Financial Analysis Report: Adelaide Brighton Ltd (ABC) - Investment

VerifiedAdded on 2019/09/30

|24

|6798

|162

Report

AI Summary

This report presents a detailed financial analysis of Adelaide Brighton Ltd (ABC), an Australian company operating in the building, construction, and infrastructure markets. The analysis examines the company's financial performance through key metrics, including liquidity (current ratio), profitability (net profit margin and return on assets), capital structure (debt ratio and interest cover ratio), and market value (price-earning ratio). The report compares ABC's performance to industry averages, providing insights into the company's competitive advantage and efficiency. Furthermore, the report includes a share valuation using the constant dividend discount model and concludes with an investment recommendation based on the financial analysis and market indicators. The analysis suggests a sustainable financial position with potential for growth, but the investor market indicates a no-buy position. The report uses data from ABC's financial statements and IBISWorld reports to support its findings.

Executive Summary

The subject of this analysis is Adelaide Brighton Ltd, established in 1882, distributed in

strategic locations across Australia. Adelaide Brighton, the largest importer of cement in

Australia, supplies building, construction and infrastructure markets with material. Proactive

management has kept costs under control with a reliable and efficient asset base.

The prime motive for business is to make a profit and for investors to have a return on their

investments. The analysis of the financial statements looked at liquidity, profitability, capital

structure and share value providing a rounded analysis. The ratios representing liquidity,

profitability and capital structure show an organisation that is sustainable in the long-term

and supports investment. Analysis of the capital structure shows potential for the

organisation to grow the capital base.

The response from the investor market shows a share value that is above the share value

calculated using the constant dividend discount model. The financial statements lean

towards a recommendation to invest, while the investor market indicates a no-buy position.

The subject of this analysis is Adelaide Brighton Ltd, established in 1882, distributed in

strategic locations across Australia. Adelaide Brighton, the largest importer of cement in

Australia, supplies building, construction and infrastructure markets with material. Proactive

management has kept costs under control with a reliable and efficient asset base.

The prime motive for business is to make a profit and for investors to have a return on their

investments. The analysis of the financial statements looked at liquidity, profitability, capital

structure and share value providing a rounded analysis. The ratios representing liquidity,

profitability and capital structure show an organisation that is sustainable in the long-term

and supports investment. Analysis of the capital structure shows potential for the

organisation to grow the capital base.

The response from the investor market shows a share value that is above the share value

calculated using the constant dividend discount model. The financial statements lean

towards a recommendation to invest, while the investor market indicates a no-buy position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

1. Introduction...........................................................................................................................................1

2. Financial Analysis...................................................................................................................................1

2.1 Liquidity: Current ratio...................................................................................................................1

2.2 Profitability: Net profit margin ratio and Return on total assets...................................................3

2.3 Capital structure: Debt ratio and Interest cover ratio....................................................................5

2.4 Market value: Price-earning (P/E) ratio.........................................................................................6

3. Share Valuation - Constant Dividend Discount Model...........................................................................8

4. Recommendation................................................................................................................................10

5. Conclusion...........................................................................................................................................11

References...................................................................................................................................................12

6. Appendix 1...........................................................................................................................................14

1 Financials.........................................................................................................................................14

2 Growth & Ratios..............................................................................................................................15

3 Industry Averages............................................................................................................................16

4 Competitive Environment................................................................................................................17

7. Appendix 2...........................................................................................................................................21

1. Introduction...........................................................................................................................................1

2. Financial Analysis...................................................................................................................................1

2.1 Liquidity: Current ratio...................................................................................................................1

2.2 Profitability: Net profit margin ratio and Return on total assets...................................................3

2.3 Capital structure: Debt ratio and Interest cover ratio....................................................................5

2.4 Market value: Price-earning (P/E) ratio.........................................................................................6

3. Share Valuation - Constant Dividend Discount Model...........................................................................8

4. Recommendation................................................................................................................................10

5. Conclusion...........................................................................................................................................11

References...................................................................................................................................................12

6. Appendix 1...........................................................................................................................................14

1 Financials.........................................................................................................................................14

2 Growth & Ratios..............................................................................................................................15

3 Industry Averages............................................................................................................................16

4 Competitive Environment................................................................................................................17

7. Appendix 2...........................................................................................................................................21

1. Introduction

Adelaide Brighton Ltd is a publicly owned company, established in 1882 and is registered on the

Australian Stock Exchange (ASX) under the code ABC. Adelaide Brighton (ABC) manufactures and

distributes material across the building construction and infrastructure markets as well as

mineral processing market. Major manufacturing facilities are strategically located in South

Australia, Western Australia and the Northern Territory, enabling ABL to supply all Australian

major centres. To support this, ABL have distribution joint ventures in Victoria and Queensland.

The majority of revenue, 104.92%, for ABC is derived from the cement, lime, concrete and

aggregates segment with concrete products providing 10.09% and unallocated industry

segments returning -15.01% (IBISWorld 2015). Adelaide Brighton has a 38.6% share of the

cement and lime-manufacturing segment, followed by Cement Australia Holdings Pty Ltd and

Boral Ltd (IBISWorld 2015).

This report on the financial analysis of ABC, to support or not support investment in ABC, will

look at liquidity using the current ratio, profitability using net profit margin and return on total

assets, and finally the capital structure using debt ratio and interest cover ratio. The results of

the analysis will be presented in the recommendation section of this report with concluding

remarks in the conclusion.

Towards the end of November 2015 the shares recovered to an upward trend. The past five

years has seen patterns of upward and downward trends. Overall, there has been an upward

trend in the share price. The cyclical nature of the share price trends for ABC has seen drops in

price close the beginning of the year with recovery around July. Recovery for 2016 was early,

around January reflecting the possibility that the share price might be over inflated and due for a

downward trend.

2. Financial Analysis

The financial analysis from financial records published by ABC and reported on by IBISWorld

(2016).

2.1 Liquidity: Current ratio

Note: Unless otherwise stated, the values used are from Appendix 1.

Page | 1

Adelaide Brighton Ltd is a publicly owned company, established in 1882 and is registered on the

Australian Stock Exchange (ASX) under the code ABC. Adelaide Brighton (ABC) manufactures and

distributes material across the building construction and infrastructure markets as well as

mineral processing market. Major manufacturing facilities are strategically located in South

Australia, Western Australia and the Northern Territory, enabling ABL to supply all Australian

major centres. To support this, ABL have distribution joint ventures in Victoria and Queensland.

The majority of revenue, 104.92%, for ABC is derived from the cement, lime, concrete and

aggregates segment with concrete products providing 10.09% and unallocated industry

segments returning -15.01% (IBISWorld 2015). Adelaide Brighton has a 38.6% share of the

cement and lime-manufacturing segment, followed by Cement Australia Holdings Pty Ltd and

Boral Ltd (IBISWorld 2015).

This report on the financial analysis of ABC, to support or not support investment in ABC, will

look at liquidity using the current ratio, profitability using net profit margin and return on total

assets, and finally the capital structure using debt ratio and interest cover ratio. The results of

the analysis will be presented in the recommendation section of this report with concluding

remarks in the conclusion.

Towards the end of November 2015 the shares recovered to an upward trend. The past five

years has seen patterns of upward and downward trends. Overall, there has been an upward

trend in the share price. The cyclical nature of the share price trends for ABC has seen drops in

price close the beginning of the year with recovery around July. Recovery for 2016 was early,

around January reflecting the possibility that the share price might be over inflated and due for a

downward trend.

2. Financial Analysis

The financial analysis from financial records published by ABC and reported on by IBISWorld

(2016).

2.1 Liquidity: Current ratio

Note: Unless otherwise stated, the values used are from Appendix 1.

Page | 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

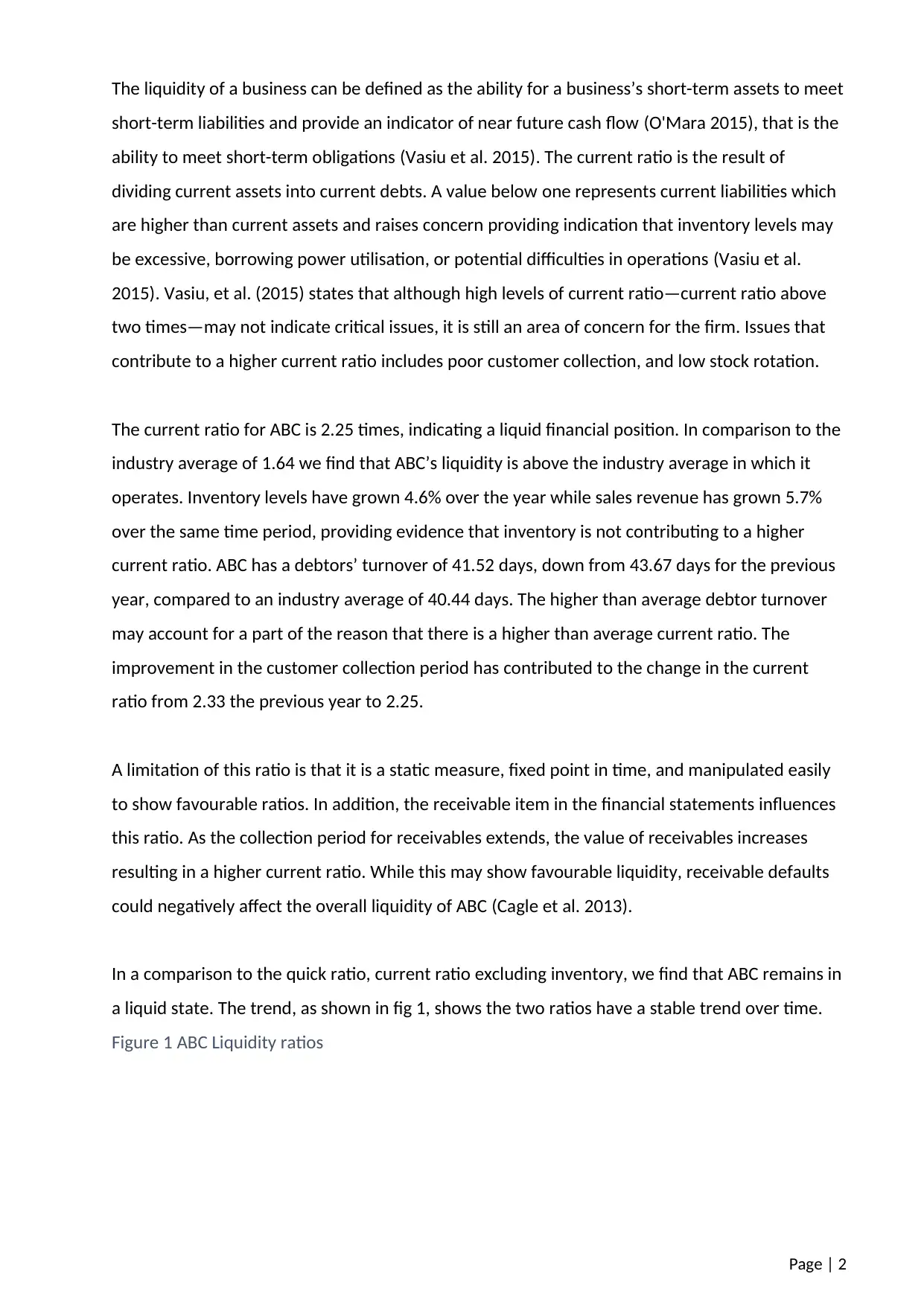

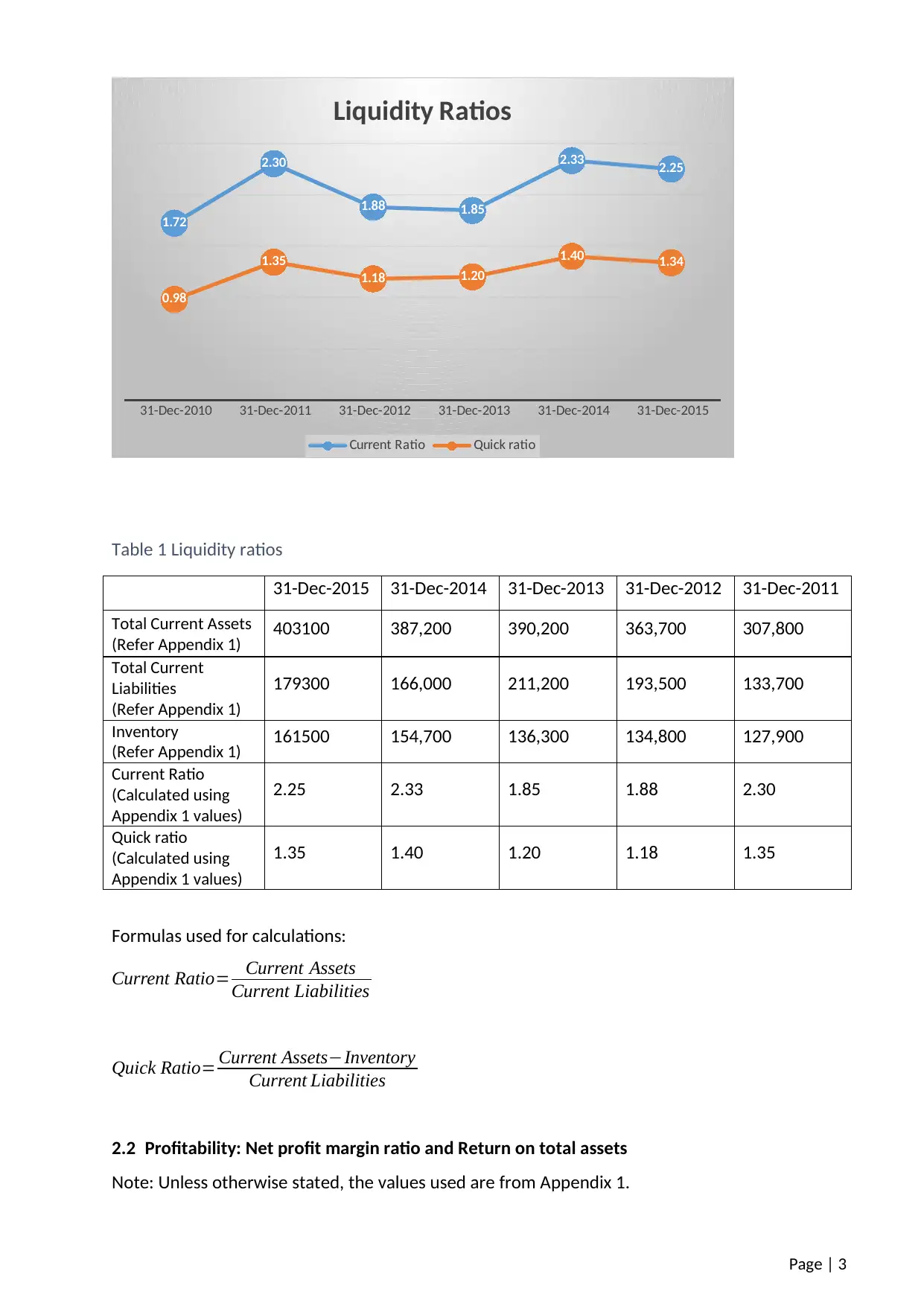

The liquidity of a business can be defined as the ability for a business’s short-term assets to meet

short-term liabilities and provide an indicator of near future cash flow (O'Mara 2015), that is the

ability to meet short-term obligations (Vasiu et al. 2015). The current ratio is the result of

dividing current assets into current debts. A value below one represents current liabilities which

are higher than current assets and raises concern providing indication that inventory levels may

be excessive, borrowing power utilisation, or potential difficulties in operations (Vasiu et al.

2015). Vasiu, et al. (2015) states that although high levels of current ratio—current ratio above

two times—may not indicate critical issues, it is still an area of concern for the firm. Issues that

contribute to a higher current ratio includes poor customer collection, and low stock rotation.

The current ratio for ABC is 2.25 times, indicating a liquid financial position. In comparison to the

industry average of 1.64 we find that ABC’s liquidity is above the industry average in which it

operates. Inventory levels have grown 4.6% over the year while sales revenue has grown 5.7%

over the same time period, providing evidence that inventory is not contributing to a higher

current ratio. ABC has a debtors’ turnover of 41.52 days, down from 43.67 days for the previous

year, compared to an industry average of 40.44 days. The higher than average debtor turnover

may account for a part of the reason that there is a higher than average current ratio. The

improvement in the customer collection period has contributed to the change in the current

ratio from 2.33 the previous year to 2.25.

A limitation of this ratio is that it is a static measure, fixed point in time, and manipulated easily

to show favourable ratios. In addition, the receivable item in the financial statements influences

this ratio. As the collection period for receivables extends, the value of receivables increases

resulting in a higher current ratio. While this may show favourable liquidity, receivable defaults

could negatively affect the overall liquidity of ABC (Cagle et al. 2013).

In a comparison to the quick ratio, current ratio excluding inventory, we find that ABC remains in

a liquid state. The trend, as shown in fig 1, shows the two ratios have a stable trend over time.

Figure 1 ABC Liquidity ratios

Page | 2

short-term liabilities and provide an indicator of near future cash flow (O'Mara 2015), that is the

ability to meet short-term obligations (Vasiu et al. 2015). The current ratio is the result of

dividing current assets into current debts. A value below one represents current liabilities which

are higher than current assets and raises concern providing indication that inventory levels may

be excessive, borrowing power utilisation, or potential difficulties in operations (Vasiu et al.

2015). Vasiu, et al. (2015) states that although high levels of current ratio—current ratio above

two times—may not indicate critical issues, it is still an area of concern for the firm. Issues that

contribute to a higher current ratio includes poor customer collection, and low stock rotation.

The current ratio for ABC is 2.25 times, indicating a liquid financial position. In comparison to the

industry average of 1.64 we find that ABC’s liquidity is above the industry average in which it

operates. Inventory levels have grown 4.6% over the year while sales revenue has grown 5.7%

over the same time period, providing evidence that inventory is not contributing to a higher

current ratio. ABC has a debtors’ turnover of 41.52 days, down from 43.67 days for the previous

year, compared to an industry average of 40.44 days. The higher than average debtor turnover

may account for a part of the reason that there is a higher than average current ratio. The

improvement in the customer collection period has contributed to the change in the current

ratio from 2.33 the previous year to 2.25.

A limitation of this ratio is that it is a static measure, fixed point in time, and manipulated easily

to show favourable ratios. In addition, the receivable item in the financial statements influences

this ratio. As the collection period for receivables extends, the value of receivables increases

resulting in a higher current ratio. While this may show favourable liquidity, receivable defaults

could negatively affect the overall liquidity of ABC (Cagle et al. 2013).

In a comparison to the quick ratio, current ratio excluding inventory, we find that ABC remains in

a liquid state. The trend, as shown in fig 1, shows the two ratios have a stable trend over time.

Figure 1 ABC Liquidity ratios

Page | 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 1 Liquidity ratios

31-Dec-2015 31-Dec-2014 31-Dec-2013 31-Dec-2012 31-Dec-2011

Total Current Assets

(Refer Appendix 1) 403100 387,200 390,200 363,700 307,800

Total Current

Liabilities

(Refer Appendix 1)

179300 166,000 211,200 193,500 133,700

Inventory

(Refer Appendix 1) 161500 154,700 136,300 134,800 127,900

Current Ratio

(Calculated using

Appendix 1 values)

2.25 2.33 1.85 1.88 2.30

Quick ratio

(Calculated using

Appendix 1 values)

1.35 1.40 1.20 1.18 1.35

Formulas used for calculations:

Current Ratio= Current Assets

Current Liabilities

Quick Ratio= Current Assets−Inventory

Current Liabilities

2.2 Profitability: Net profit margin ratio and Return on total assets

Note: Unless otherwise stated, the values used are from Appendix 1.

Page | 3

31-Dec-2010 31-Dec-2011 31-Dec-2012 31-Dec-2013 31-Dec-2014 31-Dec-2015

1.72

2.30

1.88 1.85

2.33 2.25

0.98

1.35

1.18 1.20

1.40 1.34

Liquidity Ratios

Current Ratio Quick ratio

31-Dec-2015 31-Dec-2014 31-Dec-2013 31-Dec-2012 31-Dec-2011

Total Current Assets

(Refer Appendix 1) 403100 387,200 390,200 363,700 307,800

Total Current

Liabilities

(Refer Appendix 1)

179300 166,000 211,200 193,500 133,700

Inventory

(Refer Appendix 1) 161500 154,700 136,300 134,800 127,900

Current Ratio

(Calculated using

Appendix 1 values)

2.25 2.33 1.85 1.88 2.30

Quick ratio

(Calculated using

Appendix 1 values)

1.35 1.40 1.20 1.18 1.35

Formulas used for calculations:

Current Ratio= Current Assets

Current Liabilities

Quick Ratio= Current Assets−Inventory

Current Liabilities

2.2 Profitability: Net profit margin ratio and Return on total assets

Note: Unless otherwise stated, the values used are from Appendix 1.

Page | 3

31-Dec-2010 31-Dec-2011 31-Dec-2012 31-Dec-2013 31-Dec-2014 31-Dec-2015

1.72

2.30

1.88 1.85

2.33 2.25

0.98

1.35

1.18 1.20

1.40 1.34

Liquidity Ratios

Current Ratio Quick ratio

The net profit margin reflects the outcome of operations after all the costs incurred by the

business are considered and is calculated by dividing net profit into sales. The net profit margin

demonstrates the company’s effectiveness at controlling costs (Titman et al. 2016) and should be

viewed as part of a bigger picture. In addition to profit margin, analysis of the return on the

capital investment required to produce profits and revenues is required to demonstrate further

the profitability. The sustainable part of earning is of particular interest to investors and analysts

because estimated future earnings are the basis of equity value (Amir et al. 2013)—a premium

will be paid on sustainable earnings.

The return on assets (ROA) ratio combines cost control with asset usage and presents a measure

of operating profitability (Titman et al. 2016). The return on assets is calculated by dividing the

operating profit—earnings before interest and tax (EBIT)—by the total assets. Titman (2016)

decomposes this to show the cost control and asset utilisation components, presenting the

following equation:

Returnon Assets=Operating Profit Margin ×Total Asset Turnover

Where OPM represents cost control of the firm and TATO represents the asset utilisation of the

organisation.

The net profit margin for ABC is 14.7% up in 12.9% from 2014 and an industry average of 8.4%

indicates that ABC has a competitive advantage over the average industry. The return on assets

has grown from 9.5% for 2014 to 11.3% for 2015. Comparing the ROA for ABC against the

industry average of 5.18%, the indication is that ABC is utilising their assets more efficiently than

the industry average. ABC actively engages in activities to enhance and promote company

performance and efficiency, and continually look for opportunities to improve (Brydon 2015).

Both measures are above the industry average, indicating that ABC is profitable when looking

profits against sales and profits against assets. The indication is that ABC are able to control costs

in an efficient manner as well as make use of assets efficiently. The net profit margin has shown

positive values over the past five years, with growth in the net profit margin between December

2013 and December 2015.

Page | 4

business are considered and is calculated by dividing net profit into sales. The net profit margin

demonstrates the company’s effectiveness at controlling costs (Titman et al. 2016) and should be

viewed as part of a bigger picture. In addition to profit margin, analysis of the return on the

capital investment required to produce profits and revenues is required to demonstrate further

the profitability. The sustainable part of earning is of particular interest to investors and analysts

because estimated future earnings are the basis of equity value (Amir et al. 2013)—a premium

will be paid on sustainable earnings.

The return on assets (ROA) ratio combines cost control with asset usage and presents a measure

of operating profitability (Titman et al. 2016). The return on assets is calculated by dividing the

operating profit—earnings before interest and tax (EBIT)—by the total assets. Titman (2016)

decomposes this to show the cost control and asset utilisation components, presenting the

following equation:

Returnon Assets=Operating Profit Margin ×Total Asset Turnover

Where OPM represents cost control of the firm and TATO represents the asset utilisation of the

organisation.

The net profit margin for ABC is 14.7% up in 12.9% from 2014 and an industry average of 8.4%

indicates that ABC has a competitive advantage over the average industry. The return on assets

has grown from 9.5% for 2014 to 11.3% for 2015. Comparing the ROA for ABC against the

industry average of 5.18%, the indication is that ABC is utilising their assets more efficiently than

the industry average. ABC actively engages in activities to enhance and promote company

performance and efficiency, and continually look for opportunities to improve (Brydon 2015).

Both measures are above the industry average, indicating that ABC is profitable when looking

profits against sales and profits against assets. The indication is that ABC are able to control costs

in an efficient manner as well as make use of assets efficiently. The net profit margin has shown

positive values over the past five years, with growth in the net profit margin between December

2013 and December 2015.

Page | 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 2 Net profit margin ratio

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015

13.53%

12.97%

12.33%

12.93%

14.73%

Net Profit Margin Ratio

2.3 Capital structure: Debt ratio and Interest cover ratio

Note: Unless otherwise stated, the values used are from Appendix 1.

Capital structure refers to how an organisation finances operations through debt and equity

(Farlex Financial Dictionary n.d.), specifically the percentage of the overall financing attributed to

each type of financing. The first part of this is the debt ratio, the total debt compared to total

assets, which provides a measure of financing through borrowing or debt (Titman et al. 2016). A

value below 0.5 indicates assets predominantly financed through equity while greater than 0.5

indicates financing of assets through debt (Ready Ratios 2016). The debt ratio provides an

indication of the long-term solvency of the firm (Spears & Morris 1995) but should be considered

in relation to the business model. The debt ratio of IBM in 1993 was 0.76 and was largely

attributable to a consumer-financing subsidiary.

A word of caution here is that debt ratios do not always follow sound financial guidelines, but are

subject to manager’s individualism level. Managers with high individualism tend to be

overconfident and have high optimism, which creates a bias in the debt ratio (Antoncyzk &

Salzman 2014).

The interest cover ratio (ICR) can be defined as the extent to which a company can cover interest

payments and represents the number of times interest payment can be made using EBIT over

the reporting period (Ready Ratios 2016). While a high ratio indicates financial health, it may also

indicate that the organisation is overlooking investment and growth opportunities. An

influencing factor of the ICR is covenants imposed by major lenders which require a minimum

Page | 5

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015

13.53%

12.97%

12.33%

12.93%

14.73%

Net Profit Margin Ratio

2.3 Capital structure: Debt ratio and Interest cover ratio

Note: Unless otherwise stated, the values used are from Appendix 1.

Capital structure refers to how an organisation finances operations through debt and equity

(Farlex Financial Dictionary n.d.), specifically the percentage of the overall financing attributed to

each type of financing. The first part of this is the debt ratio, the total debt compared to total

assets, which provides a measure of financing through borrowing or debt (Titman et al. 2016). A

value below 0.5 indicates assets predominantly financed through equity while greater than 0.5

indicates financing of assets through debt (Ready Ratios 2016). The debt ratio provides an

indication of the long-term solvency of the firm (Spears & Morris 1995) but should be considered

in relation to the business model. The debt ratio of IBM in 1993 was 0.76 and was largely

attributable to a consumer-financing subsidiary.

A word of caution here is that debt ratios do not always follow sound financial guidelines, but are

subject to manager’s individualism level. Managers with high individualism tend to be

overconfident and have high optimism, which creates a bias in the debt ratio (Antoncyzk &

Salzman 2014).

The interest cover ratio (ICR) can be defined as the extent to which a company can cover interest

payments and represents the number of times interest payment can be made using EBIT over

the reporting period (Ready Ratios 2016). While a high ratio indicates financial health, it may also

indicate that the organisation is overlooking investment and growth opportunities. An

influencing factor of the ICR is covenants imposed by major lenders which require a minimum

Page | 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

level ICR be maintained by the firm resulting in the reduction of optimal leverage and lowers

distress costs (Dothan 2006).

The debt ratio for ABC indicates that 34.33% of assets are financed through debt, compared to

an industry average of 44.81%. This indicates that ABC has sufficient assets to support additional

borrowings for growth. In considering this position, the capability of ABC to cover interest

payments should be assessed. The interest cover rates for ABC is 20.70 times, well above the

industry average of 7.81 times. The higher than average ratio provides evidence that ABC is

capable of meeting interest payments easily.

2.4 Market value: Price-earning (P/E) ratio.

Note: Unless otherwise stated, the values used are from Appendix 1.

The price-earning (P/E) ratio is a widely used as a stock valuation measure and calculated by the

share price divided by the earnings per share. The P/E ratio is an expression of the value of

shares in relative terms, price per dollar earned, which allows us to compare various shares

(Titman et al. 2016). The variation between P/E ratios and shares can vary widely, attributable to

the risk and expected growth of the individual firms (Titman et al. 2016). Shares can be

evaluated using the P/E ratio at current market prices or alternatively calculated future value

using require P/E and estimated future earnings. The price assessed in this analysis is the daily

close price for the share. Other prices that are used include the opening price, daily high price

and daily low price.

The measure of the P/E ratio has been shown to provide an indication of real return over the

following 10 years (Weigand & Irons 2007). Siegel, cited in Weiand & Irons (2007), states that

high P/E ratios, due to earning decline, result in real return on equities average around 9.7% per

annum for the following five years. In contrast, high P/E ratios due to rising share prices display a

real return average of only 1.1%. Values between 20 and 25 for the P/E ratio are considered high

(Weigand & Irons 2007).

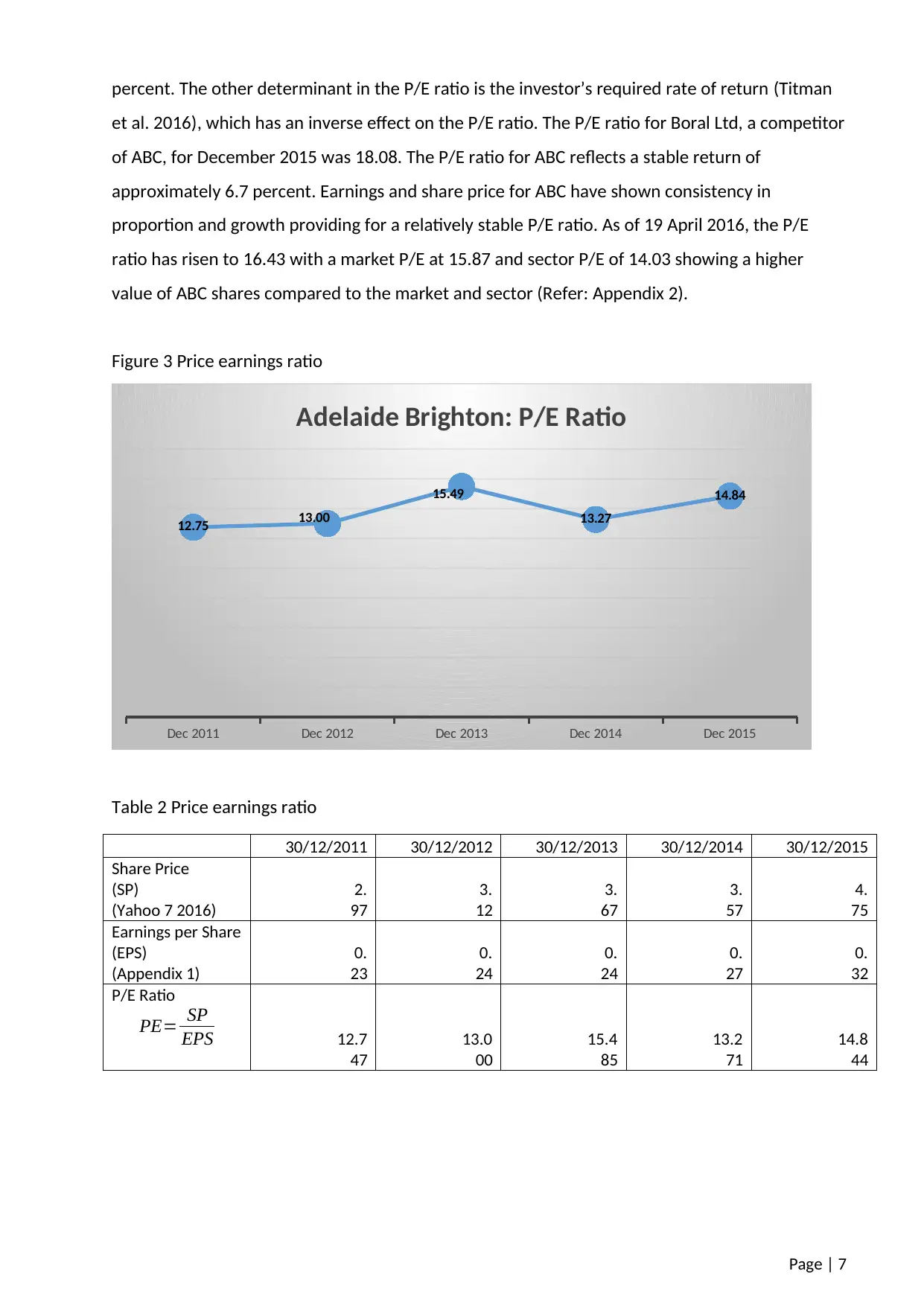

The P/E ratio for ABC as at 31 December 2015 was 14.84, with a minimum of 12.75 and

maximum of 15.49 for the period December 2011 to December 2015. The growth of dividends is

a contributor towards a higher P/E ratio (Titman et al. 2016). ABC have consistently paid

dividends over the past five years, however the growth of dividends has remained at zero

Page | 6

distress costs (Dothan 2006).

The debt ratio for ABC indicates that 34.33% of assets are financed through debt, compared to

an industry average of 44.81%. This indicates that ABC has sufficient assets to support additional

borrowings for growth. In considering this position, the capability of ABC to cover interest

payments should be assessed. The interest cover rates for ABC is 20.70 times, well above the

industry average of 7.81 times. The higher than average ratio provides evidence that ABC is

capable of meeting interest payments easily.

2.4 Market value: Price-earning (P/E) ratio.

Note: Unless otherwise stated, the values used are from Appendix 1.

The price-earning (P/E) ratio is a widely used as a stock valuation measure and calculated by the

share price divided by the earnings per share. The P/E ratio is an expression of the value of

shares in relative terms, price per dollar earned, which allows us to compare various shares

(Titman et al. 2016). The variation between P/E ratios and shares can vary widely, attributable to

the risk and expected growth of the individual firms (Titman et al. 2016). Shares can be

evaluated using the P/E ratio at current market prices or alternatively calculated future value

using require P/E and estimated future earnings. The price assessed in this analysis is the daily

close price for the share. Other prices that are used include the opening price, daily high price

and daily low price.

The measure of the P/E ratio has been shown to provide an indication of real return over the

following 10 years (Weigand & Irons 2007). Siegel, cited in Weiand & Irons (2007), states that

high P/E ratios, due to earning decline, result in real return on equities average around 9.7% per

annum for the following five years. In contrast, high P/E ratios due to rising share prices display a

real return average of only 1.1%. Values between 20 and 25 for the P/E ratio are considered high

(Weigand & Irons 2007).

The P/E ratio for ABC as at 31 December 2015 was 14.84, with a minimum of 12.75 and

maximum of 15.49 for the period December 2011 to December 2015. The growth of dividends is

a contributor towards a higher P/E ratio (Titman et al. 2016). ABC have consistently paid

dividends over the past five years, however the growth of dividends has remained at zero

Page | 6

percent. The other determinant in the P/E ratio is the investor’s required rate of return (Titman

et al. 2016), which has an inverse effect on the P/E ratio. The P/E ratio for Boral Ltd, a competitor

of ABC, for December 2015 was 18.08. The P/E ratio for ABC reflects a stable return of

approximately 6.7 percent. Earnings and share price for ABC have shown consistency in

proportion and growth providing for a relatively stable P/E ratio. As of 19 April 2016, the P/E

ratio has risen to 16.43 with a market P/E at 15.87 and sector P/E of 14.03 showing a higher

value of ABC shares compared to the market and sector (Refer: Appendix 2).

Figure 3 Price earnings ratio

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015

12.75 13.00

15.49

13.27

14.84

Adelaide Brighton: P/E Ratio

Table 2 Price earnings ratio

30/12/2011 30/12/2012 30/12/2013 30/12/2014 30/12/2015

Share Price

(SP)

(Yahoo 7 2016)

2.

97

3.

12

3.

67

3.

57

4.

75

Earnings per Share

(EPS)

(Appendix 1)

0.

23

0.

24

0.

24

0.

27

0.

32

P/E Ratio

PE= SP

EPS 12.7

47

13.0

00

15.4

85

13.2

71

14.8

44

Page | 7

et al. 2016), which has an inverse effect on the P/E ratio. The P/E ratio for Boral Ltd, a competitor

of ABC, for December 2015 was 18.08. The P/E ratio for ABC reflects a stable return of

approximately 6.7 percent. Earnings and share price for ABC have shown consistency in

proportion and growth providing for a relatively stable P/E ratio. As of 19 April 2016, the P/E

ratio has risen to 16.43 with a market P/E at 15.87 and sector P/E of 14.03 showing a higher

value of ABC shares compared to the market and sector (Refer: Appendix 2).

Figure 3 Price earnings ratio

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015

12.75 13.00

15.49

13.27

14.84

Adelaide Brighton: P/E Ratio

Table 2 Price earnings ratio

30/12/2011 30/12/2012 30/12/2013 30/12/2014 30/12/2015

Share Price

(SP)

(Yahoo 7 2016)

2.

97

3.

12

3.

67

3.

57

4.

75

Earnings per Share

(EPS)

(Appendix 1)

0.

23

0.

24

0.

24

0.

27

0.

32

P/E Ratio

PE= SP

EPS 12.7

47

13.0

00

15.4

85

13.2

71

14.8

44

Page | 7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Share Valuation - Constant Dividend Discount Model

The constant dividend discount model (CDDM) is a way of valuing a share based on the expected

future divided using the investor’s required rate of return, as there is no promise of dividend

(Titman et al. 2016). The model is sensitive to both the expected rate of return selected and the

expected growth rate and that the expected rate of return should be larger than the growth rate

(Payne & Finch 1999). The CDDM is represented using the formula:

V E= ¿1

RE−g

VE = Ordinary share value

Div1 = Dividend after 1 year (Most recent dividend increased by growth rate)

RE = Required rate of return

G = Growth rate

In terms of ABC, the most recent dividend is 0.19c per share, the required rate of return is nine

percent and the expected dividend growth rate is four percent.

V E= 0.19(1+ 4 %)

9 %−4 % =3.95

This provides us with a share value of $3.95. Comparing this to the value of ABC shares at 31

December 2015 (date of financial results) and current share value as at 18 April 2016, which

were $4.60 and $5.08 respectively, we find that the share is trading above our estimated value.

Given the expectations of dividend growth rate and required rate of return, purchasing the share

above the $3.95 level would not support a required rate of return of nine percent. Hence the

share is considered to be over-valued given the parameters and a no-go for investing. While

there has been a dividend growth over the past year of approximately 15%, the past five years

growth rate has been negative further supporting the no-go for investing.

Page | 8

The constant dividend discount model (CDDM) is a way of valuing a share based on the expected

future divided using the investor’s required rate of return, as there is no promise of dividend

(Titman et al. 2016). The model is sensitive to both the expected rate of return selected and the

expected growth rate and that the expected rate of return should be larger than the growth rate

(Payne & Finch 1999). The CDDM is represented using the formula:

V E= ¿1

RE−g

VE = Ordinary share value

Div1 = Dividend after 1 year (Most recent dividend increased by growth rate)

RE = Required rate of return

G = Growth rate

In terms of ABC, the most recent dividend is 0.19c per share, the required rate of return is nine

percent and the expected dividend growth rate is four percent.

V E= 0.19(1+ 4 %)

9 %−4 % =3.95

This provides us with a share value of $3.95. Comparing this to the value of ABC shares at 31

December 2015 (date of financial results) and current share value as at 18 April 2016, which

were $4.60 and $5.08 respectively, we find that the share is trading above our estimated value.

Given the expectations of dividend growth rate and required rate of return, purchasing the share

above the $3.95 level would not support a required rate of return of nine percent. Hence the

share is considered to be over-valued given the parameters and a no-go for investing. While

there has been a dividend growth over the past year of approximately 15%, the past five years

growth rate has been negative further supporting the no-go for investing.

Page | 8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 4 Share price and dividend

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015

2.97 3.12

3.67 3.57

4.75

0.21 0.19 0.16 0.16 0.19

Share Price and Dividend per share

Share Price Dividend

Figure 5 Weekly average share price

12/1/2011

1/26/2012

3/22/2012

5/17/2012

7/12/2012

9/6/2012

11/1/2012

12/27/2012

2/21/2013

4/18/2013

6/13/2013

8/8/2013

10/3/2013

11/28/2013

1/23/2014

3/20/2014

5/15/2014

7/10/2014

9/4/2014

10/30/2014

12/25/2014

2/19/2015

4/16/2015

6/11/2015

8/6/2015

10/1/2015

11/26/2015

1/21/2016

3/17/2016

2.5

3

3.5

4

4.5

5

5.5

Weekly Share Price

Page | 9

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015

2.97 3.12

3.67 3.57

4.75

0.21 0.19 0.16 0.16 0.19

Share Price and Dividend per share

Share Price Dividend

Figure 5 Weekly average share price

12/1/2011

1/26/2012

3/22/2012

5/17/2012

7/12/2012

9/6/2012

11/1/2012

12/27/2012

2/21/2013

4/18/2013

6/13/2013

8/8/2013

10/3/2013

11/28/2013

1/23/2014

3/20/2014

5/15/2014

7/10/2014

9/4/2014

10/30/2014

12/25/2014

2/19/2015

4/16/2015

6/11/2015

8/6/2015

10/1/2015

11/26/2015

1/21/2016

3/17/2016

2.5

3

3.5

4

4.5

5

5.5

Weekly Share Price

Page | 9

4. Recommendation

Adelaide Brighton is in a liquid position showing a current ratio of 2.25, and is in a position to

support the vertical integration strategy (Brydon 2015). Although there have been some land

sales totalling AUD 48 million, there has also been investment in operations and the purchase of

additional quarries. The outlook from a liquidity perspective is positive and supports an

investment decision from a liquidity perspective.

The above industry net profit margin and an increase in the return on assets supports the

statement in the annual general meeting report that ABC have invested in making operations

more efficient (Brydon 2015). ABC have engaged in a strategy of vertical integration (Brydon

2015), providing improved returns while keeping asset and liability variations to a minimum. ABC

retains a competitive advantage in the industry with efficient use of assts. A decision to invest

based on a profitability perspective is supported by the net profit margin and return on assets.

The capital structure reflects financing that has an equity bias. There is potential for additional

growth of the company through debt financing. The interest cover ratio adequately provides for

existing interest payments and can further service additional debt. The capital structure of ABC

further supports investment decision from a capital growth perspective in the long term.

The share market is a reflection of the overall performance of the firm and the perception of risk

in the firm by investors. The P/E ratio for ABC has remained consistent over the past five years

with a variance of 1.19 indicating stability in earnings and price growth with static risk

assessment. Investment from market perspective is that ABC is suited to long term investment

with predictable dividends and stable growth with low risk. Note that short term (less than three

years) investing shows little correlation between the P/E ratio and average returns, with long

term (five or more years) showing lower returns when P/E ratios are high (Trevino & Robertson

2002). This supports a long term investment strategy in ABC.

The CDDM provides a level of share value given the expectations of share and company

performance in terms of dividend payout. The share value calculated using CDDM is below the

market value and thus the final recommendation would be to not invest in Adelaide Brighton

Ltd.

Page | 10

Adelaide Brighton is in a liquid position showing a current ratio of 2.25, and is in a position to

support the vertical integration strategy (Brydon 2015). Although there have been some land

sales totalling AUD 48 million, there has also been investment in operations and the purchase of

additional quarries. The outlook from a liquidity perspective is positive and supports an

investment decision from a liquidity perspective.

The above industry net profit margin and an increase in the return on assets supports the

statement in the annual general meeting report that ABC have invested in making operations

more efficient (Brydon 2015). ABC have engaged in a strategy of vertical integration (Brydon

2015), providing improved returns while keeping asset and liability variations to a minimum. ABC

retains a competitive advantage in the industry with efficient use of assts. A decision to invest

based on a profitability perspective is supported by the net profit margin and return on assets.

The capital structure reflects financing that has an equity bias. There is potential for additional

growth of the company through debt financing. The interest cover ratio adequately provides for

existing interest payments and can further service additional debt. The capital structure of ABC

further supports investment decision from a capital growth perspective in the long term.

The share market is a reflection of the overall performance of the firm and the perception of risk

in the firm by investors. The P/E ratio for ABC has remained consistent over the past five years

with a variance of 1.19 indicating stability in earnings and price growth with static risk

assessment. Investment from market perspective is that ABC is suited to long term investment

with predictable dividends and stable growth with low risk. Note that short term (less than three

years) investing shows little correlation between the P/E ratio and average returns, with long

term (five or more years) showing lower returns when P/E ratios are high (Trevino & Robertson

2002). This supports a long term investment strategy in ABC.

The CDDM provides a level of share value given the expectations of share and company

performance in terms of dividend payout. The share value calculated using CDDM is below the

market value and thus the final recommendation would be to not invest in Adelaide Brighton

Ltd.

Page | 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.