Financial Performance Management (Online Exam) Analysis Report

VerifiedAdded on 2022/12/28

|10

|1965

|79

Homework Assignment

AI Summary

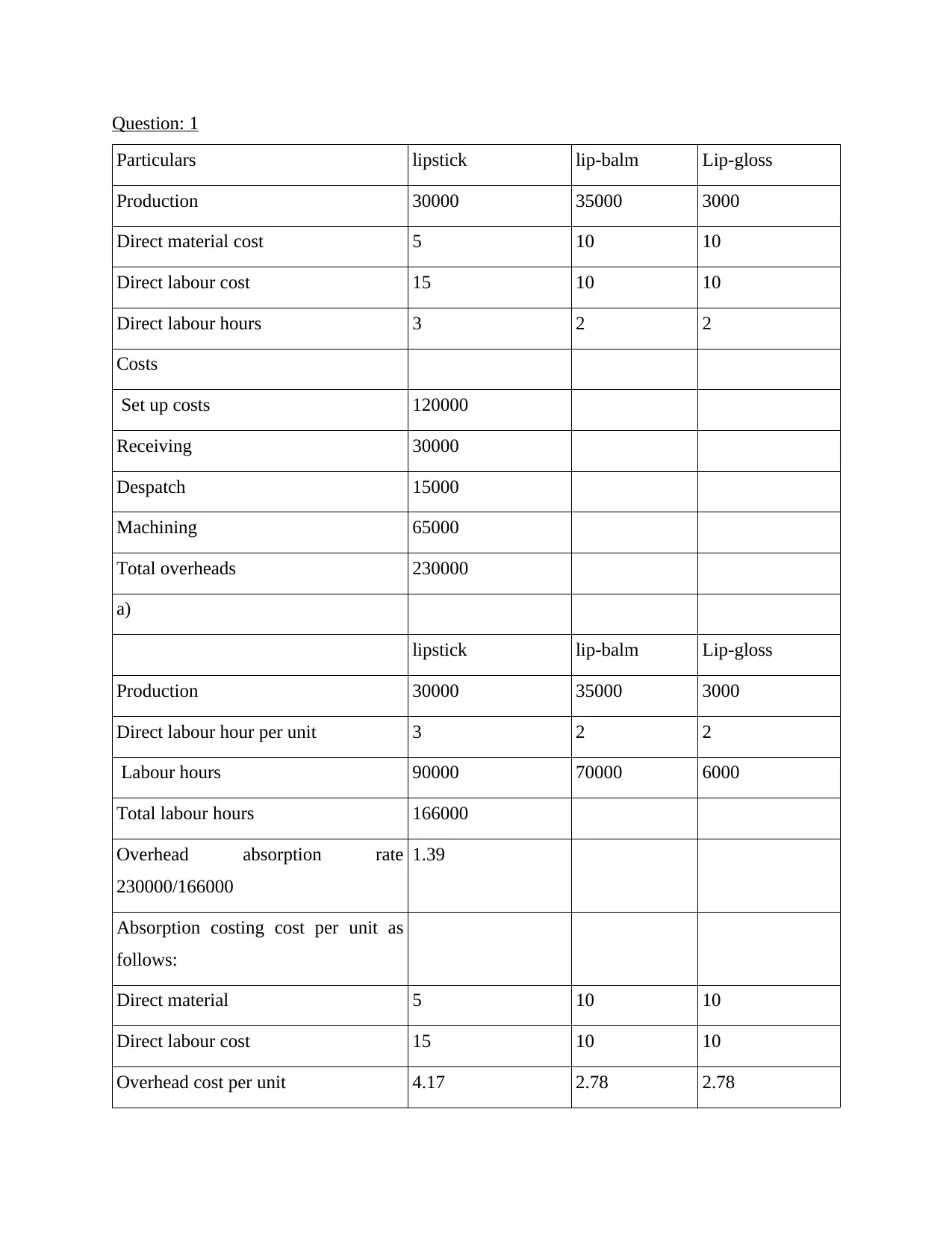

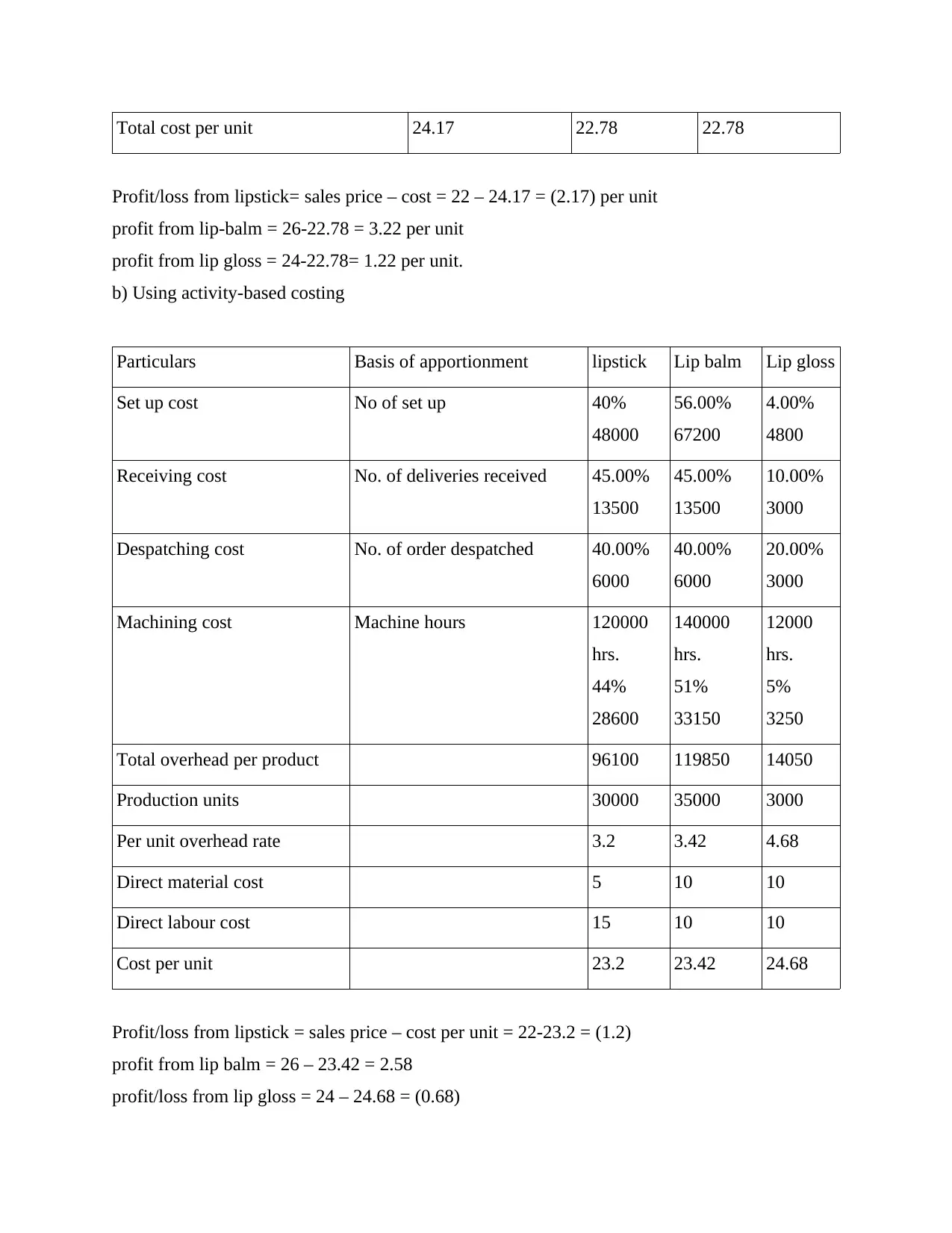

This assignment delves into various aspects of financial performance management, commencing with an analysis of overhead absorption rates and activity-based costing for different product lines (lipstick, lip balm, and lip gloss), evaluating their impact on profitability. It then explores the role of sensitivity analysis in addressing uncertainties within a business context. Furthermore, the assignment examines material variance analysis, including material usage, mix, and yield variances, and discusses the responsibilities of different managerial roles in relation to these variances. Finally, it contrasts zero-based budgeting with incremental budgeting, weighing the merits and demerits of each approach and suggesting a combined strategy for improved financial planning and control, also addressing the limitations of traditional budgeting methods.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.