Comparison of Tesco and Walmart's Financial Performance

VerifiedAdded on 2020/07/23

|26

|3672

|56

AI Summary

The assignment compares the financial performance of Tesco and Walmart, two large retail companies. It analyzes their cash flows, working capital, and financial statements to determine which company shows better growth prospects. The comparison reveals that Walmart has a stronger growth picture than Tesco, with significant improvements in net income and controlled current ratios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Analysis

Management

&

Entrepreneurship

Management

&

Entrepreneurship

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

1 Evaluation of the financial performance and financial position of Walmart and Tesco..........1

2. Evaluation of the Working Capital.......................................................................................19

3. Evaluation of cash flow.........................................................................................................20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION...........................................................................................................................1

1 Evaluation of the financial performance and financial position of Walmart and Tesco..........1

2. Evaluation of the Working Capital.......................................................................................19

3. Evaluation of cash flow.........................................................................................................20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................23

INTRODUCTION

In this report, analyses of the financial performances of two companies Walmart and

Tesco has been done. Both company has compared through ratio analysis and vertical and

horizontal analysis of both the companies. Their working capital has been evaluated in this

report, to find the efficiency of Walmart and Tesco during operations. Cash flow analysis will

recommend which company is more liquid.

Walmart is an American transnational selling corp that run as a chain of supermarket and

deduction division stores. It has 11.695 stores and approaches to 28 countries. Its has

approximate revenue of $480 billion. Tesco is also a British multinational grocery retailer as like

Walmart. It is leaded by Walmart in total number of stores. Because Tesco has only 7000 stores

across the countries. It has recorded $73.59 billion as a revenue at the end of 2016. So again

Walmart is leading with $480 billion revenue which is 5 times greater than TESCO.

1 Evaluation of the financial performance and financial position of Walmart and Tesco

To understand the value a company, investors have to look firm's financial positions

(Burns, 2010). Financial analysis involves the use of financial statements, horizontal and vertical

analysis, ratio analysis, etc. to find the actual positions of two companies. Financial statements

consists Income Statement, cash flow statement and Balance sheet of a company. Below is the

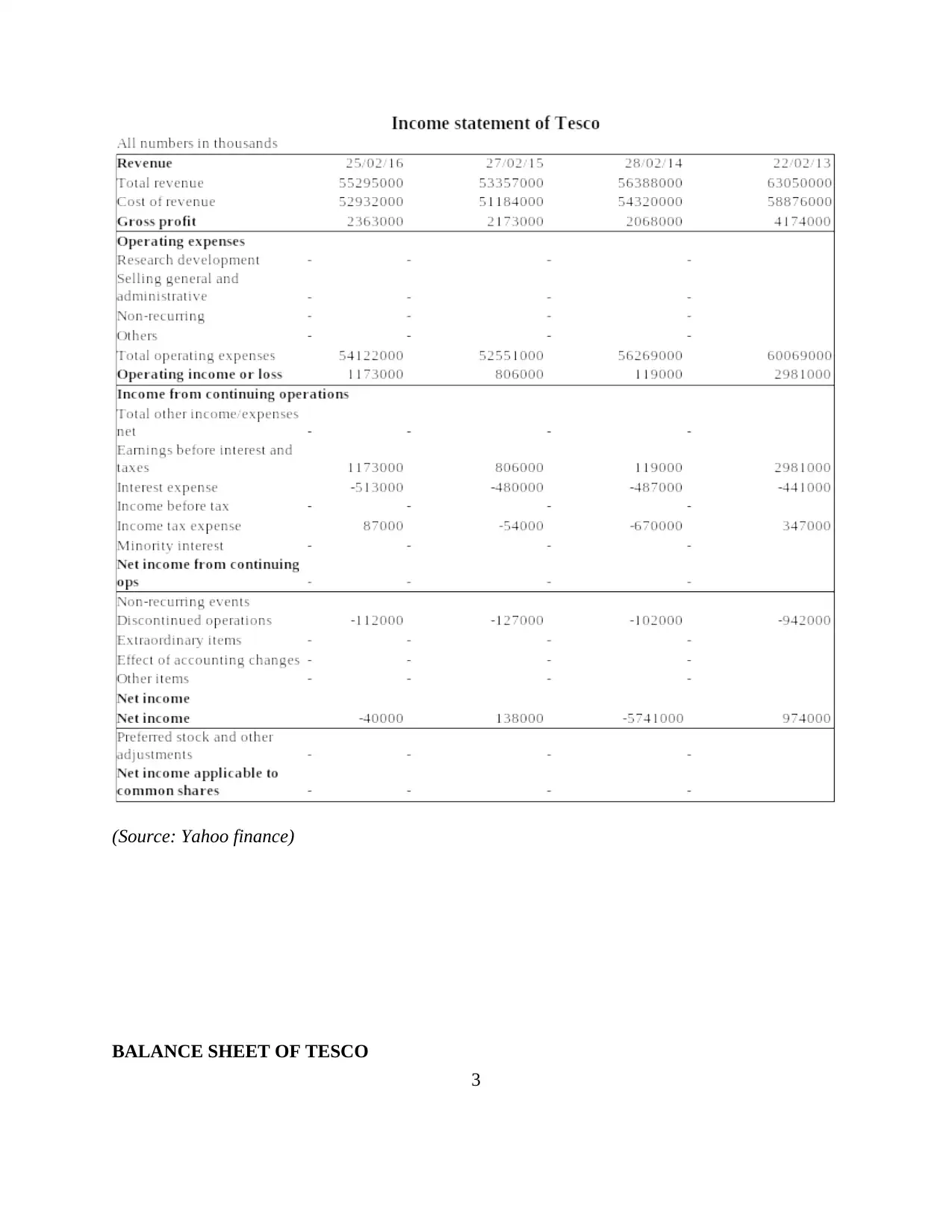

financial statements of Tesco and Walmart over 4 years from 2013 to 2016:

Horizontal Analysis of TESCO's income statement:

Total Revenue: Company's total revenue is declining continuously from 2013 to 2014 as

in 2013 it records approx $63 billion revenue which decline in 2014 by approx 11% and

2015 it again records approx 5% shortfall in revenues. But due to implementing attractive

strategies its revenue again increased approx 4.2%. Still Tesco needs more improvement.

It should increase advertisements, improve its quality services and should examine the

market.

Interest Expenses: Tesco's paying more interest on its debts, as from the figure it is

clearly shown that its besides decreasing in its total revenue, its interest expenses is

increasing continuously. Which indicates that the company is utilizing more funds

comparing to previous years. So it can use these funds either in the expansion of the

1

In this report, analyses of the financial performances of two companies Walmart and

Tesco has been done. Both company has compared through ratio analysis and vertical and

horizontal analysis of both the companies. Their working capital has been evaluated in this

report, to find the efficiency of Walmart and Tesco during operations. Cash flow analysis will

recommend which company is more liquid.

Walmart is an American transnational selling corp that run as a chain of supermarket and

deduction division stores. It has 11.695 stores and approaches to 28 countries. Its has

approximate revenue of $480 billion. Tesco is also a British multinational grocery retailer as like

Walmart. It is leaded by Walmart in total number of stores. Because Tesco has only 7000 stores

across the countries. It has recorded $73.59 billion as a revenue at the end of 2016. So again

Walmart is leading with $480 billion revenue which is 5 times greater than TESCO.

1 Evaluation of the financial performance and financial position of Walmart and Tesco

To understand the value a company, investors have to look firm's financial positions

(Burns, 2010). Financial analysis involves the use of financial statements, horizontal and vertical

analysis, ratio analysis, etc. to find the actual positions of two companies. Financial statements

consists Income Statement, cash flow statement and Balance sheet of a company. Below is the

financial statements of Tesco and Walmart over 4 years from 2013 to 2016:

Horizontal Analysis of TESCO's income statement:

Total Revenue: Company's total revenue is declining continuously from 2013 to 2014 as

in 2013 it records approx $63 billion revenue which decline in 2014 by approx 11% and

2015 it again records approx 5% shortfall in revenues. But due to implementing attractive

strategies its revenue again increased approx 4.2%. Still Tesco needs more improvement.

It should increase advertisements, improve its quality services and should examine the

market.

Interest Expenses: Tesco's paying more interest on its debts, as from the figure it is

clearly shown that its besides decreasing in its total revenue, its interest expenses is

increasing continuously. Which indicates that the company is utilizing more funds

comparing to previous years. So it can use these funds either in the expansion of the

1

business or in promotion. But Tesco has declining revenues thus it is clear that company

has invested its debt funds in opening new stores.

Net Income: Tesco's net income is not stable. As company is only earning profit in 2013

and 2015. But it has incurred huge loss in 2014 which is approx $5.74 billion. It indicates

that company was fail to control its costs of goods sold and other operating expenses with

the decline in Total revenues.

2

has invested its debt funds in opening new stores.

Net Income: Tesco's net income is not stable. As company is only earning profit in 2013

and 2015. But it has incurred huge loss in 2014 which is approx $5.74 billion. It indicates

that company was fail to control its costs of goods sold and other operating expenses with

the decline in Total revenues.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

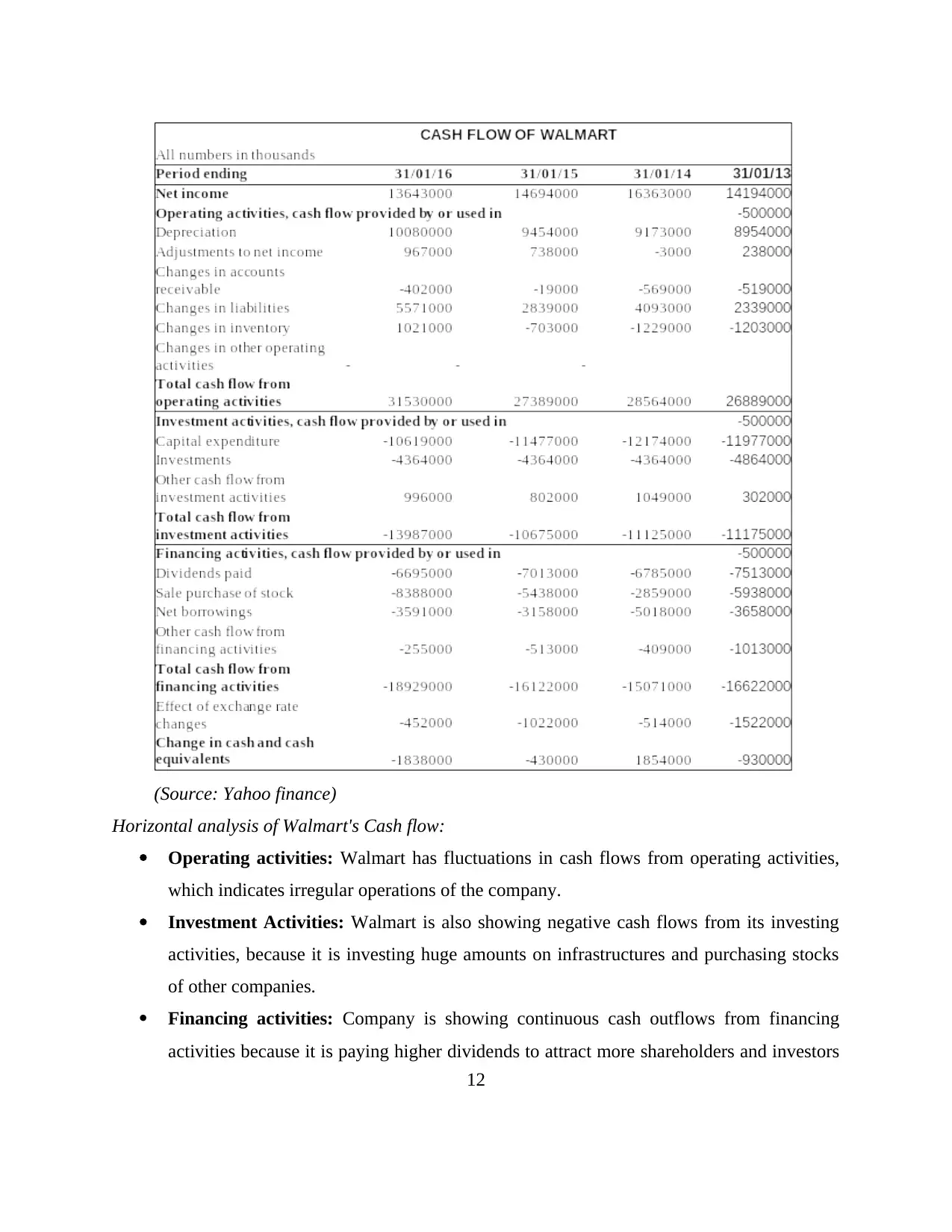

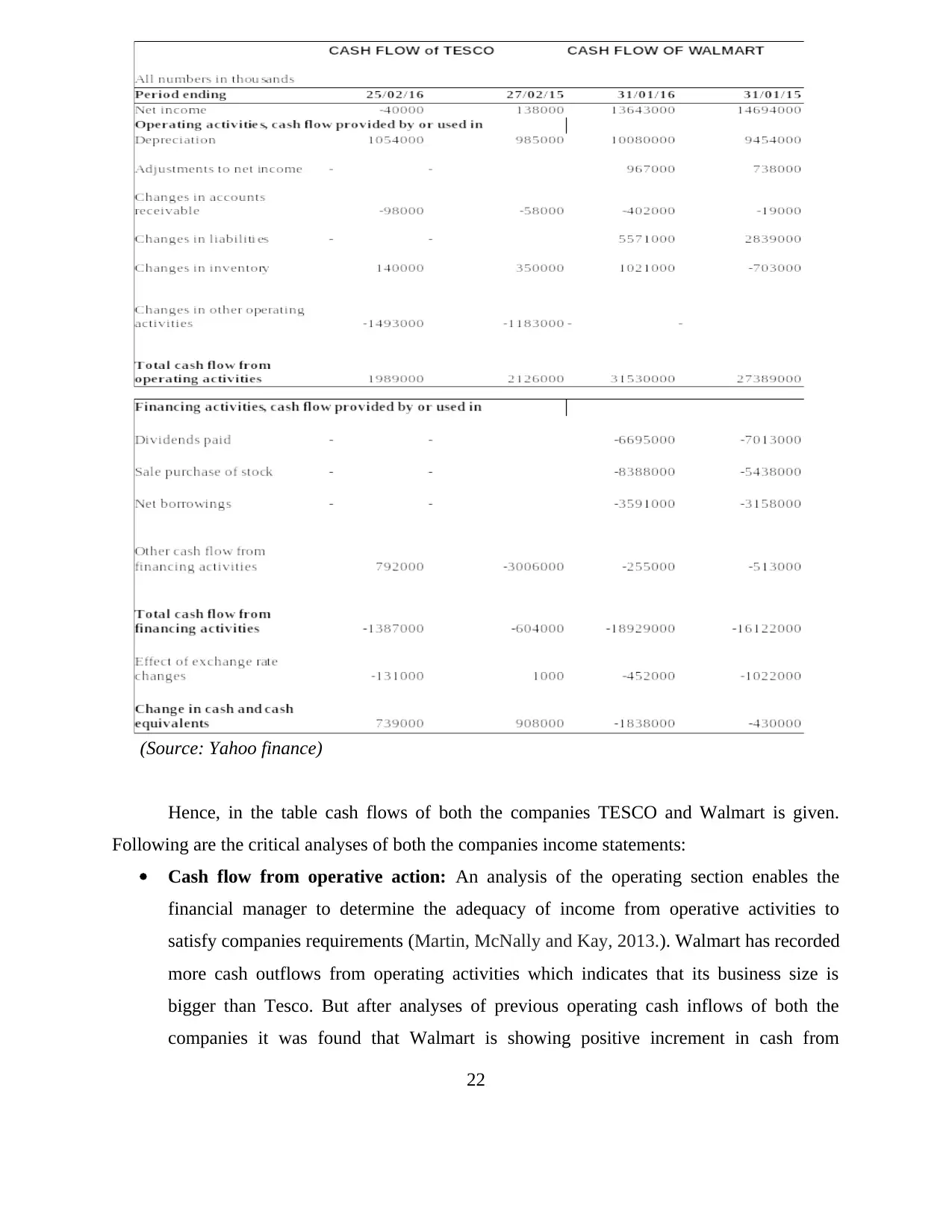

(Source: Yahoo finance)

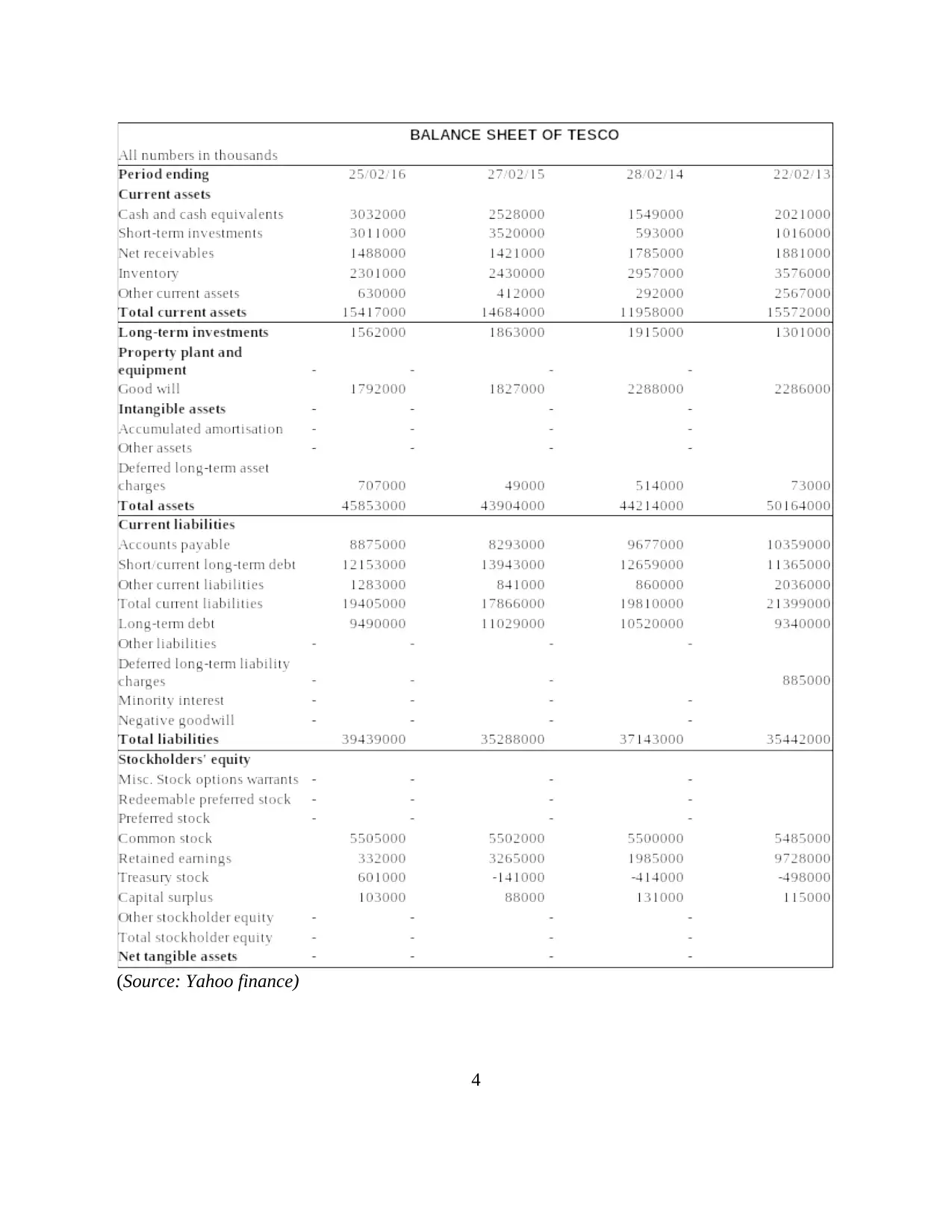

BALANCE SHEET OF TESCO

3

BALANCE SHEET OF TESCO

3

(Source: Yahoo finance)

4

4

Horizontal analysis of Tesco's balance sheet:

Total Current Assets: Companies current assets shows a huge crash in 2014, but after

that it starts improving. The main reason behind this huge declined is inventories.

Because Tesco is failed in producing more groceries due to less demand of the product.

This effect is directly linked with total revenues of the company.

Long-term Investments: Company has invested huge amount in 2014, but it reduces the

investment amount after 2014. it indicates that Tesco is diversifying its funds into

different sources to improve their portfolio.

Total Current Liabilities: Company manages to control its current liabilities to match

with inventories level. But in 2015 company is less financially leverage because its

current liabilities is decreasing with increasing in the sales as compared to 2014. This

indicates the operations efficiency of Tesco.

Equity Stocks: Companies equity stocks are stable which indicates that company is not

raising its funds through issuing stocks but through taking long term debts. Tesco doesn't

have any constant revenue so it is recommended to the company that it should raise its

funds through issuing shares,

5

Total Current Assets: Companies current assets shows a huge crash in 2014, but after

that it starts improving. The main reason behind this huge declined is inventories.

Because Tesco is failed in producing more groceries due to less demand of the product.

This effect is directly linked with total revenues of the company.

Long-term Investments: Company has invested huge amount in 2014, but it reduces the

investment amount after 2014. it indicates that Tesco is diversifying its funds into

different sources to improve their portfolio.

Total Current Liabilities: Company manages to control its current liabilities to match

with inventories level. But in 2015 company is less financially leverage because its

current liabilities is decreasing with increasing in the sales as compared to 2014. This

indicates the operations efficiency of Tesco.

Equity Stocks: Companies equity stocks are stable which indicates that company is not

raising its funds through issuing stocks but through taking long term debts. Tesco doesn't

have any constant revenue so it is recommended to the company that it should raise its

funds through issuing shares,

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

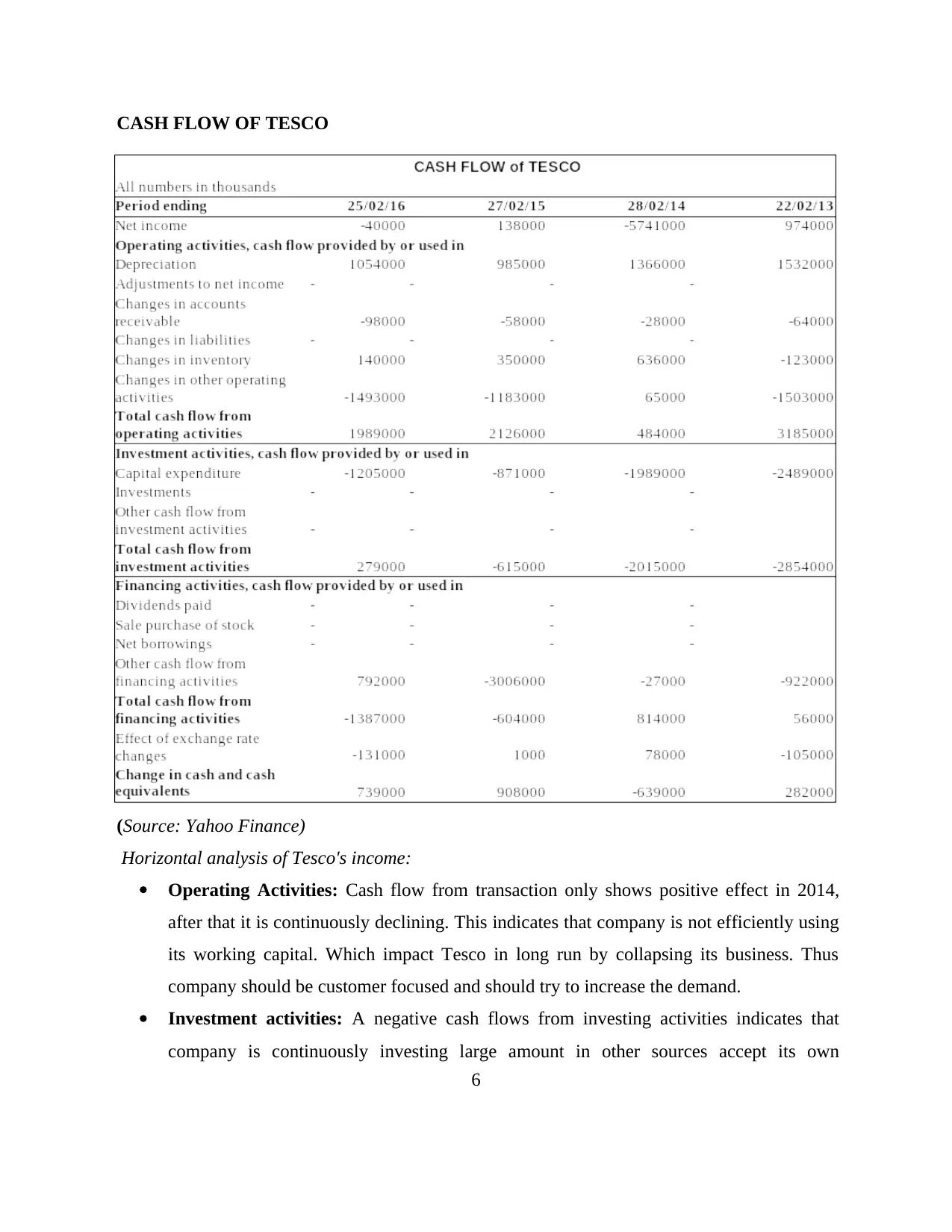

CASH FLOW OF TESCO

(Source: Yahoo Finance)

Horizontal analysis of Tesco's income:

Operating Activities: Cash flow from transaction only shows positive effect in 2014,

after that it is continuously declining. This indicates that company is not efficiently using

its working capital. Which impact Tesco in long run by collapsing its business. Thus

company should be customer focused and should try to increase the demand.

Investment activities: A negative cash flows from investing activities indicates that

company is continuously investing large amount in other sources accept its own

6

(Source: Yahoo Finance)

Horizontal analysis of Tesco's income:

Operating Activities: Cash flow from transaction only shows positive effect in 2014,

after that it is continuously declining. This indicates that company is not efficiently using

its working capital. Which impact Tesco in long run by collapsing its business. Thus

company should be customer focused and should try to increase the demand.

Investment activities: A negative cash flows from investing activities indicates that

company is continuously investing large amount in other sources accept its own

6

operations. At the same time it is not getting any cash inflows from investing activities.

Tesco is not focusing on its core activities which is also the another reason in declining in

total revenue.

Financing Activities: In 2015 and 2016, company is showing negative cash flows which

is due to taking more long-term debt and issuing more equities. As company is not paying

any dividend so this couldn't be reason behind this. But the other possibilities may be that

Tesco is repurchasing its own stock to minimise the power of decision making by other

person outside the company.

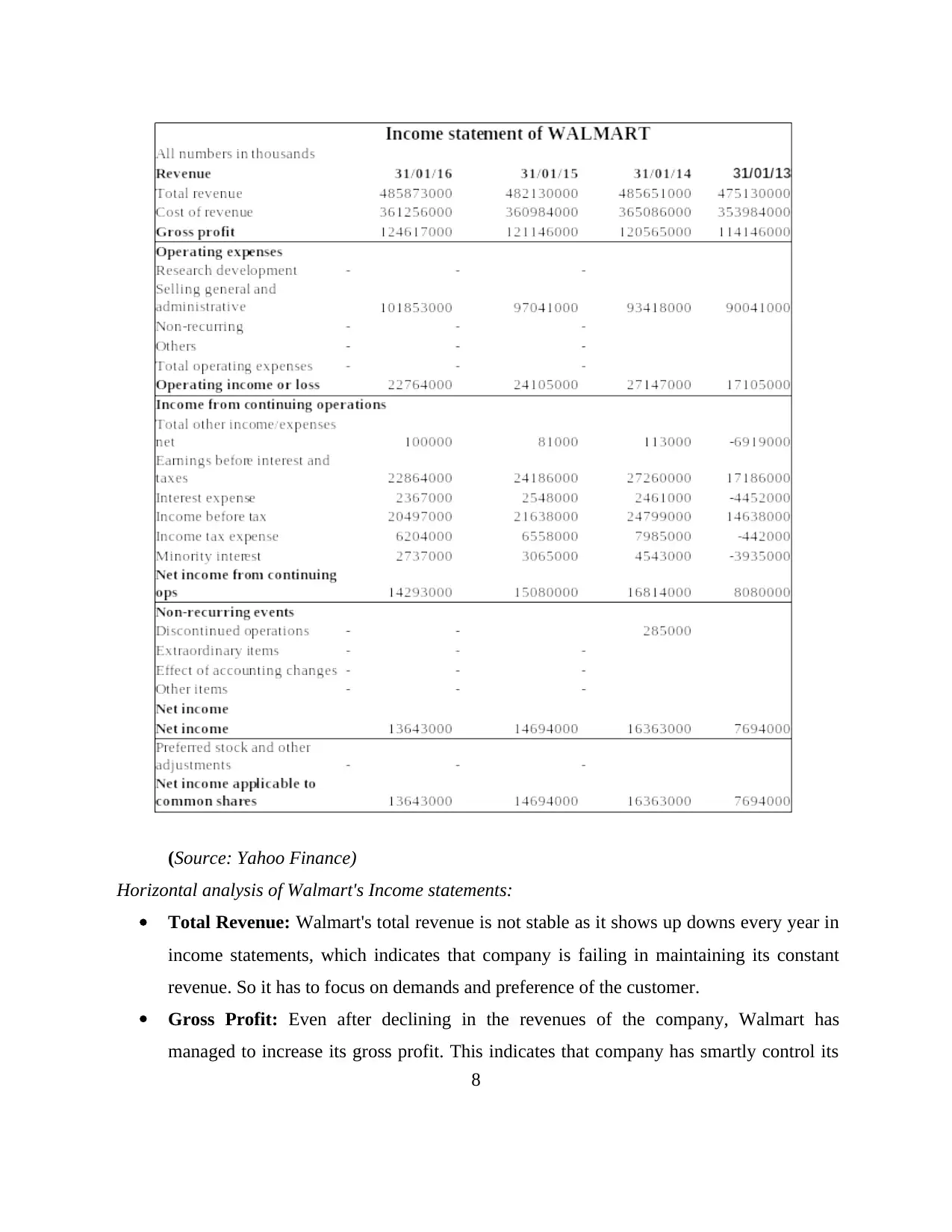

INCOME STATENT OF WALMART

7

Tesco is not focusing on its core activities which is also the another reason in declining in

total revenue.

Financing Activities: In 2015 and 2016, company is showing negative cash flows which

is due to taking more long-term debt and issuing more equities. As company is not paying

any dividend so this couldn't be reason behind this. But the other possibilities may be that

Tesco is repurchasing its own stock to minimise the power of decision making by other

person outside the company.

INCOME STATENT OF WALMART

7

(Source: Yahoo Finance)

Horizontal analysis of Walmart's Income statements:

Total Revenue: Walmart's total revenue is not stable as it shows up downs every year in

income statements, which indicates that company is failing in maintaining its constant

revenue. So it has to focus on demands and preference of the customer.

Gross Profit: Even after declining in the revenues of the company, Walmart has

managed to increase its gross profit. This indicates that company has smartly control its

8

Horizontal analysis of Walmart's Income statements:

Total Revenue: Walmart's total revenue is not stable as it shows up downs every year in

income statements, which indicates that company is failing in maintaining its constant

revenue. So it has to focus on demands and preference of the customer.

Gross Profit: Even after declining in the revenues of the company, Walmart has

managed to increase its gross profit. This indicates that company has smartly control its

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

cost of goods sold through reduced raw material costs and labour costs (Stokes, Wilson,

and Wilson, 2010).

Interest Expenses: Walmart's interest on debt was increased up-to 2015 but company

managed to reduced this expenses, because company internally analyses its strength and

evaluate that it's revenue is not constant so it should raise funds through issuing shares in

the market. This indicates that it has good capital structure.

Net Income: Companies net income is decreasing instead of increasing in gross profit

trends. This indicates that company is utilizing more cash in its operations like paying

rents, depreciations, etc.

9

and Wilson, 2010).

Interest Expenses: Walmart's interest on debt was increased up-to 2015 but company

managed to reduced this expenses, because company internally analyses its strength and

evaluate that it's revenue is not constant so it should raise funds through issuing shares in

the market. This indicates that it has good capital structure.

Net Income: Companies net income is decreasing instead of increasing in gross profit

trends. This indicates that company is utilizing more cash in its operations like paying

rents, depreciations, etc.

9

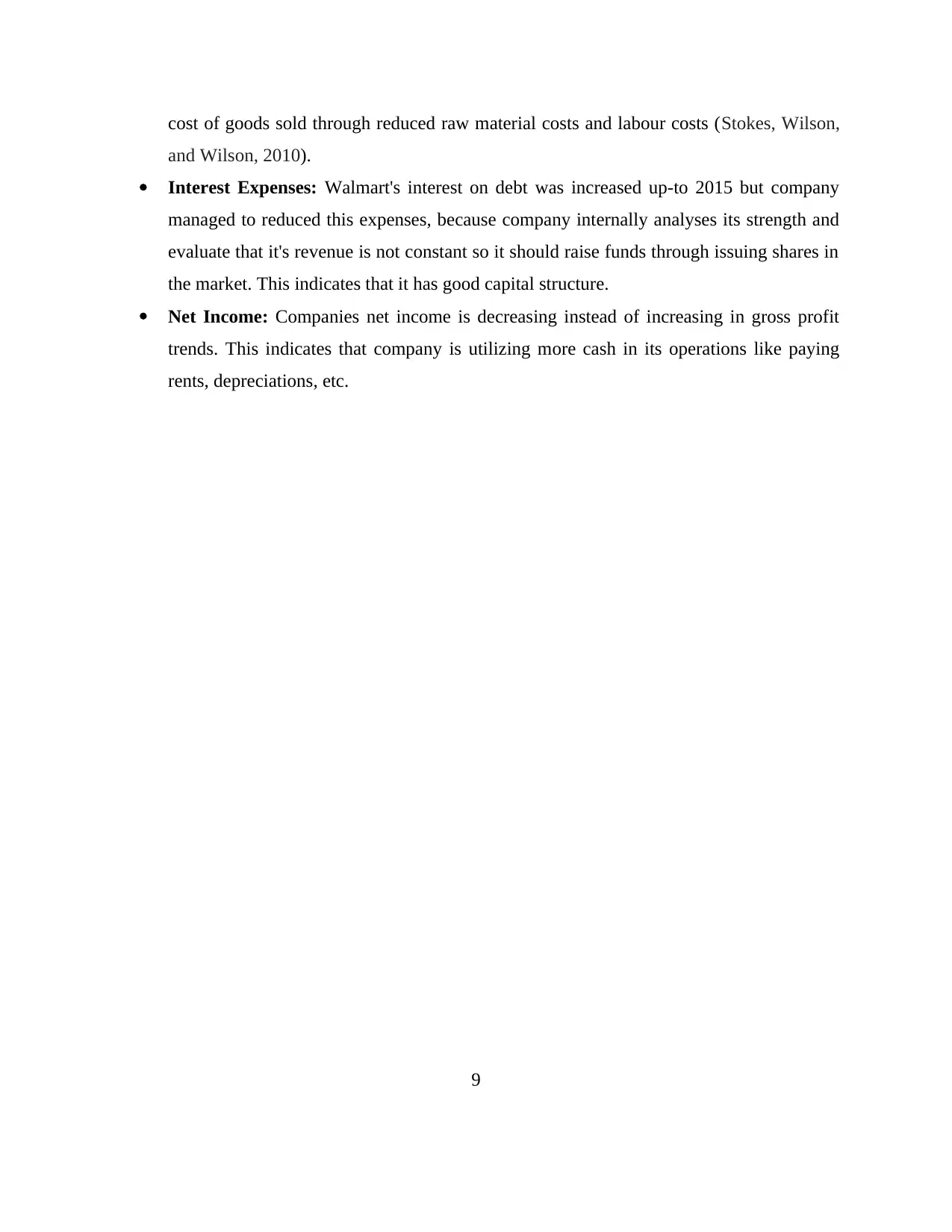

(Source: Yahoo finance)

Horizontal analysis of Walmart's Balance Sheet:

Total current Assets: Companies current assets are declining every year, because

of decreasing inventories. This indicates that Walmart is failing in deal with market

changes and thus its demand of product is declining every year.

10

Horizontal analysis of Walmart's Balance Sheet:

Total current Assets: Companies current assets are declining every year, because

of decreasing inventories. This indicates that Walmart is failing in deal with market

changes and thus its demand of product is declining every year.

10

Total Current Liabilities: Walmart's current liabilities is increasing every year

because of increasing in the number of debtors with the decreasing in number of

sales. This indicates that company is not efficiently managing its working capital as

its almost fund is stuck in operations.

Equity funds: Companies equity stock is declining every year, which indicates

that company is repurchasing its own shares.

CASH FLOW OF WALMART

11

because of increasing in the number of debtors with the decreasing in number of

sales. This indicates that company is not efficiently managing its working capital as

its almost fund is stuck in operations.

Equity funds: Companies equity stock is declining every year, which indicates

that company is repurchasing its own shares.

CASH FLOW OF WALMART

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: Yahoo finance)

Horizontal analysis of Walmart's Cash flow:

Operating activities: Walmart has fluctuations in cash flows from operating activities,

which indicates irregular operations of the company.

Investment Activities: Walmart is also showing negative cash flows from its investing

activities, because it is investing huge amounts on infrastructures and purchasing stocks

of other companies.

Financing activities: Company is showing continuous cash outflows from financing

activities because it is paying higher dividends to attract more shareholders and investors

12

Horizontal analysis of Walmart's Cash flow:

Operating activities: Walmart has fluctuations in cash flows from operating activities,

which indicates irregular operations of the company.

Investment Activities: Walmart is also showing negative cash flows from its investing

activities, because it is investing huge amounts on infrastructures and purchasing stocks

of other companies.

Financing activities: Company is showing continuous cash outflows from financing

activities because it is paying higher dividends to attract more shareholders and investors

12

and it is issuing more shares (Rothaermel, 2015). It is also repurchasing its own shares

back.

On the basis of above Horizontal analysis of both the company, below is the comparison between

Tesco and Walmart:

Factors Tesco Walmart

Total Revenue Its total revenue is sloping

downwards till 2015, in 2016 Tesco

showed improvement of 5.42%

Walmart has also don't have constant

revenue trends. There are fluctuations

in the trend of its revenue. So both

companies are at same level at this

factor.

Net Income Tesco has recorded huge loss in 2014,

and the highest net income was

earned only in 2013. After that

company doesn't have steady profits

trends.

Walmart is at stronger position in

comparing with Tesco, because this

company hasn't face any loss during

2013-16, hence it has a strong

financial position than TESCO.

Interest

Expenses

Tesco's interest expense trend is

continuously increasing because

company is raising its funds from

long-term debts.

In case of Walmart, company was

raising its fund through taking more

debt. But in 2016, it records decline in

interest expenses, which indicates that

Walmart has paid some part of debt to

reduce fixed cost.

Gross Profit Tesco's gross profit and total revenue

has a direct relationships because it is

declining with decrease in revenue

and vice-versa. This indicates that

company is failed to control its costs

of goods sold expenses.

Walmart has increasing trend of gross

profit because it is succeeded in

controlling the Cost of goods sold. So

here company has strong position

against Tesco.

Total current Tesco reported huge decline in its Walmart is showing declining trend of

13

back.

On the basis of above Horizontal analysis of both the company, below is the comparison between

Tesco and Walmart:

Factors Tesco Walmart

Total Revenue Its total revenue is sloping

downwards till 2015, in 2016 Tesco

showed improvement of 5.42%

Walmart has also don't have constant

revenue trends. There are fluctuations

in the trend of its revenue. So both

companies are at same level at this

factor.

Net Income Tesco has recorded huge loss in 2014,

and the highest net income was

earned only in 2013. After that

company doesn't have steady profits

trends.

Walmart is at stronger position in

comparing with Tesco, because this

company hasn't face any loss during

2013-16, hence it has a strong

financial position than TESCO.

Interest

Expenses

Tesco's interest expense trend is

continuously increasing because

company is raising its funds from

long-term debts.

In case of Walmart, company was

raising its fund through taking more

debt. But in 2016, it records decline in

interest expenses, which indicates that

Walmart has paid some part of debt to

reduce fixed cost.

Gross Profit Tesco's gross profit and total revenue

has a direct relationships because it is

declining with decrease in revenue

and vice-versa. This indicates that

company is failed to control its costs

of goods sold expenses.

Walmart has increasing trend of gross

profit because it is succeeded in

controlling the Cost of goods sold. So

here company has strong position

against Tesco.

Total current Tesco reported huge decline in its Walmart is showing declining trend of

13

Assets current assets during 2013-14,

because of the declining in the

inventories. But after 2014 it manages

to improve the trend of current assets

through investing in short-term

investments. So in this factor Tesco is

stronger than Walmart.

current assets in its annual report,

because companies inventories are

continuously decreasing and it hasn't

invest in short-term investments which

reduced its total current assets.

Total Current

Liabilities

Tesco in its annual report showing

irregular trend in current liabilities

due to fluctuations in short-term debt.

This company is also showing

fluctuations in current liabilities. But

the stronger point of Walmart is, this

company has reduced large amount of

short-term debt which indicates the

efficiency of its operations. Hence

Walmart is more strong than Tesco.

Operating

activities

Tesco has fluctuations in its cash

inflow trends of its operating

activities, which indicates that

company doesn't have any efficiency

in its operations.

Walmart is also facing same

consequences, hence both the

companies have same strength.

Investment

Activities

Tesco is in stronger position than

Walmart as it is showing positive cash

flows from investing activities in

2016.

Walmart has failed in its effort to

improve its cash flows from investing

activities

Financing

activities

It has shown good growth in its trends

during 2014, but later it is facing

decline in the trend of cash flows

from financing activities. While

company is not paying any dividend.

Walmart is also facing negative cash

flow effect. But the reason for this is

paying dividend to its shareholders.

Thus Walmart has more goodwill than

Tesco.

14

because of the declining in the

inventories. But after 2014 it manages

to improve the trend of current assets

through investing in short-term

investments. So in this factor Tesco is

stronger than Walmart.

current assets in its annual report,

because companies inventories are

continuously decreasing and it hasn't

invest in short-term investments which

reduced its total current assets.

Total Current

Liabilities

Tesco in its annual report showing

irregular trend in current liabilities

due to fluctuations in short-term debt.

This company is also showing

fluctuations in current liabilities. But

the stronger point of Walmart is, this

company has reduced large amount of

short-term debt which indicates the

efficiency of its operations. Hence

Walmart is more strong than Tesco.

Operating

activities

Tesco has fluctuations in its cash

inflow trends of its operating

activities, which indicates that

company doesn't have any efficiency

in its operations.

Walmart is also facing same

consequences, hence both the

companies have same strength.

Investment

Activities

Tesco is in stronger position than

Walmart as it is showing positive cash

flows from investing activities in

2016.

Walmart has failed in its effort to

improve its cash flows from investing

activities

Financing

activities

It has shown good growth in its trends

during 2014, but later it is facing

decline in the trend of cash flows

from financing activities. While

company is not paying any dividend.

Walmart is also facing negative cash

flow effect. But the reason for this is

paying dividend to its shareholders.

Thus Walmart has more goodwill than

Tesco.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Conclusion: From the above comparison it can be concluded that Walmart is at stronger position

than Tesco because of its various strong factors like goodwill, total current liabilities, gross profit

and net incomes.

15

than Tesco because of its various strong factors like goodwill, total current liabilities, gross profit

and net incomes.

15

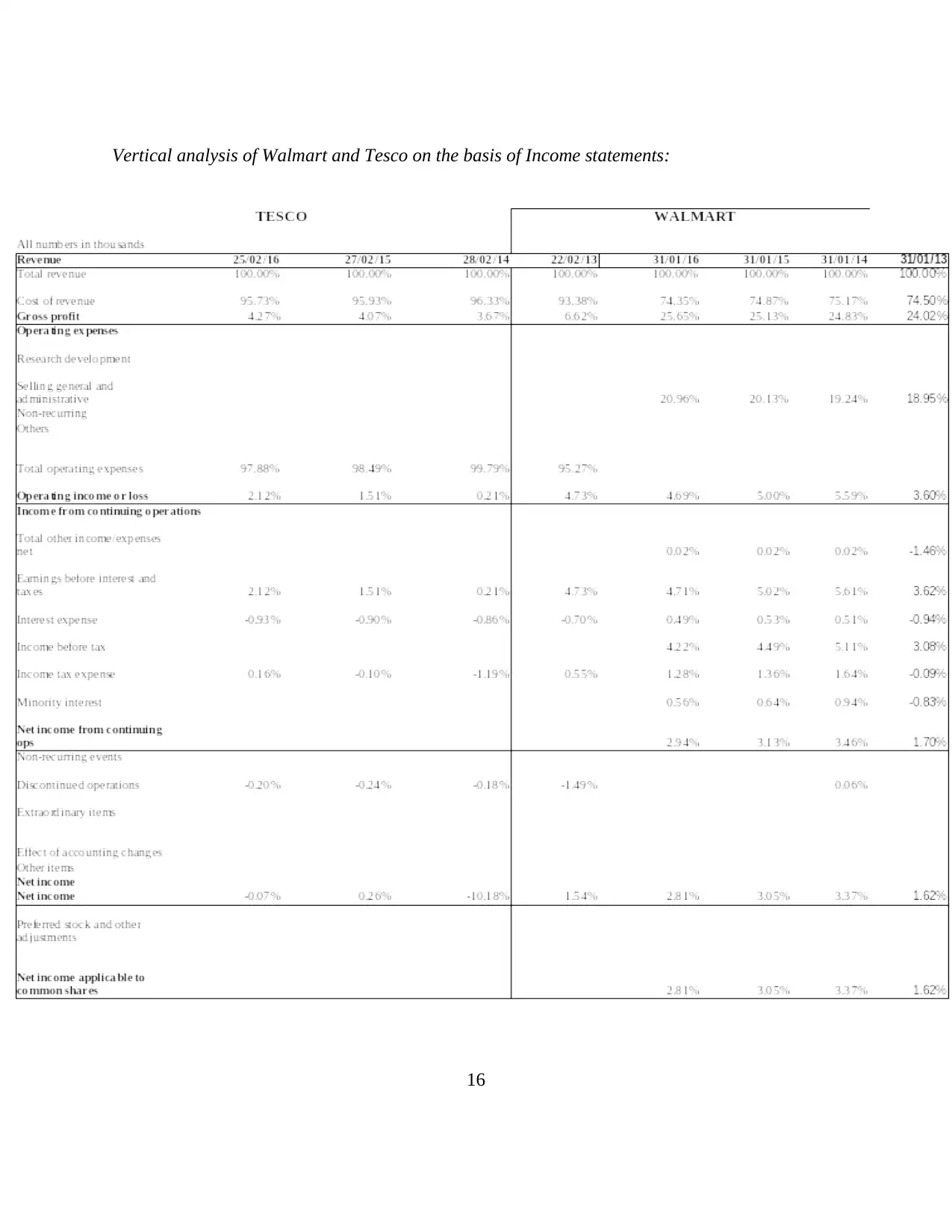

Vertical analysis of Walmart and Tesco on the basis of Income statements:

16

16

On the basis of above vertical analyses, following points can differentiate between these two

firms :

Factors Tesco Walmart

COGS Cost of goods sold of Tesco has

more weight age which is more than

92% as compare to revenues.

Which is not good for the company.

COGS of Walmart covers approx 75%

as compare to sales, which is much

less than Tesco. So Walmart is at

good position on the basis of this

comparison.

Gross Profit Because of more weight-age of

COGS, Tesco has low gross profits,

it has increasing trends since 2014.

Walmart is good enough in earning

gross profit as compared to Tesco,

because it covers less weight-age in

COGS.

Interest Expenses Tesco is showing negative

percentage value, which means its

paying more expenses than earning.

Walmart is earning more interests on

its investments than paying on debts.

That's why it has a positive figures.

Hence Walmart is doing good than

Tesco.

Net Income It has -10% in net income segment

which shows huge loss to the

company. And also companies net

profit weight-age is much less than

of Walmart

Walmart doesn't faced any negative

net income. Hence it is more stronger

than Tesco.

Ratio analysis of Tesco and Walmart( considers only 2016 data):

17

firms :

Factors Tesco Walmart

COGS Cost of goods sold of Tesco has

more weight age which is more than

92% as compare to revenues.

Which is not good for the company.

COGS of Walmart covers approx 75%

as compare to sales, which is much

less than Tesco. So Walmart is at

good position on the basis of this

comparison.

Gross Profit Because of more weight-age of

COGS, Tesco has low gross profits,

it has increasing trends since 2014.

Walmart is good enough in earning

gross profit as compared to Tesco,

because it covers less weight-age in

COGS.

Interest Expenses Tesco is showing negative

percentage value, which means its

paying more expenses than earning.

Walmart is earning more interests on

its investments than paying on debts.

That's why it has a positive figures.

Hence Walmart is doing good than

Tesco.

Net Income It has -10% in net income segment

which shows huge loss to the

company. And also companies net

profit weight-age is much less than

of Walmart

Walmart doesn't faced any negative

net income. Hence it is more stronger

than Tesco.

Ratio analysis of Tesco and Walmart( considers only 2016 data):

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

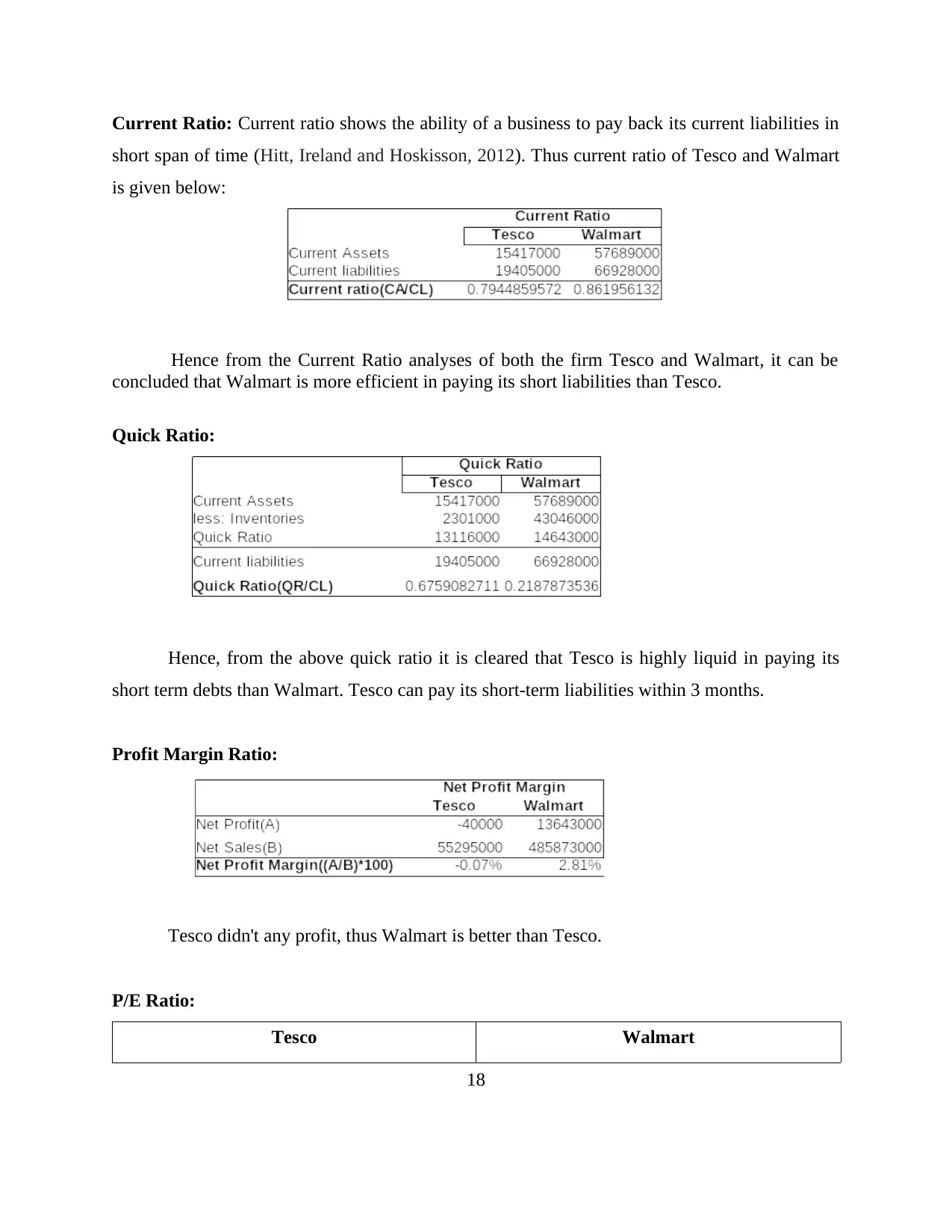

Current Ratio: Current ratio shows the ability of a business to pay back its current liabilities in

short span of time (Hitt, Ireland and Hoskisson, 2012). Thus current ratio of Tesco and Walmart

is given below:

Hence from the Current Ratio analyses of both the firm Tesco and Walmart, it can be

concluded that Walmart is more efficient in paying its short liabilities than Tesco.

Quick Ratio:

Hence, from the above quick ratio it is cleared that Tesco is highly liquid in paying its

short term debts than Walmart. Tesco can pay its short-term liabilities within 3 months.

Profit Margin Ratio:

Tesco didn't any profit, thus Walmart is better than Tesco.

P/E Ratio:

Tesco Walmart

18

short span of time (Hitt, Ireland and Hoskisson, 2012). Thus current ratio of Tesco and Walmart

is given below:

Hence from the Current Ratio analyses of both the firm Tesco and Walmart, it can be

concluded that Walmart is more efficient in paying its short liabilities than Tesco.

Quick Ratio:

Hence, from the above quick ratio it is cleared that Tesco is highly liquid in paying its

short term debts than Walmart. Tesco can pay its short-term liabilities within 3 months.

Profit Margin Ratio:

Tesco didn't any profit, thus Walmart is better than Tesco.

P/E Ratio:

Tesco Walmart

18

$20.95 $21.37

Source: Yahoo finance

Walmart's P/E Ratio is more than Tesco which indicates that company is growing more

than Tesco.

2. Evaluation of the Working Capital

Working capital has two different concepts which are gross concept and net concept.

Where gross concept indicates quantitative approach and net concept shows qualitative approach.

Accordant to quantifiable approach, the sum of working capital refers to Total liquid assets, on

the other hand qualitative approach suggests the sources of financing capital (Kojo Oseifuah,

2010). This approach gives the formulae of Total CA- total CL. Hence working capital means all

superior resources which are accessible to a concern enterprises from stockholder, investor and

creditors. These resources works in enterprise activity to make revenues and ease future

enlargement and maturation (Pierce and Aguinis, 2013). Working capital consists of those

business assets which are utilizing in actual transactions like receivables, inventories, staple,

stokes, work-in-progress and finished goods, commodity, bills receivables, cash and bank.

Analysis of capital is important both in inner and outer way. Because it has direct relationship

with underway day to day dealings of the company. The goal of working capital is to pull off

each firm's CA and CL at acceptable level. Below is the working capital of both firm's Tesco and

Walmart:

TESCO WALMART

Working capital = CA – CL

= 15417000 – 19405000

= −3988000

Working Capital = CA – CL

= 57689000 – 66928000

= −9239000

(Source: Yahoo finance)

Interpretation: From the above calculation, it is clear that both companies working capital is

negative which indicates that both company needs extra funds to run its business. But in case of

Walmart, company needs funds more than Tesco, which mean company has large operations

than Tesco. Because current ratio of Walmart is greater than Tesco.

19

Source: Yahoo finance

Walmart's P/E Ratio is more than Tesco which indicates that company is growing more

than Tesco.

2. Evaluation of the Working Capital

Working capital has two different concepts which are gross concept and net concept.

Where gross concept indicates quantitative approach and net concept shows qualitative approach.

Accordant to quantifiable approach, the sum of working capital refers to Total liquid assets, on

the other hand qualitative approach suggests the sources of financing capital (Kojo Oseifuah,

2010). This approach gives the formulae of Total CA- total CL. Hence working capital means all

superior resources which are accessible to a concern enterprises from stockholder, investor and

creditors. These resources works in enterprise activity to make revenues and ease future

enlargement and maturation (Pierce and Aguinis, 2013). Working capital consists of those

business assets which are utilizing in actual transactions like receivables, inventories, staple,

stokes, work-in-progress and finished goods, commodity, bills receivables, cash and bank.

Analysis of capital is important both in inner and outer way. Because it has direct relationship

with underway day to day dealings of the company. The goal of working capital is to pull off

each firm's CA and CL at acceptable level. Below is the working capital of both firm's Tesco and

Walmart:

TESCO WALMART

Working capital = CA – CL

= 15417000 – 19405000

= −3988000

Working Capital = CA – CL

= 57689000 – 66928000

= −9239000

(Source: Yahoo finance)

Interpretation: From the above calculation, it is clear that both companies working capital is

negative which indicates that both company needs extra funds to run its business. But in case of

Walmart, company needs funds more than Tesco, which mean company has large operations

than Tesco. Because current ratio of Walmart is greater than Tesco.

19

Thus there are following importance of analysis of working capital for both the company

Tesco and Walmart in taking decisions:

Company can know their financial status: Through analysis of working capital, Tesco

and Walmart can identify their financial status. As in the above calculations both the

companies had show negative working capital which indicates that both firms needs

external source of fund to run its operations. So management of the enterprises will take

decisions about which sources of funds should be considered either debt source or equity

source. And also management can take decisions to pay back its liabilities to improve

working capital.

It gives the information regarding the efficiency of the business: Through working

capital analysis, company can take decisions whether to grow their business or not (Misra

and Puri, 2011). A positive working capital indicates the good efficiency of the company.

Hence in the above calculations both the companies have negative working capital which

means both are not in the position to take expansion decisions as they don't have much

cash to continue their day to day operations.

3. Evaluation of cash flow

Annual cash flows of both the companies are given below:

20

Tesco and Walmart in taking decisions:

Company can know their financial status: Through analysis of working capital, Tesco

and Walmart can identify their financial status. As in the above calculations both the

companies had show negative working capital which indicates that both firms needs

external source of fund to run its operations. So management of the enterprises will take

decisions about which sources of funds should be considered either debt source or equity

source. And also management can take decisions to pay back its liabilities to improve

working capital.

It gives the information regarding the efficiency of the business: Through working

capital analysis, company can take decisions whether to grow their business or not (Misra

and Puri, 2011). A positive working capital indicates the good efficiency of the company.

Hence in the above calculations both the companies have negative working capital which

means both are not in the position to take expansion decisions as they don't have much

cash to continue their day to day operations.

3. Evaluation of cash flow

Annual cash flows of both the companies are given below:

20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

21

(Source: Yahoo finance)

Hence, in the table cash flows of both the companies TESCO and Walmart is given.

Following are the critical analyses of both the companies income statements:

Cash flow from operative action: An analysis of the operating section enables the

financial manager to determine the adequacy of income from operative activities to

satisfy companies requirements (Martin, McNally and Kay, 2013.). Walmart has recorded

more cash outflows from operating activities which indicates that its business size is

bigger than Tesco. But after analyses of previous operating cash inflows of both the

companies it was found that Walmart is showing positive increment in cash from

22

Hence, in the table cash flows of both the companies TESCO and Walmart is given.

Following are the critical analyses of both the companies income statements:

Cash flow from operative action: An analysis of the operating section enables the

financial manager to determine the adequacy of income from operative activities to

satisfy companies requirements (Martin, McNally and Kay, 2013.). Walmart has recorded

more cash outflows from operating activities which indicates that its business size is

bigger than Tesco. But after analyses of previous operating cash inflows of both the

companies it was found that Walmart is showing positive increment in cash from

22

operating activities compare to 2015. In the case of Tesco, companies showing negative

increment from 2015 to 2016 due to loss in 2016. Therefore choosing Walmart for

investment will be good.

Investing Activities: This subdivision mostly indicate the payment which a company has

spent on cost and short-term investments like new equipment, land and buildings,

purchasing the shares of other companies (Lounsbury and Hirsch, 2010). Both the

companies is showing negative cash flows from investing activities, which indicates that

they are utilizing more cash in investment activities like for acquiring new assets or

machines. That also means that both the companies is re-investing their funds to grow

their businesses. To take decision in choosing best company, investors has to consider

their earning per share values.

Financing Activities: This section tells about the events of cash, associated with outside

funding activities. Cash inflows into the business indicates that cash is elevated by

merchandising stock and bonds or through dealing from banks (Lohrke, Holloway and

Woolley, 2010). And negative cash flow is the indication of paying back of long- term

loans, dividend payments and repurchases of common stock. After comparing both the

companies investing activities, it was found that Tesco and Walmart is using cash in

paying dividends, loans and repurchases of their shares. But still it will be good decision

to select Walmart for investing funds because company is paying dividend to their

shareholders which is a positive sign for their stakeholders.

CONCLUSION

After evaluating cash flows, working capital and financial statements of Walmart and

Tesco, it was found that both firms are huge in size and are in same industries. So, it was prefect

comparison. Known investors are attracted towards those companies which produces plenty of

free cash flows. Because FCF signals that a institution is capable to fund its liability and

dividends. It can also facilitate the development of the business. After analysis of all the

comparison factors of Tesco and Walmart, it is concluded that Walmart is showing better growth

picture than Tesco. Because this company is significantly showing growth in its net income and

has also managed to control its current ratio's.

23

increment from 2015 to 2016 due to loss in 2016. Therefore choosing Walmart for

investment will be good.

Investing Activities: This subdivision mostly indicate the payment which a company has

spent on cost and short-term investments like new equipment, land and buildings,

purchasing the shares of other companies (Lounsbury and Hirsch, 2010). Both the

companies is showing negative cash flows from investing activities, which indicates that

they are utilizing more cash in investment activities like for acquiring new assets or

machines. That also means that both the companies is re-investing their funds to grow

their businesses. To take decision in choosing best company, investors has to consider

their earning per share values.

Financing Activities: This section tells about the events of cash, associated with outside

funding activities. Cash inflows into the business indicates that cash is elevated by

merchandising stock and bonds or through dealing from banks (Lohrke, Holloway and

Woolley, 2010). And negative cash flow is the indication of paying back of long- term

loans, dividend payments and repurchases of common stock. After comparing both the

companies investing activities, it was found that Tesco and Walmart is using cash in

paying dividends, loans and repurchases of their shares. But still it will be good decision

to select Walmart for investing funds because company is paying dividend to their

shareholders which is a positive sign for their stakeholders.

CONCLUSION

After evaluating cash flows, working capital and financial statements of Walmart and

Tesco, it was found that both firms are huge in size and are in same industries. So, it was prefect

comparison. Known investors are attracted towards those companies which produces plenty of

free cash flows. Because FCF signals that a institution is capable to fund its liability and

dividends. It can also facilitate the development of the business. After analysis of all the

comparison factors of Tesco and Walmart, it is concluded that Walmart is showing better growth

picture than Tesco. Because this company is significantly showing growth in its net income and

has also managed to control its current ratio's.

23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

24

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.