Accounting & Finance: Comparative Analysis of Gambling Companies

VerifiedAdded on 2024/05/17

|18

|3712

|286

Report

AI Summary

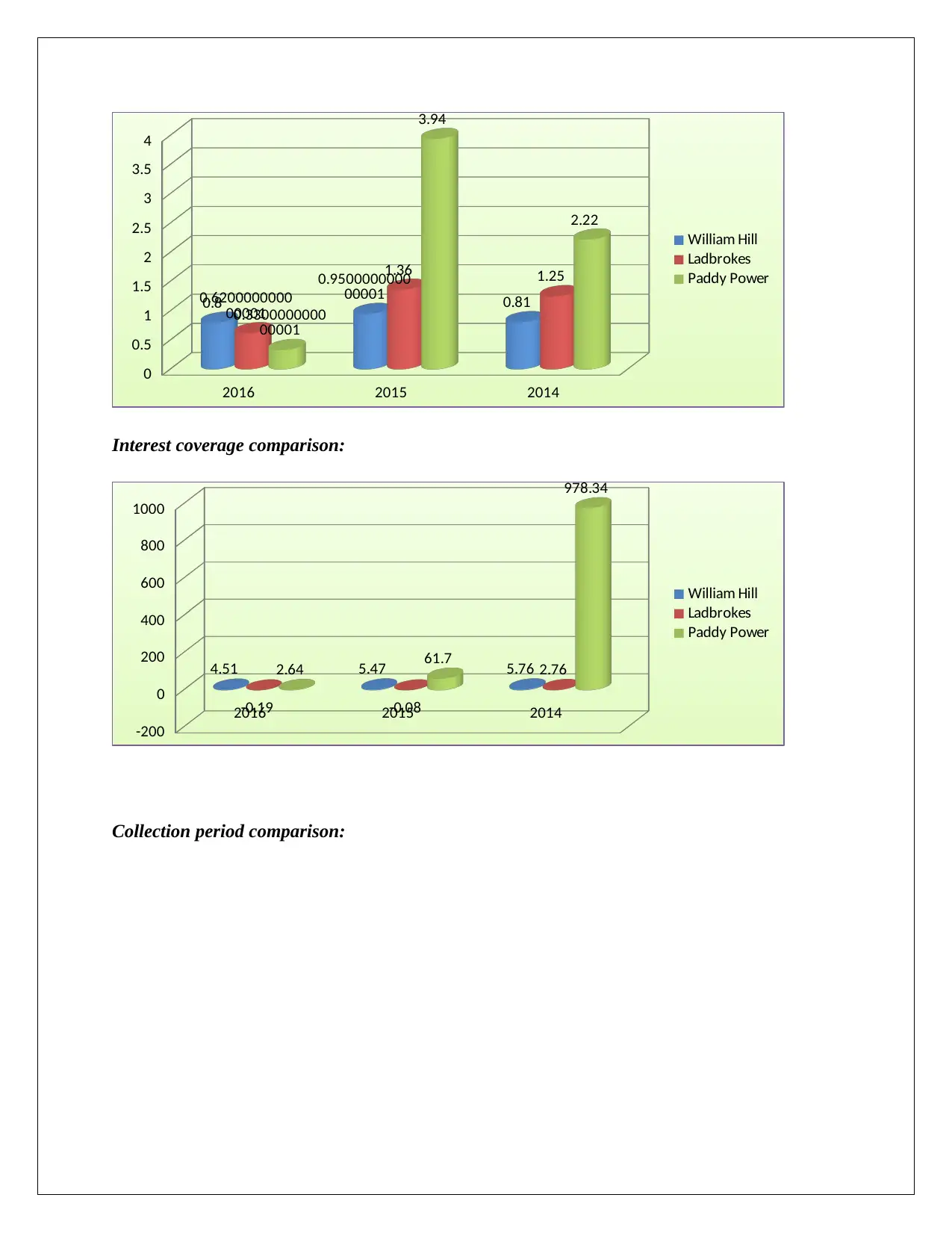

This report provides a financial analysis of three gambling companies in the United Kingdom (William Hill, Ladbrokes and Paddy Power) using financial ratios from 2014 to 2016. It assesses profitability, liquidity, operational efficiency, and gearing ratios. The analysis compares the financial performance of the three organizations, identifying Paddy Power as the best-performing company due to its superior profitability, liquidity, and operational efficiency, making it a favorable investment choice. Conversely, Ladbrokes is identified as the poorest-performing company, with suggestions for improving its profitability, efficiency, and asset management. The report concludes that while all three companies experienced similar trends, Paddy Power demonstrated greater financial stability and potential for future growth.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.