cash and current liabilities include the obligation those are payable within the 1 year period of

time (Robinson et al., 2015)

Consolidated statement for changes in the equity – Consolidated statement for changes in the

equity represents the changes in the owner’s equity over the accounting period through

presenting movements in the reserves including the shareholder’s equity. AACL’s statement for

changes in equity represents details of contributed equity, reserves and retained earnings or loss

(Robinson et al., 2015)

Statement of cash flows – Cash flow statement delivers information regarding the changes in the

cash and cash equivalents of the business through segregating the cash into operating, financing

and investing activities. Cash flow statement of AACL is prepared for 12 months period closed

on 31st March 2018. 3 sections of the statement include cash flow from the operating activities,

cash flow from the investing activities and cash flow from the financing activities (Wahlen,

Baginski & Bradshaw, 2014).

March 2018. 2 sections of the income statement include revenues and expenses (Wahlen,

Baginski & Bradshaw, 2014).

Consolidated financial position statement – it represents the total asset of the entity and how the

assets are financed through debt or through equity. Balance sheet is generally based on the

fundamental equation of “Assets = Liabilities + equity”. Consolidated statement of financial

position of AACL is segregated into assets, liabilities and equity. Total asset is further segregated

into current assets and non-current assets and total liabilities are separated into current liabilities

and non-current liabilities. Current assets includes the assets those can be quickly converted into

cash and current liabilities include the obligation those are payable within the 1 year period of

time (Robinson et al., 2015)

Consolidated statement for changes in the equity – Consolidated statement for changes in the

equity represents the changes in the owner’s equity over the accounting period through

presenting movements in the reserves including the shareholder’s equity. AACL’s statement for

changes in equity represents details of contributed equity, reserves and retained earnings or loss

(Robinson et al., 2015)

Statement of cash flows – Cash flow statement delivers information regarding the changes in the

cash and cash equivalents of the business through segregating the cash into operating, financing

and investing activities. Cash flow statement of AACL is prepared for 12 months period closed

on 31st March 2018. 3 sections of the statement include cash flow from the operating activities,

cash flow from the investing activities and cash flow from the financing activities (Wahlen,

Baginski & Bradshaw, 2014).

8FINANCIAL ANALYSIS

3.2 Performance analysis

Looking into the consolidated income statement of the company it can be identified that

the revenues from sales has been reduced from $ 746,753 thousand to $ 542,650 thousands over

the years from 2017 to 2018. The reduction was due to decrease in revenue generated from fair

value adjustments of cattle. Due to reduction in revenues operating margin of the entity reduced

from $ 241,751 thousand to $ 76,848 thousands. Net profit of the company was $ 71,586

thousands for 2017, however, the company experienced loss for an amount of $ 102,559

thousands for the year 2018 (Easton & Sommers, 2018). Hence, it can be stated that the

profitability position of the entity has been deteriorated. Looking into the statement of financial

position of the entity it can be determined that the current assets of the company reduced from $

356,527 thousand to $ 326,601 thousands whereas the current liabilities reduced from $ 44,846

thousand to 34,452 thousands. Hence, it can be stated that the ability of the company has been

increased with regard to payment of short-term obligation. However, the high amount of working

capital is indicating that the entity is not utilizing its working capital efficiently (DeFusco et al.,

2015). Looking into the cash flows statement of the entity it can be identified that the cash

outflow towards operating activities amounted to $ 39,864 thousands, cash outflow towards

investing activities amounted to $ 21,440 thousands and cash inflow from financing activities

amounted to $ 29,989 thousands. Closing cash balance of the entity for 2018 has been reduced as

compared to 2017 (Sippel, 2015).

3.3 Notes to financial statement

Financial statements are prepared on the basis of historical cost, except for the land and

buildings, derivative financial instruments and livestock those are measured at fair values.

Further, it used some critical judgments for accounting, wherever required. It also needs the

3.2 Performance analysis

Looking into the consolidated income statement of the company it can be identified that

the revenues from sales has been reduced from $ 746,753 thousand to $ 542,650 thousands over

the years from 2017 to 2018. The reduction was due to decrease in revenue generated from fair

value adjustments of cattle. Due to reduction in revenues operating margin of the entity reduced

from $ 241,751 thousand to $ 76,848 thousands. Net profit of the company was $ 71,586

thousands for 2017, however, the company experienced loss for an amount of $ 102,559

thousands for the year 2018 (Easton & Sommers, 2018). Hence, it can be stated that the

profitability position of the entity has been deteriorated. Looking into the statement of financial

position of the entity it can be determined that the current assets of the company reduced from $

356,527 thousand to $ 326,601 thousands whereas the current liabilities reduced from $ 44,846

thousand to 34,452 thousands. Hence, it can be stated that the ability of the company has been

increased with regard to payment of short-term obligation. However, the high amount of working

capital is indicating that the entity is not utilizing its working capital efficiently (DeFusco et al.,

2015). Looking into the cash flows statement of the entity it can be identified that the cash

outflow towards operating activities amounted to $ 39,864 thousands, cash outflow towards

investing activities amounted to $ 21,440 thousands and cash inflow from financing activities

amounted to $ 29,989 thousands. Closing cash balance of the entity for 2018 has been reduced as

compared to 2017 (Sippel, 2015).

3.3 Notes to financial statement

Financial statements are prepared on the basis of historical cost, except for the land and

buildings, derivative financial instruments and livestock those are measured at fair values.

Further, it used some critical judgments for accounting, wherever required. It also needs the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS

management to exercise the judgment in procedure of applying accounting policies. Areas those

involve higher level of judgment or the areas where the estimates and assumptions are significant

to financial statement are disclosed through relevant notes (Toohey, 2014). Throughout the

period till the end of 31st March 2018, the prior period comparatives are reclassified for

conforming to the presentation of current year. However, none of the reclassifications were

considered as material. The principal accounting policies those were adopted while prepared the

consolidated financial statements of the entity. Further the policies were consistently applied by

the entity for all the years for which the financial information presented (Oraman, 2014).

4. Accounting strategy evaluation

Though the disclosures to the financial statements it is identified that the company is

limited by shares that is domiciled and incorporated in Australia. Shares of the entity are publicly

traded in ASX. Consolidated financial statements of AACL for the year closed on 31st March

2018 were authorized for the purpose of issuance in accordance with the resolution of Directors

on 23rd May 2018 (Voopl.com.au, 2019). Financial statements are general purpose financial

statements and are prepared in accordance with the requirement of for-profit entity with the

requirements of Corporation Act 2001, AAS and the other authoritative pronouncement of

AASB. The financial statements are further complied with the IFRS (International Financial

Reporting Standards) that is issued by IASB (International Accounting Standard Board)

(Voopl.com.au, 2019).

Financial reports for the year closed 31st March was audited by KPMG and as per the

view of the auditors the accompanied financial report of the entity are prepared in compliance

with Corporation Act 2001. The financial reports provides true and fair view in context of the

management to exercise the judgment in procedure of applying accounting policies. Areas those

involve higher level of judgment or the areas where the estimates and assumptions are significant

to financial statement are disclosed through relevant notes (Toohey, 2014). Throughout the

period till the end of 31st March 2018, the prior period comparatives are reclassified for

conforming to the presentation of current year. However, none of the reclassifications were

considered as material. The principal accounting policies those were adopted while prepared the

consolidated financial statements of the entity. Further the policies were consistently applied by

the entity for all the years for which the financial information presented (Oraman, 2014).

4. Accounting strategy evaluation

Though the disclosures to the financial statements it is identified that the company is

limited by shares that is domiciled and incorporated in Australia. Shares of the entity are publicly

traded in ASX. Consolidated financial statements of AACL for the year closed on 31st March

2018 were authorized for the purpose of issuance in accordance with the resolution of Directors

on 23rd May 2018 (Voopl.com.au, 2019). Financial statements are general purpose financial

statements and are prepared in accordance with the requirement of for-profit entity with the

requirements of Corporation Act 2001, AAS and the other authoritative pronouncement of

AASB. The financial statements are further complied with the IFRS (International Financial

Reporting Standards) that is issued by IASB (International Accounting Standard Board)

(Voopl.com.au, 2019).

Financial reports for the year closed 31st March was audited by KPMG and as per the

view of the auditors the accompanied financial report of the entity are prepared in compliance

with Corporation Act 2001. The financial reports provides true and fair view in context of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS

financial position of the entity dated 31st March 2018 and the financial performance for the year

closed on that date. The statements are further complied with the AAS and Corporation

Regulation 2001. Further, the corporate governance statement of the entity stated the framework

for corporate governance that is adopted by the board of the company (Voopl.com.au, 2019).

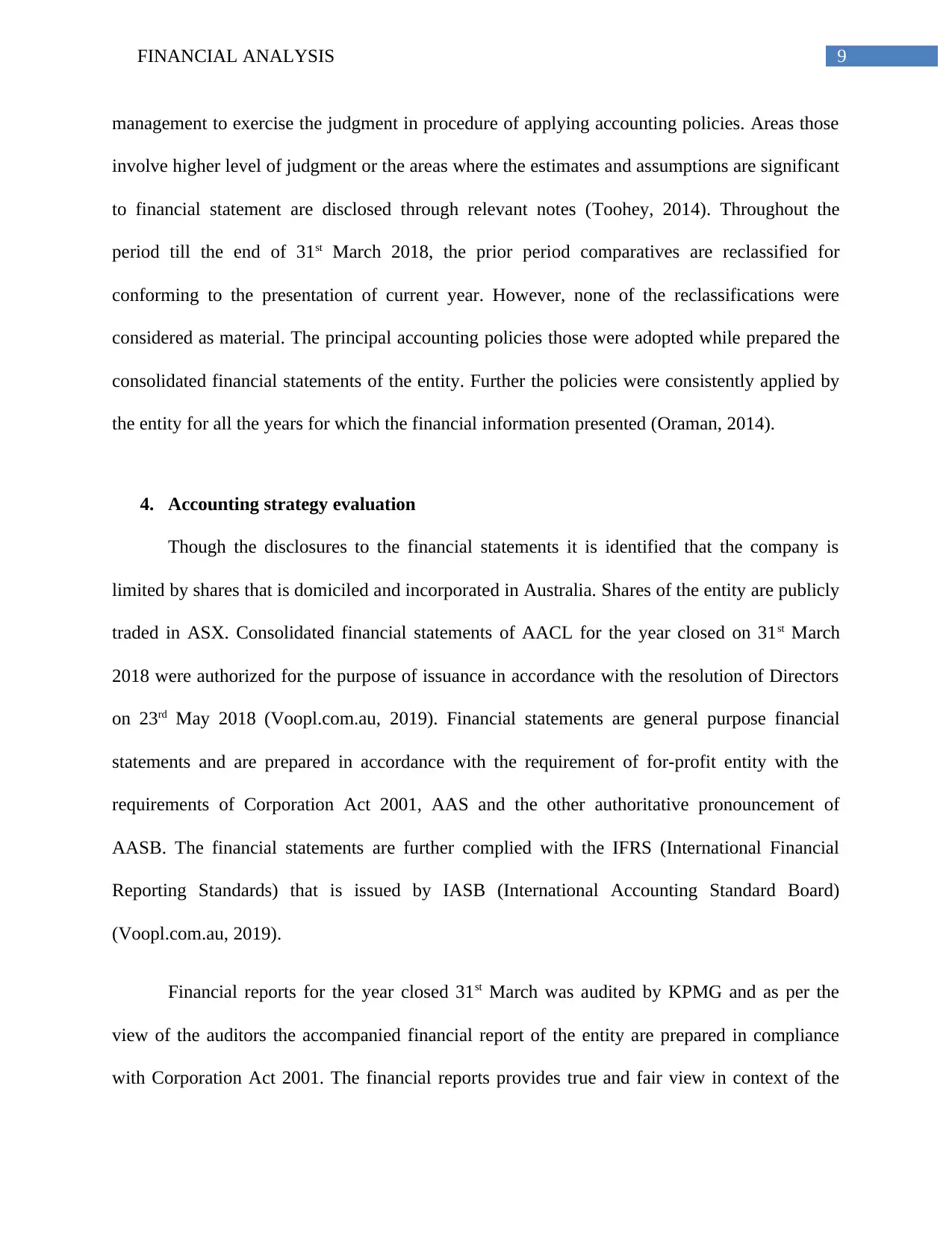

5. Recasting the financial statements

Income statement

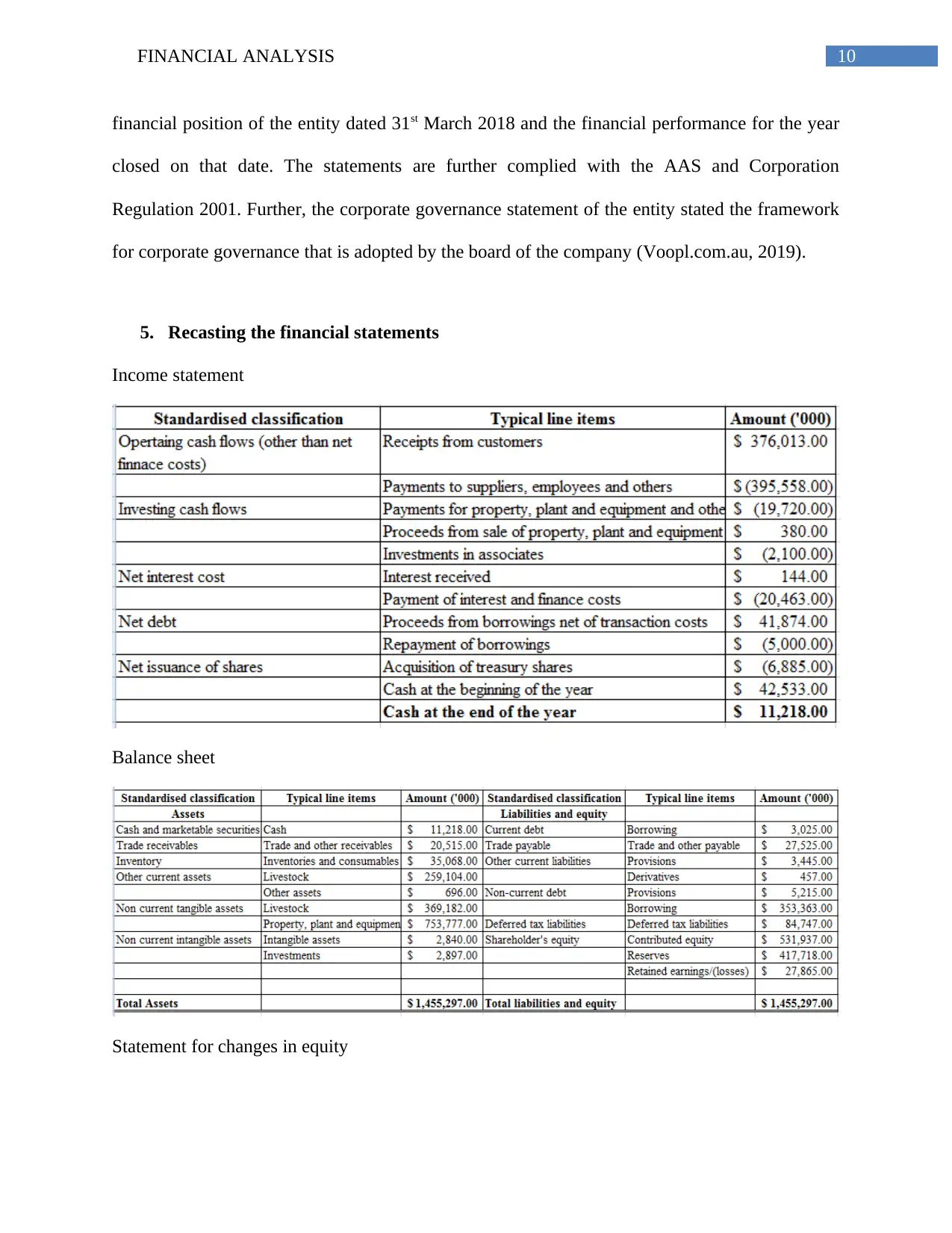

Balance sheet

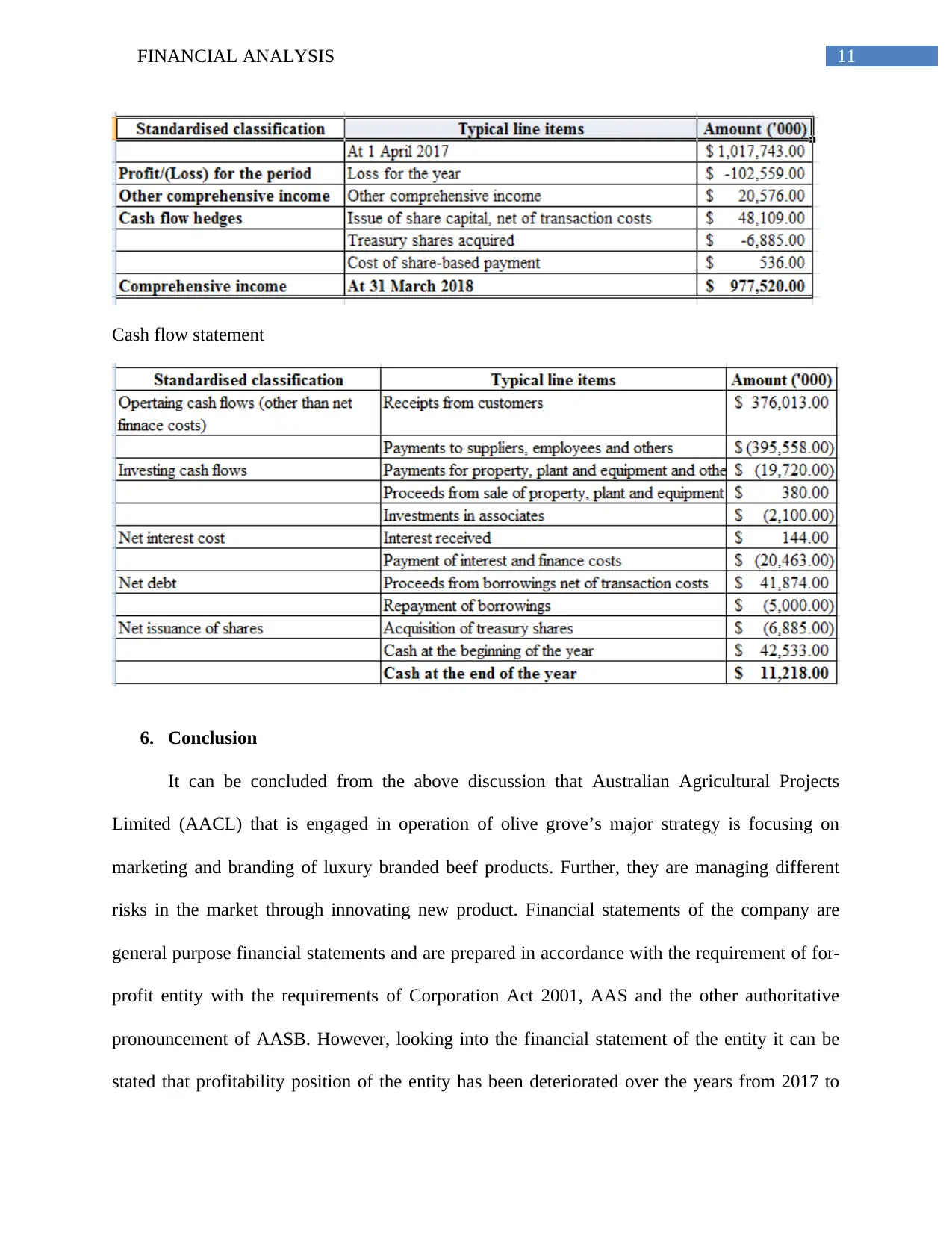

Statement for changes in equity

financial position of the entity dated 31st March 2018 and the financial performance for the year

closed on that date. The statements are further complied with the AAS and Corporation

Regulation 2001. Further, the corporate governance statement of the entity stated the framework

for corporate governance that is adopted by the board of the company (Voopl.com.au, 2019).

5. Recasting the financial statements

Income statement

Balance sheet

Statement for changes in equity

11FINANCIAL ANALYSIS

Cash flow statement

6. Conclusion

It can be concluded from the above discussion that Australian Agricultural Projects

Limited (AACL) that is engaged in operation of olive grove’s major strategy is focusing on

marketing and branding of luxury branded beef products. Further, they are managing different

risks in the market through innovating new product. Financial statements of the company are

general purpose financial statements and are prepared in accordance with the requirement of for-

profit entity with the requirements of Corporation Act 2001, AAS and the other authoritative

pronouncement of AASB. However, looking into the financial statement of the entity it can be

stated that profitability position of the entity has been deteriorated over the years from 2017 to

Cash flow statement

6. Conclusion

It can be concluded from the above discussion that Australian Agricultural Projects

Limited (AACL) that is engaged in operation of olive grove’s major strategy is focusing on

marketing and branding of luxury branded beef products. Further, they are managing different

risks in the market through innovating new product. Financial statements of the company are

general purpose financial statements and are prepared in accordance with the requirement of for-

profit entity with the requirements of Corporation Act 2001, AAS and the other authoritative

pronouncement of AASB. However, looking into the financial statement of the entity it can be

stated that profitability position of the entity has been deteriorated over the years from 2017 to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.