SP2 2022: BANK 2008 Financial Planning Assignment 1 Detailed Report

VerifiedAdded on 2023/06/12

|10

|2135

|229

Report

AI Summary

This report identifies and evaluates demographic factors impacting the aging population in developed countries. It highlights the financial planning process and assesses superannuation contribution adequacy. The report also analyzes three investment alternatives, discussing their risks and benefits, and includes the preparation of a cash flow statement and personal balance sheet. The analysis covers expected income and capital generation from investments, ranking of investment options, and the issues and benefits of investment diversification. The report concludes with a summary of findings and a list of references.

Introduction to financial

planning

planning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

a) Identification of demographic factors and evaluating its impact on rapidly ageing population

......................................................................................................................................................3

b) Process of financial planning and requirements of financial advisor......................................4

c) brief assessment of superannuation adequacy.........................................................................5

Question 2........................................................................................................................................6

a) Calculation of expected income and capital generation..........................................................6

b) Ranking of investment.............................................................................................................6

c) Risk attached to each investment alternative:..........................................................................7

d) Issues and benefits Gordon could achieve by diversification of investments.........................7

Question 3........................................................................................................................................7

a) preparation of cash flow statement..........................................................................................7

b) preparation of personal balance sheet......................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

Question 1........................................................................................................................................3

a) Identification of demographic factors and evaluating its impact on rapidly ageing population

......................................................................................................................................................3

b) Process of financial planning and requirements of financial advisor......................................4

c) brief assessment of superannuation adequacy.........................................................................5

Question 2........................................................................................................................................6

a) Calculation of expected income and capital generation..........................................................6

b) Ranking of investment.............................................................................................................6

c) Risk attached to each investment alternative:..........................................................................7

d) Issues and benefits Gordon could achieve by diversification of investments.........................7

Question 3........................................................................................................................................7

a) preparation of cash flow statement..........................................................................................7

b) preparation of personal balance sheet......................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................1

INTRODUCTION

This report will identify and evaluate the demographic factors that are the cause behind

the problem of rapid rise in ageing of population in developed countries across the world. The

report will highlight the process of financial planning.

Further in this report assessment of superannuation contribution requirements for

adequacy evaluation will be covered. This report will also analyse three investment alternatives.

In addition, preparation of cash flow and balance sheet will be discussed.

Question 1

a) Identification of demographic factors and evaluating its impact on rapidly ageing population

Demographic Factors

Demographic factors is the sum total of factors such as gender, age, race and ethnicity.

The demographic factors that are the cause reason for the issue of rapidly ageing population are

lower fertility and mortality.

Attainment of older population age structures already exists in many countries especially

the developed ones (Nepomuceno and et.al., 2020). Many developing countries are currently

facing an inclement in relative numbers of children, population within working age and older

citizens. People belonging to the age criteria sixty and sixty plus are consists of ten percent of the

world population.

Ageing of population is measured with the help of changes in the proportion of the

population based on categories namely old and middle age. The trends in fertility rates and

mortality rates are the primary determinants of population ageing.

Mortality rate: Also referred as death rate is a measure of the number of deaths in a

particular population per thousand individuals in a year (Downey, Kelly and Quinlan, 2019).

Fertility Rate: Total fertility rate of a population is the average number of children that a

woman would give birth to during her entire life if:

she was to experience the current age specific fertility rates through her lifetime,⇒

⇒ and she was to live from birth until the end of her reproductive life.

Lower mortality and fertility rate increases the share of retired people in the total

population. Increase in number of retire persons in the population exerts pressure on spending by

This report will identify and evaluate the demographic factors that are the cause behind

the problem of rapid rise in ageing of population in developed countries across the world. The

report will highlight the process of financial planning.

Further in this report assessment of superannuation contribution requirements for

adequacy evaluation will be covered. This report will also analyse three investment alternatives.

In addition, preparation of cash flow and balance sheet will be discussed.

Question 1

a) Identification of demographic factors and evaluating its impact on rapidly ageing population

Demographic Factors

Demographic factors is the sum total of factors such as gender, age, race and ethnicity.

The demographic factors that are the cause reason for the issue of rapidly ageing population are

lower fertility and mortality.

Attainment of older population age structures already exists in many countries especially

the developed ones (Nepomuceno and et.al., 2020). Many developing countries are currently

facing an inclement in relative numbers of children, population within working age and older

citizens. People belonging to the age criteria sixty and sixty plus are consists of ten percent of the

world population.

Ageing of population is measured with the help of changes in the proportion of the

population based on categories namely old and middle age. The trends in fertility rates and

mortality rates are the primary determinants of population ageing.

Mortality rate: Also referred as death rate is a measure of the number of deaths in a

particular population per thousand individuals in a year (Downey, Kelly and Quinlan, 2019).

Fertility Rate: Total fertility rate of a population is the average number of children that a

woman would give birth to during her entire life if:

she was to experience the current age specific fertility rates through her lifetime,⇒

⇒ and she was to live from birth until the end of her reproductive life.

Lower mortality and fertility rate increases the share of retired people in the total

population. Increase in number of retire persons in the population exerts pressure on spending by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

government. The government will have to spend more on the pension and healthcare services

that are needed for people in old age.

Less innovation is also a result of low fertility and mortality rates. With older or less

young people ideas of innovations are less likely to come (Allai and et.al., 2018). Low birth and

death rates possess adverse economic effects like less number of workers, consumers, older

population, decline in wealthy markets, push for automation.

b) Process of financial planning and requirements of financial advisor

Financial Planning

Financial Planning refers to the process of forecasting the requirements for capital and

determination the competition regarding it (Santos, Piresand Fernandes, 2018.). Through

financial planning policies are made in relation to acquiring, investing and administering the

funds of the company.

Process of financial planning:

Financial Situation Identification: The first step is concerned with being familiar with the

current financial situation and thinking the ways to bring about change in the situation.

Forming household budget on the basis of living expenses, managing outstanding taxes,

current investments and reserves along with all other financial obligations (Davis and

et.al., 2018).

Determination Of Financial Goals: In this financial goals such as purchasing a property,

ensuring good education to children, etc., that are to be achieved are determined.

Identification Of Various Investment Alternatives Available: All the possible alternatives

that exists to invest in are identified.

Evaluation Of Each Alternative: Each alternative identified is evaluated in accordance to

the risks attached to them in this step.

Putting Financial Plan For Implementation: This step is the action plan stage as all the

above steps are put together, based on which financial plan is created and executed. Follow-Up The Plan: Financial planning is an ongoing process. The outcomes of the

implemented financial plan are evaluation and measures are taken to correct them in case

of deviations.

Financial Advisor or Financial Planner

that are needed for people in old age.

Less innovation is also a result of low fertility and mortality rates. With older or less

young people ideas of innovations are less likely to come (Allai and et.al., 2018). Low birth and

death rates possess adverse economic effects like less number of workers, consumers, older

population, decline in wealthy markets, push for automation.

b) Process of financial planning and requirements of financial advisor

Financial Planning

Financial Planning refers to the process of forecasting the requirements for capital and

determination the competition regarding it (Santos, Piresand Fernandes, 2018.). Through

financial planning policies are made in relation to acquiring, investing and administering the

funds of the company.

Process of financial planning:

Financial Situation Identification: The first step is concerned with being familiar with the

current financial situation and thinking the ways to bring about change in the situation.

Forming household budget on the basis of living expenses, managing outstanding taxes,

current investments and reserves along with all other financial obligations (Davis and

et.al., 2018).

Determination Of Financial Goals: In this financial goals such as purchasing a property,

ensuring good education to children, etc., that are to be achieved are determined.

Identification Of Various Investment Alternatives Available: All the possible alternatives

that exists to invest in are identified.

Evaluation Of Each Alternative: Each alternative identified is evaluated in accordance to

the risks attached to them in this step.

Putting Financial Plan For Implementation: This step is the action plan stage as all the

above steps are put together, based on which financial plan is created and executed. Follow-Up The Plan: Financial planning is an ongoing process. The outcomes of the

implemented financial plan are evaluation and measures are taken to correct them in case

of deviations.

Financial Advisor or Financial Planner

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The professional providing financial services is referred to as financial advisor or financial

planner.

Requirement of financial advisor or planner:

Assistance in keeping finances in order: Financial advisor helps in putting strategies for

achieving goals and priorities based on current finances.

Help with career and business strategies: They offer solutions to handle varied phases of

the career.

Organize after retirement life and plans for future generations: They help in developing

retirement focus plans (Oehler ,and et.al., 2018). Also, helps in adopting smart financial

plan for securing future of future generations.

Develop effective insurance strategies that helps in times of crises: Financial planner

analysis insurance plans that are affordable and efficient in crises or change in situation.

c) brief assessment of superannuation adequacy

Superannuation: It the amount paid regularly by an employee into a fund towards a future

pension. In the current superannuation regime every employee whose monthly income is more

than $450 have to pay ten percent of their ordinary time earning towards the superannuation

contributions. It is before tax contribution (Hayne, 2019). Ordinary time earnings include salaries

or wages, commissions and allowances but overtime is excluded. Superannuation is mandated

for citizens earning more $450 monthly.

Assessment of adequacy of superannuation contribution requirement in providing suitable

retirement income

Adequacy Objective: To access whether the retirement income is adequate or not first

objective need to be set. Objective set reflects the income value that will be adequate.

Objective need not be same for all. Different objectives gives different perspectives for

what might be considered as adequate. Commonly objectives can be procurement of

property, attainment of certain standard of living after retirement, etc.

Indicator Measuring Adequacy: An indicator is a measure of income at retirement. The

measuring indicator should be perfect substitute for a specific objective. Although, there

exist a number of indicators but some indicators are more used and prevalent than the

others. One such indicator is the retirement income replacement rate.

planner.

Requirement of financial advisor or planner:

Assistance in keeping finances in order: Financial advisor helps in putting strategies for

achieving goals and priorities based on current finances.

Help with career and business strategies: They offer solutions to handle varied phases of

the career.

Organize after retirement life and plans for future generations: They help in developing

retirement focus plans (Oehler ,and et.al., 2018). Also, helps in adopting smart financial

plan for securing future of future generations.

Develop effective insurance strategies that helps in times of crises: Financial planner

analysis insurance plans that are affordable and efficient in crises or change in situation.

c) brief assessment of superannuation adequacy

Superannuation: It the amount paid regularly by an employee into a fund towards a future

pension. In the current superannuation regime every employee whose monthly income is more

than $450 have to pay ten percent of their ordinary time earning towards the superannuation

contributions. It is before tax contribution (Hayne, 2019). Ordinary time earnings include salaries

or wages, commissions and allowances but overtime is excluded. Superannuation is mandated

for citizens earning more $450 monthly.

Assessment of adequacy of superannuation contribution requirement in providing suitable

retirement income

Adequacy Objective: To access whether the retirement income is adequate or not first

objective need to be set. Objective set reflects the income value that will be adequate.

Objective need not be same for all. Different objectives gives different perspectives for

what might be considered as adequate. Commonly objectives can be procurement of

property, attainment of certain standard of living after retirement, etc.

Indicator Measuring Adequacy: An indicator is a measure of income at retirement. The

measuring indicator should be perfect substitute for a specific objective. Although, there

exist a number of indicators but some indicators are more used and prevalent than the

others. One such indicator is the retirement income replacement rate.

Comparing Indicator to a Target: Targets are the points that determine the adequacy of

retirement income (Haron, Razali and Mohamad, 2019). To set a target an adequacy

standard is established. Views are formed on areas like appropriate replacement rate, a

minimum standard of proxy, or the living standard that makes people live with comfort.

Overall assessment with reference to policy goals: The outcomes of adequacy indicators

are considered and compared to set targets by policy-makers across the population to

make an assessment. The assessment is for knowing whether the system provides

adequate retirement income broadly. This assessment provides the base goals for the

policymakers.

Question 2

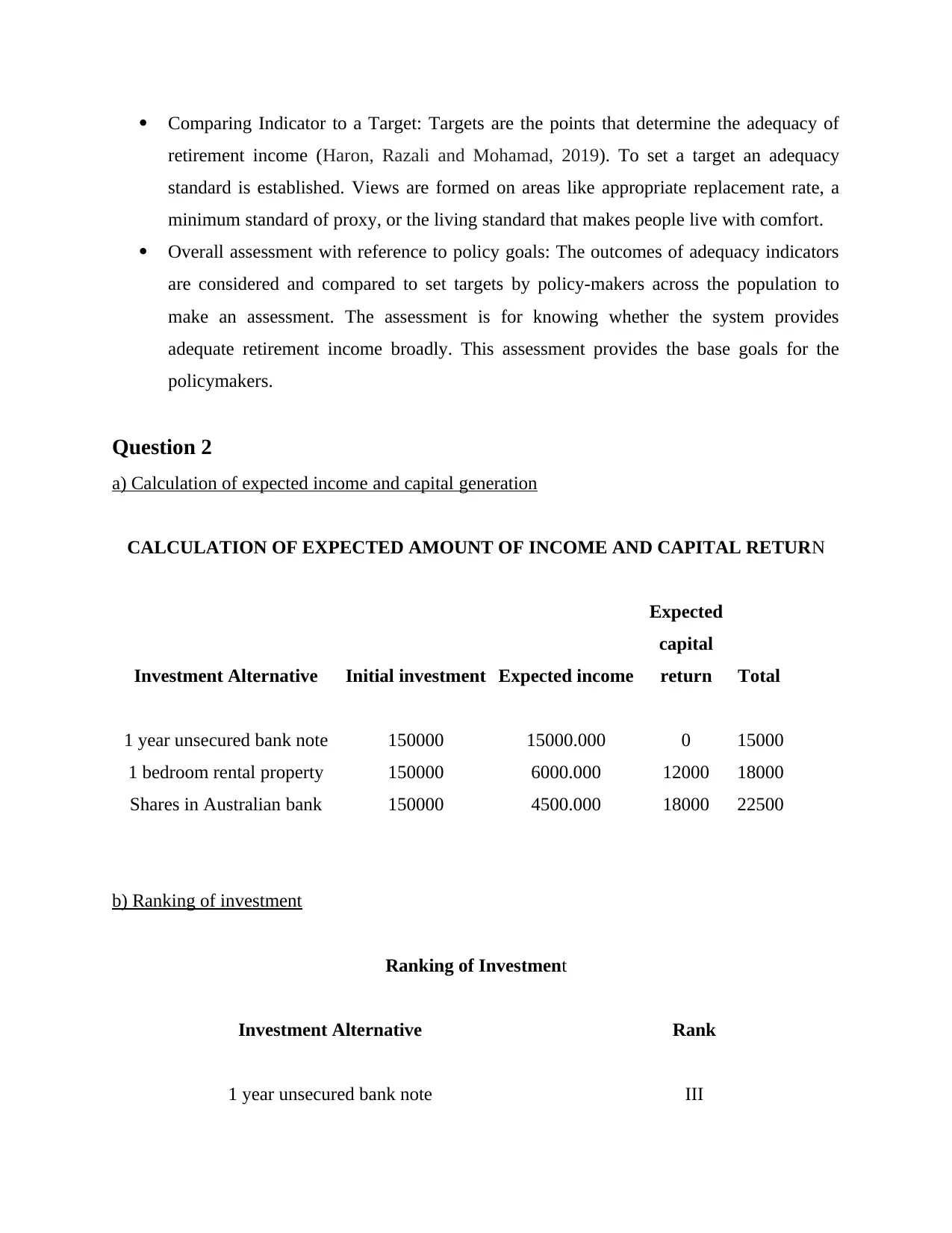

a) Calculation of expected income and capital generation

CALCULATION OF EXPECTED AMOUNT OF INCOME AND CAPITAL RETURN

Investment Alternative Initial investment Expected income

Expected

capital

return Total

1 year unsecured bank note 150000 15000.000 0 15000

1 bedroom rental property 150000 6000.000 12000 18000

Shares in Australian bank 150000 4500.000 18000 22500

b) Ranking of investment

Ranking of Investment

Investment Alternative Rank

1 year unsecured bank note III

retirement income (Haron, Razali and Mohamad, 2019). To set a target an adequacy

standard is established. Views are formed on areas like appropriate replacement rate, a

minimum standard of proxy, or the living standard that makes people live with comfort.

Overall assessment with reference to policy goals: The outcomes of adequacy indicators

are considered and compared to set targets by policy-makers across the population to

make an assessment. The assessment is for knowing whether the system provides

adequate retirement income broadly. This assessment provides the base goals for the

policymakers.

Question 2

a) Calculation of expected income and capital generation

CALCULATION OF EXPECTED AMOUNT OF INCOME AND CAPITAL RETURN

Investment Alternative Initial investment Expected income

Expected

capital

return Total

1 year unsecured bank note 150000 15000.000 0 15000

1 bedroom rental property 150000 6000.000 12000 18000

Shares in Australian bank 150000 4500.000 18000 22500

b) Ranking of investment

Ranking of Investment

Investment Alternative Rank

1 year unsecured bank note III

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 bedroom rental property II

Shares in Australian bank I

c) Risk attached to each investment alternative:

Unsecured Bank Note: It is not secured by the bank's assets. It is similar to debentures, there's

only one distinction that rate of return is higher. It is not backed by any collateral so it has higher

risk to investors.

Rental property: Rental property that is not located in good market often have trouble in

fascinating tenants. This results in extended vacant periods. Extra costs may also incur due to

damage caused to property by tenant. Another risk is non-payment of rent by tenants.

Shares in Australian bank: This investment option may result in losing some or all money. It

may happen that the shares does not perform as expected and resulting in fall in the value of

shares.

d) Issues and benefits Gordon could achieve by diversification of investments

Issues: By diversifying investments Gordon can only earn average returns. Transaction costs

associated with diversified investment options are also additional. Plus Gordon may have

difficulty in managing too many investments.

Benefits: Diversified investments helps in levelling out the volatility and risk attached.

Opportunities to generate more profits open up through diversifying investments.

Question 3

a) preparation of cash flow statement

cash flow statement

Particulars Amount

Cash flow from operating

activities

Net income 71400

Operating Expenses

Household Expenses 39000

Entertainment Expenses 25000

Net cash outflow from operating

activities 64000

Shares in Australian bank I

c) Risk attached to each investment alternative:

Unsecured Bank Note: It is not secured by the bank's assets. It is similar to debentures, there's

only one distinction that rate of return is higher. It is not backed by any collateral so it has higher

risk to investors.

Rental property: Rental property that is not located in good market often have trouble in

fascinating tenants. This results in extended vacant periods. Extra costs may also incur due to

damage caused to property by tenant. Another risk is non-payment of rent by tenants.

Shares in Australian bank: This investment option may result in losing some or all money. It

may happen that the shares does not perform as expected and resulting in fall in the value of

shares.

d) Issues and benefits Gordon could achieve by diversification of investments

Issues: By diversifying investments Gordon can only earn average returns. Transaction costs

associated with diversified investment options are also additional. Plus Gordon may have

difficulty in managing too many investments.

Benefits: Diversified investments helps in levelling out the volatility and risk attached.

Opportunities to generate more profits open up through diversifying investments.

Question 3

a) preparation of cash flow statement

cash flow statement

Particulars Amount

Cash flow from operating

activities

Net income 71400

Operating Expenses

Household Expenses 39000

Entertainment Expenses 25000

Net cash outflow from operating

activities 64000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash flow from financing

activities

Mortgage loan repayments 24000

Car loan repayments 12000

Net cash outflow from financing

activities 36000

Net decrease in cash and cash

equivalents 7400

Savings Account 6000

b) preparation of personal balance sheet

Balance Sheet

Assets

House and personal effects 650000

Superannuation 160000

3150 163150

Car 40000

Savings Account 6000

Total 859150

Liabilities

Mortgage loan 350000

repayment 24000 326000

Net income 71400

Credit Card Balance 10000

Total 407400

CONCLUSION

Based on the report the demographic factors responsible for the problem of population

ageing have been discussed. The requirements of a financial advisor or planner have been

highlighted. The adequacy of retirement income has been analysed in the report.

activities

Mortgage loan repayments 24000

Car loan repayments 12000

Net cash outflow from financing

activities 36000

Net decrease in cash and cash

equivalents 7400

Savings Account 6000

b) preparation of personal balance sheet

Balance Sheet

Assets

House and personal effects 650000

Superannuation 160000

3150 163150

Car 40000

Savings Account 6000

Total 859150

Liabilities

Mortgage loan 350000

repayment 24000 326000

Net income 71400

Credit Card Balance 10000

Total 407400

CONCLUSION

Based on the report the demographic factors responsible for the problem of population

ageing have been discussed. The requirements of a financial advisor or planner have been

highlighted. The adequacy of retirement income has been analysed in the report.

This report have also evaluated investment alternatives through varied approaches. Lastly

it has been outlined on bases of report how to prepare cash flow and balance sheet.

it has been outlined on bases of report how to prepare cash flow and balance sheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Nepomuceno, M. R. and et.al., 2020. Besides population age structure, health and other

demographic factors can contribute to understanding the COVID-19

burden. Proceedings of the National Academy of Sciences. 117(25). pp.13881-13883.

Downey, C., Kelly, M. and Quinlan, J. F., 2019. Changing trends in the mortality rate at 1-year

post hip fracture-a systematic review. World journal of orthopedics. 10(3). p.166.

Allai, L.and et.al., 2018. Supplementation of ram semen extender to improve seminal quality and

fertility rate. Animal reproduction science. 192. pp.6-17.

Hayne, K., 2019. Royal Commission into misconduct in the banking, superannuation and

financial services industry. Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry.

Haron, H., Razali, N. N. S. M. and Mohamad, F., 2019. Factors influencing financial planning

retirement amongst employees in the private sector in east coast Malaysia: Literature

review and research agenda. KnE Social Sciences. pp.1115-1129.

Santos, J . P. F. D., Pires, A. M. M. and Fernandes, P. O., 2018. The importance to financial

information in the decision-making process in company's family structure. Contaduría y

administración. 63(SPE2). pp.1091-1113.

Davis, R.A. and et.al., 2018. Inference on the tail process with application to financial time series

modeling. Journal of econometrics. 205(2). pp.508-525.

Oehler, A.,and et.al., 2018. Young adults and their finances: An international comparative study

on applied financial literacy. Economic Notes: Review of Banking, Finance and

Monetary Economics. 47(2-3). pp.305-330.

1

Nepomuceno, M. R. and et.al., 2020. Besides population age structure, health and other

demographic factors can contribute to understanding the COVID-19

burden. Proceedings of the National Academy of Sciences. 117(25). pp.13881-13883.

Downey, C., Kelly, M. and Quinlan, J. F., 2019. Changing trends in the mortality rate at 1-year

post hip fracture-a systematic review. World journal of orthopedics. 10(3). p.166.

Allai, L.and et.al., 2018. Supplementation of ram semen extender to improve seminal quality and

fertility rate. Animal reproduction science. 192. pp.6-17.

Hayne, K., 2019. Royal Commission into misconduct in the banking, superannuation and

financial services industry. Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry.

Haron, H., Razali, N. N. S. M. and Mohamad, F., 2019. Factors influencing financial planning

retirement amongst employees in the private sector in east coast Malaysia: Literature

review and research agenda. KnE Social Sciences. pp.1115-1129.

Santos, J . P. F. D., Pires, A. M. M. and Fernandes, P. O., 2018. The importance to financial

information in the decision-making process in company's family structure. Contaduría y

administración. 63(SPE2). pp.1091-1113.

Davis, R.A. and et.al., 2018. Inference on the tail process with application to financial time series

modeling. Journal of econometrics. 205(2). pp.508-525.

Oehler, A.,and et.al., 2018. Young adults and their finances: An international comparative study

on applied financial literacy. Economic Notes: Review of Banking, Finance and

Monetary Economics. 47(2-3). pp.305-330.

1

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.