Financial Management: Investment Appraisal Techniques and Valuation Models

VerifiedAdded on 2023/06/14

|13

|3693

|311

AI Summary

This report discusses practical solutions for financial management, including investment appraisal techniques and valuation models. It evaluates the effects of proposals on the company and the benefits and limitations of different investment appraisal techniques. The report also includes a valuation of Dragon Plc using different models such as price earning method and discounted cash flow method.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL

MANAGEMENT

MANAGEMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Question No 2. Various Investment Appraisal Techniques and their recommendation..............3

a) Evaluation of projects considering the following models and their recommendations: -.......3

b) Evaluation of the effects of the proposal on the company: -...................................................6

c) Benefits and limitation of the different investment appraisal techniques used in decision

making.........................................................................................................................................6

Question No 3 Valuation of Dragon Plc. using different Valuation Models along with

Recommendation on Proposed Investment.................................................................................9

a) Price Earning Method: -..........................................................................................................9

b) Discounted Cash Flow Method: -............................................................................................9

c) Dividend Valuation Method: -...............................................................................................10

d) Problems associated with the above models along with recommendation to Kings Plc. with

respect to proposed acquisition..................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Question No 2. Various Investment Appraisal Techniques and their recommendation..............3

a) Evaluation of projects considering the following models and their recommendations: -.......3

b) Evaluation of the effects of the proposal on the company: -...................................................6

c) Benefits and limitation of the different investment appraisal techniques used in decision

making.........................................................................................................................................6

Question No 3 Valuation of Dragon Plc. using different Valuation Models along with

Recommendation on Proposed Investment.................................................................................9

a) Price Earning Method: -..........................................................................................................9

b) Discounted Cash Flow Method: -............................................................................................9

c) Dividend Valuation Method: -...............................................................................................10

d) Problems associated with the above models along with recommendation to Kings Plc. with

respect to proposed acquisition..................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial management refers to preparation, categorising, guiding and monitoring of

financial activities in an establishment or an institute. It includes certain principles of

management which helps in operative and resourceful deployment of financial resources that is

useful in achieving goals and objectives to the corporate (Amel-Zadeh and Meeks, 2020). It is a

process of dealing with management of finance in an organisation in an effective way

considering time management also. This report includes practical solution with respect to

calculation of cost of capital taking into consideration historical value figures and market value

figures in capital structure. Further it involves practical approach with respect to recalculating the

cost of capital if an entity incorporates more debt in their capital structure and repurchase

ordinary shares from the market in order to cancel them. Another practical question is addressed

which consist of valuation of Dragon plc considering different models such as price earnings

ratio, Dividend valuation model etc.

TASK

Question No 2. Various Investment Appraisal Techniques and their recommendation.

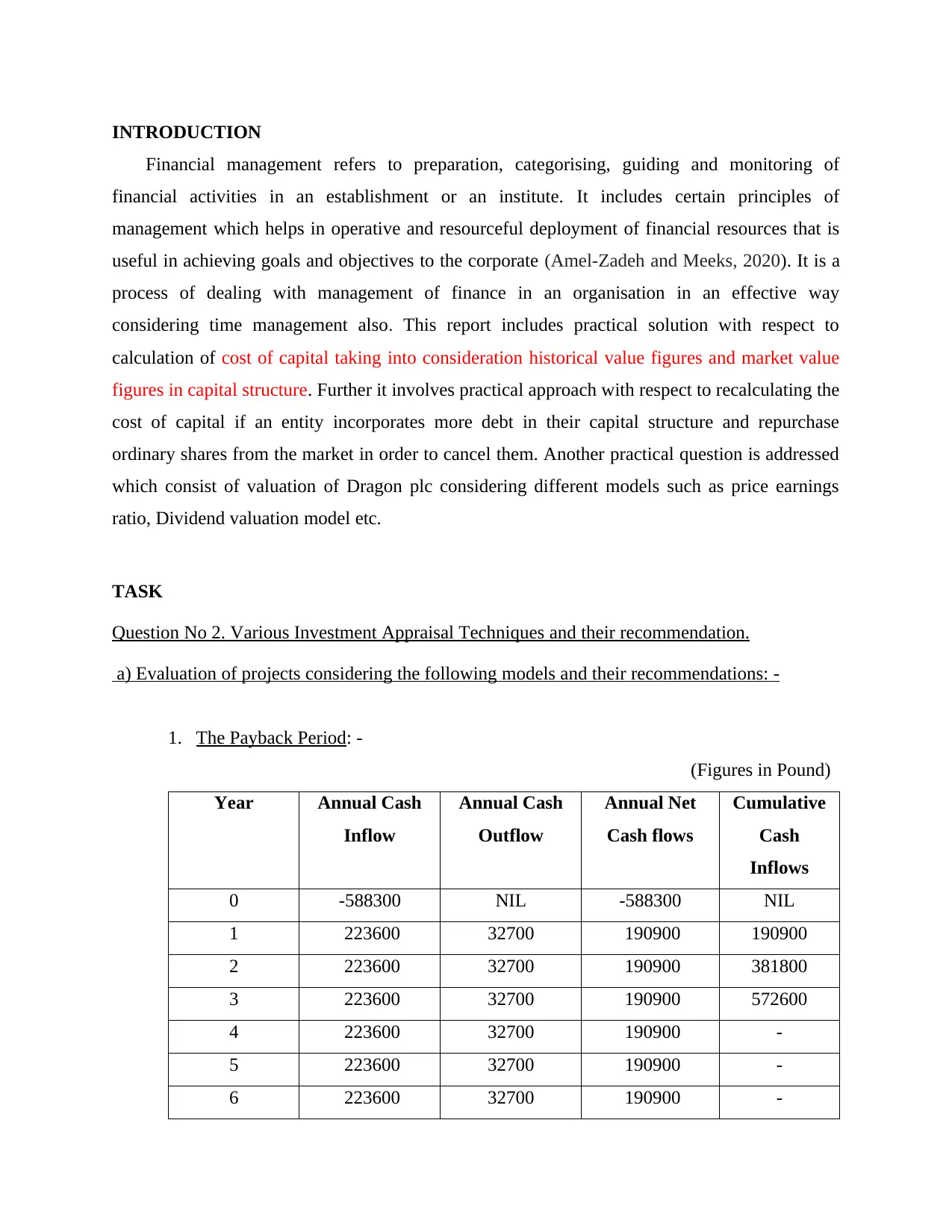

a) Evaluation of projects considering the following models and their recommendations: -

1. The Payback Period: -

(Figures in Pound)

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net

Cash flows

Cumulative

Cash

Inflows

0 -588300 NIL -588300 NIL

1 223600 32700 190900 190900

2 223600 32700 190900 381800

3 223600 32700 190900 572600

4 223600 32700 190900 -

5 223600 32700 190900 -

6 223600 32700 190900 -

Financial management refers to preparation, categorising, guiding and monitoring of

financial activities in an establishment or an institute. It includes certain principles of

management which helps in operative and resourceful deployment of financial resources that is

useful in achieving goals and objectives to the corporate (Amel-Zadeh and Meeks, 2020). It is a

process of dealing with management of finance in an organisation in an effective way

considering time management also. This report includes practical solution with respect to

calculation of cost of capital taking into consideration historical value figures and market value

figures in capital structure. Further it involves practical approach with respect to recalculating the

cost of capital if an entity incorporates more debt in their capital structure and repurchase

ordinary shares from the market in order to cancel them. Another practical question is addressed

which consist of valuation of Dragon plc considering different models such as price earnings

ratio, Dividend valuation model etc.

TASK

Question No 2. Various Investment Appraisal Techniques and their recommendation.

a) Evaluation of projects considering the following models and their recommendations: -

1. The Payback Period: -

(Figures in Pound)

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net

Cash flows

Cumulative

Cash

Inflows

0 -588300 NIL -588300 NIL

1 223600 32700 190900 190900

2 223600 32700 190900 381800

3 223600 32700 190900 572600

4 223600 32700 190900 -

5 223600 32700 190900 -

6 223600 32700 190900 -

6 (S.V) 88245 NIL 88245 -

Payback period will be: -

= 3 Years + (588300-572600) / 190900

= 3 Years + 15700/190900

= 3.08 Years.

Note: - Depreciation is the non-cash expense, since tax rate is not given in the question

hence it is ignored while decision making.

2. The Average Rate of Return: -

= Annual Average Profits / Cost of Investments * 100

= 205607.50 / 588300 * 100

= 34.95 %

Note: - Since average annual profits is not given in the question hence we have

considered average cash inflows as average profits.

3. The Net Present Value: -

Years Net Cash Inflows Discounting @ 10% PV of Cash Inflows

1 190900 .909 173528.10

2 190900 .826 157683.40

3 190900 .751 143365.90

4 190900 .683 130384.70

5 190900 .621 118548.90

6 190900 .564 107667.60

6 (S.V) 88245 .564 49770.18

PV of Cash Inflow

(A)

880948.78

PV of Cash Outflow

(B)

588300

Payback period will be: -

= 3 Years + (588300-572600) / 190900

= 3 Years + 15700/190900

= 3.08 Years.

Note: - Depreciation is the non-cash expense, since tax rate is not given in the question

hence it is ignored while decision making.

2. The Average Rate of Return: -

= Annual Average Profits / Cost of Investments * 100

= 205607.50 / 588300 * 100

= 34.95 %

Note: - Since average annual profits is not given in the question hence we have

considered average cash inflows as average profits.

3. The Net Present Value: -

Years Net Cash Inflows Discounting @ 10% PV of Cash Inflows

1 190900 .909 173528.10

2 190900 .826 157683.40

3 190900 .751 143365.90

4 190900 .683 130384.70

5 190900 .621 118548.90

6 190900 .564 107667.60

6 (S.V) 88245 .564 49770.18

PV of Cash Inflow

(A)

880948.78

PV of Cash Outflow

(B)

588300

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

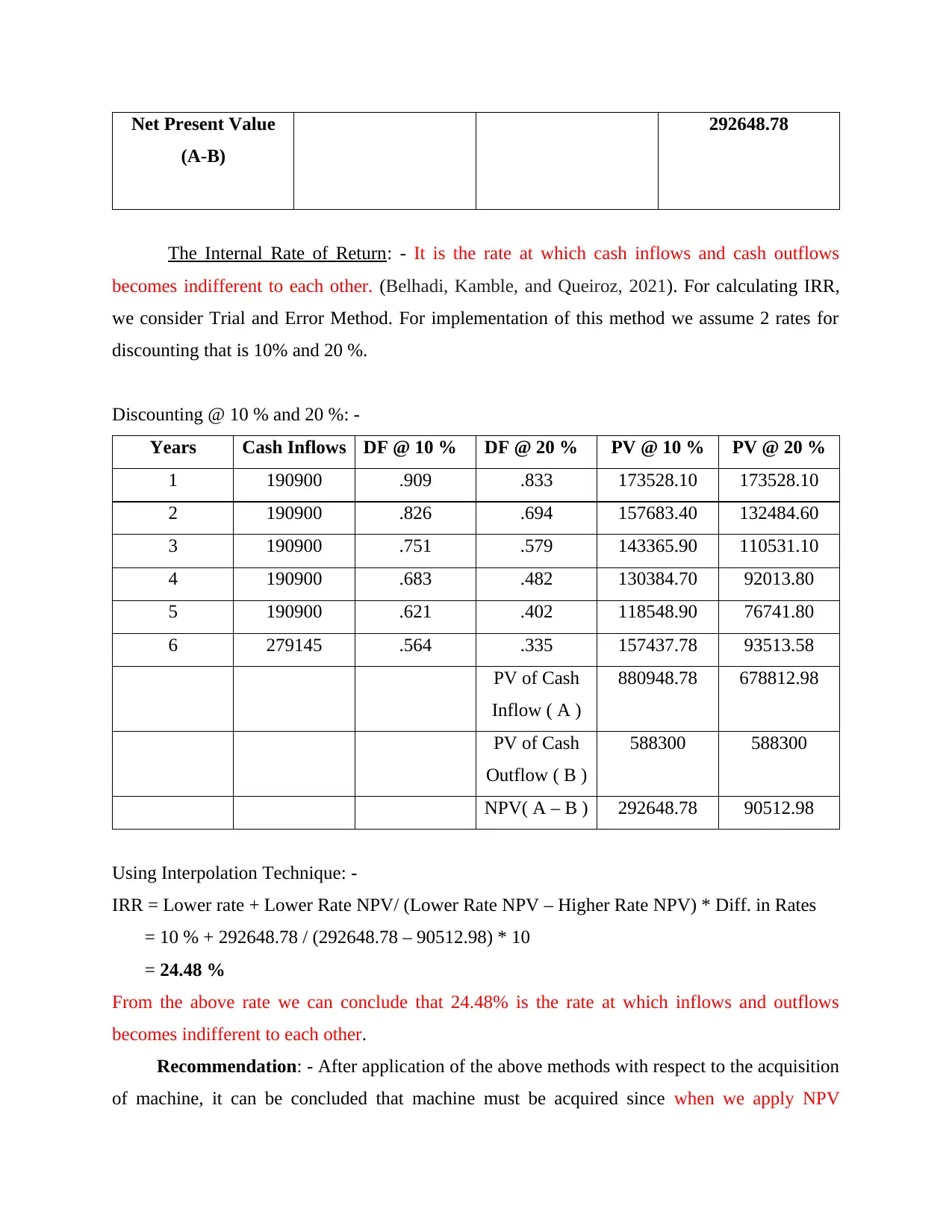

Net Present Value

(A-B)

292648.78

The Internal Rate of Return: - It is the rate at which cash inflows and cash outflows

becomes indifferent to each other. (Belhadi, Kamble, and Queiroz, 2021). For calculating IRR,

we consider Trial and Error Method. For implementation of this method we assume 2 rates for

discounting that is 10% and 20 %.

Discounting @ 10 % and 20 %: -

Years Cash Inflows DF @ 10 % DF @ 20 % PV @ 10 % PV @ 20 %

1 190900 .909 .833 173528.10 173528.10

2 190900 .826 .694 157683.40 132484.60

3 190900 .751 .579 143365.90 110531.10

4 190900 .683 .482 130384.70 92013.80

5 190900 .621 .402 118548.90 76741.80

6 279145 .564 .335 157437.78 93513.58

PV of Cash

Inflow ( A )

880948.78 678812.98

PV of Cash

Outflow ( B )

588300 588300

NPV( A – B ) 292648.78 90512.98

Using Interpolation Technique: -

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in Rates

= 10 % + 292648.78 / (292648.78 – 90512.98) * 10

= 24.48 %

From the above rate we can conclude that 24.48% is the rate at which inflows and outflows

becomes indifferent to each other.

Recommendation: - After application of the above methods with respect to the acquisition

of machine, it can be concluded that machine must be acquired since when we apply NPV

(A-B)

292648.78

The Internal Rate of Return: - It is the rate at which cash inflows and cash outflows

becomes indifferent to each other. (Belhadi, Kamble, and Queiroz, 2021). For calculating IRR,

we consider Trial and Error Method. For implementation of this method we assume 2 rates for

discounting that is 10% and 20 %.

Discounting @ 10 % and 20 %: -

Years Cash Inflows DF @ 10 % DF @ 20 % PV @ 10 % PV @ 20 %

1 190900 .909 .833 173528.10 173528.10

2 190900 .826 .694 157683.40 132484.60

3 190900 .751 .579 143365.90 110531.10

4 190900 .683 .482 130384.70 92013.80

5 190900 .621 .402 118548.90 76741.80

6 279145 .564 .335 157437.78 93513.58

PV of Cash

Inflow ( A )

880948.78 678812.98

PV of Cash

Outflow ( B )

588300 588300

NPV( A – B ) 292648.78 90512.98

Using Interpolation Technique: -

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in Rates

= 10 % + 292648.78 / (292648.78 – 90512.98) * 10

= 24.48 %

From the above rate we can conclude that 24.48% is the rate at which inflows and outflows

becomes indifferent to each other.

Recommendation: - After application of the above methods with respect to the acquisition

of machine, it can be concluded that machine must be acquired since when we apply NPV

method, the net present value is positive. Further when we apply Pay Back Period the pay back

arrives 3 years approx. which shows that the amount of investment we made at the beginning of

the year is recovered completely in 3 years itself. However, the life of the machine is 6 years,

therefore it is beneficial to acquire it from this method also. We also implement average rate of

return method to evaluate the proposal after taking certain assumptions, the ARR is 34.95%

which is considered to be good considering the proposal.

b) Evaluation of the effects of the proposal on the company: -

When STS limited repurchase some of its equity shares from the market using 40 % of the

cash outlay which is Pound 235320 (40% of 588300) then it will be regarded as a positive sign

because it means that STS believed that their shares are undervalued and they believed that the

price of the share will increase in future along with valuation of the entity. A repurchase of share

is also known as float shrink because it reduces the company’s number of freely trading shares.

Further when company pay cash dividend to its shareholders then it will increase the trust of

shareholders in the company. Payment of Dividend to equity holders on annual basis will

increase market share of the organisation is the stock market. However, it will make an impact

on the EPS of the company as due to buyback, the number of equity shares outstanding reduces

and it will ultimately affect the EPS by reducing it since the denominator while calculating the

same reduced. Repurchase of shares and payment of cash dividends to shareholders are the

alternate measures for the business concern to make payment to the shareholders, dividend

represents the current payment to an investor while the share buyback represents the future

payment. Further there is another implication of the above proposal that is payment of dividend

distribution tax to the government by the enterprise. However, as an overall consideration this

proposal can be considered to be better in building the net worth of the organisation over the

period of time. They do carry more uncertainty then payment of dividends as the buyback value

depends upon the stock future price.

c) Benefits and limitation of the different investment appraisal techniques used in decision

making.

Payback Period: It is used to calculate the time taken to recover the amount spent on the

investment of starting a new project (Bi and Wang, 2018). It is the amount of the initial

arrives 3 years approx. which shows that the amount of investment we made at the beginning of

the year is recovered completely in 3 years itself. However, the life of the machine is 6 years,

therefore it is beneficial to acquire it from this method also. We also implement average rate of

return method to evaluate the proposal after taking certain assumptions, the ARR is 34.95%

which is considered to be good considering the proposal.

b) Evaluation of the effects of the proposal on the company: -

When STS limited repurchase some of its equity shares from the market using 40 % of the

cash outlay which is Pound 235320 (40% of 588300) then it will be regarded as a positive sign

because it means that STS believed that their shares are undervalued and they believed that the

price of the share will increase in future along with valuation of the entity. A repurchase of share

is also known as float shrink because it reduces the company’s number of freely trading shares.

Further when company pay cash dividend to its shareholders then it will increase the trust of

shareholders in the company. Payment of Dividend to equity holders on annual basis will

increase market share of the organisation is the stock market. However, it will make an impact

on the EPS of the company as due to buyback, the number of equity shares outstanding reduces

and it will ultimately affect the EPS by reducing it since the denominator while calculating the

same reduced. Repurchase of shares and payment of cash dividends to shareholders are the

alternate measures for the business concern to make payment to the shareholders, dividend

represents the current payment to an investor while the share buyback represents the future

payment. Further there is another implication of the above proposal that is payment of dividend

distribution tax to the government by the enterprise. However, as an overall consideration this

proposal can be considered to be better in building the net worth of the organisation over the

period of time. They do carry more uncertainty then payment of dividends as the buyback value

depends upon the stock future price.

c) Benefits and limitation of the different investment appraisal techniques used in decision

making.

Payback Period: It is used to calculate the time taken to recover the amount spent on the

investment of starting a new project (Bi and Wang, 2018). It is the amount of the initial

investment divided by the net cash inflows. The project with the shortest time period is selected

and make a decision.

Pros Cons

It is very unpretentious to estimate as it

ponders only the annual cash flows over the

years and the initial cost on the project

(Bielstein, Fischer, and Kaserer, 2018).

It ignores the value of time and earn an

additional return on it if it is reinvested.

When the rapid changes occur in the industry

due to the technical modifications, it is hard to

project the cash flows for future. In this

circumstance, the payback period helps in

ascertaining the chance of loss and helps in

reducing the risk.

In the case of the even and uneven cash flows

over the years, this method only takes into

consideration till the time the initial cost of

capital is recovered.

Accounting Rate of Return: It depicts the pace of the rate of yield anticipated on the

initial investment or on the resources which is distinguished with the value of the investment in

the commencement of the project. It divides the average value of the cash inflows by the average

investment of the organisation for deriving the return on the project over the anticipated project

life over the years.

Benefits Demerits

It is very unassuming to work out and to

comprehend the project’s life. But the ARR

thinks of the benefits it can give to the funds

of the investment for the whole existence of

the resources in the monetary terms.

The outcomes are unique assuming it

computes the rate of term on the investment

as well as the ARR. Therefore, it creates a

confusion in making decisions.

This technique is considering all the

profitability which the project gains over the

period of time and helps in measuring the

existing performance of the tasks.

It is irrelevant for the projects which is made

at the different time periods and also ignore

the factor called time.

and make a decision.

Pros Cons

It is very unpretentious to estimate as it

ponders only the annual cash flows over the

years and the initial cost on the project

(Bielstein, Fischer, and Kaserer, 2018).

It ignores the value of time and earn an

additional return on it if it is reinvested.

When the rapid changes occur in the industry

due to the technical modifications, it is hard to

project the cash flows for future. In this

circumstance, the payback period helps in

ascertaining the chance of loss and helps in

reducing the risk.

In the case of the even and uneven cash flows

over the years, this method only takes into

consideration till the time the initial cost of

capital is recovered.

Accounting Rate of Return: It depicts the pace of the rate of yield anticipated on the

initial investment or on the resources which is distinguished with the value of the investment in

the commencement of the project. It divides the average value of the cash inflows by the average

investment of the organisation for deriving the return on the project over the anticipated project

life over the years.

Benefits Demerits

It is very unassuming to work out and to

comprehend the project’s life. But the ARR

thinks of the benefits it can give to the funds

of the investment for the whole existence of

the resources in the monetary terms.

The outcomes are unique assuming it

computes the rate of term on the investment

as well as the ARR. Therefore, it creates a

confusion in making decisions.

This technique is considering all the

profitability which the project gains over the

period of time and helps in measuring the

existing performance of the tasks.

It is irrelevant for the projects which is made

at the different time periods and also ignore

the factor called time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Present Value: It is an investment performance measure broadly utilized in money

and business land. It means distinguishing between the present worth of the cash inflows and the

cash outflows (Howe, 2019). NPV lets a financial backer know whether the venture is

accomplishing an objective yield at a given beginning of the initial investment.

Benefits Demerits

It considers the risk factor of the project and

is concerned about the wealth of the

shareholder by taking the whole life of the

project in computing.

It is very troublesome to understand this

method by the manages s it is difficult to

predict the accurate discounting rate for the

project (Jory, Ngo, and Susnjara, 2020).

It considers the worth of time and money by

considering the discounted cash are

calculated, which in turn minimises the risk

and give a better forecasted result.

It is relied on the anticipation mainly and it

increases the possibility of error. The factors

which are assumed are the returns, prevent

factors and the investment costs.

Internal Rate of Return: It is a measurement utilized in monetary investigation to

assess the productivity of expected ventures. It is a rebate rate that makes the NPV of all incomes

equivalent to focus in a limited income investigation.

Benefits Demerits

It considering the factor called time and the

money and is easy to compute and

understand. It is considering when the IRR is

greater in with minimum acceptable costs of

the capital.

It is worrisome in the cases when the projects

of different time periods and the rate of return

is difficult to be presumed, which in turn is

hard to make choices (Khan, Pal, and Saeed,

2018).

It uses all the cash flows over the time period

of the time and considers the time value of the

money of the project. It helps in knowing the

return on the investment which has been done

originally.

It does not take into consideration the cost of

capital, which is significant as it can be

utilised to contrast the project on the basis of

different time durations.

and business land. It means distinguishing between the present worth of the cash inflows and the

cash outflows (Howe, 2019). NPV lets a financial backer know whether the venture is

accomplishing an objective yield at a given beginning of the initial investment.

Benefits Demerits

It considers the risk factor of the project and

is concerned about the wealth of the

shareholder by taking the whole life of the

project in computing.

It is very troublesome to understand this

method by the manages s it is difficult to

predict the accurate discounting rate for the

project (Jory, Ngo, and Susnjara, 2020).

It considers the worth of time and money by

considering the discounted cash are

calculated, which in turn minimises the risk

and give a better forecasted result.

It is relied on the anticipation mainly and it

increases the possibility of error. The factors

which are assumed are the returns, prevent

factors and the investment costs.

Internal Rate of Return: It is a measurement utilized in monetary investigation to

assess the productivity of expected ventures. It is a rebate rate that makes the NPV of all incomes

equivalent to focus in a limited income investigation.

Benefits Demerits

It considering the factor called time and the

money and is easy to compute and

understand. It is considering when the IRR is

greater in with minimum acceptable costs of

the capital.

It is worrisome in the cases when the projects

of different time periods and the rate of return

is difficult to be presumed, which in turn is

hard to make choices (Khan, Pal, and Saeed,

2018).

It uses all the cash flows over the time period

of the time and considers the time value of the

money of the project. It helps in knowing the

return on the investment which has been done

originally.

It does not take into consideration the cost of

capital, which is significant as it can be

utilised to contrast the project on the basis of

different time durations.

Question No 3 Valuation of Dragon Plc. using different Valuation Models along with

Recommendation on Proposed Investment.

a) Price Earning Method: -

This method shows the association between the enterprise stock price and earning per

share. It is a very widespread ratio that gives the stockholder a better logic of the value of

the business concern (Marqués, García, and Sánchez, 2020). This ratio shows the

probability of the market and price per share an investor pays per unit on the current

earning of the company. Profits are important when valuation is made for the entity

because investors want to know that how profitable an enterprise is in current accounting

period and what profits they will generate in future. It can be interpreted as the number of

years it will take for the organisation to pay back the amount paid for each share.

Price earning ratio = MPS / EPS

P.E Ratio of the Kings Plc is as under: -

= 4.15 / .29

= 14.31 Times

Value of Dragon Plc. will be calculated using P.E Ratio of Kings Plc as under: -

= EPS of Dragon Plc * P.E Ratio of Kings Plc

= 40.40 / 145 * 14.31

= £M 3.99

b) Discounted Cash Flow Method: -

This method used by the organisation to value the proposed business model they want to

acquire. In this model the expected cash flows are discounted using cost of capital

(Cunha, Reis, and Teixeira, 2021). The present value of cash inflows is added together

and they will be considering as value of an organisation using this model. As an investor

this model is very useful as this model helps in calculating the present value of various

proposed investments and usually considered the who has the highest present value. The

investor considers those investments which provides highest net present value as it is less

risky compare to other projects.

Recommendation on Proposed Investment.

a) Price Earning Method: -

This method shows the association between the enterprise stock price and earning per

share. It is a very widespread ratio that gives the stockholder a better logic of the value of

the business concern (Marqués, García, and Sánchez, 2020). This ratio shows the

probability of the market and price per share an investor pays per unit on the current

earning of the company. Profits are important when valuation is made for the entity

because investors want to know that how profitable an enterprise is in current accounting

period and what profits they will generate in future. It can be interpreted as the number of

years it will take for the organisation to pay back the amount paid for each share.

Price earning ratio = MPS / EPS

P.E Ratio of the Kings Plc is as under: -

= 4.15 / .29

= 14.31 Times

Value of Dragon Plc. will be calculated using P.E Ratio of Kings Plc as under: -

= EPS of Dragon Plc * P.E Ratio of Kings Plc

= 40.40 / 145 * 14.31

= £M 3.99

b) Discounted Cash Flow Method: -

This method used by the organisation to value the proposed business model they want to

acquire. In this model the expected cash flows are discounted using cost of capital

(Cunha, Reis, and Teixeira, 2021). The present value of cash inflows is added together

and they will be considering as value of an organisation using this model. As an investor

this model is very useful as this model helps in calculating the present value of various

proposed investments and usually considered the who has the highest present value. The

investor considers those investments which provides highest net present value as it is less

risky compare to other projects.

It is given in the question that board of directors of king’s plc estimate that after tax

synergy benefit from the above takeover would be £5.25m annually. However, in this

question it is not given that how many years such benefit will last in order to discount

such cash flow using discount rate. We assume that such benefit last forever and discount

rate of Kings will be taken into consideration.

Valuation of Dragon Plc will be: -

= Annual Synergy Benefit / Cost of Capital

= 5.25 / 12 %

= £M 43.75

c) Dividend Valuation Method: -

It is a quantifiable method of valuing the price of an organisations share price which is

calculated on the assumption that the current fair value of the stock will be equals to the

sum of all the future dividends received by the company (Pehlivan and Öztemir, 2018). In

this question we considered gordens dividend growth model for valuation of the entity. It

is a very popular and straightforward alternative of the dividend discount model. This

model assumes that the dividend will grow at a constant rate forever and considers the

present value of the future dividends in order to determine the value. Because this method

assumes a constant growth rate, it is generally used when payment of dividend is made

consistently.

According to this model valuation can be done using Gordon’s model as under: -

Po = D1 / Ke - G

Here,

Po - Current Market Price per share

D1 - Expected dividend per share

Ke - Cost of Equity

G - Growth rate

Po = 14.35p / (11.80 % - 2.50 %)

= 14.35p / 9.30 %

= 154.30p or £ 1.543

synergy benefit from the above takeover would be £5.25m annually. However, in this

question it is not given that how many years such benefit will last in order to discount

such cash flow using discount rate. We assume that such benefit last forever and discount

rate of Kings will be taken into consideration.

Valuation of Dragon Plc will be: -

= Annual Synergy Benefit / Cost of Capital

= 5.25 / 12 %

= £M 43.75

c) Dividend Valuation Method: -

It is a quantifiable method of valuing the price of an organisations share price which is

calculated on the assumption that the current fair value of the stock will be equals to the

sum of all the future dividends received by the company (Pehlivan and Öztemir, 2018). In

this question we considered gordens dividend growth model for valuation of the entity. It

is a very popular and straightforward alternative of the dividend discount model. This

model assumes that the dividend will grow at a constant rate forever and considers the

present value of the future dividends in order to determine the value. Because this method

assumes a constant growth rate, it is generally used when payment of dividend is made

consistently.

According to this model valuation can be done using Gordon’s model as under: -

Po = D1 / Ke - G

Here,

Po - Current Market Price per share

D1 - Expected dividend per share

Ke - Cost of Equity

G - Growth rate

Po = 14.35p / (11.80 % - 2.50 %)

= 14.35p / 9.30 %

= 154.30p or £ 1.543

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Value of firm will be: -

= No of Equity Shares * Current market price per share

= 145 * £ 1.543

= 223.74

Working Notes: -

Calculation of Ke using Capital Asset Pricing Model (CAPM): -

= Rf + B (Rm – Rf)

Here,

Rf - Risk free rate of return

B - Beta

Rm - Market rate of return

The difference between Rm and Rf is known as market risk premium.

= 5.50 % + 1.05 (6%)

= 11.80 %

Calculation of Expected Dividend per share: -

D1 = Dividend Paid (Do) + Growth Rate (G)

= 14p + 2.50 %

= 14.35p

d) Problems associated with the above models along with recommendation to Kings Plc. with

respect to proposed acquisition.

Problems associated with these models are: -

Price Earnings Ratio Model: The biggest problem with this model is that it only

considers EPS for valuation of company’s share. Another problem with this

method is that it does not consider growth rates (Pradhan, Arvin, and Hall, 2019).

Further this model is not advisable when company needs to compare with

different industries. This model is completely based of EPS which is sometimes

considers as misleading to the stakeholders.

Discount Cash Flow Method: The main problems with this model is that it

requires large number of assumptions before implementation (Talbot, 2019).

= No of Equity Shares * Current market price per share

= 145 * £ 1.543

= 223.74

Working Notes: -

Calculation of Ke using Capital Asset Pricing Model (CAPM): -

= Rf + B (Rm – Rf)

Here,

Rf - Risk free rate of return

B - Beta

Rm - Market rate of return

The difference between Rm and Rf is known as market risk premium.

= 5.50 % + 1.05 (6%)

= 11.80 %

Calculation of Expected Dividend per share: -

D1 = Dividend Paid (Do) + Growth Rate (G)

= 14p + 2.50 %

= 14.35p

d) Problems associated with the above models along with recommendation to Kings Plc. with

respect to proposed acquisition.

Problems associated with these models are: -

Price Earnings Ratio Model: The biggest problem with this model is that it only

considers EPS for valuation of company’s share. Another problem with this

method is that it does not consider growth rates (Pradhan, Arvin, and Hall, 2019).

Further this model is not advisable when company needs to compare with

different industries. This model is completely based of EPS which is sometimes

considers as misleading to the stakeholders.

Discount Cash Flow Method: The main problems with this model is that it

requires large number of assumptions before implementation (Talbot, 2019).

Further to calculate the terminal value is difficult and it represents the large

portion in the total value. Another challenge is to determine weighted average

cost of capital.

Dividend Valuation Method: The main limitation of this model is that it assumes that the

growth rate of dividend remains constant. As it is very rare for the companies to show constant

growth rate in payment of dividend over the period of time due to their business cycle and

financial difficulty a business faces over the period (Thomas, Shooya, and Lissner, 2019). This

model is limited to those enterprises only having a constant growth rates over the period of time.

Recommendation: - It is recommended to the Kings PLC. that acquisition of Dragon Plc is

worthwhile since it provides positive synergy to the organisation. Further the valuation of the

enterprise is higher when we adopt dividend growth model for valuation. This model is best

amongst all the methods applied above as it provides accurate result to some extent.

CONCLUSION

This report includes practical solution with respect to calculation of cost of capital using

historical value of capital structure and market value capital structure. Further it involves

practical approach with respect to recalculating the cost of capital if an entity incorporates more

debt in their capital structure and repurchase ordinary shares from the market in order to cancel

them. Another practical question is addressed which consist of valuation of Dragon plc

considering different models such as price earnings ratio, Dividend valuation model etc. On the

basis of the above assignment we can conclude that Gordon model of valuation of company

share is a best method amongst all methods. This method provides reasonable output when taken

into consideration.

portion in the total value. Another challenge is to determine weighted average

cost of capital.

Dividend Valuation Method: The main limitation of this model is that it assumes that the

growth rate of dividend remains constant. As it is very rare for the companies to show constant

growth rate in payment of dividend over the period of time due to their business cycle and

financial difficulty a business faces over the period (Thomas, Shooya, and Lissner, 2019). This

model is limited to those enterprises only having a constant growth rates over the period of time.

Recommendation: - It is recommended to the Kings PLC. that acquisition of Dragon Plc is

worthwhile since it provides positive synergy to the organisation. Further the valuation of the

enterprise is higher when we adopt dividend growth model for valuation. This model is best

amongst all the methods applied above as it provides accurate result to some extent.

CONCLUSION

This report includes practical solution with respect to calculation of cost of capital using

historical value of capital structure and market value capital structure. Further it involves

practical approach with respect to recalculating the cost of capital if an entity incorporates more

debt in their capital structure and repurchase ordinary shares from the market in order to cancel

them. Another practical question is addressed which consist of valuation of Dragon plc

considering different models such as price earnings ratio, Dividend valuation model etc. On the

basis of the above assignment we can conclude that Gordon model of valuation of company

share is a best method amongst all methods. This method provides reasonable output when taken

into consideration.

REFERENCES

Books and Journals

Amel-Zadeh, A. and Meeks, G. eds., 2020. Accounting for M&A: Uses and Abuses of

Accounting in Monitoring and Promoting Merger. Routledge.

Belhadi, A., Kamble, S., and Queiroz, M.M., 2021. Building supply-chain resilience: an artificial

intelligence-based technique and decision-making framework. International Journal of

Production Research, pp.1-21.

Bi, X. and Wang, D., 2018. Top-tier financial advisors, expropriation and Chinese mergers &

acquisitions. International Review of Financial Analysis. 57.pp.157-166.

Bielstein, P., Fischer, M. and Kaserer, C., 2018. The cost of capital effect of M&A transactions:

Disentangling coinsurance from the diversification discount. European Financial

Management. 24(4). pp.650-679.

Howe, J., 2019. The impact of rural roads on poverty alleviation: a review of the literature. Rural

roads and poverty alleviation, pp.48-81.

Jory, S., Ngo, T. and Susnjara, J., 2020. Stock mergers and acquirers’ subsequent stock price

crash risk. Review of Quantitative Finance and Accounting. 54(1). pp.359-387.

Khan, F.A., Pal, N. and Saeed, S.H., 2018. Review of solar photovoltaic and wind hybrid energy

systems for sizing strategies optimization techniques and cost analysis

methodologies. Renewable and Sustainable Energy Reviews. 92. pp.937-947.

Marqués, A.I., García, V. and Sánchez, J.S., 2020. Ranking-based MCDM models in financial

management applications: analysis and emerging challenges. Progress in Artificial

Intelligence. 9.pp.171-193.

Cunha, J., Reis, V. and Teixeira, P., 2021. Development of an agent-based model for

railway infrastructure project appraisal. Transportation. pp.1-33.

Pehlivan, S. and Öztemir, A.E., 2018. Integrated risk of progress-based costs and schedule delays

in construction projects. Engineering Management Journal. 30(2). pp.108-116.

Pradhan, R.P., Arvin, M.B. and Hall, J.H., 2019. The nexus between economic growth, stock

market depth, trade openness, and foreign direct investment: the case of ASEAN

countries. The Singapore Economic Review. 64(03). pp.461-493.

Talbot, J., 2019. Ensuring your NFP merger doesn't become an unintended take-

over. Governance Directions. 71(11). pp.643-647.

Thomas, A., Shooya, O., and Lissner, T., 2019. Climate change adaptation planning in practice:

insights from the Caribbean. Regional Environmental Change. 19(7). pp.2013-2025.

Books and Journals

Amel-Zadeh, A. and Meeks, G. eds., 2020. Accounting for M&A: Uses and Abuses of

Accounting in Monitoring and Promoting Merger. Routledge.

Belhadi, A., Kamble, S., and Queiroz, M.M., 2021. Building supply-chain resilience: an artificial

intelligence-based technique and decision-making framework. International Journal of

Production Research, pp.1-21.

Bi, X. and Wang, D., 2018. Top-tier financial advisors, expropriation and Chinese mergers &

acquisitions. International Review of Financial Analysis. 57.pp.157-166.

Bielstein, P., Fischer, M. and Kaserer, C., 2018. The cost of capital effect of M&A transactions:

Disentangling coinsurance from the diversification discount. European Financial

Management. 24(4). pp.650-679.

Howe, J., 2019. The impact of rural roads on poverty alleviation: a review of the literature. Rural

roads and poverty alleviation, pp.48-81.

Jory, S., Ngo, T. and Susnjara, J., 2020. Stock mergers and acquirers’ subsequent stock price

crash risk. Review of Quantitative Finance and Accounting. 54(1). pp.359-387.

Khan, F.A., Pal, N. and Saeed, S.H., 2018. Review of solar photovoltaic and wind hybrid energy

systems for sizing strategies optimization techniques and cost analysis

methodologies. Renewable and Sustainable Energy Reviews. 92. pp.937-947.

Marqués, A.I., García, V. and Sánchez, J.S., 2020. Ranking-based MCDM models in financial

management applications: analysis and emerging challenges. Progress in Artificial

Intelligence. 9.pp.171-193.

Cunha, J., Reis, V. and Teixeira, P., 2021. Development of an agent-based model for

railway infrastructure project appraisal. Transportation. pp.1-33.

Pehlivan, S. and Öztemir, A.E., 2018. Integrated risk of progress-based costs and schedule delays

in construction projects. Engineering Management Journal. 30(2). pp.108-116.

Pradhan, R.P., Arvin, M.B. and Hall, J.H., 2019. The nexus between economic growth, stock

market depth, trade openness, and foreign direct investment: the case of ASEAN

countries. The Singapore Economic Review. 64(03). pp.461-493.

Talbot, J., 2019. Ensuring your NFP merger doesn't become an unintended take-

over. Governance Directions. 71(11). pp.643-647.

Thomas, A., Shooya, O., and Lissner, T., 2019. Climate change adaptation planning in practice:

insights from the Caribbean. Regional Environmental Change. 19(7). pp.2013-2025.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.