Financial Performance Analysis of Vodafone Plc and BT Group Plc

VerifiedAdded on 2023/01/24

|25

|4029

|59

AI Summary

This report provides a detailed analysis of the financial performance of Vodafone Plc and its competitor, BT Group Plc in the UK telecommunications sector. It includes liquidity analysis, profitability analysis, efficiency analysis, and capital structure analysis. Based on the analysis, recommendations are provided for investing in the shares of the two organizations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL MANAGEMENT

Executive Summary:

For the current report, the organisation chosen is Vodafone Plc and its major competitor, BT

Group Plc operating in the UK telecommunication and utilities sector. From the conducted

analysis, it is apparent that BT Group Plc is in a better position than Vodafone Plc in the UK

telecommunications sector owing to better financial performance in the past five years. In

addition, by considering stock market performance, the investors are recommended to invest in

the shares of BT Group for maximising their return on investment. However, the analysis is

subject to certain limitations, since it has considered historical data only for decision-making.

Therefore, research reports and price/earnings ratio have been taken into consideration, which

reveal that the performance of BT Group is expected to decline in the upcoming years, especially

in terms of earnings per share and dividend payments. Hence, the investors need to consider

these aspects as well before investing in the shares of BT Group Plc.

Executive Summary:

For the current report, the organisation chosen is Vodafone Plc and its major competitor, BT

Group Plc operating in the UK telecommunication and utilities sector. From the conducted

analysis, it is apparent that BT Group Plc is in a better position than Vodafone Plc in the UK

telecommunications sector owing to better financial performance in the past five years. In

addition, by considering stock market performance, the investors are recommended to invest in

the shares of BT Group for maximising their return on investment. However, the analysis is

subject to certain limitations, since it has considered historical data only for decision-making.

Therefore, research reports and price/earnings ratio have been taken into consideration, which

reveal that the performance of BT Group is expected to decline in the upcoming years, especially

in terms of earnings per share and dividend payments. Hence, the investors need to consider

these aspects as well before investing in the shares of BT Group Plc.

2FINANCIAL MANAGEMENT

Table of Contents

Introduction:....................................................................................................................................3

Comparison and analysis of the financial performance of Vodafone Plc and its competitor, BT

Group Plc:........................................................................................................................................4

Recommendations regarding buying shares in any of the two organisations:...............................15

Problems, limitations and assumptions:........................................................................................15

Conclusion:....................................................................................................................................16

References and Bibliographies:.....................................................................................................18

Appendices:...................................................................................................................................21

Table of Contents

Introduction:....................................................................................................................................3

Comparison and analysis of the financial performance of Vodafone Plc and its competitor, BT

Group Plc:........................................................................................................................................4

Recommendations regarding buying shares in any of the two organisations:...............................15

Problems, limitations and assumptions:........................................................................................15

Conclusion:....................................................................................................................................16

References and Bibliographies:.....................................................................................................18

Appendices:...................................................................................................................................21

3FINANCIAL MANAGEMENT

Introduction:

For the current report, the organisation chosen is Vodafone Plc and its major competitor,

BT Group Plc operating in the UK telecommunication and utilities sector. Vodafone Plc is a

leading UK-based telecommunication service provider having its operations spread in Africa,

Middle East, Europe and the Asia Pacific. The main products of the organisation include mobile

services like text, call, broadband, data, voice, telephone offerings, mobile money services and

others (Vodafone.co.uk 2019). On the other hand, BT Group Plc is a British telecommunications

firm having it’s headquarter in London, UK. The organisation has its business operations in

above 180 nations and it is the biggest provider of broadband, fixed-line and mobile services

along with IT and subscription television services in UK (Btplc.com 2019).

The UK telecommunications sector remains one of the biggest in Europe, which is

characterised by intense competition resulting in minimised pricing for the end-users. Recently,

Vodafone UK and Telefonica UK (O2) would be entering into a new infrastructure-sharing

relationship lying ahead of the 5G rollout. These two organisations have shared infrastructure

activities and the proposed plan would provide significant benefits to Vodafone Plc in terms of

capturing a greater portion of market share in UK. Vodafone would start 1,000 5G-enabled

network sites in UK by 2020 for providing fast browsing experiences to its customers, which

would assist in gaining competitive advantage over its competitor, BT Group Plc. This is because

BT Group Plc has undertaken certain developments like transfer of 31,000 staffs to Openreach

Limited and it is working with Huawei for 3Tb/s channel trial over the current fibre

(Budde.com.au 2019).

Introduction:

For the current report, the organisation chosen is Vodafone Plc and its major competitor,

BT Group Plc operating in the UK telecommunication and utilities sector. Vodafone Plc is a

leading UK-based telecommunication service provider having its operations spread in Africa,

Middle East, Europe and the Asia Pacific. The main products of the organisation include mobile

services like text, call, broadband, data, voice, telephone offerings, mobile money services and

others (Vodafone.co.uk 2019). On the other hand, BT Group Plc is a British telecommunications

firm having it’s headquarter in London, UK. The organisation has its business operations in

above 180 nations and it is the biggest provider of broadband, fixed-line and mobile services

along with IT and subscription television services in UK (Btplc.com 2019).

The UK telecommunications sector remains one of the biggest in Europe, which is

characterised by intense competition resulting in minimised pricing for the end-users. Recently,

Vodafone UK and Telefonica UK (O2) would be entering into a new infrastructure-sharing

relationship lying ahead of the 5G rollout. These two organisations have shared infrastructure

activities and the proposed plan would provide significant benefits to Vodafone Plc in terms of

capturing a greater portion of market share in UK. Vodafone would start 1,000 5G-enabled

network sites in UK by 2020 for providing fast browsing experiences to its customers, which

would assist in gaining competitive advantage over its competitor, BT Group Plc. This is because

BT Group Plc has undertaken certain developments like transfer of 31,000 staffs to Openreach

Limited and it is working with Huawei for 3Tb/s channel trial over the current fibre

(Budde.com.au 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL MANAGEMENT

Comparison and analysis of the financial performance of Vodafone Plc and its competitor,

BT Group Plc:

For conducting the financial analysis of Vodafone Plc and BT Group Plc, certain ratios

have been taken into consideration and their detailed analysis is presented as follows:

Liquidity analysis:

For carrying out the profitability analysis of Vodafone Plc and its competitor, BT Group

Plc, the two liquidity ratios that have been taken into account comprise of current ratio and quick

ratio, which are presented as follows:

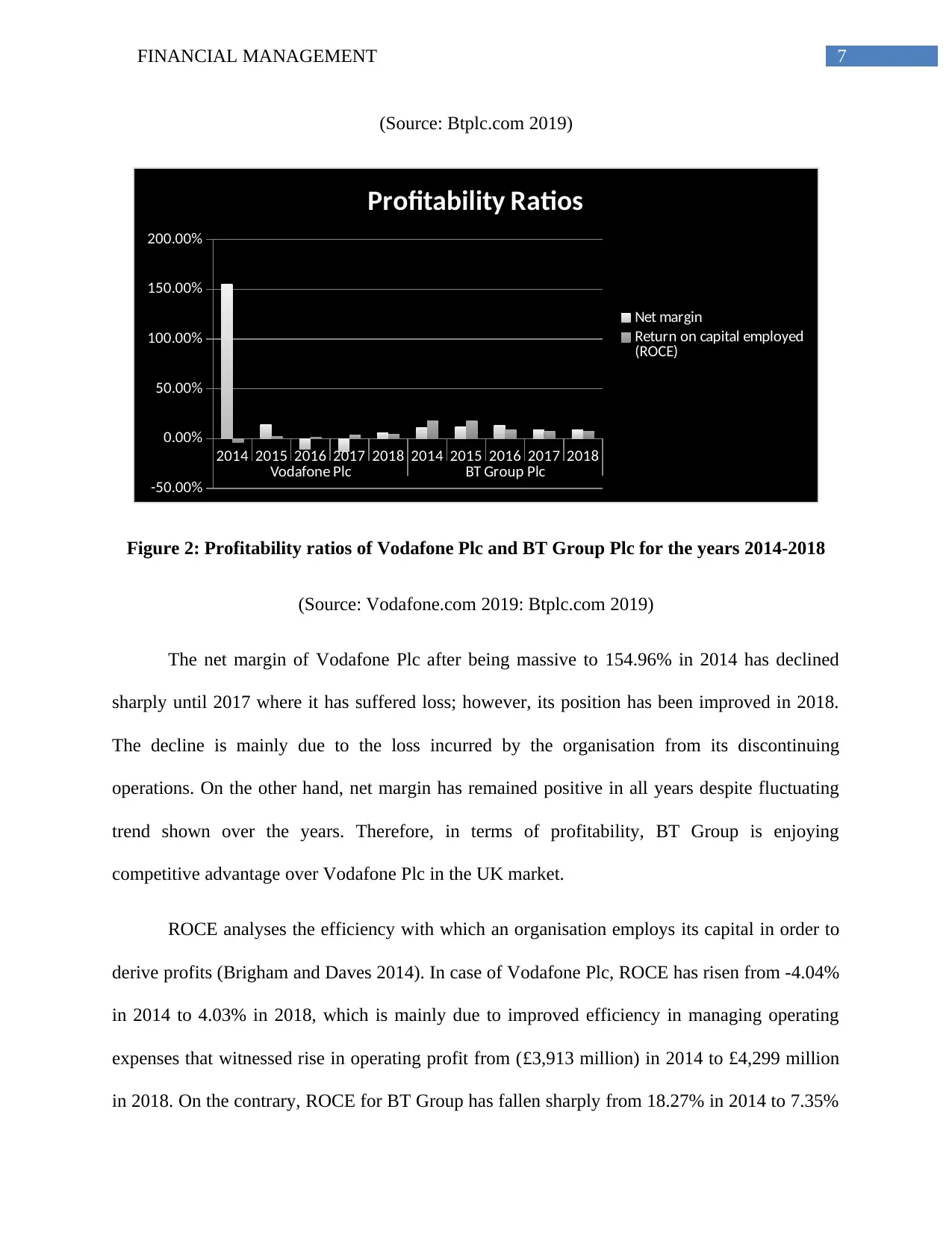

Table 1: Liquidity ratios of Vodafone Plc for the years 2014-2018

(Source: Vodafone.com 2019)

Table 2: Liquidity ratios of BT Group Plc for the years 2014-2018

(Source: Btplc.com 2019)

Comparison and analysis of the financial performance of Vodafone Plc and its competitor,

BT Group Plc:

For conducting the financial analysis of Vodafone Plc and BT Group Plc, certain ratios

have been taken into consideration and their detailed analysis is presented as follows:

Liquidity analysis:

For carrying out the profitability analysis of Vodafone Plc and its competitor, BT Group

Plc, the two liquidity ratios that have been taken into account comprise of current ratio and quick

ratio, which are presented as follows:

Table 1: Liquidity ratios of Vodafone Plc for the years 2014-2018

(Source: Vodafone.com 2019)

Table 2: Liquidity ratios of BT Group Plc for the years 2014-2018

(Source: Btplc.com 2019)

5FINANCIAL MANAGEMENT

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Vodafone Plc BT Group Plc

-

0.20

0.40

0.60

0.80

1.00

1.20

Liquidity Ratios

Current ratio

Quick ratio

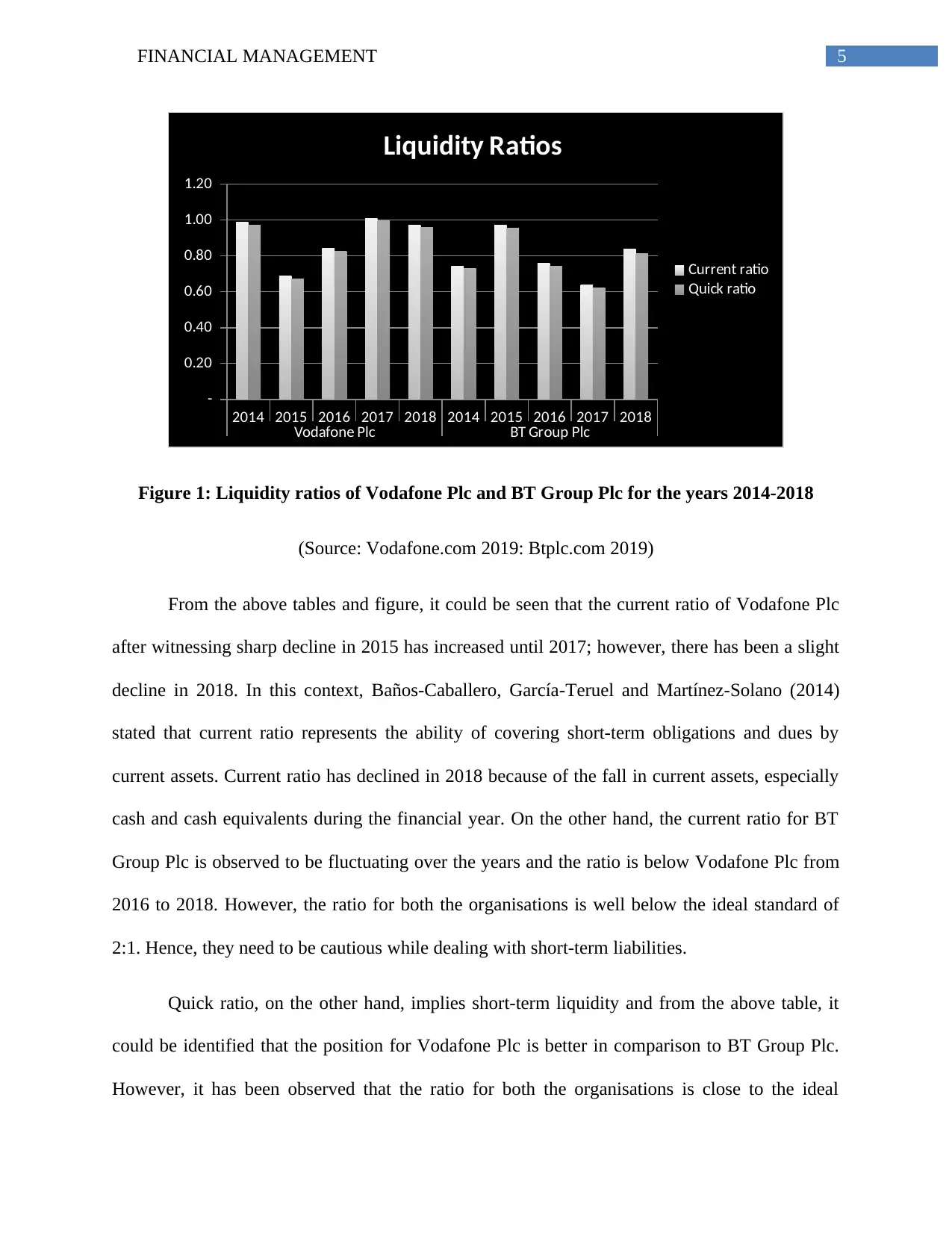

Figure 1: Liquidity ratios of Vodafone Plc and BT Group Plc for the years 2014-2018

(Source: Vodafone.com 2019: Btplc.com 2019)

From the above tables and figure, it could be seen that the current ratio of Vodafone Plc

after witnessing sharp decline in 2015 has increased until 2017; however, there has been a slight

decline in 2018. In this context, Baños-Caballero, García-Teruel and Martínez-Solano (2014)

stated that current ratio represents the ability of covering short-term obligations and dues by

current assets. Current ratio has declined in 2018 because of the fall in current assets, especially

cash and cash equivalents during the financial year. On the other hand, the current ratio for BT

Group Plc is observed to be fluctuating over the years and the ratio is below Vodafone Plc from

2016 to 2018. However, the ratio for both the organisations is well below the ideal standard of

2:1. Hence, they need to be cautious while dealing with short-term liabilities.

Quick ratio, on the other hand, implies short-term liquidity and from the above table, it

could be identified that the position for Vodafone Plc is better in comparison to BT Group Plc.

However, it has been observed that the ratio for both the organisations is close to the ideal

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Vodafone Plc BT Group Plc

-

0.20

0.40

0.60

0.80

1.00

1.20

Liquidity Ratios

Current ratio

Quick ratio

Figure 1: Liquidity ratios of Vodafone Plc and BT Group Plc for the years 2014-2018

(Source: Vodafone.com 2019: Btplc.com 2019)

From the above tables and figure, it could be seen that the current ratio of Vodafone Plc

after witnessing sharp decline in 2015 has increased until 2017; however, there has been a slight

decline in 2018. In this context, Baños-Caballero, García-Teruel and Martínez-Solano (2014)

stated that current ratio represents the ability of covering short-term obligations and dues by

current assets. Current ratio has declined in 2018 because of the fall in current assets, especially

cash and cash equivalents during the financial year. On the other hand, the current ratio for BT

Group Plc is observed to be fluctuating over the years and the ratio is below Vodafone Plc from

2016 to 2018. However, the ratio for both the organisations is well below the ideal standard of

2:1. Hence, they need to be cautious while dealing with short-term liabilities.

Quick ratio, on the other hand, implies short-term liquidity and from the above table, it

could be identified that the position for Vodafone Plc is better in comparison to BT Group Plc.

However, it has been observed that the ratio for both the organisations is close to the ideal

6FINANCIAL MANAGEMENT

standard of 1 (Bekaert and Hodrick 2017). The main reason behind such stable position in

liquidity of Vodafone Plc is the fall in short-term borrowings, which has assisted the organisation

in maintaining stable liquidity position in the market. Hence, in terms of liquidity, Vodafone Plc

is observed to be in a favourable position in comparison to BT Group Plc in the UK

telecommunications sector.

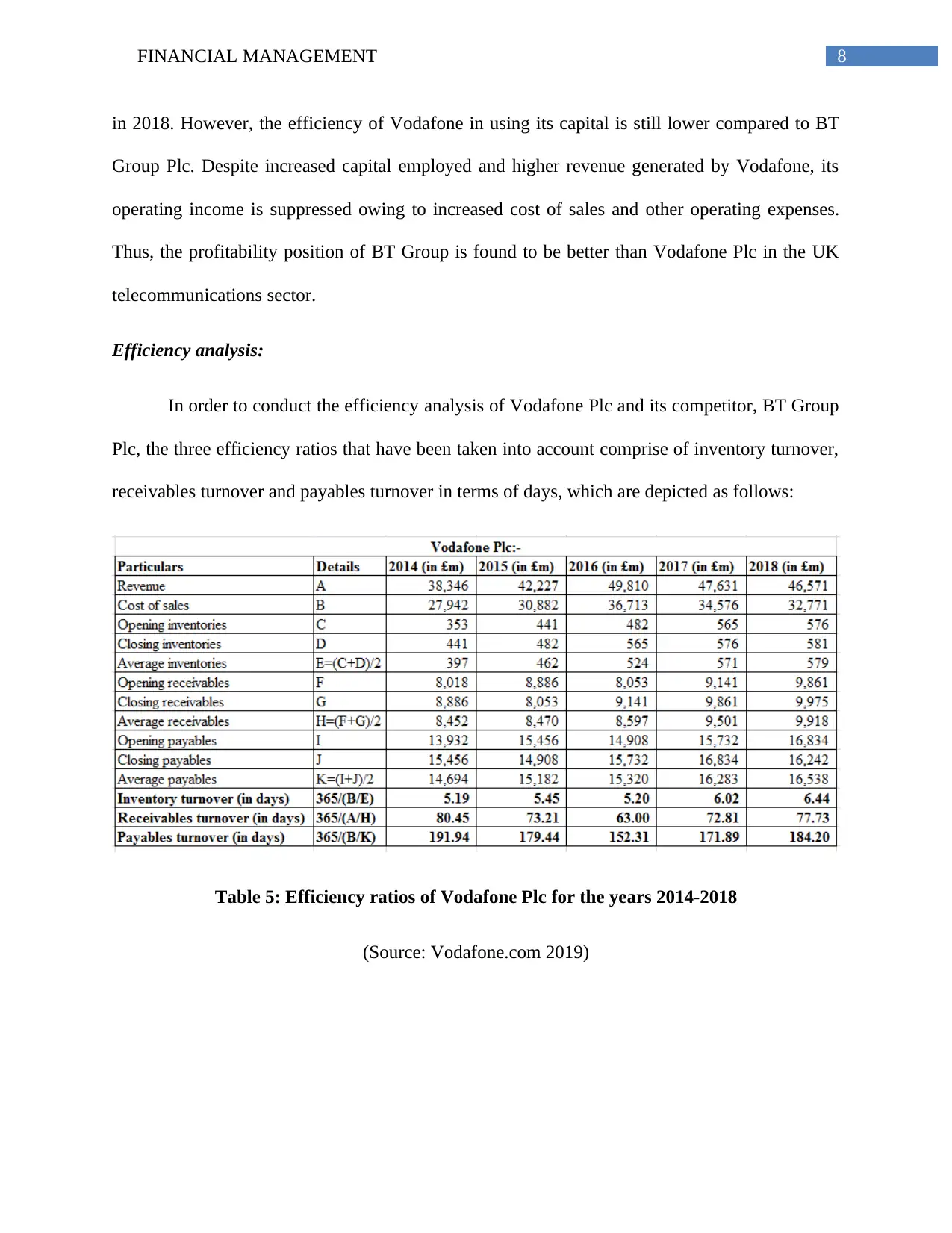

Profitability analysis:

In order to conduct the profitability analysis of Vodafone Plc and its competitor, BT

Group Plc, the two profitability ratios that have been taken into account comprise of net margin

and return on capital employed (ROCE), which are presented as follows:

Table 3: Profitability ratios of Vodafone Plc for the years 2014-2018

(Source: Vodafone.com 2019)

Table 4: Profitability ratios of BT Group Plc for the years 2014-2018

standard of 1 (Bekaert and Hodrick 2017). The main reason behind such stable position in

liquidity of Vodafone Plc is the fall in short-term borrowings, which has assisted the organisation

in maintaining stable liquidity position in the market. Hence, in terms of liquidity, Vodafone Plc

is observed to be in a favourable position in comparison to BT Group Plc in the UK

telecommunications sector.

Profitability analysis:

In order to conduct the profitability analysis of Vodafone Plc and its competitor, BT

Group Plc, the two profitability ratios that have been taken into account comprise of net margin

and return on capital employed (ROCE), which are presented as follows:

Table 3: Profitability ratios of Vodafone Plc for the years 2014-2018

(Source: Vodafone.com 2019)

Table 4: Profitability ratios of BT Group Plc for the years 2014-2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

(Source: Btplc.com 2019)

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Vodafone Plc BT Group Plc

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

Profitability Ratios

Net margin

Return on capital employed

(ROCE)

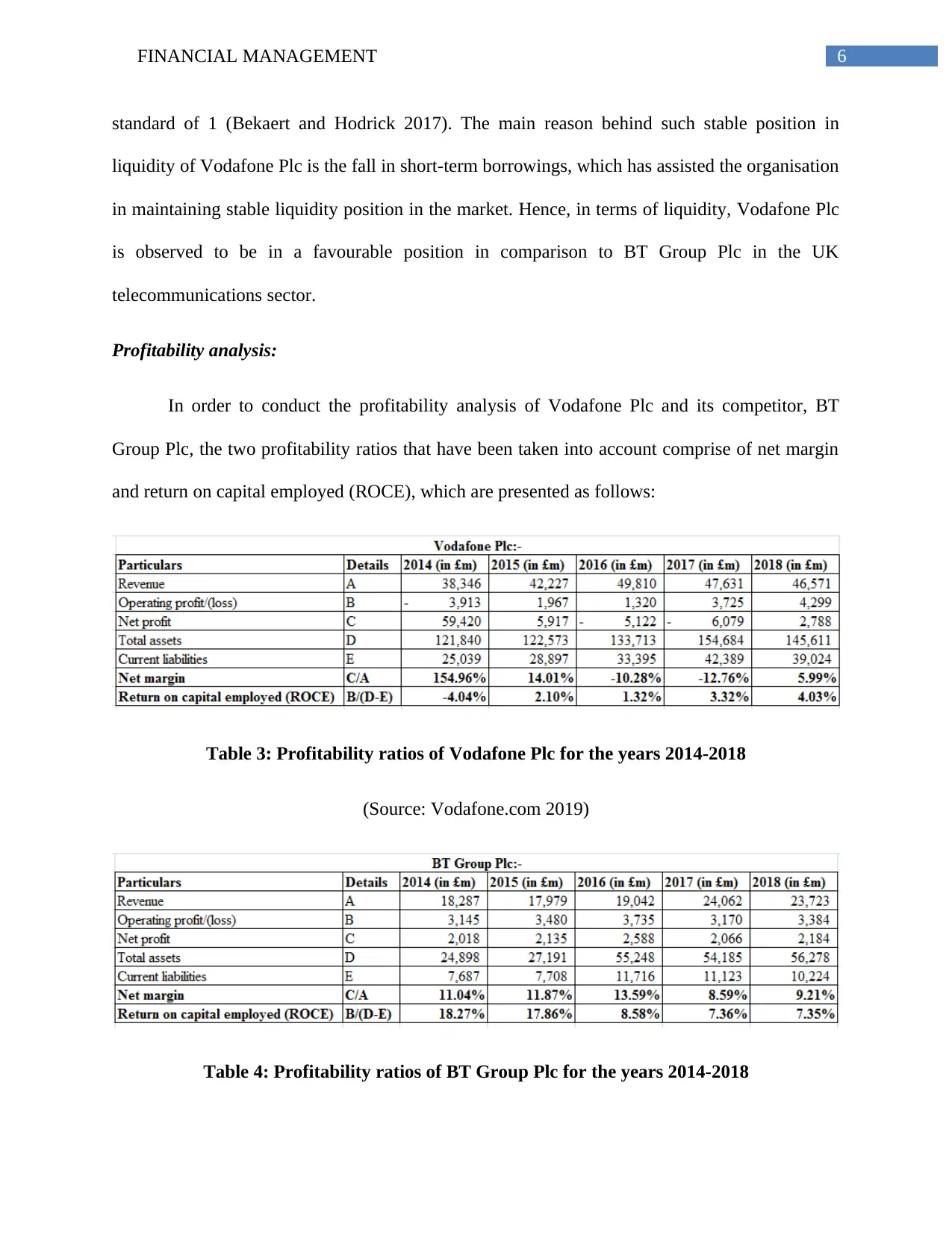

Figure 2: Profitability ratios of Vodafone Plc and BT Group Plc for the years 2014-2018

(Source: Vodafone.com 2019: Btplc.com 2019)

The net margin of Vodafone Plc after being massive to 154.96% in 2014 has declined

sharply until 2017 where it has suffered loss; however, its position has been improved in 2018.

The decline is mainly due to the loss incurred by the organisation from its discontinuing

operations. On the other hand, net margin has remained positive in all years despite fluctuating

trend shown over the years. Therefore, in terms of profitability, BT Group is enjoying

competitive advantage over Vodafone Plc in the UK market.

ROCE analyses the efficiency with which an organisation employs its capital in order to

derive profits (Brigham and Daves 2014). In case of Vodafone Plc, ROCE has risen from -4.04%

in 2014 to 4.03% in 2018, which is mainly due to improved efficiency in managing operating

expenses that witnessed rise in operating profit from (£3,913 million) in 2014 to £4,299 million

in 2018. On the contrary, ROCE for BT Group has fallen sharply from 18.27% in 2014 to 7.35%

(Source: Btplc.com 2019)

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Vodafone Plc BT Group Plc

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

Profitability Ratios

Net margin

Return on capital employed

(ROCE)

Figure 2: Profitability ratios of Vodafone Plc and BT Group Plc for the years 2014-2018

(Source: Vodafone.com 2019: Btplc.com 2019)

The net margin of Vodafone Plc after being massive to 154.96% in 2014 has declined

sharply until 2017 where it has suffered loss; however, its position has been improved in 2018.

The decline is mainly due to the loss incurred by the organisation from its discontinuing

operations. On the other hand, net margin has remained positive in all years despite fluctuating

trend shown over the years. Therefore, in terms of profitability, BT Group is enjoying

competitive advantage over Vodafone Plc in the UK market.

ROCE analyses the efficiency with which an organisation employs its capital in order to

derive profits (Brigham and Daves 2014). In case of Vodafone Plc, ROCE has risen from -4.04%

in 2014 to 4.03% in 2018, which is mainly due to improved efficiency in managing operating

expenses that witnessed rise in operating profit from (£3,913 million) in 2014 to £4,299 million

in 2018. On the contrary, ROCE for BT Group has fallen sharply from 18.27% in 2014 to 7.35%

8FINANCIAL MANAGEMENT

in 2018. However, the efficiency of Vodafone in using its capital is still lower compared to BT

Group Plc. Despite increased capital employed and higher revenue generated by Vodafone, its

operating income is suppressed owing to increased cost of sales and other operating expenses.

Thus, the profitability position of BT Group is found to be better than Vodafone Plc in the UK

telecommunications sector.

Efficiency analysis:

In order to conduct the efficiency analysis of Vodafone Plc and its competitor, BT Group

Plc, the three efficiency ratios that have been taken into account comprise of inventory turnover,

receivables turnover and payables turnover in terms of days, which are depicted as follows:

Table 5: Efficiency ratios of Vodafone Plc for the years 2014-2018

(Source: Vodafone.com 2019)

in 2018. However, the efficiency of Vodafone in using its capital is still lower compared to BT

Group Plc. Despite increased capital employed and higher revenue generated by Vodafone, its

operating income is suppressed owing to increased cost of sales and other operating expenses.

Thus, the profitability position of BT Group is found to be better than Vodafone Plc in the UK

telecommunications sector.

Efficiency analysis:

In order to conduct the efficiency analysis of Vodafone Plc and its competitor, BT Group

Plc, the three efficiency ratios that have been taken into account comprise of inventory turnover,

receivables turnover and payables turnover in terms of days, which are depicted as follows:

Table 5: Efficiency ratios of Vodafone Plc for the years 2014-2018

(Source: Vodafone.com 2019)

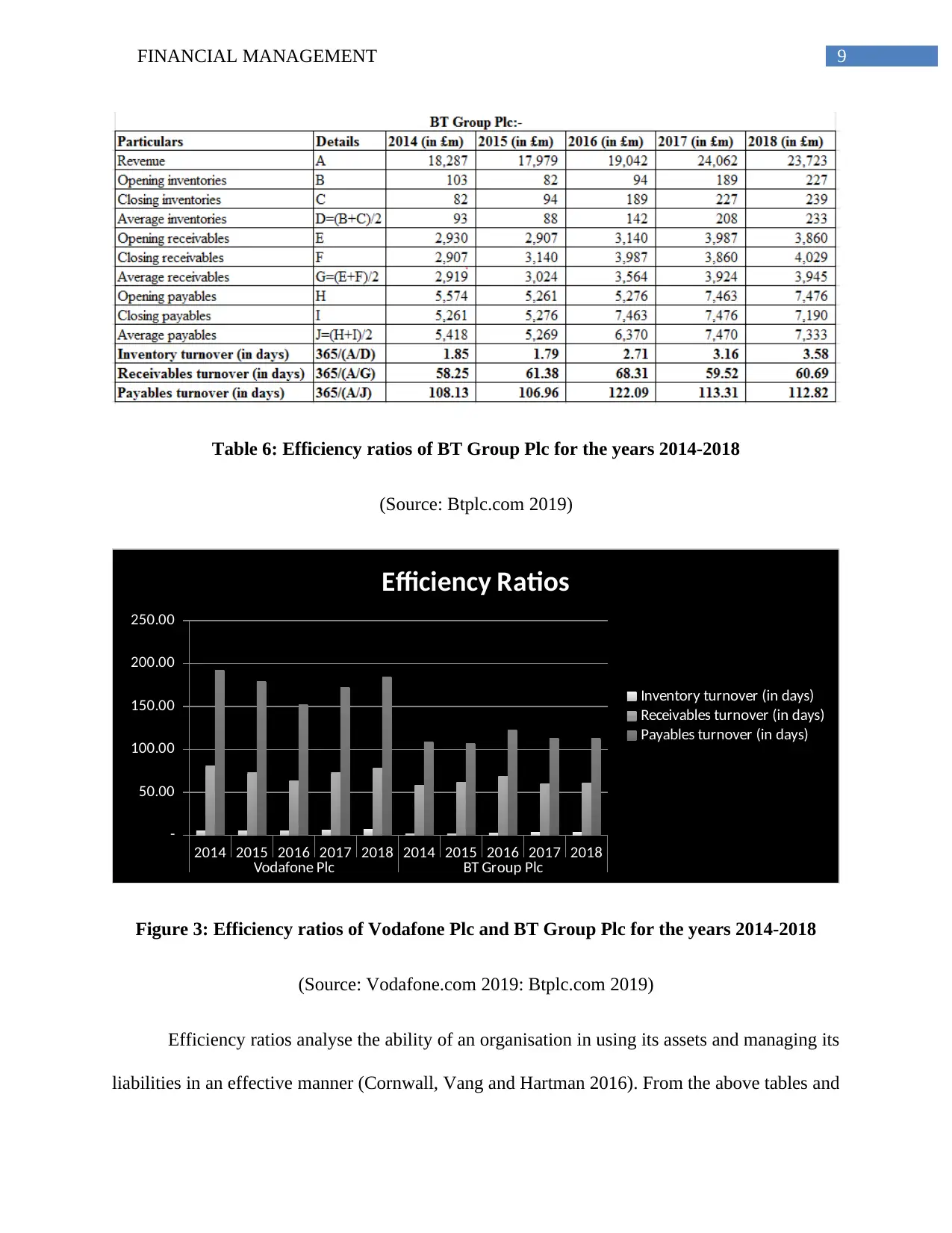

9FINANCIAL MANAGEMENT

Table 6: Efficiency ratios of BT Group Plc for the years 2014-2018

(Source: Btplc.com 2019)

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Vodafone Plc BT Group Plc

-

50.00

100.00

150.00

200.00

250.00

Efficiency Ratios

Inventory turnover (in days)

Receivables turnover (in days)

Payables turnover (in days)

Figure 3: Efficiency ratios of Vodafone Plc and BT Group Plc for the years 2014-2018

(Source: Vodafone.com 2019: Btplc.com 2019)

Efficiency ratios analyse the ability of an organisation in using its assets and managing its

liabilities in an effective manner (Cornwall, Vang and Hartman 2016). From the above tables and

Table 6: Efficiency ratios of BT Group Plc for the years 2014-2018

(Source: Btplc.com 2019)

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Vodafone Plc BT Group Plc

-

50.00

100.00

150.00

200.00

250.00

Efficiency Ratios

Inventory turnover (in days)

Receivables turnover (in days)

Payables turnover (in days)

Figure 3: Efficiency ratios of Vodafone Plc and BT Group Plc for the years 2014-2018

(Source: Vodafone.com 2019: Btplc.com 2019)

Efficiency ratios analyse the ability of an organisation in using its assets and managing its

liabilities in an effective manner (Cornwall, Vang and Hartman 2016). From the above tables and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL MANAGEMENT

figure, Vodafone Plc has taken 5-6 days in transferring its inventory into sales, while BT Group

has taken 2-4 days for converting its stock into sales. For computing inventory turnover and

payables turnover, revenue has been taken into consideration, since it has no cost of sales. This

signifies that BT Group Plc is more efficient than Vodafone Plc in terms of inventory

management. The rise in inventory turnover for Vodafone Plc denotes lack of efficiency in

inventory management despite the rise in revenues over the years, which implies that its product

demand is still stable.

In terms of receivables turnover, Vodafone has minimised 2 days from 2014-2018 to

collect due amounts from its customers, while the figure is increase in 3 days for BT Group.

However, the figure is still lower for BT Group, which implies that BT Group is collecting its

receivables more quickly compared to Vodafone Plc. Finally, in terms of payables turnover, the

figure has fallen from 191.94 days in 2014 to 184.20 days in 2018, while it has increased for BT

Group Plc from 108.13 days in 2014 to 112.82 days in 2018. Although Vodafone has managed to

reduce its supplier payment terms, BT Plc is still settling its supplier payments within shorter

timeframe, which signifies better relationship with the suppliers. However, if this is strained,

there would be decline in revenue, since the suppliers might decline the organisation additional

credit particularly on organisational inputs (Ehiedu 2014). Therefore, in terms of overall

efficiency, BT Group Plc is enjoying competitive edge over Vodafone Plc in the UK

telecommunications sector.

Capital structure analysis:

In order to conduct the solvency analysis of Vodafone Plc and its competitor, BT Group

Plc, the two capital structure ratios that have been taken into account comprise of debt/equity

ratio and interest cover ratio, which are depicted as follows:

figure, Vodafone Plc has taken 5-6 days in transferring its inventory into sales, while BT Group

has taken 2-4 days for converting its stock into sales. For computing inventory turnover and

payables turnover, revenue has been taken into consideration, since it has no cost of sales. This

signifies that BT Group Plc is more efficient than Vodafone Plc in terms of inventory

management. The rise in inventory turnover for Vodafone Plc denotes lack of efficiency in

inventory management despite the rise in revenues over the years, which implies that its product

demand is still stable.

In terms of receivables turnover, Vodafone has minimised 2 days from 2014-2018 to

collect due amounts from its customers, while the figure is increase in 3 days for BT Group.

However, the figure is still lower for BT Group, which implies that BT Group is collecting its

receivables more quickly compared to Vodafone Plc. Finally, in terms of payables turnover, the

figure has fallen from 191.94 days in 2014 to 184.20 days in 2018, while it has increased for BT

Group Plc from 108.13 days in 2014 to 112.82 days in 2018. Although Vodafone has managed to

reduce its supplier payment terms, BT Plc is still settling its supplier payments within shorter

timeframe, which signifies better relationship with the suppliers. However, if this is strained,

there would be decline in revenue, since the suppliers might decline the organisation additional

credit particularly on organisational inputs (Ehiedu 2014). Therefore, in terms of overall

efficiency, BT Group Plc is enjoying competitive edge over Vodafone Plc in the UK

telecommunications sector.

Capital structure analysis:

In order to conduct the solvency analysis of Vodafone Plc and its competitor, BT Group

Plc, the two capital structure ratios that have been taken into account comprise of debt/equity

ratio and interest cover ratio, which are depicted as follows:

11FINANCIAL MANAGEMENT

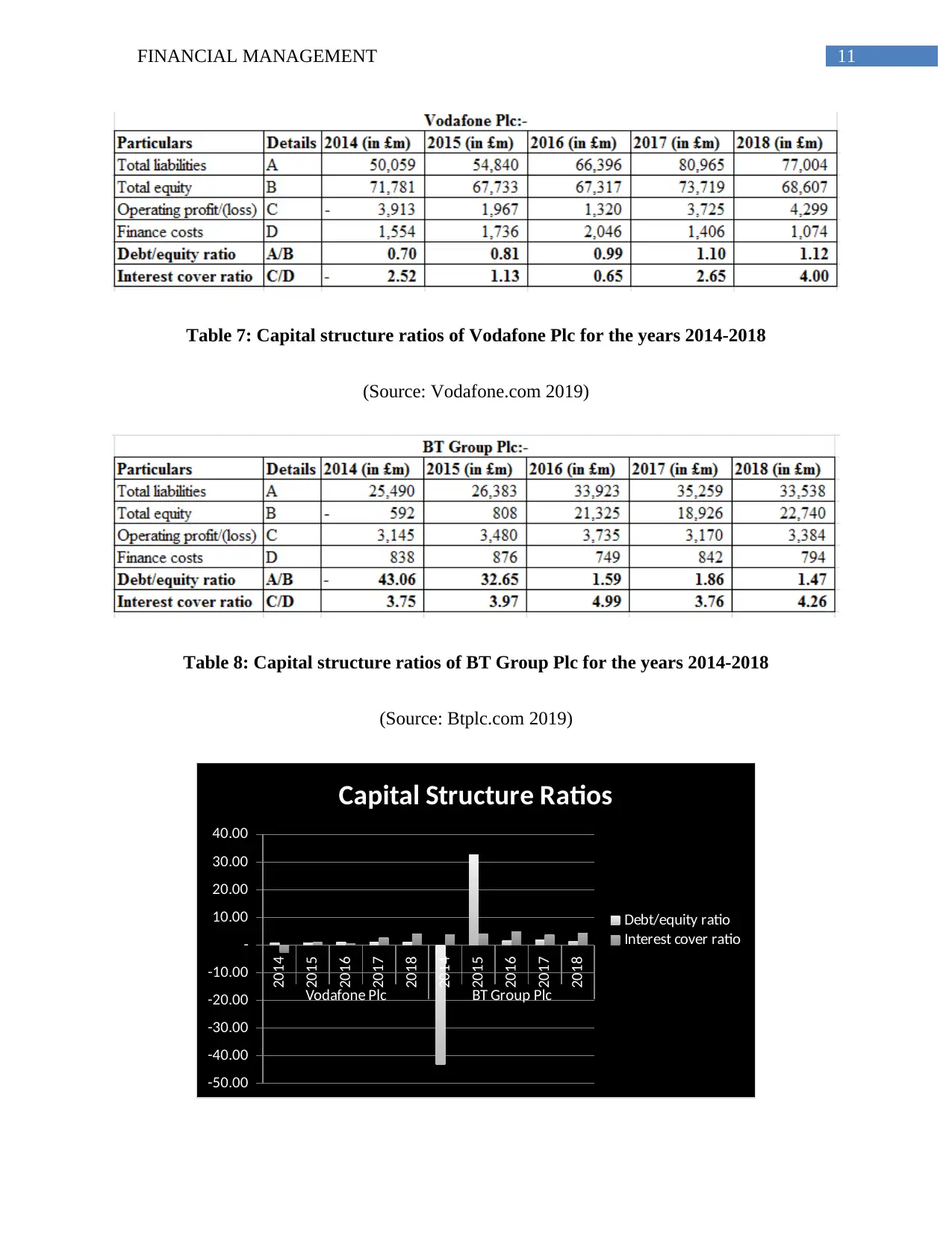

Table 7: Capital structure ratios of Vodafone Plc for the years 2014-2018

(Source: Vodafone.com 2019)

Table 8: Capital structure ratios of BT Group Plc for the years 2014-2018

(Source: Btplc.com 2019)

2014

2015

2016

2017

2018

2014

2015

2016

2017

2018

Vodafone Plc BT Group Plc

-50.00

-40.00

-30.00

-20.00

-10.00

-

10.00

20.00

30.00

40.00

Capital Structure Ratios

Debt/equity ratio

Interest cover ratio

Table 7: Capital structure ratios of Vodafone Plc for the years 2014-2018

(Source: Vodafone.com 2019)

Table 8: Capital structure ratios of BT Group Plc for the years 2014-2018

(Source: Btplc.com 2019)

2014

2015

2016

2017

2018

2014

2015

2016

2017

2018

Vodafone Plc BT Group Plc

-50.00

-40.00

-30.00

-20.00

-10.00

-

10.00

20.00

30.00

40.00

Capital Structure Ratios

Debt/equity ratio

Interest cover ratio

12FINANCIAL MANAGEMENT

Figure 4: Capital structure ratios of Vodafone Plc and BT Group Plc for the years 2014-

2018

(Source: Vodafone.com 2019: Btplc.com 2019)

The debt/equity ratio of Vodafone Plc is observed to increase over the five years from

2014 to 2018. However, this ratio for BT Group Pc is indicating a decreasing trend over the five

years span. Such results indicate that Vodafone Plc is not being efficient enough to address all its

debt obligations and is able to repay them quickly that is not evident in case of BT Group Plc, as

it is focusing on high equity financing. An increasing trend in the debt/equity ratio indicates that

Vodafone Plc. is making huge investments in its business growth through using high debts

(Salikin, AbWahab and Muhammad 2014). Whereas BT Group Ltd is using less debt finance its

assets. The interest cover ratio of Vodafone Plc. is indicating an increasing trend over the five

years from 2014 to 2018.

However, this ratio for BT Group Ltd is indicating a fluctuating trend over five years

where it is decreased in the years 2015 and 2017 and then increased in 2018. Such results signify

that Vodafone Plc. is paying off all its interest expenses based on its outstanding debt. However,

on the other hand, BT Group Ltd is observed to struggle in maintaining its financial position

stable every year through meeting its interest obligations from its operating earnings on a

constant basis (Robinson et al. 2015). The results of the capital structure ratios of both the

companies signify that Vodafone is dealing with concerns related to its high debt investments,

however is able to pay off its interest expenses in comparison to BT Group Ltd.

Stock market performance:

Figure 4: Capital structure ratios of Vodafone Plc and BT Group Plc for the years 2014-

2018

(Source: Vodafone.com 2019: Btplc.com 2019)

The debt/equity ratio of Vodafone Plc is observed to increase over the five years from

2014 to 2018. However, this ratio for BT Group Pc is indicating a decreasing trend over the five

years span. Such results indicate that Vodafone Plc is not being efficient enough to address all its

debt obligations and is able to repay them quickly that is not evident in case of BT Group Plc, as

it is focusing on high equity financing. An increasing trend in the debt/equity ratio indicates that

Vodafone Plc. is making huge investments in its business growth through using high debts

(Salikin, AbWahab and Muhammad 2014). Whereas BT Group Ltd is using less debt finance its

assets. The interest cover ratio of Vodafone Plc. is indicating an increasing trend over the five

years from 2014 to 2018.

However, this ratio for BT Group Ltd is indicating a fluctuating trend over five years

where it is decreased in the years 2015 and 2017 and then increased in 2018. Such results signify

that Vodafone Plc. is paying off all its interest expenses based on its outstanding debt. However,

on the other hand, BT Group Ltd is observed to struggle in maintaining its financial position

stable every year through meeting its interest obligations from its operating earnings on a

constant basis (Robinson et al. 2015). The results of the capital structure ratios of both the

companies signify that Vodafone is dealing with concerns related to its high debt investments,

however is able to pay off its interest expenses in comparison to BT Group Ltd.

Stock market performance:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL MANAGEMENT

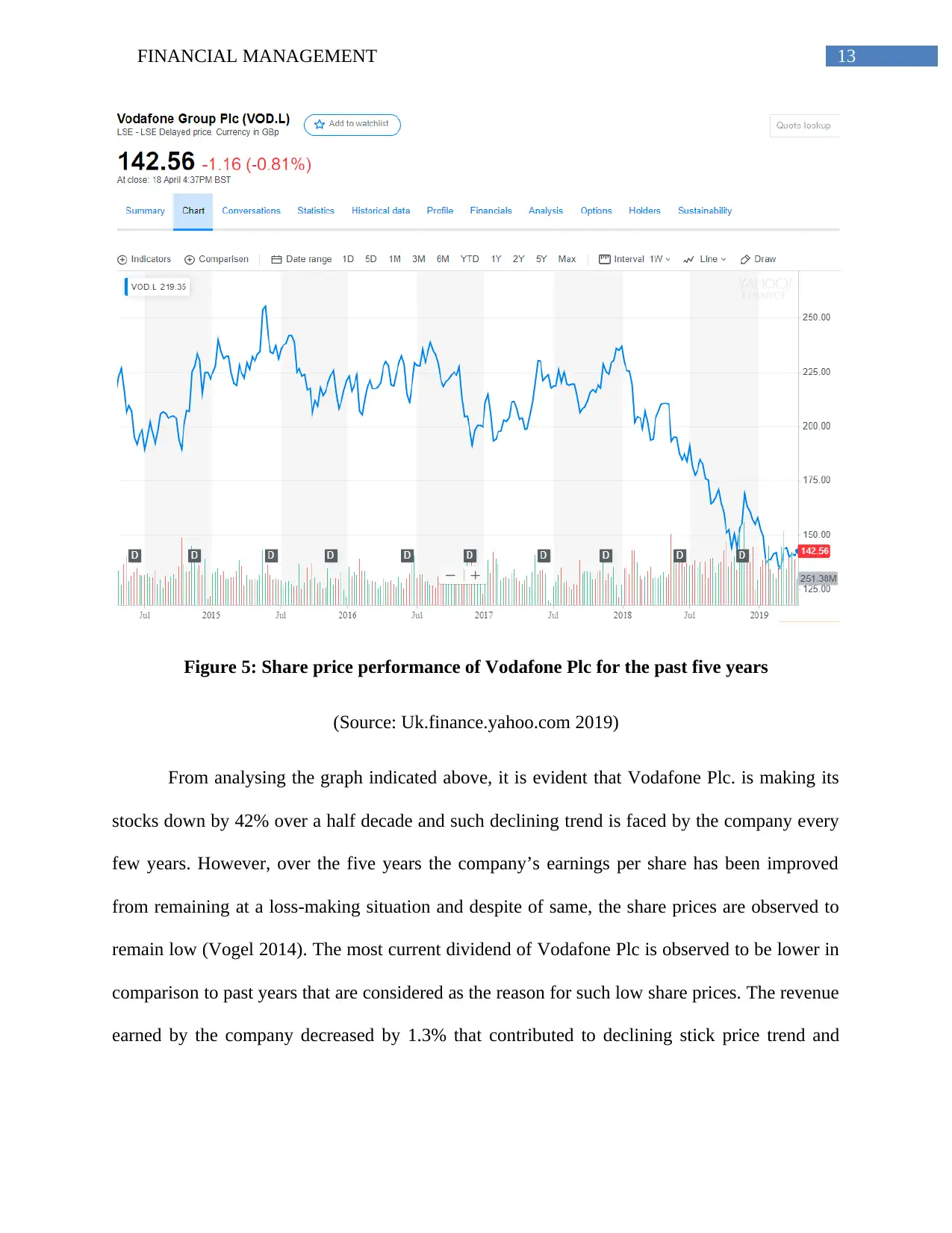

Figure 5: Share price performance of Vodafone Plc for the past five years

(Source: Uk.finance.yahoo.com 2019)

From analysing the graph indicated above, it is evident that Vodafone Plc. is making its

stocks down by 42% over a half decade and such declining trend is faced by the company every

few years. However, over the five years the company’s earnings per share has been improved

from remaining at a loss-making situation and despite of same, the share prices are observed to

remain low (Vogel 2014). The most current dividend of Vodafone Plc is observed to be lower in

comparison to past years that are considered as the reason for such low share prices. The revenue

earned by the company decreased by 1.3% that contributed to declining stick price trend and

Figure 5: Share price performance of Vodafone Plc for the past five years

(Source: Uk.finance.yahoo.com 2019)

From analysing the graph indicated above, it is evident that Vodafone Plc. is making its

stocks down by 42% over a half decade and such declining trend is faced by the company every

few years. However, over the five years the company’s earnings per share has been improved

from remaining at a loss-making situation and despite of same, the share prices are observed to

remain low (Vogel 2014). The most current dividend of Vodafone Plc is observed to be lower in

comparison to past years that are considered as the reason for such low share prices. The revenue

earned by the company decreased by 1.3% that contributed to declining stick price trend and

14FINANCIAL MANAGEMENT

considering the same it can be stated that poor revenue earnings and dividend trends have

negatively impacted the share price of Vodafone Plc.

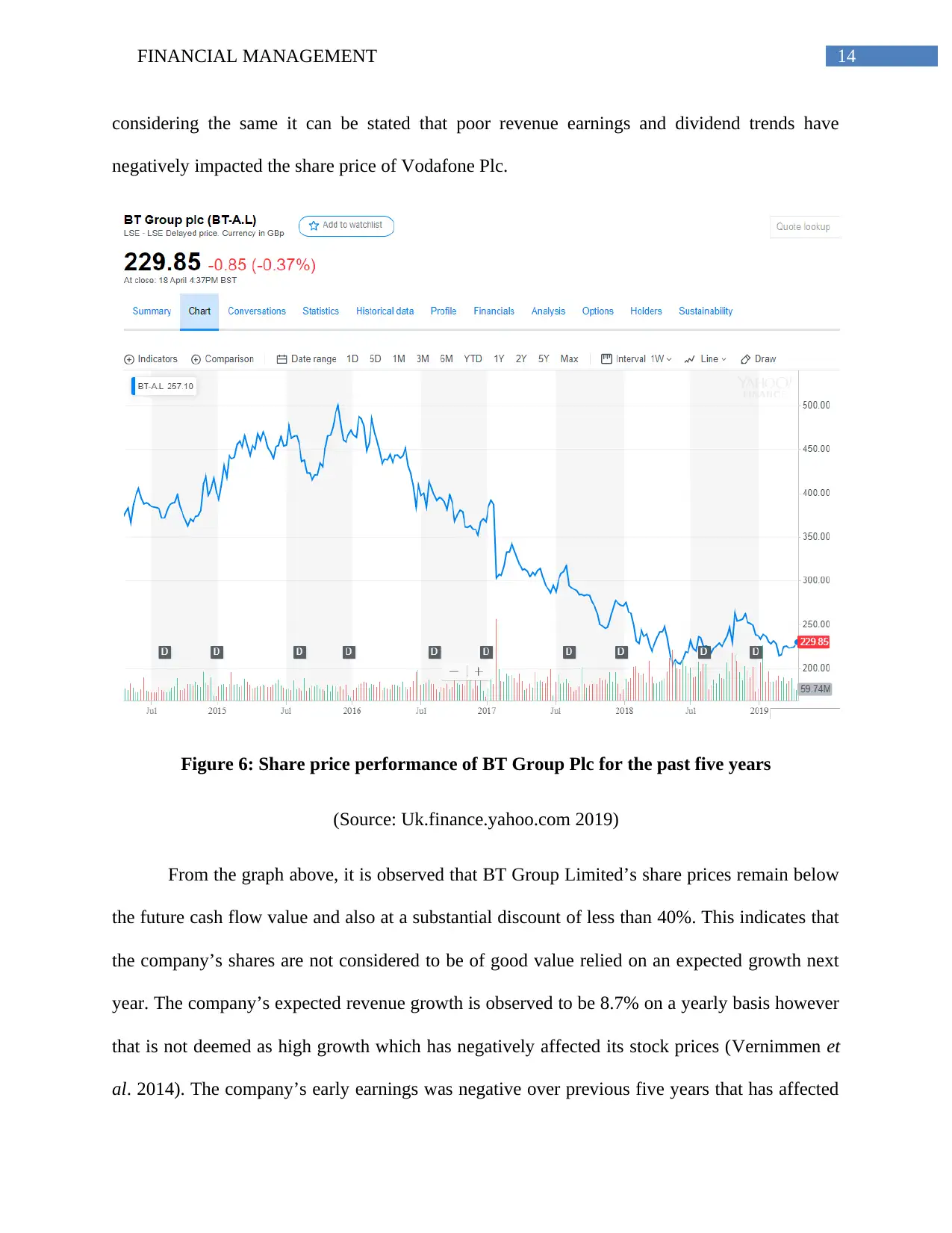

Figure 6: Share price performance of BT Group Plc for the past five years

(Source: Uk.finance.yahoo.com 2019)

From the graph above, it is observed that BT Group Limited’s share prices remain below

the future cash flow value and also at a substantial discount of less than 40%. This indicates that

the company’s shares are not considered to be of good value relied on an expected growth next

year. The company’s expected revenue growth is observed to be 8.7% on a yearly basis however

that is not deemed as high growth which has negatively affected its stock prices (Vernimmen et

al. 2014). The company’s early earnings was negative over previous five years that has affected

considering the same it can be stated that poor revenue earnings and dividend trends have

negatively impacted the share price of Vodafone Plc.

Figure 6: Share price performance of BT Group Plc for the past five years

(Source: Uk.finance.yahoo.com 2019)

From the graph above, it is observed that BT Group Limited’s share prices remain below

the future cash flow value and also at a substantial discount of less than 40%. This indicates that

the company’s shares are not considered to be of good value relied on an expected growth next

year. The company’s expected revenue growth is observed to be 8.7% on a yearly basis however

that is not deemed as high growth which has negatively affected its stock prices (Vernimmen et

al. 2014). The company’s early earnings was negative over previous five years that has affected

15FINANCIAL MANAGEMENT

its share prices negatively but its recent earnings are moving above average that can improve its

share prices in future. However, in the upcoming three years, BT Group Ltd has anticipated to

use its shareholders funds efficiently that can improve its share price movements.

Recommendations regarding buying shares in any of the two organisations:

Based on the above analysis, it could be found that Vodafone Plc has been enjoying

competitive edge over BT Group Plc in terms of liquidity in the UK market. However, in terms

of profitability, liquidity and capital structure, the position of BT Group Plc is found to be more

favourable than Vodafone Plc in the UK telecommunications industry. However, it has been

analysed both the organisations have scope for improvements in order to improve their financial

standing in the operating markets. In terms of stock market performance, the shares of BT Group

Plc are found to be performing better than Vodafone Plc in the London Stock Exchange. In

addition, BT Group has certain valuable assets in terms of human resources and specialised staffs

and its joint efforts with other organisations have definitely proved to be promising. Hence, it is

recommended to the investors to purchase the shares of BT Group Plc for generating better

returns in future. This is because investing in the shares of Vodafone Plc might result in lower

return on investment for the investors.

Problems, limitations and assumptions:

Even though recommendation has been provided to the investors, the analysis has certain

limitations. Firstly, in case of financial analysis, there has been usage of historical data for

contrasting the financial standing of Vodafone Plc and BT Group Plc. Since the analysis is based

on past information, it might not be useful for planning and undertaking decisions, since the past

does not always reflect the future. Secondly, ratio analysis and stock market performance do not

its share prices negatively but its recent earnings are moving above average that can improve its

share prices in future. However, in the upcoming three years, BT Group Ltd has anticipated to

use its shareholders funds efficiently that can improve its share price movements.

Recommendations regarding buying shares in any of the two organisations:

Based on the above analysis, it could be found that Vodafone Plc has been enjoying

competitive edge over BT Group Plc in terms of liquidity in the UK market. However, in terms

of profitability, liquidity and capital structure, the position of BT Group Plc is found to be more

favourable than Vodafone Plc in the UK telecommunications industry. However, it has been

analysed both the organisations have scope for improvements in order to improve their financial

standing in the operating markets. In terms of stock market performance, the shares of BT Group

Plc are found to be performing better than Vodafone Plc in the London Stock Exchange. In

addition, BT Group has certain valuable assets in terms of human resources and specialised staffs

and its joint efforts with other organisations have definitely proved to be promising. Hence, it is

recommended to the investors to purchase the shares of BT Group Plc for generating better

returns in future. This is because investing in the shares of Vodafone Plc might result in lower

return on investment for the investors.

Problems, limitations and assumptions:

Even though recommendation has been provided to the investors, the analysis has certain

limitations. Firstly, in case of financial analysis, there has been usage of historical data for

contrasting the financial standing of Vodafone Plc and BT Group Plc. Since the analysis is based

on past information, it might not be useful for planning and undertaking decisions, since the past

does not always reflect the future. Secondly, ratio analysis and stock market performance do not

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16FINANCIAL MANAGEMENT

consider qualitative information like management changes crucial for undertaking investment

decisions (Omar et al. 2014). In addition, comparison of the financial condition of the two

organisations does not consider the fact that BT Group has diversified operation portfolio like

healthcare and automotives, while Vodafone has its operations only on the telecommunications

sector. Finally, recommendation is provided to the investors based on the accuracy and reliability

of information contained in the annual reports of two organisations.

From the research reports, it has been evident that there would be decline in the dividend

payout ratio of BT Group to 55%, which is currently 66%. Moreover, the earnings per share of

the organisation are expected to decline to £0.22 in 2019. Thus, a falling EPS with lower payout

ratio would minimise future dividend payments (Uk.finance.yahoo.com 2019). On the other

hand, the future forecast of BT Group is conducted with the help of price/earnings ratio, which

reveals slight decline in share price performance.

Therefore, the investors need to consider these aspects as well before investing in the

shares of BT Group Plc.

Conclusion:

From the above discussion, it is apparent that BT Group Plc is in a better position than

Vodafone Plc in the UK telecommunications sector owing to better financial performance in the

past five years. In addition, by considering stock market performance, the investors are

consider qualitative information like management changes crucial for undertaking investment

decisions (Omar et al. 2014). In addition, comparison of the financial condition of the two

organisations does not consider the fact that BT Group has diversified operation portfolio like

healthcare and automotives, while Vodafone has its operations only on the telecommunications

sector. Finally, recommendation is provided to the investors based on the accuracy and reliability

of information contained in the annual reports of two organisations.

From the research reports, it has been evident that there would be decline in the dividend

payout ratio of BT Group to 55%, which is currently 66%. Moreover, the earnings per share of

the organisation are expected to decline to £0.22 in 2019. Thus, a falling EPS with lower payout

ratio would minimise future dividend payments (Uk.finance.yahoo.com 2019). On the other

hand, the future forecast of BT Group is conducted with the help of price/earnings ratio, which

reveals slight decline in share price performance.

Therefore, the investors need to consider these aspects as well before investing in the

shares of BT Group Plc.

Conclusion:

From the above discussion, it is apparent that BT Group Plc is in a better position than

Vodafone Plc in the UK telecommunications sector owing to better financial performance in the

past five years. In addition, by considering stock market performance, the investors are

17FINANCIAL MANAGEMENT

recommended to invest in the shares of BT Group for maximising their return on investment.

However, the analysis is subject to certain limitations, since it has considered historical data only

for decision-making. Therefore, research reports and price/earnings ratio have been taken into

consideration, which reveal that the performance of BT Group is expected to decline in the

upcoming years, especially in terms of earnings per share and dividend payments. Hence, the

investors need to consider these aspects as well before investing in the shares of BT Group Plc.

recommended to invest in the shares of BT Group for maximising their return on investment.

However, the analysis is subject to certain limitations, since it has considered historical data only

for decision-making. Therefore, research reports and price/earnings ratio have been taken into

consideration, which reveal that the performance of BT Group is expected to decline in the

upcoming years, especially in terms of earnings per share and dividend payments. Hence, the

investors need to consider these aspects as well before investing in the shares of BT Group Plc.

18FINANCIAL MANAGEMENT

References and Bibliographies:

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), pp.332-338.

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge University

Press.

Brigham, E.F. and Daves, P.R., 2014. Intermediate financial management. Cengage Learning.

Btplc.com., 2019. Annual reports. [online] Available at:

https://www.btplc.com/Sharesandperformance/Financialreportingandnews/

Annualreportandreview/index.htm [Accessed 22 Apr. 2019].

Btplc.com., 2019. BTPLC.com home page. [online] Available at: https://www.btplc.com/

[Accessed 22 Apr. 2019].

Budde.com.au., 2019. United Kingdom - Telecoms Infrastructure, Operators, Regulations -

Statistics and Analyses. [online] Available at: https://www.budde.com.au/Research/United-

Kingdom-Telecoms-Infrastructure-Operators-Regulations-Statistics-and-Analyses [Accessed 22

Apr. 2019].

Cornwall, J.R., Vang, D.O. and Hartman, J.M., 2016. Entrepreneurial financial management: An

applied approach. Routledge.

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: the

financial statement analysis (FSA) approach. Research Journal of Finance and Accounting, 5(5),

pp.81-90.

References and Bibliographies:

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business

Research, 67(3), pp.332-338.

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge University

Press.

Brigham, E.F. and Daves, P.R., 2014. Intermediate financial management. Cengage Learning.

Btplc.com., 2019. Annual reports. [online] Available at:

https://www.btplc.com/Sharesandperformance/Financialreportingandnews/

Annualreportandreview/index.htm [Accessed 22 Apr. 2019].

Btplc.com., 2019. BTPLC.com home page. [online] Available at: https://www.btplc.com/

[Accessed 22 Apr. 2019].

Budde.com.au., 2019. United Kingdom - Telecoms Infrastructure, Operators, Regulations -

Statistics and Analyses. [online] Available at: https://www.budde.com.au/Research/United-

Kingdom-Telecoms-Infrastructure-Operators-Regulations-Statistics-and-Analyses [Accessed 22

Apr. 2019].

Cornwall, J.R., Vang, D.O. and Hartman, J.M., 2016. Entrepreneurial financial management: An

applied approach. Routledge.

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: the

financial statement analysis (FSA) approach. Research Journal of Finance and Accounting, 5(5),

pp.81-90.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19FINANCIAL MANAGEMENT

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Mayes, T.R., 2014. Financial Analysis with Microsoft Excel. Nelson Education.

Omar, N., Koya, R.K., Sanusi, Z.M. and Shafie, N.A., 2014. Financial statement fraud: A case

examination using Beneish model and ratio analysis. International Journal of Trade, Economics

and Finance, 5(2), p.184.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Salikin, N., Ab Wahab, N. and Muhammad, I., 2014. Strengths and weaknesses among

Malaysian SMEs: Financial management perspectives. Procedia-Social and Behavioral

Sciences, 129, pp.334-340.

Uk.finance.yahoo.com., 2019. [online] Available at: https://uk.finance.yahoo.com/news/bt-

group-plc-lon-bt-072949981.html [Accessed 22 Apr. 2019].

Uk.finance.yahoo.com., 2019. [online] Available at:

https://uk.finance.yahoo.com/quote/VOD.L?p=VOD.L [Accessed 22 Apr. 2019].

Uk.finance.yahoo.com., 2019. [online] Available at: https://uk.finance.yahoo.com/quote/bt-a.l/

[Accessed 22 Apr. 2019].

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate finance:

theory and practice. John Wiley & Sons.

Vodafone.co.uk., 2019. Phone Deals, SIMs & Award-Winning Broadband | Vodafone. [online]

Available at: http://www.vodafone.co.uk/ [Accessed 22 Apr. 2019].

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Mayes, T.R., 2014. Financial Analysis with Microsoft Excel. Nelson Education.

Omar, N., Koya, R.K., Sanusi, Z.M. and Shafie, N.A., 2014. Financial statement fraud: A case

examination using Beneish model and ratio analysis. International Journal of Trade, Economics

and Finance, 5(2), p.184.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Salikin, N., Ab Wahab, N. and Muhammad, I., 2014. Strengths and weaknesses among

Malaysian SMEs: Financial management perspectives. Procedia-Social and Behavioral

Sciences, 129, pp.334-340.

Uk.finance.yahoo.com., 2019. [online] Available at: https://uk.finance.yahoo.com/news/bt-

group-plc-lon-bt-072949981.html [Accessed 22 Apr. 2019].

Uk.finance.yahoo.com., 2019. [online] Available at:

https://uk.finance.yahoo.com/quote/VOD.L?p=VOD.L [Accessed 22 Apr. 2019].

Uk.finance.yahoo.com., 2019. [online] Available at: https://uk.finance.yahoo.com/quote/bt-a.l/

[Accessed 22 Apr. 2019].

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate finance:

theory and practice. John Wiley & Sons.

Vodafone.co.uk., 2019. Phone Deals, SIMs & Award-Winning Broadband | Vodafone. [online]

Available at: http://www.vodafone.co.uk/ [Accessed 22 Apr. 2019].

20FINANCIAL MANAGEMENT

Vodafone.com., 2019. Vodafone Group Plc annual reports. [online] Available at:

https://www.vodafone.com/content/index/investors/investor_information/annual_report.html#

[Accessed 22 Apr. 2019].

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis. Cambridge

University Press.

Vodafone.com., 2019. Vodafone Group Plc annual reports. [online] Available at:

https://www.vodafone.com/content/index/investors/investor_information/annual_report.html#

[Accessed 22 Apr. 2019].

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis. Cambridge

University Press.

21FINANCIAL MANAGEMENT

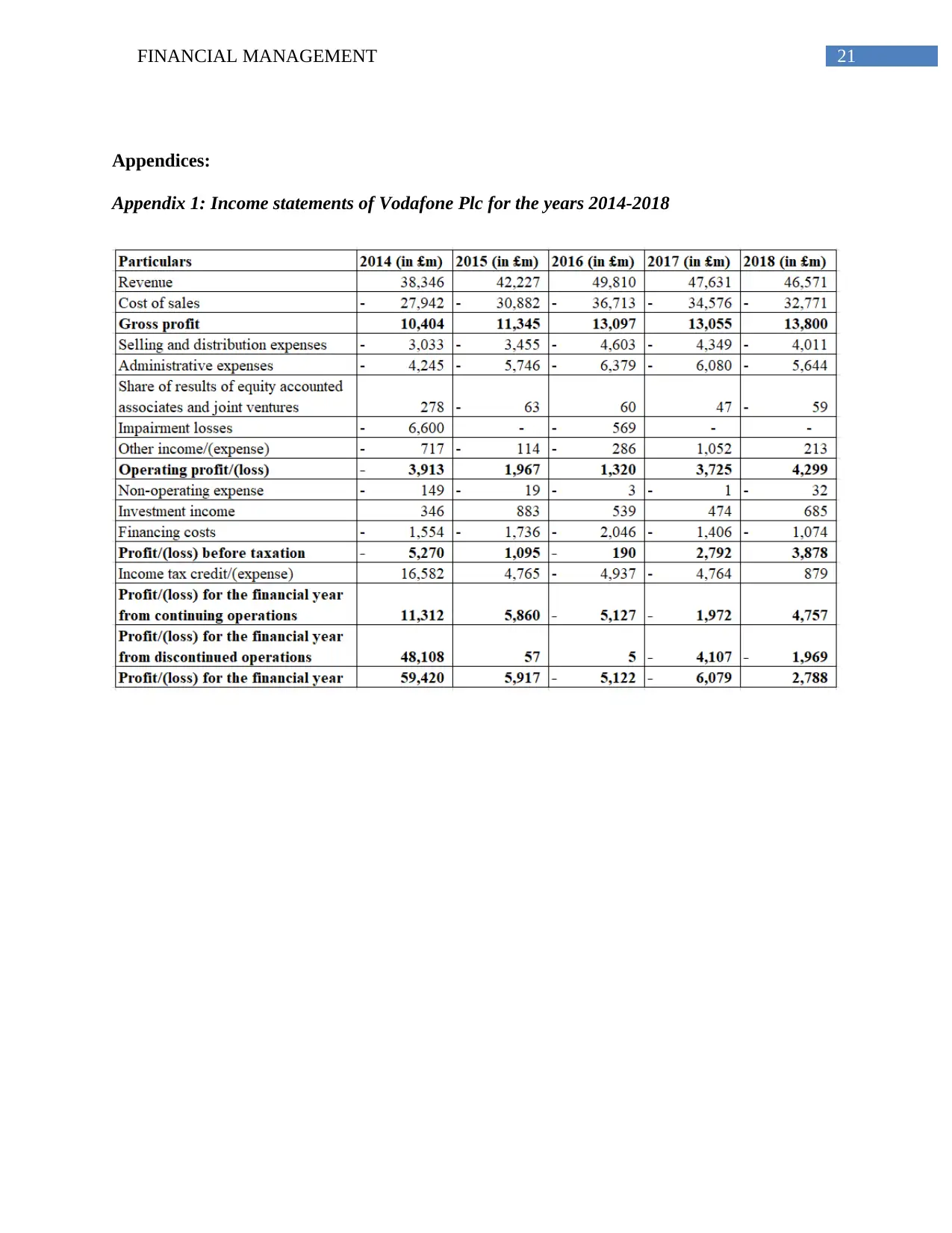

Appendices:

Appendix 1: Income statements of Vodafone Plc for the years 2014-2018

Appendices:

Appendix 1: Income statements of Vodafone Plc for the years 2014-2018

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

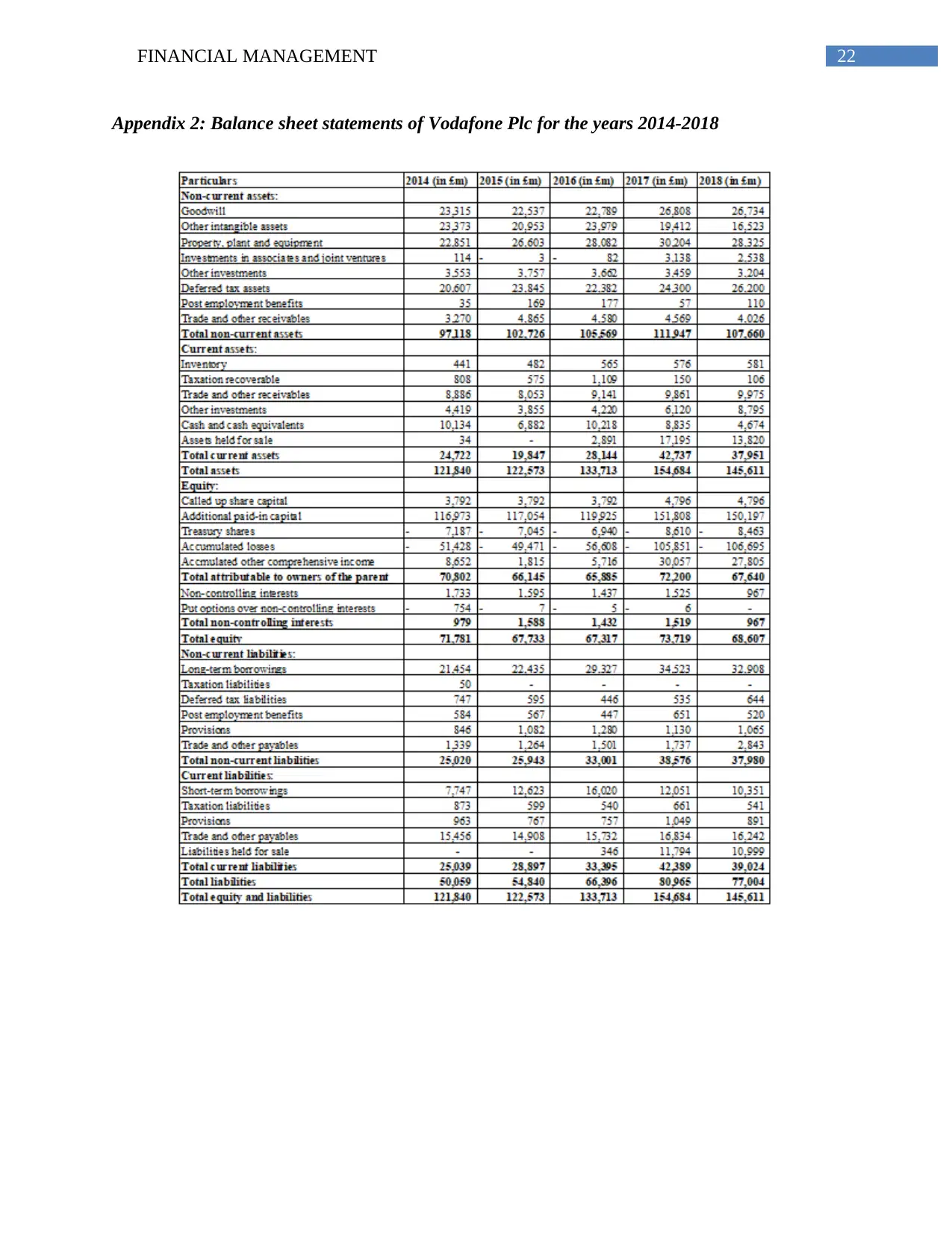

22FINANCIAL MANAGEMENT

Appendix 2: Balance sheet statements of Vodafone Plc for the years 2014-2018

Appendix 2: Balance sheet statements of Vodafone Plc for the years 2014-2018

23FINANCIAL MANAGEMENT

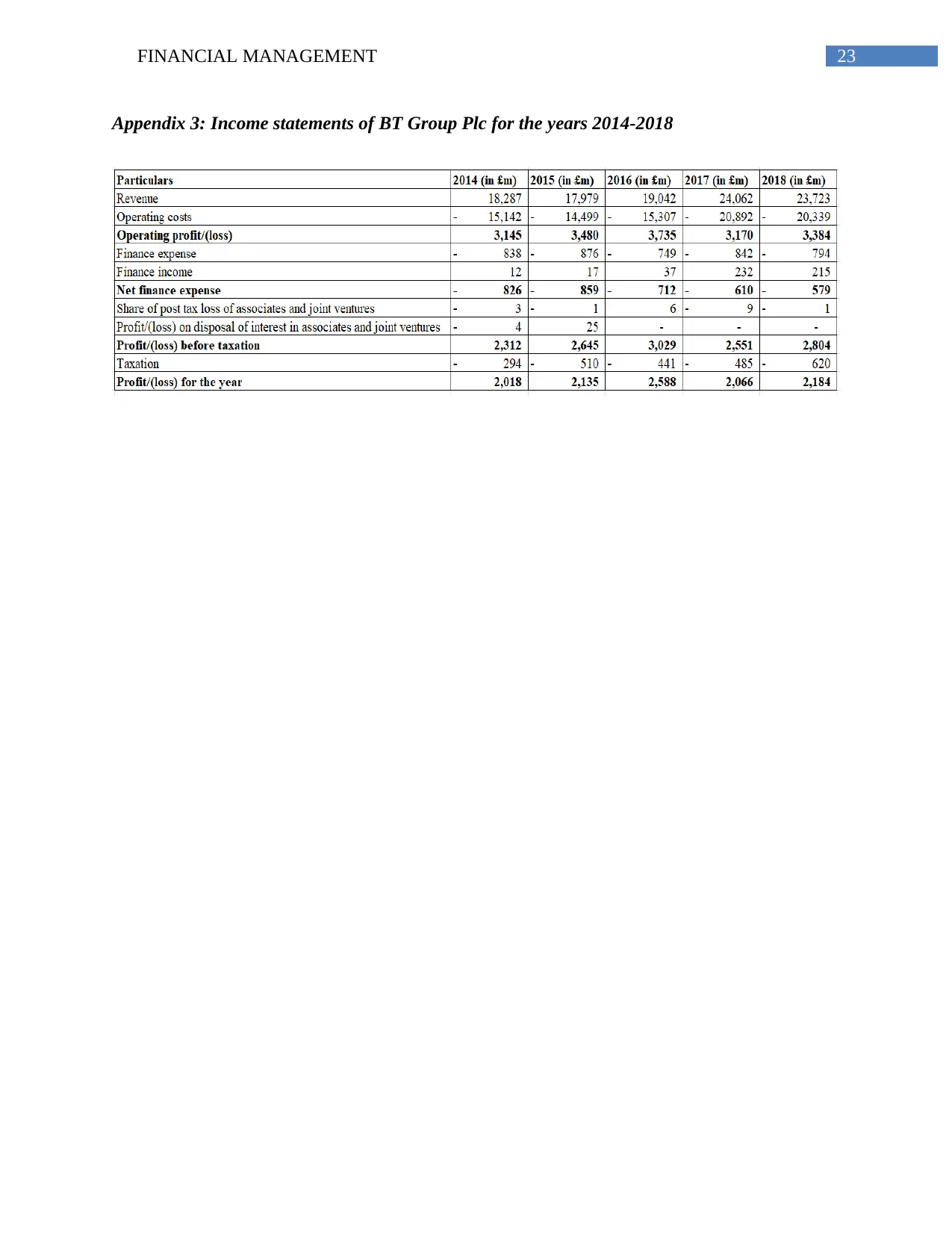

Appendix 3: Income statements of BT Group Plc for the years 2014-2018

Appendix 3: Income statements of BT Group Plc for the years 2014-2018

24FINANCIAL MANAGEMENT

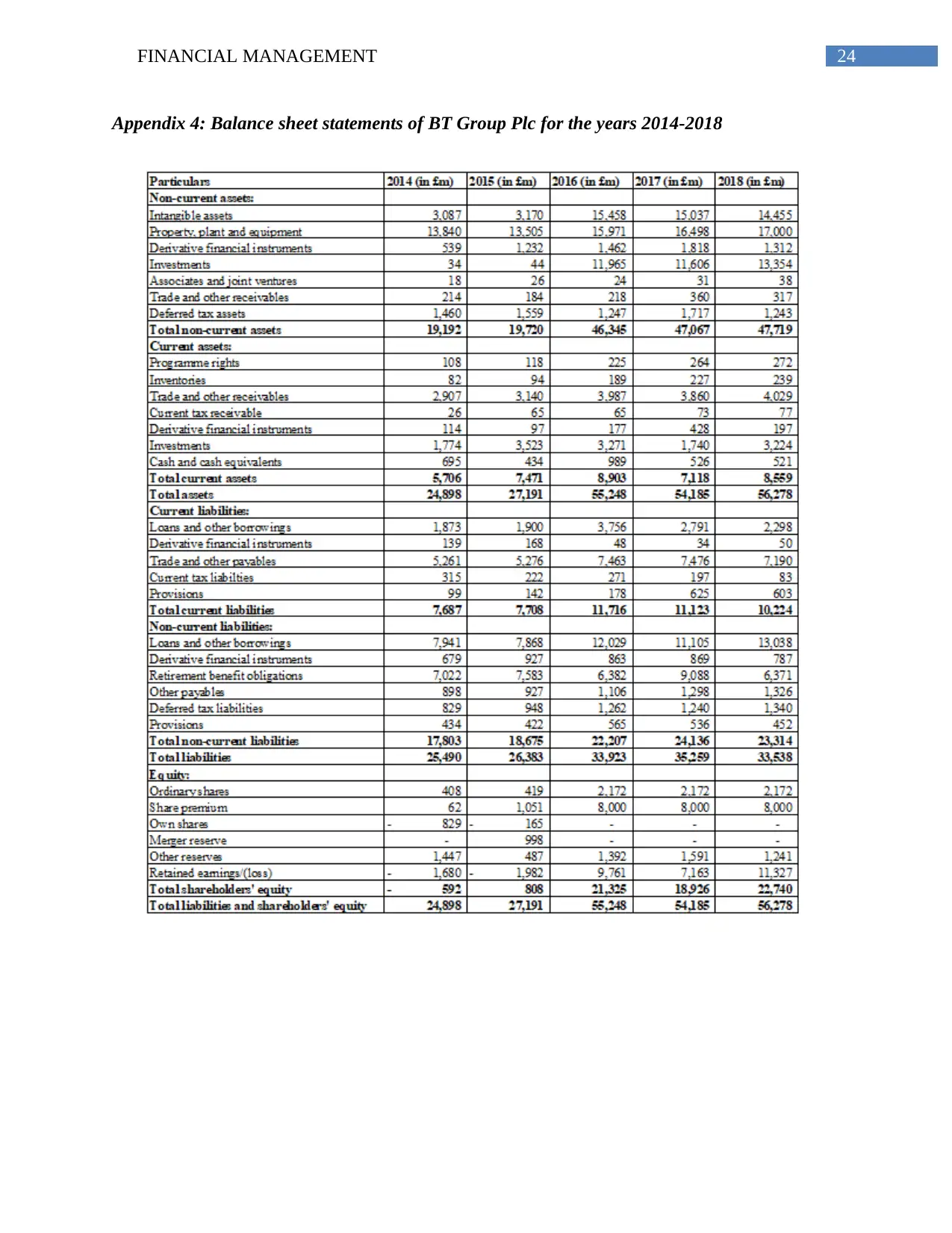

Appendix 4: Balance sheet statements of BT Group Plc for the years 2014-2018

Appendix 4: Balance sheet statements of BT Group Plc for the years 2014-2018

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.