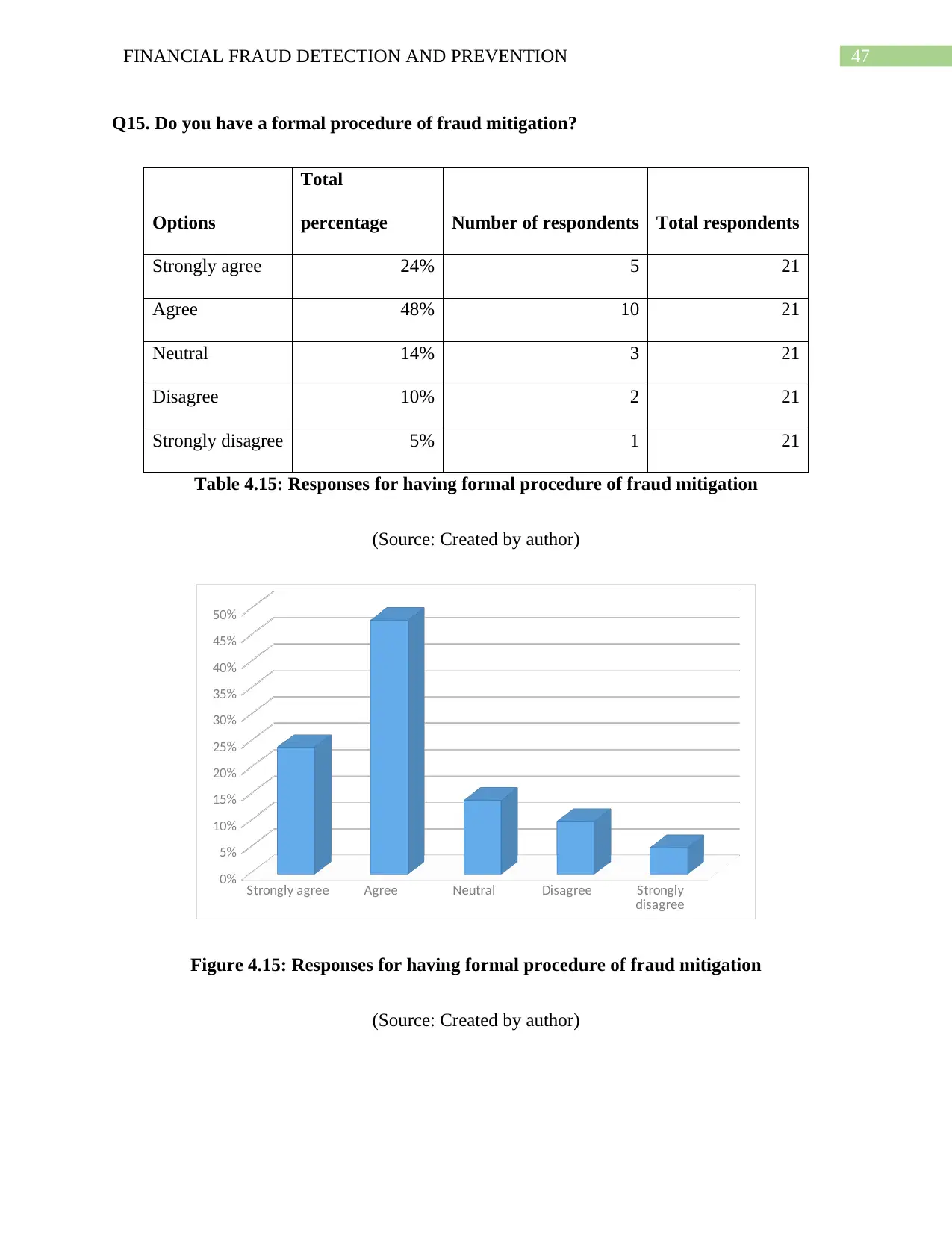

Financial Fraud Detection and Prevention | Research

VerifiedAdded on 2022/08/18

|72

|17573

|15

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL FRAUD DETECTION AND PREVENTION

Financial Fraud Detection and Prevention

Name of the Student

Name of the University

Author’s Note

Financial Fraud Detection and Prevention

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL FRAUD DETECTION AND PREVENTION

Acknowledgement

I would like to thank my University and the professor for allowing me to contribute as well as

providing opportunity to complete my research despite of all challenges that I have faced. It will

not forget the efforts that are made by the professors and other for guiding me with patience,

guidance and understanding. I would not have completed this research without their guidance

and understanding and you are all special to me.

Acknowledgement

I would like to thank my University and the professor for allowing me to contribute as well as

providing opportunity to complete my research despite of all challenges that I have faced. It will

not forget the efforts that are made by the professors and other for guiding me with patience,

guidance and understanding. I would not have completed this research without their guidance

and understanding and you are all special to me.

2FINANCIAL FRAUD DETECTION AND PREVENTION

Abstract

The research is mainly focused on the financial fraud detection and prevention that are associated

with measures of prevention and detection techniques. The primary chapter is the introduction

which centres out the common data around the thought in conjunction with the company. The

targets of the research generally has been talked around in this allocate another to the research

limitations. Other than, it in development cements the research questions close to point and

targets of the research. Insides the second chapter, it contain of composing layout which centres

out the factors that are to be tended to insides the research. It join of openings and dangers

adjoining appraisal of competitive advantage and methodologies for moving forward the

execution. In chapter three, it highlights the procedure which centres out the strategies through

which the research has been conducted. It sets the considering, approach, and organize, data

collection procedure and test of the research about sheds light. The fourth chapter joins the

results around and disclosures where the results almost about are to be surveyed and checked on

as per the current circumstance which it highlights the looking over, assessment, openings,

threats and competitive methodology. Inside the final chapter, it bargains with the conclusion

nearby proposition and utilization with the concluding contemplations have been said at the side

tending to the objectives and certain recommendation. The proposal that have been illustrated

would offer help the company to administer with the threats and challenges that are going up

against in current circumstance.

Abstract

The research is mainly focused on the financial fraud detection and prevention that are associated

with measures of prevention and detection techniques. The primary chapter is the introduction

which centres out the common data around the thought in conjunction with the company. The

targets of the research generally has been talked around in this allocate another to the research

limitations. Other than, it in development cements the research questions close to point and

targets of the research. Insides the second chapter, it contain of composing layout which centres

out the factors that are to be tended to insides the research. It join of openings and dangers

adjoining appraisal of competitive advantage and methodologies for moving forward the

execution. In chapter three, it highlights the procedure which centres out the strategies through

which the research has been conducted. It sets the considering, approach, and organize, data

collection procedure and test of the research about sheds light. The fourth chapter joins the

results around and disclosures where the results almost about are to be surveyed and checked on

as per the current circumstance which it highlights the looking over, assessment, openings,

threats and competitive methodology. Inside the final chapter, it bargains with the conclusion

nearby proposition and utilization with the concluding contemplations have been said at the side

tending to the objectives and certain recommendation. The proposal that have been illustrated

would offer help the company to administer with the threats and challenges that are going up

against in current circumstance.

3FINANCIAL FRAUD DETECTION AND PREVENTION

Table of Contents

Chapter 1: Introduction....................................................................................................................5

1.1 Background of the study........................................................................................................6

1.2 Problem statement.................................................................................................................7

1.3 Aims and Objectives..............................................................................................................8

1.4 Research Questions................................................................................................................9

1.5 Scope of the research.............................................................................................................9

Chapter 2: Literature Review.........................................................................................................11

2.1 Concept of financial fraud...................................................................................................11

2.2 Impact of financial fraud.....................................................................................................14

2.3 Prevention strategies of financial frauds..............................................................................17

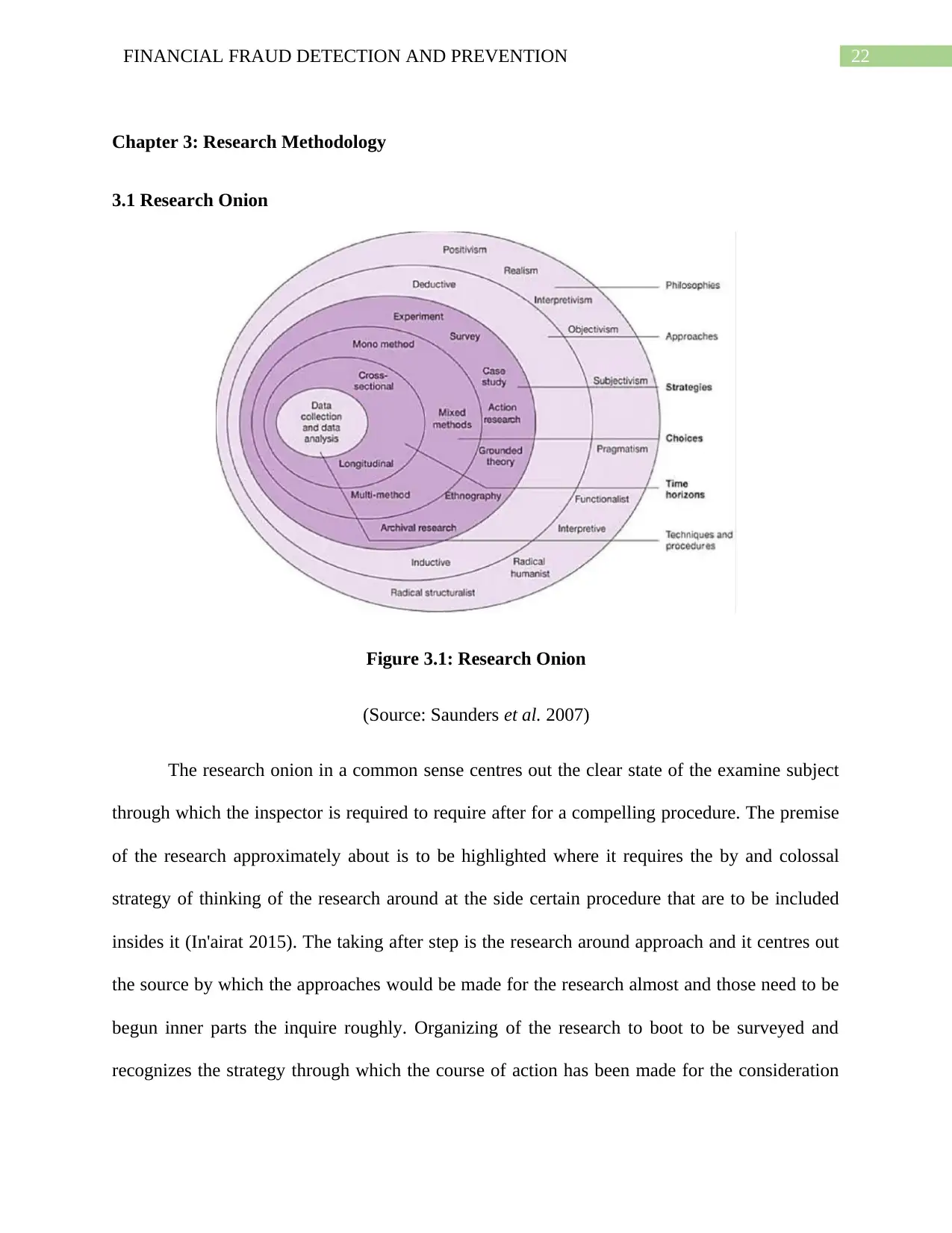

Chapter 3: Research Methodology................................................................................................22

3.1 Research Onion....................................................................................................................22

3.2 Research Philosophy............................................................................................................23

3.3 Research Approach..............................................................................................................24

3.4 Research Design..................................................................................................................24

3.5 Data Collection Process.......................................................................................................25

3.6 Sampling method and sampling size...................................................................................25

3.7 Ethical Consideration...........................................................................................................26

Table of Contents

Chapter 1: Introduction....................................................................................................................5

1.1 Background of the study........................................................................................................6

1.2 Problem statement.................................................................................................................7

1.3 Aims and Objectives..............................................................................................................8

1.4 Research Questions................................................................................................................9

1.5 Scope of the research.............................................................................................................9

Chapter 2: Literature Review.........................................................................................................11

2.1 Concept of financial fraud...................................................................................................11

2.2 Impact of financial fraud.....................................................................................................14

2.3 Prevention strategies of financial frauds..............................................................................17

Chapter 3: Research Methodology................................................................................................22

3.1 Research Onion....................................................................................................................22

3.2 Research Philosophy............................................................................................................23

3.3 Research Approach..............................................................................................................24

3.4 Research Design..................................................................................................................24

3.5 Data Collection Process.......................................................................................................25

3.6 Sampling method and sampling size...................................................................................25

3.7 Ethical Consideration...........................................................................................................26

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL FRAUD DETECTION AND PREVENTION

3.8 Summary..............................................................................................................................26

Chapter 4: Result and Analysis......................................................................................................28

Quantitative research.................................................................................................................28

Chapter 5: Discussions..................................................................................................................48

Chapter 6: Conclusion and Recommendation...............................................................................53

References and Bibliography.........................................................................................................60

Appendices....................................................................................................................................68

3.8 Summary..............................................................................................................................26

Chapter 4: Result and Analysis......................................................................................................28

Quantitative research.................................................................................................................28

Chapter 5: Discussions..................................................................................................................48

Chapter 6: Conclusion and Recommendation...............................................................................53

References and Bibliography.........................................................................................................60

Appendices....................................................................................................................................68

5FINANCIAL FRAUD DETECTION AND PREVENTION

Chapter 1: Introduction

Financial fraud detection and prevention is the procedure by which the both finances, as

well as the financial information are detected from being a fraud. Looking at the historical data

over the records which mainly stops the fraudulent activities that are associated with the business

(Olukowade and Balogun 2015). In the current world of advanced technologies, financial frauds

take place at most of the places along with its impact on the individual and organisations. In

recent years, the organisations are installed with certain fraud detection techniques which would

automatically detect the fraudulent activities that are going to take place. The automated fraud

management solution are also helpful which points out the unusual patters which are consist in

noticing the fraudulent activities and freezing the transaction before it actually takes place

(Othman et al. 2015). The fraudulent activities have special running methods which is almost

similar to genuine process but certain aspects is required to be considered for their identification.

The challenges that are faced in recent years are required to be controlled as most of the

transaction that takes place are fully automated which do not any person for its overall

verification. The sheer volume of data that are generally processed in the real time are required

to be enhanced with fraud detection techniques (Imam, Kumshe and Jajere 2015). The solution

for managing the tasks are required to be included with transaction that takes place in that period

of time.

In current world of technological advancement, there are different procedures which are

capable of mitigating the frauds and preventing them from taking place. The art of technology

can capture the nature of the frauds along with their fraudulent activities (Joseph, Albert and

Byaruhanga 2015). The transaction that takes place in recent years consist of several dollars that

are directly included with the method. The overall review of the customers for the transaction

Chapter 1: Introduction

Financial fraud detection and prevention is the procedure by which the both finances, as

well as the financial information are detected from being a fraud. Looking at the historical data

over the records which mainly stops the fraudulent activities that are associated with the business

(Olukowade and Balogun 2015). In the current world of advanced technologies, financial frauds

take place at most of the places along with its impact on the individual and organisations. In

recent years, the organisations are installed with certain fraud detection techniques which would

automatically detect the fraudulent activities that are going to take place. The automated fraud

management solution are also helpful which points out the unusual patters which are consist in

noticing the fraudulent activities and freezing the transaction before it actually takes place

(Othman et al. 2015). The fraudulent activities have special running methods which is almost

similar to genuine process but certain aspects is required to be considered for their identification.

The challenges that are faced in recent years are required to be controlled as most of the

transaction that takes place are fully automated which do not any person for its overall

verification. The sheer volume of data that are generally processed in the real time are required

to be enhanced with fraud detection techniques (Imam, Kumshe and Jajere 2015). The solution

for managing the tasks are required to be included with transaction that takes place in that period

of time.

In current world of technological advancement, there are different procedures which are

capable of mitigating the frauds and preventing them from taking place. The art of technology

can capture the nature of the frauds along with their fraudulent activities (Joseph, Albert and

Byaruhanga 2015). The transaction that takes place in recent years consist of several dollars that

are directly included with the method. The overall review of the customers for the transaction

6FINANCIAL FRAUD DETECTION AND PREVENTION

that has already taken place also points out the process of detection of frauds and preventing it as

much as possible. The patters of the financial frauds that takes place includes different aspects

that are required to be considered for the overall activities (Herawati 2015). The inclusion of

location, size and the overall frequency of the transaction are required to be considered for

detecting the frauds. More sophisticated metrics are required to be used for presenting the

financial frauds that includes the history of profiles of the customers (Enofe, Omagbon and

Ehigiator 2015). The list of the suspects are required to be kept in a safe place on which the

required is also to be reviewed as per the overall nature of the fraud along with its detection

techniques.

1.1 Background of the study

The research mainly highlights the financial frauds detection and prevention in which the

methods and the techniques have been discussed. It also includes the uniqueness of the fraud

detection techniques along with the prevention methods that are useful in mitigating the financial

loss (Zamzami, Nusa and Timur 2016). The research also sheds the light on the financial frauds

that mainly takes in place in recent world with implementation of advanced technologies which

would be helpful in preventing the financial frauds. The list of the suspect behaviour is required

to be kept which would combined to all of the issues that have been faced by the organisations

(Simha and Satyanarayan 2016). The database of the query for each of the transactions mainly

points out the detection of frauds which is required to be enables with the prevention system and

that have to be associated with faster process of massive amount of data (West and Bhattacharya

2016). The various sources of database is also required to be highlighted which includes the real

time solutions with batch data integration along with out of the box scenario for faster alerts.

that has already taken place also points out the process of detection of frauds and preventing it as

much as possible. The patters of the financial frauds that takes place includes different aspects

that are required to be considered for the overall activities (Herawati 2015). The inclusion of

location, size and the overall frequency of the transaction are required to be considered for

detecting the frauds. More sophisticated metrics are required to be used for presenting the

financial frauds that includes the history of profiles of the customers (Enofe, Omagbon and

Ehigiator 2015). The list of the suspects are required to be kept in a safe place on which the

required is also to be reviewed as per the overall nature of the fraud along with its detection

techniques.

1.1 Background of the study

The research mainly highlights the financial frauds detection and prevention in which the

methods and the techniques have been discussed. It also includes the uniqueness of the fraud

detection techniques along with the prevention methods that are useful in mitigating the financial

loss (Zamzami, Nusa and Timur 2016). The research also sheds the light on the financial frauds

that mainly takes in place in recent world with implementation of advanced technologies which

would be helpful in preventing the financial frauds. The list of the suspect behaviour is required

to be kept which would combined to all of the issues that have been faced by the organisations

(Simha and Satyanarayan 2016). The database of the query for each of the transactions mainly

points out the detection of frauds which is required to be enables with the prevention system and

that have to be associated with faster process of massive amount of data (West and Bhattacharya

2016). The various sources of database is also required to be highlighted which includes the real

time solutions with batch data integration along with out of the box scenario for faster alerts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL FRAUD DETECTION AND PREVENTION

The prevention of fraud is the technology that are required to be made with enormous

stride from the process of advanced computing and other form of machine learning. The forms of

artificial intelligence touches the every areas of live which are required to be raised with prices

and payment of goods and services (Mangala and Kumari 2015). In this case, the financial fraud

might happen which are required to be associated with the cost of the transactions that has

already taken place. The waste and abuse of improper payments is mainly referred as the fraud

which is also fragmented with the prevention with using of the rules. The different set of data is

also responsible for cross referencing the conventional tactics that are required to be associated

with the method of fraud detection (Bănărescu 2015). The overall development of the new

technologies are more inclined towards the frauds that are occurred in the organisations in real

time. The process of prevention of fraud is more like pay and chase which are required to be

traced and detected at a correct time. The complexities that have grown in the recent world are

mainly the state sponsored terrorism that are required to be included with the professional

criminals (McMahon et al. 2016). These criminals are expert in making financial frauds and that

particular fraud is required to be detected and prevented as early as possible. The comprehensive

approach of matching of data along with the activities that are associated with the fraud detection

is to be identified. The abnormal nature of the activities mainly refers to the frauds that points out

the sophisticated tactics which would be useful in digital event of data (Gbegi and Adebisi 2015).

Any kind of changes in the overall approaches also highlights the authentication, access,

location, devices and others.

1.2 Problem statement

The problem that is associated with the research mainly lies in the context itself which

mainly points out the fraudulent activities. The fraudulent activities are required to be stopped

The prevention of fraud is the technology that are required to be made with enormous

stride from the process of advanced computing and other form of machine learning. The forms of

artificial intelligence touches the every areas of live which are required to be raised with prices

and payment of goods and services (Mangala and Kumari 2015). In this case, the financial fraud

might happen which are required to be associated with the cost of the transactions that has

already taken place. The waste and abuse of improper payments is mainly referred as the fraud

which is also fragmented with the prevention with using of the rules. The different set of data is

also responsible for cross referencing the conventional tactics that are required to be associated

with the method of fraud detection (Bănărescu 2015). The overall development of the new

technologies are more inclined towards the frauds that are occurred in the organisations in real

time. The process of prevention of fraud is more like pay and chase which are required to be

traced and detected at a correct time. The complexities that have grown in the recent world are

mainly the state sponsored terrorism that are required to be included with the professional

criminals (McMahon et al. 2016). These criminals are expert in making financial frauds and that

particular fraud is required to be detected and prevented as early as possible. The comprehensive

approach of matching of data along with the activities that are associated with the fraud detection

is to be identified. The abnormal nature of the activities mainly refers to the frauds that points out

the sophisticated tactics which would be useful in digital event of data (Gbegi and Adebisi 2015).

Any kind of changes in the overall approaches also highlights the authentication, access,

location, devices and others.

1.2 Problem statement

The problem that is associated with the research mainly lies in the context itself which

mainly points out the fraudulent activities. The fraudulent activities are required to be stopped

8FINANCIAL FRAUD DETECTION AND PREVENTION

which mainly includes the identification procedures and accurately measuring the overall

experiences (Wong and Venkatraman 2015). The development of the sophisticated tactics as it

might help in changing the approaches for the total system of financial transaction. There are

certain steps that are required to be captured within the organisation along with improving the

experiences of individual as well as of the organisations. The steps are mainly mentioned in the

following part. The primary step is to capture the data that are available in nature from different

departments and includes them in the process of analysis (Kulikova and Satdarova 2016). The

monitoring of the transaction in a continuous manner also points out in the social networks that

are high risk in nature. The culture of enterprise wide is required to be installed by the process of

data visualisation along with investigating the optimisation of workflow. The security technique

is also to be introduced with different layered as it would help in preventing the financial frauds

by use of the technology.

1.3 Aims and Objectives

The aims and objectives of the study is to point out the factors that affects the financial

frauds detection and prevention along with providing with better benefits and solution for the

issues.

The aims and objectives of the study has been mentioned and discussed in the part below.

The main aim of the study is to highlight the financial fraud detection along with its

preventive measures which would be beneficial for the company. The fraudulent exercises have

uncommon running strategies which is nearly comparative to veritable handle but certain

perspectives is required to be considered for their identification (KABUE and ADUDA 2017).

The challenges that are confronted in later a long time are required to be controlled as most of

the exchange that takes put are completely mechanized which do not any individual for its

which mainly includes the identification procedures and accurately measuring the overall

experiences (Wong and Venkatraman 2015). The development of the sophisticated tactics as it

might help in changing the approaches for the total system of financial transaction. There are

certain steps that are required to be captured within the organisation along with improving the

experiences of individual as well as of the organisations. The steps are mainly mentioned in the

following part. The primary step is to capture the data that are available in nature from different

departments and includes them in the process of analysis (Kulikova and Satdarova 2016). The

monitoring of the transaction in a continuous manner also points out in the social networks that

are high risk in nature. The culture of enterprise wide is required to be installed by the process of

data visualisation along with investigating the optimisation of workflow. The security technique

is also to be introduced with different layered as it would help in preventing the financial frauds

by use of the technology.

1.3 Aims and Objectives

The aims and objectives of the study is to point out the factors that affects the financial

frauds detection and prevention along with providing with better benefits and solution for the

issues.

The aims and objectives of the study has been mentioned and discussed in the part below.

The main aim of the study is to highlight the financial fraud detection along with its

preventive measures which would be beneficial for the company. The fraudulent exercises have

uncommon running strategies which is nearly comparative to veritable handle but certain

perspectives is required to be considered for their identification (KABUE and ADUDA 2017).

The challenges that are confronted in later a long time are required to be controlled as most of

the exchange that takes put are completely mechanized which do not any individual for its

9FINANCIAL FRAUD DETECTION AND PREVENTION

generally confirmation. The sheer volume of information that are generally prepared within the

genuine time are required to be upgraded with extortion location methods. The arrangement for

overseeing the errands are required to be included with exchange that takes put in that period of

time. In later a long time, the associations are introduced with certain extortion location

procedures which would automatically detect the false exercises that are reaching to take put

(Abdallah, Maarof and Zainal 2016). The mechanized extortion administration arrangement are

too accommodating which focuses out the abnormal patters which are comprise in taking note

the false exercises and solidifying the exchange some time recently it really takes place. Looking

at the authentic information over the records which primarily stops the false exercises that are

related with the commerce. Within the current world of progressed innovations, budgetary frauds

take put at most of the places beside its effect on the person and associations.

1.4 Research Questions

The following are the research questions which has been gathered from different sources

about the financial fraud detection and prevention.

1. What are the impact of financial fraud on an organisation?

2. What are the detection procedures by which financial frauds can be detected?

3. What are preventive measures for financial frauds?

1.5 Scope of the research

The research is totally based on financial fraud detection and prevention and that have

been considered in the overall study. The patters of the financial frauds that takes put

incorporates diverse perspectives that are required to be considered for the generally exercises.

The consideration of area, estimate and the in general recurrence of the exchange are required to

generally confirmation. The sheer volume of information that are generally prepared within the

genuine time are required to be upgraded with extortion location methods. The arrangement for

overseeing the errands are required to be included with exchange that takes put in that period of

time. In later a long time, the associations are introduced with certain extortion location

procedures which would automatically detect the false exercises that are reaching to take put

(Abdallah, Maarof and Zainal 2016). The mechanized extortion administration arrangement are

too accommodating which focuses out the abnormal patters which are comprise in taking note

the false exercises and solidifying the exchange some time recently it really takes place. Looking

at the authentic information over the records which primarily stops the false exercises that are

related with the commerce. Within the current world of progressed innovations, budgetary frauds

take put at most of the places beside its effect on the person and associations.

1.4 Research Questions

The following are the research questions which has been gathered from different sources

about the financial fraud detection and prevention.

1. What are the impact of financial fraud on an organisation?

2. What are the detection procedures by which financial frauds can be detected?

3. What are preventive measures for financial frauds?

1.5 Scope of the research

The research is totally based on financial fraud detection and prevention and that have

been considered in the overall study. The patters of the financial frauds that takes put

incorporates diverse perspectives that are required to be considered for the generally exercises.

The consideration of area, estimate and the in general recurrence of the exchange are required to

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL FRAUD DETECTION AND PREVENTION

be considered for identifying the frauds. More advanced measurements are required to be utilized

for showing the monetary frauds that incorporates the history of profiles of the clients (Mansor

2015). The list of the suspects are required to be kept in a secure put on which the specified is

additionally to be reviewed as per the by and large nature of the extortion together with its

location procedures. The exchange that takes put in later a long time comprise of a few dollars

that are specifically included with the method. The generally survey of the clients for the

exchange that has as of now taken put too focuses out the method of location of frauds and

anticipating it as much as conceivable (Lin et al. 2015). In current world of innovative

progression, there are distinctive methods which are competent of relieving the frauds and

avoiding them from taking put. The craftsmanship of innovation can capture the nature of the

frauds together with their fraudulent exercises.

be considered for identifying the frauds. More advanced measurements are required to be utilized

for showing the monetary frauds that incorporates the history of profiles of the clients (Mansor

2015). The list of the suspects are required to be kept in a secure put on which the specified is

additionally to be reviewed as per the by and large nature of the extortion together with its

location procedures. The exchange that takes put in later a long time comprise of a few dollars

that are specifically included with the method. The generally survey of the clients for the

exchange that has as of now taken put too focuses out the method of location of frauds and

anticipating it as much as conceivable (Lin et al. 2015). In current world of innovative

progression, there are distinctive methods which are competent of relieving the frauds and

avoiding them from taking put. The craftsmanship of innovation can capture the nature of the

frauds together with their fraudulent exercises.

11FINANCIAL FRAUD DETECTION AND PREVENTION

Chapter 2: Literature Review

This chapter mainly focused on the review of the overall literature that are included in the

research. It includes the overall concept of the topic on the research and the strategies that would

be useful for mitigating the issue. Moreover, it also deals with the impact that might affect the

event over the time and how it would also points out the benefits as well as the limitations of the

strategies.

2.1 Concept of financial fraud

The concept of financial fraud is the event where someone takes the money and other

assets from another people by the process of deception along with other criminal activity. The

detection and prevention of fraud is totally associated with certain perspective that would

beneficial for the organisation and the individuals (Sadgali, Sael and Benabbou 2019). The

overall concept of the financial fraud are associated with finances that includes money and other

form of assets which would be beneficial for their current period of time. The process of

detection and includes the technologies which would be helpful for the organisation and their

arrangement on the complex data form (Liu et al. 2015). There are different types of financial

frauds that are currently occurring in the modern world. Identity fraud is one of the common

financial fraud that takes place in most of the cases. It mainly points out to an individual who

impersonates other people and uses their secure personal information for stealing money. This

kind of activity is mainly referred to the financial fraud of identity which would be effectively

identified (Mallika 2017). This particular type of fraud mainly takes place on the field of internet

as all of the personal information are readily available on the internet. Phishing is also another

type of fraudulent activities that points out the methods of internet banking and that would be

useful for receiving the transaction details. The clients of internet banking receives the email

Chapter 2: Literature Review

This chapter mainly focused on the review of the overall literature that are included in the

research. It includes the overall concept of the topic on the research and the strategies that would

be useful for mitigating the issue. Moreover, it also deals with the impact that might affect the

event over the time and how it would also points out the benefits as well as the limitations of the

strategies.

2.1 Concept of financial fraud

The concept of financial fraud is the event where someone takes the money and other

assets from another people by the process of deception along with other criminal activity. The

detection and prevention of fraud is totally associated with certain perspective that would

beneficial for the organisation and the individuals (Sadgali, Sael and Benabbou 2019). The

overall concept of the financial fraud are associated with finances that includes money and other

form of assets which would be beneficial for their current period of time. The process of

detection and includes the technologies which would be helpful for the organisation and their

arrangement on the complex data form (Liu et al. 2015). There are different types of financial

frauds that are currently occurring in the modern world. Identity fraud is one of the common

financial fraud that takes place in most of the cases. It mainly points out to an individual who

impersonates other people and uses their secure personal information for stealing money. This

kind of activity is mainly referred to the financial fraud of identity which would be effectively

identified (Mallika 2017). This particular type of fraud mainly takes place on the field of internet

as all of the personal information are readily available on the internet. Phishing is also another

type of fraudulent activities that points out the methods of internet banking and that would be

useful for receiving the transaction details. The clients of internet banking receives the email

12FINANCIAL FRAUD DETECTION AND PREVENTION

which mainly asks for the account details such as their account number, password and personal

details (Hamdan 2018). These information are useful for withdrawing money from the account

and performing the fraudulent activities.

Card fraud is also another type of fraud which points out the financial fraudulent

activities which includes the effective type of financial fraudulent activities. At the initial level

the card of the bank is to be stolen which points out the cards that are usable (Bhardwaj and

Gupta 2016). The fraudulent activities makes different kinds of unauthorised purchases which

are not notified by the bank. In addition to this, skimming is the type of process which involves

the process of stealing the information that highlights the extraction of the information from the

bank cards that might be both credit card and debit card (Dong, Liao and Zhang 2018). The

stealing of information from the bank card at the time of legitimate transaction also points out the

skimming if information which drags the attention of the users. The process of swiping of cards

mainly points out the using of the electronic devices that functions on the wedge and the

skimming devices along with recording of information that contains on the magnetic strip (Dong,

Liao and Zhang 2018). This can be stopped with the process of stopping the online transaction

which mainly uses the card for the purchase. Moreover, the counterfeit cards are also used for

matching the transaction that are associated with the finances. The fraudulent activities are also

performed by the process of fund transfer where the individual is being asked to transfer certain

amount of money for receiving certain amount of commission. This kind of activity is a type of

financial fraud which is required to be detected and prevented.

The list of the suspect conduct is required to be kept which would combined to all of the

issues that have been confronted by the associations. The database of the inquiry for each of the

exchanges basically focuses out the location of frauds which is required to be empowers with the

which mainly asks for the account details such as their account number, password and personal

details (Hamdan 2018). These information are useful for withdrawing money from the account

and performing the fraudulent activities.

Card fraud is also another type of fraud which points out the financial fraudulent

activities which includes the effective type of financial fraudulent activities. At the initial level

the card of the bank is to be stolen which points out the cards that are usable (Bhardwaj and

Gupta 2016). The fraudulent activities makes different kinds of unauthorised purchases which

are not notified by the bank. In addition to this, skimming is the type of process which involves

the process of stealing the information that highlights the extraction of the information from the

bank cards that might be both credit card and debit card (Dong, Liao and Zhang 2018). The

stealing of information from the bank card at the time of legitimate transaction also points out the

skimming if information which drags the attention of the users. The process of swiping of cards

mainly points out the using of the electronic devices that functions on the wedge and the

skimming devices along with recording of information that contains on the magnetic strip (Dong,

Liao and Zhang 2018). This can be stopped with the process of stopping the online transaction

which mainly uses the card for the purchase. Moreover, the counterfeit cards are also used for

matching the transaction that are associated with the finances. The fraudulent activities are also

performed by the process of fund transfer where the individual is being asked to transfer certain

amount of money for receiving certain amount of commission. This kind of activity is a type of

financial fraud which is required to be detected and prevented.

The list of the suspect conduct is required to be kept which would combined to all of the

issues that have been confronted by the associations. The database of the inquiry for each of the

exchanges basically focuses out the location of frauds which is required to be empowers with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL FRAUD DETECTION AND PREVENTION

anticipation framework which ought to be related with faster handle of enormous sum of

information (Huang et al. 2017). The different sources of database is additionally required to be

highlighted which incorporates the genuine time arrangements with bunch information

integration at the side out of the box situation for quicker cautions. It moreover incorporates the

uniqueness of the extortion location strategies alongside the anticipation strategies that are

valuable in moderating the monetary loss (Shi, Connelly and Hoskisson 2017). The inquire about

moreover sheds the light on the budgetary frauds that basically takes in put in later world with

usage of progressed innovations which would be supportive in anticipating the budgetary frauds.

The list of the suspect conduct is required to be kept which would combined for all of the

mentioned issues. The in general improvement of the new technologies are more slanted towards

the frauds that are happened within the organisations in genuine time (Klein 2015). The method

of anticipation of extortion is more like pay and chase which are required to be followed and

recognized at a correct time. The complexities that have developed within the later world are

primarily the state supported terrorism that are required to be included with the proficient

criminals. These offenders are master in making budgetary frauds which specific fraud is

required to be detected and anticipated as early as conceivable.

The comprehensive approach of coordinating of information together with the exercises

that are related with the extortion discovery is to be recognized (Umar, Samsudin and Mohamed

2016). The anomalous nature of the activities mainly alludes to the frauds that focuses out the

modern strategies which would be valuable in advanced occasion of information. Any kind of

changes within the generally approaches moreover highlights the verification, get to, area,

devices and others (Shimpi and Kadroli 2015). The avoidance of fraud is the innovation that are

required to be made with gigantic walk from the method of progressed computing and other

anticipation framework which ought to be related with faster handle of enormous sum of

information (Huang et al. 2017). The different sources of database is additionally required to be

highlighted which incorporates the genuine time arrangements with bunch information

integration at the side out of the box situation for quicker cautions. It moreover incorporates the

uniqueness of the extortion location strategies alongside the anticipation strategies that are

valuable in moderating the monetary loss (Shi, Connelly and Hoskisson 2017). The inquire about

moreover sheds the light on the budgetary frauds that basically takes in put in later world with

usage of progressed innovations which would be supportive in anticipating the budgetary frauds.

The list of the suspect conduct is required to be kept which would combined for all of the

mentioned issues. The in general improvement of the new technologies are more slanted towards

the frauds that are happened within the organisations in genuine time (Klein 2015). The method

of anticipation of extortion is more like pay and chase which are required to be followed and

recognized at a correct time. The complexities that have developed within the later world are

primarily the state supported terrorism that are required to be included with the proficient

criminals. These offenders are master in making budgetary frauds which specific fraud is

required to be detected and anticipated as early as conceivable.

The comprehensive approach of coordinating of information together with the exercises

that are related with the extortion discovery is to be recognized (Umar, Samsudin and Mohamed

2016). The anomalous nature of the activities mainly alludes to the frauds that focuses out the

modern strategies which would be valuable in advanced occasion of information. Any kind of

changes within the generally approaches moreover highlights the verification, get to, area,

devices and others (Shimpi and Kadroli 2015). The avoidance of fraud is the innovation that are

required to be made with gigantic walk from the method of progressed computing and other

14FINANCIAL FRAUD DETECTION AND PREVENTION

frame of machine learning. The shapes of counterfeit insights touches the each ranges of live

which are required to be raised with costs and instalment of products and administrations. In this

case, the financial fraud might happen which are required to be related with the fetched of the

exchanges that has as of now taken into consideration (Siering et al. 2017). The waste and

mishandle of inappropriate instalments is basically alluded as the extortion which is additionally

divided with the avoidance with utilizing of the rules. The diverse set of information is

additionally dependable for cross referencing the customary strategies that are required to be

related with the strategy of fraud location.

2.2 Impact of financial fraud

The impact of financial fraud is required to be highlighted on the business activities as

these help the companies to for defending against it. The attention on the financial frauds also

highlights the results that are quite alarming and that have to be targeted for the overall attempt

of financial fraud (Khan 2015). One of the key issues in a business is financial fraud that is

required to be highlighted by using different strategies. The companies that are suffering from

loss also included in the around 36 % of total profit. Despite of the risk, there are huge number of

business that fails for reviewing their financial frauds that take place in their business activities.

The appointed finance professionals have not reviewed the process of financial fraud in last few

years. It can also be seen that 18 % of the firms have never updated their financial statement for

detecting the financial frauds (Rahman and Iverson 2015). Fraudsters are pretty impressive on

the hit rate that are going to be the major slugger which might impact on the business. Other

authors have mentioned that, one out of six people are not aware that they are targeted for some

kind of fraudulent activities. The attempt to defraud the companies is to be prevalent and that is

required to be considered by the management (Singh and Singh 2015). The process of fraud

frame of machine learning. The shapes of counterfeit insights touches the each ranges of live

which are required to be raised with costs and instalment of products and administrations. In this

case, the financial fraud might happen which are required to be related with the fetched of the

exchanges that has as of now taken into consideration (Siering et al. 2017). The waste and

mishandle of inappropriate instalments is basically alluded as the extortion which is additionally

divided with the avoidance with utilizing of the rules. The diverse set of information is

additionally dependable for cross referencing the customary strategies that are required to be

related with the strategy of fraud location.

2.2 Impact of financial fraud

The impact of financial fraud is required to be highlighted on the business activities as

these help the companies to for defending against it. The attention on the financial frauds also

highlights the results that are quite alarming and that have to be targeted for the overall attempt

of financial fraud (Khan 2015). One of the key issues in a business is financial fraud that is

required to be highlighted by using different strategies. The companies that are suffering from

loss also included in the around 36 % of total profit. Despite of the risk, there are huge number of

business that fails for reviewing their financial frauds that take place in their business activities.

The appointed finance professionals have not reviewed the process of financial fraud in last few

years. It can also be seen that 18 % of the firms have never updated their financial statement for

detecting the financial frauds (Rahman and Iverson 2015). Fraudsters are pretty impressive on

the hit rate that are going to be the major slugger which might impact on the business. Other

authors have mentioned that, one out of six people are not aware that they are targeted for some

kind of fraudulent activities. The attempt to defraud the companies is to be prevalent and that is

required to be considered by the management (Singh and Singh 2015). The process of fraud

15FINANCIAL FRAUD DETECTION AND PREVENTION

prevention would be huge concern for the department of finance as it deals with monetary

transactions. The companies are required to review the process of fraud prevention and that are

required to be associated with the same financial year. The information are to be perspective and

that are required to be associated with the processes on the effective source of fraudulent

activities. There are around 130000 medium to large companies and the activities have been

segregated (Ahmed, Mahmood and Islam 2016). Out of the 130000 companies 98000 have been

directly targeted for successful attempt of financial fraud and 37500 are identified as the victim

of financial fraud. 7000 companies have been targeted for the execution of financial fraud and

have not a single idea about the loss that are incurred by the companies (Abu-Shanab and

Matalqa 2015). In addition to this, 45000 companies have successfully implemented the fraud

prevention policy for the current year. It can also be seen that 22000 companies have never

updated their overall process of fraud prevention along with the policies.

Fraudsters are pretty noteworthy on the hit rate that are progressing to be the major

slugger which might effect on the trade. Other creators have said that, one out of six individuals

are not mindful that they are focused on for a few kind of fraudulent exercises (Drogalas et al.

2017). The attempt to dupe the companies is to be predominant which is required to be

considered by the administration. The method of extortion avoidance would be tremendous

concern for the department of back because it bargains with financial transactions. The

companies are required to survey the method of extortion anticipation which are required to be

related with the same financial year (Ehioghiren and Atu 2016). The data are to be viewpoint

which are required to be related with the forms on the successful source of fraudulent exercises.

There are around 130000 medium to expansive companies and the exercises have been isolated.

The effect of financial fraud is required to be highlighted on the trade exercises as these offer

prevention would be huge concern for the department of finance as it deals with monetary

transactions. The companies are required to review the process of fraud prevention and that are

required to be associated with the same financial year. The information are to be perspective and

that are required to be associated with the processes on the effective source of fraudulent

activities. There are around 130000 medium to large companies and the activities have been

segregated (Ahmed, Mahmood and Islam 2016). Out of the 130000 companies 98000 have been

directly targeted for successful attempt of financial fraud and 37500 are identified as the victim

of financial fraud. 7000 companies have been targeted for the execution of financial fraud and

have not a single idea about the loss that are incurred by the companies (Abu-Shanab and

Matalqa 2015). In addition to this, 45000 companies have successfully implemented the fraud

prevention policy for the current year. It can also be seen that 22000 companies have never

updated their overall process of fraud prevention along with the policies.

Fraudsters are pretty noteworthy on the hit rate that are progressing to be the major

slugger which might effect on the trade. Other creators have said that, one out of six individuals

are not mindful that they are focused on for a few kind of fraudulent exercises (Drogalas et al.

2017). The attempt to dupe the companies is to be predominant which is required to be

considered by the administration. The method of extortion avoidance would be tremendous

concern for the department of back because it bargains with financial transactions. The

companies are required to survey the method of extortion anticipation which are required to be

related with the same financial year (Ehioghiren and Atu 2016). The data are to be viewpoint

which are required to be related with the forms on the successful source of fraudulent exercises.

There are around 130000 medium to expansive companies and the exercises have been isolated.

The effect of financial fraud is required to be highlighted on the trade exercises as these offer

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16FINANCIAL FRAUD DETECTION AND PREVENTION

assistance the companies to for guarding against it. The consideration on the budgetary frauds

moreover highlights the outcomes about that are very disturbing which need to be focused on for

the in general endeavour of financial fraud (Aduwo 2016). One of the key issues in a commerce

is monetary extortion that is required to be highlighted by utilizing diverse procedures. The

companies that are enduring from loss moreover included within the around 36 % of add up to

benefit. In spite of the hazard, there are colossal number of trade that fails for checking on their

budgetary frauds that take put in their trade exercises. The designated back experts have not

checked on the method of financial fraud in final years (Dutta, Dutta and Raahemin 2017). It can

also be seen that 18 % of the firms have never upgraded their financial statement for identifying

the financial frauds.

The fraudulent exercises are required to be halted which basically incorporates the

recognizable proof methods and precisely measuring the generally encounters. The advancement

of the advanced strategies because it might offer assistance in changing the approaches for the

overall framework of financial transaction (Olukowade and Balogun 2015). There are certain

steps that are required to be captured inside the association together with moving forward the

encounters of person as well as of the associations. The steps are basically said within the taking

after portion. The essential step is to capture the information that are accessible in nature from

distinctive offices and incorporates them within the preparation of analysis. The observing of the

transaction in a nonstop way also points out within the social systems that are tall chance in

nature (Imam, Kumshe and Jajere 2015). The culture of endeavour wide is required to be

introduced by the method of information representation besides exploring the enhancement of

workflow. The stealing of data from the bank card at the time of true blue exchange moreover

focuses out the skimming on the off chance that data which drags the consideration of the clients

assistance the companies to for guarding against it. The consideration on the budgetary frauds

moreover highlights the outcomes about that are very disturbing which need to be focused on for

the in general endeavour of financial fraud (Aduwo 2016). One of the key issues in a commerce

is monetary extortion that is required to be highlighted by utilizing diverse procedures. The

companies that are enduring from loss moreover included within the around 36 % of add up to

benefit. In spite of the hazard, there are colossal number of trade that fails for checking on their

budgetary frauds that take put in their trade exercises. The designated back experts have not

checked on the method of financial fraud in final years (Dutta, Dutta and Raahemin 2017). It can

also be seen that 18 % of the firms have never upgraded their financial statement for identifying

the financial frauds.

The fraudulent exercises are required to be halted which basically incorporates the

recognizable proof methods and precisely measuring the generally encounters. The advancement

of the advanced strategies because it might offer assistance in changing the approaches for the

overall framework of financial transaction (Olukowade and Balogun 2015). There are certain

steps that are required to be captured inside the association together with moving forward the

encounters of person as well as of the associations. The steps are basically said within the taking

after portion. The essential step is to capture the information that are accessible in nature from

distinctive offices and incorporates them within the preparation of analysis. The observing of the

transaction in a nonstop way also points out within the social systems that are tall chance in

nature (Imam, Kumshe and Jajere 2015). The culture of endeavour wide is required to be

introduced by the method of information representation besides exploring the enhancement of

workflow. The stealing of data from the bank card at the time of true blue exchange moreover

focuses out the skimming on the off chance that data which drags the consideration of the clients

17FINANCIAL FRAUD DETECTION AND PREVENTION

(Joseph, Albert and Byaruhanga 2015). The method of swiping of cards basically focuses out the

utilizing of the electronic gadgets that capacities on the wedge and the skimming gadgets

alongside recording of data that contains on the magnetic strip.

This may be halted with the method of halting the online exchange which primarily

employments the card for the buy. Moreover, the fake cards are too utilized for coordinating the

exchange that are related with the funds. The fraudulent exercises are too performed by the

method of support exchange where the person is being inquired to exchange certain sum of cash

for getting certain sum of commission (Enofe, Omagbon and Ehigiator 2015). This kind of action

may be a sort of money related extortion which is required to be recognized and avoided. Card

fraud is additionally another sort of extortion which focuses out the financial fraudulent exercises

which incorporates the viable sort of financial fraudulent exercises. At the beginning level the

card of the bank is to be stolen which focuses out the cards that are usable. The false exercises

makes diverse sorts of unapproved buys which are not informed by the bank (Zamzami, Nusa

and Timur 2016). In expansion to this, skimming is the sort of process which includes the

method of taking the data that highlights the extraction of the data from the bank cards that may

be both credit card and charge card. Phishing is additionally another sort of false exercises that

focuses out the strategies of web managing an account which would be valuable for accepting

the exchange points of interest (Simha and Satyanaray 2016). The clients of web managing an

account gets the mail which basically inquires for the account points of interest such as their

account number, watchword and individual subtle elements. These data are valuable for pulling

back cash from the account and performing the fraud activities.

(Joseph, Albert and Byaruhanga 2015). The method of swiping of cards basically focuses out the

utilizing of the electronic gadgets that capacities on the wedge and the skimming gadgets

alongside recording of data that contains on the magnetic strip.

This may be halted with the method of halting the online exchange which primarily

employments the card for the buy. Moreover, the fake cards are too utilized for coordinating the

exchange that are related with the funds. The fraudulent exercises are too performed by the

method of support exchange where the person is being inquired to exchange certain sum of cash

for getting certain sum of commission (Enofe, Omagbon and Ehigiator 2015). This kind of action

may be a sort of money related extortion which is required to be recognized and avoided. Card

fraud is additionally another sort of extortion which focuses out the financial fraudulent exercises

which incorporates the viable sort of financial fraudulent exercises. At the beginning level the

card of the bank is to be stolen which focuses out the cards that are usable. The false exercises

makes diverse sorts of unapproved buys which are not informed by the bank (Zamzami, Nusa

and Timur 2016). In expansion to this, skimming is the sort of process which includes the

method of taking the data that highlights the extraction of the data from the bank cards that may

be both credit card and charge card. Phishing is additionally another sort of false exercises that

focuses out the strategies of web managing an account which would be valuable for accepting

the exchange points of interest (Simha and Satyanaray 2016). The clients of web managing an

account gets the mail which basically inquires for the account points of interest such as their

account number, watchword and individual subtle elements. These data are valuable for pulling

back cash from the account and performing the fraud activities.

18FINANCIAL FRAUD DETECTION AND PREVENTION

2.3 Prevention strategies of financial frauds

Financial fraud is considered as one of the significant problem that are faced by every

kind of organisations and industries. There are many reasons for which the organisation have to

face financial frauds which affects the company in a severe manner (West and Bhattacharya

2016). The financial fraud comes in different forms and that have to be categorised in

misappropriation of assets, corruption and fraud in the financial statement. Therefore, these are

the schemes which are required to be enhanced for making up the fraud cases. The financial

fraud in the financial statement mainly comprised of 5 % that are included with median loss

(Mangala and Kumari 2015). It points out the schemes that mainly involves the overall process

of omitting along with misstating the information on the financial report. It might be in the form

of fictitious revenue along with hidden liabilities or the assets that are inflated in nature. The

corruption mainly falls on the middle of the schemes which made up by the employees of the

companies that are required to be influences with the overall nature of the business. Detection of

frauds includes some of the skills that are required to be considered for its prevention (Gbegi and

Adebisi 2015). Knowing the employees is one of the important aspect that is required to be

identified with potential fraud risk. The management of the company is also required to be

associated with their employees that points out the changes for cluing in the risk. An employee’s

feels a lack of appropriation which have to be controlled by certain perspective. The anger of the

employees might lead him or her to commit any kind of fraud which might affect the company in

their overall course of business (Wong and Venkatraman 2015). The type of attitude is to be

looked at which the attention towards the employees is to be considered for better retention.

The debasement primarily falls on the centre of the plans which made up by the workers

of the companies that are required to be impacts with the overall nature of the trade. Discovery of

2.3 Prevention strategies of financial frauds

Financial fraud is considered as one of the significant problem that are faced by every

kind of organisations and industries. There are many reasons for which the organisation have to

face financial frauds which affects the company in a severe manner (West and Bhattacharya

2016). The financial fraud comes in different forms and that have to be categorised in

misappropriation of assets, corruption and fraud in the financial statement. Therefore, these are

the schemes which are required to be enhanced for making up the fraud cases. The financial

fraud in the financial statement mainly comprised of 5 % that are included with median loss

(Mangala and Kumari 2015). It points out the schemes that mainly involves the overall process

of omitting along with misstating the information on the financial report. It might be in the form

of fictitious revenue along with hidden liabilities or the assets that are inflated in nature. The

corruption mainly falls on the middle of the schemes which made up by the employees of the

companies that are required to be influences with the overall nature of the business. Detection of

frauds includes some of the skills that are required to be considered for its prevention (Gbegi and

Adebisi 2015). Knowing the employees is one of the important aspect that is required to be

identified with potential fraud risk. The management of the company is also required to be

associated with their employees that points out the changes for cluing in the risk. An employee’s

feels a lack of appropriation which have to be controlled by certain perspective. The anger of the

employees might lead him or her to commit any kind of fraud which might affect the company in

their overall course of business (Wong and Venkatraman 2015). The type of attitude is to be

looked at which the attention towards the employees is to be considered for better retention.

The debasement primarily falls on the centre of the plans which made up by the workers

of the companies that are required to be impacts with the overall nature of the trade. Discovery of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19FINANCIAL FRAUD DETECTION AND PREVENTION

frauds incorporates a few of the abilities that are required to be considered for its avoidance

(Kulikova and Satdarova 2016). Knowing the representatives is one of the critical viewpoint that

is required to be recognized with potential extortion chance. The administration of the company

is additionally required to be related with their workers that points out the changes for cluing

within the risk. An employee’s feels a need of assignment which have to be controlled by certain

point of view. The outrage of the representatives might lead him or her to commit any kind of

extortion which might influence the company in their generally course of commerce (Abdallah,

Maarof and Zainal 2016). The sort of state of mind is to be looked at which the consideration

towards the workers is to be considered for superior maintenance. Budgetary extortion is

considered as one of the noteworthy issue that are confronted by each kind of associations and

businesses. There are numerous reasons for which the association have to be confront financial

frauds which influences the company in a severe manner (Sadgali, Sael and Benabbou 2019).

The money related extortion comes in numerous shapes which need to be categorised in

misappropriation of resources, debasement and extortion within the financial statement.

Subsequently, these are the plans which are required to be improved for making up the fraud

cases.

The budgetary extortion within the financial statement mainly comprised of 5 % that are

included with middle loss. It focuses out the plans that primarily includes the generally prepare

of excluding at the side misstating the data on the budgetary report (Dong, Liao and Zhang

2018). It could be within the shape of invented income together with covered up liabilities or the

resources that are expanded in nature. The database of the inquiry for each of the trades

essentially centres out the area of fakes which is required to be enables with the expectation

system which need to be related with speedier handle of enormous sum of data. The distinctive

frauds incorporates a few of the abilities that are required to be considered for its avoidance

(Kulikova and Satdarova 2016). Knowing the representatives is one of the critical viewpoint that

is required to be recognized with potential extortion chance. The administration of the company

is additionally required to be related with their workers that points out the changes for cluing

within the risk. An employee’s feels a need of assignment which have to be controlled by certain

point of view. The outrage of the representatives might lead him or her to commit any kind of

extortion which might influence the company in their generally course of commerce (Abdallah,

Maarof and Zainal 2016). The sort of state of mind is to be looked at which the consideration

towards the workers is to be considered for superior maintenance. Budgetary extortion is

considered as one of the noteworthy issue that are confronted by each kind of associations and

businesses. There are numerous reasons for which the association have to be confront financial

frauds which influences the company in a severe manner (Sadgali, Sael and Benabbou 2019).

The money related extortion comes in numerous shapes which need to be categorised in

misappropriation of resources, debasement and extortion within the financial statement.

Subsequently, these are the plans which are required to be improved for making up the fraud

cases.

The budgetary extortion within the financial statement mainly comprised of 5 % that are

included with middle loss. It focuses out the plans that primarily includes the generally prepare

of excluding at the side misstating the data on the budgetary report (Dong, Liao and Zhang

2018). It could be within the shape of invented income together with covered up liabilities or the

resources that are expanded in nature. The database of the inquiry for each of the trades

essentially centres out the area of fakes which is required to be enables with the expectation

system which need to be related with speedier handle of enormous sum of data. The distinctive

20FINANCIAL FRAUD DETECTION AND PREVENTION

sources of database in addition required to be highlighted which joins the veritable time courses

of action with bunch data integration at the side out of the box circumstance for faster cautions

(Huang et al. 2017). It additionally joins the uniqueness of the blackmail area procedures nearby

the expectation procedures that are profitable in directing the financial loss. The odd nature of

the exercises basically insinuates to the fakes that centres out the advanced methodologies which

would be profitable in progressed event of data (Shi, Connelly and Hoskisson 2017). Any kind of

changes inside the by and large approaches besides highlights the confirmation, get to, zone,

gadgets and others. The evasion of extortion is the advancement that are required to make with

precision.

The employees of the companies are required to make the consideration about the fraud

risk policy that would make them enhancing their reporting system within the organisation. All

of the other author have mentioned that the financial risk mainly includes the effective measure

of the detection policy that are required to be highlighted among the employees. Committing the

fraudulent activities might affect the employees in their employees’ period and that are required

to be associated with the management and watching the policies which would be beneficial for

the company and also for the individual. In addition to this, most of the occupational fraud

includes the detection procedures that would be highlighted by the policy and that have to be

associated with certain prevention measures. The employees of an organisation are free to report

any kind of fraudulent activities that would help the business in their growth and development.

The internal controls are required to be implemented on the business premises that would put

certain impact on safeguarding the assets of the firm. Internal control are helpful in reducing the

fraudulent activities as well as the risk that are associated with the organisation in their normal

course of business. In addition to this, documentation is one another internal control that are

sources of database in addition required to be highlighted which joins the veritable time courses

of action with bunch data integration at the side out of the box circumstance for faster cautions

(Huang et al. 2017). It additionally joins the uniqueness of the blackmail area procedures nearby

the expectation procedures that are profitable in directing the financial loss. The odd nature of

the exercises basically insinuates to the fakes that centres out the advanced methodologies which

would be profitable in progressed event of data (Shi, Connelly and Hoskisson 2017). Any kind of

changes inside the by and large approaches besides highlights the confirmation, get to, zone,

gadgets and others. The evasion of extortion is the advancement that are required to make with

precision.

The employees of the companies are required to make the consideration about the fraud

risk policy that would make them enhancing their reporting system within the organisation. All

of the other author have mentioned that the financial risk mainly includes the effective measure

of the detection policy that are required to be highlighted among the employees. Committing the