Financial Management Study Material

VerifiedAdded on 2022/12/28

|13

|4033

|65

AI Summary

This study material covers various topics in Financial Management including Weighted Average Cost of Capital, Net Present Value, Budgeting, and more. It provides solutions to assignments and essays related to these topics. The document also discusses sources of funds for SMEs and corporate social responsibility.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL MANAGEMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................1

a) Weighted Average Cost of Capital .........................................................................................1

b) Net present Value ...................................................................................................................2

c) Memo.......................................................................................................................................3

QUESTION 2...................................................................................................................................3

a) Features of activity based costing system relative traditional costing system.........................3

b) Key decisions break even and cost profit volume analysis can be used for making...............4

QUESTION 3...................................................................................................................................5

a) Budgeting as tool used for aiding control and the performance management ........................5

b) Limitations of traditional budgeting. Beyond Budgeting improving the planning system.....6

QUESTION 4 ..................................................................................................................................7

Sources of funds for SMEs..........................................................................................................7

QUESTION 5...................................................................................................................................9

Corporate Social Responsibility including the benefits of stakeholders.....................................9

REFERENCES..............................................................................................................................11

QUESTION 1...................................................................................................................................1

a) Weighted Average Cost of Capital .........................................................................................1

b) Net present Value ...................................................................................................................2

c) Memo.......................................................................................................................................3

QUESTION 2...................................................................................................................................3

a) Features of activity based costing system relative traditional costing system.........................3

b) Key decisions break even and cost profit volume analysis can be used for making...............4

QUESTION 3...................................................................................................................................5

a) Budgeting as tool used for aiding control and the performance management ........................5

b) Limitations of traditional budgeting. Beyond Budgeting improving the planning system.....6

QUESTION 4 ..................................................................................................................................7

Sources of funds for SMEs..........................................................................................................7

QUESTION 5...................................................................................................................................9

Corporate Social Responsibility including the benefits of stakeholders.....................................9

REFERENCES..............................................................................................................................11

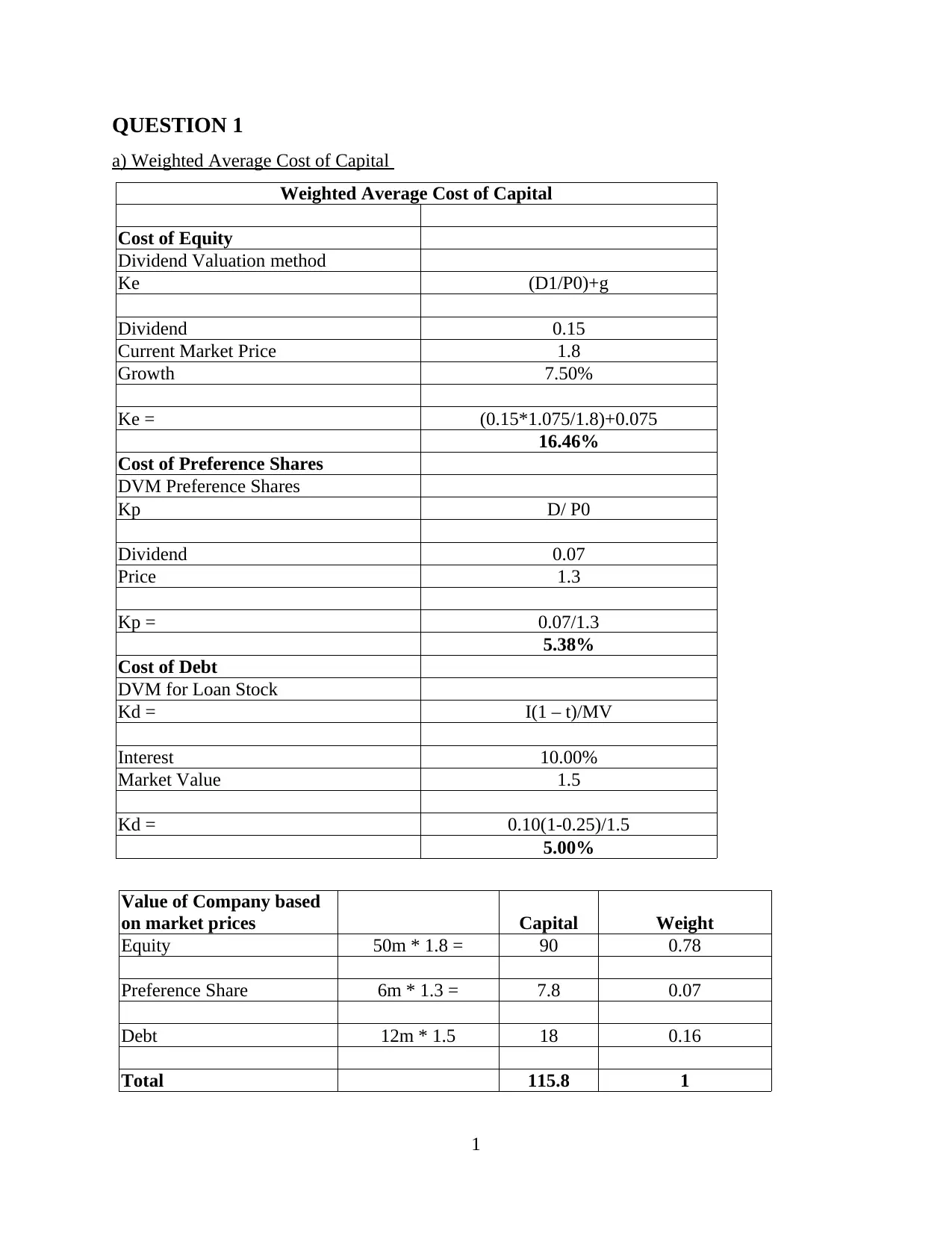

QUESTION 1

a) Weighted Average Cost of Capital

Weighted Average Cost of Capital

Cost of Equity

Dividend Valuation method

Ke (D1/P0)+g

Dividend 0.15

Current Market Price 1.8

Growth 7.50%

Ke = (0.15*1.075/1.8)+0.075

16.46%

Cost of Preference Shares

DVM Preference Shares

Kp D/ P0

Dividend 0.07

Price 1.3

Kp = 0.07/1.3

5.38%

Cost of Debt

DVM for Loan Stock

Kd = I(1 – t)/MV

Interest 10.00%

Market Value 1.5

Kd = 0.10(1-0.25)/1.5

5.00%

Value of Company based

on market prices Capital Weight

Equity 50m * 1.8 = 90 0.78

Preference Share 6m * 1.3 = 7.8 0.07

Debt 12m * 1.5 18 0.16

Total 115.8 1

1

a) Weighted Average Cost of Capital

Weighted Average Cost of Capital

Cost of Equity

Dividend Valuation method

Ke (D1/P0)+g

Dividend 0.15

Current Market Price 1.8

Growth 7.50%

Ke = (0.15*1.075/1.8)+0.075

16.46%

Cost of Preference Shares

DVM Preference Shares

Kp D/ P0

Dividend 0.07

Price 1.3

Kp = 0.07/1.3

5.38%

Cost of Debt

DVM for Loan Stock

Kd = I(1 – t)/MV

Interest 10.00%

Market Value 1.5

Kd = 0.10(1-0.25)/1.5

5.00%

Value of Company based

on market prices Capital Weight

Equity 50m * 1.8 = 90 0.78

Preference Share 6m * 1.3 = 7.8 0.07

Debt 12m * 1.5 18 0.16

Total 115.8 1

1

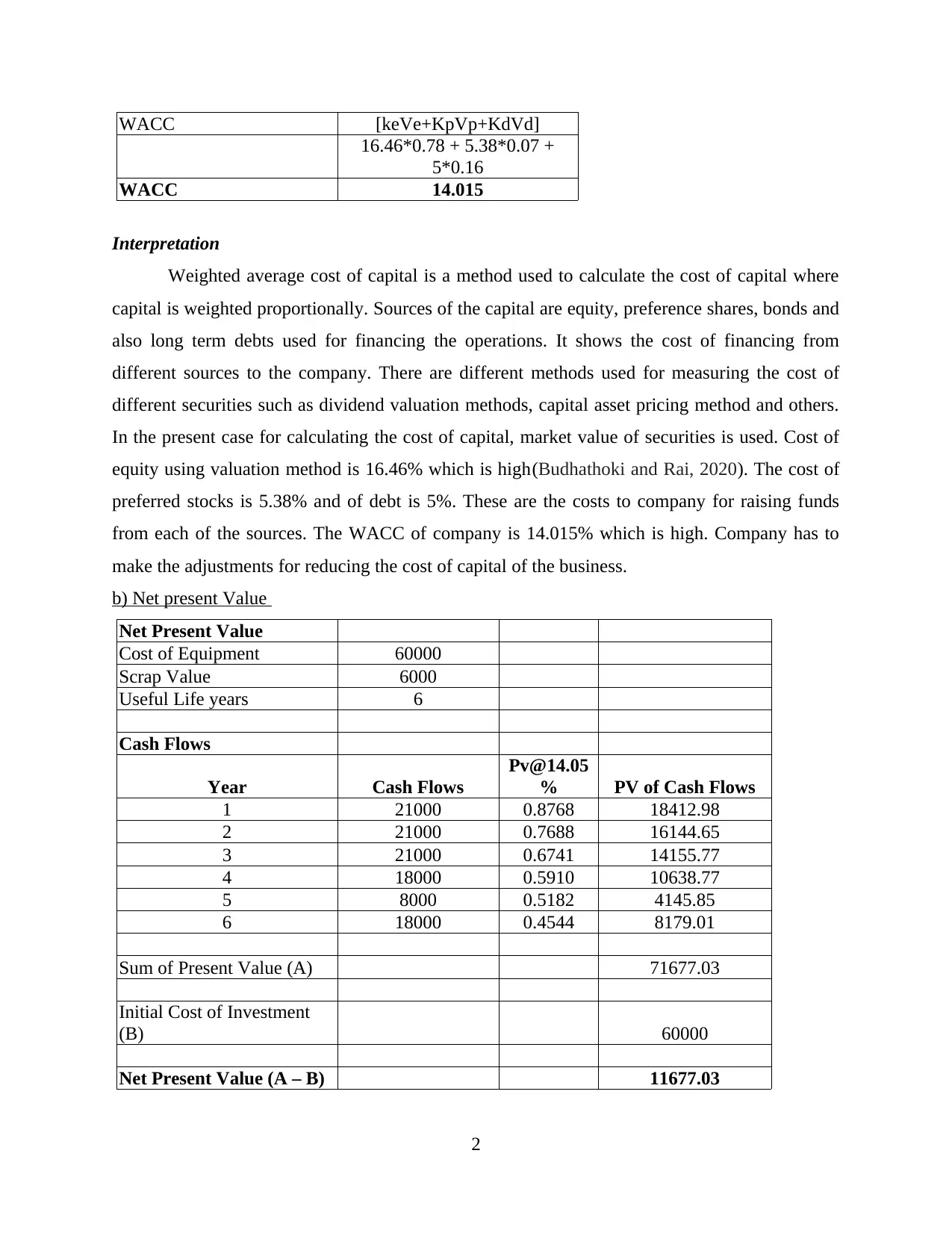

WACC [keVe+KpVp+KdVd]

16.46*0.78 + 5.38*0.07 +

5*0.16

WACC 14.015

Interpretation

Weighted average cost of capital is a method used to calculate the cost of capital where

capital is weighted proportionally. Sources of the capital are equity, preference shares, bonds and

also long term debts used for financing the operations. It shows the cost of financing from

different sources to the company. There are different methods used for measuring the cost of

different securities such as dividend valuation methods, capital asset pricing method and others.

In the present case for calculating the cost of capital, market value of securities is used. Cost of

equity using valuation method is 16.46% which is high(Budhathoki and Rai, 2020). The cost of

preferred stocks is 5.38% and of debt is 5%. These are the costs to company for raising funds

from each of the sources. The WACC of company is 14.015% which is high. Company has to

make the adjustments for reducing the cost of capital of the business.

b) Net present Value

Net Present Value

Cost of Equipment 60000

Scrap Value 6000

Useful Life years 6

Cash Flows

Year Cash Flows

Pv@14.05

% PV of Cash Flows

1 21000 0.8768 18412.98

2 21000 0.7688 16144.65

3 21000 0.6741 14155.77

4 18000 0.5910 10638.77

5 8000 0.5182 4145.85

6 18000 0.4544 8179.01

Sum of Present Value (A) 71677.03

Initial Cost of Investment

(B) 60000

Net Present Value (A – B) 11677.03

2

16.46*0.78 + 5.38*0.07 +

5*0.16

WACC 14.015

Interpretation

Weighted average cost of capital is a method used to calculate the cost of capital where

capital is weighted proportionally. Sources of the capital are equity, preference shares, bonds and

also long term debts used for financing the operations. It shows the cost of financing from

different sources to the company. There are different methods used for measuring the cost of

different securities such as dividend valuation methods, capital asset pricing method and others.

In the present case for calculating the cost of capital, market value of securities is used. Cost of

equity using valuation method is 16.46% which is high(Budhathoki and Rai, 2020). The cost of

preferred stocks is 5.38% and of debt is 5%. These are the costs to company for raising funds

from each of the sources. The WACC of company is 14.015% which is high. Company has to

make the adjustments for reducing the cost of capital of the business.

b) Net present Value

Net Present Value

Cost of Equipment 60000

Scrap Value 6000

Useful Life years 6

Cash Flows

Year Cash Flows

Pv@14.05

% PV of Cash Flows

1 21000 0.8768 18412.98

2 21000 0.7688 16144.65

3 21000 0.6741 14155.77

4 18000 0.5910 10638.77

5 8000 0.5182 4145.85

6 18000 0.4544 8179.01

Sum of Present Value (A) 71677.03

Initial Cost of Investment

(B) 60000

Net Present Value (A – B) 11677.03

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Interpretation

The net present value is method used for evaluating the viability of capital investments

for the company. It measures whether company will be able to cover the cost of investment from

the future cash flows. It brings the future cash flows at present value by discounting them using

discounting rate. The initial cost of equipment is 60000 with the scrap value of 6000 and useful

life of 6 years (Fernandez, 2019). For discounting the cash flows weighted average cost of

capital of 14.05% has been used. The net present value of equipments is computed as 11677.03

c) Memo

MEMO

To,

Board of Directors

ABC Ltd

Date: 22/1/21

Subject: Final Project Proposal

The proposal of company to acquire new equipment costing £60000 has been evaluated

using capital investment appraisal technique. It has been analysed from the net present value

method that project has positive NPV which means project will generate adequate profit for the

business. It will generate adequate returns adding value to the company. The future cash flows

are discounted by computing the cost of capital using dividend valuation method based on

market prices. Cost of capital is high of company which shows that cost of raising funds is high

which needs to be lowered down by making capital restructuring.

Considering the analysis for equipment it has been found that company should acquire

the equipment as it will be profitable for the company.

QUESTION 2

a) Features of activity based costing system relative traditional costing system

Calculating accurate manufacturing costs for every products is vital for decision-making

for company. The activity based and traditional costing method both are based over ABC and

traditional costing method for allocation of indirect costs to the products. The methods estimates

3

The net present value is method used for evaluating the viability of capital investments

for the company. It measures whether company will be able to cover the cost of investment from

the future cash flows. It brings the future cash flows at present value by discounting them using

discounting rate. The initial cost of equipment is 60000 with the scrap value of 6000 and useful

life of 6 years (Fernandez, 2019). For discounting the cash flows weighted average cost of

capital of 14.05% has been used. The net present value of equipments is computed as 11677.03

c) Memo

MEMO

To,

Board of Directors

ABC Ltd

Date: 22/1/21

Subject: Final Project Proposal

The proposal of company to acquire new equipment costing £60000 has been evaluated

using capital investment appraisal technique. It has been analysed from the net present value

method that project has positive NPV which means project will generate adequate profit for the

business. It will generate adequate returns adding value to the company. The future cash flows

are discounted by computing the cost of capital using dividend valuation method based on

market prices. Cost of capital is high of company which shows that cost of raising funds is high

which needs to be lowered down by making capital restructuring.

Considering the analysis for equipment it has been found that company should acquire

the equipment as it will be profitable for the company.

QUESTION 2

a) Features of activity based costing system relative traditional costing system

Calculating accurate manufacturing costs for every products is vital for decision-making

for company. The activity based and traditional costing method both are based over ABC and

traditional costing method for allocation of indirect costs to the products. The methods estimates

3

overhead costs of production and also assign the costs to products based over cost driver rate.

Difference lies in complexity and accuracy of two methods. ABC is more accurate and assigns

the costs to the products based over arbitrary rating where traditional costing is simplistic but

also less accurate. ABC system is used for allocating the costs accurately on various resources

for making products. It increases number of cost pools for accumulating overhead costs where

traditional method only uses single cost pool and single predetermined rate over all the costs.

Number of pools are found on basis of cost driving activities (Alkaraan, 2017). Overhead costs

are charged to different products or jobs in proportion to cost driven activities in the place of

blanket rate based over direct labour cost or the direct machine hours. It also improves

traceability of different overhead costs that results in accurate and effective unit cost for decision

making.

Reasons for developing ABC system as alternative to traditional costing

Traditional method of costing assigns the overhead costs based over single rate. It made

cost allocations to activities at predetermined rate. ABC costing system assigns the overhead

costs based over different cost pool and activities which drive the cost. Traditional method is

useful only when manufacturing process is labour based and the overheads increases on the basis

of traditional activities like direct labour hours or machine hours. It was not effective for

organisations have multiple activities and operations (Kolawale and Grace, 2017). ABC costing

is very effective when manufacturing is technology driven and the overheads are increasing

based over different activities which differ over different activities which differ for every

product.

b) Key decisions break even and cost profit volume analysis can be used for making

Break Even Analysis

It is an effective tool that is used to analyse the number of products that needs to be sold

for variable and fixed cost of production. Identifying break even gives dynamic view of

relationship between the costs, sales and the profits. The break even analysis is point at which the

company has no profit no loss. Company starts earning profits after reaching the break even

point when it meets all the costs. It involves calculation of the contribution margin of products

by measuring the variable costs (Tran and Thao, 2020). It is an effective tool for financial

analysis.

4

Difference lies in complexity and accuracy of two methods. ABC is more accurate and assigns

the costs to the products based over arbitrary rating where traditional costing is simplistic but

also less accurate. ABC system is used for allocating the costs accurately on various resources

for making products. It increases number of cost pools for accumulating overhead costs where

traditional method only uses single cost pool and single predetermined rate over all the costs.

Number of pools are found on basis of cost driving activities (Alkaraan, 2017). Overhead costs

are charged to different products or jobs in proportion to cost driven activities in the place of

blanket rate based over direct labour cost or the direct machine hours. It also improves

traceability of different overhead costs that results in accurate and effective unit cost for decision

making.

Reasons for developing ABC system as alternative to traditional costing

Traditional method of costing assigns the overhead costs based over single rate. It made

cost allocations to activities at predetermined rate. ABC costing system assigns the overhead

costs based over different cost pool and activities which drive the cost. Traditional method is

useful only when manufacturing process is labour based and the overheads increases on the basis

of traditional activities like direct labour hours or machine hours. It was not effective for

organisations have multiple activities and operations (Kolawale and Grace, 2017). ABC costing

is very effective when manufacturing is technology driven and the overheads are increasing

based over different activities which differ over different activities which differ for every

product.

b) Key decisions break even and cost profit volume analysis can be used for making

Break Even Analysis

It is an effective tool that is used to analyse the number of products that needs to be sold

for variable and fixed cost of production. Identifying break even gives dynamic view of

relationship between the costs, sales and the profits. The break even analysis is point at which the

company has no profit no loss. Company starts earning profits after reaching the break even

point when it meets all the costs. It involves calculation of the contribution margin of products

by measuring the variable costs (Tran and Thao, 2020). It is an effective tool for financial

analysis.

4

It is used for making sales decisions like number of products to be sold for meeting the

costs and number of products for earning the desired profits. It is also useful for making

decisions related to margin of safety. Based on Break even analysis it can make decisions

regarding the sales prices and also the variable costs. It can analyse the profits at different price

levels. It helps the management in taking cost decisions regarding reducing the costs or

increasing sales price. It will help in making the business more efficient and effective and

earning higher returns.

Limitations of Break even analysis

It is costs only analysis and do not tells bout sales of products at different prices. The

method also assumes the variable cost as constant per product of output and at least in range for

likely quantities of the sales. It is based over unrealistic assumption regarding fixed selling price.

Also the changes are seen in fixed costs with change in output (Almeida and Cunha, 2017). Sales

are always different from output and this thing has to be considered in the calculations. Break

even analysis should be seen more as the planning tool rather than decision-making tool.

QUESTION 3

a) Budgeting as tool used for aiding control and the performance management

On of the major element in financial activities include budgeting. Budgeting could be

described as method for resource allocation to different activities and departments of the

business. Budgeting is essential for the business to ensure that all the resources are allocated as

per the requirements of different departments. Budgeting is important planning tool used by the

business to make the effective utilisation of the existing resources. There are different methods

of preparing the budget which includes traditional, activity and zero based method of budgeting.

Firms use budget on the basis of their business's nature and size (Talmon and Faliszewski,

2019). The budgeting helps in analysing in advance about the resources required for carrying out

the different business activities and operations. If available resources are not sufficient it can

arrange for funds using most appropriate sources with minimal costs.

Budgeting is an effective and useful tool for controlling the costs and expenditures of the

business. Budgets provide the departments or divisions with specific budgets within which they

have to carry out the operations. It ensures that departments do not make exceed the given

budget. It saves unnecessary costs and expenditures of the business so that it could be used for

more productive uses. After the budget variance analysis is carried out to identify the variations

5

costs and number of products for earning the desired profits. It is also useful for making

decisions related to margin of safety. Based on Break even analysis it can make decisions

regarding the sales prices and also the variable costs. It can analyse the profits at different price

levels. It helps the management in taking cost decisions regarding reducing the costs or

increasing sales price. It will help in making the business more efficient and effective and

earning higher returns.

Limitations of Break even analysis

It is costs only analysis and do not tells bout sales of products at different prices. The

method also assumes the variable cost as constant per product of output and at least in range for

likely quantities of the sales. It is based over unrealistic assumption regarding fixed selling price.

Also the changes are seen in fixed costs with change in output (Almeida and Cunha, 2017). Sales

are always different from output and this thing has to be considered in the calculations. Break

even analysis should be seen more as the planning tool rather than decision-making tool.

QUESTION 3

a) Budgeting as tool used for aiding control and the performance management

On of the major element in financial activities include budgeting. Budgeting could be

described as method for resource allocation to different activities and departments of the

business. Budgeting is essential for the business to ensure that all the resources are allocated as

per the requirements of different departments. Budgeting is important planning tool used by the

business to make the effective utilisation of the existing resources. There are different methods

of preparing the budget which includes traditional, activity and zero based method of budgeting.

Firms use budget on the basis of their business's nature and size (Talmon and Faliszewski,

2019). The budgeting helps in analysing in advance about the resources required for carrying out

the different business activities and operations. If available resources are not sufficient it can

arrange for funds using most appropriate sources with minimal costs.

Budgeting is an effective and useful tool for controlling the costs and expenditures of the

business. Budgets provide the departments or divisions with specific budgets within which they

have to carry out the operations. It ensures that departments do not make exceed the given

budget. It saves unnecessary costs and expenditures of the business so that it could be used for

more productive uses. After the budget variance analysis is carried out to identify the variations

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

between actual and budgeted outputs. On the basis of variance analysis report, management

frame the strategies for appropriate allocation and reducing the variances.

It also helps in performance evaluation and management. The budget target makes the

departments responsible to reach the objectives. Managers can take follow up of budgets

prepared for comparing actual outcomes with the managers. Any differences could be identified

in advance and corrections could be made timely (Chohan and Jacobs, 2018). They can

investigate the reasons of variations for taking the actions. Based on this managers can evaluate

the performance and establish procedures that will increase the efficiency of working process.

b) Limitations of traditional budgeting. Beyond Budgeting improving the planning system

Traditional method of budgeting is method used by number of companies for allocating

the resources and planning purposes. It is simple and easy method which is used from ancient

times. Though it is highly used but method is often criticised by the users for strong focus over

resource allocation and the inflexibility. It is not useful in complex business environment having

different business operations. The traditional method prepares budget based on previous budgets

of last year. It is kept as base for preparing the current year. Management analysing the current

trends make adjustments to the budget like inflation, demand and supply, economic environment.

It is not prepared by making complete analysis and just some adjustments are made to budget.

Traditional budget is prepared only by management and executives and made to comply by all

the departments. It makes disconnection with actual strategic plan of business and results in high

variations between the budgeted figures and actual outcomes. The traditional budgeting also do

not allow the company to assess the actual activities and is inefficient in organisation having

different process activities and those process that have high degree of changes. It is useful only

when production process do not see any changes.

Beyond Budgeting

Beyond budgeting refers to method of abolishing the process of traditional budgeting for

eventually improving the management control over the organisation. Abandoning the traditional

budgeting process company aim at establishing highly decentralised system and the adaptive sets

for management process. It involves re- examining the costs and expenditures about how they

could be managed better and improved (May, 2017). It focus over binding the people for a

common cause. It also focuses over shared values and making sound judgements for the benefit

of organisation in place of making rigid rules and regulations for the business. Beyond budgeting

6

frame the strategies for appropriate allocation and reducing the variances.

It also helps in performance evaluation and management. The budget target makes the

departments responsible to reach the objectives. Managers can take follow up of budgets

prepared for comparing actual outcomes with the managers. Any differences could be identified

in advance and corrections could be made timely (Chohan and Jacobs, 2018). They can

investigate the reasons of variations for taking the actions. Based on this managers can evaluate

the performance and establish procedures that will increase the efficiency of working process.

b) Limitations of traditional budgeting. Beyond Budgeting improving the planning system

Traditional method of budgeting is method used by number of companies for allocating

the resources and planning purposes. It is simple and easy method which is used from ancient

times. Though it is highly used but method is often criticised by the users for strong focus over

resource allocation and the inflexibility. It is not useful in complex business environment having

different business operations. The traditional method prepares budget based on previous budgets

of last year. It is kept as base for preparing the current year. Management analysing the current

trends make adjustments to the budget like inflation, demand and supply, economic environment.

It is not prepared by making complete analysis and just some adjustments are made to budget.

Traditional budget is prepared only by management and executives and made to comply by all

the departments. It makes disconnection with actual strategic plan of business and results in high

variations between the budgeted figures and actual outcomes. The traditional budgeting also do

not allow the company to assess the actual activities and is inefficient in organisation having

different process activities and those process that have high degree of changes. It is useful only

when production process do not see any changes.

Beyond Budgeting

Beyond budgeting refers to method of abolishing the process of traditional budgeting for

eventually improving the management control over the organisation. Abandoning the traditional

budgeting process company aim at establishing highly decentralised system and the adaptive sets

for management process. It involves re- examining the costs and expenditures about how they

could be managed better and improved (May, 2017). It focus over binding the people for a

common cause. It also focuses over shared values and making sound judgements for the benefit

of organisation in place of making rigid rules and regulations for the business. Beyond budgeting

6

analyses all the activities and the resources required for carrying out that process so that

resources could be allocated more effectively without sacrificing the quality of products and

services. It aims at improvising the products and services with optimum utilisation of the

business resources.

QUESTION 4

Sources of funds for SMEs

Financing is the process of providing funds to business to carry out its operation

effectively. In the current era Small Medium Enterprise (SME) can reach full potential only if

they get finance to start, sustain and grow. There are various sources through which SME can get

funds to meet its business objectives. These principal means through which small and medium

enterprise can get finance are Business angels, factoring and invoicing, leasing, bank finance,

venture capital, friends and family.

Own Funds

Business owners can bring their own funds for carrying out the operations of business.

These funds could be borrowed from friends or family. These could also be the personal savings

of owners that could be brought for business. The liability of own funds is unlimited and puts

extra pressure to generate adequate profits for making repayments if funds are borrowed from

others.

Angel Investors

Business angel refers to individuals that are willing to invest in SMEs by taking risk.

This option can be very useful for small and medium scale enterprise as they will get expertise in

turn of part of business (Shrotriya, 2019). These type of angel partners can provide contacts to

small businesses which will help the organization to grow. Angel partners can serve various

benefits to medium scale firm which includes minimal paperwork, building strategic ideas,

guidance and support. This option of financing might affect business concern by expecting high

share of organization, unclear roles and terms can be very ambiguous.

Bank Finance

For sourcing fund small and medium business can use option of bank financing. Such

organisation usually does not use this financing way as enterprise may not be able to pay the loan

back in case of medium term and long term. Moreover small business does not have such

collateral property in against of which they can take loan. Business units prefer short term

7

resources could be allocated more effectively without sacrificing the quality of products and

services. It aims at improvising the products and services with optimum utilisation of the

business resources.

QUESTION 4

Sources of funds for SMEs

Financing is the process of providing funds to business to carry out its operation

effectively. In the current era Small Medium Enterprise (SME) can reach full potential only if

they get finance to start, sustain and grow. There are various sources through which SME can get

funds to meet its business objectives. These principal means through which small and medium

enterprise can get finance are Business angels, factoring and invoicing, leasing, bank finance,

venture capital, friends and family.

Own Funds

Business owners can bring their own funds for carrying out the operations of business.

These funds could be borrowed from friends or family. These could also be the personal savings

of owners that could be brought for business. The liability of own funds is unlimited and puts

extra pressure to generate adequate profits for making repayments if funds are borrowed from

others.

Angel Investors

Business angel refers to individuals that are willing to invest in SMEs by taking risk.

This option can be very useful for small and medium scale enterprise as they will get expertise in

turn of part of business (Shrotriya, 2019). These type of angel partners can provide contacts to

small businesses which will help the organization to grow. Angel partners can serve various

benefits to medium scale firm which includes minimal paperwork, building strategic ideas,

guidance and support. This option of financing might affect business concern by expecting high

share of organization, unclear roles and terms can be very ambiguous.

Bank Finance

For sourcing fund small and medium business can use option of bank financing. Such

organisation usually does not use this financing way as enterprise may not be able to pay the loan

back in case of medium term and long term. Moreover small business does not have such

collateral property in against of which they can take loan. Business units prefer short term

7

financing from bank in form of overdraft which ease their process of sourcing easy and flexible.

SMEs can take various benefits from this option of sourcing fund like increasing reputation of

company as well as it gives competitive edge advantage.

Venture Capital

venture capital is a source of finance that allow small and medium scale business to start

their organisation. It generally comes from financial institution, investment bank and well off

investors. It is necessary that venture capital take form in monetary, it can also come in way of

technicals and managerial proposal. It is good source of finance for SME as they get many

benefits through this options such as valuable guidance, helpful in building system and relation,

easy expansion etc. there are disadvantages also that business face are weakening of ownership

and control and it may also result in lead undervaluation

Factoring and Invoice Discounting

Both of these option helps organization to get fund in against of documents related to

outstanding receivables. The biggest benefit that organization get through this option is their

outstanding receivables increases as business concern grows which allow them to factor or

discount invoicing more than previous (Huang, Yang and Tu, 2020). However it is expensive

from overdraft but can be use by SMEs in case of urgency. It might decrease its profit that can

make it more volatile.

Leasing

It is good option to lease an asset rather than buying it as it reduced requirement of

capital. It provides benefits to enterprise of maintaining its cash outflow, low capital expenditure,

tax benefits and better planning (Gong and et.al., 2020). Some drawbacks that SMEs face due to

leasing includes maintenance of assets, no ownership and lease expenses.

Supply chain Financing

Supply chain financing is technique and tool used by banks to control capital invested to

minimizes risk for involved parties. It provides merits of good buyer-suppler

relationship,increased liquidity, improved efficiency, cash flow control,good credit rating and

flexibility (Liu, Zhang and Xiong). On other side it has demerit like mismanage and inadequate

implementation which affect the organisation negatively.

Above mentioned are the means of finance for small and medium enterprise which help

business to start their operations, sustain in market and grow in industry. These options of

8

SMEs can take various benefits from this option of sourcing fund like increasing reputation of

company as well as it gives competitive edge advantage.

Venture Capital

venture capital is a source of finance that allow small and medium scale business to start

their organisation. It generally comes from financial institution, investment bank and well off

investors. It is necessary that venture capital take form in monetary, it can also come in way of

technicals and managerial proposal. It is good source of finance for SME as they get many

benefits through this options such as valuable guidance, helpful in building system and relation,

easy expansion etc. there are disadvantages also that business face are weakening of ownership

and control and it may also result in lead undervaluation

Factoring and Invoice Discounting

Both of these option helps organization to get fund in against of documents related to

outstanding receivables. The biggest benefit that organization get through this option is their

outstanding receivables increases as business concern grows which allow them to factor or

discount invoicing more than previous (Huang, Yang and Tu, 2020). However it is expensive

from overdraft but can be use by SMEs in case of urgency. It might decrease its profit that can

make it more volatile.

Leasing

It is good option to lease an asset rather than buying it as it reduced requirement of

capital. It provides benefits to enterprise of maintaining its cash outflow, low capital expenditure,

tax benefits and better planning (Gong and et.al., 2020). Some drawbacks that SMEs face due to

leasing includes maintenance of assets, no ownership and lease expenses.

Supply chain Financing

Supply chain financing is technique and tool used by banks to control capital invested to

minimizes risk for involved parties. It provides merits of good buyer-suppler

relationship,increased liquidity, improved efficiency, cash flow control,good credit rating and

flexibility (Liu, Zhang and Xiong). On other side it has demerit like mismanage and inadequate

implementation which affect the organisation negatively.

Above mentioned are the means of finance for small and medium enterprise which help

business to start their operations, sustain in market and grow in industry. These options of

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

sourcing fund have its own advantages and disadvantage that impact concern enterprise in both

positive and negative manner.

QUESTION 5

Corporate Social Responsibility including the benefits of stakeholders

Corporate social responsibility refers to that corporate activates that are taken by

businesses to influence society and stakeholders positively. Stakeholders are those who have

interest in operations of organisation and get affected from their decision-making process.

Stakeholders include employees, customers, society etc.

Responsibility related to employees

First responsibility of any organization is to generate employment opportunities. Keeping

employees happy by giving them derivable remuneration is part of corporate responsibility of

business (Abbas, 2020). In addition to this providing clean, safe and suitable environment to

employees is primary responsibility of organization. There are some rules and regulations also

that government has made regarding employment generation which every enterprise need to

fulfil.

Responsibility related to customers

To be a successful organization fulfilling customers needs become essential activity for

business. Moreover, providing goods and service with standard quality is primary responsibility

of every business. It also helps organisation to attract customers attention by making them

believe that organization is concern about their health. By completing corporate responsibility

company gain trust of customers as well as.

Responsibility to society

Business provide job, service and products to society so it must be adhered responsibility

related to it. The tax that company pay are used by government for formation of schools, better

infrastructure and hospital. There are various companies that also take initiation for charity and

formation of infrastructure that are essential for day to day life of common people. Some

responsibilities include activities of legal accountability, public transparency and environmental

performance in turn which allow company to use resources for production of goods. Company

can not perform good until it fulfil its corporate responsibility as it is dependent on society for

employees, customers, suppliers, investors, lenders etc.

Responsibility of environment protection

9

positive and negative manner.

QUESTION 5

Corporate Social Responsibility including the benefits of stakeholders

Corporate social responsibility refers to that corporate activates that are taken by

businesses to influence society and stakeholders positively. Stakeholders are those who have

interest in operations of organisation and get affected from their decision-making process.

Stakeholders include employees, customers, society etc.

Responsibility related to employees

First responsibility of any organization is to generate employment opportunities. Keeping

employees happy by giving them derivable remuneration is part of corporate responsibility of

business (Abbas, 2020). In addition to this providing clean, safe and suitable environment to

employees is primary responsibility of organization. There are some rules and regulations also

that government has made regarding employment generation which every enterprise need to

fulfil.

Responsibility related to customers

To be a successful organization fulfilling customers needs become essential activity for

business. Moreover, providing goods and service with standard quality is primary responsibility

of every business. It also helps organisation to attract customers attention by making them

believe that organization is concern about their health. By completing corporate responsibility

company gain trust of customers as well as.

Responsibility to society

Business provide job, service and products to society so it must be adhered responsibility

related to it. The tax that company pay are used by government for formation of schools, better

infrastructure and hospital. There are various companies that also take initiation for charity and

formation of infrastructure that are essential for day to day life of common people. Some

responsibilities include activities of legal accountability, public transparency and environmental

performance in turn which allow company to use resources for production of goods. Company

can not perform good until it fulfil its corporate responsibility as it is dependent on society for

employees, customers, suppliers, investors, lenders etc.

Responsibility of environment protection

9

Business is responsible to accomplishing its duty of environment protection by taking

major actions. Resources of world are limited so using them in appropriate manner become must

for enterprises. Resources like plants, animals, metals etc. should not be use abundantly so that

upcoming generation can utilize them (Ali, Danish and Asrar‐ul‐Haq, 2020). Stakeholders

support those businesses that adhere its responsibility related to environment as people are aware

of nature's importance. Government of every company have made strict standards affiliated to

environment so that company feel fear of strict action. Many parties have conducted research on

importance of environment which encouraged companies to spread less pollution.

These are areas where firm should focus for fulfilling social responsibility to maintain

interest of stakeholders in organisation and to cope up with government regulations related to

corporate obligation.

10

major actions. Resources of world are limited so using them in appropriate manner become must

for enterprises. Resources like plants, animals, metals etc. should not be use abundantly so that

upcoming generation can utilize them (Ali, Danish and Asrar‐ul‐Haq, 2020). Stakeholders

support those businesses that adhere its responsibility related to environment as people are aware

of nature's importance. Government of every company have made strict standards affiliated to

environment so that company feel fear of strict action. Many parties have conducted research on

importance of environment which encouraged companies to spread less pollution.

These are areas where firm should focus for fulfilling social responsibility to maintain

interest of stakeholders in organisation and to cope up with government regulations related to

corporate obligation.

10

REFERENCES

Books and Journals

Abbas, J., 2020. Impact of total quality management on corporate green performance through the

mediating role of corporate social responsibility. Journal of Cleaner Production. 242.

p.118458.

Ali, H. Y., Danish, R. Q. and Asrar‐ul‐Haq, M., 2020. How corporate social responsibility boosts

firm financial performance: The mediating role of corporate image and customer

satisfaction. Corporate Social Responsibility and Environmental Management. 27(1).

pp.166-177.

Alkaraan, F., 2017. Strategic investment appraisal: multidisciplinary perspectives. In Advances

in Mergers and Acquisitions. Emerald Publishing Limited.

Almeida, A. and Cunha, J., 2017. The implementation of an Activity-Based Costing (ABC)

system in a manufacturing company. Procedia manufacturing. 13. pp.932-939.

Brown, R. and Rocha, A., 2020. Entrepreneurial uncertainty during the Covid-19 crisis:

Mapping the temporal dynamics of entrepreneurial finance. Journal of Business

Venturing Insights. 14. p.e00174.

Budhathoki, P.B. and Rai, C.K., 2020. The Impact of the Debt Ratio, Total Assets, and Earning

Growth Rate on WACC: Evidence from Nepalese Commercial Banks. Asian Journal of

Economics, Business and Accounting. pp.16-23.

Chohan, U.W. and Jacobs, K., 2018. Public Value as Rhetoric: a budgeting

approach. International Journal of Public Administration, 41(15), pp.1217-1227.

Fernandez, P., 2019. WACC and CAPM according to Utilities Regulators: Confusions, Errors

and Inconsistencies. Errors and Inconsistencies (February 19, 2019).

Gong, D. and et.al., 2020. Who benefits from online financing? A sharing economy E-tailing

platform perspective. International Journal of Production Economics. 222. p.107490.

Huang, J., Yang, W. and Tu, Y., 2020. Financing mode decision in a supply chain with financial

constraint. International Journal of Production Economics. 220. p.107441.

Kolawale, O.A. and Grace, O.O.B., 2017. Assessment of viability appraisal practice by estate

surveyors and valuers in lagos metropolis, Nigeria. International Journal of Built

Environment and Sustainability. 4(1).

Liu, W., Zhang, Y. and Xiong, W., 2020. Financing the Belt and Road Initiative. Eurasian

Geography and Economics. 61(2). pp.137-145.

May, A.U., 2017. Traditional budgeting in today’s business environment. Journal of Applied

Finance & Banking. 7(3). pp.111-120.

Shrotriya, D. V., 2019. Internal sources of finance for business organizations. International

Journal of Research and Analytical Reviews. 6(2). pp.933-940.

Talmon, N. and Faliszewski, P., 2019, July. A framework for approval-based budgeting methods.

In Proceedings of the AAAI Conference on Artificial Intelligence (Vol. 33, No. 01, pp.

2181-2188).

Tran, T. and Thao, N., 2020. Factors affecting the application of ABC costing method in

manufacturing firms in Vietnam. Management Science Letters. 10(11). pp.2625-2634.

11

Books and Journals

Abbas, J., 2020. Impact of total quality management on corporate green performance through the

mediating role of corporate social responsibility. Journal of Cleaner Production. 242.

p.118458.

Ali, H. Y., Danish, R. Q. and Asrar‐ul‐Haq, M., 2020. How corporate social responsibility boosts

firm financial performance: The mediating role of corporate image and customer

satisfaction. Corporate Social Responsibility and Environmental Management. 27(1).

pp.166-177.

Alkaraan, F., 2017. Strategic investment appraisal: multidisciplinary perspectives. In Advances

in Mergers and Acquisitions. Emerald Publishing Limited.

Almeida, A. and Cunha, J., 2017. The implementation of an Activity-Based Costing (ABC)

system in a manufacturing company. Procedia manufacturing. 13. pp.932-939.

Brown, R. and Rocha, A., 2020. Entrepreneurial uncertainty during the Covid-19 crisis:

Mapping the temporal dynamics of entrepreneurial finance. Journal of Business

Venturing Insights. 14. p.e00174.

Budhathoki, P.B. and Rai, C.K., 2020. The Impact of the Debt Ratio, Total Assets, and Earning

Growth Rate on WACC: Evidence from Nepalese Commercial Banks. Asian Journal of

Economics, Business and Accounting. pp.16-23.

Chohan, U.W. and Jacobs, K., 2018. Public Value as Rhetoric: a budgeting

approach. International Journal of Public Administration, 41(15), pp.1217-1227.

Fernandez, P., 2019. WACC and CAPM according to Utilities Regulators: Confusions, Errors

and Inconsistencies. Errors and Inconsistencies (February 19, 2019).

Gong, D. and et.al., 2020. Who benefits from online financing? A sharing economy E-tailing

platform perspective. International Journal of Production Economics. 222. p.107490.

Huang, J., Yang, W. and Tu, Y., 2020. Financing mode decision in a supply chain with financial

constraint. International Journal of Production Economics. 220. p.107441.

Kolawale, O.A. and Grace, O.O.B., 2017. Assessment of viability appraisal practice by estate

surveyors and valuers in lagos metropolis, Nigeria. International Journal of Built

Environment and Sustainability. 4(1).

Liu, W., Zhang, Y. and Xiong, W., 2020. Financing the Belt and Road Initiative. Eurasian

Geography and Economics. 61(2). pp.137-145.

May, A.U., 2017. Traditional budgeting in today’s business environment. Journal of Applied

Finance & Banking. 7(3). pp.111-120.

Shrotriya, D. V., 2019. Internal sources of finance for business organizations. International

Journal of Research and Analytical Reviews. 6(2). pp.933-940.

Talmon, N. and Faliszewski, P., 2019, July. A framework for approval-based budgeting methods.

In Proceedings of the AAAI Conference on Artificial Intelligence (Vol. 33, No. 01, pp.

2181-2188).

Tran, T. and Thao, N., 2020. Factors affecting the application of ABC costing method in

manufacturing firms in Vietnam. Management Science Letters. 10(11). pp.2625-2634.

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.