Comprehensive Financial Performance Analysis of Small Businesses

VerifiedAdded on 2020/01/23

|8

|2239

|212

Report

AI Summary

This report presents a comprehensive financial analysis of small businesses, focusing on key performance indicators and financial ratios. The analysis includes profitability ratios (gross profit, net profit, return on equity, and return on assets), an assessment of internal financing, and an examination of accounts receivable and inventory turnover. The report evaluates the liquidity of a firm by calculating the current ratio and interprets the results of TUST Ply Ltd for 2012 and 2013. A case study analysis compares the financial performance of Qantas Airways and Virgin Australia Holdings, examining EBIT margin, ROE, ROA, debt-to-equity ratio, current ratio, and net profit margin. The report uses financial data and ratios to assess the financial health, efficiency, and performance of the businesses, and to provide insights into their financial strategies.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Small Business Analysis 1...............................................................................................................3

(A) Profitability ratios..................................................................................................................3

(B) Extent to which internal sources have been used to finance asset acquisitions....................4

© Find out rapidity with which accounts receivable are collected..............................................4

(D) Measure the ability of the entity to meet unexpected demands for working capital.............4

(E) Compute the length of time taken by the entity to sell its inventories..................................5

Small Business Analysis 2...............................................................................................................5

Small Business Analysis 3: Case Study Analysis............................................................................6

Table 1Calculation of profitability ratio..........................................................................................3

Table 2 Calculation of ROCE..........................................................................................................4

Table 3 Calculation of debtor turnover ratio...................................................................................4

Table 4 Calculation of current ratio.................................................................................................4

Table 5 Calculation of inventory turnover ratio..............................................................................5

Table 6 Ratios of TUST Ply Ltd for 2012 and 2013.......................................................................5

Table 7Ratios of Virgin holding and Quanta’s airlines...................................................................6

Small Business Analysis 1...............................................................................................................3

(A) Profitability ratios..................................................................................................................3

(B) Extent to which internal sources have been used to finance asset acquisitions....................4

© Find out rapidity with which accounts receivable are collected..............................................4

(D) Measure the ability of the entity to meet unexpected demands for working capital.............4

(E) Compute the length of time taken by the entity to sell its inventories..................................5

Small Business Analysis 2...............................................................................................................5

Small Business Analysis 3: Case Study Analysis............................................................................6

Table 1Calculation of profitability ratio..........................................................................................3

Table 2 Calculation of ROCE..........................................................................................................4

Table 3 Calculation of debtor turnover ratio...................................................................................4

Table 4 Calculation of current ratio.................................................................................................4

Table 5 Calculation of inventory turnover ratio..............................................................................5

Table 6 Ratios of TUST Ply Ltd for 2012 and 2013.......................................................................5

Table 7Ratios of Virgin holding and Quanta’s airlines...................................................................6

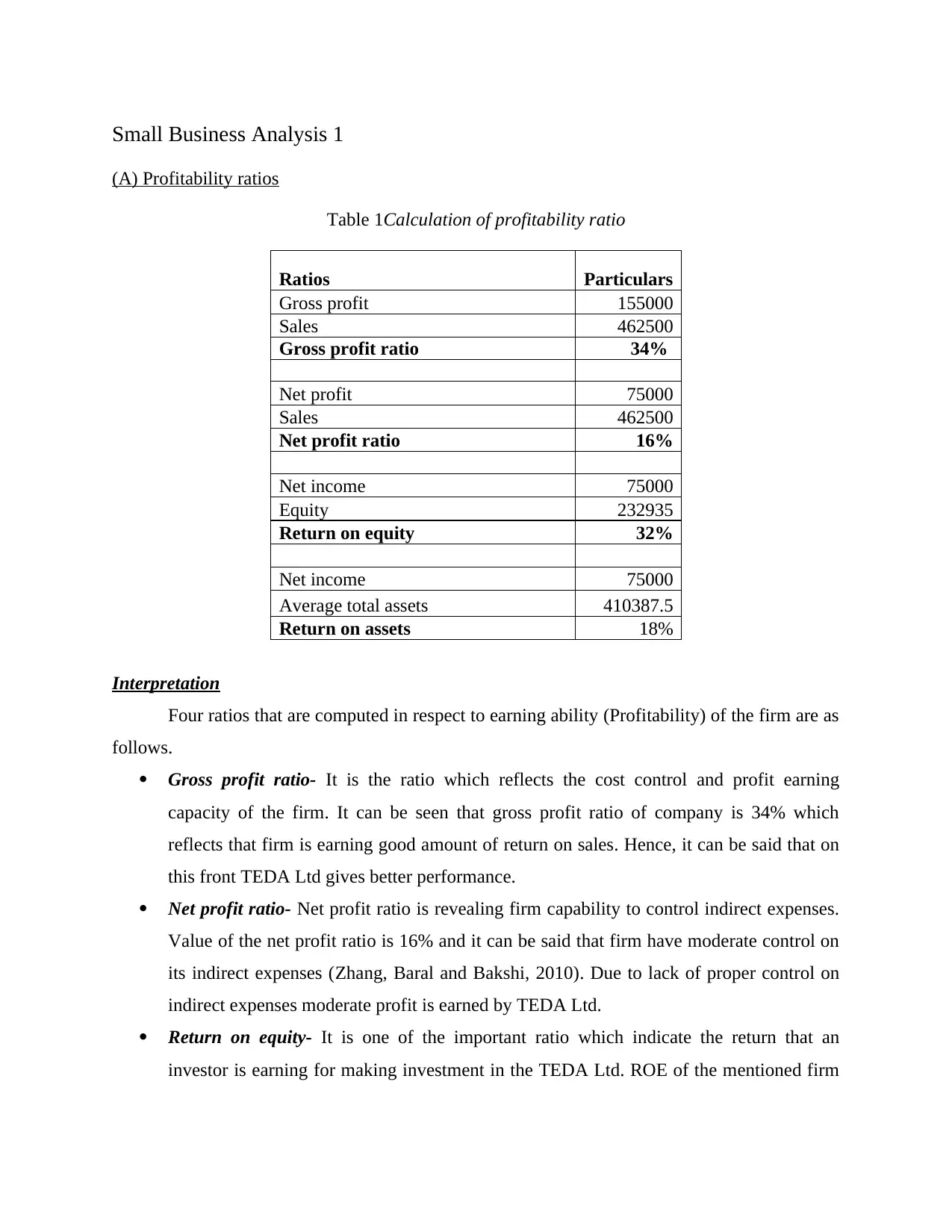

Small Business Analysis 1

(A) Profitability ratios

Table 1Calculation of profitability ratio

Ratios Particulars

Gross profit 155000

Sales 462500

Gross profit ratio 34%

Net profit 75000

Sales 462500

Net profit ratio 16%

Net income 75000

Equity 232935

Return on equity 32%

Net income 75000

Average total assets 410387.5

Return on assets 18%

Interpretation

Four ratios that are computed in respect to earning ability (Profitability) of the firm are as

follows.

Gross profit ratio- It is the ratio which reflects the cost control and profit earning

capacity of the firm. It can be seen that gross profit ratio of company is 34% which

reflects that firm is earning good amount of return on sales. Hence, it can be said that on

this front TEDA Ltd gives better performance.

Net profit ratio- Net profit ratio is revealing firm capability to control indirect expenses.

Value of the net profit ratio is 16% and it can be said that firm have moderate control on

its indirect expenses (Zhang, Baral and Bakshi, 2010). Due to lack of proper control on

indirect expenses moderate profit is earned by TEDA Ltd.

Return on equity- It is one of the important ratio which indicate the return that an

investor is earning for making investment in the TEDA Ltd. ROE of the mentioned firm

(A) Profitability ratios

Table 1Calculation of profitability ratio

Ratios Particulars

Gross profit 155000

Sales 462500

Gross profit ratio 34%

Net profit 75000

Sales 462500

Net profit ratio 16%

Net income 75000

Equity 232935

Return on equity 32%

Net income 75000

Average total assets 410387.5

Return on assets 18%

Interpretation

Four ratios that are computed in respect to earning ability (Profitability) of the firm are as

follows.

Gross profit ratio- It is the ratio which reflects the cost control and profit earning

capacity of the firm. It can be seen that gross profit ratio of company is 34% which

reflects that firm is earning good amount of return on sales. Hence, it can be said that on

this front TEDA Ltd gives better performance.

Net profit ratio- Net profit ratio is revealing firm capability to control indirect expenses.

Value of the net profit ratio is 16% and it can be said that firm have moderate control on

its indirect expenses (Zhang, Baral and Bakshi, 2010). Due to lack of proper control on

indirect expenses moderate profit is earned by TEDA Ltd.

Return on equity- It is one of the important ratio which indicate the return that an

investor is earning for making investment in the TEDA Ltd. ROE of the mentioned firm

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is 32% and it can be said that it gives good performance in its business. Control on

expenses is one of the main reason that contribute to mentioned sort of performance.

Return on assets- It is another ratio that is used to measure firm revenue earning

capacity. ROA of the firm is 18% which is low in the business. It can be said that TEDA

Ltd is not making proper use of assets and due to this reason less return is generated on

assets.

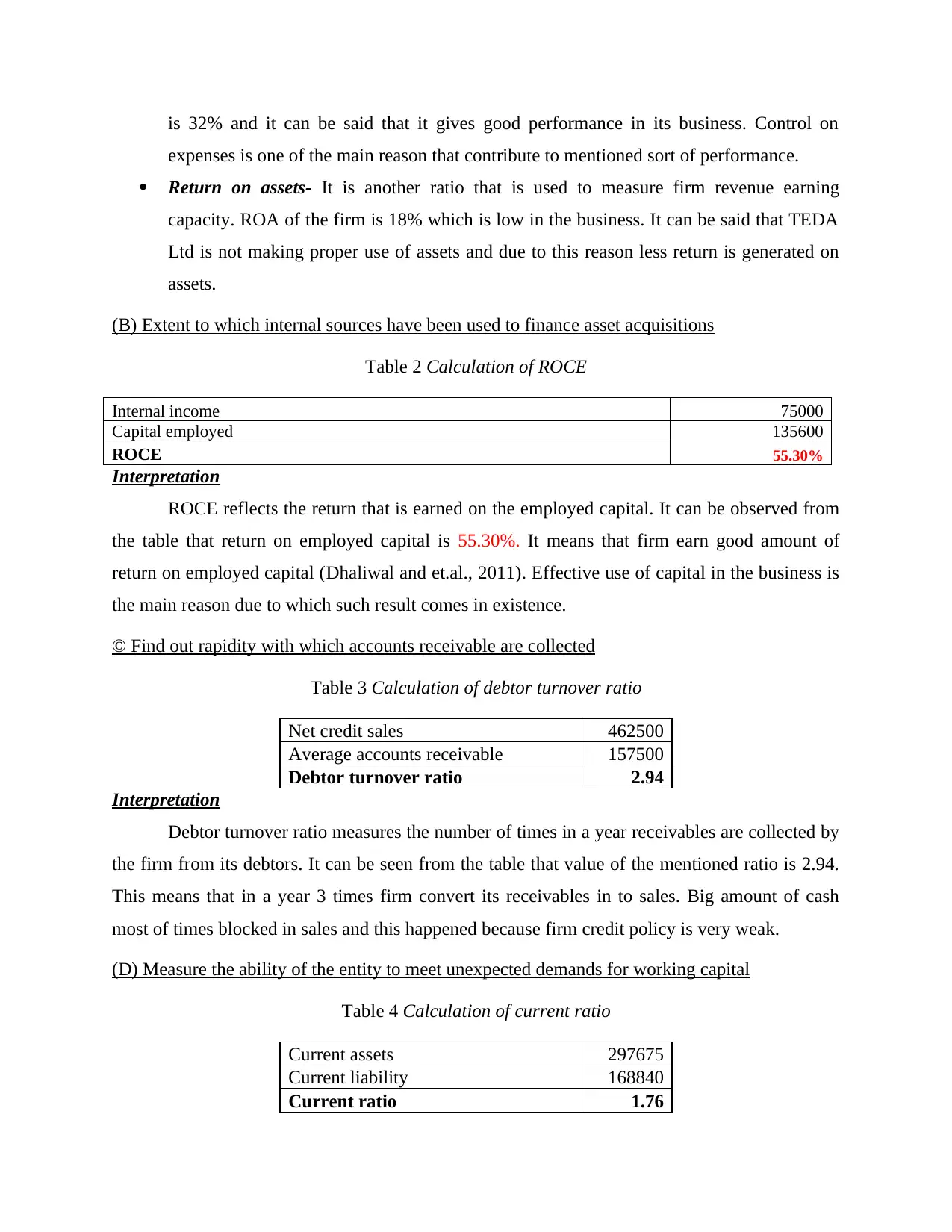

(B) Extent to which internal sources have been used to finance asset acquisitions

Table 2 Calculation of ROCE

Internal income 75000

Capital employed 135600

ROCE 55.30%

Interpretation

ROCE reflects the return that is earned on the employed capital. It can be observed from

the table that return on employed capital is 55.30%. It means that firm earn good amount of

return on employed capital (Dhaliwal and et.al., 2011). Effective use of capital in the business is

the main reason due to which such result comes in existence.

© Find out rapidity with which accounts receivable are collected

Table 3 Calculation of debtor turnover ratio

Net credit sales 462500

Average accounts receivable 157500

Debtor turnover ratio 2.94

Interpretation

Debtor turnover ratio measures the number of times in a year receivables are collected by

the firm from its debtors. It can be seen from the table that value of the mentioned ratio is 2.94.

This means that in a year 3 times firm convert its receivables in to sales. Big amount of cash

most of times blocked in sales and this happened because firm credit policy is very weak.

(D) Measure the ability of the entity to meet unexpected demands for working capital

Table 4 Calculation of current ratio

Current assets 297675

Current liability 168840

Current ratio 1.76

expenses is one of the main reason that contribute to mentioned sort of performance.

Return on assets- It is another ratio that is used to measure firm revenue earning

capacity. ROA of the firm is 18% which is low in the business. It can be said that TEDA

Ltd is not making proper use of assets and due to this reason less return is generated on

assets.

(B) Extent to which internal sources have been used to finance asset acquisitions

Table 2 Calculation of ROCE

Internal income 75000

Capital employed 135600

ROCE 55.30%

Interpretation

ROCE reflects the return that is earned on the employed capital. It can be observed from

the table that return on employed capital is 55.30%. It means that firm earn good amount of

return on employed capital (Dhaliwal and et.al., 2011). Effective use of capital in the business is

the main reason due to which such result comes in existence.

© Find out rapidity with which accounts receivable are collected

Table 3 Calculation of debtor turnover ratio

Net credit sales 462500

Average accounts receivable 157500

Debtor turnover ratio 2.94

Interpretation

Debtor turnover ratio measures the number of times in a year receivables are collected by

the firm from its debtors. It can be seen from the table that value of the mentioned ratio is 2.94.

This means that in a year 3 times firm convert its receivables in to sales. Big amount of cash

most of times blocked in sales and this happened because firm credit policy is very weak.

(D) Measure the ability of the entity to meet unexpected demands for working capital

Table 4 Calculation of current ratio

Current assets 297675

Current liability 168840

Current ratio 1.76

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

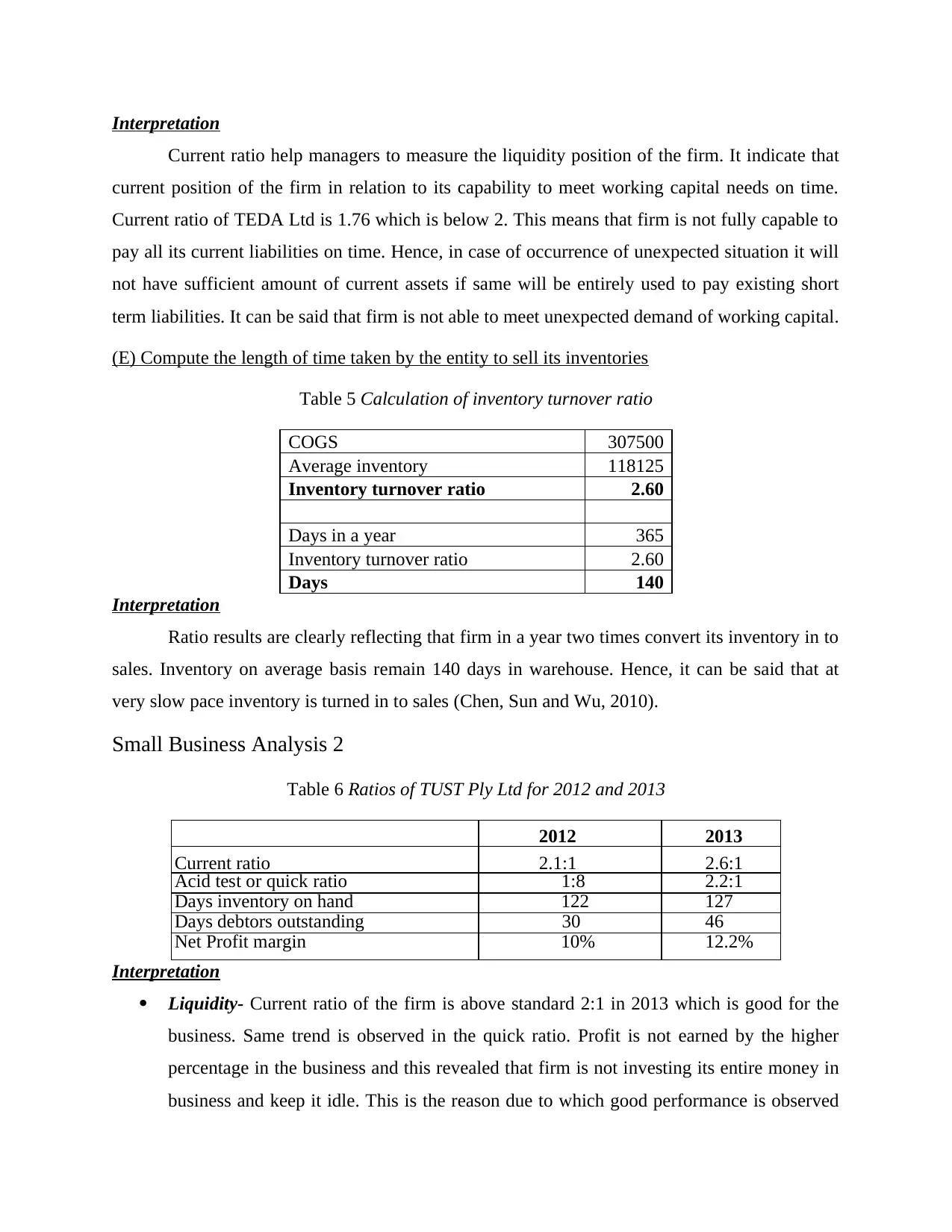

Interpretation

Current ratio help managers to measure the liquidity position of the firm. It indicate that

current position of the firm in relation to its capability to meet working capital needs on time.

Current ratio of TEDA Ltd is 1.76 which is below 2. This means that firm is not fully capable to

pay all its current liabilities on time. Hence, in case of occurrence of unexpected situation it will

not have sufficient amount of current assets if same will be entirely used to pay existing short

term liabilities. It can be said that firm is not able to meet unexpected demand of working capital.

(E) Compute the length of time taken by the entity to sell its inventories

Table 5 Calculation of inventory turnover ratio

COGS 307500

Average inventory 118125

Inventory turnover ratio 2.60

Days in a year 365

Inventory turnover ratio 2.60

Days 140

Interpretation

Ratio results are clearly reflecting that firm in a year two times convert its inventory in to

sales. Inventory on average basis remain 140 days in warehouse. Hence, it can be said that at

very slow pace inventory is turned in to sales (Chen, Sun and Wu, 2010).

Small Business Analysis 2

Table 6 Ratios of TUST Ply Ltd for 2012 and 2013

2012 2013

Current ratio 2.1:1 2.6:1

Acid test or quick ratio 1:8 2.2:1

Days inventory on hand 122 127

Days debtors outstanding 30 46

Net Profit margin 10% 12.2%

Interpretation

Liquidity- Current ratio of the firm is above standard 2:1 in 2013 which is good for the

business. Same trend is observed in the quick ratio. Profit is not earned by the higher

percentage in the business and this revealed that firm is not investing its entire money in

business and keep it idle. This is the reason due to which good performance is observed

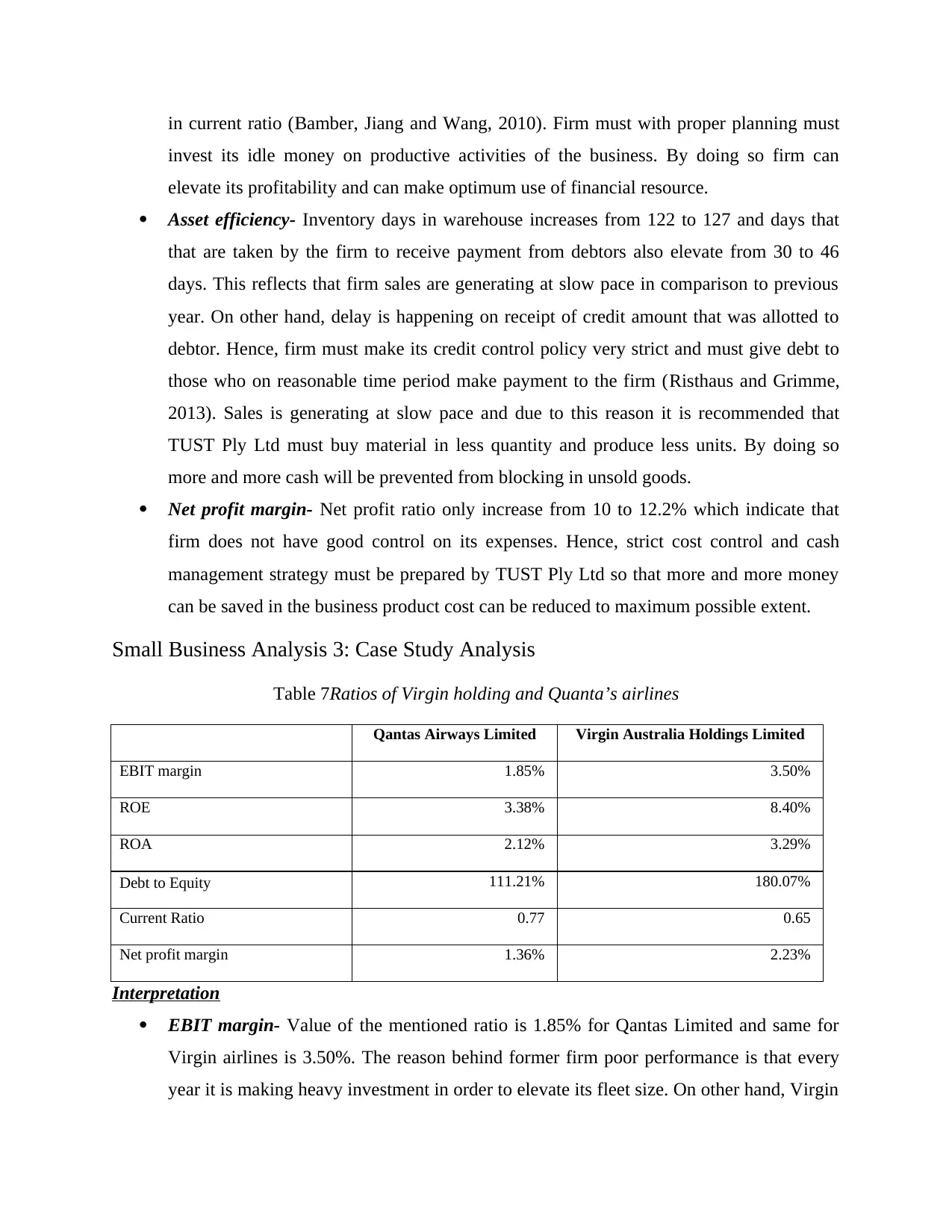

Current ratio help managers to measure the liquidity position of the firm. It indicate that

current position of the firm in relation to its capability to meet working capital needs on time.

Current ratio of TEDA Ltd is 1.76 which is below 2. This means that firm is not fully capable to

pay all its current liabilities on time. Hence, in case of occurrence of unexpected situation it will

not have sufficient amount of current assets if same will be entirely used to pay existing short

term liabilities. It can be said that firm is not able to meet unexpected demand of working capital.

(E) Compute the length of time taken by the entity to sell its inventories

Table 5 Calculation of inventory turnover ratio

COGS 307500

Average inventory 118125

Inventory turnover ratio 2.60

Days in a year 365

Inventory turnover ratio 2.60

Days 140

Interpretation

Ratio results are clearly reflecting that firm in a year two times convert its inventory in to

sales. Inventory on average basis remain 140 days in warehouse. Hence, it can be said that at

very slow pace inventory is turned in to sales (Chen, Sun and Wu, 2010).

Small Business Analysis 2

Table 6 Ratios of TUST Ply Ltd for 2012 and 2013

2012 2013

Current ratio 2.1:1 2.6:1

Acid test or quick ratio 1:8 2.2:1

Days inventory on hand 122 127

Days debtors outstanding 30 46

Net Profit margin 10% 12.2%

Interpretation

Liquidity- Current ratio of the firm is above standard 2:1 in 2013 which is good for the

business. Same trend is observed in the quick ratio. Profit is not earned by the higher

percentage in the business and this revealed that firm is not investing its entire money in

business and keep it idle. This is the reason due to which good performance is observed

in current ratio (Bamber, Jiang and Wang, 2010). Firm must with proper planning must

invest its idle money on productive activities of the business. By doing so firm can

elevate its profitability and can make optimum use of financial resource.

Asset efficiency- Inventory days in warehouse increases from 122 to 127 and days that

that are taken by the firm to receive payment from debtors also elevate from 30 to 46

days. This reflects that firm sales are generating at slow pace in comparison to previous

year. On other hand, delay is happening on receipt of credit amount that was allotted to

debtor. Hence, firm must make its credit control policy very strict and must give debt to

those who on reasonable time period make payment to the firm (Risthaus and Grimme,

2013). Sales is generating at slow pace and due to this reason it is recommended that

TUST Ply Ltd must buy material in less quantity and produce less units. By doing so

more and more cash will be prevented from blocking in unsold goods.

Net profit margin- Net profit ratio only increase from 10 to 12.2% which indicate that

firm does not have good control on its expenses. Hence, strict cost control and cash

management strategy must be prepared by TUST Ply Ltd so that more and more money

can be saved in the business product cost can be reduced to maximum possible extent.

Small Business Analysis 3: Case Study Analysis

Table 7Ratios of Virgin holding and Quanta’s airlines

Qantas Airways Limited Virgin Australia Holdings Limited

EBIT margin 1.85% 3.50%

ROE 3.38% 8.40%

ROA 2.12% 3.29%

Debt to Equity 111.21% 180.07%

Current Ratio 0.77 0.65

Net profit margin 1.36% 2.23%

Interpretation

EBIT margin- Value of the mentioned ratio is 1.85% for Qantas Limited and same for

Virgin airlines is 3.50%. The reason behind former firm poor performance is that every

year it is making heavy investment in order to elevate its fleet size. On other hand, Virgin

invest its idle money on productive activities of the business. By doing so firm can

elevate its profitability and can make optimum use of financial resource.

Asset efficiency- Inventory days in warehouse increases from 122 to 127 and days that

that are taken by the firm to receive payment from debtors also elevate from 30 to 46

days. This reflects that firm sales are generating at slow pace in comparison to previous

year. On other hand, delay is happening on receipt of credit amount that was allotted to

debtor. Hence, firm must make its credit control policy very strict and must give debt to

those who on reasonable time period make payment to the firm (Risthaus and Grimme,

2013). Sales is generating at slow pace and due to this reason it is recommended that

TUST Ply Ltd must buy material in less quantity and produce less units. By doing so

more and more cash will be prevented from blocking in unsold goods.

Net profit margin- Net profit ratio only increase from 10 to 12.2% which indicate that

firm does not have good control on its expenses. Hence, strict cost control and cash

management strategy must be prepared by TUST Ply Ltd so that more and more money

can be saved in the business product cost can be reduced to maximum possible extent.

Small Business Analysis 3: Case Study Analysis

Table 7Ratios of Virgin holding and Quanta’s airlines

Qantas Airways Limited Virgin Australia Holdings Limited

EBIT margin 1.85% 3.50%

ROE 3.38% 8.40%

ROA 2.12% 3.29%

Debt to Equity 111.21% 180.07%

Current Ratio 0.77 0.65

Net profit margin 1.36% 2.23%

Interpretation

EBIT margin- Value of the mentioned ratio is 1.85% for Qantas Limited and same for

Virgin airlines is 3.50%. The reason behind former firm poor performance is that every

year it is making heavy investment in order to elevate its fleet size. On other hand, Virgin

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

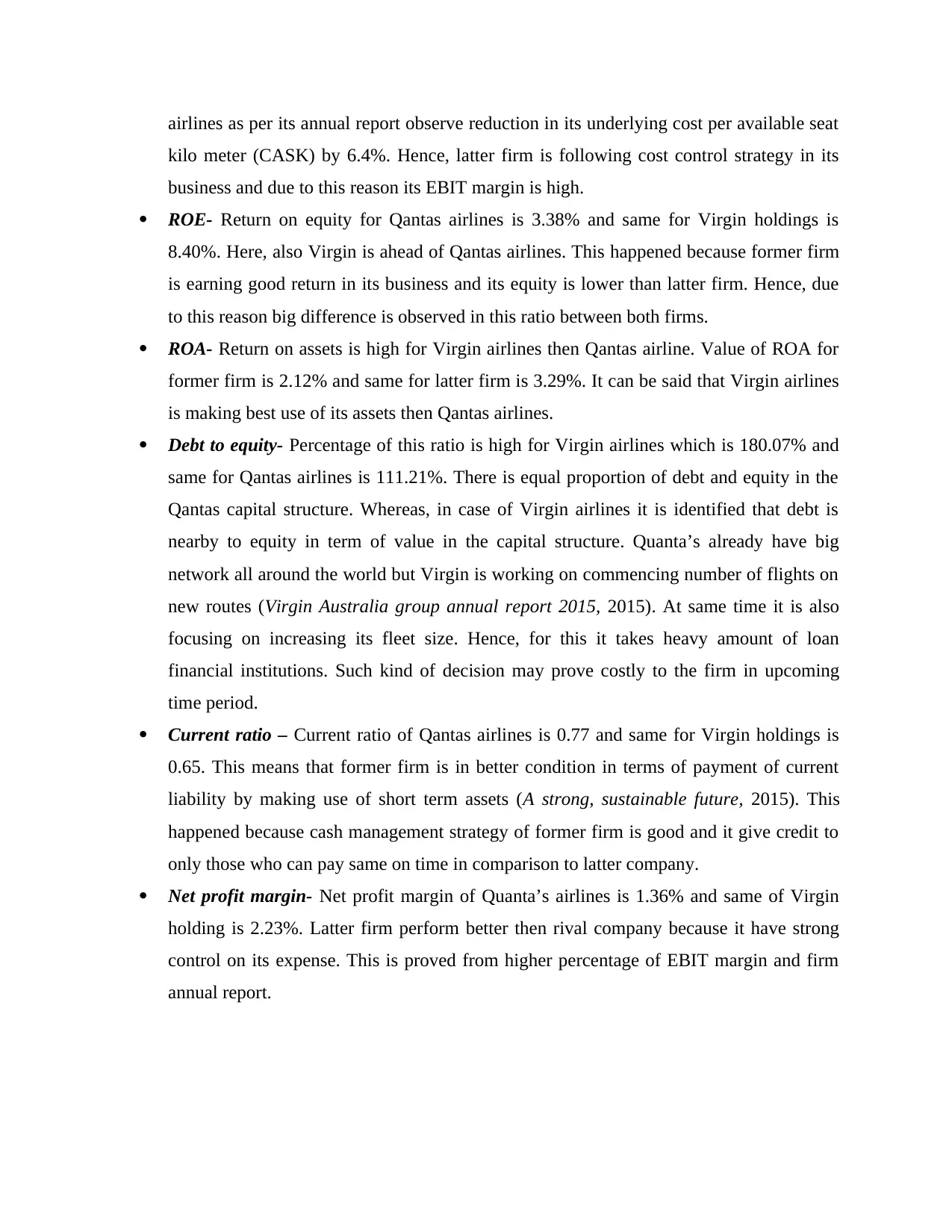

airlines as per its annual report observe reduction in its underlying cost per available seat

kilo meter (CASK) by 6.4%. Hence, latter firm is following cost control strategy in its

business and due to this reason its EBIT margin is high.

ROE- Return on equity for Qantas airlines is 3.38% and same for Virgin holdings is

8.40%. Here, also Virgin is ahead of Qantas airlines. This happened because former firm

is earning good return in its business and its equity is lower than latter firm. Hence, due

to this reason big difference is observed in this ratio between both firms.

ROA- Return on assets is high for Virgin airlines then Qantas airline. Value of ROA for

former firm is 2.12% and same for latter firm is 3.29%. It can be said that Virgin airlines

is making best use of its assets then Qantas airlines.

Debt to equity- Percentage of this ratio is high for Virgin airlines which is 180.07% and

same for Qantas airlines is 111.21%. There is equal proportion of debt and equity in the

Qantas capital structure. Whereas, in case of Virgin airlines it is identified that debt is

nearby to equity in term of value in the capital structure. Quanta’s already have big

network all around the world but Virgin is working on commencing number of flights on

new routes (Virgin Australia group annual report 2015, 2015). At same time it is also

focusing on increasing its fleet size. Hence, for this it takes heavy amount of loan

financial institutions. Such kind of decision may prove costly to the firm in upcoming

time period.

Current ratio – Current ratio of Qantas airlines is 0.77 and same for Virgin holdings is

0.65. This means that former firm is in better condition in terms of payment of current

liability by making use of short term assets (A strong, sustainable future, 2015). This

happened because cash management strategy of former firm is good and it give credit to

only those who can pay same on time in comparison to latter company.

Net profit margin- Net profit margin of Quanta’s airlines is 1.36% and same of Virgin

holding is 2.23%. Latter firm perform better then rival company because it have strong

control on its expense. This is proved from higher percentage of EBIT margin and firm

annual report.

kilo meter (CASK) by 6.4%. Hence, latter firm is following cost control strategy in its

business and due to this reason its EBIT margin is high.

ROE- Return on equity for Qantas airlines is 3.38% and same for Virgin holdings is

8.40%. Here, also Virgin is ahead of Qantas airlines. This happened because former firm

is earning good return in its business and its equity is lower than latter firm. Hence, due

to this reason big difference is observed in this ratio between both firms.

ROA- Return on assets is high for Virgin airlines then Qantas airline. Value of ROA for

former firm is 2.12% and same for latter firm is 3.29%. It can be said that Virgin airlines

is making best use of its assets then Qantas airlines.

Debt to equity- Percentage of this ratio is high for Virgin airlines which is 180.07% and

same for Qantas airlines is 111.21%. There is equal proportion of debt and equity in the

Qantas capital structure. Whereas, in case of Virgin airlines it is identified that debt is

nearby to equity in term of value in the capital structure. Quanta’s already have big

network all around the world but Virgin is working on commencing number of flights on

new routes (Virgin Australia group annual report 2015, 2015). At same time it is also

focusing on increasing its fleet size. Hence, for this it takes heavy amount of loan

financial institutions. Such kind of decision may prove costly to the firm in upcoming

time period.

Current ratio – Current ratio of Qantas airlines is 0.77 and same for Virgin holdings is

0.65. This means that former firm is in better condition in terms of payment of current

liability by making use of short term assets (A strong, sustainable future, 2015). This

happened because cash management strategy of former firm is good and it give credit to

only those who can pay same on time in comparison to latter company.

Net profit margin- Net profit margin of Quanta’s airlines is 1.36% and same of Virgin

holding is 2.23%. Latter firm perform better then rival company because it have strong

control on its expense. This is proved from higher percentage of EBIT margin and firm

annual report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & journals

Bamber, L.S., Jiang, J. and Wang, I.Y., 2010. What's my style? The influence of top managers

on voluntary corporate financial disclosure. The accounting review. 85(4). Pp.1131-1162.

Chen, S., Sun, S.Y. and Wu, D., 2010. Client importance, institutional improvements, and audit

quality in China: An office and individual auditor level analysis. The Accounting Review.

85(1). Pp.127-158.

Dhaliwal, D.S. and et.al., 2011. Voluntary nonfinancial disclosure and the cost of equity capital:

The initiation of corporate social responsibility reporting. The accounting review. 86(1).

Pp.59-100.

Duska, R., Duska, B.S. and Ragatz, J.A., 2011. Accounting ethics. John Wiley & Sons.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Risthaus, T. and Grimme, S., 2013. Benchmarking of London dispersion-accounting density

functional theory methods on very large molecular complexes. Journal of chemical theory

and computation. 9(3). Pp.1580-1591.

Zhang, Y.I., Baral, A. and Bakshi, B.R., 2010. Accounting for ecosystem services in life cycle

assessment, part II: toward an ecologically based LCA. Environmental science &

technology. 44(7). Pp.2624-2631.

Online

A strong, sustainable future, 2015. [PDF]. Available through :<

https://www.qantas.com.au/infodetail/about/investors/2015AnnualReport.pdf>.[Accessed

on 23rd September 2016].

Virgin Australia group annual report 2015, 2015. [PDF]. Available through :<

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/webcontent/

~edisp/annual-report-2015.pdf>. [Accessed on 23rd September 2016].

Books & journals

Bamber, L.S., Jiang, J. and Wang, I.Y., 2010. What's my style? The influence of top managers

on voluntary corporate financial disclosure. The accounting review. 85(4). Pp.1131-1162.

Chen, S., Sun, S.Y. and Wu, D., 2010. Client importance, institutional improvements, and audit

quality in China: An office and individual auditor level analysis. The Accounting Review.

85(1). Pp.127-158.

Dhaliwal, D.S. and et.al., 2011. Voluntary nonfinancial disclosure and the cost of equity capital:

The initiation of corporate social responsibility reporting. The accounting review. 86(1).

Pp.59-100.

Duska, R., Duska, B.S. and Ragatz, J.A., 2011. Accounting ethics. John Wiley & Sons.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Risthaus, T. and Grimme, S., 2013. Benchmarking of London dispersion-accounting density

functional theory methods on very large molecular complexes. Journal of chemical theory

and computation. 9(3). Pp.1580-1591.

Zhang, Y.I., Baral, A. and Bakshi, B.R., 2010. Accounting for ecosystem services in life cycle

assessment, part II: toward an ecologically based LCA. Environmental science &

technology. 44(7). Pp.2624-2631.

Online

A strong, sustainable future, 2015. [PDF]. Available through :<

https://www.qantas.com.au/infodetail/about/investors/2015AnnualReport.pdf>.[Accessed

on 23rd September 2016].

Virgin Australia group annual report 2015, 2015. [PDF]. Available through :<

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/webcontent/

~edisp/annual-report-2015.pdf>. [Accessed on 23rd September 2016].

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.