Financial Analysis Report: Gatsby Grange Hotel Industry, UK

VerifiedAdded on 2023/01/10

|14

|3273

|93

Report

AI Summary

This report presents a financial analysis of the Gatsby Grange, a UK-based hotel, focusing on key financial ratios to assess its performance. The analysis covers profitability ratios, including Return on Capital Employed, Gross Profit Margin, and Net Profit Margin, revealing the hotel's efficiency in utilizing resources and generating profits. Liquidity ratios, such as the Current Ratio and Quick Ratio, are examined to evaluate the hotel's ability to meet short-term obligations. Efficiency ratios, including Debtor Days, Creditor Days, and Inventory Turnover, are analyzed to assess operational efficiency. Finally, the gearing ratio is explored to evaluate the hotel's financial risk and capital structure. The report highlights trends, fluctuations, and the importance of ratio analysis for hotel management, emphasizing its role in understanding financial performance, making comparisons, and informing future strategies. The report also discusses the benefits and limitations of ratio analysis in decision-making within the hotel and tourism segment. The analysis is based on data from 2018 and 2019, providing a comparative view of the hotel's financial health.

FINANCIAL MANAGEMENT

FOR HOTEL INDUSTRY

FOR HOTEL INDUSTRY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a. Financial analysis of the Gatsby Grange..................................................................................1

b. Stating an importance of ratio and fluctuations for the hotel management ...........................6

c. Evaluating the benefits and the limitation of ratio analysis that helps in decision making in

hotel & tourism segment .............................................................................................................6

TASK 2............................................................................................................................................8

Presentation..................................................................................................................................8

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a. Financial analysis of the Gatsby Grange..................................................................................1

b. Stating an importance of ratio and fluctuations for the hotel management ...........................6

c. Evaluating the benefits and the limitation of ratio analysis that helps in decision making in

hotel & tourism segment .............................................................................................................6

TASK 2............................................................................................................................................8

Presentation..................................................................................................................................8

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

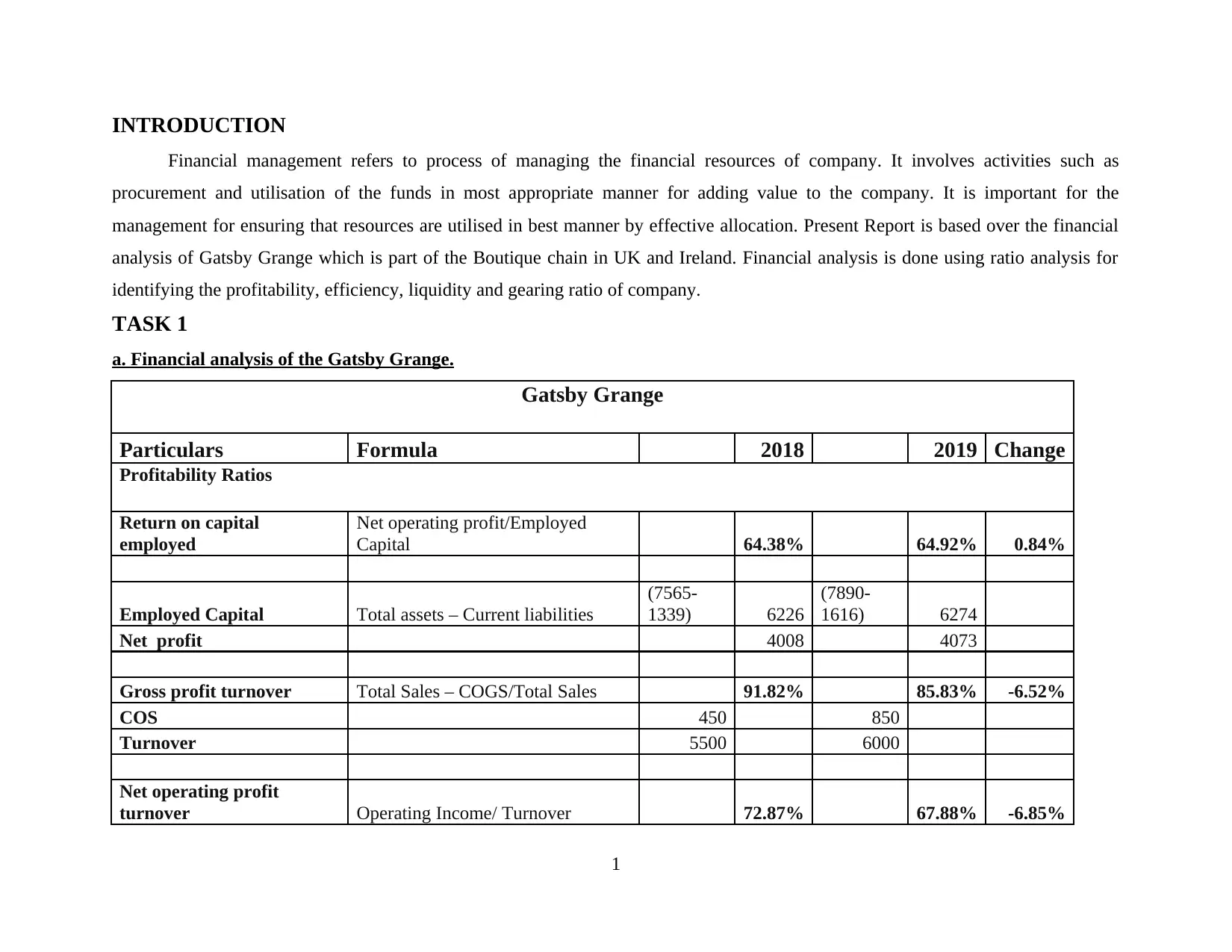

INTRODUCTION

Financial management refers to process of managing the financial resources of company. It involves activities such as

procurement and utilisation of the funds in most appropriate manner for adding value to the company. It is important for the

management for ensuring that resources are utilised in best manner by effective allocation. Present Report is based over the financial

analysis of Gatsby Grange which is part of the Boutique chain in UK and Ireland. Financial analysis is done using ratio analysis for

identifying the profitability, efficiency, liquidity and gearing ratio of company.

TASK 1

a. Financial analysis of the Gatsby Grange.

Gatsby Grange

Particulars Formula 2018 2019 Change

Profitability Ratios

Return on capital

employed

Net operating profit/Employed

Capital 64.38% 64.92% 0.84%

Employed Capital Total assets – Current liabilities

(7565-

1339) 6226

(7890-

1616) 6274

Net profit 4008 4073

Gross profit turnover Total Sales – COGS/Total Sales 91.82% 85.83% -6.52%

COS 450 850

Turnover 5500 6000

Net operating profit

turnover Operating Income/ Turnover 72.87% 67.88% -6.85%

1

Financial management refers to process of managing the financial resources of company. It involves activities such as

procurement and utilisation of the funds in most appropriate manner for adding value to the company. It is important for the

management for ensuring that resources are utilised in best manner by effective allocation. Present Report is based over the financial

analysis of Gatsby Grange which is part of the Boutique chain in UK and Ireland. Financial analysis is done using ratio analysis for

identifying the profitability, efficiency, liquidity and gearing ratio of company.

TASK 1

a. Financial analysis of the Gatsby Grange.

Gatsby Grange

Particulars Formula 2018 2019 Change

Profitability Ratios

Return on capital

employed

Net operating profit/Employed

Capital 64.38% 64.92% 0.84%

Employed Capital Total assets – Current liabilities

(7565-

1339) 6226

(7890-

1616) 6274

Net profit 4008 4073

Gross profit turnover Total Sales – COGS/Total Sales 91.82% 85.83% -6.52%

COS 450 850

Turnover 5500 6000

Net operating profit

turnover Operating Income/ Turnover 72.87% 67.88% -6.85%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Income 4008 4073

Revenues 5500 6000

Assets Turnover Sales / Capital Employed 88.34% 95.63% 8.26%

Turnover 5500 6000

Capital Employed 6226 6274

Liquidity Ratios

Current assets 3065 3240

Current liabilities 1339 1616

Inventory 1450 1420

Quick assets 1615 1820

Current ratio Current assets / current liabilities 2.29 2 -12.41%

Acid test ratio Current assets - Inventory / Sales 1.21 1.13 -6.62%

Debtors 1600 1800

Creditors 800 870

Days 365 365

Debtor days

Trade Receivables /Credit

Sales*365 106.18 109.5 3.13%

Creditor days Trade Payables / Credit Sales *365 53.09 52.93 -0.31%

Gearing Ratio

Long-term debt 150 145

Shareholder's equity 6076 6129

2

Revenues 5500 6000

Assets Turnover Sales / Capital Employed 88.34% 95.63% 8.26%

Turnover 5500 6000

Capital Employed 6226 6274

Liquidity Ratios

Current assets 3065 3240

Current liabilities 1339 1616

Inventory 1450 1420

Quick assets 1615 1820

Current ratio Current assets / current liabilities 2.29 2 -12.41%

Acid test ratio Current assets - Inventory / Sales 1.21 1.13 -6.62%

Debtors 1600 1800

Creditors 800 870

Days 365 365

Debtor days

Trade Receivables /Credit

Sales*365 106.18 109.5 3.13%

Creditor days Trade Payables / Credit Sales *365 53.09 52.93 -0.31%

Gearing Ratio

Long-term debt 150 145

Shareholder's equity 6076 6129

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

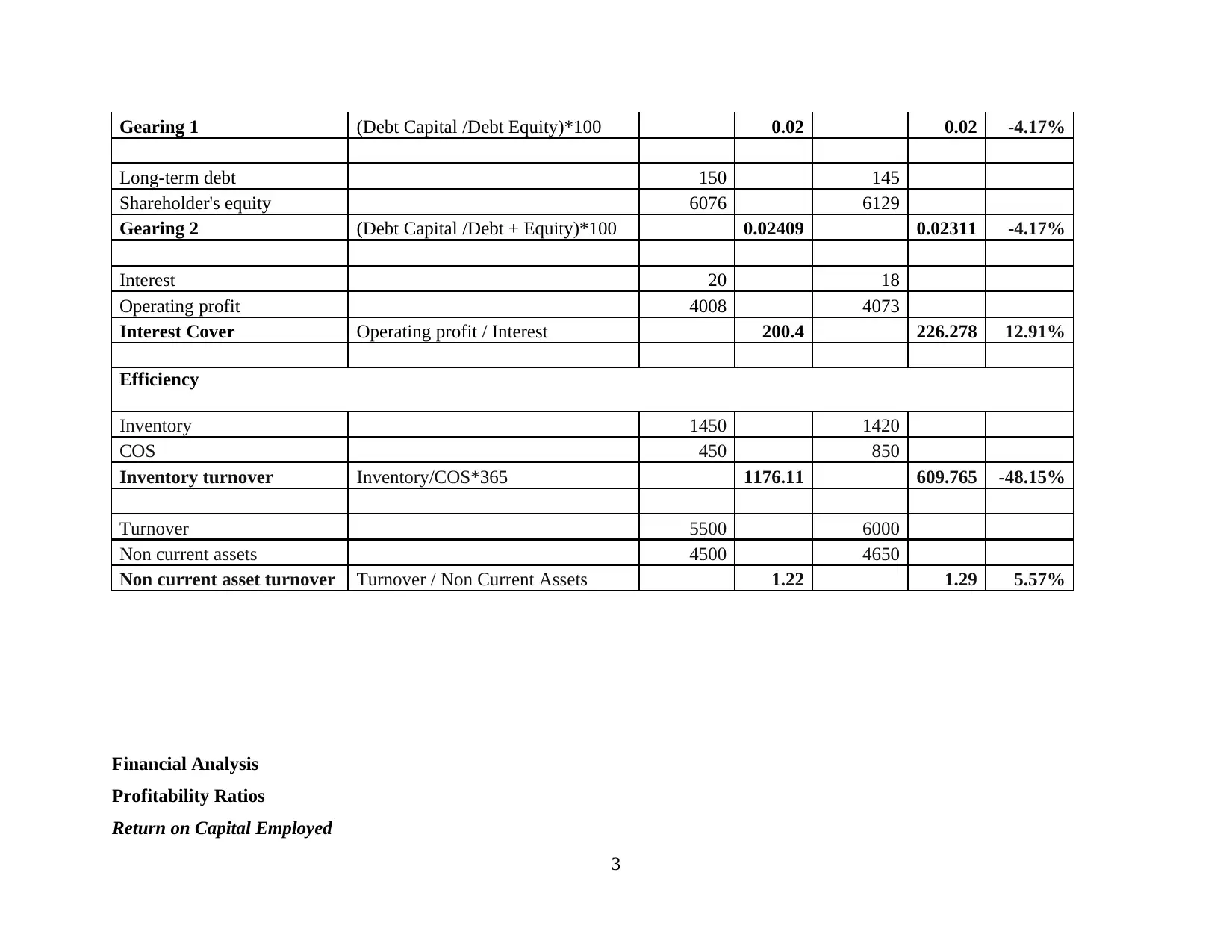

Gearing 1 (Debt Capital /Debt Equity)*100 0.02 0.02 -4.17%

Long-term debt 150 145

Shareholder's equity 6076 6129

Gearing 2 (Debt Capital /Debt + Equity)*100 0.02409 0.02311 -4.17%

Interest 20 18

Operating profit 4008 4073

Interest Cover Operating profit / Interest 200.4 226.278 12.91%

Efficiency

Inventory 1450 1420

COS 450 850

Inventory turnover Inventory/COS*365 1176.11 609.765 -48.15%

Turnover 5500 6000

Non current assets 4500 4650

Non current asset turnover Turnover / Non Current Assets 1.22 1.29 5.57%

Financial Analysis

Profitability Ratios

Return on Capital Employed

3

Long-term debt 150 145

Shareholder's equity 6076 6129

Gearing 2 (Debt Capital /Debt + Equity)*100 0.02409 0.02311 -4.17%

Interest 20 18

Operating profit 4008 4073

Interest Cover Operating profit / Interest 200.4 226.278 12.91%

Efficiency

Inventory 1450 1420

COS 450 850

Inventory turnover Inventory/COS*365 1176.11 609.765 -48.15%

Turnover 5500 6000

Non current assets 4500 4650

Non current asset turnover Turnover / Non Current Assets 1.22 1.29 5.57%

Financial Analysis

Profitability Ratios

Return on Capital Employed

3

This ratio is used for analysing the efficiency of the management in utilising the capital resources for generating returns.

Return on capital employed of the company is 64.92% and no major fluctuations are seen in the return. It shows that company is

effectively using the existing resources for generating return for the company. A company with high ROCE is seen as highly efficient

in using the resource by properly allocating the resources over the places where they could be used properly (Benavides, and et.al.,

2017). ROCE of company is high which will help in attracting new investments from the investors as it gives confidence that their

funds will be more effectively used by the company to maximise their returns.

This is used for analysing the efficiency of management in generating returns for the company. Asset turnover of company is

high which shows that strategies of the management for running the business are running efficiently. High returns over equity make

the business attractive for investors. They invest in companies that are generating high returns over the equity. This shows that

business is performing extremely well and has high growth prospects. Firm is required to maintain stability over the returns by laying

effective strategies.

Gross Profit Margins

The ratio is used for evaluating the gross profits of company. It is the amount left with the company after covering all the costs

associated with the sales of goods. Company is having gross profit of 85.83% in 2019 and has shown downward movement of 6.52%.

the decline is seen as the cost of sales have increased of the hotels. Being service industry gross profit is high. It could be evaluated

from the ratio that it is using cost efficient strategies for controlling and reducing the cost of sales. Gross profit of the firm should be

high as it has to carry out number of transactions for running the operations (Hirshleifer, Hsu and Li, 2018). Insufficient gross profit

may reduce some of the expenses that are essential for promoting the growth of the organisation. It has to maintain control over the

increasing costs as it may further reduce the gross profit of company.

Net Profit Margin

Net profit margin of the Boutique is 67.88 %. There is a downward movement of 6.85% from last year. This is seen due to

decrease in the gross profits of company. Net profits of Boutique are high this is essential for the business. High profitability brings

4

Return on capital employed of the company is 64.92% and no major fluctuations are seen in the return. It shows that company is

effectively using the existing resources for generating return for the company. A company with high ROCE is seen as highly efficient

in using the resource by properly allocating the resources over the places where they could be used properly (Benavides, and et.al.,

2017). ROCE of company is high which will help in attracting new investments from the investors as it gives confidence that their

funds will be more effectively used by the company to maximise their returns.

This is used for analysing the efficiency of management in generating returns for the company. Asset turnover of company is

high which shows that strategies of the management for running the business are running efficiently. High returns over equity make

the business attractive for investors. They invest in companies that are generating high returns over the equity. This shows that

business is performing extremely well and has high growth prospects. Firm is required to maintain stability over the returns by laying

effective strategies.

Gross Profit Margins

The ratio is used for evaluating the gross profits of company. It is the amount left with the company after covering all the costs

associated with the sales of goods. Company is having gross profit of 85.83% in 2019 and has shown downward movement of 6.52%.

the decline is seen as the cost of sales have increased of the hotels. Being service industry gross profit is high. It could be evaluated

from the ratio that it is using cost efficient strategies for controlling and reducing the cost of sales. Gross profit of the firm should be

high as it has to carry out number of transactions for running the operations (Hirshleifer, Hsu and Li, 2018). Insufficient gross profit

may reduce some of the expenses that are essential for promoting the growth of the organisation. It has to maintain control over the

increasing costs as it may further reduce the gross profit of company.

Net Profit Margin

Net profit margin of the Boutique is 67.88 %. There is a downward movement of 6.85% from last year. This is seen due to

decrease in the gross profits of company. Net profits of Boutique are high this is essential for the business. High profitability brings

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

several opportunities for the company. It represents the image of management and their efforts. Firm is seen as having highly effective

leaders who are driving the company towards success for achieving the goals and objectives of the organisation. It has to effectively

control the business operations and costs and expenses for maintaining the profitability. Net profit represents whether carrying on the

business is successful or not during the period.

Asset turnover ratio-

It has been seen from analysis that asset turnover ratio of the company is increasing which means that company is utilising its

assets effectively. A company must utilise the assets of company for generating higher sales for having higher returns. It is making

efficient use of the assets to generate revenues.

Liquidity Ratios

Current Ratio

Current Ratio is 2 in 2019 and was 2.29 in 2018. Downward movement of 12.41% in the ratio is seen from last year. Current

ratio assess the ability of company to meet the short term obligations from the available assets. Current ratio is adequate as per the

industry standards and is required to be maintained. Further increase will represent blocked investment in the Boutique therefore it has

to ensure that the liquidity does not fall or move above the set standards. All the stakeholders are concerned with liquidity of company

as inadequate funds may affect the operations of business affecting the working of the entity. Strong liquidity represents it has having

strong and big capital base and is able to meet the requirements of company. Inadequate assets to meet the obligations will require the

Boutique to borrow funds from external sources that will increase costs of the hotel.

Quick / Acid test ratio

It is a measure of the liquidity excluding inventory from the current assets. Stocks are not considered liquid as they could not

be sold immediately in case of need. Therefore they are not considered current for measuring liquidity (Ardekani, Distinguin and

Tarazi, 2020). Quick ratio of company is 1.13 and has decreased from 1.13 in 2018. It could be evaluated that company is able to meet

5

leaders who are driving the company towards success for achieving the goals and objectives of the organisation. It has to effectively

control the business operations and costs and expenses for maintaining the profitability. Net profit represents whether carrying on the

business is successful or not during the period.

Asset turnover ratio-

It has been seen from analysis that asset turnover ratio of the company is increasing which means that company is utilising its

assets effectively. A company must utilise the assets of company for generating higher sales for having higher returns. It is making

efficient use of the assets to generate revenues.

Liquidity Ratios

Current Ratio

Current Ratio is 2 in 2019 and was 2.29 in 2018. Downward movement of 12.41% in the ratio is seen from last year. Current

ratio assess the ability of company to meet the short term obligations from the available assets. Current ratio is adequate as per the

industry standards and is required to be maintained. Further increase will represent blocked investment in the Boutique therefore it has

to ensure that the liquidity does not fall or move above the set standards. All the stakeholders are concerned with liquidity of company

as inadequate funds may affect the operations of business affecting the working of the entity. Strong liquidity represents it has having

strong and big capital base and is able to meet the requirements of company. Inadequate assets to meet the obligations will require the

Boutique to borrow funds from external sources that will increase costs of the hotel.

Quick / Acid test ratio

It is a measure of the liquidity excluding inventory from the current assets. Stocks are not considered liquid as they could not

be sold immediately in case of need. Therefore they are not considered current for measuring liquidity (Ardekani, Distinguin and

Tarazi, 2020). Quick ratio of company is 1.13 and has decreased from 1.13 in 2018. It could be evaluated that company is able to meet

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the current liabilities from the available assets. It can make short term investments to earn short term returns that could be used for

meeting the working capital requirements of the business. Management has to effectively manage the activities for having adequate

cash flows. It should increase quick ratio by implementing effective strategies and managing the resources.

Efficiency Ratios

Creditor Days

Creditor days of Boutique are 53 and has remained same as per last year. These days are half of the debtor days. Credit period

should be higher so that company could manage the funds for payments. It should increase the creditor days to further extent for

having adequate cash cycle to meet the cash requirements of business. Operations of the business will be affected without the efficient

cash inflows.

Debtor Days

Debtors Days are 109 which is not high as per the industry average. The debtor days should be decided as per the cash cycle. It

is having high debtor days as it is one of the strategy to promotes sales of the hotel. When credit is given to the customers sales is

increased to considerable extent (Burns and et.al., 2020). It has to manage the cash cycle for meeting the working capital requirements

of business.

Inventory Days

Inventory days are used for assessing the efficiency of management in moving the goods from factory. Inventory days are

significantly high as Boutique is serving in service industry. It has large stocks of inventory that are very slow moving. Management

has reduced inventory days to 609 which is half from last year. Stocks level is same but cost of sales had increased decreasing the

inventory days.

Non-current asset ?

6

meeting the working capital requirements of the business. Management has to effectively manage the activities for having adequate

cash flows. It should increase quick ratio by implementing effective strategies and managing the resources.

Efficiency Ratios

Creditor Days

Creditor days of Boutique are 53 and has remained same as per last year. These days are half of the debtor days. Credit period

should be higher so that company could manage the funds for payments. It should increase the creditor days to further extent for

having adequate cash cycle to meet the cash requirements of business. Operations of the business will be affected without the efficient

cash inflows.

Debtor Days

Debtors Days are 109 which is not high as per the industry average. The debtor days should be decided as per the cash cycle. It

is having high debtor days as it is one of the strategy to promotes sales of the hotel. When credit is given to the customers sales is

increased to considerable extent (Burns and et.al., 2020). It has to manage the cash cycle for meeting the working capital requirements

of business.

Inventory Days

Inventory days are used for assessing the efficiency of management in moving the goods from factory. Inventory days are

significantly high as Boutique is serving in service industry. It has large stocks of inventory that are very slow moving. Management

has reduced inventory days to 609 which is half from last year. Stocks level is same but cost of sales had increased decreasing the

inventory days.

Non-current asset ?

6

The ratio is used for measuring the efficiency of management in generating over the non current assets. it could be analysed

from the ratio that boutique is making efficient use of the non current for earning revenues. Management of the company is effectively

using the non current assets and has achieved a growth of 5 % from last year

Gearing Ratio

Gearing 1 Leverage ?

It is used for assessing the proportion of debt capital in the total capital structure of the company. from the above analysis it

could be seen that boutique is having gearing ratio of 0.02 that represent that it is having 2% of debt in the total capital structure of the

boutique. There is very low financial risk in the business as it does not have high debt. It is self sufficient for meeting the requirements

of business and in carrying out the operations of business

Debt to capital

It is used for assessing the proportion of debt in the capital of company. Boutique is having debt equity of 0.02 over the two

years. It is having very low debt in proportion to the equity. It could be evaluated that it does not uses debt for raising funds to meet

the capital requirements or funding the operations of business. (Muthee, Adudah,and Ondigo, 2019). Debt equity is also used for

analysing capital structure of the firm. It should use debt for raising funds for business as it provides tax benefits over capital cost and

also interest cost.

Interest cover ?

7

from the ratio that boutique is making efficient use of the non current for earning revenues. Management of the company is effectively

using the non current assets and has achieved a growth of 5 % from last year

Gearing Ratio

Gearing 1 Leverage ?

It is used for assessing the proportion of debt capital in the total capital structure of the company. from the above analysis it

could be seen that boutique is having gearing ratio of 0.02 that represent that it is having 2% of debt in the total capital structure of the

boutique. There is very low financial risk in the business as it does not have high debt. It is self sufficient for meeting the requirements

of business and in carrying out the operations of business

Debt to capital

It is used for assessing the proportion of debt in the capital of company. Boutique is having debt equity of 0.02 over the two

years. It is having very low debt in proportion to the equity. It could be evaluated that it does not uses debt for raising funds to meet

the capital requirements or funding the operations of business. (Muthee, Adudah,and Ondigo, 2019). Debt equity is also used for

analysing capital structure of the firm. It should use debt for raising funds for business as it provides tax benefits over capital cost and

also interest cost.

Interest cover ?

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The ratio is used for measuring the amount of interest in the operating profits of company. It could be analysed from the above

ratio that boutique is having very low interest expense as compared with the operating expenses. Company does not uses debt capital

for meeting the funding requirements of business.

b. Stating an importance of ratio and fluctuations for the hotel management

Ratio analysis includes evaluation of the data from historical and current financial statements for understanding financial

performance and the position of an enterprise in overall industry. It helps in setting out the trend of the company's performance over

the period that reflects whether the firm is achieving growth or not. Understanding final report are critical for the hotel management as

it helps in making comparison of the numbers presented in statement. Furthermore, it enables in estimating the numbers from profit &

loss statement and the balance sheet for future (Arkan, 2016). Ratio analysis seems as crucial in understanding the ability of firm in

generating profit and developing efficiency in using its assets and inventory.

With hospitality sector, it is extremely essential for defining set of the financial ratios which could be used for assessing

organizations around an overall industry, irrespective of the operations. Hotel management industry comprises heavy proportion of the

fixed and the tangible assets and thus needs specific set of financial ratios for accurately analysing industry & performance of each

company (Andjelic and Vesic, 2017). As hospitality sector encompasses with several sub sectors, it seems as difficult for comparing

the companies within the hospitality segment. Some helpful ratios could be put for achieving the comparative analysis against the

benchmark.

For hospitality sector, companies are having lot of short term liabilities in form of the wages and salaries, current equipment

leasing and the current liabilities. This industry is seen as cyclical, that makes it imperative for the firms having sufficient current

assets in order to cover the short term obligations even in the economic downturn. The stakeholders desire for seeing high CR higher

than 1 for determining the company within hospitality sector remains as strong. The companies functioning under hospitality industry

have high amount of long term debts so it essential for such firms to measure their debt ratio. The D/E ratio of an entity need to have

the low debt ratio which means that long term assets outweigh debt used for purchasing it.

8

ratio that boutique is having very low interest expense as compared with the operating expenses. Company does not uses debt capital

for meeting the funding requirements of business.

b. Stating an importance of ratio and fluctuations for the hotel management

Ratio analysis includes evaluation of the data from historical and current financial statements for understanding financial

performance and the position of an enterprise in overall industry. It helps in setting out the trend of the company's performance over

the period that reflects whether the firm is achieving growth or not. Understanding final report are critical for the hotel management as

it helps in making comparison of the numbers presented in statement. Furthermore, it enables in estimating the numbers from profit &

loss statement and the balance sheet for future (Arkan, 2016). Ratio analysis seems as crucial in understanding the ability of firm in

generating profit and developing efficiency in using its assets and inventory.

With hospitality sector, it is extremely essential for defining set of the financial ratios which could be used for assessing

organizations around an overall industry, irrespective of the operations. Hotel management industry comprises heavy proportion of the

fixed and the tangible assets and thus needs specific set of financial ratios for accurately analysing industry & performance of each

company (Andjelic and Vesic, 2017). As hospitality sector encompasses with several sub sectors, it seems as difficult for comparing

the companies within the hospitality segment. Some helpful ratios could be put for achieving the comparative analysis against the

benchmark.

For hospitality sector, companies are having lot of short term liabilities in form of the wages and salaries, current equipment

leasing and the current liabilities. This industry is seen as cyclical, that makes it imperative for the firms having sufficient current

assets in order to cover the short term obligations even in the economic downturn. The stakeholders desire for seeing high CR higher

than 1 for determining the company within hospitality sector remains as strong. The companies functioning under hospitality industry

have high amount of long term debts so it essential for such firms to measure their debt ratio. The D/E ratio of an entity need to have

the low debt ratio which means that long term assets outweigh debt used for purchasing it.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. Evaluating the benefits and the limitation of ratio analysis that helps in decision making in hotel & tourism segment

Benefits-

Ratio analysis is used as the powerful tool of the final report assessment and establishes numerical or the quantitative

relationship in between the two figures of final report for ascertaining strengths & weaknesses of an entity and its current final

state and the historical performance. It enables several interested users in making evaluation of various aspects of company's

performance.

The trend in the sales, cost, profits and the other facts could be known by calculating ratios of the appropriate accounting

figures for previous years (Barth and Miller, 2018). Such trend analysis with the use of ratios seems as useful in planning &

forecasting the future activities of business.

It indicates a degree of an efficiency in utilization and managing its assets where different efficiency ratios reflects the

operational efficiency.

Ratios are counted as an effective means of the communication & plays a crucial role in stating the progress made by business

enterprise to owners or the other parties.

It could be used for controlling performances of the different divisions or the functions of an enterprise and also control costs.

It helps the managers in taking decisions as like whether to make supply of the goods on credit to firm, whether bank loan

would be made available etc.

Limitations-

Ratios are computed from information recorded in final report which includes estimations and assumptions that in turn affect

quality of the ratios.

Final report facilitates historical information as they do not reflect the current conditions and thus is not found as useful in

predicting future.

Different policies of accounting relating to valuing inventory and charging depreciation makes an accounting data &

accounting ratios of the two companies as non-comparable.

9

Benefits-

Ratio analysis is used as the powerful tool of the final report assessment and establishes numerical or the quantitative

relationship in between the two figures of final report for ascertaining strengths & weaknesses of an entity and its current final

state and the historical performance. It enables several interested users in making evaluation of various aspects of company's

performance.

The trend in the sales, cost, profits and the other facts could be known by calculating ratios of the appropriate accounting

figures for previous years (Barth and Miller, 2018). Such trend analysis with the use of ratios seems as useful in planning &

forecasting the future activities of business.

It indicates a degree of an efficiency in utilization and managing its assets where different efficiency ratios reflects the

operational efficiency.

Ratios are counted as an effective means of the communication & plays a crucial role in stating the progress made by business

enterprise to owners or the other parties.

It could be used for controlling performances of the different divisions or the functions of an enterprise and also control costs.

It helps the managers in taking decisions as like whether to make supply of the goods on credit to firm, whether bank loan

would be made available etc.

Limitations-

Ratios are computed from information recorded in final report which includes estimations and assumptions that in turn affect

quality of the ratios.

Final report facilitates historical information as they do not reflect the current conditions and thus is not found as useful in

predicting future.

Different policies of accounting relating to valuing inventory and charging depreciation makes an accounting data &

accounting ratios of the two companies as non-comparable.

9

No fixed or set of standards could be laid down for the ideal ratios. For instance- CR is said to be as ideal if the CA resulted

twice the CL (Pasciuto and et.al., 2017). But this might not be counted as justifiable in the situation that have adequate

arrangements with their respective bankers for facilitating funds when it requires, it might perfectly ideal if the current assets

equates to or little higher than CL.

It is tool that considers quantitative analysis and the qualitative factors are been ignored at the time of computing ratios.

With the use of this tool, there are chances of window dressing which reflects presenting the final report is such manner for

showing better position of company than what it actually shown. For example- low depreciation is been charged, revenue

expense is been treated as the capital expense.

TASK 2

Presentation

Overview

It has highly efficient performance over the years and strong financial position. This is highly profitable boutique with returns

and profits. It has sound growth opportunities for business expansion. It is highly liquid firm with the sufficient assets for meeting

short term obligations of the enterprise. Management is highly efficient in meeting the cash requirement by effectively managing the

cash cycle. It can further improve efficiency of the cash cycle by managing the debtor and creditor days. It is having strong capital

structure with low debt and low financial risks. It could raise funds through debt for meeting the requirements of business.

CONCLUSION

It could be concluded that Gatsby is performing efficiently in the market earning high revenues. Financial analysis is essential

for measuring the performance and position of the enterprise. Financial analysis is done using ratio analysis which shows the

efficiency of management in using the resources of company for generating returns and maximising wealth of shareholders.

10

twice the CL (Pasciuto and et.al., 2017). But this might not be counted as justifiable in the situation that have adequate

arrangements with their respective bankers for facilitating funds when it requires, it might perfectly ideal if the current assets

equates to or little higher than CL.

It is tool that considers quantitative analysis and the qualitative factors are been ignored at the time of computing ratios.

With the use of this tool, there are chances of window dressing which reflects presenting the final report is such manner for

showing better position of company than what it actually shown. For example- low depreciation is been charged, revenue

expense is been treated as the capital expense.

TASK 2

Presentation

Overview

It has highly efficient performance over the years and strong financial position. This is highly profitable boutique with returns

and profits. It has sound growth opportunities for business expansion. It is highly liquid firm with the sufficient assets for meeting

short term obligations of the enterprise. Management is highly efficient in meeting the cash requirement by effectively managing the

cash cycle. It can further improve efficiency of the cash cycle by managing the debtor and creditor days. It is having strong capital

structure with low debt and low financial risks. It could raise funds through debt for meeting the requirements of business.

CONCLUSION

It could be concluded that Gatsby is performing efficiently in the market earning high revenues. Financial analysis is essential

for measuring the performance and position of the enterprise. Financial analysis is done using ratio analysis which shows the

efficiency of management in using the resources of company for generating returns and maximising wealth of shareholders.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.